Red Stag Fulfillment: Understanding DIM Pricing for Ecommerce Fulfillment

Upload

trevor-simsCategory

view

215download

1

Prentice Hall, 2003

Chapter 10

Payments and Order Fulfillment

1

Prentice Hall, 2003 2

Learning Objectives

Understand the crucial factors determining the success of e-payment methodsDescribe the key elements in securing an e-paymentDiscuss the players and processes involved in using credit cards onlineDescribe the uses and benefits of purchase cards

Prentice Hall, 2003 3

Describe different categories and potential uses of smart cardsDiscuss various online alternatives to credit card payments and identify under what circumstances they are best usedDescribe the processes and parties involved in e-checking

Learning Objectives (cont.)

Prentice Hall, 2003 4

Learning Objectives (cont.)

Describe the role of order fulfillment and back-office operations in ECDescribe the EC order fulfillment process.Describe the major problems of EC order fulfillmentDescribe various solutions to EC order fulfillment problems

Prentice Hall, 2003 5

LensDoc Organizes Payment Online

The ProblemLensDoc—online retailer of contact lenses, sun and magnifying glassesDental care and personal care productsCustomers pay by credit card (90% of all online purchases in the U.S.)

Easy to purchaseEasy to purchase fraudulentlyContact lenses cannot be returned once used, but unsatisfied customers want their money back

Prentice Hall, 2003 6

LensDoc (cont.)

Solutions:Process credit card purchases by handRequire:

Home addressShipping address

Assumption is that if the card being used is a fraudulent one, the perpetrator is unlikely to know the cardholder’s address

Prentice Hall, 2003 7

LensDoc (cont.)

The ResultsInvestigating alternative methods of payment

Cash cardsSpecial card-swiping peripheralsCredit card processing services

Currently disadvantages outweigh advantages of any of these alternatives

Prentice Hall, 2003 8

Electronic Payments

Paying with credit cards onlineUntil recently consumers were extremely reluctant to use their credit card numbers on the WebThis is changing because:

Many of people who will be on the Internet in 2004 have not even had their first Web experience today85% of the transactions that occur on the Web are B2B rather than B2C (credit cards are rarely used in B2B transactions)

Prentice Hall, 2003 9

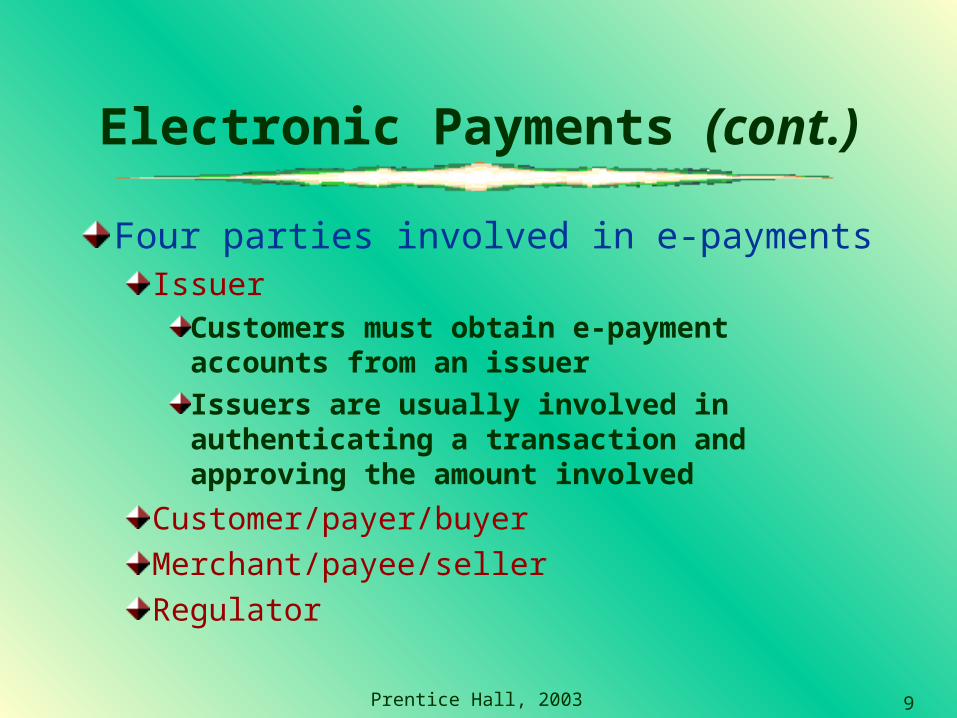

Electronic Payments (cont.)

Four parties involved in e-paymentsIssuer

Customers must obtain e-payment accounts from an issuerIssuers are usually involved in authenticating a transaction and approving the amount involved

Customer/payer/buyerMerchant/payee/sellerRegulator

Prentice Hall, 2003 10

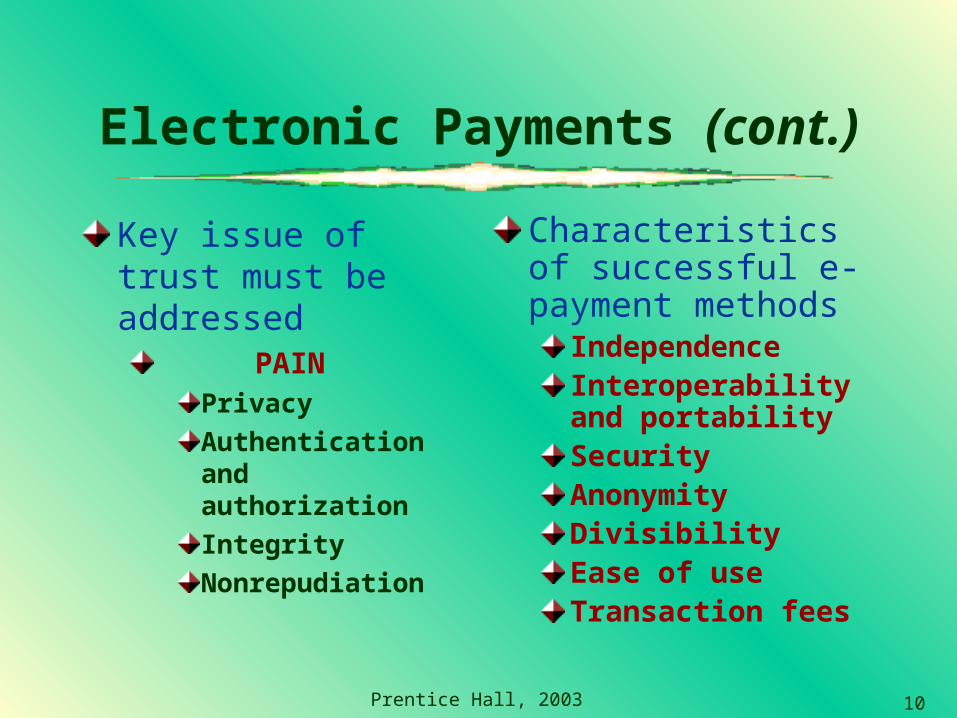

Electronic Payments (cont.)

Key issue of trust must be addressed

PAINPrivacyAuthentication and authorizationIntegrityNonrepudiation

Characteristics of successful e-payment methods

IndependenceInteroperability and portabilitySecurityAnonymityDivisibilityEase of useTransaction fees

Prentice Hall, 2003 11

Security for E-Payments

Public key infrastructure (PKI)—a scheme for securing e-payments using public key encryption and various technical componentsFoundation of a number of network applications:

Supply chain managementVirtual private networksSecure e-mailIntranet applications

Prentice Hall, 2003 12

Security for E-Payments

Public key encryptionEncryption (cryptography)—the process of scrambling (encrypting) a message in such a way that it is difficult, expensive, or time consuming for an unauthorized person to unscramble (decrypt) it

Prentice Hall, 2003 13

Security for E-Payments (cont.)

All encryption has four basic parts:Plaintext—an unencrypted message in human-readable formCiphertext—a plaintext message after it has been encrypted into unreadable formEncryption algorithm—the mathematical formula used to encrypt the plaintext into ciphertext and vice versaKey—the secret code used to encrypt and decrypt a message

Prentice Hall, 2003 14

Security for E-Payments (cont.)

Two major classes of encryption systems:

Symmetric (private key)Used to encrypt and decrypt plain textShared by sender and receiver of text

Asymmetric (public key)Uses a pair of keysPublic key to encrypt the messagePrivate key to decrypt the message

Prentice Hall, 2003 15

Security for E-Payments (cont.)

Public key encryption—method of encryption that uses a pair of keys—a public key to encrypt a message and a private key (kept only by its owner) to decrypt it, or vice versa

Private key—secret encryption code held only by its ownerPublic key—secret encryption code that is publicly available to anyone

Prentice Hall, 2003 16

Exhibit 10.1Private Key Encryption

Prentice Hall, 2003 17

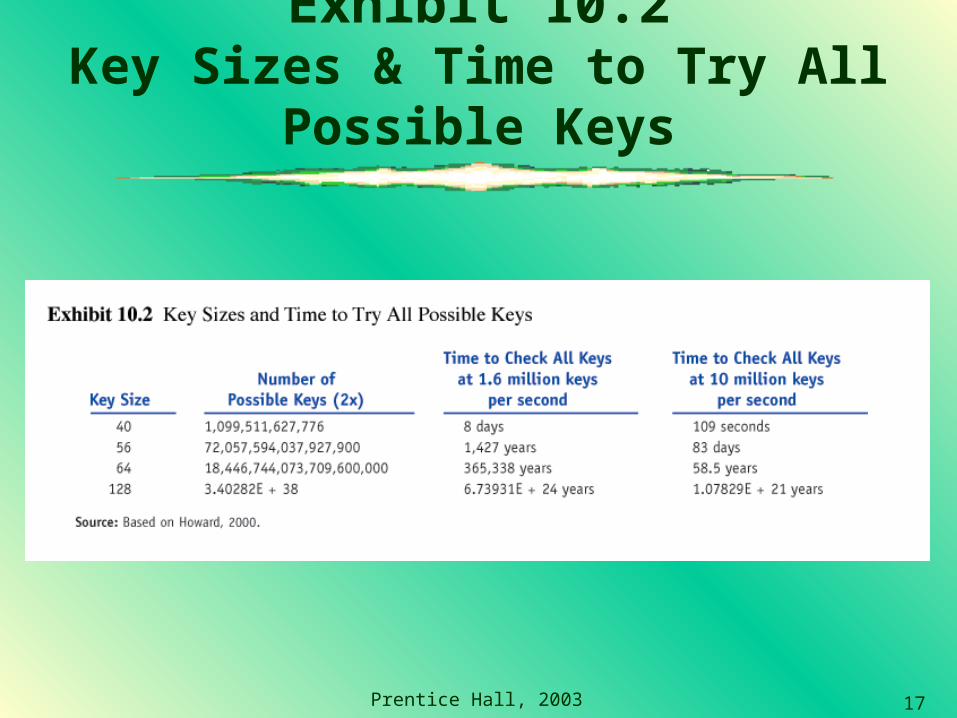

Exhibit 10.2Key Sizes & Time to Try All Possible Keys

Prentice Hall, 2003 18

Digital signatures—an identifying code that can be used to authenticate the identity of the sender of a message or documentUsed to:

Authenticate the identity of the sender of a message or documentEnsure the original content of the electronic message or document is unchanged

Security for E-Payments (cont.)

Prentice Hall, 2003 19

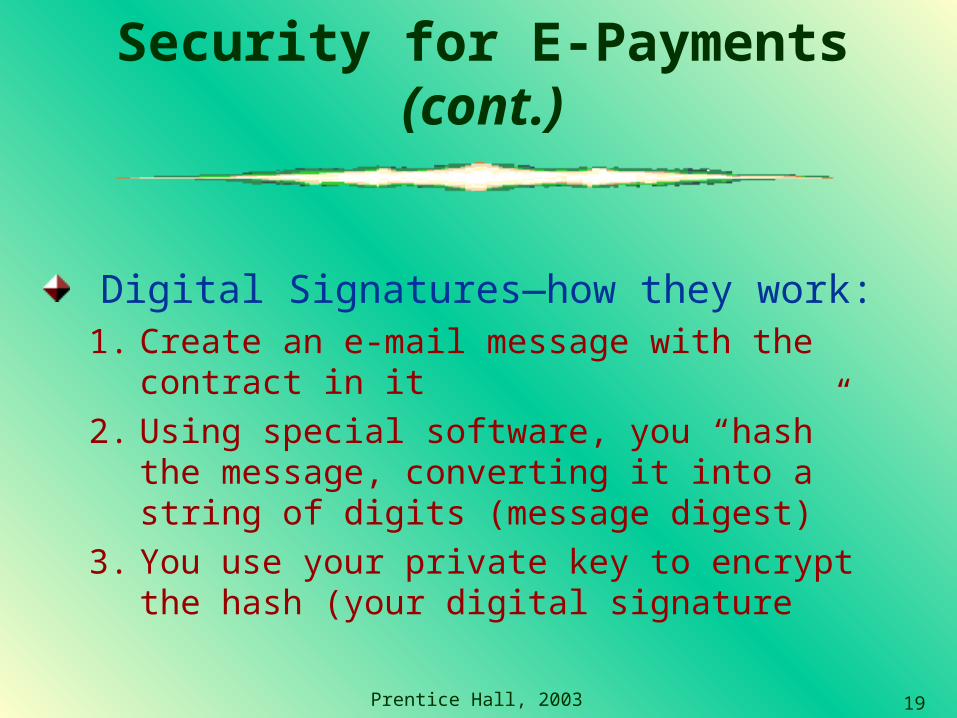

Security for E-Payments (cont.)

Digital Signatures—how they work:1. Create an e-mail message with the

contract in it2. Using special software, you “hash” the

message, converting it into a string of digits (message digest)

3. You use your private key to encrypt the hash (your digital signature

Prentice Hall, 2003 20

Security for E-Payments (cont.)

4. E-mail the original message along with the encrypted hash to the receiver

5. Receiver uses the same special software to hash the message they received

6. Company uses your public key to decrypt the message hash that you sent. If their hash matches the decrypted hash, then the message is valid

Prentice Hall, 2003 21

Exhibit 10.3Digital Signatures

Prentice Hall, 2003 22

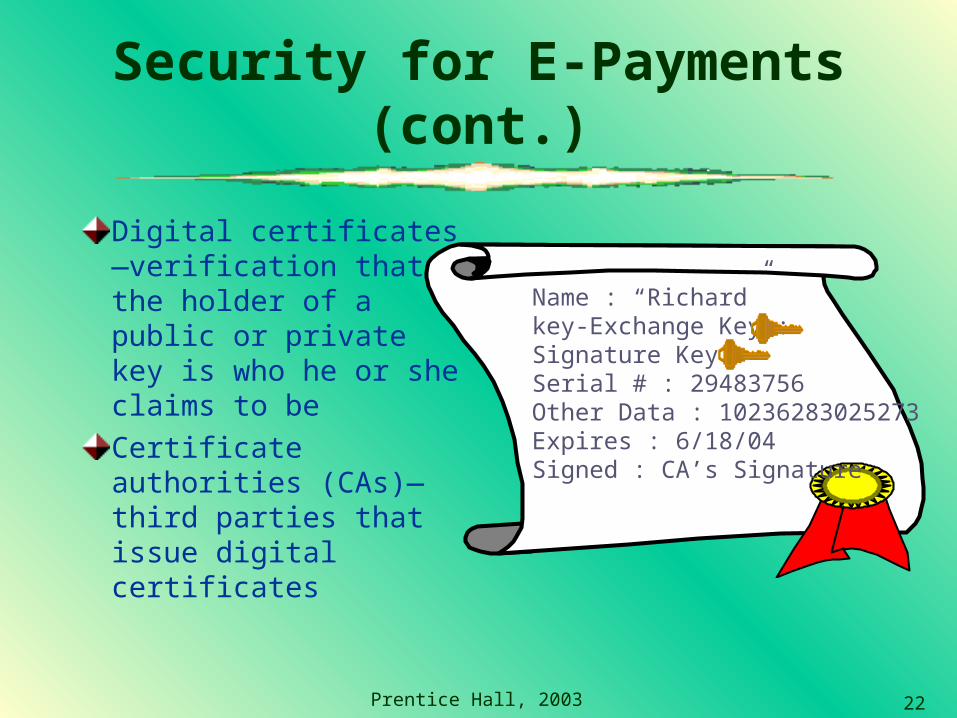

Security for E-Payments (cont.)

Digital certificates—verification that the holder of a public or private key is who he or she claims to be

Certificate authorities (CAs)—third parties that issue digital certificates

Name : “Richard”key-Exchange Key :Signature Key :Serial # : 29483756Other Data : 10236283025273Expires : 6/18/04Signed : CA’s Signature

Prentice Hall, 2003 23

Standards for E-Payments

Secure socket layer (SSL)—protocol that utilizes standard certificates for authentication and data encryption to ensure privacy or confidentialityTransport Layer Security (TLS)—as of 1996, another name for the Secure Socket Layer protocol

Prentice Hall, 2003 24

Standards for E-Payments (cont.)

Secure Electronic Transaction (SET)—a protocol designed to provide secure online credit card transactions for both consumers and merchants; developed jointly by Netscape, Visa, MasterCard, and others

Prentice Hall, 2003 25

Electronic Cards and Smart Cards

Payment cards—electronic cards that contain information that can be used for payment purposes

Credit cards—provides holder with credit to make purchases up to a limit fixed by the card issuerCharge cards—balance on a charge card is supposed to be paid in full upon receipt of monthly statementDebit card—cost of a purchase drawn directly from holder’s checking account (demand-deposit account)

Prentice Hall, 2003 26

Electronic Cards and Smart Cards (cont.)

The PlayersCardholderMerchant (seller)Issuer (your bank)Acquirer (merchant’s financial institution, acquires the sales slips)Card association (VISA, MasterCard)Third-party processors (outsourcers performing same duties formerly provided by issuers, etc.)

Prentice Hall, 2003 27

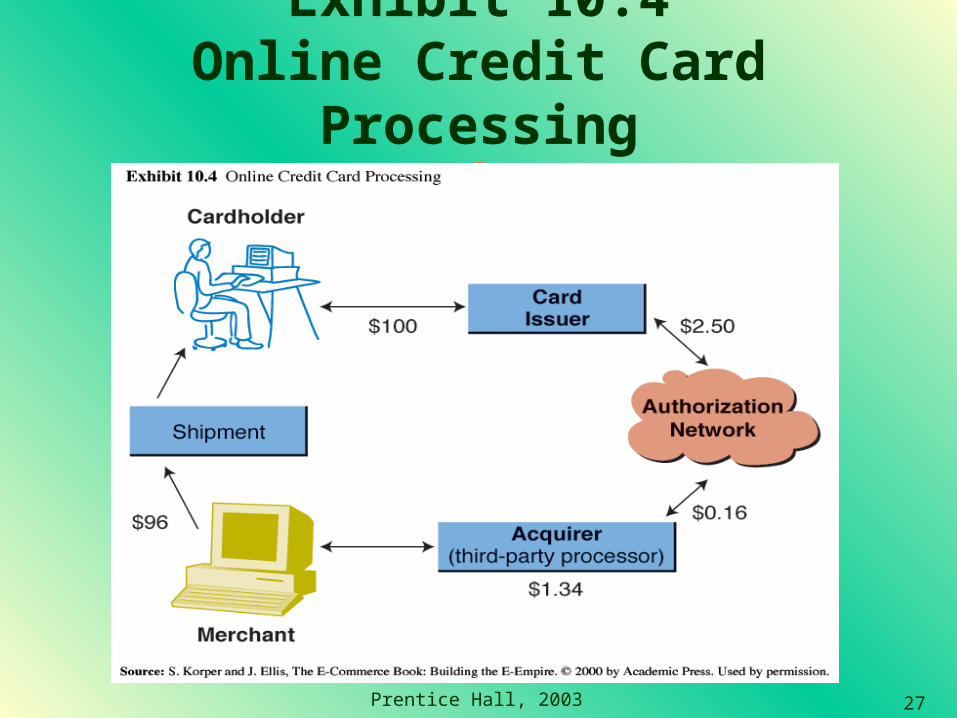

Exhibit 10.4Online Credit Card Processing

Prentice Hall, 2003 28

Electronic Cards and Smart Cards (cont.)

Credit card gateway—an online connection that ties a merchant’s systems to the back-end processing systems of the credit card issuer

Virtual credit card—an e-payment system in which a credit card issuer gives a special transaction number that can be used online in place of regular credit card numbers

Prentice Hall, 2003 29

Electronic Cards and Smart Cards (cont.)

Electronic wallets (e-wallets)—a software component in which a user stores credit card numbers and other personal information; when shopping online; the user simply clicks the e-wallet to automatically fill in information needed to make a purchase

One-click shopping—saving your order information on retailer’s Web serverE-wallet—software downloaded to cardholder’s desktop that stores same information and allows one-click-like shopping

Prentice Hall, 2003 30

Electronic Cards and Smart Cards (cont.)

Security risks with credit cardsStolen cardsReneging by the customer—authorizes a payment and later denies itTheft of card details stored on merchant’s computer—isolate computer storing information so it cannot be accessed directly from the Web

Prentice Hall, 2003 31

Electronic Cards and Smart Cards (cont.)

Purchasing cards—special-purpose payment cards issued to a company’s employees to be used solely for purchasing nonstrategic materials and services up to a preset dollar limit

Instrument of choice for B2B purchasing

Prentice Hall, 2003 32

E-Cards (cont.)

Benefits of using purchasing cardsProductivity gainsBill consolidationPayment reconciliationPreferred pricingManagement reportsControl

Prentice Hall, 2003 33

Exhibit 10.5Participants & Process of Using a Purchasing Card

Prentice Hall, 2003 34

Smart Cards

Smart card—an electronic card containing an embedded microchip that enables predefined operations or the addition, deletion, or manipulation of information on the card

Prentice Hall, 2003 35

Smart Cards (cont.)

Categories of smart cardsContact card—a smart card containing a small gold plate on the face that when inserted in a smart-card reader makes contact and so passes data to and from the embedded microchipContactless (proximity) card—a smart card with an embedded antenna, by means of which data and applications are passed to and from a card reader unit or other device

Prentice Hall, 2003 36

Smart Cards (cont.)

Securing smart cardsTheoretically, it is possible to “hack” into a smart card

Most cards can now store the information in encrypted formSame cards can also encrypt and decrypt data that is downloaded or read from the card

Cost to the attacker of doing so far exceeds the benefits

Prentice Hall, 2003 37

Smart Cards (cont.)

Important applications of smart card use:LoyaltyFinancialInformation technologyHealth and social welfareTransportationIdentification

Prentice Hall, 2003 38

E-Cash and Innovative Payment Methods

E-cash—the digital equivalent of paper currency and coins, which enables secure and anonymous purchase of low-priced itemsMicropayments—small payments, usually under $10

Prentice Hall, 2003 39

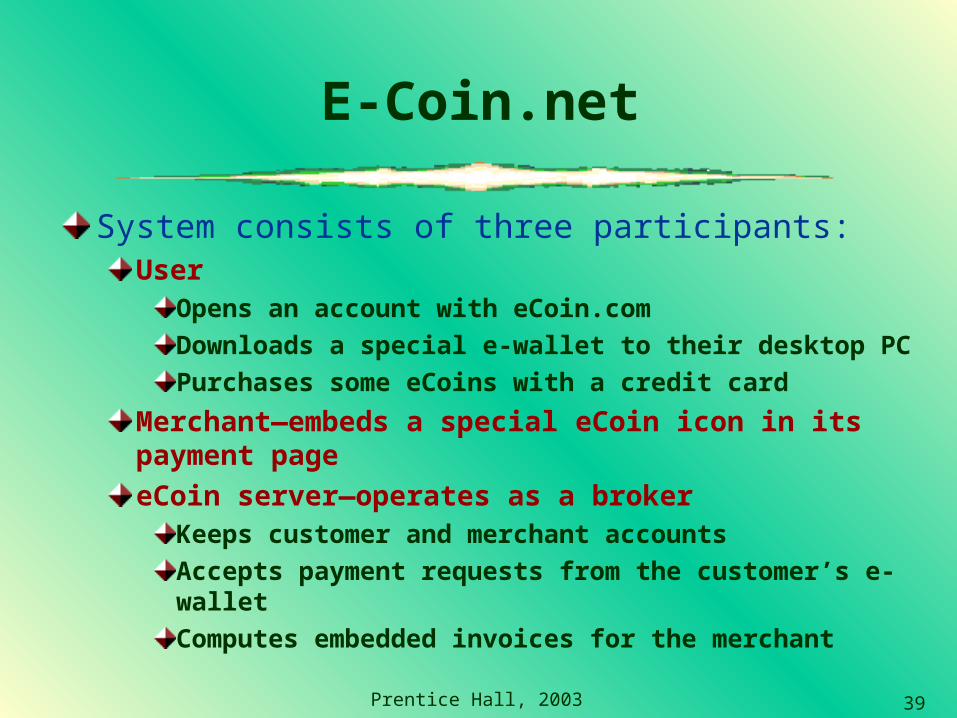

E-Coin.net

System consists of three participants:User

Opens an account with eCoin.comDownloads a special e-wallet to their desktop PCPurchases some eCoins with a credit card

Merchant—embeds a special eCoin icon in its payment pageeCoin server—operates as a broker

Keeps customer and merchant accountsAccepts payment requests from the customer’s e-walletComputes embedded invoices for the merchant

Prentice Hall, 2003 40

E-Cash and Payment Card Alternatives (cont.)

Wireless paymentsVodafone “m-pay bill” system that enables wireless subscribers to use their mobile phones to make micropayments

Qpass (qpass.com)Charges to qpass account, are charged to a specified credit card on a monthly basis

Prentice Hall, 2003 41

Stored-Value Cards

Stores cash downloaded from bank or credit card account

Visa cash—a stored-value card designed to handle small purchases or micropayments; sponsored by VisaMondex—a stored-value card designed to handle small purchases or micropayments; sponsored by Mondex, a subsidiary of MasterCard

Prentice Hall, 2003 42

E-Loyalty and Reward Programs

Loyalty programs onlineB2C sites spend hundreds of dollars acquiring new customersPayback only comes from repeat customers who are likely to refer other customers to a site

Electronic script—a form of electronic money (or points), issued by a third party as part of a loyalty program; can be used by consumers to make purchases at participating stores

Prentice Hall, 2003 43

E-Loyalty and Reward Programs (cont.)

Beenz—a form of electronic script offered by beenz.com that consumers earn at participating sites and redeem for products or services

Consumer earns beenz by visiting, registering, or purchasing at 300 participating sitesBeenz are stored and used for later purchasesPartnered with MasterCard to offer rewardzcard—stored-value card used in U.S. and Canada for purchases where MasterCard is acceptedTransfer beenz into money to spend on Web, by phone, mail order, physical stores

Prentice Hall, 2003 44

E-Loyalty and Reward Programs (cont.)

MyPoints-CyberGoldCustomers earn cash for viewing adsCash used for later purchases or applied to credit card account

Prepaid stored value cards—used online and off-line

RocketCashCombines online cash account with rewards programUser opens account and adds fundsUsed to make purchases at participating merchants

Prentice Hall, 2003 45

Internetcash

Teenage market—primary reason for going online

Communicating with friends via email and chat rooms homeworkResearching informationPlaying gamesDownloading music or videos

Prentice Hall, 2003 46

Internetcash (cont.)

Why they do not shop onlineParents will not let them children their (the parents) credit cards onlineThey cannot touch the productsIt is difficult to return items purchased on the WebThey do not have the moneyTransaction may be insecure

Prentice Hall, 2003 47

Internetcash (cont.)

InternetCash offers prepaid stored-value cards sold in amounts of $10, $20, $50, and $100

Must be activated to workGives the user shopping privileges at online stores that carry an InternetCash iconPurchases are automatically deducted from the value of the cardInternetCash’s transactions are anonymous

Prentice Hall, 2003 48

Internetcash (cont.)

InternetCash is facing obstaclesFirst, they have to find retailers willing to sell the cardsMust persuade merchants to accept the card for online purchasesLegal issues

Prentice Hall, 2003 49

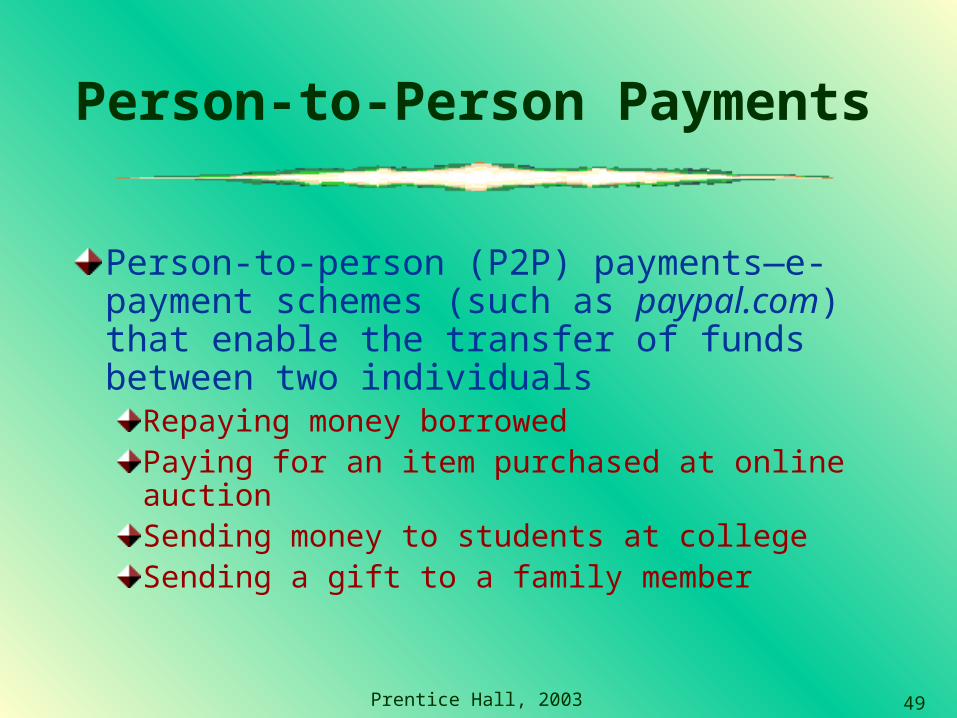

Person-to-Person Payments

Person-to-person (P2P) payments—e-payment schemes (such as paypal.com) that enable the transfer of funds between two individuals

Repaying money borrowedPaying for an item purchased at online auctionSending money to students at collegeSending a gift to a family member

Prentice Hall, 2003 50

Global B2B Payments

Letters of credit (LC)—a written agreement by a bank to pay the seller, on account of the buyer, a sum of money upon presentation of certain documentsTradeCard (tradecard.com)—innovative e-payment method that uses a payment card

Prentice Hall, 2003 51

Electronic Letters of Credit (LC)

Benefits to sellersCredit risk is reducedPayment is highly assuredPolitical/country risk is reduced

Benefits to the buyer

Allows buyer to negotiate for a lower purchase priceBuyer can expand its source of supplyFunds withdrawn from buyer’s account only after the documents have been inspected by the issuing bank

Prentice Hall, 2003 52

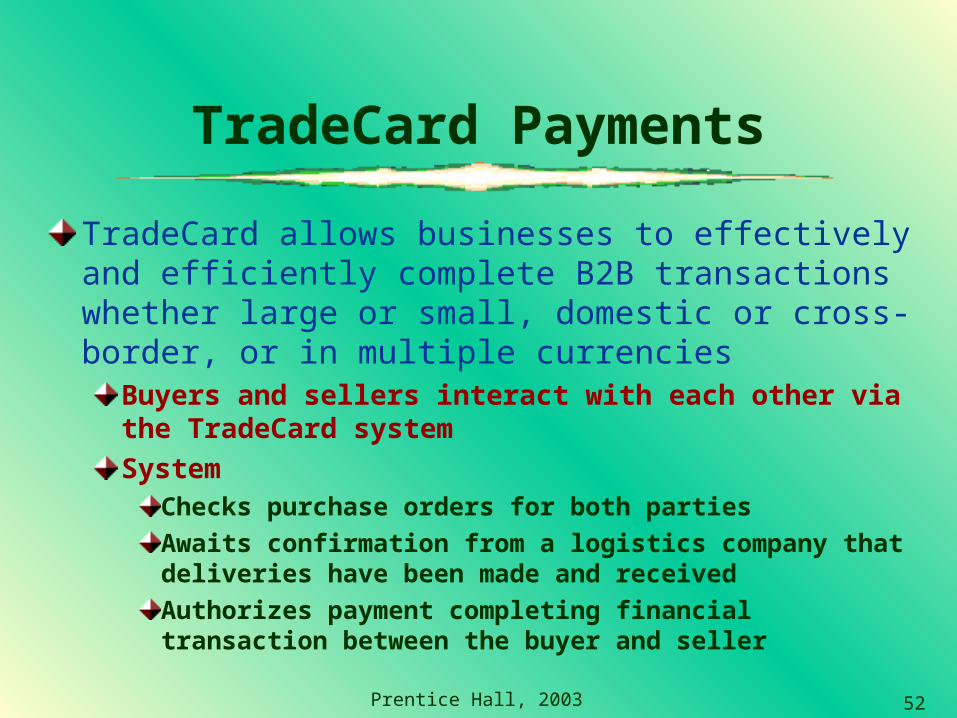

TradeCard Payments

TradeCard allows businesses to effectively and efficiently complete B2B transactions whether large or small, domestic or cross-border, or in multiple currencies

Buyers and sellers interact with each other via the TradeCard systemSystem

Checks purchase orders for both partiesAwaits confirmation from a logistics company that deliveries have been made and receivedAuthorizes payment completing financial transaction between the buyer and seller

Prentice Hall, 2003 53

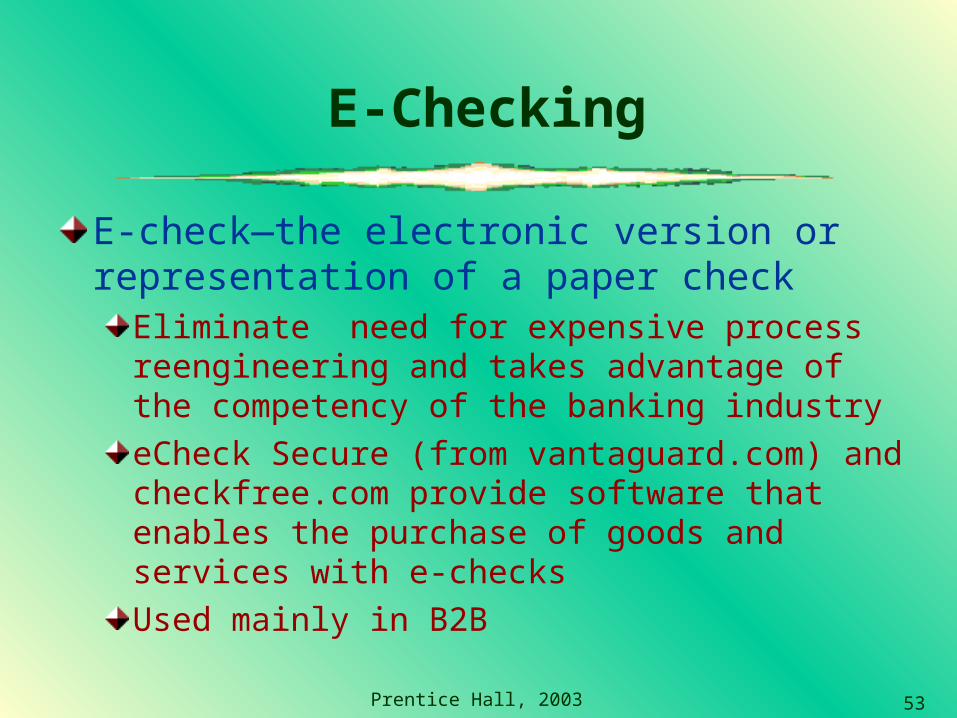

E-Checking

E-check—the electronic version or representation of a paper check

Eliminate need for expensive process reengineering and takes advantage of the competency of the banking industryeCheck Secure (from vantaguard.com) and checkfree.com provide software that enables the purchase of goods and services with e-checksUsed mainly in B2B

Prentice Hall, 2003 54

Order Fulfillment: Overview

Order fulfillment—all the activities needed to provide customers with ordered goods and services, including related customer services

Back-office operations—the activities that support fulfillment of sales, such as accounting and logisticsFront-office operations—the business processes, such as sales and advertising, that are visible to customers

Prentice Hall, 2003 55

Overview of Logistics

Logistics—the operations involved in the efficient and effective flow and storage of goods, services, and related information from point of origin to point of consumptionDelivery of materials or services

Right timeRight placeRight cost

Prentice Hall, 2003 56

Exhibit 10.9Order Fulfillment and Logistics Systems

Prentice Hall, 2003 57

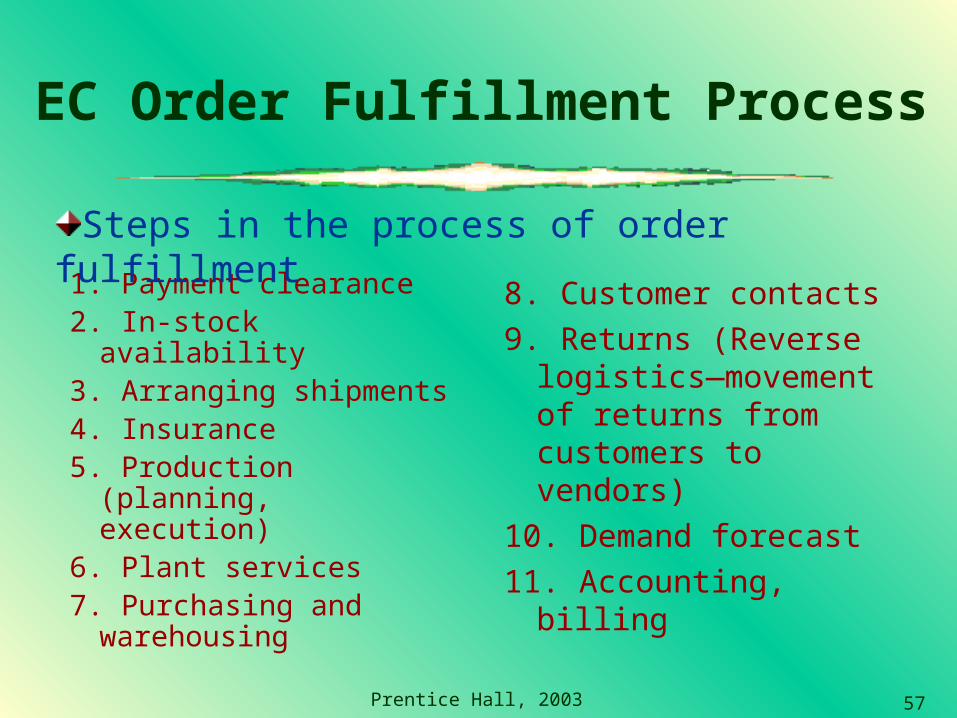

EC Order Fulfillment Process

1. Payment clearance2. In-stock availability3. Arranging shipments4. Insurance 5. Production

(planning, execution)6. Plant services7. Purchasing and

warehousing

8. Customer contacts

9. Returns (Reverse logistics—movement of returns from customers to vendors)

10. Demand forecast

11. Accounting, billing

Steps in the process of order fulfillment

Prentice Hall, 2003 58

Order Fulfillment and the Supply Chain

Order fulfillment and order taking are integral parts of the supply chain. Flows of orders, payments, and materials and parts need to be coordinated among

Company’s internal participantsExternal partners

The principles of supply chain management must be considered in planning and managing the order fulfillment process

Prentice Hall, 2003 59

Problems in Order Fulfillment

Manufacturers, warehouses, and distribution channels were not in sync with the e-tailersHigh inventory costsQuality problems exist due to misunderstandingsShipments of wrong products, materials, and partsHigh cost to expedite operations or shipments

Prentice Hall, 2003 60

Problems in Order Fulfillment (cont.)

UncertaintiesMajor source of uncertainty is demand forecastDemand is influenced by

Consumer behaviorEconomic conditionsCompetitionPricesWeather conditionsTechnological developmentsCustomers’ confidence

Prentice Hall, 2003 61

Problems in Order Fulfillment (cont.)

Demand forecast should be conducted frequently with collaborating business partners along the supply chain in order to correctly gauge demand and make plans to meet itDelivery times depend on factors ranging from machine failures to road conditionsQuality problems of materials and parts (may create production time delays)Labor troubles (such as strikes) can interfere with shipments

Prentice Hall, 2003 62

Problems in Order Fulfillment (cont.)

Order fulfillment problems are created due by lack of coordination and inability or refusal to share informationBullwhip effect—large fluctuations in inventories along the supply chain, resulting from small fluctuations in demand for finished products

Prentice Hall, 2003 63

Solutions to Order Fulfillment Problems

Improvements to order taking processOrder taking can be done on EDI, EDI/Internet, or an extranet, and it may be fully automated.In B2B, orders are generated and transmitted automatically to suppliers when inventory levels fall below certain levels. Result is a fast, inexpensive, and a more accurate process

Web-based ordering using electronic forms expedites the processMakes it more accurate Reduces the processing cost for sellers

Prentice Hall, 2003 64

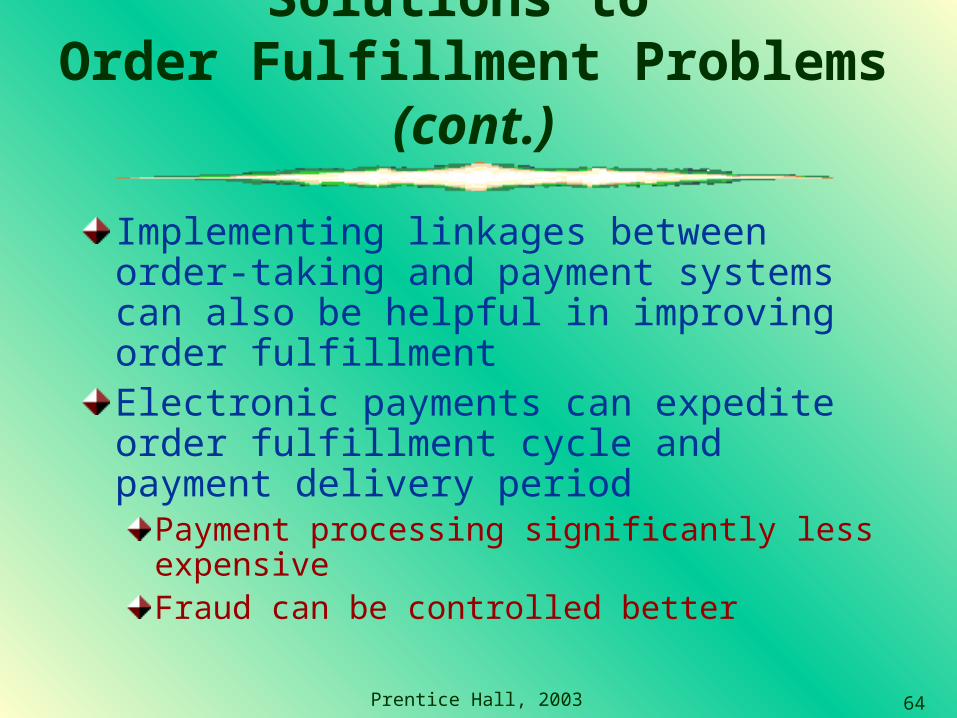

Solutions to Order Fulfillment Problems (cont.)

Implementing linkages between order-taking and payment systems can also be helpful in improving order fulfillmentElectronic payments can expedite order fulfillment cycle and payment delivery period

Payment processing significantly less expensiveFraud can be controlled better

Prentice Hall, 2003 65

Inventory Management Improvements

Inventories can be minimized by:Introducing a make-to-order (pull) production processProviding fast and accurate demand information to suppliers

Inventory management can be improved (inventory levels and administrative expenses) can be minimized by:

Allowing business partners to electronically track and monitor orders and production activitiesHaving no inventory at by digitizing products

Prentice Hall, 2003 66

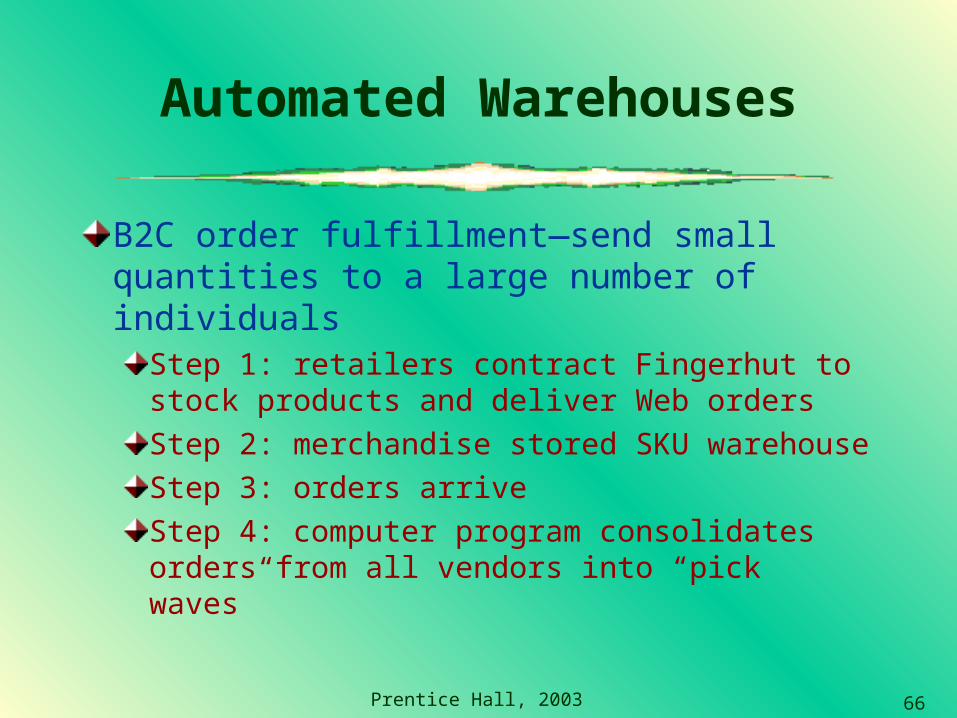

Automated Warehouses

B2C order fulfillment—send small quantities to a large number of individuals

Step 1: retailers contract Fingerhut to stock products and deliver Web ordersStep 2: merchandise stored SKU warehouseStep 3: orders arriveStep 4: computer program consolidates orders from all vendors into “pick waves”

Prentice Hall, 2003 67

Automated Warehouses (cont.)

Step 5: picked items moved by conveyors to packing area; computer configures size and type of packing; types special packing instructionsStep 6: conveyer takes packages to scanning station (weighed)Step 7: scan destination; moved by conveyer to waiting trucksStep 8: full trucks depart for Post Offices

Prentice Hall, 2003 68

Same Day, Even Same Hour Delivery

Role of FedEx and similar shippersFrom a delivery to all-logisticsMany servicesComplete inventory controlPackaging, warehousing, reordering, etc.Tracking services to customers

Prentice Hall, 2003 69

Same Day, Even Same Hour Delivery (cont.)

Supermarket deliveriesTransport of fresh food to people who are in homes only at specific hoursDistribution systems are criticalFresh food may be spoiled

Prentice Hall, 2003 70

Partnering Efforts

Collaborative commerce among members of the supply chain results in:

Shorter cycle timesMinimal delays and work interruptionsLower inventoriesLess administrative costMinimize bullwhip effect problem

Prentice Hall, 2003 71

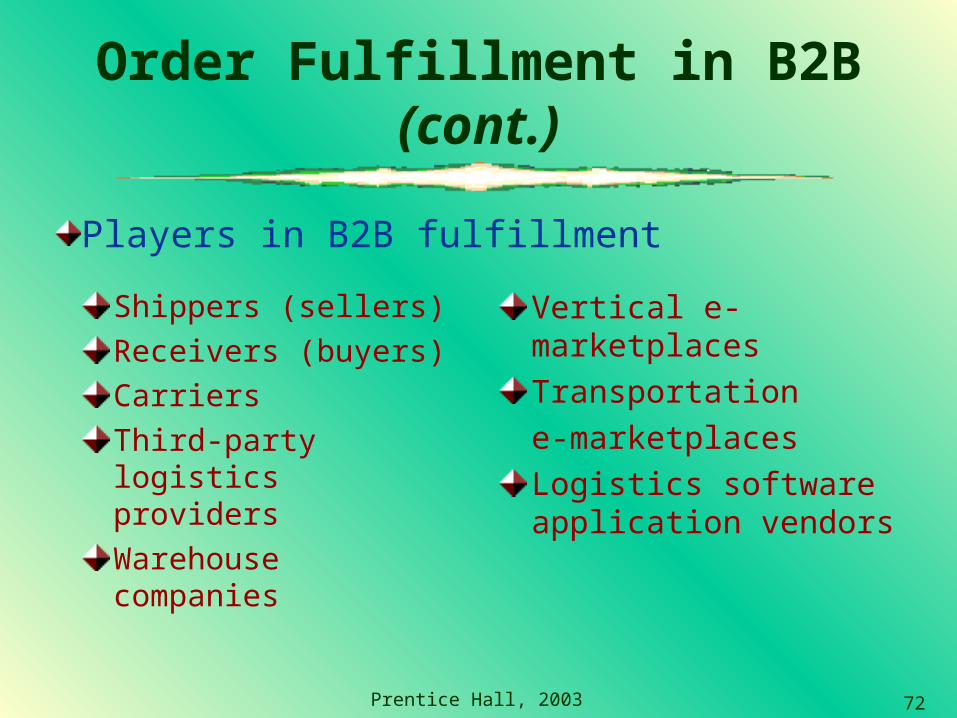

Order Fulfillment in B2B

Using e-marketplaces and exchanges to ease order fulfillment problemsBoth public and private marketplaces

E-procurement system controlled by one large buyer, suppliers adjust their activities and IS to fit the IS of the buyerCompany-centric marketplace can solve several supply chain problemsUse an extranetUse a vertical exchange

Prentice Hall, 2003 72

Order Fulfillment in B2B (cont.)

Shippers (sellers)Receivers (buyers)CarriersThird-party logistics providersWarehouse companies

Vertical e-marketplaces Transportation e-marketplaces Logistics software application vendors

Players in B2B fulfillment

Prentice Hall, 2003 73

Handling Returns

Necessary for maintaining customer trust and loyalty using:

Return item to place it was purchasedSeparate logistics of returns from logistics of deliveryCompletely outsource returnsAllow customer to physically drop returned items at collection stations

Prentice Hall, 2003 74

UPS Provides Broad EC Services

Electronic tracking of packagesElectronic supply chain services for corporate customers by industry including:

Portal page with industry-related informationStatistics

Calculators for computing shipping feesHelp customers manage electronic supply chains

Prentice Hall, 2003 75

The UPS Strategy (cont.)

Improved inventory management, warehousing, and deliveryIntegration with shipping management systemNotify customers by e-mail of:

Delivery statusExpected time of arrival of incoming packages

Prentice Hall, 2003 76

The UPS Strategy (cont.)

Representative tools7 transportation and delivery applications

Track packagesAnalyze shipping historyCalculate exact time-in-transit

Downloadable toolsProof of deliveryOptimal routing features

Delivery of digital documentsWireless access to UPS system

Prentice Hall, 2003 77

Managerial Issues

What B2C payment methods should we use?What B2B payment methods should we use?Should we use an in-house payment mechanism or outsource it?How secure are e-payments?

Have we planned for order fulfillment?How should we handle returns?Do we want alliances in order fulfillment?What EC logistics applications would be useful?

Prentice Hall, 2003 78

Summary

Crucial factors determining the success of an e-payment methodKey elements in securing an e-paymentOnline credit card players and processesThe uses and benefits of purchasing cardsCategories and potential uses of smart cardsOnline alternatives to credit card payments

Prentice Hall, 2003 79

Summary (cont.)

E-check processes and involved partiesThe role of order fulfillment and back-office operations in ECThe order fulfillment processProblems in order fulfillmentSolutions to order fulfillment problems