Pitchbook US template - Investor Relations - TodayIR.com · 2014-08-19 · Do not refresh this file...

19

0 19 AUGUST 2014 Interim Results 2014 (0975.HK)

Transcript of Pitchbook US template - Investor Relations - TodayIR.com · 2014-08-19 · Do not refresh this file...

Do not refresh this file

0

Object title

Conclusion

R0.G0.B102

Table column

heading shading

R234.G234.B234

color 1

1st level bullet

R255.G102.B0

color 2

R0228.G172.B105

color 3

R168.G174.B203

color 4

R90.G106.B154

color 5

R0.G0.B102

color 6

R215.G212.B206

color 8

R0.G0.B0

Highlight

R153.G0.B0

ObjectFoundation

White

R255.G255.B255

2nd, 3rd & 4th

level Bullet

Lt. divider line

R192.G192.B192

Text

R0.G0.B0

Connector lines

Dk. divider line

128.G128.B128

Table highlight

R244.G225.B206

color 7

R171.G161.B149

Do not refresh this file

1 9 AU G U S T 2 0 1 4

Interim Results 2014

(0975.HK)

Do not refresh this file

1

Object title

Conclusion

R0.G0.B102

Table column

heading shading

R234.G234.B234

color 1

1st level bullet

R255.G102.B0

color 2

R0228.G172.B105

color 3

R168.G174.B203

color 4

R90.G106.B154

color 5

R0.G0.B102

color 6

R215.G212.B206

color 8

R0.G0.B0

Highlight

R153.G0.B0

ObjectFoundation

White

R255.G255.B255

2nd, 3rd & 4th

level Bullet

Lt. divider line

R192.G192.B192

Text

R0.G0.B0

Connector lines

Dk. divider line

128.G128.B128

Table highlight

R244.G225.B206

color 7

R171.G161.B149

Disclaimer

Forward-looking statements

We have included in this presentation forward-looking statements. All statements that are not historical facts, including statements about

our intentions, beliefs, expectations or predictions for the future, are forward-looking statements. The reliance on any forward-looking

statement involves risks and uncertainties, and although we believe the assumptions on which the forward-looking statements are based

are reasonable, any or all of those assumptions could prove to be inaccurate and as a result, the forward-looking statements based on

those assumptions could also be incorrect.

We undertake no obligation to publicly update or revise any forward-looking statements contained in this presentation, whether as a result

of new information, future events or otherwise, except as required by applicable laws, rules and regulations. In light of these and other

risks and uncertainties, the inclusion of forward-looking statements should not be regarded as representations by us that our plans and

objectives will be achieved.

Note: All numbers in this presentation are approximate rounded values for particular items

Do not refresh this file

2

Object title

Conclusion

R0.G0.B102

Table column

heading shading

R234.G234.B234

color 1

1st level bullet

R255.G102.B0

color 2

R0228.G172.B105

color 3

R168.G174.B203

color 4

R90.G106.B154

color 5

R0.G0.B102

color 6

R215.G212.B206

color 8

R0.G0.B0

Highlight

R153.G0.B0

ObjectFoundation

White

R255.G255.B255

2nd, 3rd & 4th

level Bullet

Lt. divider line

R192.G192.B192

Text

R0.G0.B0

Connector lines

Dk. divider line

128.G128.B128

Table highlight

R244.G225.B206

color 7

R171.G161.B149

Agenda

Operating environment

Business review

Financial review

Outlook

Do not refresh this file

3

Object title

Conclusion

R0.G0.B102

Table column

heading shading

R234.G234.B234

color 1

1st level bullet

R255.G102.B0

color 2

R0228.G172.B105

color 3

R168.G174.B203

color 4

R90.G106.B154

color 5

R0.G0.B102

color 6

R215.G212.B206

color 8

R0.G0.B0

Highlight

R153.G0.B0

ObjectFoundation

White

R255.G255.B255

2nd, 3rd & 4th

level Bullet

Lt. divider line

R192.G192.B192

Text

R0.G0.B0

Connector lines

Dk. divider line

128.G128.B128

Table highlight

R244.G225.B206

color 7

R171.G161.B149

193 210 224

237 234

197 207 216 230 232

1H2010 1H2011 1H2012 1H2013 1H2014

Coke production Coke consumption

Witnessing market corrections towards adjusting supply and demand imbalances

234 253 268 269 274 265 280 291

309 309

1H2010 1H2011 1H2012 1H2013 1H2014

Coking coal production Coking coal consumption

323 351 357

390 412

307 335 338

365 375

1H2010 1H2011 1H2012 1H2013 1H2014

Crude steel production Crude steel consumption

Source: World Steel Association, China Coal Resources, National Bureau of Statistics of China

(Mt) (Mt)

(Mt)

22.4 19.2 27.6

35.3 30.9

8.4% 6.8%

9.5% 11.4%

10.0%

1H2010 1H2011 1H2012 1H2013 1H2014

Coking coal imports % of coking coal consumption

Crude steel production and consumption Coking coal production and consumption

Coke production and consumption Coking coal imports

(Mt)

Operating environment

Chinese coking coal supply and demand dynamics

Do not refresh this file

4

Object title

Conclusion

R0.G0.B102

Table column

heading shading

R234.G234.B234

color 1

1st level bullet

R255.G102.B0

color 2

R0228.G172.B105

color 3

R168.G174.B203

color 4

R90.G106.B154

color 5

R0.G0.B102

color 6

R215.G212.B206

color 8

R0.G0.B0

Highlight

R153.G0.B0

ObjectFoundation

White

R255.G255.B255

2nd, 3rd & 4th

level Bullet

Lt. divider line

R192.G192.B192

Text

R0.G0.B0

Connector lines

Dk. divider line

128.G128.B128

Table highlight

R244.G225.B206

color 7

R171.G161.B149

MMC strengthened its position as a leading Mongolian coal exporter

Australia 40%

Mongolia 20%

Others 40%

Australia 49%

Mongolia 24%

Others 27%

MMC exports ~31%

Others 69%

MMC exports ~34%

Others 66%

Source: Company data, China Coal Resource

Source: The World Bank, National Statistical Office of Mongolia (“NSO”), Bank of Mongolia, Bloomberg Note: 1 2011 GDP splits by sector at current price levels; GDP computed by dividing MNT amount by average USD:MNT exchange rate of each year from Bloomberg; 2 2011FY GDP is a preliminary estimation provided by

the NSO as at January 2012; 3 Total assets, loans and deposits in US$ computed by diving MNT amount by average USD:MNT exchange rate of each year from Bloomberg

FY2013 1H2014

FY2013 1H2014

MMC remains the only major washed coking coal producer and exporter from Mongolia

Coking coal imports to China are dominated by Australia and Mongolia

Operating environment

Increasing coking coal import competition to China

Do not refresh this file

5

Object title

Conclusion

R0.G0.B102

Table column

heading shading

R234.G234.B234

color 1

1st level bullet

R255.G102.B0

color 2

R0228.G172.B105

color 3

R168.G174.B203

color 4

R90.G106.B154

color 5

R0.G0.B102

color 6

R215.G212.B206

color 8

R0.G0.B0

Highlight

R153.G0.B0

ObjectFoundation

White

R255.G255.B255

2nd, 3rd & 4th

level Bullet

Lt. divider line

R192.G192.B192

Text

R0.G0.B0

Connector lines

Dk. divider line

128.G128.B128

Table highlight

R244.G225.B206

color 7

R171.G161.B149

Amendment to the Law on Minerals was approved by

Parliament 01 Jul 2014, with major impact being

lifting the three and a half year moratorium on new

exploration licenses in Mongolia

Resumption of exploration activities in Mongolia is

expected to assist restoration of foreign and domestic

investor confidence, increasing foreign direct investment to

the benefit of Mongolia’s economy

Introduced regulation to set processes of applying,

negotiating and executing an IA, and provide

provisions on monitoring after execution. The GoM

may enter into an IA with investors seeking to invest

more than MNT500 billion

Stability for investors through stabilization of their

operational and tax environment

New law was approved by Parliament 01 Jul 2014 A major step in upgrading the business and investment

climate of the country’s petroleum industry, with potential to

positively impact fuel supplies in medium to long term

GoM adopted new regulation to calculate coal export

royalties, based upon individual contract price per

tonne, instead of set reference price

Effective from 01 Apr 2014, and expected to make a

realistic contribution to relieving the tax burdens for coal

exporters until 01 Jan 2015

MNS 6456:2014 and MNS 6457:2014 standards with

regard to “Coal classification” and “Coal and coal

product classification” were approved and added to

the national registry of Mongolia in Jun 2014

Adoption of these standards will improve the

competitiveness of Mongolian coal products and streamline

the flow of coal exports

Investors involved in large-scale development

projects incl. construction of plants are entitled to

apply for partial payment conditions or extension of

its VAT and/or customs duty payments for a period of

2 years

Improvement to the overall investment climate, by

decreasing tax burden especially during the capital

intensive construction phase of major projects

Key measures

Law on Minerals

Investment Agreement

(IA)

Law on Petroleum

Change of royalty

calculation method

Coal classification

standards

Amendment to the Law

on Custom Tariff and

Duty

Description Impact

Operating environment

Mongolian Government taking supportive measures

Do not refresh this file

6

Object title

Conclusion

R0.G0.B102

Table column

heading shading

R234.G234.B234

color 1

1st level bullet

R255.G102.B0

color 2

R0228.G172.B105

color 3

R168.G174.B203

color 4

R90.G106.B154

color 5

R0.G0.B102

color 6

R215.G212.B206

color 8

R0.G0.B0

Highlight

R153.G0.B0

ObjectFoundation

White

R255.G255.B255

2nd, 3rd & 4th

level Bullet

Lt. divider line

R192.G192.B192

Text

R0.G0.B0

Connector lines

Dk. divider line

128.G128.B128

Table highlight

R244.G225.B206

color 7

R171.G161.B149

Operating environment

Business review

Financial review

Outlook

Agenda

Do not refresh this file

7

Object title

Conclusion

R0.G0.B102

Table column

heading shading

R234.G234.B234

color 1

1st level bullet

R255.G102.B0

color 2

R0228.G172.B105

color 3

R168.G174.B203

color 4

R90.G106.B154

color 5

R0.G0.B102

color 6

R215.G212.B206

color 8

R0.G0.B0

Highlight

R153.G0.B0

ObjectFoundation

White

R255.G255.B255

2nd, 3rd & 4th

level Bullet

Lt. divider line

R192.G192.B192

Text

R0.G0.B0

Connector lines

Dk. divider line

128.G128.B128

Table highlight

R244.G225.B206

color 7

R171.G161.B149

ROM coal production

3.3 Mt of ROM coal was mined, down 21% YoY compared to 1H2013

Production output adjusted downward to minimize total cash cost, whilst

utilizing available inventories to meet forecast sales volumes

21.3 Mbcm overburden moved at stripping ratio of 6.5, but 2014 full year

stripping ratio of 5.5 still expected

Overburden was dumped at shortest possible distance from the mining faces,

to constrain total mining costs, with short dump volume identified not

considered in LOM plan remaining to be used in second half of 2014

Lost Time Injury Frequency Rate (“LTIFR”) of 0.7 YTD signifies improvement

compared to 2013 where the full year statistic equated to 1.2

3.7 4.9

4.2 5.0

3.3

0.4

0.4 0.5 4.1

5.3

4.2

5.5

3.3

6.3 5.1

5.9 5.4 6.5

1H2012 2H2012 1H2013 2H2013 1H2014

UHG Coal BN Coal Strip Ratio

(Mt)

1.5

2.4 2.4 2.9

1.8

0.6

1.0 1.3

1.0

0.6 2.1

3.4 3.7

3.9

2.4

1H2012 2H2012 1H2013 2H2013 1H2014

Primary product Secondary product

Processed product

Culminated medium term capital expenditure plan with regard to processing

capacity with the completion of Module III

Achieved total yield of 70%, (primary yield 51%, secondary yield 19%), per

forecast strategy of inventory utilization

Installed capacity allowed for major planned maintenance events to be

performed in parallel to operation

Trialed contract washing on a fee-for-service basis in limited volumes to take

advantage of installed capacity available

The Belt Filter Press (“BFP”), commissioned in 4Q2013, has operated according

to plan providing for improved recycling of water used in fine coal processing

circuits compared to tailings dam reclamation methods

(Mt)

Deliberate adjustment to meet committed sales volumes whilst maximizing use of inventories

Business review

Tailoring production output in line with cost control and liquidity management

(BCM/ROMt)

Do not refresh this file

8

Object title

Conclusion

R0.G0.B102

Table column

heading shading

R234.G234.B234

color 1

1st level bullet

R255.G102.B0

color 2

R0228.G172.B105

color 3

R168.G174.B203

color 4

R90.G106.B154

color 5

R0.G0.B102

color 6

R215.G212.B206

color 8

R0.G0.B0

Highlight

R153.G0.B0

ObjectFoundation

White

R255.G255.B255

2nd, 3rd & 4th

level Bullet

Lt. divider line

R192.G192.B192

Text

R0.G0.B0

Connector lines

Dk. divider line

128.G128.B128

Table highlight

R244.G225.B206

color 7

R171.G161.B149

Focus on transportation cost reduction aligned with the production and export plans

Transportation Volume

Improved alignment of long haul transportation with contracted sales

volume for better overall inventory management

Optimized inventory level at TKH stockpiles near the border by hauling

2.9Mt of coal products from UHG to TKH stockpiles in 1H2014, compared

to 3.2Mt exports

Continued involvement in the operation and maintenance of the UHG-GS

Paved Road, and maintained full access to the road and border crossing

facilities after the transfer of these facilities to GoM in February 2014

Completed 100% of domestic coal haulage using the Group’s owned fleet

of double trailer heavy haul trucks

Transportation Cost

Maintained high level of utilization of the Group’s own truck fleet while

further reducing the fixed cost base of the long-haul section by 18% to

US$6.7/t in 1H2014

Continued to decrease short-haul transportation to US$7.9/t, a 16%

reduction from 1H2013, through renegotiation with third-party contractors

Significant cost savings in the short-haul section is expected to be achieved

in 2015 after the completion of the Cross-Border Railway

(Mt)

Business review

Continuing to improve transportation efficiency

2.1

3.7 3.5

3.3

2.9

2.3

3.3 3.1

2.6

3.2

1H2012 2H2012 1H2013 2H2013 1H2014

Long Haul (UHG-TKH) Short Haul (TKH-GM)

(US$/t)

12.6 11.4 8.2 8.0 6.7

9.0 10.6

9.4 8.0

7.9

21.6 22.0

17.6 16.0

14.6

1H2012 2H2012 1H2013 2H2013 1H2014

Long Haul (UHG-TKH) Short Haul (TKH-GM)

Do not refresh this file

9

Object title

Conclusion

R0.G0.B102

Table column

heading shading

R234.G234.B234

color 1

1st level bullet

R255.G102.B0

color 2

R0228.G172.B105

color 3

R168.G174.B203

color 4

R90.G106.B154

color 5

R0.G0.B102

color 6

R215.G212.B206

color 8

R0.G0.B0

Highlight

R153.G0.B0

ObjectFoundation

White

R255.G255.B255

2nd, 3rd & 4th

level Bullet

Lt. divider line

R192.G192.B192

Text

R0.G0.B0

Connector lines

Dk. divider line

128.G128.B128

Table highlight

R244.G225.B206

color 7

R171.G161.B149

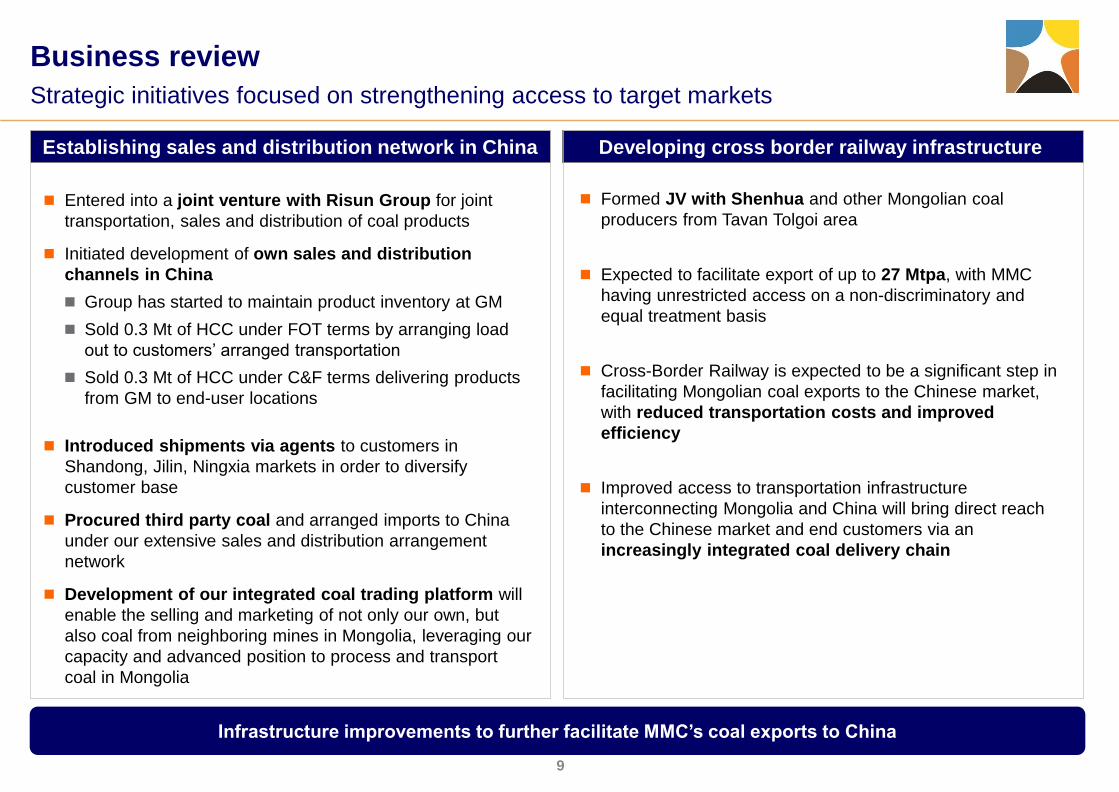

Establishing sales and distribution network in China Developing cross border railway infrastructure

Entered into a joint venture with Risun Group for joint

transportation, sales and distribution of coal products

Initiated development of own sales and distribution

channels in China

Group has started to maintain product inventory at GM

Sold 0.3 Mt of HCC under FOT terms by arranging load

out to customers’ arranged transportation

Sold 0.3 Mt of HCC under C&F terms delivering products

from GM to end-user locations

Introduced shipments via agents to customers in

Shandong, Jilin, Ningxia markets in order to diversify

customer base

Procured third party coal and arranged imports to China

under our extensive sales and distribution arrangement

network

Development of our integrated coal trading platform will

enable the selling and marketing of not only our own, but

also coal from neighboring mines in Mongolia, leveraging our

capacity and advanced position to process and transport

coal in Mongolia

Formed JV with Shenhua and other Mongolian coal

producers from Tavan Tolgoi area

Expected to facilitate export of up to 27 Mtpa, with MMC

having unrestricted access on a non-discriminatory and

equal treatment basis

Cross-Border Railway is expected to be a significant step in

facilitating Mongolian coal exports to the Chinese market,

with reduced transportation costs and improved

efficiency

Improved access to transportation infrastructure

interconnecting Mongolia and China will bring direct reach

to the Chinese market and end customers via an

increasingly integrated coal delivery chain

Infrastructure improvements to further facilitate MMC’s coal exports to China

Business review

Strategic initiatives focused on strengthening access to target markets

Do not refresh this file

10

Object title

Conclusion

R0.G0.B102

Table column

heading shading

R234.G234.B234

color 1

1st level bullet

R255.G102.B0

color 2

R0228.G172.B105

color 3

R168.G174.B203

color 4

R90.G106.B154

color 5

R0.G0.B102

color 6

R215.G212.B206

color 8

R0.G0.B0

Highlight

R153.G0.B0

ObjectFoundation

White

R255.G255.B255

2nd, 3rd & 4th

level Bullet

Lt. divider line

R192.G192.B192

Text

R0.G0.B0

Connector lines

Dk. divider line

128.G128.B128

Table highlight

R244.G225.B206

color 7

R171.G161.B149

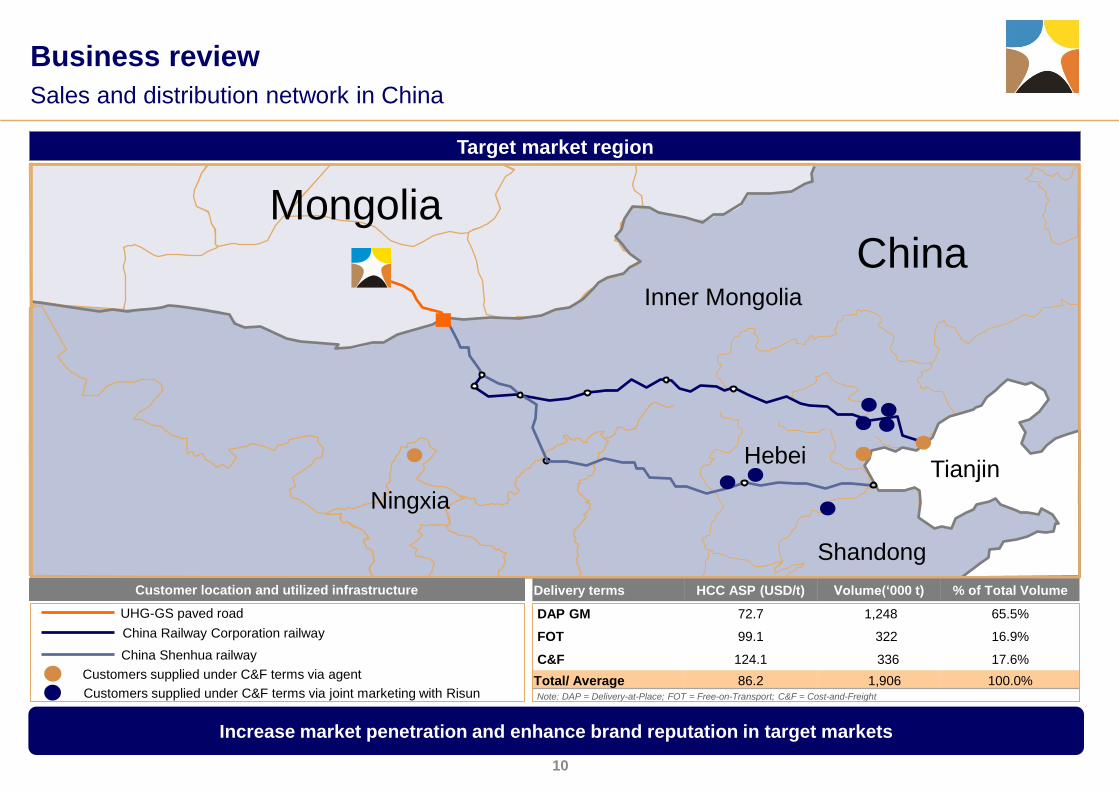

Target market region

Business review

Sales and distribution network in China

Mongolia China

Inner Mongolia

Ningxia

Hebei

Shandong

Tianjin

UHG-GS paved road

Customers supplied under C&F terms via agent

Customers supplied under C&F terms via joint marketing with Risun

China Railway Corporation railway

China Shenhua railway

Customer location and utilized infrastructure

Note: DAP = Delivery-at-Place; FOT = Free-on-Transport; C&F = Cost-and-Freight

Increase market penetration and enhance brand reputation in target markets

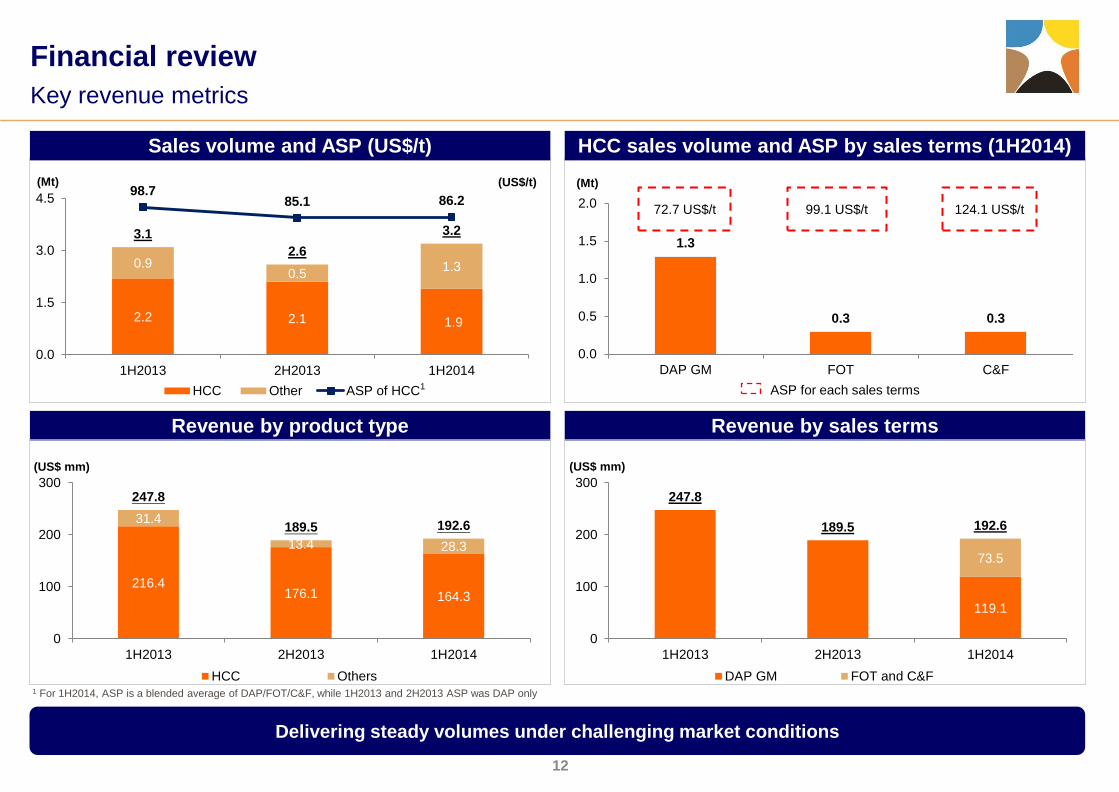

Delivery terms HCC ASP (USD/t) Volume(‘000 t) % of Total Volume

DAP GM 72.7 1,248 65.5%

FOT 99.1 322 16.9%

C&F 124.1 336 17.6%

Total/ Average 86.2 1,906 100.0%

Do not refresh this file

11

Object title

Conclusion

R0.G0.B102

Table column

heading shading

R234.G234.B234

color 1

1st level bullet

R255.G102.B0

color 2

R0228.G172.B105

color 3

R168.G174.B203

color 4

R90.G106.B154

color 5

R0.G0.B102

color 6

R215.G212.B206

color 8

R0.G0.B0

Highlight

R153.G0.B0

ObjectFoundation

White

R255.G255.B255

2nd, 3rd & 4th

level Bullet

Lt. divider line

R192.G192.B192

Text

R0.G0.B0

Connector lines

Dk. divider line

128.G128.B128

Table highlight

R244.G225.B206

color 7

R171.G161.B149

Agenda

Operating environment

Business review

Financial review

Outlook

Do not refresh this file

12

Object title

Conclusion

R0.G0.B102

Table column

heading shading

R234.G234.B234

color 1

1st level bullet

R255.G102.B0

color 2

R0228.G172.B105

color 3

R168.G174.B203

color 4

R90.G106.B154

color 5

R0.G0.B102

color 6

R215.G212.B206

color 8

R0.G0.B0

Highlight

R153.G0.B0

ObjectFoundation

White

R255.G255.B255

2nd, 3rd & 4th

level Bullet

Lt. divider line

R192.G192.B192

Text

R0.G0.B0

Connector lines

Dk. divider line

128.G128.B128

Table highlight

R244.G225.B206

color 7

R171.G161.B149

216.4 176.1 164.3

31.4

13.4 28.3

247.8

189.5 192.6

0

100

200

300

1H2013 2H2013 1H2014

HCC Others

Delivering steady volumes under challenging market conditions

2.2 2.1 1.9

0.9 0.5

1.3

3.1

2.6

3.2

98.7 85.1 86.2

0.0

1.5

3.0

4.5

1H2013 2H2013 1H2014

HCC Other ASP of HCC

(Mt) (Mt)

72.7 US$/t 99.1 US$/t 124.1 US$/t

(US$/t)

ASP for each sales terms

(US$ mm) (US$ mm)

1

1 For 1H2014, ASP is a blended average of DAP/FOT/C&F, while 1H2013 and 2H2013 ASP was DAP only

Sales volume and ASP (US$/t)

Revenue by product type Revenue by sales terms

HCC sales volume and ASP by sales terms (1H2014)

Financial review

Key revenue metrics

1.3

0.3 0.3

0.0

0.5

1.0

1.5

2.0

DAP GM FOT C&F

119.1

73.5

247.8

189.5 192.6

0

100

200

300

1H2013 2H2013 1H2014

DAP GM FOT and C&F

Do not refresh this file

13

Object title

Conclusion

R0.G0.B102

Table column

heading shading

R234.G234.B234

color 1

1st level bullet

R255.G102.B0

color 2

R0228.G172.B105

color 3

R168.G174.B203

color 4

R90.G106.B154

color 5

R0.G0.B102

color 6

R215.G212.B206

color 8

R0.G0.B0

Highlight

R153.G0.B0

ObjectFoundation

White

R255.G255.B255

2nd, 3rd & 4th

level Bullet

Lt. divider line

R192.G192.B192

Text

R0.G0.B0

Connector lines

Dk. divider line

128.G128.B128

Table highlight

R244.G225.B206

color 7

R171.G161.B149

8.2 6.7

9.4

7.9

17.6

14.6

0

5

10

15

20

Long haul (UHG-TKH) Short haul (TKH-GM)

1H2013

1H2013 1H2013

5.0 5.4

4.4 4.7

9.4 10.1

0

4

8

12

Cash cost Non-cash cost

72.1

68.5

60

65

70

75

1H2013 1H2014

38.2

36.6

30

32

34

36

38

40

(US$/t)

(US$/t)

(US$/t)

1 Net washed HCC delivered cash cost at GM, includes mining, processing, handling, transportation, logistics, site administration, inventory losses, royalties and fees

(US$/t)

Transportation cost Total operating cash cost at GM¹

Maintaining effective cost control whilst focusing on operational productivity

Mining cost Processing cost

Financial review

Key cost metrics (per HCC product sold)

1H2014 1H2014

1H2014

Do not refresh this file

14

Object title

Conclusion

R0.G0.B102

Table column

heading shading

R234.G234.B234

color 1

1st level bullet

R255.G102.B0

color 2

R0228.G172.B105

color 3

R168.G174.B203

color 4

R90.G106.B154

color 5

R0.G0.B102

color 6

R215.G212.B206

color 8

R0.G0.B0

Highlight

R153.G0.B0

ObjectFoundation

White

R255.G255.B255

2nd, 3rd & 4th

level Bullet

Lt. divider line

R192.G192.B192

Text

R0.G0.B0

Connector lines

Dk. divider line

128.G128.B128

Table highlight

R244.G225.B206

color 7

R171.G161.B149

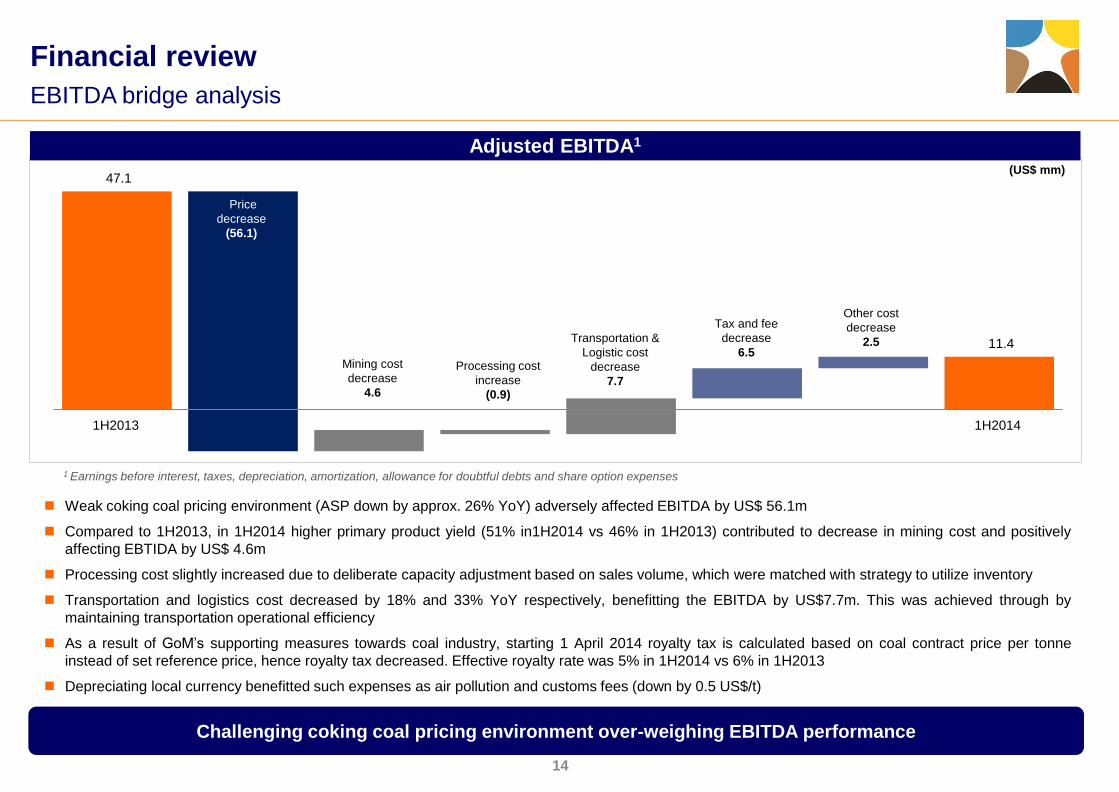

1H2013

47.1

11.4

US$m

Tax and fee

decrease

6.5 Processing cost

increase

(0.9)

Other cost

decrease

2.5

Mining cost

decrease

4.6

Price

decrease

(56.1)

Transportation &

Logistic cost

decrease

7.7

Challenging coking coal pricing environment over-weighing EBITDA performance

1 Earnings before interest, taxes, depreciation, amortization, allowance for doubtful debts and share option expenses

Weak coking coal pricing environment (ASP down by approx. 26% YoY) adversely affected EBITDA by US$ 56.1m

Compared to 1H2013, in 1H2014 higher primary product yield (51% in1H2014 vs 46% in 1H2013) contributed to decrease in mining cost and positively

affecting EBTIDA by US$ 4.6m

Processing cost slightly increased due to deliberate capacity adjustment based on sales volume, which were matched with strategy to utilize inventory

Transportation and logistics cost decreased by 18% and 33% YoY respectively, benefitting the EBITDA by US$7.7m. This was achieved through by

maintaining transportation operational efficiency

As a result of GoM’s supporting measures towards coal industry, starting 1 April 2014 royalty tax is calculated based on coal contract price per tonne

instead of set reference price, hence royalty tax decreased. Effective royalty rate was 5% in 1H2014 vs 6% in 1H2013

Depreciating local currency benefitted such expenses as air pollution and customs fees (down by 0.5 US$/t)

Adjusted EBITDA1

Financial review

EBITDA bridge analysis

(US$ mm)

1H2014

Do not refresh this file

15

Object title

Conclusion

R0.G0.B102

Table column

heading shading

R234.G234.B234

color 1

1st level bullet

R255.G102.B0

color 2

R0228.G172.B105

color 3

R168.G174.B203

color 4

R90.G106.B154

color 5

R0.G0.B102

color 6

R215.G212.B206

color 8

R0.G0.B0

Highlight

R153.G0.B0

ObjectFoundation

White

R255.G255.B255

2nd, 3rd & 4th

level Bullet

Lt. divider line

R192.G192.B192

Text

R0.G0.B0

Connector lines

Dk. divider line

128.G128.B128

Table highlight

R244.G225.B206

color 7

R171.G161.B149

13.6

80.2

142.3

87.1

15.3

16.2

54.8

23.2

28.3

14.4

27.7

19.9

73.9

50.6

12.2

47.9

49.5

21.6

- 5.5

7.3

24.9

63.0

204.9

296.2

212.5

41.9

9.3

0

50

100

150

200

250

300

2009 2010 2011 2012 2013 1H2014

CHPP Water and Power Others Road Railway

(US$ mm)

Note: Others include workers’ camp, township, airport, trucks, workshops, main office building, warehouse and other PPE

With established production capacity, MMC is well positioned to benefit from market recovery

Capital expenditure profile

Financial review

Development capital expenditure plan has been accomplished

Do not refresh this file

16

Object title

Conclusion

R0.G0.B102

Table column

heading shading

R234.G234.B234

color 1

1st level bullet

R255.G102.B0

color 2

R0228.G172.B105

color 3

R168.G174.B203

color 4

R90.G106.B154

color 5

R0.G0.B102

color 6

R215.G212.B206

color 8

R0.G0.B0

Highlight

R153.G0.B0

ObjectFoundation

White

R255.G255.B255

2nd, 3rd & 4th

level Bullet

Lt. divider line

R192.G192.B192

Text

R0.G0.B0

Connector lines

Dk. divider line

128.G128.B128

Table highlight

R244.G225.B206

color 7

R171.G161.B149

Operating environment

Business review

Financial review

Outlook

Agenda

Do not refresh this file

17

Object title

Conclusion

R0.G0.B102

Table column

heading shading

R234.G234.B234

color 1

1st level bullet

R255.G102.B0

color 2

R0228.G172.B105

color 3

R168.G174.B203

color 4

R90.G106.B154

color 5

R0.G0.B102

color 6

R215.G212.B206

color 8

R0.G0.B0

Highlight

R153.G0.B0

ObjectFoundation

White

R255.G255.B255

2nd, 3rd & 4th

level Bullet

Lt. divider line

R192.G192.B192

Text

R0.G0.B0

Connector lines

Dk. divider line

128.G128.B128

Table highlight

R244.G225.B206

color 7

R171.G161.B149

Recovery trajectory for the pricing of coking coal in China and globally remains uncertain in 2H2014

Sizeable reduction in forecast coal output for 2H2014 was announced in August 2014 by some of the largest coal producers in

China, signaling that other Chinese coal producers may follow suit

The Group will aim to expand its sales and distribution channels reaching its end-user customers located in the main steel

producing regions in China. As such, it is expected to sell up to 40% of washed HCC volumes through its sales and distribution

network whilst focusing on improving efficiency of inland logistics arrangements

Group’s full year sales volume target 4.5-5.0 Mt washed HCC and 1.8-2.0 Mt middlings, subject to market conditions

The Group will continue to monitor and assess the market situation whilst prioritizing its focus on liquidity, working capital

management, cost control, operational efficiency and productivity, while, continuing to enhance the Group’s core

competitiveness, allowing it to maintain its market share and sales volumes in 2014

ROM coal mining and processing volumes to be adjusted to actual sales volumes

Overall management strategy is to reduce product coal inventory levels, with production costs expected to be controlled for the

remainder of the year

The Group, together with its joint-venture partners, will remain fully committed to support the successful execution of Cross-

Border Railway project

Once complete, the Cross-Border Railway is expected to facilitate export from Mongolia to China, with the Group having

unrestricted access on a non-discriminatory and equal treatment basis

The Cross-Border Railway is expected to significantly improve logistics efficiency and further reduce transportation costs

Market conditions

Cost control and

liquidity

management

Cross-Border

Railway project

Outlook

Outlook

To continue focus on optimizing the allocation of resources & driving efficiency

THANK YOU

Mongolian Mining Corporation

16F Central Tower

Sukhbaatar District

Ulaanbaatar 14200

Mongolia

www.mmc.mn

![What is the name of the R2 unit that flies with Luke? 2 A]R2D8 B]R2D2 C]R234 D]Han Solo A]R2D8 B]R2D2 C]R234 D]Han Solo.](https://static.fdocuments.us/doc/165x107/56649ce55503460f949b200f/what-is-the-name-of-the-r2-unit-that-flies-with-luke-2-ar2d8-br2d2-cr234.jpg)