Presentation 3: Objectives To introduce you with the Principles of Investment Strategy for asset...

48

Presentation 3: Objectives To introduce you with the Principles of Investment Strategy for asset allocation and Modern Portfolio Theory Topics to be covered Capital Allocation Line, Sharpe Ratio, Optimal Portfolio, Capital Market Line, CAPM, APT, EMH 1

-

Upload

gabriella-jefferson -

Category

Documents

-

view

214 -

download

1

Transcript of Presentation 3: Objectives To introduce you with the Principles of Investment Strategy for asset...

Presentation 3: ObjectivesTo introduce you with the Principles of

Investment Strategy for asset allocation and Modern Portfolio Theory

Topics to be covered Capital Allocation Line, Sharpe Ratio,

Optimal Portfolio, Capital Market Line, CAPM, APT, EMH

1

Risk

Retu

rnEfficient

Background

6-3

rf rf

E(rp) p

y = % in p (1-y) = % in rf

Capital Allocation Line

PC y

( ) ( )c f P fE r r y E r r

6-4

Rearrange and substitute y=sC/sP:

Sharpe Ratio

fPP

CfC rrErrE

P

fP rrESlope

Capital Allocation Line

Risk Tolerance and Asset Allocation

22

2

21])([

21)(

pfpf

Cc

AyrrEyr

ArEUMax

2* )(

p

fp

A

rrEy

Investor’s risk aversion level =3. Fund manager A

E(R): 9% SD: 15%.

Fund manager B E(R): 18% SD: 25%.

T-bill : 6% What is the optimal position these two fund manager should

take for this investor (if this investor becomes one of their clients)?

Risk Tolerance and Asset Allocation

2* )(

p

fp

A

rrEy

ExampleIn risky portfolio – we have stocks

and bondNow we include a risk free asset

giving a return of 3%

Optimal Risky Portfolio with a Risk Free Asset

Optimal Risky Portfolio with a Risk Free Asset

ER(%)

ER(%)

31.24%

23.76%

45.00%

Bond Stock

Tbill

Optimal Risky Portfolio with a Risk Free Asset

Efficient Diversification with three risky assets

0.05 0.1 0.15 0.2 0.25 0.3 0.350

0.05

0.1

0.15

0.2

0.25

Exp

ecte

d R

e-

turn

Standard Devi-ation

A

B

C

3 assets portfolio

0.05 0.1 0.15 0.2 0.25 0.3 0.350

0.05

0.1

0.15

0.2

0.25

1&2

1&3

2&3

Mixed

Exp

ecte

d R

e-

turn

Standard Devi-ation

A

B

C

3 assets portfolio

Efficient Diversification with three risky assets

Efficient Diversification with many risky assets

Capital Market Line

Short Selling

fmm

pfp rrErrE

Capital Market LineSeparation TheoremJames Tobin (1958) paper said if you

hold risky securities and are able to borrow - buying stocks on margin - or lend - buying risk-free assets - and you do so at the same rate, then the efficient frontier is a single portfolio of risky securities plus borrowing and lending…

Capital Market LineTobin's Separation Theorem separate

the problem into :first finding that optimal combination

of risky securities deciding whether to lend or borrow,

depending on your attitude toward risk.

if there's only one portfolio plus borrowing and lending, it's got to be the market.

Rf

M

CML

Borrowing

Lendin

g

Exp

ect

ed

Retu

rn

Standard Deviation

Capital Market Line

sm

Rf

A

M.B

..

CMLE

xp

ect

ed

Retu

rn

Standard Deviation

Capital Market Line

Capital Market Line

2211 RXRXRE p

12212122

22

21

21

2 2 XXXXp

12212122

22

21

21

2 2 XXXXp

11 Xp

Capital Market LineTobin's Separation Theorem separate

the problem into :first finding that optimal combination

of risky securities deciding whether to lend or borrow,

depending on your attitude toward risk.

if there's only one portfolio plus borrowing and lending, it's got to be the market.

CAPMWilliam F. SharpeSharpe, W. (1964) A Theory of the Market

Equilibrium under conditions of Risk, Journal of Finance, 19, 425-442

Noble Prize in Economics 1990

google image

20

21

CAPMTreynor, J. (1961) Toward a Theory of Market

Value of Risky Assets, unpublished manuscript.

J. Lintner (1965) The valuation of Risk Assets and the Selection of Risky Investments in Stock Portfolios and Capital Budgets, Review of Economics and Statistics 47, 13-37

J. Mossin (1966) Equilibrium in a Capital Asset Market” Econometrica, 34, 768-783

22

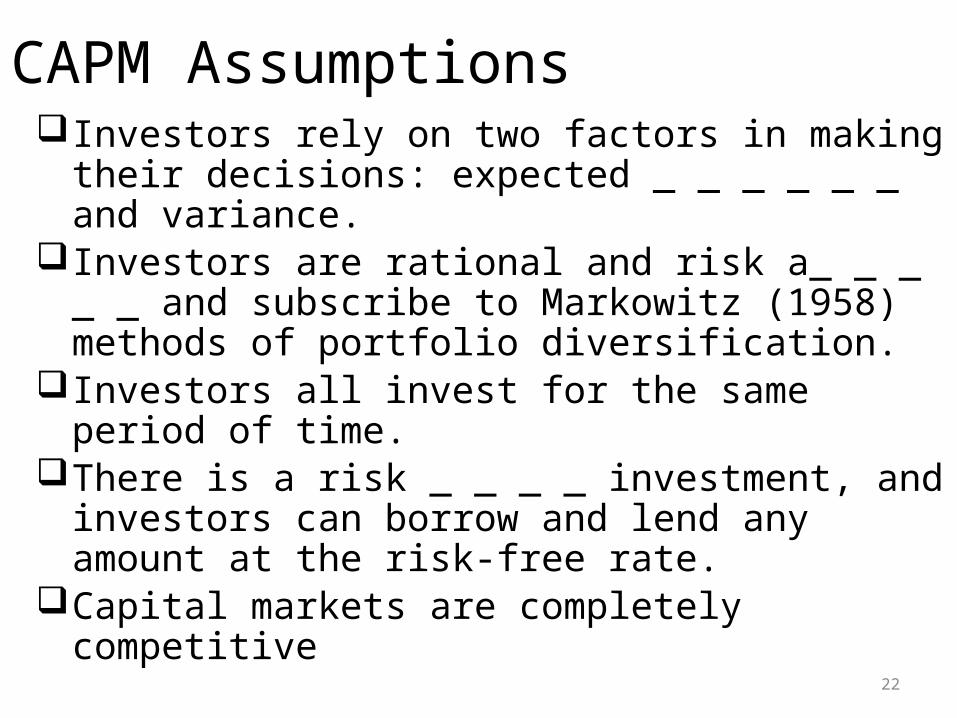

CAPM AssumptionsInvestors rely on two factors in making their

decisions: expected _ _ _ _ _ _ and variance. Investors are rational and risk a_ _ _ _ _ and

subscribe to Markowitz (1958) methods of portfolio diversification.

Investors all invest for the same period of time.

There is a risk _ _ _ _ investment, and investors can borrow and lend any amount at the risk-free rate.

Capital markets are completely competitive

23

In the development of portfolio theory Markowitz (1958) defined the variance of the rate of return as the appropriate measure of risk.

However this can be sub-divided into two general types of risk: systematic and unsystematic risk.

William Sharpe (1963) defined systematic risk as the portion of an assets variability that can be attributed to a common factor.

Systematic (or market risk) is the minimum level of risk

CAPM Terminologies: Systematic and Unsystematic risk

24

Sharpe (1963) defined the portion of an assets variability that can be diversified away as unsystematic (or unique) risk.

CAPM Terminologies: Systematic and Unsystematic risk

Total Risk:

Systematic + Unsystematic

25

CAPM Terminologies: Systematic and Unsystematic risk

Select from the following as cause for systematic and Unsystematic Risks :InflationAnnouncement of a small oil strike by a

companyGovernment Tax Policy RecessionDecision of management of the company

to expand/ contract

26

CAPM Terminologies: Systematic and Unsystematic risk

AKA (Systematic or Unsystematic?)Diversifiable riskAsset specific risksMarket risksUnique riskControllableIdiosyncratic riskUncontrollablePortfolio risk

27

CAPM Terminologies: Systematic and Unsystematic risk

Sta

ndar

d D

evia

tion

of R

etur

n

Number of Stocks in the Portfolio

Standard Deviation of the Market Portfolio (systematic risk)

Systematic Risk

Total Risk

CAPM Terminologies: Systematic and Unsystematic risk

Even a little diversification can substantially reduce variability. Unsystematic Risk can be reduced by diversification

Market risk

Unique risk

Expected Return on Individual security (using CAPM)The b is the covariance between the

return of a security and the market return divided by the variance of the market return.

It is a stock’s sensitivity to changes in the value of the market portfolio

29

)(RVariance

)R ,(RCovarianceβ

m

mi

Expected Return on Individual security (using CAPM):

If an investor wants to avoid risk altogether, he must invest in a portfolio consisting entirely of ………………………. such as ……………………..

30

Expected Return on Individual security (using CAPM): If an investor wants to avoid risk altogether, he must

invest in a portfolio consisting entirely of risk free securities such as Government Debt

If the investor holds only an undiversified portfolio of shares he will suffer unsystematic risk as well as systematic risk.

If an investor holds a ‘balanced portfolio’ of all the stocks and shares on the stock market, he will suffer risk which is the same as the average systematic risk in the market.

Individual shares will have risk characteristics which are different to this market average.

Their risk will be determined by the industry sector and gearing. Some shares will be more risky and some less.

31

The market portfolio (remember, this is the portfolio of all the shares in the market weighted by capitalization) is taken to be the benchmark and is given a β factor of 1.

All other shares or portfolios will have a β factor greater or smaller than 1 depending on their systematic risk which is measured by considering their required returns. If a share or portfolio has a β factor of 0.5 it will move in line with the market movements but only half as much. If the share or portfolio has a β factor of 2, it will again move in line with the market but twice as much.

32

Expected Return on Individual security (using CAPM)

Expected Return on Individual security (using CAPM)If a stock has the same risk as the

whole market portfolio then, B = ……..

If asset is less risky than the whole market portfolio then Beta = ………

If asset is more risky than the whole market portfolio then Beta = ……..

33

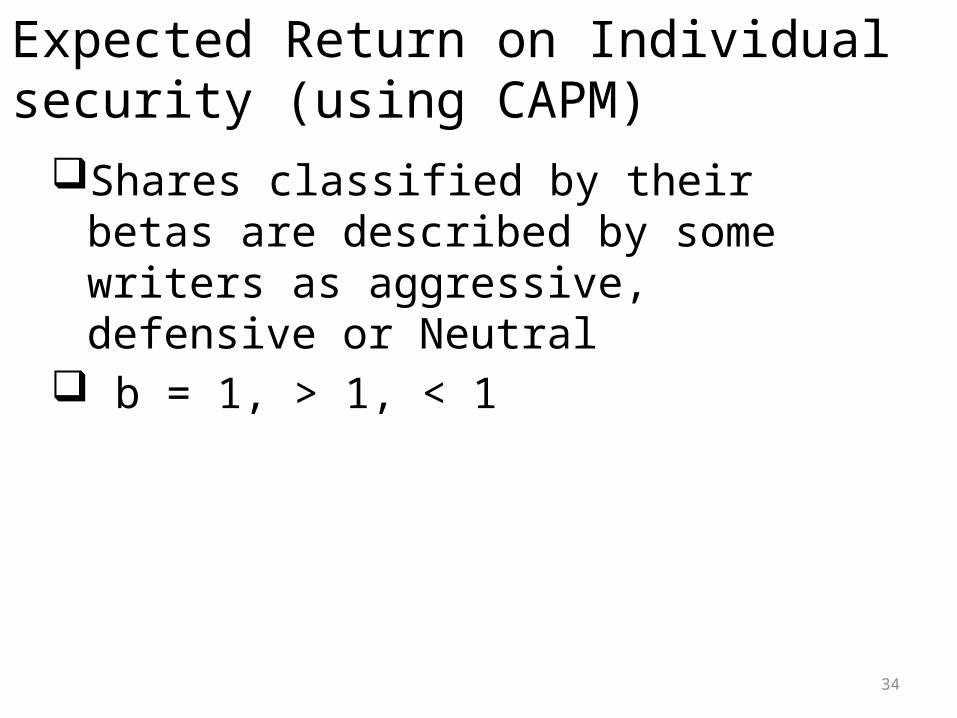

Expected Return on Individual security (using CAPM)Shares classified by their betas are

described by some writers as aggressive, defensive or Neutral

b = 1, > 1, < 1

34

Shows the relationship between the return of a equity and the β of the equity

Higher b means higher risk premium

35

Rf

= 1b

Rm

SML

Expe

cted

Ret

urn

CAPM: The Security Market Line (SML)

Suppose Rf is 6 %, Rm is 10% and if b = 1 then Return on equity (also, Cost of equity) =

= 6% + 1 x (10% - 6%) = 10% Now suppose the b is 0.5 then = 6% + 0.5 x (10% - 6%) = 8% Again if b = 2 = 14%

36

)R(RβRR RFMRFi

CAPM: The Security Market Line (SML)

CAPM: The Security Market Line (SML)

SML then will be

37

6%

= 1b

10%

SML

Expe

cted

Ret

urn

= 0.5b = 2b

8%

14%

EMH

19th Sept :$ 93.8914th Oct :$ 84.9528th Oct :$ 99.68

38

21/10/2014 90.9

22/10/2014 91.63

23/10/2014 94.45

24/10/2014 95.76

27/10/2014 97.79

28/10/2014 99.68

EMH“Don’t bother if the bill were

real someone would have picked it up already”

Markets are generally very efficient but rewards to the especially - diligent, Intelligent, Creative may in fact be waiting

Random Walks "The Theory of Speculation” Random Walk – 114 Years

Karl Pearson (1905), walk of

drunk, Nature.

Burton Malkiel, A Random Walk Down Wall Street, 1973.

Louis Bachelier

Market is IrrationalKendall and Hill (1953)

Stock Price -No logical rulesErratic Market Psychology AKA “Animal Spirits”

Prices seems to evolve randomly -Market is Irrational

£103.00

£100.00

£106.09

£100.43

£97.50

£100.43

£95.06

Coin Toss Game

Head

Head

Head

Tail

Tail

Tail

Random Walks

43

Informational Efficiency - Efficient Markets Hypothesis (EMH)

Fama (1970) - identified three classifications of efficiency:-Weak form - prices reflect all _ _ _ _information.Semi-strong form - prices reflect all past and _

_ _ _ _ _ _ publicly available information.Strong form - prices reflect all public AND _ _ _

_ _ _ _ information - may include privileged (_ _ _ _ _ _ ) information.

Empirical evidence suggests all major stock markets are at least _ _ _ _ form efficient.

44

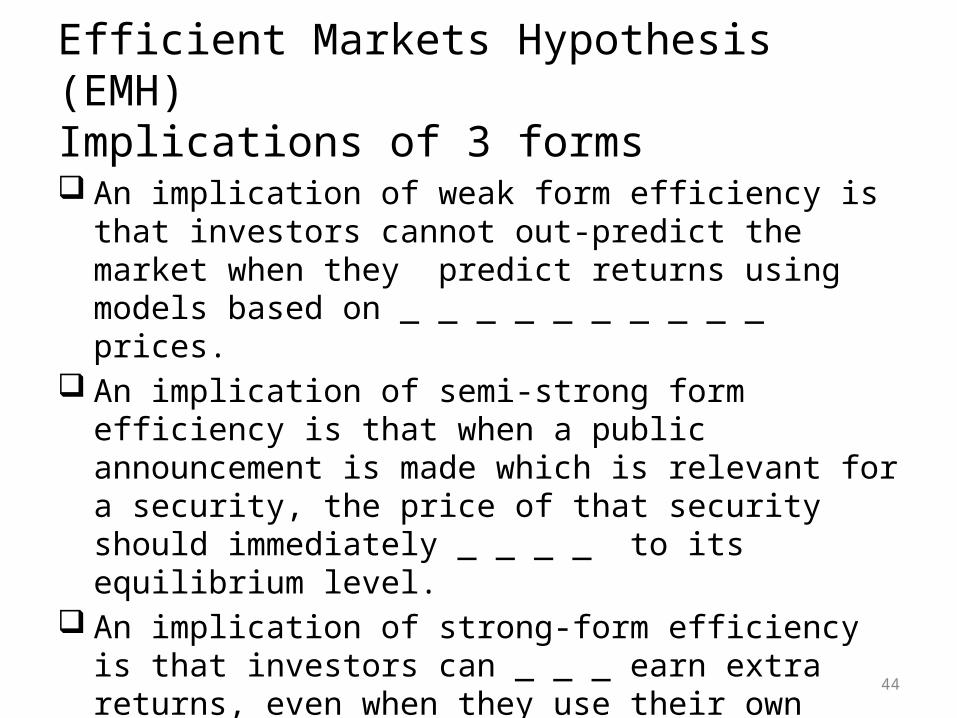

Efficient Markets Hypothesis (EMH)Implications of 3 forms

An implication of weak form efficiency is that investors cannot out-predict the market when they predict returns using models based on _ _ _ _ _ _ _ _ _ _ prices.

An implication of semi-strong form efficiency is that when a public announcement is made which is relevant for a security, the price of that security should immediately _ _ _ _ to its equilibrium level.

An implication of strong-form efficiency is that investors can _ _ _ earn extra returns, even when they use their own private information to forecast future returns and prices.

45

EMH - exampleCompany X has 1 m shares and a market value

of £3million.On 1/12/2013 it considers a project which will

cost £2million and yield cash flows of £0.5million per year forever.

The discount rate is 20%.On 4/12/2013 the board disclose details of the

project to the market but do not mention additional redundancy costs of £0.4million.

On 10/12/2013 all relevant information is released to the market.

46

Opening Share Price : = …………per shareSemi-Strong form efficiency:

1/12/2013 : _ _ change as no info is made public.

4/12/2013 : NPV of project = ……………… Share Price = …………….

10/12/13 : All information is made public.Share Price = ………………

EMH - example

47

Strong Form efficiency:Provided all financial implications

were known on 1/12/2013 the share price would immediately go to ………….

Final price is the same but speed of adjustment is quicker.

EMH - example

Event StudiesRead the news5th January 2009 Read the news : Fortunately, after

further testing, my doctors think they have found the cause—a hormone imbalance that has been “robbing” me of the proteins my body needs to be healthy. Sophisticated blood tests have confirmed this diagnosis.

48

![Lecture 38: Register Allocationinst.eecs.berkeley.edu/~cs164/sp19/lectures/lecture38.pdf · Lecture 38: Register Allocation [AdaptedfromnotesbyR.BodikandG.Necula] Topics: • MemoryHierarchyManagement](https://static.fdocuments.us/doc/165x107/5f6c0d25f2e45652766be94b/lecture-38-register-cs164sp19lectureslecture38pdf-lecture-38-register-allocation.jpg)