23 jan final slides copy (dr pooja-vaio's conflicted copy 2013-12-14)

Preparing for a Regulatory Exam

Copy of Slides

• To access a copy of the slides from today’s presentation please go to:

www.RIA-Compliance-Consultants.com/PreparingForRegulatoryExam.html

PresentersBryan HillPresidentRIA Compliance Consultants

Tammy EmsickSenior Compliance ConsultantRIA Compliance Consultants

Presentation Disclosures• Although the sponsor of this presentation, RIA Compliance Consultants, Inc. (“Sponsor”), is an affiliate of a law firm and

Sponsor may have an individual on its staff that is also licensed as an attorney providing legal services in a completely separate capacity, Sponsor is not a law firm and does not provide legal services or legal advice. A consulting relationship with Sponsor does not provide the same protections as an attorney-client relationship.

• This presentation is offered for educational purposes only and should not be considered an engagement with Presenter or Sponsor. This presentation should not be considered a comprehensive review or analysis of the topics discussed today. These materials are not a substitute for consulting with an attorney or compliance consultant in a one-on-one context whereby all the facts of your situation can be considered in their entirety.

• Despite efforts to be accurate and current, this presentation may contain out-of-date information. Additionally, Presenter and Sponsor will not be under an obligation to advise you of any subsequent changes.

• Information provided during this presentation is provided "as is" without warranty of any kind, either express or implied, including, without limitation, warranties and merchantability, fitness for a particular purpose, or non-infringement. Presenter and Sponsor assume no liability or responsibility for any errors or omissions in the content of the presentation.

• There is no guarantee or promise that concepts, opinions and/or recommendations discussed will be favorably received by any particular court, arbitration panel or securities regulator or result in a certain outcome.

• To the extent that you provide RCC with your email address, it will be added to RCC’s electronic newsletter mailing list regarding compliance issues for investment advisors. You may opt out at any time by calling RCC at 877-345-4034 or clicking at any time the “unsubscribe” link on the electronic newsletter.

• Communication with today’s webinar presenter is not protected by attorney-client privilege. Please keep questions during this seminar in a hypothetical form. This seminar session and/or the presentation materials may be recorded, copied and/or shared with third parties and/or posted to our public website.

Agenda• Section 204 of the Investment Advisers Act of

1940• Examination Process Overview• General Recommendations• Key Examination Focus and Topics• Common Deficiencies• Office of Compliance Inspections and

Examinations Investment Adviser Examinations: Core Initial Request for Information

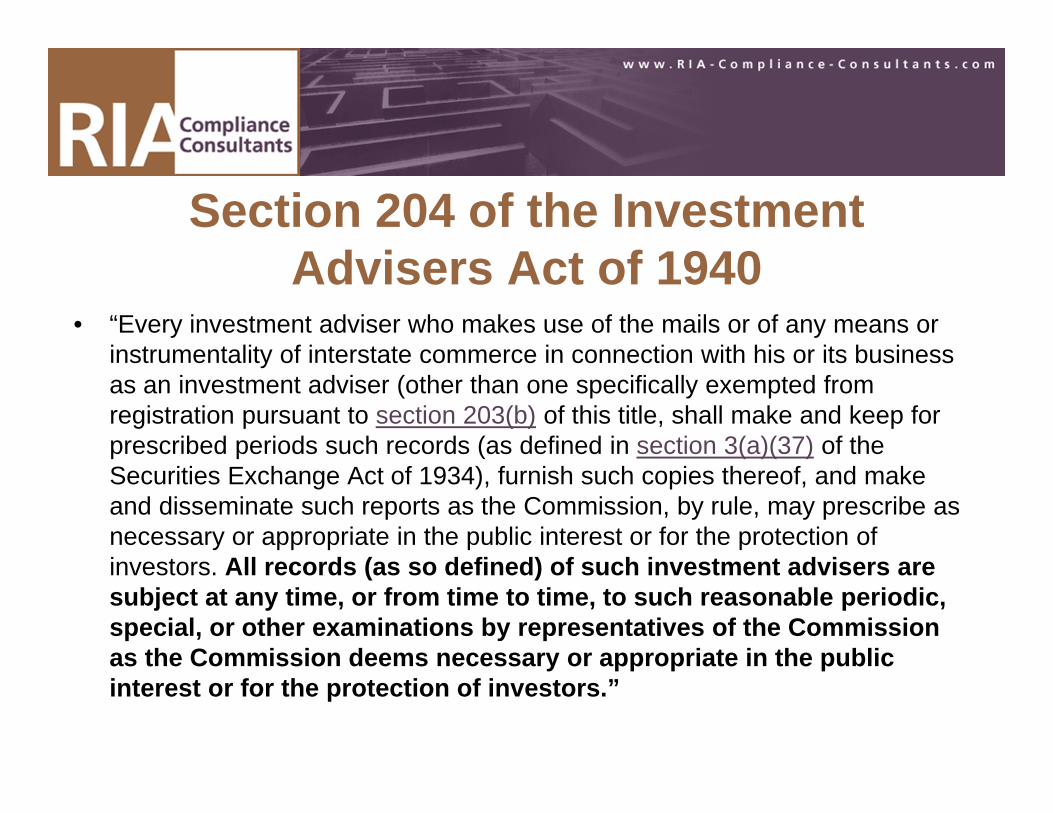

Section 204 of the Investment Advisers Act of 1940

• “Every investment adviser who makes use of the mails or of any means or instrumentality of interstate commerce in connection with his or its business as an investment adviser (other than one specifically exempted from registration pursuant to section 203(b) of this title, shall make and keep for prescribed periods such records (as defined in section 3(a)(37) of the Securities Exchange Act of 1934), furnish such copies thereof, and make and disseminate such reports as the Commission, by rule, may prescribe as necessary or appropriate in the public interest or for the protection of investors. All records (as so defined) of such investment advisers are subject at any time, or from time to time, to such reasonable periodic, special, or other examinations by representatives of the Commission as the Commission deems necessary or appropriate in the public interest or for the protection of investors.”

Section 204 of the Investment Advisers Act of 1940

• According to the SEC’s Division of Investment Management and Office of Compliance Inspections and Examinations, “the purpose of SEC examinations is to protect investors by determining whether registered firms are complying with the law, adhering to the disclosures that they have provided to their clients, and maintaining appropriate compliance programs to ensure compliance with the law. If you are examined, you are required to provide examiners with access to all requested advisory records that you maintain (under certain conditions, documents may remain private under the attorney-client privilege)”

http://www.sec.gov/divisions/investment/advoverview.htm

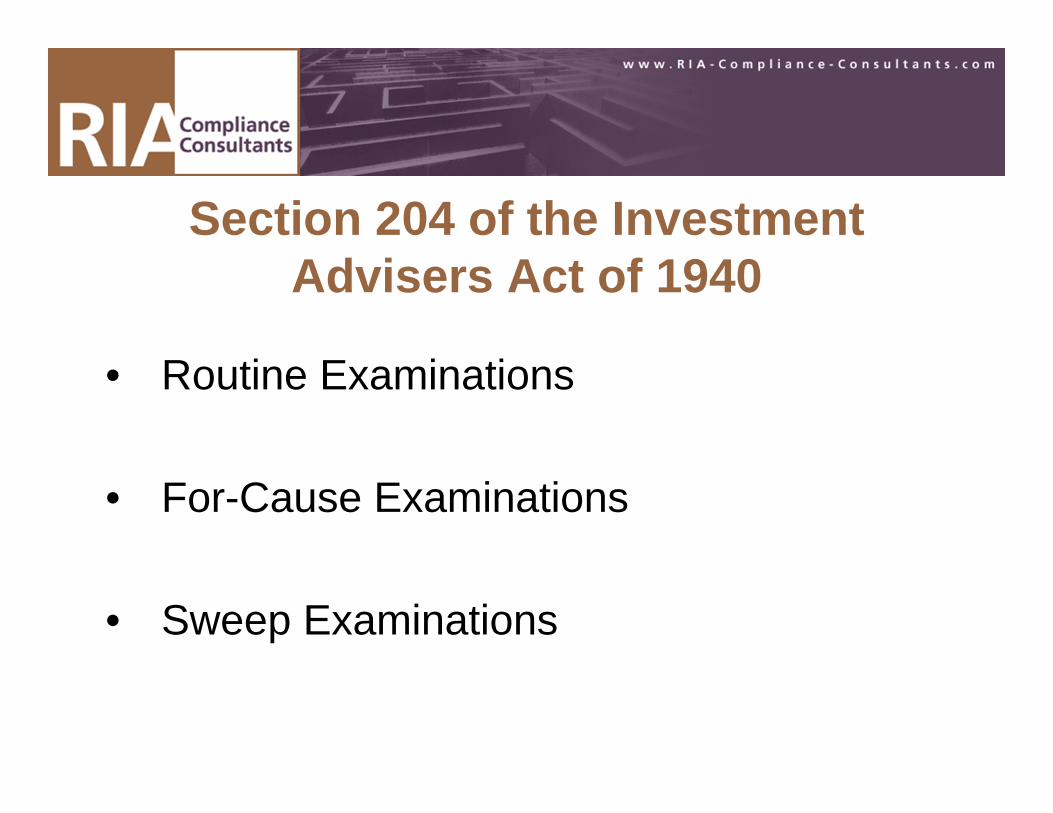

Section 204 of the Investment Advisers Act of 1940

• Routine Examinations

• For-Cause Examinations

• Sweep Examinations

SEC Office of Compliance Inspections and Examinations

• The SEC’s Office of Compliance Inspections and Examinations (“OCIE”) is responsible for conducting examinations of investment advisors through the home office in Washington, DC and regional offices located in Atlanta, Boston, Chicago, Denver, Fort Worth, Los Angeles, Miami, New York, Philadelphia, Salt Lake City, and San Francisco.

• A self-assessment of the examination program was conducted in 2010 and the findings were discussed in a report released by OCIE in February 2011, http://www.sec.gov/about/offices/ocie/ocieoverview.pdf.

SEC Office of Compliance Inspections and Examinations

• According to the report, “The goals of the examinations conducted by the staff in the National Examination Program include detecting possible violations of the securities laws and regulations (including fraud), fostering strong compliance and risk management practices (i.e., to improve the level of compliance with federal securities laws by registered entities), monitoring risk, and providing the Commission and its policy divisions with information about the industry’s compliance and the implementation of rules and laws.”

SEC Office of Compliance Inspections and Examinations

• The report states that the due to the number of registrants and the breadth of their operations, OCIE staff continue to focus examination resources on those registrants and activities where the staff in the National Examination Program believes that the investing public is at most risk.

SEC Office of Compliance Inspections and Examinations

• The following are some of the sources used by OCIE to identify higher risk registrants:– tips, complaints, and referrals; – analysis of outlier or aberrational information provided to

investors; – prior examinations findings; – significant changes in registrants’ business activities; and – registrant or investment advisor representatives

disclosures regarding regulatory and other actions brought against them.

Impact of Dodd-Frank Act• SEC will take on some new advisors due to

registration requirements for certain private funds.

• Mid-sized advisors will transition from SEC to state registration. State registered advisors will be covered under the state examination programs. States must have an examination program in order for a mid-sized advisor to register with the state securities regulator.

Examination Process Overview• Examiner will request the investment advisor’s

books and records, interview management and firm employees, and analyze the firm’s operations. (Note: Examinations do not always include an on-site visit.)

• Two primary goals are to test the investment advisor’s compliance with securities laws and regulations and to determine the safety of client assets.

Examination Process Overview• Process typically begins prior to on-site visit.• Examination process will typically continue after

the on-site visit.• In some examinations, the examiner may be

focused on a particular risk or risks that led to the examination. In other instances, the examiner may seek to identify risks requiring attention, and also seek to obtain a more general understanding of the entity’s compliance and internal control environment.

Examination Process Overview• In many cases, the examiner will consider the

quality of the investment advisor’s compliance systems and internal control environment when determining the scope of the examination.

• Examination staff may contact investment advisor in advance. Prior notice can range from a few days to a few weeks. Surprise examinations can also be conducted with no advance notice.

Examination Process Overview

– Organizational structure

– Affiliations with other entities

– Operations– Key personnel

– Supervisory systems– Compliance systems– Customers– Sources of revenue– Major liabilities

Examination staff will typically request an initial interview with responsible management. For example, during the initial interview the examination staff may discuss:

Examination Process Overview

• Examiners will provide a list of records that will be reviewed during the examination process. Lists will vary depending on the nature and focus of the exam. OCIE’s Core Initial Request for Information can be found at

http://www.sec.gov/info/cco/requestlistcore1108.htm

Examination Process Overview• Examiners will frequently have questions during

the examination process and the investment advisor must make sure to accommodate a prompt response to any inquiries. Questions are not necessarily asked because the staff suspects wrongdoing but, rather, because the staff needs more information regarding certain records.

Examination Process Overview• The examination staff will typically conduct an exit

interview or exit conference call as part of the examination process. This is to help facilitate the earliest possible implementation of corrective actions. Additionally, the examiners will obtain agreement on any outstanding documentation or information requests for providing such information. Responses provided during the exit interview are not considered a substitute for the investment advisor’s written responses to any deficiency letters received.

Examination Process Overview• Results

– No findings– Deficiency letters (most common)– Special meeting or conference call- When the

examination staff identifies compliance deficiencies or internal control weaknesses that appear too serious for a deficiency letter alone, but do not warrant referral to enforcement staff. Followed by written deficiency letter.

Examination Process Overview

– Referral to Division of Enforcement- When the staff believes findings are serious enough that investor funds or securities are at risk.

– Information provided to another office or division- When examinations identify recurring problems or gaps in regulatory coverage, the examination staff may raise their concerns with another office or division of the SEC, such as Division of Trading and Markets or Division of Investment Management.

General Recommendations• Acknowledge Announcement. Immediately respond to the

examination announcement. Once you are contacted, it is important to communicate with the lead examiner. This time should be used to ensure the firm and examiner are in agreement with the time and date of the visit. In some cases, the examiner may be willing to reschedule the time and/or dates if it does not fit your schedule, so don’t be afraid to ask.

• Answer Requests Promptly. Reply to all requests in a timely manner. During the pre-audit period, your firm will be asked to provide the examiners with several documents, which may include the firm’s sample investment advisory client agreements currently used, current investment advisory client list, investment advisory clients participating in wrap fee programs, organizational chart, financial statements, and written compliance programs including its code of ethics and supervisory procedures. It is important to provide these documents by the deadline identified by examiner.

General RecommendationsPrepare Background Presentation. Consider preparing a short (20 – 30

minute) presentation, along with PowerPoint slides, providing an overview of the investment advisor firm. The presentation should be given at the beginning of the examination process as part of, or even before, the initial interview process. The presentation allows your investment advisor firm to take control of the investment advisor examination and sets a tone of seriousness and professionalism. Topics could include the registered investment advisor firm’s organization, culture of compliance, lines of business, affiliated entities, types of investment advisor clients and investment advisory services provided.

Make Key Staff Available. Have essential personnel available for interviews with examiners. This could include executives, managers, investment advisor representatives and compliance staff of the investment advisor.

Designate CCO as Primary Communication Channel. The Chief Compliance Officer (“CCO”) should be involved in all meetings and discussions with examiners. The CCO should be the main contact and coordinator of the examination of the registered investment advisor.

General RecommendationsAct Honestly. Cooperate with examiners and be honest.

Educate Employees. Prepare and educate all employees of the registered investment advisor for the examination. Provide them with instructions for when and how to communicate with examiners.

Keep IA Records Separate from Other Business. Keep investment advisory books and records separate from files for other lines of business. Remember, the examiner is there to review your investment advisory business. Provide what is requested by the examiners. Do not provide more than what is asked for or needed by the examiner.

Track All Documents Provided to SEC. Prepare a method for tracking all documents requested by and provided to the examiner. The best method is to prepare an Excel spreadsheet outlining all documents requested by the examiner, sorted by the corresponding item number on the document request list. Prepare a separate file folder for each document actually provided to the examiner and keep the files in a box sorted by the corresponding item number on the document request list.

General RecommendationsRetain Copy of All Documents. Make a copy of every document provided to the examiner and notate the date, time, and the member of the examination staff that received such documents.

Provide Adequate Work Space. Have a nice, clean space prepared for the examiners to work.

Request Exit Interview. Most examiners will conduct an exit interview to discuss their initial findings of their inspection of your registered investment advisor. If not offered, request such a meeting with the examiner. Items discussed during the exit interview are often unofficial; however, your registered investment advisor firm will be able to begin working on any expected deficiencies before the final investment advisor examination letter is received.

General RecommendationsPrepare for a Deficiency Letter. Expect a deficiency letter. The majority of examinations identify at least one deficiency.

Answer Deficiency Letter. Respond to the examiner’s post-audit letter by the given deadline. If you cannot meet the deadline, inform the examiner immediately. The examiners are usually willing to work with you and may provide additional time.

File for FOIA Treatment. Consider filing a request to the SEC so that information provided to SEC examiners will not be disclosed to third-parties under the Freedom of Information Act. You may contact the SEC examiners to discuss the procedures for filing such a request.

SEC Examination Hotline• The Hotline can be reached at 202-551-EXAM or via e-mail at

[email protected]• Available to any registrant with a question, complaint, or concern about

an SEC examination• On the Hotline, registrants can direct their question, complaint, or

concern to either the examination program's Office of Chief Counsel or to the Commission's Office of Inspector General. The Office of Inspector General is an independent office within the SEC that conducts audits of SEC programs and investigates allegations of employee misconduct.

• SEC has developed an Internal Hotline for examination staff use

Examination Areas of Focus

• According to the SEC OCIE report issued in February 2011, “OCIE, working through the home and regional offices, has improved its risk assessment procedures and techniques to better identify areas of risk to investors. Such improvements include requiring routine outreach to third parties such as custodians, counter-parties, and customers during the examination to verify the existence and integrity of client assets managed by the firm; and conducting more rigorous reviews of firms before the examiners enter the premises.”

Examination Areas of Focus• According to the OCIE report, the staff has

identified the following as the current select focus areas during investment advisor examinations:– Control Environment– Conflicts of Interest– Portfolio Management– Pricing of Clients’ Portfolios and Calculation of Net

Asset Value– Performance Advertising and Marketing– Safety of Client Assets

Key Topics Covered During 2010 Examinations

• The OCIE report indicated that the key topics in an examination included, but were not limited to reviewing whether:1. Blocked trades and initial public offerings are

allocated fairly and are consistent with disclosures;2. Client assets are prices accurately;3. If required, clients receive periodic account

statements from third parties;

Key Topics Covered During 2010 Examinations

4. Information created, recorded, maintained, and reported is protected from unauthorized alteration and destruction;

5. Portfolio management decisions are consistent with client mandates;

6. Clients’ funds and assets are safely maintained;7. The firm maintains a strong compliance culture;8. The firm’s control systems are subject to override by

control persons; and9. Performance information provided to clients is presented

fairly.

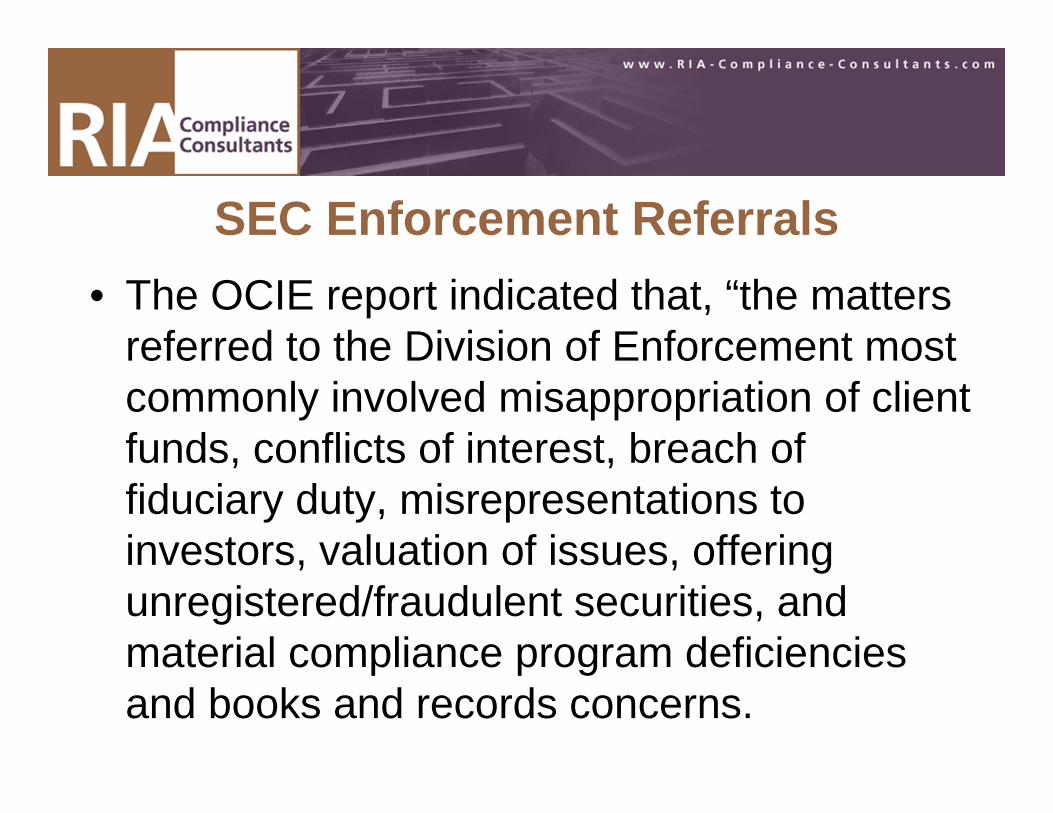

SEC Enforcement Referrals• The OCIE report indicated that, “the matters

referred to the Division of Enforcement most commonly involved misappropriation of client funds, conflicts of interest, breach of fiduciary duty, misrepresentations to investors, valuation of issues, offering unregistered/fraudulent securities, and material compliance program deficiencies and books and records concerns.

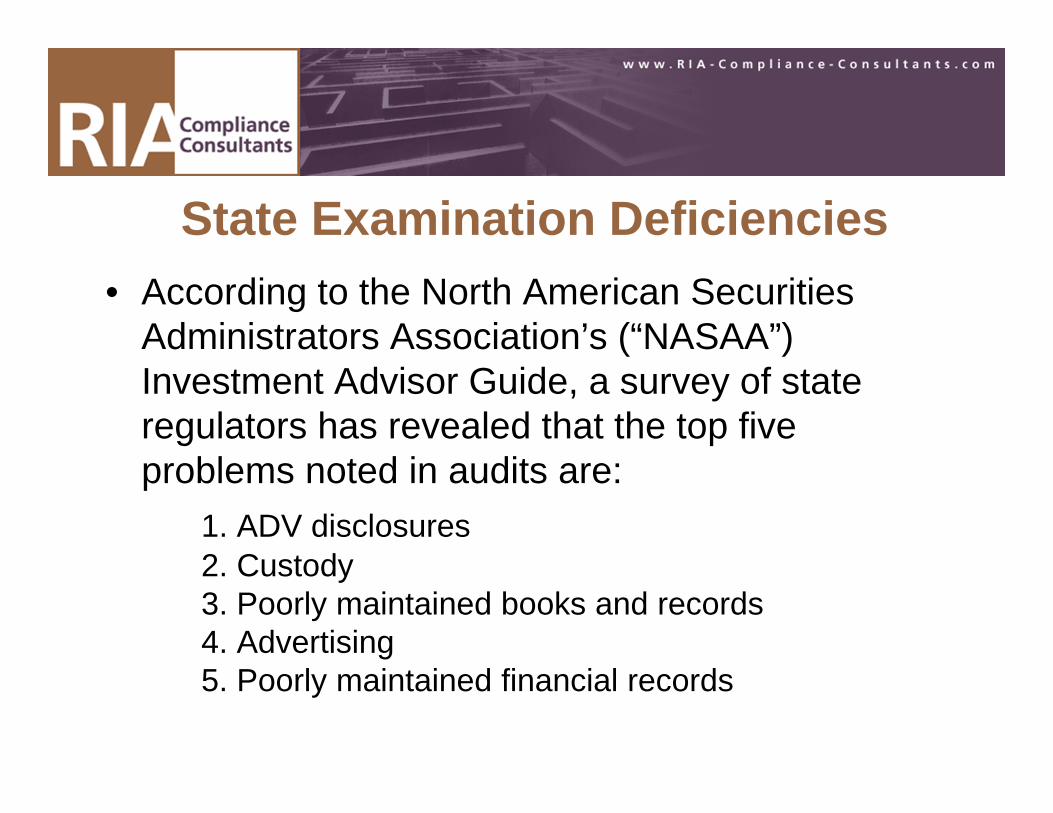

State Examination Deficiencies• According to the North American Securities

Administrators Association’s (“NASAA”) Investment Advisor Guide, a survey of state regulators has revealed that the top five problems noted in audits are:

1. ADV disclosures2. Custody 3. Poorly maintained books and records4. Advertising5. Poorly maintained financial records

State Examination Deficiencies• Other information found on various state

securities administrator websites indicated the following common deficiencies in addition to those previously listed:– Conflicts of Interest – Performance Claims – Suitability – Investment Advisor Representative Registration

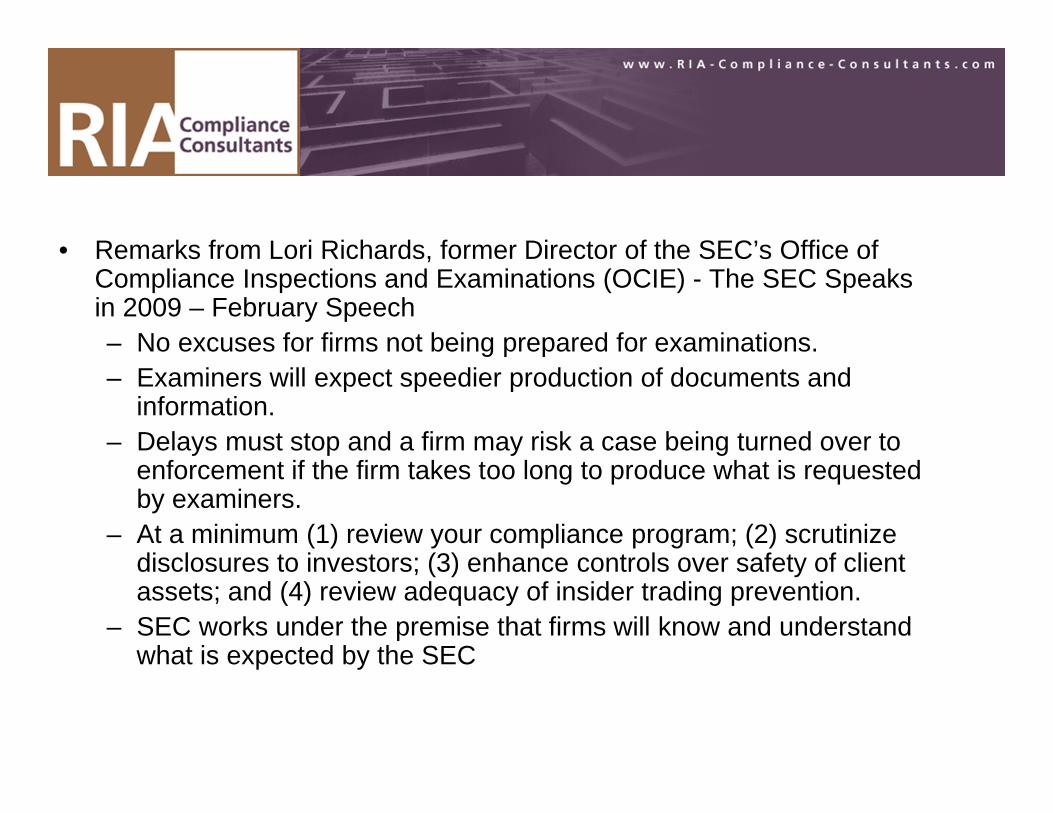

• Remarks from Lori Richards, former Director of the SEC’s Office of Compliance Inspections and Examinations (OCIE) - The SEC Speaks in 2009 – February Speech– No excuses for firms not being prepared for examinations. – Examiners will expect speedier production of documents and

information. – Delays must stop and a firm may risk a case being turned over to

enforcement if the firm takes too long to produce what is requested by examiners.

– At a minimum (1) review your compliance program; (2) scrutinize disclosures to investors; (3) enhance controls over safety of client assets; and (4) review adequacy of insider trading prevention.

– SEC works under the premise that firms will know and understand what is expected by the SEC

OCIE: Core Initial Request for Information - General Information

• Organizational structure, affiliations, and control persons• Current and former officers and/or directors• Employees who were disciplined and/or terminated and information

regarding reason for the action • Threatened, pending and settled litigation or arbitration involving the

Adviser or any supervised person• Standard client advisory contracts or agreements• Sub-advisory agreements executed with other investment advisers • Current fee schedules• Any power of attorney obtained from clients• Joint ventures or other businesses (with respect to the firm or any

officer, director, portfolio manager, or trader)• Disclosure documents and filings with regulators • Service providers and the services they perform

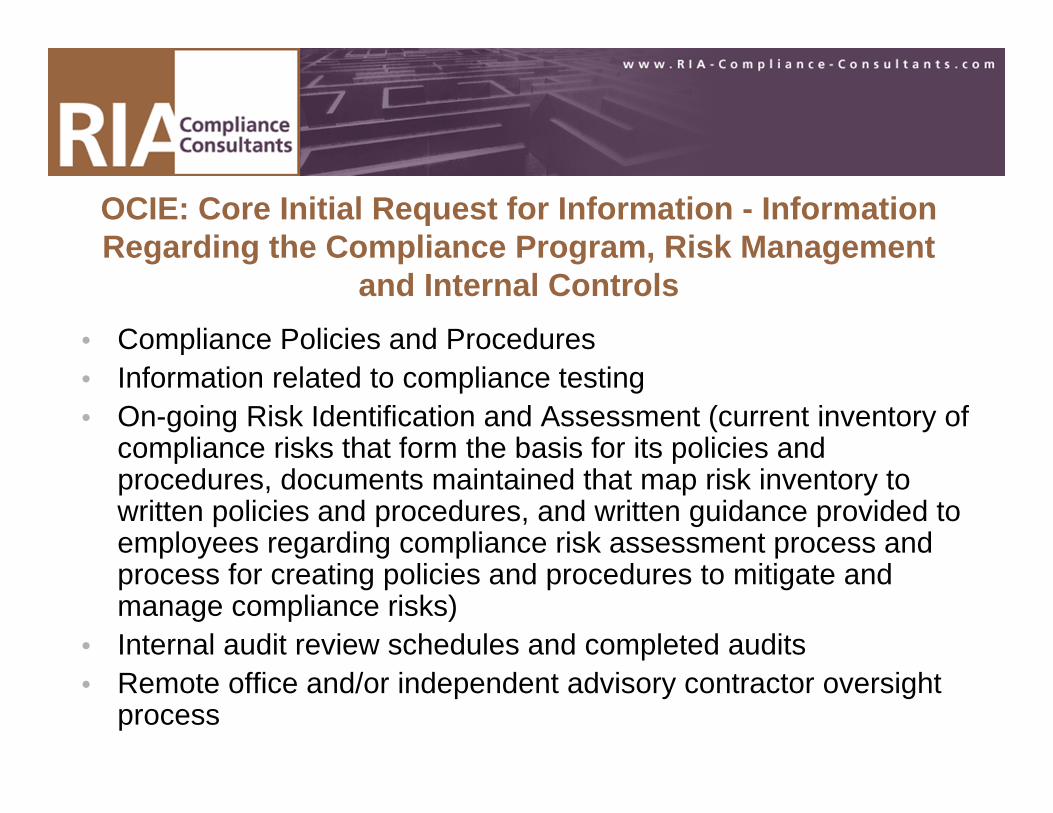

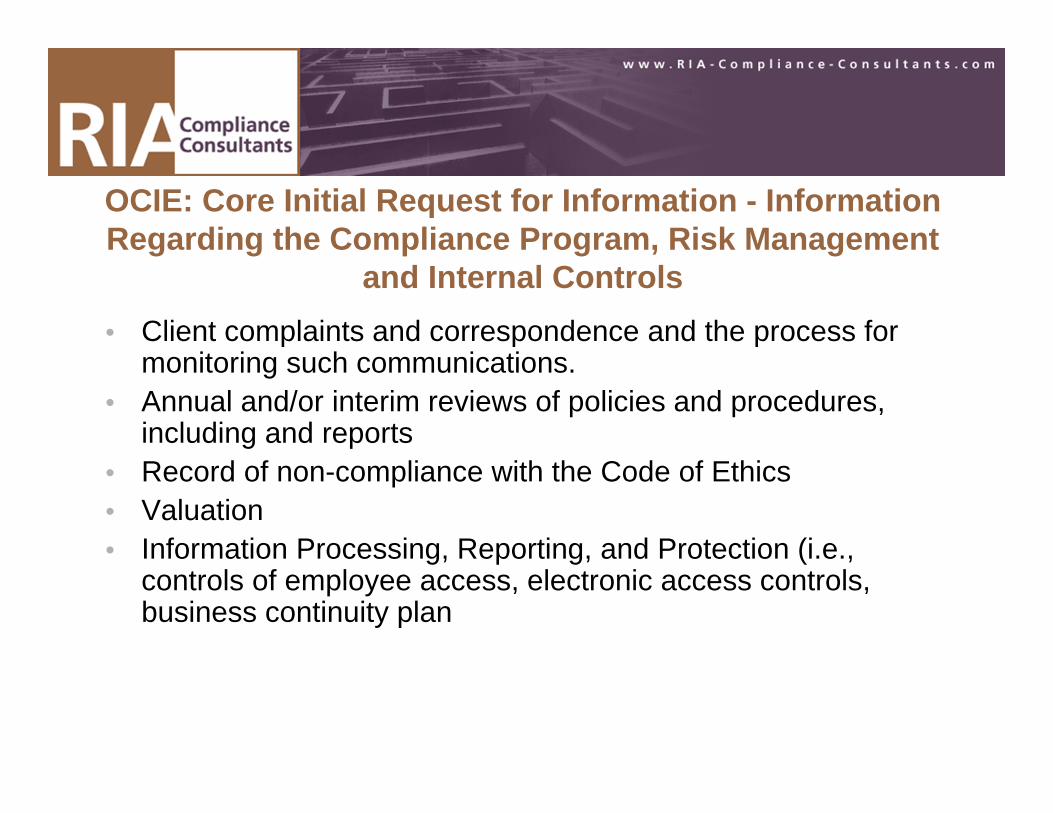

OCIE: Core Initial Request for Information - Information Regarding the Compliance Program, Risk Management

and Internal Controls• Compliance Policies and Procedures• Information related to compliance testing • On-going Risk Identification and Assessment (current inventory of

compliance risks that form the basis for its policies and procedures, documents maintained that map risk inventory to written policies and procedures, and written guidance provided to employees regarding compliance risk assessment process and process for creating policies and procedures to mitigate and manage compliance risks)

• Internal audit review schedules and completed audits• Remote office and/or independent advisory contractor oversight

process

OCIE: Core Initial Request for Information - Information Regarding the Compliance Program, Risk Management

and Internal Controls• Client complaints and correspondence and the process for

monitoring such communications. • Annual and/or interim reviews of policies and procedures,

including and reports• Record of non-compliance with the Code of Ethics • Valuation • Information Processing, Reporting, and Protection (i.e.,

controls of employee access, electronic access controls, business continuity plan

OCIE: Core Initial Request for Information - Information to Facilitate Testing with Respect to Advisory Trading

Activities• Trade blotter• Advisory Information for Individual Clients • Portfolio Management• Brokerage Arrangements• Trade Allocations• Conflicts of Interest and/or Insider Trading

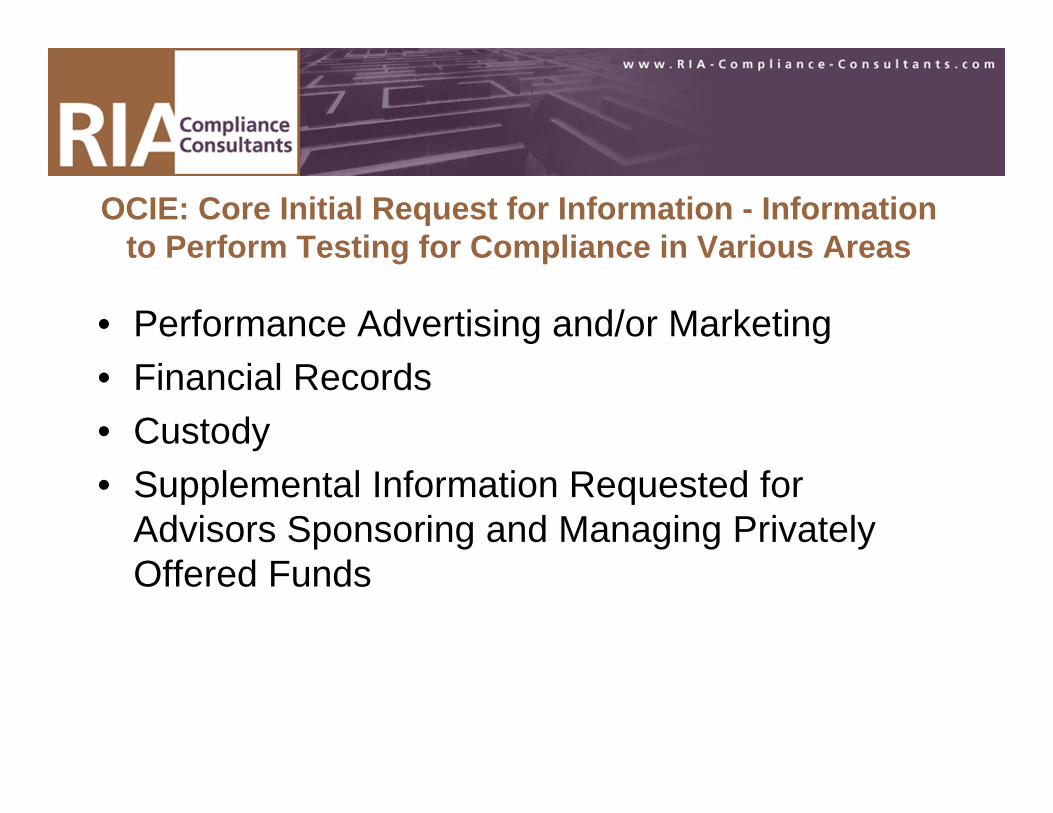

OCIE: Core Initial Request for Information - Information to Perform Testing for Compliance in Various Areas

• Performance Advertising and/or Marketing • Financial Records • Custody • Supplemental Information Requested for

Advisors Sponsoring and Managing Privately Offered Funds

OCIE: Core Initial Request for Information –Additional Information

Preceding slides included only summary of OCIE Core Initial Request for Information

Read the entire list and further information at

http://www.sec.gov/info/cco/requestlistcore1108.htm

About UsServe Over 500 Investment Advisor FirmsPrincipals Are Industry Experienced Working in Compliance or Law Departments & Hold Professional CredentialsConsult with Retail & Institutional FirmsOffer Full Array of IA Compliance ServicesReasonably Priced at Midwest Rates

RIA Compliance Consultants, Inc. is not a law firm and does not provide legal services.

Copy of Slides

• To access a copy of the slides from today’s presentation please go to:

www.RIA-Compliance-Consultants.com/PreparingForRegulatoryExam.html

Schedule Introductory Call via Online Appointment System

https://my.timedriver.com/QQ21L

Thank You

Tammy EmsickSenior Compliance Consultant

RIA Compliance Consultants, Inc.877-345-4034 x 102

![[ COPY ] Memory and Learning - Psychology slides](https://static.fdocuments.us/doc/165x107/587c3d9a1a28ab5a1d8b58b3/-copy-memory-and-learning-psychology-slides.jpg)