Preliminary Results 2006 30 November 2006. 2 European specialist holiday group European specialist...

32

Preliminary Results Preliminary Results 2006 2006 30 November 2006

-

date post

19-Dec-2015 -

Category

Documents

-

view

215 -

download

0

Transcript of Preliminary Results 2006 30 November 2006. 2 European specialist holiday group European specialist...

Preliminary Results Preliminary Results 20062006

30 November 2006

2 European specialist holiday groupEuropean specialist holiday group

Carl Michel (Group Chief Executive)- Introduction

Bob Baddeley (Group Finance Director)- Financial Review

Carl Michel (Group Chief Executive) - Divisional Review- Strategy- Opportunities- Summary

Q&A

Holidaybreak plcToday’s presentation

3 European specialist holiday groupEuropean specialist holiday group

Holidaybreak plcIntroduction

Good results demonstrating another robust performance

Market leaders with industry-leading margins Continue to search out acquisitions that will

add to our product and market positions Current trading is in line with our expectations

- confident of achieving another satisfactory performance

2007 a year of investment

4 European specialist holiday groupEuropean specialist holiday group

BOB BADDELEYGROUP FINANCE DIRECTOR

Results for year ended 30 September 2006

Holidaybreak plc

5 European specialist holiday groupEuropean specialist holiday group

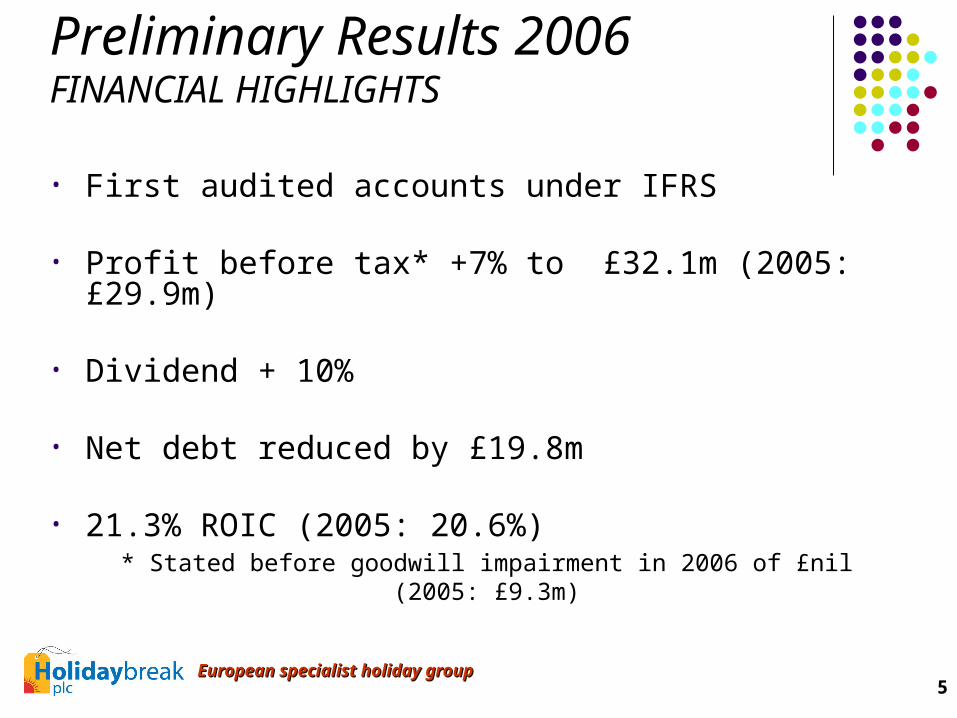

Preliminary Results 2006FINANCIAL HIGHLIGHTS

• First audited accounts under IFRS

• Profit before tax* +7% to £32.1m (2005: £29.9m)

• Dividend + 10%

• Net debt reduced by £19.8m

• 21.3% ROIC (2005: 20.6%)* Stated before goodwill impairment in 2006 of £nil (2005:

£9.3m)

6 European specialist holiday groupEuropean specialist holiday group

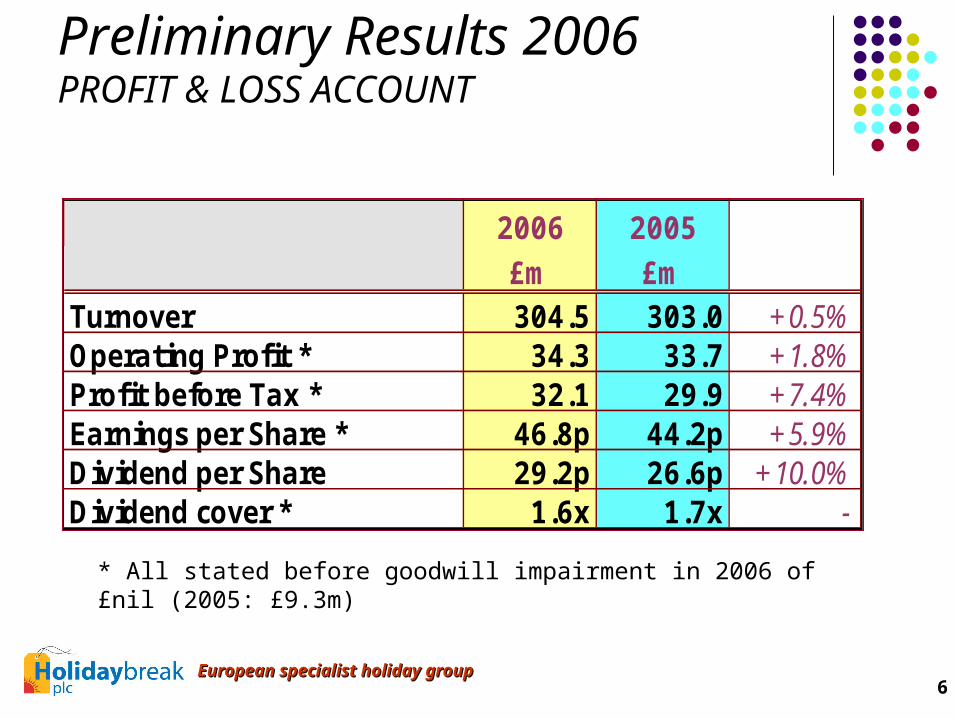

Preliminary Results 2006PROFIT & LOSS ACCOUNT

* All stated before goodwill impairment in 2006 of £nil (2005: £9.3m)

2006 2005£m £m

Turnover 304.5 303.0 +0.5%Operating Profit * 34.3 33.7 +1.8%Profit before Tax * 32.1 29.9 +7.4%Earnings per Share * 46.8p 44.2p +5.9%Dividend per Share 29.2p 26.6p +10.0%Dividend cover * 1.6x 1.7x -

7 European specialist holiday groupEuropean specialist holiday group

Preliminary Results 2006DIVISIONAL RESULTS

Hotel Breaks Adventure Camping Group

Travel

£m £m £m £m

Turnover 2006 122.7 76.3 105.5 304.5v 2005 -3.1% +22.0% -7.3% +0.5%

PBIT* 2006 16.2 5.6 12.5 34.3v 2005 -3.6% +47.4% -3.8% +1.8%

2. * Stated before goodwill impairment in 2006 of £nil (2005: £9.3m)

Note:1. * Includes £0.3m non-recurring costs in relation to the Camping

disposal and two potential acquisitions

8 European specialist holiday groupEuropean specialist holiday group

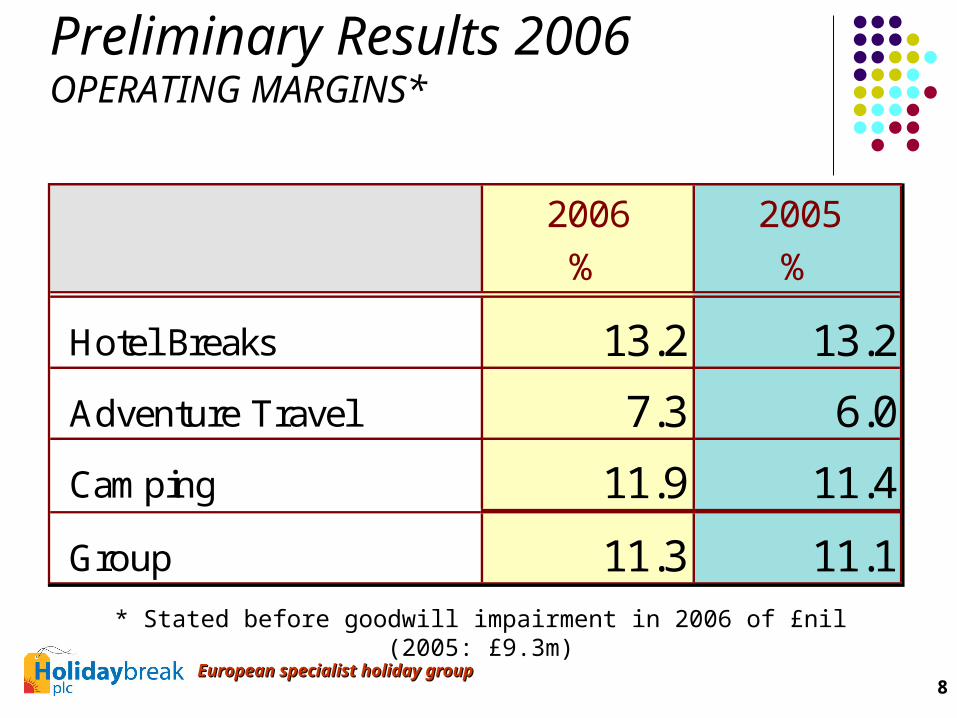

2006 2005% %

Hotel Breaks 13.2 13.2

Adventure Travel 7.3 6.0

Camping 11.9 11.4

Group 11.3 11.1

Preliminary Results 2006OPERATING MARGINS*

* Stated before goodwill impairment in 2006 of £nil (2005: £9.3m)

9 European specialist holiday groupEuropean specialist holiday group

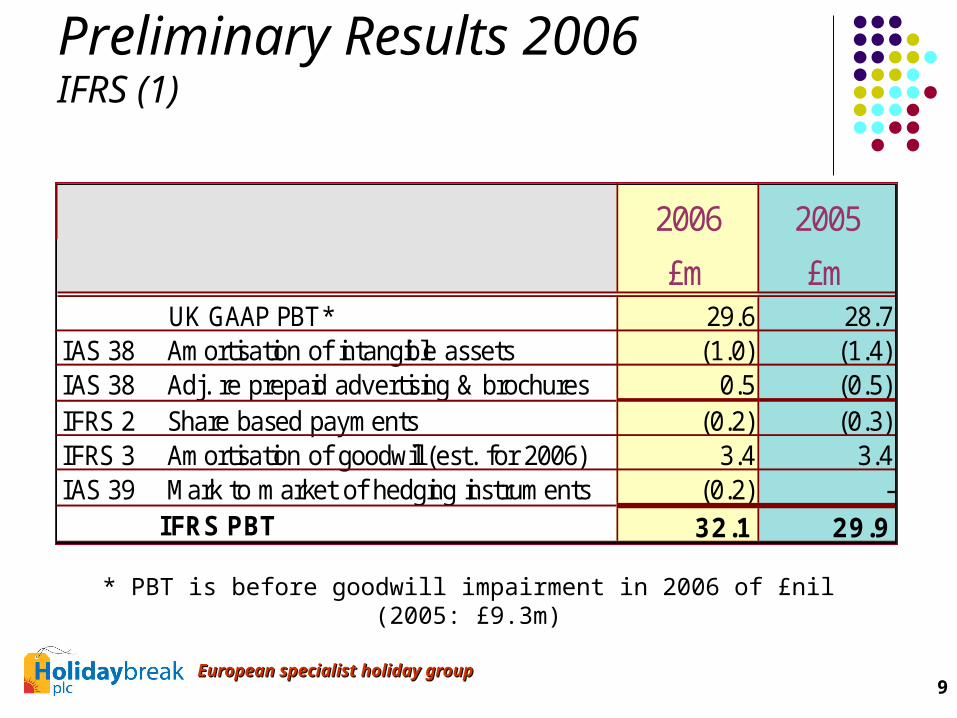

Preliminary Results 2006IFRS (1)

2006 2005

£m £m UK GAAP PBT* 29.6 28.7IAS 38 Amortisation of intangible assets (1.0) (1.4)IAS 38 Adj. re prepaid advertising & brochures 0.5 (0.5)IFRS 2 Share based payments (0.2) (0.3)IFRS 3 Amortisation of goodwill (est. for 2006) 3.4 3.4IAS 39 Mark to market of hedging instruments (0.2) - IFRS PBT 32.1 29.9

* PBT is before goodwill impairment in 2006 of £nil (2005: £9.3m)

10 European specialist holiday groupEuropean specialist holiday group

Preliminary Results 2006IFRS (2)

* PBT is before goodwill impairment of £9.3m

Restatement of IFRS results for 2005 previously announced:

£mPBT* as reported 30.4

Adj. re Djoser 2005 marketing spend (0.5)

Restated 29.9

Note: under IFRS, Djoser 2005 results now include 9 months sales but 12 months marketing and

brochure costs

11 European specialist holiday groupEuropean specialist holiday group

• Net debt reduced by £19.8m, despite

acquisition of carpe diem and TravelWorks

• Interest cover (pre-goodwill impairment)

15.7 times (2005 : 7.7 times)

• Average interest rate 5.5% inclusive of

margin

Preliminary Results 2006CASH FLOW

12 European specialist holiday groupEuropean specialist holiday group

Preliminary Results 2006FREE CASH FLOW – by Division

2006 2005£m £m

Hotel Breaks 18.4 14.9Adventure Travel 3.1 12.7Camping 22.7 22.0Interest & tax (9.1) (11.4)Group 35.1 38.2

Free cash flow = Operating cash flow after net capex, interest & tax

13 European specialist holiday groupEuropean specialist holiday group

• Net debt reduced to £3.1m- £4.0m (net) spent on acquisitions- Gearing 5% (2005: 48%)- Average debt over year £25.3m (2005: £42.6m)

• Acquired intangibles £9.7m (2005 : £8.3m)- Annual amortisation under IAS 38: £1.0m

• Bank facilities £140m- Minimum headroom £56m

Holidaybreak plcBALANCE SHEET

14 European specialist holiday groupEuropean specialist holiday group

• 2006 capex (net of disposals) of £4.6m (2005: £2.4m)

• Mobile-homes capacity reduced in 2006 by 16% to 8,463- further 2% reduction in 2007

• 2007 Camping capex to be at historic levels – c.900 mobile-homes to be replaced- anticipated spend £9.5m

• 2007 Group capex increase to c.£16.0m- incl. £4.0m on IT

Preliminary Results 2006CAPITAL EXPENDITURE & DISPOSALS

15 European specialist holiday groupEuropean specialist holiday group

• Low fixed costs in Hotel Breaks and Adventure Travel

• Double digit margins – well above travel industry norms

• All divisions cash generative- But capex to be substantially higher in 2007

• Healthy return on invested capital

Holidaybreak plcFINANCIAL SUMMARY

16 European specialist holiday groupEuropean specialist holiday group

CARL MICHELGROUP CHIEF EXECUTIVE

Divisional ReviewStrategy

OpportunitiesSummary

Holidaybreak plc

17 European specialist holiday groupEuropean specialist holiday group

Divisional operating profit down 4% at £16.2m- London bombings in July 2005 affected market until Spring

- Bookings were further impacted by the FIFA World Cup in June and the unusually hot weather in July.

UK market now recovering well – led by resurgence of London and theatre market

Significant increase in range of hotels outside UK- 1,600 hotels (Sept 2005) - 2,400 (Sept 2006)- target of 3,200 (end year)

Outlook is good, with current sales growth of about +8%

Holidaybreak plc Hotel Breaks

18 European specialist holiday groupEuropean specialist holiday group

2006 divisional operating profit £5.6m (£3.8m)

Underlying demand still good- Middle East (16% of turnover) down as a result of

Lebanon war, but not material

Emphasis on expanding range of tours (e.g. 70 new tours added in UK)

Current trading showing +5% sales growth

Holidaybreak plc Adventure Travel

19 European specialist holiday groupEuropean specialist holiday group

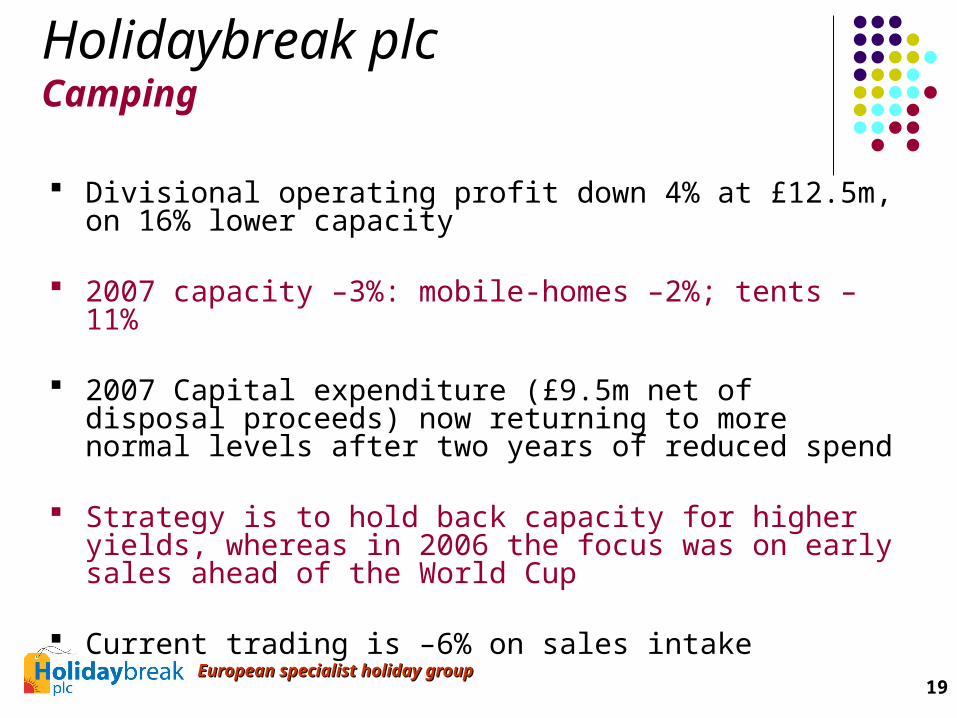

Divisional operating profit down 4% at £12.5m, on 16% lower capacity

2007 capacity –3%: mobile-homes –2%; tents –11%

2007 Capital expenditure (£9.5m net of disposal proceeds) now returning to more normal levels after two years of reduced spend

Strategy is to hold back capacity for higher yields, whereas in 2006 the focus was on early sales ahead of the World Cup

Current trading is –6% on sales intake

Holidaybreak plc Camping

20 European specialist holiday groupEuropean specialist holiday group

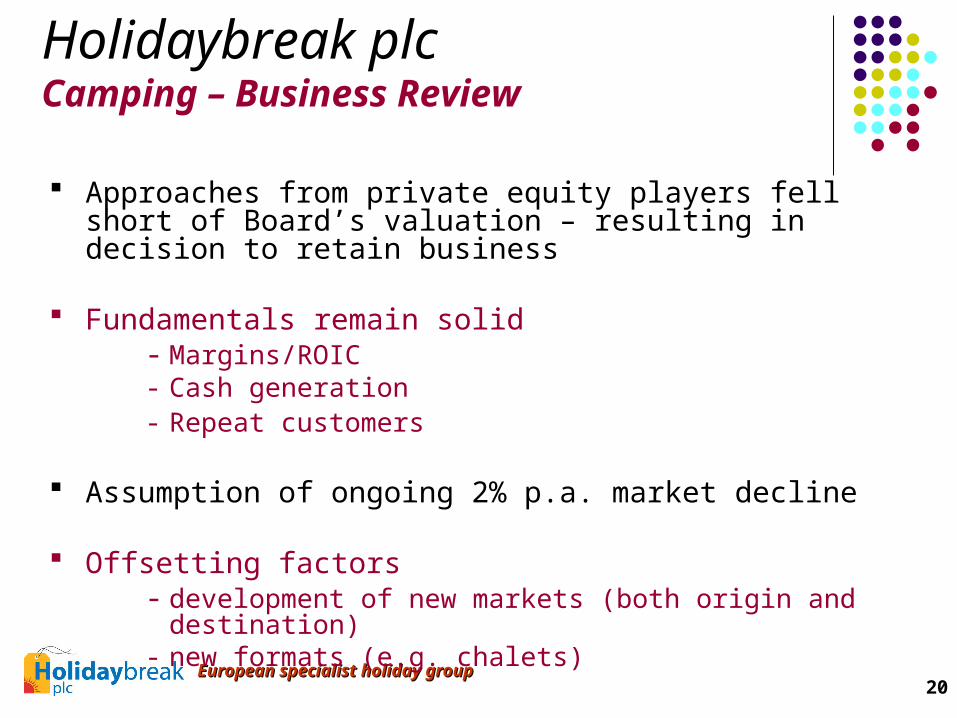

Approaches from private equity players fell short of Board’s valuation – resulting in decision to retain business

Fundamentals remain solid- Margins/ROIC- Cash generation- Repeat customers

Assumption of ongoing 2% p.a. market decline

Offsetting factors - development of new markets (both origin and

destination) - new formats (e.g. chalets)

Holidaybreak plc Camping – Business Review

21 European specialist holiday groupEuropean specialist holiday group

1. Build on core competences: leverage synergies

2. Develop a multi-path approach: avoid being ‘boxed in’

3. Pursue sustainable faster growth - Secure strong positions in higher margin businesses

4. Diversify sales mix

Holidaybreak plc Strategy

22 European specialist holiday groupEuropean specialist holiday group

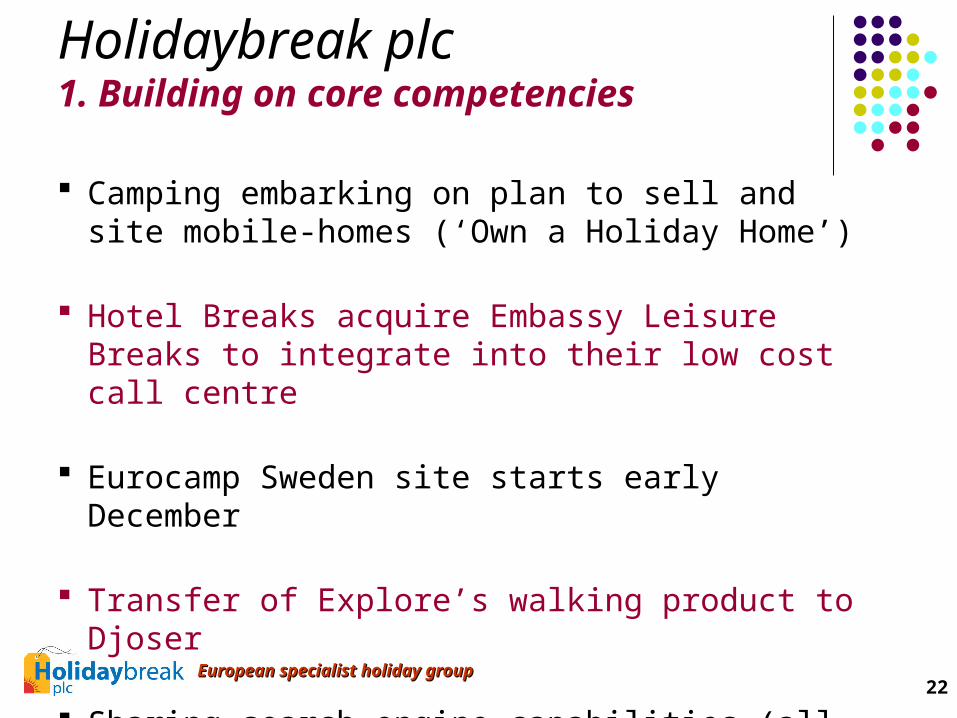

Camping embarking on plan to sell and site mobile-homes (‘Own a Holiday Home’)

Hotel Breaks acquire Embassy Leisure Breaks to integrate into their low cost call centre

Eurocamp Sweden site starts early December

Transfer of Explore’s walking product to Djoser

Sharing search engine capabilities (all divisions)

Holidaybreak plc1. Building on core competencies

23 European specialist holiday groupEuropean specialist holiday group

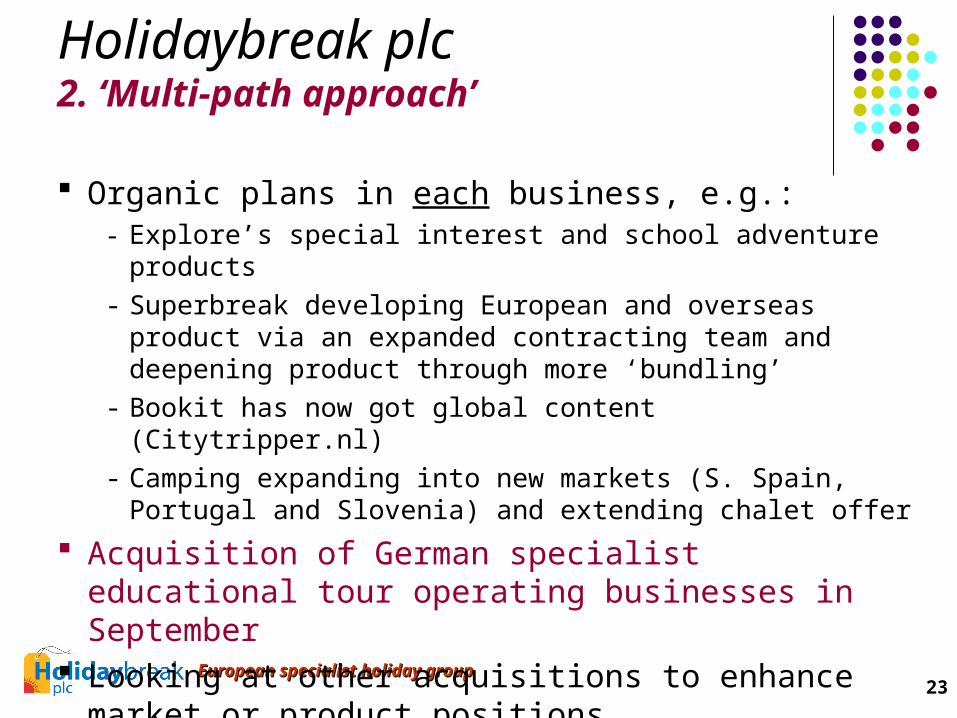

Organic plans in each business, e.g.:- Explore’s special interest and school adventure products- Superbreak developing European and overseas product

via an expanded contracting team and deepening product through more ‘bundling’

- Bookit has now got global content (Citytripper.nl) - Camping expanding into new markets (S. Spain, Portugal

and Slovenia) and extending chalet offer

Acquisition of German specialist educational tour operating businesses in September

Looking at other acquisitions to enhance market or product positions

Holidaybreak plc2. ‘Multi-path approach’

24 European specialist holiday groupEuropean specialist holiday group

carpe diem and TravelWorks are leading players in specialist educational travel in Germany- Net margins of 10% with a clearly differentiated

offer- Historical sales growth of 10-15% p.a.

Look to acquire other businesses with strong positions and good margins

Holidaybreak plc3. Sustainable faster growth

25 European specialist holiday groupEuropean specialist holiday group

Non-UK was 27% of business in 2005/06 (compared to 18% in 2003/04) and is forecast to grow further

Some sectors (on-line hotels) expected to experience much faster growth in continental Europe than in the UK- Growth both organically and through selective acquisitions

Adventure Travel has potential to develop global customer base- We look to grow this division by acquisition

Holidaybreak plc4. Diversify sales mix

26 European specialist holiday groupEuropean specialist holiday group

UK: consolidate pre-eminent position in London and focus on more ‘packaged breaks’

More resource added to improve online functionality and web content

Increased hotel contracting team to develop international offering

Extra investment of up to £2m p.a.

Holidaybreak plcOpportunities – Hotel Breaks

27 European specialist holiday groupEuropean specialist holiday group

Sector remains fragmented

Socio-economic trends indicate robust growth

Development focus:- new customer markets (Europe and English-

speaking world)- new customer groups (e.g. schools, individuals) - new products (e.g. special interest, more extreme

adventure)

Holidaybreak plcOpportunities – Adventure Travel

28 European specialist holiday groupEuropean specialist holiday group

Offering mobile-homes for residential use in France - exploit buying power- leverage customer contacts in a fragmented market

Continue to use marketing and online to appeal to couples and pre-school families

New locations in Southern Spain, Portugal and Slovenia

Holidaybreak plcOpportunities - Camping

29 European specialist holiday groupEuropean specialist holiday group

Strict criteria

Pipeline of potential targets – mostly in the Adventure/Activity sector

Resourced to investigate opportunities at an earlier stage (before a competitive auction)

Resources to fund large deal

Developing additional specialist tour operating businesses as ‘fourth division’ a possibility

Holidaybreak plcOpportunities – Acquisitions

30 European specialist holiday groupEuropean specialist holiday group

Holidaybreak plcOpportunities – IT / web investment

Camping investing £1m in new reservation system

New websites for Keycamp trade (with XML links), Eurocamp Independent, Easycamp and Eurocamp Sweden

Bookit outsourcing development work to India- Launched Citytripper.nl

Superbreak: new web resource and content management system- New website with ‘mash ups’ (e.g. Google maps, customer

feedback) due mid 2007

Explore redesigning website and also developing Web 2.0 (social content)

31 European specialist holiday groupEuropean specialist holiday group

Focus on specialization - Reduces risk of disintermediation and thus margin pressure- We will continue to look to increase the ‘value added’ in what we do for our customers (consumer and trade)

Driving customer/trade loyalty- High repeat business (30%)- Our web strategy and loyalty rewards support these behaviours, but excellent customer service has to be the driving force

Creating common platforms - we are now looking at how we can create the necessary shared systems/capabilities to enable potential acquisitions to prosper

Seeking mutually beneficial commercial relationships - we encourage both sales synergies (e.g. Bookit selling camping) and cost benefits (e.g. single suppliers) between and within the divisions, as well as transfer of knowledge

Holidaybreak plcOpportunities - Group

32 European specialist holiday groupEuropean specialist holiday group

Holidaybreak plcSUMMARY Strategy is well on track – with a mix of organic and

acquisition led growth

Vital that we retain the flexibility to exploit opportunities as they arise

Aim to achieve above average margins and a superior return on capital employed

Group’s balance sheet strength can help strengthen the portfolio of businesses. Board retains the option of considering a return of value to shareholders if sensible opportunities to acquire are not realised

Current trading in line with expectations. Confident of achieving another satisfactory performance in 2007