Preliminary Results - enterprise-inns Group Website...Preliminary Results 2008 Financial highlights...

33

Preliminary Results 2008 Preliminary Results 30 September 2008 VISIT OUR WEBSITE www.enterpriseinns.com

Transcript of Preliminary Results - enterprise-inns Group Website...Preliminary Results 2008 Financial highlights...

Preliminary Results 2008

Preliminary Results

30 September 2008

VISIT OUR WEBSITE www.enterpriseinns.com

Preliminary Results 2008

Financial highlights 12 months to 30 September 2008

EBITDA reduced by 3% to £512m

Profit before tax and exceptional items fell by 13% to £263m

Adjusted earnings per share down just 1% to 39.2 pence

Full year dividend up 4% to 16.2 pence

Flexible financing structure in place

Preliminary Results 2008

EBITDA EBITDA of £512m

12 months to

30 September Variance

£m 2008 Pro forma

2007 %

Revenue 880 918 (4)%

Cost of sales (336) (358) 6%

Gross profit 544 560 (3)%

Administrative expenses (32) (34) 6%

EBITDA 512 526 (3)%

Preliminary Results 2008

Profit & loss account Adjusted EPS down just 1% 12 Months to

30 September

£m 2008 2007

Revenue 880 921

EBITDA 512 528

Depreciation (8) (7)

Interest (241) (220)

PBT (pre exceptional items) 263 301

Taxation (68) (85)

Profit after tax (pre exceptional items) 195 216

Adjusted EPS (p) 39.2 39.6

Weighted average no. of shares (m) 497.4 545.0

Dividend per share (p) 16.2 15.6

Preliminary Results 2008

Gross margin analysis Increased margin on beer sales

£m Beer, cider &

fabs

Licensee discounts Wines, spirits & minerals

Rent Machines & other Total

Contractual Special 2007/08

Turnover 618 (44) (6) 32 258 22 880

Cost of sales (305) - - (25) (6) - (336)

Gross profit 313 (44) (6) 7 252 22 544

Gross margin % 50.6% 61.8%

2006/07 – Proforma

Turnover 651 (50) (1) 33 260 25 918

Cost of sales (325) - (26) (7) - (358)

Gross profit 326 (50) (1) 7 253 25 560

Gross margin % 50.1% 61.0%

Preliminary Results 2008

Cash flow statement Free cash inflow of £62m

12 months to

30 September

£m 2008 2007

Operating profit 502 521

Operating cash inflow 536 523

Interest (246) (220)

Tax (77) (71)

Free cash flow pre investment 213 232

Dividends (81) (79)

Pub capital expenditure (68) (75)

Other capital expenditure (2) (3)

Free cash inflow 62 75

Preliminary Results 2008

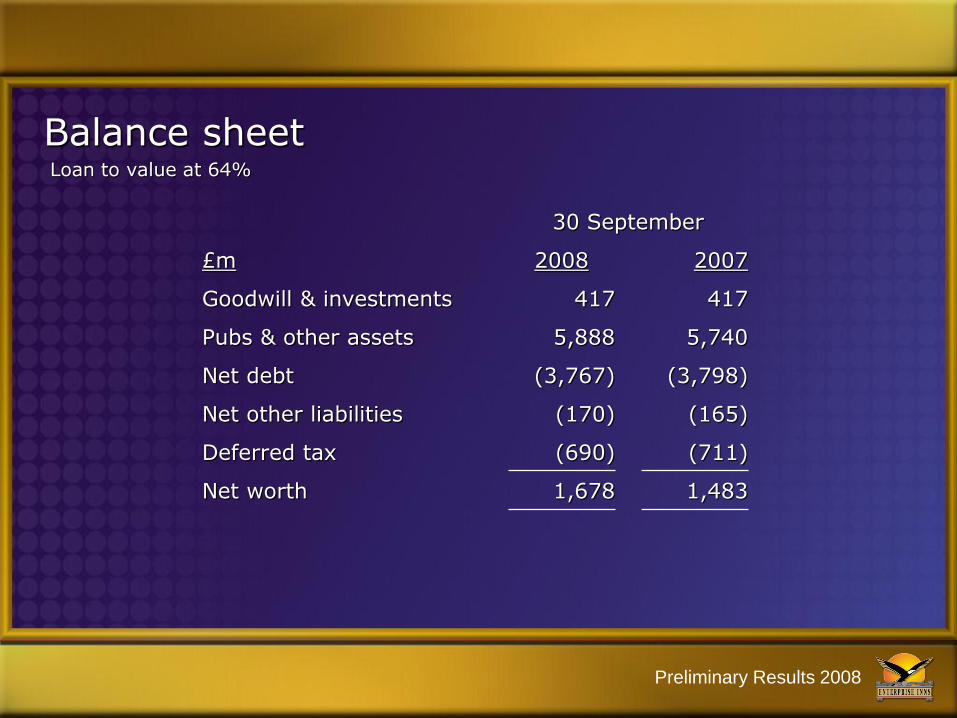

Balance sheet Loan to value at 64%

30 September

£m 2008 2007

Goodwill & investments 417 417

Pubs & other assets 5,888 5,740

Net debt (3,767) (3,798)

Net other liabilities (170) (165)

Deferred tax (690) (711)

Net worth 1,678 1,483

Preliminary Results 2008

Debt structure Underlying net debt reduced by £12m

As at 30 September

£m 2008 2007

Bank debt (1,031) (1,035)

Corporate bonds (1,185) (1,185)

Securitised bonds (1,586) (1,586)

Gross debt (3,802) (3,806)

Cash 98 90

Underlying net debt (3,704) (3,716)

Other (including mark to market of swaps) (63) (82)

Net debt (3,767) (3,798)

Preliminary Results 2008

Weighted average life & cost of debt 89% fixed at 6.5% for an average of 10 years

As at 30 Sept 2008

Facility Weighted

average life

Weighted

average cost

Bank debt 3 yrs 6.2%

Corporate bonds 14 yrs 6.5%

Securitised bonds 12 yrs 6.4%

Total 10 yrs 6.5%

Preliminary Results 2008

Three pronged financing Flexible debt structure

Bank debt Corporate bonds Securitised bonds

£m

Preliminary Results 2008

Three pronged financing Loan to value at 64%

£m

Corporate bonds Bank debt Securitised bonds

Gross

debt

Pub

value

Gross

debt

Pub

value

Gross

debt

Pub

value

Preliminary Results 2008

ETI pub value headroom Pub value headroom of 17%

Headroom

£m

Bank debt

Pub value

secured

against debt

Corporate bonds Total ETI

Gross

debt

Gross

debt

Gross

debt

• No pub value covenant in the securitised bonds

Preliminary Results 2008

Bank debt Headroom of £94m

£m

As at 30 Sept 2008 As at 30 Sept 2007

Facility Drawn Headroom Facility Drawn Headroom

Club facility

1,000 1,000 - 1,000 1,000 -

Committed facility

100 31 69 - - -

Uncommitted facility

- -

- 100 35 65

Total

1,100 1,031 69 1,100 1,035 65

Overdraft*

25 - 25 25 9 16

* Additional borrowing of a further £100m allowed under the bank facility

Preliminary Results 2008

Bank debt Comfortable covenant headroom

Annualised as at

Covenant 30 Sept 2008

31 March 2008

30 Sept 2007

Net debt : EBITDA* 6.5x 5.80x 5.71x 5.74x

Interest cover 2.0x 2.62x 2.75x 3.09x

First charge assets ratio 1.0x 1.44x 1.43x 1.34x

Total property assets ratio 1.5x 2.00x 1.92x 1.82x

* EBITDA includes dividends from Unique of circa £70m per annum

Covenants tested semi annually on a MAT basis

Preliminary Results 2008

Corporate bonds Flexibility to match actual leverage to covenant

At 30 September 2008 Asset cover Income cover

Bond Covenant Actual Covenant Actual

1. £60m due 2014 1.50x 1.58x 1.50x 2.39x

2. £600m due 2018 1.67x 1.80x 2.00x 2.00x

3. £125m due 2021 1.50x 1.75x 1.50x 1.85x

4. £125m due 2025 1.50x 1.73x 1.50x 1.84x

5. £275m due 2031 1.67x 1.70x 1.50x 1.90x

• Post substitution of pubs

• Pubs withdrawn or introduced as necessary to ensure covenant compliance

• Covenants tested annually on a MAT basis

Preliminary Results 2008

Securitised bonds £115m of debt prepaid

Next mandatory repayments: June 2010 £2m, Sept 2010 £7m.

£m

A2N

201m

A4

£535m

A3

£435m

Preliminary Results 2008

Securitised bonds Significant liquidity and headroom on covenants

Covenant Sept 2008 March 2008 Sept 2007

Debt Service Cover Ratio (DSCR) 1.10x 2.06x 2.15x 2.14x

Net worth £m 150 1,448 1,401 1,385

Covenants

Liquidity

Liquidity facility - £190m

Cash balance of £89m at 30 September 2008

• No pub value covenant

• DSCR cash trap test at 1.5x

• Covenants tested quarterly on a MAT basis

Preliminary Results 2008

Debt reduction programme Significant debt reduction potential

£m 2008 Actual

2009 Scoping

Comments

From To

Free cash flow pre investment 213 150 200 For illustrative purposes, not a forecast

Capital on existing estate (68) (50) (40) Normal capital expenditure of c£45m

Acquisition of pubs (48) (5) (5) Acquisitions team redeployed to sell non viable pubs

Disposals of pubs 30 50 100

Potential cash generation 127 145 255

Preliminary Results 2008

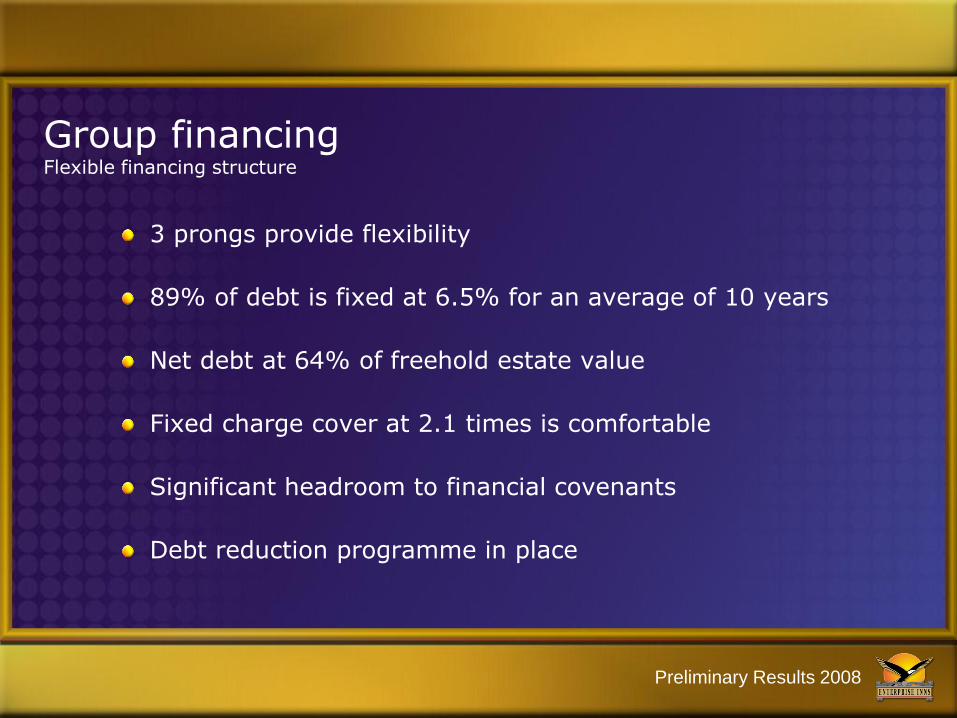

Group financing Flexible financing structure

3 prongs provide flexibility

89% of debt is fixed at 6.5% for an average of 10 years

Net debt at 64% of freehold estate value

Fixed charge cover at 2.1 times is comfortable

Significant headroom to financial covenants

Debt reduction programme in place

Preliminary Results 2008

Operating highlights 12 months to 30 September 2008

Group EBITDA of £512m, operating cash inflow £536m

Solid performance in a tough market

Increased support for licensees through discounts and concessions

Average EBITDA per pub up 2% in 82% of estate let on substantive agreements

£68m capital expenditure invested into the estate

58 high quality acquisitions for £48m

Surplus land, underperforming & HAUV pubs sold for £30m

Preliminary Results 2008

Adjusted earnings per share Resilient performance in a tough market

% increase in adj EPS 33% 17% 16% (1%)

Dividend 9.0p 13.5p 15.6p 16.2p

% increase in dividend 50% 50% 16% 3.8%

Dividend cover (adj EPS) 3.2x 2.5x 2.5x 2.4x

Preliminary Results 2008

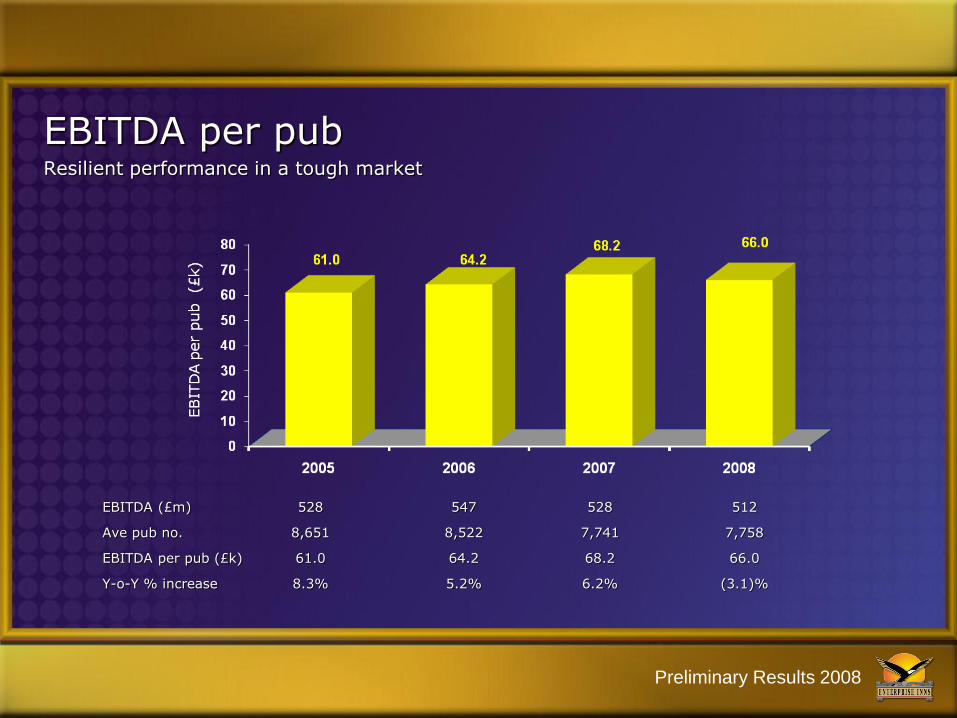

EBITDA (£m) 528 547 528 512

Ave pub no. 8,651 8,522 7,741 7,758

EBITDA per pub (£k) 61.0 64.2 68.2 66.0

Y-o-Y % increase 8.3% 5.2% 6.2% (3.1)%

EBITDA per pub Resilient performance in a tough market

Preliminary Results 2008

Top quality pub estate Enterprise secured the best available pub assets

Original pubs

acquired

Pubs at Sept 08

% retained

Historic* cost (£m)

Current value (£m)

Income % of

historic cost

Income % of

current value

Pre float 490 174 36% 34 93 29% 10%

Other 2,267 1,150 51% 436 745 17% 10%

2001 Managed pubs (Whitbread and S&N) 840 685 82% 467 631 13% 10%

2002 Laurel (Whitbread leases) 1,860 1,634 88% 882 1,263 13% 9%

2004 Unique (Grand Met and M&B) 3,955 3,498 88% 2,165 2,672 12% 10%

Individual acquisitions 726 622 86% 363 458 10% 8%

Scotland 141 - 0%

TOTAL 10,279 7,763 76% 4,347 5,861 13% 10%

• Historic cost includes post acquisition capital expenditure

Preliminary Results 2008

Pub estate valuation No of pubs

£m £m Value/pub

£k

Pub value as at 30 Sept 07 7,763 5,713 736

Capital investment & churn 76

Impact of year end estate valuation:

Increase/no change in value 5,283 318

Reduction in value 2,480 (246)

Revaluation increase 72

Pub value as at 30 Sept 08 7,763 5,861 755

Pub estate valuation: Financial statements:

Increase in revaluation reserve (Balance Sheet) 123

Pubs valued below historic cost (P&L exceptional item) (51)

Revaluation increase 72

Preliminary Results 2008

Capital investment Consistent investment targeting 12% return

12 months to 30 Sept 2008

Investment

spend

Total

Investment*

(£m)

No of

projects

£200k + 22 69

£100-£200k 16 115

£50-£100k 13 186

£10-£50k 17 734

£5-£10k 7 483

Total 75 1,587

Projects

£m No.

Sept 05 49 1,093

Sept 06 54 1,390

Sept 07 75 1,594

Sept 08 68 1,587

* Value of projects completed £75m, cash paid out £68m.

Preliminary Results 2008

Acquisitions & disposals Effective estate churn

£m

58 acquisitions (48)

Disposals (inc land) 30

Net cash outflow (18)

Acquisitions Disposals

No. £m No. £m

FY05 21 14 158 47

FY06 95 80 107 48

FY07 108 91 17 13

FY08 58 48 58 30

• FY06 excludes sale of 769 pubs to Admiral Taverns for £318m

• FY07 excludes sale of 137 pubs to Retail & Licensed Properties Ltd for £115m

Preliminary Results 2008

Estimate of potential licensee profitability

£’000 2008 % of T/O

2007 % of T/O

% change

Turnover Wet 236 232

Food 65 60

Other 13 14

Total turnover 314 306 3%

Gross margin 172 55% 168 55%

Overheads (103) 33% (95) 31%

Pre rent profit 69 22% 73 24% (5)%

Rent (34) (36)

Cash profit 35 37 (5)%

Domestic accommodation 10 10

Post rent licensee profit 45 14% 47 15% (4)%

Source: Estates Review – completed September 2008

Preliminary Results 2008

Estimate of potential licensee profitability

£’000

All Bands £15-30k £30-45k £45-60k £60-75k Over £75k

Turnover 314 201 269 353 443 607

Gross margin 172 101 142 197 255 366

Overheads (103) (66) (86) (115) (147) (211)

Pre rent profit 69 35 56 82 108 155

Rent (34) (16) (28) (41) (54) (76)

Cash profit 35 19 28 41 54 79

Domestic accommodation 10 8 9 11 12 16

Post rent licensee profit 45 27 37 52 66 95

No of pubs* 1,502 3,130 1,767 815 483

Source: Estates Review – completed September 2008

* Excludes 66 pubs, the majority of which are closed pending disposal

Preliminary Results 2008

Estimate of actual licensee profitability

£’000 2008

Estimated Actual

Memo: 2008 FMT Potential

2008 Actual assumptions

Turnover 292 314 Wet turnover is based on actual sales and food income broadly steady at c20% of sales.

Gross margin 162 172

Overheads (100) (103) Fixed costs in line with FMT potential with moderate savings in variable costs

Pre rent profit 62 69

Rent (31) (34) Actual annual rent at September 08

Cash profit 31 35

Domestic accommodation 10 10

Post rent licensee profit 41 45

Source: Estates Review – completed September 2008

Preliminary Results 2008

Licensee profitability What’s it really like out there?

7,161 enquiries converted to 1,566 formal applications

577 fully screened applicants on the database

80% of estate let on long term assignable leases

483 lease assignments, average premium £63k (£79k including tenants fixtures

and fittings)

Rent concessions increased to 2.1% of rent roll at the year end

915 rent reviews were completed at an average annual increase of 2.2%

Overdue balances at less than 1% of turnover, bad debts low at 0.1% of

turnover

Preliminary Results 2008

Plan for 2008-09

Maximise pub estate potential

Support licensees as appropriate

Minimal acquisitions

Return to normal levels of capital investment

Accelerate the disposal programme

Manage cash flows and debt profile

Preliminary Results 2008

Summary

1% decline in adjusted earnings per share

Best quality pub estate

Tenanted model remains robust and fair

Strong cash generation

Debt reduction programme in place

Well placed to benefit from recovery