Polymers special update Facts and figures - TransGraph · While expected start-up of their...

13

Polymers special update – Facts and figures TransGraph Consulting Pvt. Ltd. Oct 2011

Transcript of Polymers special update Facts and figures - TransGraph · While expected start-up of their...

Polymers special update – Facts and

figures

TransGraph Consulting Pvt. Ltd.

Oct 2011

PP and PET production process and price determinants

Crude oil

Naphtha

PP

PROPYLENE XYLENE ETHYLENE

MEG PARA-XYLENE

PTA PET

Immediate Feedstock

End Product

Product Raw material Correlation

PET

PTA 0.9199

MEG 0.5174

Crude Oil 0.6765

Naphtha 0.7516

Para-Xylene 0.8274

PP

Propylene 0.9152

Crude Oil 0.8587

Naphtha 0.9055

Correlation: Jan 2007 – Oct 2011

Immediate feedstock's having high correlation as compared to parent materials Crude oil

and naphtha.

Parent material having very high correlation with downstream products emphasizes

impact of upstream energy prices on latter prices.

60

95

130

165

200

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 Apr-11 Jul-11 Oct-11

PP price trend since Jan' 2010

PP Naphtha Propylene

Peak demand season ahead for polyesters shall keep PTA and MEG prices on higher momentum

giving positive support to PET prices over medium term.

Ample supplies on back up of plant restarts in key Asian and Middle east markets coupled with dried

demand could pressurize prices propylene and PP downwards over medium term.

Volatile energy prices specifically crude oil and lingering economic concerns across US and

European front could adversely impact demand from these regions.

Prices indexed to 100, Jan 2007 taken as 100

50

100

150

200

50

85

120

155

190

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 Apr-11 Jul-11 Oct-11

PET price trend since Jan' 2010

PET Paraxylene

PTA MEG

MEG on RHS, others on LHS

Price Trends vis-à-vis feedstock's

Supply-demand balance and trends

PP INDIA (Mtpa) 2008-09 2009-10 2010-11p

Demand 1.80 2.03 2.27

Capacity 2.12 3.02 3.70

Import 0.21 0.10 0.08

Export 0.24 0.75 1.00

Capacity Utilization (%) 86.62 88.68 86.31

PET INDIA (Mtpa) 2008-09 2009-10 2010-11p

Demand 0.499 0.562 0.647

Capacity 0.959 1.023 1.069

Import 0.95 0.121 0.128

Export 0.485 0.528 0.584

Capacity Utilization (%) 92.66 94.73 103.19

PP GLOBAL (Mtpa) 2009 2010e 2011p

Capacity 54.11 58.51 62.11

Demand 47.84 50.07 54.15

Capacity Utilization (%) 93.64 90.33 90.79

PET GLOBAL (Mtpa) 2009 2010e 2011p

Capacity 18.50 19.50 19.78

Demand 14.61 15.54 16.62

Capacity Utilization (%) 78.97 79.67 84.02

Strong demand growth for PP at global and Indian front – higher capacity utilization levels – bright pricing

prospects

PET capacity utilization to witness rise in the coming year both at global and Indian front – No net

change in export potential

PP Supply Demand Analysis for H2’ 2011

Region Demand Supply

Global

Lingering concerns over economic

growth in US and European countries to

impact demand from these regions in

H2’11

Despite prevailing economic concerns,

relatively better demand from FMCG and

Automobile industry in developing regions

shall keep over all demand prospects on

a bright note in respective regions

China and India shall continue to be the

major drivers in demand at Asian front.

Ample availability specifically on

Middle East front coupled with brand new

start ups shall negate any supply

concerns.

Volatile upstream product cost

coupled with falling PP prices could

incline regional producers to reduce their

operating rates.

End of maintenance season across

key Asian markets of China and Taiwan

expected to keep supplies on surging

mode.

Indian

With festive season at its last leg,

demand for packaging films could be

seen showing signs of weakness.

Approaching kharif crop harvesting

season to keep PP demand intact at

agricultural front.

Depreciation of Indian currency to

subdue the import volumes.

No new expansion planned in H2’2011

Robust demand and depreciating

currency could lead to regional

producers ramping up the operating

rates to propel profitability.

Exports volumes could see upward

momentum.

PET Supply Demand Analysis for H2’2011

Region Demand Supply

Global

Lingering concerns over economic growth in

US and European countries to impact demand

from these regions in H2’11

Approaching winter season in West shall

adversely impact demand from CSD segments

Polyester demand to be kept intact owing to

robust growth in textile industry specifically on

Chinese front.

Additional capacities of around 1

million tons (18.5 to 19.5 million

tons) to be added during the year

Shutdown of plants in western

countries (US and Europe) to keep

excess capacity in check.

Indian

With winter peak polyester demand season

set to begin, PET prices could be kept on

buoyant note.

With festive season on verge of end, PET

films demand could be adversely impacted.

Demand for PET products from key end user

industries as aerated drinks, packaged mineral

water, beverages etc, to keep growth

momentum intact

Amid depreciation of Indian

currency, ample regional availability

shall keep brighter export prospects

intact .

No capacity expansion/addition in

any grades of the PET is planned

during the period.

Margins Movements – feedstock’s

47.86

15.93

39.01

5

15

25

35

45

55

65

75

85

28-Oct-10 17-Dec-10 5-Feb-11 27-Mar-11 16-May-11 5-Jul-11 24-Aug-11 13-Oct-11

Polymer Feedstock Margins

Naptha-Crude diff (%) Ethylene margin (%) Propylene margin (%)

Hist (Since Apr '09) avg. margins

Naphtha = 28 %Ethylene = 44 %

Sharp fall in feedstock margins and simultaneous rally in Naphthamargins signals undervalued prices for feedstock . Such a scenariofurther signals of ample feedstock supply prevailing in the marketwhich shall keep prices subdued in the near term.

However, such sharp fall in margins shall keep medium termprospects on positive tone

Margins Movements - Products

28.06

30.81

15.61

-10

0

10

20

30

40

50

60

28-Oct-10 17-Dec-10 5-Feb-11 27-Mar-11 16-May-11 5-Jul-11 24-Aug-11 13-Oct-11

Polymer Product Margins

HDPE margin (%) PP margin (%) PET margin (%)

Hist (Since Apr '09) avg. margins

HDPE = 23%PP = 26 %PET = 17 %

Rising margins at PE front signalling an optimistic outlook over medium term entails that producers could be left with cushion off reducing their prices levels.

However on PP and PET front, fall in margins owing to ample avaliability of former and weakening demand of the feedstock of latter could lead to producers cutting back the operating rates curbing supplies over medium term.

Factors affecting prices in Q3’11 - Review

Volatile crude oil and naphtha prices coupled with robust demand at Indian and Asian front

imparted positive momentum in PP and PET prices during the period.

Demand pick ahead of festive season start up at Indian front, national holiday at Chinese

front and post Ramadan demand from Middle East and some of the south east Asian

countries kept prices on firm tone during the period.

Large number of crackers planned and unplanned shutdown at Asian front squeezing

demand supply gap for feedstock’s, pushing up prices of the same too added positive

momentum in prices during the period.

Rapid rise in Chinese textile exports coupled with sharp fluctuations of Cotton prices led to

rapid incline in Xylene prices which further imparted positive momentum in PTA and MEG

prices.

At another front, sharp depreciation in Indian currency during the quarter pushing up prices

of raw materials further landed additional support to downstream products prices in the

region.

Start-up of some of the textiles mills in China, Italy and in some other European countries

pushing up demand for PET synthetic fibers kept PET prices on firm tone.

Demand pull from textiles sector coupled with delay in start-up of production units of

capacity 1.4 Mtpa pushing up prices of feedstock PTA prompted PET producers to revise up

their offer rates during the period.

Critical factors in the coming 2-3 months

Expected positive momentum in crude oil over supply concerns from north sea and naphtha

prices over escalating demand from South Korea could negate any steep downslides in

downstream product prices in the near term.

Upcoming winter season expected to push up LPG demand for heating purpose making it

less economical for crackers in the West to rely on alternative LPG feedstock shall lend

additional pressure to naphtha demand in the medium term.

While expected start-up of their respective crackers by Formosa, Mitsubishi Chemical and

Sumitomo Chemical with a combined capacity of over 2 Mtpa shall on one hand push up

naphtha demand and prices while at another hand could improve feedstock supply.

Ample supplies of feedstock across key Asian markets on back up of plant restarts coupled

with increased imports from Middle east following post holiday restarts shall negate any

supply concerns in the near term.

Restart of CNOOC 840 KTPA Xylene unit coupled with capacity addition of around 200 Ktpa

by Samsung Petrochemicals shall negate any supply concerns of PET feedstock’s at Asian

front.

Approaching winter pointing towards increase in use of PTA and MEG from polyester

segment thereby pushing up the prices of the same could narrow down PET producers

margins prompting them to revise up their offer rates in the medium term

Upcoming festive season of Christmas expected to push up buying momentum in next one-

month shall lend support to producers demand for increase in prices during the period.

Critical factors in the coming 2-3 months – contd.

While end of festive demand at Indian front post Diwali shall impart some weakness in the

near term, start-up of Kharif crop harvesting season across the country and upcoming

marriage season ahead shall keep medium term prospects on bright note.

Post harvesting season demand for woven sacks for packaging and big dooms for storage

shall lend support to demand for PP in particular.

Expectation of further depreciation in Indian Rupee in next 3-4 weeks shall keep imported

raw material prices higher which could negate nay near term sharp fall in downstream

products prices at Indian front.

At economic front, concerns over the economic revival across the globe shall keep over all

demand sentiments weak which could prompt producers to negate possibility of any sharp

rise in products prices in the medium term.

Concisely: PP prices are expected see further downside revision of around INR 1.5/2 per kg while PET prices shall revise down by INR 2.5 per kg in next 3-4 weeks before resuming its positive trend.

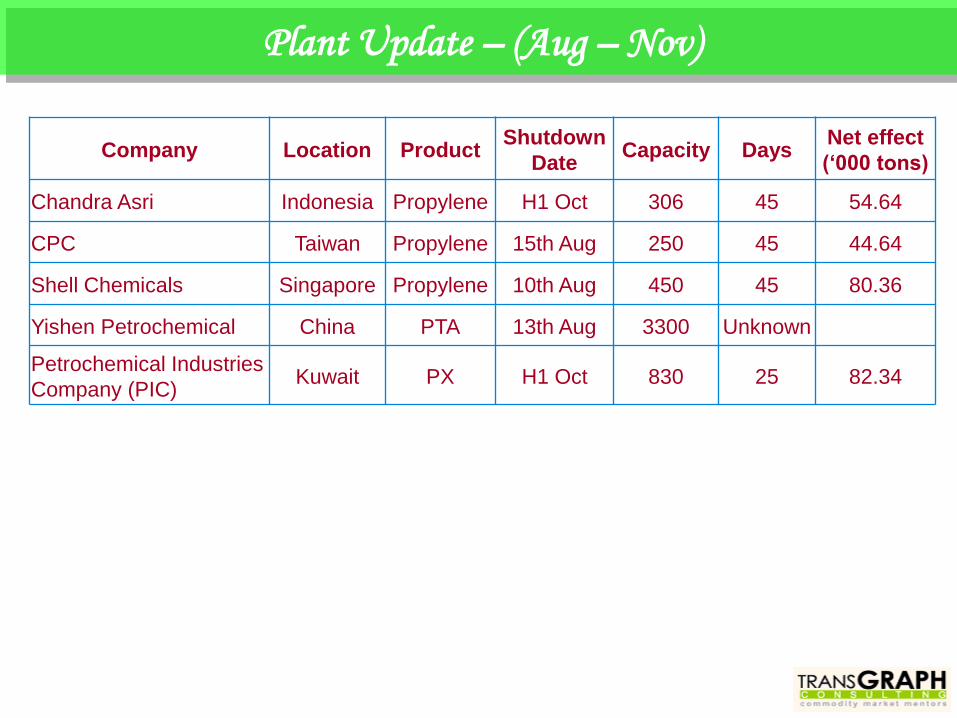

Plant Update – (Aug – Nov)

Company Location Product Shutdown

Date Capacity Days

Net effect

(‘000 tons)

Chandra Asri Indonesia Propylene H1 Oct 306 45 54.64

CPC Taiwan Propylene 15th Aug 250 45 44.64

Shell Chemicals Singapore Propylene 10th Aug 450 45 80.36

Yishen Petrochemical China PTA 13th Aug 3300 Unknown

Petrochemical Industries

Company (PIC) Kuwait PX H1 Oct 830 25 82.34

Thank you

TransGraph Consulting Pvt. Ltd.

# 6-3-655 / 2/1, III Floor,

A.P. Civil Supplies Bhavan Lane, Somajiguda, Hyderabad – 82,

Tel: +91-40-30685001-04: Facsimile: +91-40-30685002

E-mail: [email protected]

www.transgraph.com