Platinum Group Metals Ltd. (An Exploration and...

43

Platinum Group Metals Ltd. (An Exploration and Development Stage Company) Condensed Consolidated Interim Financial Statements (unaudited) For the three months ended November 30, 2014 Filed: January 13, 2015

Transcript of Platinum Group Metals Ltd. (An Exploration and...

Platinum Group Metals Ltd. (An Exploration and Development Stage Company)

Condensed Consolidated Interim Financial Statements (unaudited) For the three months ended November 30, 2014

Filed: January 13, 2015

PLATINUM GROUP METALS LTD. (An exploration and development stage company) Condensed Consolidated Interim Statements of Financial Position (Unaudited – in thousands of Canadian dollars)

See accompanying notes to the consolidated financial statements 2

November 30, 2014 August 31, 2014

ASSETS

Current Cash and cash equivalents $ 65,208 $ 108,150 Amounts receivable (Note 3) 7,958 13,848 Prepaid expenses 780 714

Total current assets 73,946 122,712 Other assets (Note 1) - 4,206 Performance bonds (Note 4 (ii)) 5,373 5,101 Exploration and evaluation assets (Note 5) 34,711 30,612 Property, plant and equipment (Note 4) 431,039 387,608

Total assets $ 545,069 $ 550,239

LIABILITIES

Current Accounts payable and accrued liabilities $ 26,907 $ 28,576

Total current liabilities 26,907 28,576 Deferred income taxes 11,720 11,585 Asset retirement obligation 1,692 1,636

Total liabilities 40,319 41,797

SHAREHOLDERS’ EQUITY Share capital (Note 6) 589,782 590,774 Contributed surplus 22,385 22,374 Accumulated other comprehensive loss (63,494) (63,980) Deficit (119,482) (120,484)

Total shareholders’ equity attributable to shareholders of Platinum Group Metals Ltd. 429,191 428,684

Non-controlling interest (Note 4 (i)) 75,559 79,758

Total shareholders’ equity 504,750 508,442

Total liabilities and shareholders’ equity $ 545,069 $ 550,239

CONTINGENCIES AND COMMITMENTS (NOTE 8) SUBSEQUENT EVENTS (NOTE 11) Approved by the Board of Directors and authorized for issue on January 13, 2015

“Iain McLean”

Iain McLean, Director

“Eric Carlson”

Eric Carlson, Director

PLATINUM GROUP METALS LTD. (An exploration and development stage company) Condensed Consolidated Interim Statements of Income (Loss) and Comprehensive Income (Loss) (Unaudited – in thousands of Canadian dollars, except share data)

See accompanying notes to the consolidated financial statements 3

For the three months ended November 30, 2014 2013

EXPENSES

General and administrative $ 1,803 $ 1,399 Foreign exchange (gain) loss (947) (887) Stock compensation expense (Note 6(c)) 11 - Termination and finance fees (Note 1) 1,766 - Write-down of other assets (Note 1) 4,206 -

(6,839) (512)

Finance income 1,217 976

Income (Loss) for the period (5,622) 464 Items that may be subsequently reclassified to net loss Exchange differences in translating foreign operations 2,911 2,887

Comprehensive income (loss) for the period $ (2,711) $ 3,351

Income (Loss) attributable to: Shareholders of Platinum Group Metals Ltd. (5,708) 447 Non-controlling interests 86 17

$ (5,622) $ 464

Comprehensive income (loss) attributable to: Shareholders of Platinum Group Metals Ltd. (3,902) 3,208 Non-controlling interests 1,191 143

$ (2,711) $ 3,351

Basic and diluted income (loss) per common share $ (0.01) $ 0.00

Weighted average number of common shares outstanding: Basic and diluted 551,312,842 402,759,542

PLATINUM GROUP METALS LTD. (An exploration and development stage company)

Condensed Consolidated Interim Statements of Changes in Equity (Unaudited – in thousands of Canadian dollars, except share data)

See accompanying notes to the consolidated financial statements 4

# of Common Shares

Share Capital

Contributed Surplus

Accumulated Other

Comprehensive Income (loss) Deficit

Attributable to Shareholders of the Parent

Company

Non-Controlling

Interest Total

Balance, August 31, 2013 402,759,542 $ 425,435 $ 18,593 $ (61,481) $ (85,349) $ 297,198 $ 54,410 $ 351,608

Share issue costs - (119) - - - (119) - (119)

Funding of non-controlling interest - - - - (5,029) (5,029) 5,029 -

Foreign currency translation - - - 2,761 - 2,761 126 2,887

Net income for the period - - - - 447 447 17 464

Balance, November 30, 2013 402,759,542 $ 425,316 $ 18,593 $ (58,720) $ (89,931) $ 295,258 $ 59,582 $ 354,840

Stock based compensation - - 3,803 - - 3,803 - 3,803

Share issuance – financing 148,500,000 175,230 - - - 175,230 - 175,230

Share issuance costs - (9,849) - - - (9,849) - (9,849)

Issued upon the exercise of options 53,300 77 (22) - - 55 - 55

Transactions with non-controlling interest (Note 4) - - - (1,387) (19,668) (21,055) 21,055 -

Foreign currency translation adjustment - - - (3,873) - (3,873) (841) (4,714)

Net loss for the period - - - - (10,885) (10,885) (38) (10,923)

Balance, August 31, 2014 551,312,842 590,774 22,374 (63,980) (120,484) 428,684 79,758 508,442

Stock based compensation - - 11 - - 11 - 11

Share issuance costs1 - (992) - - - (992) - (992)

Transactions with non-controlling interest (Note 4) - - - (1,320) 6,710 5,390 (5,390) -

Foreign currency translation adjustment - - - 1,806 - 1,806 1,105 2,911

Net loss for the period - - - - (5,708) (5,708) 86 (5,622)

Balance, November 30, 2014 551,312,842 $ 589,782 $ 22,385 $ (63,494) $ (119,482) $ 429,191 $ 75,559 $ 504,750

1Costs incurred relating to December 31, 2014 equity financing (see Note 11 Subsequent Events)

PLATINUM GROUP METALS LTD. (An exploration and development stage company) Condensed Consolidated Interim Statements of Cash Flows (Unaudited – in thousands of Canadian dollars)

See accompanying notes to the consolidated financial statements 5

For the three months ended November 30, 2014 2013

OPERATING ACTIVITIES (Loss) Income for the period $ (5,622) $ 464 Add items not affecting cash: Depreciation 116 116 Foreign exchange gain (39) (852) Stock compensation expense 11 - Write-down of other assets 4,206 - Net change in non-cash working capital (Note 9) (742) 50

(2,070) (222)

INVESTING ACTIVITIES Acquisition of property, plant and equipment (41,726) (43,777)

Exploration expenditures, net of recoveries (5,000) (1,446) South African VAT 5,363 3,525 Performance bonds (201) (1,125)

Restricted cash - 10,272

(41,564) (32,551)

Net decrease in cash and cash equivalents (43,634) (32,773) Effect of foreign exchange on cash and cash equivalents 692 911 Cash and cash equivalents, beginning of period 108,150 111,784

Cash and cash equivalents, end of period $ 65,208 $ 79,922

Platinum Group Metals Ltd.

(An exploration and development stage company) Notes to the condensed consolidated interim financial statements

For the three months ended November 30, 2014 (in thousands of Canadian dollars unless otherwise noted)

6

1. NATURE OF OPERATIONS AND LIQUIDITY Platinum Group Metals Ltd. (the “Company”) is a British Columbia, Canada, company amalgamated on February 18, 2002. The Company’s shares are publicly listed on the Toronto Stock Exchange in Canada and the NYSE MKT LLC in the United States. The Company’s address is Suite 788-550 Burrard Street, Vancouver, British Columbia, V6C 2B5. The Company is an exploration and development company conducting work on mineral properties it has staked or acquired by way of option agreements in the Republic of South Africa and Canada. The Company is currently developing the Project 1 platinum mine located on the Bushveld Complex in the Republic of South Africa (“Project 1”). Project 1 is owned through the operating company Maseve Investments 11 (Pty.) Ltd. (“Maseve”), in which the Company held a 82.9% working interest as of November 30, 2014 and the Company’s Black Economic Empowerment (“BEE”) partner, Africa Wide Mineral Prospecting and Exploration (Pty) Ltd. (“Africa Wide”), a wholly owned subsidiary of Wesizwe Platinum Ltd., owned 17.1%. A formal mining right was granted for Project 1 on April 4, 2012 by the Government of South Africa (the “Mining Right”). The Company is also advancing the Waterberg Joint Venture Project and Waterberg Extension Project with a pre-feasability study scheduled for Q2 of calendar 2015. These financial statements include the accounts of the Company and its subsidiaries. The Company’s subsidiaries are as follows:

Place of incorporation and operation

Proportion of ownership interest and voting power

held

Name of subsidiary Principal activity November 30,

2014 August 31,

2014

Platinum Group Metals (RSA) (Pty) Ltd. Exploration South Africa 100% 100% Maseve Investments 11 (Pty) Ltd Mining South Africa 82.9%1 78.7%1

Wesplats Holdings (Pty) Limited Holding company South Africa 100% 100% Platinum Group Metals (Barbados) Ltd. Holding company Barbados 100% 100% Mnombo Wethu Consultants (Pty) Limited. Exploration South Africa 49.9% 49.9%

1See Note 4(i) “Ownership of Project 1”

On December 6, 2012, the Company announced that a syndicate of lead arrangers had obtained credit committee approval for a US$260 million project loan facility to Maseve for the construction of the Project 1 platinum mine. The Company later entered into a new mandate letter on November 8, 2013 with a modified syndicate of lead arrangers for a US$195 million project loan to partially fund construction on Project 1. On October 31, 2014, the Company determined not to proceed with the proposed project loan facility. On November 3, 2014 the Company announced its intention to offer 150,000 units consisting of US$150,000,000 aggregate principal amount of senior notes due 2021 and the right for noteholders to receive an aggregate of 55,200,000 common share purchase warrants. On December 9, 2014 this unit offering was discontinued due to market conditions. Deferred finance costs previously classifed as other current assets, amounting to $4.2 million that were associated with the proposed loan facility were written off in the current period. Termination and finance fees related to the proposed loan facility and the unit offering of $1.8 million were incurred in the current period as well. On December 9, 2014 the Company announced that it had entered into a term sheet for a senior secured operating loan facility of up to US$40 million. The Facility is planned to be available at the delivery and sale of first commercial concentrate from the WBJV Project 1 targeted for the fourth quarter of calendar

Platinum Group Metals Ltd.

(An exploration and development stage company) Notes to the condensed consolidated interim financial statements

For the three months ended November 30, 2014

(in thousands of Canadian dollars unless otherwise noted)

7

2015. The loan facility is subject to certain terms and conditions as well as the implementation of a definitive credit agreement by January 30, 2015.

On December 9, 2014, the Company announced a bought deal financing for 214.8 million common shares of the Company at a price of US$0.53 ($0.61) per share resulting in gross proceeds of US$113.8 million ($132 million). The offering closed December 31, 2014 with net proceeds to the Company after fees, commissions and costs of approximately US$106 million ($123 million).

2. BASIS OF PRESENTATION AND SIGNIFICANT ACCOUNTING POLICIES

These unaudited condensed consolidated interim financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) and International Financial Reporting Interpretations Committee (“IFRIC”) interpretations as issued by the International Accounting Standards Board (“IASB”) applicable to the preparation of interim financial statements, including IAS 34, Interim Financial Reporting. The consolidated financial statements have been prepared under the historical cost convention. These unaudited condensed consolidated interim financial statements do not include all the information and note disclosures required by IFRS for annual financial statements and therefore should be read in conjunction with the Company’s audited consolidated financial statements for the year ended August 31, 2014. The consolidated financial statements are presented in Canadian dollars.

These interim financial statements follow the same significant accounting principles as those outlined in the notes to the annual financial statements for the year ended August 31, 2014 with the following standards adopted in the current fiscal period:

Amendment to IAS 36, Impairment of Assets where the circumstances are reduced in which the reocoverable amount of assets or cash-generateing units is required to be disclosed and to introduce the explicit requirement to disclose the discount rate used in determining impairment.

IFRS 8 Operating Segments where disclosures of the judgements made by management in aggregating operating segments and a reconciliation of segment assts to total assets when segment assets are reported.

These new standards adopted have not resulted in any material change to the results and financial position of the Company. A number of new standards, amendments to standards and interpretations applicable to the Company are not yet effective for the current accounting period and have not been applied in preparing these consolidated financial statements. These include:

IFRS 15 Revenue from contracts with customers (effective for annual period commencing January 1, 2017) which is intended to establish a new control-based revenue recognition model and change the basis for deciding whether revenue is to be recognized over time or at a point in time.

IFRS 9 Financial Instruments: Classification and Measurement (effective for annual periods commencing on or after January 1, 2018) which applies to classification and measurement of financial assets and liabilities as defined in IAS 39.

The Company is currently considering the possible effect of the new and revised standards which will be effective to the Company’s consolidated financial statements in the future.

Platinum Group Metals Ltd.

(An exploration and development stage company) Notes to the condensed consolidated interim financial statements

For the three months ended November 30, 2014

(in thousands of Canadian dollars unless otherwise noted)

8

3. AMOUNTS RECEIVABLE

November 30, 2014 August 31, 2014

South African VAT $ 6,439 $ 11,820 Foreign jurisdiction tax payable to be recovered 744 744 Due from JOGMEC (Note 5) 222 479 Other receivables 178 382 Interest 55 93 Canadian sales tax 69 84 Due from related parties (Note 7) 251 246

$ 7,958 $ 13,848

Platinum Group Metals Ltd.

(An exploration and development stage company) Notes to the condensed consolidated interim financial statements

For the three months ended November 30, 2014 (in thousands of Canadian dollars unless otherwise noted)

9

4. PROPERTY, PLANT AND EQUIPMENT

Development

assets Construction

work-in-progress Land Buildings Office

Equipment Mining

Equipment Total

COST

Balance, August 31, 2013 $ 161,097 $ 29,400 $ 12,924 $ 3,442 $ 1,713 $ 27,746 $ 236,322

Additions 92,341 57,649 - 1,616 323 11,326 163,255

Foreign exchange movement (1,518) (286) (125) (33) (7) (270) (2,239)

Balance, August 31, 2014 251,920 86,763 12,799 5,025 2,029 38,802 397,338

Additions 21,267 18,640 - - 109 148 40,164

Foreign exchange movement 3,372 1,192 175 69 15 533 5,356

Balance, November 30, 2014 $ 276,559 $ 106,595 $ 12,974 $ 5,094 $ 2,153 $ 39,483 $ 442,858

ACCUMULATED DEPRECIATION

Balance, August 31, 2013 $ - $ - $ - $ 374 $ 822 $ 2,409 $ 3,605

Additions - - - 233 240 5,683 6,156

Foreign exchange movement - - - (4) (4) (23) (31)

Balance, August 31, 2014 - - - 603 1,058 8,069 9,730

Additions - - - 88 76 1,799 1,963

Foreign exchange movement - - - 8 7 111 126

Balance, November 30, 2014 $ - $ - $ - $ 699 $ 1,141 $ 9,979 $ 11,819

Net book value, August 31, 2014 $ 251,920 $ 86,763 $ 12,799 $ 4,422 $ 971 $ 30,733 $ 387,608

Net book value, November 30, 2014 $ 276,559 $ 106,595 $ 12,974 $ 4,395 $ 1,012 $ 29,504 $ 431,039

Platinum Group Metals Ltd.

(An exploration and development stage company) Notes to the condensed consolidated interim financial statements

For the three months ended November 30, 2014 (in thousands of Canadian dollars unless otherwise noted)

10

Project 1

Project 1 is located in the Western Bushveld region of South Africa and is currently in development. Project 1 costs are classified as development assets and construction in progress in Property, Plant and Equipment.

i. Ownership of Project 1

Under the terms of a consolidation transaction completed on April 22, 2010, the Company acquired a 74% interest in Projects 1 and 3 of the former Western Bushveld Joint Venture through its holdings in Maseve, while the remaining 26% was acquired by Africa Wide. In consideration for the Company increasing its holdings to 74%, the Company paid subscription funds into Maseve, creating an escrow fund for application towards Africa Wide’s 26% share of capital requirements. These funds were classified as restricted cash and were fully depleted in the previous year. No work was carried out on Project 3 during the period ended November 30, 2014. The Company consolidated the results of Maseve from the effective date of the reorganization. The portion of Maseve not owned by the Company, calculated at $70,943 at November 30, 2014 ($75,741 – August 31, 2014), is accounted for as a non-controlling interest. On October 18, 2013, Africa Wide informed the Company that it would not be funding its share of a project budget and cash call unanimously approved by the board of directors of Maseve. On March 3, 2014, Africa Wide informed the Company that it would not be funding its approximately US$21.52 million share of a second cash call. As a result of Africa Wide’s October 18, 2013 funding failure, the Company and Africa Wide entered into arbitration proceedings to determine Africa Wide’s diluted interest in Maseve, and therefore Project 1 and Project 3, in accordance with the terms of the Maseve Shareholders Agreement. On August 20, 2014, an arbitrator ruled in the Company’s favour on all matters and determined that Africa Wide’s interest in Maseve would first be reduced to approximately 21.28%. As a result of the second missed cash call, Africa Wide’s interest in Maseve was further diluted in the current period to approximately a 17.1% holding. Accordingly the Company held 82.9% of Maseve at November 30, 2014. Legislation and regulations in South Africa require a 26% equity interest by a BEE entity in order to maintain the Mining Right in good standing. Because Africa Wide is the Company’s BEE partner for Project 1, the Company advised the Department of Mineral Resources (the “DMR”) on October 19, 2013 of Africa Wide’s decision to not fund the cash call and the associated dilution implications. On October 24, 2013, the DMR provided the Company with a letter stating that it will apply the provisions of the Mineral and Petroleum Resources Development Act, 28 of 2002 (the “MPRDA”) to any administrative processes or decisions to be conducted or taken within a reasonable time and in accordance with the principles of lawfulness, reasonableness and procedural fairness in giving the Company the opportunity to remedy the effect of Africa Wide’s dilution. The Company is currently working on alternatives to sell the diluted percentage interest in Maseve previously held by Africa Wide to an alternative, qualified BEE company, or to otherwise bring qualified BEE investment into Maseve if and when instructed by the DMR. The Company may also undertake a transaction unilaterally. The Company is presently considering Mnombo as the BEE entity for such a transaction. The Company currently owns 49.9% of the issued and outstanding shares of Mnombo. Mnombo acts as the Company’s BEE partner in respect of the Waterberg Projects. Under the terms of the Maseve Shareholders Agreement, if Maseve is instructed by the DMR to increase its BEE ownership, any agreed costs or dilution of interests shall be borne equally by the Company and Africa Wide, notwithstanding that Africa Wide now holds only approximately 17.1% of the equity in Maseve.

Platinum Group Metals Ltd.

(An exploration and development stage company) Notes to the condensed consolidated interim financial statements

For the three months ended November 30, 2014

(in thousands of Canadian dollars unless otherwise noted)

11

ii. Other financial information – Project 1

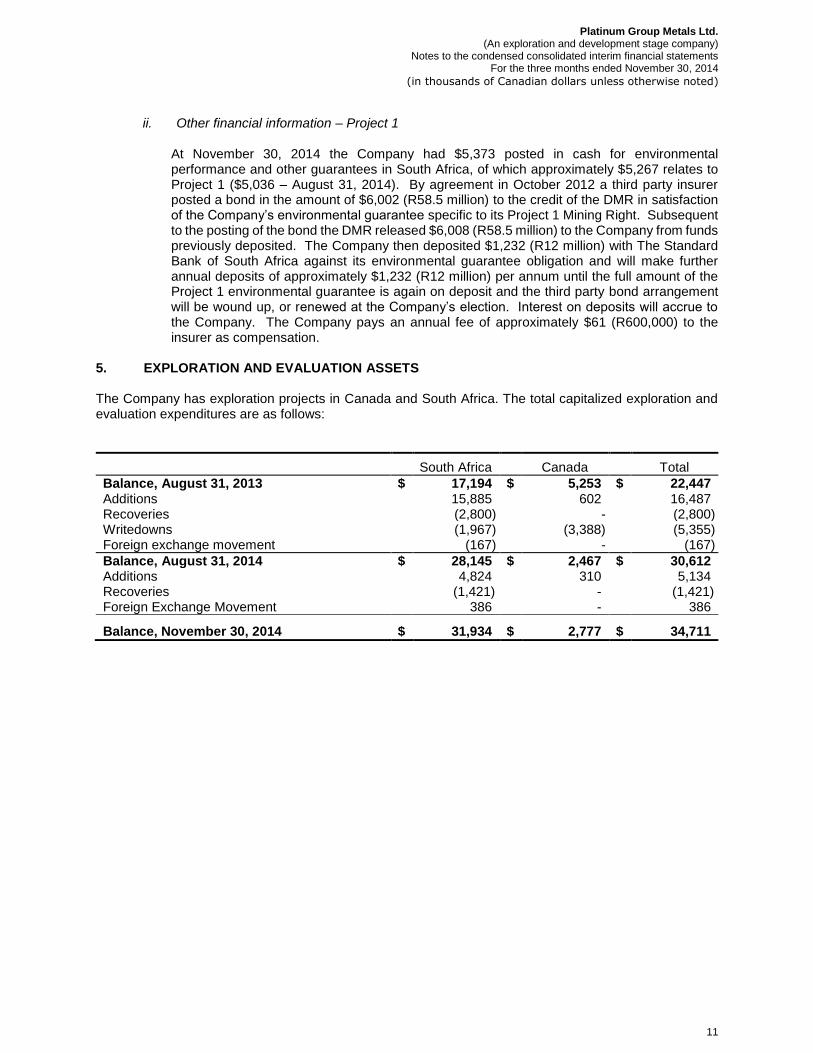

At November 30, 2014 the Company had $5,373 posted in cash for environmental performance and other guarantees in South Africa, of which approximately $5,267 relates to Project 1 ($5,036 – August 31, 2014). By agreement in October 2012 a third party insurer posted a bond in the amount of $6,002 (R58.5 million) to the credit of the DMR in satisfaction of the Company’s environmental guarantee specific to its Project 1 Mining Right. Subsequent to the posting of the bond the DMR released $6,008 (R58.5 million) to the Company from funds previously deposited. The Company then deposited $1,232 (R12 million) with The Standard Bank of South Africa against its environmental guarantee obligation and will make further annual deposits of approximately $1,232 (R12 million) per annum until the full amount of the Project 1 environmental guarantee is again on deposit and the third party bond arrangement will be wound up, or renewed at the Company’s election. Interest on deposits will accrue to the Company. The Company pays an annual fee of approximately $61 (R600,000) to the insurer as compensation.

5. EXPLORATION AND EVALUATION ASSETS The Company has exploration projects in Canada and South Africa. The total capitalized exploration and evaluation expenditures are as follows:

South Africa Canada Total

Balance, August 31, 2013 $ 17,194 $ 5,253 $ 22,447 Additions 15,885 602 16,487 Recoveries (2,800) - (2,800) Writedowns (1,967) (3,388) (5,355) Foreign exchange movement (167) - (167)

Balance, August 31, 2014 $ 28,145 $ 2,467 $ 30,612 Additions 4,824 310 5,134 Recoveries (1,421) - (1,421) Foreign Exchange Movement 386 - 386

Balance, November 30, 2014 $ 31,934 $ 2,777 $ 34,711

Platinum Group Metals Ltd.

(An exploration and development stage company) Notes to the condensed consolidated interim financial statements

For the three months ended November 30, 2014

(in thousands of Canadian dollars unless otherwise noted)

12

REPUBLIC OF SOUTH AFRICA

November 30, 2014 August 31, 2014

Project 3 – see Note 4(i) $ 3,204 $ 3,161 Waterberg JV Acquisition costs 29 21 Exploration and evaluation costs 32,357 27,811 Recoveries (13,136) (11,557)

19,250 16,275

Waterberg Extension Acquisition costs 27 22 Exploration and evaluation costs 9,363 8,653

9,390 8,675

War Springs Acquisition costs - 128 Exploration and evaluation costs - 3,377 Recoveries - (2,104) Writedown - (1,401)

- -

Tweespalk Acquisition costs - 73 Exploration and evaluation costs - 634 Recoveries - (157) Writedown - (550)

- -

Other Acquisition costs 8 10 Exploration and evaluation costs 1,090 1,029 Recoveries (1,008) (1,005)

90 34

Total South Africa Exploration $ 31,934 $ 28,145

Waterberg JV Project

The Waterberg JV Project is comprised of a contiguous granted prospecting right area of approximately 255 km2 located on the North Limb of the Bushveld Complex, approximately 70 kilometers north of the town of Mokopane (formerly Potgietersrus). Platinum Group Metals (RSA) (Pty) Ltd. (“PTM RSA”) applied for the original 137 km2 prospecting right for the Waterberg JV Project area in 2009. In September 2009, the DMR granted PTM RSA the prospecting right until September 1, 2012. Application for the renewal of this prospecting right for a further three years has been made and acknowledged by the DMR. Under the MPRDA, the prospecting right remains valid pending the grant of the renewal. The original prospecting right was enlarged by a section 102 legal amendment in January 2013 and two further prospecting rights were granted to PTM RSA for the Waterberg JV Project and were executed on October 2, 2013. These prospecting rights are valid until October 1, 2018 and may each be renewed for a further period of three years thereafter.

In October 2009, PTM RSA, Japan Oil, Gas and Metals National Corporation (“JOGMEC”) and Mnombo entered into an agreement (as amended, the ‘‘JOGMEC Agreement’’) whereby JOGMEC could earn up to a 37% participating interest in the project for an optional work commitment of US$3.2 million over four

Platinum Group Metals Ltd.

(An exploration and development stage company) Notes to the condensed consolidated interim financial statements

For the three months ended November 30, 2014

(in thousands of Canadian dollars unless otherwise noted)

13

years. At the same time, Mnombo could earn a 26% participating interest in exchange for matching JOGMEC’s expenditures on a 26/74 basis (US$1.12 million).

On November 7, 2011 the Company entered into an agreement with Mnombo whereby the Company acquired 49.9% of the issued and outstanding shares of Mnombo in exchange for cash payments totalling R1.2 million and an agreement that the Company would pay for Mnombo's 26% share of costs on the Waterberg Joint Venture until the completion of a feasibility study. When combined with the Company's 37% direct interest pursuant to the JOGMEC Agreement, the 12.974% indirect interest acquired through Mnombo brings the Company's effective interest in the Waterberg JV Project to 49.974%.

In April 2012, JOGMEC completed its US$3.2 million earn-in requirement to earn its 37% interest in the Waterberg JV Project. Following JOGMEC’s earn-in, the Company funded Mnombo’s US$1.12 million share of costs until earn-in phase of the joint venture ended in May 2012. Since then and up to November 30, 2014 an additional US$29.4 million has been spent on the joint venture. The Company has funded the Company and Mnombo’s combined 63% share of this work for a cost of US$18.5 million with the remaining US$10.9 million funded by JOGMEC. As of November 30, 2014, an amount of US$0.194 million is due from JOGMEC against its 37% share of approved joint venture work completed in fiscal 2015.

Waterberg Extension The Waterberg Extension Project comprises contiguous granted and applied-for prospecting rights with a combined area of approximately 864 km2 adjacent and to the north of the Waterberg JV Project. Two of the prospecting rights were executed on October 2, 2013 and each is valid for a period of five years, expiring on October 1, 2018. The third prospecting right was executed on October 23, 2013 and is valid for a period of five years, expiring on October 22, 2018. The Company has made an application under section 102 of the MPRDA to the DMR to increase the size of one of the granted prospecting rights by 44 km2. The Company has the exclusive right to apply for renewals of the prospecting rights for periods not exceeding three years each and the exclusive right to apply for a mining right over these prospecting right areas. Applications for a fourth and a fifth prospecting right covering 331 km2 were accepted for filing with the DMR on February 7, 2012 for a period of five years. These applications, which are not directly on the trend of the primary exploration target, are in process with the DMR. PTM RSA holds the prospecting rights filed with the DMR for the Waterberg Extension Project, and Mnombo is identified as the Company’s BEE partner. The Company holds a direct 74% interest and Mnombo holds a 26% interest in the Waterberg Extension Project, leaving the Company with an 86.974% effective interest by way of the Company’s 49.9% shareholding in Mnombo. The Company and Mnombo are negotiating a formal joint venture agreement to govern the participating rights in and obligations towards the Waterberg Extension Project. The Company is currently carrying Mnombo’s 26% share of ongoing costs on the Waterberg Extension Project. War Springs and Tweespalk On June 3, 2002, the Company acquired an option to earn a 100% interest in the 2,396 hectare War Springs property and the 2,177 hectare Tweespalk property both located in the Northern Limb or Platreef area of the Bushveld Complex, north of Johannesburg. The Company can settle the vendors’ residual interests in these mineral rights at any time for US$690 per hectare. The Company pays annual prospecting fees to the vendors of US$3.25 per hectare. The vendors retain a 1% Net Smelter Return Royalty (“NSR”) on the property, subject to the Company’s right to purchase the NSR at any time for US$1,400. BEE groups Africa Wide and Taung Minerals (Pty) Ltd., a subsidiary of Platmin Limited, have each acquired a 15% interest in the Company’s rights to the War Springs project carried to bankable feasibility. The Company retains a net 70% project interest. Africa Wide also has a 30% participating interest in the Tweespalk property. As no work was carried out on the War Springs or Tweespalk properties during the previous year the Company wrote off all deferred costs related to these properties while continuing to hold them.

Platinum Group Metals Ltd.

(An exploration and development stage company) Notes to the condensed consolidated interim financial statements

For the three months ended November 30, 2014

(in thousands of Canadian dollars unless otherwise noted)

14

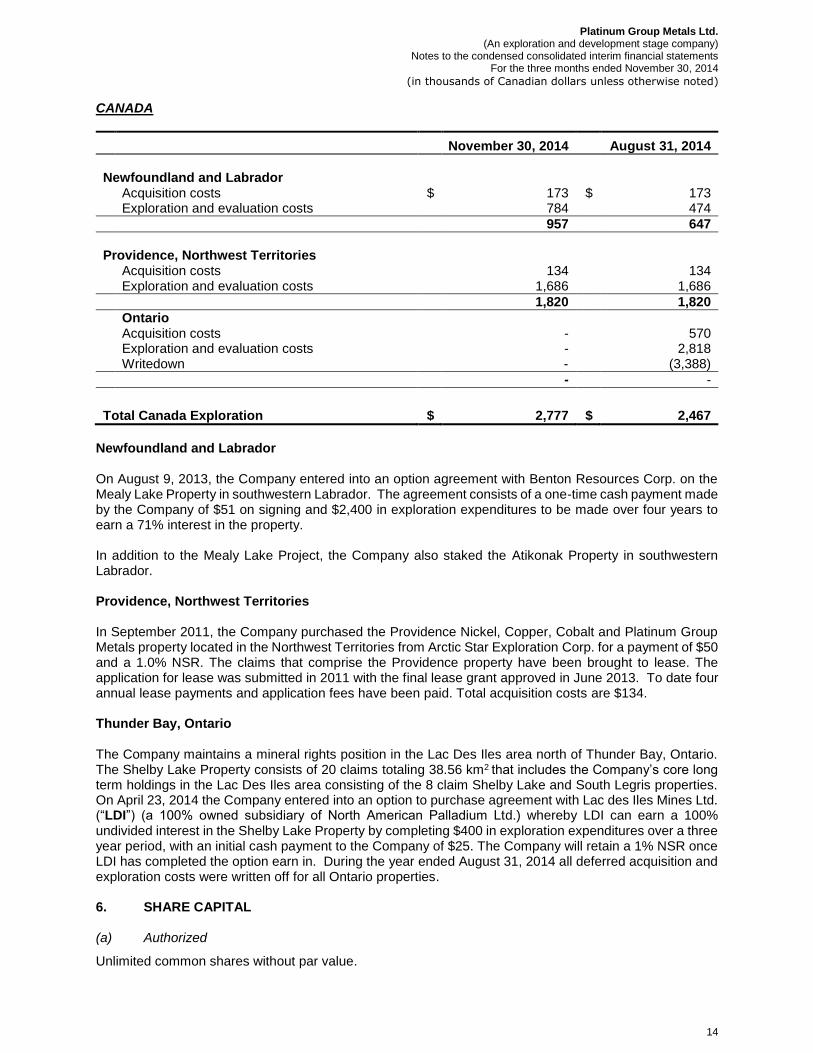

CANADA

November 30, 2014 August 31, 2014

Newfoundland and Labrador Acquisition costs $ 173 $ 173 Exploration and evaluation costs 784 474

957 647

Providence, Northwest Territories Acquisition costs 134 134 Exploration and evaluation costs 1,686 1,686

1,820 1,820

Ontario Acquisition costs - 570 Exploration and evaluation costs - 2,818 Writedown - (3,388)

- -

Total Canada Exploration $ 2,777 $ 2,467

Newfoundland and Labrador On August 9, 2013, the Company entered into an option agreement with Benton Resources Corp. on the Mealy Lake Property in southwestern Labrador. The agreement consists of a one-time cash payment made by the Company of $51 on signing and $2,400 in exploration expenditures to be made over four years to earn a 71% interest in the property. In addition to the Mealy Lake Project, the Company also staked the Atikonak Property in southwestern Labrador. Providence, Northwest Territories

In September 2011, the Company purchased the Providence Nickel, Copper, Cobalt and Platinum Group Metals property located in the Northwest Territories from Arctic Star Exploration Corp. for a payment of $50 and a 1.0% NSR. The claims that comprise the Providence property have been brought to lease. The application for lease was submitted in 2011 with the final lease grant approved in June 2013. To date four annual lease payments and application fees have been paid. Total acquisition costs are $134. Thunder Bay, Ontario The Company maintains a mineral rights position in the Lac Des Iles area north of Thunder Bay, Ontario. The Shelby Lake Property consists of 20 claims totaling 38.56 km2 that includes the Company’s core long term holdings in the Lac Des Iles area consisting of the 8 claim Shelby Lake and South Legris properties. On April 23, 2014 the Company entered into an option to purchase agreement with Lac des Iles Mines Ltd. (“LDI”) (a 100% owned subsidiary of North American Palladium Ltd.) whereby LDI can earn a 100% undivided interest in the Shelby Lake Property by completing $400 in exploration expenditures over a three year period, with an initial cash payment to the Company of $25. The Company will retain a 1% NSR once LDI has completed the option earn in. During the year ended August 31, 2014 all deferred acquisition and exploration costs were written off for all Ontario properties. 6. SHARE CAPITAL (a) Authorized

Unlimited common shares without par value.

Platinum Group Metals Ltd.

(An exploration and development stage company) Notes to the condensed consolidated interim financial statements

For the three months ended November 30, 2014

(in thousands of Canadian dollars unless otherwise noted)

15

(b) Issued and outstanding At November 30, 2014, there were 551,312,842 shares outstanding. Subsequent to period end, on December 9, 2014, the Company announced a bought deal financing for 214.8 million common shares of the Company at a price of US$0.53 ($0.61) per share resulting in gross proceeds of US$113.8 million ($132 million). The offering closed December 31, 2014 with net proceeds to the Company after fees, commissions and costs of approximately US$106 million ($123 million).

(c) Incentive stock options

The Company has entered into Incentive Stock Option Agreements (“Agreements”) under the terms of its stock option plan with directors, officers, consultants and employees. Under the terms of the Agreements, the exercise price of each option is set, at a minimum, at the fair value of the common shares at the date of grant. Stock options granted to certain employees, directors and officers of the Company are subject to vesting provisions, while others vest immediately.

The following tables summarize the Company’s outstanding stock options:

Number of Shares

Average Exercise Price

Options outstanding at August 31, 2013 15,808,500 $ 1.58 Granted 6,575,000 1.30 Exercised (53,300) 1.00 Expired (2,585,700) 1.63

Options outstanding at August 31, 2014 19,744,500 1.48 Granted 25,000 1.20

Options outstanding at November 30, 2014 19,769,500 $ 1.48

Number Outstanding and

Exercisable at November 30, 2014 Exercise Price

Average Remaining Contractual Life

(Years)

3,274,000 $ 0.96 2.77 100,000 1.05 3.50 125,000 1.20 2.64

10,034,000 1.30 3.06 75,000 1.38 2.22 35,000 1.40 2.57

3,699,000 2.05 1.43 2,327,500 2.10 0.99

50,000 2.20 1.02 50,000 2.57 1.10

19,769,500 2.45

The stock options outstanding have an intrinsic value of $nil at November 30, 2014. During the three months ended November 30, 2014, the Company granted 25,000 stock options (November 30, 2013 - Nil). The Company recorded $11 of stock compensation expense for the period ended November 30, 2014 (November 30, 2013 - $Nil).

The Company uses the Black-Scholes model to determine the grant date fair value of stock options granted. The following assumptions were used in valuing stock options granted during the period ended November 30, 2014 and the year ended August 31, 2014:

Platinum Group Metals Ltd.

(An exploration and development stage company) Notes to the condensed consolidated interim financial statements

For the three months ended November 30, 2014

(in thousands of Canadian dollars unless otherwise noted)

16

Period ended November 30, 2014 August 31, 2014

Risk-free interest rate 1.56% 1.47% Expected life of options 3.7 years 3.7 years Annualized volatility 58% 60% Forfeiture rate 0% 0% Dividend rate 0.00% 0.00%

7. RELATED PARTY TRANSACTIONS Transactions with related parties are as follows:

(a) During the three months ended November 30, 2014, $65 ($145 – November 30, 2013) was paid to

independent directors for directors’ fees and services.

(b) During the three months ended November 30, 2014, the Company accrued or received payments of $26 ($26 – November 30, 2013) from West Kirkland Mining Inc., a company with two directors in common, for administrative services. Amounts receivable at the end of the period include an amount of $23 ($121 – November 30, 2013) due from West Kirkland.

(c) During the three months ended November 30, 2014, the Company accrued or received payments of

$Nil ($15 – November 30, 2013) from Nextraction Energy Corp., a company with three directors in common, for administrative services. Amounts receivable at the end of the period include an amount of $206 ($185 – November 30, 2013) due from Nextraction.

All amounts in amounts receivable and accounts payable owing to or from related parties are non-interest bearing with no specific terms of repayment.

These transactions are in the normal course of business and are measured at the estimated fair value, which is the consideration established and agreed to by the noted parties.

8. CONTINGENCIES AND COMMITMENTS

The Company’s remaining minimum payments under its office and equipment lease agreements in Canada and South Africa total approximately $3,007 to August 31, 2020. The Company’s project operating subsidiary, Maseve, is party to a long term 40MVA electricity supply agreement with South African power utility, ESKOM. In consideration Maseve is to pay connection fees and guarantees totaling R142.22 million ($14,715 at November 30, 2014) to fiscal 2015. The Company has paid R70.42 million ($7,286 at November 30, 2014), therefore R71.8 million ($7,429 at November 30, 2014) of the commitment remains outstanding. These fees are subject to possible change based on ESKOM’s cost to install. ESKOM’s schedule to deliver power is also subject to potential for change. On March 26, 2013 the Company waived an outstanding condition precedent to a water off-take agreement with the Magalies Water Board for the long term supply of water to the Project 1 mine site. The agreement is now in effect and the Project 1 estimated cost as per the agreement is R142.0 million ($14.69 million at November 30, 2014) for Maseve. The Company has paid an amount of R49.0 million ($5.07 million) at November 30, 2014 with an amount of R93.0 million ($9.62 million) still outstanding. Tenders for the primary mill components, mining development and equipment and other project expenditures have been adjudicated and orders have now been placed resulting in a commitment of R727 million ($75 million at November 30, 2014) over the next three years.

Platinum Group Metals Ltd.

(An exploration and development stage company) Notes to the condensed consolidated interim financial statements

For the three months ended November 30, 2014

(in thousands of Canadian dollars unless otherwise noted)

17

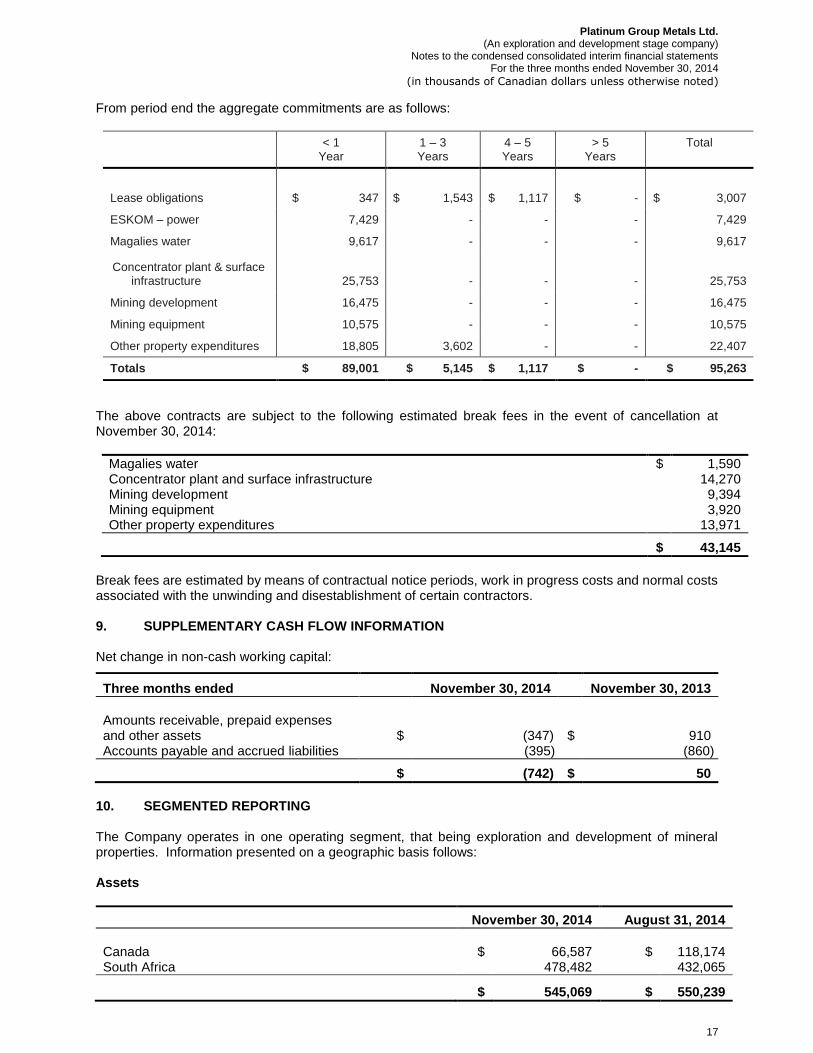

From period end the aggregate commitments are as follows:

< 1 Year

1 – 3 Years

4 – 5 Years

> 5 Years

Total

Lease obligations

$ 347

$ 1,543

$ 1,117

$ -

$ 3,007

ESKOM – power 7,429 - - - 7,429

Magalies water 9,617 - - - 9,617

Concentrator plant & surface infrastructure 25,753

- -

-

25,753

Mining development 16,475 - - - 16,475

Mining equipment 10,575 - - - 10,575

Other property expenditures 18,805 3,602 - - 22,407

Totals $ 89,001 $ 5,145 $ 1,117 $ - $ 95,263

The above contracts are subject to the following estimated break fees in the event of cancellation at November 30, 2014:

Magalies water $ 1,590 Concentrator plant and surface infrastructure 14,270 Mining development 9,394 Mining equipment 3,920 Other property expenditures 13,971

$ 43,145

Break fees are estimated by means of contractual notice periods, work in progress costs and normal costs associated with the unwinding and disestablishment of certain contractors. 9. SUPPLEMENTARY CASH FLOW INFORMATION Net change in non-cash working capital:

Three months ended November 30, 2014 November 30, 2013

Amounts receivable, prepaid expenses and other assets $ (347) $ 910 Accounts payable and accrued liabilities (395) (860)

$ (742) $ 50

10. SEGMENTED REPORTING

The Company operates in one operating segment, that being exploration and development of mineral properties. Information presented on a geographic basis follows: Assets

November 30, 2014 August 31, 2014

Canada $ 66,587 $ 118,174 South Africa 478,482 432,065

$ 545,069 $ 550,239

Platinum Group Metals Ltd.

(An exploration and development stage company) Notes to the condensed consolidated interim financial statements

For the three months ended November 30, 2014

(in thousands of Canadian dollars unless otherwise noted)

18

Substantially all of the Company’s capital expenditures are made in the South Africa; however the Company also has exploration properties in Canada. Income (Loss) attributable to the shareholders of Platinum Group Metals Ltd.

Three months ended November 30, 2014 November 30, 2013

Canada $ (6,211) $ 725 South Africa 503 (278)

$ (5,708) $ 447

11. SUBSEQUENT EVENTS The following events occurred subsequent to period end. These events and other non-material subsequent events may be mentioned elsewhere in the financial statements.

On December 9, 2014 the Company announced that due to general market conditions that it discontinued the private offering of 150,000 units consisting of US$150,000,000 aggregate principal amount of Senior Unsecured Notes due 2021.

On December 9, 2014 the Company announced that it had entered into a term sheet for a senior secured operating loan facility of up to US$40 million. The Facility is planned to be available at the delivery and sale of first commercial concentrate from the WBJV Project 1 targeted for the fourth quarter of calendar 2015. The loan facility is subject to certain terms and conditions as well as the implementation of a definitive credit agreement before being finalized.

On December 9, 2014, the Company announced a bought deal financing for 214.8 million common shares of the Company at a price of US$0.53 ($0.61) per share resulting in gross proceeds of US$113.8 million ($132 million). The offering closed December 31, 2014 with net proceeds to the Company after fees, commissions and costs of approximately US$106 million ($123 million).

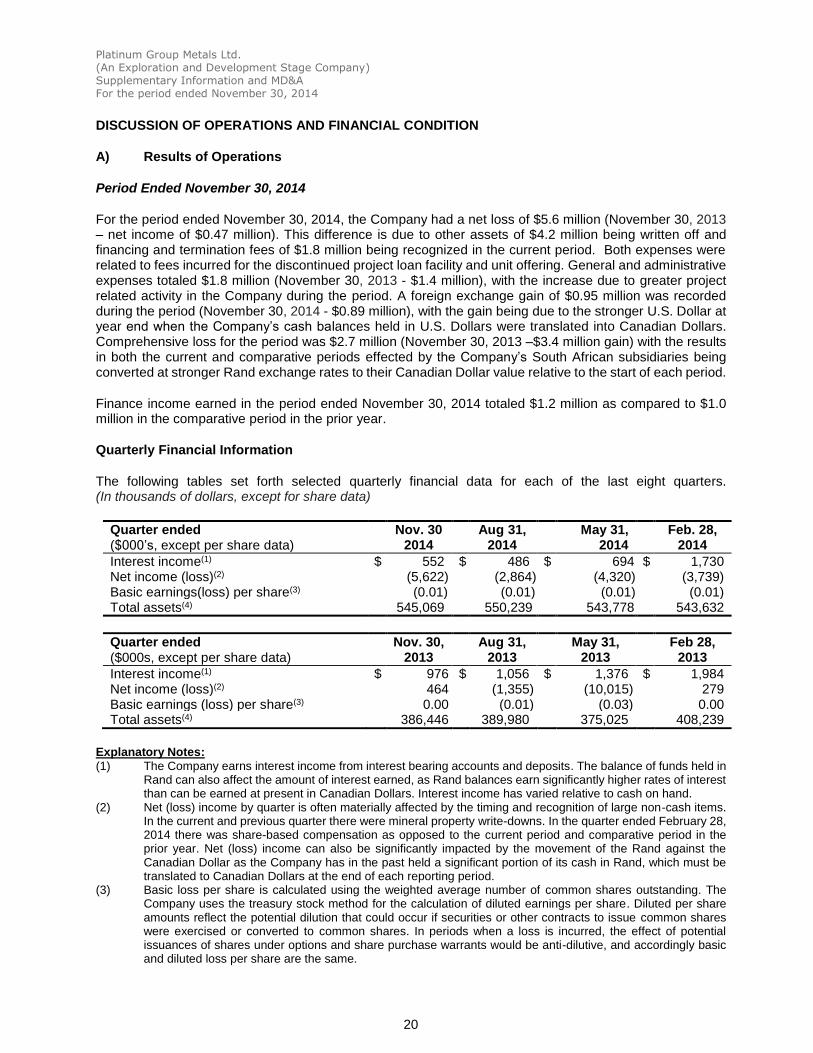

Platinum Group Metals Ltd. (An Exploration and Development Stage Company) Supplementary Information and MD&A For the period ended November 30, 2014 This Management’s Discussion and Analysis is prepared as of January 13, 2015

A copy of this report will be provided to any shareholder who requests it.

Platinum Group Metals Ltd. (An Exploration and Development Stage Company) Supplementary Information and MD&A For the period ended November 30, 2014

2

MANAGEMENT’S DISCUSSION AND ANALYSIS

This management’s discussion and analysis (“MD&A”) of Platinum Group Metals Ltd. (“Platinum Group”, the “Company” or “PTM”) is dated as of January 13, 2015 and focuses on the Company’s financial condition and results of operations for the period ended November 30, 2014. This MD&A should be read in conjunction with the Company’s unaudited condensed consolidated interim financial statements for the period ended November 30, 2014 together with the notes thereto (the “Financial Statements”).

The Company prepares its financial statements in accordance with International Financial Reporting Standards (“IFRS”) and in accordance with International Accounting Standard 34 – Interim Financial Reporting. All dollar figures included therein and in the following MD&A are quoted in Canadian Dollars unless otherwise noted. All references to “U.S. Dollars” or to “US$” are to United States Dollars. All references to “R” or to “Rand” are to South African Rand.

PRELIMINARY NOTES

NOTE REGARDING FORWARD-LOOKING STATEMENTS:

This MD&A and the documents incorporated by reference herein contain “forward-looking statements” and “forward-looking information” within the meaning of applicable U.S. and Canadian securities legislation (collectively, “Forward-Looking Statements”). All statements, other than statements of historical fact that address activities, events or developments that the Company believes, expects or anticipates will, may, could or might occur in the future are Forward-Looking Statements. The words “expect,” “anticipate,” “estimate,” “may,” “could,” “might,” “will,” “would,” “should,” “intend,” “believe,” “target,” “budget,” “plan,” “strategy,” “goals,” “objectives,” “projection” or the negative of any of these words and similar expressions are intended to identify Forward-Looking Statements, although these words may not be present in all Forward-Looking Statements. Forward-Looking Statements included or incorporated by reference in this MD&A include, without limitation, statements with respect to:

capital-raising activities and the adequacy of capital;

revenue, cash flow and cost estimates and assumptions;

production estimates and assumptions, including production rate, grade per tonne and smelter recovery;

project economics;

future metal prices and exchange rates;

mineral reserve and mineral resource estimates;

production timing; and

potential changes in the ownership structures of the Company’s projects.

Forward-Looking Statements reflect the current expectations or beliefs of the Company based on information currently available to the Company. Forward-Looking Statements in respect of capital costs, operating costs, production rate, grade per tonne and smelter recovery are based upon the estimates in the technical reports described herein and ongoing cost estimation work, and the Forward-Looking Statements in respect of metal prices and exchange rates are based upon the three year trailing average prices and the assumptions contained in such technical reports and ongoing estimates.

Forward-Looking Statements are subject to a number of risks and uncertainties that may cause the actual events or results to differ materially from those discussed in the Forward-Looking Statements, and even if events or results discussed in the Forward-Looking Statements are realized or substantially realized, there

Platinum Group Metals Ltd. (An Exploration and Development Stage Company) Supplementary Information and MD&A For the period ended November 30, 2014

3

can be no assurance that they will have the expected consequences to, or effects on, the Company. Factors that could cause actual results or events to differ materially from current expectations include, among other things:

inability of the Company to find an additional and suitable joint venture partner for the Project 1 (“Project 1”) and Project 3 (“Project 3”) platinum mines of what was formerly the Western Bushveld Joint Venture (the “WBJV”);

failure of the Company or its joint venture partners to fund their pro-rata share of funding obligations;

additional financing requirements;

the Company’s history of losses and ability to continue as a going concern;

the Company’s negative cash flow;

the inability of the Company to make payments on its indebtedness, if any, and restrictions on the Company’s operations owing to its indebtedness;

no known mineral reserves on most of the Company’s properties and delays in, or inability to achieve, planned commercial production;

discrepancies between actual and estimated mineral reserves and mineral resources, between actual and estimated development and operating costs, between actual and estimated metallurgical recoveries and between estimated and actual production;

fluctuations in the relative values of the Canadian Dollar as compared to the Rand and the U.S. Dollar;

volatility in metals prices;

difficulty enforcing certain judgments involving United States federal securities laws;

delays in the start-up of the Project 1 platinum mine;

the ability of the Company to retain its key management employees; conflicts of interest;

any disputes or disagreements with the Company’s joint venture partners;

the costs of increasing Black Economic Empowerment ("BEE") in the Company's mining and prospecting operations;

certain potential adverse Canadian tax consequences for foreign-controlled Canadian companies that acquire common shares of the Company;

the Company’s designation as a “passive foreign investment company” and potential adverse U.S. federal income tax consequences for U.S. shareholders;

exploration, development and mining risks and the inherently dangerous nature of the mining industry, including environmental hazards, industrial accidents, unusual or unexpected formations, safety stoppages (whether voluntary or regulatory), pressures, mine collapses, cave ins or flooding and the risk of inadequate insurance or inability to obtain insurance to cover these risks and other risks and uncertainties;

property and mineral title risks including defective title to mineral claims or property;

Platinum Group Metals Ltd. (An Exploration and Development Stage Company) Supplementary Information and MD&A For the period ended November 30, 2014

4

changes in national and local government legislation, taxation, controls, regulations and political or economic developments in Canada, South Africa or other countries in which the Company does or may carry out business in the future;

equipment shortages and the ability of the Company to acquire the necessary access rights and infrastructure for its mineral properties;

environmental regulations and the ability to obtain and maintain necessary permits, including environmental authorizations;

extreme competition in the mineral exploration industry;

risks of doing business in South Africa, including but not limited to, labour, economic and political instability and potential changes to legislation;

no expectation of paying dividends, share price volatility, global financial conditions and dilution due to future issuances of equity securities; and

the other risks disclosed under the heading “Risk Factors” in the Company’s Annual Information Form dated November 24, 2014 (the “AIF”).

These factors should be considered carefully, and investors should not place undue reliance on the Company’s Forward-Looking Statements. In addition, although the Company has attempted to identify important factors that could cause actual actions or results to differ materially from those described in Forward-Looking Statements, there may be other factors that cause actions or results not to be as anticipated, estimated or intended.

The mineral resource and mineral reserve figures referred to in this MD&A are estimates and no assurances can be given that the indicated levels of platinum (“Pt”), palladium (“Pd”), rhodium (“Rh”) and gold (“Au”) (collectively referred to as “4E”) will be produced. Such estimates are expressions of judgment based on knowledge, mining experience, analysis of drilling results and industry practices. Valid estimates made at a given time may significantly change when new information becomes available. By their nature, mineral resource and mineral reserve estimates are imprecise and depend, to a certain extent, upon statistical inferences which may ultimately prove unreliable. Any inaccuracy or future reduction in such estimates could have a material adverse impact on the Company.

Any Forward-Looking Statement speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any Forward-Looking Statement, whether as a result of new information, future events or results or otherwise.

NOTE TO U.S. INVESTORS REGARDING RESOURCE ESTIMATES:

Estimates of mineralization and other technical information included or incorporated by reference herein have been prepared in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”). The definitions of proven and probable reserves used in NI 43-101 differ from the definitions in SEC Industry Guide 7 of the U.S. Securities and Exchange Commission (the “SEC”). Under SEC Industry Guide 7 standards, a “final” or “bankable” feasibility study is required to report reserves, the three year historical average price is used in any reserve or cash flow analysis to designate reserves and the primary environmental analysis or report must be filed with the appropriate governmental authority. As a result, the reserves reported by the Company in accordance with NI 43-101 may not qualify as “reserves” under SEC standards. In addition, the terms “mineral resource,” “measured mineral resource,” “indicated mineral resource” and “inferred mineral resource” are defined in and required to be disclosed by NI 43-101; however, these terms are not defined terms under SEC Industry Guide 7 and normally are not permitted to be used in reports and registration statements filed with the SEC. Mineral resources that are not mineral reserves do not have demonstrated economic viability. Investors are cautioned not to assume that any part or all of the

Platinum Group Metals Ltd. (An Exploration and Development Stage Company) Supplementary Information and MD&A For the period ended November 30, 2014

5

mineral deposits in these categories will ever be converted into reserves. “Inferred mineral resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian securities laws, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. Additionally, disclosure of “contained ounces” in a resource is permitted disclosure under Canadian securities laws; however, the SEC normally only permits issuers to report mineralization that does not constitute “reserves” by SEC standards as in place tonnage and grade without reference to unit measurements. Accordingly, information contained in this MD&A and the documents incorporated by reference herein containing descriptions of the Company’s mineral deposits may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements of United States federal securities laws and the rules and regulations thereunder.

TECHNICAL AND SCIENTIFIC INFORMATION:

The technical and scientific information contained in this MD&A has been reviewed and approved by R. Michael Jones, P.Eng, President and Chief Executive Officer and a director of the Company. Mr. Jones is a non-independent “qualified person” as defined in NI 43-101 (a “Qualified Person”).

1. DESCRIPTION OF BUSINESS

Platinum Group Metals Ltd. is a British Columbia, Canada, company amalgamated on February 18, 2002 pursuant to an order of the Supreme Court of British Columbia approving an amalgamation between Platinum Group Metals Ltd. and New Millennium Metals Corporation. The Company is a platinum-focused exploration and development company conducting work primarily on mineral properties it has staked or acquired by way of option agreements or applications in the Republic of South Africa and in Canada.

The Company’s business is currently focused on the construction of the Project 1 platinum mine and the exploration and initial engineering on the Waterberg platinum deposit, where the Company is the operator of the 255 km2 Waterberg joint venture project (the “Waterberg JV Project”) with the Japan Oil, Gas and Metals National Corporation (“JOGMEC”) and Mnombo Wethu Consultants (Pty) Ltd. (“Mnombo”). The Company has also expanded its exploration on to the prospecting rights covering 864 km2 immediately adjacent and north of the Waterberg JV Project property (the “Waterberg Extension Project” and, together with the Waterberg JV Project, the “Waterberg Projects”).

The Company’s current complement of managers, staff and consultants in Canada consists of approximately 12 individuals and the Company’s complement of managers, staff, consultants, security and casual workers in South Africa consists of approximately 209 individuals.

Project 1 is operated by the Company on an “owner managed-contractor” basis. As at November 30, 2014, the Company has 56 staff, 83 technical services and security staff and 15 human resources and labour consultants assigned to Project 1 while underground mining contractor JIC Mining Services (“JIC”) has approximately 817 people, including mining sub-contractors assigned to working on both the north and south mine areas at Project 1. JIC was engaged in July 2011. Having been appointed in December 2010, DRA Mining (Pty) Ltd., the engineering, procurement, construction and management (“EPCM”) contractor, completed its initial engagement with the Company for Phase 1 establishment of the underground development of the north mine declines in mid-2012, after which Company personnel assumed management over underground services provided by JIC. In December 2012, DRA Mineral Projects (Pty) Ltd. (“DRA”) was formally engaged as the EPCM contractor for commencement of Phase 2 surface infrastructure, including mill and flotation circuit construction. At November 30, 2014 DRA was managing approximately 734 people working onsite at Project 1 assigned to civil works, construction of surface and underground infrastructure, steelwork erection and mechanical installations of the concentrator plant. At November 30, 2014, there were approximately 1,705 people onsite with approximately half working on the underground development team active on the Project 1 platinum mine. Approximately 22% of the labour force is sourced from the local community.

Platinum Group Metals Ltd. (An Exploration and Development Stage Company) Supplementary Information and MD&A For the period ended November 30, 2014

6

2. PROPERTIES

Under IFRS, the Company defers all acquisition, exploration and development costs related to mineral properties. The recoverability of these amounts is dependent upon the existence of economically recoverable mineral reserves, the ability of the Company to obtain the necessary financing to complete the development of the property, and any future profitable production; or alternatively upon the Company’s ability to dispose of its interests on an advantageous basis.

The Company evaluates the carrying value of its property interests on a regular basis. Any properties management deems to be impaired are written down to their estimated net recoverable amount or written off. For more information on mineral properties, see below and Notes 4 and 5 of the Company’s Financial Statements.

SOUTH AFRICAN PROPERTIES

The Company conducts its South African exploration and development work through its wholly-owned direct subsidiary Platinum Group Metals RSA (Pty.) Ltd. (“PTM RSA”). Development of Project 1 is conducted through Maseve Investments 11 (Pty) Ltd. (“Maseve”), a company which at November 30, 2014 was held 82.9% by PTM RSA and 17.1% by Africa Wide Mineral Prospecting and Exploration (Pty) Limited (“Africa Wide”), which is in turn owned 100% by Johannesburg Stock Exchange listed Wesizwe Platinum Limited (“Wesizwe”). See “Project 1 and Project 3 – Africa Wide Dilution” for details regarding the dilution of Africa Wide’s shareholding in Maseve.

The Company is the operator of the Waterberg Projects, consisting of the Waterberg JV Project and the Company’s exploration on prospecting rights on the Waterberg Extension Project. The Company conducts all of its exploration activities at the Waterberg Projects through PTM RSA. As a result of the resource scale and thickness of the Waterberg deposit, exploration activities at the Waterberg Projects have increased in importance in the Company’s business. A pre-feasibility study is in progress on the Waterberg JV Project (approximately 49.9% effective interest of the Company) and exploration drilling continues to define the scale of the deposit on the Waterberg Extension Project (approximately 87% effective interest of the Company).

Project 1 and Project 3, South Africa

During the three months ended November 30, 2014, the Company incurred $45.5 million (November 30, 2013 - $36.1 million) in development, construction, equipment and other costs for Project 1 and did not incur any significant costs on Project 3, located adjacent and to the north of Project 1. In the prior year ended August 31, 2014 total Project 1 development, construction, equipment and other expenditures amounted to $161 million and there were no significant costs incurred on Project 3. At November 30, 2014, the Company carried total deferred acquisition, development, construction, equipment and other costs related to Project 1 of $431 million and another $3.2 million related to Project 3. Of the total deferred costs for Project 1 at November 30, 2014 an amount of $362 million (approximately US$343 million) related to Phase 1 and Phase 2 development, construction, equipment and other costs. Africa Wide’s non-controlling interest in Maseve as at November 30, 2014 was recorded at $71 million. Project 1 is estimated to be approximately 70% complete as of November 30, 2014.

A Phase 1 development program at Project 1, consisting of the twin set of north declines and related surface infrastructure, was completed in March 2013 at a total cost of Rand 777.20 million; however, a further amount of Rand 81.3 million related to deferred expenditures for electrical services was subsequently incurred, bringing the Phase 1 total cost essentially to budget. Phase 1 was completed approximately 12 weeks behind original schedule as a result of delays obtaining permits and suboptimal civil contractor performance early in the programme. These delays caused difficulty in the scheduling of duties and handover between civil and underground contractors. Initial underground mining cycle times and face advance were less than planned as well, a situation which was later rectified. During the period from February 2013 to December 2014, advance was halted or delayed approximately two months in the aggregate due to notices under section 54 of the Mine Health and Safety Act (1996) (“MHSA”) issued to Maseve.

Platinum Group Metals Ltd. (An Exploration and Development Stage Company) Supplementary Information and MD&A For the period ended November 30, 2014

7

The north decline box cut excavation brings the working area down an access ramp from surface for 128 meters linear and 20 meters vertical to where the north declines enter the underground. From the portal entrance or “collar” the north declines are now approximately 1,420 meters linear (at November 30, 2014) and approximately 225 meters vertical (at November 30, 2014) into the underground. Approximately 1,412 meters (at November 30, 2014) of lateral development and reef drives have been completed. This brings development to the first infrastructure level in order to provide for storage bins for conveyor transfers from various mining blocks at depth as well as workshops, reef drive take offs, ventilation headings and other ancillary excavation totaling 1,646 meters (at November 30, 2014). Break away declines are underway to mining block 11 totaling 1,013 meters linear (371 meters vertical) (at November 30, 2014) and block 12 totaling 844 meters linear (323 meters vertical) (at November 30, 2014). Multiple cross cuts between declines of 10 meters in length and multiple re-muck bays have also been installed as well as sumps and water management facilities. Two ventilation raise bore shafts have been completed and commissioned. In total over 7,638 meters of access development has now been completed in the North mine. Initial raises are in development and ore stockpiling has commenced. Geotechnical work and preparations for an additional ventilation shaft are complete and ready for a raise bore machine to establish site while preparation work for another ventilation shaft is in progress.

On March 28, 2013, the Merensky Reef (“MR”) was intercepted in the north declines as anticipated in the mine geological model. Underground drives along the strike of the deposit have now advanced on the MR approximate position northward for approximately 541 meters along the reef plane (at November 30, 2014), exposing approximately 259 meters of MR and 210 meters in the hanging wall (at November 30, 2014). Raise development of 476 meters (at November 30, 2014) has commenced into the mining blocks and continues. Shallow MR mine blocks are exhibiting rolling features where the critical zone of the Bushveld Igneous Complex is in close proximity to the Transvaal Sediment floor rocks. This condition, referred to as an abutment facies of the MR, is common to the shallow portions of the adjacent operating mine. Stock piling of MR development material on surface has begun with approximately 106,084 tonnes on surface (at November 30, 2014). As development opens areas of MR, evaluation of the initial mining blocks is being completed by Company geologists and engineers. Work to date indicates that the areas opened so far are consistent with the Company’s geological model for these areas. In addition to the drives along the reef position laterally, the north declines have now turned and are continuing from the first infrastructural level targeting deeper mine blocks.

The rate of underground development in the north and south declines continues to be an important factor with respect to future mine start-up dates and production rates. Delays in underground development, stoping rates and planned tonnages may result in delayed start-up of production and may have a negative impact on peak funding and working capital requirements. The south box cut is complete, and underground mining has advanced the material decline for approximately 949 meters and the conveyor decline for approximately 741 meters (at November 30, 2014). Multiple cross cuts between declines of 10 meters in length and multiple re-muck bays have also been installed as well as sumps and water management facilities. In total over 2,206 meters of access development has now been completed in the South mine. The south decline Phase 2 development is behind the original planned schedule. The early development of the south declines progressed slower than anticipated due to poor ground conditions in the first 50 meters vertical from surface. Work to deal with these conditions included consolidation support, grouting, void filling and the installation of steel sets. The south declines are now advanced into more competent rock. Development rates are improving and are currently at or near the rates called for in the current schedule. On June 14, 2013, the Company announced that as a result of the slower development rates in the south decline and delays as a result of safety work stoppages pursuant to section 54 of the MHSA, the targeted start date for first concentrate production was adjusted by six months to mid-2015. As a result of Africa Wide’s decision on October 18, 2013 not to fund an approved cash call by Maseve and the consequent delays in finalization of the Project 1 finance package, including project lending, a procurement freeze was implemented on Project 1 for approximately 12 weeks from late 2013 into 2014, which resulted in delays to the acquisition and procurement of various goods and services, delaying mill and surface infrastructure construction. The delay in implementing construction contracts combined with potential delays in ramping-

Platinum Group Metals Ltd. (An Exploration and Development Stage Company) Supplementary Information and MD&A For the period ended November 30, 2014

8

up mining ore resulted in a decision to further delay the completion of mill construction and the first concentrate sales to the fourth quarter of calendar 2015. The ramp-up profile for production from commencement forward over the following two years is similar to previous projections when the start date delay is considered. Delays in the ramp-up profile could occur if underground development rates fall behind plan or if mining produces less tonnes or grade than predicted by the geological model, potentially resulting in delayed or reduced revenue from concentrate sales, which would negatively impact peak funding requirements. The Company and DRA have been working on design work and preparations for the Phase 2 construction of milling, concentrating and tailings facilities since late 2012. Tenders for the primary mill components, mining development and equipment and other project expenditures have been adjudicated and all material orders have now been placed and construction is well advanced. The overall planned commitment for the milling, concentrator and tailings facilities as at November 30, 2014 was Rand 2.38 billion ($246 million at November 30, 2014) to the fourth quarter of calendar 2015, of which Rand 1.80 billion ($186 million at November 30, 2014) has already been committed. Phase 2 construction at Project 1 commenced in early January 2013. Phase 2 includes the completion of an additional twin decline access into the southern portion of the deposit, a milling, concentrating and tailings facility and extensive underground development. As of the date of this MD&A, earth works and laydown areas for mill and concentrator facilities are now complete. Foundations for major crusher, mill and concentrator components are complete and steel erection and equipment installation is underway. Expected deliveries for all major components remain on schedule. Ancillary servicing for the north decline site, including buildings, piping, cabling, fencing and security, has been completed. Cleaner flotation cells have been delivered to site by Metso Mining and Construction (South Africa) Pty Ltd. Rougher cells and flotation units are being assembled and installed. Change houses, shops and stores facilities are substantially complete. The filter press building and infrastructure is nearing completion with the filter press having been tested in Finland and released for delivery to site, which is now expected to occur in January 2015. The primary run of mine ball mill was delivered to site by Outotec RSA (Pty) Ltd. in June 2014 and as of November 14, 2014 the primary mill shell and related ends, trunions and gears were substantially installed on their supports. Conveyors, crushers and an ore silo are well advanced. Ground preparations for the Project 1 tailings storage facility (“TSF”) commenced in late 2013 on surface rights owned by Maseve. Further work was postponed in mid-2014 due to concerns raised by Royal Bafokeng Platinum Ltd. (“RBPlat”), who own the prospecting rights below the planned TSF site. RBPlat’s primary concern is with regard to the allocation of legal responsibility under the MHSA and associated regulations where Project 1’s surface mining activities overlay the underground areas where RBPlat holds prospecting rights. The Company and RBPlat have now executed an agreement with regard to a path forward and RBPlat has withdrawn their complaints to the regulators. RBPlat and the Company are currently in discussions with the Department of Mineral Resources (“DMR”) and other regulators to clarify this issue to the benefit of both parties. To date, the current construction postponement on the TSF has not negatively affected the projected date of first production. Project 1 - Social Development and Responsibilities

Feedback from the public consultation processes for the environmental assessment and Social and Labour Plan development has been constructive and positive. The mine capital development plan includes a significant investment in training through the life of mine, allocated to a social and labour plan to ensure maximum value from the project for all stakeholders, including local residents. Based on interaction with the community, the completion of a skill and needs assessment, and the Company’s training plans, the project is planning for 2,700 jobs with a target of 30% from the local communities. To assist the Company in achieving these goals, the Company has contracted the services of an experienced and professional HR company, Requisite Business Solutions (Pty) Ltd. Additionally, the Project 1 platinum mine’s financial estimates include an accumulated charge per tonne to create a fund for eventual closure of the mine.

Platinum Group Metals Ltd. (An Exploration and Development Stage Company) Supplementary Information and MD&A For the period ended November 30, 2014

9

Project 1 - Financial Overview

The Company completed a definitive feasibility study in July 2008 and on November 25, 2009, the Company published an updated feasibility study on Project 1 entitled ‘‘Updated Technical Report (Updated Feasibility Study) Western Bushveld Joint Venture Project 1 (Elandsfontein and Frischgewaagd)’’ dated November 20, 2009 with an effective date of October 8, 2009 (the “2009 UFS”) for Project 1, which was at that time a portion of the WBJV. Included in each study was a declaration of 4E reserve ounces.

The base case for the mineral reserve estimate in the 2009 UFS was modeled using three year trailing metal prices at September 2009, including US$1,343 per ounce platinum and US$322 per ounce palladium, and an exchange rate of R8 to the U.S. Dollar. During and after the period there has been significant volatility in the market prices for base metals and for gold and other precious metals such as platinum and palladium. The December 31, 2014 spot prices of 4E in aggregate denominated in U.S. Dollars were lower than the base case, long term metal prices as set out in the 2009 UFS, but are within the range (in aggregate, including exchange rates for the MR pricing) of the sensitivity analysis contained in the 2009 UFS. Weakening metal prices are offset by a weaker Rand and affect peak funding estimates for Project 1. The escalation of costs, metal price volatility, production ramp-up timing and Rand volatility are all material risk factors for the commercial viability of Project 1.

In April 2012, the Company completed a revised cost budget estimate based on post-2009 UFS work for inclusion in a financial model for a syndicate of lead arrangers. The Company referred to industry sources and Qualified Persons for updated cost information and also applied experience gained during procurement and construction under early project construction and development. The revised peak funding estimate, which is calculated in Rand, was published in April 2012. The revised estimate was approximately US$506 million (at R8 to the US$) for the construction and commissioning of Project 1, representing an escalation of approximately 14% since the 2009 UFS. Operating costs per tonne were estimated to have escalated approximately 24% since the 2009 UFS. These operating cost escalation estimates are in keeping with inflation rates and industry experience in South Africa since 2009.

In June 2014, the Association of Mineworkers and Construction Union (“AMCU”) accepted a negotiated wage settlement to end a five month long strike affecting a significant proportion of the platinum industry. The wage increases agreed to by the major producers will increase labour costs for Project 1 as mining contractors renew certain labour agreements into 2015. The Company is assessing the impact this may have on the Company. Although the Company is encouraged by the current Rand/U.S. Dollar rate, which is better than the base case assumption of 8:1, increasing wages may have a material negative influence on the Company.

On September 5, 2012, Maseve received notice from Rustenburg Platinum Mines Ltd. (“RPM”), a wholly owned subsidiary of Anglo American Platinum Limited (“Amplats”), regarding RPM’s exercise of its 60-day right of first refusal to enter into an agreement with Maseve on terms equivalent to indicative terms agreed to by Maseve with another commercial off-taker for the sale of concentrate produced from Project 1 and Project 3. Formal legal off-take agreements were executed in April 2013 based on the third party indicative terms. The terms of the executed off-take agreement with RPM are not materially different than those modeled in the 2009 UFS.

At November 30, 2014, approximately Rand 3.3 billion (US$343 million at average exchange rates during the development period) has been invested in Phase 1 and Phase 2 development assets and construction in progress (including mining equipment and excluding land or non-mining related buildings). Project 1 is estimated to be approximately 70% complete as of November 30, 2014.

As construction continues at Project 1, the Company continues to see escalation in Rand terms for some costs such as labour, diesel fuel, power and certain supplies. These escalations continue to be consistent with those seen in the South African mining industry in general over recent years. Major service contracts and equipment purchase contracts are collectively in keeping with previous cost estimates plus industry escalation. The Company’s original cost estimates were modelled at 8 Rand to the U.S. Dollar. With the Rand currently weakening relative to the U.S. Dollar, these cost escalations are substantially offset in dollar

Platinum Group Metals Ltd. (An Exploration and Development Stage Company) Supplementary Information and MD&A For the period ended November 30, 2014

10

terms. Diesel and other petroleum products, however, are marked to U.S. Dollar prices and a weakening Rand has the effect of raising Rand-based fuel costs, while recent decreases in the global price of oil has partially offset such increases.

The Company also notes that weakening metal price assumptions or a stronger Rand each have a negative effect on peak funding estimates for Project 1. Delays in underground development or delays in delivery of ore tonnage to surface stockpiles will also have a negative effect on peak funding requirements. The escalation of costs, metal price volatility, production ramp-up timing and Rand volatility are all material risk factors for Project 1.

Apart from past delays and updated financial estimates as discussed above, the general mine plan for Project 1 is substantially unchanged from the 2009 UFS, with a steady state production rate of 275,000 4E from decline-accessed Merensky and UG2 ore. For a description of recent financings undertaken by the Company see discussion at item F) “Liquidity and Capital Resources” below.