Porvair ppt prelims_final

20

1 Presentation Year ended 30 November 2014 Ben Stocks Chief Executive Chris Tyler Finance Director Specialist filtration & environmental technology

-

Upload

company-spotlight -

Category

Investor Relations

-

view

995 -

download

0

Transcript of Porvair ppt prelims_final

1

Presentation Year ended 30 November 2014

Ben Stocks Chief Executive

Chris Tyler Finance Director

Specialist filtration & environmental technology

2

Consistent strategy 2009 - 2014

In the year ended 30 November

2014

Niche positions in growing,

regulated markets

New product development

and intellectual property

13% CAGR in revenue

£52m cash from operations

47% return on operating capital employed

23% revenue growth to

£104m

17% EPS growth to 14.4p

£5.3m Net cash

SUMMARY Consistent strategy delivering results

£19m invested

£19m debt reduction

3

SPECIALIST FILTRATION And environmental technology

Specialist filters are used to protect costly or complex downstream systems

Attractive business characteristics

Niche positions: Consumables Long life cycles Bespoke

Robust demand drivers: Secular trends Regulation/legislation Process reliability

Barriers to entry: Patent protection Quality accreditation Design rights

4

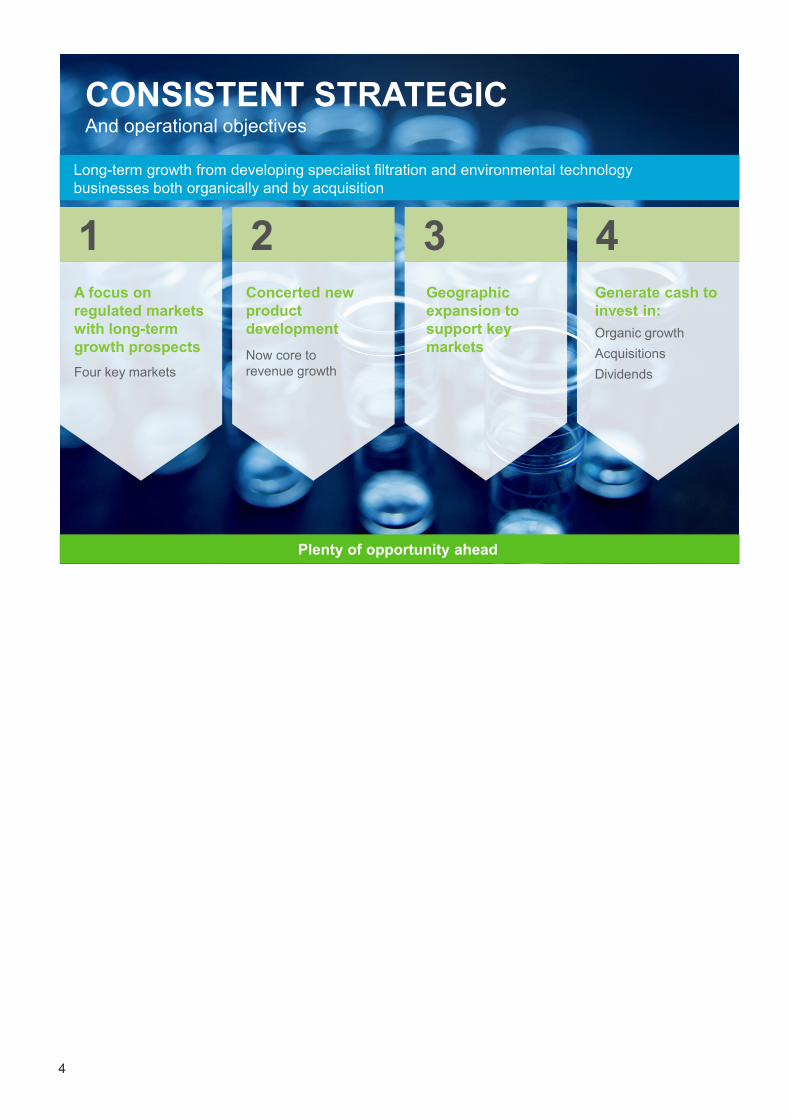

CONSISTENT STRATEGIC And operational objectives

Long-term growth from developing specialist filtration and environmental technology businesses both organically and by acquisition

1 2 3 4 A focus on regulated markets with long-term growth prospects Four key markets

Concerted new product development Now core to revenue growth

Geographic expansion to support key markets

Generate cash to invest in: Organic growth Acquisitions Dividends

Plenty of opportunity ahead

5

A FOCUS ON REGULATED MARKETS With long-term growth prospects

1 2 3 4

Growth in pax revenue miles 2013 - 2033 (Source: Boeing 2014)

FAA, CAA, EASA and other specific accreditations

5.0% p.a.

Growth in gasification 2011 - 2016 (Source: US DOE 2010)

International nuclear standards: NQA1, ASME, etc

11.5% p.a.

Growth in water analysis consumables 2011 - 2016 (Source: SDI Research 2012)

Approved methods: EPA, SEPA, EU water directives

5.6% p.a.

Growth in primary aluminium usage 2015 (source: Alcoa 2015)

ISO and customer accreditations; extensive qualification requirements

7.0% p.a.

Aviation

Energy and industrial process

Environmental laboratory supplies

Molten metals

Regulation Market Growth Markets

6

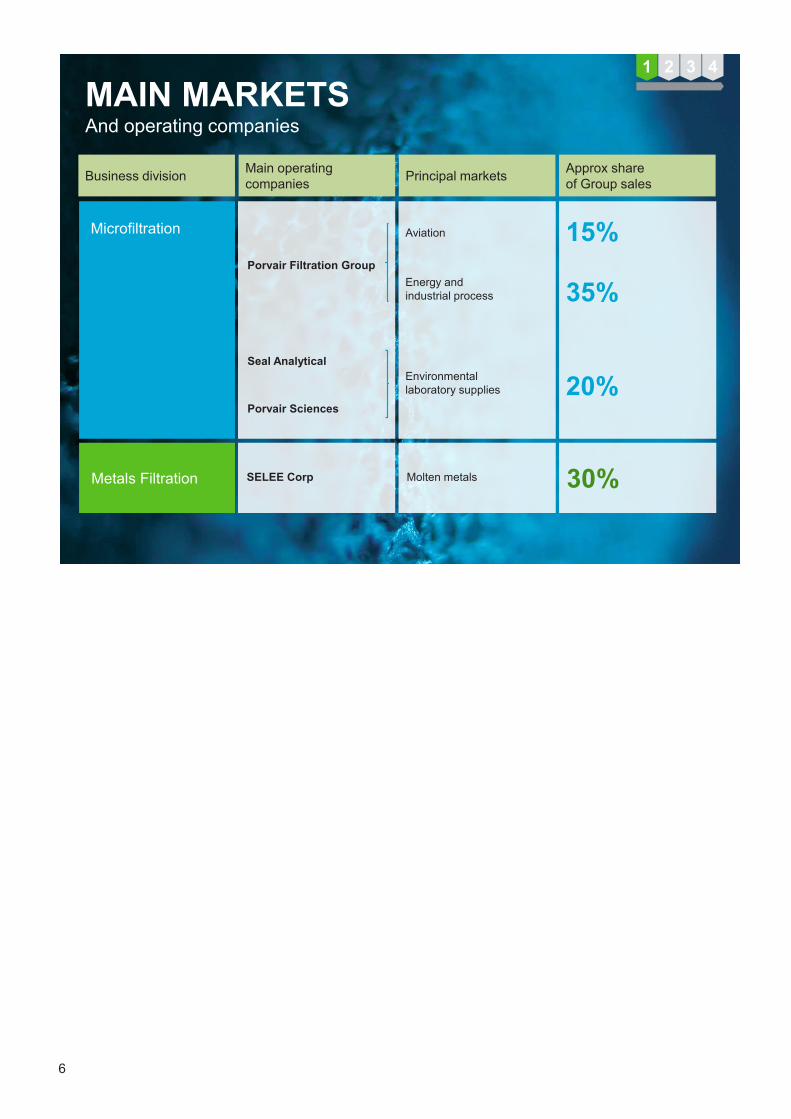

MAIN MARKETS And operating companies

1 2 3 4

Porvair Filtration Group

Seal Analytical

Porvair Sciences

Aviation

Energy and industrial process

Environmental laboratory supplies

15%

35%

20%

SELEE Corp Molten metals 30%

Microfiltration

Metals Filtration

Business division Main operating companies Principal markets Approx share

of Group sales

7

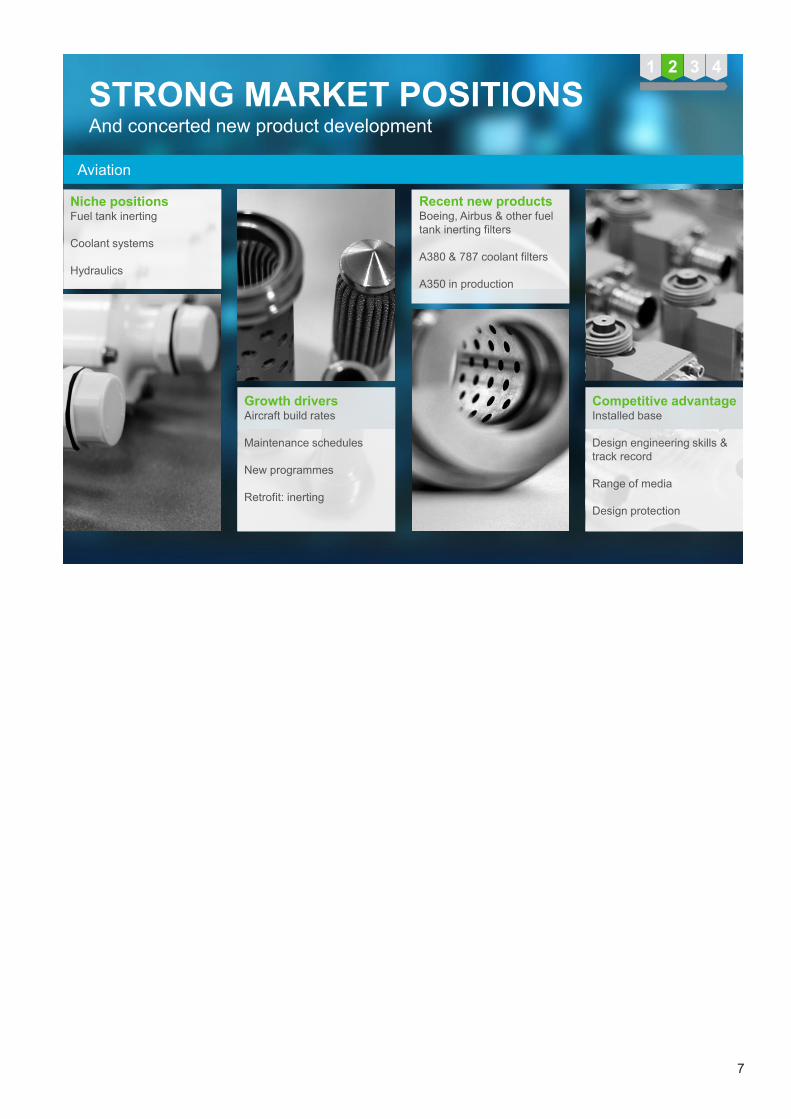

Niche positions Fuel tank inerting Coolant systems Hydraulics

Growth drivers Aircraft build rates Maintenance schedules New programmes Retrofit: inerting

Competitive advantage Installed base Design engineering skills & track record Range of media Design protection

Recent new products Boeing, Airbus & other fuel tank inerting filters A380 & 787 coolant filters A350 in production

STRONG MARKET POSITIONS And concerted new product development

Aviation

1 2 3 4

8

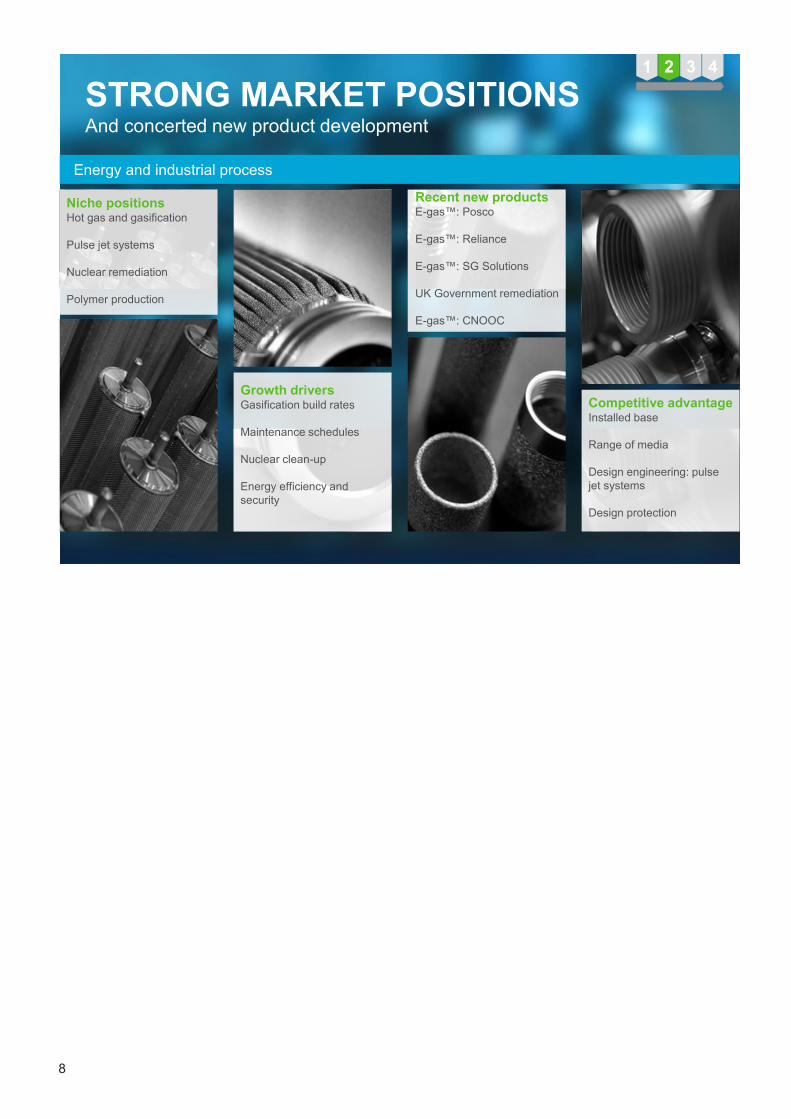

STRONG MARKET POSITIONS And concerted new product development

Energy and industrial process

1 2 3 4

Niche positions Hot gas and gasification Pulse jet systems Nuclear remediation Polymer production

Growth drivers Gasification build rates Maintenance schedules Nuclear clean-up Energy efficiency and security

Competitive advantage Installed base Range of media Design engineering: pulse jet systems Design protection

Recent new products E-gas™: Posco E-gas™: Reliance E-gas™: SG Solutions UK Government remediation E-gas™: CNOOC

9

Niche positions Analysis of inorganic chemicals in water Associated consumables Porous plastics

Growth drivers Regulated water testing Higher environmental standards Developing markets Bioscience growth

Competitive advantage Installed base Instrument design protection Porous plastics IP and related patents

Recent new products Quaatro 39 AA1 method development AQ2 upgrade Bioscience filters Chromatrap™

STRONG MARKET POSITIONS And concerted new product development

Environmental laboratory supplies

1 2 3 4

10

Niche positions Aluminium cast house filtration Gray and ductile iron filtration Super alloys

Growth drivers Aluminium consumption US auto and light truck production Increased use of high grade and exotic alloys

Competitive advantage Patent protection Metallurgical expertise US manufacture (for the Americas)

Recent new products Selee CSX™ Selee IC™ Selee SA™ Range extensions

STRONG MARKET POSITIONS And concerted new product development

Molten Metals

1 2 3 4

11

GEOGRAPHIC EXPANSION TO KEY MARKETS: Recent developments and 2014 revenue by destination

1 2 3 4

Microfiltration plants

Metals Filtration plants

Americas

40%

UK

17% Europe

11% Asia

30%

US

Caribou, ME, plant extended Options to grow Ashland, VA, being considered Mequon, WI, manufacturing capability extended

UK and Europe

New plant in New Milton fitted out Machining capacity increased in Fareham

Asia

First phase Xiaogan, China, plant completed in 2013 Xiaogan plant extended in 2015

12

CONSISTENT STRATEGY: Revenue growth and profitability improvement

13% revenue CAGR since 2009 EPS growth trend established

Net debt eliminated Revenue growth coming from US and Asia

0

20

40

60

80

100

120

2009 2014

£mill

ions

Others

Asia

Americas

Europe United Kingdom

02468

10121416

2009 2010 2011 2012 2013 2014

Half year

Final

Pen

ce p

er s

hare

0

20

40

60

80

100

120

2009 2010 2011 2012 2013 2014

Half year

Final

£ m

illio

ns

-9

-4

1

6

11

16

2009 2010 2011 2012 2013 2014

Half year

Final £

mill

ions

1 2 3 4

13

RECORD PERFORMANCE For the year ended 30 November 2014

Revenue up

23% to £104.0m

Revenue up

33% in Microfiltration

Revenue up

6% in Metals Filtration

PBT up

10% to £8.4m

EPS up

17% to 14.4p

Net cash up to

£5.3m

14

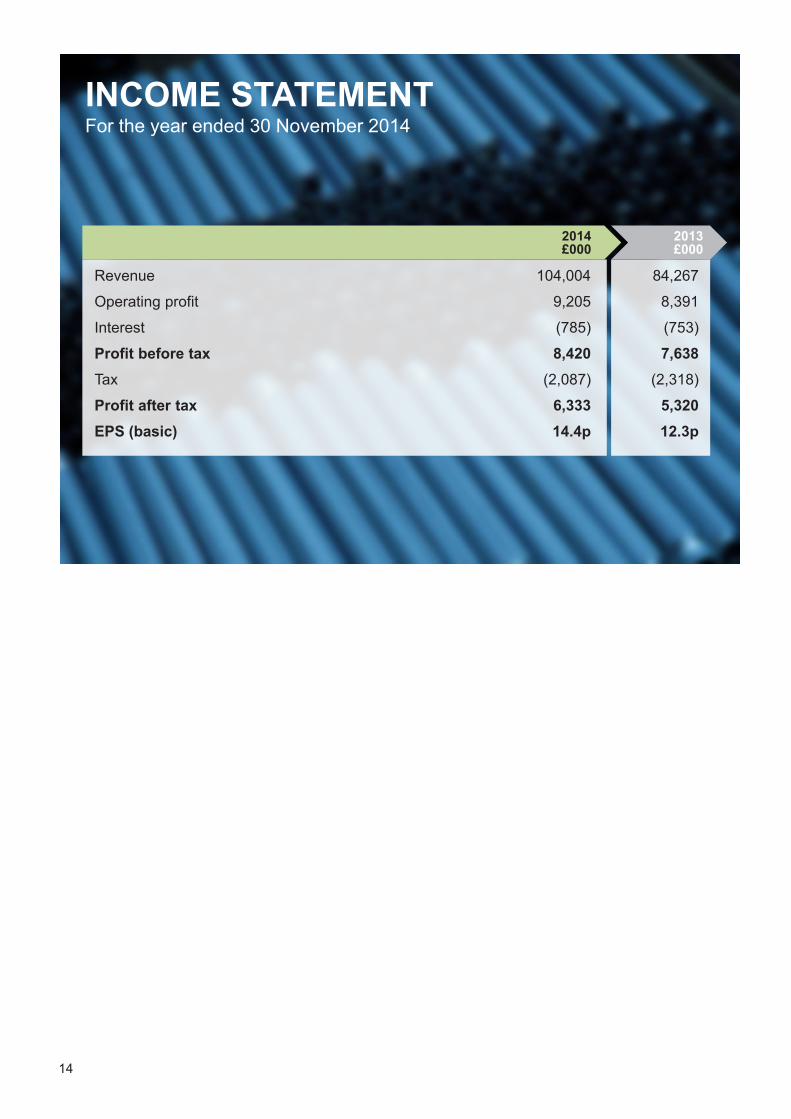

INCOME STATEMENT For the year ended 30 November 2014

2013 £000

2014 £000

Revenue 104,004 84,267

Operating profit 9,205 8,391

Interest (785) (753)

Profit before tax 8,420 7,638 Tax (2,087) (2,318)

Profit after tax 6,333 5,320 EPS (basic) 14.4p 12.3p

15

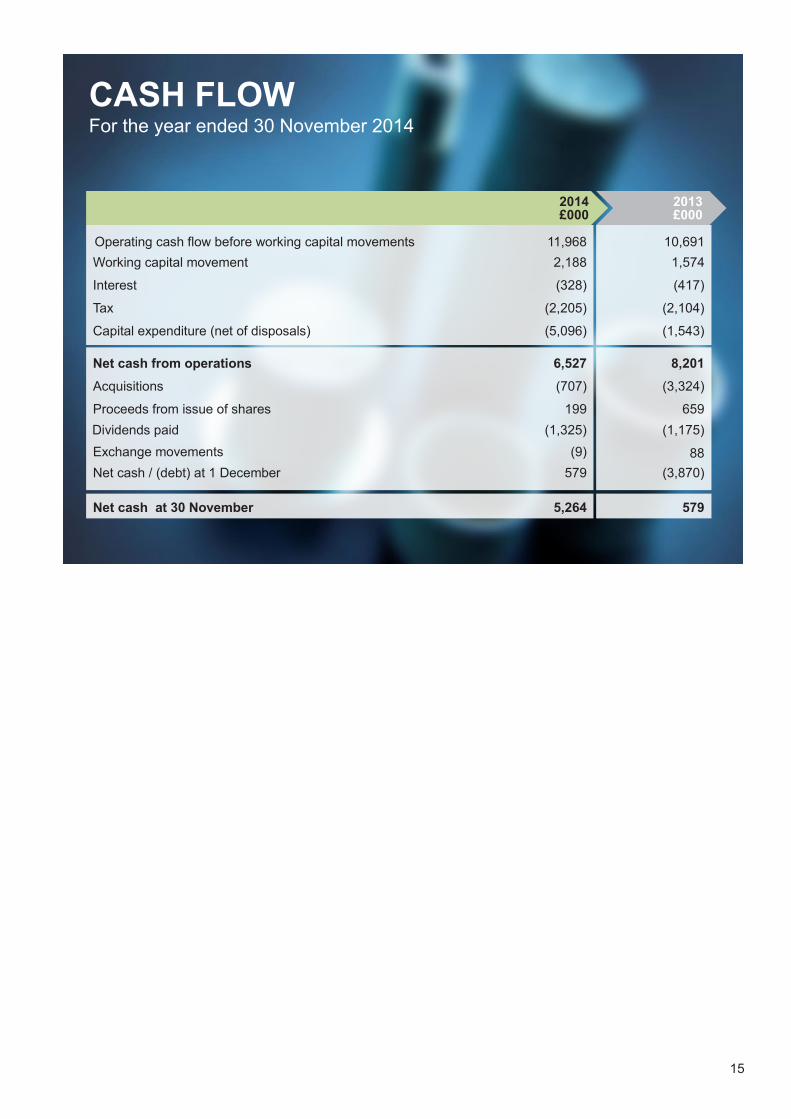

CASH FLOW For the year ended 30 November 2014

2013 £000

2014 £000

10,691 Operating cash flow before working capital movements 11,968 1,574 Working capital movement 2,188

(417) Interest (328)

(2,104) Tax (2,205)

(1,543) Capital expenditure (net of disposals) (5,096)

8,201 Net cash from operations 6,527 (3,324) Acquisitions (707)

659 Proceeds from issue of shares 199

88 Exchange movements (9)

(3,870) Net cash / (debt) at 1 December 579

579 Net cash at 30 November 5,264

(1,175) Dividends paid (1,325)

16

METALS FILTRATION Results and progress – year ended 30 November 2014

2013 £000

2014 £000

Revenue 30.1 28.5

Operating profit 2.6 2.4

Revenue to £30.1m record

11% growth at constant currency Steady market share gains from patented products Operating profit margin approaching 10%

New product development

Promising development pipeline Lithium aluminium alloy filter trials successful Selee CSX and Selee IC range extensions

2015 outlook

Positive start to 2015 China investment to expand production

17

MICROFILTRATION Results and progress – year ended 30 November 2014

2013 £000

2014 £000

Revenue 73.9 55.8

Operating profit 8.7 8.6

Revenue up 33% to £73.9m

Large projects progressing well: £19.5m revenue (2013: £6.0m). 2015 revenue likely to be closer to 2013 Operating profit held back by project accounting, dollar weakness, restructuring costs 9% underlying revenue growth 13% growth in Seal Analytical

Year of investment

UK expansion for aviation and industrial US expansion for industrial. 18% growth in 2014

2015 outlook

Healthy order books; $10m gasification order for CNOOC Further benefit from large projects

18

2015 – 2017 OPPORTUNITIES Market growth, market share gains and margin growth

Aviation Energy and industrial process

Laboratory supplies

Molten metals

Market growth

Market share gains

Margin growth

Inerting developments

US expansion

A350 in production

UK capacity increases

Airbus NEO qualified

Airbus A380 and Boeing 787

US sales and manufacturing

Large contracts + CNOOC Pipeline promising Gasification spares and service

Caribou capacity increase & cross-selling

Longer life hot gas filters

Improved analyser range designs

Bioscience licensing growth with Thermo

Bioscience filtration development

US manufacture of two product ranges

Regulated markets with long term growth prospects – long product lifecycles

New China plant expansion Incremental product and process improvements

Steady market share gains from IP protected ranges

Product range extensions

Initial orders for next generation of new products

Thomas Cain integration

19

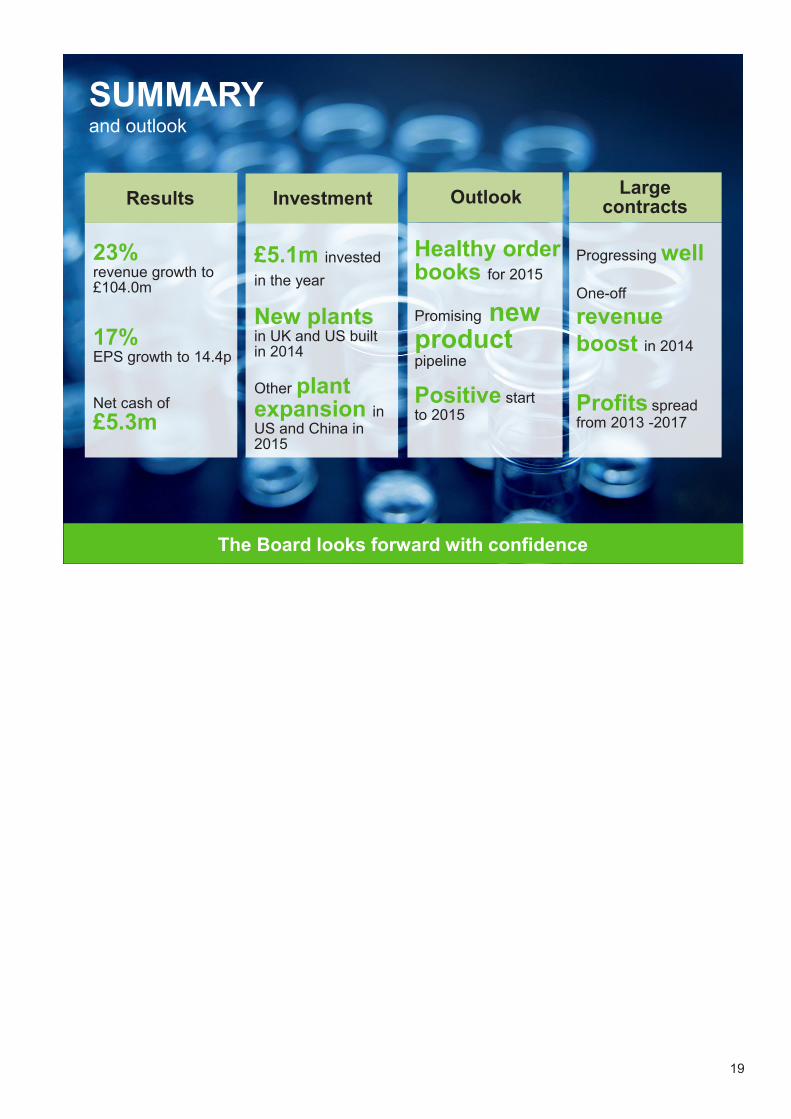

SUMMARY and outlook

The Board looks forward with confidence

Large contracts

£5.1m invested in the year New plants in UK and US built in 2014 Other plant expansion in US and China in 2015

Healthy order books for 2015 Promising new product pipeline Positive start to 2015

23% revenue growth to £104.0m 17% EPS growth to 14.4p Net cash of £5.3m

Results Outlook Investment

Progressing well One-off

revenue boost in 2014 Profits spread from 2013 -2017

20

Presentation Year ended 30 November 2014

Ben Stocks Chief Executive

Chris Tyler Finance Director

Specialist filtration & environmental technology