Politics for the 1% The 1% are well resourced- have capital and can raise more through partnerships...

37

-

Upload

trevor-wheelock -

Category

Documents

-

view

217 -

download

1

Transcript of Politics for the 1% The 1% are well resourced- have capital and can raise more through partnerships...

Politics for the 1%

The 1% are well resourced- have capital and can raise more through partnerships or loans through their contacts, or get state financial support

Well connected – in elite clubs, schools, personal contacts, knowledge of politicians –its not what you know but who you know

Well informed – get insider information, can buy research, hire people in the know

Well represented – get the best lawyers, lobbyistsWell presented – own the electronic media, papers, hire PR agencies to

organise their propoganda campaigns behind the scenes setting the public agenda, fund universities and think tanks

Well hidden – in tax havens and secrecy jurisdictionsWell protected – the police and armed forces are there to protect and

advance their interests first and foremost

The Money System as a Problem

• Money as a means of exchange

• The money system at the service of society

• Newly created money devoted to public and collective purposes

• Money as the goal of exchange

• A money system run by ‘money junkies’ to

whom everything else takes second place to getting their next fix

• “The love of money is the root of all evil”

What is the current financial system for now and what should it be there for?

• Now• Speculation, • gambling on real estate

prices, • lending money to

governments that they could create themselves via central banks...

• What we need• Raising resources to

transform the energy, transport and cultivation system

• Investment in industries that meet the ordinary needs of people

And the bankers do control the money of a country

• 97% of the money in circulation is created by the banks when they lend

• The money is backed by debt – a contract to repay, with interest and to forfeit collateral if the debtor cannot repay – which puts all the risk of ventures on debtors

• It is not surprising that there is too much debt – for the money supply to increase people and companies have to go into debt....

• This system is inevitably creates too much debt..

Personal Financial Debts

• Britain's households owe £1.451 trillion in mortgages, overdrafts, loans and credit cards - a little more than the country’s annual output.

• The collateral underpinning this debt are mostly people’s houses whose prices have fallen over 20% since the bubble burst

• The average Britain now owes £29,500, about 123 per cent of average earnings – just over £4,000 is for consumer loans, the rest mortgages

• According to the Office of Budget Responsibility, UK personal debt will grow by nearly 50 per cent between now and the end of this parliament. Come 2015, it is forecast to reach £2.12 trillion pounds

• Research by Morrisons, the supermarket group, estimates that three in ten of its customers run out of cash at the end of every month. For some of these, borrowing on credit cards (average interest rate: 18.5 per cent) offers a quick but unsustainable fix.

So do the banks use the power to create money (as debt) wisely and carefully?

• It is claimed and enshrined in the Treaty of Maastricht that governments must not create money for public purposes – they must tax or borrow from the finance sector.

• Supposedly only banks can be trusted to create money otherwise states would create too much money and that would lead to inflation.

Yet when banks create money...

• In booms they create too much, lending recklessly and often in an orgy of speculation creating inflations in asset prices(eg house and land prices)

• In slumps when money needs to be put into circulation to stimulate economic activity and use spare capacity banks will not lend and people don’t want to borrow.

• They create too much money in a boom and not enough in a slump

• Only 8% lent to businesses for productive investment

The “euphoric economy”• The manic craze for personal

gain, spurred on by the bonus economy creates an orgy of reckless criminality in the finance sector

• William K Black estimate 0.5 million financial crimes in the US real estate and finance boom prior to the 2007 crash.

• A similar reckless drive overexpanding lending to earn bonuses characterised UK banks like HBOS and RBS

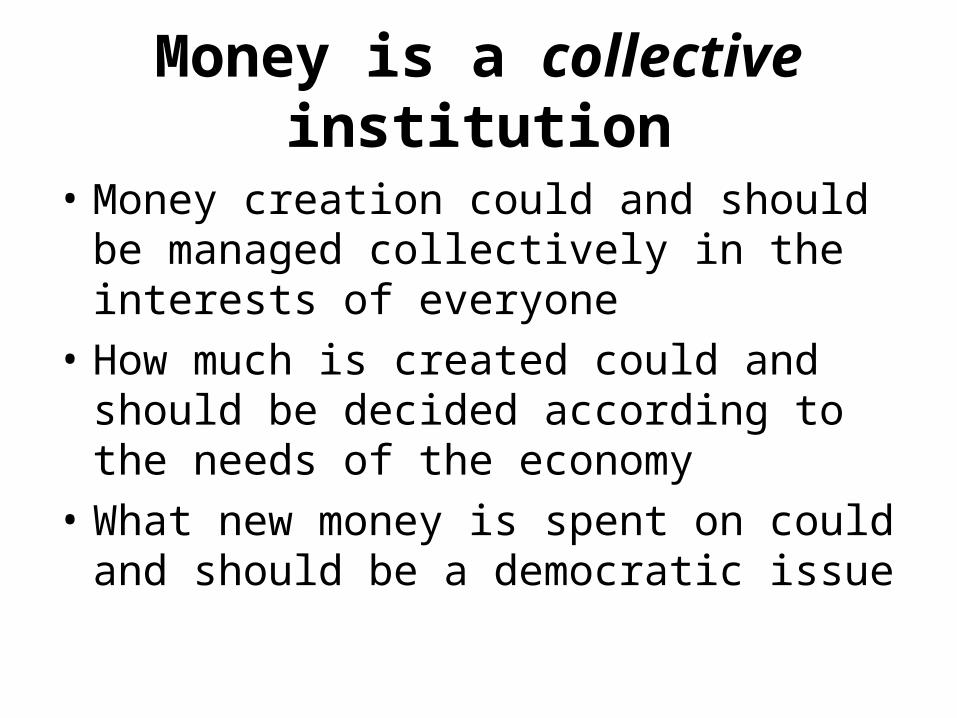

Money is a collective institution

• Money creation could and should be managed collectively in the interests of everyone

• How much is created could and should be decided according to the needs of the economy

• What new money is spent on could and should be a democratic issue

Would this not create inflation?

• If too much money is created and chases too few goods it does create inflation

• However not when there are unemployed resources in the economy – more money demand is needed to get the unemployed resources used

• If inflation happens it should be cured by taxation – taxation of the rich

This is the cure for inflation – taking money out of the economy

The problem is that the City of London makes its money through being part of a network of tax and regulation evasion

• At the end of the British empire the City had to re-invent itself.

• The euro-dollar market enabled London to offer the evasion of Federal Reserve Regulation on dollars held here instead of the USA

• This idea of London as a place to evade financial regulation was then extended by a network of tax havens and secrecy jurisdictions in the remaining network of colonies – like the Channel Island, Isle of Man – and above all the Cayman Islands

• The British elite sold its services to kleptocrats the world over – that is how London remains a major centre

My interim conclusion

• We are governed by an elite who kept a world role after the collapse of empire by providing a network of “bolt holes” for the tax evaders and dubious practices of the super rich the world over.... and this makes it rather difficult to imagine the British state and finance system being used to help resolve the even bigger problems facing humanity.

What are these bigger problems?

The Limits to Growth Crisis

The ecological crisis

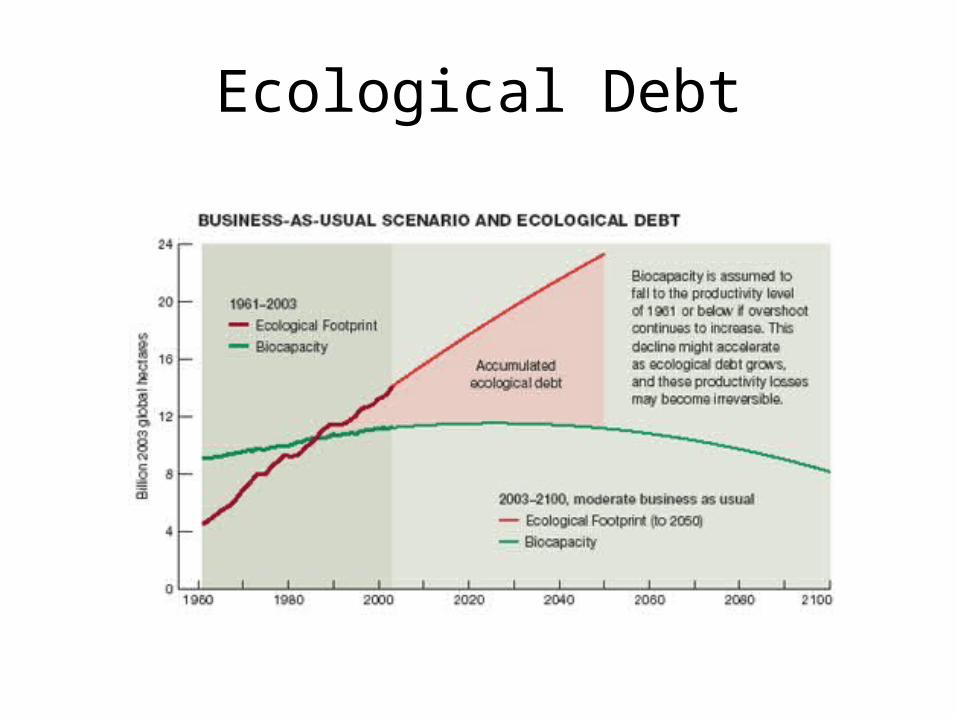

Ecological Debt

Crossing Planetary Boundraries

Example Water Crises• Between 2000-2011 Syria

experienced four severe droughts, which the UN estimate left 2-3 million people in extreme poverty, and wiped out 80-85% of herders livestock.

• Poor rains could lead to two of Syria’s arterial rivers, the Jordan and Euphrates to lose more than half their flow adding to the problems

But never mind - there are good profit opportunities here for the PR industry

“Buy when there is blood on the streets” Mayer Amschel Rothschild

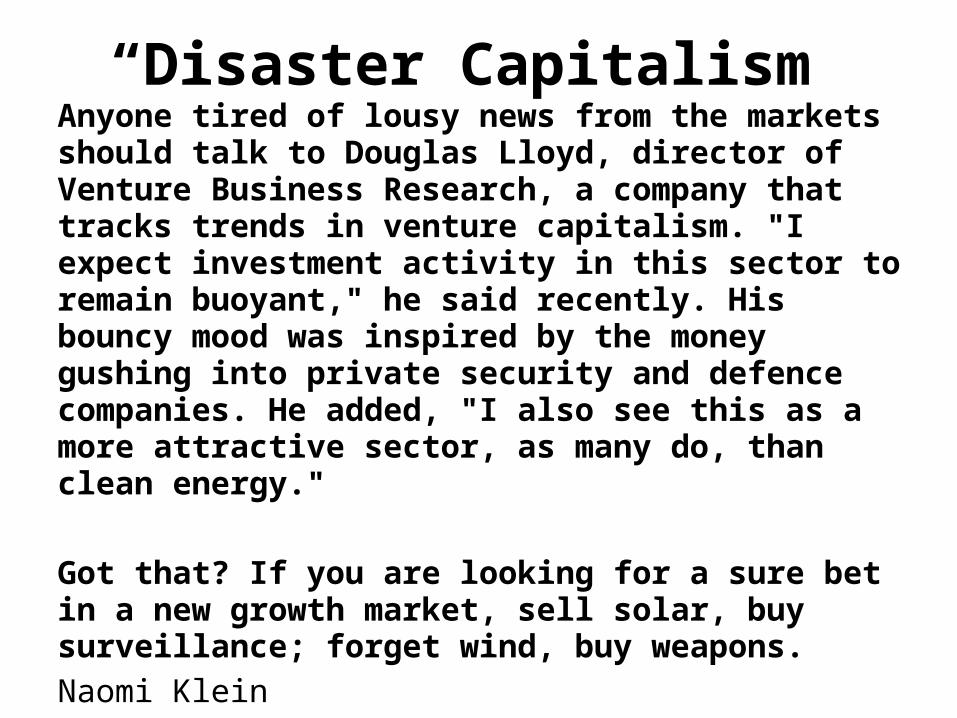

“Disaster Capitalism”

Anyone tired of lousy news from the markets should talk to Douglas Lloyd, director of Venture Business Research, a company that tracks trends in venture capitalism. "I expect investment activity in this sector to remain buoyant," he said recently. His bouncy mood was inspired by the money gushing into private security and defence companies. He added, "I also see this as a more attractive sector, as many do, than clean energy."

Got that? If you are looking for a sure bet in a new growth market, sell solar, buy surveillance; forget wind, buy weapons.

Naomi Klein

Communities must develop alternatives to ‘disaster capitalism’ based on collective management of

common resources• The crisis forces people to change in

more than small increments – this is often frightening, involving uncertainty and insecurity, even disorientation. Change is forced in many dimensions at the same time – earning a living, finding new places to live, new relationships and developing new skills.

• We need to develop lifeboat projects to help – offering “packages of support” – helping each other with food and energy and living spaces - with new relationships and motivations.

A “Solidarity Economy”• A network where otherwise vulnerable

people can share basic domestic and provisioning resources, develop new skills in energy, food and domestic activities, save resources and find ethical and supportive relationships.

• For example - community gardens, community supported agriculture, community energy projects, community currency and exchange networks, community care arrangements, community transport arrangements like car pools, resource centres etc

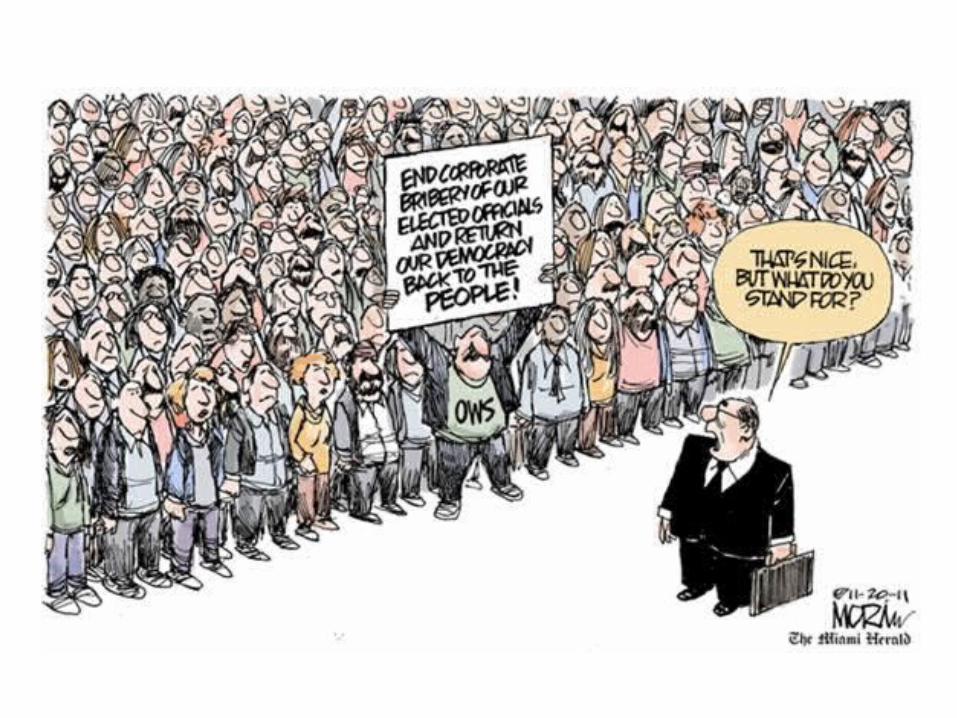

Instead of Political Economy for the 1%

The 1% are well resourced- have capital and can raise more through partnerships or loans through their contacts, or get state financial support

Well connected – in elite clubs, schools, personal contacts, knowledge of politicians –its not what you know but who you know

Well informed – get insider information, can buy research, hire people in the know

Well represented – get the best lawyers, lobbyistsWell presented – own the electronic media, papers, hire PR agencies to

organise their propaganda campaigns behind the scenes setting the public agenda, fund universities and think tanks

Well hidden – in tax havens and secrecy jurisdictionsWell protected – the police and armed forces are there to protect and

advance their interests first and foremost

We need Political Economy for the 99%

The “99%” need to pool and share their resources Develop our own “well connectedness” in social economy and community

networks around shared alternative values, resolving conflicts and realising synergies between projects and groups as appropriate

Develop our own sources of information, research and long term strategic perspectives

Develop lobbies/advocacy based on shared values and community interests to take back collective influence over the state, firstly at local level – as a precondition for radical reform of institutional and policy frameworks

Develop our own media and means of group and mass communication and seek to develop agendas jointly with radical academics

Work for transparency as a principle and highlight secret agendas of the eliteDevelop strategies to defuse dangerous confrontations with the power elite

Debt Jubilee and reform of the finance sector

• We need growing organisation in the ‘solidarity economy’ also to give us enough political influence to bring in changes to the rest of the economy – particularly vis a vis the finance sector which has huge political influence.

• We particularly need to deal with the debt crisis bailing out the banks by bailing out the people first – then radically reforming the bank and finance sector.

• In the history of humanity many societies overwhelmed by debts have cancelled them. In the Ancient World, in Mesopotamia in the era around 2000 BC, debts were written off every 50 years in what was called a Jubilee.

• We need a modern Jubilee to cancel financial debts..... • ......and to construct a finance sector that can help us start to “cancel

ecological debts” by financing a transformation of energy, transport and cultivation.

Debt cancellation pure and simple cannot be the solution

• The banks and financial institutions to whom the money was owed would go bust and then there would be no money available to make day to day financial transactions. Everything would grind to a halt.

• Nor would that be particularly just – why should people who have accumulated debts in a consumption orgy be bailed out and those who did not get nothing?

• Also, what about ‘ecological debts’ – would it be fair to future generations to simply “press a restart button” on the economy and start the next consumption boom – how would this help deal with the limits to economic growth?

The solution (1) Bail out the people in a way that leaves the banks solvent

• Create central bank money and give....say £25,000.... to everyone equally to pay down any debts to Financial Services Agency registered lenders

• Where people have no debts require their share of this central bank money to go to buy a share for them in an energy bank or a similar eco-focused investment – this would help to deal with the eco-debt crisis too!

The solution (2) Clip the wings of the banks -remove their right to create money• Paid back debts would leave the banks flush with cash but

solvent – if the present system continued they could then use this as backing for a massive surge of new bank debt money – which would put us back where we started.

• So “repaid cash” needs to be “sterilised” in a banking reform that prevents this happening.

• The banks could lend this repaid money on but they could not “leverage it” as cash backing for more debt money creation

• Henceforth new money would be created and put into circulation only in community controlled processes

• Private banks would lose the right to create deposit money.

Alternatively we can hitch ourselves to this kind of process: