PowerPoint Presentation · This presentation contains forward-looking statements and information...

33

June 2014

Transcript of PowerPoint Presentation · This presentation contains forward-looking statements and information...

June 2014

Cautionary Information

This presentation contains forward-looking statements and information that are based on management’s current expectations. Such statements may include projections, Outlook and estimates regarding (i) leasing demand and demand for our wireless infrastructure, including small cells and distributed antenna systems (“DAS”), (ii) our growth, growth prospects and opportunities, including drivers of demand, (iii) shareholder returns, (iv) adoption of smartphones and cloud-based applications and consumption of mobile video, (v) U.S. mobile data demand, traffic, usage and growth,(vi) carrier capital expenditures and network investments, (vii) capital expenditures, (viii) U.S. wireless market, including the potential benefits, opportunities and returns therefrom, (ix) customer service, (x) capital allocation and capital structure, (xi) our investments, including investments in the land under our wireless infrastructure, (xii) our cost structure, including ground lease expense, (xiii) network density, (xiv) adjusted funds from operations (“AFFO”), including on a per share basis, (xv) margins, including site rental gross margin and incremental margin, (xvi) revenues, including site rental revenues, and (xvii) cash flows. The term “including”, and any variation thereof, means “including, without limitation.” Such forward-looking statements are subject to certain risks, uncertainties and assumptions, including prevailing market conditions and other factors. Should one or more of these risks or uncertainties materialize, or should any underlying assumptions prove incorrect, actual results may vary materially from those expected. More information about potential risk factors which could affect our results is included in our filings with the Securities and Exchange Commission. The Company assumes no obligation to update publicly any forward-looking statements, whether as a result of new information, future events or otherwise. This presentation may include certain non-GAAP financial measures, including AFFO. Tables reconciling such non-GAAP financial measures are set forth in the appendix hereto and the Supplemental Information Package posted in the Investors section of Crown Castle’s website at http://investor.crowncastle.com.

2

Company Overview

Real Estate Provider to the Wireless Industry

4

Largest U.S. Provider of Wireless Infrastructure

5

Well-positioned for continued stability and growth with key presence in top 100 and top 50 U.S. Basic Trading Areas (BTAs) Top 100 BTAs

represent approximately 74% of U.S. population

71% of towers in top 100 BTAs

56% of towers in top 50 BTAs

Crown Castle currently owns approximately 12,000 small cell nodes and rights to use 6,200 miles of fiber

Company History

Note: Chart area represents approximate quantity of assets at fiscal year end

0

10

20

30

40

50

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Towers (in thousands)

6

AT&T Transaction

T-Mobile Transaction

and WCP Acquisitions

Global Signal Acquisition

Mountain Union

Acquisition

Disposition of UK Business

Initial Public Offering

Acquired BellSouth ,

Bell Atlantic and GTE towers

Acquired Powertel towers

Growth through Execution and Disciplined Capital Allocation

7

$2.09 $2.43

$2.77

$3.67

$4.04 to

$4.08

2010 2011 2012 2013 2014 AFFOOutlook

(1) Outlook issued on April 23, 2014

Maximize Long-Term Total Shareholder Returns

(1)

Manage our capital structure and optimize our cost of capital

Effectively allocate capital by making accretive investments

Continue to extend and secure the land underneath our towers

Leverage existing assets to drive organic growth

Maintain and improve upon industry-leading customer service to maximize opportunity

AFFO per Share

$217 $484

$843

$1,372 $1,585

$1,779 $2,057

$377

$697

$1,286

$1,854

$2,124

$2,504

$2,988

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014E

Site Rental Gross Margin Site Rental Revenue

Proven Track Record of Stability and Growth

8

(1) Midpoint of guidance issued April 23, 2014

($ in millions)

NextG, WCP and T-Mobile Transactions

AT&T Transaction

(1)

2001 – 2006 CAGR Site Rental Revenue: 13%

Site Rental Gross Margin: 17% Incremental Margin: 84%

Global Signal Merger

2007 – 2011 CAGR Site Rental Revenue: 10%

Site Rental Gross Margin: 13% Incremental Margin: 93%

Significant Opportunity to Create Shareholder Returns by Leasing Up Less Mature Towers

(1) Yield is calculated as LQA site rental gross margin divided by invested capital. (2) Represents approximate yield at time of acquisition.

15%

7%

Greater than10 years

Less than10 years

$94

$55 2.8

2.0

Greater than10 years

Less than10 years

Yield (1) Last Quarter Annualized (“LQA”) Site Rental Revenue and Tenancy per Tower

% of Towers by Years of Operation by Crown

Greater than 10 years

28% Less than 10 years

72%

~4% - 5% Initial Yield (2)

9

($ in thousands)

12% 17%

72%

Leased< 10 Years

LeasedBetween

10 - 20 Years

Owned orLeased > 20

Years

Top 50 BTA 56% Top 100

BTA 15%

Other 29%

Attractive, U.S. Focused Portfolio

10

U.S. Site Count by BTA

Crown owns or controls the land underneath sites generating 72% of site rental gross margin for greater than 20 years Approximately one-third of site

rental gross margin generated on sites where Crown owns the land

Remaining two-thirds have an approximate lease term of 30 years

Note: Components may not sum due to rounding (1) Based on LQA Q1 2014 reported site rental gross margin

Domestic vs. International Site Mix

96%

4%

Domestic

International

Crown’s U.S. site footprint is approximately 40,000 sites

56% and 71% of U.S. sites located in the top 50 and 100 markets, respectively, where leasing is expected to be the highest

The recent T-Mobile and AT&T transactions reflect Crown’s continued belief that the U.S. market represents a compelling risk-adjusted environment for capital investments

Ground Profile by Margin(1)

Compelling U.S. Market Provides Greatest Risk-Adjusted Returns

11

$29.6 $32.4

$34.3 $32.7

2012 2013 2014E 2015E

$11.12

$33.36

$50.08

Emerging Markets Developed Markets U.S.

207 338

2,700

2012 2013 2018E

Q4 2013 Monthly ARPU(1) Forecasted U.S. Mobile Data Usage(2)

(petabyte per month)

Projected U.S. Wireless Carrier Capital Expenditures ($ in billions) (3)

↑ 52% CAGR

Each of the Big 4 wireless carriers has communicated multi-year network deployment plans

Potential new entrants (e.g. Dish and FirstNet) and currently un-deployed spectrum create further growth opportunities

(1) Source: Wall Street research; weightings based on average wireless service revenues per country (2) Source: Cisco VNI, 2014 (3) Source: Wall Street Research; includes AT&T, Sprint, T-Mobile, Leap, U.S. Cellular, and Verizon

Attractive Business Fundamentals

Stable and Long-Term Contracted Revenues Long-Term Control of Assets(2)

Attractive Tower Footprint Significant Network Demand Driven by Data Usage

…weighted average remaining current term, typically with annual escalators ~ 7

Years …of site rental gross margins generated on sites that reside on owned land(3) or have 10+ year ground leases ~88%

…largest shared wireless infrastructure provider in the U.S., with attractive portfolio footprint ~40k

towers

<10 yr Leases ~12%

>10 yr Leases or Owned

~88%

…expected growth in U.S. mobile data traffic from 2013 to 2018 ~ 8x

$3

$22

LQA Q1 2014Site Rental Revenues

RemainingContracted Payments

Site Rental Revenue ($bn)

7x

338

2,700

2013 2018E

Forecasted U.S. Mobile Data Usage(4)

(PB per month)

8x

(1)

12

(1) Excludes renewals at the customers’ option (2) Based on LQA Q1 2014 site rental gross margin (3) Includes perpetual and long-term easements (4) Cisco VNI 2014

96% 4%

International (Australia) Domestic

Business Model

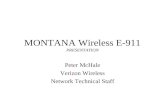

Carrier Build vs Lease Decision: Quantitative Aspects

Significant economic incentives exist for carriers to choose a shared infrastructure model over building their own site

Lower costs: Over a 10- and 20-year period, tower leasing results in cost savings of approximately $200,000 and $130,000, respectively

Better capital allocation: Yield on a carrier’s tower build is well below a carrier’s cost of capital

Carrier Build Scenario

$300,000 construction cost

$1,500 monthly operating expenses with 3% annual escalator

6.5% Weighted Average Cost of Capital (WACC)

Tower Lease Scenario

$2,200 monthly lease with 3.5% annual escalator

6.5% WACC

(1) For illustrative purposes only

Term Carrier Build Tower Lease Savings

10 years $433,541 $232,929 $200,611

20 Years $541,598 $407,967 $133,631

Carrier Build vs. Tower Leasing – Present Value of Costs Yield on Investment vs. Cost of Capital

2.8%

6.5%

Yield on Carrier Build Cost of Capital

Construction Costs [A] $300,000

Annual Rent Savings $26,400

Annual Operating Expenses $18,000

Gross Margin [B] $8,400

Yield on Investment ([B] / [A]) 2.8%

(1) (1)

14

Carrier Build vs Lease Decision: Qualitative Aspects

Factors Impacting Build vs. Lease Decision

COST

CONTROL SPEED TO MARKET

EXECUTION

Build Lease Comments

Cost Tower leasing results in lower cost to carriers and allows carriers to better allocate capital

Speed to Market

Independent tower operators have extensive tower portfolios and operational expertise necessary to help carriers quickly deploy their networks

Execution Tower leasing allows carriers to focus on their core business

Control Building a tower allows a carrier to retain control of critical infrastructure

15

Illustrative Tower Economics(1)

High Incremental Margins Associated with Lease-Up

(1) For illustrative purposes only

$8,400 (32%)

$33,800 (64%)

$59,200 (75%)

$26,400

$52,800

$79,200

One Tenant Two Tenants Three Tenants

Site Rental Gross Margin Site Rental Revenue

96% Incremental

Margin

96% Incremental

Margin

16

Recurring Long-Term Revenue Stream

Multiple tenants lease space on the tower and portions of the ground for their wireless communications equipment

Typical lease terms are non-cancellable with an initial term of 5 to 15 years with multiple 5 to 10 year renewal periods and annual lease escalators of approximately 3.5%

Leased vertical space on the tower

Weight placed on tower from equipment and coax lines

Square footage leased on the ground

Generally portfolio-based pricing based on previously negotiated agreements, not on a site-by-site basis

Source of Revenues

Factors Affecting Tenant Rent Pricing

$2,773 $2,858 $2,945 $3,019

2015E 2016E 2017E 2018E

Projected Site Rental Revenues, as Adjusted from Existing Customer Contracts (1)

High Degree of Visibility into Future Revenues

(1) Based on existing contracts as of March 31, 2014. All contracts, except for Sprint contracts associated with the iDen network and contracts where termination notices have been received, are assumed to renew for a new term at current term end date. CPI-linked customer contracts are assumed to escalate at 3% per annum. Assumes a US dollar to Australian dollar exchange rate of 0.89 US dollar to 1.0 Australian dollar.

17

High Quality Long-Term Revenue Stream

18

29%

23% 22%

14%

4% 9%

Tenants by Site Rental Revenue(1)

(1) Based on Q1 2014 site rental revenue, annualized (2) Based on latest publically available company data (3) Based on latest publically available company data; pro forma for the acquisition of Oi’s

tower portfolio in Brazil (4) Excludes renewals at the customers’ option (5) Weighted by revenue

Total: $3 billion

Remaining Contracted Cash Rent Receipts from Customer Leases

Approximately 87% of Crown’s site rental revenue is generated from the Big 4 wireless carriers

Crown estimates that remaining contracted cash rent receipts from customer leases total approximately $22 billion(4)

Crown’s leases have a weighted average remaining term of approximately 7 years(5), excluding renewals at the customers’ option

$3

$22

LQA SiteRental Revenues

RemainingContracted Receipts(1) (4)

AT&T

Sprint T-Mobile

Verizon

Australia Other

($ in billions)

7x

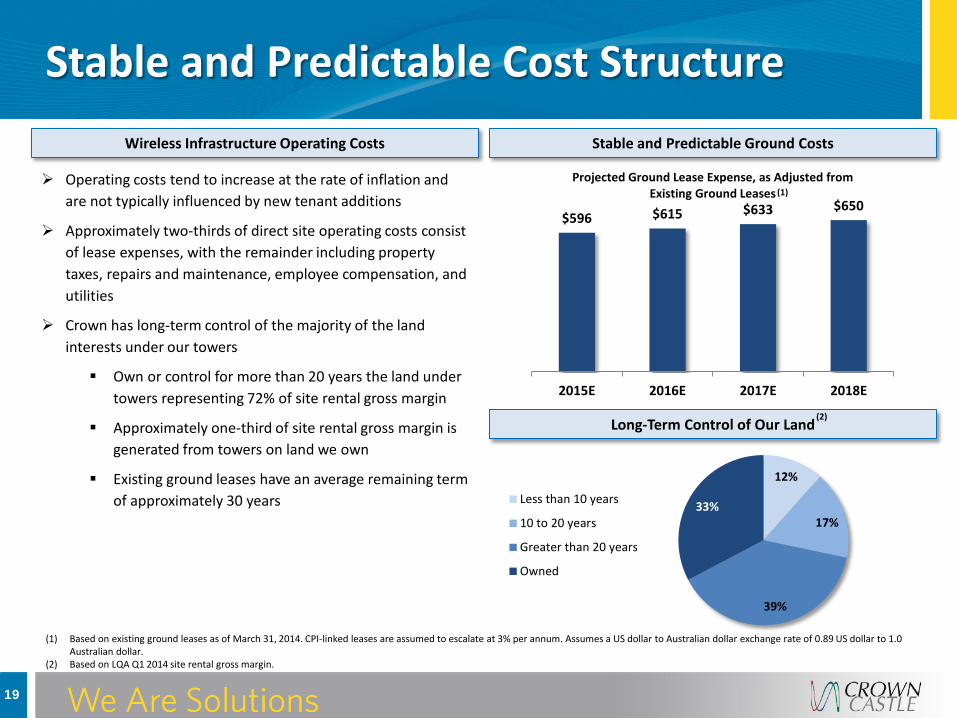

Stable and Predictable Cost Structure

19

$596 $615 $633 $650

2015E 2016E 2017E 2018E

Projected Ground Lease Expense, as Adjusted from Existing Ground Leases (1)

(1) Based on existing ground leases as of March 31, 2014. CPI-linked leases are assumed to escalate at 3% per annum. Assumes a US dollar to Australian dollar exchange rate of 0.89 US dollar to 1.0 Australian dollar.

(2) Based on LQA Q1 2014 site rental gross margin.

Operating costs tend to increase at the rate of inflation and are not typically influenced by new tenant additions

Approximately two-thirds of direct site operating costs consist of lease expenses, with the remainder including property taxes, repairs and maintenance, employee compensation, and utilities

Crown has long-term control of the majority of the land interests under our towers

Own or control for more than 20 years the land under towers representing 72% of site rental gross margin

Approximately one-third of site rental gross margin is generated from towers on land we own

Existing ground leases have an average remaining term of approximately 30 years

Wireless Infrastructure Operating Costs Stable and Predictable Ground Costs

Long-Term Control of Our Land

12%

17%

39%

33% Less than 10 years

10 to 20 years

Greater than 20 years

Owned

(2)

1.9% 1.8% 1.4% 1.3%

1.7% 1.9%

2008 2009 2010 2011 2012 2013

Low Ongoing Capital Intensity

20

Sustaining Capex as a % of Site Rental Revenues Crown’s wireless infrastructure portfolio requires minimal sustaining capital expenditures, including maintenance and other non-discretionary capital expenditures

Sustaining capital expenditures typically equate to less than 2% of site rental revenues

$222 $120 $95 $128

$270

$436

$201

$25 $109

$196

$134

$85 $27

$28 $24

$23

$37

$48

2008 2009 2010 2011 2012 2013

Revenue Generating Capex LandPurchases

SustainingCapex

Discretionary

($ in millions)

2008 2009 2010 2011 2012 2013 # of towers at

period end 22,489 22,365 23,845 23,783 31,545 41,322

Comparison to Other REITs(1)

21

(1) Wall Street research

Key Characteristics Tower Industry More Traditional Real Estate Comments

Typical lease term 5-10 years 5-10 years

Tower leases typically include multiple renewal periods at the tenant's option of 5-10 years each

Annual rent escalations 3-5% or CPI-based 1-3% or CPI-based-

Maintenance capex as % of base rent ~2% 5-15%-

Current occupancy 50-60% 90-95%

Towers are typically constructed to support three to five tenants; capacity can be increased with minimal incremental costs

Tenant concentration High LowConcentration is with the well capitalized Big 4 carriers

Industry concentration High Low-

Land ownership Low High

Crown owns or controls for greater than 20 years the land under sites representing 72% of our site rental gross margin; average remaining term of ~30 years on land leases

AFFO per share growth Teens High single digit-

AFFO multiple 15-20x 15-22x-

Industry Overview

2012 2013 2014E 2015E 2016E 2017E

Consumer video (64% CAGR) Consumer Web (46% CAGR)

Business video (60% CAGR) Business Web (48% CAGR)

Consumer file sharing (55% CAGR) Business file sharing (49% CAGR)

Secular Growth in Mobile Data Drives Demand

23

United States Mobile Data Traffic

57% CAGR (2012-2017E)

Adoption of smart connected devices that, on average, generate significantly more traffic than non-smart devices

On average, smartphones generated 48x more mobile data traffic than basic feature phones in 2013

As of March 2014, approximately 69% of U.S. mobile subscribers owned smartphones

Adoption of mobile cloud-based applications

Mobile cloud traffic is expected to increase 12x between 2013 and 2018

Consumption of mobile video applications

Mobile video traffic is expected to grow at a CAGR of 69% between 2013 and 2018, the fastest expected growth rate of any mobile application category.

Increasing mobile network speeds, which leads to increased usage

Mobile network connection speeds in North America are expected to grow at a CAGR of 21% between 2013 and 2018

Key Factors Driving Data Growth (1)

(1)

(2)

(1) Cisco VNI Mobile, 2014 (2) comScore

(1)

(1)

(1)

(petabyte per month)

$0

$5

$10

$15

$20

$25

$30

$35

$40

'95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

Demand Trends Drive Significant Ongoing Network Investment

24

U.S. Carrier Wireless Capex (billions)

1G/2G = voice & text

3G = mobile web 1.0 (Email)

4G = mobile apps & video

(1)

(1) CTIA and Wall Street research

Addressing the Rapid Growth in Data

25

0

500

1,000

1,500

2,000

2,500

3,000

2013 2018E

in P

etab

ytes

(1)

Column1

(1) Cisco VNI 2014

8x Increase

More cell sites (i.e. cell splitting), including macro and small cell architectures

Carriers can increase the density of their networks, and therefore the capacity, by adding new cell sites

Verizon and AT&T are increasingly focused on adding capacity/density to their 4G networks, while Sprint and T-Mobile are primarily focused on coverage build-out

More spectrum

Potential for the amount of deployed spectrum to double over the next several years

Technology gains, including increased spectral efficiency, associated with migration to next-generation networks (i.e. 3G to 4G)

4G download speeds can be up to 10x faster than 3G

Three Primary “Tools” for Carriers to Manage Data Growth U.S. Monthly Mobile Demand

Increasing Density of Networks

Cell Tower

Coverage weakens further away from the cell tower due to more subscribers served and spectrum limitations

Initial Buildout - Coverage

Initial networks built for voice were primarily focused on coverage

Increased Adoption - Congestion Continued Investment - Capacity

Increased number of subscriber and adoption of smartphone leads to congested networks

To meet increasing data demand and rising penetration of data-driven devices, carriers have invested in increased infrastructure

Cell splitting, or reducing the service radius served by a cell tower, allows a carrier to focus on a smaller customer population and improve quality

26

Asset Overview

28

Wireless Tower Basics Key Components of a Tower

1. Antenna Array and Platform

Tenants deploy antennas which transmits the signal between the tower and the mobile device

2. Microwave Antenna “Dish”

A specific type of antenna used for point-to-point communications, including wireless backhaul

3. Coaxial Cabling

Transmission lines that transport the signal between the antennas and the base station

4. Shelter

Structures at the base of the tower used by tenants to house their wireless communications equipment

5. Ground Space

A secure area around the base of the tower where tenants deploy their shelters and backup generators

Sample Ownership of Tower Infrastructure

29

Typical Ownership Split

Crown Castle Assets

The steel tower structure that typically has capacity for at least four tenants

The ground space, which Crown either owns or operates pursuant to a long-term lease

Customer Assets

Antenna equipment

Coaxial cabling

Shelters at the base of the tower, including all of the equipment housed in the shelters

How Do Wireless Networks Work?

30

1. Wireless networks automatically route traffic to a mobile user using a cell site with the strongest signal. The signal then travels between the handset and the tower-mounted antennas.

2. Transceivers, typically referred to as “radios” send and receive signals at a specific frequency to the mobile device

3. The base station processes the signals and send them to switching elements which then route the traffic both within and to other networks (mobile, IP or wireline)

4. Backhaul (wireline/fiber or wireless) is used to transport traffic to and from the tower to the switching elements

Non-GAAP Reconciliations

Non-GAAP Reconciliations

32

(1) Inclusive of the noncontrolling interest related to real estate related depreciation, amortization, and accretion and asset write-downs. (2) Adjusts the income tax provision to reflect our estimate of the cash taxes had we been a REIT, which predominately related to foreign taxes paid. As a result, income tax expense (benefit) is

lower by the amount of the adjustment.

Adjusted Funds From Operations for the years ended December 31, 2010, 2011, 2012, and 2013 are computed as follows:

For the Years Ended December 31,(in millions, except per share data) 2010 2011 2012 2013

Net income (loss) (311.3)$ 171.5$ 200.9$ 93.9$ Real estate related depreciation, amortization and accretion 522.5 531.9 601.4 761.1 Asset write-down charges 13.7 22.3 15.5 14.9 Adjustment for noncontrolling interest(1) 0.3 (0.4) (12.3) (3.8) Dividends on preferred stock (19.9) (19.5) (2.5) —

Funds from Operations 205.4$ 705.7$ 803.0$ 866.0$

Funds from Operations (from above) 205.4$ 705.7$ 803.0$ 866.0$ Straight-line revenue (161.7) (200.0) (251.3) (218.6) Straight-line expense 38.8 39.0 54.1 81.0 Stock-based compensation expense 40.0 36.0 47.4 41.8 Non-cash portion of tax provision(2) (29.0) 5.0 (106.7) 191.7 Non-real estate related depreciation, amortization and accretion 18.3 21.1 21.2 13.1 Amortization of non-cash interest expense 85.5 102.9 109.3 99.2 Other (income) expense 0.6 5.6 5.4 3.9 Gains (Losses) on retirement of long-term obligations 138.4 — 132.0 37.1 Net gain (loss) on interest rate swaps 286.4 — — —Acquisition and integration costs 2.1 3.3 18.3 26.0 Adjustment for noncontrolling interest(1) (0.3) 0.4 12.3 3.8 Capital improvement Capex (14.8) (14.0) (21.6) (19.3) Corporate Capex (9.5) (9.4) (15.5) (28.4)

Adjusted Funds From Operations 599.7$ 695.7$ 807.8$ 1,097.3$ Weighted-average common shares outstanding – diluted 286.8 285.9 291.3 299.3 Adjusted Funds From Operations per Share 2.09$ 2.43$ 2.77$ 3.67$

Non-GAAP Reconciliations (continued)

33

(1) Inclusive of the noncontrolling interest related to real estate related depreciation, amortization, and accretion and asset write-downs. (2) Adjusts the income tax provision to reflect our estimate of the cash taxes had we been a REIT, which predominately related to foreign taxes paid. As a result, income tax expense (benefit) is

lower by the amount of the adjustment.

Adjusted Funds From Operations for the year ending December 31, 2014 is forecasted as follo

Full Year 2014(in millions, except share and per share amounts) OutlookNet income (loss) $298 to $382

Real estate related depreciation, amortization and accretion $970 to $985Asset write-down charges $6 to $16Adjustment for noncontrolling interest(1) $(7) to $1Dividends on preferred stock $(44) to $(44)

Funds from Operations $1,276 to $1,291

Funds from Operations (from above) $1,276 to $1,291Straight-line revenue $(196) to $(181)Straight-line expense $94 to $109Stock-based compensation expense $55 to $60Non-cash portion of tax provision(2) $(10) to $5Non-real estate related depreciation, amortization and accretion $21 to $26Amortization of non-cash interest expense $75 to $86Other (income) expense $3 to $5Gains (Losses) on retirement of long-term obligations $46 to $46Acquisition and integration costs $13 to $23Adjustment for noncontrolling interest(1) $7 to $(1)Capital improvement Capex $(35) to $(33)Corporate Capex $(41) to $(39)

Adjusted Funds From Operations $1,346 to $1,361Weighted-average common shares outstanding – diluted 333.3 Adjusted Funds From Operations per Share $4.04 to $4.08