Power transactions and trends - Ernst & Young · · 2015-07-292013 review and 2014 outlook Power...

24

2013 review and 2014 outlook Power transactions and trends Global power and utilities mergers and acquisitions

Transcript of Power transactions and trends - Ernst & Young · · 2015-07-292013 review and 2014 outlook Power...

2013 review and 2014 outlook

Power transactions and trendsGlobal power and utilities mergers and acquisitions

Power transactions and trends

Matt RennieGlobal TAS Power & Utilities Leader@MattRennie_EY

IntroductionI am very pleased to introduce EY’s annual Power transactions and trends report, which presents our review of deals in 2013 and an outlook for 2014.

2013 has been an exciting and active year in power and utilities transactions. Deal volumes have risen considerably over the year — driven by industry consolidation, market reforms and continued opportunities in developing countries — and are expected to increase throughout 2014 with many large transactions now in the pipeline. Recent survey results from EY’s

point to capital being more available, with the C-suite showing a renewed interest in upstream and downstream acquisitions and a focus on innovation. In an environment of wholesale price pressure in Europe and the United States, utilities are showing they are keen to pursue cross-border transactions, where synergies can be exploited and returns can be

This edition of Power transactions and trends provides a detailed roundup of 2013 activity and, at the request of our clients, more regional information than before. We have also included

pages 8-19) in the locations that we expect to be in focus for utilities in 2014 and 2015. In particular, the Japanese electricity

far-reaching implications both for the utilities already operating in that market and for new entrants. In Africa, inbound investment from China and other countries to meet the rapid rising demand for power is leading to large and innovative opportunities for

Our global power and utilities Transaction Advisory Services

a network of over 860 professionals. Our deep expertise is one of the principal reasons our clients choose to work with us. Our goal as a practice is to grow and foster the most successful global transactions business in this sector.

Please feel free to contact me with any comments on this report and EY’s other thought leadership publications, or if EY can assist you in any way.

Contents2013: a year in review 1

Global snapshot and regional overview 4

Perspectives on the ground 7

Africa 8

Brazil 10

Gulf region, Middle East and North Africa 12

Japan 14

United States 16

2014 transaction outlook 18

EY Global TAS Power & Utility contacts 20

1Global power and utilities mergers and acquisitions — 2013 review and 2014 outlook

2013 was a strong year for power and utility transactions, with deal activity increasing over the year and volumes reaching a three-year high. At 398 total deals with a value of US$125.4b over the year, transaction activity is showing signs of recovery; these numbers represent growth of 30.1% in deal volumes and 4.1% in deal value respectively, compared to 2012.

Three drivers began to emerge in Q3 and Q4, which we expect to continue to drive activity in 2014:

1. Utilities in developed markets are rebalancing their portfolios as they deal with low wholesale prices, increasing consumer price elasticity and regulatory intervention, leading to acquisitions upstream and downstream in the supply chain.

2. Reform initiatives by governments — often in relation to rising price levels — are leading to industry unbundling in some parts of the world such as Japan and, conversely, to vertical integration in regions with government-owned entities, such as Australia.

3. Developing markets in Asia and Africa continue to receive large-scale inbound investment in response to government

Overwhelmingly, rebalancing and consolidation drove transaction activity during 2013.

Utilities rebalance and consolidate against a backdrop of low wholesale prices and excess capacity

Low expected returns in many developed markets are driving

European utilities sustained their focus on fortifying balance sheets during 2013, restructuring their asset portfolios by announcing a number of asset disposals throughout the year; 2013 saw cumulative asset divestments of around US$30b.1

1. According to EY analysis.

2013: a year in reviewRebalancing, reform and emerging markets: three dominant

drivers behind power and utility transactions in 2013.

Germany’s E.ON SE exceeded its disposal target of €15b 2 RWE AG remains keen to

explore disposal of many of its assets if reasonable valuations can be met by the market.

Low wholesale prices, weak demand for energy and increasing shares of renewable power capacity are also driving transactions elsewhere. Italy’s Enel SpA, Denmark’s Dong Energy and Finland’s Fortum Corporation announced large asset disposals during 2013.

Much of the capital raised from divestments and cost cutting has been diverted to the emerging markets of Latin America and Eastern Europe. We are also increasingly seeing utilities extend

management services, to consolidate existing market shares and focus on new areas where higher returns can be achieved. E.ON and GDF Suez were involved in multiple acquisitions of energy services companies, in Europe and elsewhere, during 2013.

2. “E.ON To Sell 73% Stake In E.ON Mitte In EUR 610 Mln Cash Deal,” NASDAQ, www.nasdaq.com/article/eon-to-sell-73-stake-in-eon-mitte-in-eur-610-mln-cash-deal-20131217-01084, accessed 17 December 2013.

Figure 1. Global P&U transaction snapshot

Source: EY analysis based on Mergermarket data

Note: regional deal breakdown excludes transactions in the Middle East and Africa totaling close to US$1.4b.

Americas Europe

Generation

US$4.4b

US$12.4b

US$10.9b

Renewables

US$6.1b

US$5.7b

US$4.6b

Integrated,water and others

US$21.8b

US$8.9b

US$17.1b

T&D

US$2.7b

US$7.5b

US$23.1b

2 Power transactions and trends

Growing numbers of utilities are also acquiring upstream assets, particularly in the UK with Centrica Plc and GDF Suez acquiring licences to explore and extract shale gas. EY’s October 2013

echoed this trend, with the utility company C-suite increasingly preferring to explore opportunities upstream and downstream in the supply chain and focus on exploiting new technologies.

The continued regulatory push for renewable power, particularly in Germany, prompted many European utilities to close or

renewable power during 2013. Financial investors, particularly pension and infrastructure funds, showed keen interest in European renewable assets over the year, reporting that the returns offered by renewable energy plants beat those for many government bonds.

US sees multiple asset sales; business case ripe for more consolidation

In the US, low wholesale prices, stringent environmental regulations and portfolio optimization by hybrid utilities

such as FirstEnergy and Dominion Resources, announced multiple asset sales during the year as part of their strategy to shift the asset portfolio towards stable, cash-accretive regulated operations. Prominent deals included Dynegy’s acquisition of Ameren’s competitive business for US$599m, Energy Capital

Resources for US$650m, and FirstEnergy’s sale of non-strategic generation assets.

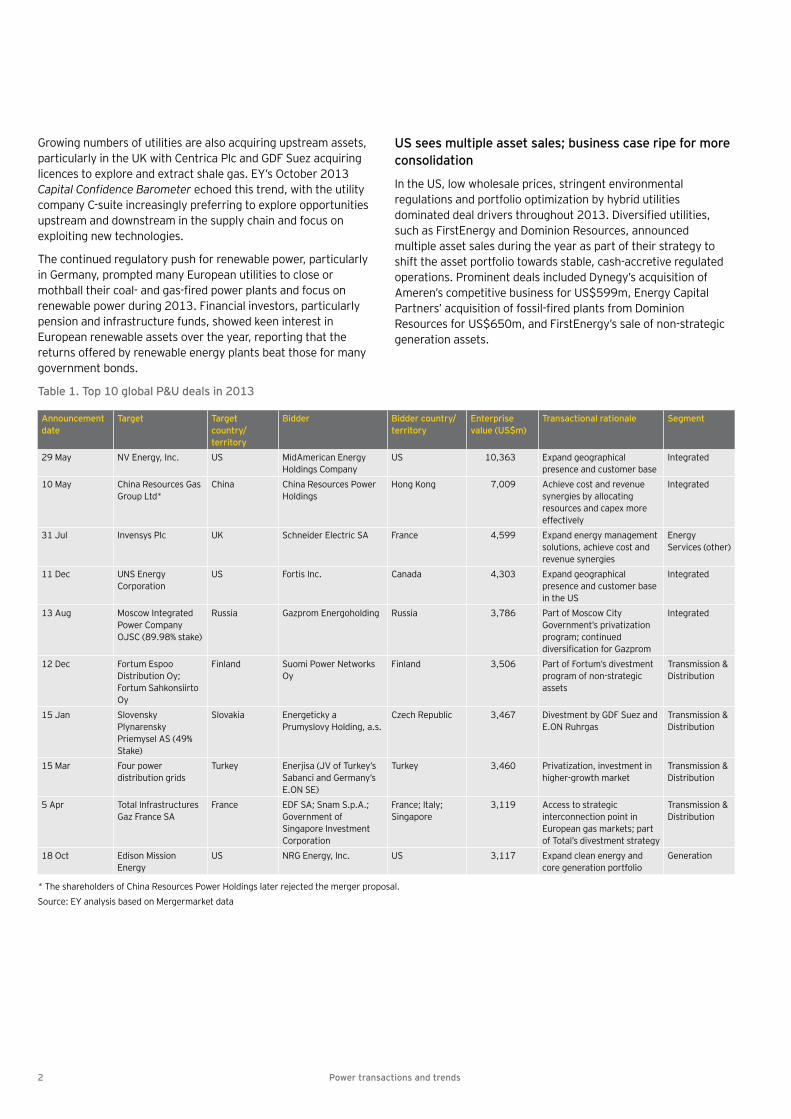

Table 1. Top 10 global P&U deals in 2013

Source: EY analysis based on Mergermarket data* The shareholders of China Resources Power Holdings later rejected the merger proposal.

Announcement date

Target Target country/territory

Bidder Bidder country/territory

Enterprise value (US$m)

Transactional rationale Segment

29 May NV Energy, Inc. US MidAmerican Energy Holdings Company

US 10,363 Expand geographical presence and customer base

Integrated

10 May China Resources Gas Group Ltd*

China China Resources Power Holdings

Hong Kong 7,009 Achieve cost and revenue synergies by allocating resources and capex more effectively

Integrated

31 Jul Invensys Plc UK Schneider Electric SA France 4,599 Expand energy management solutions, achieve cost and revenue synergies

Energy

11 Dec UNS Energy Corporation

US Fortis Inc. Canada 4,303 Expand geographical presence and customer base in the US

Integrated

13 Aug Moscow Integrated Power Company

Russia Gazprom Energoholding Russia 3,786 Part of Moscow City Government’s privatization program; continued

Integrated

12 Dec Fortum Espoo Distribution Oy; Fortum Sahkonsiirto Oy

Finland Suomi Power Networks Oy

Finland 3,506 Part of Fortum’s divestment program of non-strategic assets

Transmission & Distribution

15 Jan Slovensky Plynarensky

Stake)

Slovakia Energeticky a Prumyslovy Holding, a.s.

Czech Republic 3,467 Divestment by GDF Suez and E.ON Ruhrgas

Transmission & Distribution

15 Mar Four power distribution grids

TurkeySabanci and Germany’s E.ON SE)

Turkey 3,460 Privatization, investment in higher-growth market

Transmission & Distribution

5 Apr Total Infrastructures Gaz France SA

France EDF SA; Snam S.p.A.; Government of Singapore Investment Corporation

France; Italy; Singapore

3,119 Access to strategic interconnection point in European gas markets; part of Total’s divestment strategy

Transmission & Distribution

18 Oct Edison Mission Energy

US NRG Energy, Inc. US 3,117 Expand clean energy and core generation portfolio

Generation

3Global power and utilities mergers and acquisitions — 2013 review and 2014 outlook

strengthen their portfolio at a time of relatively low valuations. The Carlyle Group, for example, invested more than US$1.2b in power assets after the acquisition of Cogentrix in late 2012.3

the 823 MW Red Oak natural gas power plant in New Jersey, as 4

The slow demand growth outlook makes the business case ripe for further consolidation, as seen from some of the megadeals undertaken during the year. Large utilities and conglomerates with proven experience in managing service territories in multiple jurisdictions remained at the forefront, acquiring utilities with

MidAmerican Energy Holdings announced the acquisition of NV Energy, Inc., a Nevada-based public utility, for US$10.4b and TECO Energy signed an agreement to buy New Mexico Gas Company for US$950m. The NV Energy, Inc. deal was the largest deal in the sector for 2013. The healthy premium offered on both

revenue stream, favorable regulatory environment and revenue upside opportunities.

The trend continued in the latter part of the year with NRG Energy, Inc. expanding its core generation and wind power holdings by acquiring Edison Mission Energy for US$2.64b in the fourth quarter. Separately, Washington’s Avista Corporation announced its expansion into the state of Alaska with the

Investment and activity continues in emerging markets and cross-border activity remains strong

2013 saw a growing number of utilities looking beyond their primary markets and expanding their global footprints.

European utilities tended to acquire assets in the emerging markets of Latin America, Eastern Europe and Africa. Chinese investors continued to focus on expansion into a much wider range of areas across the world, supported by their surplus forex reserves and in response to domestic policies to reduce the

3. “The Carlyle group to acquire six power plants in California, New Jersey,” Marketwatch, 9 September 2013.4. “Carlyle to acquire 823-MW NJ gas plant after closing purchase of 5 Calif. Plants,” SNL Financial, 9 September 2013.

extent of domestic carbon-intensive generation. Li Ka-shing’s Cheung Kong Holdings Ltd and partners agreed to buy Dutch

processing investment by Cheung Kong Holdings Ltd in the year following the US$405m purchase of New Zealand’s EnviroWaste announced in January.

electricity transmission company acquired a 60% stake in SPIAA and a 19.9% stake in SP AusNet, both Australian assets owned by Singapore Power. The company had earlier acquired a 40% stake in South Australian electricity supplier ElectraNet.

in Europe during 2013 in search of stable returns. 2013 also saw

and waste management utilities in Europe. Sumitomo Corporation

Water PLC for about US$260m in February. We expect that the 5 will also see

Asian and European investors begin to assess the potential for returns in the newly deregulated market.

from 11.7% to 36.1% in March 2013. E.ON followed this with the

oil and gas company OGX Petroleo e Gas Participaçoes SA. Enel

growth, along with Africa.6

Canadian utility investors remained keen to pursue transactions in the US regulated utilities’ market. In December 2013, Canada’s Fortis Inc. acquired Arizona-based UNS Energy Corporation for US$2.5b, which represents the utility’s second acquisition in the US in two years, after the US$969m acquisition of CH Energy Group, Inc., which was completed in June 2013. Watch out for more strategic cross-border deals in the coming months.

5. “Japan passes law to launch reform of electricity sector,” Reuters, www.reuters.com/article/2013/11/13/japan-power-deregulation-idUSL4N0IY08820131113, accessed 13 November 2013.6. “Enel Green Power looks to Africa, Latin America for growth,” Reuters, www.reuters.com/

6 November 2013.

4 Power transactions and trends

0

30 21.7 26.0

47.9

19.027.6 25.3

33.0 31.7 35.560

90

120

150

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Total deal value (US$b) Deal volume

Global snapshot and regional overviewDespite the impact of broad macro themes, today’s transaction

transformation within each region.

Figure 2. Global P&U deal value and volume Q4 2011-Q4 2013

Source: EY analysis based on Mergermarket data

Figure 3. Segment contribution to total deal value (US$b) Q1 2012-Q4 2013

Source: EY analysis based on Mergermarket data

0

10

20

30

40

50

60

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Generation T&D Renewables Others

2013 was a strong year in terms of power and utility deal activity, with each quarter seeing a steady increase in deal volume and three of the four quarters seeing deal value exceed US$30b. While many of the large billion-dollar-plus transactions involved

integrated utilities, particularly in Europe and the US, renewables deals dominated the overall transaction volume, accounting for

overview of 2013 transactions.

Americas

Deal activity in the Americas increased by 36% over the year; the US gas surplus and sustained interest from European investors in the growing markets of Latin America drove transactions in the region.

Improved credit quality and low interest rates sustained activity in capital markets. While there have been recent rises in interest rates, there is evidence of improved access to capital, which will fuel activity in 2014.

A number of larger utilities acquired smaller/mid-size utilities outside their territories during the year; new acquisitions boosted the predictability

distributed generation continue to reduce energy demand in the US.

Latin America emerged as a hot spot for European investors looking to diversify. 2013 saw deal volumes rise by over 45%, focused on hydro and

attracting investor attention. Wind power is emerging as a competitive source of energy in the region.

According to Spanish utility Iberdrola’s Chairman and CEO Ignacio Galan, up

and Mexico, where the company expects higher growth and stability.7

Uncertainty in relation to the generation mix in Japan incentivized Japanese investors to pursue outbound investment in 2013 with investments in generation and shale gas assets in the US.

7. “Iberdrola bets on foreign grids as EU utility industry struggles,” Reuters, http://uk.reuters.com/article/2013/10/22/iberdrola-strategy-idUKL5N0IC07F20131022, accessed 22 October 2013.

Announcement date

Target Target country/territory

Bidder Bidder country/territory Enterprise value (US$m)

29 May NV Energy, Inc. US MidAmerican Energy Holdings Company US 10,36311 Dec UNS Energy US Fortis Inc. Canada 4,30318 Oct Edison Mission Energy US NRG Energy, Inc. US 3,1175 Jul Energisa SA 2,0772 Jul Midland Cogeneration Venture US GSIA: a consortium of pension funds Japan; Canada 2,000

Source: EY analysis based on Mergermarket data

5Global power and utilities mergers and acquisitions — 2013 review and 2014 outlook

Europe

The prolonged energy crisis in Europe provided an impetus for utilities to actively divest and diversify, increasing the number of transaction by 19% over the year. Fewer large deals in Q4 resulted in deal value declining by 19% over the year.

Disposals of non-core assets remained the key driver of M&A activity in the region, with utilities increasingly exploring organic and inorganic growth

and Southeastern Europe.

Announcement date

Target Target country/territory

Bidder Bidder country/territory

Enterprise value (US$m)

31 Jul Invensys Plc UK Schneider Electric SA France 4,59913 Aug Moscow Integrated Power Company Russia Gazprom Energoholding Russia 3,786

12 Dec Fortum Espoo Distribution Oy; Fortum Sahkonsiirto Oy

Finland Suomi Power Networks Oy Finland 3,506

15 Jan Slovensky Plynarensky Priemysel AS Slovakia Energeticky a Prumyslovy Holding, a.s. Czech Republic 3,467

15 Mar Toroslar power distribution grid; Ayedas power grid; Vangolu, or Lake Van power distribution network; Dicle network

Turkey Enerjisa; Turkerler Insaat; Iskaya Dogu OGG

Germany, Turkey 3,460

Source: EY analysis based on Mergermarket data

8. “Next steps for shale gas production,” Department of Energy & Climate Change, UK, 17 December 2013.

2013 saw a number of acquisitions of upstream shale and natural gas assets

gain further momentum with the UK Government announcing favorable policies for exploration of shale gas and publishing a regulatory roadmap to 2020, which many see as favorable to shale oil and gas developers. The

be produced by 2020 in the UK, which is close to three times the country’s current gas demand.8

largely attributed to heightened interest in regulated electricity transmission

the globe, evidenced by the acquisition of NET4GAS from RWE AG by Germany’s Allianz Capital Markets GmbH and Canada-based infrastructure

With utilities such as E.ON, Vattenfall, Veolia and Fortum planning large asset sales, divestments are expected to dominate the M&A portfolio in Europe.

6 Power transactions and trends

$3.2b,* 2 deals

$0.6b, 3 deals

$1.1b, 7 deals$7.3b, 11 deals $1.4b, 2 deals

$1.7b, 8 deals

Flow of funds (M&A 2013)

revealed, but industry estimates peg the value at approximately US$3.2b. Source: EY analysis.

Announcement date

Target Target country/territory

Bidder Bidder country/territory

Enterprise value (US$m)

10 May China Resources Gas Group Limited*

Hong Kong China Resources Power Holdings Co Ltd Hong Kong 7,009

17 Dec AustraliaPipeline Trust)

Australia 3,105

18 Nov Castle Peak Power Company Hong Kong CLP Power Hong Kong Ltd.; China Southern Power Hong Kong 3,096

5 Feb LongTan Hydropower Development China Guangxi Guiguan Electric Power Co. Ltd. China 2,485

19 Oct Guodian Anhui Power Co. Ltd. China GD Power Development Co. Ltd. China 1,600

Source: EY analysis based on Mergermarket data* The shareholders of China Resources Power Holdings later rejected the merger proposal.

space in 2013, driving a 43% increase in deal activity and 15% increase in deal value over the year.

China dominated the transaction markets, leading both domestic and cross-border deals in the region. Domestic consolidation, particularly in the gas T&D market, produced several megadeals in the region. The domestic deals in the country accounted for over US$15b of deal value, excluding the US$7b proposal to merge China Resources Power Holdings with China Resources Gas Group, which was later rejected by the shareholders.9

bloomberg.com/news/2013-07-22/china-resources-power-shareholders-reject-merger-plan.html, accessed 22 July 2013.

Attractive valuations and distressed assets have encouraged investors in China and Japan to explore growth opportunities in developed markets. While China’s largest utility picked up stakes in electricity T&D assets in Australia, Japanese investors were active in Europe, acquiring key regulated assets in the region.

Privatization of utility assets in Australia and New Zealand sought to attract interest from investors across the globe. New Zealand emerged as the global

in 2013.10 The government sold a 49% stake in Meridian Energy, raising close to US$1.56b.

In Australia, the New South Wales Government initiated a privatization program for its electricity assets with the sale of power plants owned by Eraring Energy and Delta Electricity in mid-2013. The Government has also recently announced AGL Energy as the successful bidder for the State’s

AUD$1.7bn.

While we expect privatization programs in Oceania and consolidation in China to continue to contribute to deal activity in the region, we are carefully watching the deregulation of the Japanese utility sector, which may set the scene for revitalized M&A activity in the near to medium term.

The Wall Street Journal, http://online.

5 November 2013.

Volume Value (US$b)China - Australia 2China - Europe 2 1.4Japan - US 3 0.6Japan - Europe 8 1.7Europe - Latin America 7 1.1Canada - US 11 7.3

7Global power and utilities mergers and acquisitions — 2013 review and 2014 outlook

In the last few editions of Power transactions and trends, readers will have noticed an increasing focus on the markets of Japan, Africa and the Americas. These areas have been particularly interesting during 2013, not only because they have been host to a number of large and complex transactions, but because they are expected to see increased activity from 2014 to 2017. They

in markets that are at quite different stages of development.

The recently announced reforms in Japan, comprising the unbundling of its 10 vertically integrated monopolies, the introduction of competition and the inevitable increase in the complexity and range of the regulatory regime, will alter the Japanese market and its composition fundamentally. Our interview with Kenneth Smith, Managing Partner of EY’s

The African market, and its diversity, is similarly exciting. With 54 countries in Africa, a population of over 1 billion,11 and a need for around 30 GW of new installed capacity by 2030, we are seeing extraordinary demand for inbound investment and activity. This report features an in-depth interview with EY Africa TAS

meeting the needs of inbound and resident utility clients looking

This edition also features interviews with our Americas TAS Power & Utilities Leader, Joseph Fontana, our South America TAS Power & Utilities Leader, Lucio Teixeira, and our Middle East TAS Power & Utilities Leader, David Lloyd. Participants in these markets are rebalancing their portfolios in response to commercial and institutional drivers, and there are considerable opportunities as a consequence.

it will be in 2014 and 2015. With Chinese, US, Middle East and Japanese investors potentially looking to outbound investment in higher-yield markets, there are opportunities for reforming governments, if they are conscious of the needs of investors, to attract new capital. We expect to see transaction volumes rise in 2014 as the North American market continues to consolidate, Africa and the Middle East continue their expansion and reform programs, and Japan calls out its intentions on its energy market transformation and starts to make serious inroads on implementation.

In all cases, governments will need to work actively to attract new capital and be conscious of the signals they are sending to equity and debt providers. While our surveys suggest that capital is becoming more available, a careful approach to the

governments commencing reform programs.

Perspectives on the ground

Power transactions and trends

2013 was a year when a number of African countries continued to lay the groundwork for a different kind of future. Market reform and the development of new generation capacity are changing the face of the power sector on the continent.

the lack of reliable electricity is putting a brake on economic growth. Combined with

participation in the electricity sectors in South Africa and Nigeria), individual countries’ responses to climate change commitments and new resource discoveries, this is a recipe for change.

There’s also increased awareness that the private sector has a key role to play in introducing private capital, innovation, new technology and in supporting skills development and new industries.

Large-scale transactions for Nigeria and South Africa

One of the biggest deals in 2013 was the privatization of Nigeria’s electricity companies. The sale of 5 generation and 10 distribution companies attracted strong interest from several international players, including:

Development, PSL Engineering), which acquired Ughelli Power for US$300m

Mainstream Energy Solutions, which acquired Kainji Power for US$100m

North-South Power, which acquired Shiroro Power for US$100m

The transaction appears to have run successfully, with ownership transferring in November 2013, but it’s too early to really understand the true value inherent in the deal.

Deals change the face of Africa’s powerThose closest to African markets seem to be the most bullish about it. So what is really happening on the ground?

“ There is now a sense of urgency about investing in Africa, with widespread agreement that the lack of reliable electricity is putting a brake on economic growth.”

EY

8

Brunhilde Barnard Africa TAS Power & Utilities LeaderJohannesburg, South [email protected]

Africa

Perspectives on the ground

9Global power and utilities mergers and acquisitions — 2013 review and 2014 outlook

Falling outside the traditional deal structure was another massive undertaking: South Africa’s Renewable Energy Independent Power Producer Procurement Program. This is being run by the Department of Energy, which has already procured 2.4 GW of renewable energy. Since 2012, 47 projects worth circa US$7.6b

under construction. In 2013, a further 17 projects with a capital value of US$4.4b and representing 1,456 MW were awarded

in 2014. This program is setting the foundation for an active and vibrant private sector participation in South Africa’s electricity supply industry.

According to our EY Africa Attractiveness report, nearly 40% of all infrastructure project activity and one-quarter of the more than US$700b in estimated project value was directed into the power sector. We expect to see sustained activity in this area.

development of new build base-load projects with the private sector acting as strategic partners, as well as projects under the US Power Africa initiative and the European Union’s Sustainable Energy for All initiative. South Africa’s renewables procurement program may well serve as a blueprint for other countries, both on the continent and

Navigating through a complex market

Those outside the African market can be daunted by its complexity, with 54 countries

and holds considerable opportunity. Our advice to investors is:

1) First, identify geographies where the groundwork has been done and governments have commenced programs. This indicates that the preparatory work has been done or there are clear advances toward implementation, a legal and regulatory framework is in place or under active development, and contracts will be enforced. In

strong political and operational program leadership before committing.

often been followed by lengthy time frames before action. For example, the 2013 privatization of Nigeria’s electricity sector took place eight years after legislation

insight and expertise to avoid “knocking on doors that no one is yet ready to open,” which could result in frustration and unnecessary expense.

new frontier. Huge offshore gas and coal discoveries in Mozambique suggest it will be amongst the leading producers worldwide, and it has a relatively stable political and economic environment. Substantial gas deposits have also been found in Tanzania and Uganda, increasing the attractiveness and pipeline of deals in the East African region, for example.

Careful planning, continuous monitoring and evaluation of strategy, together with

adaptability are needed to capitalize on African opportunities.

Outlook for 2014

Past not a predictor of the future

One of the advantages of an emerging market is its ability to leapfrog technologies, which creates completely different development curves and timescales. Investors need to understand that the past is not a predictor of the future and not simply assume that emerging countries will follow the path of more established markets.

I, together with my colleagues at EY, am unashamedly optimistic about Africa. It is exhilarating to be part of South Africa’s ground-breaking renewables program, for example. Decision

on a country’s, a region’s and a continent’s competitiveness, as well as on the quality and pace of human and economic development. Working in a sector that is making a long-term positive change to people’s lives is exhilarating.

Power transactions and trends10

Strategy rethink impacts M&AFollowing the market reform of the previous year, utilities reconsidered their strategy in 2013 and set about rebalancing

construction is creating multiple transaction opportunities. Report by Lucio Teixeira.

2013 saw utilities adjusting to the new market environment. There are still plenty of

destinations of emerging market investments. The previous year’s regulatory changes cut into some generation and transmission revenues with a consequent impact on

12 This drove portfolio rebalancing and consolidation in the regulated market.

Wind power continues to rise as government focuses on increased capacity

plan that calls for more than US$85b of investment in electricity generation through 2022 to support national growth targets and meet increased energy demand.

Government-run auctions of rights to run generation assets were based on renewable generation. Wind power continued to be a competitive source of energy in the wholesale

97 of the 119 successful energy projects in the latest round of auctions and 67% of

renewable energy developer Renova Energia. Other utilities, including CPFL Energia and

opportunities. A large number of wind farms are currently in construction and many more are due to start soon, which could increase deal opportunities for overseas and domestic investors in coming years.

12. See Power transactions and trends - 2012 review and 2013 outlook, EY, January 2013.

“ Overseas investors are increasingly using their established

platform to grow in the region … We think this could lead to a much more integrated South American market in the next few years.”

Lucio Teixeira EY

Perspectives on the ground

Lucio TeixeiraSouth America TAS Power & Utilities Leader Sao Paulo, [email protected]

11Global power and utilities mergers and acquisitions — 2013 review and 2014 outlook

deal activity in 2014.16

but companies held back because they were concerned to understand the market and the new regulation better before progressing to investments. Now that the market has settled, utilities can come forward to take opportunities. 2014 will be a year to consolidate plans made in 2013.

Meanwhile companies from, for example, Chile and Peru are also continuing to

South American market in the next few years, with a potential knock-on effect on the number of deals done.

16. EY’s latest is at its highest point in two years, and 93% of executives interviewed considered credit either stable or improving — also the highest level in two years.

Distressed asset sale boosts Energisa; Eletrobras rethinks strategy for distribution

15 included the sale of distressed assets belonging to Grupo Rede Energia, a

victorious buyer and, as a result, will increase its presence in

reported losses in its quarterly and annual results in 2013 and has embarked on a restructuring program. The company is seeking approval from the Government to sell its six distribution

2012. It’s still far too early to say whether deals will crystallize as a result, but the market will certainly be anticipating this.

15. See page 4.

On the transmission front, the Government is also using the auction mechanism to increase grid coverage and connect ongoing and planned generation projects. The 2013 auction of rights to build and operate new transmission lines and substations

with a Spanish and a Chinese company each taking just one lot

regulator ANEEL.13

Meanwhile, a large number of further projects are ready to go to auction once the price is right. Rather than wait, some players are studying alternatives to sell energy to large consumers, independently of the auction process.

Brazil attracts investments from top European utilities

Germany’s E.ON SE was among the year’s big inbound European

11.7% to 36.1% in March 2013. MPX owns close to 15% of

10 GW of thermal and renewable power capacity. Enel Green

growth.14 The company’s business unit, Endesa, is seeking to

Chile) by 2017.

13. Winning offers were determined by whoever accepted the lowest annual revenue to operate the assets.14. “Enel Green Power looks to Africa, Latin America for growth,” Reuters.com,

24 January 2014.

Outlook for 2014

Power transactions and trends

or public sector-owned monopolies largely operating in an administered rather than competitive environment, there is not a lot of private sector to private sector M&A. Transaction activity is largely based on participation of the private sector in capital projects and commercial undertakings.

As markets and competition in generation becomes more established, we expect growth rather than consolidation to be a dominant driver of activity, and more deals to be done between state-owned businesses and the private sector.

That said, deals are being done, both between companies already based in the Gulf and between international players. In an interesting move, a Saudi Arabian public pension agency picked up 19.4% of ACWA Power, an independent Saudi power company with a mixture of public and private shareholders. We’re likely to see more of these kinds of transactions.

Another interesting deal was the acquisition of Amendis and Redal, providers of water, wastewater and electricity services, by the UK’s Actis Capital LLP from Veolia Services à l’Environnement Maroc SA17 for an estimated US$481.4m, in a leveraged buyout transaction.

Gulf countries subsidize utility end users heavily,18 but the rate of population growth is creating concern about possible future budgetary constraints. This has created a

way utility enterprises operate. In turn, this is likely to open up opportunities for private

and provision of utility services.

Several Gulf markets are in the early stages of electricity and water market reform, with Oman and Abu Dhabi among the most advanced: these two have already introduced a degree of utility unbundling, independent regulation and partial market structures

17. A business unit of Veolia Environnement SA’s Veolia Water SA.

and gas prices.

Domestic focus for dealsWith market reform gaining momentum, utility unbundling and the increasing role of the private sector in both generation and water could boost opportunities for large-scale transactions in the future. Renewables looks to be a fertile growth area. Report by David Lloyd.

Gulf region, Middle East and North Africa

“ Even the hydrocarbon-rich countries realize that capital resources are not limitless, given the amount they need to invest in generation and subsidies. There’s

switching fuel sources and raising capital from the private sector around the IPP model.”

David Lloyd, EY

12

Perspectives on the ground

David LloydMiddle East TAS Power & Utilities Leader Riyadh, Saudi [email protected]

13Global power and utilities mergers and acquisitions — 2013 review and 2014 outlook

As this process continues, we will see further transaction activity associated with commercialization and unbundling, as well as large-scale development of publicly owned power and water companies.

Some appetite for outbound investment; main focus is domestic

A number of Middle East funds are also planning to diversify their investments and acquire assets across the globe. For example, Kuwait and Qatar’s sovereign wealth funds were eyeing the UK utility sector in 2013.19 Saudi Arabia’s ACWA Power has recently started to internationalize20

quasi-sovereign) is already the owner of several large-scale renewable assets internationally. Several other utilities in the Gulf

IPP-type companies, which can compete in international markets for new projects using their substantial capital base and their

at Hinkley Point in the UK. The Kuwait Investment Authority plans to invest as much as US$5b

20. For example, the company is currently pursuing a power-generating opportunity in Turkey.

Even the hydrocarbon-rich countries of the Gulf recognize that their resources and capital may not be limitless, given the massive investment needed in generation and

private sector around the IPP model.

is renewables — mainly solar and some wind. Several substantial renewable energy

will see extensive use of IPPs, with foreign private sector capital coming in to fund, build and operate renewable energy plants.

between international and domestic companies, with the international companies contributing their renewables expertise and local partners drawing on their local knowledge of land, regulation, environmental issues and power off-take permitting. The Middle East continues to be one of the world’s biggest markets for IPPs, and a number of global independent power companies are active in the region and continually looking at new projects.

Institutional investors might consider ways to play in this developing renewable

are structured, this is probably more of a long-term play.

Libya, Syria and Iraq, for example, are all going to require infrastructure repair and rebuilding, which will obviously need multilateral backing and support. We expect to see very substantial capital requirements — involving export credit agencies and multilateral funding bodies — to rebuild essential power and utility infrastructure in these troubled areas. The big international contractors and independent US power companies are likely to take an active interest.

Outlook for 2014

deep experience of the IPP model. This could have the impact of increasing competition for regulated and renewable assets in Europe.

domestic investment. There is a massive need for new power and water capacity, driven by population growth and the increased industrialization of the region’s economies. For example, in Saudi Arabia, the SEC’s projections for new capacity over the next few years exceed the total new capacity planned for the whole of the US over the same period. These projections are dramatic and encompass not just generation but basic infrastructure. It’s estimated that as much as US$283b will be invested in the Middle East and North African electricity generation alone between 2014 and 2018.21 Meanwhile, the GCC states are projecting investment of more than US$300b in some 20 energy projects by 2020, which will generate 8 GW of additional power.22 This will open up substantial opportunity for private sector involvement and transactions.

Financial Centre.

Power transactions and trends

M&A activity in Japan’s power and utilities sector slowed slightly in 2013 amid ongoing uncertainty about the decision to restart the country’s stalled nuclear plants. While Prime Minister Shinzo Abe is keen to return nuclear to the energy mix, public opposition to this remains strong and political will across different regions is divided. I doubt that any decision will be forthcoming in the short- to mid-term.

Of the deals that occurred during 2013, outbound M&A dominated with trading houses

For Japan’s 10 major utilities,23 the focus was cutting costs in the face of the nuclear freeze, a weakened yen and the slowing demand of an aging population. The sector is also preparing for Japan’s proposed reforms of the electricity market, expected to kick off in 2015.

Utilities cut costs, discretely divest

In 2013, Japan’s 10 major utilities kept their focus primarily at a domestic level. The lack of nuclear energy is driving deals aimed at rebalancing portfolios with many utilities, including TEPCO, moving to divest a relatively large number of non-core assets. While I would expect to see this trend continue, it should be noted that divestment will be tempered by the strong obligation felt by many of these utilities as major employers in many areas outside Tokyo and Osaka. I would not expect to see large-scale closures but rather deals to sell off some smaller subsidiaries throughout 2014.

While deregulation of the electricity market looms large, I see this having little real impact on M&A activity in the sector just yet. The big 10 are still trying to grasp the implications of unbundling and are in the early stages of addressing its challenges. The exception to this may be what I see as perhaps the most intriguing deal of the year — Chubu Electric Power’s acquisition of a 49% stake in Gunkul Powergen Co Ltd, a Thailand-based solar power plant operator. While Chubu Electric Power has a history in Thailand,

big 10 to rebalance investment across countries and expand into renewables as reforms progress.

Power Company, Chugoku Electric Power Company, Shikoku Electric Power Company, Tohoku Electric Power Company, Chubu Electric Power Company, Hokuriku Electric Power Company and Kyusha Electric Power Company.

Trading houses drive activity as reform looms2013 saw relatively subdued M&A activity in Japan although some

of most deals, with trading houses doing bigger outbound deals as the sector prepares for reform. Report by Kenneth G. Smith.

Japan

Perspectives on the ground

“ Promised electricity sector reform is likely to boost M&A activity and attract new players to a liberalized market.”

Kenneth G. Smith EY

14

Kenneth G. SmithJapan TAS Power & Utilities Leader Tokyo, [email protected]

15Global power and utilities mergers and acquisitions — 2013 review and 2014 outlook

Trading houses target renewables

Meanwhile, it is a somewhat different story for Japan’s six biggest general trading companies,24 which dominated utilities M&A activity in 2013 and drove the year’s big trend in outbound transactions.

Many of these deals focused on overseas renewable assets,

stake in 56 MW of PV in France from EDF Energies Nouvelles.

In other deals, Mitsui strengthened its relationship with France-based GDF Suez, buying a 28% stake in the company’s Australian arm in a deal that will allow it to develop a presence in the Australian energy sector. In the US, Mitsui also bought a

Suez while Marubeni acquired a 90% stake in EDF’s wind energy project in California.

24. Mitsubishi Corporation, Mitsui and Company, Itochu Corporation, Marubeni Corporation, Sumitomo Corporation and Sojitz Corporation.

While we have seen trading houses buy stakes in renewable energy projects before, I believe that the bigger size of these

target these projects. They see them as solid investments but are also keen to gather much-needed expertise in the renewables sector. Expect to see similar deals in 2014.

Consolidation in gas

Of the few inbound deals of the year, Kanto Natural Gas Development’s acquisition of a 38.13% stake in Otaki Gas Company Limited is worth noting. The deal between the two

consolidation in the natural gas sector, which aims to increase

shareholders.

quickly resolved — the focus for the Japanese utility sector in the next few years will be the ongoing deregulation process. We expect this to emerge as a strong catalyst for M&A

US, Asian and European investors begin to assess the potential for returns in the newly deregulated market.

Reforms are already beginning to attract new players to the utilities sector, as illustrated by the recent deal by Japanese cable TV company Jupiter Telecommunications to acquire IP Power Systems, in a move that will allow it to expand its electricity distribution service business and create synergies with its cable and internet business. Japanese paper manufacturer Oji Holdings Corporation has also announced plans to spend US$309.1m on new electricity generation plants by FY2015, as part of a strategy to sell to retail electricity customers. We expect to see similar interest from other non-traditional players in what promises to be a more robust M&A environment in Japan in 2014.

Outlook for 2014

Power transactions and trends

2013 proved an exciting and varied year for power and utility transactions, driven by continued low wholesale prices, weak demand growth and portfolio optimization by hybrid utilities in search of stable earnings. Across the Americas region, deal activity in the sector rose by over one third on 2012 levels. The US hosted 3 of the year’s top 10 global deals,25 including the world’s largest as MidAmerican Energy Holdings announced its US$10.4b acquisition of Nevada-based public utility NV Energy, Inc.

Canadian utility investors, hungry for returns, continued to show interest in the US regulated utilities market. In December 2013, Canada’s Fortis Inc. acquired Arizona-based UNS Energy Corporation for US$4.3b. It was the utility’s second acquisition in the US in two years, following its US$969m acquisition of CH Energy Group, Inc., which was completed in June 2013. Watch out for more cross-border deals

and contracted generation opportunities.

This drove US utilities to divest market-exposed generation assets: early in 2013,

2012) to sell off non-economic power plants. Toward the end of the year, Edison Mission Energy went into bankruptcy and sold its coal, gas and wind generation assets to NRG Energy, Inc. Hybrid utilities will continue the multi-year strategy of deleveraging exposure to competitive generation, acquiring rate-regulated businesses, or both. Finding buyers or merger partners will be the biggest challenge.

With the short- to medium-term outlook for power prices weak in most parts of the US, we expect portfolio rebalancing to continue to drive deals as utilities reshape their mix of businesses, switch away from coal or simply move out of generation. Oversupply on wholesale markets, coupled with slow demand growth, will create prime conditions for further consolidation in coming months, just as they did in 2013.

25. See Table 2, page 2.

Energy shift boosts deal levels in an active year 2013 saw increased M&A activity and megadeals. Sales of generation assets and acquisitions of rate-regulated businesses are likely to be a continuing focus for utility executives in coming months as utilities rebalance portfolios. Report by Joseph Fontana.

United States

Perspectives on the ground

“ Hybrid utilities will continue to sharpen their strategies to alleviate pressure on generation assets. We’ll see further sales of generation portfolios and further acquisition of rate-regulated businesses.”

Joseph Fontana EY

16

Joseph FontanaAmericas TAS Power & Utilities LeaderNew York, [email protected]

17Global power and utilities mergers and acquisitions — 2013 review and 2014 outlook

One route to deliver earnings to shareholders could be

utility skill set. With expectations of US energy independence and an abundance of cheap natural gas, US utilities with midstream pipeline experience are well placed to take advantage of opportunities ranging from developing interstate pipeline businesses to exporting natural gas from new LNG facilities.

Several utilities moved forward along these lines in 2013. March 2013 saw the formation of a Master Limited Partnership26

and ArcLight Capital Partners, creating a sizeable midstream company to take advantage of the growing need for natural gas pipeline construction. The venture, called Enable Midstream, will own and operate strategically located natural gas and crude oil infrastructure assets.27

26. An MLP is a structure that allows US businesses involved in exploration, production or transportation of natural resources to pay no income taxes at the entity level. 27. Upon formation, the venture will have about 11,000 miles of gathering pipelines, 11 major processing plants, approximately 7,800 miles of interstate pipelines, 2,300 miles of intrastate pipelines and 8 storage facilities.

In September 2013, Dominion contributed its Cove Point

Midstream business to an MLP. The Cove Point Project, expected to be completed in March 2017, was the third project in 2013 to receive Department of Energy approval to export LNG to countries without a free trade agreement. This includes Japan, where the price of delivered LNG is dramatically higher than the cost of US natural gas. Even factoring in the cost of processing and transportation, exported US LNG will provide a valuable resource at a competitive price.

LNG participants will need to evaluate the potential effect on market pricing if more of the 10 LNG export projects under consideration by the Department of Energy gain approval.

2014 is set to be another active year, with the same basic market dynamics remaining in operation and driving deals. Hybrid utilities will continue to sharpen their strategies to alleviate pressure on generation assets. We will see further sales of generation portfolios and further acquisition of rate-regulated businesses.

We can count on continued regulatory support for the establishment of new solar and wind projects. On the distributed solar side, the marketplace of multiple small players is ripe for consolidation, creating transaction opportunities.

There’s every reason to assume capital will continue to be readily available to the big

recently, in particular those in renewables. Some of the new business structures could make it easier to attract investors and funding. For example, if regulatory changes are introduced that enable alternative energy enterprises to qualify for MLP status, it will boost the industry and should increase the volume of transactions.

Another interesting development to watch for is major utility and renewable energy

of NRG YieldCo, which was set up in mid-2103. Fixed-income investors are chasing higher yields at lower risks: YieldCos comprise long-term contracted assets and can provide investors with a competitive return compared with the low interest rates available from US Treasuries and other debt instruments. New YieldCos are likely to become active buyers, as they seek to build portfolios of contracted assets. However, rising interest rates could dampen the excitement about these vehicles.

gas businesses and are keen to exit. Examples are Detroit, which is in bankruptcy and is transferring customers of its electric business to Detroit Edison, and Philadelphia, which is currently looking to sell its gas business. We expect to see more activity of this kind

distressed state of certain cities: this is not a long-term trend.

Outlook for 2014

2014Transaction outlookWith the transformation agenda as the key discussion point in utility boardrooms, transactions

2014. Expect cross-border deals to dominate the year as utilities look for growth beyond domestic boundaries. Report by Matt Rennie. US set for M&A opportunities in response to changing demand dynamics

Despite the gradual recovery in the US economic climate, the US power sector is expecting a decline in electricity demand due to moderating load growth, greater

and increasing distributed generation. These factors will push utilities to look beyond their service territories, to seek opportunities in areas that are growing faster than the national average. States such as Arizona and Nevada are ripe for consolidation, given their favorable

southwest region of the country hosted three megadeals with a cumulative value of over US$15.5b in 2013.

In the current environment of depressed power and natural gas prices, several

utilities are looking to reduce their exposure to unregulated assets, which will create a healthy pipeline of discounted power plants available for sale. Financial investors are likely to emerge as natural buyers of most of these assets, which they are likely to hold on to in anticipation of a rise in natural gas prices. Desire for assets with long-term power purchase

rate-base areas, is likely to push the premium up.

Infrastructure build-out and capacity expansion will drive emerging markets investment

Emerging markets opportunities are under scrutiny by many utilities. Market reforms

infrastructure expansion over the last couple of years have placed several countries center stage for growth

Countries such as Chile and Peru in Latin America are also gearing up to host global utility deals, driven primarily by growth in renewables and opportunities for

generation segment alone represents close to US$85b investment opportunity through 2022. The planned restructuring

M&A opportunities if it is approved.

Africa, which is fast attracting interest

is likely to host the next wave of capital investments. The average economic growth rate for African countries is likely to exceed 6% per year between 2010 and 2040, driven by surging populations, improved education and technology absorption. This continuing growth and prosperity will swell the demand for infrastructure, opening up opportunities across the utility value chain. Foreign investors, particularly from China, Japan and the US, have been active in the region’s generation and transmission segments. We expect this trend to continue, with heavy investments to be

Regulatory and market reforms open up transaction opportunities

Unbundling in Japan, liberalization of the energy sector in Mexico, and privatization in Australia and New Zealand have opened opportunities for investors across the globe who are watching these developments with interest.

In addition to unbundling regional energy companies in Japan, TEPCO is considering spending about US$25.6b on strategic investments through partnerships: upstream energy projects, overseas electricity business and fresh capital are key on the agenda. The expectation of sweeping reforms has triggered the entry of new players into the sector, such as paper manufacturer Oji Holdings Corporation and Japanese cable TV company Jupiter Telecommunications.

18 Power transactions and trends

19Global power and utilities mergers and acquisitions — 2013 review and 2014 outlook

In Australia, we expect the privatization process to continue beyond the sales of Macquarie Generation in New South Wales. We anticipate sales of generators in Queensland, merger and transaction activity in Western Australia around generation and networks, and the creation of new and innovative methods of involving private sector capital in the long-term operation of state-owned network companies across the country. Similarly, Mexico’s announcement to open up its energy sector for private investments has already placed the country on the watch list of global investors.

Cross-border activity to remain strong as investors focus on growth

One of the key messages from EY’s October 2013

report is the preference of the utilities C-suite for growth via access to new markets/technologies; this is especially evident in the power and utilities sector. This year, capital mobility is essential to connect opportunities in emerging and reforming markets with companies looking to diversify away from underperforming local wholesale markets.

High population growth rates and increased industrialization in the Middle East, particularly in the GCC countries, has created an urgent need for power and water capacity expansion. Renewable power is one area where we expect substantial participation from foreign

investors, primarily in the form of partnerships with local players. Indeed, with so many markets in different stages of development and supply/demand balance, capital mobility has never been so important. The most successful inbound markets will be those where governments

and where processes and communications are tailored appropriately.

Sustained pressure on utility balance sheets to continue to drive M&A in Europe

High levels of renewable subsidies coupled with increasing network charges have resulted in higher consumer power prices in much of Europe. With the economy continuing to be stressed and unemployment remaining high, energy costs are expected to be a major political issue in the region in the coming months, putting further pressure on utilities’ earnings.

European utilities are attempting to wade through the tough economic climate of low earnings and high debt by shedding non-strategic assets. Italy’s Enel has announced a target of raising up to US$8b by the end of 2014 through asset sales. Finland-based energy company Fortum, France-based water utility Veolia Environnement, and Swedish utility

plans for the year.

“ Capital mobility will be an essential driver of transactions during 2014 as companies looking to diversify away from markets with excess capacity and low returns shift their focus towards emerging and reforming markets. We expect Africa, Japan, the Gulf States and South America to be focus areas for cross-border investors.”

Matt Rennie EY

20 Power transactions and trends

EY Global TAS Power & Utilities contacts

Global contacts

Matthew Rennie Global TAS Power & Utilities Leader

+61 7 3011 3239 [email protected]

Cara Graham Director Global TAS Power & Utilities

+61 7 3011 3145 [email protected]

Robert StallUS South East TAS Power & Utilities LeaderAtlanta, US+1 404 817 [email protected]

Miles HuqUS East Central TAS Power & Utilities Leader

+1 410 783 [email protected]

Veeral PatelUS Mid West TAS Power & Utilities LeaderChicago, US+1 312 879 [email protected]

Deborah Byers US South West TAS Power & Utilities LeaderHouston, US+1 713 750 [email protected]

Joseph Fontana Americas TAS Power & Utilities Leader New York, US +1 212 773 3382 [email protected]

Lucio TeixeiraSouth America TAS Power & Utilities Leader

+55 112 573 [email protected]

Gerard McInnisTAS Power & Utilities LeaderAlberta, Canada+1 403 206 [email protected]

Americas

21Global power and utilities mergers and acquisitions — 2013 review and 2014 outlook

Stéphane Kraft TAS Power & Utilities Leader Paris, France+33 1 55 61 09 [email protected]

Thomas Kästner Germany TAS Power & Utilities Leader Munich, Germany+49 160 93 917 [email protected]

Andrea GuerzoniMediterranean TAS Power & Utilities LeaderMilan, Italy+39 0280 669 707 [email protected]

René Coenradie TAS Power & Utilities LeaderRotterdam, Netherlands+31 88 407 [email protected]

Remigiusz Chlewicki TAS Power & Utilities LeaderWarsaw, Poland+48 22 557 74 [email protected]

Julie HoodTAS Power & Utilities LeaderMelbourne, Australia+61 3 8650 [email protected]

Alex ZhuChina TAS Power & Utilities Leader

+86 10 5815 [email protected]

Lynn ThoASEAN TAS Power & Utilities Leader Singapore+65 6309 [email protected]

Björn GustafssonTAS Power & Utilities Leader Stockholm, Sweden+46 8 520 594 [email protected]

Tony WardEMEIA TAS Power & Utilities Leader London, UK+44 121 535 [email protected]

Ian WhitlockUKI TAS Power & Utilities LeaderLondon, UK+44 20 7951 [email protected]

Europe Asia-Pac

Kenneth G. SmithJapan TAS Power & Utilities Leader Tokyo, Japan+81 34 582 [email protected]

JapanMiddle East

Africa

David LloydMiddle East TAS Power & Utilities LeaderRiyadh, Saudi Arabia+966 11 215 [email protected]

Brunhilde BarnardAfrica TAS Power & Utilities LeaderJohannesburg, South Africa+27 11 502 [email protected]

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

About EY’s Global Power & Utilities CenterIn a world of uncertainty, changing regulatory frameworks and environmental challenges, utility companies need to maintain asecure and reliable supply, while anticipating change and reacting to it quickly. EY’s Global Power & Utilities Center brings together aworldwide team of professionals to help you succeed — a team with deep technical experience in providing assurance, tax, transaction and advisory services. The Center works to anticipate market trends identify the implications and develop points of view on relevant sector issues. Ultimately it enables us to help you meet your goals and compete more effectively.

© 2014 EYGM Limited. All Rights Reserved.

EYG no. DX0240CSG/GSC2014/1279107ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com/powerandutilities

EY | Assurance | Tax | Transactions | Advisory

Doing the right deal in power and utilitiesDoing the right deal right can make a power and utility business more competitive and profitable. Clients turn to EY member firms’ Transaction Advisory Services professionals for advice and support through the life cycle of a transaction, from early stage to execution and post-deal activities. Whether the transaction involves acquisitions, alliances, joint ventures, sales, divestitures or securitizations, we help clients do the right deal at the right price. We help to determine the true value of an asset, set up the business and tax structure, optimize their position in the regulated revenue and pricing environments and execute the deal. We combine proven practices and consistent methodologies with fresh thinking, giving the advice our clients need to make informed decisions, potentially reduce risks and achieve successful outcomes.

Data source and industry scopeThe transactions and trends identified in this report are informed by analyses and engagements undertaken by Ernst & Young Global Limited member firm transactions partners globally and Mergermarket data. “Power and utilities” covers electricity generation networks and retail organizations, gas networks and retail organizations, and water wholesale networks and retail organizations. It also includes renewable energy companies. Deal activity and valuations may fluctuate slightly based on the final date of data collection and analysis conducted by EY.

Follow us on Twitter @EY_PowerUtility

Power & Utilities insights LinkedIn group

![IEEE TRANSACTIONS ON POWER SYSTEMS, VOL. 28, …ecs.syr.edu/faculty/sara/papers/impact.pdf · IEEE TRANSACTIONS ON POWER SYSTEMS, ... connected power system. Authors in [14] ... aggregated](https://static.fdocuments.us/doc/165x107/5ac51ca37f8b9a333d8dacd1/ieee-transactions-on-power-systems-vol-28-ecssyredufacultysarapapers.jpg)