Preparatory Survey on Chittagong Area - JICAopen_jicareport.jica.go.jp/pdf/12233870_01.pdf ·...

368

Preparatory Survey on Chittagong Area Coal Fired Power Plant Development Project in Bangladesh Final Report on Power Plant / Port / Transmission Line / Access Road / Execution Survey of Natural Condition Book 4 For Publishing March 2015 Japan International Cooperation Agency (JICA) Tokyo Electric Power Services Co., LTD Tokyo Electric Power Co., LTD Ministry of Power, Energy and Mineral Resources People's Republic of Bangladesh

Transcript of Preparatory Survey on Chittagong Area - JICAopen_jicareport.jica.go.jp/pdf/12233870_01.pdf ·...

Preparatory Survey on Chittagong Area

Coal Fired Power Plant Development Project in Bangladesh

Final Report

on

Power Plant / Port /

Transmission Line / Access Road /

Execution Survey of Natural Condition

Book 4

For Publishing

March 2015

Japan International Cooperation Agency (JICA)

Tokyo Electric Power Services Co., LTD

Tokyo Electric Power Co., LTD

Ministry of Power, Energy and Mineral Resources

People's Republic of Bangladesh

Preparatory Survey on Chittagong Area

Coal Fired Power Plant Development Project in Bangladesh

Final Report

on

Power Plant / Port /

Transmission Line / Access Road /

Execution Survey of Natural Condition

Book 4

For Publishing

March 2015

Japan International Cooperation Agency (JICA)

Tokyo Electric Power Services Co., LTD

Tokyo Electric Power Co., LTD

Ministry of Power, Energy and Mineral Resources

People's Republic of Bangladesh

Preparatory Survey on Chittagong Area Coal Fired Power Plant Development Project in Bangladesh Final Report on Power Plant / Port / Transmission Line / Access Road / Execution Survey of Natural Condition

i

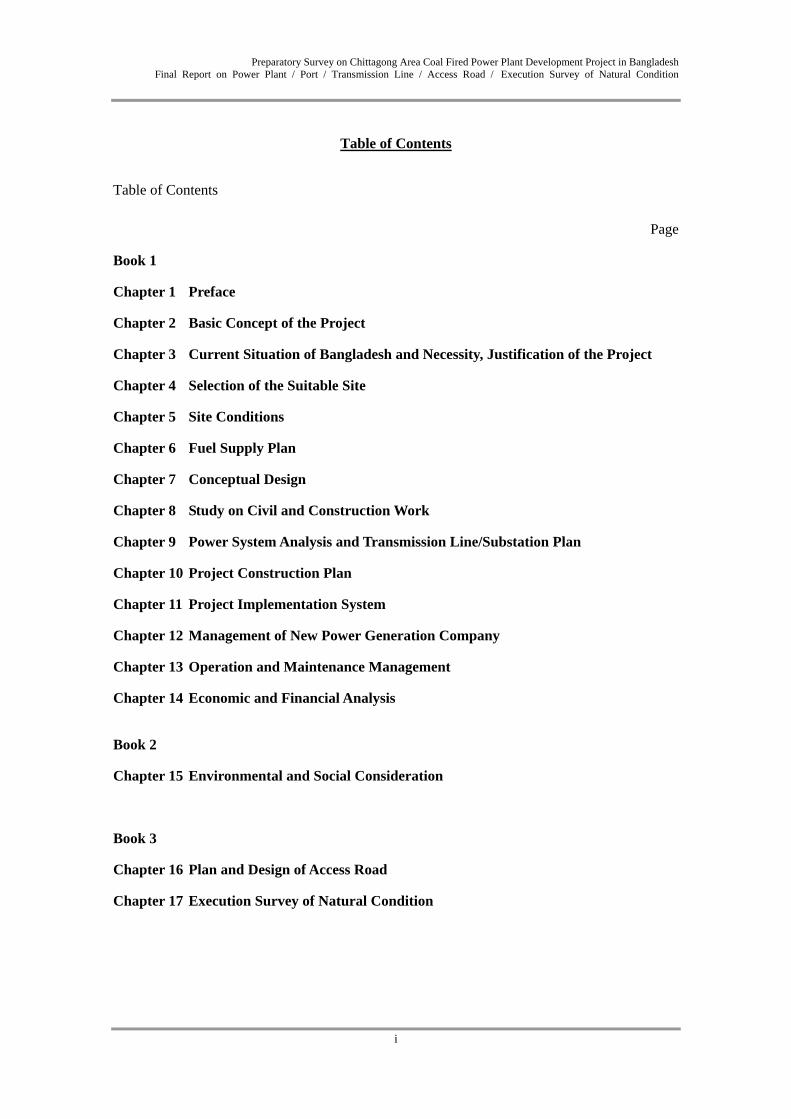

Table of Contents

Table of Contents

Page

Book 1

Chapter 1 Preface

Chapter 2 Basic Concept of the Project

Chapter 3 Current Situation of Bangladesh and Necessity, Justification of the Project

Chapter 4 Selection of the Suitable Site

Chapter 5 Site Conditions

Chapter 6 Fuel Supply Plan

Chapter 7 Conceptual Design

Chapter 8 Study on Civil and Construction Work

Chapter 9 Power System Analysis and Transmission Line/Substation Plan

Chapter 10 Project Construction Plan

Chapter 11 Project Implementation System

Chapter 12 Management of New Power Generation Company

Chapter 13 Operation and Maintenance Management

Chapter 14 Economic and Financial Analysis

Book 2

Chapter 15 Environmental and Social Consideration

Book 3

Chapter 16 Plan and Design of Access Road

Chapter 17 Execution Survey of Natural Condition

Preparatory Survey on Chittagong Area Coal Fired Power Plant Development Project in Bangladesh Final Report on Power Plant / Port / Transmission Line / Access Road / Execution Survey of Natural Condition

ii

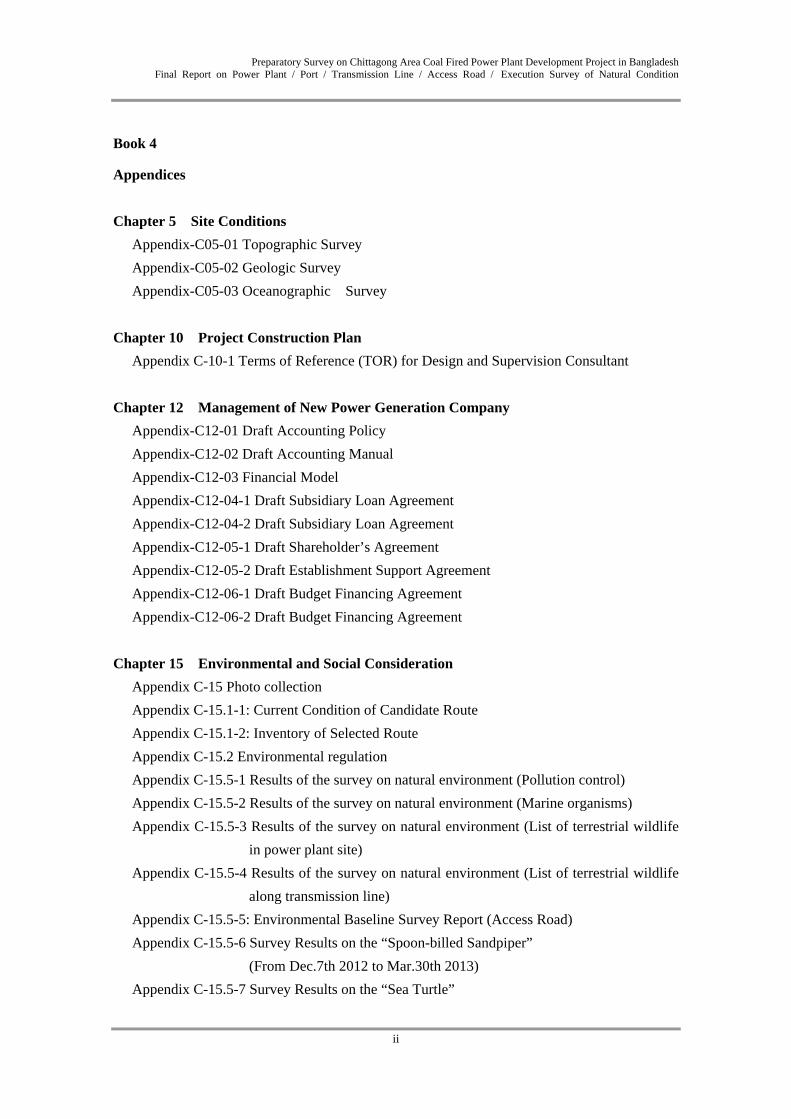

Book 4

Appendices

Chapter 5 Site Conditions

Appendix-C05-01 Topographic Survey

Appendix-C05-02 Geologic Survey

Appendix-C05-03 Oceanographic Survey

Chapter 10 Project Construction Plan

Appendix C-10-1 Terms of Reference (TOR) for Design and Supervision Consultant

Chapter 12 Management of New Power Generation Company

Appendix-C12-01 Draft Accounting Policy

Appendix-C12-02 Draft Accounting Manual

Appendix-C12-03 Financial Model

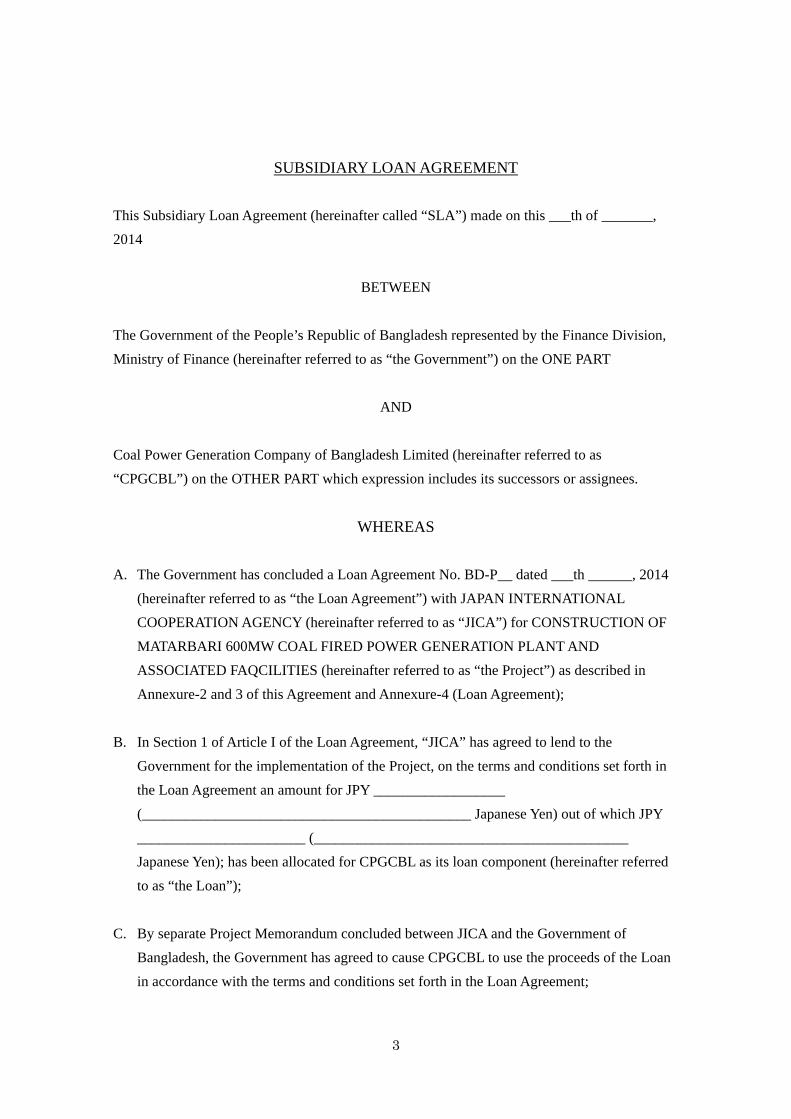

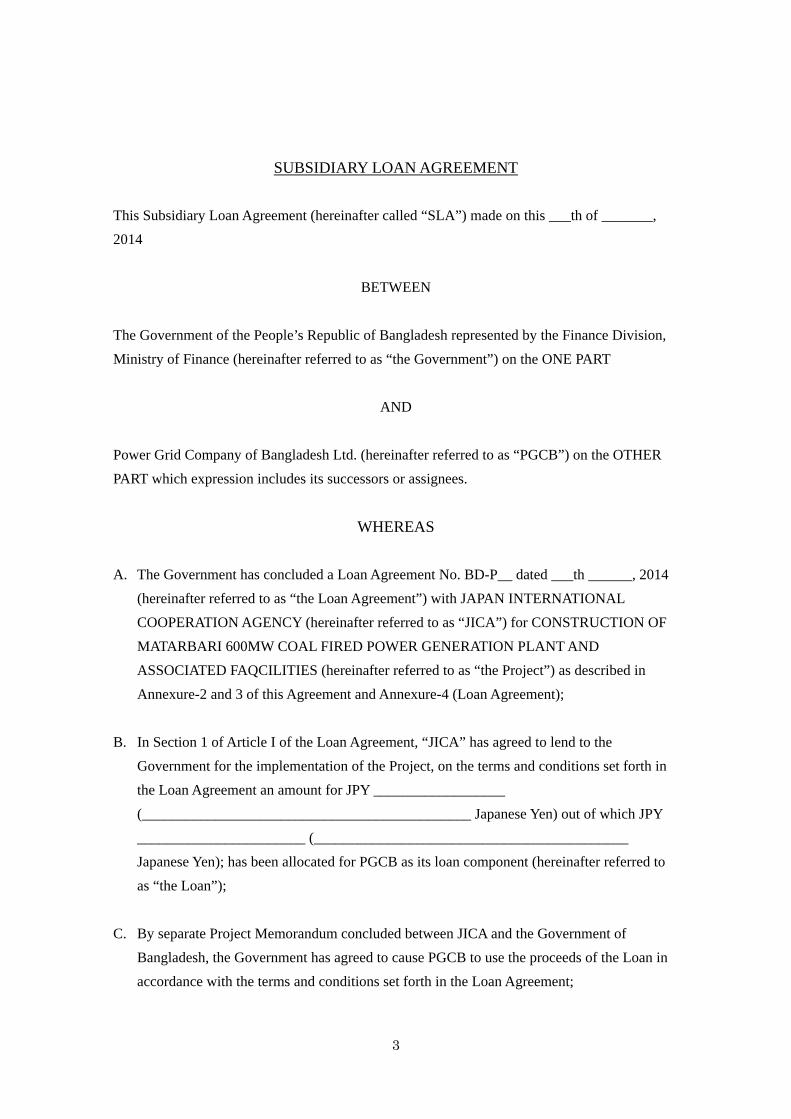

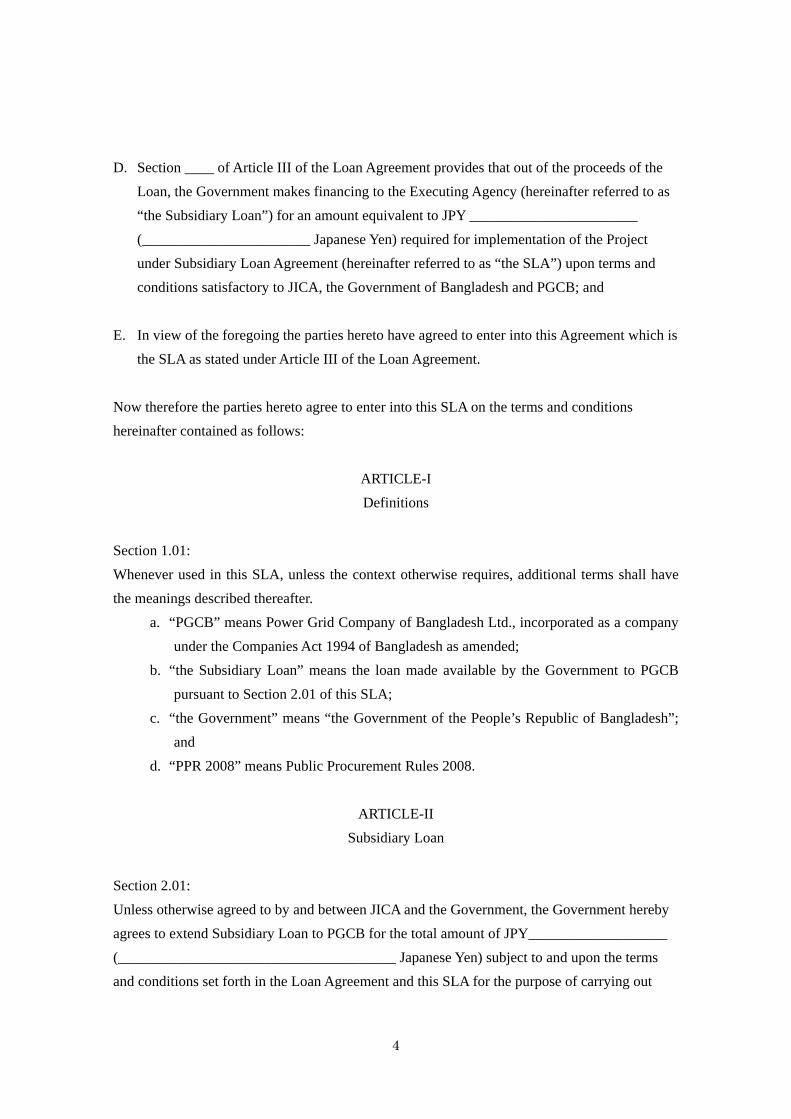

Appendix-C12-04-1 Draft Subsidiary Loan Agreement

Appendix-C12-04-2 Draft Subsidiary Loan Agreement

Appendix-C12-05-1 Draft Shareholder’s Agreement

Appendix-C12-05-2 Draft Establishment Support Agreement

Appendix-C12-06-1 Draft Budget Financing Agreement

Appendix-C12-06-2 Draft Budget Financing Agreement

Chapter 15 Environmental and Social Consideration

Appendix C-15 Photo collection

Appendix C-15.1-1: Current Condition of Candidate Route

Appendix C-15.1-2: Inventory of Selected Route

Appendix C-15.2 Environmental regulation

Appendix C-15.5-1 Results of the survey on natural environment (Pollution control)

Appendix C-15.5-2 Results of the survey on natural environment (Marine organisms)

Appendix C-15.5-3 Results of the survey on natural environment (List of terrestrial wildlife

in power plant site)

Appendix C-15.5-4 Results of the survey on natural environment (List of terrestrial wildlife

along transmission line)

Appendix C-15.5-5: Environmental Baseline Survey Report (Access Road)

Appendix C-15.5-6 Survey Results on the “Spoon-billed Sandpiper”

(From Dec.7th 2012 to Mar.30th 2013)

Appendix C-15.5-7 Survey Results on the “Sea Turtle”

Preparatory Survey on Chittagong Area Coal Fired Power Plant Development Project in Bangladesh Final Report on Power Plant / Port / Transmission Line / Access Road / Execution Survey of Natural Condition

iii

(From Dec.7th 2012 to Mar.30th 2013)+ (Inc. Addistional)+

Appendix C-15.5-8 Materials for Stakeholder meeting

Appendix C-15.5-9 Minutes of Stakeholder meeting

Appendix C-15.6 Results of the Air Pollutant Diffusion Simulation on the case of theLower

Stack (200m)

Appendix C-15.9-1 Land Acquisition and Resettlement Action Plan (Draft)

(Power Plant, Port Facility and Transmission Line)

Appendix C-15.9-2: Land Acquisition and Resettlement Action Plan(LARAP)

(Access Road)

Appendix C-15.9-3 Materials for public consultation meeting

Appendix C-15.9-4 Minutes of public consultation meeting

Book 5

Appendices for

Chapter 16

Chapter 17

Appendix-C05-01

Topographic Survey

1

Topographic Survey

The topographical survey has been conducted in the survey area with the following procedure.

(1) Overview

-Survey period

・ From September 28, 2012, to October 12, 2012

-Survey area

・ The survey area is located at Matarbari, Cox’s Bazar.

(2) Methodology

-Working grids

・ To execute the field survey the survey area was divided into squares of 100m×100m by

fixing northing and easting at 100m center to center.

・ All the data taken is based on N, E, and Z as

N ; Northing

E ; Easting

Z ; Leveling / Elevation

-Instrumental Values

・Total Station : Leica 09 - 2 set

・RTK GPS Total Station : Trimble5700 - 1 set

・Auto Level : SokkiaB2 - 2 set

・ GPS (Handheld) : Germin Tracker - 2 setInstruments used: Total Station (TOP CON-105)

・ Level Instrument Nikon

(3) Bench Mark

All TMBs were established using RTK GPS and Total Station. The base station for thereference

was SoB GPS BM No 322. This BM is located at SW corner of play ground of Maijpara

Registered non govt primary school, east side of Chittagong- Coxs bazar highway and 22 m SW

from the SW corner of school building of villaga Maijpara, upozila Chokoria and district Cox’s

Bazar.

-Position of SoB GPS BM No 322:

Latitude = 21º 39' 49.54171"

Longitude = 92º 04' 30.39946"

RL = 4.6182m MSL

In WGS 84 coordinate system

The Values of TBMs are as follows in UTM GRID:

2

-TBM-1

X= 383604.569mE、Y= 2400623.167mN、Z= 2.341mMSL

-TBM-5

X= 383602.853mE、Y= 2400589.010mN、Z= 2.725mMSL

Figure -1 Reference SoB GPS BM No 322

Figure -2 Topographic Survey at TBM-1

(4) Mapping

The total area to be mapped for the power plant site of this project is 4.0 sq km.

A drawing of the Topographical Map of the survey Area is provided in Figure -3.

3

Figure -3 Drawing of a topographical map of the project site

TBM-1 EL=2.341m(MSL)

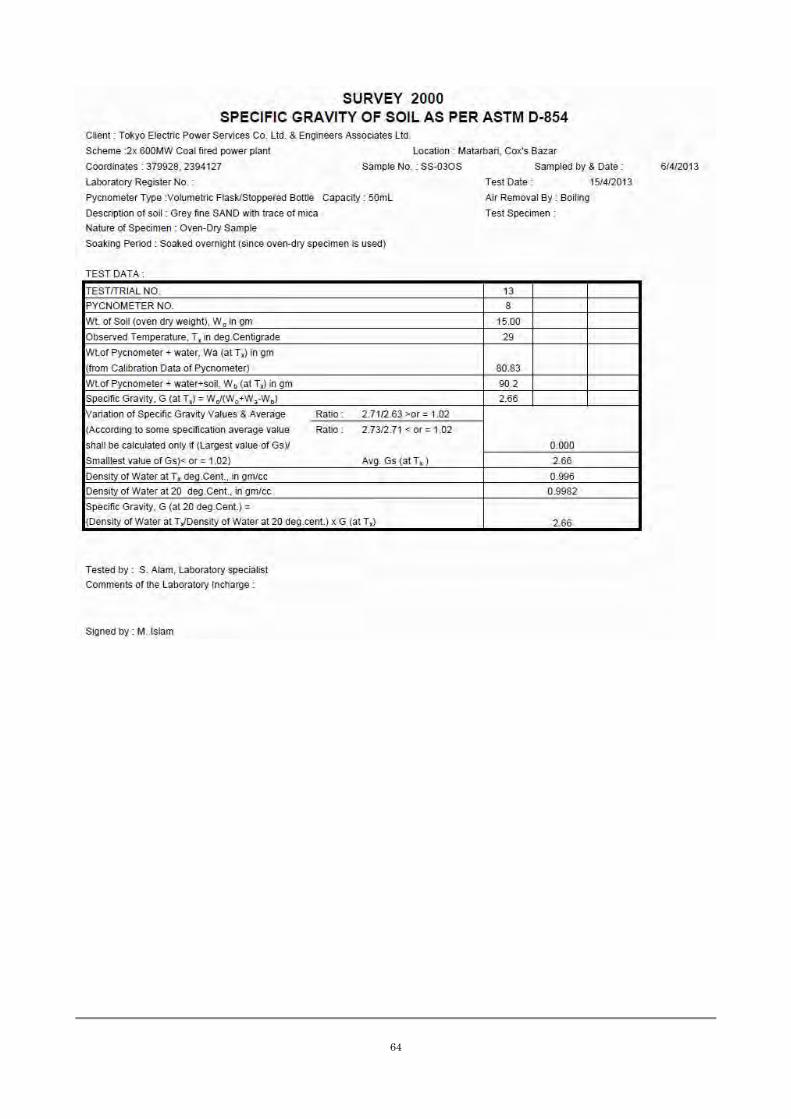

Appendix-C05-02

Geologic Survey

1

Geologic Survey

The topographical survey has been conducted in the survey area with the following procedure.

(1) Overview

-Survey period

・ From September 28, 2012 to October 15, 2012

-Survey area

・ The project site is located at Matarbari, Cox’s Bazar

(2) Methodology

(3) Methodology

-Execution of Boring

The field boring was conducted using 100mm dia casing (BH-1~BH-6) and 120mm dia casing

(BH-01~BH-03). The method consists in first driving in a casing through which a hollow drill rod

with a sharp chisel or chopping bit at the lower end is inserted. Water is forced under pressure

through the drill rod which is alternatively raised and dropped, and also rotated. The soil cuttings are

forced up and dropped and also rotated. The soil cuttings are forced up to the ground in the drilled

rod and casing. Before taking a Standard Penetration Test (SPT) and collection of disturbed and

undisturbed soil samples, the bore hole is cleaned with repeated circulation of mud slurry.

-SPT (Standard Penetration Test)

SPTs were performed in all the bore holes. The tests were executed by using a thick walled split

sampler of 35 mm inner diameter and 50.8 mm outer diameter and 63.5 kg hammer falling freely

from a constant height of 75 cm. The SPT values (N-values) were taken as the summation of blows

required in the 2nd and 3rd 15 cm of penetration of the sampler. The SPT values (N-values) are shown

on the bore hole logs against the respective interval of tests.

The SPT provides considerable knowledge on the density and consistency of the soil layer

encountered and in addition yields disturbed /semi disturbed soil samples from within the split spoon

sampler used during the tests.

-Disturbed Sample Collection

The disturbed samples were collected with the help of a split spoon sampler used during the SPTs.

The collected samples were classified on site and were preserved in water tight polythene bags with

proper identification marks for onward transmission to the laboratory for further analysis.

The disturbed samples were also used to reconstruct depth wise stratification of bore holes

depending on their classifications.

2

-Undisturbed Sample Collection

The undisturbed samples were collected whenever feasible from the cohesive layers with the help of

thin walled Shelby tubes 76 mm diameter. Thin walled Shelby tubes are penetrated into the

undisturbed soil formation at the bottom of the borehole by applying rapid but continuous force.

The samples recovered within the Shelby tubes were wax sealed at both ends and transmitted to the

laboratory with proper identification marks.

-Recording of Ground Water

The ground water table was recorded in each of the boreholes by rope/rod sounding after 24 hours

of completion of the drilling and sampling operation.

-Other Field Tests

Other field tests, which were conducted at the site, were done according to AASHTO/ASTM

standards.

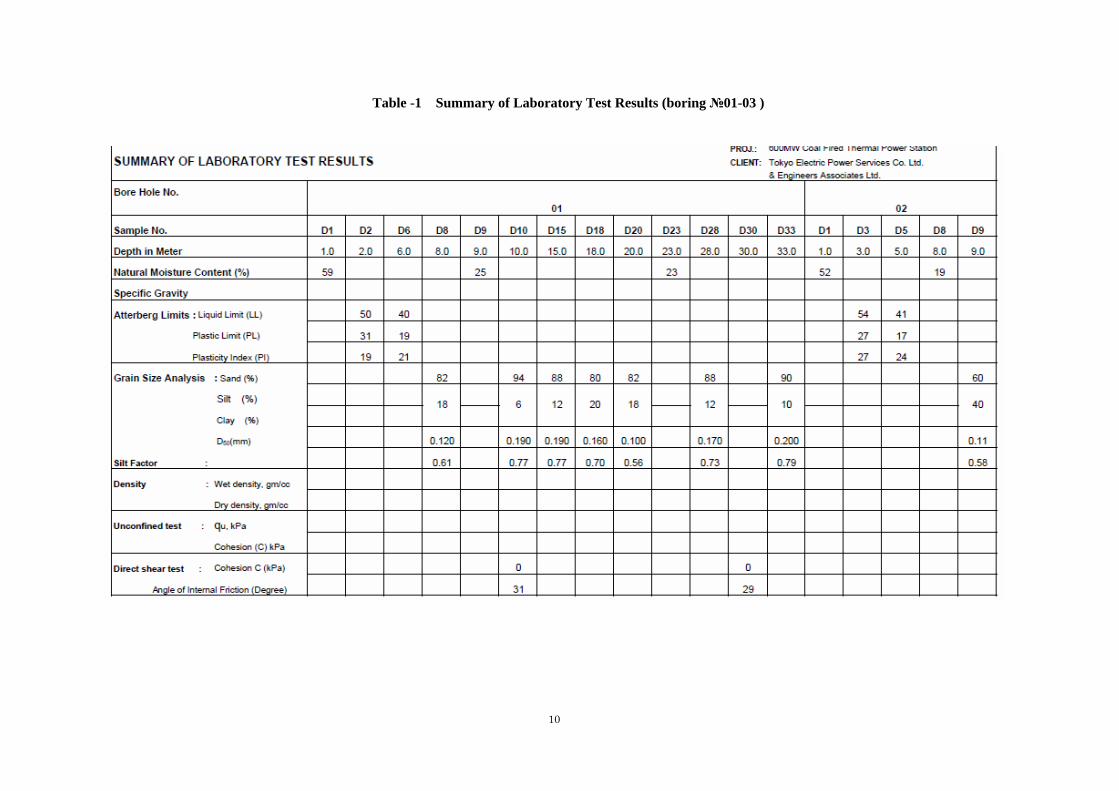

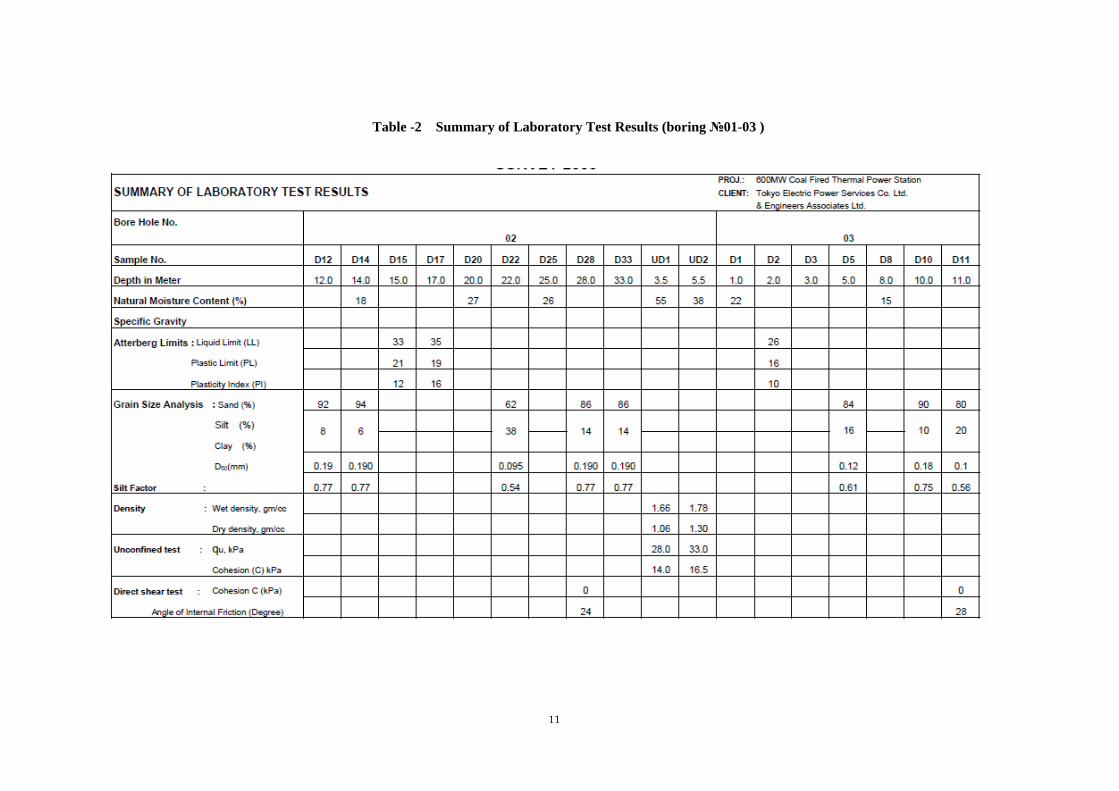

-Laboratory Tests

Different types of laboratory tests were performed in the laboratory to evaluate the physical and

engineering properties of the sub-soil formation to facilitate determination of soil bearing capacities

and to recommend foundation type and magnitude.

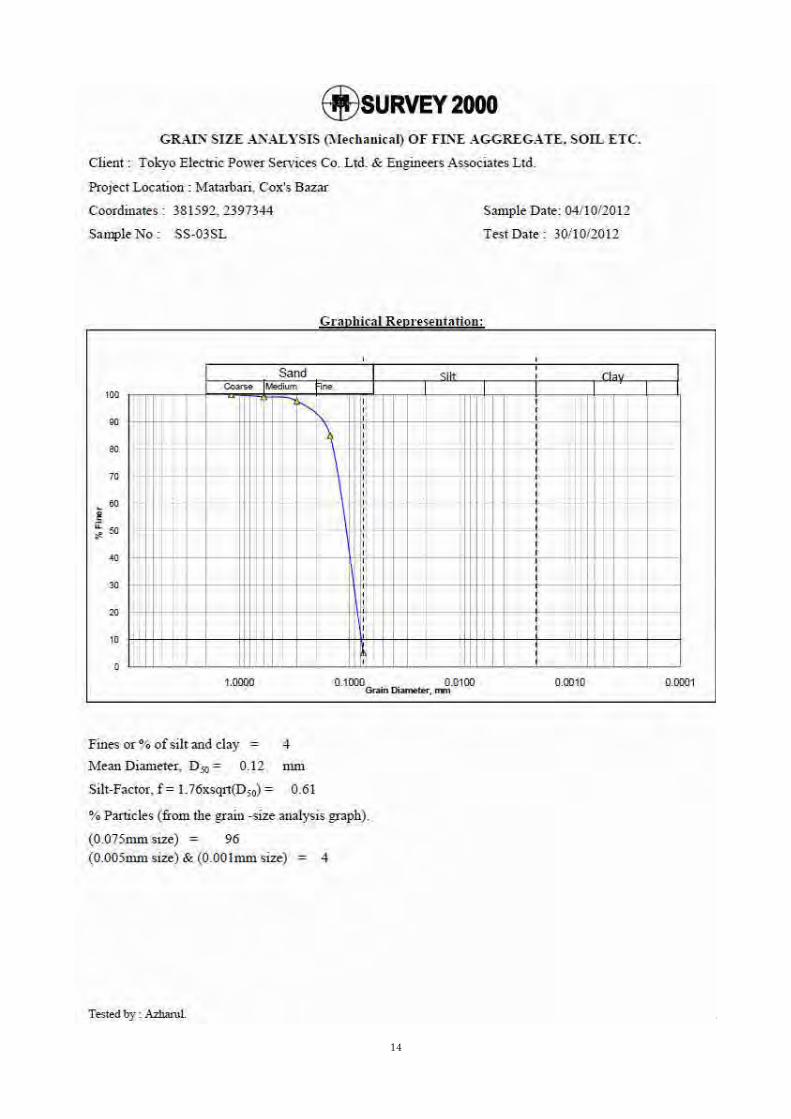

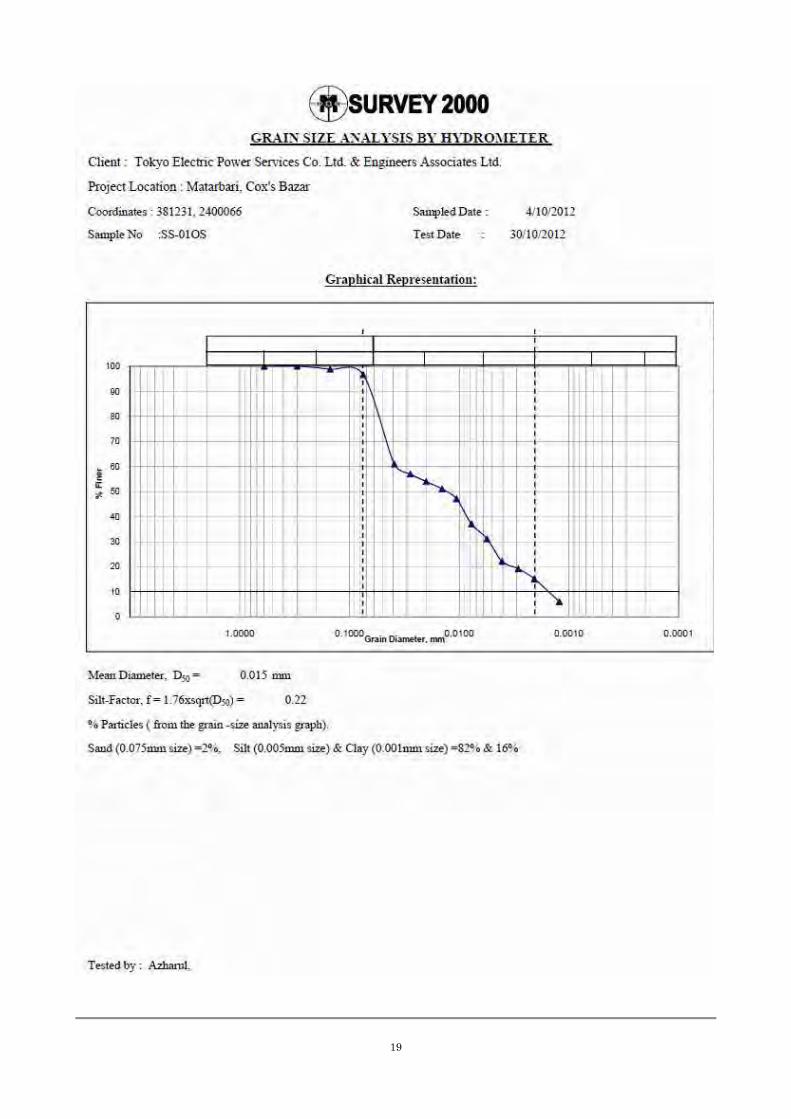

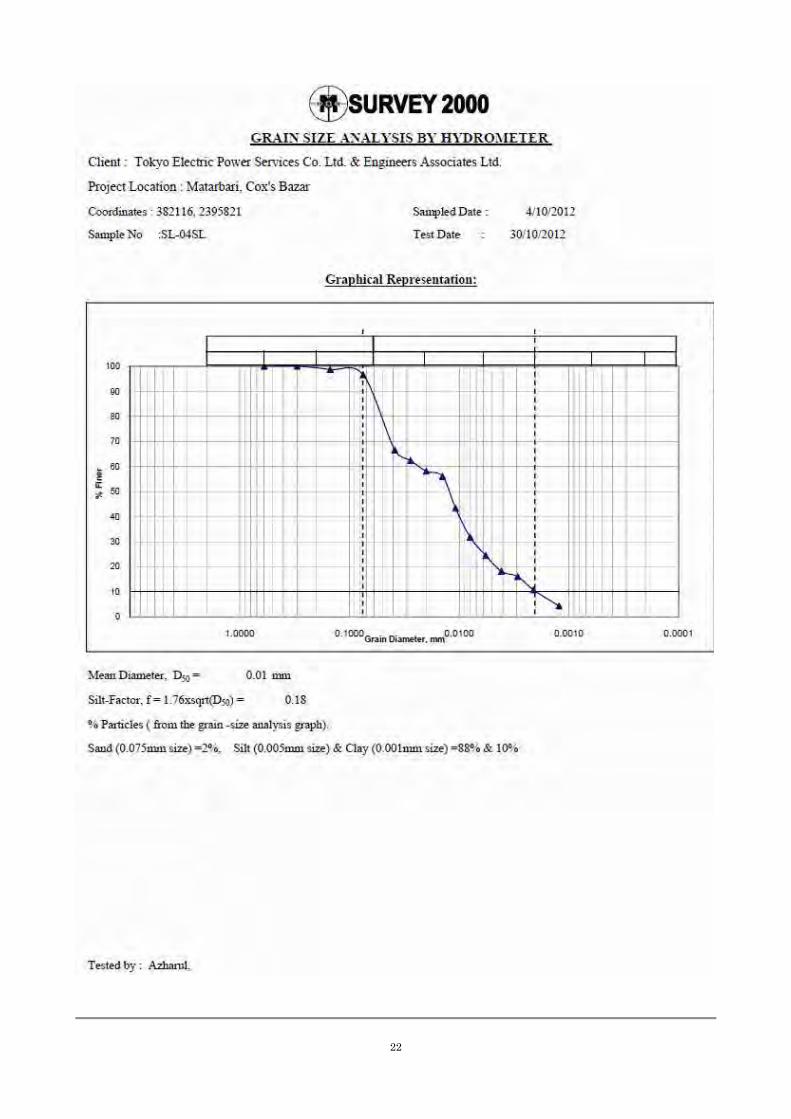

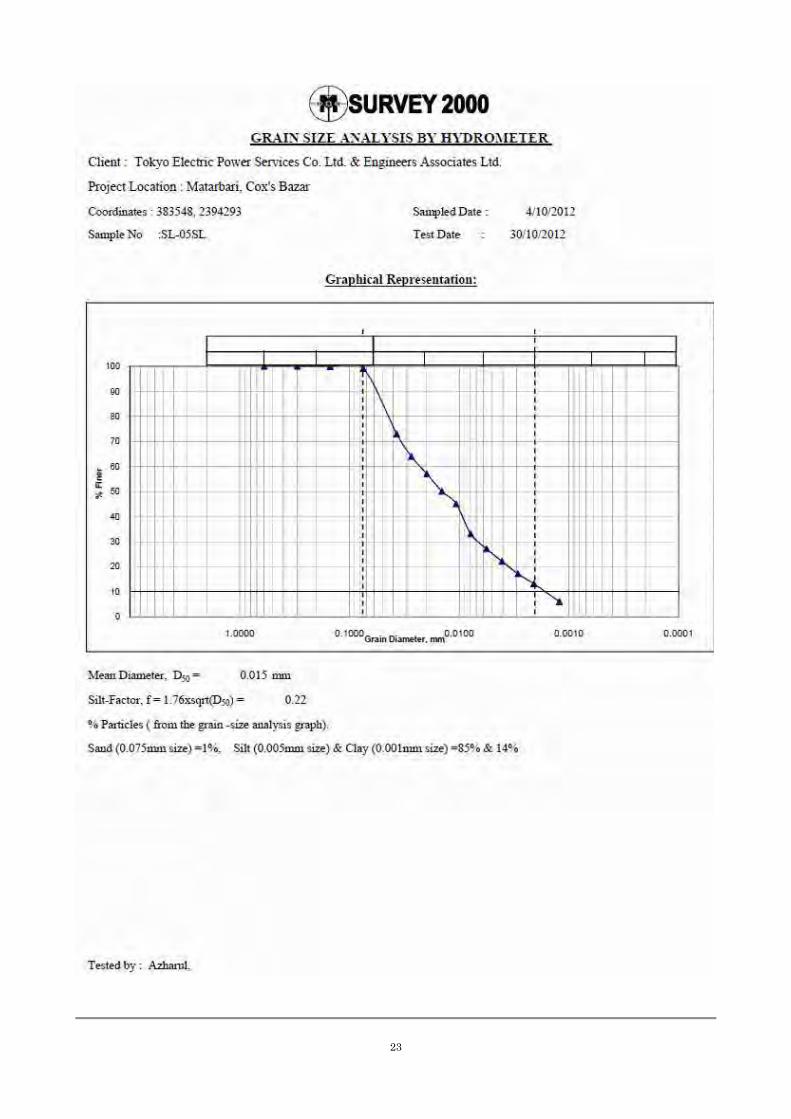

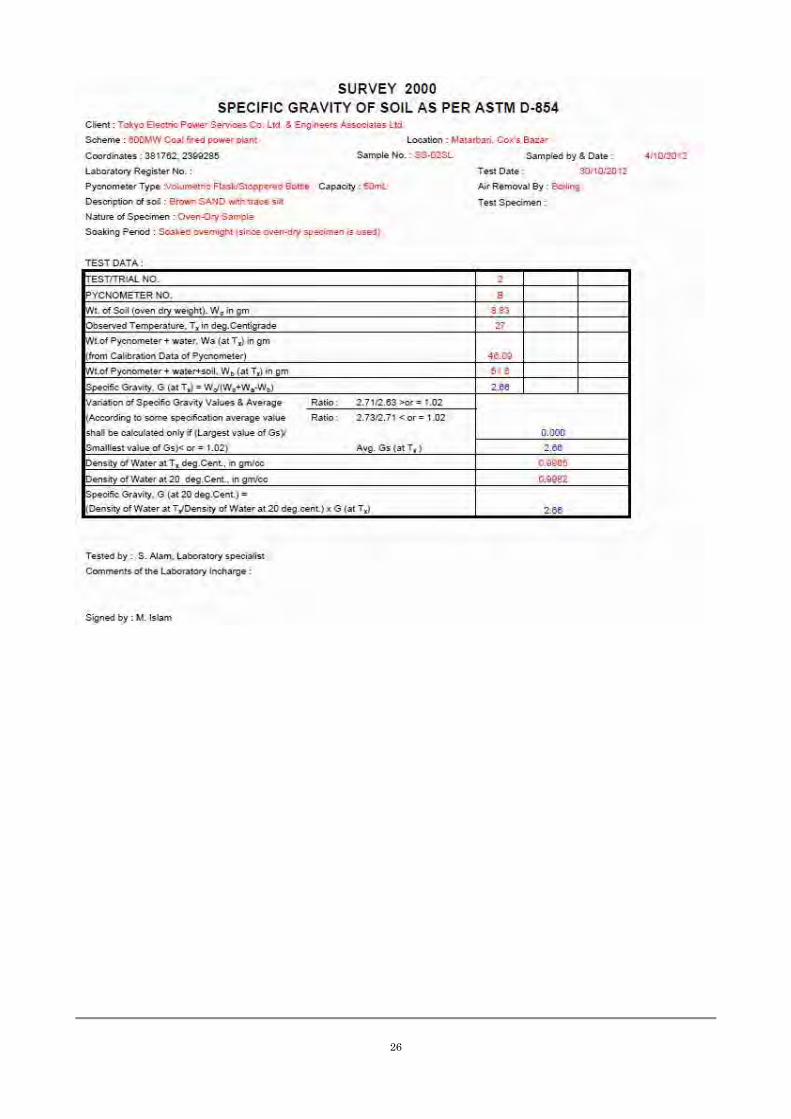

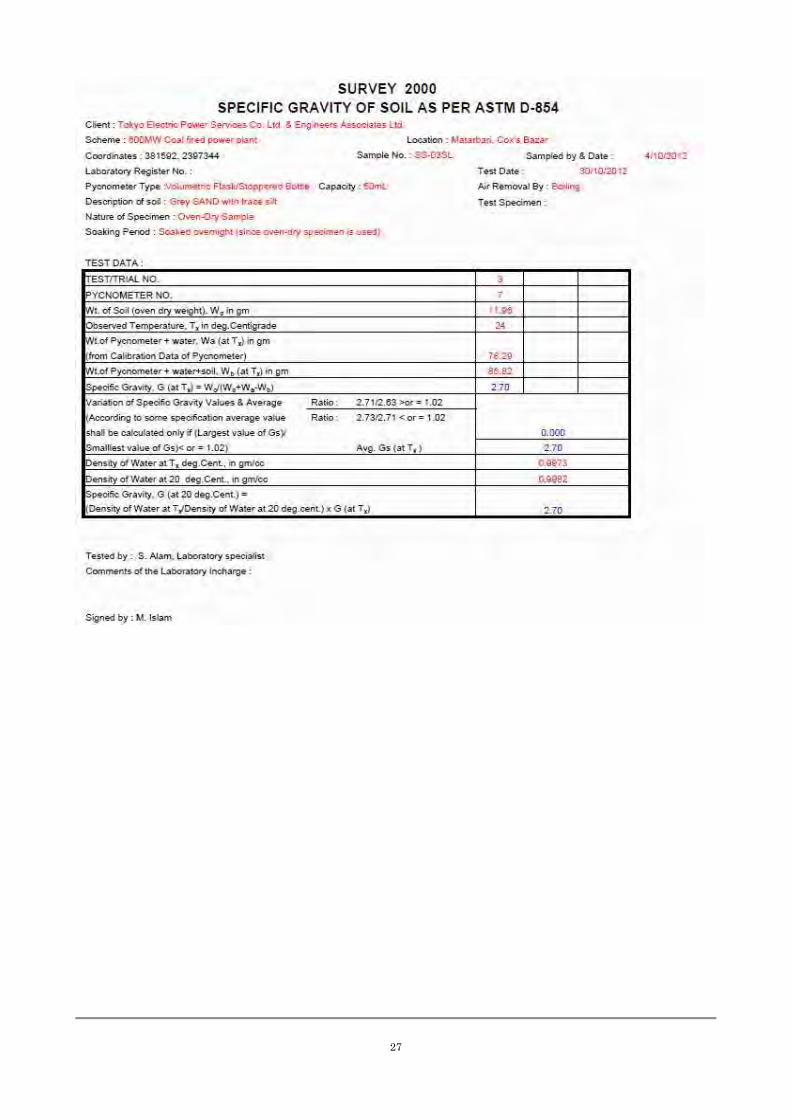

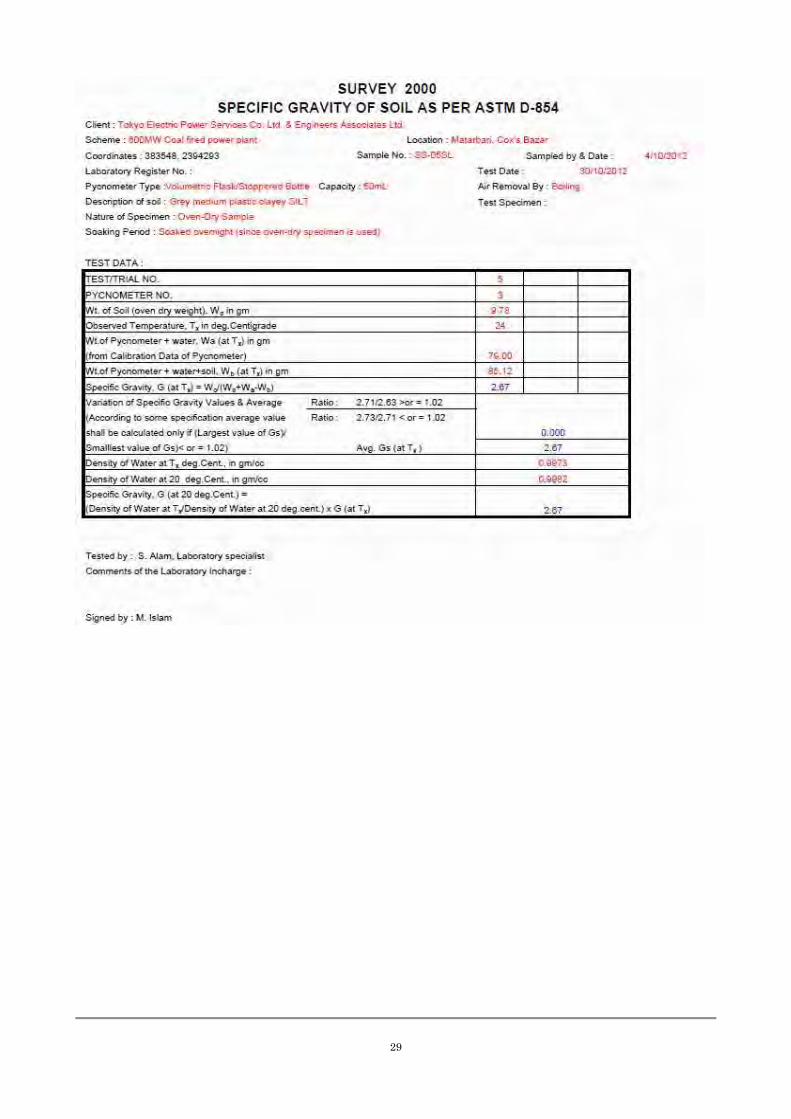

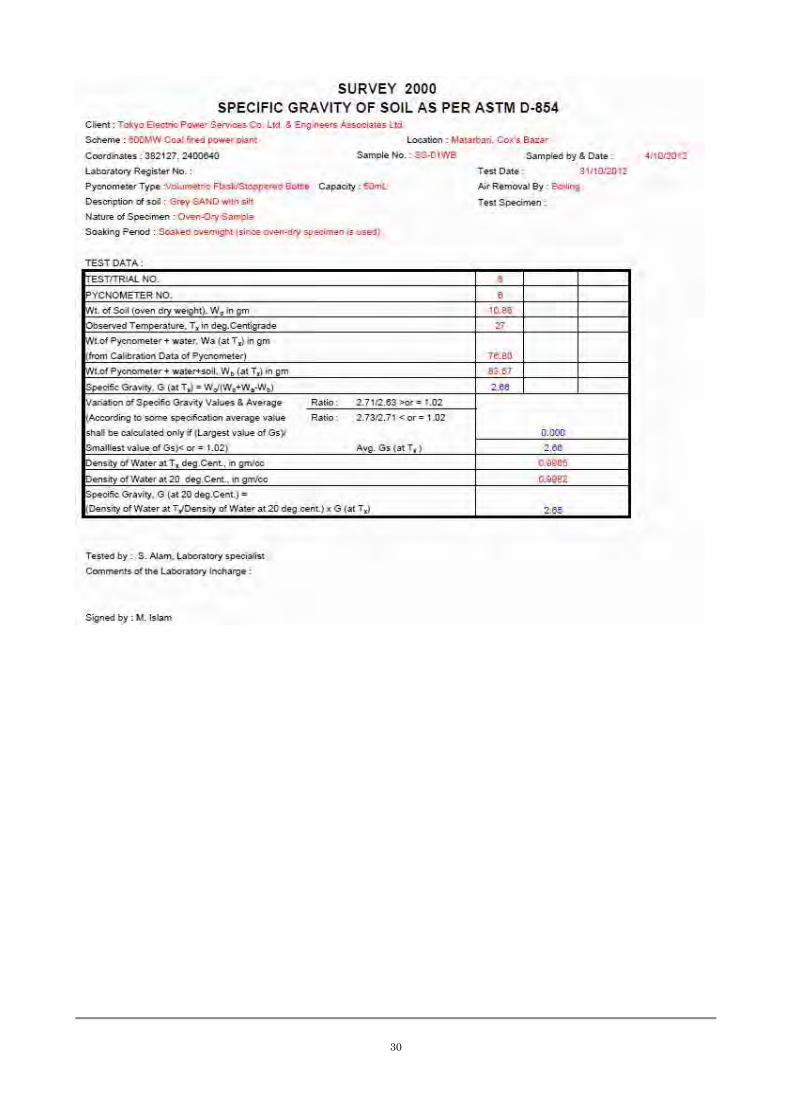

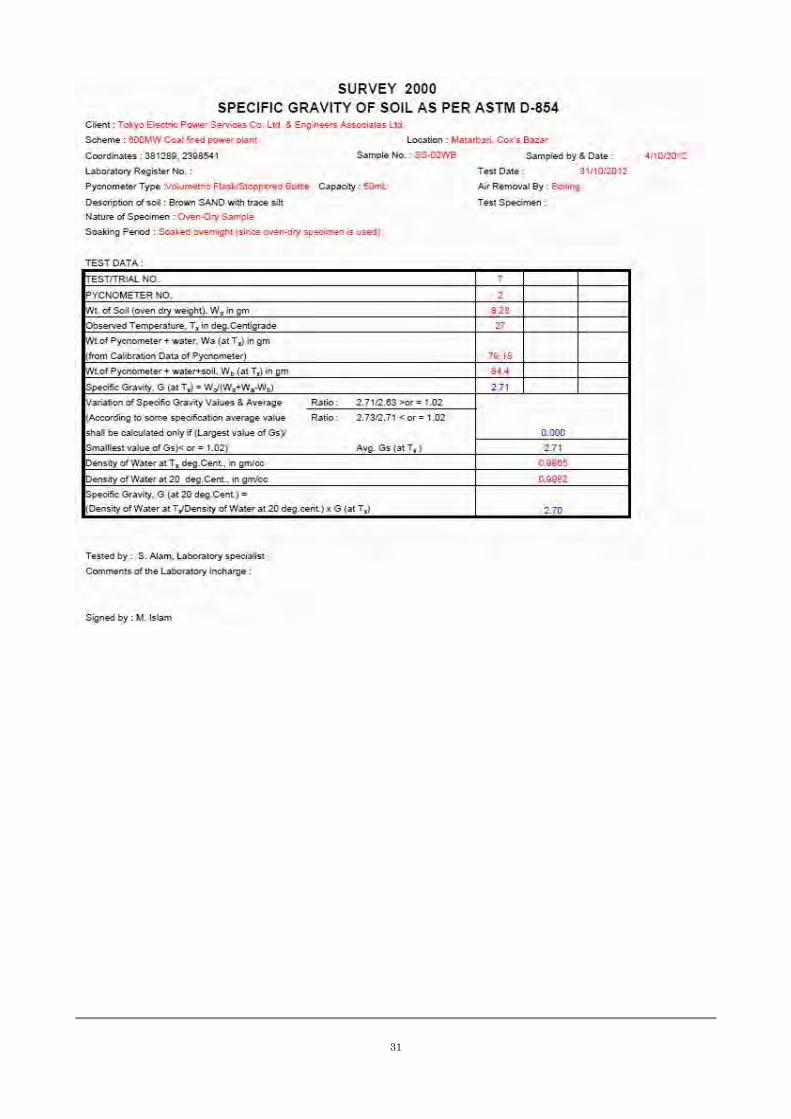

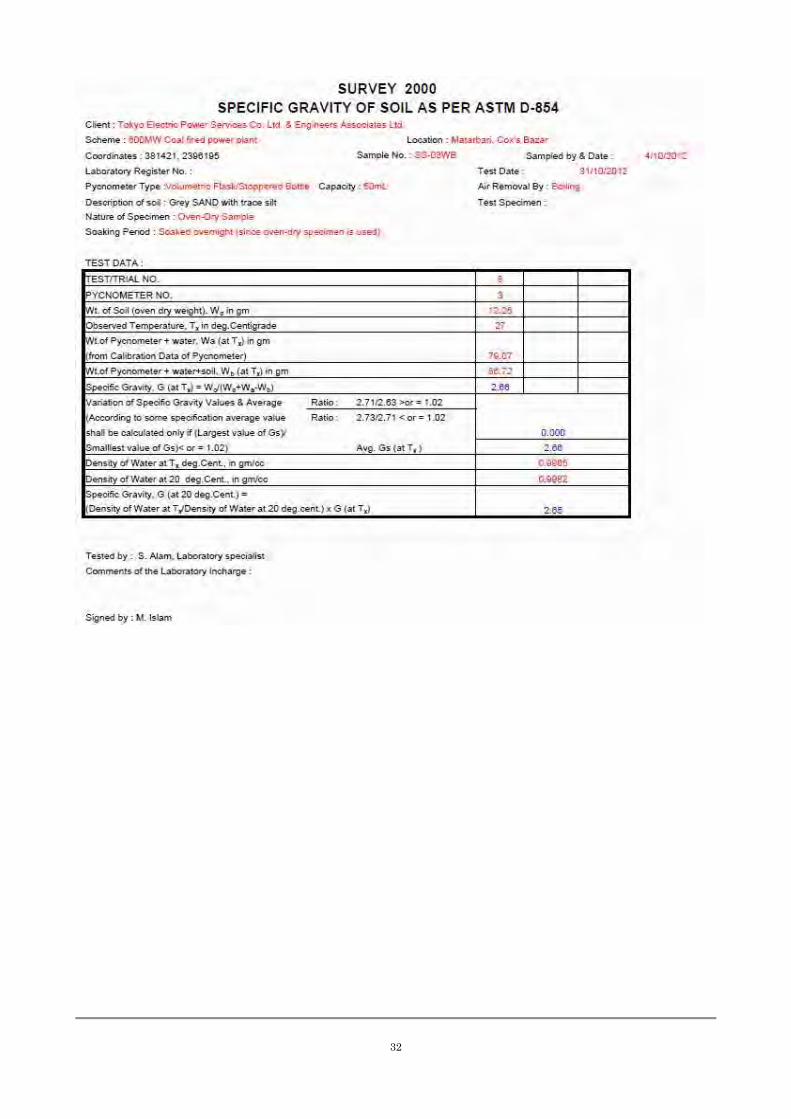

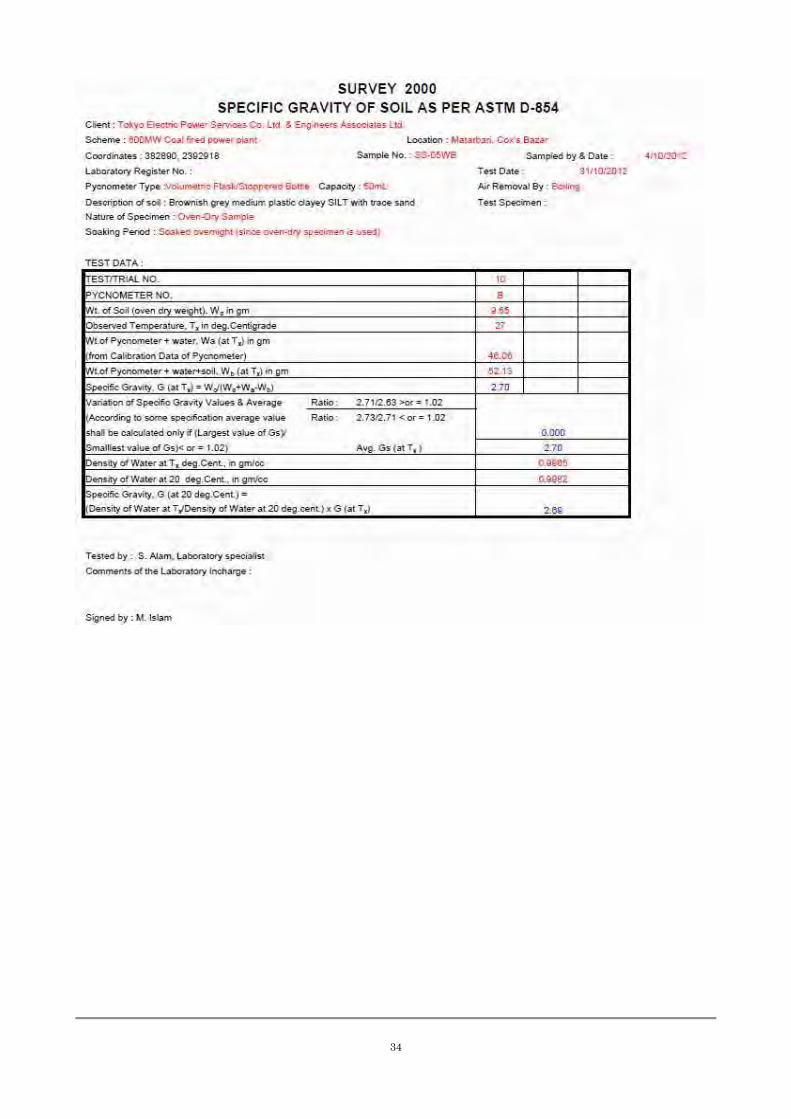

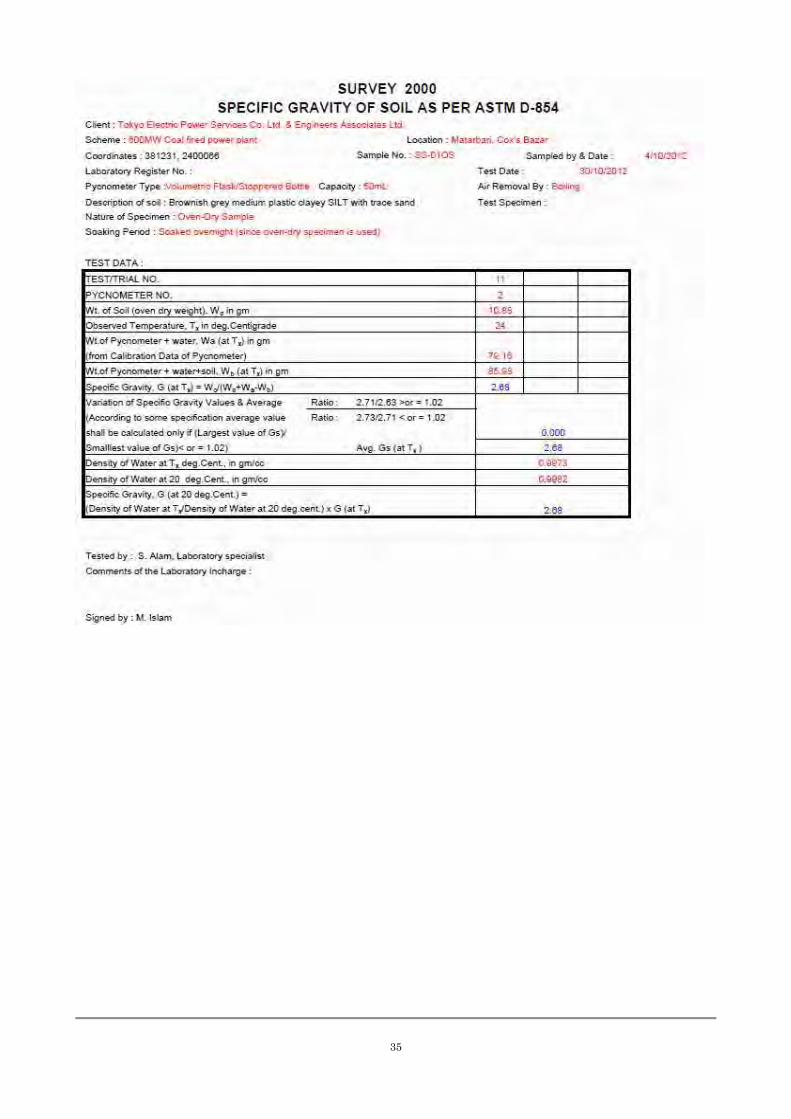

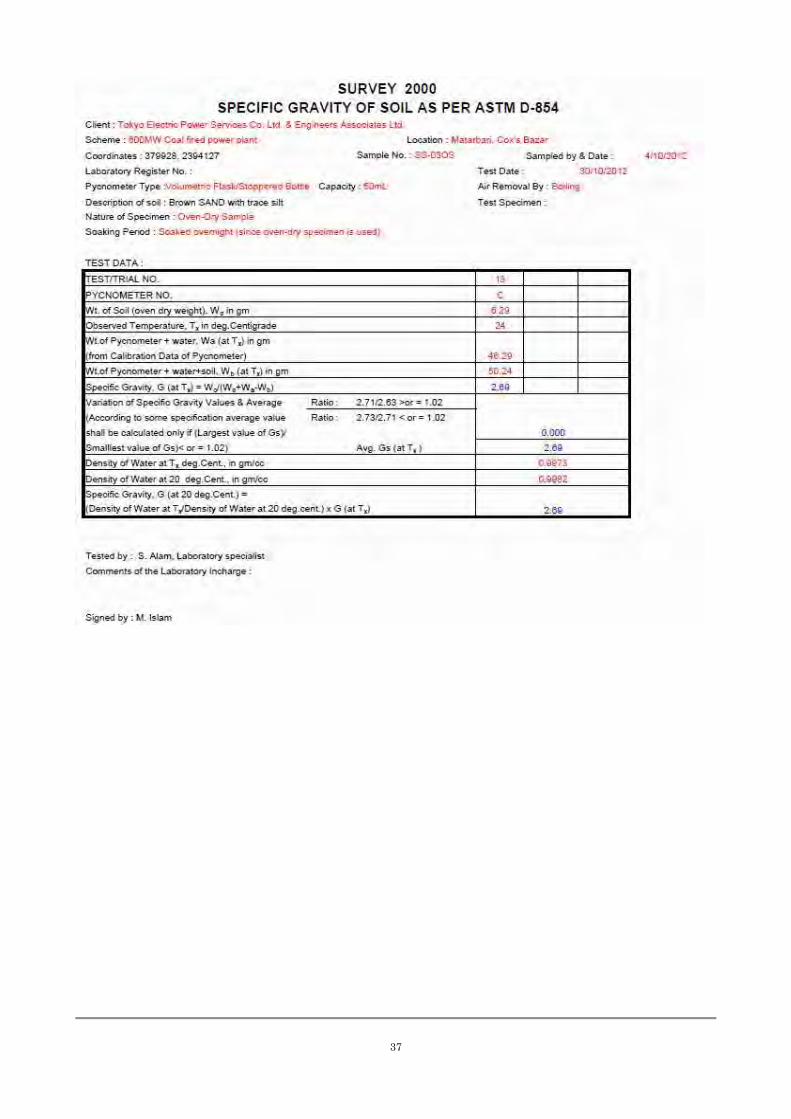

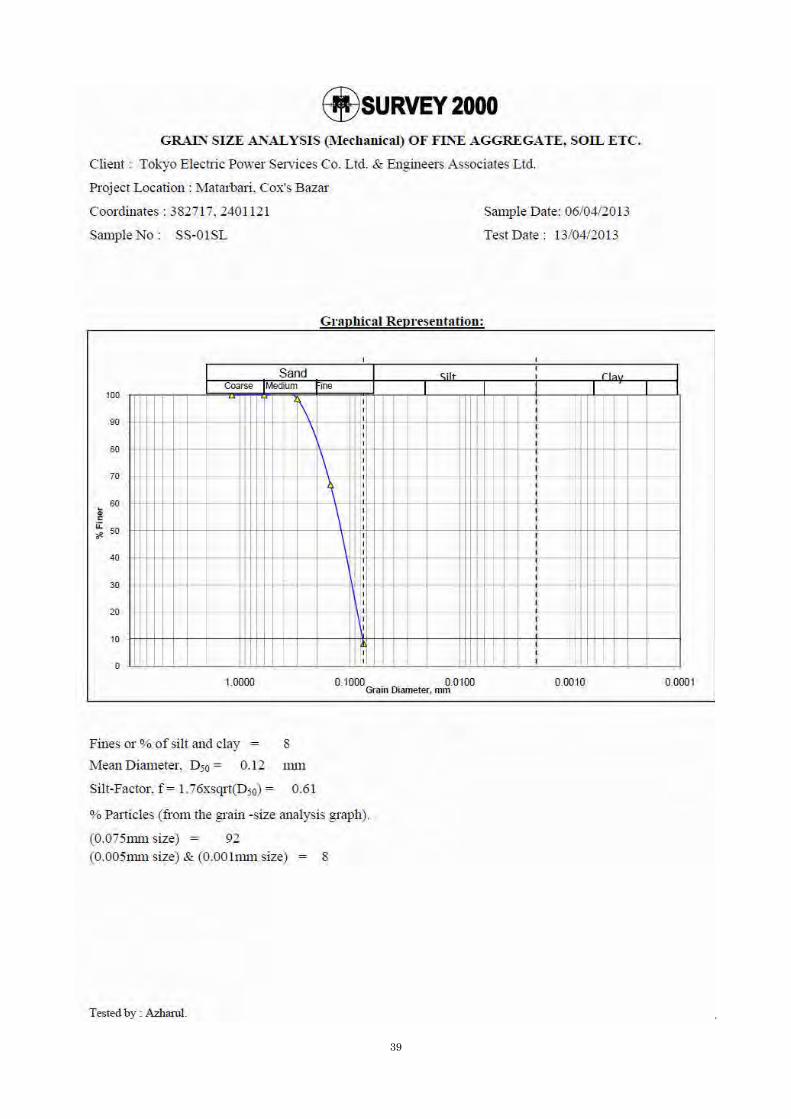

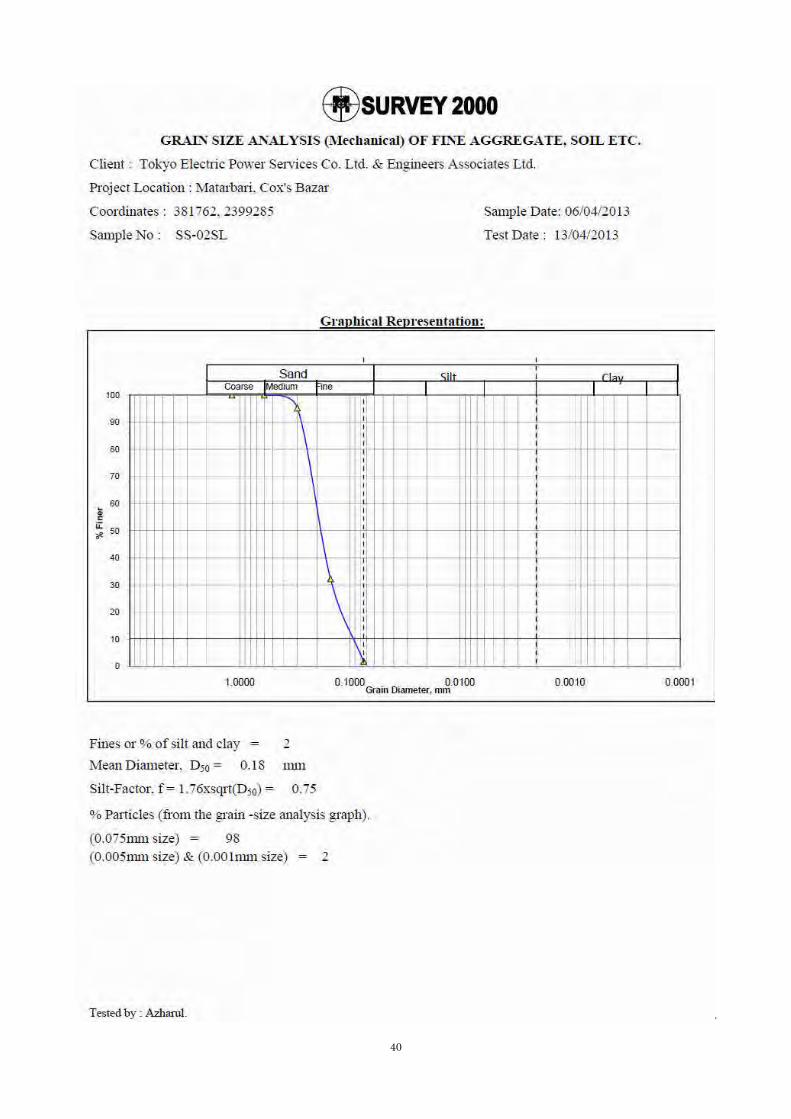

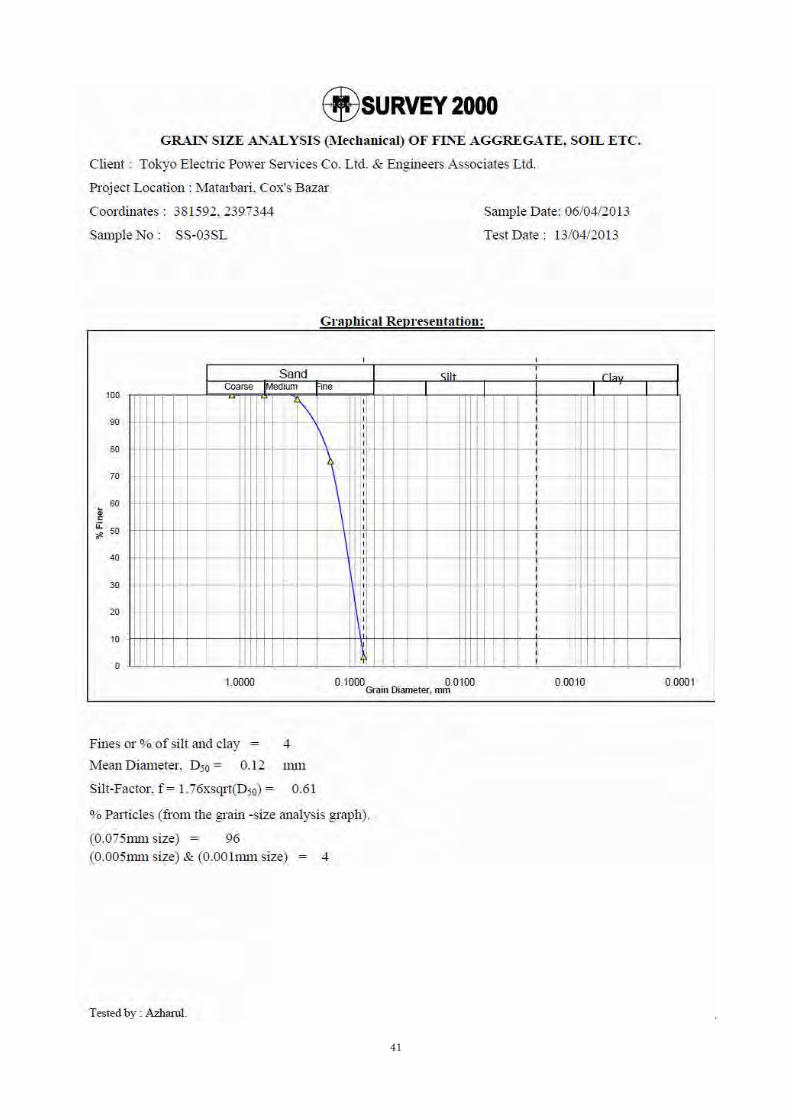

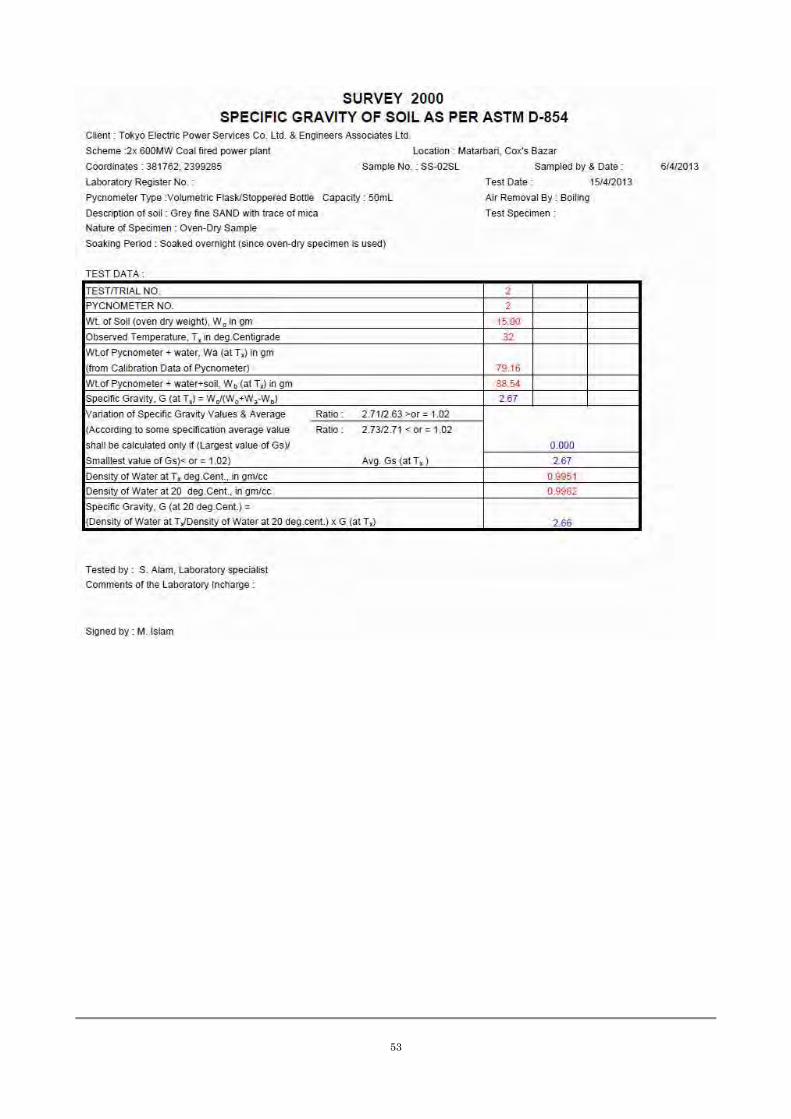

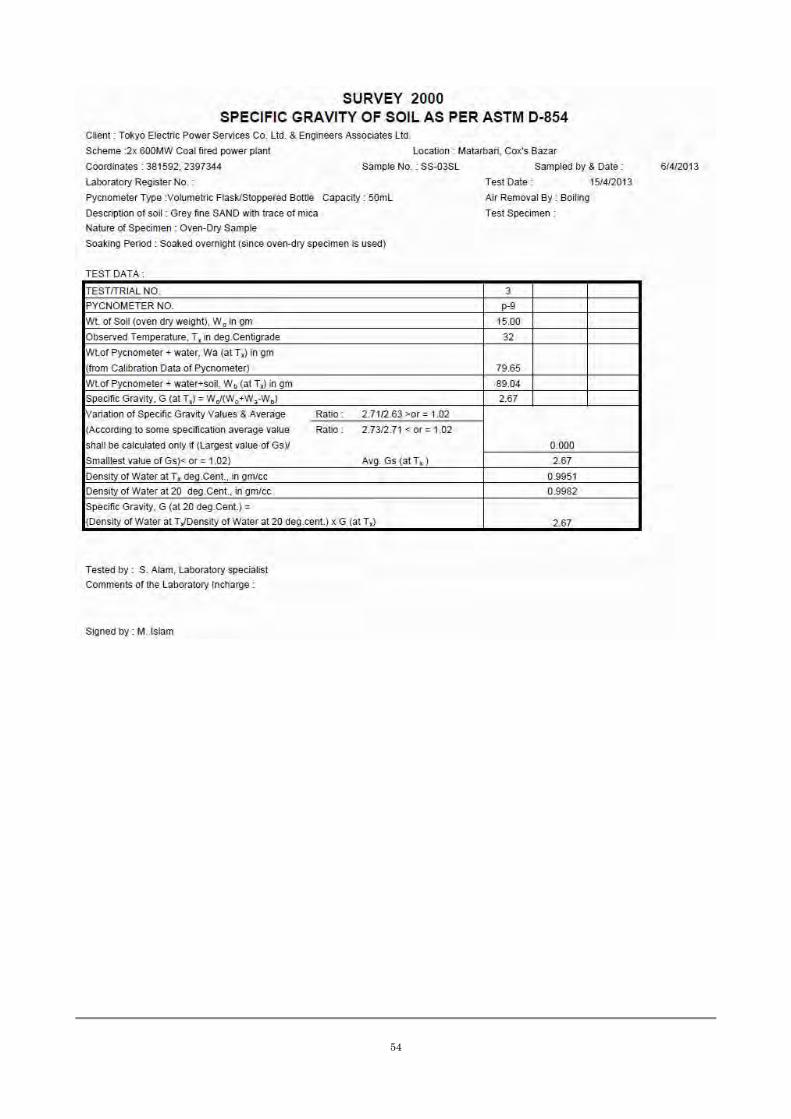

Grain size Analysis, Atterberg Limit and Sp .Gravity tests were performed to ascertain the detailed

composition of the soil and to evaluate the physical parameters of the formation. These tests also

help in classifying the soils properly for geological and geological interpretation.

Unconfined compression, density and shear tests were done to evaluate the shear characteristics of

the soils, which directly help in bearing capacity calculation.

Consolidation tests provide data on consolidation behavior of the sub-soil formation.

The laboratory tests were performed according to AASHTO/ASTM standards.

3

Figure -1 Soil boring at Matarbari site

Figure -2 Soil Sample collection at Matarbari

4

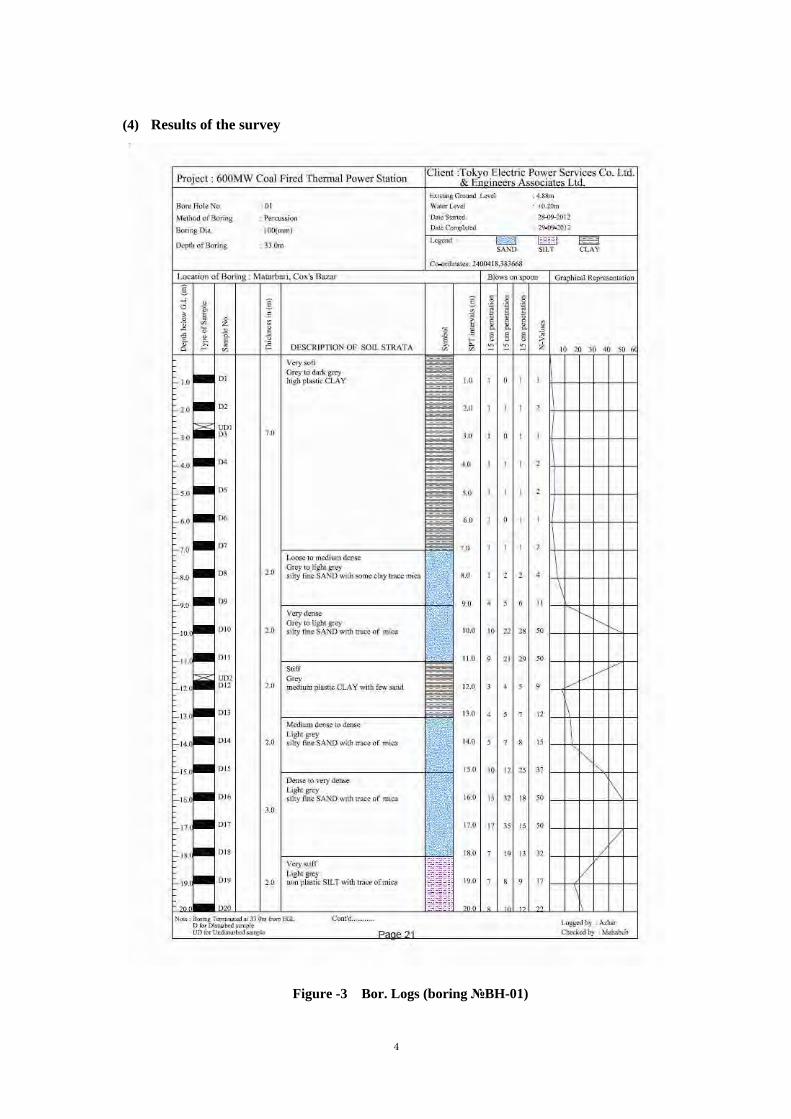

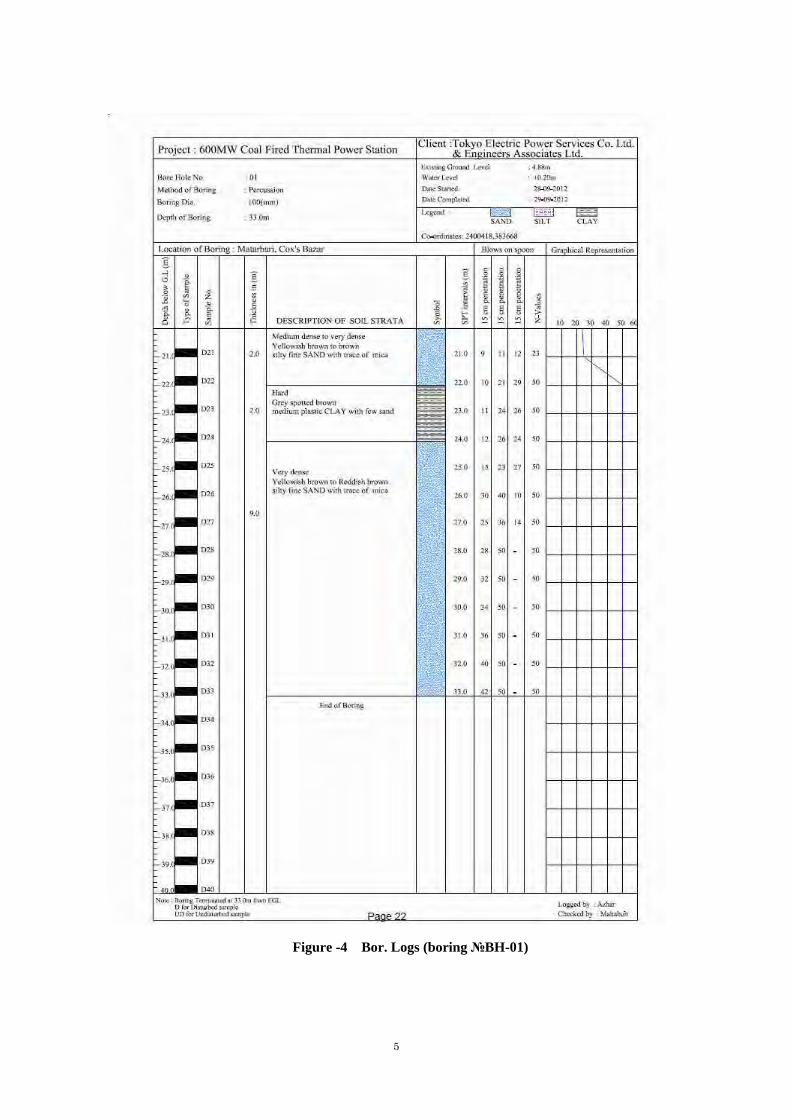

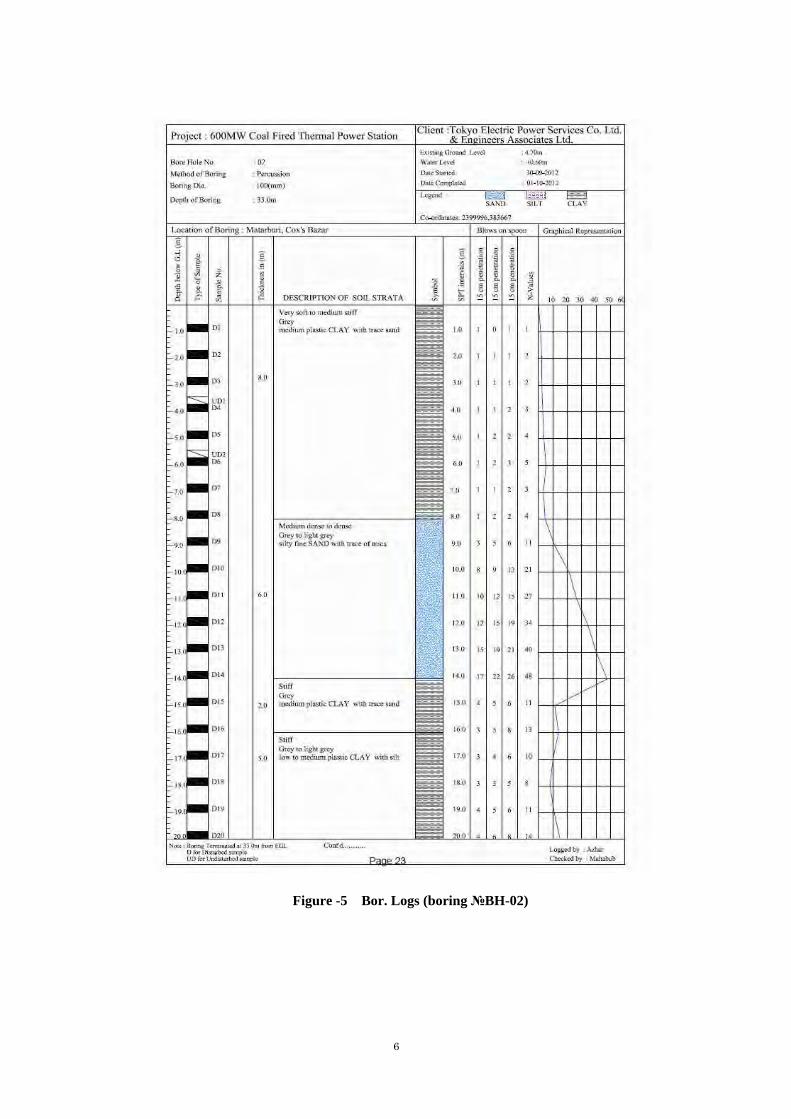

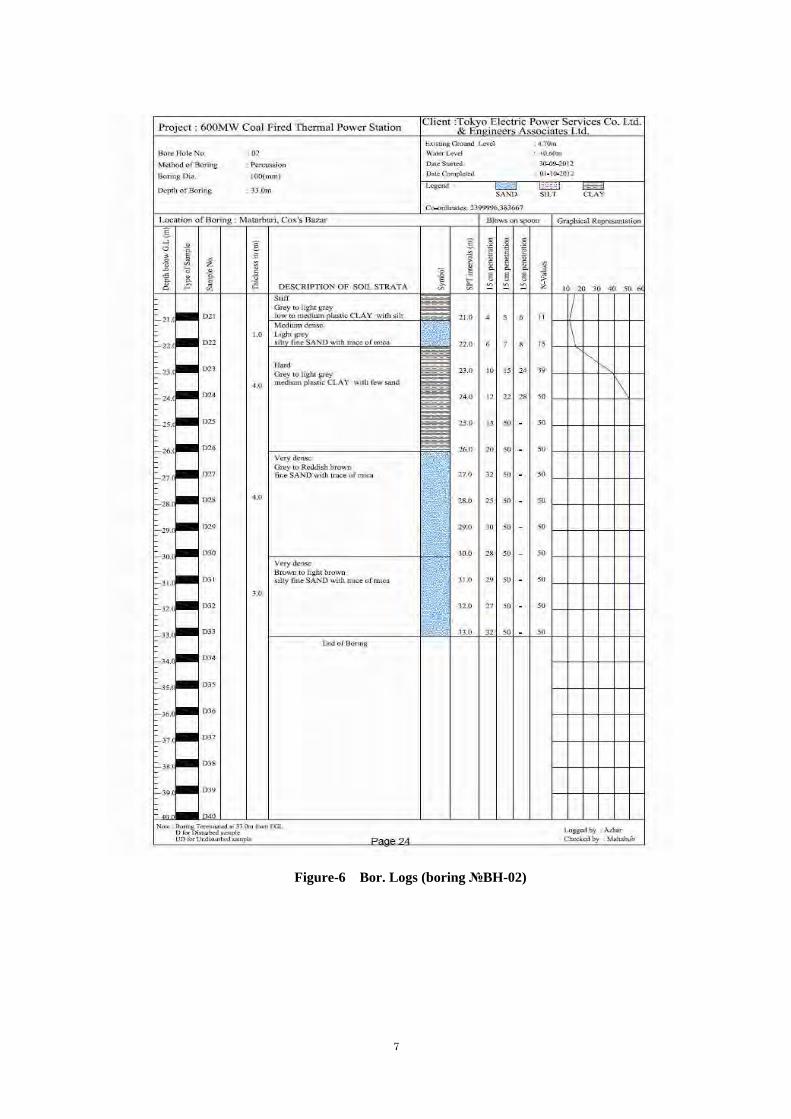

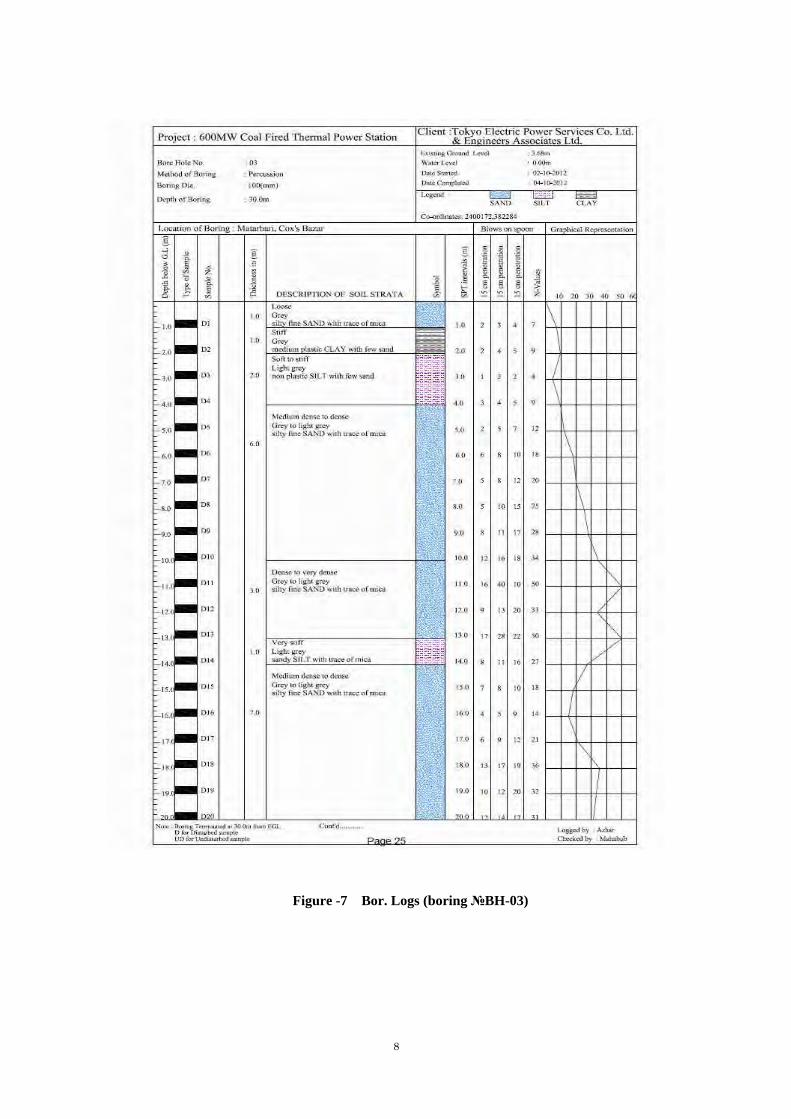

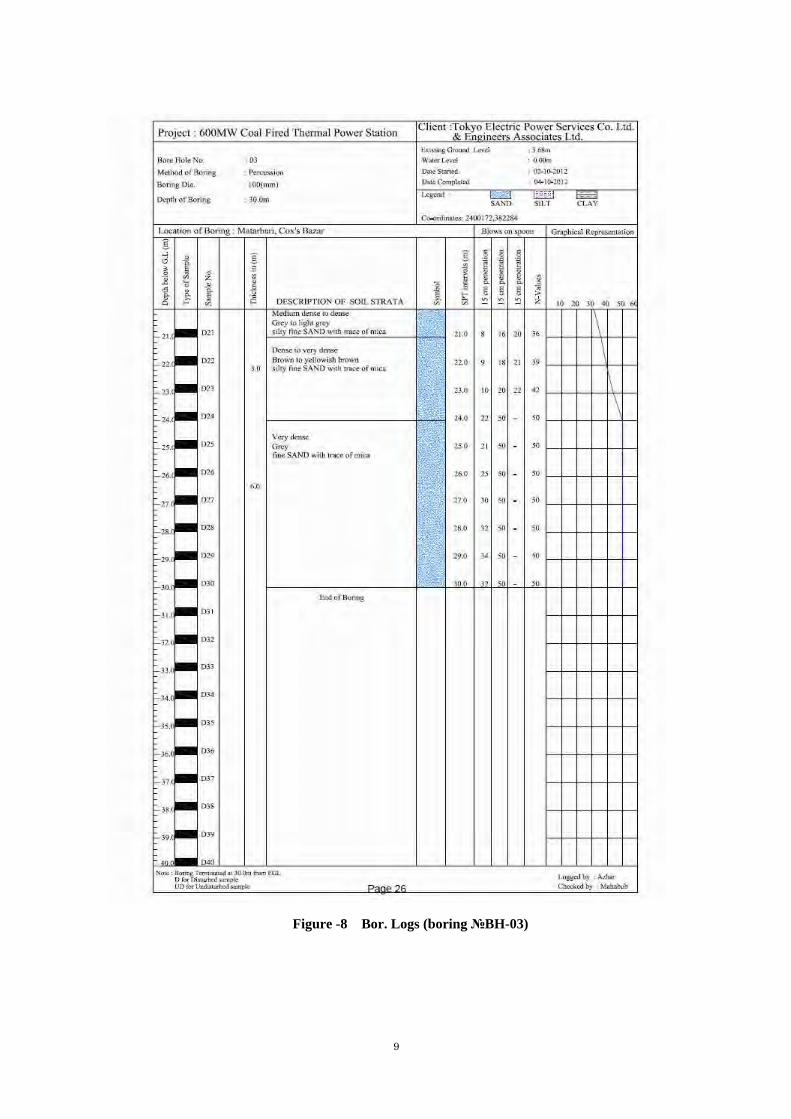

(4) Results of the survey

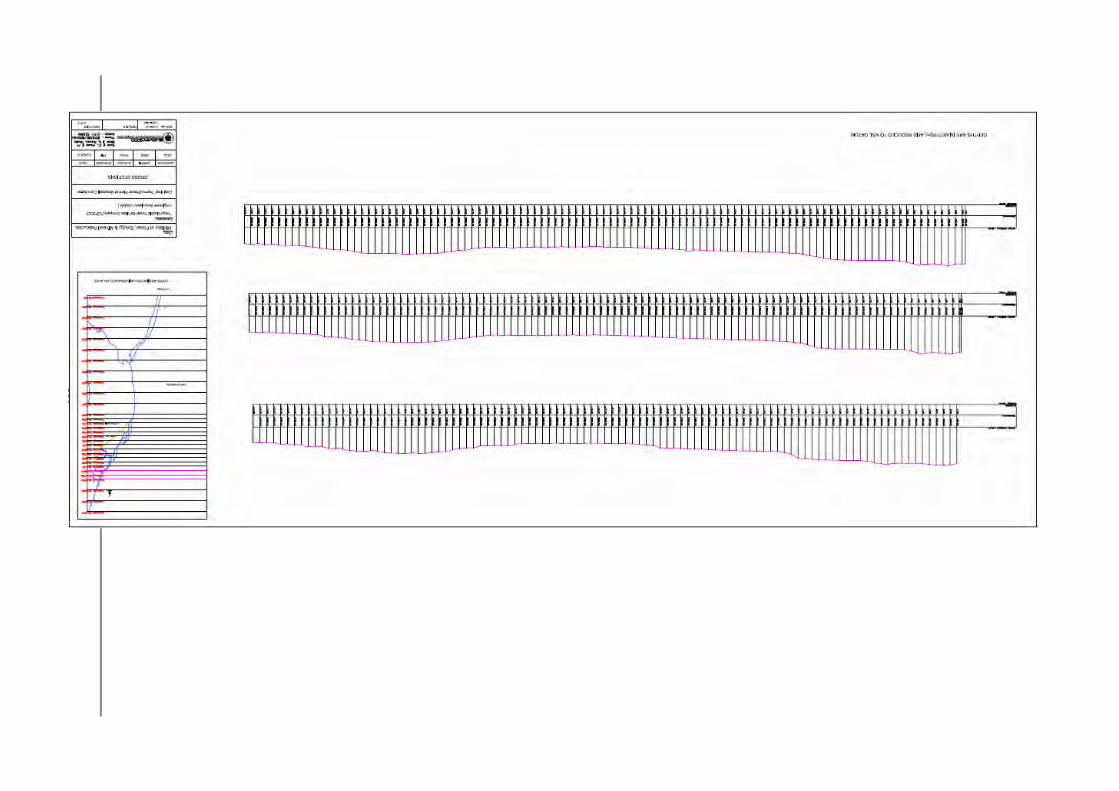

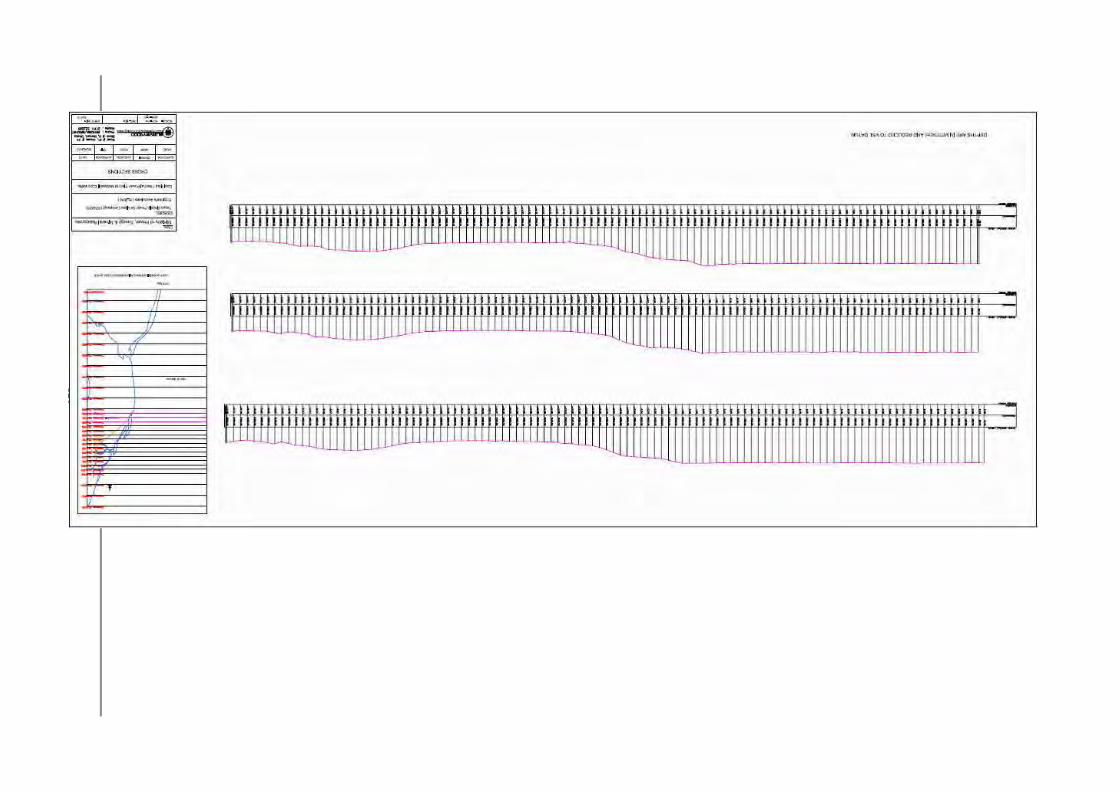

Figure -3 Bor. Logs (boring №BH-01)

5

Figure -4 Bor. Logs (boring №BH-01)

6

Figure -5 Bor. Logs (boring №BH-02)

7

Figure-6 Bor. Logs (boring №BH-02)

8

Figure -7 Bor. Logs (boring №BH-03)

9

Figure -8 Bor. Logs (boring №BH-03)

10

Table -1 Summary of Laboratory Test Results (boring №01-03 )

11

Table -2 Summary of Laboratory Test Results (boring №01-03 )

12

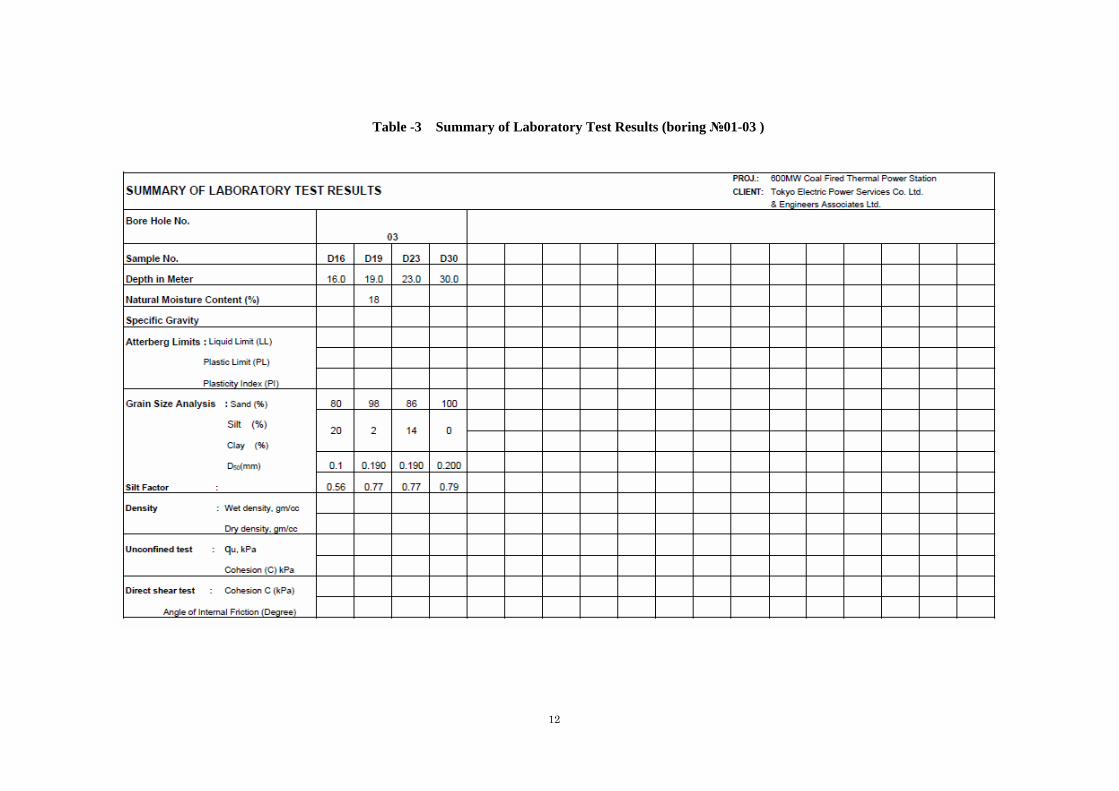

Table -3 Summary of Laboratory Test Results (boring №01-03 )

13

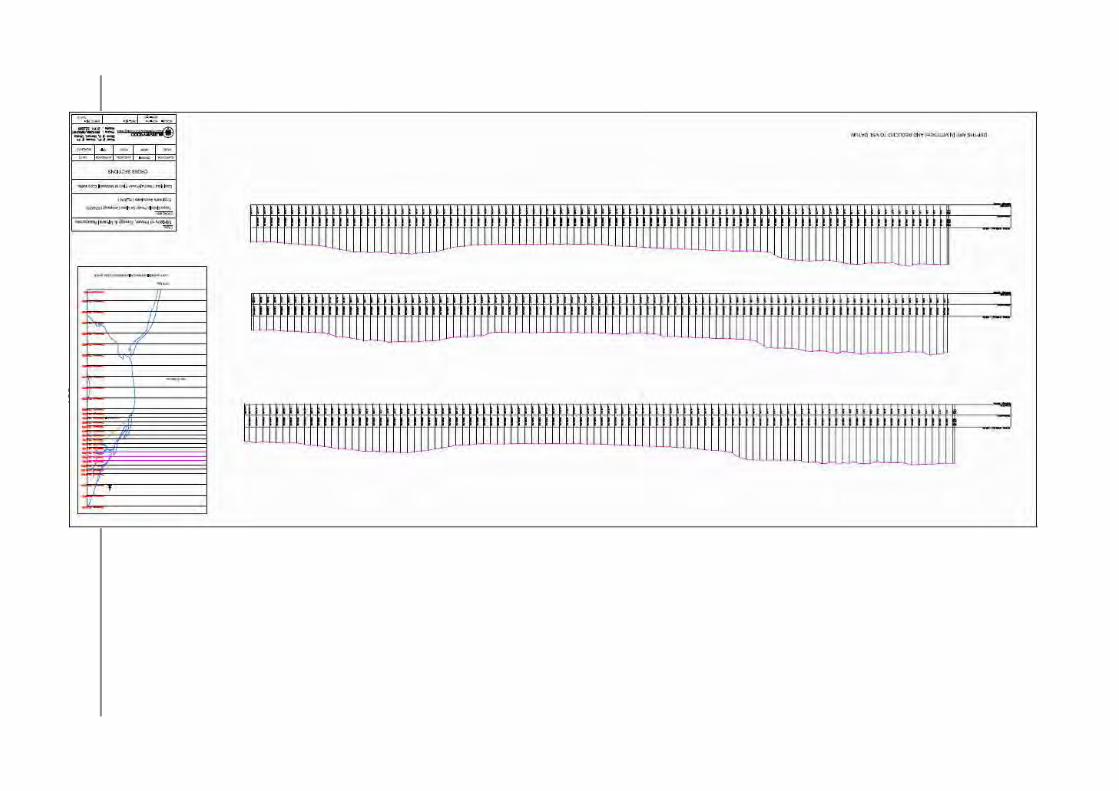

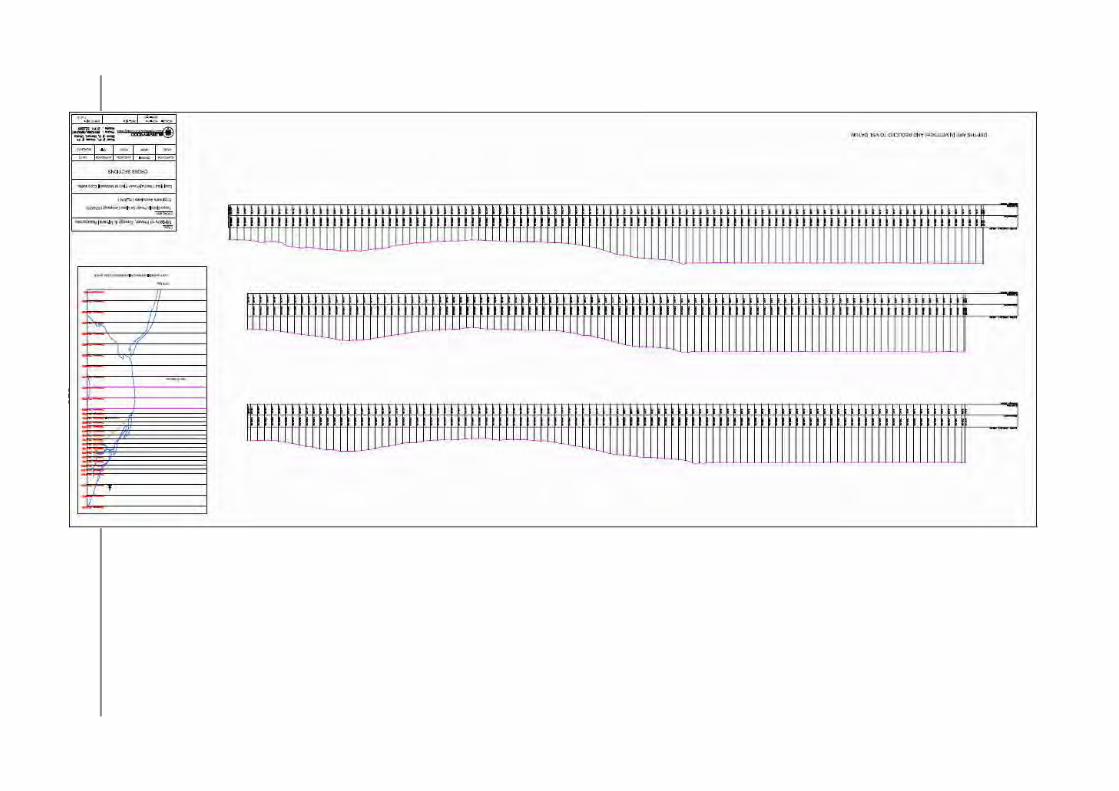

Figure -9 Bor. Logs (boring №BH-1)

14

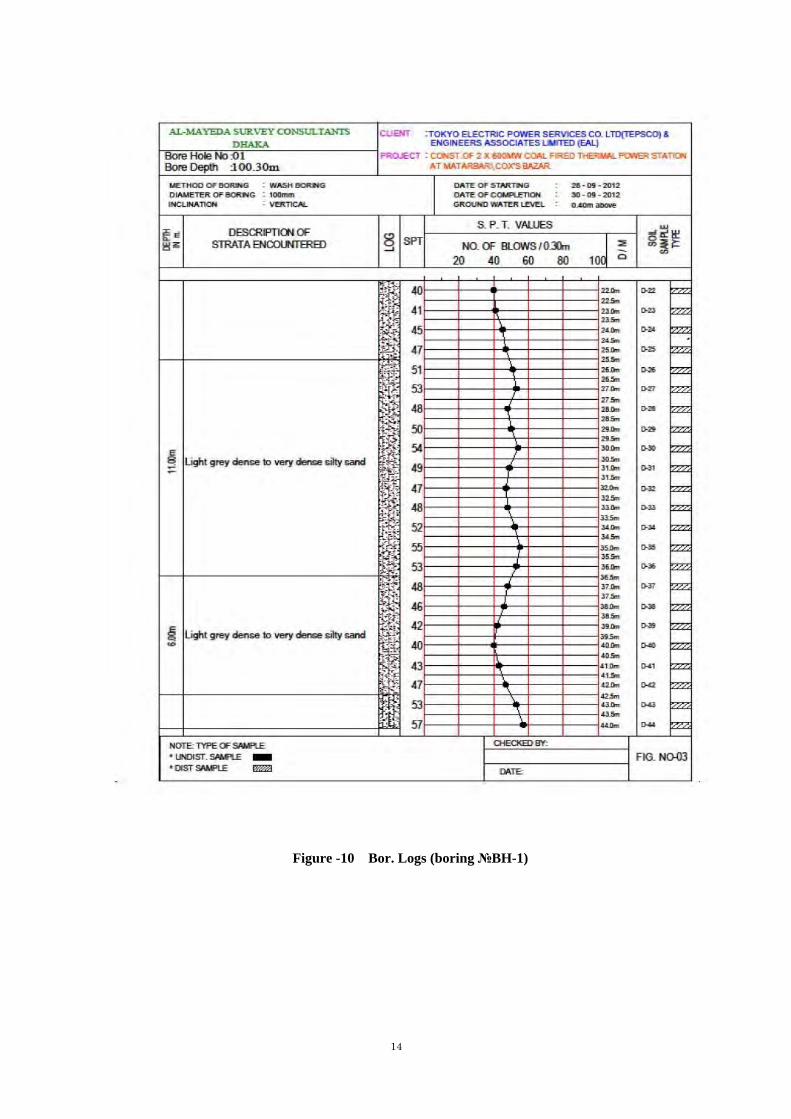

Figure -10 Bor. Logs (boring №BH-1)

15

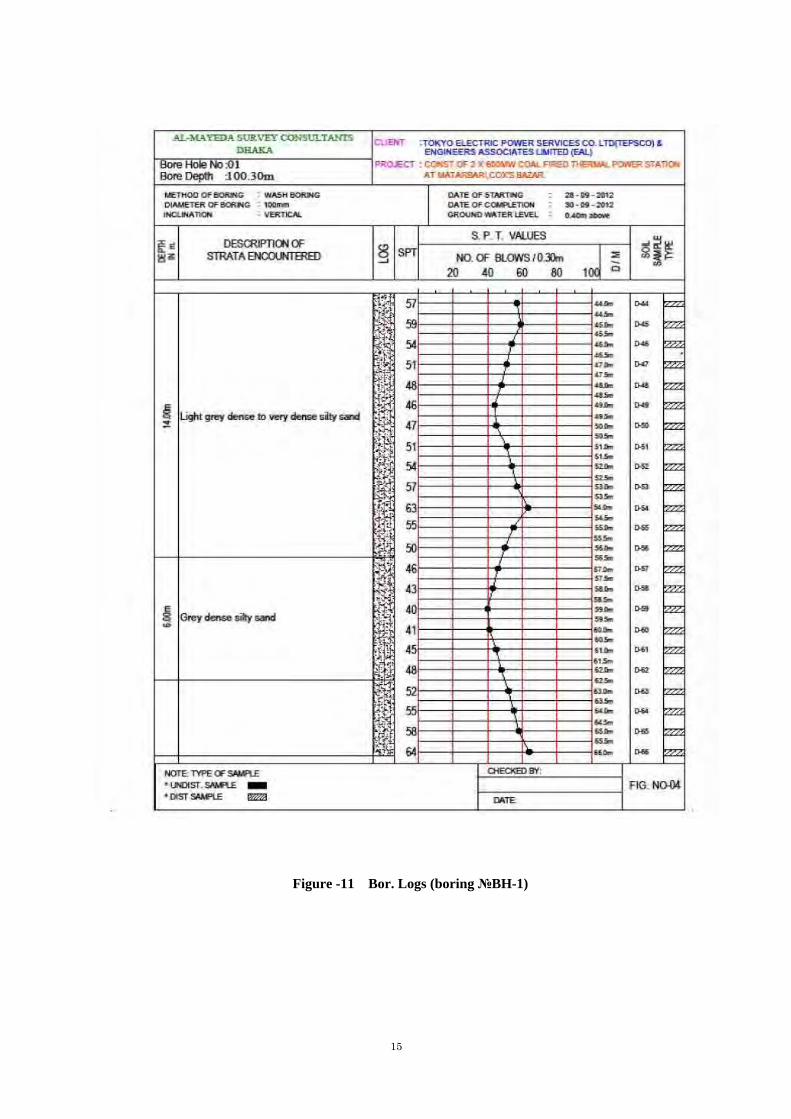

Figure -11 Bor. Logs (boring №BH-1)

16

Figure -12 Bor. Logs (boring №BH-1)

17

Figure -13 Bor. Logs (boring №BH-1)

18

Figure -14 Bor. Logs (boring №BH-2)

19

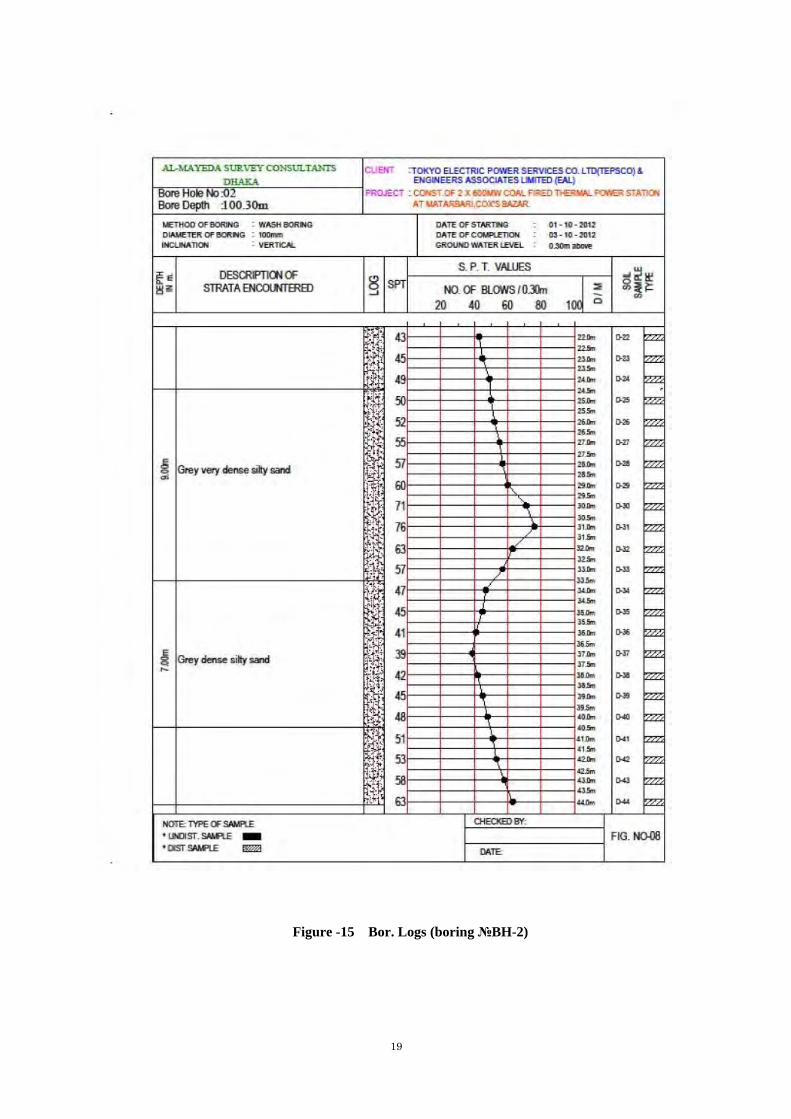

Figure -15 Bor. Logs (boring №BH-2)

20

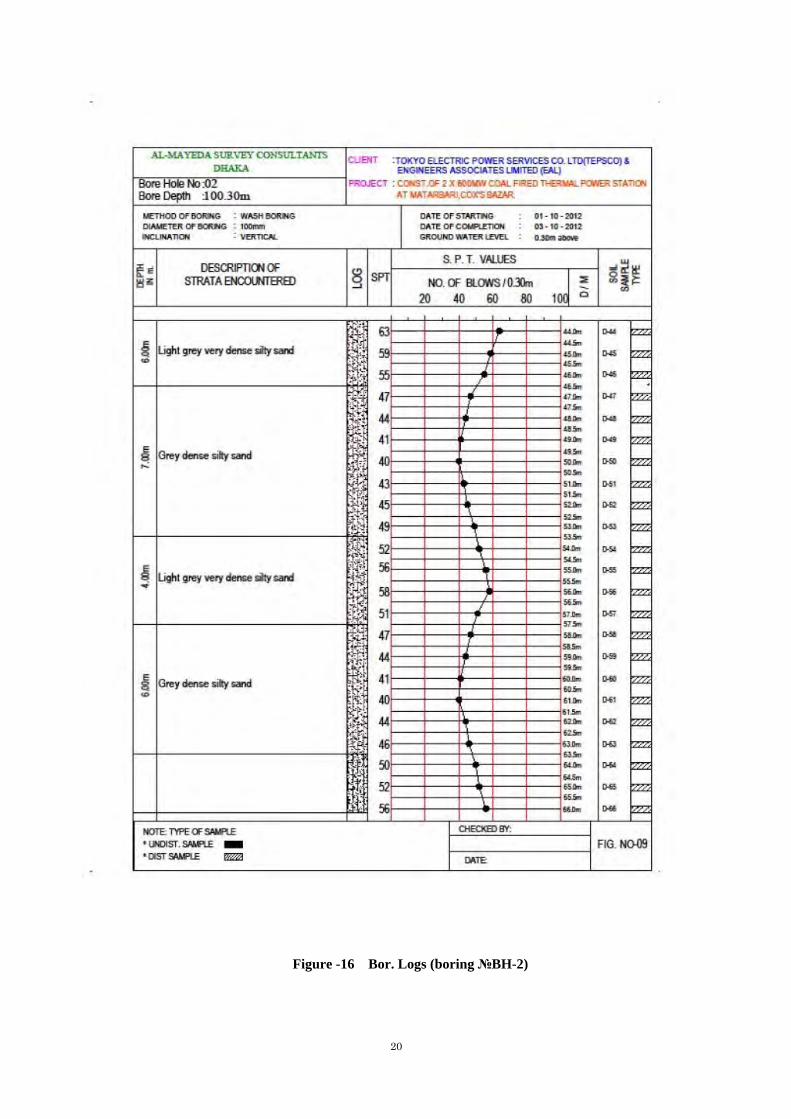

Figure -16 Bor. Logs (boring №BH-2)

21

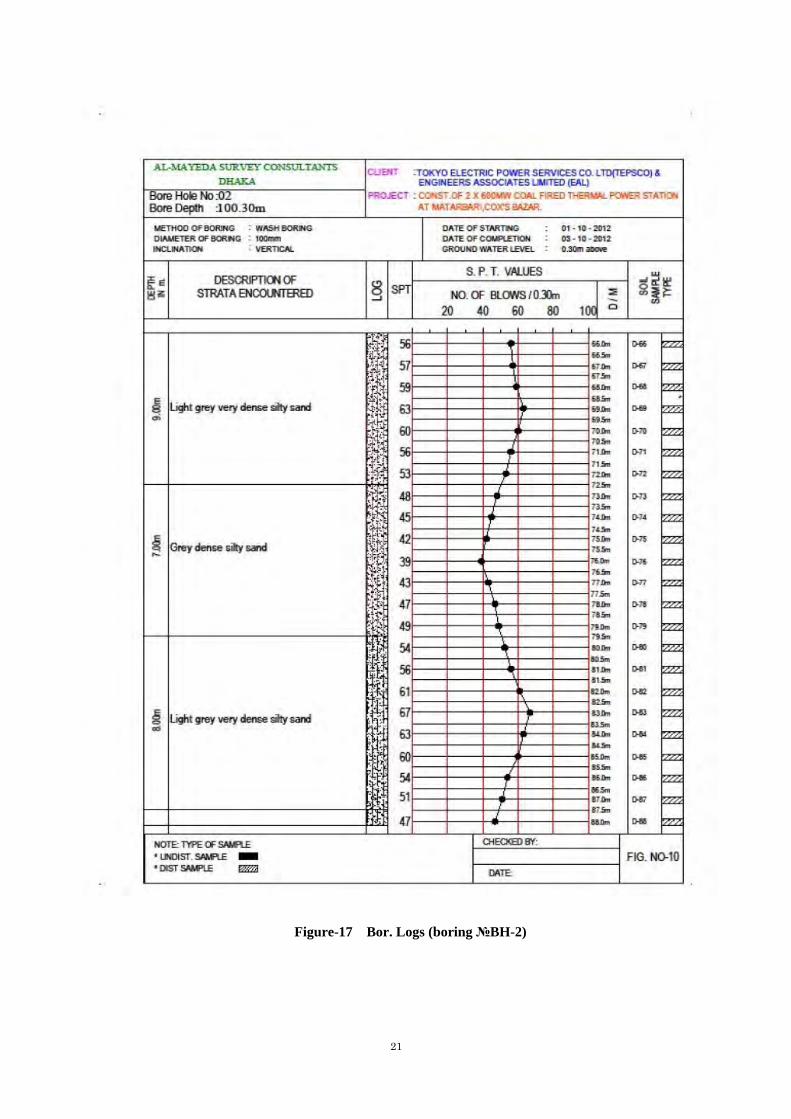

Figure-17 Bor. Logs (boring №BH-2)

22

Figure -18 Bor. Logs (boring №BH-2)

23

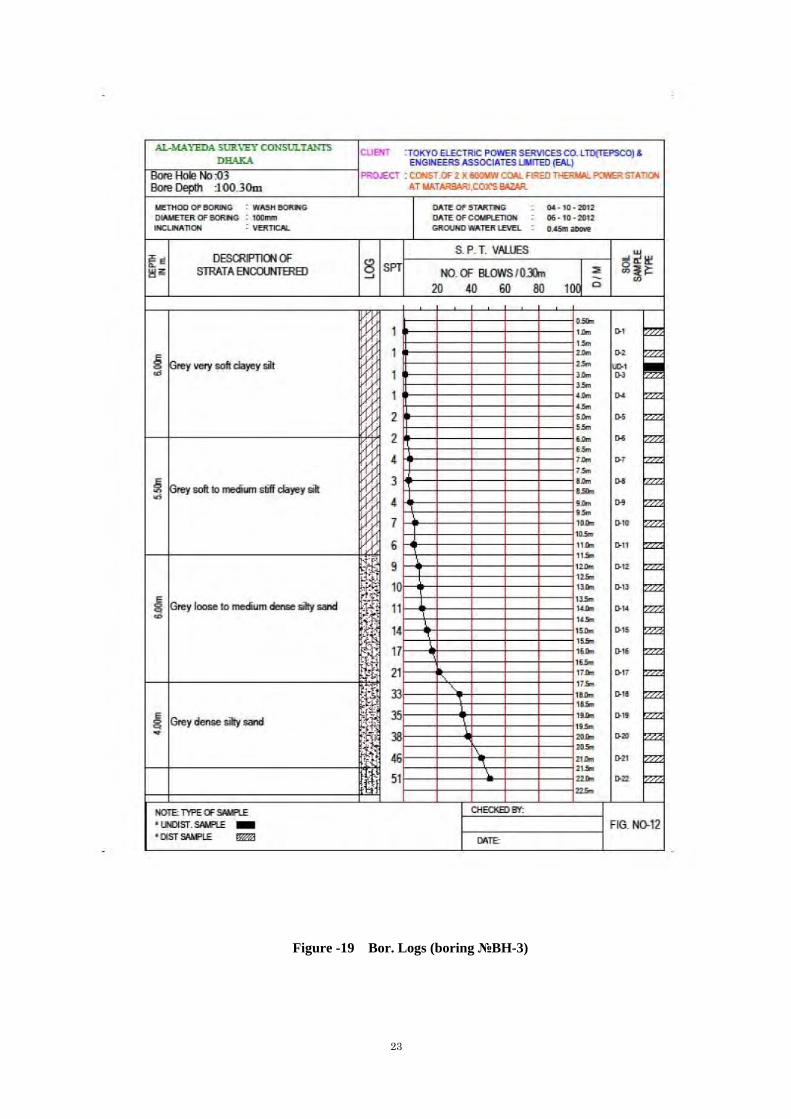

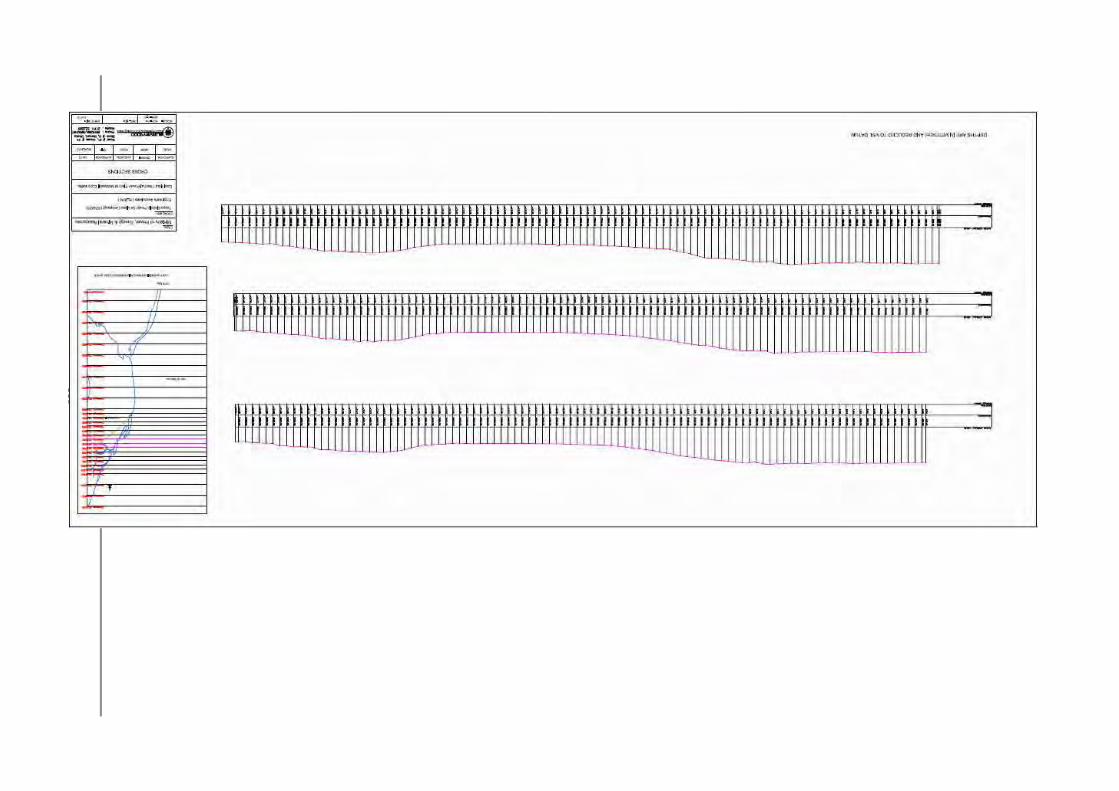

Figure -19 Bor. Logs (boring №BH-3)

24

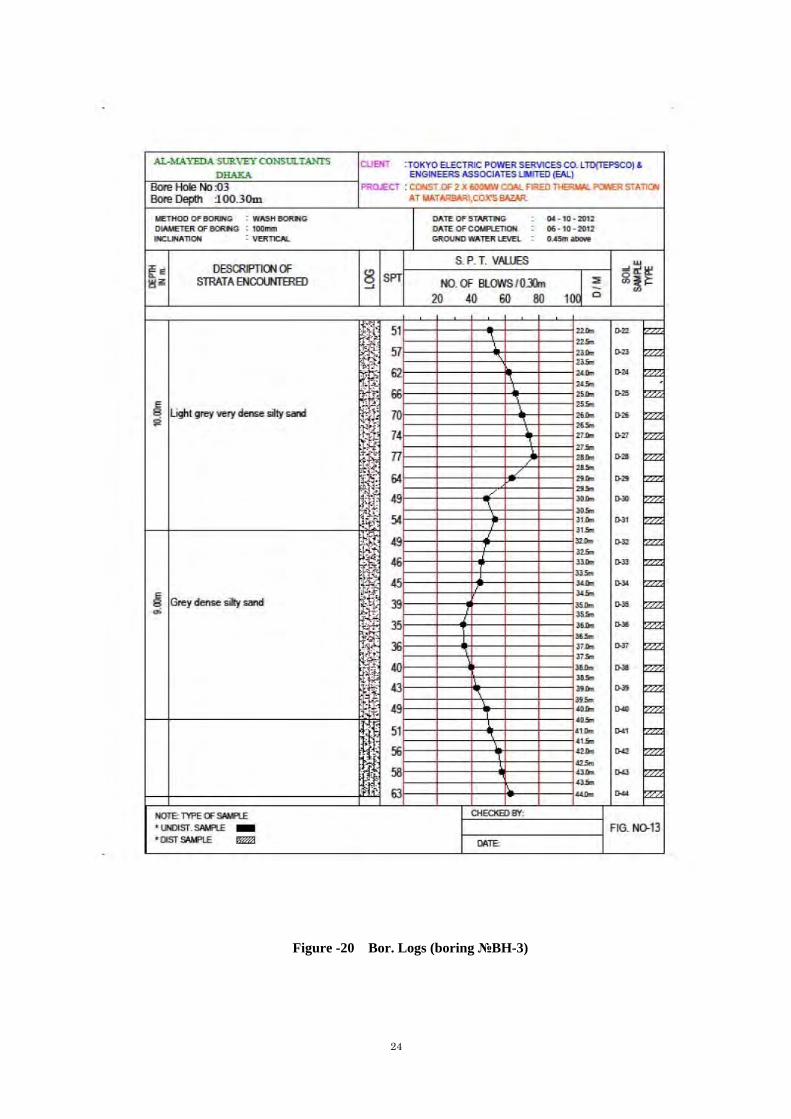

Figure -20 Bor. Logs (boring №BH-3)

25

Figure -21 Bor. Logs (boring №BH-3)

26

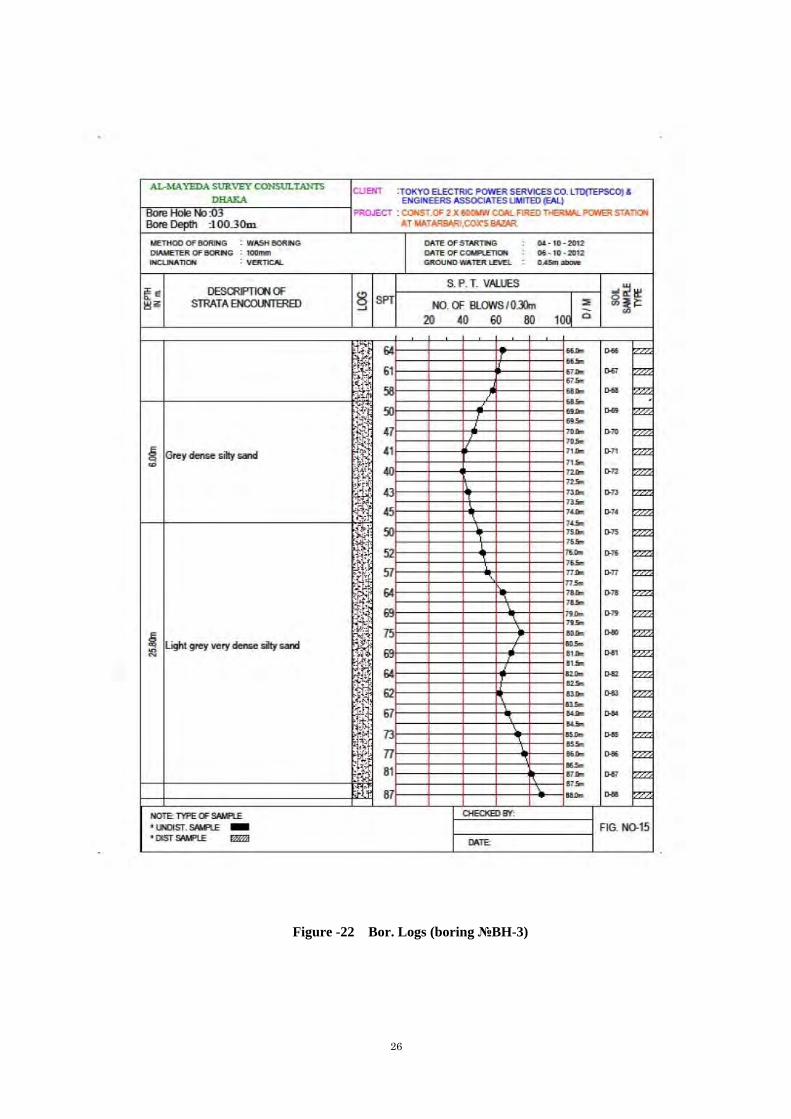

Figure -22 Bor. Logs (boring №BH-3)

27

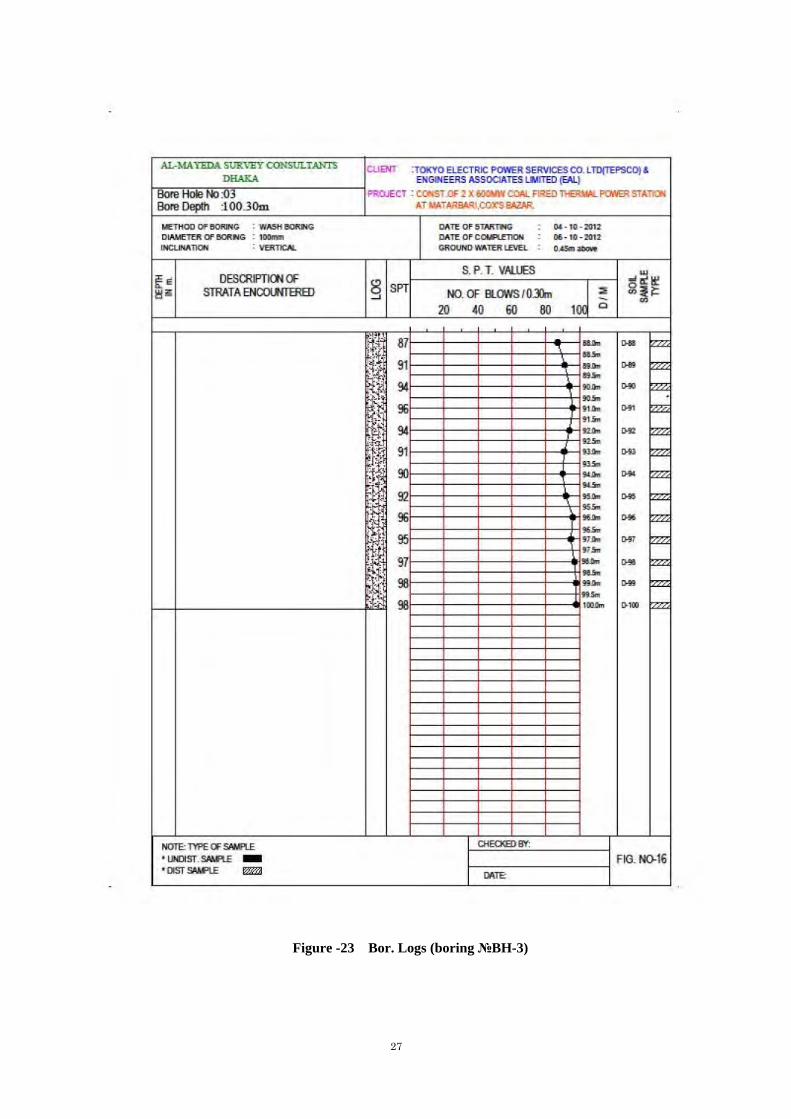

Figure -23 Bor. Logs (boring №BH-3)

28

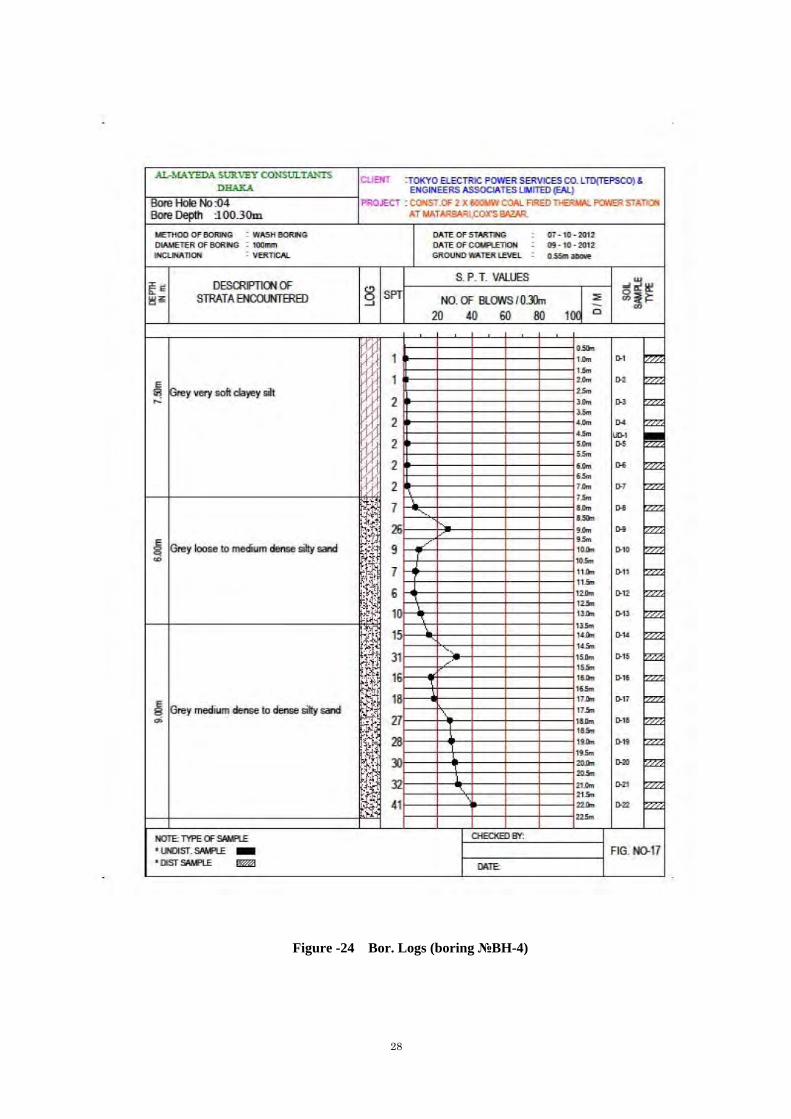

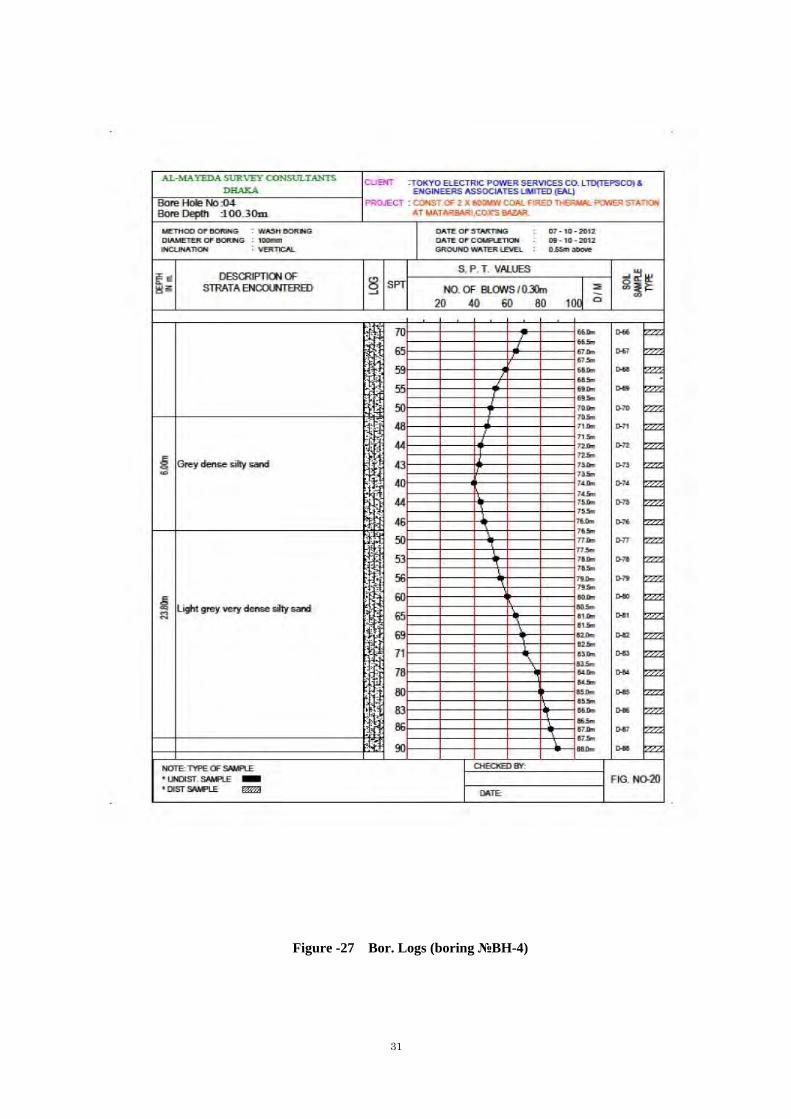

Figure -24 Bor. Logs (boring №BH-4)

29

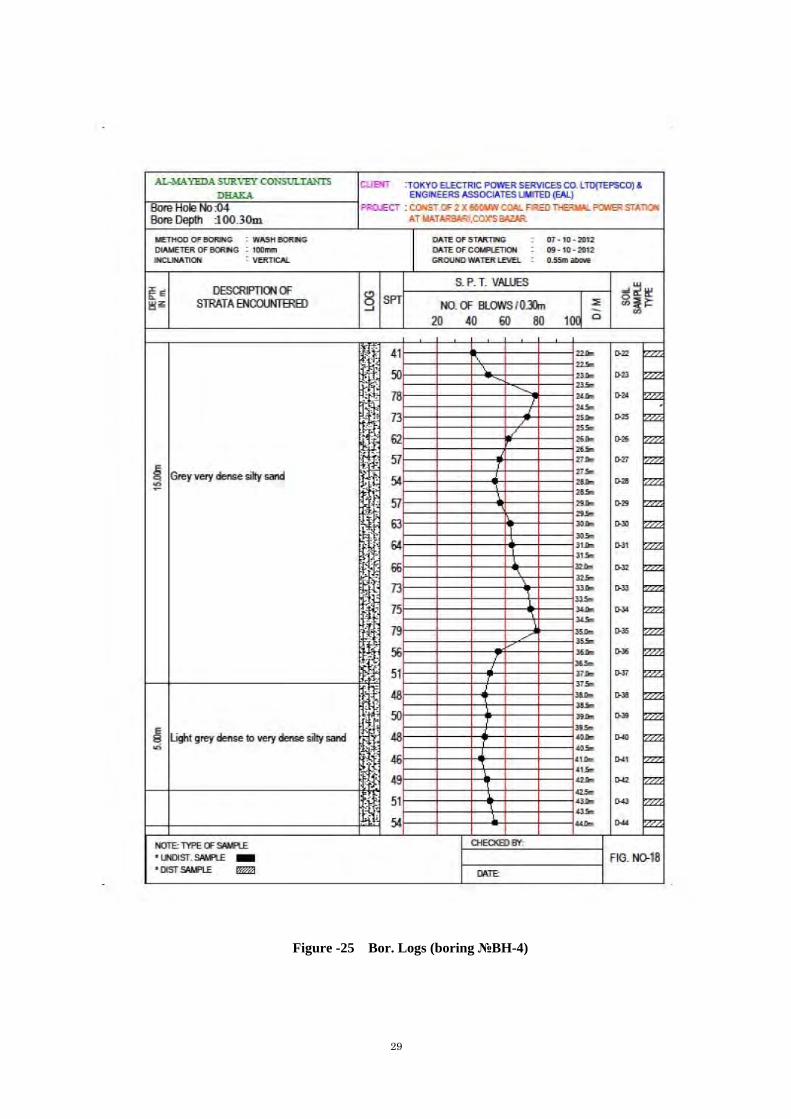

Figure -25 Bor. Logs (boring №BH-4)

30

Figure -26 Bor. Logs (boring №BH-4)

31

Figure -27 Bor. Logs (boring №BH-4)

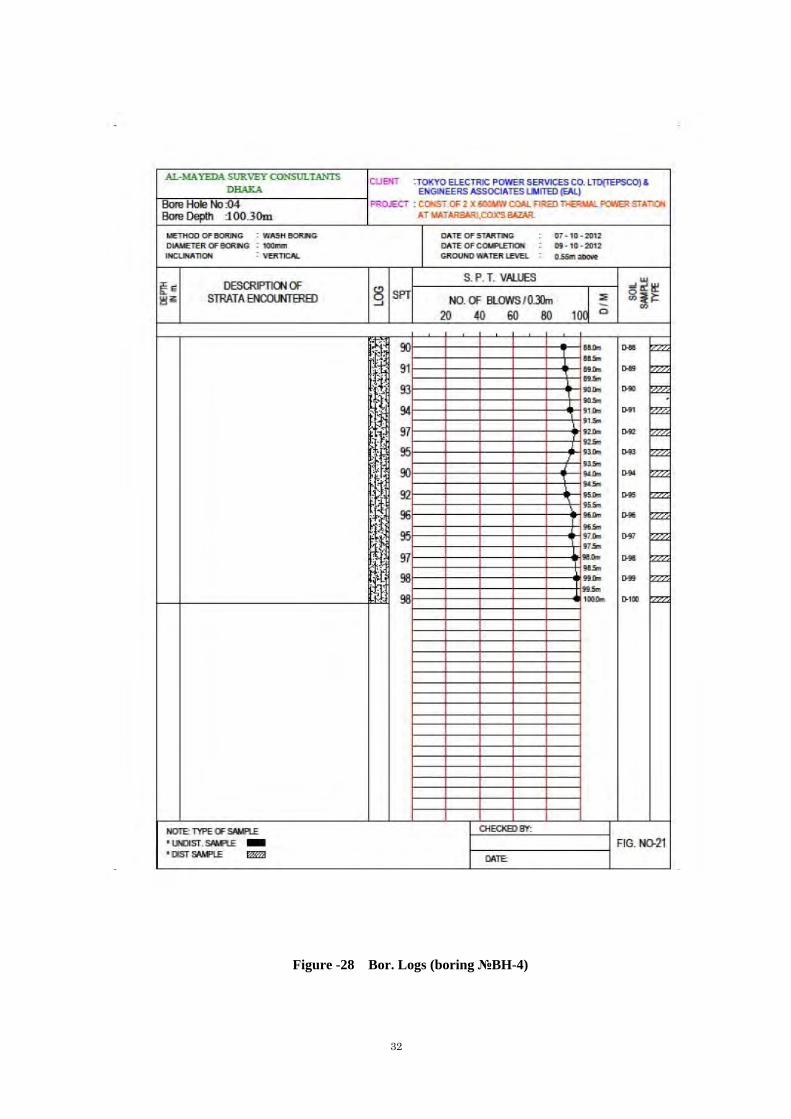

32

Figure -28 Bor. Logs (boring №BH-4)

33

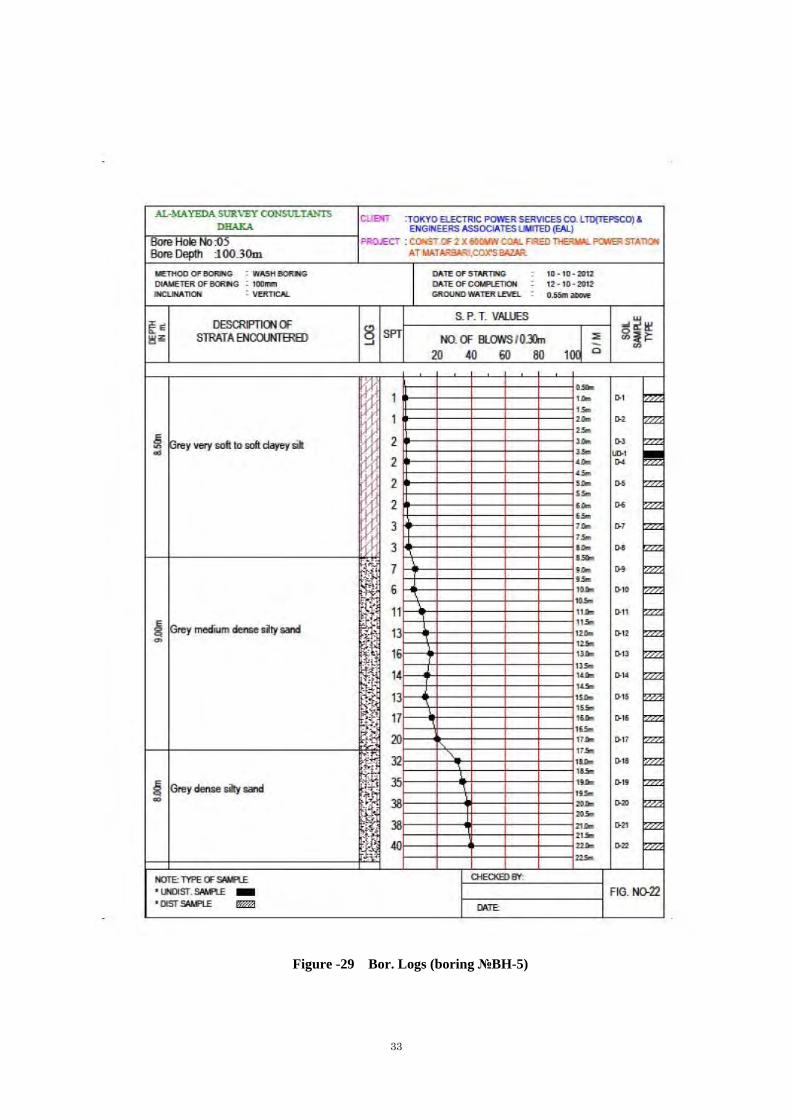

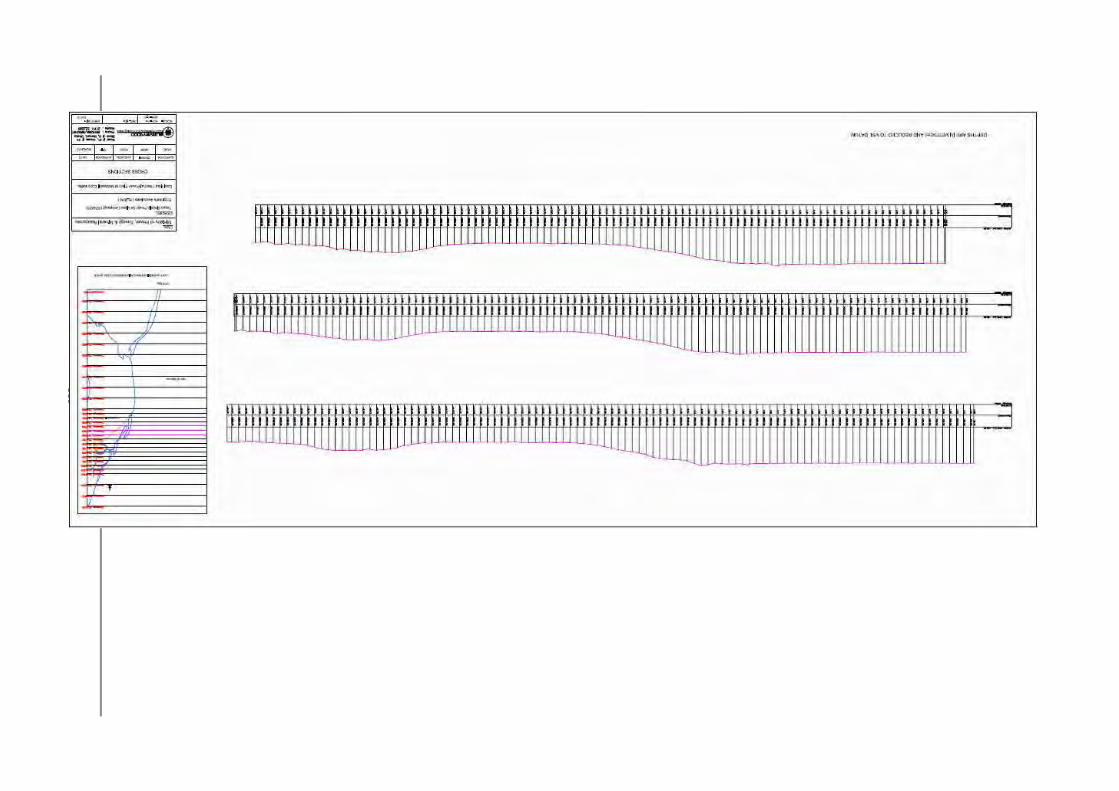

Figure -29 Bor. Logs (boring №BH-5)

34

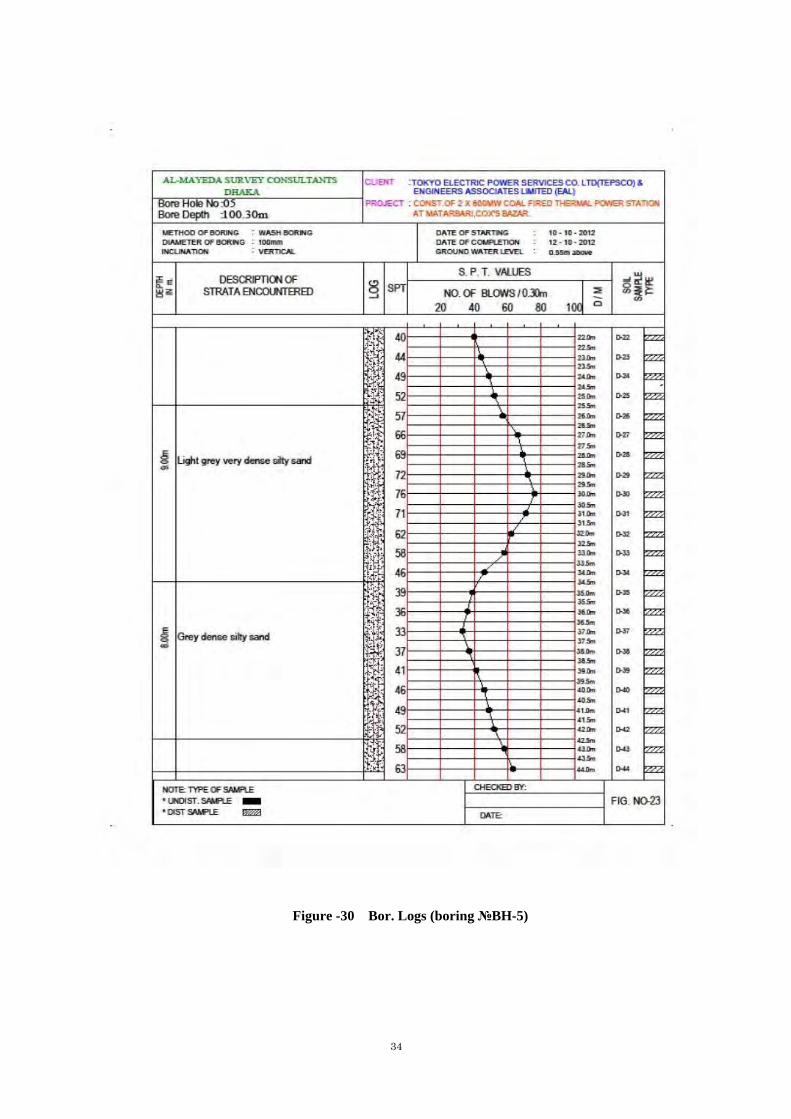

Figure -30 Bor. Logs (boring №BH-5)

35

Figure -31 Bor. Logs (boring №BH-5)

36

Figure -32 Bor. Logs (boring №BH-5)

37

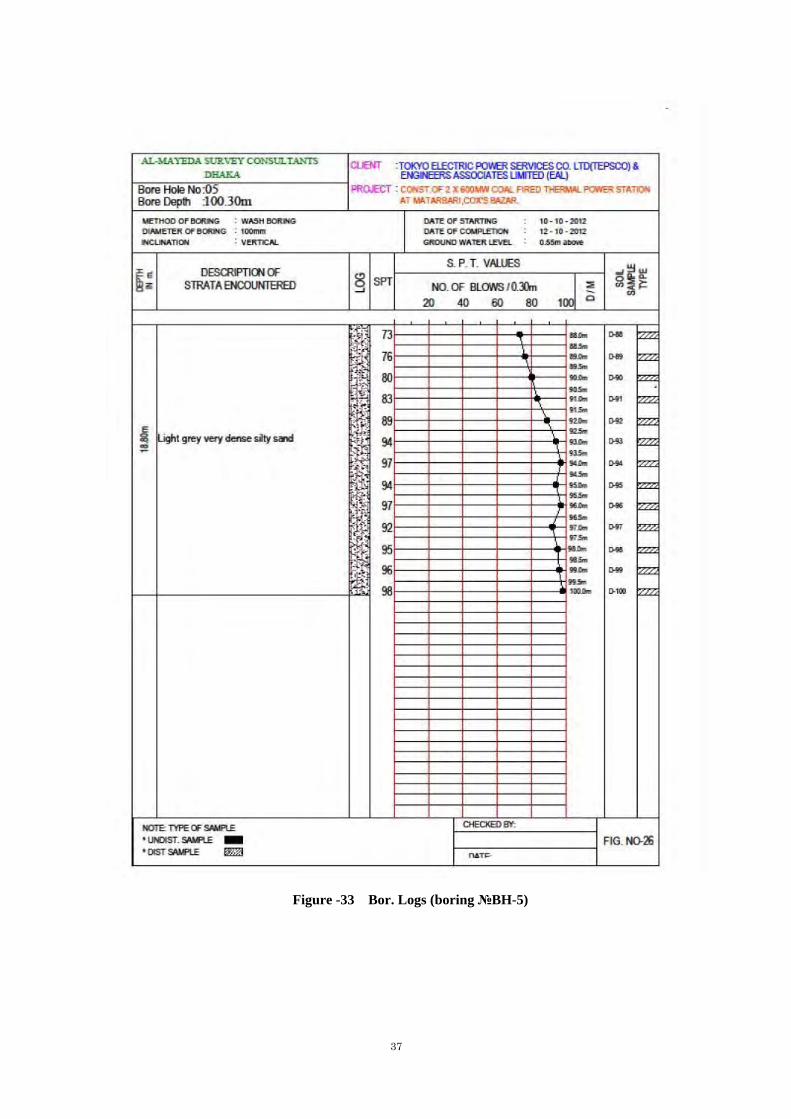

Figure -33 Bor. Logs (boring №BH-5)

38

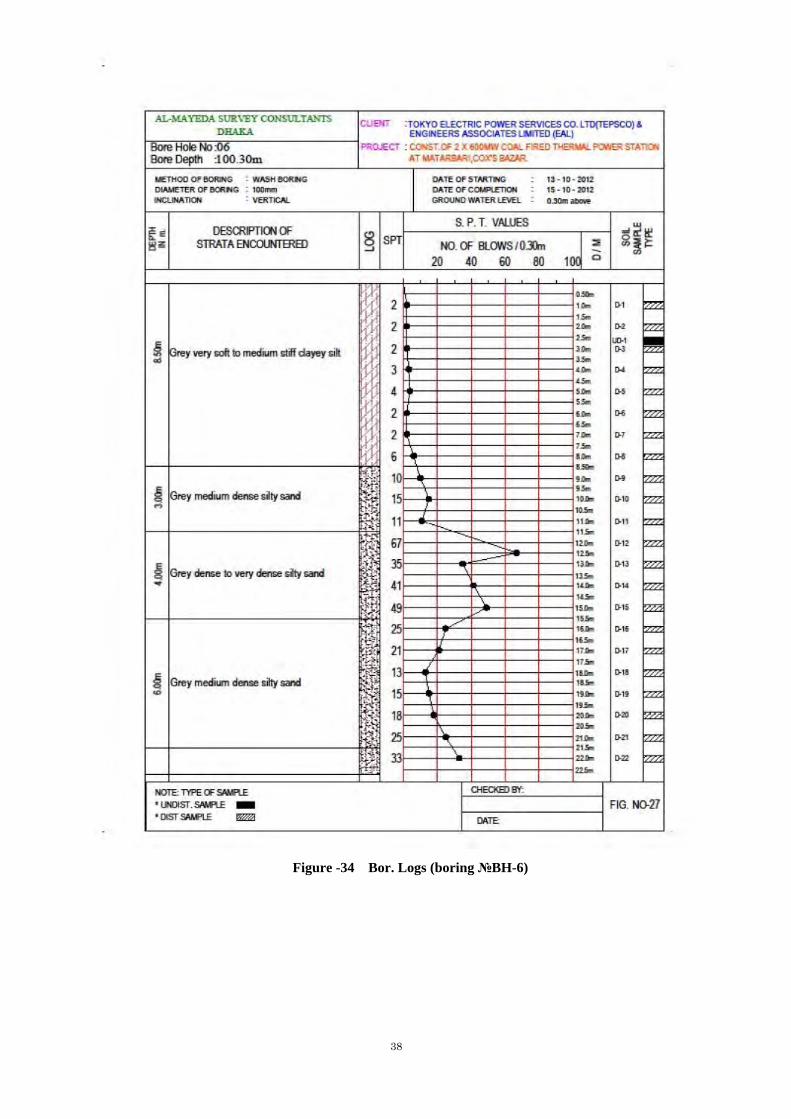

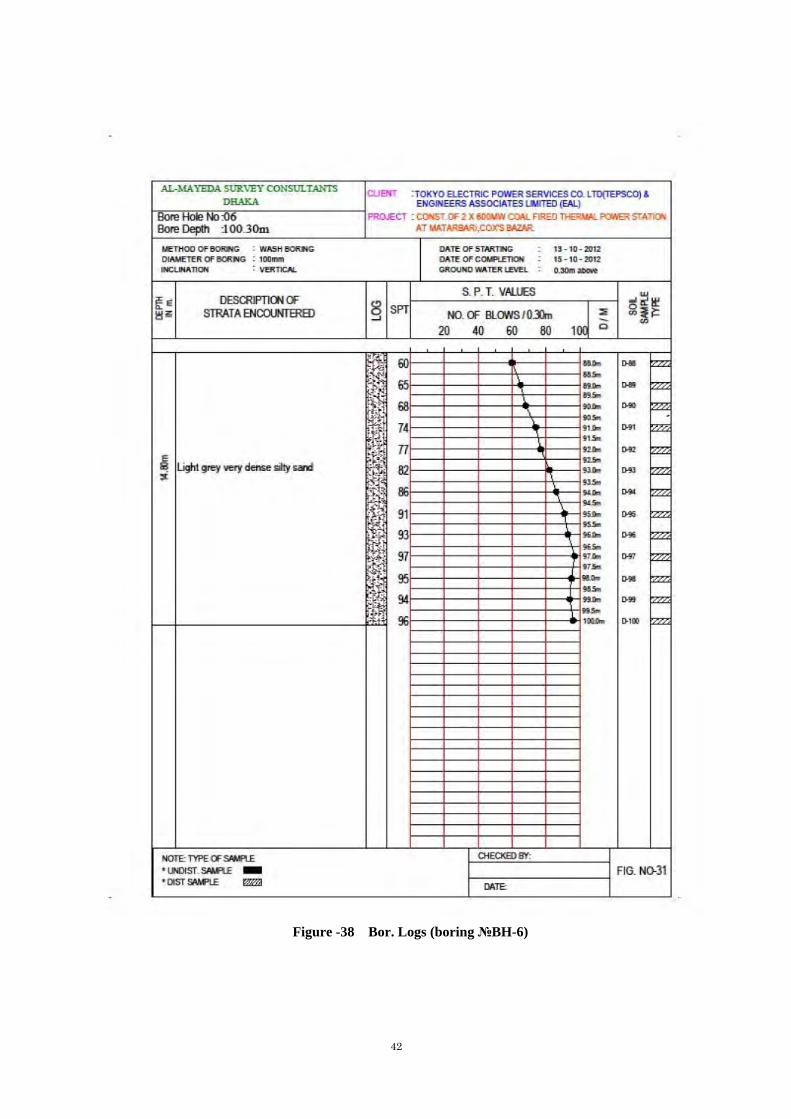

Figure -34 Bor. Logs (boring №BH-6)

39

Figure -35 Bor. Logs (boring №BH-6)

40

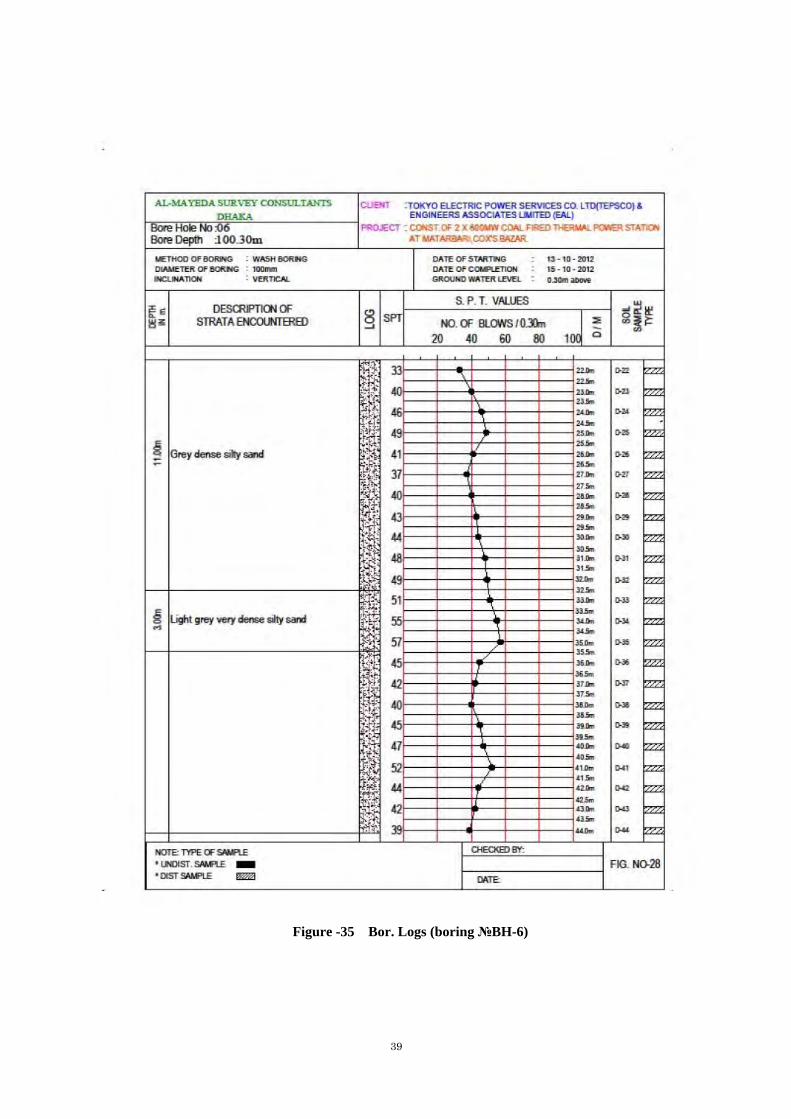

Figure -36 Bor. Logs (boring №BH-6)

41

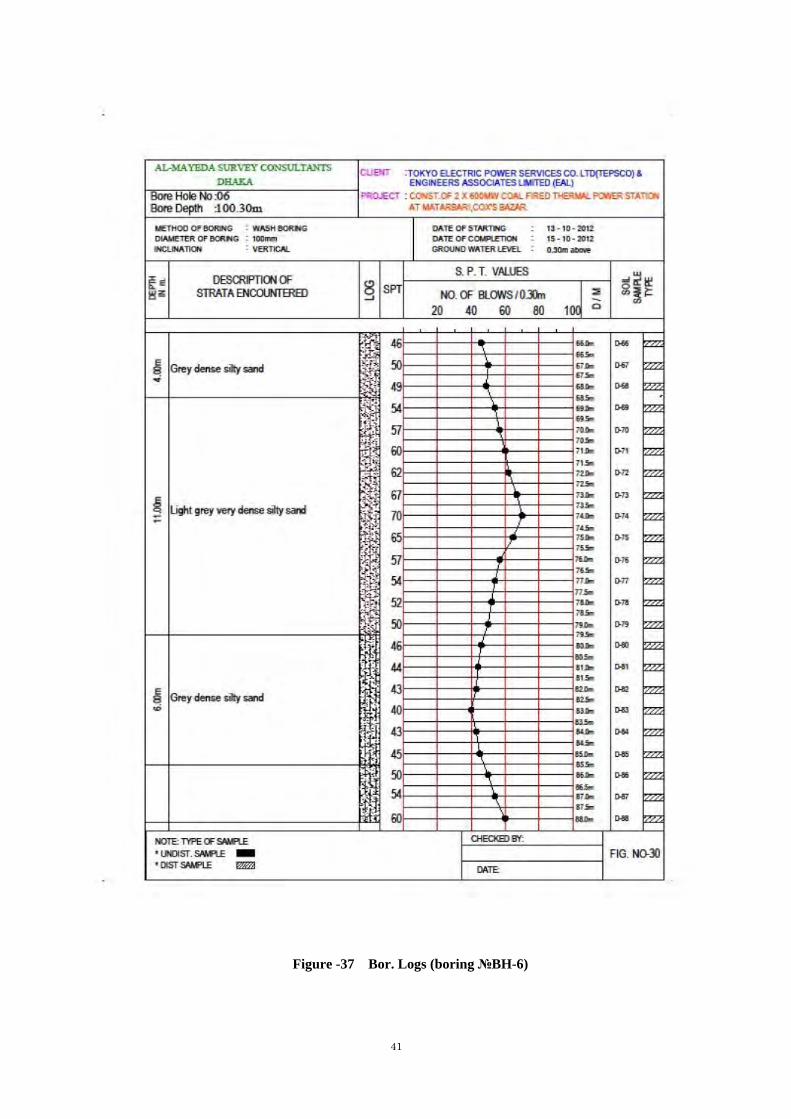

Figure -37 Bor. Logs (boring №BH-6)

42

Figure -38 Bor. Logs (boring №BH-6)

43

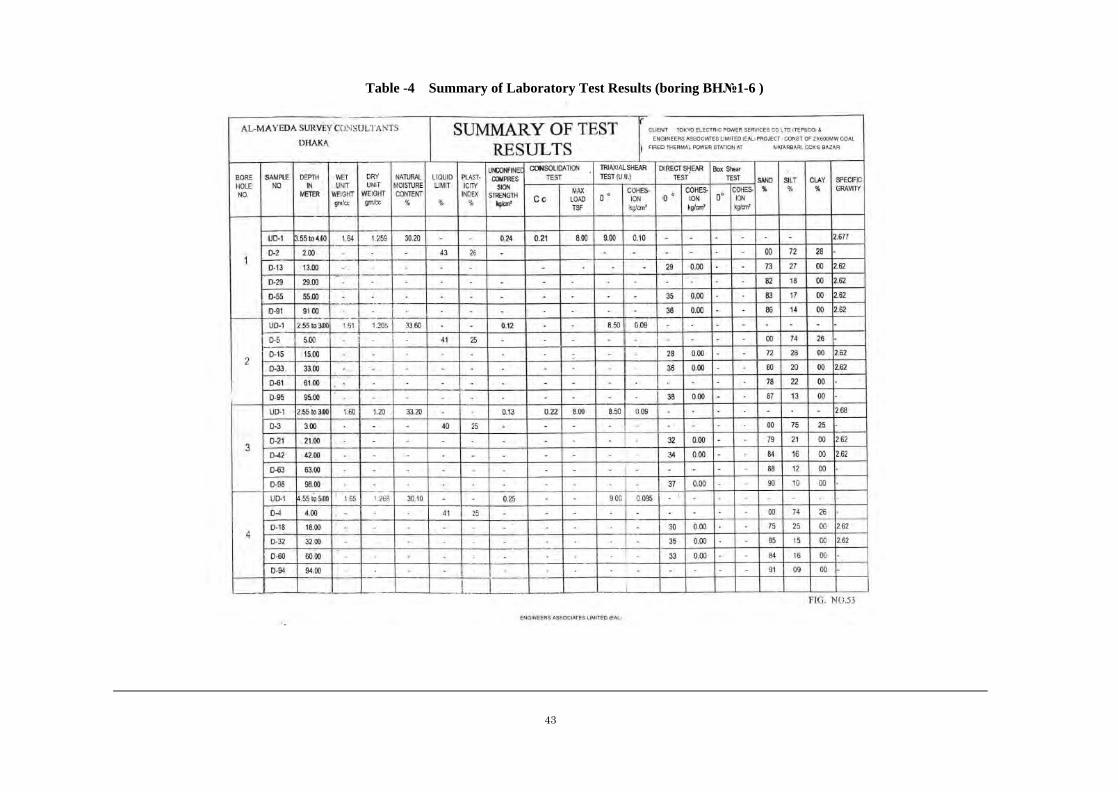

Table -4 Summary of Laboratory Test Results (boring BH№1-6 )

44

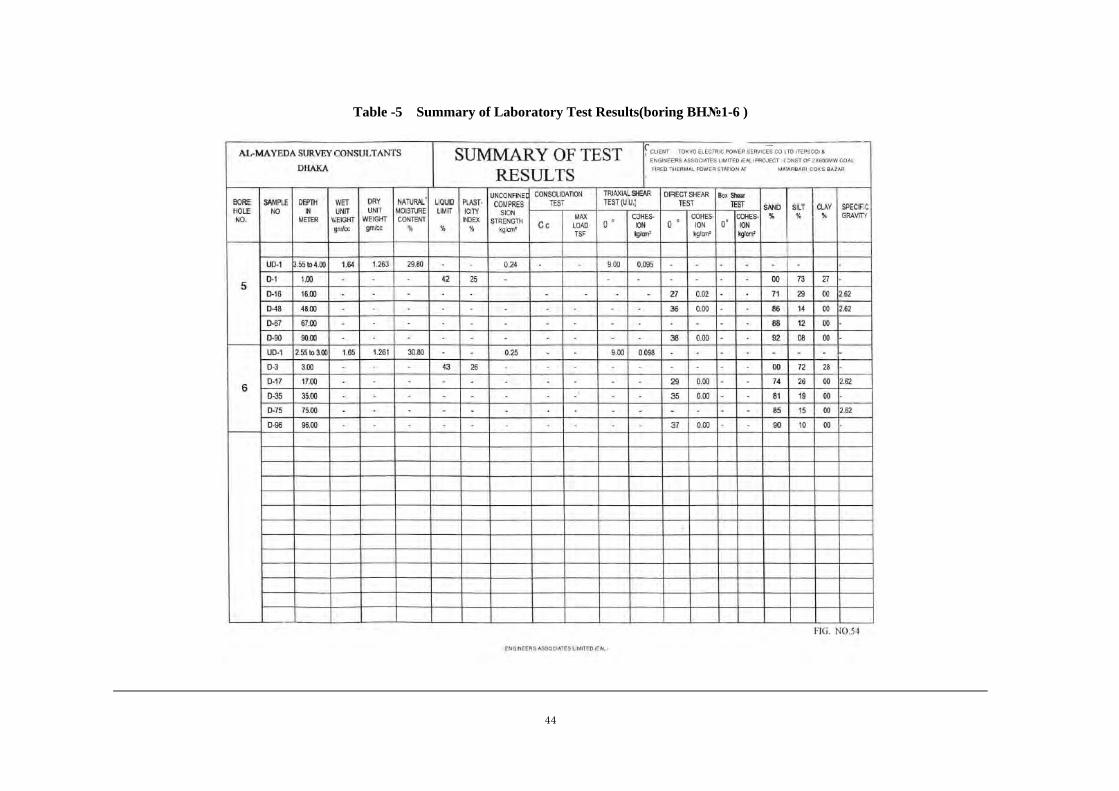

Table -5 Summary of Laboratory Test Results(boring BH№1-6 )

Appendix-C05-03

Oceanographic Survey

1

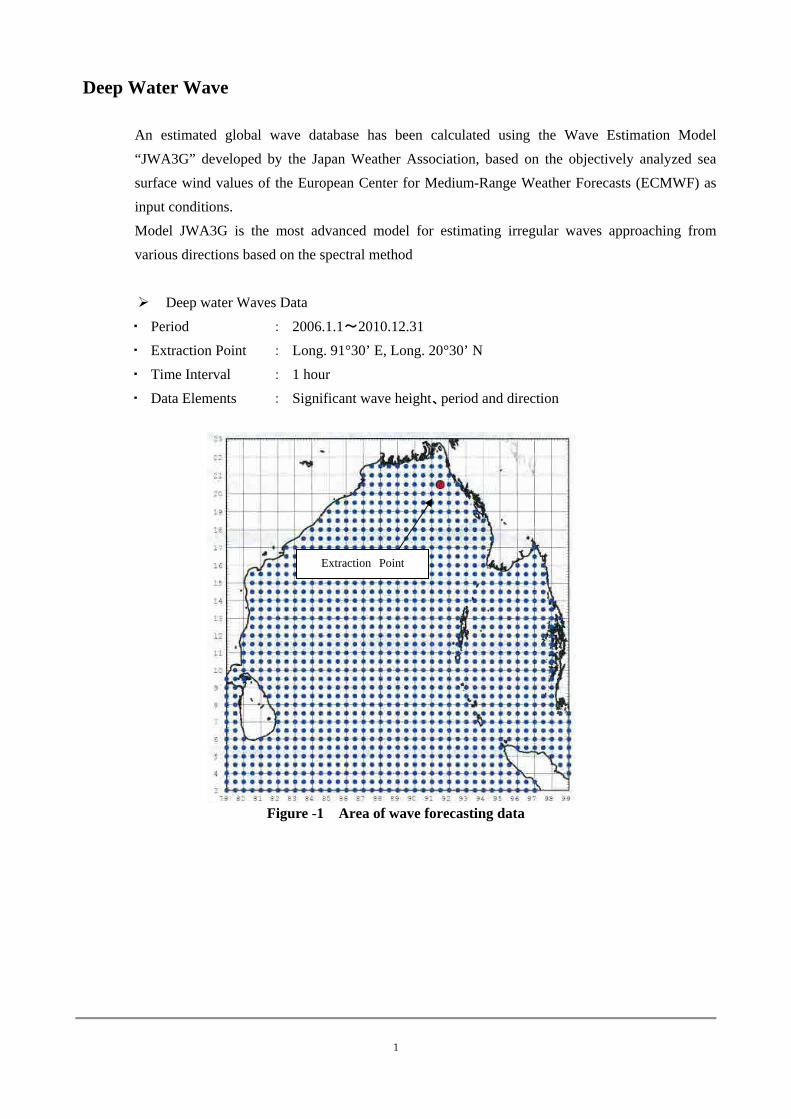

Deep Water Wave

An estimated global wave database has been calculated using the Wave Estimation Model

“JWA3G” developed by the Japan Weather Association, based on the objectively analyzed sea

surface wind values of the European Center for Medium-Range Weather Forecasts (ECMWF) as

input conditions.

Model JWA3G is the most advanced model for estimating irregular waves approaching from

various directions based on the spectral method

Deep water Waves Data

・ Period : 2006.1.1~2010.12.31

・ Extraction Point : Long. 91°30’ E, Long. 20°30’ N

・ Time Interval : 1 hour

・ Data Elements : Significant wave height、period and direction

Figure -1 Area of wave forecasting data

Extraction Point

2

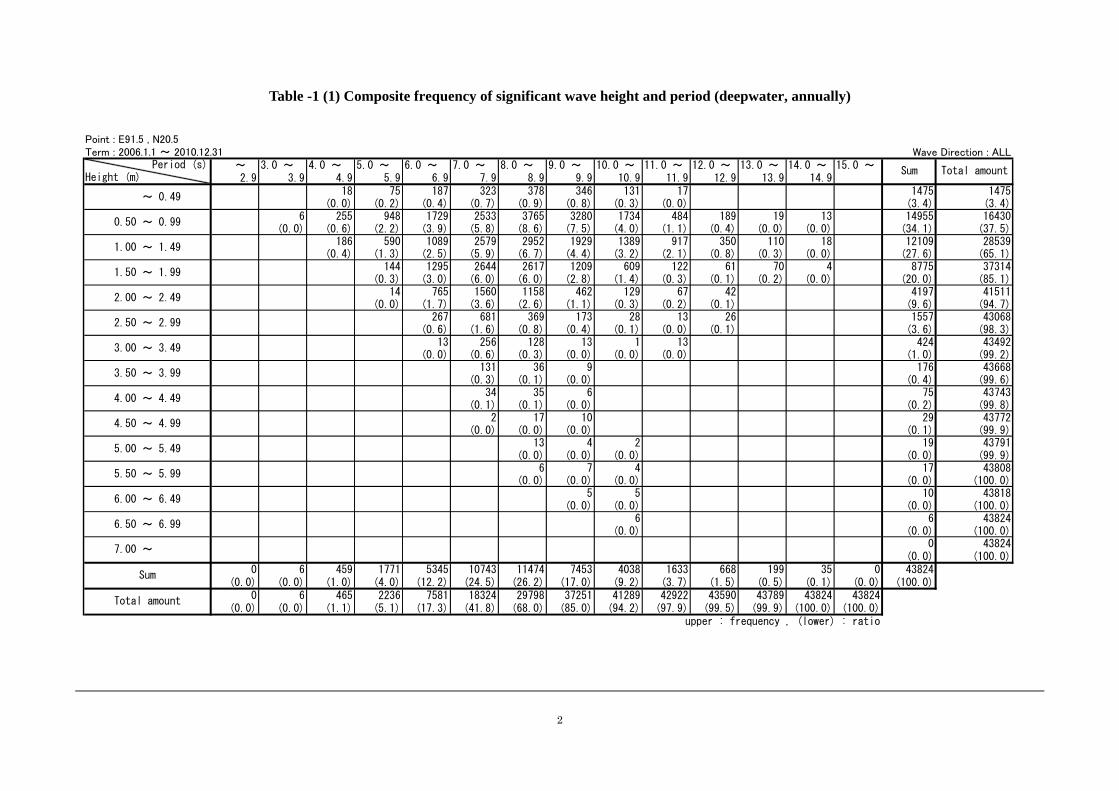

Table -1 (1) Composite frequency of significant wave height and period (deepwater, annually)

Point : E91.5 , N20.5Term : 2006.1.1 ~ 2010.12.31 Wave Direction : ALL

~ 3.0 ~ 4.0 ~ 5.0 ~ 6.0 ~ 7.0 ~ 8.0 ~ 9.0 ~ 10.0 ~ 11.0 ~ 12.0 ~ 13.0 ~ 14.0 ~ 15.0 ~2.9 3.9 4.9 5.9 6.9 7.9 8.9 9.9 10.9 11.9 12.9 13.9 14.9

18 75 187 323 378 346 131 17 1475 1475(0.0) (0.2) (0.4) (0.7) (0.9) (0.8) (0.3) (0.0) (3.4) (3.4)

6 255 948 1729 2533 3765 3280 1734 484 189 19 13 14955 16430(0.0) (0.6) (2.2) (3.9) (5.8) (8.6) (7.5) (4.0) (1.1) (0.4) (0.0) (0.0) (34.1) (37.5)

186 590 1089 2579 2952 1929 1389 917 350 110 18 12109 28539(0.4) (1.3) (2.5) (5.9) (6.7) (4.4) (3.2) (2.1) (0.8) (0.3) (0.0) (27.6) (65.1)

144 1295 2644 2617 1209 609 122 61 70 4 8775 37314(0.3) (3.0) (6.0) (6.0) (2.8) (1.4) (0.3) (0.1) (0.2) (0.0) (20.0) (85.1)

14 765 1560 1158 462 129 67 42 4197 41511(0.0) (1.7) (3.6) (2.6) (1.1) (0.3) (0.2) (0.1) (9.6) (94.7)

267 681 369 173 28 13 26 1557 43068(0.6) (1.6) (0.8) (0.4) (0.1) (0.0) (0.1) (3.6) (98.3)

13 256 128 13 1 13 424 43492(0.0) (0.6) (0.3) (0.0) (0.0) (0.0) (1.0) (99.2)

131 36 9 176 43668(0.3) (0.1) (0.0) (0.4) (99.6)

34 35 6 75 43743(0.1) (0.1) (0.0) (0.2) (99.8)

2 17 10 29 43772(0.0) (0.0) (0.0) (0.1) (99.9)

13 4 2 19 43791(0.0) (0.0) (0.0) (0.0) (99.9)

6 7 4 17 43808(0.0) (0.0) (0.0) (0.0) (100.0)

5 5 10 43818(0.0) (0.0) (0.0) (100.0)

6 6 43824(0.0) (0.0) (100.0)

0 43824(0.0) (100.0)

0 6 459 1771 5345 10743 11474 7453 4038 1633 668 199 35 0 43824(0.0) (0.0) (1.0) (4.0) (12.2) (24.5) (26.2) (17.0) (9.2) (3.7) (1.5) (0.5) (0.1) (0.0) (100.0)

0 6 465 2236 7581 18324 29798 37251 41289 42922 43590 43789 43824 43824(0.0) (0.0) (1.1) (5.1) (17.3) (41.8) (68.0) (85.0) (94.2) (97.9) (99.5) (99.9) (100.0) (100.0)

upper : frequency , (lower) : ratio

~ 0.49

0.50 ~ 0.99

1.00 ~ 1.49

1.50 ~ 1.99

4.50 ~ 4.99

5.00 ~ 5.49

5.50 ~ 5.99

2.00 ~ 2.49

2.50 ~ 2.99

3.00 ~ 3.49

3.50 ~ 3.99

Total amount

Sum

Total amount

Period (s)Height (m)

6.00 ~ 6.49

6.50 ~ 6.99

7.00 ~

Sum

4.00 ~ 4.49

3

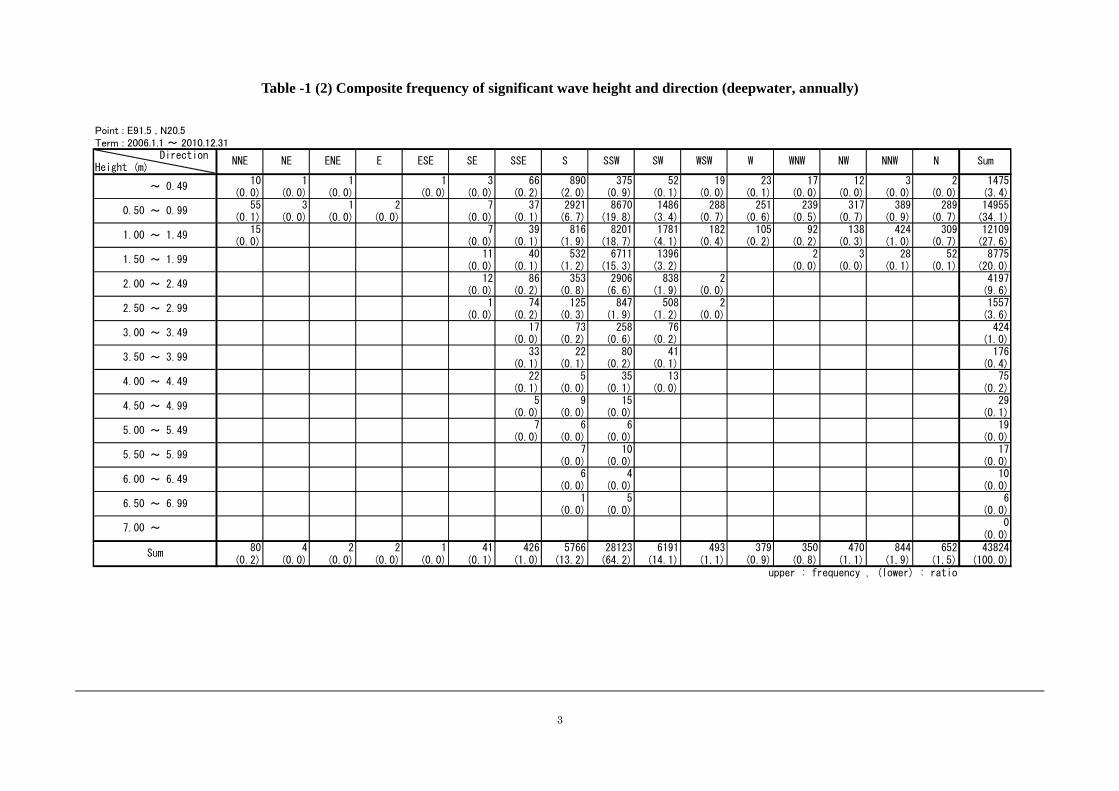

Table -1 (2) Composite frequency of significant wave height and direction (deepwater, annually)

Point : E91.5 , N20.5Term : 2006.1.1 ~ 2010.12.31

10 1 1 1 3 66 890 375 52 19 23 17 12 3 2 1475(0.0) (0.0) (0.0) (0.0) (0.0) (0.2) (2.0) (0.9) (0.1) (0.0) (0.1) (0.0) (0.0) (0.0) (0.0) (3.4)

55 3 1 2 7 37 2921 8670 1486 288 251 239 317 389 289 14955(0.1) (0.0) (0.0) (0.0) (0.0) (0.1) (6.7) (19.8) (3.4) (0.7) (0.6) (0.5) (0.7) (0.9) (0.7) (34.1)

15 7 39 816 8201 1781 182 105 92 138 424 309 12109(0.0) (0.0) (0.1) (1.9) (18.7) (4.1) (0.4) (0.2) (0.2) (0.3) (1.0) (0.7) (27.6)

11 40 532 6711 1396 2 3 28 52 8775(0.0) (0.1) (1.2) (15.3) (3.2) (0.0) (0.0) (0.1) (0.1) (20.0)

12 86 353 2906 838 2 4197(0.0) (0.2) (0.8) (6.6) (1.9) (0.0) (9.6)

1 74 125 847 508 2 1557(0.0) (0.2) (0.3) (1.9) (1.2) (0.0) (3.6)

17 73 258 76 424(0.0) (0.2) (0.6) (0.2) (1.0)

33 22 80 41 176(0.1) (0.1) (0.2) (0.1) (0.4)

22 5 35 13 75(0.1) (0.0) (0.1) (0.0) (0.2)

5 9 15 29(0.0) (0.0) (0.0) (0.1)

7 6 6 19(0.0) (0.0) (0.0) (0.0)

7 10 17(0.0) (0.0) (0.0)

6 4 10(0.0) (0.0) (0.0)

1 5 6(0.0) (0.0) (0.0)

0(0.0)

80 4 2 2 1 41 426 5766 28123 6191 493 379 350 470 844 652 43824(0.2) (0.0) (0.0) (0.0) (0.0) (0.1) (1.0) (13.2) (64.2) (14.1) (1.1) (0.9) (0.8) (1.1) (1.9) (1.5) (100.0)

upper : frequency , (lower) : ratio

N

Sum

DirectionHeight (m)

6.00 ~ 6.49

6.50 ~ 6.99

7.00 ~

Sum

4.00 ~ 4.49

4.50 ~ 4.99

5.00 ~ 5.49

5.50 ~ 5.99

2.00 ~ 2.49

2.50 ~ 2.99

3.00 ~ 3.49

3.50 ~ 3.99

~ 0.49

0.50 ~ 0.99

1.00 ~ 1.49

1.50 ~ 1.99

NNE NE ENE E ESE SE SSE S WNW NW NNWSSW SW WSW W

4

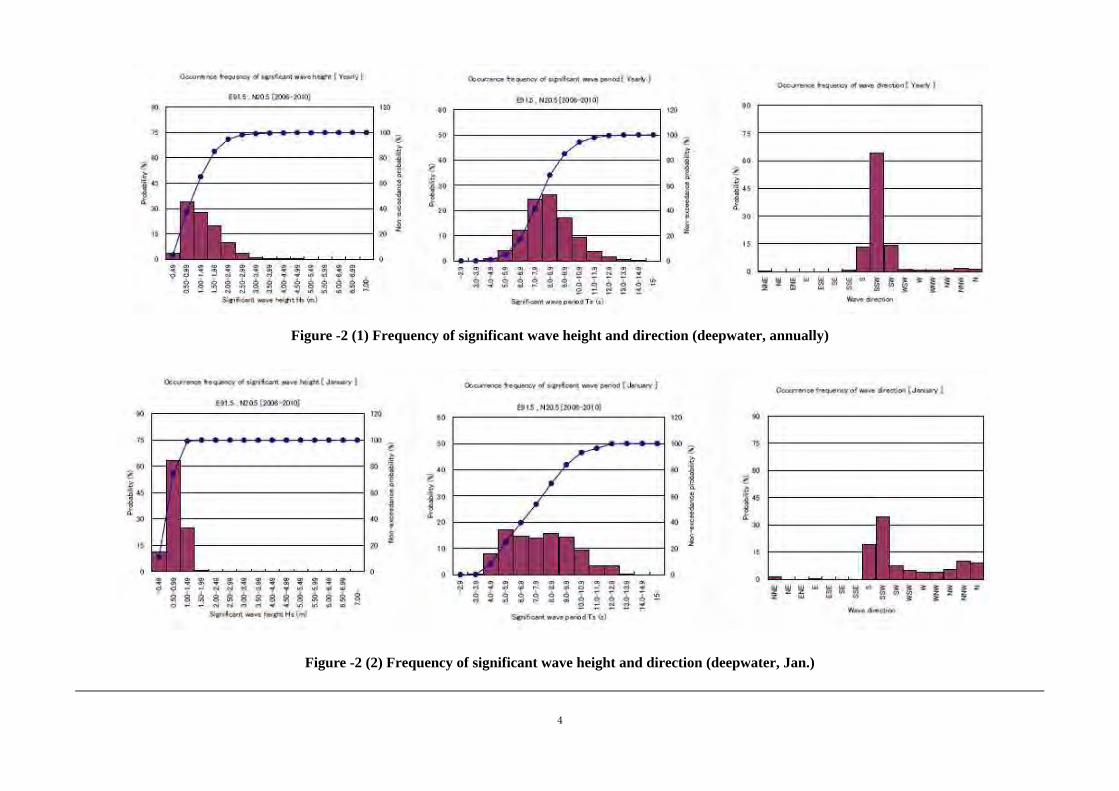

Figure -2 (1) Frequency of significant wave height and direction (deepwater, annually)

Figure -2 (2) Frequency of significant wave height and direction (deepwater, Jan.)

5

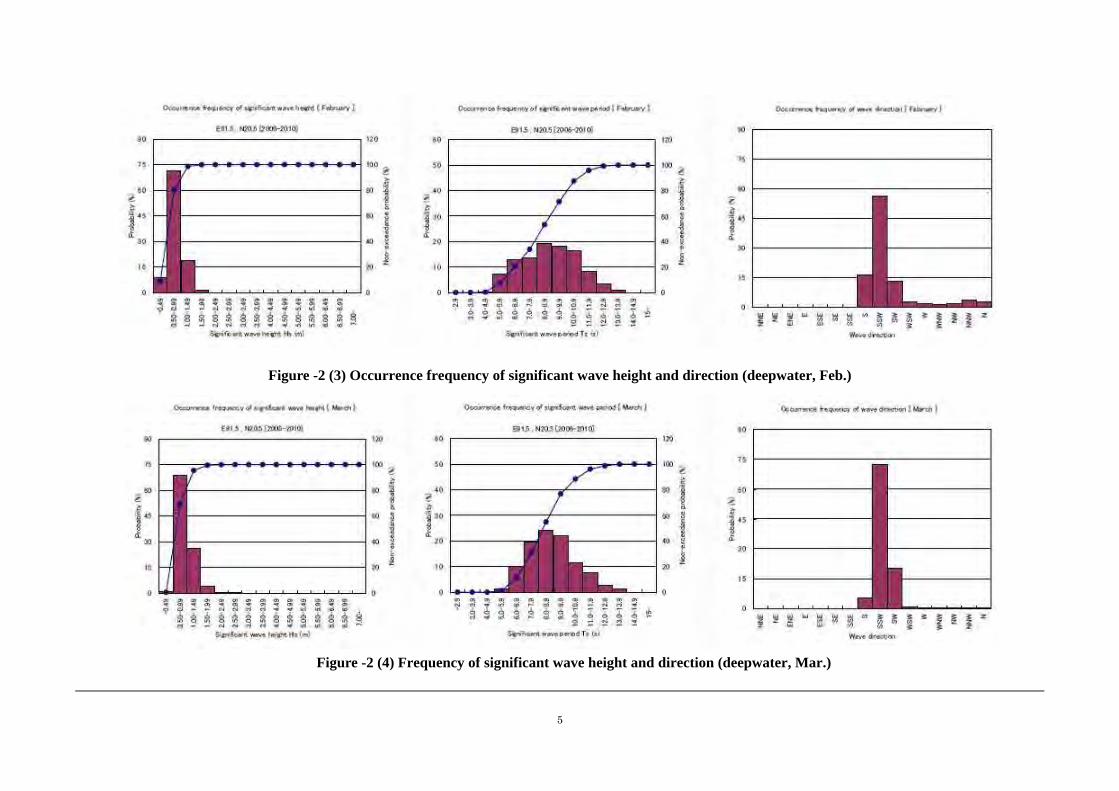

Figure -2 (3) Occurrence frequency of significant wave height and direction (deepwater, Feb.)

Figure -2 (4) Frequency of significant wave height and direction (deepwater, Mar.)

6

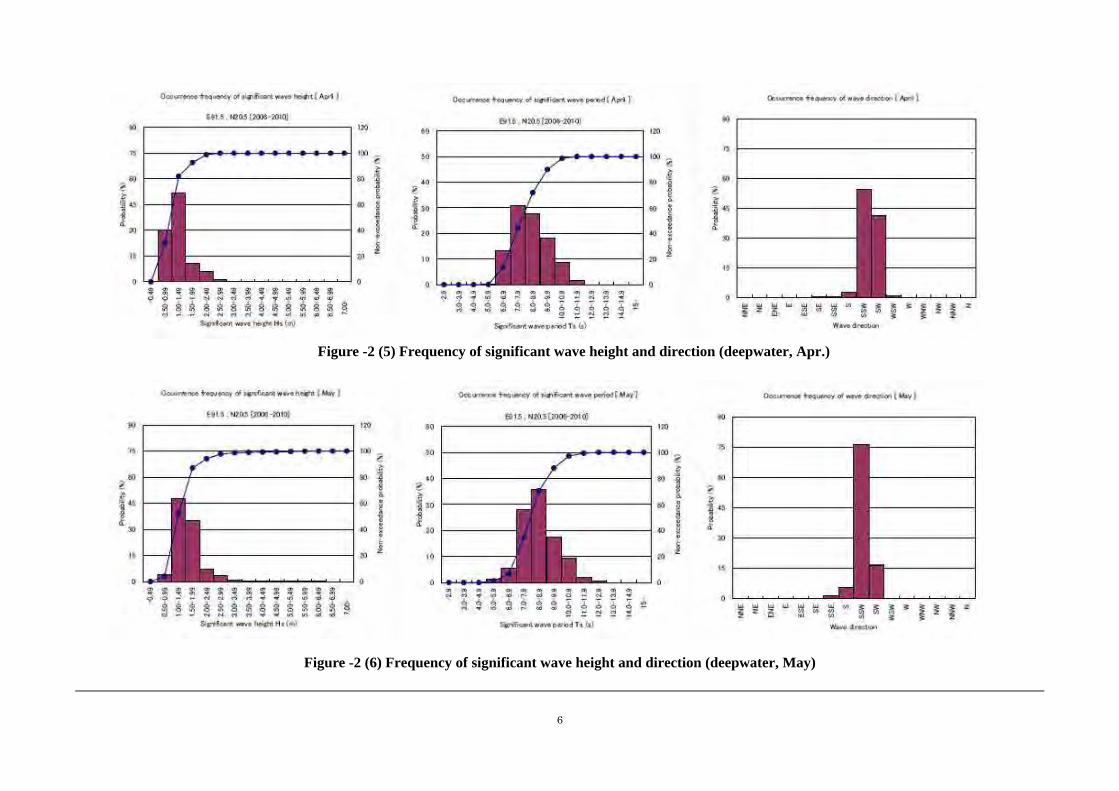

Figure -2 (5) Frequency of significant wave height and direction (deepwater, Apr.)

Figure -2 (6) Frequency of significant wave height and direction (deepwater, May)

7

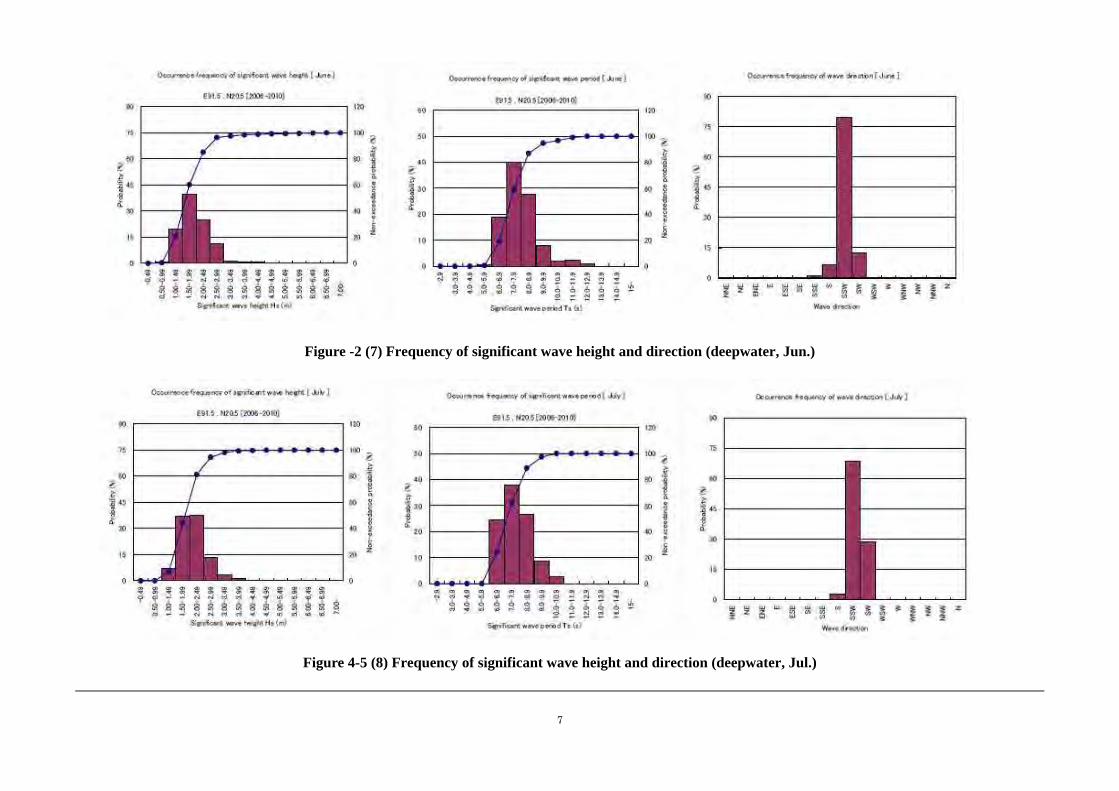

Figure -2 (7) Frequency of significant wave height and direction (deepwater, Jun.)

Figure 4-5 (8) Frequency of significant wave height and direction (deepwater, Jul.)

8

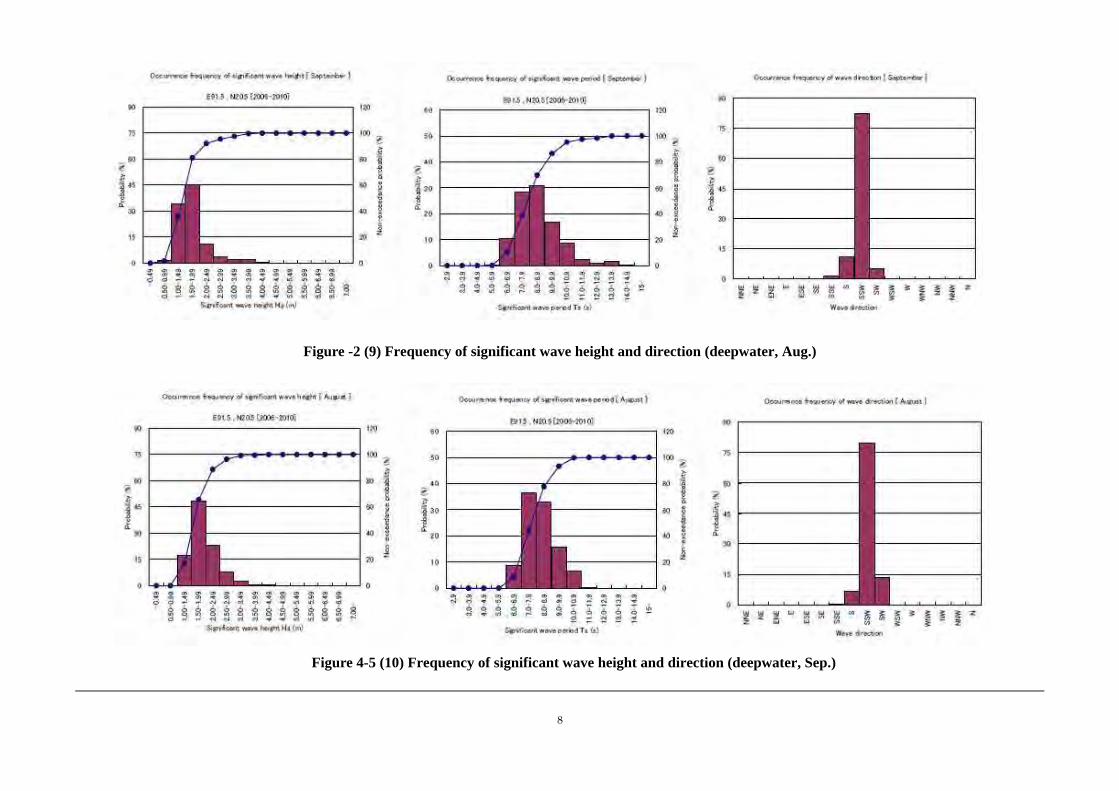

Figure -2 (9) Frequency of significant wave height and direction (deepwater, Aug.)

Figure 4-5 (10) Frequency of significant wave height and direction (deepwater, Sep.)

9

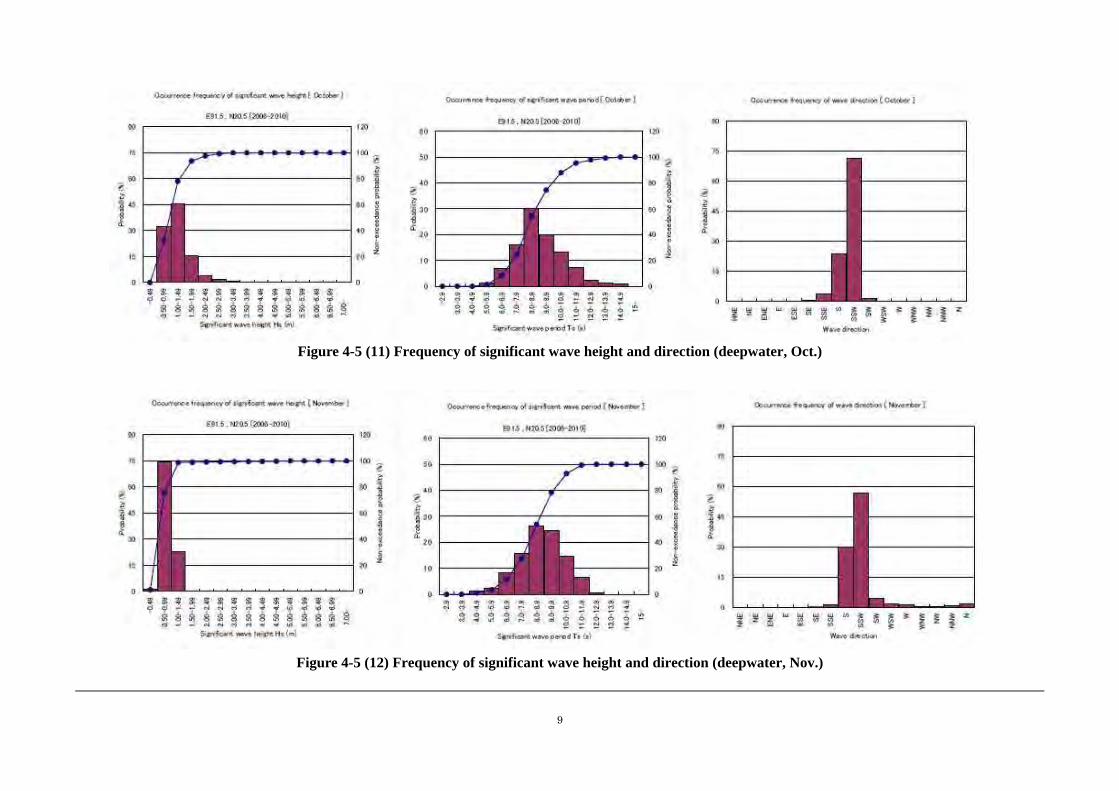

Figure 4-5 (11) Frequency of significant wave height and direction (deepwater, Oct.)

Figure 4-5 (12) Frequency of significant wave height and direction (deepwater, Nov.)

10

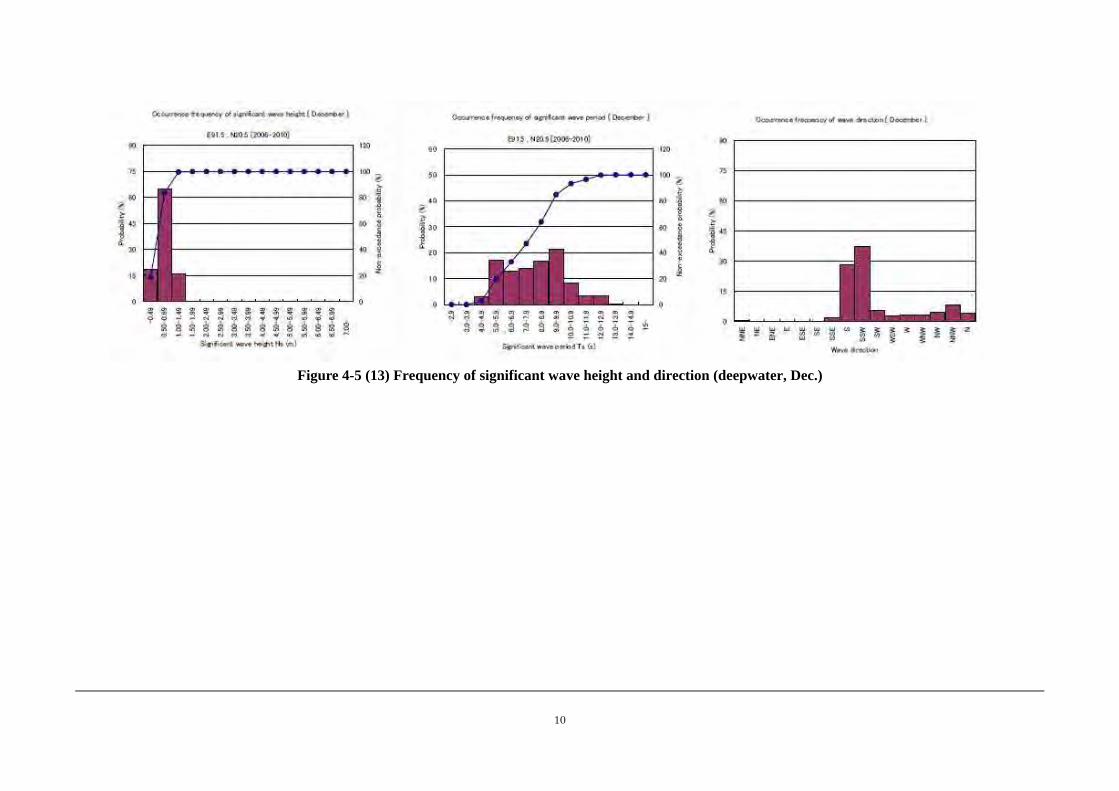

Figure 4-5 (13) Frequency of significant wave height and direction (deepwater, Dec.)

11

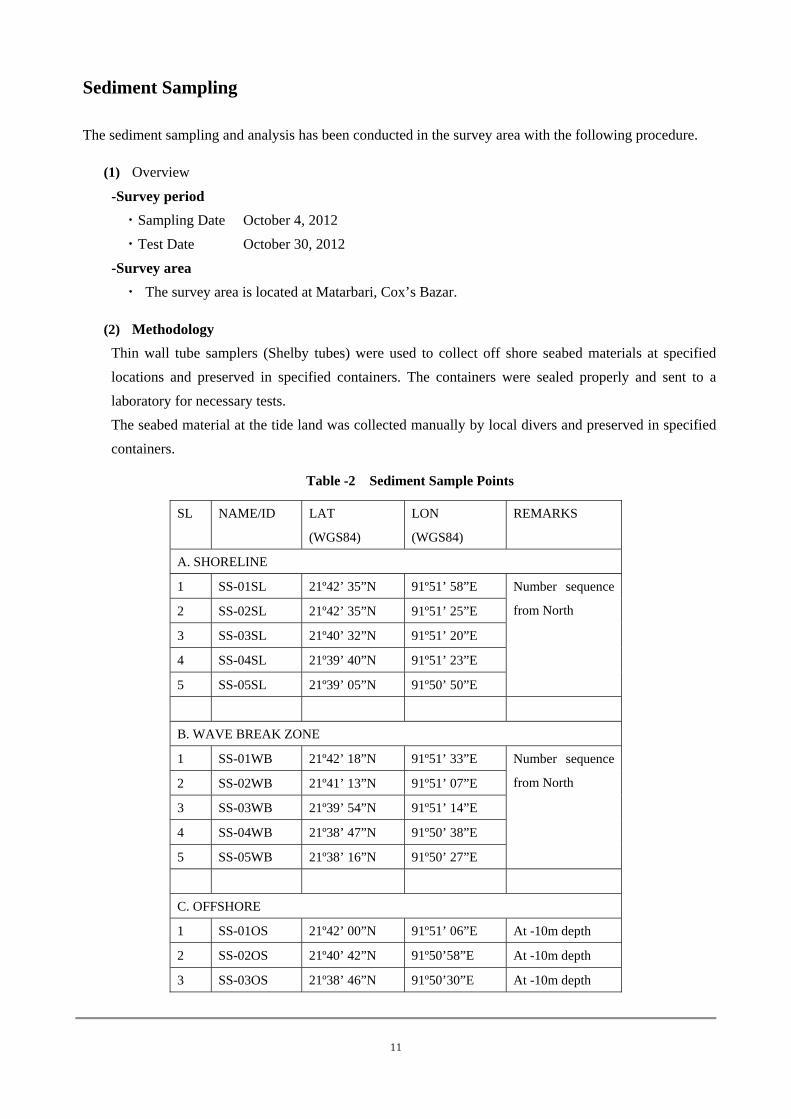

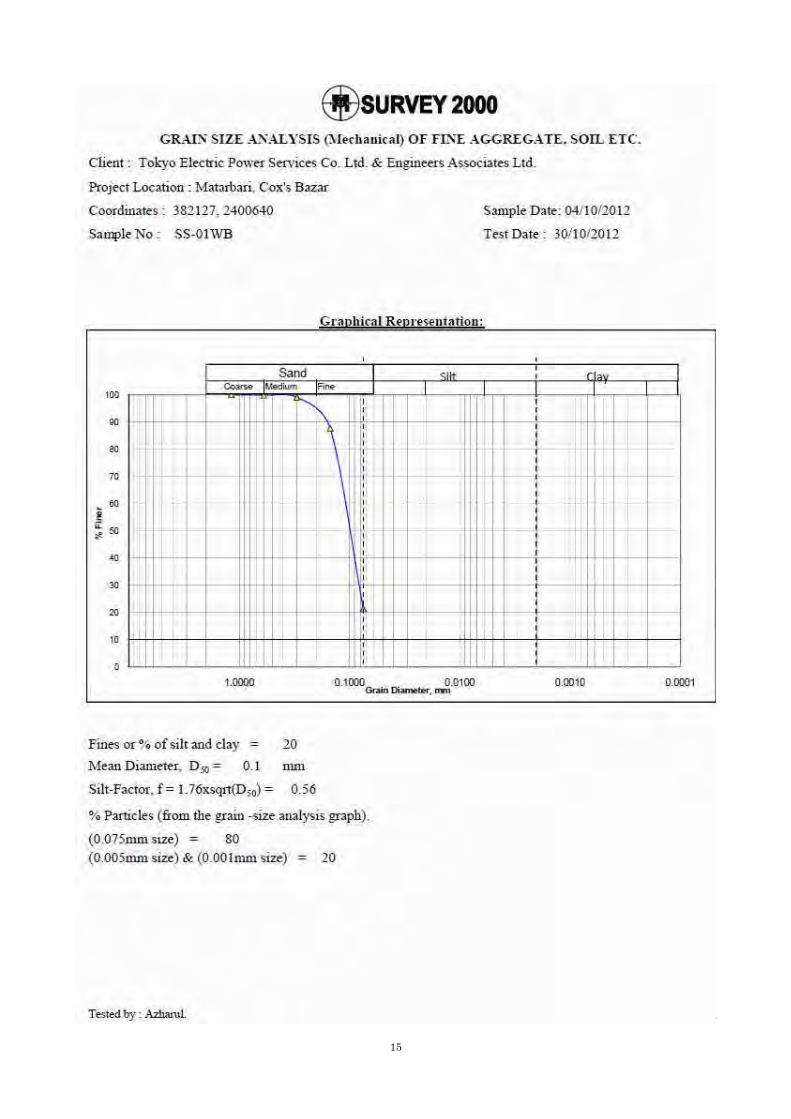

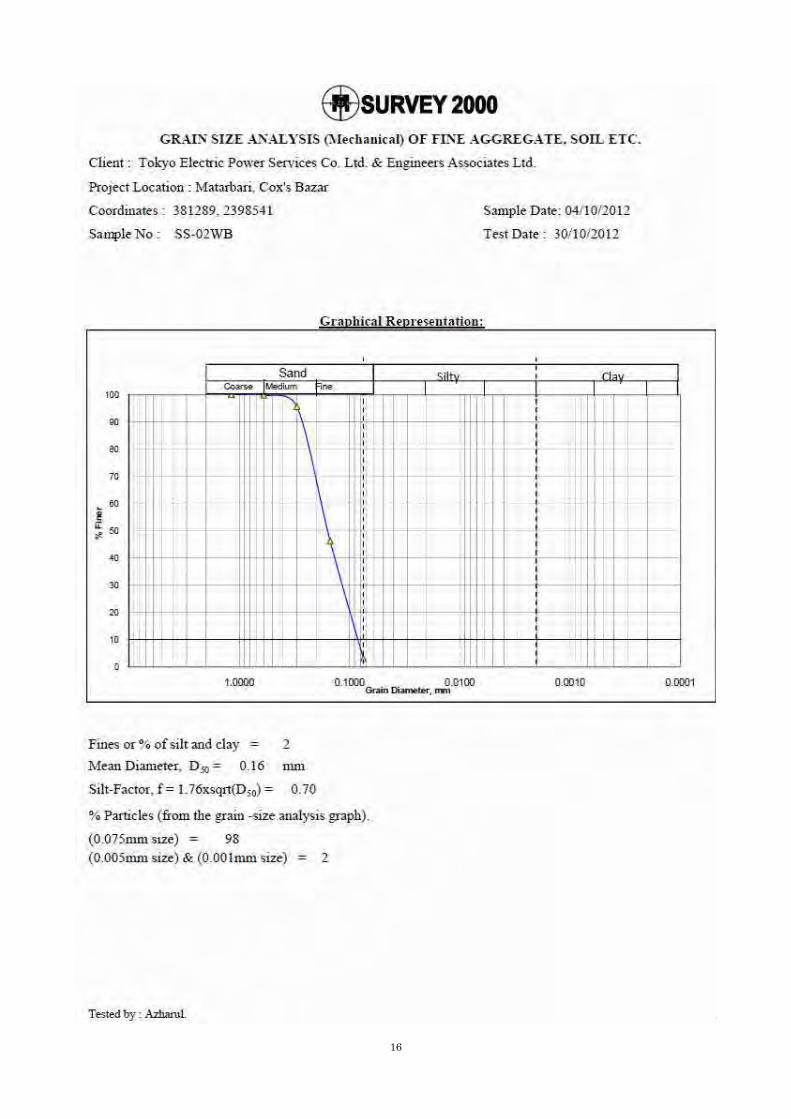

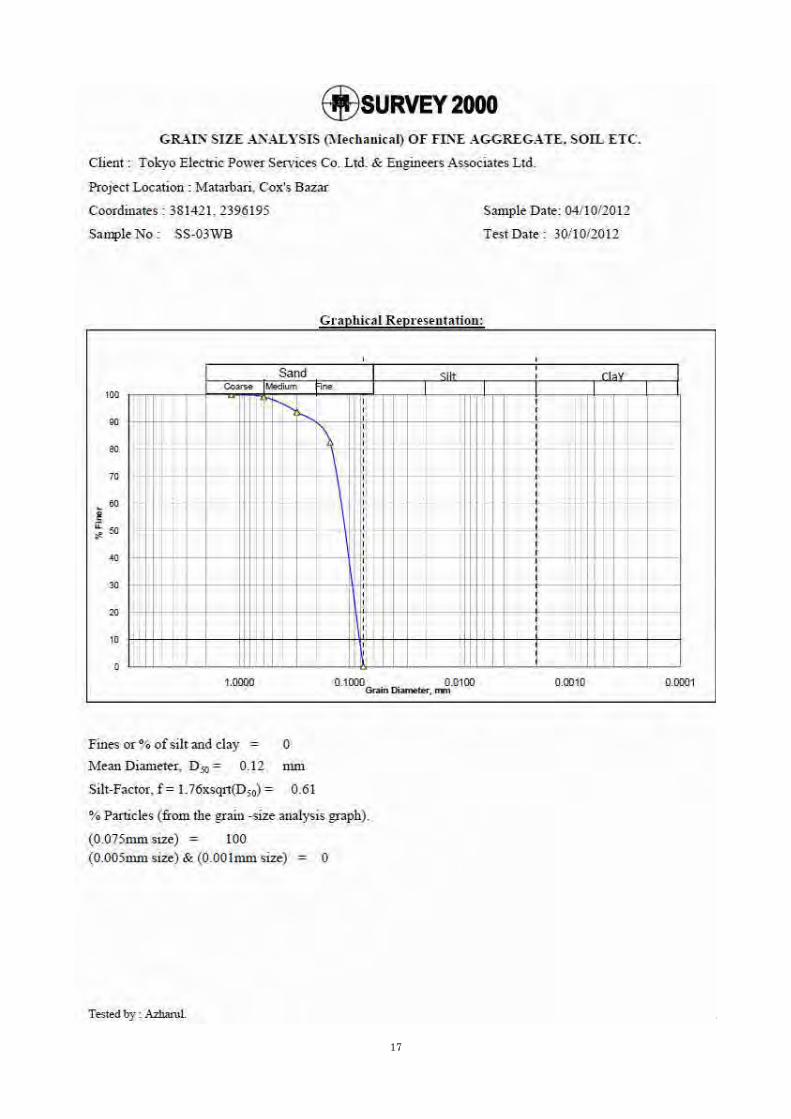

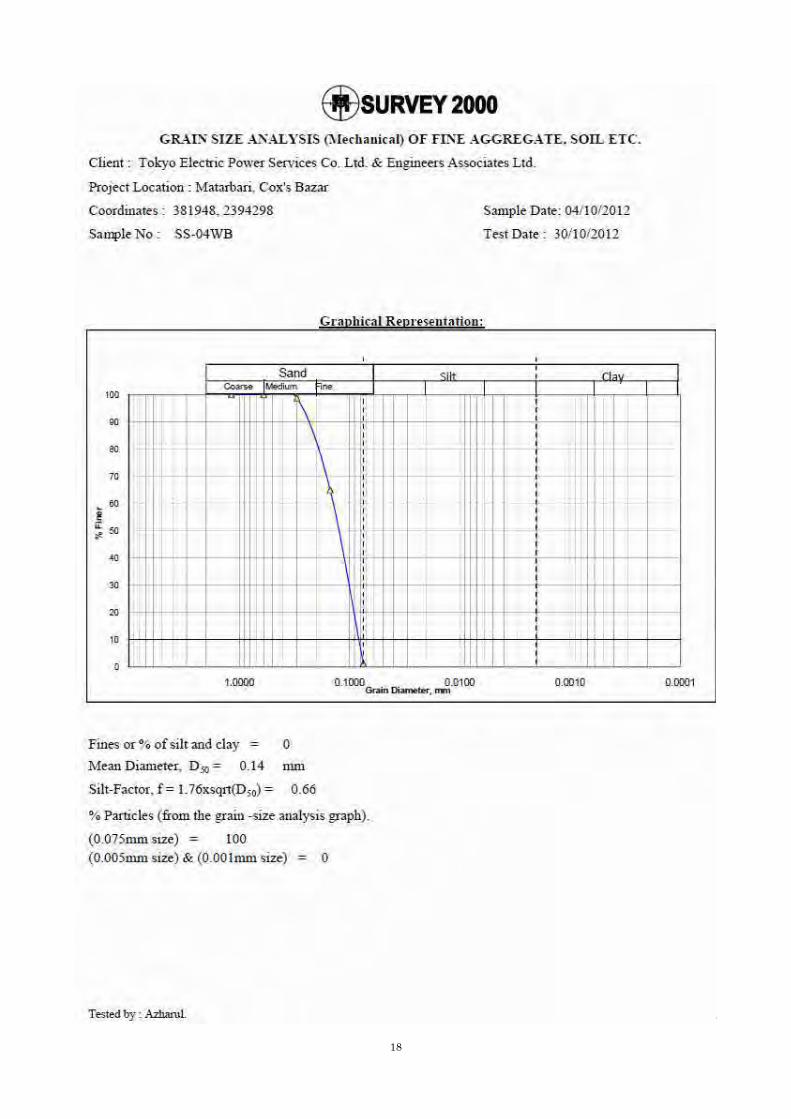

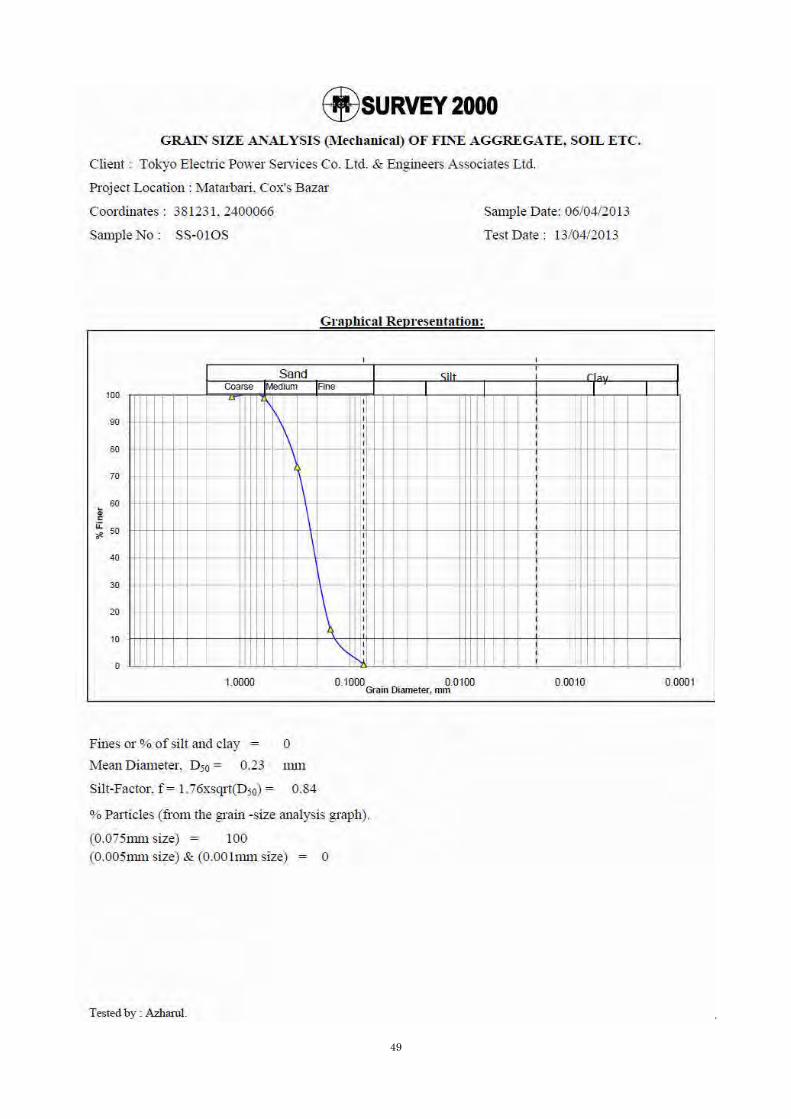

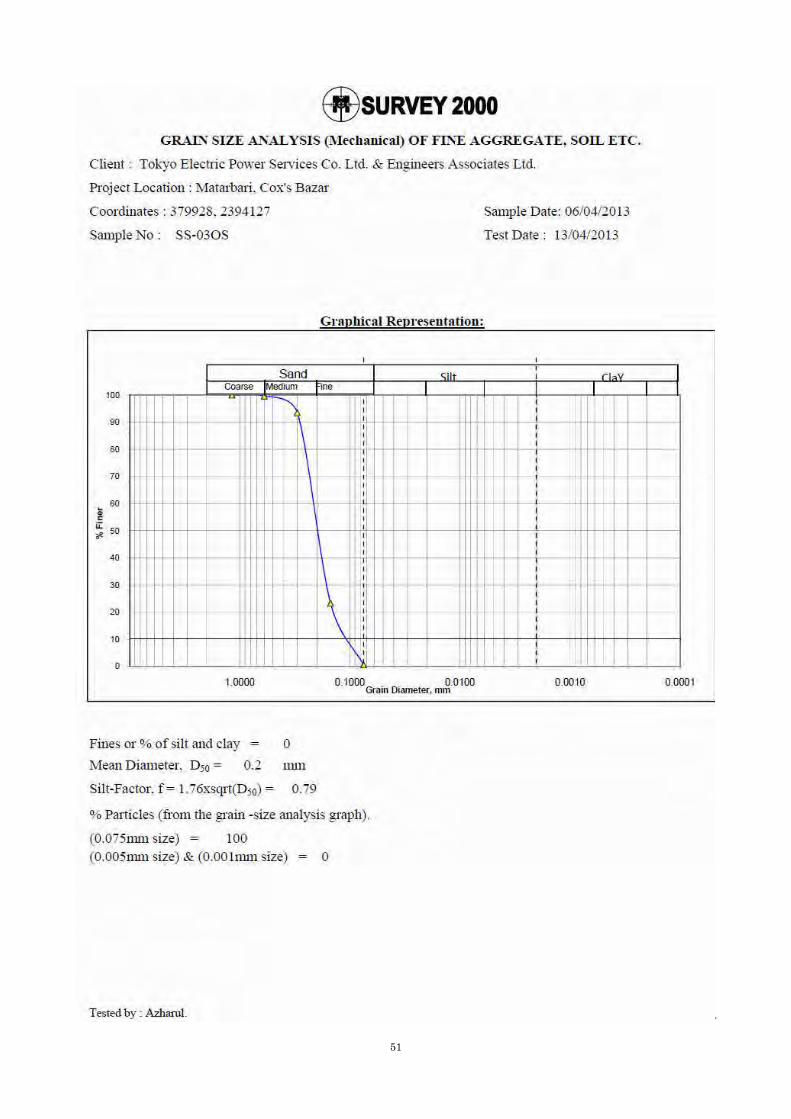

Sediment Sampling

The sediment sampling and analysis has been conducted in the survey area with the following procedure.

(1) Overview

-Survey period

・Sampling Date October 4, 2012

・Test Date October 30, 2012

-Survey area

・ The survey area is located at Matarbari, Cox’s Bazar.

(2) Methodology

Thin wall tube samplers (Shelby tubes) were used to collect off shore seabed materials at specified

locations and preserved in specified containers. The containers were sealed properly and sent to a

laboratory for necessary tests.

The seabed material at the tide land was collected manually by local divers and preserved in specified

containers.

Table -2 Sediment Sample Points

SL NAME/ID LAT

(WGS84)

LON

(WGS84)

REMARKS

A. SHORELINE

1 SS-01SL 21º42’ 35”N 91º51’ 58”E Number sequence

from North 2 SS-02SL 21º42’ 35”N 91º51’ 25”E

3 SS-03SL 21º40’ 32”N 91º51’ 20”E

4 SS-04SL 21º39’ 40”N 91º51’ 23”E

5 SS-05SL 21º39’ 05”N 91º50’ 50”E

B. WAVE BREAK ZONE

1 SS-01WB 21º42’ 18”N 91º51’ 33”E Number sequence

from North 2 SS-02WB 21º41’ 13”N 91º51’ 07”E

3 SS-03WB 21º39’ 54”N 91º51’ 14”E

4 SS-04WB 21º38’ 47”N 91º50’ 38”E

5 SS-05WB 21º38’ 16”N 91º50’ 27”E

C. OFFSHORE

1 SS-01OS 21º42’ 00”N 91º51’ 06”E At -10m depth

2 SS-02OS 21º40’ 42”N 91º50’58”E At -10m depth

3 SS-03OS 21º38’ 46”N 91º50’30”E At -10m depth

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

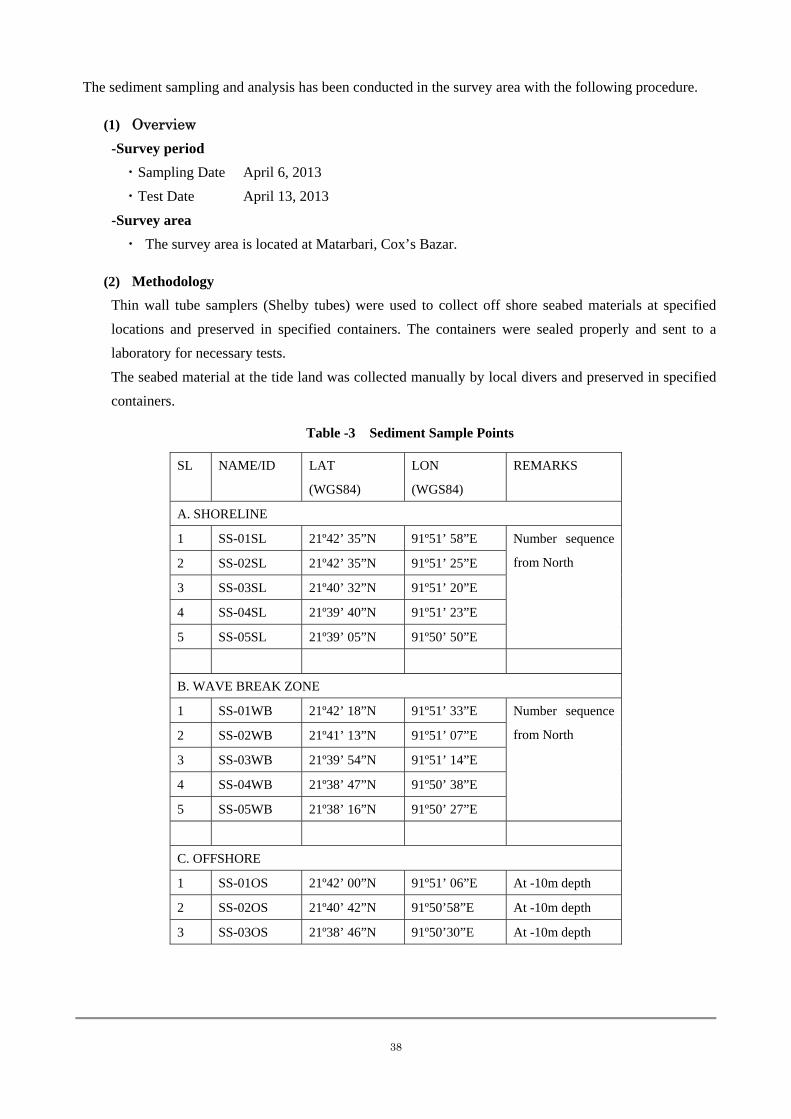

The sediment sampling and analysis has been conducted in the survey area with the following procedure.

(1) Overview

-Survey period

・Sampling Date April 6, 2013

・Test Date April 13, 2013

-Survey area

・ The survey area is located at Matarbari, Cox’s Bazar.

(2) Methodology

Thin wall tube samplers (Shelby tubes) were used to collect off shore seabed materials at specified

locations and preserved in specified containers. The containers were sealed properly and sent to a

laboratory for necessary tests.

The seabed material at the tide land was collected manually by local divers and preserved in specified

containers.

Table -3 Sediment Sample Points

SL NAME/ID LAT

(WGS84)

LON

(WGS84)

REMARKS

A. SHORELINE

1 SS-01SL 21º42’ 35”N 91º51’ 58”E Number sequence

from North 2 SS-02SL 21º42’ 35”N 91º51’ 25”E

3 SS-03SL 21º40’ 32”N 91º51’ 20”E

4 SS-04SL 21º39’ 40”N 91º51’ 23”E

5 SS-05SL 21º39’ 05”N 91º50’ 50”E

B. WAVE BREAK ZONE

1 SS-01WB 21º42’ 18”N 91º51’ 33”E Number sequence

from North 2 SS-02WB 21º41’ 13”N 91º51’ 07”E

3 SS-03WB 21º39’ 54”N 91º51’ 14”E

4 SS-04WB 21º38’ 47”N 91º50’ 38”E

5 SS-05WB 21º38’ 16”N 91º50’ 27”E

C. OFFSHORE

1 SS-01OS 21º42’ 00”N 91º51’ 06”E At -10m depth

2 SS-02OS 21º40’ 42”N 91º50’58”E At -10m depth

3 SS-03OS 21º38’ 46”N 91º50’30”E At -10m depth

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

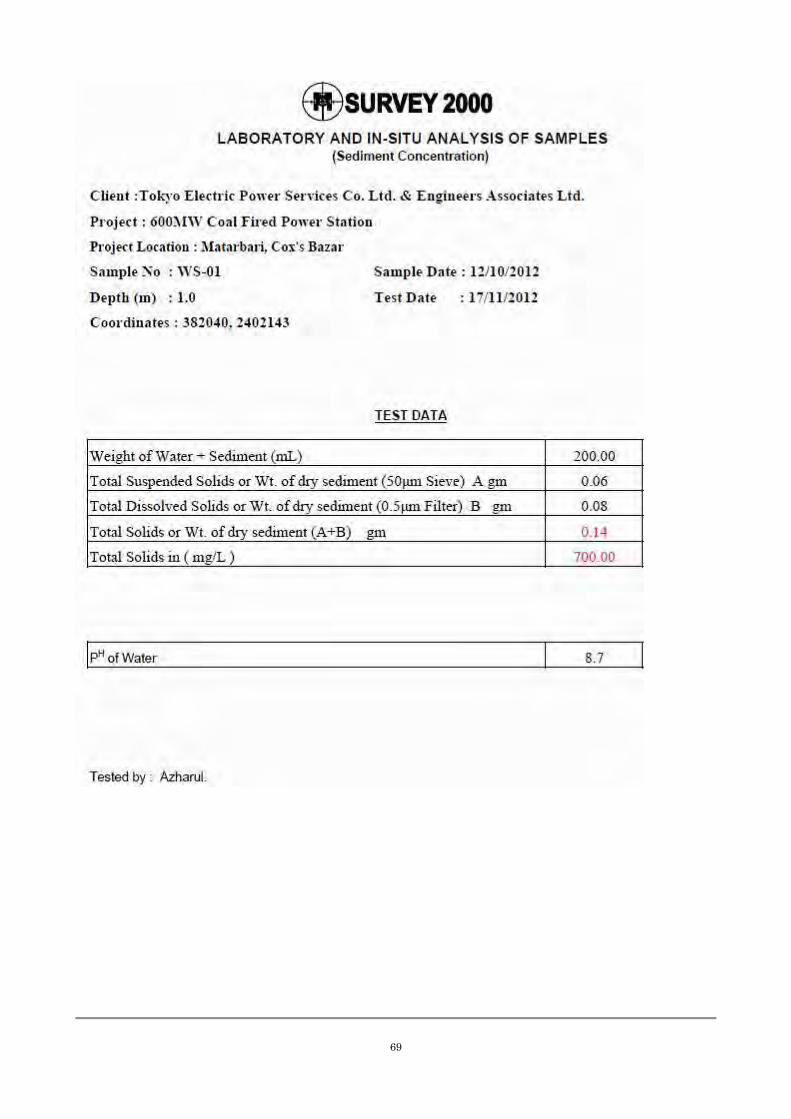

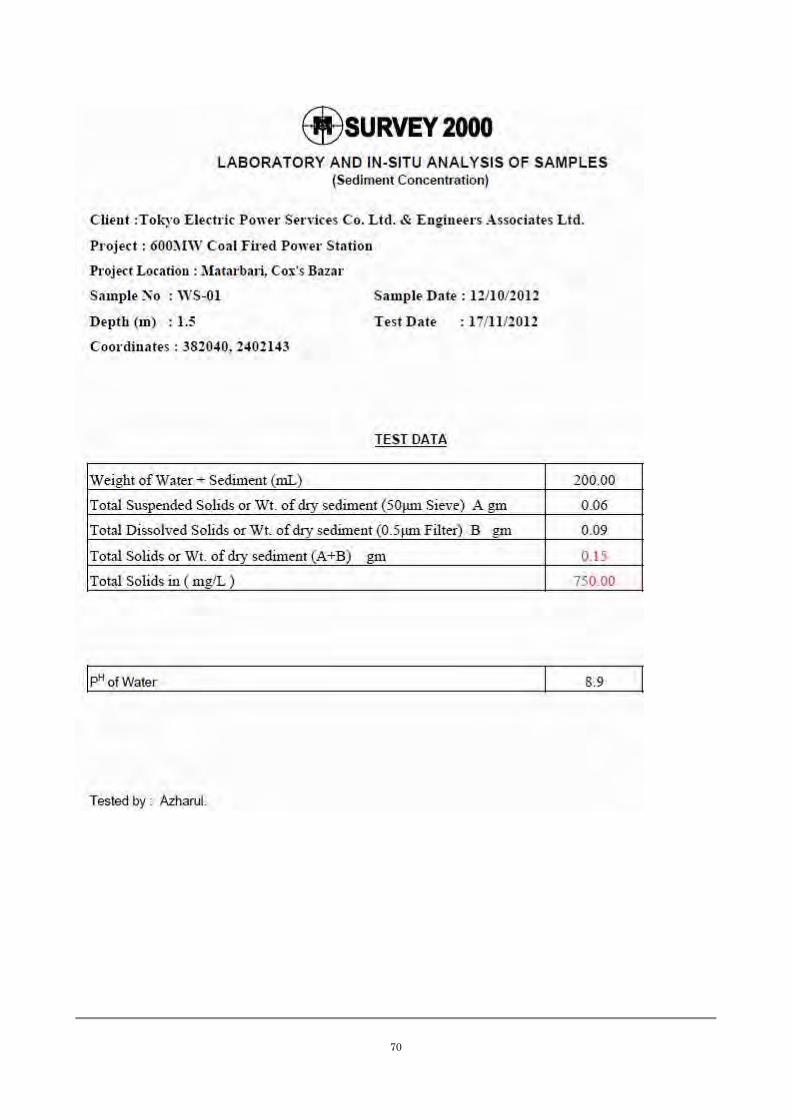

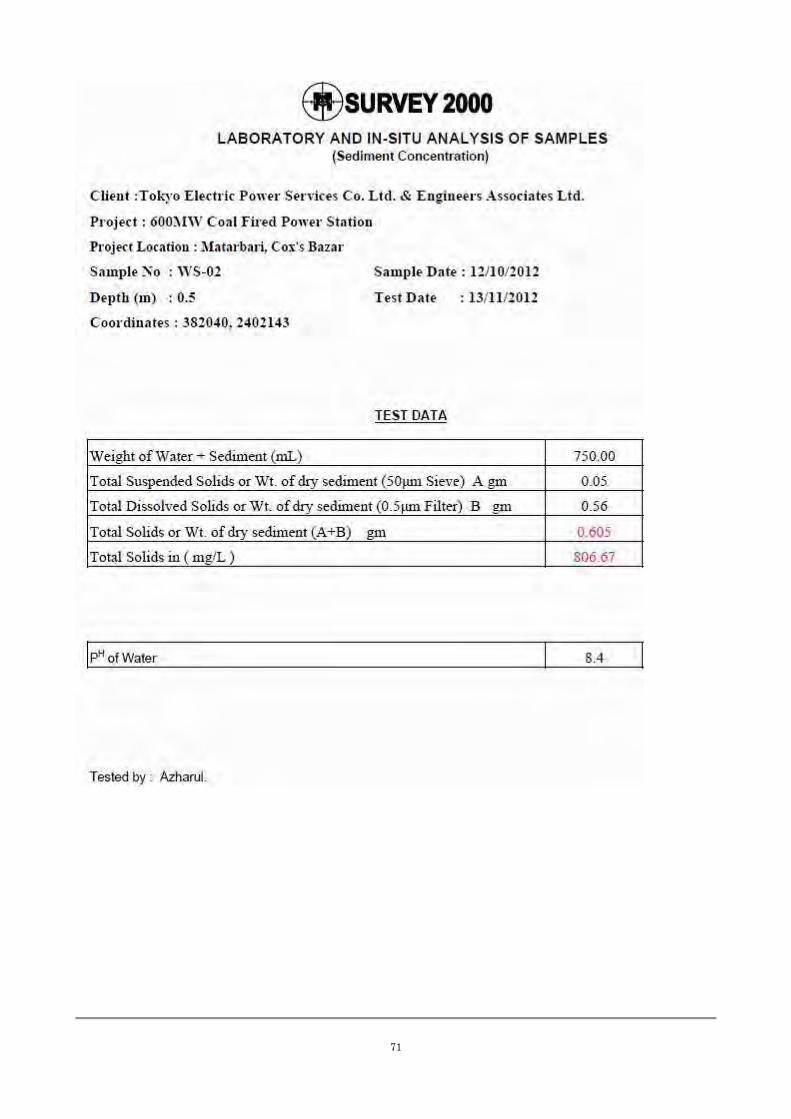

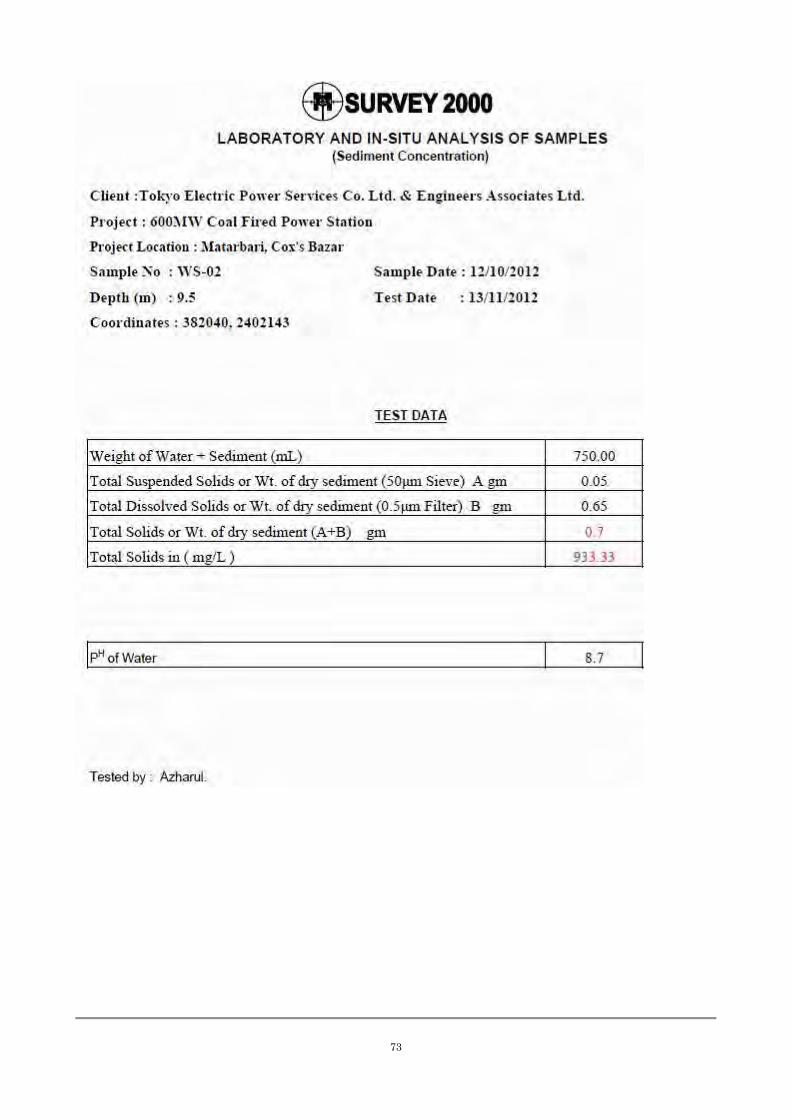

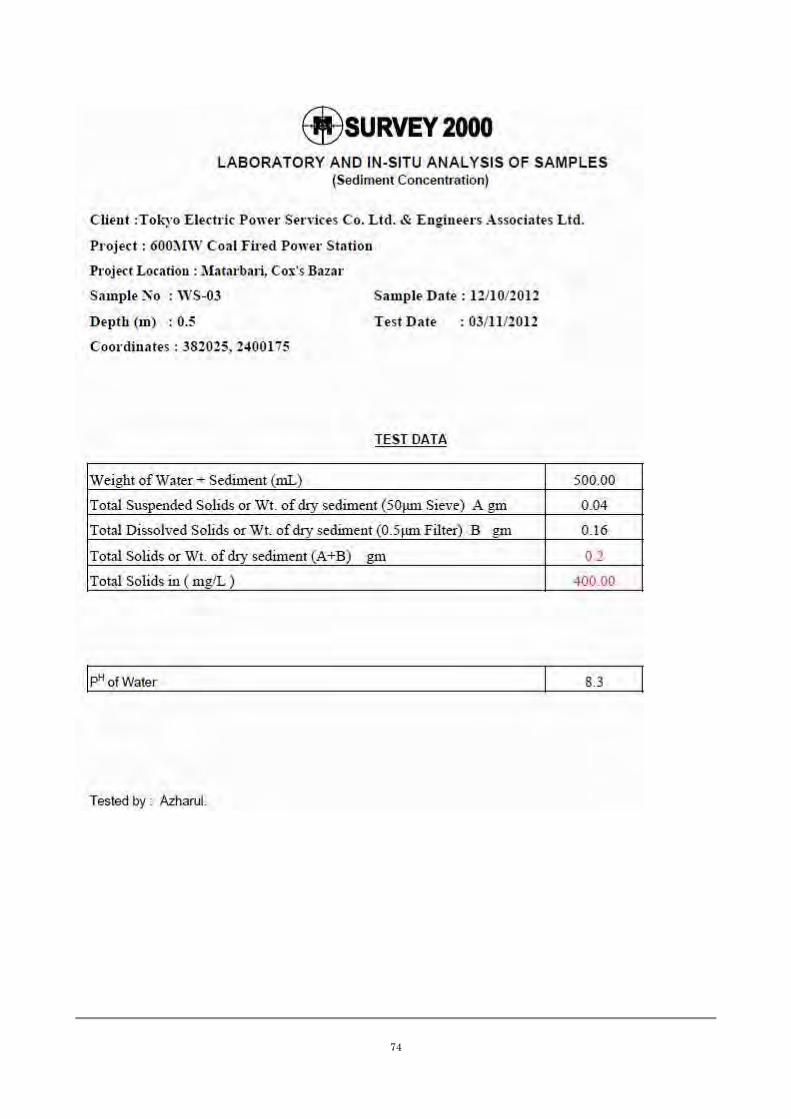

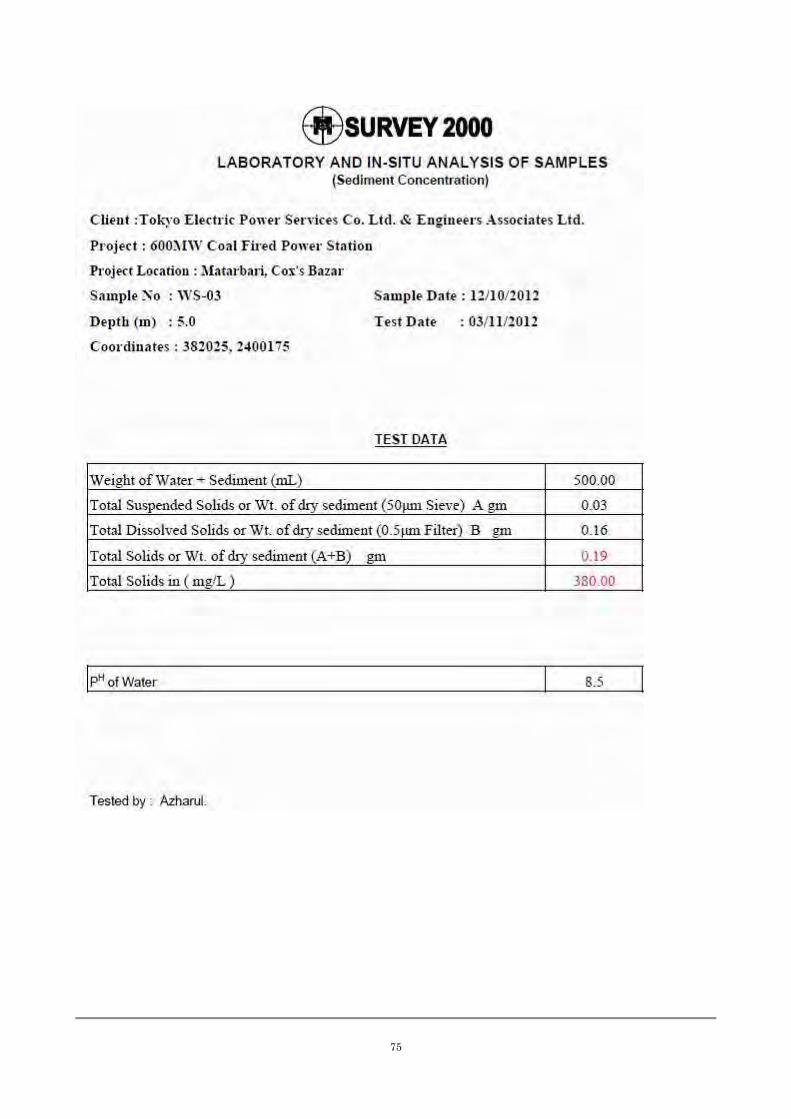

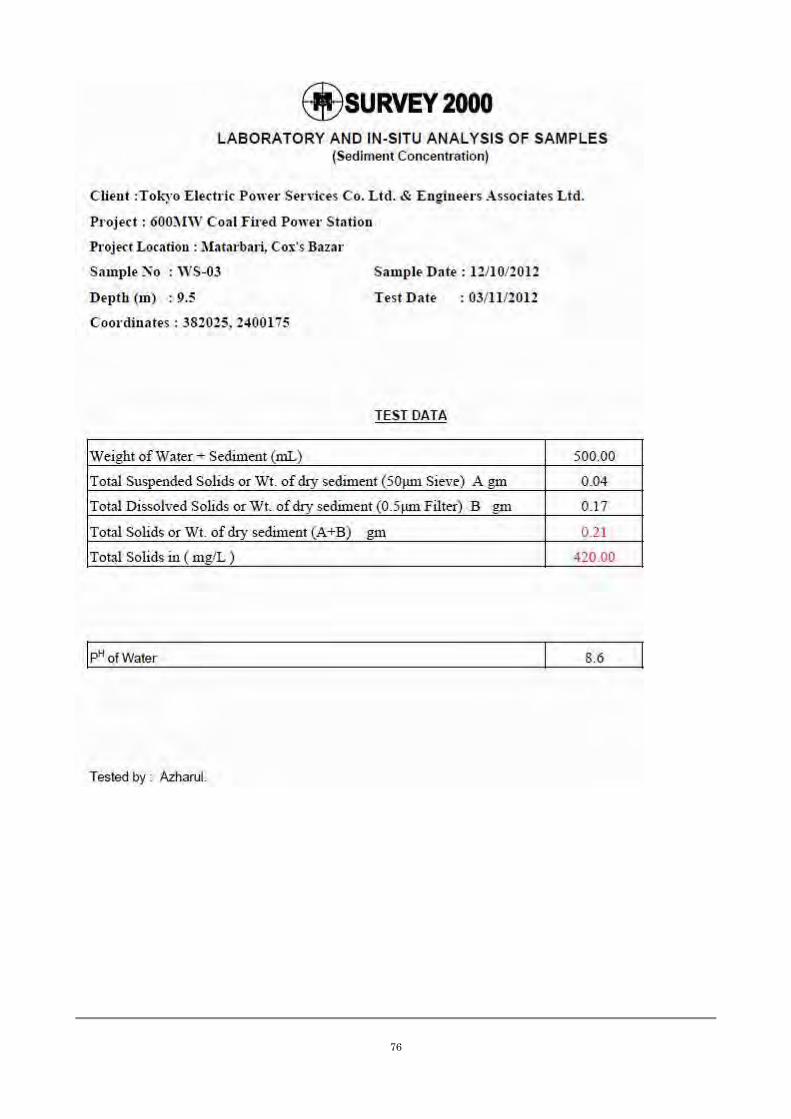

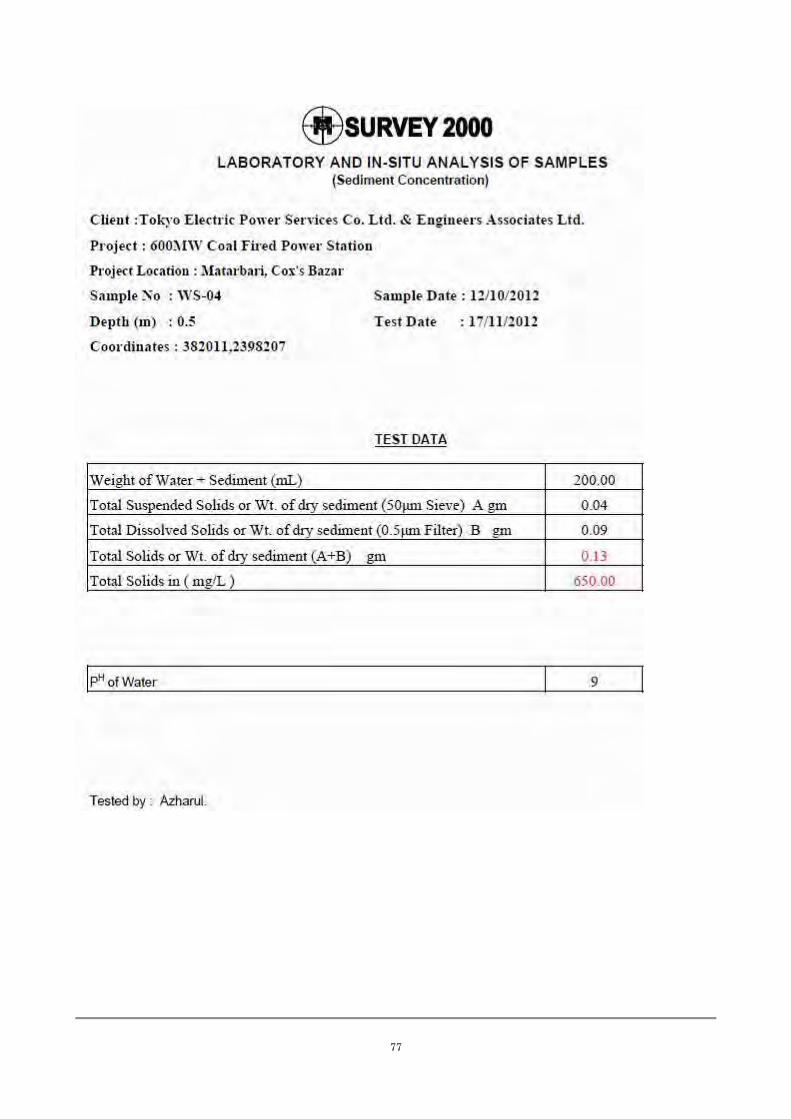

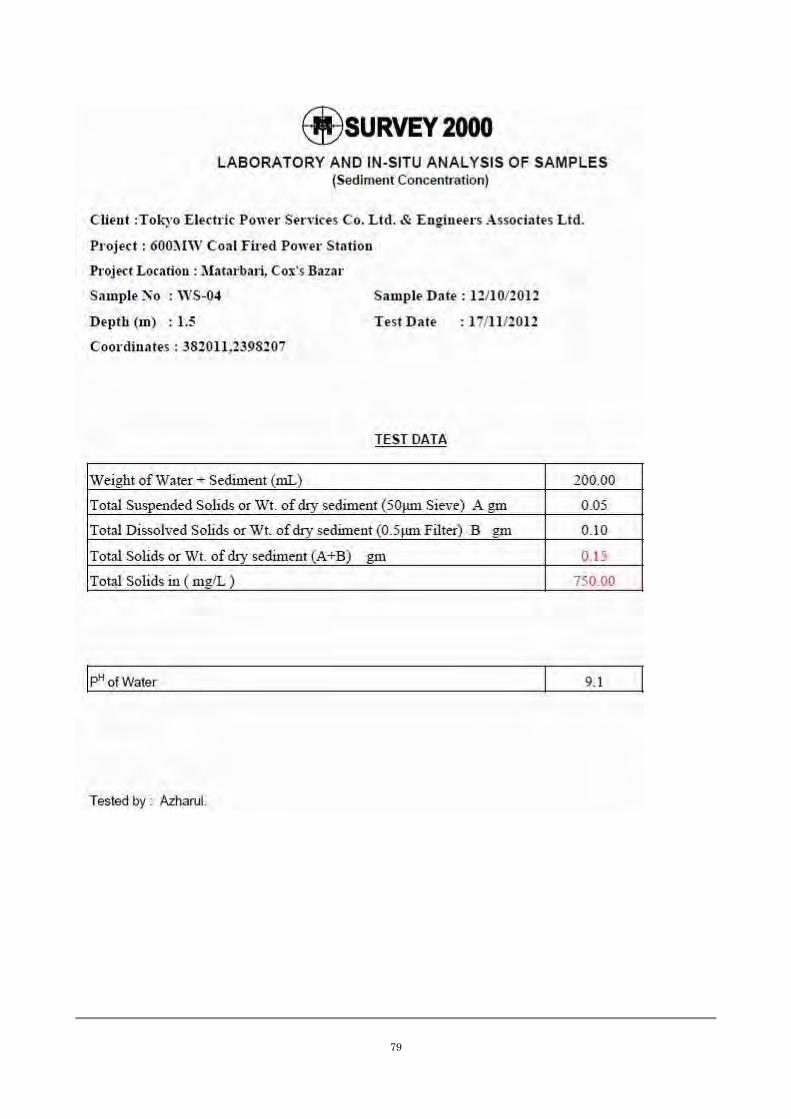

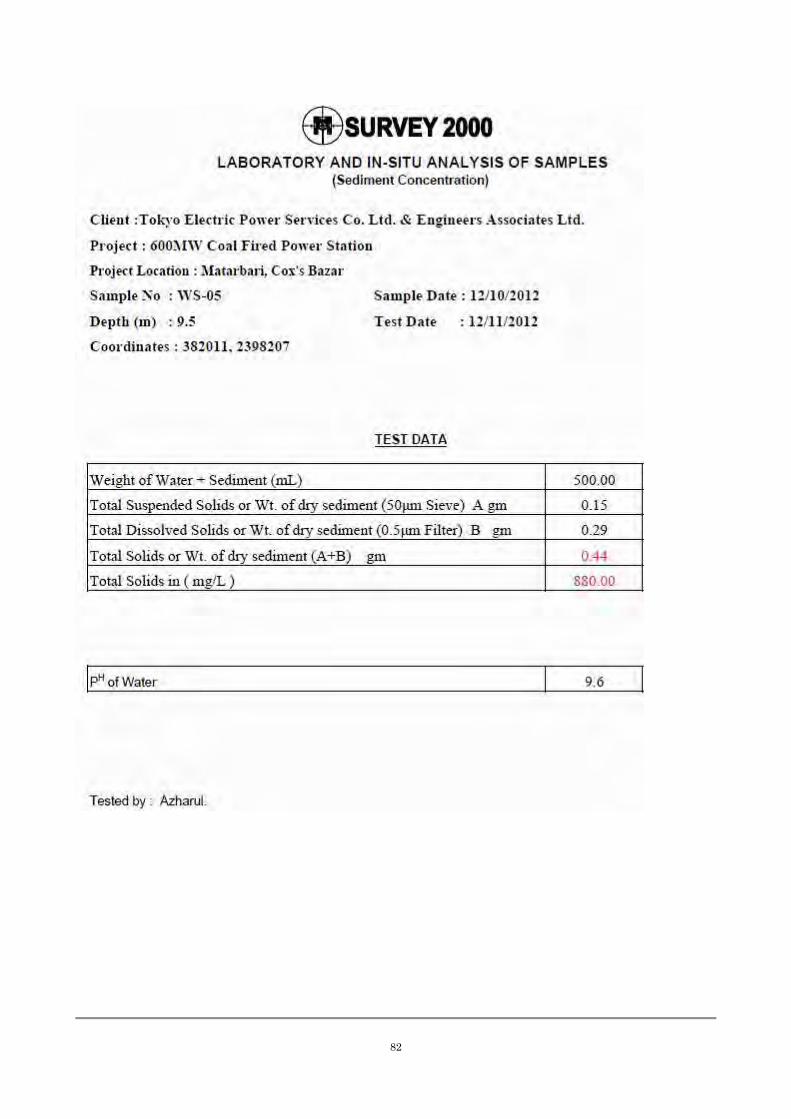

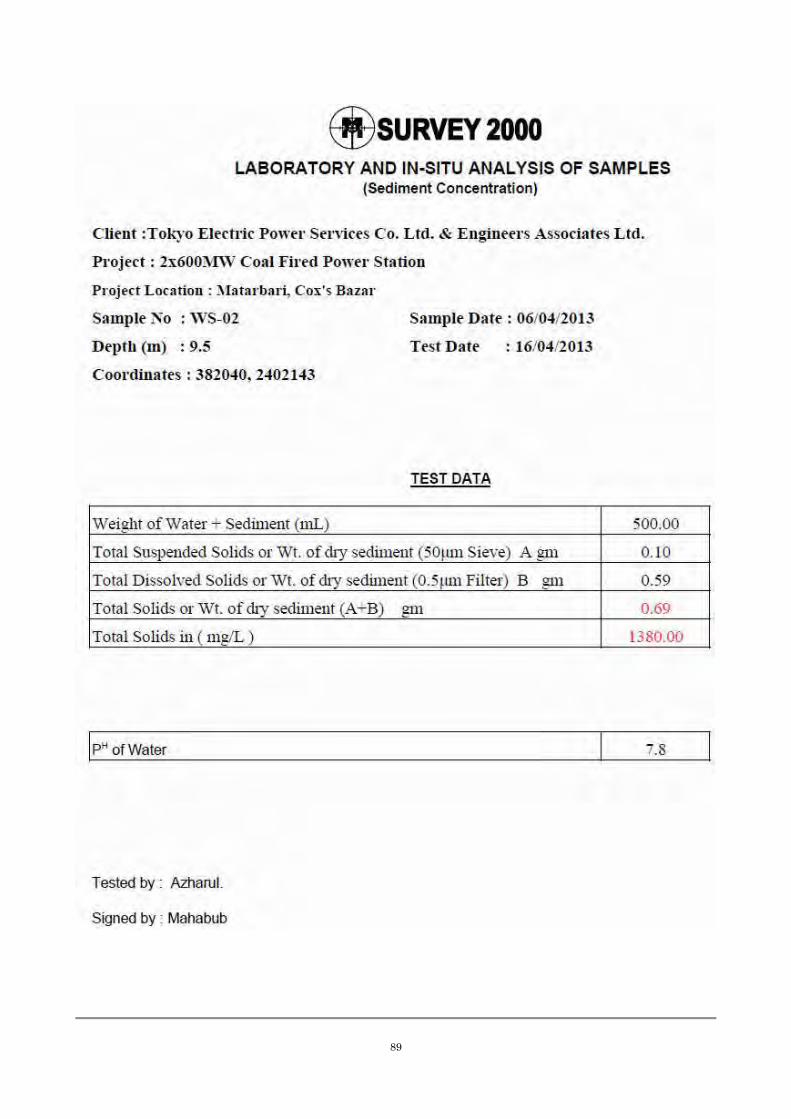

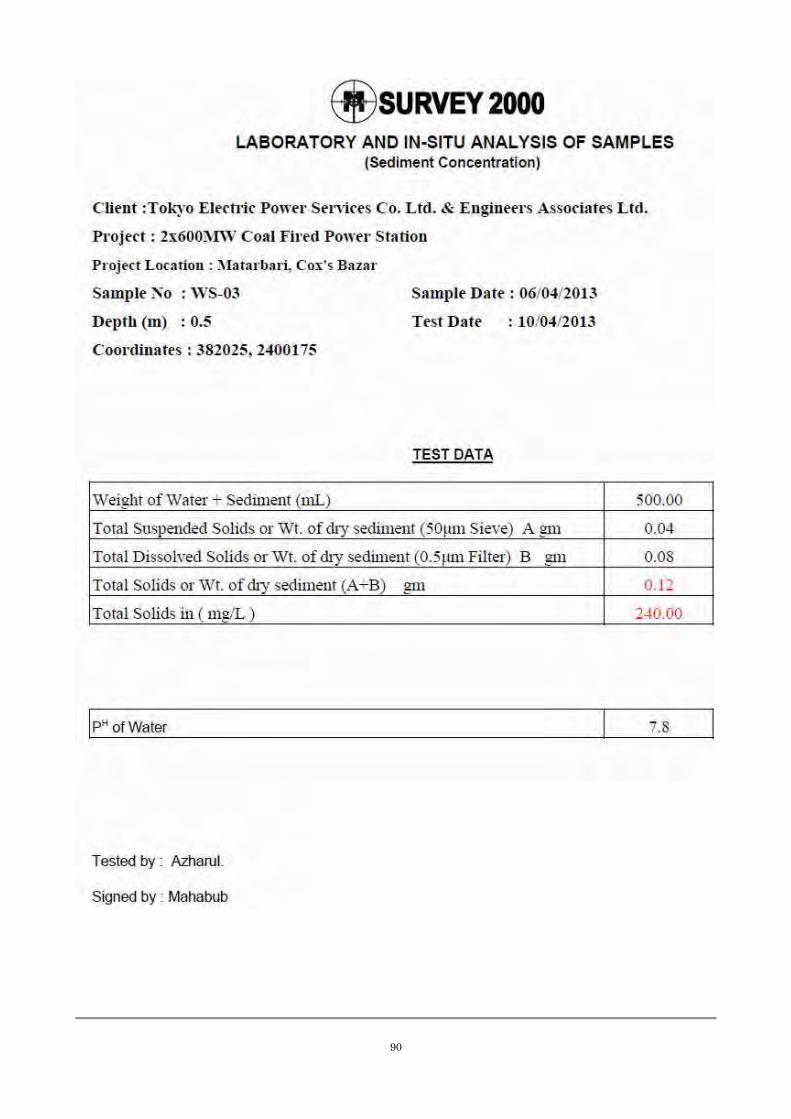

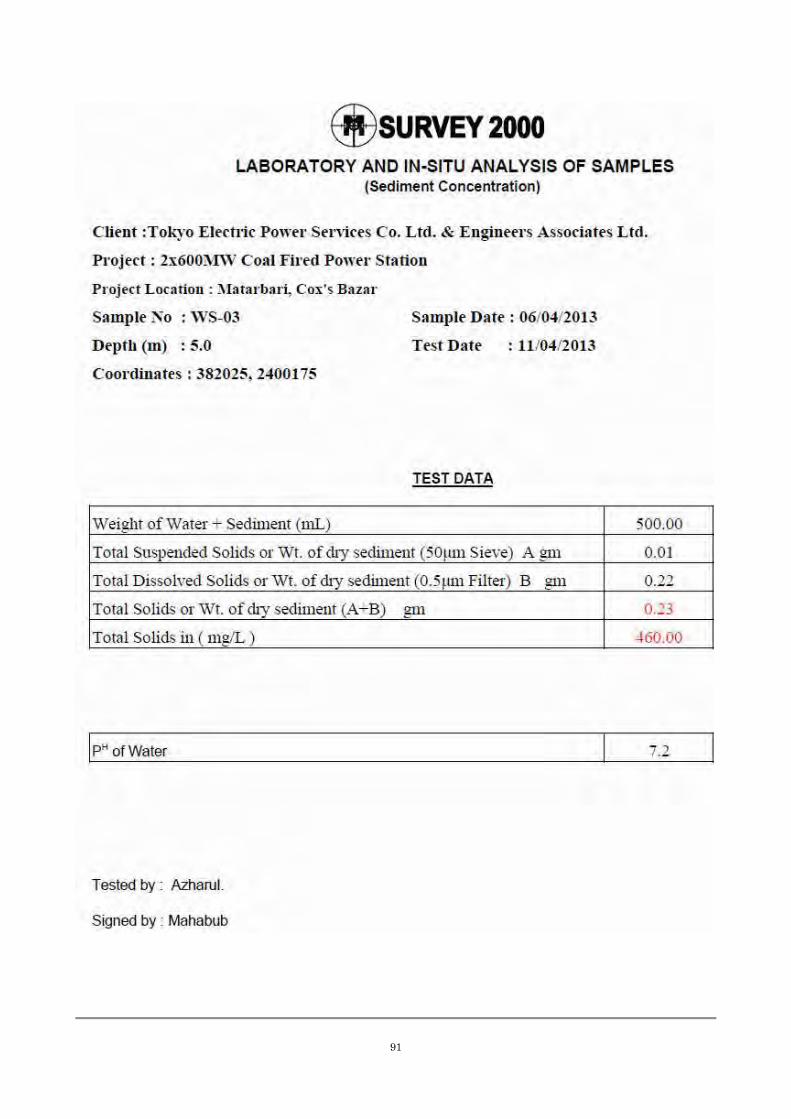

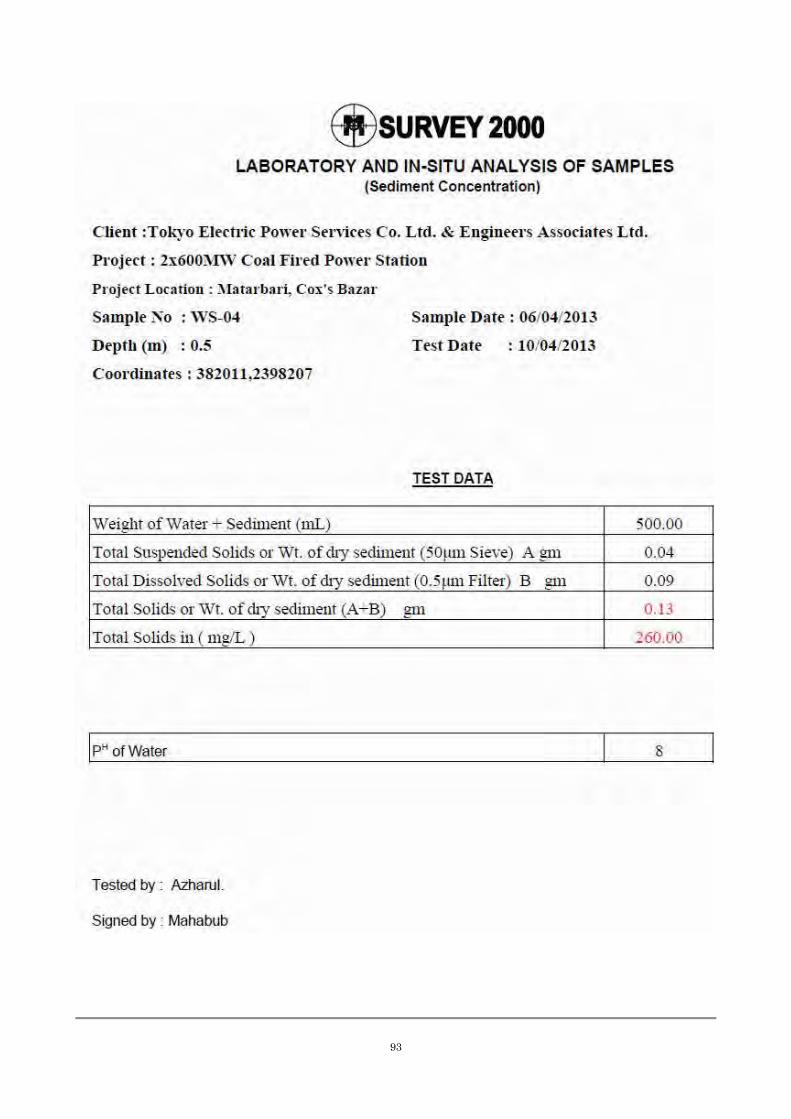

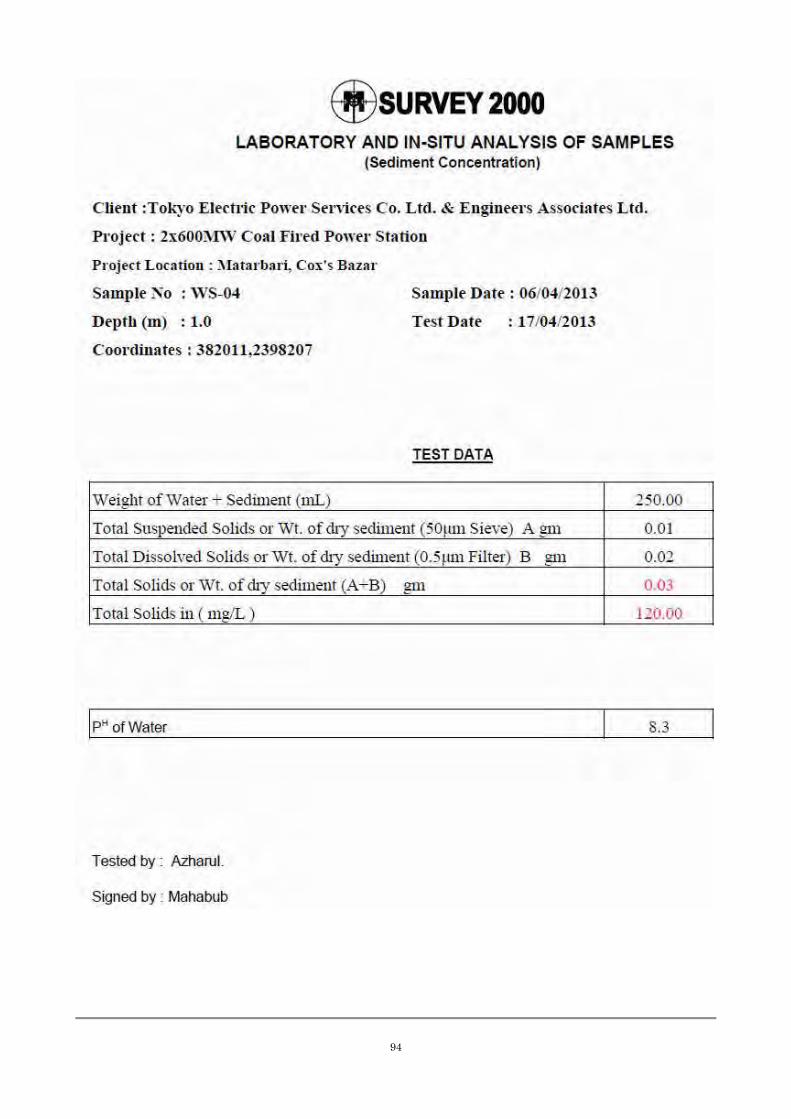

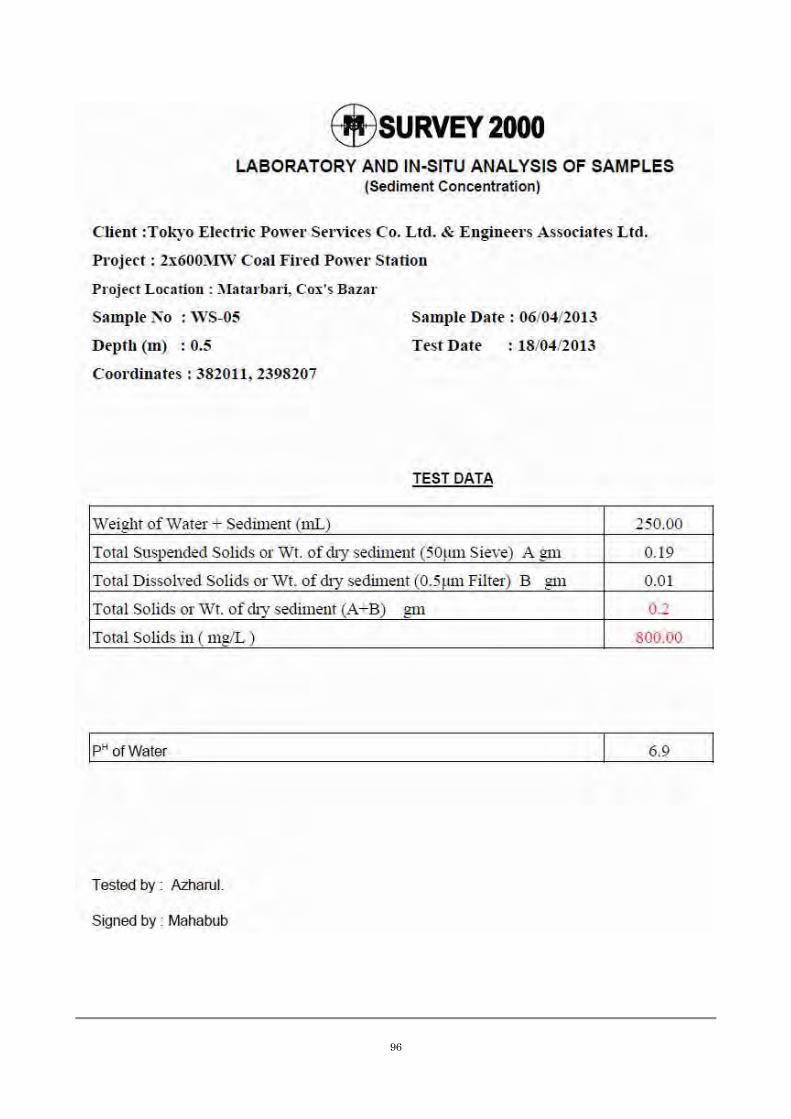

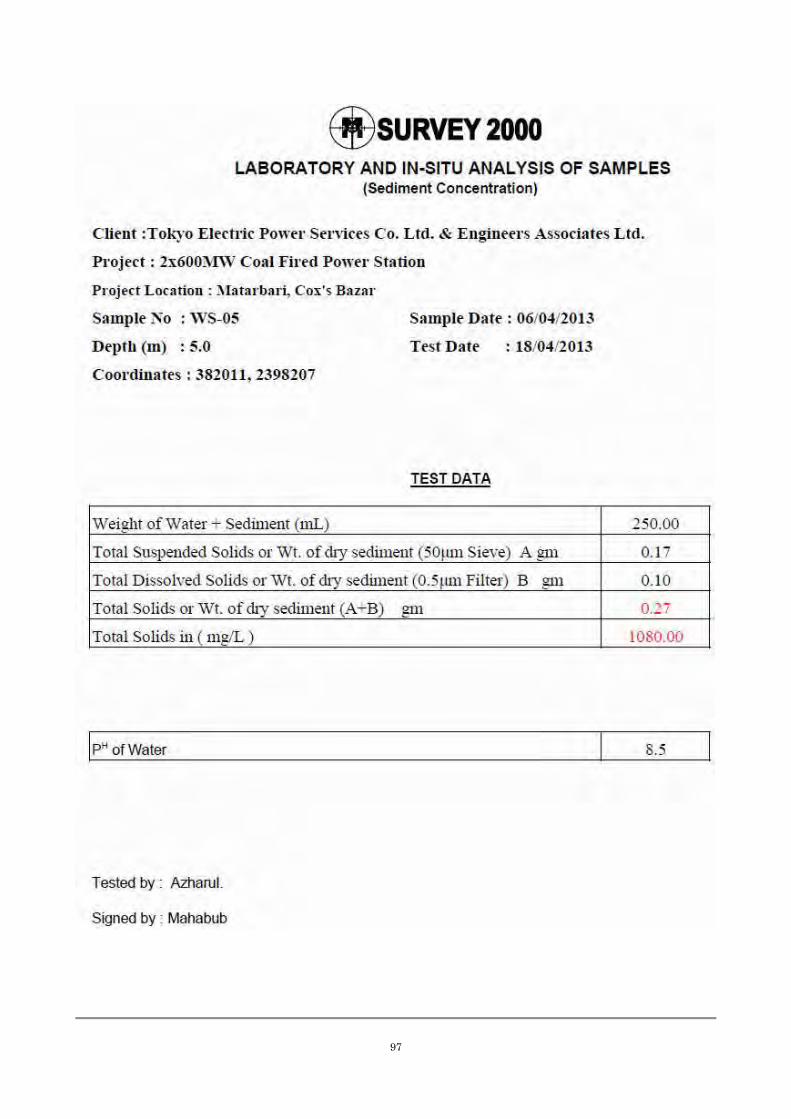

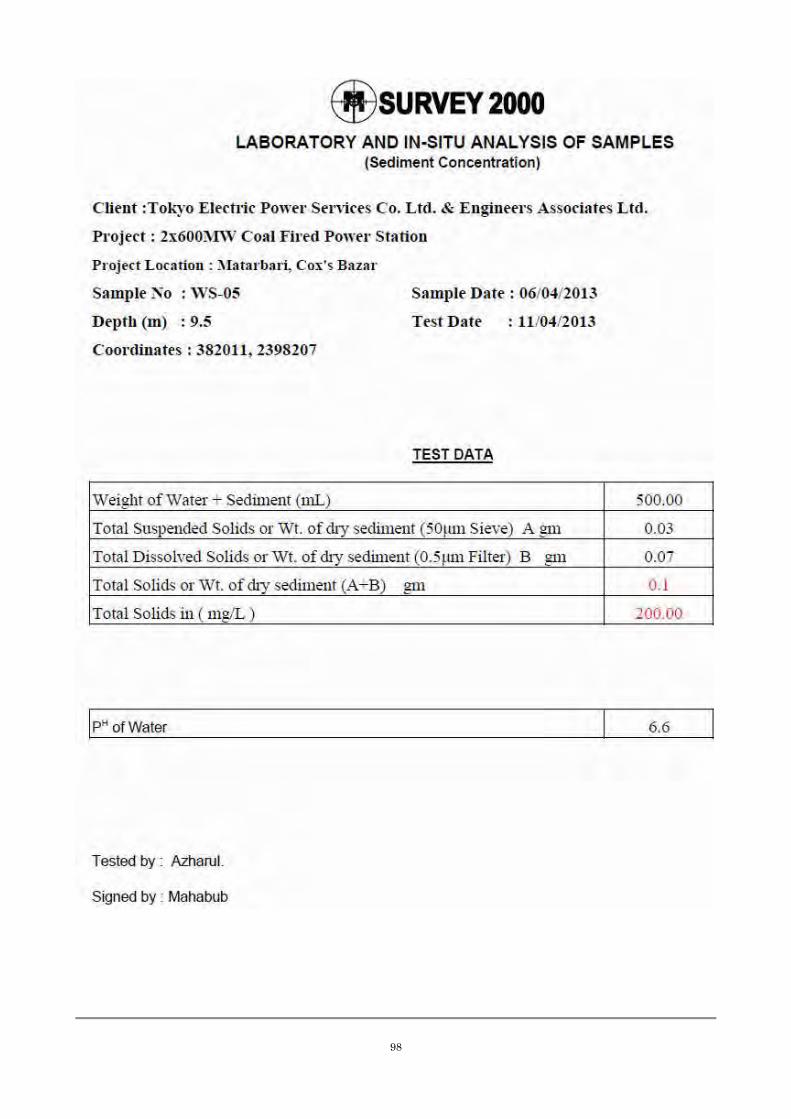

Water Quality

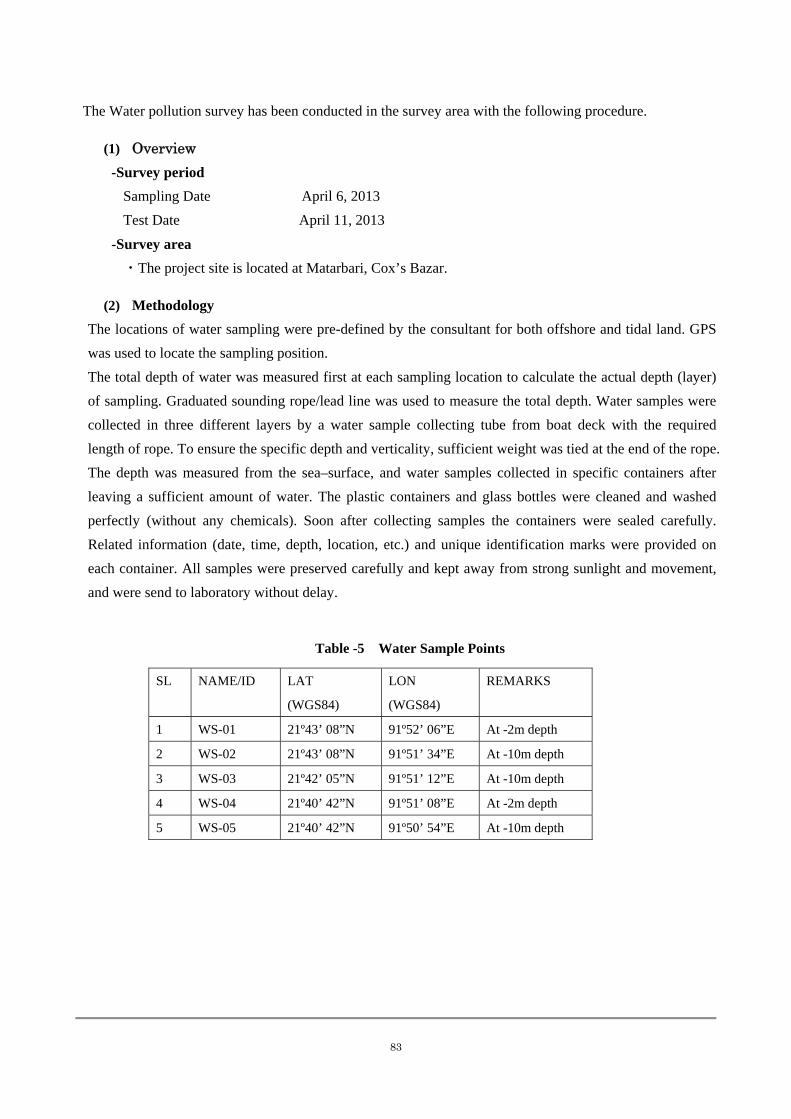

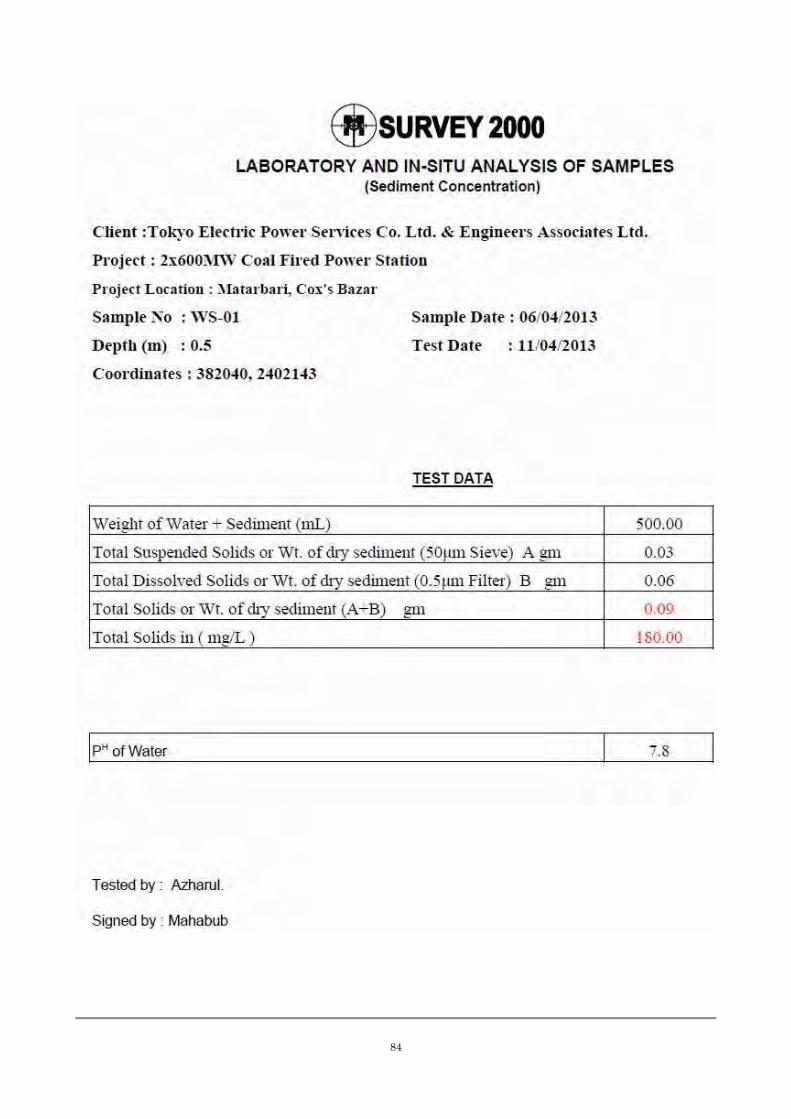

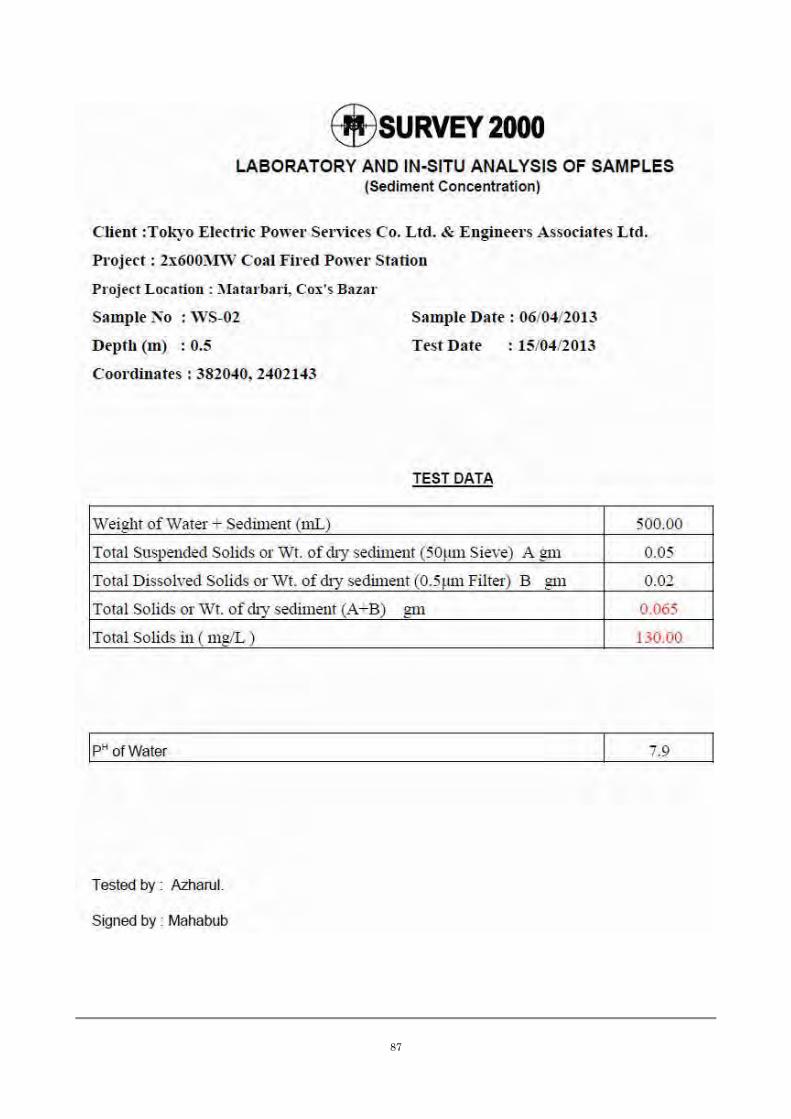

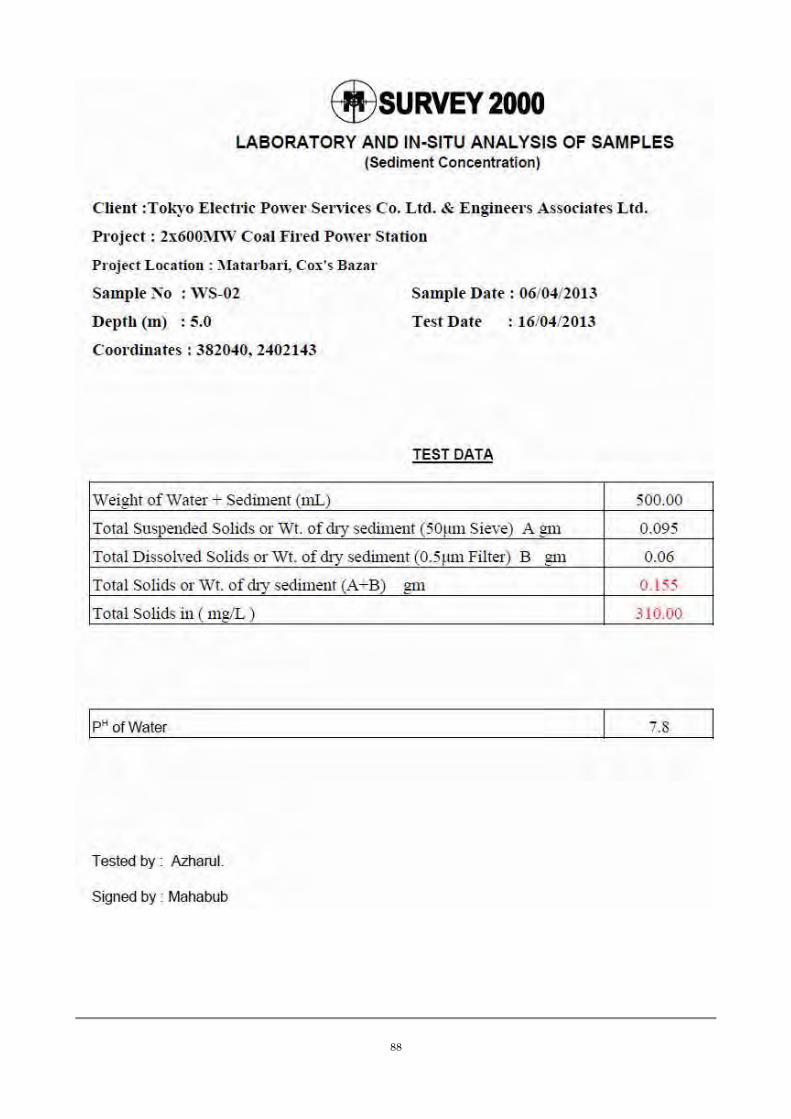

The Water pollution survey has been conducted in the survey area with the following procedure.

(1) Overview

-Survey period

Sampling Date October 12, 2012

Test Date November 3-17, 2012

-Survey area

・The project site is located at Matarbari, Cox’s Bazar.

(2) Methodology

The locations of water sampling were pre-defined by the consultant for both offshore and tidal land. GPS

was used to locate the sampling position.

The total depth of water was measured first at each sampling location to calculate the actual depth (layer)

of sampling. Graduated sounding rope/lead line was used to measure the total depth. Water samples were

collected in three different layers by a water sample collecting tube from boat deck with the required

length of rope. To ensure the specific depth and verticality, sufficient weight was tied at the end of the rope.

The depth was measured from the sea–surface, and water samples collected in specific containers after

leaving a sufficient amount of water. The plastic containers and glass bottles were cleaned and washed

perfectly (without any chemicals). Soon after collecting samples the containers were sealed carefully.

Related information (date, time, depth, location, etc.) and unique identification marks were provided on

each container. All samples were preserved carefully and kept away from strong sunlight and movement,

and were send to laboratory without delay.

Table -4 Water Sample Points

SL NAME/ID LAT

(WGS84)

LON

(WGS84)

REMARKS

1 WS-01 21º43’ 08”N 91º52’ 06”E At -2m depth

2 WS-02 21º43’ 08”N 91º51’ 34”E At -10m depth

3 WS-03 21º42’ 05”N 91º51’ 12”E At -10m depth

4 WS-04 21º40’ 42”N 91º51’ 08”E At -2m depth

5 WS-05 21º40’ 42”N 91º50’ 54”E At -10m depth

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

The Water pollution survey has been conducted in the survey area with the following procedure.

(1) Overview

-Survey period

Sampling Date April 6, 2013

Test Date April 11, 2013

-Survey area

・The project site is located at Matarbari, Cox’s Bazar.

(2) Methodology

The locations of water sampling were pre-defined by the consultant for both offshore and tidal land. GPS

was used to locate the sampling position.

The total depth of water was measured first at each sampling location to calculate the actual depth (layer)

of sampling. Graduated sounding rope/lead line was used to measure the total depth. Water samples were

collected in three different layers by a water sample collecting tube from boat deck with the required

length of rope. To ensure the specific depth and verticality, sufficient weight was tied at the end of the rope.

The depth was measured from the sea–surface, and water samples collected in specific containers after

leaving a sufficient amount of water. The plastic containers and glass bottles were cleaned and washed

perfectly (without any chemicals). Soon after collecting samples the containers were sealed carefully.

Related information (date, time, depth, location, etc.) and unique identification marks were provided on

each container. All samples were preserved carefully and kept away from strong sunlight and movement,

and were send to laboratory without delay.

Table -5 Water Sample Points

SL NAME/ID LAT

(WGS84)

LON

(WGS84)

REMARKS

1 WS-01 21º43’ 08”N 91º52’ 06”E At -2m depth

2 WS-02 21º43’ 08”N 91º51’ 34”E At -10m depth

3 WS-03 21º42’ 05”N 91º51’ 12”E At -10m depth

4 WS-04 21º40’ 42”N 91º51’ 08”E At -2m depth

5 WS-05 21º40’ 42”N 91º50’ 54”E At -10m depth

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

100

101

Water Depth

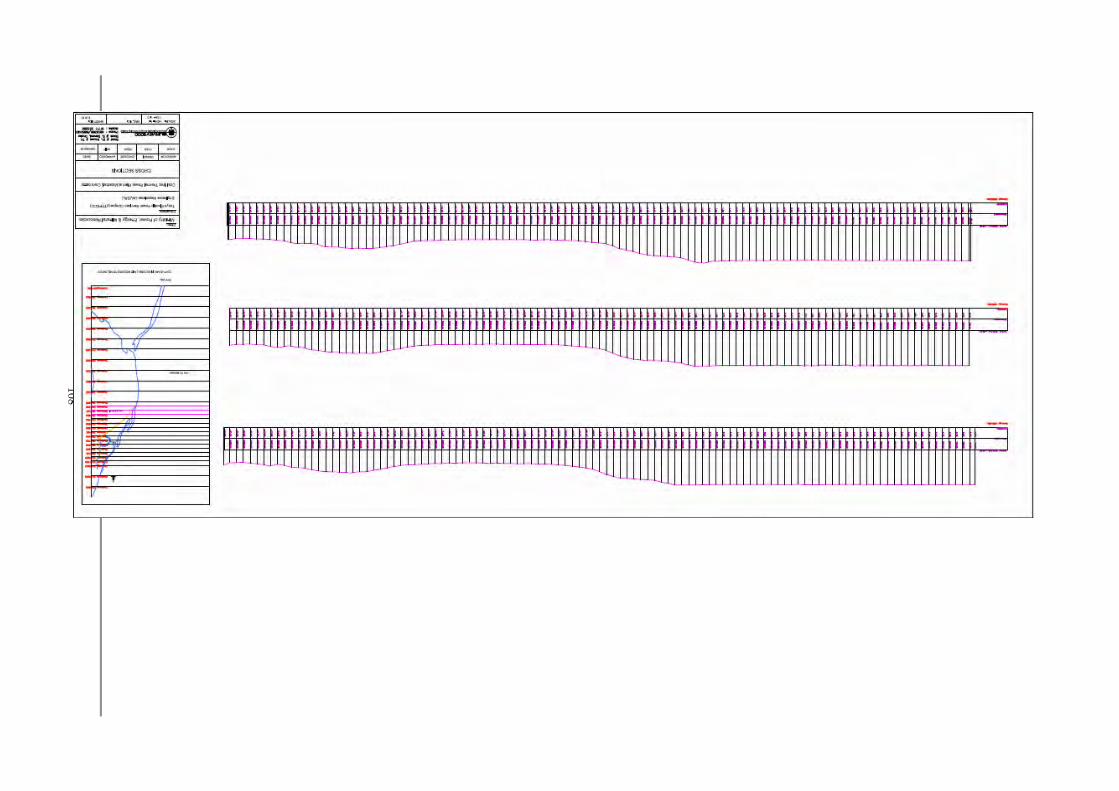

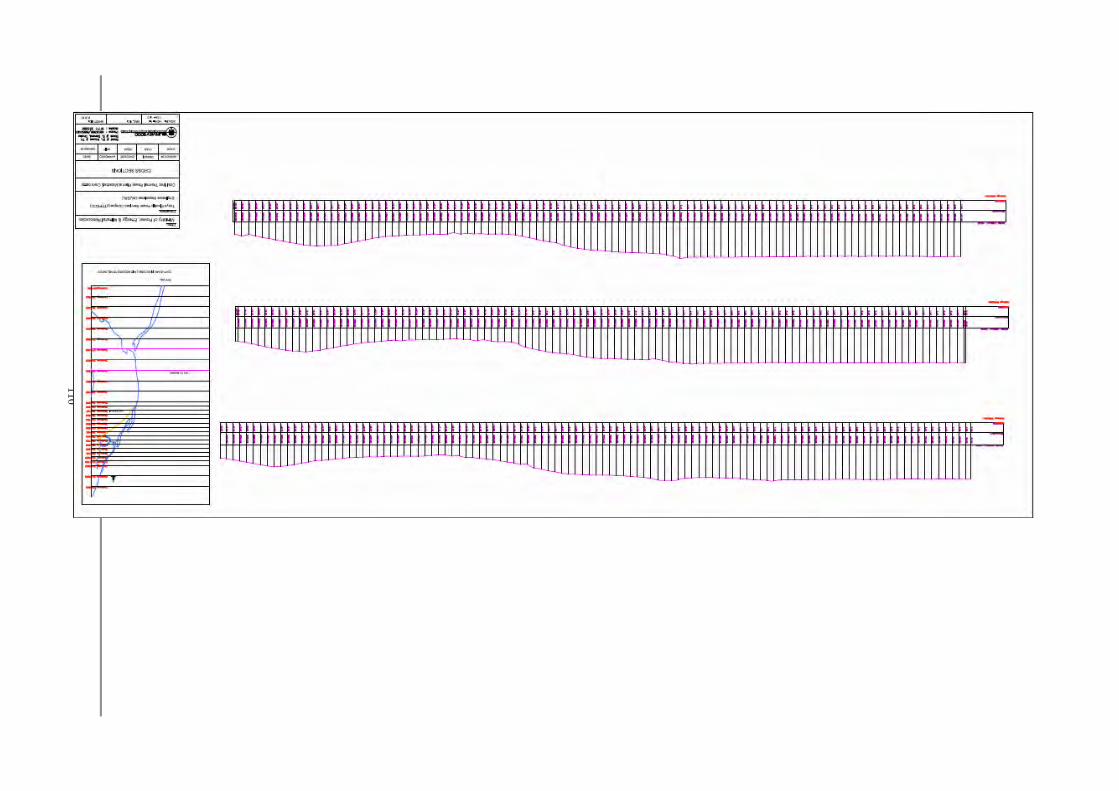

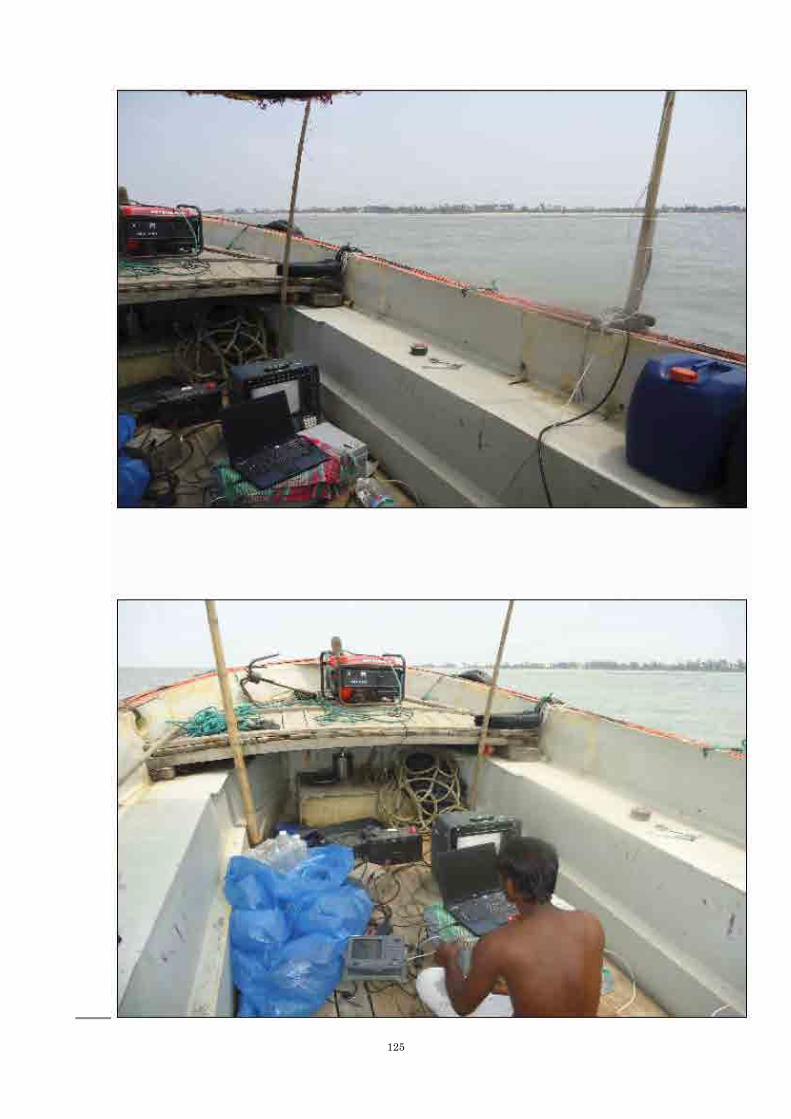

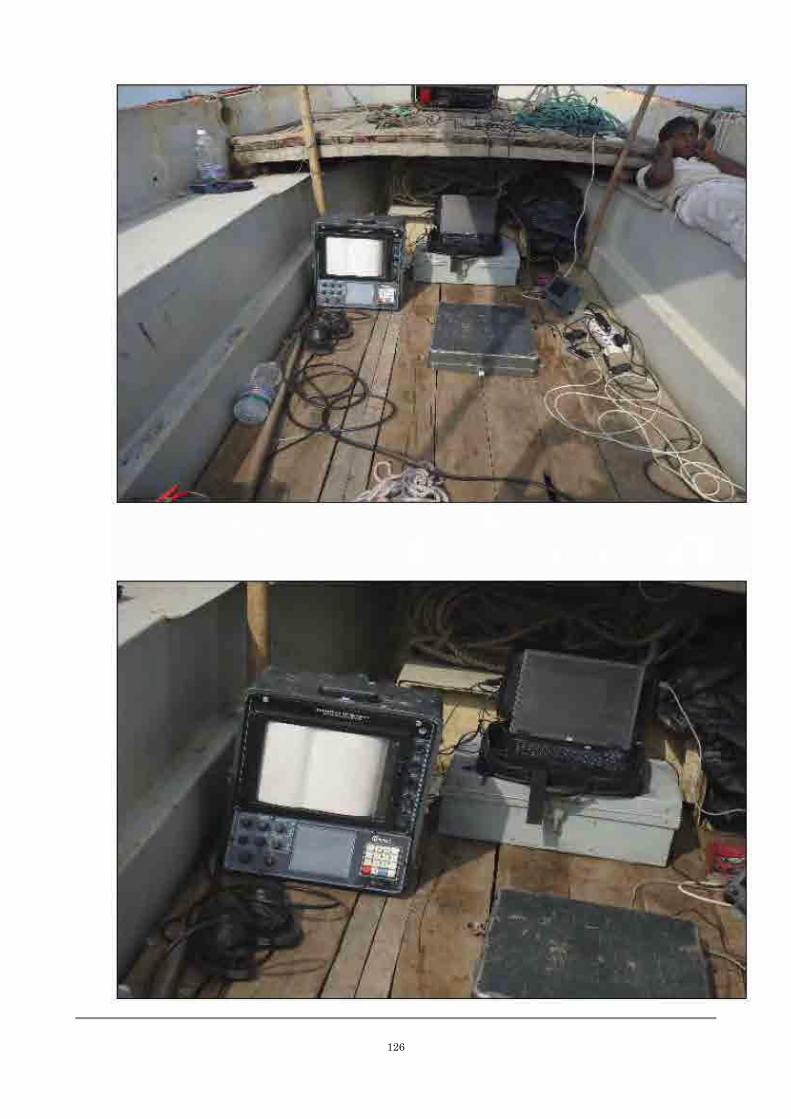

The bathymetric survey has been conducted in the survey area with the following procedure.

(1) Overview

-Survey period

From October 8, 2012, to October 24, 2012.

-Survey area

The project site is located at Matarbari, Cox’s Bazar.

(2) Methodology

The survey was conducted using fourteen hydrographic survey lines at 200m intervals with 50m

interval sounding, and 16 hydrographic survey lines at 500m intervals with 50m interval sounding. The

length of the survey line was 5km and the reference coordinates were as follows:

Latitude N21°42'12”N Longitude E91°52'31”E RTK GPS.

An echo sounder was used connected with the navigation and data acquisition PC via interface cable

and synchronized with the hydrographic software HYPAC. Before conducting the survey, a line of

survey was created as per the directions. A navigation module guided the surveyor for the run line of

the survey vessel and data acquisition. Using a computer screen the hydrographic surveyor could know

his position, speed and direction of the survey vessel, and the depth profile, etc. The survey vessel was

run at a maximum of 6 knots per hour for data acquisition. Calibration for the echo sounder was done

prior to the survey run everyday using a bar check plate.

Tide levels were recorded at half hourly intervals for tidal correction of bathymetric height.

102

103

104

105

106

107

108

109

110

111

112

113

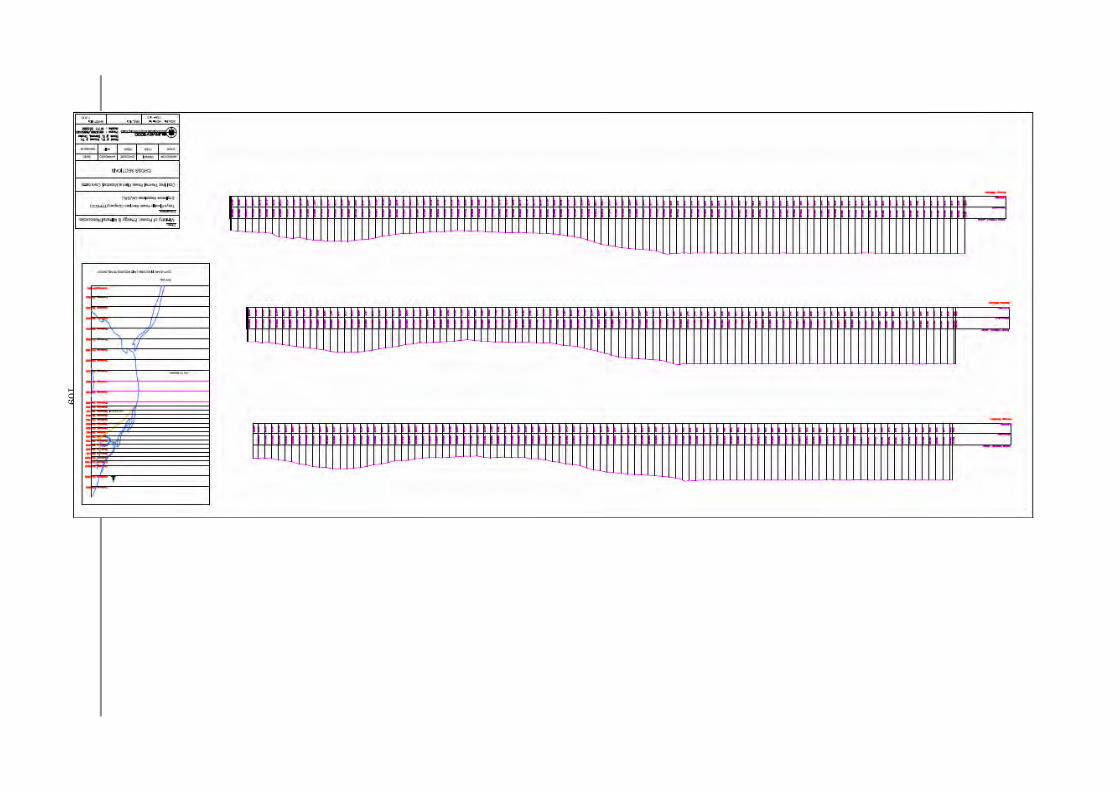

The bathymetric survey has been conducted in the survey area with the following procedure.

(1) Overview

-Survey period

From March 28, 2013, to April 11, 2013.

-Survey area

The project site is located at Matarbari, Cox’s Bazar.

(2) Methodology

The survey was conducted using fourteen hydrographic survey lines at 200m intervals with 50m

interval sounding, and 16 hydrographic survey lines at 500m intervals with 50m interval sounding. The

length of the survey line was 5km and the reference coordinates were as follows:

Latitude N21°42'12”N Longitude E91°52'31”E RTK GPS.

An echo sounder was used connected with the navigation and data acquisition PC via interface cable

and synchronized with the hydrographic software HYPAC. Before conducting the survey, a line of

survey was created as per the directions. A navigation module guided the surveyor for the run line of

the survey vessel and data acquisition. Using a computer screen the hydrographic surveyor could know

his position, speed and direction of the survey vessel, and the depth profile, etc. The survey vessel was

run at a maximum of 6 knots per hour for data acquisition. Calibration for the echo sounder was done

prior to the survey run everyday using a bar check plate.

Tide levels were recorded at half hourly intervals for tidal correction of bathymetric height.

114

115

116

117

118

119

120

121

122

123 T

idal O

bservation

124

125

126

127

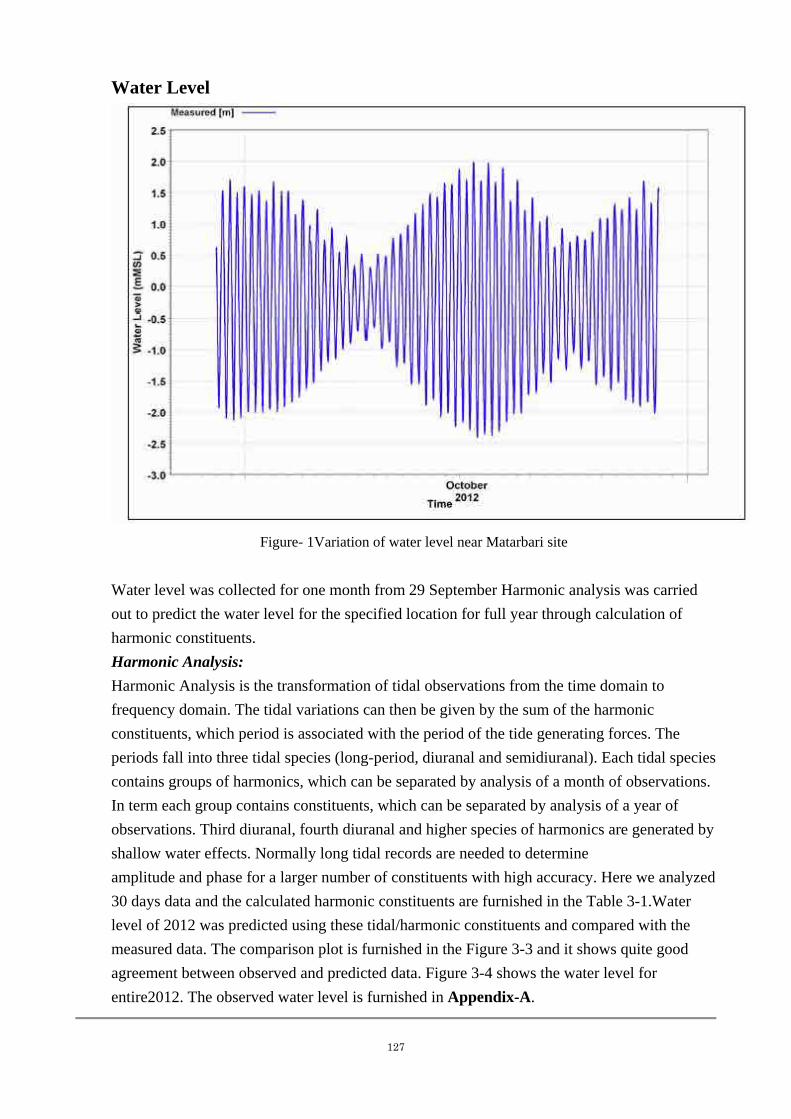

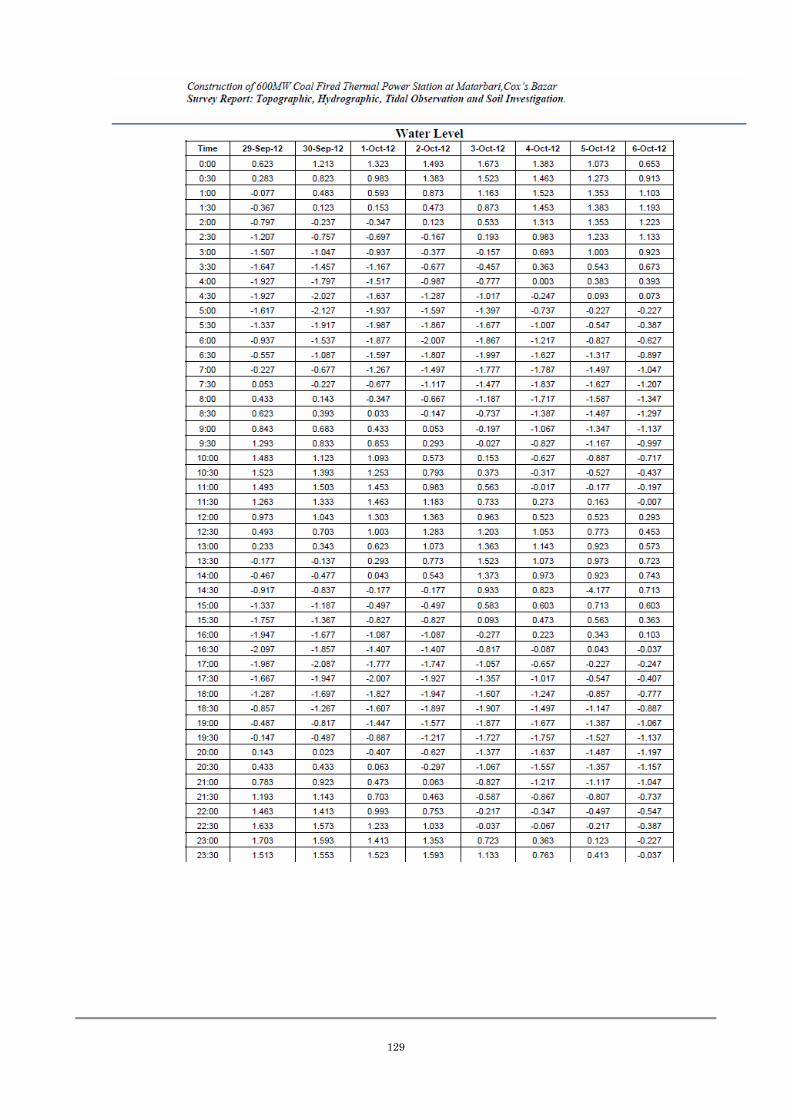

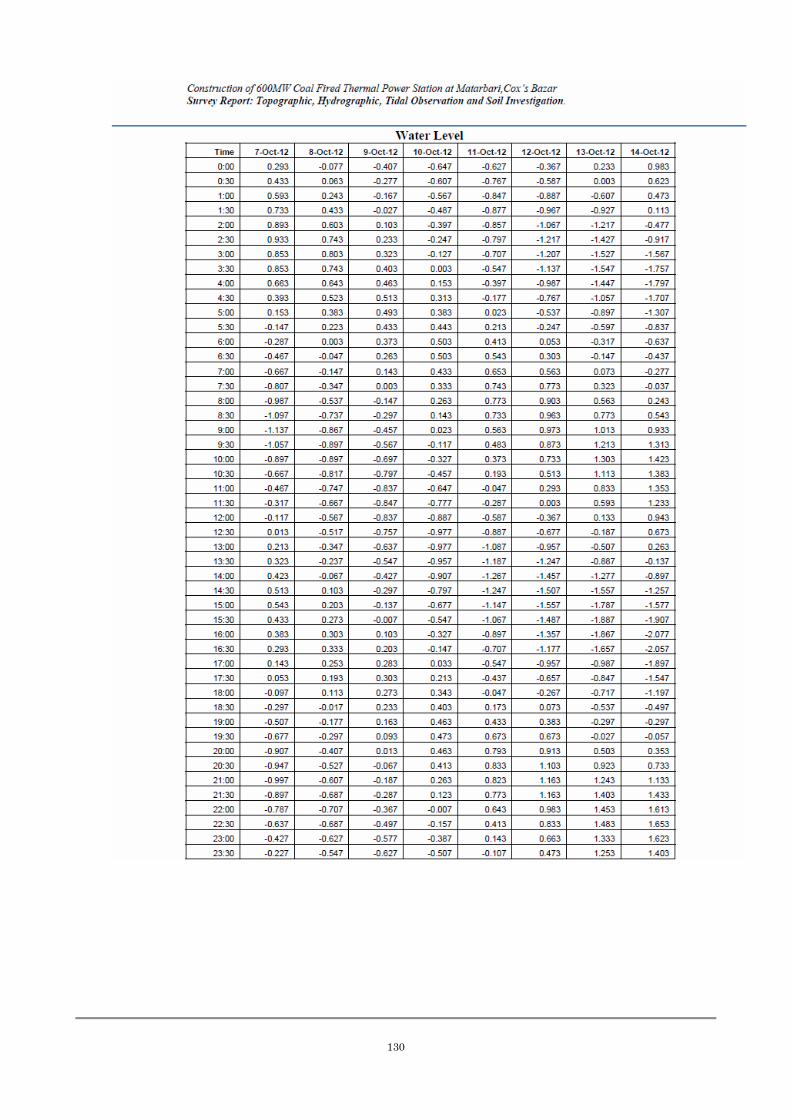

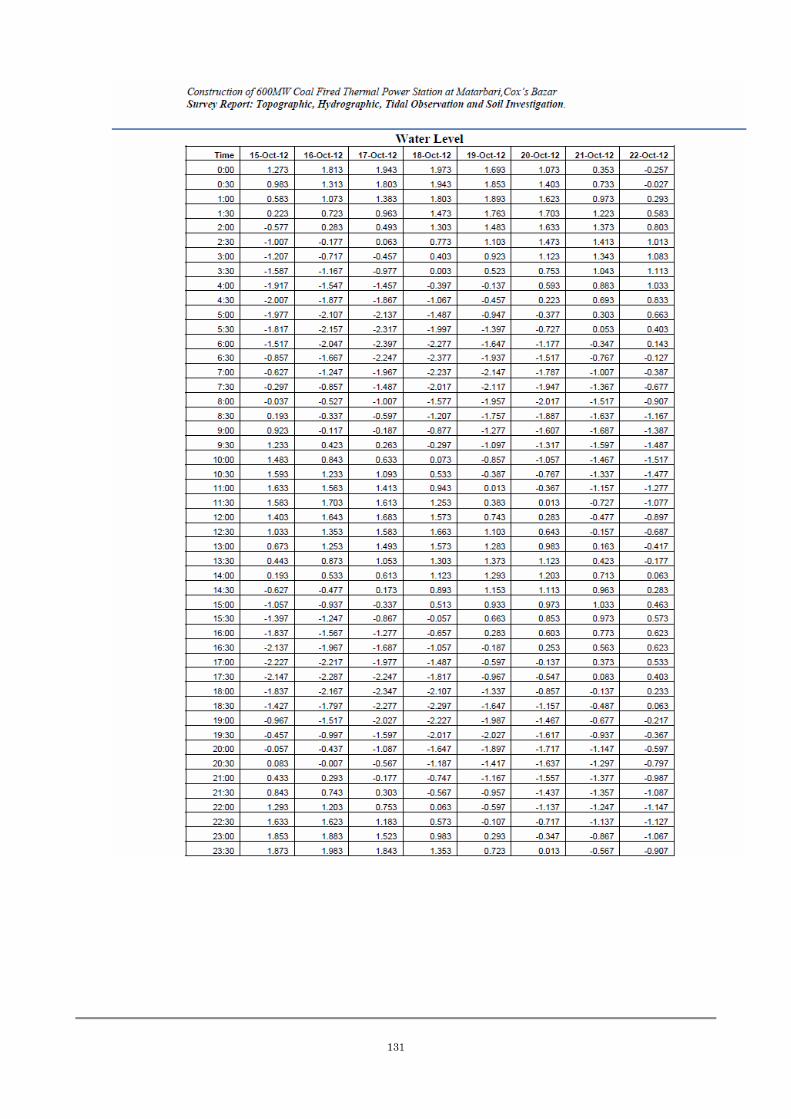

Water Level

Figure- 1Variation of water level near Matarbari site

Water level was collected for one month from 29 September Harmonic analysis was carried

out to predict the water level for the specified location for full year through calculation of

harmonic constituents.

Harmonic Analysis:

Harmonic Analysis is the transformation of tidal observations from the time domain to

frequency domain. The tidal variations can then be given by the sum of the harmonic

constituents, which period is associated with the period of the tide generating forces. The

periods fall into three tidal species (long-period, diuranal and semidiuranal). Each tidal species

contains groups of harmonics, which can be separated by analysis of a month of observations.

In term each group contains constituents, which can be separated by analysis of a year of

observations. Third diuranal, fourth diuranal and higher species of harmonics are generated by

shallow water effects. Normally long tidal records are needed to determine

amplitude and phase for a larger number of constituents with high accuracy. Here we analyzed

30 days data and the calculated harmonic constituents are furnished in the Table 3-1.Water

level of 2012 was predicted using these tidal/harmonic constituents and compared with the

measured data. The comparison plot is furnished in the Figure 3-3 and it shows quite good

agreement between observed and predicted data. Figure 3-4 shows the water level for

entire2012. The observed water level is furnished in Appendix-A.

128

Table-3 List and value of constituent

129

130

131

132

133

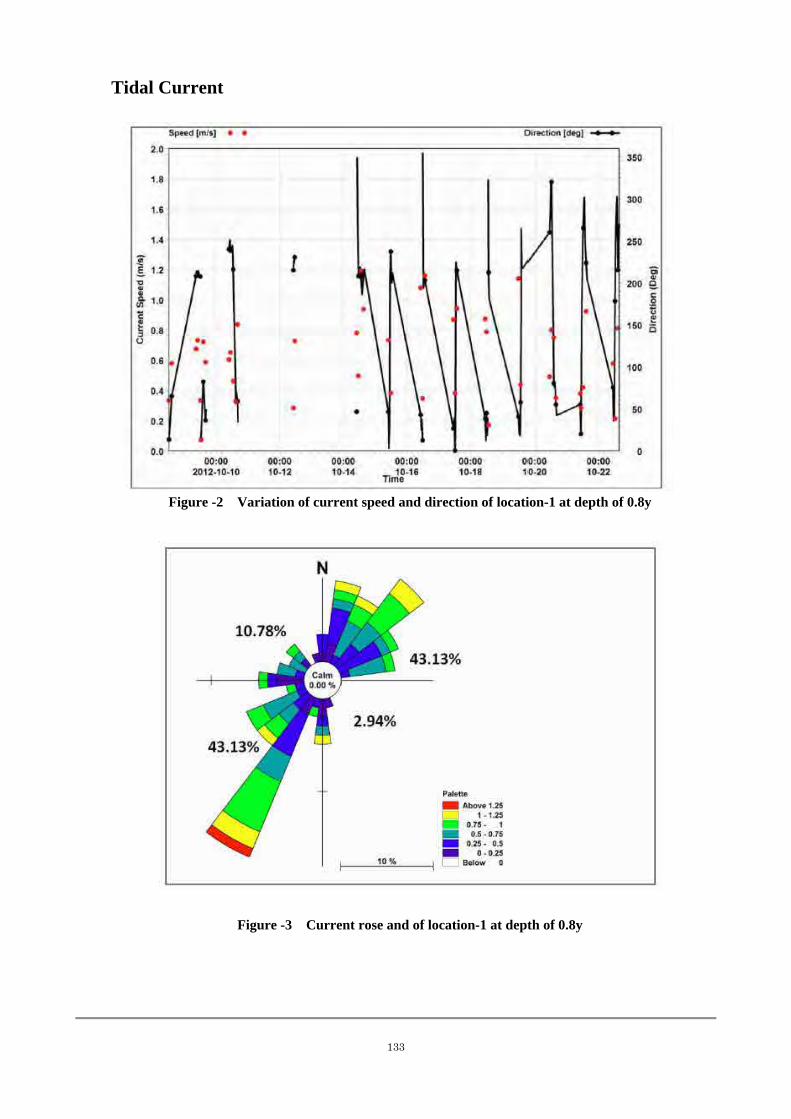

Tidal Current

Figure -2 Variation of current speed and direction of location-1 at depth of 0.8y

Figure -3 Current rose and of location-1 at depth of 0.8y

134

Figure -1 Variation of current speed and direction at location-1 at depth of 0.2y

Figure -5 Current rose and of location-1 at depth of 0.2y

135

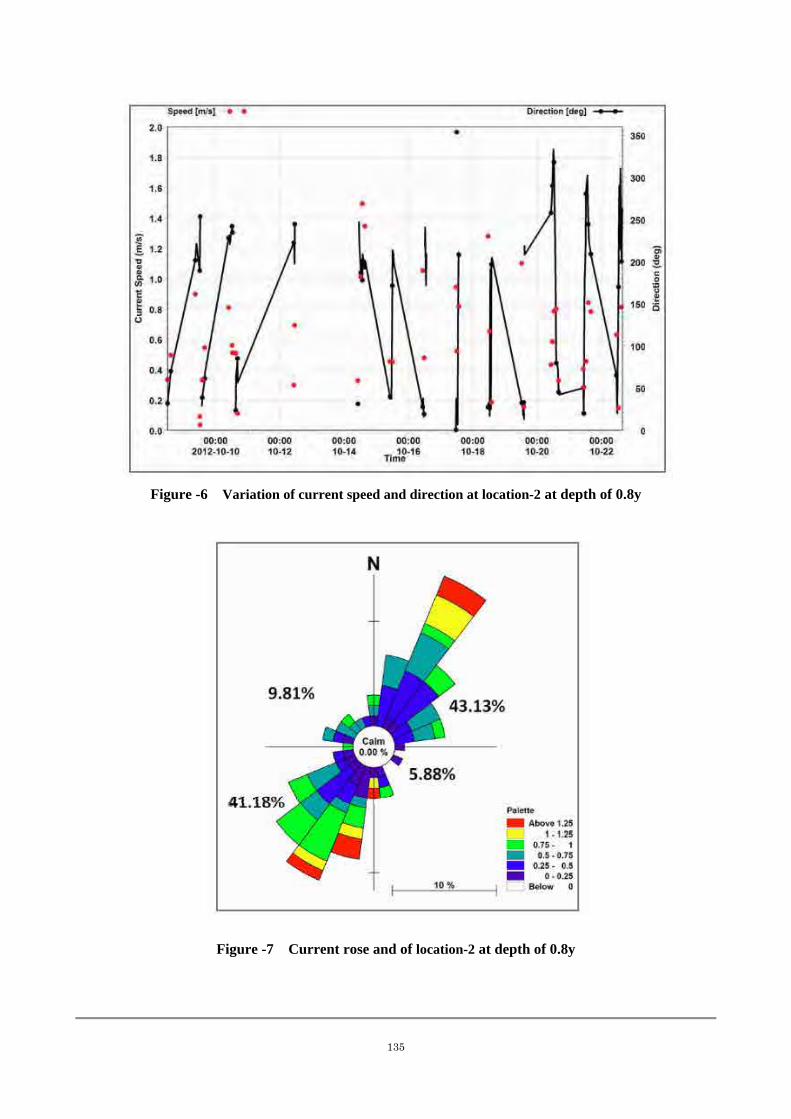

Figure -6 Variation of current speed and direction at location-2 at depth of 0.8y

Figure -7 Current rose and of location-2 at depth of 0.8y

136

Figure -8 Variation of current speed and direction at location-2 at depth of 0.2y

Figure -9 Current rose and of location-2 at depth of 0.2y

137

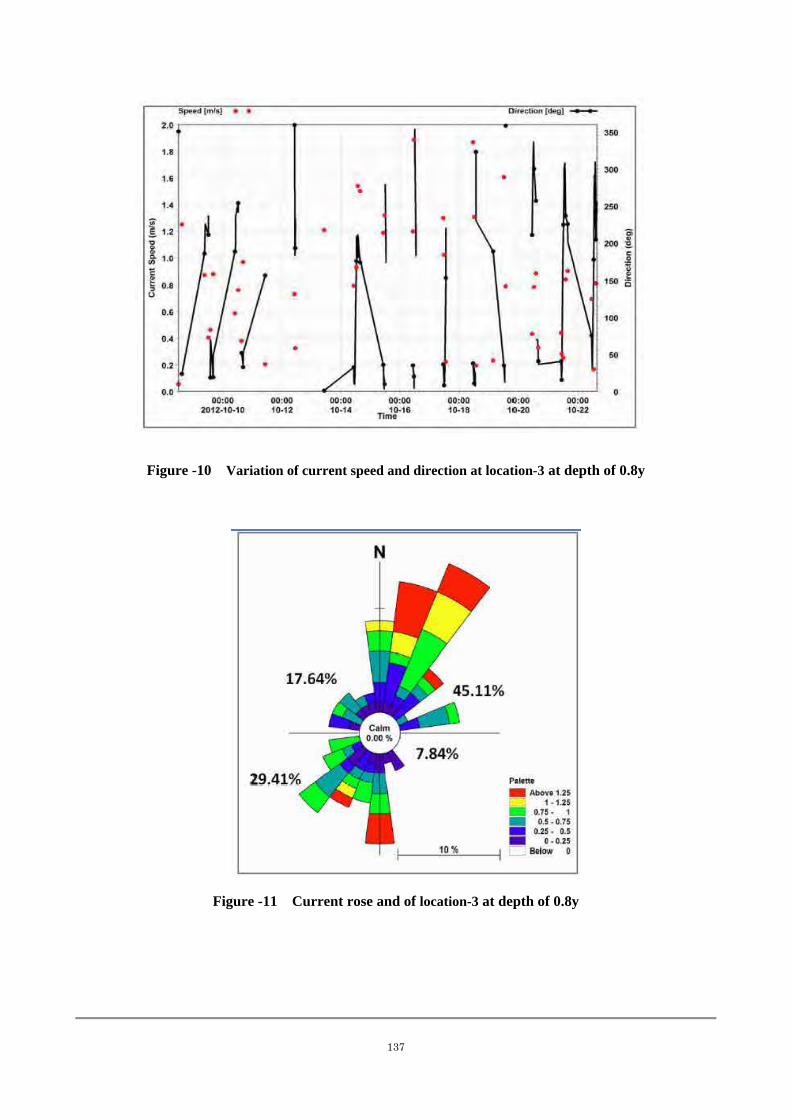

Figure -10 Variation of current speed and direction at location-3 at depth of 0.8y

Figure -11 Current rose and of location-3 at depth of 0.8y

138

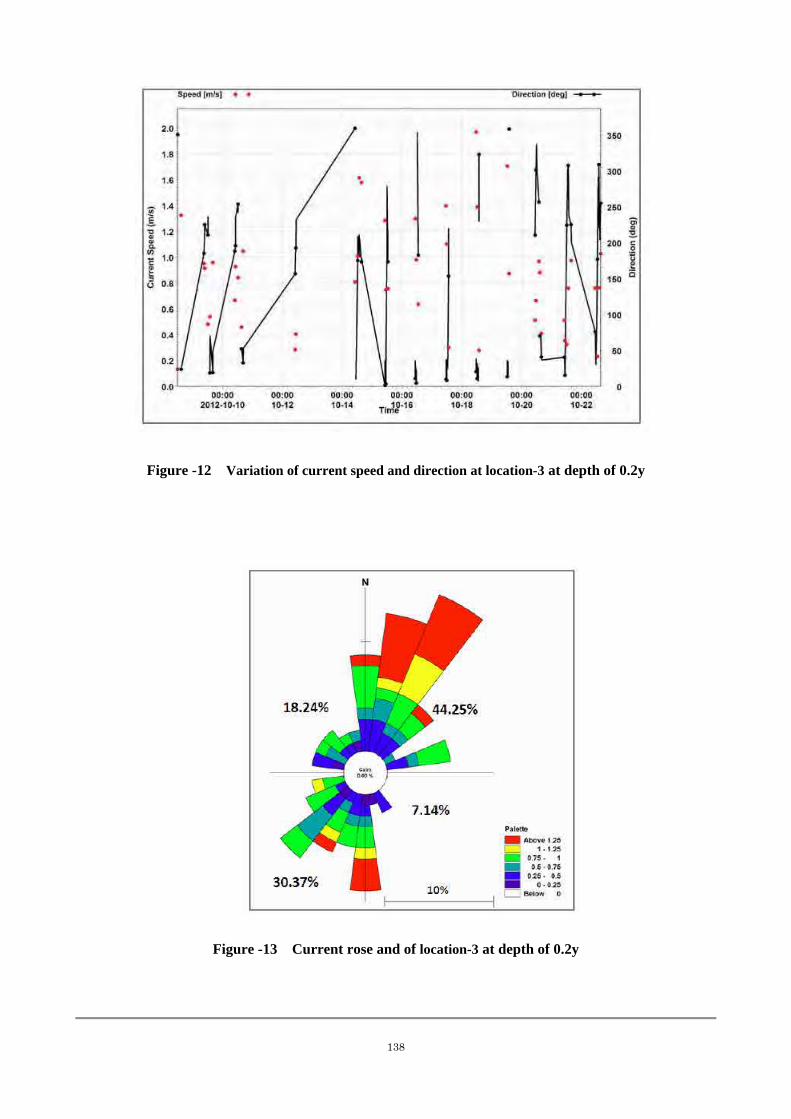

Figure -12 Variation of current speed and direction at location-3 at depth of 0.2y

Figure -13 Current rose and of location-3 at depth of 0.2y

139

Figure -14 Variation of current speed and direction at location-4 at depth of 0.8y

Figure -15 Current rose and of location-4 at depth of 0.8y

140

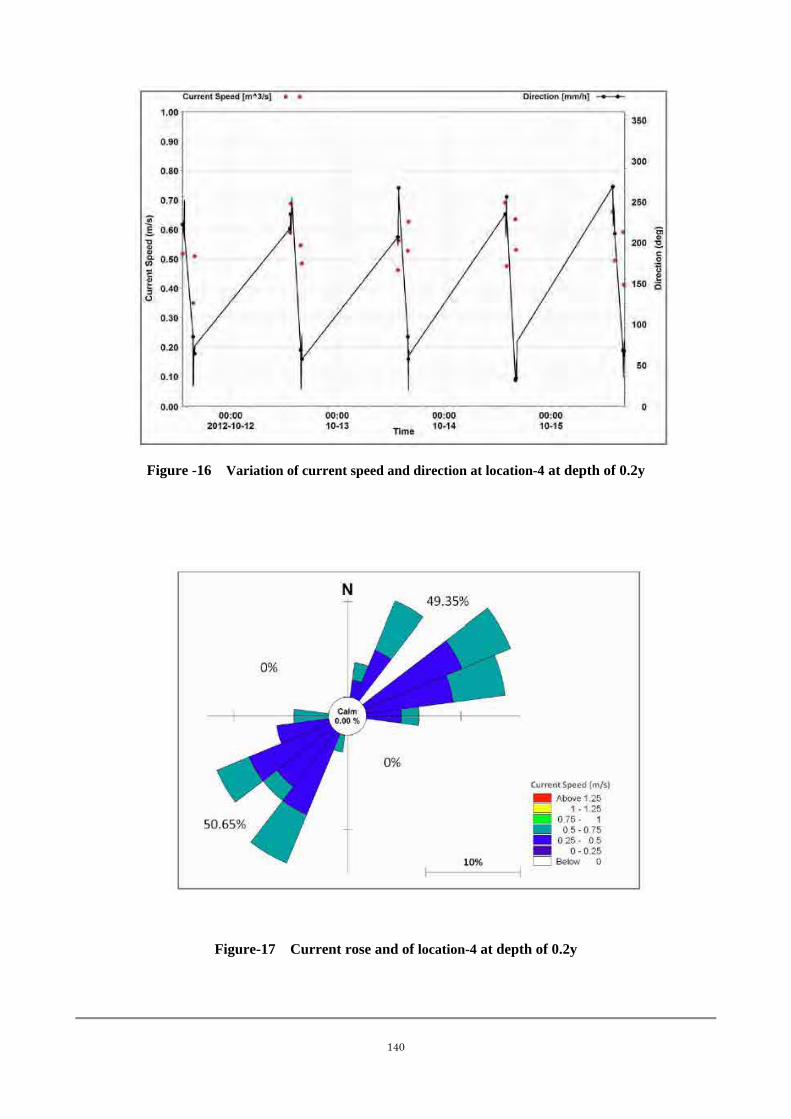

Figure -16 Variation of current speed and direction at location-4 at depth of 0.2y

Figure-17 Current rose and of location-4 at depth of 0.2y

141

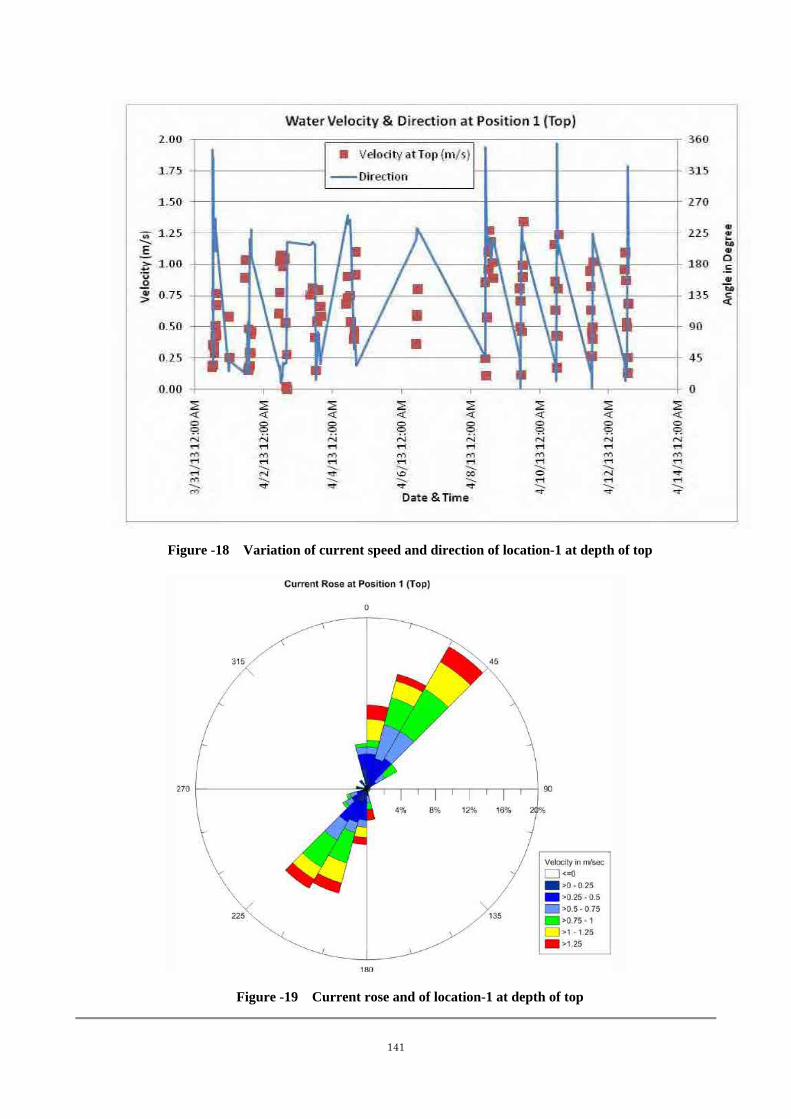

Figure -18 Variation of current speed and direction of location-1 at depth of top

Figure -19 Current rose and of location-1 at depth of top

142

Figure -20 Variation of current speed and direction at location-1 at depth of bottom

Figure -21 Current rose and of location-1 at depth of bottom

143

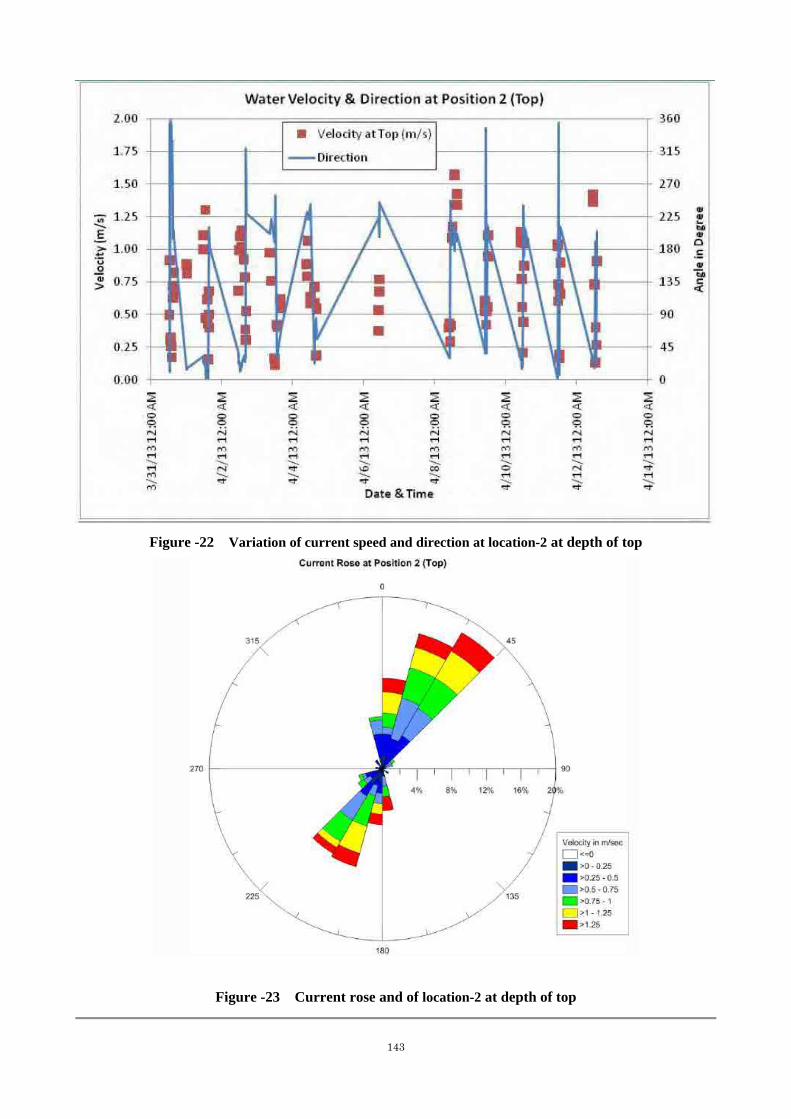

Figure -22 Variation of current speed and direction at location-2 at depth of top

Figure -23 Current rose and of location-2 at depth of top

144

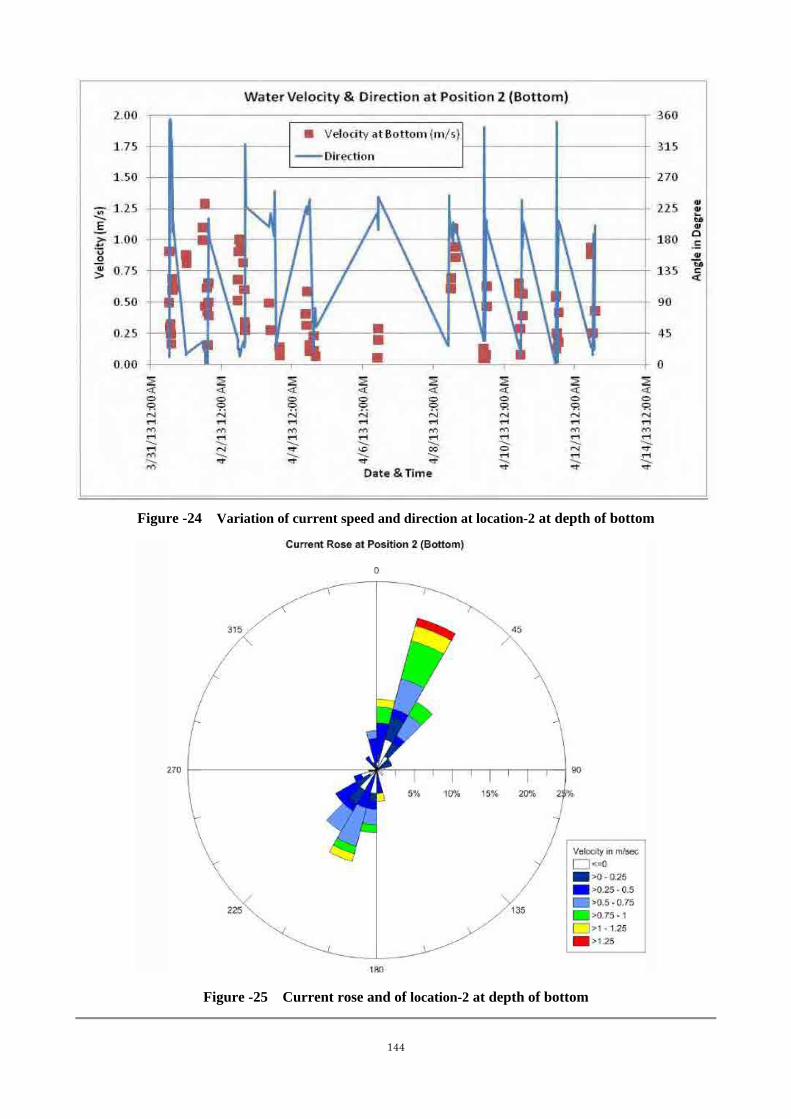

Figure -24 Variation of current speed and direction at location-2 at depth of bottom

Figure -25 Current rose and of location-2 at depth of bottom

145

Figure -26 Variation of current speed and direction at location-3 at depth of top

Figure -27 Current rose and of location-3 at depth of top

146

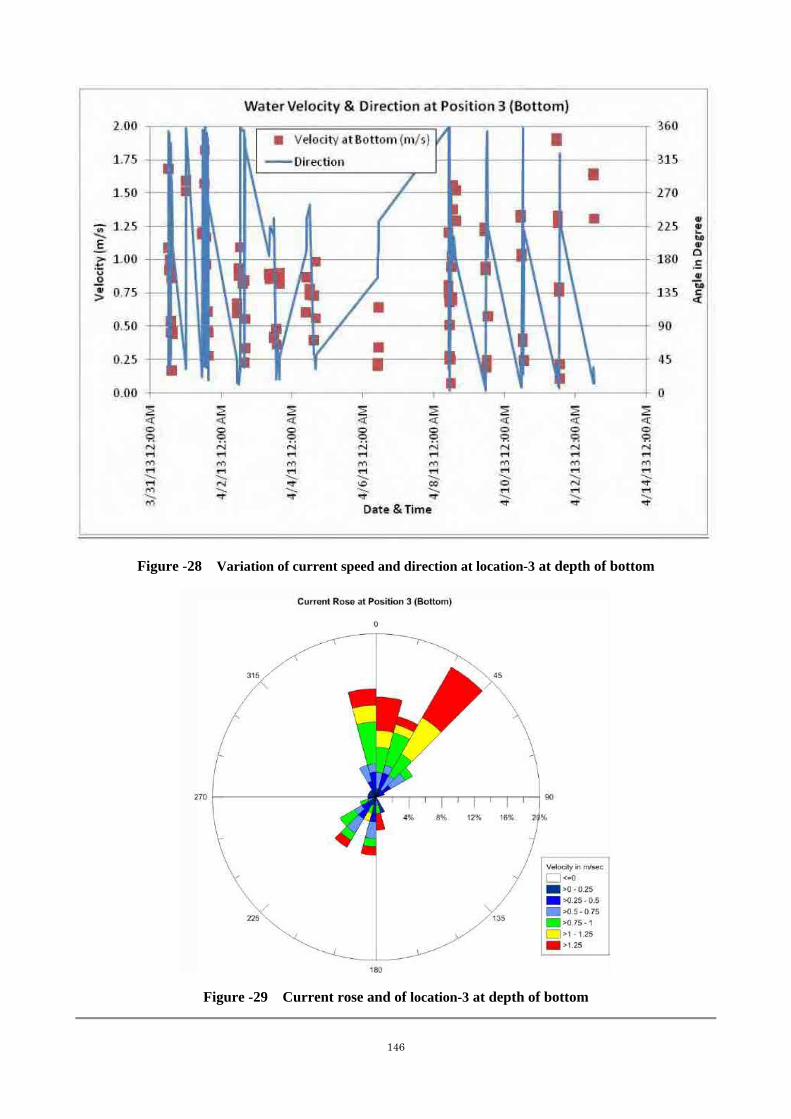

Figure -28 Variation of current speed and direction at location-3 at depth of bottom

Figure -29 Current rose and of location-3 at depth of bottom

147

Salinity and Temperature

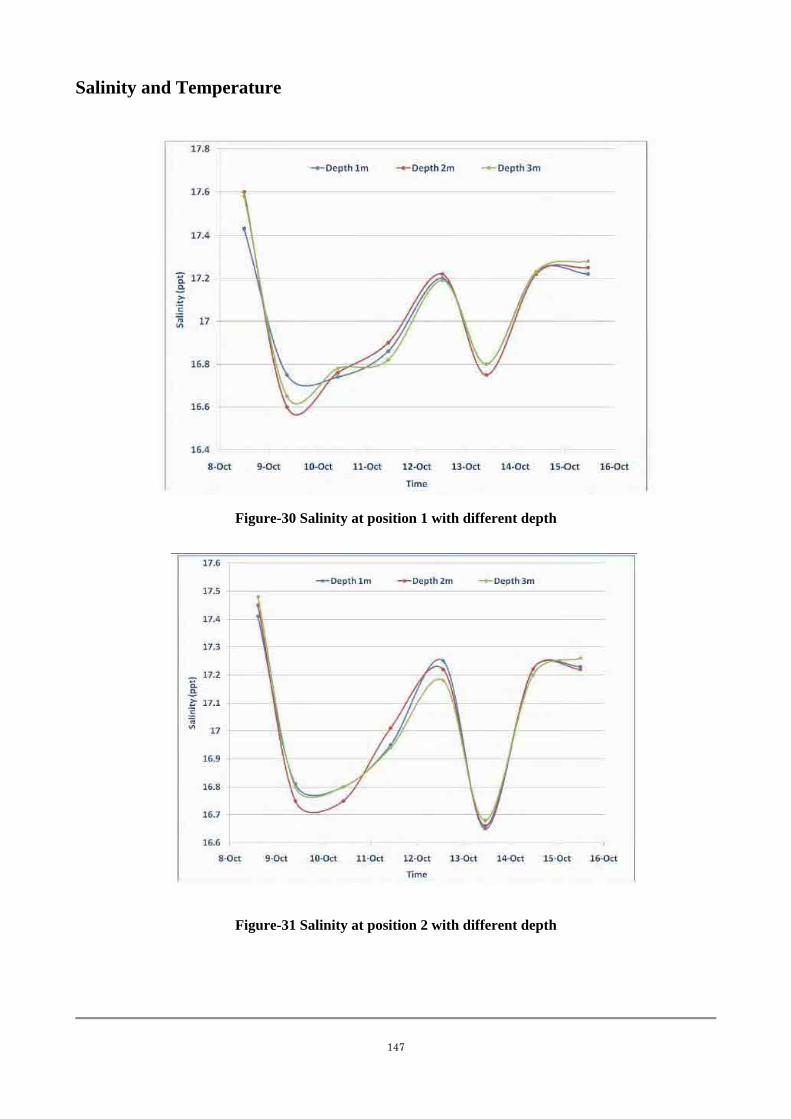

Figure-30 Salinity at position 1 with different depth

Figure-31 Salinity at position 2 with different depth

148

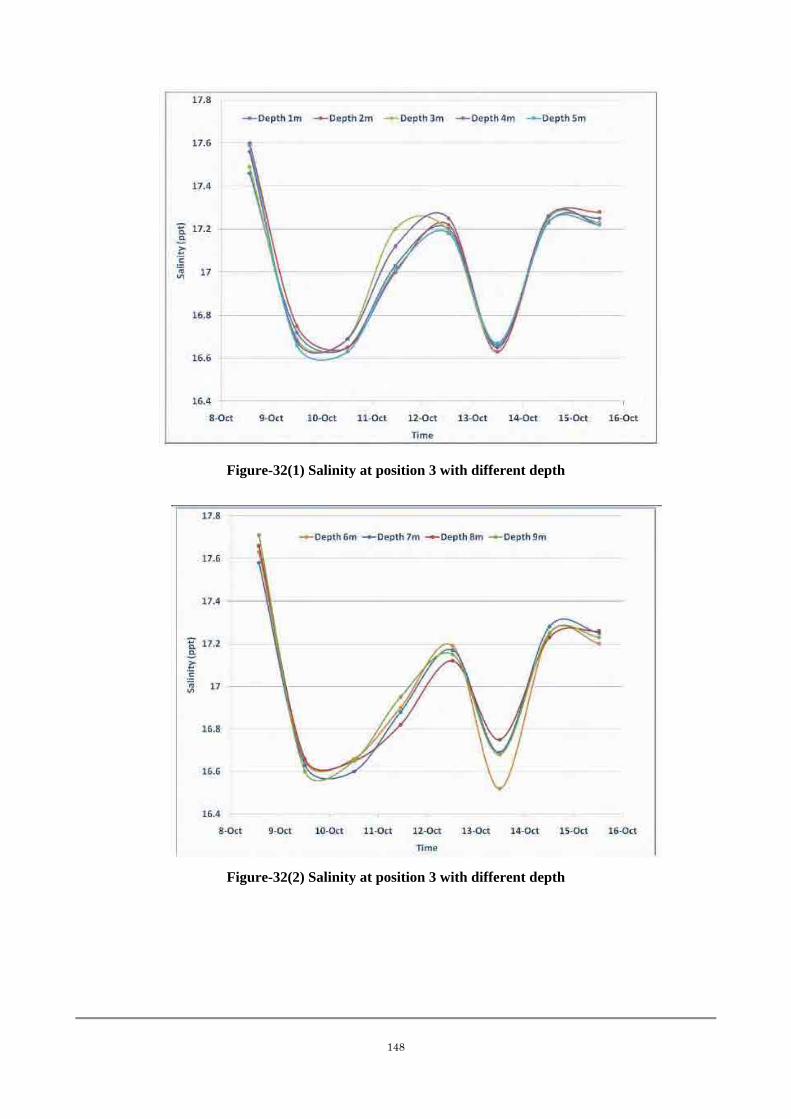

Figure-32(1) Salinity at position 3 with different depth

Figure-32(2) Salinity at position 3 with different depth

149

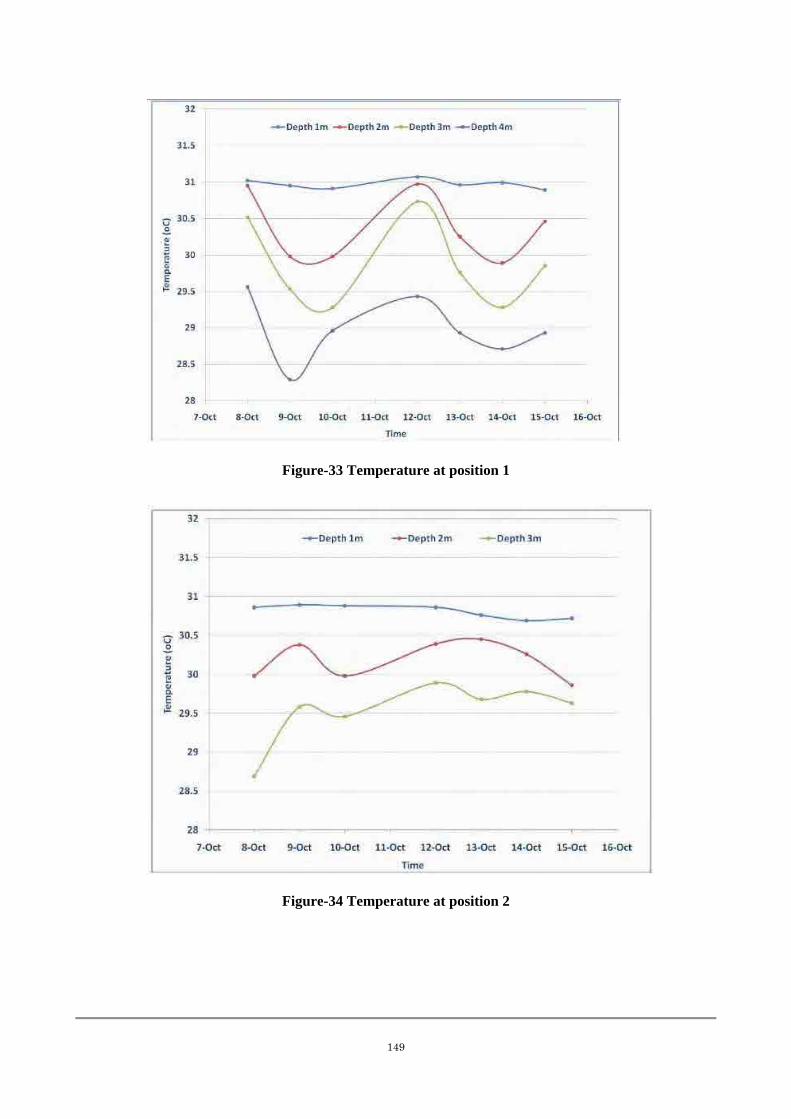

Figure-33 Temperature at position 1

Figure-34 Temperature at position 2

150

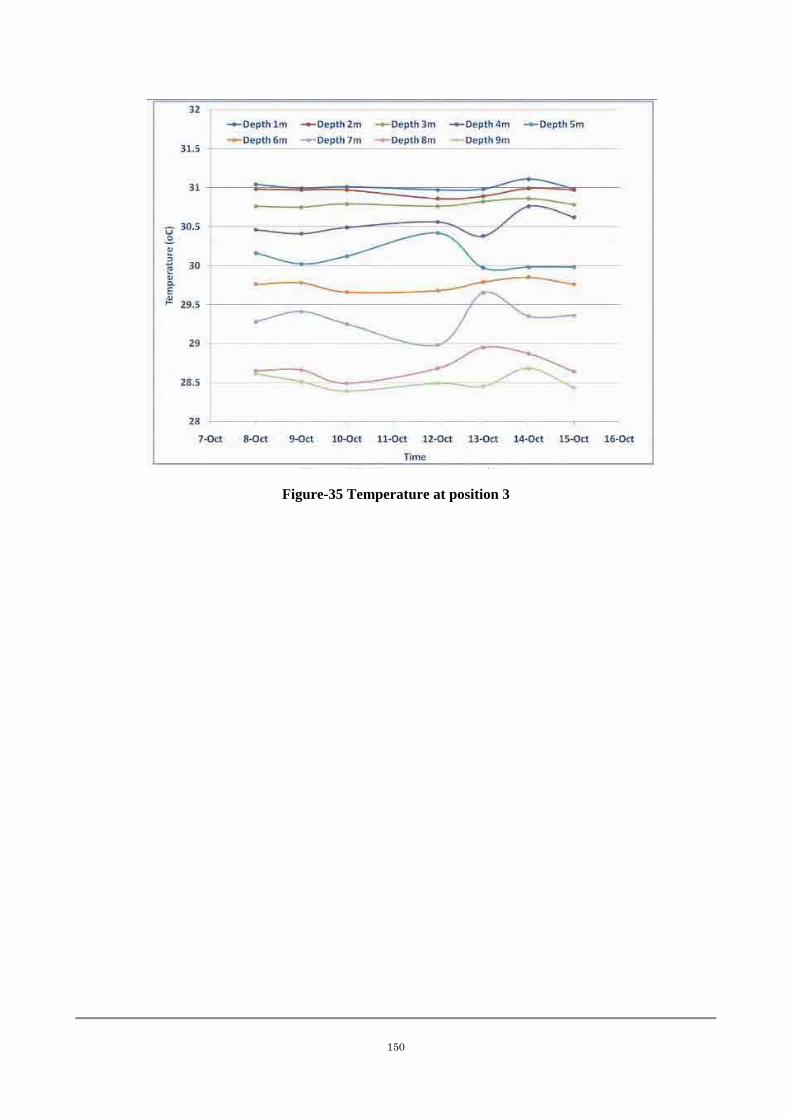

Figure-35 Temperature at position 3

151

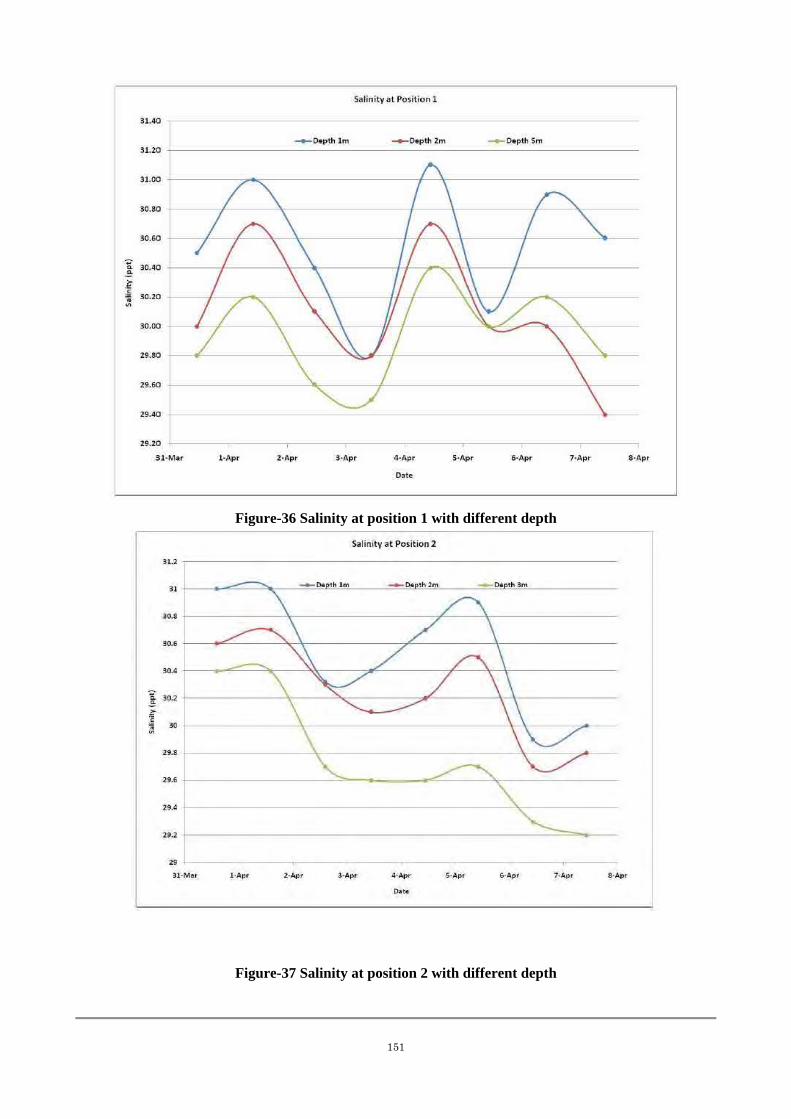

Figure-36 Salinity at position 1 with different depth

Figure-37 Salinity at position 2 with different depth

152

Figure-38 Salinity at position 3 with different depth

153

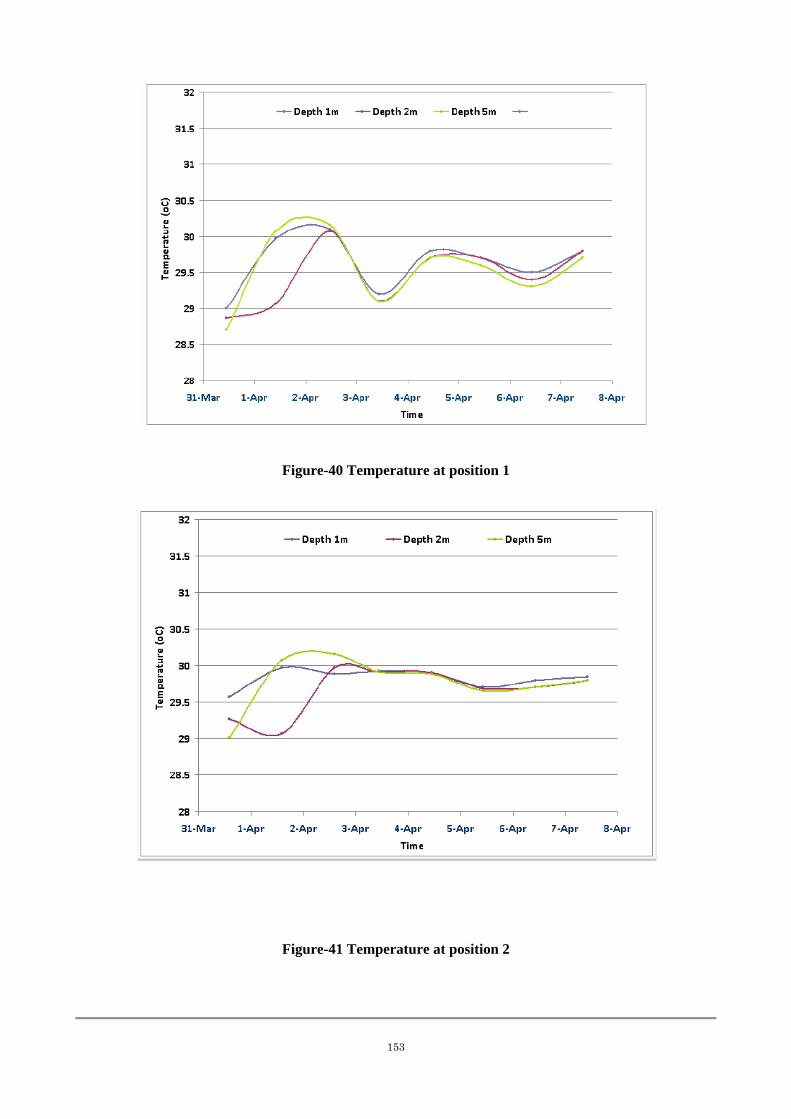

Figure-40 Temperature at position 1

Figure-41 Temperature at position 2

154

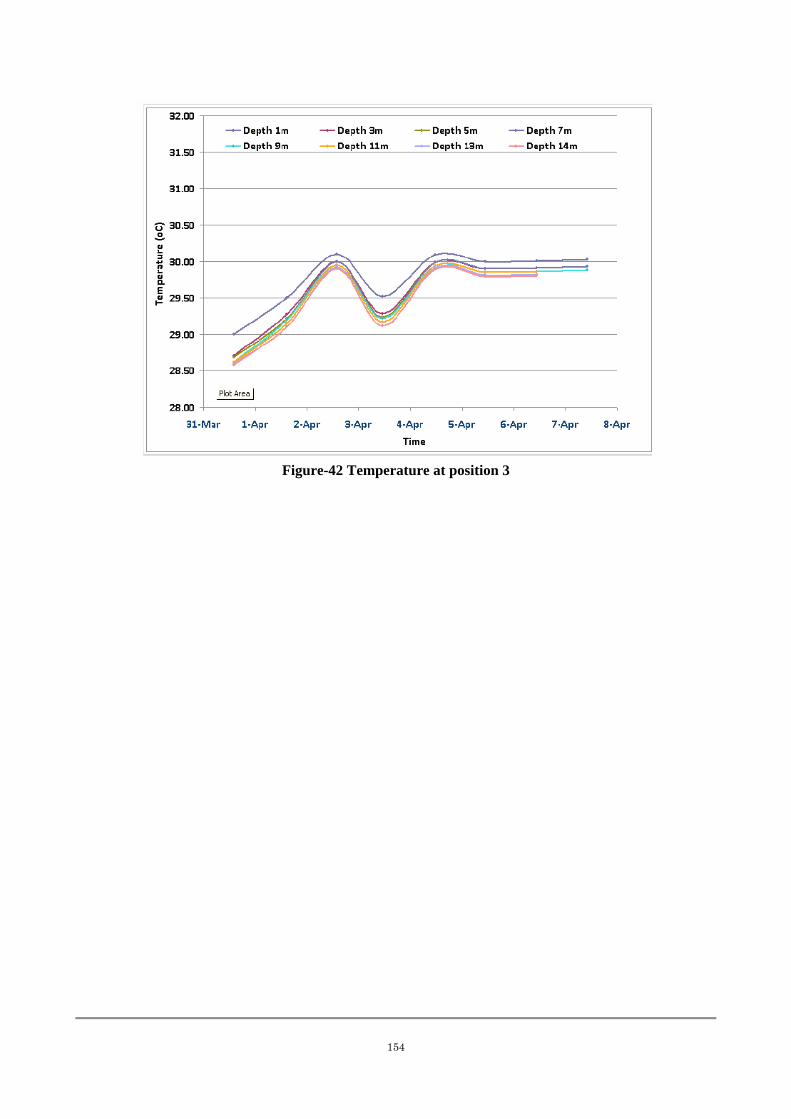

Figure-42 Temperature at position 3

155

156

Appendix-C10-1

Terms of Reference (TOR) for Design and Supervision

Consultant

1

Revised Draft Terms of Reference for Design and Supervision Consultant for Matarbari

Coal-Fired Power Plant Project in Bangladesh - Access Road-

Chapter1. Background

The Government of Bangladesh has received a loan from the Japan International

Cooperation Agency (hereinafter referred to as "JICA") to finance the Matarbari Coal-Fired

Power Plant Project including its Access Road in Bangladesh which is to secure the power

supply and to develop a policy of power source diversification in the Power sector which

highly depends on natural gas.

The Project comprises of the following components:

Lot 1(1): Power Plant- Port & Harbor and Civil Work

Lot 1(2): Power Plant- Boiler and Auxiliaries

Lot 1(3): Power Plant- Turbine, Generator and Auxiliaries

Lot 1(4): Power Plant- Coal and Ash handling

Lot 2: 400kV Transmission line to Anowara Substation

Lot 3: Access Road

- Construction of new road and new bridge

- Reconstruction of jetty

- Rehabilitation and repair of existing road

- Road repair work

ToR for the construction project of the access road for the Project (hereinafter referred to as

“Access Road Project”) has been designated as follows.

GOB intends to use part of the proceeds of the loan for eligible payments for consulting

services for which this ToR is issued.

The Access Road Project is expected to be completed by December 2020.

Location of the Project: Chittagon Area

Executing Agency: Roads and Highways Department (hereinafter referred to as “RHD”)

Technical information:

Feasibility Study Report, “Preparatory Survey on Matarbari Coal-Fired Power Plant

Development Project in Bangladesh” (hereinafter referred to as "the F/S" )

2

Chapter2. Objectives of consulting services

The consulting services shall be provided by an international consulting firm (hereinafter referred to

as "the Consultant") in association with national consultants in compliance with Guidelines for the

Employment of Consultants under Japanese ODA Loans (April 2012). The objective of the

consulting services is to achieve the efficient and proper preparation and implementation of the

Access Road Project through the following works;

(1) Detailed design

(2) Tender assistance

(3) Construction supervision

(4) Facilitation of implementation of Environmental Management Plan (EMP), Environmental

Monitoring Plan (EMoP) and Resettlement Action Plan (RAP)

3

Chapter3. Scope of consulting services

3.1 General Terms of Reference

(1) Detailed design

The Consultant shall:

(a) Review and verify all available primary and secondary data collected during the JICA’s

preparatory survey for the Access Road Project;

(b) Carry out all the required engineering surveys and investigations such as topographical

survey, hydrological survey, geotechnical survey, material availability survey, etc., as

applicable to the concerned project components.

(c) Prepare detailed work plan, progress reports and implementation schedule for the Access

Road Project to ensure effective monitoring and timely project outputs, and regularly

update the same; and

(d) Prepare the detailed design of the Access Road Project in sufficient detail to ensure clarity

and understanding by RHD, contractors and other relevant stakeholders. All the design

should be in conformity with the Bangladesh’s Standards (if available), or with the

appropriate international standards. The detailed design will, as a minimum, include

construction drawings, detailed cost estimates, necessary calculations to determine and

justify the engineering details for the Access Road Project, associated contract

documentation to include detailed specifications, bill of quantities (BOQ) and

implementation schedule for the Access Road Project. Such specifications will contain

those in relation to i) quality control of materials and workmanship, ii) safety, and iii)

protection of the environment. The detailed design shall be prepared in close consultation

with, and to meet the requirements of RHD and will be incorporated into the detailed

design report to be submitted for approval of RHD.

(2) Tender assistance

Assistance in Pre-Qualification (PQ)

The Consultant shall:

(a) Define technical and financial requirements, capacity and/or experience for PQ criteria

taking into consideration technical feature of the Access Road Project;

(b) Prepare PQ documents in accordance with the latest version of Standard Prequalification

Documents under Japanese ODA Loans;

(c) Assist RHD in PQ announcement, addendum/corrigendum, and clarifications to the

applicants’ queries;

(d) Evaluate PQ applications in accordance with the criteria set forth in PQ documents; and

4

(e) Prepare a PQ evaluation report for approval of the PQ evaluation committee.

Assistance in the Bidding Procedures

The Consultant shall:

(a) Prepare bidding documents in accordance with the latest version of Standard Bidding

Documents under Japanese ODA Loans for Procurement of Works together with all

relevant specifications, drawings and other documents;

(b) Prepare bidding documents which includes the clauses to have Contractor comply with the

requirement of the Environmental Management Plan (EMP) and JICA Guidelines for

environmental and social considerations (April 2010) (JICA Environmental Guidelines);

(c) Assist RHD in issuing bid invitation, conducting pre-bid conferences, issuing

addendum/corrigendum, and clarifications to bidders’ queries;

(d) Evaluate bids in accordance with the criteria set forth in the bidding documents. In such

evaluation, the Consultant shall carefully confirm that bidders’ submissions in their

technical proposal including, but not limited to, site organization, mobilization schedule,

method statement, construction schedule, safety plan, and EMP have been prepared in

harmony each other and will meet such requirements set forth in applicable laws and

regulations, specifications and other parts of the bidding documents;

(e) Prepare a bid evaluation report for approval of the bid evaluation committee;

(f) Assist RHD in contract negotiation by preparing agenda and facilitating negotiations

including preparation of minutes of negotiation meeting; and

(g) Prepare a draft and final contract agreement.

(3) Construction supervision

The Consultant shall perform his duties during the construction period in accordance with the

contracts to be executed between the Employer and the contractors. FIDIC MDB Harmonized

Edition (2010) complemented with the Specific Provisions as included in the Standard Bidding

Documents under Japanese ODA Loans for Procurement of Works will be applied to the civil

works of the Project. In this context, the Consultant shall:

(a) Act as the Engineer to execute construction supervision and contract administration services

in accordance with the power and authority to be delegated by RHD;

(b) Provide assistance to the Employer concerning variations and claims which are to be

ordered/issued at the initiative of the Employer;

(c) Issue the commencement order to the Contractors;

(d) Provide recommendation to RHD for acceptance of the Contractor Performance security,

advance payment security and required insurances;

5

(e) Review and approve the proposals submitted by the contractors which include work

program, method statements, material sources, manpower and equipment deployment. In

light of Section 3.03 of Guidelines for the Employment of Consultants under Japanese ODA

Loans (April 2012), the Consultant shall pay attention, in particular, to whether such

proposals will meet the safety requirements set forth in the applicable laws and regulations,

the specifications or other parts of the contract;

(f) Explain and/or adjust ambiguities and/or discrepancies in the Contract Documents and issue

any necessary clarifications or instructions;

(g) Review, verify and further detail the design of the works, approve the Contractors’ working

drawings and, if necessary, issue further drawings and/or give instructions to the Contractor;

(h) Liaise with the appropriate authorities to ensure that all the affected utility services are

promptly relocated.

(i) Carry out field inspections on the contractor’s setting out to ensure that the works are

carried out in accordance with drawings and other design details;

(j) Regularly monitor physical and financial progress against the milestones as per the contract

so as to ensure completion of contract in time;

(k) Supervise the works so that all the contractual requirements will be met by the contractors,

including those in relation to i) quality of the works, ii) safety and iii) protection of the

environment. In light of Section 3.03 of Guidelines for the Employment of Consultants

under Japanese ODA Loans (April 2012), the Consultant shall confirm that an accident

prevention officer proposed by contractor is duly assigned at the project site and that

construction works are carried out according to the requirements set forth in the applicable

laws and regulations, the specifications or other parts of the contract;

(l) Supervise field tests, sampling and laboratory test to be carried out by the contractors;

(m) Inspect the construction method, equipment to be used, workmanship at the site, and attend

shop inspection and manufacturing tests in accordance with the specifications;

(n) Survey and measure the work output performed by the contractors and issue payment

certificates such as interim payment certificates and final payment certificate as specified in

the contract;

(o) Coordinate the works among different contractors employed for the Access Road Project;

(p) Modify the designs, technical specifications and drawings, relevant calculations and cost

estimates as may be necessary in accordance with the actual site conditions and issue

variation orders (including necessary actions in relation to the works performed by other

contractors working for other projects, if any);

(q) Carry out timely reporting to RHD for any inconsistency in executing the works and

suggesting appropriate corrective measures to be applied;

6

(r) Inspect, verify and determine claims issued by the parties to the contract (i.e. RHD and

contractors) in accordance with the civil works contract;

(s) Perform the inspection of the works and to issue certificates such as the Taking-Over

Certificate, Performance Certificate as specified in the civil works contract;

(t) Provide inspection services during defects liability period and if any defects are noted,

instruct the contractor to rectify;

(u) Check and certify as-built drawings for the parts of the works designed by the contractors, if

any;

(v)

(4) Facilitation of implementation of Environmental Management Plan (EMP), Environmental

Monitoring Plan (EMoP) and Resettlement Action Plan (RAP)

The Consultant shall:

(a) Update EMP as appropriate, incorporate necessary technical specifications with design and

contract documentation;

(b) During the preparation of bidding documents, clearly identify environmental

responsibilities as explained in the EIA/IEE and EMP;

(c) Assist RHD to review the Construction Contractor’s Environmental Program to be

prepared by the contractor in accordance with EMP, relevant plans and JICA

Environmental Guidelines and to make recommendations to RHD regarding any necessary

amendments for its approval;

(d) Assist RHD to implement the measures identified in the EMP;

(e) Monitor the effectiveness of EMP and negative impacts on environment caused by the

construction works and provide technical advice, including a feasible solution, so that RHD

can improve situation when necessary;

(f) Assist RHD in monitoring the compliance with conditions stated in the EPC and the

requirements under EMP and JICA Environmental Guidelines;

(g) Assist RHD in preparation of the answer to the request from JICA’s advisory committee

for environmental and social considerations, if necessary;

(h) Assist RHD in the capacity building of RHD staff on environmental management through

on-the-job training on environmental assessment techniques, mitigation measure planning,

supervision and monitoring and reporting;

(i) Update and/or prepare RAP as necessary based on detailed design in accordance with the

agreed resettlement framework, including entitlement matrix and compensation plan;

coordinate with various agencies in preparing the procedures for timely land acquisition

and disbursement of compensation to project affected persons (PAPs);

7

(j) Assist RHD in identifying the eligible PAPs, and in preparation/updating of the list of

eligible PAPs and ‘Payment Statement’ for individual eligible PAPs. The places where

each eligible PAPs will relocate to are necessary to be recorded so that RHD could

implement monitoring on income and living conditions of resettled persons;

(k) Assist RHD in conducting social assessment during early stage of the detailed design stage

and review the existing income restoration plan and special assistance plan for vulnerable

PAPs and revise/update the contents of the plans, if necessary based on priorities identified

with support of relevant government agencies and Non-Governmental Organizations

(NGOs). The following contents should be included in the plans;

i. Skills Training

ii. Project related Job Opportunities

iii. Provision of social welfare grant

iv. Provision of Agricultural Extension Services

v. Provision of the special allowance to vulnerable PAPs

(l) Assist RHD to implement the measures identified in the revised RAP;

(m) Monitor land acquisition and compensation activities being undertaken by RHD and/or

competent authorities, and report the results in monthly progress reports;

(n) Assist in procurement of implementation NGO (INGO) and external monitoring agency

(EMA);

(o) Assist RHD in facilitating stakeholder’s participation (including focus group discussions

for vulnerable PAPs) and providing feedback their comments on RAP;

(p) Assist RHD in establishment of grievance redress mechanism including formation of

Grievance Redress Committee;

(q) Assist RHD to ensure that the PAPs are fully aware of the grievance redress procedure and

the process of bringing their complaints, investigate the veracity of the complaints, and

recommends actions/measures to settle them amicably, fairly and transparently before they

go to the redress committee or the courts of law; and

(r) Provide technical services with grievance redress committee for keeping and updating

records when necessary.

3.2 Specific Terms of Reference

(1) Safety Control of the Project

In an effort to assure the safety during the work of the Project, RHD shall take following actions

and the Consultant shall obey the proposal related to the safety control from RHD;

8

(a) Bidding documents for procurement of works require that;

i) The safety requirements in accordance with the laws and regulations in Bangladesh and

relevant international standards (including guidelines of international organization), if

any, shall be clearly stipulated in the contract.

ii) Bidders shall furnish a safety plan to meet the safety requirements stipulated in the

bidding documents.

iii) The personnel for key positions to be proposed by bidders shall include an accident

prevention officer.

(b) The Consultant shall take following actions to secure the safety in the project;

i) When preparing or reviewing bidding documents for procurement of works, the

Consultant shall make sure that the requirements stipulated in (a) above will fully be

met.

ii) The Consultant shall review the safety plans submitted by the bidders.

iii) During the supervision of the construction work, the Consultant shall confirm that an

accident prevention officer proposed by the contractor is duly assigned at the project

site and that the construction work is carried out according to the safety requirements

stipulated in the contract. If the Consultant recognize any questions regarding the

safety measures including the ones mentioned above, the Consultant shall require the

contractors to take appropriate remedies.

9

Chapter4. Expected Time Schedule

The total duration of consulting services will be 71 months follows by 12 months of defect

liability period. The implementation schedule expected is as shown in Table 1.

Table 1 : Implementation Schedule Expected

(This table has been removed because of confidential information.)

10

Chapter5. Staffing (Expertise required)

4 of Professional (A) consultants and 30 of Professional (B) consultants will be engaged, over

71 month’ duration of consulting services, for a total of 115 person-months for Professional (A)

and 557 person-months for Professional (B) consultants. Total consulting input is 672

person-months.

(1) Qualification of key Team Members

The qualification of key Team Members is shown in Table 2.

Table 2 : Qualification of key Team Members

Designation Qualification International Consultants (Pro-A)

Team Leader/ Civil Engineer 1

Education: • Graduate in Civil Engineering Experience: • Experience in Road Related Field: 15 years or more • Experience of design and construction supervision in road sector projects: 10 years or more • Experience of construction supervision for road project in ICB contract: 2 projects or more • Experience of leading a consultants’ team as the Team Leader or the Deputy Team Leader: Once or more

Bridge Engineer 1

Education: Graduate in Civil Engineering Experience: • Experience in design of Road Bridges: 10 years or more • Experience of construction supervision for bridge project in ICB contract: 2 projects or more • Experience as a bridge design specialist/structure engineer: 2 projects or more

Local Consultants (Pro-B)

Civil Engineer 2

Education: • Graduate in Civil Engineering Experience: • Experience in Road Related Field: 15 years or more • Experience of design and construction supervision in road sector projects: 15 years or more

Bridge Engineer 2

Education: • Graduate in Civil Engineering Experience: • Experience in design of road bridges: 10 years or more • Experience as a bridge design specialist: 2 projects or more

11

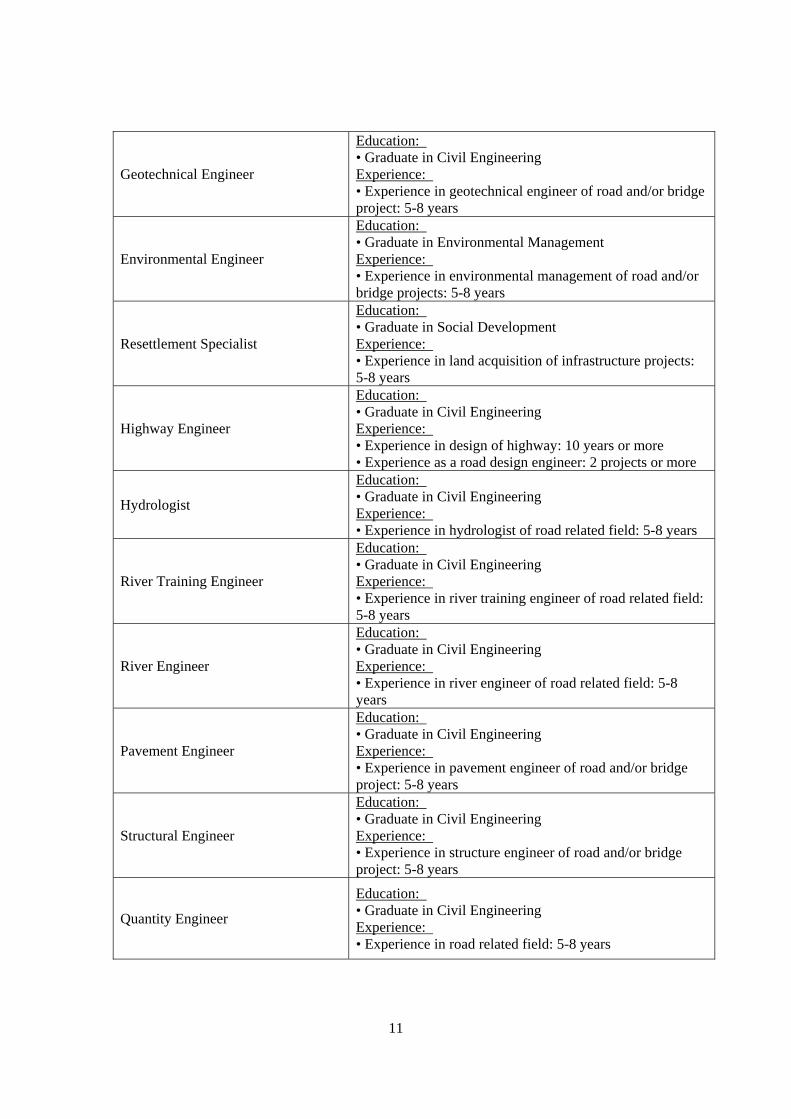

Geotechnical Engineer

Education: • Graduate in Civil Engineering Experience: • Experience in geotechnical engineer of road and/or bridge project: 5-8 years

Environmental Engineer

Education: • Graduate in Environmental Management Experience: • Experience in environmental management of road and/or bridge projects: 5-8 years

Resettlement Specialist

Education: • Graduate in Social Development Experience: • Experience in land acquisition of infrastructure projects: 5-8 years

Highway Engineer

Education: • Graduate in Civil Engineering Experience: • Experience in design of highway: 10 years or more • Experience as a road design engineer: 2 projects or more

Hydrologist

Education: • Graduate in Civil Engineering Experience: • Experience in hydrologist of road related field: 5-8 years

River Training Engineer

Education: • Graduate in Civil Engineering Experience: • Experience in river training engineer of road related field: 5-8 years

River Engineer

Education: • Graduate in Civil Engineering Experience: • Experience in river engineer of road related field: 5-8 years

Pavement Engineer

Education: • Graduate in Civil Engineering Experience: • Experience in pavement engineer of road and/or bridge project: 5-8 years

Structural Engineer

Education: • Graduate in Civil Engineering Experience: • Experience in structure engineer of road and/or bridge project: 5-8 years

Quantity Engineer

Education: • Graduate in Civil Engineering Experience: • Experience in road related field: 5-8 years

12

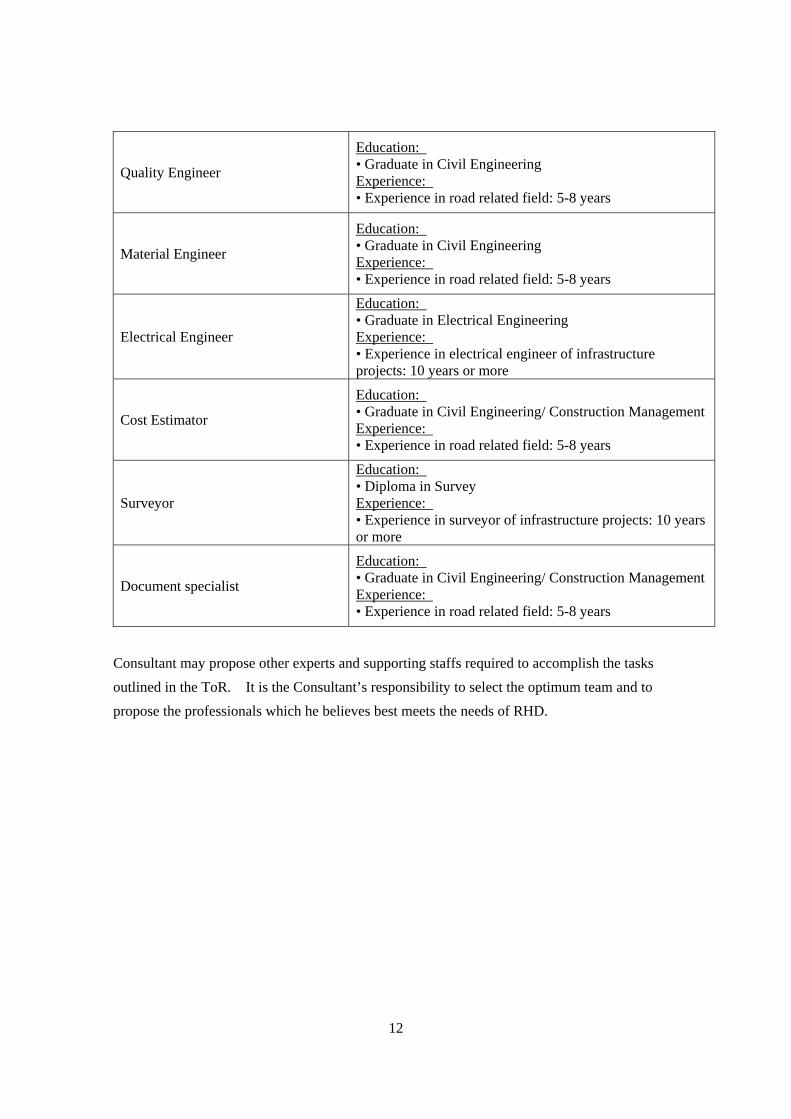

Quality Engineer

Education: • Graduate in Civil Engineering Experience: • Experience in road related field: 5-8 years

Material Engineer

Education: • Graduate in Civil Engineering Experience: • Experience in road related field: 5-8 years

Electrical Engineer

Education: • Graduate in Electrical Engineering Experience: • Experience in electrical engineer of infrastructure projects: 10 years or more

Cost Estimator

Education: • Graduate in Civil Engineering/ Construction ManagementExperience: • Experience in road related field: 5-8 years

Surveyor

Education: • Diploma in Survey Experience: • Experience in surveyor of infrastructure projects: 10 years or more

Document specialist

Education: • Graduate in Civil Engineering/ Construction ManagementExperience: • Experience in road related field: 5-8 years

Consultant may propose other experts and supporting staffs required to accomplish the tasks

outlined in the ToR. It is the Consultant’s responsibility to select the optimum team and to

propose the professionals which he believes best meets the needs of RHD.

13

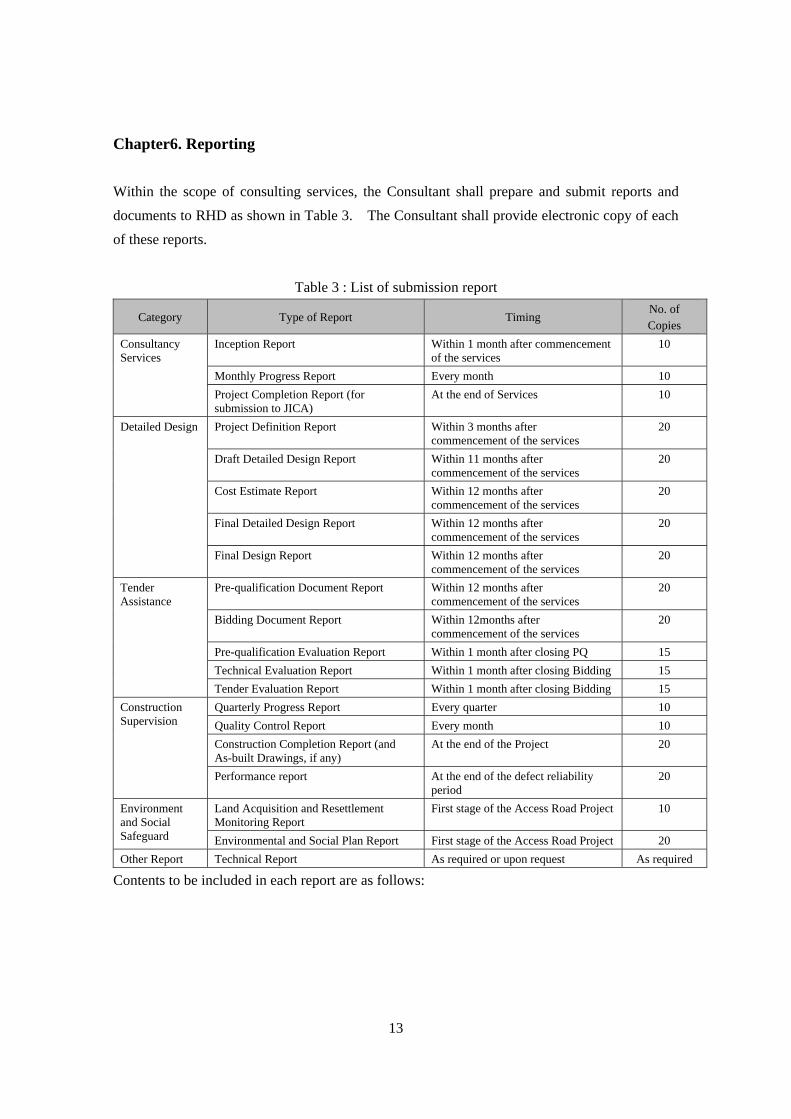

Chapter6. Reporting

Within the scope of consulting services, the Consultant shall prepare and submit reports and

documents to RHD as shown in Table 3. The Consultant shall provide electronic copy of each

of these reports.

Table 3 : List of submission report

Category Type of Report Timing No. of Copies

Consultancy Services

Inception Report Within 1 month after commencement of the services

10

Monthly Progress Report Every month 10

Project Completion Report (for submission to JICA)

At the end of Services 10

Detailed Design Project Definition Report Within 3 months after commencement of the services

20

Draft Detailed Design Report Within 11 months after commencement of the services

20

Cost Estimate Report Within 12 months after commencement of the services

20

Final Detailed Design Report Within 12 months after commencement of the services

20

Final Design Report Within 12 months after commencement of the services

20

Tender Assistance

Pre-qualification Document Report Within 12 months after commencement of the services

20

Bidding Document Report Within 12months after commencement of the services

20

Pre-qualification Evaluation Report Within 1 month after closing PQ 15

Technical Evaluation Report Within 1 month after closing Bidding 15

Tender Evaluation Report Within 1 month after closing Bidding 15

Construction Supervision

Quarterly Progress Report Every quarter 10

Quality Control Report Every month 10

Construction Completion Report (and As-built Drawings, if any)

At the end of the Project 20

Performance report At the end of the defect reliability period

20

Environment and Social Safeguard

Land Acquisition and Resettlement Monitoring Report

First stage of the Access Road Project 10

Environmental and Social Plan Report First stage of the Access Road Project 20

Other Report Technical Report As required or upon request As required

Contents to be included in each report are as follows:

14

(Monthly Progress report and Inception report)

a) Monthly Progress Report: Describes briefly and concisely all activities and progress for the

previous month by the 10th day of each month. Problems encountered or anticipated will be

clearly stated, together with actions to be taken or recommendations on remedial measures for

correction. Also indicates the work to be performed during the coming month.

b) Inception Report, to be submitted within 1 month after the commencement of the services,

presenting the methodologies, schedule, organization, etc.

(Detailed Design)

a) Project Definition Report, to be submitted in the 3rd month after the commencement of services,

presenting the design criteria and standards.

b) Draft Detailed Design Report, to be submitted in the 11th month after the commencement of

services, presenting detailed engineering design.

c) Cost Estimate Report, to be submitted in the 12th month after the commencement of services,

presenting detailed cost estimate.

d) Final Detailed Design Report, to be submitted in the 12th month after the commencement of

services, compiling all the items carried out during services.

e) Final Design Report, to be submitted in the 12th month after the commencement of services,

finalizing detailed design, cost estimate, bid plan, bid evaluation criteria, technical evaluation criteria

and bidding documents through the incorporation of comments on the Draft Design Report, provided

by RHD and the Consultant.

(Tender Assistance)

a) Pre-qualification Document Report, to be submitted in the 12th month after the commencement of

the services, presenting the pre-qualification documents and its evaluation criteria.

b) Bidding Document Report, to be submitted in the 12th month after the commencement of the

services, presenting the bidding documents and bid evaluation criteria.

c) Pre-qualification Evaluation Report, to present the results of the evaluation and to select the

qualified applicants.

d) Technical Evaluation Report, to present the results of technical evaluation and to recommend the

qualified applicants.

e) Tender Evaluation Report, to present the results of the tenders to select the most responsible

15

contractors.

(Construction Supervision)

a) Quarterly Progress Report, to be submitted at every three (3) months during construction,

presenting the progress status of the Project.

b) Quality Control Report, to be submitted at every month during construction, containing

record of quality control activities for the appropriate quality of all project facilities.

c) Construction Completion Report, to be submitted within three (3) month after completion of

construction, which comprises a full size of as-built drawings for all the structures and facilities

completed, and the final details of the construction completed together with all data, records,

material tests results, field books.

d) Performance Report, to be submitted at the end of the defect reliability period, containing

record of quality of all facilities whether those are satisfied with specification of tender

documents.

(Assistance in Environmental and Social Monitoring)

a) Land Acquisition and Resettlement Monitoring Report, to be submitted at first stage of the Access

Road Project.

b) Environmental and Social Safeguard Evaluation Report, to be submitted at first stage of the

Access Road Project, presenting the EMP, EMoP and RAP prepared.

(Other Report)

a) Technical Report, to be submitted as required or upon request, advising on technical issues

that need to be resolved.

16

Chapter7. Obligations of RHD

A certain range of arrangements and services will be provided by RHD to the Consultant for

smooth implementation of the Consulting Services. In this context, RHD will:

(1) Report and data Make available to the Consultant existing reports and data related to the Access Road Project; (2) Office space Provide an office spaces in the Headquarters of RHD with necessary equipment, furniture and utility. However, the Consultant’s requirement for office space, including necessary equipment, furniture and utilities, should be clearly stated in the proposal with its rental cost for the case where RHD would be unable to provide such facilities; (3) Cooperation and counterpart staff Appoint counterpart officials, agent and representative as may be necessary for effective implementation of the Consulting Services; (4) Assistance and exemption Use its best efforts to ensure that the assistance and exemption, as described in the Standard Request for Proposal issued by JICA, will be provided to the Consultant, in relation to

- work permit and such other documents; - entry and exit visas, residence permits, exchange permits and such other documents;- clearance through customs; - instructions and information to officials, agent and representatives of Bangladesh; - exemption from any requirement for registration to practice their profession; - privilege pursuant to the applicable law in Bangladesh.

17

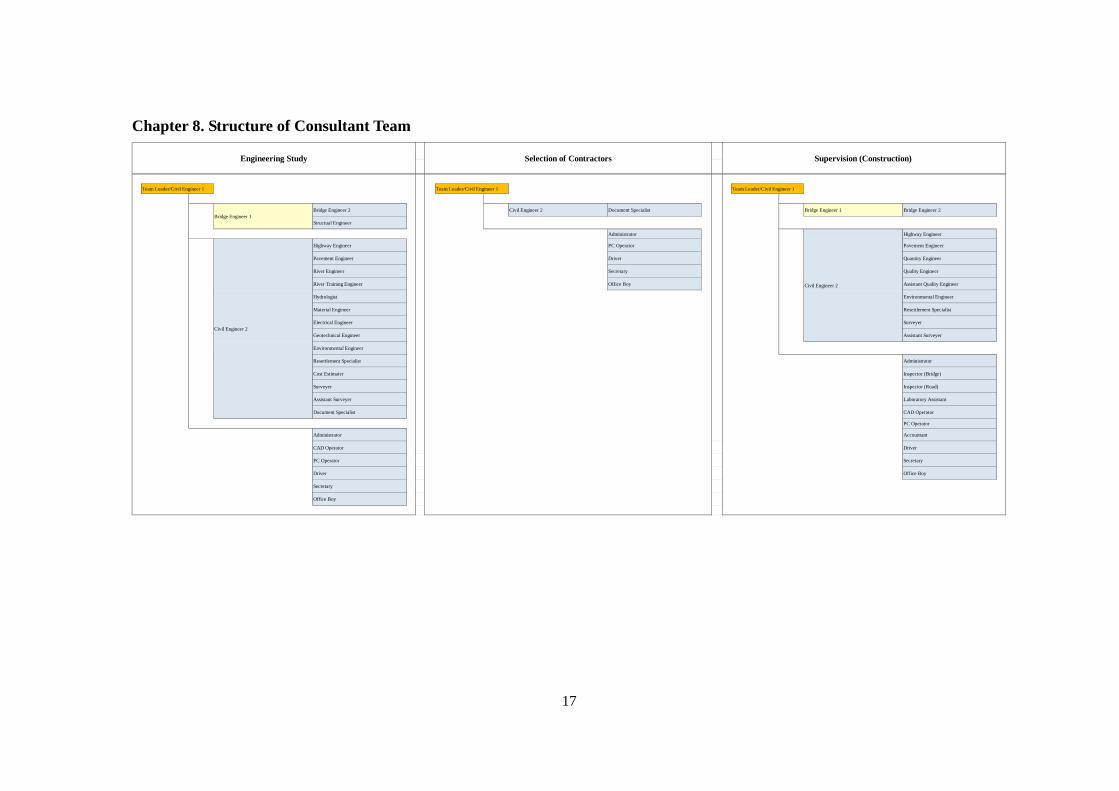

Chapter 8. Structure of Consultant Team

Bridge Engineer 2 Civil Engineer 2 Document Specialist Bridge Engineer 1 Bridge Engineer 2

Structual Engineer

Administrator Highway Engineer

Highway Engineer PC Operator Pavement Engineer

Pavement Engineer Driver Quantity Engineer

River Engineer Secretary Quality Engineer

River Training Engineer Office Boy Assistant Quality Engineer

Hydrologist Environmental Engineer

Material Engineer Resettlement Specialist

Electrical Engineer Surveyer

Geotechnical Engineer Assistant Surveyer

Environmental Engineer

Resettlement Specialist Administrator

Cost Estimater Inspector (Bridge)

Surveyer Inspector (Road)

Assistant Surveyer Laboratory Assistant

Document Specialist CAD Operator

PC Operator

Administrator Accountant

CAD Operator Driver

PC Operator Secretary

Driver Office Boy

Secretary

Office Boy

Bridge Engineer 1

Supervision (Construction)

Team Leader/Civil Engineer 1

Civil Engineer 2

Civil Engineer 2

Team Leader/Civil Engineer 1

Engineering Study Selection of Contractors

Team Leader/Civil Engineer 1

18

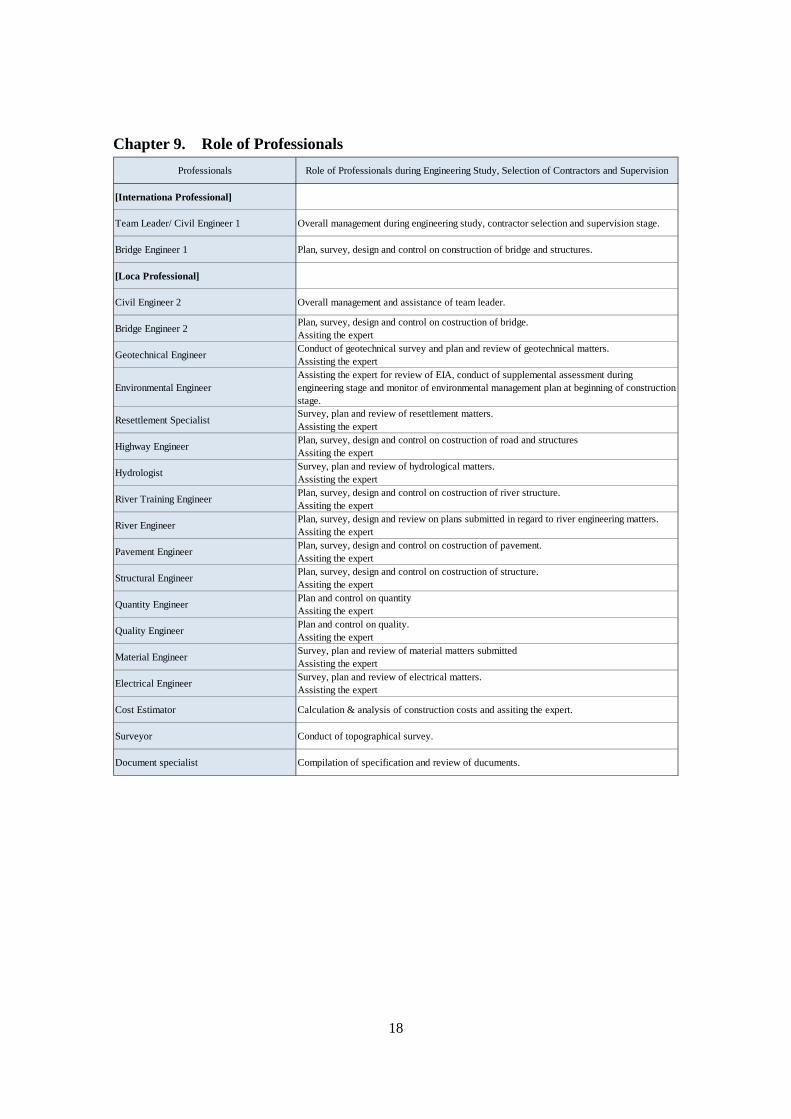

Chapter 9. Role of Professionals

Professionals Role of Professionals during Engineering Study, Selection of Contractors and Supervision

[Internationa Professional]

Team Leader/ Civil Engineer 1 Overall management during engineering study, contractor selection and supervision stage.

Bridge Engineer 1 Plan, survey, design and control on construction of bridge and structures.

[Loca Professional]

Civil Engineer 2 Overall management and assistance of team leader.

Bridge Engineer 2Plan, survey, design and control on costruction of bridge.Assiting the expert

Geotechnical EngineerConduct of geotechnical survey and plan and review of geotechnical matters.Assisting the expert

Environmental EngineerAssisting the expert for review of EIA, conduct of supplemental assessment duringengineering stage and monitor of environmental management plan at beginning of constructionstage.

Resettlement SpecialistSurvey, plan and review of resettlement matters.Assisting the expert

Highway EngineerPlan, survey, design and control on costruction of road and structuresAssiting the expert

HydrologistSurvey, plan and review of hydrological matters.Assisting the expert

River Training EngineerPlan, survey, design and control on costruction of river structure.Assiting the expert

River EngineerPlan, survey, design and review on plans submitted in regard to river engineering matters.Assiting the expert

Pavement EngineerPlan, survey, design and control on costruction of pavement.Assiting the expert

Structural EngineerPlan, survey, design and control on costruction of structure.Assiting the expert

Quantity EngineerPlan and control on quantityAssiting the expert

Quality EngineerPlan and control on quality.Assiting the expert

Material EngineerSurvey, plan and review of material matters submittedAssisting the expert

Electrical EngineerSurvey, plan and review of electrical matters.Assisting the expert

Cost Estimator Calculation & analysis of construction costs and assiting the expert.

Surveyor Conduct of topographical survey.

Document specialist Compilation of specification and review of ducuments.

Appendix-C12-01

Draft Accounting Policy

1

Draft Accounting Policy

The principle accounting policy applied in the preparation of the financial statements are set out

below. The policy is to be applied consistently to all the years presented, unless otherwise stated.

The policy is selected and applied by the company’s management for significant transactions

and events that have a material effect within the framework of BAS-1 “Presentation of Financial

Statements” in preparation and presentation of financial statements. Accounting and valuation

methods are disclosed properly for reasons of clarity.

1. Basis of preparation of the financial statements

(1) Accounting Standards

The financial statements of the company are to be prepared in accordance with Bangladesh

Accounting Standards (BAS) and Bangladesh Financial Reporting Standards (BFRS) adopted

by the Institute of Chartered Accountants of Bangladesh 8ICAB).

(2) Accounting Convention

The financial statements of the company are to be made up to 30 June each year and are

prepared under the historical cost convention.

(3) Legal Compliance

The financial statements are to be prepared and the disclosures of information made in

accordance with the requirements of the Companies Act 1944 and BAS and BFRS adopted by

ICAB.

(4) Critical Accounting Estimates, Assumptions and Judgments

The preparation of the financial statements requires the use of certain critical accounting

estimates in accordance with BFRS. It also requires management to exercise its judgment in the

process of applying the company’s accounting policy.

2. Functional and Presentation Currency

The financial statements are to be prepared in Bangladesh Taka which comprises the company’s

functional currency.

3. Level of Precision

The figures of the financial statements are to be presented in Taka which are to be rounded off

to the nearest integer.

2

4. Foreign Currency Translation

Foreign currency transactions are to be translated and recorded at the applicable rates of

exchange ruling at the date of transaction in accordance with BAS 21 “The Effects of Changes

in Foreign Exchange Rates”. Foreign currency monetary assets and liabilities at the balance

sheet date are to be translated at the rates prevailing on that date. The exchange differences at

the balance sheet date are to be adjusted and recorded to the balance sheet and/or profit and loss

statement.

5. Reporting Period

The financial statements are to cover one year starting from July 1 to June 30 of the succeeding

year.

6. Cash Flow Statement

BAS 1 “Presentation of Financial Statements” requires that a cash flow statement is to be

prepared as it provides information about cash flows of the enterprise which is useful in

providing users of financial statements with a basis to assess the ability of the enterprise to

generate cash and cash equivalents and the needs of the enterprise to utilize those cash flows.

Cash flow statement of the company is to be prepared under the direct method for the period,

classified by operating, investing and financing activities as prescribed in BAS 7 “Cash Flow

Statements”.

7. Comparative Information

As per guided in BAS 1 “Presentation of Financial Statements” comparative information in

respect of the previous year is to be presented in all numerical information in the financial

statements and the narrative and descriptive information where it is relevant for understanding

of the current year’s financial statements.

8. Assets and their Valuation

8.1 Property, Plant and Equipment

Tangible fixed assets are to be accounted according to BAS 16 “Property, Plant and Equipment”

at their historical cost less cumulative depreciation and the capital work-in-progress is to be

stated at cost. The historical cost includes expenditure that is directly attributable to the

acquisition of the items. The cost of an item of property, plant and equipment comprises its

purchase price, import duties and non-refundable taxes, after deducting trade discount and

rebates and any costs directly attributable to bringing the assets to the location and condition

3

necessary for it to be capable of operating in the intended manner. The software that is integral

to the functionality of the related equipment is to be capitalized as a part of the equipment.

8.2 Subsequent Costs

Subsequent costs are to be included in the asset’s carrying amount or recognized as separate

asset, as appropriate, only when it is probable that future economic benefits associate with the

item will flow to the company and the cost of the item can be measured reliably. The carrying

amount of the replaced part is to be de-recognized. All other repairs and maintenance are to be

charged to the profit and loss account during the financial period in which they are incurred.

8.3 Depreciation of the Fixed Assets

No depreciation is to be charged on land, land development and capital work-in-progress. For

addition of fixed assets during the year, depreciation is to be charged at a half of the full rate. In

case of disposal of fixed assets, no depreciation is to be charged in the year of disposal.

Depreciation of all properties is to be computed using the straight line method. Considering the

estimated useful life of the assets, the rates of depreciation are fixed as follows;

Building: ______ %

Plant & Machinery: _______ %

Motor Vehicles: ______ %

Office equipment: _______ %

Computer and Peripherals: ______ %

Furniture & Fixtures: ______ %

Other Assets: ______ %

8.4 Capital Work-in-Progress

The capital work-in-progress consists of all costs related to projects including civil construction,

land development, consultancy, interest, exchange gain/loss, import duties, non-refundable taxes

and VAT. Property, plant and equipment that is being under construction and/or acquisition is

also accounted for as the capital work-in-progress until the construction and/or acquisition is

completed and measured at cost.

8.5 Retirement and Disposal

An item of property, plant and equipment is de-recognized on disposal or when no further

economic benefits are expected from its use, whichever comes earlier. Gains or losses arising

from the retirement or disposal of property, plant and equipment are to be determined by

comparing the proceeds from disposal with the carrying amount of the same, and are to be

4

recognized the net in the ‘other income’ account in the profit and loss statement.

9. Inventories

Inventories consisting of spare parts and materials are to be valued at lower of cost and net

realizable value in accordance with the provision of BAS 2 2Inventories”. The cost of

inventories include the expenditure incurred inn acquiring the inventories and other cost

incurred in bringing them to their existing location and condition. The cost of inventories is to

be determined by using the weighted average cost formula. The net realizable value is to be

based on the estimated selling price less estimated costs necessary to make the sale.

10. Financial Instruments

Non derivative financial instruments comprise of cash and cash equivalents, accounts and other

receivables, loans and borrowings and other payables.

10.1 Cash and Cash Equivalents

Cash and cash equivalents comprise of cash on hand and cash at bank including fixed deposits

having maturity up to one year which are available for use by the company without restriction.

10.2 Accounts and other Receivables

Accounts and other receivables are to be recognized initially at cost which is the fair value of

the consideration given in return. After initial recognition, these are to be carried at cost less

impairment losses due to uncollectibility of any amount so recognized.

11. Provisions

A provision is to be made in the balance sheet when the company has a legal or constructive

obligation and the probable impairment of the assets as a result of past event and it is probable

that an outflow of economic benefits will be required to settle the obligation and the impairment

of the assets and a reliable estimate can be made of an amount of the obligation. Provision is

ordinarily measured at the best estimate of the expenditure required to settle the present

obligation and the probable impairment of the assets at the balance sheet date

12. Deferred Tax

Deferred tax is recognized using the balance sheet method, providing for temporary differences

between the carrying amounts of assets and liabilities for financial reporting purposes and

amounts used for taxation purposes. Deferred tax is measured at the tax rates that are expected

to be applied to the temporary differences when they are reversed, based on the income tax law

that has been enacted or substantively enacted by the reporting date. Deferred tax assets and

5

liabilities are offset if there is a legally enforceable right to offset current tax liabilities and

assets, and they relate to income taxes levied by the same tax authority on the same taxable

entity. A deferred tax asset is to be recognized to the extent that it is probable that future taxable

profits will be available against which the deductible temporary difference can be utilized.

Deferred tax assets are reviewed at each reporting date and are reduced to the extent that it is no

longer probable that the related tax benefit will be realized.