Power Transmission in India Requirements, Plans, Technologies and Regulation.pdf

27

5 th Annual Conference on Power Transmission in India Requirements, Plans, Technologies and Regulation April 30 – May 1, 2012 Key Trends and Outlook

-

Upload

surendra-mallenipalli -

Category

Documents

-

view

6 -

download

3

Transcript of Power Transmission in India Requirements, Plans, Technologies and Regulation.pdf

5th Annual Conference on

Power Transmission in India Requirements, Plans, Technologies and Regulation

April 30 – May 1, 2012

Key Trends and Outlook

Agenda

• State of the Sector

• Plans and Achievements

• Market Structure

• Regulations

• Technology Trends

• Issues and Challenges

• Conclusion

2

Sector Size and Growth

• The transmission line length has been

growing at a CAGR of 7% between 2007-

08 and 2011-12

− Growth driven by 400 kV lines

− 765 kV line length has doubled

between 2009-10 and 2011-12

− While interstate transmission lines

have grown at a CAGR of 11%,

intrastate has grown at 5% only

• Substation capacity grew at a CAGR of

9% between 2007-08 and 2011-12

− Interstate transformer capacity grew

at a CAGR of 14% while intrastate at

a much lower 7%

Growth in Line Length

Growth in Substation Capacity

3

210,004 222,746

236,467 254,536

274,882

-

50,000

100,000

150,000

200,000

250,000

300,000

2007-08 2008-09 2009-10 2010-11 2011-12

ct. k

m

273,862 292,891

310,051 345,513

383,465

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

2007-08 2008-09 2009-10 2010-11 2011-12

MV

A

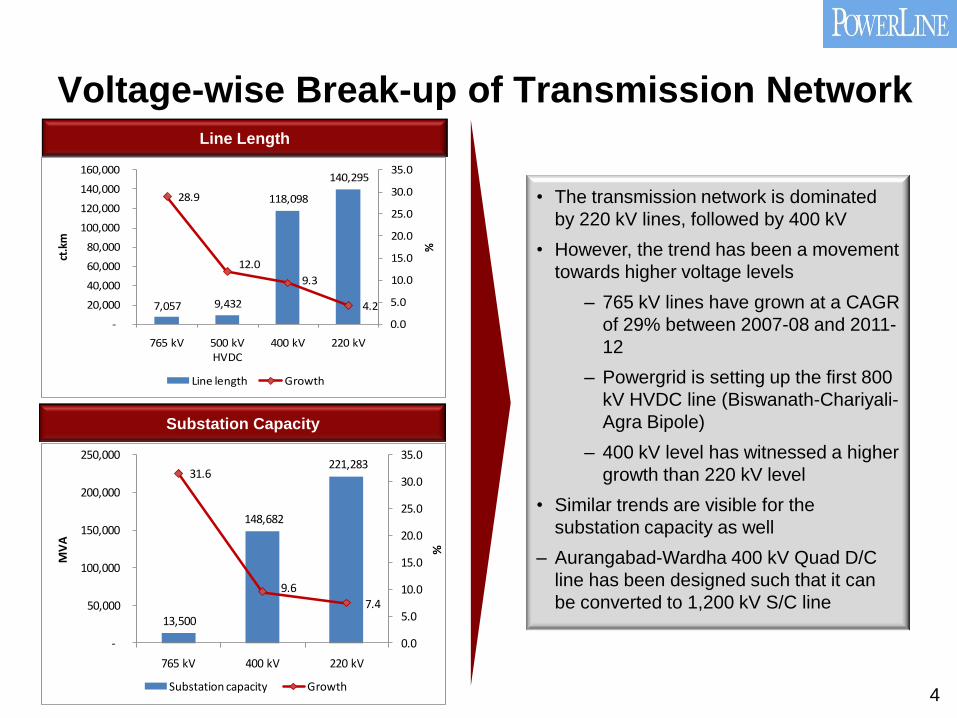

Voltage-wise Break-up of Transmission Network

• The transmission network is dominated

by 220 kV lines, followed by 400 kV

• However, the trend has been a movement

towards higher voltage levels

– 765 kV lines have grown at a CAGR

of 29% between 2007-08 and 2011-

12

– Powergrid is setting up the first 800

kV HVDC line (Biswanath-Chariyali-

Agra Bipole)

– 400 kV level has witnessed a higher

growth than 220 kV level

• Similar trends are visible for the

substation capacity as well

– Aurangabad-Wardha 400 kV Quad D/C

line has been designed such that it can

be converted to 1,200 kV S/C line

Line Length

Substation Capacity

4

13,500

148,682

221,283 31.6

9.67.4

-

50,000

100,000

150,000

200,000

250,000

765 kV 400 kV 220 kV

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

MV

A

%

Substation capacity Growth

7,057 9,432

118,098

140,295

28.9

12.0

9.3

4.2

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

765 kV 500 kV HVDC

400 kV 220 kV

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

ct.k

m

%

Line length Growth

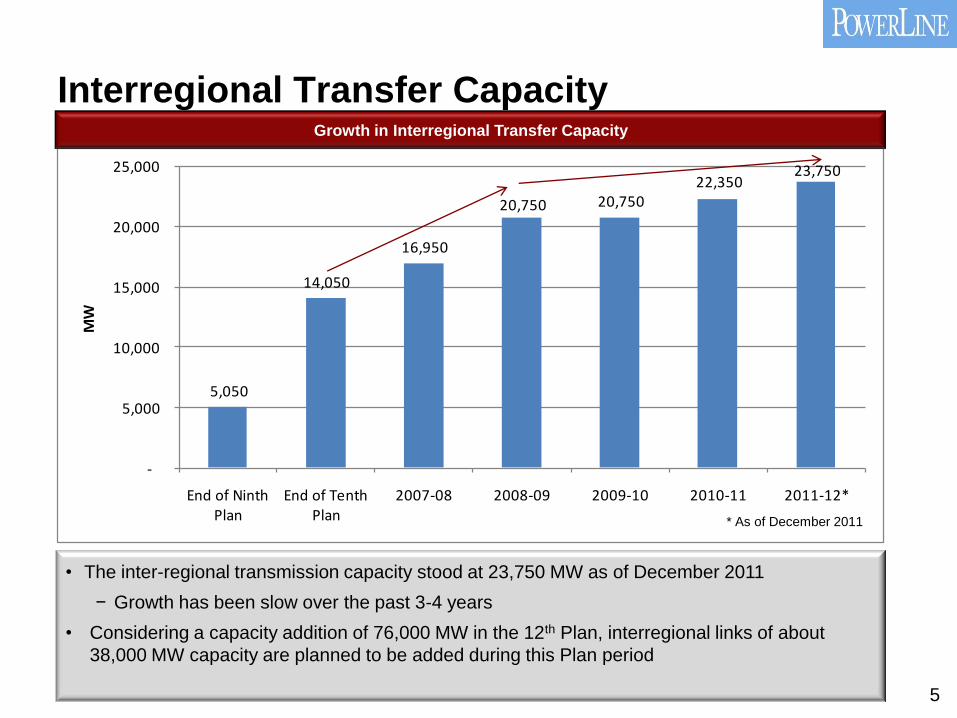

Interregional Transfer Capacity

• The inter-regional transmission capacity stood at 23,750 MW as of December 2011

− Growth has been slow over the past 3-4 years

• Considering a capacity addition of 76,000 MW in the 12th Plan, interregional links of about

38,000 MW capacity are planned to be added during this Plan period

5

5,050

14,050

16,950

20,750 20,750 22,350

23,750

-

5,000

10,000

15,000

20,000

25,000

End of Ninth Plan

End of Tenth Plan

2007-08 2008-09 2009-10 2010-11 2011-12*

MW

Growth in Interregional Transfer Capacity

* As of December 2011

Agenda

• State of the Sector

• Plans and Achievements

• Market Structure

• Regulations

• Technology Trends

• Issues and Challenges

• Conclusion

6

Eleventh Plan Targets and Achievements

• The total programme for the Eleventh Plan

was around 84,000 ct. km line length and

134,000 MVA substation capacity

• More than 69,000 ct. km line length has

been added implying 82% achievement

• Around 130,000 MVA substation capacity

has been added implying 97% achievement

• Private sector (through JVs) has

contributed 3,700 ct. km and 2,197 MVA

• 765 kV and ± 500 kV HVDC levels have

seen good growth during the Plan period

Transmission Line Length (ct. km)

Substation Capacity (MVA)

7

1,530 2,269

49,396

32,139

3,560 3,288

40,066

26,122

-

10,000

20,000

30,000

40,000

50,000

60,000

± 500 kV HVDC 765 kV 400 kV 220 kV

Programme Achievement

2,500 6,484

60,750 66,654

1,000

13,500

52,275

64,387

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

± 500 kV HVDC 765 kV 400 kV 220 kV

Programme Achievement

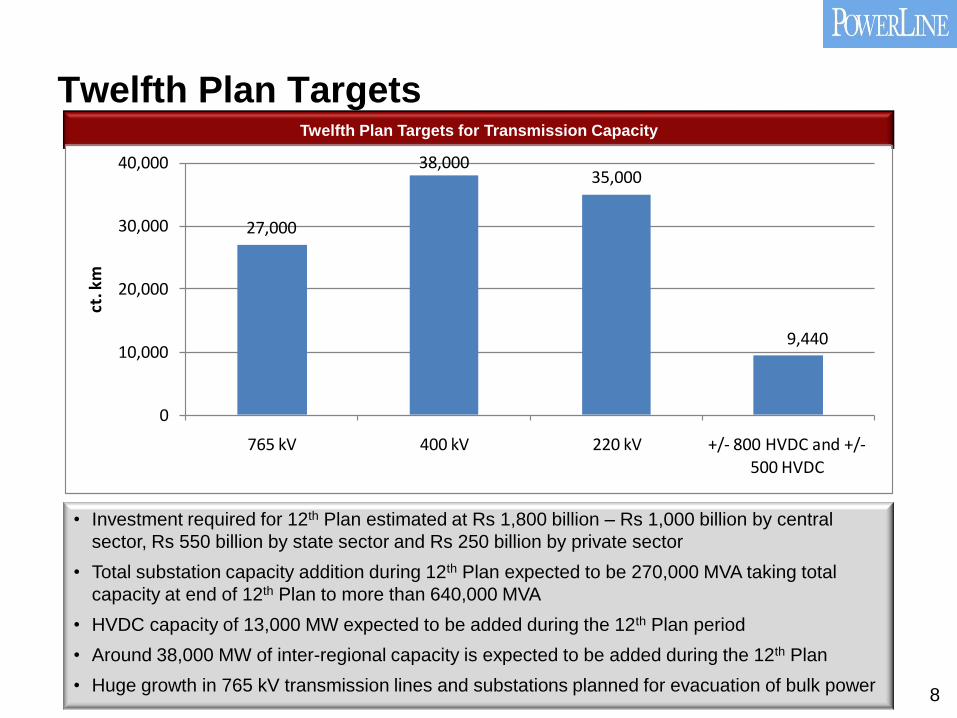

Twelfth Plan TargetsTwelfth Plan Targets for Transmission Capacity

• Investment required for 12th Plan estimated at Rs 1,800 billion – Rs 1,000 billion by central

sector, Rs 550 billion by state sector and Rs 250 billion by private sector

• Total substation capacity addition during 12th Plan expected to be 270,000 MVA taking total

capacity at end of 12th Plan to more than 640,000 MVA

• HVDC capacity of 13,000 MW expected to be added during the 12th Plan period

• Around 38,000 MW of inter-regional capacity is expected to be added during the 12th Plan

• Huge growth in 765 kV transmission lines and substations planned for evacuation of bulk power8

27,000

38,00035,000

9,440

0

10,000

20,000

30,000

40,000

765 kV 400 kV 220 kV +/- 800 HVDC and +/-

500 HVDC

ct. k

m

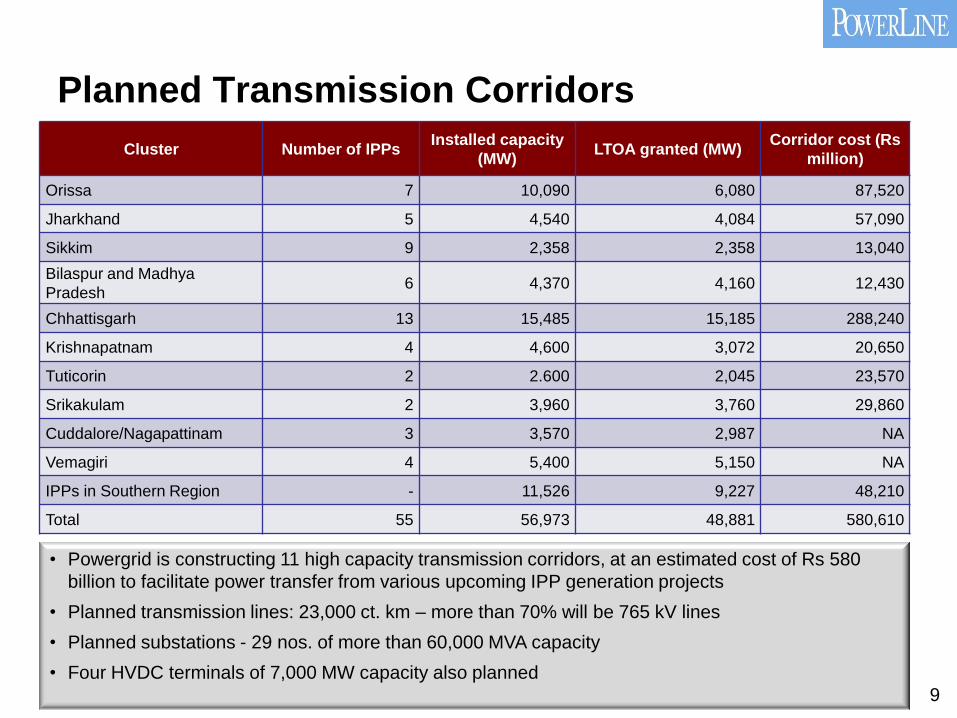

Planned Transmission Corridors

9

Cluster Number of IPPsInstalled capacity

(MW)LTOA granted (MW)

Corridor cost (Rs

million)

Orissa 7 10,090 6,080 87,520

Jharkhand 5 4,540 4,084 57,090

Sikkim 9 2,358 2,358 13,040

Bilaspur and Madhya

Pradesh6 4,370 4,160 12,430

Chhattisgarh 13 15,485 15,185 288,240

Krishnapatnam 4 4,600 3,072 20,650

Tuticorin 2 2.600 2,045 23,570

Srikakulam 2 3,960 3,760 29,860

Cuddalore/Nagapattinam 3 3,570 2,987 NA

Vemagiri 4 5,400 5,150 NA

IPPs in Southern Region - 11,526 9,227 48,210

Total 55 56,973 48,881 580,610

• Powergrid is constructing 11 high capacity transmission corridors, at an estimated cost of Rs 580

billion to facilitate power transfer from various upcoming IPP generation projects

• Planned transmission lines: 23,000 ct. km – more than 70% will be 765 kV lines

• Planned substations - 29 nos. of more than 60,000 MVA capacity

• Four HVDC terminals of 7,000 MW capacity also planned

Agenda

• State of the Sector

• Plans and Achievements

• Market Structure

• Regulations

• Technology Trends

• Issues and Challenges

• Conclusion

10

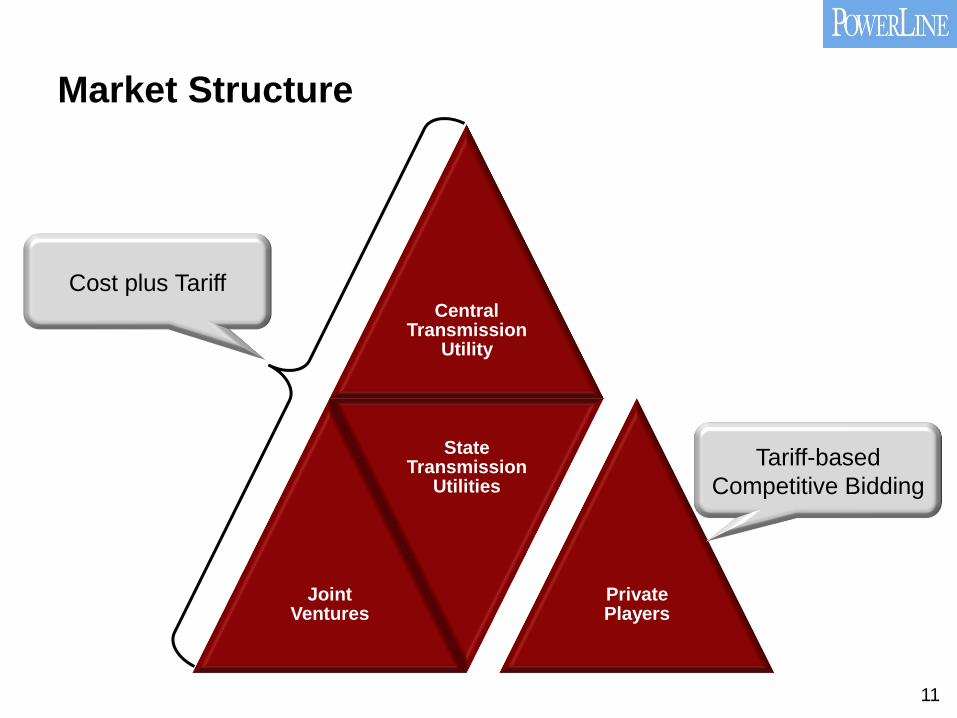

Market Structure

Central Transmission

Utility

Joint Ventures

State Transmission

Utilities

Private Players

Tariff-based

Competitive Bidding

Cost plus Tariff

11

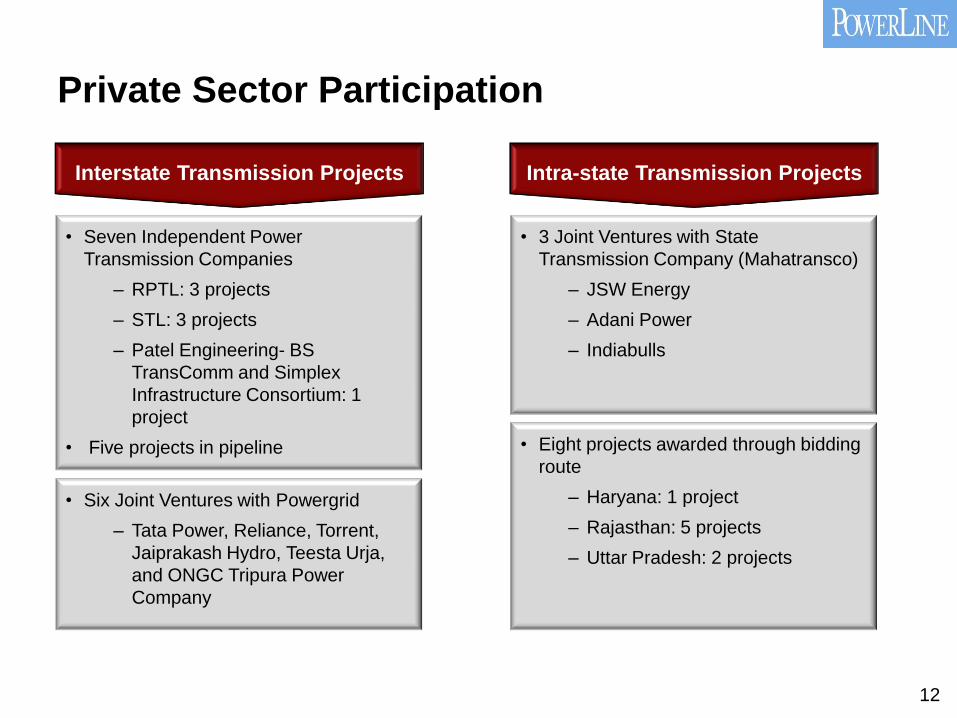

Private Sector Participation

12

• Seven Independent Power

Transmission Companies

– RPTL: 3 projects

– STL: 3 projects

– Patel Engineering- BS

TransComm and Simplex

Infrastructure Consortium: 1

project

• Five projects in pipeline

• 3 Joint Ventures with State

Transmission Company (Mahatransco)

– JSW Energy

– Adani Power

– Indiabulls

• Six Joint Ventures with Powergrid

– Tata Power, Reliance, Torrent,

Jaiprakash Hydro, Teesta Urja,

and ONGC Tripura Power

Company

• Eight projects awarded through bidding

route

– Haryana: 1 project

– Rajasthan: 5 projects

– Uttar Pradesh: 2 projects

Interstate Transmission Projects Intra-state Transmission Projects

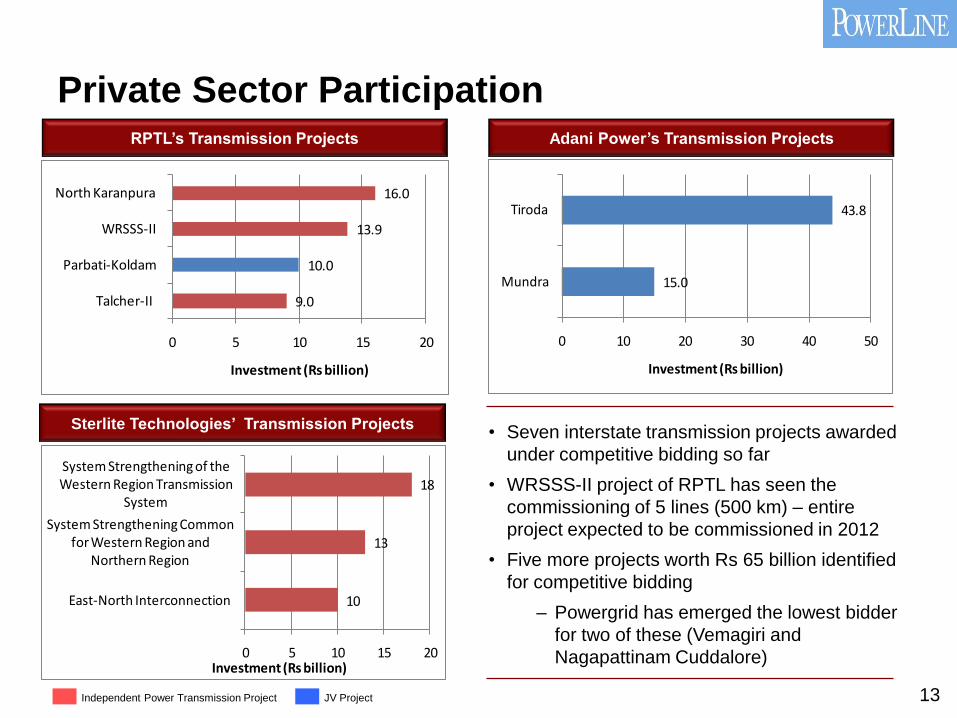

Private Sector ParticipationRPTL’s Transmission Projects

Sterlite Technologies’ Transmission Projects

Adani Power’s Transmission Projects

• Seven interstate transmission projects awarded

under competitive bidding so far

• WRSSS-II project of RPTL has seen the

commissioning of 5 lines (500 km) – entire

project expected to be commissioned in 2012

• Five more projects worth Rs 65 billion identified

for competitive bidding

– Powergrid has emerged the lowest bidder

for two of these (Vemagiri and

Nagapattinam Cuddalore)

15.0

43.8

0 10 20 30 40 50

Mundra

Tiroda

Investment (Rs billion)

9.0

10.0

13.9

16.0

0 5 10 15 20

Talcher-II

Parbati-Koldam

WRSSS-II

North Karanpura

Investment (Rs billion)

10

13

18

0 5 10 15 20

East-North Interconnection

System Strengthening Common for Western Region and

Northern Region

System Strengthening of the Western Region Transmission

System

Investment (Rs billion)

Independent Power Transmission Project JV Project 13

Private Sector ParticipationTransmission Projects of other Players

• Almost a dozen transmission systems associated with private generation projects being developed

by private players either independently or in JV with the CTU or STUs

• Maharashtra, Haryana, Rajasthan and Uttar Pradesh have implemented PPP in state level

transmission projects involving over 4,300 km of lines at investment of over Rs 25 billion

– Three projects in Maharashtra (one is operational) being executed in JV with the STU

– Projects in the remaining states have/will be awarded through the bidding route

10.0

8.6

7.0

4.53.8

3.2 3.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Jaypee Essar Power Teesta Urja JSW Energy Kalpataru and Techno Electric

Torrent Power Patel Engg, BS Transcomm

and Simplex Infra

Inve

stm

en

t (R

s b

illi

on

)

14

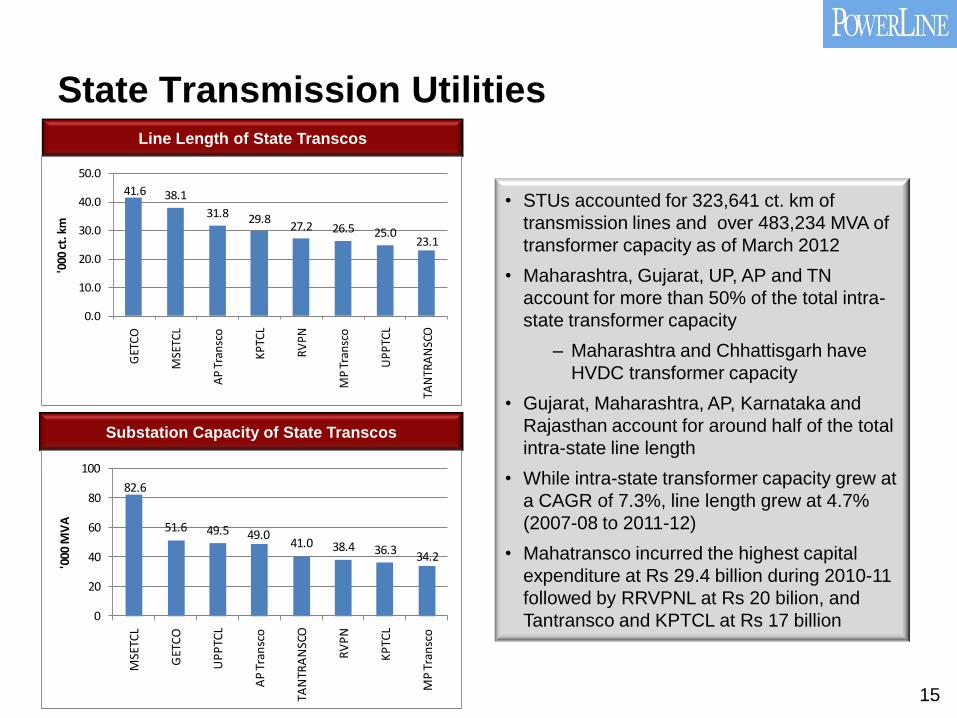

State Transmission UtilitiesLine Length of State Transcos

Substation Capacity of State Transcos

• STUs accounted for 323,641 ct. km of

transmission lines and over 483,234 MVA of

transformer capacity as of March 2012

• Maharashtra, Gujarat, UP, AP and TN

account for more than 50% of the total intra-

state transformer capacity

– Maharashtra and Chhattisgarh have

HVDC transformer capacity

• Gujarat, Maharashtra, AP, Karnataka and

Rajasthan account for around half of the total

intra-state line length

• While intra-state transformer capacity grew at

a CAGR of 7.3%, line length grew at 4.7%

(2007-08 to 2011-12)

• Mahatransco incurred the highest capital

expenditure at Rs 29.4 billion during 2010-11

followed by RRVPNL at Rs 20 bilion, and

Tantransco and KPTCL at Rs 17 billion

15

41.6 38.1

31.8 29.827.2 26.5 25.0

23.1

0.0

10.0

20.0

30.0

40.0

50.0

GET

CO

MSE

TCL

AP

Tra

nsc

o

KP

TCL

RV

PN

MP

Tra

nsc

o

UP

PTC

L

TAN

TRA

NSC

O

'000

ct.

km

82.6

51.6 49.5 49.041.0 38.4 36.3

34.2

0

20

40

60

80

100

MSE

TCL

GET

CO

UP

PTC

L

AP

Tra

nsc

o

TAN

TRA

NSC

O

RV

PN

KP

TCL

MP

Tra

nsc

o

'000

MV

A

Agenda

• State of the Sector

• Plans and Achievements

• Market Structure

• Regulations

• Technology Trends

• Issues and Challenges

• Conclusion

16

Key Regulations and their Impact

Transmission

Tariff

• Point of Connection method for sharing the cost of and losses in the

interstate transmission system (ISTS) implemented from July 1, 2011

• New pricing framework sensitive to distance, direction and quantum of

power flow

• PoC tariffs based on load flow analysis and capture utilisation of each

network element by the customers

• All designated ISTS customers are default signatories of TSA, ensuring

payment of PoC charge for use of the network

• As per amendment introduced in March 2012, there will be 3 slab rates for

injection and demand PoC charges till 2013-14

• The implementing agency will aggregate PoC charges for geographically

and electrically contiguous nodes on the ISTS to create zones within the

state boundary and arrive at a uniform zonal rate

• Any interstate generating station directly connected to the 400 kV ISTS will

be treated as a separate zone and not clubbed with other generator nodes

Connectivity

and Open

Access

• Generation stations granted connectivity to the grid allowed to inject infirm

power into the grid during testing upto 6 months after first synchronisation

• The CTU or transmission licensee to take up construction of dedicated

transmission line in phases after ensuring that advance payment for main

plant equipment orders have been made (for 500 MW and above thermal

plants and 250 MW and above hydro plants)

17

Key Regulations and their Impact

• The recent amendment has tightening of the operational frequency band

from ‘50.2 to 49.5 Hz’ to ‘50.2 to 49.7 Hz’ aimed at ensuring better

operational performance of the grid

• In the case of forced outages of generating units, the schedule of all

beneficiaries will be reduced on a pro-rata basis

• For new wind energy plants, all fluctuations within ±30% of the schedule will

be borne by all users of the interstate grid

• For solar power, there is no such band and all fluctuations for new solar

power plants have to be borne by users of the interstate grid

• Allows new wind energy generators to fine tune their schedules, based on

forecasting, as close as three hours before actual generation

IEGC

UI Charges

Amendment

• High UI charges as deterrent for overdrawl from the grid

– UI charges specified in the frequency band of 50.2 to 49.5 Hz

– A maximum UI charge of Rs 9.0 per unit is applicable at grid

frequencies below 49.7 Hz

– Additional UI charges: 49.7-49.5 Hz – 20% of the maximum UI charge;

49.5-49.2 Hz – 40% of maximum UI charge; below 49.2 Hz – 100% of

maximum UI charge

18

Agenda

• State of the Sector

• Plans and Achievements

• Market Structure

• Regulations

• Technology Trends

• Issues and Challenges

• Conclusion

19

Technology Trends

Move to higher

voltage levels

• Necessitated by the need to increase the MW flow per metre of RoW

• First line (Biswanath Chariyali - Agra bi-pole line) at 800 kV HVDC level

expected to be completed by August 2013

• Powergrid engaged in developing the 1,200 kV transmission system – UHV

AC test station is under development at Bina, Madhya Pradesh

Conductor

configurations

and materials

• Increasing the thermal capacity of the conductors and use of high

temperature low sag (HTLS) conductors to increase transmission capacity

• High Surge Impedance Loading (HSIL) technology to increase the load of

the lines

• Low resistance conductors (AL59 alloy conductors) and dull surface finish

conductors are some of the upcoming kinds of conductors.

Others

• Tower design improvements

– Compact/pole type towers for to tackle RoW issues

– Multicircuit towers

• Substation automation

• Compact substations - gas insulated switchgear

20

Smart Grid Initiatives in Transmission

21

• Key smart-grid technologies deployed in transmission:

– Synchronized Phasor Measurements using Wide Area Monitoring Systems

like PMUs

– Self Healing Power Systems

– Adaptive Islanding Systems

• Remote operations of substation – 27 unmanned substations as of today

– Setting up of National Transmission Monitoring Centre (NTMC) by 2013

– Remote monitoring and operation of 192 Substations

• Powergrid has commissioned 8 PMUs in the northern grid under the first WAMS

pilot project

– Pilot projects being implemented in other regions: Western Region (25

PMUs), Eastern Region (25 PMUs), Southern Region (6 PMUs), North

Eastern Region (6 PMU)

– Power grid plans to cover all 400 kV and above substations by installing

around 1,000 PMUs by 2015

Key Initiatives by CTU

Agenda

• State of the Sector

• Plans and Achievements

• Market Structure

• Regulations

• Technology Trends

• Issues and Challenges

• Conclusion

22

Demand

Centres

Generation

Centres

Need for bulk power

transfer over long

distance through strong

national electricity grid

Issues and Challenges

23

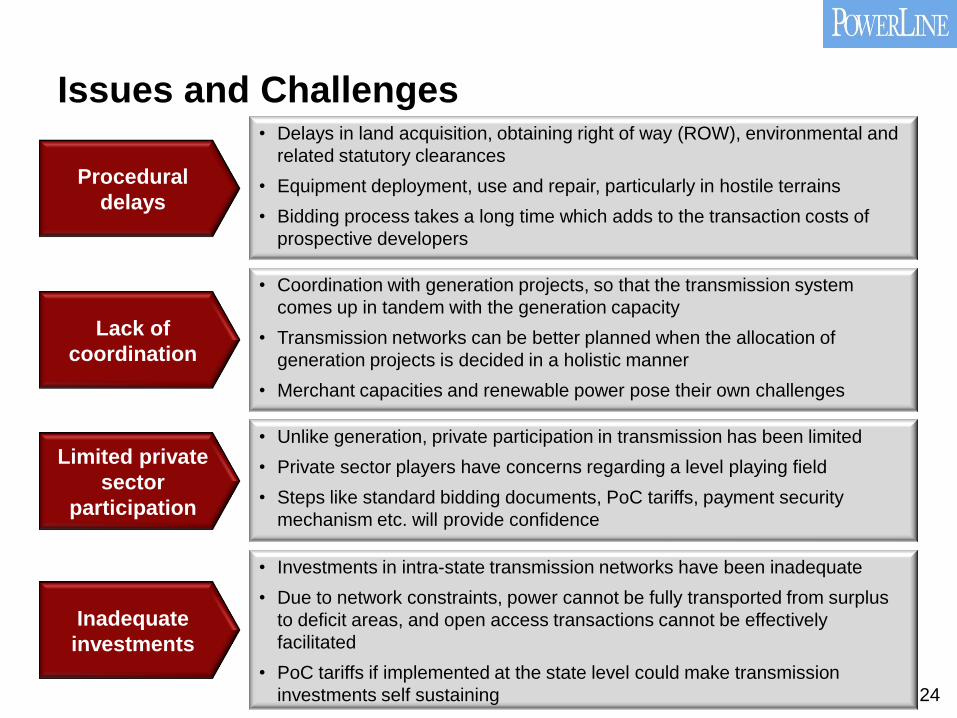

Issues and Challenges

Procedural

delays

• Delays in land acquisition, obtaining right of way (ROW), environmental and

related statutory clearances

• Equipment deployment, use and repair, particularly in hostile terrains

• Bidding process takes a long time which adds to the transaction costs of

prospective developers

Lack of

coordination

• Coordination with generation projects, so that the transmission system

comes up in tandem with the generation capacity

• Transmission networks can be better planned when the allocation of

generation projects is decided in a holistic manner

• Merchant capacities and renewable power pose their own challenges

Limited private

sector

participation

• Unlike generation, private participation in transmission has been limited

• Private sector players have concerns regarding a level playing field

• Steps like standard bidding documents, PoC tariffs, payment security

mechanism etc. will provide confidence

Inadequate

investments

• Investments in intra-state transmission networks have been inadequate

• Due to network constraints, power cannot be fully transported from surplus

to deficit areas, and open access transactions cannot be effectively

facilitated

• PoC tariffs if implemented at the state level could make transmission

investments self sustaining 24

Agenda

• State of the Sector

• Plans and Achievements

• Market Structure

• Regulations

• Technology Trends

• Issues and Challenges

• Conclusion

25

Summing Up

26

• Move to higher voltages including 765 kV, 800 kV HVDC and 1,200 kV

• Smart grid projects

• GIS substations, SCADA, ERP

• Open access, power trading, ABT regime are new sector challenges

• Transmission investments in increasing system redundancies and a strong grid

• Synchronisation of all regional grids to ensure seamless flow of power

• Targeted increase in inter-regional capacity to 75,000 MW by 2017

• 76,000 MW planned capacity addition in 12th Plan

• Generation and load centresdispersed

• High amount of renewable power capacity coming up

Generation capacity addition

National grid

Technology upgradation

Emerging requirements

Thank You

![Complete Grand Regulation[1] - pianotreff.nupianotreff.nu/tidigare_treffar/2006/Complete Grand Regulation.pdf · Complete Grand Regulation By Roger Jolly (with Eugenia Carter, ...](https://static.fdocuments.us/doc/165x107/5a86a6797f8b9a001c8d3398/complete-grand-regulation1-grand-regulationpdfcomplete-grand-regulation-by.jpg)

![0030-4[1]- Shipping regulation.pdf](https://static.fdocuments.us/doc/165x107/577ca7bd1a28abea748c88f0/0030-41-shipping-regulationpdf.jpg)