PP Domestic Resource Mobilization October 2001

9

Domestic Resource Mobilization / 1 Annex 4. Financing for Development: Domestic Resource Mobilization Filomeno S. Sta. Ana III October 2001 This paper attempts to develop a civil society policy agenda on domestic resource mobilization towards influencing the global Financing for Development (FfD) process initiated by the United Nations. The preparations for the FfD include a series of United Nations meetings that will come out with analyses and recommendations on a broad range of financing and related issues. The process will culminate in an international conference in March 2001. The FfD is an opportunity not only to address the global concerns and their impact on the Philippines but also to provide a boost to the national reform initiatives. The FfD can thus be a means to speed up the tax reform agenda that the Macapagal-Arroyo administration has to put in place. National Context Public finance reforms have gained greater urgency especially in the wake of reversals during the Estrada administration. During the short term of Estrada, for example, the national government incurred a serious deficit arising from dismal revenue collection and excessive, unwise spending. This deficit is hounding the Macapagal-Arroyo administration in its effort to revive economic growth. The Department of Finance (DoF) estimates that the deficit in the national government balance (revenues less expenditures) in 2001 is equivalent to 4.0 of gross domestic product (GDP). Nonetheless, domestic resource mobilization is a perennial issue, regardless of who is in power. The Philippines has been called the “sick man of Asia,” afflicted with low domestic savings, low tax effort, and low growth. Two other factors make domestic resource mobilization crucial in the current period. The first relates to the impact and the lingering effects of the financial crisis that struck the country and the rest of the world in 1997. A major lesson drawn from the crisis is to depend less on foreign capital and correspondingly to increase domestic savings and investments. The second is the implication of the September 11 terrorist attack in the United States. That is, it has pushed the US into a recession and has shaken the global economy. For the Philippines, this means solidifying an economic strategy that focuses on stimulating and expanding the domestic market. Again, this would necessitate a greater effort in mobilizing domestic resources. Focus of Paper It goes without saying that domestic resource mobilization encompasses a wide range of issues and concerns. Even if we divide the concerns into the roles of the public and private sectors, the set of issues for both the private sector and the public sector is still large. Public policy that covers both private and public activities likewise has a broad scope. We can

-

Upload

socialwatchphilippines -

Category

Documents

-

view

212 -

download

0

description

Â

Transcript of PP Domestic Resource Mobilization October 2001

Domestic Resource Mobilization / 1

Annex 4.

Financing for Development: Domestic Resource Mobilization Filomeno S. Sta. Ana III

October 2001

This paper attempts to develop a civil society policy agenda on domestic resource mobilization towards influencing the global Financing for Development (FfD) process initiated by the United Nations.

The preparations for the FfD include a series of United Nations meetings that will come

out with analyses and recommendations on a broad range of financing and related issues. The process will culminate in an international conference in March 2001.

The FfD is an opportunity not only to address the global concerns and their impact on the

Philippines but also to provide a boost to the national reform initiatives. The FfD can thus be a means to speed up the tax reform agenda that the Macapagal-Arroyo administration has to put in place. National Context

Public finance reforms have gained greater urgency especially in the wake of reversals during the Estrada administration. During the short term of Estrada, for example, the national government incurred a serious deficit arising from dismal revenue collection and excessive, unwise spending. This deficit is hounding the Macapagal-Arroyo administration in its effort to revive economic growth. The Department of Finance (DoF) estimates that the deficit in the national government balance (revenues less expenditures) in 2001 is equivalent to 4.0 of gross domestic product (GDP).

Nonetheless, domestic resource mobilization is a perennial issue, regardless of who is in power. The Philippines has been called the “sick man of Asia,” afflicted with low domestic savings, low tax effort, and low growth. Two other factors make domestic resource mobilization crucial in the current period. The first relates to the impact and the lingering effects of the financial crisis that struck the country and the rest of the world in 1997. A major lesson drawn from the crisis is to depend less on foreign capital and correspondingly to increase domestic savings and investments. The second is the implication of the September 11 terrorist attack in the United States. That is, it has pushed the US into a recession and has shaken the global economy. For the Philippines, this means solidifying an economic strategy that focuses on stimulating and expanding the domestic market. Again, this would necessitate a greater effort in mobilizing domestic resources. Focus of Paper It goes without saying that domestic resource mobilization encompasses a wide range of issues and concerns. Even if we divide the concerns into the roles of the public and private sectors, the set of issues for both the private sector and the public sector is still large. Public policy that covers both private and public activities likewise has a broad scope. We can

Domestic Resource Mobilization / 2

enumerate a long list of concerns: taxation, public expenditure, monetary policy, banking and finance, trade and industry, agriculture, health environment, social insurance and protection, market regulation, rule of law, etc. All this is closely linked to the mobilization of domestic resources. Not to be overwhelmed, this paper narrows the subject to what it believes is the most crucial challenge confronting the Macapagal-Arroyo administration in relation to the mobilization of domestic resources. This is none other but the implementation of a coherent and practicable tax reform agenda whose goal is to increase the tax effort (measured as taxes as a proportion of gross domestic product) to a significant level and hence contribute to augmenting the country’s domestic savings. Furthermore, this paper gives more attention to identifying or proposing the reforms that can be advocated by civil society organizations. In this sense, the paper can serve as a basis for developing a civil society position on a progressive tax reform agenda. The paper is divided into two general sections, namely the reforms that can be done at the national level, which can be pursued with or without the FfD. Of course, a favorable enabling international environment for internal reforms is most welcome. It thus matters that the second section deals with taxation issues arising from globalization. And the issues here are precisely the issues that the FfD must tackle. Tax Reform Agenda at the National Level

To reiterate, the Philippines has a very low saving rate and a low tax effort (taxes as a proportion of national output).1

The chronic problem of weak tax effort was aggravated during the Estrada administration. The low revenue collection and the overspending resulted in an unwarranted budget deficit, which peaked at 4.1 percent of GDP in 2000. It must be said that the budget deficit per se is not the main problem.

In turn, the low savings and weak revenues contribute to the country's low growth rate.

2

1 The Philippines has one of the lowest saving rate in Asia. Its tax effort, compared to East Asian countries, is also lower. 2 In a different context, having a budget deficit may be necessary for growth and employment. In addition, a deficit of 4 percent of GDP is not alarming for a developing country. In highly developed countries, say member countries of the European Union, a deficit of 3 percent of output is acceptable.

It is but the by-product of excessive, unproductive government spending and the lack of political will to collect taxes and more importantly to fight tax evasion. With respect to revenues, Rosario Manasan (2001) states that the overall tax effort fell from 18.7 percent of GNP (gross national product) in 1997 to 13.2 percent of GNP in 2000.

For the medium-term however, the budget deficit has to be brought down significantly. Table 1 below shows the government's objective to achieve fiscal balance by 2006. This may have a painful tradeoff, that is, a balanced budget at the expense of sacrificing public spending that is necessary to achieve poverty reduction targets.

Domestic Resource Mobilization / 3

Nevertheless, for a country like the Philippines that has low savings, aiming for a fiscal surplus is a virtue. Reducing the fiscal deficit is therefore a key objective of the medium-term development plan.. But to repeat, closing the budget gap must be constrained by the financing requirements of the anti-poverty program. Hence, the deficit problem should be resolved mainly through increasing revenues and not through cutting spending 3 Table 1 Projected Fiscal Balance (in billion pesos) 2000 2001 2002 2003 2004 2005 2006 Revenues 514.8 558.2 624.3 701.5 775.6 882.8 1007.5 Percent of GDP 15.6% 15.4% 15.8% 16.1% 16.2% 16.6% 17.1% Expenditures 649.0 703.2 754.3 800.0 819.3 904.6 1007.53 Percent of GDP 18.6% 18.4% 18.0% 17.4% 16.1% 16.0% 16.0% Surplus/(Deficit) (134.2) (145.0) (130.0) (98.4) (43.8) (21.9) (0.0) Percent of GDP -4.1% -4.0% -3.3% -2.3% -0.9% -0.4% 0.0% Source: Department of Finance

To pursue the tax reform agenda and guide our advocacy, it makes sense to reaffirm some basic taxation principles The characteristics of a desirable tax system are: 1) a progressive and equitable system of taxation, 2) a buoyant tax system to keep revenues flowing to sustain development programs, and 3) an efficient tax system characterized by administrative simplicity that increases the tax base and plugs the loopholes to minimize tax evasion and avoidance.

It is also worth affirming that fiscal policy, including taxation, serve the central

development objective of reducing poverty and promoting equity.

Direct taxes (on income, capital, and other assets) are invariably associated with a progressive system of taxation. The question is: Up to what extent or degree can a national government rely on direct taxation, without incurring greater costs resulting from the failure to

Progressive Taxation

It is always desirable to have a progressive tax system. Unfortunately, global competition compels nations to sacrifice progressivity in favor of tax rates and a tax system that are generous to capital and internationally mobile, highly skilled labor.

3 This is not to suggest that there is no room for cutting budgetary items. For example, discretionary and non- transparent funds as well as pork barrel deserve to be reduced sharply.

Domestic Resource Mobilization / 4

attract capital and technology or even from the departure of its own mobile factors of production?

In the Philippines, corporate income tax and individual income tax are the biggest

internal revenue earners.4

4The Bureau of Internal; Revenue (BIR) accounts for approximately 78 percent of total tax revenues (Republic of the Philippines, Budget of Expenditures and Sources of Financing 2001).

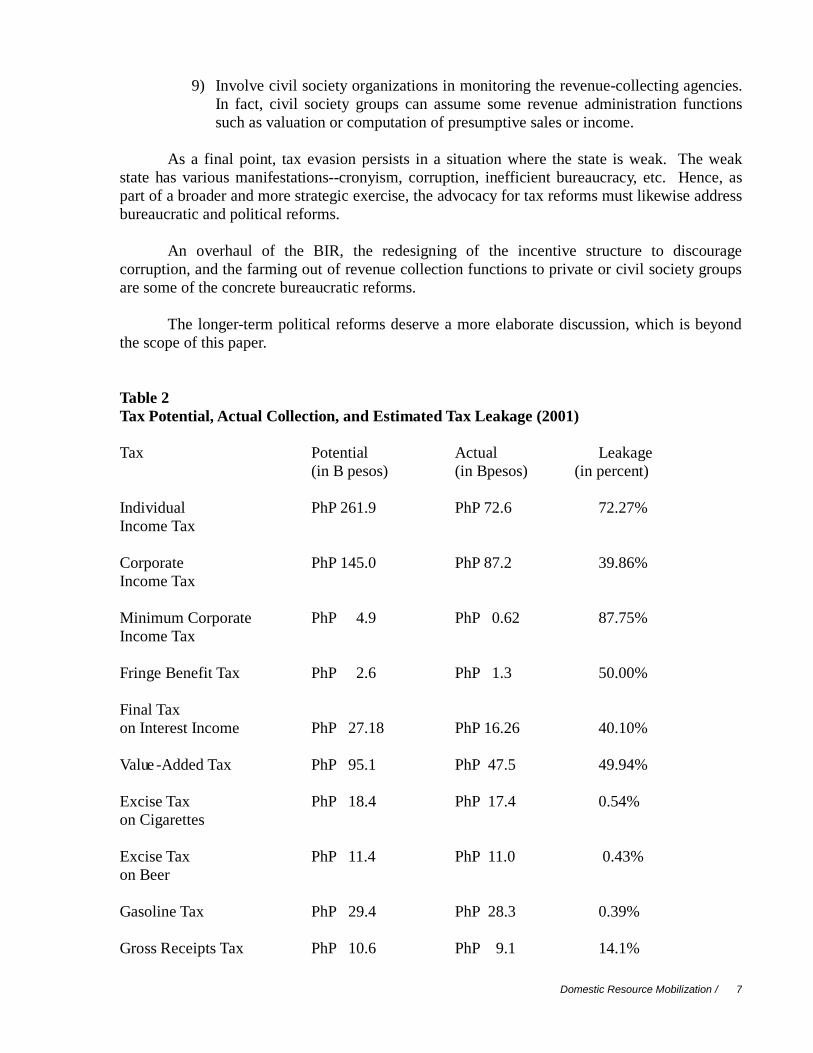

However, actual collection is far from approximating the tax potential. To illustrate, the Department of Finance (DoF) estimates that for 2001, the leakage (actual collection as proportion of the potential revenue) is: a) from the individual income tax, 72.27 percent, b) from the corporate income tax, 39.86 percent, and c) from the minimum corporate income tax, 87.75 percent. (See table 2 for more information on estimates of actual amount, potential amount, and the leakage for the different taxes.) It is overwhelmingly in the area of direct taxes in which tax evasion is high (even as it is observed that tax compliance in relation to the value-added tax or vat is also low). The high level of tax evasion thus makes the Philippine tax structure (with a top rate of 34 percent for individual income tax) progressive only on paper.

It was thought that the lowering of income tax rates would have effectively addressed the leakage problem. (Conventional wisdom says that a lower tax rate would encourage people to pay taxes.) The lowering of tax rates was a key feature of the comprehensive tax reform legislation that was passed during the Ramos administration. While it may be too early to make a definitive assessment of the comprehensive tax reform legislation, it is quite apparent that in the case of lowering the income tax rate for individuals and corporations, this is neither sufficient nor decisive to improve tax compliance and enhance tax revenues. For the principal problem regarding tax evasion is the non-declaration as well as under-declaration of income.

Recognizing the need to rectify the weakness of the comprehensive tax reform law, especially in relation to income taxation, the Macapagal-Arroyo administration is proposing a new piece of legislation. The proposal is to adopt a modified gross income tax for corporations. As a sweetener, the proposal includes a reduction of marginal income tax rates.

Ironically, this proposal, notwithstanding the intention to make the tax structure simpler,

will aggravate the fiscal degradation. The modified gross income tax does not result in its ostensible objective of reducing discretion and harassment. For one thing, it is difficult to operationalize the "cost of goods sold," Different firms and industries have varying cost structures; many businesses, especially in the service sector, have a large portion of costs that could not be classified under cost of goods sold. The effect of this is having different sets of complicated rules, .thus undermining the supposed objective of administrative simplicity. A modified gross income tax would likewise distort the behavior of taxpayers--through reporting lower revenues but charging higher expenses (such as out-of-pocket expenses) that would be then included as part of cost of goods sold. Furthermore, it violates the principle of equity, for it penalizes firms and industries that have high turnover but narrow profit margins.

Last but not the least, given all the weaknesses enumerated above, the modified gross income tax proposal in combination with the other proposal to lower the marginal tax rates for individual income tax, would further reduce revenue collection and thus worsen the fiscal degradation.

Domestic Resource Mobilization / 5

Take the case of the individual income tax leakage. The reason behind the huge leak—72 percent of potential revenue—is that the tax net fails to capture significant proportion of business and professional income of individuals. Individual income tax relies heavily on wage or compensation income. As Manasan points out in a preliminary study (2001), the share of individual income tax from wage/compensation income is 78 percent in 2000 although compensation income accounts for less than half (48 percent) of total personal income. Furthermore, Manasan states that the average effective tax rate in 2000 for wage/consumption income is about 5 percent, and this is five times higher than the rate for non-wage (or business/professional) income.

Revenue-Enhancing Measures Instead of being engrossed with the modified gross income taxation, the Macapagal-Arroyo administration should pursue measures that will clearly and unquestionably lead to increased revenues.

Tax administration is the main challenge, considering the high rate of leakage. The data on table 2 suggests that efficient tax collection is the main obstruction to revenue enhancement.

5

5 Manasan defines the average effective tax rate for wage/compensation income as “the ratio of collections from the individual [income] tax from salaried individuals to the compensation income of households in the National Income Accounts.” She defines the average effective tax rate for business and professional income as “the ratio of collections of the individual income tax from the self-employed to the net operating surplus of households in the National Income Accounts.”

In relation to corporate income taxation, the DoF has identified the overstatement of deductions and underdeclaration of sales as among the main problems. It does not help either that the government has yet to issue the implementing rules and regulations for the 1997 comprehensive tax reform legislation--a failure of the deposed Estrada administration.

With regard to the tax structure, the government can still use indirect taxes to enhance revenues. Government can design the indirect taxes in a way that will reduce their regressivity. In truth, some indirect taxes enhance progressivity. For example, the government should impose higher excise taxes on luxurious/affluent consumption (e.g., luxury vehicles). A tax on affluent consumption, thereby reducing the propensity for such consumption, may have the additional benefit of inducing the rich to use their surplus to build up domestic capital formation.

It is also to the public interest to penalize consumption of “sin” goods (e.g., tobacco and

liquor). The increase in specific taxes on tobacco and liquor should be done through the indexation of the tax rates in relation to inflation.

As part of revenue-enhancing measures, the government should be reminded of the huge

opportunity costs (foregone taxes) of subsidies, privileges or protection given to a few sectors. Government has to decisively implement the following tasks, among other things.

Domestic Resource Mobilization / 6

1) Rationalize and substantially reduce the many fiscal incentives given to

investments. After all, it has been established that fiscal incentives are not the primary factor to attract investments.

2) Impose (high) tariffs, instead of quantitative restrictions, on sensitive agricultural

goods.

3) End the duty-free privileges for Clark and Subic. It is common knowledge that this has abetted technical smuggling.

Innovative and firm measures in the tax structure but more so in tax administration are

necessary to enhance revenue collection and fight tax evasion. Some crucial measures that have to be carried out are the following:

1) Introduce presumptive taxation on hard-to-tax income groups (self-employed professionals like lawyers, doctors, accountants, etc)

2) Proceed with the full computerization the Bureau of Internal Revenue's data base

and procedures

3) Order the BIR to complete at the soonest possible time the implementing rules related to the caps set on allowable deductions on corporate income.

4) Increase the withholding tax of high-income earners. This has met stiff resistance

from certain sectors such as the film industry. The key is to educate the public and counter the misinformation being peddled by some that the expansion of the withholding tax is an increase in tax.

5) Promote the use of third-party information to widen the tax base. A number of

institutions such as the local government units and the Social Security System can provide additional data or information.

6) Prosecute big tax evaders and corrupt high-level revenue officials to send a

powerful signal that government is serious in fighting corruption and tax evasion.

7) Provide friendly assistance to taxpayers. Taxpayers encounter a myriad of problems in paying the right amount of tax. The paper work and the administrative process can still be simplified. The proposal to exempt pure wage/compensation income earners from filing income tax returns (after all, they are already subjected to the withholding tax) should be done at the soonest.

8) Intensify the monitoring at the Bureau of Customs (BoC), especially in relation to

exemptions and import valuation. Revenues from the BoC can still be enhanced, despite the lowering of tariffs and the decline of imports resulting from the weak economy.

Domestic Resource Mobilization / 7

9) Involve civil society organizations in monitoring the revenue-collecting agencies. In fact, civil society groups can assume some revenue administration functions such as valuation or computation of presumptive sales or income.

As a final point, tax evasion persists in a situation where the state is weak. The weak

state has various manifestations--cronyism, corruption, inefficient bureaucracy, etc. Hence, as part of a broader and more strategic exercise, the advocacy for tax reforms must likewise address bureaucratic and political reforms.

An overhaul of the BIR, the redesigning of the incentive structure to discourage

corruption, and the farming out of revenue collection functions to private or civil society groups are some of the concrete bureaucratic reforms.

The longer-term political reforms deserve a more elaborate discussion, which is beyond

the scope of this paper. Table 2 Tax Potential, Actual Collection, and Estimated Tax Leakage (2001) Tax Potential Actual Leakage (in B pesos) (in Bpesos) (in percent) Individual PhP 261.9 PhP 72.6 72.27% Income Tax Corporate PhP 145.0 PhP 87.2 39.86% Income Tax Minimum Corporate PhP 4.9 PhP 0.62 87.75% Income Tax Fringe Benefit Tax PhP 2.6 PhP 1.3 50.00% Final Tax on Interest Income PhP 27.18 PhP 16.26 40.10% Value -Added Tax PhP 95.1 PhP 47.5 49.94% Excise Tax PhP 18.4 PhP 17.4 0.54% on Cigarettes Excise Tax PhP 11.4 PhP 11.0 0.43% on Beer Gasoline Tax PhP 29.4 PhP 28.3 0.39% Gross Receipts Tax PhP 10.6 PhP 9.1 14.1%

Domestic Resource Mobilization / 8

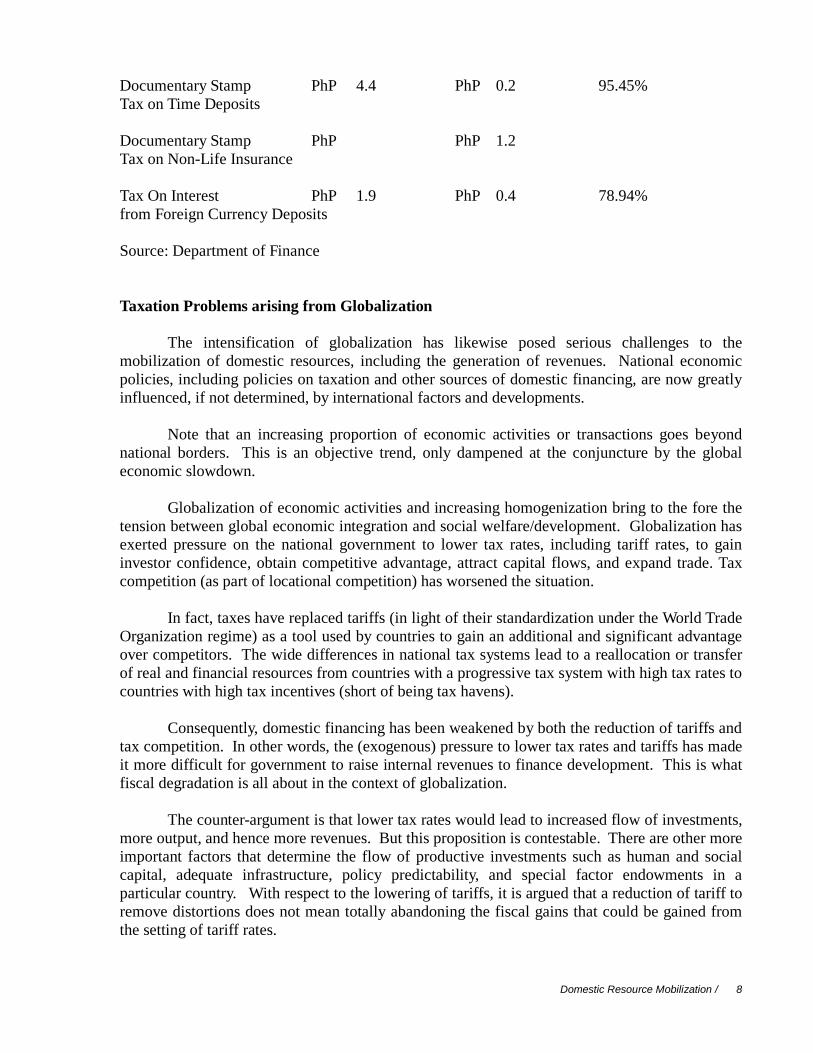

Documentary Stamp PhP 4.4 PhP 0.2 95.45% Tax on Time Deposits Documentary Stamp PhP PhP 1.2 Tax on Non-Life Insurance Tax On Interest PhP 1.9 PhP 0.4 78.94% from Foreign Currency Deposits Source: Department of Finance Taxation Problems arising from Globalization The intensification of globalization has likewise posed serious challenges to the mobilization of domestic resources, including the generation of revenues. National economic policies, including policies on taxation and other sources of domestic financing, are now greatly influenced, if not determined, by international factors and developments.

Note that an increasing proportion of economic activities or transactions goes beyond national borders. This is an objective trend, only dampened at the conjuncture by the global economic slowdown.

Globalization of economic activities and increasing homogenization bring to the fore the tension between global economic integration and social welfare/development. Globalization has exerted pressure on the national government to lower tax rates, including tariff rates, to gain investor confidence, obtain competitive advantage, attract capital flows, and expand trade. Tax competition (as part of locational competition) has worsened the situation.

In fact, taxes have replaced tariffs (in light of their standardization under the World Trade

Organization regime) as a tool used by countries to gain an additional and significant advantage over competitors. The wide differences in national tax systems lead to a reallocation or transfer of real and financial resources from countries with a progressive tax system with high tax rates to countries with high tax incentives (short of being tax havens).

Consequently, domestic financing has been weakened by both the reduction of tariffs and tax competition. In other words, the (exogenous) pressure to lower tax rates and tariffs has made it more difficult for government to raise internal revenues to finance development. This is what fiscal degradation is all about in the context of globalization.

The counter-argument is that lower tax rates would lead to increased flow of investments,

more output, and hence more revenues. But this proposition is contestable. There are other more important factors that determine the flow of productive investments such as human and social capital, adequate infrastructure, policy predictability, and special factor endowments in a particular country. With respect to the lowering of tariffs, it is argued that a reduction of tariff to remove distortions does not mean totally abandoning the fiscal gains that could be gained from the setting of tariff rates.

Domestic Resource Mobilization / 9

In this light, global rules have become relevant. The question is what specific global rules are needed. In the context of furthering the capacity of nation-states mobilize domestic resources, the following functions are important:

1. Put in place mechanisms and arrangements for coordination and harmonization

where appropriate and necessary. 2. Tackle tax evasion problems at the international level, including the problems

posed by tax-haven countries.

3. Prevent locational competition from becoming a race to the bottom.

4. Give room to nation-states to exercise flexibility and autonomy amidst economic homogenization.

Global rules or arrangements necessitate the establishment of an international structure

that has the legitimacy to apply moral suasion and more importantly, has the power to make countries follow such rules and arrangements. In this regard, the FfD is a most appropriate vehicle to develop the global rules and the corresponding institutions. In particular, we should fully support the recommendation of the high-level planning on FfD to have an International Tax Organization (ITO) whose mandate is broad enough to cover information gathering, maintaining surveillance, regulation of tax competition and tax evasion, and arbitration.

In many international summits, documents are long in principles but short in specific commitments. For the FfD, while there are many critical issues that have to be resolved, the passage of the ITO should count as a principal accomplishment.