POLICIES AND PROCEDURES - Ortem Securities

33

POLICIES AND PROCEDURES ORTEM SECURITIES LIMITED

Transcript of POLICIES AND PROCEDURES - Ortem Securities

POLICIES AND PROCEDURES

ORTEM SECURITIES LIMITED

INDEX

SL NO

NAME OF THE POLICY

PAGE NOS.

MANDATORY POLICIES AS PRESCRIBED BY EXCHANGES

1. Risk Management Policy

2. Surveillance Policy 3. PMLA Policy 4. Inactive/Dormant A/C Policy 5. Policy for Client Code Modification 6. Policy for Pre-Funded Instruments / Electronic Transfers 7. Blog Chat Policy 8. Policy on Conflict of Interest 9. Internal Control Policy

10. Policy for Identification of Beneficial Ownership 11. Policy Guidelines on Outsourcing of Activities

RISK MANAGEMENT POLICY

Preface:

This document shall be Risk Management Policy of the Company while carrying out its

business activities as a Member of National Stock Exchange of India Ltd and Bombay

Stock Exchange Ltd.

This document shall be used as guidelines for the activities namely client identifications

and introductions, surveillance, record keeping for executing and carrying out the day to

day transactions by the Company and its business associates.

A. Pre-Trading

1. Registration of Client / KYC:

a. Collection of KYC form:

Collection of KYC form from the prospective client with in person verifications procedure

Receipt of duly filled Client Registration Application Forms, with supporting documents

Checking of Application Forms and allotment of the unique client code

Re-checking of Forms and capturing of information into the system

Final checking of Forms

Documentation of Forms.

b. Checking of Application Forms and information capturing in the system.

The forms shall be checked for their completeness and correctness with the supporting

documents, by the designated staff and the key fields are entered into system. A Unique

Client Code (Trading Code) shall be allotted to the clients. Allocation of Client code is

systemized so that the same code is not allotted to another client.

c. Final checking of Forms

Forms shall be once again re-checked with the information captured in the system under

Maker-Checker concept.

2. Provision of Money Laundering Act 2002:

It is the policy of the Company to ensure that effective KYC programme is put in place

by establishing appropriate procedures and ensuring their effective implementation. It

covers proper management oversight, system and controls, segregation of duties,

training and helps in fighting against money laundering and thereby detects, deters and

disrupts money laundering.

Dispatch of KYC Kit

The Company should send the KYC, UCC detail & all other documents as executed by

clients along with the welcome letter to the clients directly so that the client should have a

copy of the documents signed with the company.

It is the policy of the Company to introduce clients who are known directly or indirectly

to the Directors of the Company. The Company do not entertain walk-in clients. The Sub-

brokers / Authorised Persons introducing their clients shall carry out the due-diligence of

the prospective clients as to their financial standing, risk profile, past and present stock

market and other business activities , their reference from commonly known person and

shall evaluate suitability of the proposed nature of their dealings in the context of

information gathered as above. The due-diligence of the direct clients shall be on same

line by the key personnel of the Company. B. Trading

a. Margin:

The client is required to pay initial margin as specified by NSE / BSE / SEBI before

placing any order. The Company reserves the right not to execute the order if the client

has not placed the required initial margin.

Total deposits of the clients are uploaded in the system and clients are provided exposure

on the basis of margin applicable for respective security as per VAR based margining

system of the Stock Exchange and / or margin defined by RMS based on their risk

perception.

b. Illiquid Securities / Penny Stocks:

The Company does trading of “Penny Stock / Illiquid Securities and Z Group Securities”

subject to rules, regulation, Articles, Byelaws, Circulars, Directives and Guidelines of

SEBI and Exchange as well as considering the prevalent market and other circumstances

at related point of time. The Company reserves the right to restrict the clients to buy / sell

in penny stocks / illiquid securities only on the basis of 100% upfront margin and on

Delivery basis. Also the Company may have in place further restrictions in terms of

quantity / value in each / all penny stock / illiquid securities.

C. Post Trading

a. Ongoing due diligence of KYC:

In addition to the due diligence, the Company shall carry out further due diligence while

verifying the KYC document on regular basis.

b. Client Modification:

The Company shall adhere with the Circulars, Rules and Regulations laid down by NSE /

BSE / SEBI from time to time.

c. Receiving, validating and entering the orders of Client in the trading platform:

i. The new clients shall be assigned and introduced to a specific terminal operator and

the operator shall be briefed about client’s requirement for trading, investments and

his risk taking abilities. Accordingly the terminal operator shall under instruction

from the officials, allow the clients to place the orders during the live market subject

to his risk profiles.

ii. The dealers who are registered as terminal users with the Exchange shall be allowed

to operate the terminals and place the orders in the respective accounts and in the

accounts of the clients on the basis of the risk profile of the clients.

d. Collection and release of payment to clients:

i. The client shall be required to make the payment as per the daily debit

obligation on T+1 basis.

ii. The pay-out of funds shall be made on T+2 basis after confirming the

successful pay-in of the securities by the client.

iii. The Exchange / segment wise segregated ledger account shall be maintained.

e. Collection and delivery of securities to the Clients:

i. Collection of deliveries of securities from clients shall normally be called

from the clients on T+1 basis.

ii. In case of delivery of pay-in obligations of large quantity / value scrips shall

be called for prior to pay-in to make early pay-in or as early as possible after

the execution of sell order and shall be tendered to the clearing house under

early-pay in mechanism to the extent required.

iii. Deliveries of securities to the clients shall be effective within 24 hrs from the

pay-out.

D. Operations and Compliance Requirements:

a. The day to day operations are being looked after by the Designated Officials of

the Company.

b. The on-line surveillance desk is to be monitored by Designated Officials where

real time client wise / scrip wise position, M to M Margin requirements, available

margin and exposure limits with all exchange segments are monitored.

c. Various types of limits on trading terminals are being set up and uploaded

dynamically during the live market.

d. The various compliance requirements of all the Exchange / Segment shall be

ensured by the Compliance officer under the supervision of the Director

.

SURVEILLANCE POLICY

1. PREFACE:

Surveillance is the process of collecting and analyzing information concerning markets in order

to detect unfair transactions that may violate securities related laws, rules and regulations.

In Securities Market, it is imperative to have in place an effective market surveillance

mechanism in order to alert the customers with respect to their obligations, open positions,

market conditions, margin requirements, regulatory requirements and steps initiated by brokers

in case of changing market situations.

With a view to enhance customer knowledge, ensure investor protection and safeguard integrity

of the markets ORTEM SECURITIES LIMITED have devised a comprehensive Surveillance

Policy to make sure that customers are aware of the criteria based on which ORTEM monitors

risks and initiates actions to safeguard the interest.

2. POLICY:

The below mentioned policy made as per NSE circular no. NSE/INVG/22908 dated

March 7, 2013 for surveillance is to be implemented by the company and all the employees are

required to follow the same and take due care for its proper implementation.

The policy is made to facilitate effective surveillance mechanism in our organization. We will be

downloading the alerts based on the trading activity of the client from the Exchange through

Member Portal. The Compliance officer will have to analyze these alerts and seek client

information and other documentary evidences and submit the same to the exchange within the

prescribed time limit.

A) Following are the transactional alerts to be covered in surveillance:

Sr.

No.

Transactional Alerts Segments

1. Significant increase in client activity Cash

2. Sudden trading activity in dormant account Cash

3. Clients/Group of Client(s) dealing in common scrips Cash

4. Client(s)/Group of Client(s) concentrated in a few illiquid

scrips

Cash

5. Client(s)/Group of Client(s) dealing in scrip in minimum lot

size

Cash

6. Client(s)/Group of Client(s) concentration in a scrip Cash

7. Circular Trading Cash

8. Pump and Dump Cash

9. Wash Sales Cash and Derivatives

10. Reversal of Trades Cash & Derivatives

11. Front Running Cash

12. Concentrated position in the Open interest/ High Turnover

concentration

Derivatives

13. Order Book Spoofing i.e. large orders away from market Cash

The above transactional alerts can be modified to add any other type of alerts as and when

required.

3. PROCESS OF IDENTIFICATION OF SUSPICIOUS/MANIPULATIVE ACTIVITY:

In case of any alert being received either from the exchange or generated at our end, following

procedure is to be followed:

i) To review the type of alert downloaded by the exchange or generated at our end.

ii) Financial details of the client.

iii) Past trading pattern of the clients/client group.

iv) Bank/Demat transaction details.

iv) Other connected clients having common email/mobile number/address or any other linkages.

v) Other publicly available information.

After analyzing the alerts generated and in case of any adverse findings, the same shall be

communicated to the exchange within 45 days from the alert generated. The Company may seek

extension of time period from the exchange, wherever required.

In order to have in-depth analysis of the above transactional alerts, the following due diligence

shall be taken based on the following parameters:

A) Client(s) Information:

Due diligence of clients to be done on a continuous basis. Further, Ortem Securities Limited

shall ensure that key KYC parameters are updated on a yearly basis and latest information of the

client is in updated Unique Client Code (UCC) database of the Exchange and the same shall be

updated in back office also. Based on this information the company shall establish

groups/association amongst clients to identify multiple accounts/common account/group of

clients. Clients trading in derivative segment have to furnish the following relevant documents

pertaining to financial details on a yearly basis:

Copy of ITR Acknowledgement

Copy of Annual Accounts

Copy of Form 16 in case of salary income

Net Worth Certificate

Salary Slip

Bank account statement for last 6 months

Copy of demat account Holding statement

Any other relevant documents substantiating ownership of assets

Self declaration along with relevant supporting.

4) ANALYSIS:

In order to analyze the trading activity of the Client(s) / Group of Client(s) or scrips identified

based on above alerts received from the exchange the following information shall be sought from

the clients:

a) Seek explanation from such identified Client(s) / Group of Client(s) for entering into such

transactions. Letter/email to be sent to client asking the client to confirm that client has adhered

to trading regulations and details may be sought pertaining to funds and securities and other trading pattern.

b) Seek documentary evidence such as bank statement / Demat transaction statement or any

other documents to support the statement provided by the clients:

i. In case of funds, Bank statements of the Client(s)/Group of Client(s) from which funds pay-in

have been met, to be sought. In case of securities, demat account statements of the Client(s) /

Group of Client(s) from which securities pay-in has been met, to be sought.

ii. The period for such statements may be at least 15 days from the date of transactions to verify

whether the funds / securities for the settlement of such trades actually belongs to the client for

whom the trades were transacted.

c) After analyzing the documentary evidences, including the bank / demat statement, the

Company will record its observations for such identified transactions or Client(s) / Group of

Client(s). In case adverse observations are recorded, the Compliance Officer shall report all such

instances to the Exchange within 45 days of the alert generation. The Company may seek

extension of the time period from the Exchange, wherever required.

5) MONITORING AND REPORTING:

For effective monitoring the company shall maintain a register which shall record time frame for

disposition of alerts, the findings, and if there is any delay in disposition, the reasons for the

same, etc.

The surveillance process shall be conducted under overall supervision of the Compliance Officer

and based on facts and circumstances he is required to take adequate precaution. Compliance

Officer would be responsible for all surveillance activities and for the record maintenance and

reporting of such activities.

The Company shall prepare quarterly MIS and shall put to the Board of Directors the number

of alerts pending at the beginning of the quarter, generated during the quarter, disposed off

during the quarter and pending at the end of the quarter. Reasons for pendency shall be discussed

and appropriate action shall be taken. In case of any exception noticed during the disposition of alerts,

the same shall be put up to the Board.

Internal Auditor of the Company shall review its surveillance policy, its implementation,

effectiveness and review the alerts generated during the period of audit. Internal Auditor shall

record the observations with respect to the same in their report.

6) REVIEW POLICY:

This policy shall be reviewed by the Board and any necessary changes shall be introduced as and

when it is found necessary due to business needs and the same shall be communicated to the

compliance officer. The compliance Officer shall make necessary modifications communicated

to him and hence the new modified policy shall come into effect.

PMLA POLICY

1. PREFACE:

This document is the PMLA policy of Ortem Securities Limited while carrying out its business activities as

a member of National Stock Exchange of India Limited and Bombay stock Exchange Limited. This policy is

designed to prohibit and actively prevent money laundering.

This policy provides a detailed account of the procedures and obligations to be followed to ensure

compliance with issues related to KNOW YOUR CLIENT (KYC) Norms, ANTI MONEY LAUNDERING (AML),

CLIENT DUE DILIGENCE (CDD) and COMBATING FINANCING OF TERRORISM (CFT). Policy specifies the

need for additional disclosures to be made by the clients to address concerns of Money Laundering and

Suspicious transactions undertaken by clients and reporting to FINANCIAL INTELLIGENT UNIT (FIU-IND).

These policies are applicable to both Branch and Head Office operations and are reviewed from time to

time.

2. INTRODUCTION:

A. Background:

Pursuant to the recommendations made by Financial Action Task Force (FATF) on Anti Money

Laundering Standards, SEBI issued a Master Circular on Anti Money Laundering vide circular no.

CIR/ISD/AML/3/2010 dated 31st December, 2010.

SEBI master circular invokes the PML Act/Rules and mandates detailed activities upon all intermediaries

regulated by SEBI while accepting clients. As per the SEBI guidelines, all intermediaries have been

advised to ensure that proper policy frameworks are put in place as per the guidelines on Anti Money

Laundering standards notify by SEBI.

B. What is Money Laundering?

Money Laundering is the process of engaging in financial transactions which involve income derived

from criminal activities, transactions designed to conceal the true origin of criminally derived proceeds

and appears to have been received through legitimate sources/funds.

C. The Prevention of Money Laundering Act, 2002 (PMLA)

The Prevention of Money Laundering Act, 2002 has been brought into effect from 1st July, 2005 and

certain amendments have been made in the year 2012. Necessary notifications/Rules under the said act

have been published in the Gazette of India by the department of revenue, ministry of Finance,

Government of India.

As per PMLA, every intermediary shall have to maintain a record of all transactions, the nature and value

which have been prescribed in the Rules notified under PMLA. For the purpose of PMLA,

‘Suspicious Transaction’ means a transaction whether or not made in cash which to a person acting in

good faith-

i) Gives rise to reasonable ground of suspicion that it may involve proceeds of crime.

ii) Appears to be made in circumstances of unusual or unjustified complexity.

iii) Appears to have no economic rationale or bonafide purpose.

3. POLICIES AND PROCEDURES TO COMBAT MONEY LAUNDERING:

The policies and procedures adopted to combat money laundering are as follows:

i) Communication of group policies relating to Prevention of Money Laundering and Terrorist

Financing to all management and relevant staff that handles account information, securities

transactions, client records, etc.

ii) Client acceptance policy and client due diligence measures including requirements for

proper identification.

iii) Maintenance of records.

iv) Compliance with relevant statutory and regulatory requirements.

v) Co-operation with relevant law enforcement authorities, including timely disclosure of

information.

vi) Conduction of internal audits to ensure compliance with the policies, procedures and

controls relating to the Prevention of Money Laundering and Terrorist Financing.

4. PROCEDURES TO IMPLEMENT ANTI-MONEY LAUNDERING MEASURES:

The company has adopted written procedures to implement Anti-Money Laundering provisions as

envisaged. Such procedures include the following three parameters which are related to the overall

“Client Due Diligence” process:

a) Policy for acceptance of clients.

b) Procedure for identifying the clients.

c) Transaction monitoring and reporting especially Suspicious Transaction Reporting.

A. Policy for acceptance of clients:

Before registering a client, we need to identify the following details of the prospective client:

i) Ascertain the category of client before registration as a client (i.e. individual, Corporate, FII

or other)

ii) Obtain all necessary documents for registration (photograph, proof of address, etc.)

iii) Documents should be verified with original and the same to be countersigned by the

Authorized Representative of the company.

iv) Registration of client to be made in the physical presence of the prospective client.

v) Ensure that registration is to be made in clients name only.

vi) Ensure that no account is to be opened in fictitious or benami name.

vii) Ensure that all details of KYC should be completed in all respect. Incomplete KYC shall not be

accepted by the company.

viii) Ensure that the client does not have any criminal background or whether he has been at any

point of time associated in any civil or criminal proceedings anywhere.

ix) Ensure that the client has not been banned at any time from trading in the Stock Market.

B. Procedure for identifying the clients:

To follow the client identification procedure we need to follow the below mentioned factors:

i) The “Know Your Client” policy should be strictly observed with respect to client

identification procedures.

ii) The client should be identified using reliable sources including documents/information.

Obtain adequate information to satisfactorily establish the identity of each new client and

the purpose of the intended nature of the relationship.

iii) The information should be adequate enough to satisfy competent authorities. Each original

document should be seen prior to acceptance of a copy duly verified and attested.

iv) Failure by prospective client to provide satisfactory evidence of identity should be noted

and reported to the higher authority within the organization.

Identification on Risk based approach:

All clients are to be classified as per risk into 3 categories i.e. Low, Medium or High risk.

i. Category A- Low Risk- Clients of this category are those who pose low or nil risk. Such clients

have a respectable social and financial standing. These clients make payments on time and

give delivery of the shares on time

ii. Category B-Medium Risk- Clients of this category are those who are intra-day/speculative

clients. These are the clients who maintain running accounts. However clients who provide

front end margin before exposure or company hold their shares either in hold back accounts

or margin accounts do not fall in this category and may be classified as Low Risk.

iii. Category C-High Risk- Clients of this category are those who have defaulted in the past, have

suspicious background, etc. Apart from these it also includes Clients of Special Category (CSC).

Provided those clients whose risk profile is examined by the company from time to time shall

not fall in the category. Their category shall be classified by the director of the company. Such

clients are:

a) Non-resident clients.

b) High Net worth clients.

c) Politically Exposed person (PEP)

d) Trusts, NGOs and organizations receiving donation.

e) Politically exposed person of foreign origin.

f) Clients in high risk countries.

g) Non face to face clients.

h) Clients with dubious reputation as per public information available.

i) Companies offering foreign exchange offerings.

j) Current/Former Head of State, Current or Former senior High Profile politicians and

connected persons (immediate family, close advisors and companies in which such

individuals have interest or significant influence).

C. Transaction monitoring and Reporting especially Suspicious Transaction Reporting:

Ongoing monitoring is an essential element of effective KYC procedures. We can effectively control and

reduce the risk by having an understanding of the normal and reasonable activity of the client.

Special attention should be paid to all complex unusually large transactions and all unusual patterns

which have no apparent economic or lawful purpose.

Suspicious Transaction Reporting:

Suspicious transactions are reported by the Principal Officer to FIU on being satisfied that the

transaction is suspicious.

The following transactions shall be considered as suspicious:

i) If the size of the order is not commensurate with client income level or if it is more than its usual

order size.

ii) Any sudden activity in dormant account.

iii) Any transaction which is unusually large or is complex should be immediately brought to the notice of

the compliance department.

iv) Client whose identity verification seems difficult or client appears not to cooperate.

v) When the source of funds for any transaction is not clear.

vi) Transactions by clients in high risk jurisdictions.

vii) Request to transfer money or securities to third parties with or without any known connection

between customers.

viii) Transaction is not in accordance with clients normal activity.

ix) Cash movements in and out of an account within a short period of time.

The above mentioned instances are only a few examples of suspicious transactions and include many

more instances of suspicious activity.

The principal officer is responsible for timely submission of CTR and STR to FIU-IND. The reports will be

submitted in electronic format through FINnet Gateway by the Principal Officer. Nil submission is not

required to be made in case no such occurrence of suspicious transactions takes place.

5. PROCESSING OF SUSPICIOUS TRANSACTION ALERTS:

When alerts are generated at our end or received from the Exchange (to be downloaded through

member portal), the following procedure is to be followed:

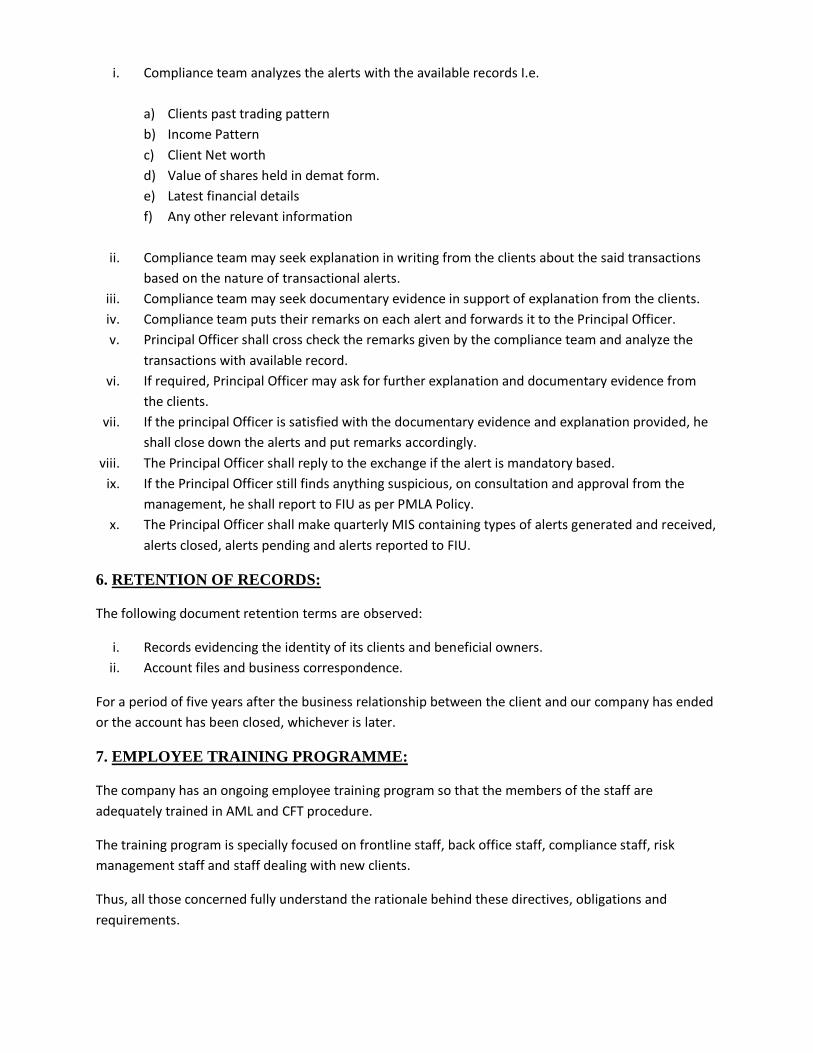

i. Compliance team analyzes the alerts with the available records I.e.

a) Clients past trading pattern

b) Income Pattern

c) Client Net worth

d) Value of shares held in demat form.

e) Latest financial details

f) Any other relevant information

ii. Compliance team may seek explanation in writing from the clients about the said transactions

based on the nature of transactional alerts.

iii. Compliance team may seek documentary evidence in support of explanation from the clients.

iv. Compliance team puts their remarks on each alert and forwards it to the Principal Officer.

v. Principal Officer shall cross check the remarks given by the compliance team and analyze the

transactions with available record.

vi. If required, Principal Officer may ask for further explanation and documentary evidence from

the clients.

vii. If the principal Officer is satisfied with the documentary evidence and explanation provided, he

shall close down the alerts and put remarks accordingly.

viii. The Principal Officer shall reply to the exchange if the alert is mandatory based.

ix. If the Principal Officer still finds anything suspicious, on consultation and approval from the

management, he shall report to FIU as per PMLA Policy.

x. The Principal Officer shall make quarterly MIS containing types of alerts generated and received,

alerts closed, alerts pending and alerts reported to FIU.

6. RETENTION OF RECORDS:

The following document retention terms are observed:

i. Records evidencing the identity of its clients and beneficial owners.

ii. Account files and business correspondence.

For a period of five years after the business relationship between the client and our company has ended

or the account has been closed, whichever is later.

7. EMPLOYEE TRAINING PROGRAMME:

The company has an ongoing employee training program so that the members of the staff are

adequately trained in AML and CFT procedure.

The training program is specially focused on frontline staff, back office staff, compliance staff, risk

management staff and staff dealing with new clients.

Thus, all those concerned fully understand the rationale behind these directives, obligations and

requirements.

INACTIVE/DORMANT ACCOUNT POLICY

1. PREFACE:

This document shall be the Inactive/Dormant Account Policy of Ortem securities Limited while carrying

out its business activities as a member of National Stock Exchange of India Limited and Bombay Stock

Exchange Limited.

2. OBJECTIVE:

The objective of this policy is to appropriately deal with the Inactive/Dormant Clients i.e. the clients who

have not traded for more than 11 continuous months.

The policy is also applicable for accounts which have been marked as inactive on account of Rules,

Byelaws, Circulars and guidelines issued by SEBI, Exchanges and internal Risk Management policies.

3. POLICY:

A. Procedure to handle Inactive/Dormant Accounts:

If the client does not undertake any transaction (buy/sell) for 11 continuous months in any financial year

then such accounts shall be marked as Inactive/Dormant.

All the accounts marked as Inactive/Dormant are monitored carefully in order to avoid any unauthorized

transactions in the account. In case of any transactions in dormant account the same shall be treated as

suspicious transaction and appropriate disciplinary action shall be taken as mentioned in the PMLA

policy of the company.

B. Process of Reactivation of Inactive/Dormant Accounts:

An Inactive/dormant account can be reactivated on submission of the below mentioned documents:

i) Reactivation request Form (Attached here as Annexure A)

ii) Self attested copy of PAN Card.

iii) Copy of latest address proof.

iv) Copy of Latest bank statement for a period of six months (if dealing in F&O segment)

v) Any other necessary documentary evidence for any change in information provided in KYC

at the time of registration along with written request.

On verification of the same the Compliance Officer authorizes the activation of such inactive accounts.

C. Consequences of Inactive/Dormant Accounts:

On a client being declared inactive, the client’s funds and Demat account shall be settled.

Settlement of clients accounts shall be done as per the periodicity (monthly/quarterly) opted by the

client and his/her assets (funds, securities or any other collateral) shall be returned and the statement

for the same to be sent to the clients.

Proof of sending the statement of settlement of accounts is maintained. Settlement of clients account is

done at least once in a calendar quarter.

D. Controls after activation of Inactive Accounts:

i) Trades in such accounts shall be confirmed with respective clients by a person from Head Office who

has note punched/received such orders.

ii) Regular monitoring of such accounts is to be done and in case of generation of alert necessary

disciplinary action shall be taken as per the PMLA policy of the company and rules, byelaws and

guidelines of SEBI and Exchanges.

4. REVIEW POLICY:

This policy may be reviewed by the board as and when there are any changes introduced by any

statutory authority and or as and when it is found necessary to change on account of business needs

and Risk Management Policy.

FROM:_________________________

______________________________

______________________________

Date:

To, Ortem Securities Limited 59, Bentick Street, 1st Floor Kolkata- 700069. Sub: Reactivation of Trading Account. Client Code: __________________

Sir,

I/We ____________________________________________ (name of the individual/non-individual), having

trading account with Unique Client Code ___________________ allotted to me/us by your broking house

am/are not trading in Cash/Future & Options segment(s) on the NSE trading platform since

_________________ (last trade date). However I/We am/are desirous to start trading again in Cash/Future &

Options segment(s) on the NSE trading platform. In this regard, you are requested to reactivate my/our

trading account and allow trading with immediate effect.

I/We hereby undertake that:

1. I/We have submitted the below mentioned necessary documents required for reactivation of my/our

trading account:

Self attested copy of PAN Card.

Copy of latest address proof.

Copy of latest bank statement for a period of six months (if dealing in F&O segment)

Any other necessary documentary evidence for any change in information provided in KYC at the

time of registration along with written request.

My present Mobile No. is

My present email id is ______________________________________

2. I/We have submitted necessary supporting documents along with written request for changes in

information (if any) provided in KYC at the time of registration as client.

Yours Faithfully __________________________________ (Signature of the Individual Client) OR For (Name of the Non-Individual Client) _________________________________

(Name & Signature of the Authorized Signatory-Designated Director/Managing Partner/Karta/Proprietor)

POLICY FOR CLIENT CODE MODIFICATION/ERROR ACCOUNT

1. PREFACE:

This document shall be the policy for Client Code Modification/Error account while carrying out its

business activities as a member of National Stock Exchange of India Limited and Bombay Stock Exchange

Limited.

2. OBJECTIVE:

The main objective of this policy is to deal with modification of client code after the execution of trade

and to create awareness amongst our clients and relevant staff such as dealers, Branch-in charge,

Compliance officer, Sub-Broker and Authorized Persons.

3. BACKGROUND:

SEBI vide its circular no. CIR/DNPD/6/2011 dated July 5, 2011 and National Stock Exchange vide circular

nos. NSE/INVG/2011/18281 dated July 5, 2011,NSE/INVG/2011/18484 dated July 29, 2011 and

NSE/INVG/2011/18716 dated August 26, 2011 directed that modifications of client codes of non-

institutional trades are done only to rectify a genuine error in entry of client code at the time of placing

/modifying the related order.

The Company shall have the absolute discretion to accept, refuse or partially accept the Client Code

Modification requests based on risk perception and other factors considered relevant by the Company.

4. ERROR TRADES:

Dealers are advised to hear patiently the Client Code/Scrip name and reconfirm the same to their best

possible efforts before placing order into the system. However, the following are considered as Genuine

Errors as per the Circulars issued by SEBI/Exchanges:

i) Where original client code/name and modified client code/name are similar to each other

but such modifications are not repetitive.

ii) Error due to communication and / or punching or typing such that the original client

code/name and the modified client code/name are similar to each other.

iii) Modification within relatives (‘Relatives’ for this purpose would mean ‘Relative’ as defined

under the Companies Act, 1956 which is annexed herewith as Annexure 1.)

Provided there is no consistent pattern in the above mentioned modifications.

5. POLICY:

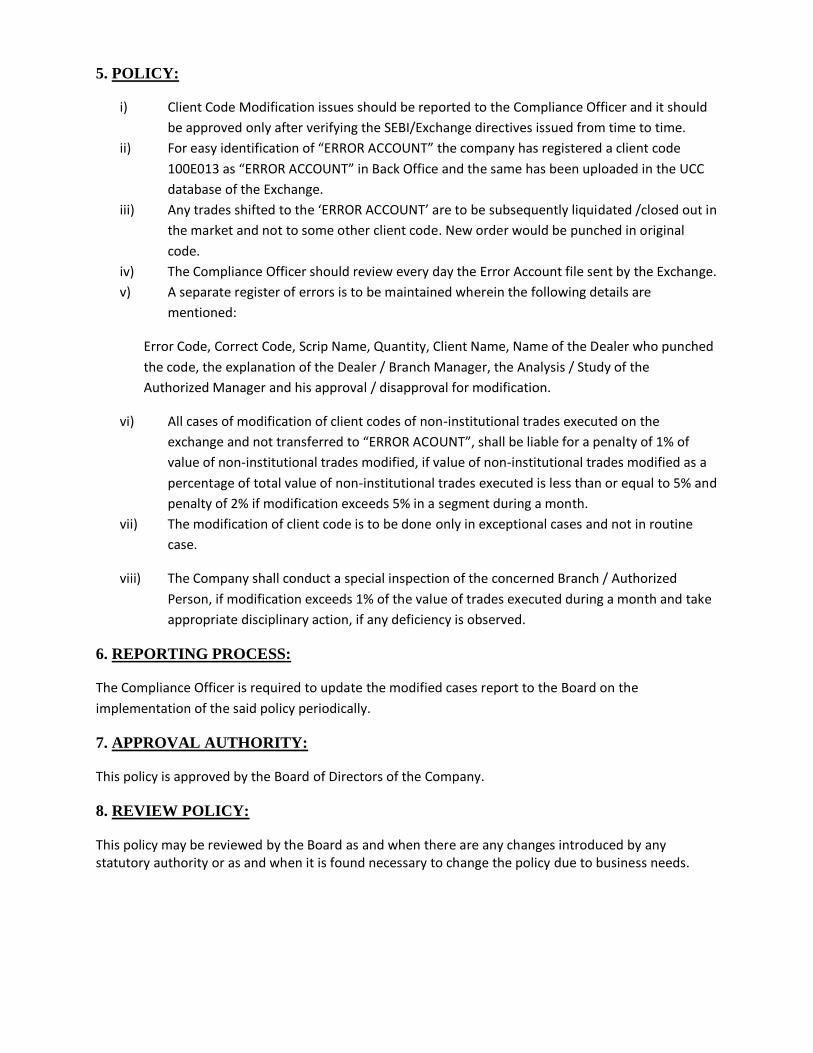

i) Client Code Modification issues should be reported to the Compliance Officer and it should

be approved only after verifying the SEBI/Exchange directives issued from time to time.

ii) For easy identification of “ERROR ACCOUNT” the company has registered a client code

100E013 as “ERROR ACCOUNT” in Back Office and the same has been uploaded in the UCC

database of the Exchange.

iii) Any trades shifted to the ‘ERROR ACCOUNT’ are to be subsequently liquidated /closed out in

the market and not to some other client code. New order would be punched in original

code.

iv) The Compliance Officer should review every day the Error Account file sent by the Exchange.

v) A separate register of errors is to be maintained wherein the following details are

mentioned:

Error Code, Correct Code, Scrip Name, Quantity, Client Name, Name of the Dealer who punched

the code, the explanation of the Dealer / Branch Manager, the Analysis / Study of the

Authorized Manager and his approval / disapproval for modification.

vi) All cases of modification of client codes of non-institutional trades executed on the

exchange and not transferred to “ERROR ACOUNT”, shall be liable for a penalty of 1% of

value of non-institutional trades modified, if value of non-institutional trades modified as a

percentage of total value of non-institutional trades executed is less than or equal to 5% and

penalty of 2% if modification exceeds 5% in a segment during a month.

vii) The modification of client code is to be done only in exceptional cases and not in routine

case.

viii) The Company shall conduct a special inspection of the concerned Branch / Authorized

Person, if modification exceeds 1% of the value of trades executed during a month and take

appropriate disciplinary action, if any deficiency is observed.

6. REPORTING PROCESS:

The Compliance Officer is required to update the modified cases report to the Board on the

implementation of the said policy periodically.

7. APPROVAL AUTHORITY:

This policy is approved by the Board of Directors of the Company.

8. REVIEW POLICY:

This policy may be reviewed by the Board as and when there are any changes introduced by any statutory authority or as and when it is found necessary to change the policy due to business needs.

POLICY FOR PRE-FUNDED INSTRUMENTS / ELECTRONIC

TRANSFERS

1. PREFACE: This document shall be the Policy for Pre-Funded Instruments / Electronic Transfers while carrying out its business activities as a member of National Stock Exchange of India Limited and Bombay Stock Exchange Limited.

2. OBJECTIVE: The objective of this policy is to prevent acceptance of third party funds and to prescribe process to deal with instruments issued by third party when received. The policy also focuses on minimizing the frequency of acceptance of Pre funded instrument especially Demand Draft where there is a difficulty in tracking the correct source of issuance.

3. BACKGROUND:

SEBI vide Circular no. SEBI/MRD/SE/Cir-33/2003/27/08 dated August 27, 2003 has specified that the stock brokers can accept demand drafts from their clients. However, SEBI vide Circular no. CIR/MIRSD/03/2011 dated June 9, 2011 and National Stock Exchange vide its circular no. NSE/INSP/18024 dated June 9, 2011 has advised stock brokers to maintain an audit trail while receiving funds from the clients through Demand Draft (DD) / Pay Order (PO) / Bankers Cheque (BC) since such third party pre-paid instruments do not contain the details like the name of the client, bank account number are not mentioned on such instruments. Non maintenance of audit trail may result in flow of third party funds or unidentified money which may result into breach of regulations issued under PMLA and SEBI circulars.

4. POLICY:

SEBI vide circular no. SEBI/MRD/SE/Cir-33/2003/27/08 dated August 27, 2003 has specified that the stock brokers can accept demand drafts from their clients. However, in accordance with SEBI circular no. CIR/MIRSD/03/2011 dated June 9, 2011 the following are complied: i. A “Pre-paid instrument received register” with columns for date, name of the client, amount, instrument drawn on (bank name) and such other columns as found necessary is maintained. The register is maintained in electronic form. ii. Pre-paid instruments of the value less than may be accepted from the client. Whenever such instruments are received, entry shall be made into “Pre-paid instruments received register”. iii. If the pre-paid instrument is for value more than 50,000 or if the aggregate value of pre-funded instruments is Rs. 50,000 or more per day per client is received for acceptance then such instrument or instruments may be accepted only if the same is/are accompanied by the name of the bank account holder and number of the bank account debited for the purpose, duly certified by the issuing bank. The mode of certification may include the following:

a. Certificate from the issuing bank on its letter head on a plain paper with the seal of the issuing bank.

b. Certified copy of the requisition slip (portion which is retained by the bank) to issue the instrument.

c. Certified copy of the passbook / bank statement for the account debited to issue the instrument.

d. Authentication of the bank account number debited and name of the account holder by the issuing bank on the reverse of the instrument.

iv. If a client submits pre-paid instruments at different times during the day, details and certificates as stated above may be collected along with the instrument with which the aggregate value of pre-paid instruments submitted exceeds Rs. 50,000 for that date. v. In case of any receipt of funds by way of Electronic Fund Transfer, an audit trail to ensure that funds are received from respective client only has to be maintained. Necessary details may be collected from banker at which the amount is received. vi. If the pre-paid instrument is received through post or any other method where the client does not directly interface for the submission of the instrument and the instrument does not contain the information as required above, the following action may be taken:

a. Contact the client immediately and seek information. Not to bank the instrument until the information is given by the client.

b. If the pre-paid instrument is bank transfer, contact banker immediately for the details; not utilize the amount so credited until the details are received and not to give credit to the customer until banker gives the details / certification.

vii. While giving credit to respective client’s ledger, Head Office needs to cross check / verify with documents that such instrument received from respective clients.

5. REVIEW POLICY:

This policy may be reviewed by the board as and when there are any changes introduced by any statutory authority and or as and when it is found necessary to change on account of business needs.

BLOG CHAT POLICY

1. PREFACE:

This document shall be the Blog Chat Policy of Ortem securities Limited while carrying out its business

activities as a member of National Stock Exchange of India Limited and Bombay Stock Exchange Limited.

2. OBJECTIVE:

The objective of this policy is to protect the investor by stopping unauthentic news circulation by the

staff / temporary staff / dealing person and by the Company.

3. POLICY:

As per the code of conduct for Stock Broker in SEBI (Stock Brokers and Sub-Brokers) Regulations, 1992

and SEBI Circular Cir/ISD/1/2011 dated March 23,2011, all SEBI registered market intermediaries are

required to have proper internal code of conduct to govern the conduct of its employees.

In view of the same, ORTEM SECURITIES LIMITED implements code of conduct for communicating

through various modes of communication. Employees / Temporary staff are prohibited from:

1. Circulation of unauthenticated news related to various scrips in blogs/chat forums/e-mails etc.

2. Encouraging or circulating rumours or unverified information obtained from client, industry, any

trade or any other source without verification.

3. Forwarding any market related news received either in their official mail/ personal mail/ blog or

in any other manner except after the same has been seen and approved by the Compliance

Officer.

If any employee fails to do so, he/she will be deemed to have violated the various provisions contained

in SEBI Act/Rules/Regulation etc. and shall be liable for actions.

The Compliance Officer shall also be held liable for breach of duty in this regard.

Access to blogs/chat forums/messengers sites etc. has been restricted by the Company and access is not

allowed.

4. REVIEW POLICY:

This policy may be reviewed by the board as and when there are any changes introduced by any

statutory authority.

POLICY ON CONFLICT OF INTEREST

Pursuant to the SEBI Circular no. CIR/MIRSD/5/2013 dated August 27, 2013 wherein members are

required to lay down policies and procedures to identify and to avoid or deal with Conflict of Interest.

Accordingly, this document shall be the Policy on Conflict of Interest of the company. The policy is

mentioned below:

i) The company at all times shall maintain high standards of integrity in the conduct of its

business. The company shall have high standards of honesty and truthfulness while dealing

in the business of securities market.

ii) The company ensures to give fair treatment to its clients and not discriminate amongst

them i.e. it shall give equal amount of good services to all its clients.

iii) The company shall ensure that any person dealing for and on behalf the company with any

of its clients, there shall not be any conflict in his duty towards the client and the client’s

interest shall always be of primary importance.

iv) Any employee of the company while dealing with the clients shall ensure that if at all there

is bound to be conflict of interest, the proper disclosure shall be made to the client to

ensure that fair and unbiased services are rendered to the clients. The copy of such

disclosure shall be given to the Compliance Department.

v) If any employee of the company has any conflict of interest then he/she shall inform to the

Compliance Department.

vi) Any employee/sub-broker/authorized person of the company shall not communicate to the

clients about unpublished information of the company.

vii) The company and its employees shall not indulge in manipulation of demand and supply of

securities which influences the price of the securities.

viii) The company and its employees shall not share information about the scrip received from

the clients.

The above policy may be revised from time to time by the board as and when required to meet the

needs of the business.

INTERNAL CONTROL POLICY

1. CLIENT REGISTRATION, DOCUMENTS MAINTENANCE PROCEDURES:

Client registration form/ booklet (KYC) be made available to the client and explain the contents

and requirements in details

Upon receipt of duly filled KYC, the same should be thoroughly scrutinized by an officer.

All the original documents be verified and obtain documents as per SEBI uniform documentary

requirements.

In person verification of the client be done by a staff. In case of clients introduced by the sub-

broker, in presence of the Sub-Broker.

Unique client Code (UCI), to be allotted, the same should be uploaded and reported to the

exchange via UCI upload facility available on www.connect2nse.com/UCI/

UCI so allotted be communicated to the client and photocopies of KYC be sent to the client.

2. POLICY:

We shall register clients who are known to the Directors and / or clients who are introduced by a

known reference.

In case of clients introduced by the Sub-Broker, we shall convey our policy to them and ensure the

Sub-Broker implements.

We shall not entertain walk in clients.

3. CLOSURE OF CLIENT ACCOUNT / DORMANT ACCOUNTS

An account shall be closed only upon receipt of a written notice of the clients

as per the relevant clause of the Company’s policies and procedures..

Trading desk and back office shall make necessary note of the closure.

4. ORDER RECEIPT AND EXECUTION.

The orders shall be executed by the dealers which are communicated to them. The mode of

communication could be

Verbal i.e. telephonic, or

in person visit of the client.

Dealers should take care to identify the client before executing the order and take clear and

proper instructions.

Dealer shall not exercise any discretion in executing clients order.

Upon execution of the trade, the same shall be communicated to the client telephonically, via

SMS or any other electronic mode in addition to the mandatory contract note which shall be

sent in hard copy via courier at the end of the day.

5. SENDING CONTRACT NOTES, DAILY MARGIN STATEMENT, QUARTERLY STATEMENT OF ACCOUNTS TO CLIENTS

Contract Note

We follow the practice of issuing contract note through courier.

At the end of the day, the contract notes should be issued to all the clients who have traded for

the day.

Daily Margin Statement

Daily margin statement shall be generated at the end of the day and shall be sent to the client

electronically.

Quarterly statement of Accounts

The quarterly statement of funds and securities shall / be sent to all along with error reporting

clause within 30 days from the end of the quarter.

Additionally trade details, client ledger (net position), and Trail Balance Position report are to be

uploaded on our website www.ortemsecurities.com.

6. COLLECTION OF PAY IN, MARGINS, LIMITS SETTING FOR EXPOSURES & TURNOVER FOR CLIENTS, TERMINALS, BRANCHES & SUB-BROKER LEVEL

A designated officer under managerial guidance shall be responsible for the collection of funds,

and securities for pay in for cash segment, and collection of margin and mark to market losses

for F&O Segment

Top priority shall be given to high value transactions.

Securities and funds, for which the payout has completed, shall be adjusted first towards the

client’s obligation for the subsequent settlement before releasing the funds / securities.

Penalties levied by the exchange for shortage of securities/funds/margins for a client shall be

recovered from the client.

The management shall review and monitor outstanding obligation on a daily basis and instruct

dealer to take one or all of the following.

Liquidate / close out all the open position

Sell securities received from client as collaterals.

Adjust payout of funds from one segment with that of other.

The client shall be intimated in writing about the above action taken by the management.

7. LIMITS SETTINGS

Limit setting for exposure for each NEAT terminals and branches shall be done by the Director /

Wholetime Director i.e User id_____. The limit settings shall be done by analysing the past trading

history and the market risk prevailing from time to time.

A designated branch Manager shall be responsible for setting up turnover limits at the branch level.

NEAT system does not provide the setting up of turnover limits / exposure limits at client level.

However, each dealer shall be instructed to execute trades as per the profile of the client handled by

them and shall take prior approval from management before executing large trade.

The limits for the clients who are availing internet trading facility shall be set by the designated

officer after obtaining consent from the management.

The limit shall be set using NOW admin terminal

8. MONITORING OF DEBIT BALANCES

The account department has been trained to ensure that the client’s dues are collected on T+1

basis.

All the outstanding debit balances are constantly followed up with the client by the back office

and the management is informed about the status.

Long over dues debits if any are handled by the management.

The management shall take necessary action including restriction of fresh trading till the dues are

cleared; sell securities held as collaterals, reducing existing position, adjustments of credits in

other segments etc.

9. ALLOTMENT, SURRENDER OF TRADING TERMINALS

The management shall take the decisions about allotment of additional trading terminals at the

existing location as and when the need for the same arises.

The allotment shall be made to a person who has passed the NCFM dealer module and / or is

eligible as per the exchange rules to be authorized user of trading terminals.

The necessary details shall be uploaded to the exchange through ENIT.

10. OPENING AND CLOSING OF THE BRANCHES / SUB-BROKERS OFFICES

We do not follow policy of aggressive expansion through opening of branches franchise

location / Sub Broker.

We shall open a branch only if it can be managed by us or any person whom we feel has

enough experience and is known to us for reasonable period of time.

The decision to close any existing branch shall also be made by the management if the need so

arises.

The proposals to open Branch Office by the Sub-Broker shall be considered favorably if the

Sub-Broker has the

Required qualification

Necessary infrastructure

Reasonable experience

11. PAYMENT / RECEIPT OF FUNDS FROM/ TO CLIENTS.

The back office shall ensure the receipts of funds from clients for pay-in obligation on T+2 basis.

Any deviation shall be reported to the management.

No cash transactions shall be permitted.

Checks shall be provided to ensure that the funds are received from respective clients account.

The payout of funds shall be done within 24 hours of the exchange payout

In cases where the authorization for running account is received the same shall be settled

monthly / quarterly.

12. RECEIPT / DELIVERY OF SECURITIES FROM / TO CLIENTS

The back office shall ensure that all clients who have sold shares are received in our pool account

before the scheduled pay in. Checks shall be in place for ensuring receipt of securities from

respective client beneficiary account.

Payout of securities to clients who have bought the shares shall be done directly to the respective

beneficiary through exchange by uploading ____files before the payout.

Shares payout may be withheld in case the funds pay in is not received from client. The shares so

withheld shall be released within 24 hours of the receipt of the payment.

13. SQUARE OFF OF POSITIONS / LIQUIDATION OF SECURITIES WITHOUT CONSENT OF CLIENTS

The management policy is such that it does not encourage excessive speculative activities and

ensures that client trades only after assessing his risk taking capacity and risk profile. Consequently,

so far the company has never had to square off the clients’ position due to Margin/Pay in defaults.

In the unfortunate circumstances of such a default occurring, the procedure shall be as under.

The dealer shall close out / liquidate all outstanding position / securities so as to meet all the

outstanding obligation of the client after obtaining written approval from management and the

compliance officer.

The client shall be communicated in writing detailing the above action.

14. POLICY ON INTERNAL SHORTAGES

Internal shortage shall be dealt with by buying the security in the subsequent settlement on behalf

of the client who has failed to deliver the securities after obtaining mutual consent of buyer. In case

the security is not available for any reason whatsoever, the same shall be dealt with as per close out

policy laid down by the exchange.

15. INVESTOR REDRESSAL MECHANISM

We have a dedicated email id for customer grievances and the same is communicated to our clients

through letters, websites, contract notes and bills etc. So far we have not received any complaints

but in case if we come across in future then we have adequate system in place to redress such

grievance.

16. DIRECTION BY THE COMPANY

The Internal Control Policy covers a wide range of business practices and procedures. It sets out basic

principles to guide all employees of the firm. It is supplemented by our Policies, Guidelines and

Procedures, which collectively provide a framework for prudent decision-making.

17. REVIEW POLICY:

This policy may be reviewed by the board as and when there are any changes introduced by any

statutory authority and or as and when it is found necessary to change on account of business needs.

POLICY FOR IDENTIFICATION OF BENEFICIAL OWNERSHIP

1. PREFACE:

This document shall be the Policy for Identification of Beneficial Ownership of Ortem securities Limited

while carrying out its business activities as a member of National Stock Exchange of India Limited and

Bombay Stock Exchange Limited.

2. OBJECTIVE:

The objective of this policy is to identify and verify the identity of persons who beneficially own or

control the securities account.

This policy is applicable to those persons who ultimately own, control or influence a client and/or person

on whose behalf a transaction is being conducted and also who exercises ultimate effective control over

a legal person or arrangement.

3. BACKGROUND:

SEBI vide its Master Circular No. CIR/ISD/AML/3/2010 dated December 31, 2010 mandated all registered

intermediaries to obtain, as part of their Client Due Diligence policy, sufficient information from their

clients in order to identify and verify the identity of persons who beneficially own or control the

securities account.

Further, SEBI vide Circular No. CIR/MIRSD/2/2013 dated January 24, 2013 laid down the Guidelines on

identification of Beneficial Ownership for the Intermediaries.

4. POLICY:

In accordance with SEBI Circular No. CIR/MIRSD/2/2013 dated January 24, 2013, following guidelines

have to be complied with:

A. For Clients other than Individuals or Trusts:

Where the client is a person other than an individual or trust, viz., company, partnership or

unincorporated association/body of individuals, the company shall identify the beneficial owners of

the client and take reasonable measures to verify the identity of such persons, through the following

information:

The identity of the natural person, who, whether acting alone or together, or through one or more juridical person, exercises control through ownership or who ultimately has a controlling ownership interest.

In cases where there exists doubt under as to whether the person with the controlling ownership interest is the beneficial owner or where no natural person exerts control through ownership interests, the identity of the natural person exercising control over the juridical person through other means.

Where no natural person is identified, the identity of the relevant natural person who holds the position of senior managing official.

B. For Client which is a Trust:

Where the client is a trust, the company shall identify the beneficial owners of the client and take reasonable measures to verify the identity of such persons, through the identity of the settler of the trust, the trustee, the protector, the beneficiaries with 15% or more interest in the trust and any other natural person exercising ultimate effective control over the trust through a chain of control or ownership. C. Exemption in case of Listed Companies: Where the client or the owner of the controlling interest is a company listed on a stock exchange, or is a majority-owned subsidiary of such a company, it is not necessary to identify and verify the identity of any shareholder or beneficial owner of such companies.

5. REVIEW POLICY:

This policy may be reviewed by the board as and when there are any changes introduced by any statutory authority.

POLICY GUIDELINES ON OUTSOURCING OF ACTIVITIES

1. PREFACE

This document shall be the Policy on Outsourcing of Activities of Ortem Securities Limited while carrying

out its business activities as a member of National Stock Exchange of India Limited and Bombay Stock

Exchange Limited.

2. BACKGROUND

SEBI Vide Circular CIR/MIRSD/24/2011 dated 15.12.2011 issued a circular regarding outsourcing of activities by intermediaries. According to the same:

SEBI has defined outsourcing as the use of one or more than one third party – either within or outside the group – by registered intermediary to perform the activities associated with services which the intermediaries offers.

The risks associated with outsourcing may be operational risk, reputational risk, legal risk, country risk, strategy risk, exit-strategy risk, counter party risk, concentration and systemic risk.

SEBI has framed and laid down the principles for outsourcing by intermediaries

Intermediaries desirous of outsourcing their activities shall not outsource their core business activities and compliance function. A few examples of core business activities may include – execution of orders and monitoring of trading activities of clients in case of stock brokers, dematerialization of securities in case of Depository Participants, investment related activities in case of mutual funds and Portfolio managers.

The intermediary shall be responsible for reporting of any suspicious transactions / reports to FIU or any other competent authority in respect of activities carried out by the third parties.

In view of the changing business activities and complexities of various financial products, the intermediary shall bring its existing outsourcing arrangements in line with the requirements of guidelines / principles.

3. ACTIVITIES OF THE COMPANY

A. STOCK BROKING ACTIVITIES

Ortem Securities Limited is a SEBI registered member of National Stock Exchange of India Limited (NSEIL) and Bombay Stock Exchange (BSE) and is governed by the circulars issued by SEBI, NSE & BSE from time to time.

B. DEPOSITORY PARTICIPANT ACTIVITIES Ortem Securities Limited is a SEBI registered Depository Participant with National Securities & Depository Limited (NSDL) and is governed by Depositories Act, 1996, SEBI (Depositories & Participant) Regulations, 1996 and circulars issued by SEBI & NSDL from time to time.

4. OUTSOURCING OF ACTIVITIES

Ortem Securities Limited has not so far availed any outsourced activity. If it intends to outsource any of the activities associated with services which the intermediaries’ offers, would formulate relevant policy and take appropriate approval. Also, we will not outsource any core business activities and compliance functions as stipulated by Securities Exchange Board of India (SEBI).

5. REVIEW POLICY:

This policy may be reviewed by the board as and when there are any changes introduced by any statutory authority and or as and when it is found necessary to change on account of business needs.