PITCH MADISON ADVERTISING REPORT 2018 · PDF fileSam Balsara Vikram Sakhuja Nilesh Bagaria The...

15

ADEX GROWTH AFFECTED BY AFTER-EFFECTS OF DEMONETIZATION AND GST 2017 GROWTH IS 7.4%; WITH TRADITIONAL MEDIA GROWING ONLY 4% 2018 GROWTH EXPECTED TO BE 12.03%, AFTER TWO DISAPPOINTING YEARS PITCH MADISON ADVERTISING REPORT 2018

Transcript of PITCH MADISON ADVERTISING REPORT 2018 · PDF fileSam Balsara Vikram Sakhuja Nilesh Bagaria The...

ADEX GROWTH AFFECTED BY AFTER-EFFECTS OF

DEMONETIZATION AND GST

2017 GROWTH IS 7.4%;

WITH TRADITIONAL MEDIA GROWING ONLY 4%

2018 GROWTH EXPECTED TO

BE 12.03%, AFTER TWO

DISAPPOINTING YEARS

PITCH MADISON ADVERTISING REPORT 2018

Sam Balsara Vikram Sakhuja Nilesh Bagaria

The Indian Media & Advertising industry suffered the after-effects of demonetization and introduction of the Goods & Services Tax (GST), severely

stunting the growth of Adex in 2017. Upsetting our projected growth rate of 13.5% for 2017, the industry actually grew by only 7.4%, with traditional media showing just 4% growth. 2018 promises to be a better year, with the economy expected to recover and market to grow 12.03%, adding Rs 6,392

crore to Adex to reach a total size of Rs 59,530 crore

That 2017 was a bad year in terms of growth is well-known. But how bad was it for the Indian Media and Advertising

industry? We are sorry to report that our analysis shows that Traditional Media during 2017 grew by only 4% - the lowest in half a decade. It is thanks to Digital Media, which continued its onward march and grew by 27.2% in 2017, that we are able to report an overall Adex growth of 7.4%, taking the total market up from Rs 49,480 crore to Rs 53,138 crore.

Readers will recall that in 2016, on the back of demonetization, the Indian advertising market had lost Rs 1,650 crore in two

months - November and December. The total Adex, which had been growing by 16% till October 2016, came down to 12.5%, for the whole year. Adex was slow to recover from the impact of demonetization and the first quarter of 2017 saw a de-growth of -2% and growth of

a mere 2% in the second quarter on the back of IPL, which garnered close to Rs 1,300 crore in advertising money, and a huge shift in demand for FTA channels because of rural viewership registered by BARC. Just when we expected Adex to gather steam, the Goods and Services Tax (GST) was announced in July and the market saw a drop of close to 20% in traditional media over June 2017, and a drop of 5% as compared to July 2016. Mercifully, the festive period brought cheer to Adex, and it grew from August, 2017 to December, 2017 by 13%. But because of the slow start in the first half and a drop in July, the whole year’s Adex is estimated at Rs 53,138 crore, i.e., growth of a mere 7.4%. With a growth rate of 7.4%, the Indian market has lost its stellar position of being the fastest growing advertising market in the world and has conceded that position to Russia, going by WARC estimates of international markets.

`25,026

`49,480GROWTH %

YE

AR

LY S

PE

ND

S (R

s C

RO

RE

)

2010 2011 2012 2013 2014 2015 2016 2017

INDIAN ADVERTISING MARKET OVER LAST 8 YEARS

`53,138

12.03%

`27,433`28,854

`32,106 `37,405`43,991

PITCH MADISON AD REPORT 2018

5.2%

9.6%

12.5%

11.3%

16.5%

17.6%

7.4%

27.8%

4 5

GROWTH FORECAST FOR 2018

CATEGORY CONTRIBUTION & CATEGORY GROWTH ACROSS TV + PRINT + RADIO IN 2017

FMCG

Auto

Telecom

Education

Real Estate & Home Improvement

HH Durables

e-commerce

Clothing, Fashion Jewellery

BFSI

Retail

Travel & Tourism

Media

Corporate

Alcoholic Beverages

Others

TOTAL

12919

4217

3153

2099

1798

1719

1634

1553

1445

1317

714

681

567

251

6098

40165

32%

10%

8%

5%

4%

4%

4%

4%

4%

3%

2%

2%

1%

1%

15%

100%

3%

5%

7%

6%

-3%

2%

7%

6%

4%

7%

8%

2%

4%

1%

2%

4%

427

187

193

111

-55

37

113

88

60

88

53

10

24

1

97

1434

30%

13%

13%

8%

-4%

3%

8%

6%

4%

6%

4%

1%

2%

0%

7%

100%

TV + Print + Radio - 2017

Product Category

Category Contribution

In Rs crore

in %

Category Growth %

2017/ 16

Contribution to Growth

in %In Rs crore

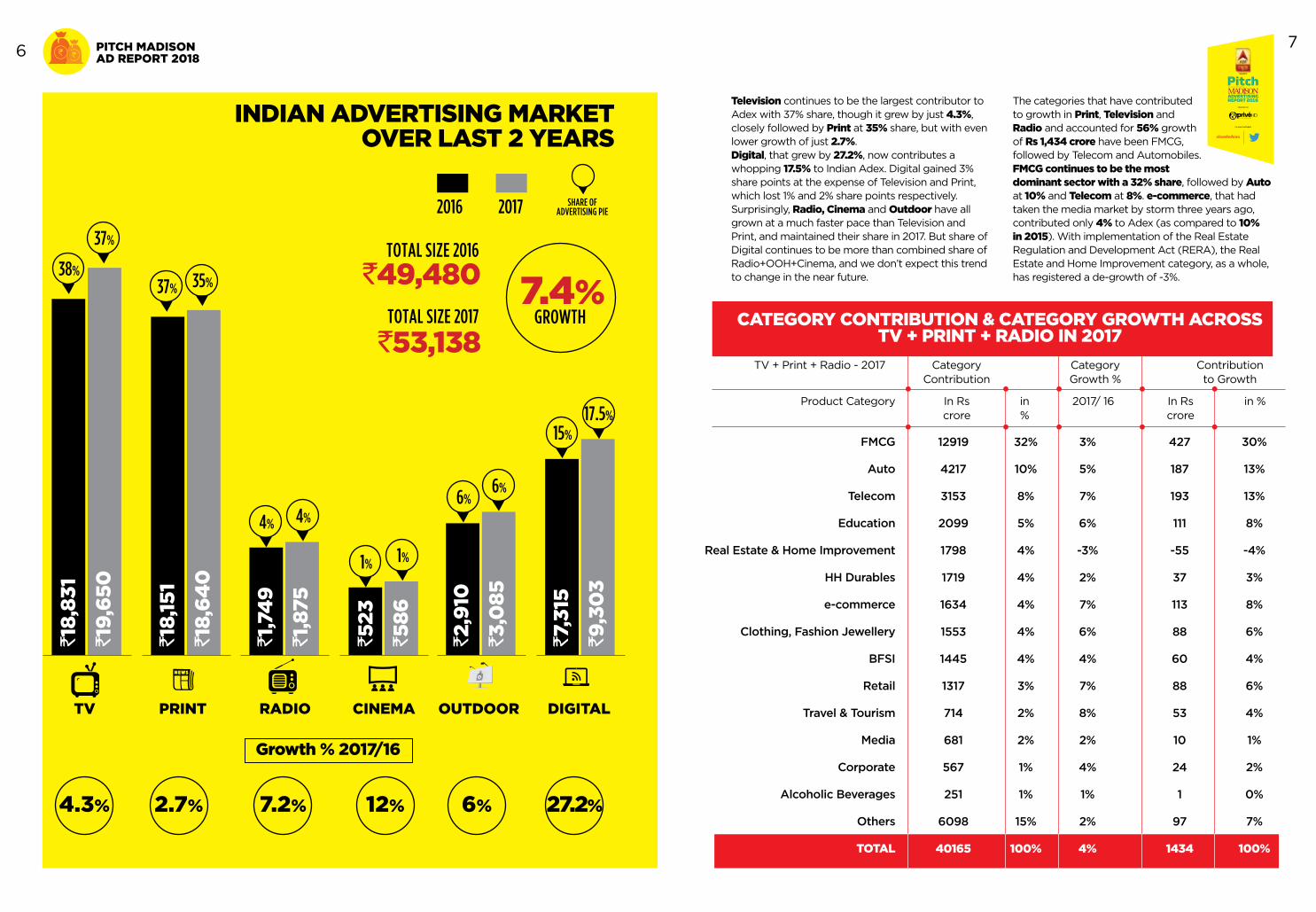

Television continues to be the largest contributor to Adex with 37% share, though it grew by just 4.3%, closely followed by Print at 35% share, but with even lower growth of just 2.7%. Digital, that grew by 27.2%, now contributes a whopping 17.5% to Indian Adex. Digital gained 3% share points at the expense of Television and Print, which lost 1% and 2% share points respectively. Surprisingly, Radio, Cinema and Outdoor have all grown at a much faster pace than Television and Print, and maintained their share in 2017. But share of Digital continues to be more than combined share of Radio+OOH+Cinema, and we don’t expect this trend to change in the near future.

The categories that have contributed to growth in Print, Television and Radio and accounted for 56% growth of Rs 1,434 crore have been FMCG, followed by Telecom and Automobiles. FMCG continues to be the most dominant sector with a 32% share, followed by Auto at 10% and Telecom at 8%. e-commerce, that had taken the media market by storm three years ago, contributed only 4% to Adex (as compared to 10% in 2015). With implementation of the Real Estate Regulation and Development Act (RERA), the Real Estate and Home Improvement category, as a whole, has registered a de-growth of -3%.

`18,

831

`18,

151

`1,7

49

`523

`2,9

10

`7,3

15

`19,

650

`18,

640

`1,8

75

`586

`3,0

85

`9,3

03

2016 2017 SHARE OF ADVERTISING PIE

38%

37%

37% 35%

4% 4%

1% 1%

6%6%

15%

17.5%

TV PRINT RADIO CINEMA OUTDOOR DIGITAL

INDIAN ADVERTISING MARKET OVER LAST 2 YEARS

4.3% 2.7% 7.2% 12% 6% 27.2%

Growth % 2017/16

`49,480

`53,138

TOTAL SIZE 2016

TOTAL SIZE 2017

PITCH MADISON AD REPORT 20186 7

7.4%GROWTH

Coming on the back of two poor years - we saw growth suppressed to 12.5% in 2016 and 7.4% in 2017 - we are tempted to predict a high growth year 2018, that is in keeping with the growth rates achieved in the last decade. For, you can’t keep

advertising - or for that matter the Indian economy - down for too long! However, our optimism is tempered by the fact that the Government is set on its reform agenda for long term good of the economy. Some other reform introduced during the year, which is good for the economy in the long run, may have the short term impact of destabilizing the economy once again, the way demonetization and GST did. However, there are a number of factors that lead us to believe that growth of Adex should be good in 2018. Some of these are:

Signs of return of Consumer spending

Benefits of GST to start accruing

Eight State Assembly elections scheduled during the year, preceded by State Government publicity drives on their achievements

Increased publicity by the Central Government on account of ensuing Lok Sabha elections in 2019

As many as 16 new launches by automobile companies

Increased activity in the sporting arena from both cricketing and non-cricketing leagues and FIFA World Cup

Strong come-back by FMCG companies on the back of increased Rural demand

Launch of new Ayurvedic lines by FMCG companies

Increased activity in BFSI area, especially small banks and payment banks

Taking into account all of the above, we expect Adex to grow by 12.03%, taking it to a total of Rs 59,530 crore or nearly Rs 60,000 crore in 2018. The highest growth rate should be achieved by Digital (25%), followed by Cinema (14%), TV (13%), Radio & Outdoor (10% each) and Print (5%) in 2018.

The year 2018 should provide relief to the Media market after two disappointing years. The general expectation is that with Lok Sabha elections in 2019, the Government is likely to support all sections of industry, including Media and all classes of consumers. Gains from implementation of GST should also begin to flow into the economy. Investment in infrastructure and rural schemes should put more money in the hands of consumers, which should lead to a buoyant economy, and a buoyant economy always translates to happy times for Media.

8 9

TELEVISION10 11

Television grew a mere 4.3% - its lowest in the last five years – adding just Rs 820 crore to Adex in 2017 to reach a size of

Rs 19,650 crore. However, it still remained the largest contributor to the advertising

pie. In 2018, Television is expected to grow 13% on the back of FMCG

players targeting Rural, election-related advertising and increased spends around sporting properties and by BFSI players

In 2017, the Television Adex grew by a mere 4.3% and reached Rs 19,650 crore. This is the lowest growth Television has witnessed in the last five

years. Growth remained flat in the January-March 2017 period on account of the after-effects of demonetization and even in the latter part of the year, it did not grow as expected on account of GST, belying our projected growth of 13%.

It is significant to note that growth is low, despite the addition of 100 new channels including cable channels, which in turn contributed to an increase in FCT supply of 11% in 2017. The new channels launched were mainly in News and Movie genres. These new channels contributed Rs 100 crore to Adex. On the other hand, our comparison of only like-to-like channels shows an increased FCT supply of 7% leading one to conclude that on an average, television rates were suppressed. However, advertisers could not take full advantage of lower rates, because of even lower viewership and TV ratings of most used programmes resulting in increase in Cost Per Rating Point (CPRP) to the advertiser.

HD emerged stronger during the year with the

launch of 22 HD channels now reaching 50 million homes, split equally between Urban and Rural. Viewership of HD channels has also seen exponential growth and we estimate that HD is today a Rs 2,000 crore advertising market, contributing over 10% to the Television Adex.

While growth may have been low during the year at just 4.3%, Television continues to be the largest contributor to the advertising pie.

FMCG continues to rule the roost, contributing 51% to the total Television advertising spends, followed by Telecom at 12% and Auto at 8%. It’s the same three categories that have mainly contributed to the growth of Rs 820 crore in Television Adex in 2017. E-Commerce maintained its contribution at 4%.

Hindi GECs, including FTA, contributed 28% of overall Television Adex, with Hindi being by far the largest contributor. FTA channels have seen robust growth in viewership during the year and account for 19% of the Hindi GEC plus FTA genre.

In terms of FCT growth, Hindi Movies, English Info/Movies and South regional show substantial increase in 2017.

201338.7% 37.9% 39.24% 38.06% 36.98% 37.3%

2014 2015 2016 2017 2018 P

`12,419`14,158

`17,261

`18,831`19,650

`22,205GROWTH %

SHARE OF ADEX

YE

AR

LY S

PE

ND

S (R

s C

RO

RE

)

13%

9%

22%

14%

8%4%

TV – GENRE-WISE REVENUE CONTRIBUTION IN 2017

Hindi GEC + FTANews

Tamil SatSports

Hindi Sat - MoviesTelugu Sat

Marathi SatKannada Sat

Bengali SatMusic

KidsMalayalam Sat

InfoMovies EngEng Niche

Others

28%11%9%9%5%5%4%4%4%3%3%3%3%3%2%6%

4%4%10%-7%35%24%-10%9%21%-17%0%18%31%21%-8%9%

5500 – 60002000 – 24001800 – 20001700 – 1900900 – 1100900 – 1100800 – 1000700 – 800650 – 750550 – 650500 – 600500 – 600500 – 600500 – 600300 – 400

1300 – 1400

GenresRevenue

Contribution in 2017

FCT Growth

2017 / 16

Approx Revenue

in Rs crore

In 2017, the Television Adex grew by a mere

4.3% and reached Rs 19,650 crore.

This is the lowest growth Television has witnessed in

the last five years

TV ADEX

CATEGORY CONTRIBUTION & CATEGORY GROWTH IN TV IN 2017

FMCGTelecom

AutoHH Durablese-commerce

Real Estate & Home ImprovementClothing Fashion Jewellery

BFSIMedia

CorporateTravel & Tourism

Alcoholic BeveragesEducation

RetailOthersTOTAL

1006124491513859855575531403392292246238220181834

19650

51%12%8%4%4%3%3%2%2%1%1%1%1%1%4%

100%

4%8%6%5%5%1%3%3%-5%2%7%1%6%6%4%4%

37017887424461811

-207172121135819

45%22%11%5%5%1%2%1%

-2%1%2%0%1%1%4%

100%

TV - 2017

Product Category

Category Contribution

in %

Category Growth %

2017 / 16

Contribution to Growth

in %In Rs crIn Rs cr

FORECAST FOR 2018

TELEVISION

We expect Television Adex to grow by another Rs 2,555 crore or 13% in 2018 to reach Rs 22,205 crore. The key factors that will lead to this high growth are:

12 13

FMCG marketers, who are turning

bullish on the back of expectation of revival

of Rural demand

Increased activity in sporting arena from both cricketing and

non-cricketing leagues

Publicity by the Government on account of ensuing eight State

Assembly Elections and Lok Sabha Elections in 2019, which will lead to a spurt in Television campaigns

to announce government achievements and election-

related advertising

On the negative side, Television may start to lose some advertising to OTT platforms, because

some viewers may prefer to watch Television content on OTT platforms, thanks to low data

tariffs. With this growth of 13%, TV is expected to maintain its share of Adex at 37%.

Increased activity in BFSI area

FMCGAuto

EducationRetail

Real Estate & Home ImprovementClothing, Fashion Jewellery

BFSIHH Durables

E – CommerceTelecom

Travel & TourismCorporate

MediaAlcoholic Beverages

OthersTOTAL

2692256918201044103595690580968659238123817111

473018640

14%14%10%6%6%5%5%4%4%3%2%1%1%0%25%

100%

2%4%5%7%-7%7%4%-1%11%1%8%9%13%-9%1%3%

51899468-806438-8655

291920-137

489

10%18%19%14%-16%13%8%-2%13%1%6%4%4%0%8%

100%

PRINT – 2017

PRODUCT CATEGORY

CATEGORY CONTRIBUTION

in %

CATEGORY GROWTH %

2017 / 16

CONTRIBUTION TO GROWTH

in %In Rs crIn Rs cr

DISMAL GROWTHPrint Adex grew only 2.7% in 2017, the lowest seen in nine years. Despite this, it continues to be the second highest contributor to Adex, after TV, with a share of 35%. In 2018, the Print advertising market is expected to grow by 5% to come close to Rs 20,000 crore, with regional publications leading the growth

Print grew by a mere 2.7% during the year. This is the lowest growth we have seen in nine years. But it continues to be the second

highest contributor after Television with a share of 35% in the Adex. It is significant to note that for the last three years, Print has been steadily losing share at a rate of 1% share point every year, but this year, the decline accelerated and Print lost 2% share points. Dailies increased 3.4%, a bit higher than the total Print Adex, because Magazines as a medium failed to gain advertiser interest for the third year in succession.

Print, like the overall Adex, de-grew in the first quarter by as much as -5%, and then marginally grew by 3% in the second quarter before growing at 9% in the last quarter. One could thus conclude that Print bore the biggest brunt on account of demonetization and GST.

FMCG, Auto, Education and Retail, the main categories that used Print, increased their dominance from 50% share last year to 62% in 2017. In terms of category contribution, FMCG and Auto are the largest contributors to the Print

pie with a contribution of 14% each, followed by education at 10%. The Real Estate category, again a staple for newspapers, saw a degrowth of -7%, thanks to RERA.

While only four categories account for 75% of Television advertising, it takes as many as 13 categories to contribute the same percentage to Print advertising, demonstrating once again that Print has a wide-spread clientele and, therefore, is less vulnerable.

In terms of volume, Hindi publications continue to be ahead of English publications, contributing 34% of the total volume. English publications come close behind at 27%. Contrary to popular belief, volume in English publications has grown by 4% while volume in Hindi publications degrew by -4%. The degrowth in volume of Hindi publications has been observed for the first time in many years. Among other languages, Kannada and Gujarati publications have shown a substantial increase in volume, but Punjabi, Urdu and Tamil publications show a decline.

2013 2014 2015 2016 2017 2018 P

`13,167`15,274

`16,935

`18,151 `18,640

`19,571GROWTH %

YE

AR

LY S

PE

ND

S (R

s C

RO

RE

)

11%

16%

1O%

3% 5%7%

14 15

41% 40.8% 38.5% 36.7% 35.1% 32.9%SHARE

OF ADEX

CATEGORY CONTRIBUTION & CATEGORY GROWTH IN PRINT IN 2017

PRINT ADEX

PRINT – LANGUAGE-WISE PUBLICATION VOLUME IN COLUMN CENTIMETRES IN 2017 (CC IN MILLION)

HindiEnglishMarathiTelugu

TamilGujarati

KannadaMalayalam

OriyaBengaliPunjabi

AssameseUrdu

TOTAL

119.888.529.323.621.913.813.310.79.25.32.72.51.2

342

114.892.229.623.421.314.715.011.09.15.52.22.41.1

342

-4%4%1%-1%-3%6%13%2%0%3%

-19%-4%-8%

0%

34%27%9%7%6%4%4%3%3%2%1%1%0%

100%

Language Yr 2016 Yr 2017Growth %( Yr 17 /

16)

Contribution in %

(2017)

FORECAST FOR 2018 We expect Print Adex to grow by 5% in 2018, taking the Print market close to Rs 20,000 crore. Findings from the just-released IRS Survey are likely to be used (and misused!) by various publications to show growth in readership, although the coveted Average Issue Readership at the macro level has not grown.

We expect growth to come in from regional publications despite the fact that most languages have dropped in Average Issue Readership. Print loyalists like Auto and Mobile handsets (both because of new launches) and Education, besides the Government and election-related advertising, are likely to be growth drivers.

Robust growth in magazine readership, as discovered by IRS, should result in a spurt and growth of this sector.

16

OOH

2013 2014 2015 2016 2017 2018 P

`2,027`2,333

`2,665`2,910

`3,085`3,395GROWTH %

YE

AR

LY S

PE

ND

S (R

s C

RO

RE

)

14%15%

9%

6%9%

10%

IT WAS A ‘JIO’ YEAR

In 2017, the Out of Home (OOH) market grew by 6% and now stands at Rs 3,085 crore. While Retail topped the list of spenders on OOH, Telecom recorded the highest growth in OOH advertising, courtesy the high-voltage launch of Reliance Jio. In 2018, Outdoor is expected to grow by 10% to reach a size of Rs 3,395 crore, on the back of upcoming elections and Government campaigns

The Out of Home (OOH) advertising market has grown by 6% in 2017 to reach a size of Rs 3,085 crore.

Its contribution to the advertising pie was 5.8%. The conventional OOH market grew at 7% and Transit Media at 4%.

Retail, Consumer Services and Real Estate are the top three consuming categories of OOH. However, Consumer Services (Hospital, Restaurant and Education) reduced spends by 8% and Real Estate spends too declined by 11%. The highest growth was recorded by the Telecom category at 29%, attributable to the launch of Reliance Jio with its aggressive pricing strategy. Mumbai continues to be the largest contributor to OOH at 18%, followed by Delhi at 14% and Bangalore at 11%.

CATEGORY CONTRIBUTION & CATEGORY GROWTH IN OOH IN 2017

Organized Retail Hospitals, Restaurants, Education

Real Estate & ConstructionTelecom

FMCGFinancial Services

AutoMedia

E-CommerceElectronic Durables

Petroleum/LubricantsPharmacy

EnergyOthers

TOTAL

4813873622852682542231551237024240

427

3085

16%13%12%9%9%8%7%5%4%2%1%1%0%14%

100%

8%-8%-11%29%16%7%6%14%12%-11%17%-14%-75%18%

6%

34-34-43643716131913-83-4-265

175

19%-19%-24%37%21%9%8%11%7%-5%2%-2%-1%37%

100%

OOH 2017

PRODUCT CATEGORY

CATEGORY CONTRIBUTION

in %

CATEGORY GROWTH %

2017 / 16

CONTRIBUTION TO GROWTH

in %In Rs crIn Rs crFORECAST FOR 2018 We expect the Outdoor advertising sector to grow by 10% in 2018, taking its Adex to Rs 3,395 crore. Outdoor is expected to substantially gain from the Central and State Government’s publicity and election campaigns, because of the ensuing eight State Assembly Elections in 2018 and Lok Sabha Elections in 2019.

18 19

6.3% 6.2% 6.1% 5.9% 5.8% 5.7%SHARE

OF ADEX

OOH ADEX

DIGITAL

2013 2014 2015 2016 2017 2018 P

`3,050`3,970

`5,120

`7,315`9,303

`11,629GROWTH %

YE

AR

LY S

PE

ND

S (R

s C

RO

RE

)

43%

29%30%32%

27%25%

Digital grew by 27%, adding nearly Rs 2000 crore to Adex,

to reach a size of Rs 9,303 crore in 2017. It now contributes a whopping 17.5%

to Indian Adex, with Video gaining huge ground, along with Search, Display, Native

and Programmatic advertising. Digital advertising is projected to grow by about 25% to cross the Rs 10,000 crore mark and

grow to Rs 11,629 crore in 2018

Digital Adex continues to grow unabated and in 2017, grew by a further 27% on the back of 43%

growth in 2016 over 2015. As you will see from the table below, in the last five years, Digital has grown at a compounded annual growth rate of 32%. At Rs 9,303 crore, Digital is 17.5% of Adex in 2017. It was only 8% of Adex in 2012.

Though there has been exponential growth in video consumption over the past year, Display, Native and Programmatic have also picked up rather well with Mobile becoming the primary choice to consume content. Newer display advertising elements, Mobile, Online Video and Programmatic are all helping attract more advertising investment into Digital.

BOOMING!

Vertical 2015 2016 2017Search 1860 2660 3010

Display + Programmatic + Ad Networks + Native 2315 2765 2993

Video 945 1890 3300

Total 5120 7315 9303

Video as % of total 18% 26% 35%

Platform 2015 2016 2017Mobile 2700 4550 7256

Desktop 2420 2765 2047

Total 5120 7315 9303

Mobile as % of Total 53% 62% 78%

DIGITAL ADEX OVER LAST 3 YEARS (IN RS CRORE)

(Ad spend figures in Rupees crore)

FORECAST FOR 2018 We expect the momentum in Digital to continue and project a growth rate of 25%, taking the Digital Adex up to Rs 11,629 crore in 2018. As the reach of Digital crosses 450 million and the smartphone Internet user-base crosses 300 million, Digital is likely to hit the big boys of Media in a bigger way than it already has. FMCG, Telecom, BFSI and Real Estate will continue to be growth drivers for Digital. e-commerce will remain the backbone of Digital Adex.

Facebook and YouTube will continue to dominate the video platform along with OTTs such as Hotstar, Voot and SonyLiv making their presence felt on the back of investments in original content.

With Mobile ruling the roost, Desktop advertising will get marginalized. We expect Native and Programmatic advertising to make rapid strides in 2018.

Digital Adex will continue to register the highest growth in Adex for the 10th year in a row.

20 21

9.5% 10.6% 11.6% 14.8% 17.5% 19.5%SHARE

OF ADEX

DIGITAL ADEX

RADIO

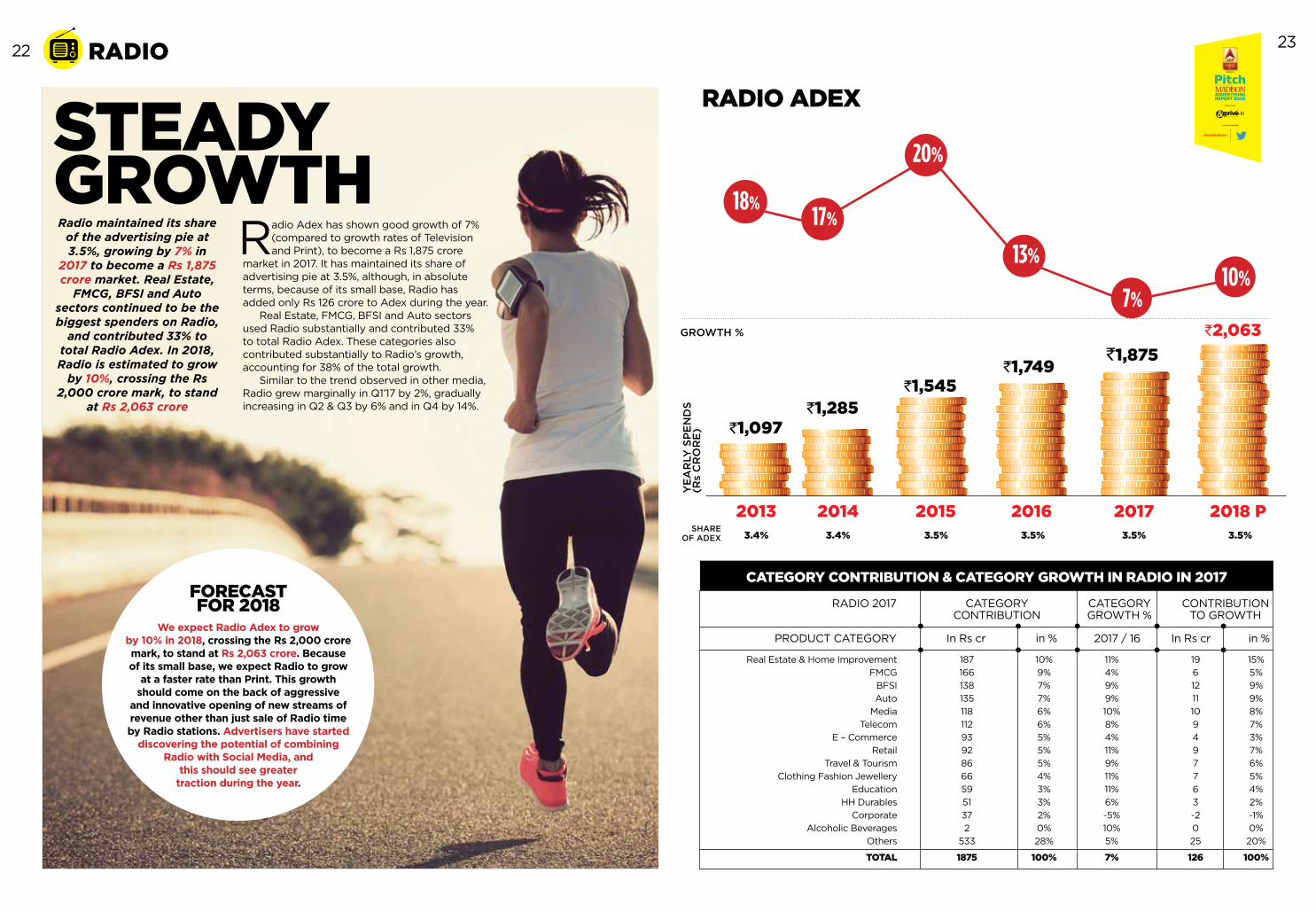

STEADY GROWTHRadio maintained its share

of the advertising pie at 3.5%, growing by 7% in

2017 to become a Rs 1,875 crore market. Real Estate,

FMCG, BFSI and Auto sectors continued to be the biggest spenders on Radio,

and contributed 33% to total Radio Adex. In 2018, Radio is estimated to grow

by 10%, crossing the Rs 2,000 crore mark, to stand

at Rs 2,063 crore

Radio Adex has shown good growth of 7% (compared to growth rates of Television and Print), to become a Rs 1,875 crore

market in 2017. It has maintained its share of advertising pie at 3.5%, although, in absolute terms, because of its small base, Radio has added only Rs 126 crore to Adex during the year.

Real Estate, FMCG, BFSI and Auto sectors used Radio substantially and contributed 33% to total Radio Adex. These categories also contributed substantially to Radio’s growth, accounting for 38% of the total growth.

Similar to the trend observed in other media, Radio grew marginally in Q1’17 by 2%, gradually increasing in Q2 & Q3 by 6% and in Q4 by 14%.

2013 2014 2015 2016 2017 2018 P

`1,097`1,285

`1,545`1,749

`1,875`2,063GROWTH %

YE

AR

LY S

PE

ND

S (R

s C

RO

RE

)

20%

17%18%

7%10%

13%

CATEGORY CONTRIBUTION & CATEGORY GROWTH IN RADIO IN 2017

Real Estate & Home ImprovementFMCG

BFSIAuto

MediaTelecom

E – CommerceRetail

Travel & TourismClothing Fashion Jewellery

EducationHH Durables

CorporateAlcoholic Beverages

Others

TOTAL

187166138135118112939286665951372

533

1875

10%9%7%7%6%6%5%5%5%4%3%3%2%0%28%

100%

11%4%9%9%10%8%4%11%9%11%11%6%-5%10%5%

7%

1961211109497763-2025

126

15%5%9%9%8%7%3%7%6%5%4%2%-1%0%20%

100%

RADIO 2017

PRODUCT CATEGORY

CATEGORY CONTRIBUTION

in %

CATEGORY GROWTH %

2017 / 16

CONTRIBUTION TO GROWTH

in %In Rs crIn Rs cr

FORECAST FOR 2018

We expect Radio Adex to grow by 10% in 2018, crossing the Rs 2,000 crore mark, to stand at Rs 2,063 crore. Because of its small base, we expect Radio to grow

at a faster rate than Print. This growth should come on the back of aggressive

and innovative opening of new streams of revenue other than just sale of Radio time by Radio stations. Advertisers have started

discovering the potential of combining Radio with Social Media, and

this should see greater traction during the year.

22 23

3.4% 3.4% 3.5% 3.5% 3.5% 3.5%SHARE

OF ADEX

RADIO ADEX

CINEMA

NOT YET A BLOCKBUSTERA low base helped Cinema advertising grow in double digits, i.e., 12%, in 2017, with Adex reaching Rs 586 crore. Cinema remains a marginal player as it has failed to capture the imagination of brand managers, and this is not expected to change. However, Cinema is expected to grow at 14% in 2018, the second highest growth rate behind Digital, to reach Rs 668 crore

Cinema continues to be a marginal player in Adex, constituting approximately 1% share of the

advertising pie, and notching up total ad spends of Rs 586 crore in 2017. However, Cinema is the only traditional medium that has registered growth in double digits in 2017 – 12% - but because of its low base, the figure does not amount to much.

2013 2014 2015 2016 2017 2018 P

`347`385

`465`523 `586

`668GROWTH %

YE

AR

LY S

PE

ND

S (R

s C

RO

RE

)

21%

11%11%12%12%

14%

FORECAST FOR 2018 We expect Cinema to grow by 14% in 2018, the second

highest growth rate after Digital, taking its Adex to Rs 668 crore. Cinema has been growing steadily in the last

few years due to an increase in number of multiplexes in both the larger cities and towns, digitization of single screens and

growth in regional cinema. However, Cinema has failed to capture the imagination of brand managers, in the face of

aggressive and stiff sales pitches by other Media, and we do not expect this situation to change in 2018.

24 25

CINEMA ADEX

1.1% 1.03% 1.06% 1.06% 1.1% 1.12%SHARE

OF ADEX

Our list of the Top 50 Advertisers in India in 2017 features five new entrants - Honda Cars,

Reliance Retail, Future Retail, United Spirits and Vicco Laboratories – in this elite category. The list includes advertisers from diverse categories, including FMCG, Telecom, Auto, e-commerce and Modern Retail.

In keeping with the tumultuous nature of the year, there are a large number of shifts in the pecking order, with 17 advertisers gaining rank and 22 advertisers dropping rank. Among those who gained rank are Vivo(+30), Reliance Jio(+29), Oppo(+26), Patanjali(+10), Godrej Consumer(+3), Samsung(+3) are Hero(+2), while those that have dropped in rank include Airtel(-9), ITC(-7), Mondelez(-2), Honda Motors(-2), LIC(-1) and Colgate(-1).

The Top 50 advertisers account

for 34% of the advertising market. This number is significant, considering that there are over two lakh advertisers in Print and over 12,500 advertisers on TV. The Top 10 advertisers account for as much as 16% of the total market and contribute to 46% of the total 50 list.

HUL, Amazon, P&G & Reckitt continue to lead the pack of top advertisers of India in 2017 as well.

We may mention that many Madison clients feature in this list, but we have strictly refrained from using any confidential information that we are privy to, and arrived at our list and ranking using a standard, structured process.

* A note of caution here - some advertisers who in our list rank above 50 may well be in the Top 50 list in reality or vice-versa.

Moved up in Rank Moved down in Rank

26 27APPROX SPENDS

IN RS CRORE

2700 - 3000900 – 1100600 – 700500 – 600500 – 600500 – 600500 – 600500 – 600400 – 500400 – 500400 – 500400 – 500400 – 500400 – 500300 – 400300 – 400300 – 400300 – 400300 – 400250 – 350250 – 350250 – 350250 – 350250 – 350250 – 350250 – 350200 – 300200 – 300200 – 300200 – 300200 – 300200 – 300200 – 300200 – 300150 – 200150 – 200150 – 200150 – 200150 – 200150 – 200150 – 200150 – 200150 – 200150 – 200150 – 200150 – 200150 – 200100 – 150100 – 150100 – 150

ADVERTISERS

Hindustan Unilever LtdAmazon Online India Procter & GambleReckitt Benckiser Patanjali Ayurved LtdMaruti Suzuki India Godrej Consumer Products LtdSamsung India Oppo IndiaHero MotocorpMondelezVivo Mobile India Glaxo SmithklineITC LtdReliance Jio Honda Motorcycle Bharti AirtelLife Insurance Corp Of IndiaEmami LimitedColgate Palmolive GoogleMarico LtdMahindra & MahindraFlipkart.ComTata MotorsL Oreal IndiaVodafone Coca Cola IndiaHyundai MotorsNestle IndiaIdea CellularBajaj AutoTVS MotorDabur IndiaJohnson & JohnsonPepsi CoApple ComputerHonda Cars IndiaTitan CompanyAsian PaintsVini ProductRenault IndiaReliance Retail LtdNissan Motor Co LtdFuture RetailFord India Wipro GCMMF (Amul)United SpiritsVicco Laboratories

RANK IN 2016

1234156101135129

42167

441481721194920225

29282523242718382631373443

NEW39413233

NEW36

NEW305047

NEWNEW

RANK IN 2017

1234567891011121314151617181920212223242526272829303132333435363738394041424344454647484950