Polarcus Limited

30

www.polarcus.com 1 13 November, 2012 Rolf Ronningen, CEO Tom Henrik Sundby, CFO Polarcus Limited

Transcript of Polarcus Limited

www.polarcus.com 1

13 November, 2012

Rolf Ronningen, CEO

Tom Henrik Sundby, CFO

Polarcus Limited

www.polarcus.com 2

Disclaimer

This Presentation of Polarcus Limited (the “Company”) has been prepared solely for information purposes. This Presentation may not be

distributed, reproduced or used without the consent of the Company.

The information contained herein does not purport to contain all information concerning the Company. No party has made any kind of

independent verification of any of the information set forth herein, including any statements with respect to projections or prospects of the

business or the assumptions on which such statements are based. The Company nor any of its subsidiaries make any representations or

warranty, express or implied, as to the accuracy, reliability or completeness of this Presentation or of the information contained herein and shall

have no liability for the information contained in, or any omissions from, this Presentation.

Included in this Presentation are various “forward-looking statements”, including statements regarding the intent, opinion, belief or current

expectations of the Company or its management. Such forward-looking statements are not guarantees of future performance and involve known

and unknown risks, uncertainties and other factors that may cause the actual results, performance and outcomes to be materially different from

any future results, performance or outcomes expressed or implied by such forward-looking statements, including, among others, risks or

uncertainties associated with the Company’s business, segments, development, growth management, financing, market acceptance and

relations with customers, and, more generally, general economic and business conditions, changes in domestic and foreign laws and

regulations, taxes, changes in competition and pricing environments, fluctuations in currency exchange rates and interest rates and other

factors, including lack of operating history. Should one or more of these risks or uncertainties materialize, or should underlying assumptions

prove incorrect, actual results may vary materially from those described in this document.

No information contained herein constitutes, or shall be relied upon as constituting, any advice relating to the future performance of the

Company. The Company undertakes no obligation to publicly update or revise any forward-looking statements included in this Presentation.

www.polarcus.com 3

Agenda

Highlights

Financials

Operations & Market update

Summary & Q&A

Appendices

1

2

3

4

5

www.polarcus.com 4

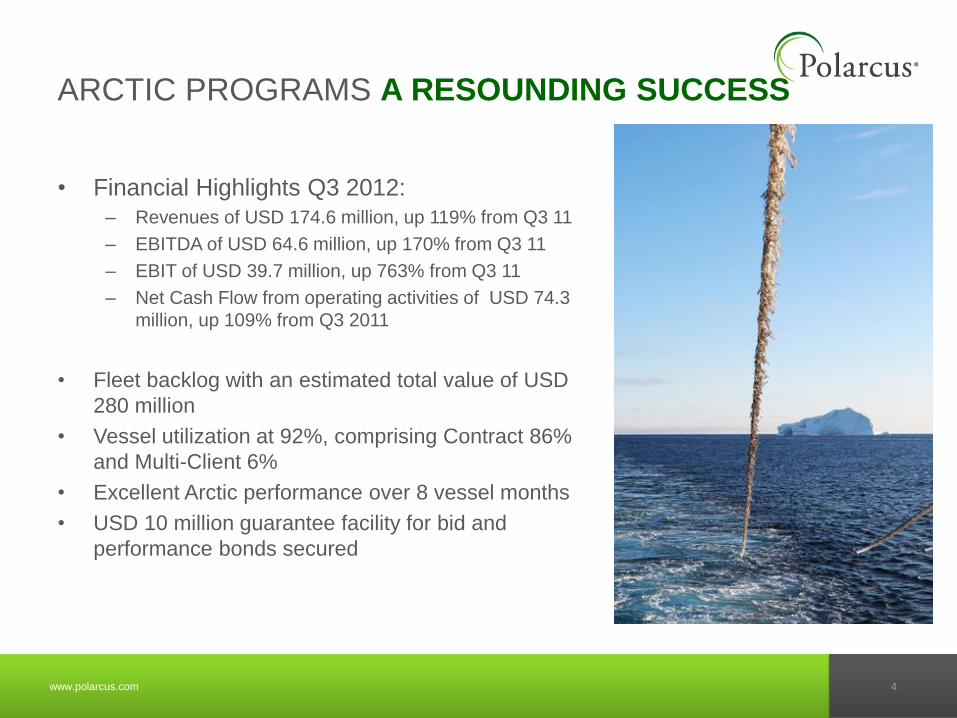

ARCTIC PROGRAMS A RESOUNDING SUCCESS

• Financial Highlights Q3 2012: – Revenues of USD 174.6 million, up 119% from Q3 11

– EBITDA of USD 64.6 million, up 170% from Q3 11

– EBIT of USD 39.7 million, up 763% from Q3 11

– Net Cash Flow from operating activities of USD 74.3

million, up 109% from Q3 2011

• Fleet backlog with an estimated total value of USD

280 million

• Vessel utilization at 92%, comprising Contract 86%

and Multi-Client 6%

• Excellent Arctic performance over 8 vessel months

• USD 10 million guarantee facility for bid and

performance bonds secured

www.polarcus.com 5

Agenda

Highlights

Financials

Operations & Market update

Summary & Q&A

Appendices

1

2

3

4

5

www.polarcus.com 6

Consolidated income statement

Quarter ended Nine months ended Year ended

(In thousands of USD) Notes 30-Sep-12 30-Sep-11 30-Sep-12 30-Sep-11 31-Dec-11

Revenues

Contract revenue 170,232 62,292 374,408 176,118 274,757

Multi-client revenue 3,943 17,543 10,317 17,543 20,571

Other income 471 - 4,171 - 3,248

Total Revenues 174,646 79,835 388,897 193,661 298,577

Operating expenses

Vessel Operating expenses (103,831) (49,369) (237,168) (130,624) (199,460)

Sales, general and administrative costs (6,261) (6,521) (18,054) (17,829) (22,799)

Depreciation and amortisation 10 (24,847) (19,338) (62,513) (42,462) (60,802)

Total Operating expenses (134,939) (75,228) (317,735) (190,915) (283,061)

Gross profit/(loss) 39,707 4,607 71,162 2,746 15,516

Financial Expenses

Finance costs 11 (21,407) (15,522) (70,941) (39,380) (59,472)

Finance income 12 3,032 692 9,528 1,279 5,761

Changes in fairvalue of financial instruments 5 - 4,363 48 6,099 6,720

Gain on acquisition of joint-venture - - 3,602 - -

Net Financial Expenses (18,375) (10,468) (57,763) (32,002) (46,991)

Profit/(loss) for the period before tax 21,332 (5,861) 13,398 (29,256) (31,475)

Income tax expense (258) - (315) (1) (24)

Profit/(loss) for the period 21,074 (5,861) 13,083 (29,257) (31,499)

Other comprehensive income

Other comprehensive income/(loss) for the period - - - - -

Total comprehensive income/(loss) for the period 21,074 (5,861) 13,083 (29,257) (31,499)

Profit/(Loss) per share during the period (In USD)

- Basic

0.042

(0.014)

0.026

(0.071)

(0.075)

- Diluted

0.040

(0.024)

0.025

(0.082)

(0.086)

www.polarcus.com 7

Cash flow

Quarter ended Nine months ended Year ended

(In thousands of USD) 30-Sep-12 30-Sep-11 30-Sep-12 30-Sep-11 Dec-11

Cash flows from operating activities

Profit/(loss) for the period 21,074 (5,861) 13,083 (29,257) (31,499)

Depreciation, amortization and changes in fair value of financial instruments 25,703 15,470 64,478 37,986 56,152

Net Interest expenses 18,158 14,563 61,311 37,440 53,277

Other adjustments 1,665 - (1,898) - -

Net working capital 7,683 11,665 28,990 265 (30,368)

Net cash flows from operating activities 74,283 35,838 165,964 46,435 47,561

Cash flows from investing activities

Decrease/(Increase) in restricted cash 2,927 73,893 17,178 95,031 87,066

Purchases of property, plant and equipment (14,265) (81,432) (295,683) (275,885) (303,579)

Payments for multi-client project library (8,640) (13,397) (19,221) (13,397) (17,282)

Other - (63) (4,984) (178) (219)

Net cash flows used in investing activities (19,978) (20,999) (302,711) (194,429) (234,013)

Cash flows from financing activities

Net proceeds from the issuance of financial instruments (52) - 305,873 178,610 255,058

Repayment of lease liabilities, long-term debt and bonds (13,893) (17,025) (89,688) (32,754) (35,996)

Net interest paid (12,738) (26,513) (52,701) (52,630) (59,111)

Net cash flows from financing activities (26,682) (43,538) 163,485 93,226 159,951

Net increase/(decrease) in cash and cash equivalents 27,623 (28,700) 26,739 (54,768) (26,501)

Cash and cash equivalents at the beginning of the period 59,451 60,768 60,336 86,836 86,836

Cash and cash equivalents at the end of the period 87,074 32,068 87,074 32,068 60,336

www.polarcus.com 8

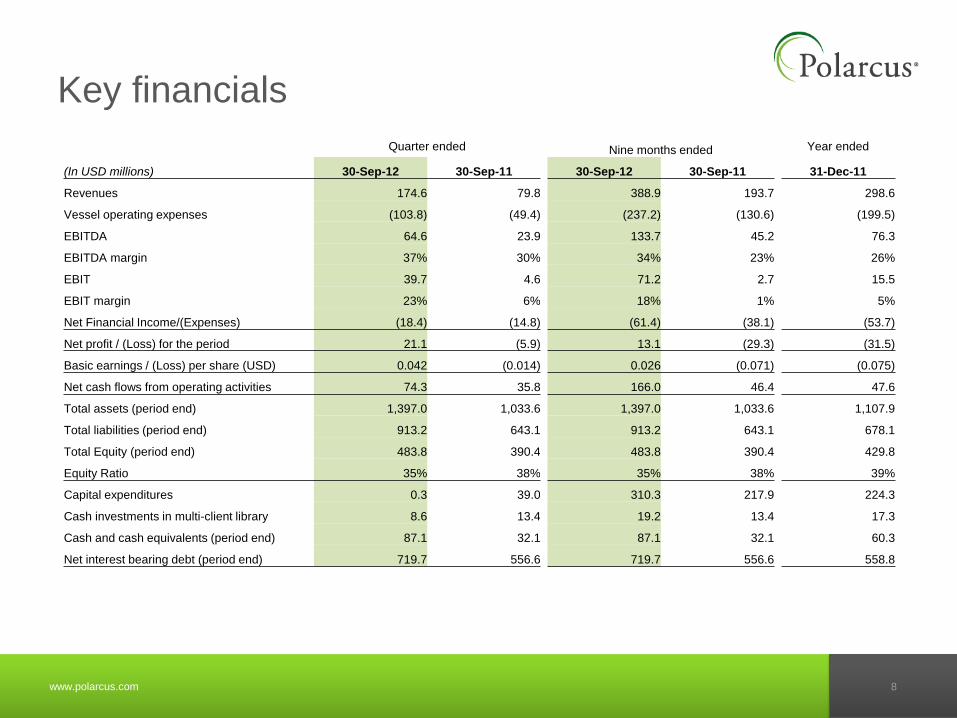

Key financials

Quarter ended Nine months ended Year ended

(In USD millions) 30-Sep-12 30-Sep-11 30-Sep-12 30-Sep-11 31-Dec-11

Revenues 174.6 79.8 388.9 193.7 298.6

Vessel operating expenses (103.8) (49.4) (237.2) (130.6) (199.5)

EBITDA 64.6 23.9 133.7 45.2 76.3

EBITDA margin 37% 30% 34% 23% 26%

EBIT 39.7 4.6 71.2 2.7 15.5

EBIT margin 23% 6% 18% 1% 5%

Net Financial Income/(Expenses) (18.4) (14.8) (61.4) (38.1) (53.7)

Net profit / (Loss) for the period 21.1 (5.9) 13.1 (29.3) (31.5)

Basic earnings / (Loss) per share (USD) 0.042 (0.014) 0.026 (0.071) (0.075)

Net cash flows from operating activities 74.3 35.8 166.0 46.4 47.6

Total assets (period end) 1,397.0 1,033.6 1,397.0 1,033.6 1,107.9

Total liabilities (period end) 913.2 643.1 913.2 643.1 678.1

Total Equity (period end) 483.8 390.4 483.8 390.4 429.8

Equity Ratio 35% 38% 35% 38% 39%

Capital expenditures 0.3 39.0 310.3 217.9 224.3

Cash investments in multi-client library 8.6 13.4 19.2 13.4 17.3

Cash and cash equivalents (period end) 87.1 32.1 87.1 32.1 60.3

Net interest bearing debt (period end) 719.7 556.6 719.7 556.6 558.8

www.polarcus.com 9

Key financials – historic development

4.6

39.7

(10.00)

-

10.00

20.00

30.00

40.00

50.00

Q1-10 Q2-10 Q3-10 Q4-10 Q1-11 Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 Q3-12

EBIT

23%

6%

79.8

174.6

(20.00)

20.00

60.00

100.00

140.00

180.00

Q1-10 Q2-10 Q3-10 Q4-10 Q1-11 Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 Q3-12

Revenues

23.9

64.6

(20.00)

-

20.00

40.00

60.00

80.00

Q1-10 Q2-10 Q3-10 Q4-10 Q1-11 Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 Q3-12

EBITDA 37%

30% 35.6

74.3

(20.00)

-

20.00

40.00

60.00

80.00

Q1-10 Q2-10 Q3-10 Q4-10 Q1-11 Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 Q3-12

Cash from operations

www.polarcus.com 10

Fleet Utilization 87% YTD

Including Vyacheslav Tikhonov

55%

81% 79%

89% 85%

73%

53%

73% 77%

81% 86%

30%

8% 3%

8%

6%

35%

9% 17%

10% 13%

25%

13% 16% 18%

7% 7% 10% 10%

4% 1% 2% 3% 5% 3% 2% 4% 1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q1-10 Q2-10 Q3-10 Q4-10 Q1-11 Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 Q3-12

Yard stay (including shakedown)

Transit

Multi-Client Seismic Contract

Exclusive Seismic Contract

www.polarcus.com 11

Funding overview

• Total funding of USD 1.5 B

• Continued de-levering by repayment of

USD 14 million in principal debt in Q3

2012

• Gross debt USD 845 million by end Q3

2012

• USD 10 million guarantee facility for

bid and performance bonds secured

547

160

80

70

180

40

410

0

200

400

600

800

1000

1200

1400

1600

1

Bank loan

Unsecured Bonds

Sale lease back

Vendor financing

Bonds

Convertibles

Equity

www.polarcus.com 12

0

20

40

60

80

100

120

140

160

180

200

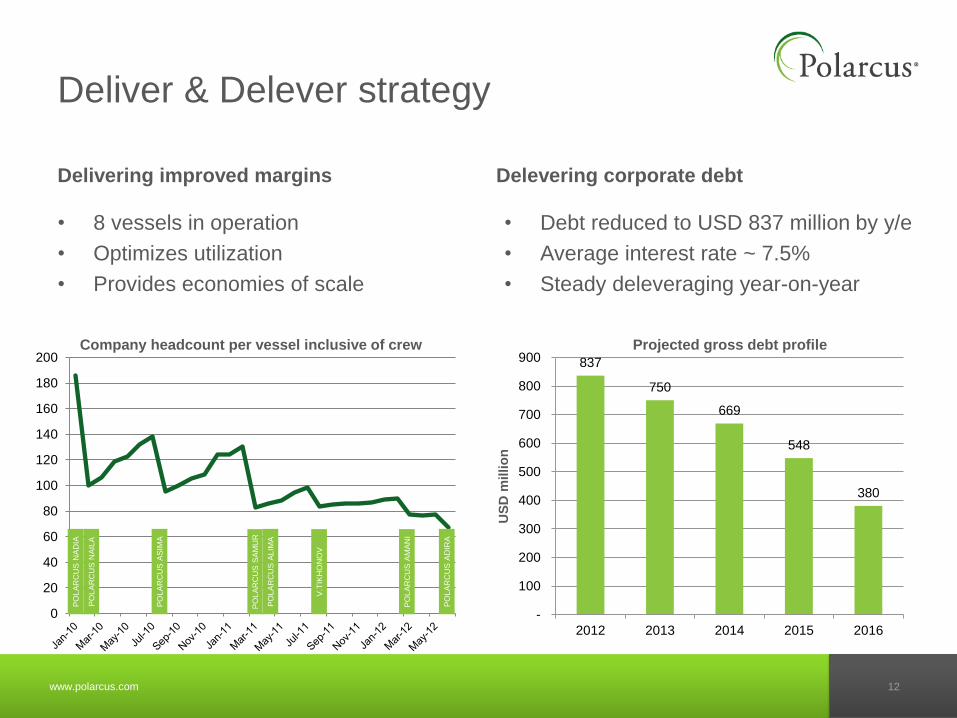

Deliver & Delever strategy

Delivering improved margins

• 8 vessels in operation

• Optimizes utilization

• Provides economies of scale

Delevering corporate debt

837

750

669

548

380

-

100

200

300

400

500

600

700

800

900

2012 2013 2014 2015 2016

US

D m

illio

n

• Debt reduced to USD 837 million by y/e

• Average interest rate ~ 7.5%

• Steady deleveraging year-on-year

PO

LA

RC

US

NA

DIA

PO

LA

RC

US

NA

ILA

PO

LA

RC

US

AS

IMA

PO

LA

RC

US

SA

MU

R

V.T

IKH

ON

OV

PO

LA

RC

US

AM

AN

I

PO

LA

RC

US

AD

IRA

PO

LA

RC

US

AL

IMA

Projected gross debt profile Company headcount per vessel inclusive of crew

www.polarcus.com 13

Polarcus Share

• Listed on the Oslo Stock

Exchange

• Market Cap ~500 MUSD

• High liquidity in the shares

• ~2500 shareholders

• Management and BoD

represents 21%

Shareholder Share %

ZICKERMAN HOLDING LT 40,571,476 8.00

DRYDOCKS WORLD LLC 37,500,000 7.39

ZICKERMAN GROUP LTD 22,948,081 4.52

VARMA MUTUAL PENSION 19,648,025 3.87

BANK OF AMERICA MERR 17,384,469 3.43

BARCLAYS CAPITAL SEC 13,225,166 2.61

MORGAN STANLEY & CO 13,134,609 2.59

VERDIPAPIRFONDET DNB 9,991,137 1.97

JO HAMBRO CAP MGT UM 9,338,596 1.84

AWILCO INVEST AS 8,450,000 1.67

CREDIT SUISSE SECURI 7,839,325 1.55

SKANDINAVISKA ENSKIL 7,631,938 1.50

BANK OF NEW YORK MEL 7,076,565 1.40

JP MORGAN CLEARING C 7,041,571 1.39

EUROCLEAR BANK S.A./ 7,005,782 1.38

VERDIPAPIRFONDET DEL 5,564,917 1.10

CLEARSTREAM BANKING 5,327,371 1.05

BANK OF NEW YORK MEL 5,212,618 1.03

CREDIT SUISSE SECURI 4,733,702 0.93

STATE STREET BANK & 4,521,365 0.89

Top 20 Shareholders 254,146,713 50.11%

Other shareholders 253,049,466 49.89%

Total 507,196,179 100%

Top 20 Shareholders (as per 31 Oct)

www.polarcus.com 14

Agenda

Highlights

Financials

Operations & Market update

Summary & Q&A

Appendices

1

2

3

4

5

www.polarcus.com 15

Global player specializing in Arctic & ESSA

Current vessel locations

Completed surveys

Arctic and ESSA (Environmentally Sensitive Sea Areas)

Polarcus Samur

Polarcus Naila

Polarcus Nadia

Polarcus Asima Polarcus Alima

Polarcus Amani

Polarcus Selma*

Polarcus Adira

Note: *Vyacheslav Tikhonov (Polarcus Selma) on charter to Sovcomflot

Sources:

www.imo.org

www.biosecurity.govt.nz

>25% project awards in Arctic / ESSA

www.polarcus.com 16

2012 Arctic program: a resounding success

• ~10 000 sq km acquired in ice

infested waters

• Two vessels in First Pass™ mode

• Low technical downtime

• Ice management executed to plan

to optimise acquisition window

www.polarcus.com 17

Dynamic ice management critical due to the high concentration of icebergs

Extensive support vessel fleet supporting logistics & ice management

Ice-1A Support Fleet

Ice management key to Arctic success

www.polarcus.com 18

Arctic strategy pays off

• Ice Class 1A vessels: 8 vessel months in Baffin Bay

• Optimum 3D spreads providing top tier performance

• Importance of Arctic vessel technology acknowledged

• Emissions reduction in focus by clients

• Triple E energy efficiency initiative across fleet

• Marine mammal mitigations in place across fleet

• Flexible geophysical solution to geological challenges

• Ice management capabilities demonstrated

• Arctic / remote logistics executed safely & efficiently

RIGHTSIZE

RIGHTDESIGN

RIGHTPLAN

www.polarcus.com 19

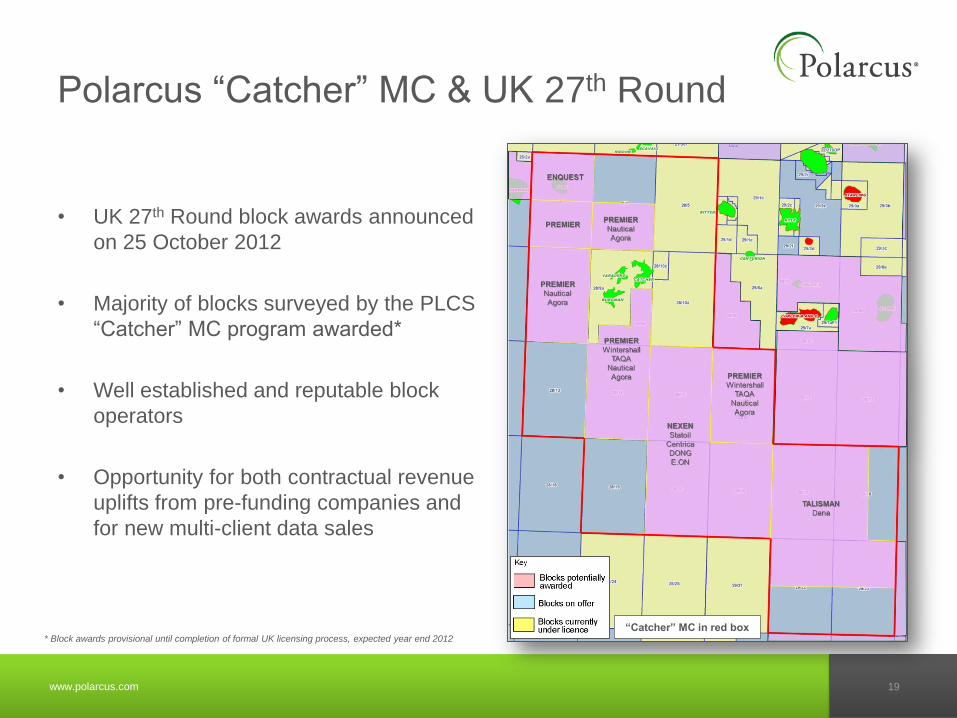

Polarcus “Catcher” MC & UK 27th Round

• UK 27th Round block awards announced

on 25 October 2012

• Majority of blocks surveyed by the PLCS

“Catcher” MC program awarded*

• Well established and reputable block

operators

• Opportunity for both contractual revenue

uplifts from pre-funding companies and

for new multi-client data sales

“Catcher” MC in red box * Block awards provisional until completion of formal UK licensing process, expected year end 2012

www.polarcus.com 20

Global 3D Seismic fleet capacity

46%

3% 25%

10%

16%

1 - 5 years

6 - 10 years

11 - 15 years

16 - 19 years

20+ years

Fleet age profile 2012

Global 3D 6+ streamer fleet

• Estimated seismic fleet growth 2013

– 2015 net 2% Year on Year

assuming 4 vessels being stacked

• Lead time for new build capacity

traditionally between 24 – 36 months

• Further fleet retirement expected

excludes COSL (3 vessels) & Sinopec (1 vessel)

59 60 62 63 64

0

10

20

30

40

50

60

70

2011 2012 2013 2014 2015

www.polarcus.com 21

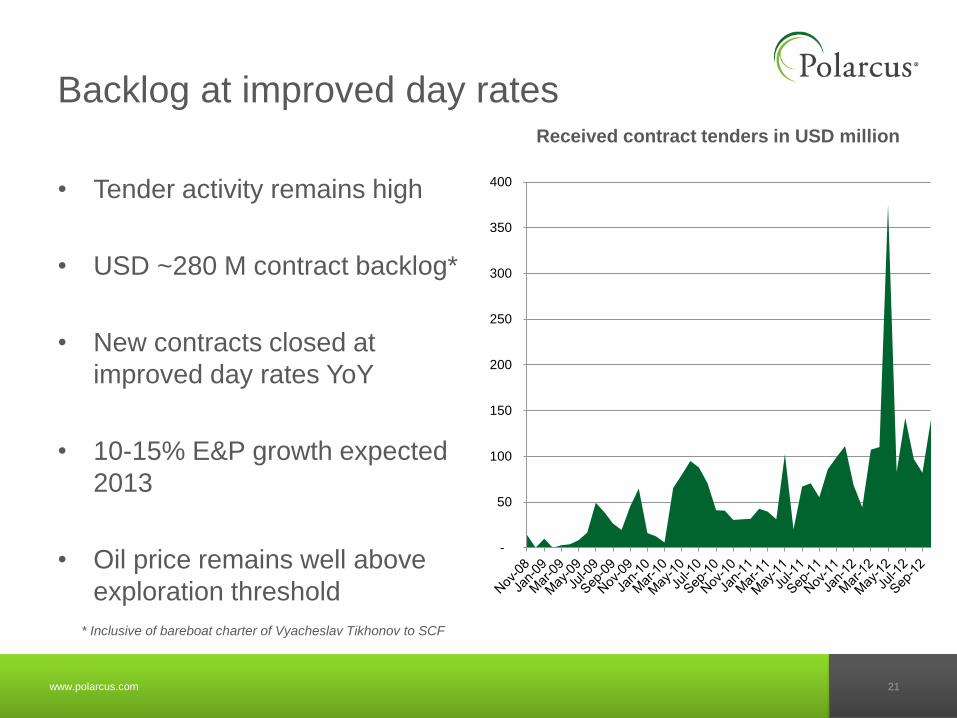

Backlog at improved day rates

• Tender activity remains high

• USD ~280 M contract backlog*

• New contracts closed at

improved day rates YoY

• 10-15% E&P growth expected

2013

• Oil price remains well above

exploration threshold

* Inclusive of bareboat charter of Vyacheslav Tikhonov to SCF

Received contract tenders in USD million

-

50

100

150

200

250

300

350

400

www.polarcus.com 22

Agenda

Highlights

Financials

Operations & Market update

Summary & Q&A

Appendices

1

2

3

4

5

www.polarcus.com 23

RIGHTSIZE, RIGHTDESIGN, RIGHTPLAN

• Delivering & delevering

• Successful execution in true Arctic environment

• Polarcus strategy continues to pay off

www.polarcus.com 24

Agenda

Highlights

Financials

Operations & Market update

Summary & Q&A

Appendices

1

2

4

5

3

www.polarcus.com 25

Polarcus in brief

• 8 high-end 3D seismic vessels representing 12% market share

• Youngest most uniform fleet in industry

• 500+ professionals and global presence

• State of the art technology with complete broadband solution

• Specialized Arctic and low environmental impact offerings

• Clear strategy for delivery and deleveraging

• Listed on Oslo Børs Main List

2008 2009 2010

Polarcus

launched

2008

2012 2011

Polarcus Asima in operation offshore west Greenland

www.polarcus.com 26

Polarcus Fleet

• 8 new and uniform 3D seismic

vessels in operation

• Polarcus Amani and Polarcus Adira

delivered on time and on budget

• Reduced noise and vibrations

• Ice class 1A

• Improved transit performance

POLARCUS NADIA &

POLARCUS NAILA

12 Streamer 3D vessel

POLARCUS ASIMA &

POLARCUS ALIMA

12 Streamer 3D vessel

POLARCUS SAMUR &

Vyacheslav Tikhonov

8 Streamer 3D vessel

POLARCUS AMANI &

POLARCUS ADIRA

12-14 Streamer 3D vessel

www.polarcus.com 27

First

Pass

Wide tow

High

Density

3D

Base-

line 4D

High

density

4D

4D

Monitor

Multi-

vessel

3D

Multi-

vessel

4D

Monitor

Arctic

Operations

Multi

Azimuth

Vessel +

Equipment Personnel +

Procedures

Acquisition

Portfolio

Broadband Solutions

Polarcus offering

www.polarcus.com 28

Awards through RIGHTDESIGN

ICE-1A or 1A* Class1

Safe Arctic operations 1 POLARCUS ASIMA, ALIMA,

SAMUR, SELMA, AMANI & ADIRA

ULSTEIN X-BOW®

Improved efficiency and

reduced emissions Fuel: MGO with low

sulfur content

BWM-T 2

Removal of invasive species from ballast water 2 POLARCUS ASIMA, ALIMA, SAMUR, SELMA, AMANI & ADIRA

IMO Green Passport

Multiple main engines and independent

propellers in case of failure

DYNPOS-AUTR

Systems redundancy

with DP2

CLEAN DESIGN

High specification

exhaust catalysts

Double hull – no oil contact

with outer skin

Bilge water cleaning system to

reduce contaminants to <5ppm

Triple – E™

Environmental &

Energy Efficiency Sentinel® solid streamers

www.polarcus.com 29

Debt overview

Debt Security Size Balance

30 Sep 2012 Tenure Maturity Interest

Vendor Financing Seismic Equipment USD 70m USD 13m 2.5 years Jun-13 8%

Convertible Bond Unsecured USD 35m USD 35m 5 years Jul-13 8.50%

Unsecured Bond Unsecured NOK 240m NOK 240m 3 years Nov-14 14%

Senior secured bond 2nd priority

5 vessel fleet USD 80m USD 80m 5 years Oct-15 12.50%

Senior Secured Convertible bond Selma USD 125m USD 125m 5 years Apr-16 2.88%

Sale leaseback Nadia & Naila USD 180m USD 167m 10 years Sep-19 ~12%

Fleet bank facility

Tranche 1 Asima USD 80m USD 67m 12 years Aug-22 6.20%

Fleet bank facility

Tranche 2 Alima USD 55m USD 48m 12 years Mar-23 5.10%

Fleet bank facility

Tranche 3 Amani USD 114m USD 109m 12 years Mar-24 5.60%

Fleet bank facility

Tranche 4 Adira USD 114m USD 114m 12 years Jun-24 5.60%

Fleet bank facility

Tranche 5 Samur USD 47m USD 47m 12 years Jun-24 5.40%

www.polarcus.com 30