Potential Accounting Tunneling Fraud at China Environment (Part 3)

12

1 Potential Accounting Tunneling Fraud at China Environment (CENV SP)? By Terence CHUA Tong Liang and KIM Jia Liang Roy 23 rd February 2015 1 Introduction The third part of our report on China Environment raises questions on the accounting quality of their audited statements, some of the concerns we have also include the continuous need to raise money from investors. We strongly encourage readers to read the first two parts of the report in order to gain a more complete picture of China Environment. Part 1: http://asianextractor.com/2015/02/10/potential-accounting-tunneling-fraud-at- china-environment/ Part 2: http://asianextractor.com/2015/02/17/potential-accounting-tunneling-fraud-at- china-environment-part-2/ 2 CAPEX Spending In China Env’s Oct 2013 presentation, they announced the completion of the Anhui’s factory in Aug 2013 (see Figure 3). The completion of the Anhui factory was again emphasized in Nov 2013 ppt (see Figure 4). However China Env failed to transfer the construction work-in-progress portion of Anhui factory in its FY13 annual report for the year ended 31 Dec 2013 (see Figure 1), even though it repeated twice that it was completed at Aug 2013. As per its accounting policies (see Figure 2), the future economic benefits of the Anhui factory would have been recognized at its completion and so it should be transferred out of the WIP account. Ever since acquiring the land for Anhui factory in April 2012 for RMB49m, progress on building the factory has been rapid. , 90% of the cost (RMB246m) for Anhui factory has been incurred by Sep 2012. The land for Fujian factory is acquired in Nov 2010 for RMB4.4m. For the Fujian and Anhui factory, the estimated total cost is RMB326.7m (see Figure 5). For RMB326.7m capex project, the management implied that the cost will be funded entirely by internally generated funds (see Figure 4). To us, Internal generated funds = Net cash generated from operating activities. We shall break down China Env’s cash flow from operations (CFO) over the years to determine fairly its ability to substantiate its ability to fund entirely its capex by internally generated funds. Year CFO (in RMB’m) 2009 -65m 2010 -64m 2011 -15m 2012 284m 2013 -98m Total 42m While China Env had positive cash flow in excess of RMB284m in FY12, total capex totaled RMB326.7m. It would be unfair to say that it was funded entirely by

-

Upload

asianextractor -

Category

Business

-

view

2.537 -

download

3

Transcript of Potential Accounting Tunneling Fraud at China Environment (Part 3)

1

Potential Accounting Tunneling Fraud at China Environment (CENV SP)? By Terence CHUA Tong Liang and KIM Jia Liang Roy 23rd February 2015 1 Introduction The third part of our report on China Environment raises questions on the accounting quality of their audited statements, some of the concerns we have also include the continuous need to raise money from investors. We strongly encourage readers to read the first two parts of the report in order to gain a more complete picture of China Environment. Part 1: http://asianextractor.com/2015/02/10/potential-accounting-tunneling-fraud-at-china-environment/ Part 2: http://asianextractor.com/2015/02/17/potential-accounting-tunneling-fraud-at-china-environment-part-2/ 2 CAPEX Spending In China Env’s Oct 2013 presentation, they announced the completion of the Anhui’s factory in Aug 2013 (see Figure 3). The completion of the Anhui factory was again emphasized in Nov 2013 ppt (see Figure 4).

However China Env failed to transfer the construction work-in-progress portion of Anhui factory in its FY13 annual report for the year ended 31 Dec 2013 (see Figure 1), even though it repeated twice that it was completed at Aug 2013. As per its accounting policies (see Figure 2), the future economic benefits of the Anhui factory would have been recognized at its completion and so it should be transferred out of the WIP account.

Ever since acquiring the land for Anhui factory in April 2012 for RMB49m, progress on building the factory has been rapid. , 90% of the cost (RMB246m) for Anhui factory has been incurred by Sep 2012. The land for Fujian factory is acquired in Nov 2010 for RMB4.4m. For the Fujian and Anhui factory, the estimated total cost is RMB326.7m (see Figure 5). For RMB326.7m capex project, the management implied that the cost will be funded entirely by internally generated funds (see Figure 4). To us, Internal generated funds = Net cash generated from operating activities. We shall break down China Env’s cash flow from operations (CFO) over the years to determine fairly its ability to substantiate its ability to fund entirely its capex by internally generated funds.

Year CFO (in RMB’m)

2009 -65m

2010 -64m

2011 -15m

2012 284m

2013 -98m

Total 42m

While China Env had positive cash flow in excess of RMB284m in FY12, total capex totaled RMB326.7m. It would be unfair to say that it was funded entirely by

2

internally generated funds. Cumulative CFO for 5 years totaled a meagre RMB42m. Bad operating cash flow management over the years due to the build-up of trade receivables which almost totaled a full year of revenue in FY13. Trade receivables increased from 40% of revenue in FY2009 to 94% of revenue in FY2013.

So the question that we wished to bring forward is as follows; “Is it fair to say that China Env funded entirely its RMB326.7m capex by internally generated funds?”. For us, the answer is No.

Figure 1 (PPE in 2013AR)

3

Figure 2

Figure 3 (Oct 2013 ppt)

Figure 4 (Nov 2013 ppt)

Figure 5 (23 Nov 2012 SGX filing) 3 China Env’s auditor, Baker Tilly

4

China Env entered into a reverse takeover (RTO) with Gates Electronic in Aug 2009. Baker Tilly took over as auditor of the China Env from Mazars LLP after the completion of the RTO in Aug 2009. The auditor partner-in-charge was changed to Ms Tiang Yii from Baker Tilly as of 31 Dec 2009.

Then Gates Electronic Chief Financial Officer Ms Jaslyn Tey resigned due to personal reason and was replaced by Mr Chiar Choon Teck in June 2010. The reason for the hiring of Mr Chiar Choon Teck was given as per SGX filing on 26 May 2010;

link: http://infopub.sgx.com/Apps?A=COW_CorpAnnouncement_Content&B=AnnouncementLast5thYearSecurity&F=30BD7BEE81E642CE48257729002ED4F2&H=08cc979ed1bf0c13504b961b648c4fcb6f9d91922fb44bf4d234c5f959ab03d3#.VONY6XacxEw “ The Board, having reviewed and talked to a few potential candidates, has approved the appointment of Mr Chiar as the Chief Financial Officer of the Company, in view of his past working experience and his familiarity with the Group as he was the audit manager in charge of the external audit of the Group. As such, he is familiar with the accounting functions, internal control as well as the staff and management of the Group. ”

Baker Tilly has been appointed auditor since Aug 2009 and Mr Chiar was appointed as CFO on June 2010. It seems that Mr Chiar has been audit manager auditing China Env for <1 year and he was deemed to be familiar with China Env’s accounting functions (see Figure 6). After Mr Chiar was appointed CFO, Baker Tilly remained as its auditor.

As per China Env’s 2013 annual report, Baker Tilly was referred to as “independent auditor” (see Figure 7). We are of the opinion that China Env should have its shareholders’ interest in mind and suggest a change of auditors eg every 5 years. This is so as the CFO was formerly from Baker Tilly and was auditing China Env when he was the audit manager. Considering the scale of China Env’s business, a Big 4 auditor firm would be well-suited for them.

Ms Tiang Yii has been the auditor partner-in-charge of China Env since 31 Dec 2009. While we are not doubtful of Ms Tiang Yii’s ability, she has however received negative publicity in the press for her role in City Harvest trial regarding her role in Xtron Productions as she signed off on her audit of Xtron Productions as per Asiaone article (see Figure 8). In comparison, China Env’s accounts have been signed off by her since her appointment at 31 Dec 2009.

link to article: http://news.asiaone.com/news/crime/city-harvest-trial-full-scale-probe-auditor-says-defence 4 Trade Receivables Past Due As of FY2013, trade receivables totaled RMB491.4m. Of the RMB491.4m, RMB235.5m are not past due yet. However, the other RMB255.9m are past due (see Figure 9). That implies that 52% of receivables are past due and none are impaired in 2013. The reason China Env gave for the increase in receivables (as per Q3’2014 earnings commentary) are; “ The increase in trade receivables was due to overall slower debt collection as a result of tighter government credit control in PRC.Over the past three years, the Group has had no

5

bad debt or doubtful debt provision. This is the result of the Group’s stringent policy in selecting high quality customers. “

Figure 9 (2013AR ageing analysis of trade receivables)

If we choose to be prudent and impair those receivables past due more than 90 days, an impairment of RMB90.9m would have to be recorded. Compare this to FY13 net profit of RMB74.6m, impairment would wipe out its entire net profit for the year. Recording this impairment would result in tax loss carryforwards which may not be a bad outcome for the company. While we acknowledge China Env has paid the relevant income tax, the large increase in trade receivables is still a huge concern. We reckon that the auditor should have raised the awareness of subjecting these past due receivables for impairments. With the Chinese government easing the credit over the past few months via several policies, we believe the credit condition in China will improve and China Env should ought to record a significant drop in its past due receivables over the next few quarters. 5 Insider Ownership (Huang Min) We then examine Huang Min, ex-CEO & current Chairman, for his share ownership since taking control of China Env after its RTO in 2009 (see Figure 10). We have illustrated his transactions on China Env’s price chart (see Figure 11). Numerous buys of <1m shares in 2010 were followed by several sales of >10m shares in 2013. We are concerned about small buy orders being accompanied by gigantic sell orders. Since 2010 till now, Huang Min’s share holdings has been reduced from 241m shares to 149m, a reduction of 38%. To us, this feels like a lack of confidence in China Env. In addition, we are concerned that China Env did not give a detailed disclosure regarding the 36m shares foreclosure by BHP on Huang Min as the shares involved represented 4.5% of shares outstanding.

6

Figure 10 (Huang Min’s Share Transactions of China Env)

Figure 11 (Huang Min’s Share Transactions on China Env’s chart) 6 Why is there a need to raise more money? We were surprised by the need for China Environment’s latest fund raising exercise just 3 months ago on the 12th of December 2014 given that they’ve already secured two credit facilities in the same year for a total of RMB250 million. According to the same announcement, the directors have sought to affirm investors that it is the view of the directors that the current credit facilities are sufficient to meet the needs of the group. (They had explained in the same filing that this was for future expansion purposes, but left it vague what exactly it is to be used for) Which begs the question, why is there a need to raise additional capital when there are bank credit facilities available? According to their company filing on the 13th of November 2014, titled “Change in use of net proceeds of the placement of 65 million ordinary shares in the capital of China Environment Ltd” http://infopub.sgx.com/FileOpen/CEL_Change_In_Use_Of_Proceeds.ashx?App=Announcement&FileID=324401

Transaction Date Noofshares('000) Averagecost($) SharesOwned('000) CommentsBUY 26/02/10 1,000 0.32 241,050

BUY 01/03/10 360 0.37 241,410

TRANSFER 16/04/10 35,000 241,410 Transfer35msharestoLGTBank(citibankcustodian)

BUY 18/05/10 720 242,130

BUY 19/05/10 280 242,410

BUY 10/06/10 1,018 243,428

TRANSFER 29/07/10 10,000 243,428 Transfer35msharestoLGTBank(citibankcustodian)

BUY 26/08/10 360 243,788

BUY 27/08/10 640 244,428

BUY 16/06/11 780 245,208

BUY 17/06/11 500 245,708

SELL 10/06/13 10,000 235,728

SELL 05/09/13 10,000 0.25 225,728 10mvendorsharesinsecoffering

SELL 16/09/13 25,000 0.33 200,728

SELL 23/10/13 20,000 0.53 180,728 SubsequentlyHunagMinloan$12mtoFujianDongyuan

TRANSFER 18/11/13 135,728 180,728 Transfer136msharestoCreditSuissecustodian

BUY 26/03/14 288 0.46 181,016

BUY 27/03/14 112 0.45 181,128

BUY 08/05/14 1,000 0.40 182,128

BUY 09/05/14 200 0.40 182,328

BUY 04/09/14 171 182,499 1sttransactionaftersteppingdownasCEO

BUY 05/09/14 477 182,976

BUY 09/09/14 1,000 183,976

BUY 10/09/14 343 184,319

FORECLOSURE 12/01/15 36,000 148,319 BHPforecloseon36mshares.Noreasondisclosed

BUY 19/01/15 1,000 0.25 149,319

7

The announcement was a follow up of the announcement on the 22nd August 2013. This fund raising exercise was also highlighted in the report in Part 2 of the report on Potential Tunneling in China Environment. According to the announcement above, there is a balance of the net proceeds which amounted to approximately S$2.9 million (RMB13.28 mn). They have now announced that they intend to utilize their net proceeds for general working capital purposes principally to fund the general working capital requirement of the Company (Suggesting that they have spare capital within the company) A month later however, the company on the 12th of December 2014 announced their intention to have placement of new ordinary shares and warrants. http://infopub.sgx.com/FileOpen/China_Env_Announcement_on_placement.ashx?App=Announcement&FileID=327980 Their proposal will increase the total amount of new ordinary shares by 72,500,000 new shares and is to be fully subscribed by Global Win.

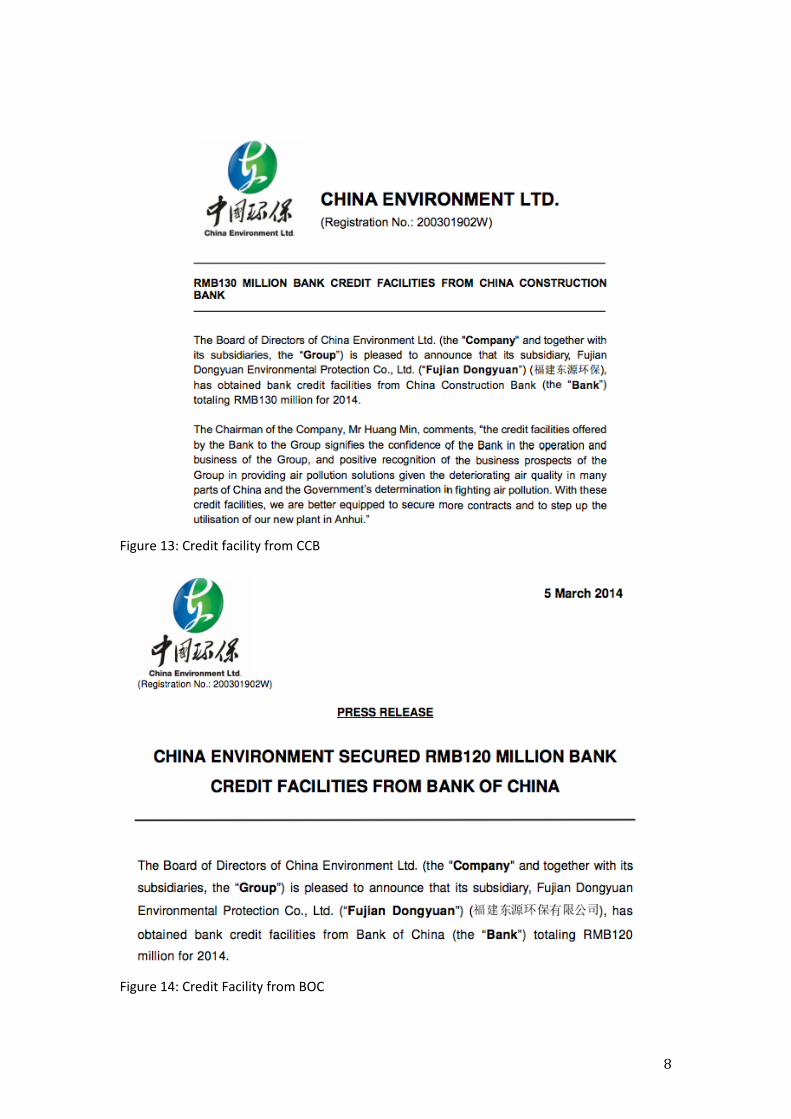

Figure 12: Use of Proceeds The company expects the entire placement to net an estimated S$14.98 million. For consistency, we have used the same exchange rate conversion (1 SGD/ 4.58 CNY) in all our reports. Readers should be aware that actual conversion might differ slightly. This means that they will net an approximate RMB68.8m. According to their filings on the 13th of January 2014, they have secured RMB130 million in credit facilities from China Construction Bank, this was followed up by their announcement on the 5th of March 2014 that they have secured an RMB120 million bank credit facilities from Bank of China. http://infopub.sgx.com/FileOpen/CEL_BankCreditFacilities.ashx?App=Announcement&FileID=1329 http://infopub.sgx.com/FileOpen/CEL_RMB120MILLION_FACILITIES_FROM_BOC.ashx?App=Announcement&FileID=284958

8

Figure 13: Credit facility from CCB

Figure 14: Credit Facility from BOC

9

According to their 2014 filings, their subsidiary Fujian Dongyuan has secured a total of 10 new contracts worth a total of RMB560.4 million. The first announcement was made on the 20th of January 2014 for two new contracts worth RMB393.6 million and the second was an announcement made on the 15th of May 2014 worth RMB166.8 million. http://infopub.sgx.com/FileOpen/CEL_Contracts_Won_PressRelease.ashx?App=Announcement&FileID=2023 http://infopub.sgx.com/FileOpen/CEL_ContractsWon_PressRelease_15May2014.ashx?App=Announcement&FileID=297370 Followers of our second report will again notice the uncanny coincidence in the fund raising activities of the firm and the expiry of their contract. We attached the second page of both reports here.

Figure 15: Contract won in January

Figure 16: Contract won in May Given that both contracts are close to completion or are already completed, why did the management of the company not use these contracts to borrow debt from the banks instead? Given that the amount they are trying to raise in December 2014 is only 12.3% (68.8 / 560.4) of the total contract volume, raising the money from the bank or having a credit facility would have been a cheaper alternative instead especially since they have no immediate plans for the money raised.

10

Instead, as we have noticed in their fourth quarter results announcements for 2013 and most latest quarter’s financial statements (3rd quarter 2014), they have not resorted to this form of financing; http://infopub.sgx.com/FileOpen/CEL4Q2013.ashx?App=Announcement&FileID=283536

Figure 17: Details of collateral http://infopub.sgx.com/FileOpen/CEL_3Q2014.ashx?App=Announcement&FileID=323955

11

Figure 18: Details of collateral third quarter 2014 (Latest results release at time of publication) 7 Days Sales Outstanding and Gross Margin disparity

Gross Margin 2010 2011 2012 2013

Fujian Longking Co Ltd (600388 CH) 19.9% 23.2% 21.8% 19.6%

Zhejiang Feida (600526 CH) 13.5% 15.3% 15.5% 15.6%

China Environment 28.6% 25.1% 22.3% 24.5%

Days Sales Outstanding 2010 2011 2012 2013

Fujian Longking Co Ltd (600388 CH) 101.7 122.2 117.8 114.0

Zhejiang Feida (600526 CH) 63.0 71.0 78.2 105.6

China Environment 266.2 369.8 292.3

Figure 19: Peer comparison From the table above, we can see that Days sales outstanding is easily one year, and more than twice that of their closest competitors. Market Capitalization: Fujian Longking (RMB 14.7bn); Zhejiang Feida (RMB 6.07bn)1 versus China Environments RMB 656 mn. According to the SGX query in 2013; From SGX Query in 2013: http://infopub.sgx.com/FileOpen/Responses_SGX_Queries_3Q2013_results.ashx?App=Announcement&FileID=48993 "Our standard contract with our customers provides for progressive payments; payment milestone will be based on different completion stages of a project. The payment schedule varies from project to project depending on negotiated terms. The range of payment schedules could be as follows:

1 Financial Times on the 20th of February 2015

12

a) 10% to 30% of the contract sum is paid upon signing of the contract; b) 0% to 30% of the contract sum is paid upon delivery of the industrial waste gas solution system to our customer’s site; c) 30% to 80% of the contract sum is paid upon installation and commissioning of the industrial waste gas solution system; d) 10% of the contract sum is to be paid after expiry of the 12-month warranty period as retention money. Typically, we will offer a credit period of up to 30 days for each payment milestone. " Days Sales outstanding is easily one year. When China Environment went for RTO, the DSO was only around days, in line with the peers’ average. Why did it differ by so much now? 8 Appendix Fujian Longking Co., LTD is principally engaged in manufacture, distribution and installation of electro filter equipment and related devices. The Company also involves in operation of desulphurization projects, property distribution and leasing, property management, materials distribution, technology services, hydropower generation and transportation services. http://markets.ft.com/research/Markets/Tearsheets/Business-profile?s=600388:SHH ZHEJIANG FEIDA ENVIRONMENTAL SCIENCE & TECHNOLOGY CO., LTD. is principally engaged in the research, development, design, manufacture and sale of environmental protection equipment. The Company provides electrostatic precipitators, pneumatic conveying equipment, fuel gas desulfurization equipment, electrical component parts, switch cabinets, waste incineration flue gas treatment equipment and bag dust collectors, among others. It also provides installation and technical services. Through its subsidiaries, the Company is involved in the manufacture and sale of environmental protection equipment and chemical products. The Company distributes its products within domestic market and to overseas markets. http://markets.ft.com/research/Markets/Tearsheets/Business-profile?s=600526:SHH