PPP PUBLIC PRIVATE PARTNERSHIP - IRAS Times · Characteristics –Public authority •Can enter...

18

PPP PUBLIC PRIVATE PARTNERSHIP

-

Upload

duongquynh -

Category

Documents

-

view

217 -

download

0

Transcript of PPP PUBLIC PRIVATE PARTNERSHIP - IRAS Times · Characteristics –Public authority •Can enter...

PPP PUBLIC PRIVATE PARTNERSHIP

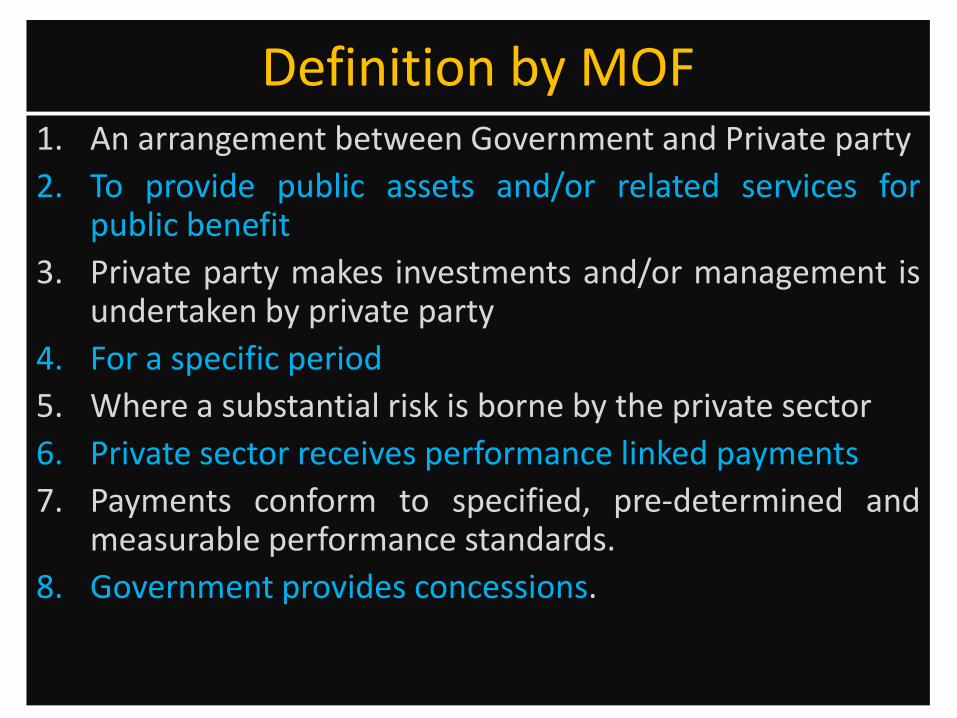

Definition by MOF 1. An arrangement between Government and Private party

2. To provide public assets and/or related services for public benefit

3. Private party makes investments and/or management is undertaken by private party

4. For a specific period

5. Where a substantial risk is borne by the private sector

6. Private sector receives performance linked payments

7. Payments conform to specified, pre-determined and measurable performance standards.

8. Government provides concessions.

Design risk

Construction risk

Operational /Revenue

Tolls/user charges Services at pre determined quality

Concession granting Authority

Concession agreement

Service receivers

Financiers •Equity investors

•Lenders •Guarantors •Insurers

RISKS

Financial

SPV Risk

allocation Contracts

Final responsibility for service delivery rests with the Public sector agency

It bridges the investment gap faced by Government in providing Public goods

Performance obligations Debt/Equity

Characteristics – Public authority

• Can enter into long term PPP contracts

• will have only one contract with private party

• Risk sharing with private party

• Monitor the service delivery by single point of responsibility and accountability

• Final responsibility of service delivery rests with Public authority.

– Private party

• can innovate

• Brings in its skills and technology to provide public service

• Focuses on Life cycle costs as O&M is their responsibility

• Private party brings the Capital

Public procurement Vs PPP Public procurement PPP

Product oriented Service Oriented Ex: service of

No concept of life cycle Life cycle concept is considered

Short term contracts Long term contracts

Many contracts to procure a product. Mismatch in qualities will spoil the final product

Single contract by public authority with private party.

Risk is totally borne by the Public sector

Risk is transferred Pvt party and in turn allocated to other parties who can best manage it.

The continuum

Works and service contracts

Management and maintenance contracts

Operation and Maintenance contracts

Build operate and Transfer concessions: BOT,BOOT ,DFBOT etc

Full Privatization

Low Extent of Private Partnership High

Key Element Issues in Structuring

Scope • Scope of the PPP project need not be same as that of overall project •Scope is defined in terms of tasks and responsibilities between Parties •Related to the assets that are to be designed, built, financed maintained and operated

Cost Recovery

•Whether project is bankable based on user charges ? •Demand forecasting- demand conversion into revenue stream •Willingness of the users – ability to pay •Any possibility of windfall profits to private party? • Annuity based approach?

Duration •Long term •Can duration be bidding parameter?

PPP model • Selection of suitable model based on • Risk allocation •Nature of the project

Structuring a PPP project

Financial analysis and structuring • Financial analysis covers : Pre project and project phases. • Pre-Project questions:

– Is the project warranted? • Current asset utilization • Rehabilitation or new project • Alternatives

– Future demand analysis • Demand analysis • Sustainability and elasticity of demand • Competing alternatives – effect on project inflows

• Project initiation stage – Cost estimation

• Need for accurate cost estimation • Involves life cycle costing unlike in case of public

procurement.

Financing the project • Capital providers to the project

– Debt

• Banks, Development partners, Bonds, Government

– Equity

• Sponsors/promoters, Government.

– Equity is costlier than debt

• equity provider is at higher risk.

• After taxes, OpEx and debt servicing only dividend payment is possibly

• Project finance involves high levels of debt.

Financial analysis contd..

Project finance Corporate Finance

No or limited recourse to sponsor’s assets Recourse to sponsor’s assets

Bankability of the project is based on debt service capacity

Bankability is based on debt service capacity and Collateral value

Debt service capacity is based on future cash flows

Debt service capacity is based on future cash flows taking into account prior performance

Non Recourse Financing : In this, the lender is satisfied to look initially to the projected cash flows and earnings of that project as the source of funds from which a loan will be repaid and to the assets of the project as collateral for the loan.

Bidding & Contracting Process

• RFQ: Request for Qualification

– Eligibility criteria- threshold technical capacity

– Eligible and prospective bidders are pre-qualified

• RFP ( Request for Proposal)

– From pre qualified bidders

– Financial bid

• Evaluation

Concession agreements • A concession is a bundle of rights conferred on the private entity in

return of certain specified obligations to be undertaken • Major elements of Concessional Agreements:

– Risk mitigation framework • Spell out service obligations • Performance linked payment

– Rights and obligations of the parties • Conditions Precedent to be fulfilled • Financial close

– O&M obligations • O&M manual, practices, penalties etc

– User fees • Determination, Collection and appropriation ,Discounts • Revision of fee etc

– Force Majeure • Non Political & Political

– Defaults – Termination Payments – Dispute resolution Mechanism

13

0.0

50.0

100.0

150.0

200.0

250.0

300.0

US

$ B

n.

Projected Investment in Twelfth Plan

XI Plan:

Revised Projections:

US $ 514 bn.

(Rs. 20,54,205 cr.)

XII Plan:

Projected: US $ 1,025 bn.

(Rs. 40,99,240 cr.)

Business as Usual: US $ 857 bn.

(Rs. 34,28,918 cr.)

0

30

60

90

120

150

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Energy Telecoms Transport Water and sewerage Total

Source: World Bank & PPIAF

PPP Investment in Infrastructure in India (USD billions)

Period Approx Infra Sector Investment

Estimated PPP % Estimated PPP Investment

10th Plan 222 25 56

11th Plan 500 37 185

12th Plan (Projection) 1000 50 500

Source: Planning Commission Documents

IFRS Treatment of Concession agreements

• A service concession arrangement contractually obliges the operator to provide the services to the public on behalf of the public sector entity.

IFRIC 12 Service Concession Arrangements applies to

public-to-private service concession arrangements if:

(a) The grantor controls or regulates what services the operator must provide with the infrastructure, to whom it must provide them, and at what price; and

(b) The grantor control – through ownership, beneficial entitlement or otherwise – any significant residual interest in the infrastructure at the end of the term of the arrangement. [IFRIC 12.5]

Issues addressed in IFRIC 12 Treatment

a) Treatment of the operator’s right over the infrastructure

Paragraph 11

The operator does not recognize infrastructure as property, plant and equipment or as a leased asset because the contractual service arrangement does not convey the right to control the use of the public service infrastructure to the operator.

(b) Consideration given by the grantor

Paragraphs 15-19

The operator recognize consideration for construction or upgrade services at fair value. The consideration may be rights, financial assets of intangible assets.

(c) Items provided to the operator by the grantor

Infrastructure items to which the operator is given access by the grantor for the purposes of the service arrangement are not recognized as property, plant and equipment of the operator.

Thank you