Predicting Valuations of Venture Capital Funded Private...

1

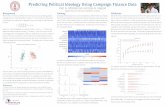

Company Valuation Industry Market Location Funding raised First funded Last funded Rounds raised Year founded Headcount Twitter followers Web traffic Top Investors Top Alma Maters Top Former Employers Uber $51B Mobile & Telecom Real-time SF Bay Area $9.00475B 08/01/09 08/19/15 12 2009 5257 373815 15153116 NEA, Crunchfund, Google Ventures, Goldman Sachs, Accel, KPCB Harvard, MIT Microsoft, Facebook x (i) y (i) Predicting Valuations of Venture Capital Funded Private Companies Weighted Log Linear Regression Simple Linear Regression Startups are difficult for the Silicon Valley spectator to value, since typically only angel, venture capital and private equity investors are privy to the financial records and business details of these private companies. External technology enthusiasts must rely on public indicators to compare and contrast what they deem to be similar companies in order to determine the value of a private company. However, by choosing to only examine the obvious comparable competitor companies, the enthusiast is disregarding a large amount of relevant data across the wider market. Feeding metadata about these startups into a family of supervised learning algorithms allows the user to consume and analyze large amounts of data in a short period of time and take into account the larger startup ecosystem. Motivation Training sample Log Linear Regression After trying linear regression, we quickly decided that we did not want to minimize the distance between our hypothesis and the actual valuation. For example, for Uber’s $51B valuation we were off by $10M; for tiny StarMobile, we were also off its $4M valuation by $10M. These costs are not equal to us. $10M is a fraction of Uber’s valuation, while it is nearly double StarMobile’s. We then changed our cost function to instead minimize the distance of 1 minus the hypothesis divided by the actual valuation. However, now we saw a new error: an overestimate of 5x was not weighted equally with an underestimate of 5x. We jumped again to our final core cost function, where we minimized the difference between the log of the hypothesis and the log of the actual valuation. In this way, the logs corrected for the previous error and now an overestimate of 5x was weighted equally with an underestimate of 5x. Above, we calculate all the costs of the different hypotheses according to this function, while the graphs demonstrate the minimization to each particular cost function. Finally, we decided to fit our data better after discussing overfitting and underfitting costs and benefits. Cross validation on weighted log linear regression has performed the best on our data set. Results Results Caroline Frost Tigran Askaryan

Transcript of Predicting Valuations of Venture Capital Funded Private...

Company Valuation Industry Market Location Funding raised First funded

Last funded Rounds raised Year founded Headcount Twitter

followers Web traffic Top Investors Top Alma Maters Top Former Employers

Uber $51B Mobile & Telecom Real-time SF Bay Area $9.00475B 08/01/09 08/19/15 12 2009 5257 373815 15153116 NEA, Crunchfund, Google Ventures,

Goldman Sachs, Accel, KPCB Harvard, MIT Microsoft, Facebook

x (i)y (i)

Predicting Valuations of Venture Capital Funded Private Companies

Weighted Log Linear Regression

Simple Linear Regression

Startups are difficult for the Silicon Valley spectator to value, since typically only angel, venture capital and private equity investors are privy to the financial records and business details of these private companies. External technology enthusiasts must rely on public indicators to compare and contrast what they deem to be similar companies in order to determine the value of a private company. However, by choosing to only examine the obvious comparable competitor companies, the enthusiast is disregarding a large amount of relevant data across the wider market. Feeding metadata about these startups into a family of supervised learning algorithms allows the user to consume and analyze large amounts of data in a short period of time and take into account the larger startup ecosystem.

Motivation

Training sample

Log Linear Regression

After trying linear regression, we quickly decided that we did not want to minimize the distance between our hypothesis and the actual valuation. For example, for Uber’s $51B valuation we were off by $10M; for tiny StarMobile, we were also off its $4M valuation by $10M. These costs are not equal to us. $10M is a fraction of Uber’s valuation, while it is nearly double StarMobile’s. We then changed our cost function to instead minimize the distance of 1 minus the hypothesis divided by the actual valuation. However, now we saw a new error: an overestimate of 5x was not weighted equally with an underestimate of 5x. We jumped again to our final core cost function, where we minimized the difference between the log of the hypothesis and the log of the actual valuation. In this way, the logs corrected for the previous error and now an overestimate of 5x was weighted equally with an underestimate of 5x. Above, we calculate all the costs of the different hypotheses according to this function, while the graphs demonstrate the minimization to each particular cost function. Finally, we decided to fit our data better after discussing overfitting and underfitting costs and benefits. Cross validation on weighted log linear regression has performed the best on our data set.

Results

Results

Caroline FrostTigran Askaryan