Prentice-Hall, Inc.1 Chapter 17 Estate Planning: Saving Your Heirs Money and Headaches.

52

rentice-Hall, Inc. Chapter 17 Estate Planning: Saving Your Heirs Money and Headaches

-

Upload

lesley-wright -

Category

Documents

-

view

216 -

download

1

Transcript of Prentice-Hall, Inc.1 Chapter 17 Estate Planning: Saving Your Heirs Money and Headaches.

Prentice-Hall, Inc. 1

Chapter 17

Estate Planning: Saving Your Heirs Money and Headaches

Prentice-Hall, Inc. 2

Objectives of Estate PlanningDistribute propertyProvide for dependentsSelect guardians for minorsMinimize estate and inheritance taxesMinimize settlement costs, including

legal and accounting feesAppoint power of attorney in case of

physical or mental impairment

Prentice-Hall, Inc. 3

The Estate Planning Process

Step 1: Determine what your estate is worth.– Estate net worth = value of estate’s assets – value

of estate liabilities

Step 2: Choose your heirs and decide what they receive.

Prentice-Hall, Inc. 4

The Estate Planning Process (cont’d)

Step 3: Determine the cash needs of the estate.– Liquid assets are needed to pay estate

taxes

Step 4: Select and implement your estate planning techniques.

Prentice-Hall, Inc. 5

Understanding and Avoiding Estate Taxes

Estate taxes Gift taxes Unlimited marital

deduction The generation-

skipping tax Calculating estate

taxes

Prentice-Hall, Inc. 6

Estate Taxes

$675,000 tax-free transfer threshold for 2000/2001 increasing to $1 million in 2006.

Tax rates of 37% to 55%, determined by exact value, will be assessed on estates valued over the tax-free transfer threshold.

Special treatment for small business and family farm owners.

Prentice-Hall, Inc. 7

Gift Taxes

An individual can give $10,000 ($20,000 per couple) per year tax-free to an unlimited number of people.

The $10,000 amount will be indexed to inflation, but only in $1,000 increments.

Gifts in excess of the limit are nontax-exempt.

Prentice-Hall, Inc. 8

Unlimited Marital DeductionThere is no limit on the value of an

estate that can be passed tax-free to a spouse who is a U.S. citizen.

Unlimited marital deduction does not apply to non-U.S. citizen spouses.

Tax-free gift per year to non-citizen spouses is $100,000, beyond the tax-free transfer threshold.

Prentice-Hall, Inc. 9

The Generation-Skipping Tax

Flat 55% tax, in addition to the regular estate tax, imposed on any wealth or property transfers to a person 2 or more generations younger than the donor.

Prentice-Hall, Inc. 10

The Generation-Skipping Tax

Exemptions apply:– $10,000 gift tax exclusion as well as

education and medical expense gift tax exclusions apply

– Exemption of $1 million per individual ($2 million per couple) may be passed on to grandchildren

Prentice-Hall, Inc. 11

Calculating Your Estate Taxes

Step 1: Calculate the value of the gross estate

Step 2: Calculate your taxable estateStep 3: Calculate your gift-adjusted

taxable estateStep 4: Calculate your estate taxes

Prentice-Hall, Inc. 12

Step 1: Calculate the Value of the Gross Estate

This is the value of all of the deceased’s assets.

This includes life insurance, pensions, investments, and any real or personal property.

Prentice-Hall, Inc. 13

Step 2: Calculate Your Taxable Estate

This is equal to the gross value of the deceased’s estate minus funeral and administrative expenses, debts, liabilities, taxes and any marital or charitable deductions.

Prentice-Hall, Inc. 14

Step 3: Calculate Your Gift-Adjusted Taxable Estate

This is equal to the deceased’s taxable estate plus any taxable lifetime gifts (cumulative).

Prentice-Hall, Inc. 15

Step 4: Calculate Your Estate Taxes

Estate taxes are equal to the gift-adjusted taxable estate multiplied by the appropriate tax rate.

To determine the net tax owed calculate the total tax owed and subtract the unified gift and estate tax credit.

In 2000/2001, the $675,000 estate tax transfer threshold equaled a credit of $220,500.

Prentice-Hall, Inc. 16

Wills and What They Do Will -- a legal document that transfers an

estate after death Beneficiaries -- the people who receive your

property Executor or personal representative -- the

person who is responsible for carrying out the provisions of the will

Guardian -- cares for minor children and manages their property

Prentice-Hall, Inc. 17

Wills and the Probate Process

Probate -- the process of distributing an estate's assets

Purposes of the probate process– appoint an executor, if one is not named– validate the will– allow for challenges to the will– oversee the distribution of assets– file a report with the court and close the estate

Prentice-Hall, Inc. 18

Wills and the Probate Process (cont’d)

Disadvantages of the probate process– Numerous costs and fees – legal fees,

executor fees, court fees – that can run to 1% to 8% of the estate value

– Process can be slow, especially if there are challenges to the will or tax problems

Prentice-Hall, Inc. 19

Why Do You Need a Will?

So state law will not dictate the– distribution of your assets– custody of children or care for those with

special needsTo avoid a court-appointed

administrator and associated costs

Prentice-Hall, Inc. 20

The Basics of Writing a Will

Wills can be handwritten, computer generated, or oral

The safest way is to have a will drawn up by a lawyer

Wills must be signed, witnessed by 2 or more people, and notarized

Prentice-Hall, Inc. 21

The Basics of Writing a Will (cont’d)

Wills should be stored in a safe place; however, a safety deposit box is not always a good place because it may be sealed upon your death.

Note: Always tell someone you trust where your will is so it can be found upon your death.

Prentice-Hall, Inc. 22

The Basic Organization of a Will

Introductory statementPayment of debt and taxes clauseDisposition of property clauseAppointment clauseCommon disaster clauseAttestation and witness clause

Prentice-Hall, Inc. 23

Introductory Statement

Identifies the owner of the will and revokes all previous copies of the will

Prentice-Hall, Inc. 24

Payment of Debt and Taxes Clause

Directs the payment of debts, death and funeral expenses, and taxes.

Prentice-Hall, Inc. 25

Disposition of Property Clause

Allows for the distribution of money and property.

Names the beneficiaries.Contains a remainder clause stipulating

the disposition of any assets not directly given.

Prentice-Hall, Inc. 26

Appointment Clause

Names the executor of the will

Appoints guardians for all children under 18 years of age

Prentice-Hall, Inc. 27

Common Disaster Clause

Identifies which spouse is assumed to have died first in the event of simultaneous death

Prentice-Hall, Inc. 28

Attestation and Witness Clause

Dates and validates the will with a signature before 2 or more witnesses, who also must sign the document.

Prentice-Hall, Inc. 29

Requirements of a Valid Will

Mental competenceUnder no undue influence from another

personWill must conform to the state laws

Prentice-Hall, Inc. 30

Updating or Changing Your Will -- The Codicil

Institutes minor changes in the original will

Must be signed, witnessed, and attached to the original will

Note: If the changes are major then a new will should be drafted.

Prentice-Hall, Inc. 31

Letter of Last InstructionNot a legally binding agreementProvides information and direction,

Including the location of your willLists the people to be notified of your

deathLists the location of all pertinent legal

documentsContains funeral and burial instructions

Prentice-Hall, Inc. 32

The Duties of an Executor

Ensures that the deceased's wishes are carried out

Sends copies of the will to all beneficiaries Publishes the death notice Pays debts and liabilities on behalf of the

estate Manages the deceased's property until the

will is executed and the estate closed

Prentice-Hall, Inc. 33

Other Estate -- Planning Documents

Durable power of attorney

Living will Health care proxy

Prentice-Hall, Inc. 34

Durable Power of Attorney

Provides for someone to act on your behalf in the event you should become mentally or physically incapacitated.

This document is separate from the will and goes into effect before death.

This document should be very specific as to which legal powers it transfers.

Prentice-Hall, Inc. 35

Living Will and Health Care Proxy

A living will states your wishes regarding medical treatment in the event of a terminal illness or injury.

A health care proxy designates someone to make health care decisions should you be unable to do so for yourself.

Prentice-Hall, Inc. 36

Ways to Avoid Probate

Joint ownership– tenancy by the entirety– joint tenancy with the right of survivorship– tenancy in common -- will controls

distribution of deceased’s share– community property -- state law and will

control distribution of the property

Prentice-Hall, Inc. 37

Ways to Avoid Probate (cont’d)

Gifts– Exception for life insurance policies– Unlimited gift tax exclusion on payments made for

medical and educational expenses– Charities

Naming beneficiaries in contracts Trusts

– Living -- take effect before death– Testamentary -- take effect upon death

Prentice-Hall, Inc. 38

The Benefits of Using Trusts for Estate Transfer

Avoid probateAre much more difficult to challenge in

court than are willsReduce estate taxesAllow for professional managementProvide for confidentiality

Prentice-Hall, Inc. 39

The Benefits of Using Trusts for Estate Transfer (cont’d)

Can be used to provide for children with special needs

Can be used to hold money until a child reaches maturity

Can assure that children from a previous marriage will receive some inheritance

Prentice-Hall, Inc. 40

Living Trusts

Revocable trust Irrevocable living

trusts

Prentice-Hall, Inc. 41

Revocable Trusts

Allow for unlimited control by the trust’s owner, because the owner retains title to all the assets in the trust.

Do not provide any tax advantages.Do not pass through probate.Provide greater ease and privacy of

distribution upon death.

Prentice-Hall, Inc. 42

Irrevocable Living Trusts

Can not be changed by the owner once established, because the trust becomes another entity which owns all the assets contained in the trust.

Are not subject to estate taxes.Do not pass through probate.

Prentice-Hall, Inc. 43

Testamentary trusts

Standard family trusts

Qualified terminable interest property (Q-TIP) trusts

Sprinkling trusts

Prentice-Hall, Inc. 44

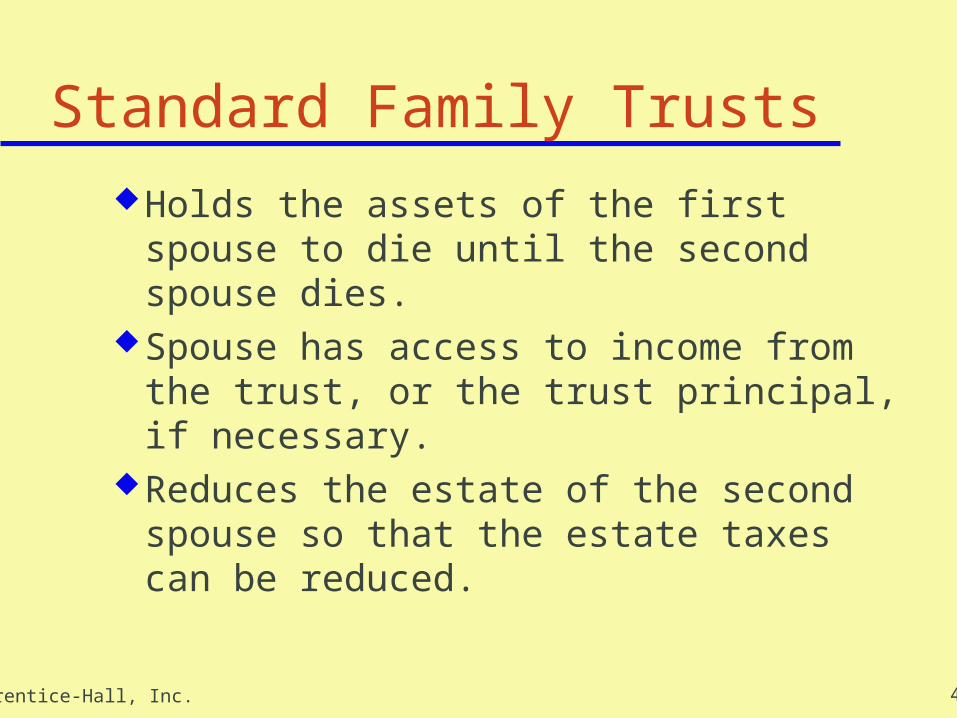

Standard Family Trusts

Holds the assets of the first spouse to die until the second spouse dies.

Spouse has access to income from the trust, or the trust principal, if necessary.

Reduces the estate of the second spouse so that the estate taxes can be reduced.

Prentice-Hall, Inc. 45

Qualified Terminable Interest Property (Q-TIP) Trusts

Provides a means to pass income to the surviving spouse without turning over control of the assets.

Ensures that assets will be passed to your children upon the death of the surviving spouse.

Prentice-Hall, Inc. 46

Sprinkling Trusts

Distributes assets on a need basis rather than according to some preset plan to a designated group of beneficiaries.

Prentice-Hall, Inc. 47

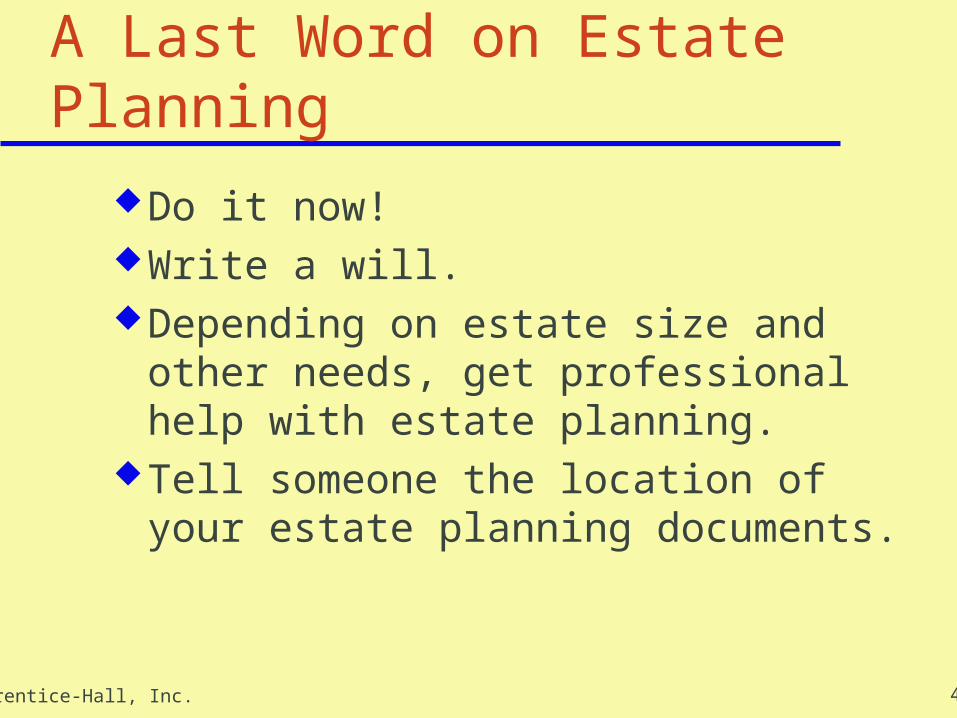

A Last Word on Estate Planning

Do it now!Write a will.Depending on estate size and other

needs, get professional help with estate planning.

Tell someone the location of your estate planning documents.

Prentice-Hall, Inc. 48

What Should You Do for 2000/2001?

If your estate is worth less than $675,000 you have no estate tax problems.– Write a will– Consider a trust for managing property of children

If you’re married and your estate value is between $675,000 and $1.35M, to avoid taxes– Take advantage of the tax-free estate transfer– Consider a standard family trust

Prentice-Hall, Inc. 49

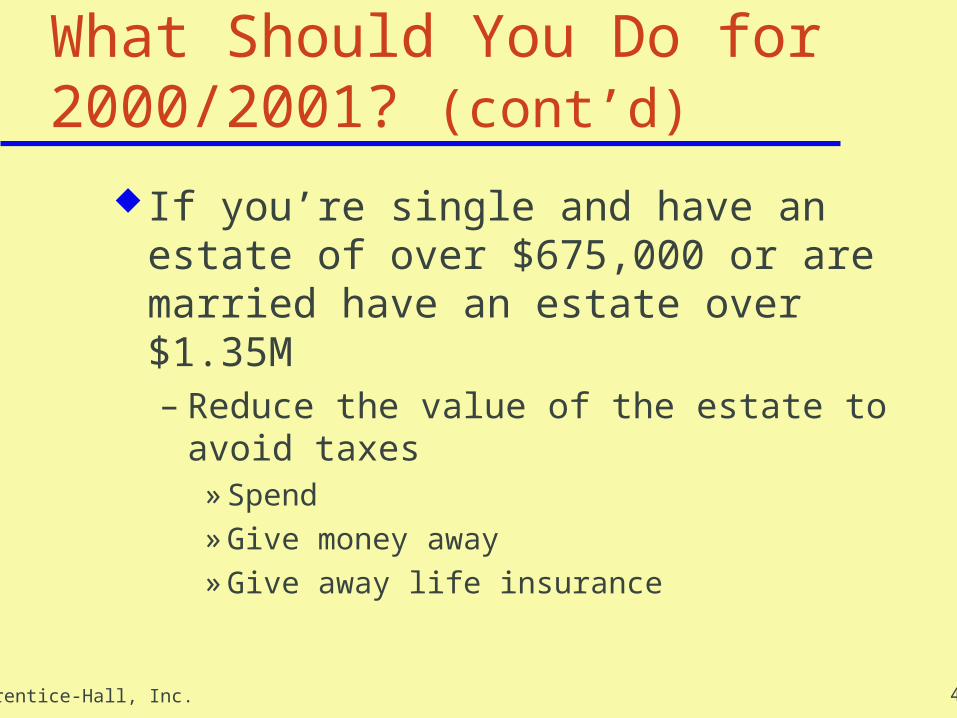

What Should You Do for 2000/2001? (cont’d)

If you’re single and have an estate of over $675,000 or are married have an estate over $1.35M– Reduce the value of the estate to avoid

taxes» Spend» Give money away » Give away life insurance

Prentice-Hall, Inc. 50

Summary

The estate planning process consists of– determining what your estate is worth.– choosing your heirs and deciding what

they receive.– determining the cash needs of the estate.– selecting and implementing your estate

planning techniques.Your will and the probate process

Prentice-Hall, Inc. 51

Summary (cont’d)

Other estate planning documents– Durable power of attorney– Living will– Letter of last instruction

Types of trusts– living trusts -- take effect before death– testamentary trusts -- take effect upon

death

Prentice-Hall, Inc. 52

Summary (cont’d)

Benefits of using trusts– avoid probate– more difficult to challenge than are wills– reduce estate taxes– allow for professional management– provide for confidentiality– allow options for meeting the needs of children

Reducing the taxable value of an estate

![storage.googleapis.com€¦ · [katheryne davis] [and heirs and assigns] [john mchale] [and heirs and assigns] [ricki reese] [and heirs and assigns] [nicole phelps] [and heirs and](https://static.fdocuments.us/doc/165x107/5f06dad27e708231d41a1204/katheryne-davis-and-heirs-and-assigns-john-mchale-and-heirs-and-assigns.jpg)