Potential upside 13% Hotel Leela (HOTLEE) - ICICI...

18

1 | Page Hotel Leela (HOTLEE) Check out … Hotel Leela, one of the leading players in premium hotel business, has capex planned to the tune of Rs 2,400 crore to increase its room capacity by 63% to 1,600 by FY10 from the current 985 and push it up by 168% to 2,644 rooms across all major cities by FY11. Tardy expansion plans Hotel Leela has expansion plans for all its hotels. Leela Bangalore is expected to add 105 rooms to its existing 252 rooms not before FY08 while expansion plans for Goa, management contract for hotel in Gurgaon would come on stream by FY09 and new hotel at Udaipur to come by FY10. Expansion project at its Mumbai hotel has been awaiting approvals from concerned authorities since FY05. The expansions have been tardy and we foresee them getting delayed. The hotel will lose the opportunity to maximize gains from the demand bounty. Undiversified market presence till 2011 The hotel sector is seeing demand-driven by business as well as leisure segment in metros and other major cities. Hotel Leela has a dominant presence in Mumbai, Bangalore, Goa and Kovalam. Leela’s long absence from major markets like Delhi, Hyderabad, Chennai, Kolkatta, Pune, Jaipur, Agra, etc leaves a lacunae for competitors to score. Rooms to come with competition Although Hotel Leela has undertaken expansion plans to New Delhi, Pune, Chennai and Hyderabad, the company is not expecting any of the fresh capacities to be operational before FY11. By 2010, the hotel sector should witness huge supplies coming in at major cities resulting in rationalisation of average room rates (ARRs) and cooling down of the occupancies. Valuations We believe that Hotel Leela is expensively valued and would continue to underperform the sector and advise clients to switch to better performing stocks in the sector. Given the delayed expansion plans and absence in major markets till 2010, we feel Leela’s current valuations have factored in the business growth till FY09. At the current price of Rs 44, the stock trades at P/E of 16.2x FY08E EPS of Rs 2.7 and 16.8x FY09E EPS of Rs 2.6. We rate the stock as HOLD with a price target of Rs 42, 16x FY09E. Exhibit 1: Key Financials Year to March 31 FY06 FY07 FY08E FY09E Net Profit 73.17 126.43 100.44 97.06 Shares in issue (crore) 7.37 37.03 37.03 37.03 Diluted EPS (Rs) 1.99 3.41 2.71 2.62 % Growth 57.1% 71.9% -20.5% -3.3% P/E (x) 21.16 12.89 16.22 16.79 Price/Book (x) 1.97 1.81 1.63 1.48 EV/EBIDTA 15.82 14.12 13.75 14.75 RoNW (%) 8.9% 14.0% 10.0% 8.8% RoCE (%) 8.1% 9.7% 8.4% 7.5% Source: ICICIdirect Research Initiating Coverage ICICIdirect | Equity Research September 5, 2007 | Hotel Potential upside 13% Time frame 12 months Time frame 12 months HOLD Current price Rs 44 Target price Rs 42 Potential downside 4.5% Time Frame 12 mths Himani Singh [email protected] Sales & EPS trend 0 100 200 300 400 500 FY03 FY04 FY05 FY06 FY07 FY08E FY09E Rs Crore 0 1 2 3 4 Sales Diluted EPS Stock metrics Promoters holding 49.07% Market Cap Rs1629 crore 52 Week H/L 80 / 37 Sensex 15447 Average volume 419,172 Comparative return metrics Stock return 3 M 6M 12M Indian Hotel -15.2% -14.1% -1.9% East India Hotel 8.3% 15.8% 11.0% Asian Hotel -5.3% -6.7% 19.1% Hotel Leela -33.3% -31.0% 32.0% Price Trend 30 40 50 60 70 80 Aug-06 Sep-06 Oct-06 Nov-06 Dec-06 Jan-07 Feb-07 Mar-07 Apr-07 May-07 Jun-07 Jul-07 Aug-07 Target price Absolute sell

Transcript of Potential upside 13% Hotel Leela (HOTLEE) - ICICI...

1 | P a g e

Hotel Leela (HOTLEE)

Check out … Hotel Leela, one of the leading players in premium hotel business, has capex planned to the tune of Rs 2,400 crore to increase its room capacity by 63% to 1,600 by FY10 from the current 985 and push it up by 168% to 2,644 rooms across all major cities by FY11.

Tardy expansion plans Hotel Leela has expansion plans for all its hotels. Leela Bangalore is expected to add 105 rooms to its existing 252 rooms not before FY08 while expansion plans for Goa, management contract for hotel in Gurgaon would come on stream by FY09 and new hotel at Udaipur to come by FY10. Expansion project at its Mumbai hotel has been awaiting approvals from concerned authorities since FY05. The expansions have been tardy and we foresee them getting delayed. The hotel will lose the opportunity to maximize gains from the demand bounty. Undiversified market presence till 2011

The hotel sector is seeing demand-driven by business as well as leisure segment in metros and other major cities. Hotel Leela has a dominant presence in Mumbai, Bangalore, Goa and Kovalam. Leela’s long absence from major markets like Delhi, Hyderabad, Chennai, Kolkatta, Pune, Jaipur, Agra, etc leaves a lacunae for competitors to score. Rooms to come with competition

Although Hotel Leela has undertaken expansion plans to New Delhi, Pune, Chennai and Hyderabad, the company is not expecting any of the fresh capacities to be operational before FY11. By 2010, the hotel sector should witness huge supplies coming in at major cities resulting in rationalisation of average room rates (ARRs) and cooling down of the occupancies.

Valuations We believe that Hotel Leela is expensively valued and would continue to underperform the sector and advise clients to switch to better performing stocks in the sector. Given the delayed expansion plans and absence in major markets till 2010, we feel Leela’s current valuations have factored in the business growth till FY09. At the current price of Rs 44, the stock trades at P/E of 16.2x FY08E EPS of Rs 2.7 and 16.8x FY09E EPS of Rs 2.6. We rate the stock as HOLD with a price target of Rs 42, 16x FY09E.

Exhibit 1: Key Financials Year to March 31 FY06 FY07 FY08E FY09E Net Profit 73.17 126.43 100.44 97.06 Shares in issue (crore) 7.37 37.03 37.03 37.03 Diluted EPS (Rs) 1.99 3.41 2.71 2.62 % Growth 57.1% 71.9% -20.5% -3.3% P/E (x) 21.16 12.89 16.22 16.79 Price/Book (x) 1.97 1.81 1.63 1.48 EV/EBIDTA 15.82 14.12 13.75 14.75 RoNW (%) 8.9% 14.0% 10.0% 8.8% RoCE (%) 8.1% 9.7% 8.4% 7.5% Source: ICICIdirect Research

Initiating Coverage

ICICIdirect | Equity Research

September 5, 2007 | Hotel

Potential upside 13% Time frame 12 months

Potential upside 13%

Time frame 12 months

HOLD

Current price Rs 44

Target price Rs 42

Potential downside 4.5%

Time Frame 12 mths

Himani Singh [email protected]

Sales & EPS trend

0

100

200

300

400

500

FY03 FY04 FY05 FY06 FY07 FY08E FY09E

Rs C

rore

0

1

2

3

4

Sales Diluted EPS Stock metrics Promoters holding 49.07% Market Cap Rs1629 crore 52 Week H/L 80 / 37 Sensex 15447 Average volume 419,172 Comparative return metrics

Stock return 3 M 6M 12M

Indian Hotel -15.2% -14.1% -1.9% East India Hotel 8.3% 15.8% 11.0% Asian Hotel -5.3% -6.7% 19.1% Hotel Leela -33.3% -31.0% 32.0%

Price Trend

30

40

50

60

70

80

Aug

-06

Sep-

06

Oct-0

6

Nov

-06

Dec-

06

Jan-

07

Feb-

07

Mar

-07

Apr

-07

May

-07

Jun-

07

Jul-0

7

Aug

-07

Target price

Absolute sell

2 | P a g e

Exhibit 2: Business Profile

Company Background Hotel Leela, incorporated in 1981, entered into collaboration with Kempinski Hotels, to set up and operate 5-star hotels. The company set up its first 5-star deluxe hotel, Leela Penta, in Bombay in 1986. It was renamed Leela Kempinski in 1988, following the change in its marketing and sales tie-up. The Leela Palace, Goa, started its operation in Sept 1998. The hotel has been upgraded to a world-class beach resort and has been acclaimed as one of the finest resorts in the world. The 300-room Bangalore five-star hotel had a soft launch on July 15, 2001. In July 2005, the company acquired majority stake in Kovalam Hotels Ltd. Consequently Kovalam Hotels Ltd became a subsidiary of the company and now is known as 'Leela Kovalam Beach, Kerala'. The company operates four hotels with 985 rooms under the ‘Leela’ brand.

Share holding pattern

Share holder % holding Promoters 49.07 Institutional investors 23.79 Other investors 11.53 General public 15.61 Promoter & Institutional holding trend

48.90 49.03 49.07 49.07

25.72 26.58 26.62 23.79

0

10

20

30

40

50

60

Q2FY07 Q3FY07 Q4FY07 Q1FY08

%

Promoter Holding % Institutional Holding %

Hotel Leela Ventures 95% of revenues

Kovalam (subsidiary) 5% of revenues

Room Revenue 67% of revenue

Food & Beverage 27% of revenue

Room Revenue 63% of revenue

Food & Beverage 33% of revenue

Hotel Leela

Source: ICICIdirect Research

3 | P a g e

INVESTMENT RATIONALE Tardy expansion plans Hotel Leela has expansion plans for all its hotels. Leela Bangalore is expected to add 105 rooms to its existing 252 rooms but this addition is expected to commission by third quarter of FY08. Expansion plans for Goa to add 29 luxury rooms is expected to get functional by FY09. Hotel Leela has been planning to launch its new hotel at Udaipur since FY05. The company is expecting the hotel to be operational in FY10. Expansion project at its Mumbai hotel has been awaiting approvals from concerned authorities. Hotel Leela has entered into management contract for a 409 rooms luxury hotel in Gurgaon which is expected to get commissioned by 2009. The expansions have been tardy and seem missing to maximize gains from the demand bounty.

Exhibit 3: Room base

413 413 333 400 400 400 400

252 252252

252 252 357 357

152 152 152152125 181181 181

81

181152

152

0

200

400

600

800

1000

1200

1400

FY03 FY04 FY05 FY06 FY07 FY08E FY09E

Num

ber o

f Roo

ms

Mumbai Bangalore Goa Kovalam Udaipur

Bangalore

Bangalore currently has an inventory of 1815 rooms in the 5-star and 5 star deluxe category. Leela palace holds the highest market share of room inventory at 14% with ITC Windsor and Chancery Pavilion close at 13% each and Le Meridien at 11% of the total room base. By 2009, the room supply at Bangalore is expected to increase to 2,960 with new hotels by JW Marriott, Radisson-Unitech, Taj and Hyatt getting operational. Post Leela Palace expansion, it would lose to be the market leader with a reduced market share of 12.6%. In 2010, the Bangalore market will witness more than 1300 rooms coming through various ventures and is expected to more than double its current supply. In such scenario Leela Palace would see a sharp fall in its market share to 8.6%.

Exhibit 4: Operational efficiency of hotels in Bangalore

Taj Residency

The Oberoi

The Taj West End

ITC Windsor Manor

The Leela Palace Kempinski Bangalore

Grand Ashok4000

6000

8000

10000

12000

14000

16000

18000

70 72 74 76 78 80 82

Occupancy

ARRs

Source: Company, ICICIdirect Research

Size of the bubble represents room capacity Source: CRIS INFAC, ICICIdirect Research

Average room rates have started showing signals of rationalisation in Bangalore

4 | P a g e

Exhibit 5: ARRs to rationalise in Bangalore

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

FY06 FY07P FY08E FY09E

Rs.

0

10

20

30

40

50

60

70

80

90

ARR (LHS) RevPAR (LHS) Occupancy rate (%)

North Mumbai Mumbai is a very competitive territory for hotel sector with a current total inventory of 6,750 rooms in the 5-star category. North Mumbai has a current capacity of 4,600 5-star and 5-star deluxe rooms, of which Leela Kempinski has a sizable 8.6% amongst the who’s who of hotel industry. Leela Kempinski boasts of one of the top four RevPARs (revenue per available room) in North Mumbai. By 2009, North Mumbai would see an addition of 1,250 premium rooms through expansions in existing properties and through new on the block entries like The Park, Sea Rock. Amidst this supply bonanza Leela kempinski would witness a substantial fall in its market share to 6.8%. By 2010, North Mumbai deluxe room inventory would have increased to 6,280 with Leela’s share shrunk to 6.3%.

Exhibit 6: North Mumbai hotel operating efficiency

Holiday InnIntercontinental The

Grand

ITC Grand Maratha

JW Marriott

The Leela Kempinski

Orchid

Taj Lands End

Renaissance Hotel Sea Princess

Ramada Hotel Palm Grove

Sun-N-Sand

Le Royal Meridien

Grand Hyatt

3000

4000

5000

6000

7000

8000

9000

10000

60 65 70 75 80 85 90 95 100 105

Occupancy

ARRs

Size of the bubble represents room capacity Source: CRIS INFAC, ICICIdirect Research

Source: CRIS INFAC, ICICIdirect Research

Mumbai market has high visibility from all the major players of the hospitality business

5 | P a g e

Exhibit 7: Occupancy set to fall in North Mumbai

0

2,000

4,000

6,000

8,000

10,000

12,000

FY06 FY07P FY08E FY09E

Rs.

7475767778798081828384

ARR (LHS) RevPAR (LHS) Occupancy rate (%)

Goa Goa is one segment where most of the prominent players already have their presence and not much of influx of supply is scheduled for the future in the premium segment. Currently Leela Resort enjoys 6% market share with 152 rooms out of total 2,565 5-star room inventory of Goa. With additional 29 rooms getting functional by 2009, Leela is expected to increase its market share to 6.8%. Goa has been witnessing narrowing off season period and increasing influx of tourists, a situation that augurs well for the company.

Exhibit 8: Goa – A healthy market for all to thrive

Fort Aguada ResortGoa Marriot Resort

Intercontinental The Grand Resort Goa

Park Hyatt

Radisson White Sands

Renaissance Goa Resort

Cidade De Goa

Taj Holiday Village

Holiday Inn Resort

The Leela Palace

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

30 40 50 60 70 80 90

Occupancy

ARR

s

Exhibit 9: Goa business to remain strong

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

FY06 FY07P FY08E FY09E

Rs.

62

64

66

68

70

72

74

ARR (LHS) RevPAR (LHS) Occupancy rate (%)

Size of the bubble represents room capacity Source: CRIS INFAC, ICICIdirect Research

Source: CRIS INFAC, ICICIdirect Research

Source: CRIS INFAC, ICICIdirect Research

Leela Resorts enjoys a premium placement in the Goa properties therefore not much of a risk is foreseen in this territory

6 | P a g e

Kovalam Travel and tourism is one of the largest industries in Kerala contributing around 4% to the gross state product (GSP) and is expected to rise to 5.2% by 2013 according to World Travel & Tourism Council (WTTC). Kerala’s coastal resorts of Cochin, Kovalam, Thiruvananthapuram, Thekkady, Kozhikode and Ernakulam account for more than 75% of the total tourism traffic in Kerala. In Kovalam, Leela shares space with Taj Green Cove Resort. Leela beach resort leads in respect of room availability in Kovalam. Prospects for tourism in Kerala are bright with the state government’s interest. With major density of players being in Kochi, the leading position of Leela at Kovalam is expected to be beneficial for the company.

Exhibit 10: Kovalam yet to grow into major contributor

Leela Kovalam Beach Resort

Taj Green Cove Resort,Kovalam

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

61 62 63 64 65 66 67 68 69 70 71

Occupancy

ARRs

Exhibit 11: Kerala tourism looking upwards

0

1000

2000

3000

4000

5000

6000

Rs.

55

56

57

58

59

60

61

62

63

64

ARR (LHS) RevPAR (LHS) Occupancy rate (%)

Source: CRIS INFAC, ICICIdirect Research

Size of the bubble represents room capacity Source: CRIS INFAC, ICICIdirect Research

7 | P a g e

Undiversified market presence till 2011 The hotel sector is seeing demand driven by business as well as leisure in metros and other major cities. Hotel Leela has a dominant presence in Mumbai, Bangalore, Goa and Kovalam. Leela Palace, Bangalore and Leela Kempinski, Mumbai together contributed around 81% of the total revenues in FY07. Bangalore hotel market is seeing the peaking of ARRs, which can have significant impact on the top line. Such high dependence of revenue on two locations may put a strain on the company’s profitability in tackling any kind of adversity in these locations caused by increased competition or external environmental factors. Leela’s long absence from major markets like Delhi, Hyderabad, Chennai, Kolkatta, Pune, Jaipur, Agra etc over the years has left a lacuna for competitors to score.

Exhibit 12: Room revenue drivers

FY07

Bangalore43% Goa

12%

Kovalam7%

Mumbai38%

FY09EBangalore

44%

Goa13%

Mumbai34%

Kovalam9%

Exhibit 13: Sensitivity Analysis Occupancy ARR Net Sales PAT EPS Target Price Variance

75% 8661 431 97 2.61 42 - Inc by 10% Inc by 10% 498 126 3.37 54 29% Inc by 5% Inc by 5% 464 111 2.98 48 14% Inc by 10% - 469 113 3.02 48 16% Inc by 10% 457 109 2.92 47 12% Inc by 5% - 450 105 2.82 45 8% Inc by 5% 444 103 2.76 44 6% Dec by 5% 417 92 2.45 39 -6% Dec by 5% 412 90 2.40 38 -8% Dec by 10% 404 86 2.30 37 -12% Dec by 10% 392 82 2.19 35 -16% Dec by 5% Dec by 5% 399 84 2.25 36 -14% Dec by 10% Dec by 10% 368 71 1.91 31 -27%

Leela, unlike other major hotel chains in the country, does not have any near term plans to enter the mid-segment market to cater to domestic tourism. Till then such concentration on the upper cream of the business also exposes the company to the constraint of presence in only metro cities and tourist spots focused on foreign tourists.

Source: ICICIdirect Research

Source: Company, ICICIdirect Research

Hotel Leela would struggle to reduce its dependence on Bangalore and Mumbai till 2010

Probabale improvements in the ARRs or occupancies would not affect revenues or target price in a major way

8 | P a g e

Rooms to come with competition Although Hotel Leela has undertaken expansion plans to New Delhi, Pune, Chennai and Hyderabad, the company is not expecting any of the fresh capacities to be operational before CY10. By 2010 hotel sector should witness huge supplies coming in at major cities resulting in rationalisation of average room rates (ARRs) and cooling down of the occupancies.

Location Number of Rooms Capex Expected Commencement

Goa Additional 29 rooms 25 Cr Q1FY09 Udaipur 81 97 Cr Q1FY10 Gurgaon Mgmt Contract 319 rooms & 90 serviced residence Q3FY10 Delhi 205 927 Cr CY2010 Pune 200 320 Cr CY2010 Chennai 380 637 Cr CY2010 Hyderabad 250 385 Cr CY2010

NCR New Delhi is the official host for the 2010 Commonwealth Games. The games will span over a period of 11 days from October 3 to 14. During this period there would be a pressure to meet the accommodation requirement for around 40,000 international and inter-state visitors. Hotel Leela is foraying into Delhi NCR segment to participate in the race through a management contract for a five star deluxe hotel with 319 guest rooms and 90 serviced apartments. The hotel is expected to be fully operational by winter 2009. Currently, NCR has 7300 five star and deluxe rooms. Year 2009 is expected to increase the inventory by 870 rooms while by 2010 the capital is forecasted to have premium room inventory increased to 9090 with additions coming from Leela, Oberoi, Claridges, etc. Delhi & NCR hotel business would see ARRs and RevPARs peaking in 2010 during the Commonwealth games. Post-games, ARRs would rationalise and occupancies are expected to come down from the peaks encountered during October 2010.

In addition to the management contract, Leela has acquired a three-acre land in South Delhi for Rs 611 crore in April 2007. Hotel Leela Ventures intends to build an up-market hotel with a 205-room capacity on the site.

Udaipur Leela Palace, Udaipur will be strategically located besides the lake Pichola. The project will have 80 deluxe rooms. The hotel is expected to open by 2009.

Chennai Hotel Leela would be the only beach facing luxury hotel at prime Marina beach at Chennai. The property will sprawl over 7 acres with 380 luxury rooms. Work on the Hotel is under progress and the opening is slotted for 2010. Currently Chennai has room base of 1,541, which is expected to more than double to 3300 by 2010. Hotel Leela would have to brace itself for huge competition coming from the existing hotels as well as new entrants like Viceroy, Hilton, Taj etc.

Hyderbad The Leela Kempinski Hyderabad is being developed on prime location of Banjara hills. The 250-room hotel is expected to be commissioned by 2010. By the time Hyderabad project becomes operational, the city would have doubled its existing room inventory from 1365 to 2683 in 2010. The increase comes from expansion projects by Accor, Viceroy, Taj and from new entrants like Le Meridien, The Park and Taj GVK.

Current luxury room inventory of 7,300 rooms to grow to 9,090 rooms by 2010

Chennai room base to double by 2010 to 3300 from current 1541

Hyderabad too would double its room base from 1365 to 2683 by 2010

9 | P a g e

Pune The Leela Kempinski, Pune would be set in four acres designed as an urban resort. The property will also have an IT Park and commercial complex. This project is also expected to come onstream by 2010. Currently Pune has room count of 512 deluxe rooms while by the time Leela Kempinski would be entering Pune sector, the room base would have increased by 200% to 1538 rooms.

SWOT Risks to our call Hotel Leela’s is subject to very high dependence on the business

generated from the Bangalore (43% FY07) and Mumbai (38% FY07) properties. In case of delays in execution of the announced projects of these cities, ARRs, which are forecast to taper off and the occupancies to dip from the peak might continue to be strong. This would turn out to be a positive for the company.

The two major revenue drivers in Leela’s portfolio of porperties are business hotels. Cases of economic slowdown in competitor countries / cities, shifting of business interest towards the cities where Leela operates, medical hazard or terrorist activities in other geographies, would lead to an inflow of guests and would eventually benefit the company’s earnings.

Strengths Premium brand image enables it to

command high ARRs

Market leadership position in Bangalore territory

Weaknesses Excess dependence of revenue on Mumbai

and Bangalore

No presence in mid segment could lead to missing the spurt in Indian tourist interests

Opportunities Boom in hotel industry

Commonwealth games to propel demand

Threats Upcoming huge room

supply in all major cities

Civic unrest or acts of terror

10 | P a g e

Financials

The year that was… Hotel Leela saw its top line expanding by 16% to Rs 380 crore in FY07 against a 27% rise to Rs 327 crore in FY06. The reduction in the growth rate can be accounted on the reduced growth rate of room revenues, which slowed from Rs 214 crore, a 31% growth rate y-o-y in FY06, to Rs 256 crore, a 19% y-o-y growth in FY07. Company also made a non- recurring income through the sale of its business park in Mumbai for Rs 40.93 crore. EBIDTA saw a y-o-y growth of 14.5% to Rs 182 crores while EBIDTA margins took a hit of 81 basis points to settle at 47.8%. Leela’s bottom line showed a growth of 72.8% y-o-y to Rs 126.4 crore while net profit margin witnessed a jump of 1082 basis points to 33.2% on the back of the non recurring sale.

Exhibit 14: Revenue breakup (in Rs crore)

76.30 118.69 163.31 214.57 256.15 285.83 281.70

39.7655.73 71.82 83.32 95.70 110.60 116.56

18.36 20.99 21.56 29.06 29.01 32.20 32.50

0%

20%

40%

60%

80%

100%

FY03 FY04 FY05 FY06 FY07 FY08E FY09E

Room Revenue Food & Beverage Other Services

Food & Beverage support top line growth In the period FY07-09E, revenue from food & beverages is expected to grow at a CAGR of 10%, greater than the revenue growth of CAGR 6%. We foresee revenue generated from food & beverage to increase its contribution towards the top line to 27% at Rs 110 crore in FY08E and Rs 116 crore in FY09E. Room revenue is expected to grow at a CAGR of 5% to Rs 286 crore in FY08E and Rs 282 crore in FY09E.

Exhibit 15: Food & beverage to grow at greater pace than top line (in Rs crore)

0

100

200

300

400

500

FY03 FY04 FY05 FY06 FY07 FY08E FY09E

0

20

40

60

80

100

120

140

Revenue Food & Beverage

Source: Company, ICICIdirect Research

Source: Company, ICICIdirect Research

11 | P a g e

Pressure on EBIDTA margins The management contract for the Gurgaon hotel is expected to contribute 10% of revenue to the company’s top line. We expect Hotel Leela to encounter margin pressure in FY09. We forecast the Food & Beverage cost to grow at a CAGR of 10.78% during FY07-09E to Rs 39.3 crore in FY09E impacting the total expenditure to grow at CAGR 6.16% to Rs 288 crore in FY09E. While operating profits should witness a CAGR 6.56% growth in FY07-09E, we fear operating profit margins would be flat at 48% in FY08E-09E post a 47 basis point increase in FY08E to 48.3% from 47.8% in FY07.

Exhibit 16: Margins lose strength

43%

44%

45%

46%

47%

48%

49%

FY05 FY06 FY07 FY08E FY09E

OPM

0%

5%

10%

15%

20%

25%

30%

35%

NPM

Operating Margin (%) Net Profit Margin (%)

Return expectations fall short Hotel Leela’s return ratios seem to be strained due to slower bottom line growth. Due to the non-recurring income in FY07, return on net worth showed a bounce of 515 basis points to record 14%. If we exclude the sale proceeds of Business Park then FY07 would have registered an increase of 54 basis points in RONW to 9.4%. Going forward we expect RONW to increase by 63 basis points (ex non recurring income) to 10% in FY08E. But in FY09E, due to pressures on ARR and occupancy we forecast the RONW to retrace to 8.8%. Company could see its returns on capital employed slip below the 9% mark during the period FY07-08E settling at 7.5% in FY09E post recording 8.4% in FY08E from 9.7% in FY07.

Exhibit 17: Reducing returns

0%

2%

4%

6%

8%

10%

12%

14%

16%

FY05 FY06 FY07 FY08E FY09E

RONW ROCE

Source: Company, ICICIdirect Research

Source: Company, ICICIdirect Research

12 | P a g e

Revenue Model Number of Rooms FY06 FY07 FY08E FY09E

Mumbai 400 400 400 400 Bangalore 252 252 357 357 Goa 152 152 152 181 Kovalam 125 181 181 181

Occupancy Mumbai 75% 80% 78% 78% Bangalore 71% 75% 75% 75% Goa 71% 74% 74% 74% Kovalam 50% 70% 70%

ARR Mumbai 6000 8000 8000 8000 Bangalore 13000 15500 13000 12000 Goa 5500 7200 7200 7200 Kovalam 5000 5000 5000

RevPAR Mumbai 4500 6400 6240 6240 Bangalore 9230 11650 9750 9000 Goa 3905 5328 5328 5328 Kovalam 2500 3500 3500

Source: Company, ICICIdirect Research

13 | P a g e

Valuation We believe that Hotel Leela is richly valued and would continue to underperform the sector. We feel Leela’s current valuations have factored in the business growth till FY09. At the current price of Rs 44, the stock trades at P/E of 16.2x FY08E EPS of Rs 2.7 and 16.8x FY09E EPS of Rs 2.6. We don’t find much upside to these valuations for a company that is expecting most of its expansion plans to roll out post FY10. Moreover with an EV/EBIDTA at 14.75x in FY09E, current valuations seem to be rich in comparison to its peers.

Exhibit 18: Peer Comparison Company Year EPS P/E (x) EV/EBIDTA Indian Hotels FY06 30.5 44.5 21.5 FY07 5.2 27.8 14.2 FY08E 7.6 16.7 10.2 FY09E 9.0 14.1 9.1 EIH FY06 34.6 20.6 11.3 FY07 4.9 19.3 10.2 FY08E 5.5 19.8 12.5 FY09E 6.4 17.0 12.4 Hotel Leela FY06 9.9 22.1 15.8 FY07 3.4 12.8 14.1 FY08E 2.7 16.2 13.7 FY09E 2.6 16.8 14.7 Exhibit 19: Valuation

0

10

20

30

40

50

60

FY05 FY06 FY07 FY08E FY09E

P / E

0

1

2

3

4

EPS

P / E Diluted EPS

Currently, the stock is trading at 1.5 times its FY09 book value of Rs 29.6. We rate the stock as HOLD with a price target of Rs 42, 16x FY09E.

Exhibit 20: One year rolling PE band

0

10

20

30

40

50

60

70

80

90

Apr-0

4

Jun-

04

Aug-

04

Oct-0

4

Dec-

04

Feb-

05

Apr-0

5

Jun-

05

Aug-

05

Oct-0

5

Dec-

05

Feb-

06

Apr-0

6

Jun-

06

Aug-

06

Oct-0

6

Dec-

06

Feb-

07

Apr-0

7

20x

16x

8x

12x

Source: ICICIdirect Research

Source: ICICIdirect Research, Reuters Consensus Estimates

Source: Company, ICICIdirect Research

14 | P a g e

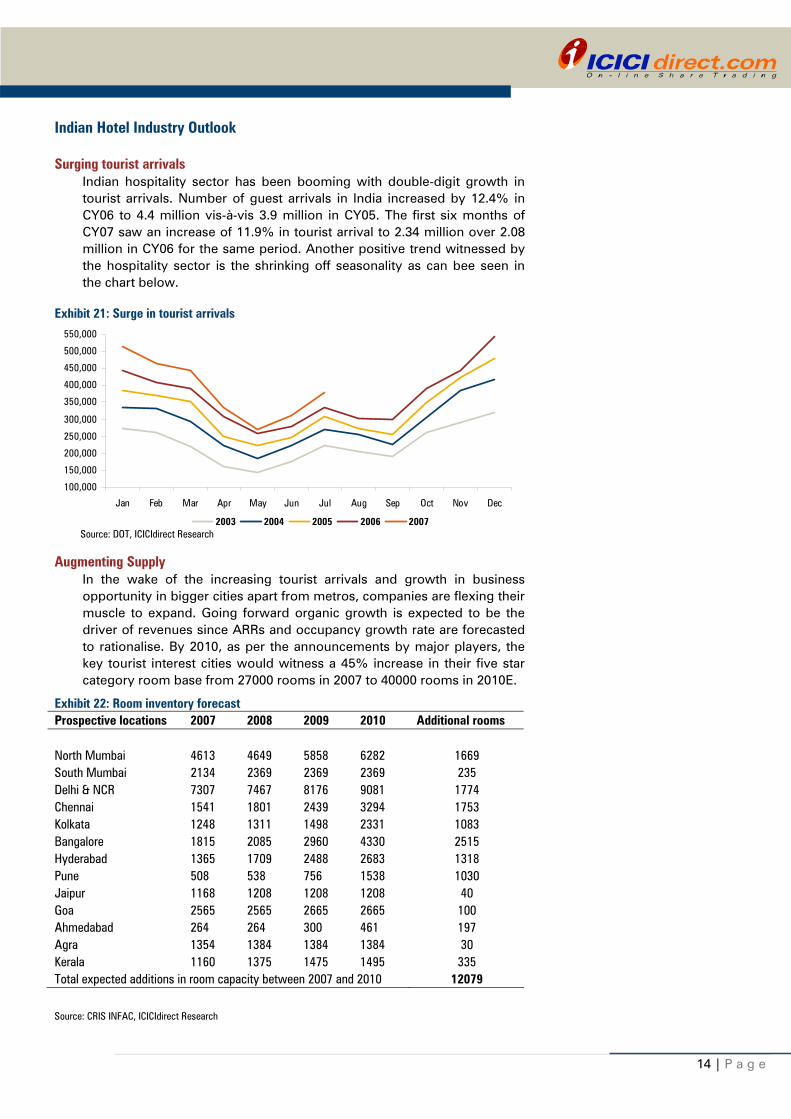

Indian Hotel Industry Outlook Surging tourist arrivals

Indian hospitality sector has been booming with double-digit growth in tourist arrivals. Number of guest arrivals in India increased by 12.4% in CY06 to 4.4 million vis-à-vis 3.9 million in CY05. The first six months of CY07 saw an increase of 11.9% in tourist arrival to 2.34 million over 2.08 million in CY06 for the same period. Another positive trend witnessed by the hospitality sector is the shrinking off seasonality as can bee seen in the chart below.

Exhibit 21: Surge in tourist arrivals

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2003 2004 2005 2006 2007

Augmenting Supply In the wake of the increasing tourist arrivals and growth in business opportunity in bigger cities apart from metros, companies are flexing their muscle to expand. Going forward organic growth is expected to be the driver of revenues since ARRs and occupancy growth rate are forecasted to rationalise. By 2010, as per the announcements by major players, the key tourist interest cities would witness a 45% increase in their five star category room base from 27000 rooms in 2007 to 40000 rooms in 2010E.

Exhibit 22: Room inventory forecast Prospective locations 2007 2008 2009 2010 Additional rooms North Mumbai 4613 4649 5858 6282 1669 South Mumbai 2134 2369 2369 2369 235 Delhi & NCR 7307 7467 8176 9081 1774 Chennai 1541 1801 2439 3294 1753 Kolkata 1248 1311 1498 2331 1083 Bangalore 1815 2085 2960 4330 2515 Hyderabad 1365 1709 2488 2683 1318 Pune 508 538 756 1538 1030 Jaipur 1168 1208 1208 1208 40 Goa 2565 2565 2665 2665 100 Ahmedabad 264 264 300 461 197 Agra 1354 1384 1384 1384 30 Kerala 1160 1375 1475 1495 335 Total expected additions in room capacity between 2007 and 2010 12079 Source: CRIS INFAC, ICICIdirect Research

Source: DOT, ICICIdirect Research

15 | P a g e

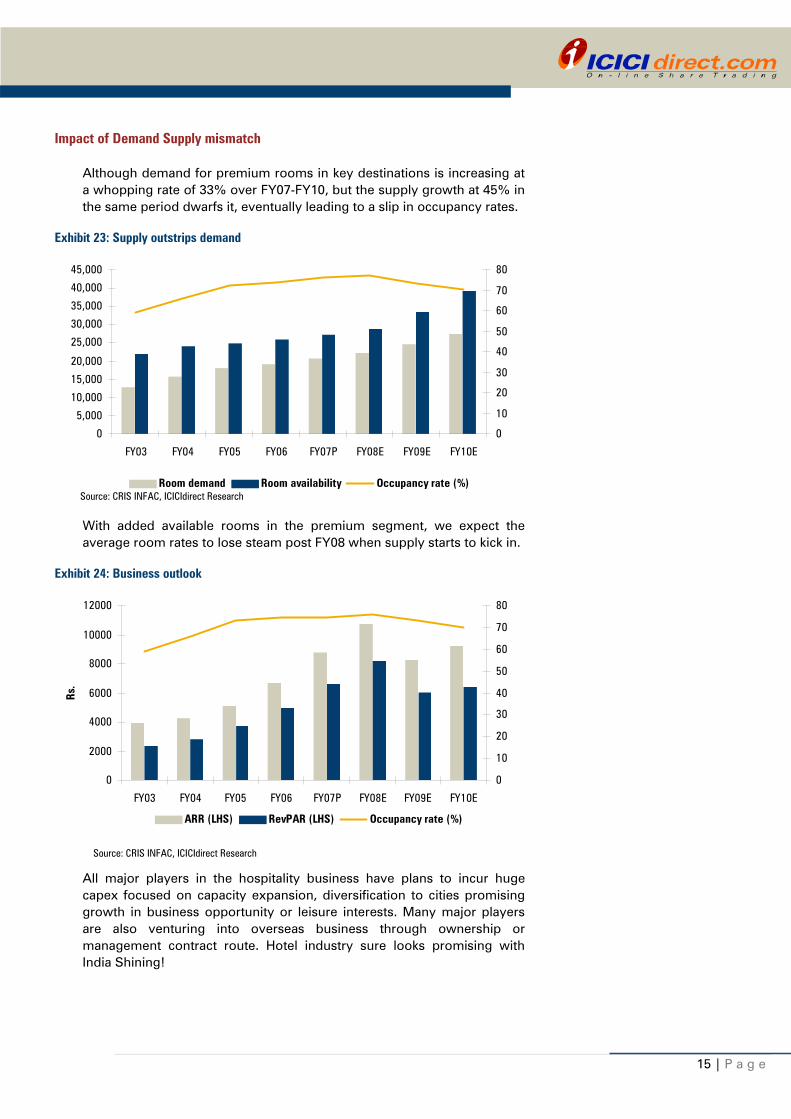

Impact of Demand Supply mismatch

Although demand for premium rooms in key destinations is increasing at a whopping rate of 33% over FY07-FY10, but the supply growth at 45% in the same period dwarfs it, eventually leading to a slip in occupancy rates.

Exhibit 23: Supply outstrips demand

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

FY03 FY04 FY05 FY06 FY07P FY08E FY09E FY10E

0

10

20

30

40

50

60

70

80

Room demand Room availability Occupancy rate (%)

With added available rooms in the premium segment, we expect the average room rates to lose steam post FY08 when supply starts to kick in.

Exhibit 24: Business outlook

0

2000

4000

6000

8000

10000

12000

FY03 FY04 FY05 FY06 FY07P FY08E FY09E FY10E

Rs.

0

10

20

30

40

50

60

70

80

ARR (LHS) RevPAR (LHS) Occupancy rate (%)

All major players in the hospitality business have plans to incur huge capex focused on capacity expansion, diversification to cities promising growth in business opportunity or leisure interests. Many major players are also venturing into overseas business through ownership or management contract route. Hotel industry sure looks promising with India Shining!

Source: CRIS INFAC, ICICIdirect Research

Source: CRIS INFAC, ICICIdirect Research

16 | P a g e

Financial Summary Profit & Loss Account (Rs crore) Year ending March 31 FY06 FY07 FY08E FY09E Net Sales 326.95 380.86 428.63 430.76 Other Income 19.49 71.54 30.00 30.00 Total Expenditure 168.00 198.80 221.70 224.04 Operating Profit 158.95 182.06 206.93 206.72 Interest 33.00 30.16 47.55 54.75 Depreciation 36.17 37.84 39.40 38.50 Profit Befor Tax 111.54 189.70 149.98 144.97 Tax 38.37 63.27 49.54 47.92 Net Profit 73.17 126.43 100.44 97.06 Operating Margin 48.6% 47.8% 48.3% 48.0% Profit Margin 22.4% 33.2% 23.4% 22.5% Outstanding Shares 7.37 37.03 37.03 37.03 Diluted EPS (Rs) 1.99 3.41 2.71 2.62 Balance Sheet (Rs crore) Year ending March 31 FY06 FY07 FY08E FY09E Equity Share Capital 112.46 74.06 74.06 74.06 Reserves & Surplus 711.59 827.12 927.55 1024.61 Secured Loans 683.11 591.72 990.65 1140.65 Unsecured Loans 373.23 361.07 364.84 364.84 Deferred Tax Liability 36.28 75.25 105.25 134.24 Total Liabilities 1916.67 1929.23 2462.35 2738.40 Net Block 1400.02 1517.21 1525.17 1623.02 Capital Work in Progress 145.50 193.60 593.60 823.60 Investments 59.92 59.92 59.92 59.92 Net Current Assets 311.23 158.51 283.67 231.86 Misc. Expense w/o 0.00 0.00 0.00 0.00 Total Assets 1916.67 1929.23 2462.35 2738.40

Laggard growth in revenue expected

Capex funding to pose burden on leverage

17 | P a g e

Ratios (Rs crore) Year ending March 31 FY06 FY07 FY08E FY09E Diluted EPS (Rs.) 1.99 3.41 2.71 2.62 Cash EPS (Rs.) 17.09 4.10 4.30 4.10 Book Value (Rs.) 111.79 24.34 27.05 29.67 Operating Margin (%) 48.6% 47.8% 48.3% 48.0% Net Profit Margin (%) 22.4% 33.2% 23.4% 22.5% RoNW(%) 8.9% 14.0% 10.0% 8.8% RoCE(%) 8.1% 9.7% 8.4% 7.5% Debt / Equity 1.28 1.06 1.35 1.37 Fixed Asset Turnover Ratio 0.21 0.22 0.20 0.18 Enterprise Value (Rs. Cr.) 2515.33 2571.44 2845.02 3049.25 EV/EBIDTA 15.82 14.12 13.75 14.75 Sales to Equity 44.36 10.29 11.58 11.63 Market Capitalisation (Rs. Cr.) 1621.65 1629.33 1629.33 1629.33 Market Cap to Sales 4.96 4.28 3.80 3.78 Price to Book Value 1.97 1.81 1.63 1.48 Cash Flow (Rs crore) Year ending March 31 FY06 FY07 FY08E FY09E Opening Cash 52.06 162.65 10.70 139.81 Profit After Tax 73.17 126.43 100.44 97.06 Depreciation 32.45 35.78 39.40 38.50 Dividend Paid & Others 22.81 -23.03 0.00 0.00 Cash Profit 128.43 139.18 139.83 135.56 Changes in WC Net Increase in CL 1.00 34.78 10.98 -1.09 Net increase in CA -44.31 -42.86 7.03 1.34 Cash Flow after change in working capital 173.74 216.82 143.78 133.13 Cash Flow from investing activity -342.15 -124.49 -447.36 -366.36 Cash Flow from financing activity 279.00 -244.28 402.69 150.00 Net Cash inflow 110.59 -151.95 99.12 -83.23 Closing Cash 162.65 10.70 109.81 56.58

Margins to hover in the same range without any signs of improvement

15 | P a g e

ICICIDirect endeavours to provide objective opinions and recommendations. ICICIdirect assigns ratings to its stocks according to their notional target price vs current market price and then categorises them as Outperformer, Performer, Hold, and Underperformer. The performance horizon is 2 years unless specified and the notional target price is defined as the analysts' valuation for a stock.

RATING RATIONALE

Outperformer: 20% or more; Performer: Between 10% and 20%; Hold: +10% return; Underperformer: -10% or more.

Harendra Kumar Head - Research & Advisory [email protected] ICICIdirect Research Desk, ICICI Securities Limited, 2nd Floor, Stanrose House, Appasaheb Marathe Marg, Prabhadevi, Mumbai – 400 025 [email protected]

Disclaimer The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities Ltd (I-Sec). The author of the report does not hold any investment in any of the companies mentioned in this report. I-Sec may be holding a small number of shares/position in the above-referred companies as on date of release of this report. This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein is solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This report may not be taken in substitution for the exercise of independent judgement by any recipient. The recipient should independently evaluate the investment risks. I-Sec and affiliates accept no liabilities for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Actual results may differ materially from those set forth in projections. I-Sec may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject I-Sec and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.