Power, International & Energy Services - Enbridge/media/Enb/Documents/Investor Relations...Power,...

13

Power, International & Energy Services J. Richard Bird Executive Vice President, Chief Financial Officer & Corporate Development

Transcript of Power, International & Energy Services - Enbridge/media/Enb/Documents/Investor Relations...Power,...

Power, International & Energy Services J. Richard Bird

Executive Vice President, Chief Financial Officer & Corporate Development

This presentation includes certain forward looking information (FLI) to provide Enbridge shareholders and

potential investors with information about Enbridge and management’s assessment of its future plans and

operations, which may not be appropriate for other purposes. FLI is typically identified by words such as

“anticipate”, “expect”, “project”, “estimate”, “forecast”, “plan”, “intend”, “target”, “believe” and similar words

suggesting future outcomes or statements regarding an outlook. Although we believe that our FLI is

reasonable based on the information available today and processes used to prepare it, such statements are

not guarantees of future performance and you are cautioned against placing undue reliance on FLI. By its

nature, FLI involves a variety of assumptions, risks, uncertainties and other factors which may cause actual

results, levels of activity and achievements to differ materially from those expressed or implied in our FLI.

Material assumptions include assumptions about: the expected supply and demand for crude oil, natural gas

and natural gas liquids; prices of crude oil, natural gas and natural gas liquids; expected exchange rates;

inflation; interest rates; the availability and price of labour and pipeline construction materials; operational

reliability; anticipated in-service dates and weather.

Our FLI is subject to risks and uncertainties pertaining to operating performance, regulatory parameters,

weather, economic conditions, exchange rates, interest rates and commodity prices, including but not limited

to those discussed more extensively in our filings with Canadian and US securities regulators. The impact of

any one risk, uncertainty or factor on any particular FLI is not determinable with certainty as these are

interdependent and our future course of action depends on management’s assessment of all information

available at the relevant time. Except to the extent required by law, we assume no obligation to publicly

update or revise any FLI, whether as a result of new information, future events or otherwise. All FLI in this

presentation is expressly qualified in its entirety by these cautionary statements.

This presentation will make reference to certain financial measures, such as adjusted net income, which are

not recognized under GAAP. Reconciliations to the most closely related GAAP measures are included in the

earnings release and also in the Management Discussion and Analysis posted to the website.

Legal Notice

2

New Growth Platform Leadership Team

VP Green Power & Transmission

Don Thompson

Senior VP Energy Marketing & International

Leigh Cruess

VP Alternative & Emerging Technology

Chuck Szmurlo

3

Executive VP, CFO, & Corporate Development

J. Richard Bird

VP International

Lino Luison

4

North American Power Market Fundamentals

• Modest long term power demand growth

• Gas-fired and renewable sources dominate 2010 - 2020 supply

growth investment of ~$500 billion

• $100 billion of 2010 - 2020 transmission investment required

Source: Wood Mackenzie 2013

0

1,000

2,000

3,000

4,000

5,000

6,000

2013 2015 2017 2019 2021 2023 2025 2027 2029

Nuclear Hydro Fuel Oil Coal Gas Renewables

TWH

North American Power Demand ~1% Annual Growth

5

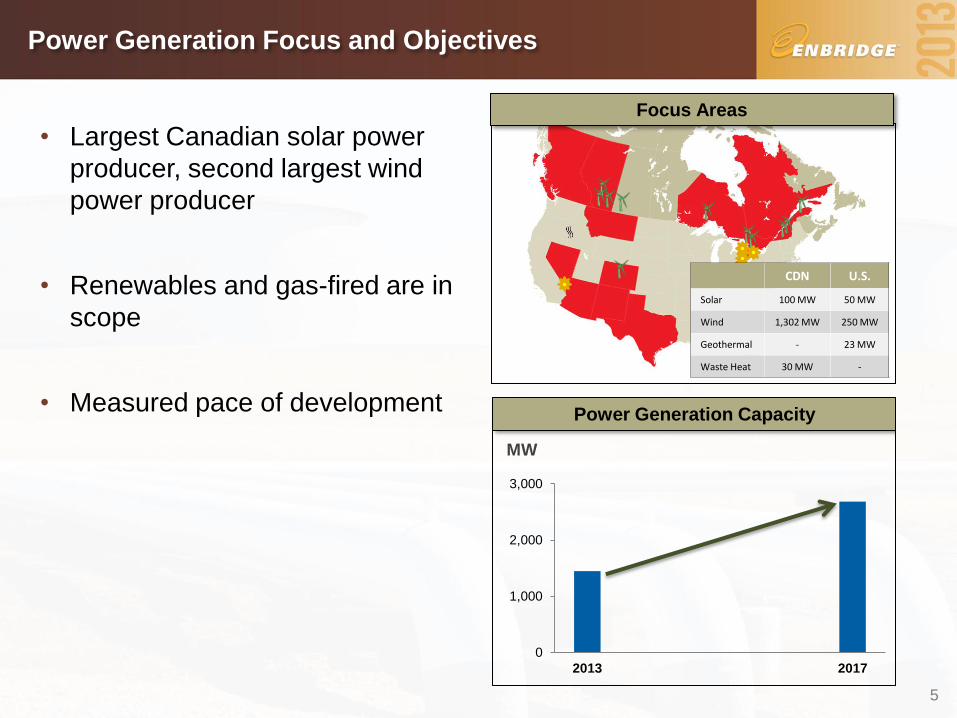

Power Generation Focus and Objectives

• Largest Canadian solar power

producer, second largest wind

power producer

• Renewables and gas-fired are in

scope

• Measured pace of development

0

1,000

2,000

3,000

2013 2017

MW

Power Generation Capacity

CDN U.S.

Solar 100 MW 50 MW

Wind 1,302 MW 250 MW

Geothermal - 23 MW

Waste Heat 30 MW -

Focus Areas

6

Power Transmission Focus and Objectives

• Montana-Alberta Tie Line (MATL)

is in-service

• Enbridge/Nextera/Borealis

consortium selected for Ontario

East-West project

• Focus is on MATL expansion,

Ontario and Alberta

• Measured pace of development

Focus Areas

0

500

1000

2013 2017

MW

Transmission Capacity

International Fundamentals

7

0

10

20

30

40

50

60

0

2

4

6

8

10

12

14

2012 2013 2014 2015 2016 2017 2018

TC

F

BC

F/d

Production (BCF/d) Consumption (BCF/d)

Net exports (BCF/d) Reserves (TCF) RHS

Australia Natural Gas Market Balance

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0

100

200

300

400

500

600

2012 2013 2014 2015 2016 2017 2018

bn

bo

e

Mb

oe/d

Production (Mboe/d Consumption (Mboe/d)

Net exports (Mboe/d) Reserves (bn boe) RHS

Peru Hydrocarbon Market Balance

0

50

100

150

200

250

300

350

400

450

2015 2020 2025 2030 2035 2040

Qu

ad

rillio

n B

tu

OECD Asia Other Non-OECD Asia India China

Asian Demand Growth

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0

200

400

600

800

1,000

1,200

1,400

1,600

2012 2013 2014 2015 2016 2017 2018

MM

bb

l

Mb

bl/

d

Production (Mbbl/d) Consumption (Mbbl/d)

Net exports (Mbbl/d) Reserves (MMbbl) RHS

Colombia Crude Oil Market Balance

Source: Business Monitor International Source: Business Monitor International

Source: Business Monitor International Source: EIA

International Focus

8

Colombia

• Measured pace of development

– Colombia

– Oleoducto al Pacífico

– Peru

– Australia

• Primary focus is greenfield

development

• Cenit (Ecopetrol subsidiary)

joined OAP as a funding

partner

Energy Services Fundamentals

Condensate:

Edmonton: $99

Mt. Belvieu: $88

Conway: $85

*Brent price is a landed price on US East Coast/ US Gulf

Coast. Assumed tanker freight cost of US$2.00 per bbl.

Asia

$96

WCS

Bakken

Light

Brent

Maya

$108 $72

LLS

WTI

$112 *

$96

$103

$105

Light Crude

Heavy Crude

$89

Alberta

Light

Pricing as at September 25, 2013

(USD per barrel)

9

WTS: $101 US Sour: $99

Energy Services Business Strategies

10

EdmontonChicago

Cushing

Transportation

Buy: WCS @ Edmonton, AB ($82.00)

Tariff and TVM ($6.00)

Sell: WCS @ Cushing, OK $90.00

Transportation Margin $2.00

Simultaneously Buy & Sell WCS

Spearhead

Enbridge Mainline

Refinery Supply

Simultaneously Buy & Sell Bakken

STORAGE

TANK

Storage

Buy- February

$100.00 / bbl

Sell – March

$101.15 / bbl

Enbridge N.D. Pipeline

Buy: DOM @ Cushing, AB ($100.00)

Storage Fee and TVM ($0.65)

Sell: DOM @ Cushing, OK $101.15

Storage Margin $0.50

Buy: Bakken @ North Dakota ($83.00)

Truck fees, Tariff & TVM ($5.00)

Sell: Bakken @ Clearbrook, MN $90.00

Refinery Supply Margin $2.00

North Dakota

Field Location

Refinery

Minnesota

Condensate Transportation

Rail from Chicago to Edmonton

Transport

by pipe to

Chicago

Chicago

Mont Belvieu, Texas

Conway , Kansas

Edmonton,

Alberta

Buy: CON @ Mt. Belvieu, TX ($91.00)

Sell: CON @ Edmonton, AB $93.00

(net of Tariff, Terminal

Fees, Rail & TVM)

Transportation Margin $2.00

Energy Services Focus and Objectives

11

0

25

50

75

100

125

150

2007 2008 2009 2010 2011 2012 2013 2017

$ m

illio

ns

Earnings Contribution • Continued replacement and

expansion of current strategies

– Low risk arbitrage

– Producer and refiner services

• Extension of business model

– Rail niche markets

– Geographic expansion

– Long-term transactions

New Growth Platforms Summary

12

• Well positioned to provide modest near term growth,

base for increased longer term growth and diversification

Near Term Growth Longer Term Potential

Growth / Diversification

Power Generation

Power Transmission

International

Energy Services

Power, International & Energy Services