Powers of Attorney: A Changing Landscape - Cassels Brock1).pdf · • POA should not expressly...

20

Ambie Edgar-Chana Presented to: RBC Wealth Management April 25, 2013 Powers of Attorney: A Changing Landscape

Transcript of Powers of Attorney: A Changing Landscape - Cassels Brock1).pdf · • POA should not expressly...

Ambie Edgar-Chana

Presented to:

RBC Wealth Management

April 25, 2013

Powers of Attorney: A Changing Landscape

slide | 2

“Money is the Root of All Evil”– Apostle Paul

slide | 3

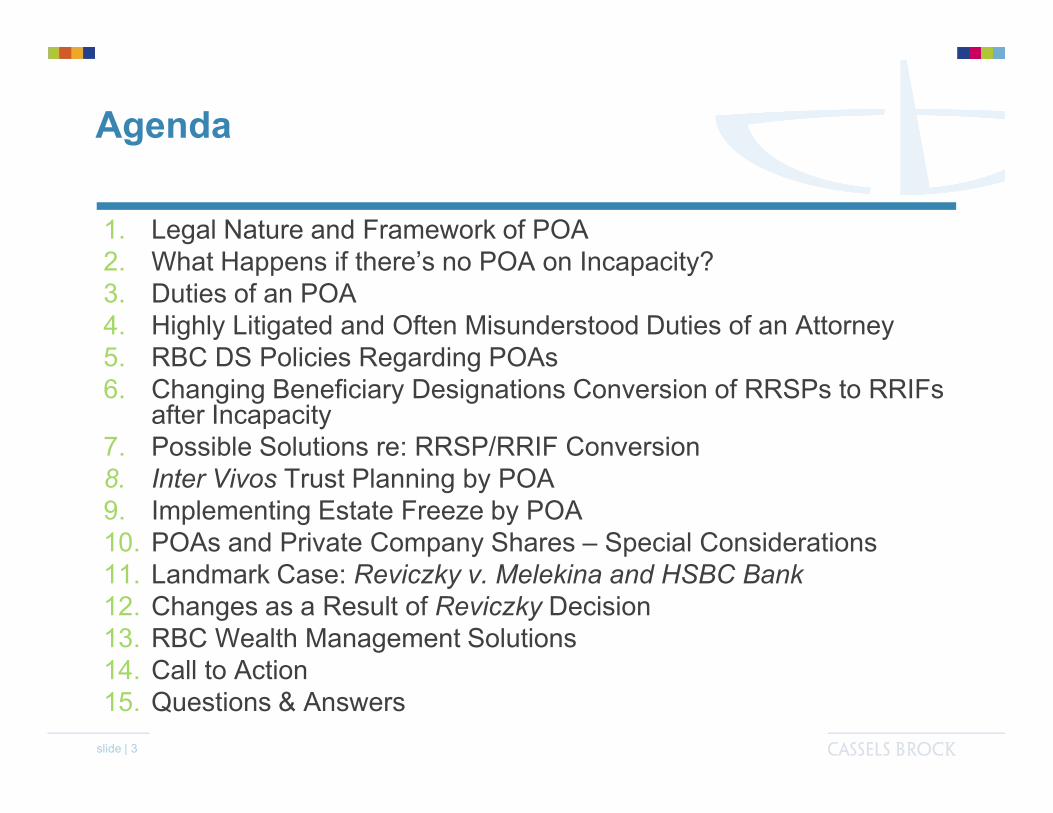

Agenda

1. Legal Nature and Framework of POA2. What Happens if there’s no POA on Incapacity?3. Duties of an POA4. Highly Litigated and Often Misunderstood Duties of an Attorney5. RBC DS Policies Regarding POAs6. Changing Beneficiary Designations Conversion of RRSPs to RRIFs

after Incapacity7. Possible Solutions re: RRSP/RRIF Conversion8. Inter Vivos Trust Planning by POA9. Implementing Estate Freeze by POA10. POAs and Private Company Shares – Special Considerations11. Landmark Case: Reviczky v. Melekina and HSBC Bank 12. Changes as a Result of Reviczky Decision13. RBC Wealth Management Solutions14. Call to Action15. Questions & Answers

slide | 4

Legal Nature and Framework of a Power of Attorney for Property (“POA”)

● Agency Relationship while capacitated

● Banton v. Banton (1998), 164 D. L. R. (4th) (Ont. Ct. (Gen. Div.))

● duty owed to principle

● Act in accordance with instructions

● Account

● Fiduciary/Trustee Responsibilities after incapacity

● duties owed to incapacitated principle AND others

● standard of care heightened – different for whether taking compensation or not

● Substitute Decisions Act (“SDA”) provides legislative framework for capacity

slide | 5

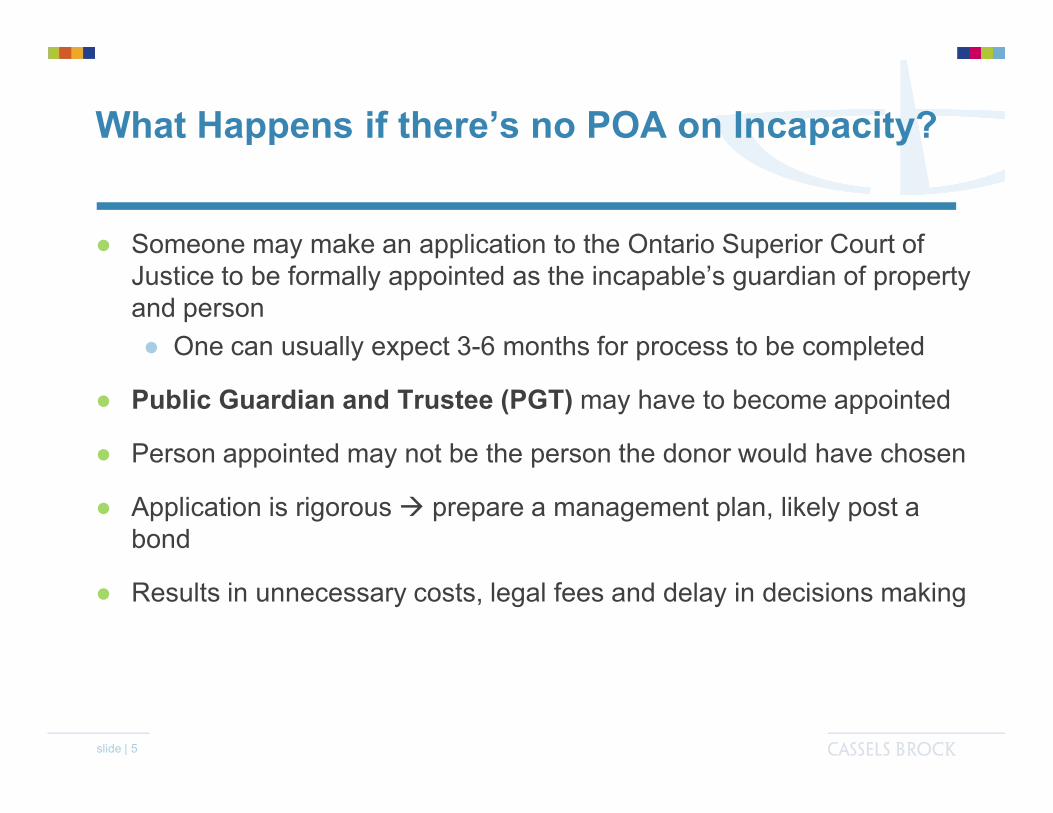

What Happens if there’s no POA on Incapacity?

● Someone may make an application to the Ontario Superior Court of Justice to be formally appointed as the incapable’s guardian of property and person

● One can usually expect 3-6 months for process to be completed

● Public Guardian and Trustee (PGT) may have to become appointed

● Person appointed may not be the person the donor would have chosen

● Application is rigorous prepare a management plan, likely post a bond

● Results in unnecessary costs, legal fees and delay in decisions making

slide | 6

Duties of an Attorney under the SDA

● Deems attorney to be a fiduciary act in donor’s best interests

● Make expenditures on the donor’s behalf for:

● Donor’s support, education and care

● Support education and care of donor’s dependents

● Satisfy donor’s other legal obligations

● Under certain circumstances, gifts and loans to donor’s friends/relatives, and/or charitable gifts

● Consider the personal comfort and well being of the donor

● Explain duties of the attorney to the donor

● Encourage the donor to, to the extent possible, participate in decisions regarding his/her property

● Consult with the donor’s supportive family and friends who are in regular personal contact or from whom donor receives personal care

● Interpreted as a duty to inform where conflict exists

● Questionable who is ‘supportive’ – outside scope of SDA

● Determine whether the donor has a Will and if so, have regard to the provisions of the donor’s Will

● Not dispose of property that the attorney knows is subject to a specific testamentary gift, except for money and certain circumstances

● Obligation to keep accounts keep detailed records of all transactions, supporting receipts, and be ready to produce those accounts, keep all donor’s money separate and apart from personal property of attorney and others

● At common law cannot delegate unless instrument provides otherwise, cannot make, change or revoke will, cannot allow personal interests to conflict with those of the donor

slide | 7

Highly Litigated and Often Misunderstood Duties of an Attorney

● Duty to account

● Fareed v. Wood 2005 CarswellOnt. 2572 (Ont. S.C.J.) court held attorney has a duty to account for ALL transactions during the time of the attorney’s involvement – including those that the grantor made himself/herself (while capable). Does this include the duty to protect a capable grantor from his/her own decisions

● Make expenditures on the donor’s behalf for support education and care of donor’s dependents

● Has to be enough money to meet the required expenditures of the donor and his/her other legal obligations

● Guiding principles consider value of property, accustomed standard of living, nature of other legal obligations

● Under certain circumstances, gifts and loans to donor’s friends/relatives, and/or charitable gifts

● Donor previously made similar gifts or loans, or indicated would

● Charitable gifts shall not exceed 20% of income in year of gift OR maximum provided in POA

● Consult with the donor’s supportive family and friends who are in regular personal contact or from whom donor receives personal care

● Interpreted as a duty to inform where disharmony exists consultation would lead to more conflict, delay

● Who is ‘supportive’ gauged in regards to relationship to incapable person, related is not enough to be considered supportive

slide | 8

RBC DS Policies Regarding POAs

● RBC DS requires official documentation (e.g., invoice) to allow payments to be made to a third party

● Funds can be transferred to donor’s bank account upon request

● Changes to beneficiary designations are NOT allowed, even when converting RRSP to RRIF and when moving from one account to another (e.g., non-managed to PIM)

● RBC DS requires a letter signed by the physician confirming incapacity in order to allow POA to sign on behalf of the donor

slide | 9

Changing Beneficiary DesignationsConversion of RRSPs to RRIFs after Incapacity

● Issue of whether attorney under POA can make a beneficiary designation on behalf of an incapable grantor appears fairly well settled RRSP/RRIF/Insurance/TFSA designation is a ‘testamentary disposition’ and ultra vires an attorney

● Legislation: Substitute Decisions Act s. 7(2), Succession Law Reform Act s. 1(1) definition of “will”

● Common Law: Fontana v. Fontana, (1987), 28 C. C. L. I. 232 (B.C.S.C), Richardson Estate v. Mew 310 DLR (4th) 21 (O.N.C.A.)

● Conversion of RRSP to RRIF at age 70

● No Ontario cases on point

● Bramley v. Bramley Estate (2003) 3 E.T.R. (3d) 191 (B.C.S.C.) a beneficiary designation will not survive transition from RRSP to RRIF

● Descharnais v. Toronto Dominion Bank (2002) 3 E.T.R. (3d) 221 (B.C.C.A.)

designation should carry on transfer of RRSP from one bank to another

slide | 10

Possible Solutions re: RRSP/RRIF Conversion

● Logically designation should be the same on conversion. If cannot effect by POA, make application to Court to intervene and exercise inherent jurisdiction to preserve intentions of incapable donor

● Possible to include specific authorization in POA to allow attorney to designate the same beneficiary on a RRIF who was designated on the converted RRSP

● Authorization is ultra vires

● Goes to establishing intention of donor

● Lawyer negligent?

● Lawyer can discuss conversion with donor and make detailed notes regarding intention on conversion of RRSP to RRIF will go to intention without being ultra vires

● Attorney may wish to make application to court while donor is still alive and incapable rather than waiting until death when RRIF is paid out to the estate

slide | 11

Inter Vivos Trust Planning by POA

● Banton v. Banton (1998), 164 D. L. R. (4th) (Ont. Ct. (Gen. Div.)) unlimited POA allowed establishment of inter vivos trust to protect father’s assets, but breached fiduciary duty – deprived him of his property rights further than was reasonably required to protect his interests.

● Bank of Nova Scotia Trust Co. v. Lawson (2005), 22 E.T.R. (3d) 198 (Ont. S.C.J.) variation of inter vivos trust was held invalid – variation had effect of changing manner in which capital of the inter vivos trust was to be distributed on grantor’s death is a testamentary disposition (deals with the disposition of settlors’ estates after death).

slide | 12

Implementing Estate Freeze by POA

● Yet to be specifically considered in Ontario

● Insights from British Columbia:

● O’Hagan v. O’Hagen [2003] 31 E.T.R. (2d) 3 (B.C.C.A.) estate freeze approved. Standard is whether a reasonable and prudent business person would think transaction is beneficial to grantor considering present circumstances and future possibilities

● Callender v. Callender (2001) 40 E.T.R. (2d) (198) (B.C.C.A.) corporate trustee was not removed for carrying out estate freeze (previously approved by court order) or refusal to pursue litigation on behalf of incapable which would have been costly and have little chance of success

● Recommendations in Ontario:• apply for court approval of plan under 39(1) of SDA

• POA should not expressly prohibit planning, or expressly allows for planning following incapacity

• Grantor should be adequately provided for after freeze

• Freeze benefits donor (or is at least neutral) and not just the beneficiaries

• Donor can resume control if regained capacity

• Plan is consistent with donor’s last will or at least not contrary to it

• Donor expressed interest in freeze while capable or was one to engage in tax planning (not critical)

• Reasonable and prudent business person would freeze in respect of his/her own property if capable

slide | 13

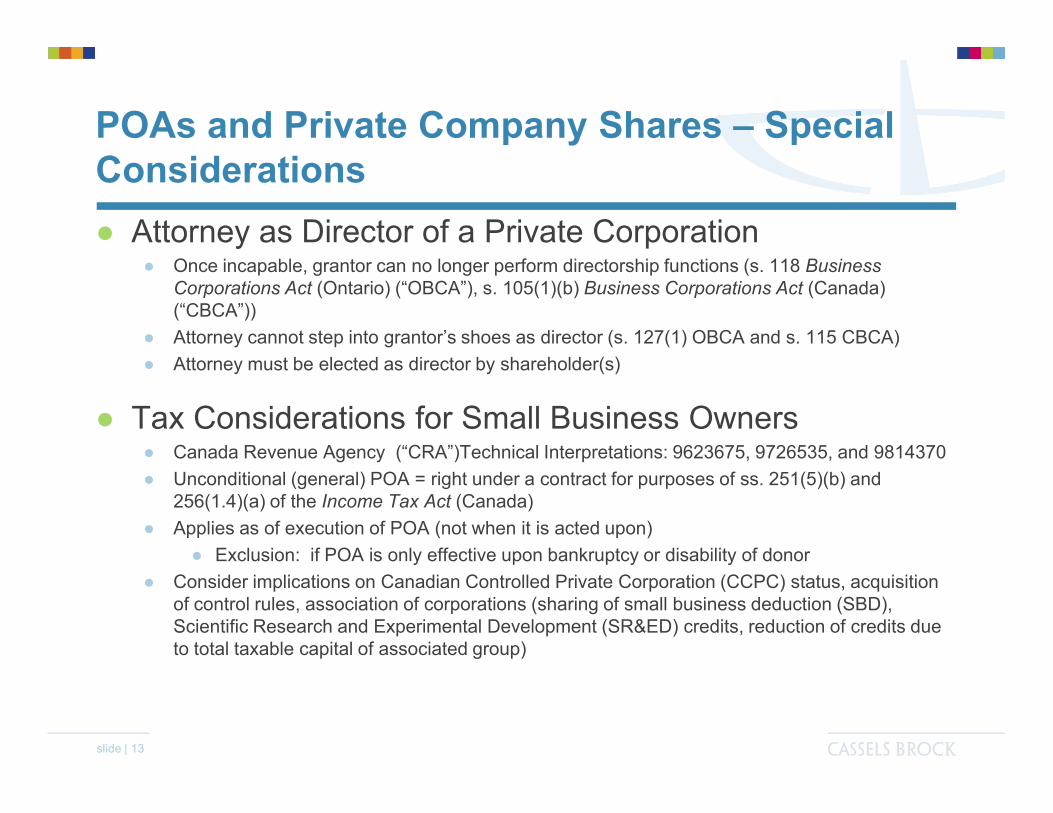

POAs and Private Company Shares – Special Considerations

● Attorney as Director of a Private Corporation● Once incapable, grantor can no longer perform directorship functions (s. 118 Business

Corporations Act (Ontario) (“OBCA”), s. 105(1)(b) Business Corporations Act (Canada) (“CBCA”))

● Attorney cannot step into grantor’s shoes as director (s. 127(1) OBCA and s. 115 CBCA)

● Attorney must be elected as director by shareholder(s)

● Tax Considerations for Small Business Owners● Canada Revenue Agency (“CRA”)Technical Interpretations: 9623675, 9726535, and 9814370

● Unconditional (general) POA = right under a contract for purposes of ss. 251(5)(b) and 256(1.4)(a) of the Income Tax Act (Canada)

● Applies as of execution of POA (not when it is acted upon)

● Exclusion: if POA is only effective upon bankruptcy or disability of donor

● Consider implications on Canadian Controlled Private Corporation (CCPC) status, acquisition of control rules, association of corporations (sharing of small business deduction (SBD), Scientific Research and Experimental Development (SR&ED) credits, reduction of credits due to total taxable capital of associated group)

slide | 14

Landmark Case: Reviczky v. Melekina & HSBC

● Forged POA to fraudulently sell an elderly man’s real estate investment property (title fraud)

● Involved a bank’s duty of care to review POA instructive to all financial institutions accepting instructions from an attorney under a POA

● POA was unusual:● Gave the donee the power to “manage and conduct all my affairs and to exercise

all of my legal rights and powers”

● Attorney was “durable” and “shall not be affected by my ability or lack of mental competence, except as may be provided otherwise by applicable state statute” (emphasis added)

● Signed by only one witness

● Stated that donor was personally known by the witness and had produced “driver’s license No...”

● Contained dates of birth for donor and donee

slide | 15

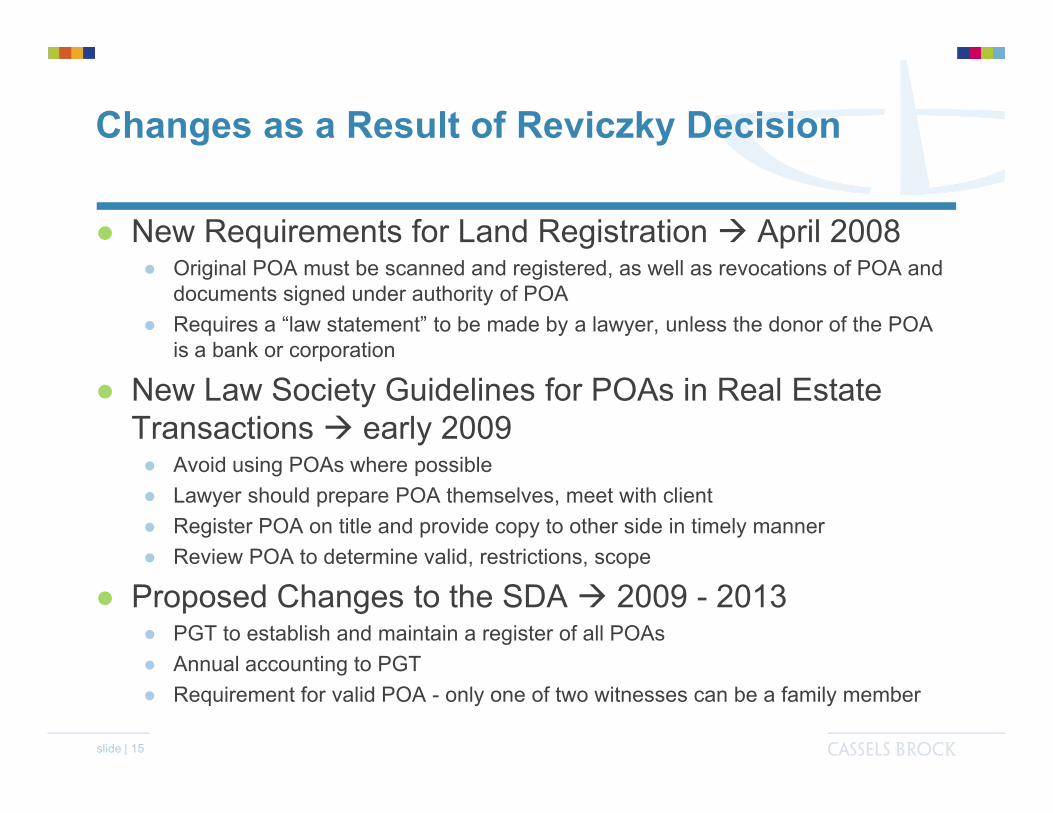

Changes as a Result of Reviczky Decision

● New Requirements for Land Registration April 2008● Original POA must be scanned and registered, as well as revocations of POA and

documents signed under authority of POA

● Requires a “law statement” to be made by a lawyer, unless the donor of the POA is a bank or corporation

● New Law Society Guidelines for POAs in Real Estate Transactions early 2009

● Avoid using POAs where possible

● Lawyer should prepare POA themselves, meet with client

● Register POA on title and provide copy to other side in timely manner

● Review POA to determine valid, restrictions, scope

● Proposed Changes to the SDA 2009 - 2013● PGT to establish and maintain a register of all POAs

● Annual accounting to PGT

● Requirement for valid POA - only one of two witnesses can be a family member

slide | 16

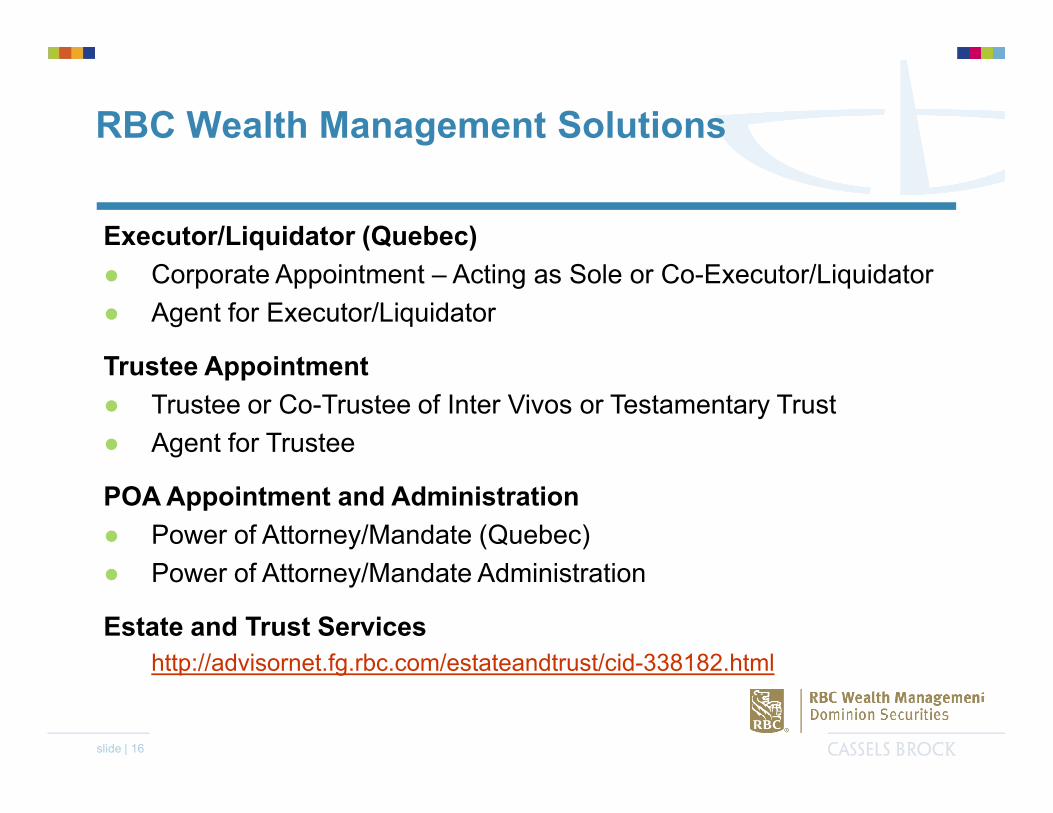

RBC Wealth Management Solutions

Executor/Liquidator (Quebec)

● Corporate Appointment – Acting as Sole or Co-Executor/Liquidator

● Agent for Executor/Liquidator

Trustee Appointment

● Trustee or Co-Trustee of Inter Vivos or Testamentary Trust

● Agent for Trustee

POA Appointment and Administration

● Power of Attorney/Mandate (Quebec)

● Power of Attorney/Mandate Administration

Estate and Trust Services

http://advisornet.fg.rbc.com/estateandtrust/cid-338182.html

slide | 17

Call to Action

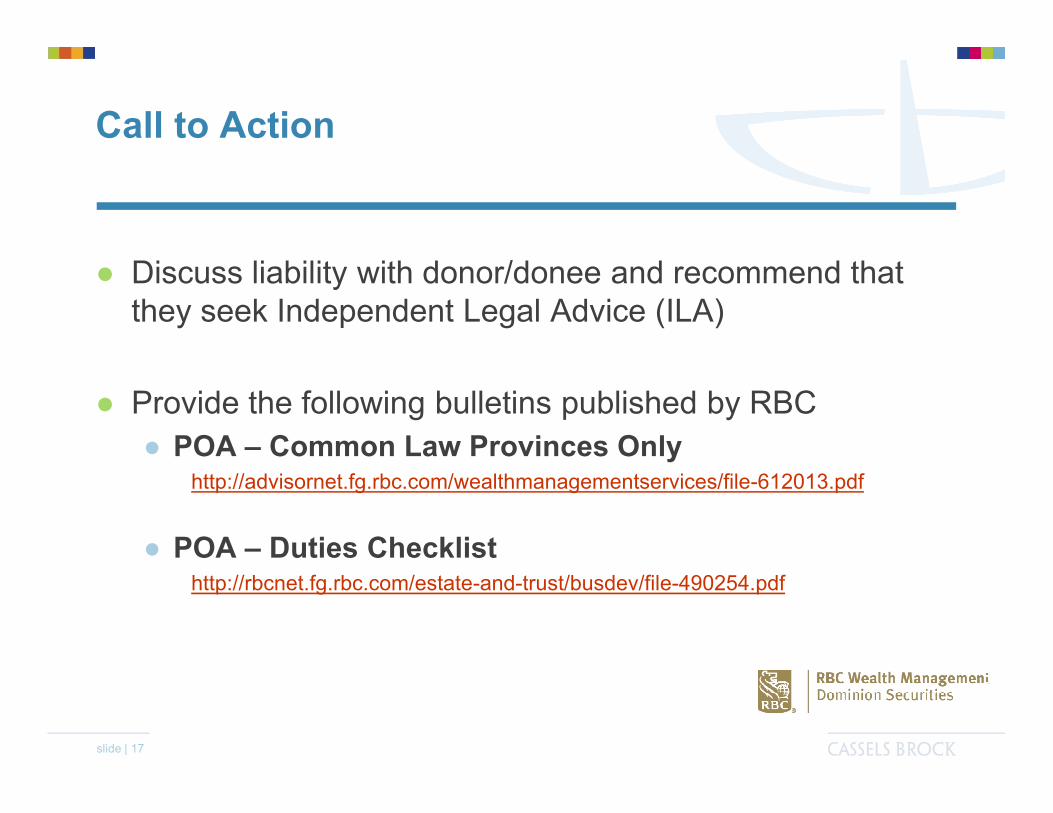

● Discuss liability with donor/donee and recommend that they seek Independent Legal Advice (ILA)

● Provide the following bulletins published by RBC

● POA – Common Law Provinces Onlyhttp://advisornet.fg.rbc.com/wealthmanagementservices/file-612013.pdf

● POA – Duties Checklisthttp://rbcnet.fg.rbc.com/estate-and-trust/busdev/file-490254.pdf

slide | 18

Thank you

● Questions & Answers

slide | 19

Disclaimer

This handout is provided as an information service only. It is current only as of the date of the handout and does not reflect subsequent changes in the law. This handout is distributed with the understanding that it does not constitute legal advice or establish a solicitor/client relationship by way of any information contained herein. The contents are intended for general information purposes only and under no circumstances can be relied upon for legal decision-making. Readers are advised to consult with a qualified lawyer and obtain a written opinion concerning the specifics of their particular situation.

© 2011–2013 CASSELS BROCK & BLACKWELL LLP. ALL RIGHTS RESERVED.

This document and the information in it is for illustration only and does not constitute legal advice. The information is subject to changes

in the law and the interpretation thereof. This document is not a substitute for legal or other professional advice. Users should consult

legal counsel for advice regarding the matters discussed herein.

Cassels Brock & Blackwell LLP

Suite 2100, Scotia Plaza Suite 2200, HSBC Building

40 King Street West 885 West Georgia Street

Toronto, ON Canada M5H 3C2 Vancouver, BC Canada V6C 3E8

Tel: 416 869 5300 Tel: 604 691 6100

Fax: 416 350 8877 Fax: 604 691 6120

Ambie [email protected](416) 860-6557