Pillar_III_ABR_29.05.2015

23

1 Alpha Bank Romania Pillar III Disclosures of the year 2014 (In accordance with Regulation (EU) 575/2013)

-

Upload

coconea-nicoleta -

Category

Documents

-

view

214 -

download

1

description

alpha bank

Transcript of Pillar_III_ABR_29.05.2015

1

Alpha Bank Romania Pillar III Disclosures of the year 2014

(In accordance with Regulation (EU) 575/2013)

2

Contents 1 General Information ................................................................................................................................................................................................. 3

1.1 Introduction ........................................................................................................................................................................................................ 3

1.2 Regulatory Framework .................................................................................................................................................................................... 3

1.3 Compliance with the disclosure requirements of CRR / CRD IV .............................................................................................................. 3

1.4 Bank’s Governance .......................................................................................................................................................................................... 3

2 Capital Adequacy Framework ................................................................................................................................................................................ 4

2.1 Alpha Bank’s approach to Pillar I ................................................................................................................................................................... 4

2.2 Pillar II ................................................................................................................................................................................................................. 4

2.3 Own Funds ........................................................................................................................................................................................................ 5

2.3.1 Own Funds structure ................................................................................................................................................................................ 5

2.4 Capital Adequacy .............................................................................................................................................................................................. 6

2.4.1 Main developments and changes impacting capital adequacy ratios Regulatory changes - Implementation of Basel III (CRR 575/2013 and CRD IV) ............................................................................................................................................................................ 6

2.4.2 Capital calculation process ...................................................................................................................................................................... 6

2.4.3 Capital requirements ................................................................................................................................................................................. 7

2.4.4 Capital ratios .............................................................................................................................................................................................. 7

3 Risk Management .................................................................................................................................................................................................... 7

3.1 Risk Management Framework and Principles ............................................................................................................................................. 7

3.2 Risk Governance Structure ............................................................................................................................................................................. 8

3.3 Risk Profile ......................................................................................................................................................................................................... 8

3.4 Risk Management Policies .............................................................................................................................................................................. 9

4 Credit Risk ................................................................................................................................................................................................................. 9

4.1 General information .......................................................................................................................................................................................... 9

4.2 Disclosures with respect to Credit Risk and Asset Quality of Bank’s exposures ................................................................................. 11

4.3 Disclosures for portfolios subject to Standardized Approach .................................................................................................................. 14

5 Credit risk mitigation .............................................................................................................................................................................................. 15

5.1 Collateral valuation and management policies and procedures .............................................................................................................. 15

5.2 Description of the main collateral types eligible for Pillar I calculations ................................................................................................. 15

6. Counterparty credit risk (CCR) ........................................................................................................................................................................... 16

7. Market Risk ............................................................................................................................................................................................................ 17

8. Operational Risk.................................................................................................................................................................................................... 17

9. Interest Rate Risk in the Banking Book ............................................................................................................................................................. 18

9.1 Interest Rate Risk Definition ......................................................................................................................................................................... 18

9.2 Interest Rate Risk Framework ...................................................................................................................................................................... 18

9.3 Interest Rate Risk Identification and Assessment ..................................................................................................................................... 18

9.4 Interest Rate Risk Monitoring ....................................................................................................................................................................... 20

10 Disclosures on Liquidity Risk ............................................................................................................................................................................. 21

11 Leverage ............................................................................................................................................................................................................... 22

12 Remuneration Policy ........................................................................................................................................................................................... 22

12.1 Principles of Remuneration Structuring .................................................................................................................................................... 23

12.2 Remuneration Committee ........................................................................................................................................................................... 23

12.3 Other relevant Stakeholders/Parties ......................................................................................................................................................... 23

3

1 General Information

1.1 Introduction Alpha Bank Romania is one of the Top 10 banks of the financial sector in Romania; The Bank offers a wide range

of high quality financial products and services, including retail banking, SMEs and corporate banking. The Bank operates under the approval of the National Bank of Romania and is subject to the Romanian banking

and accounting law and the specific European regulatory Framework. The Bank with strong position in the local banking system has a high capital ratio. The branch network consisted of 149 Branches as of 31.12.2014.

With consistency and credibility, Alpha Bank Romania supports individual and business clients contributing to the country's economic development.

1.2 Regulatory Framework Alpha Bank Romania is supervised by the National Bank of Romania according to the new “Capital Adequacy of

investment firms and credit institutions” framework, widely known as Basel III, as formalized through the EU Regulation 575/2013 dated 26 June 2013, along with the EU directive 2013/36 dated 26 June 2013. The fundamental principles of the above directive have been incorporated in NBR Regulation 5/2013.

1.3 Compliance with the disclosure requirements of CRR / CRD IV The Bank considers that good governance structures, transparency and disclosure are essential for the purposes

of strengthening market discipline and enhancing financial stability. In this context, the Bank has set a robust internal governance framework, including adequate, efficient and strong internal control and risk management systems.

1.4 Bank’s Governance The leadership and management of the Bank is entrusted to the Board of Directors consisted of up to 9 (nine)

members which have the responsibility to decide on the person who undertakes the Presidency of the Board.

The Members of the Board of Directors have the appropriate qualifications to cover the ”fit and proper criteria” i.e. good reputation, character and integrity, financial or other professional or business experience adequate to the nature and complexity of the credit institution's activity and or the entrusted responsibilities. They must exercise their duties aiming at the proper and effective functioning of the BoD and of the bank in the context of the applicable legal and regulatory framework specific to their position.

The committees of the Board of Directors are the following: • Audit Committee. • Risk Management Committee • Remuneration Committee • Nominations Committee

The Nomination Committee is created in 2014 as a consultative body to the Board of Directors with the objective to assist the Board in what regards its structure and componence

The Nominations Committee consists of the Chairman and of two Members, appointed by the Board of Directors and selected among its Non-Executive Members.

The Members of the Committee have the required expertise and experience.

The Nominations Committee: • assesses the composition, structure size and performance of the Board of Directors and makes recommendations

with regard to any changes. To this end, reviews the appropriateness of the size of the Board relative to its various responsibilities, the overall composition of the Board, taking into considerations such factors as business experience and specific areas of expertise of each Board member; assesses the effectiveness of the Board in meeting its responsibilities.

• recommends to the Board the number, structure and responsibilities of Board committees, advising as well the

Board on the Chair and members of each committee, possible removal from committees, rotation of committee members.

• reviews the adequacy of the charters adopted by each committee of the Board and recommends changes when

necessary.

• assists the Board in developing criteria regarding the independence of members, for identifying and selecting qualified individuals who may be nominated for election to the Board, including replacement in case of l vacancies

• assesses and reports annually to the Board on the individual members and Board’s performance

The Risk Management Committee of the Bank is created in 2014 as a consultative body of the Board of Directors

and consists of the Chairman and of two Members.

The Risk Management Committee is appointed by the Board of Directors and selected from among its Non-Executive Members.

All the Members of the Committee have knowledge of the financial sector and possess experience in the banking sector, especially in risk undertaking and capital management.

The Risk Management Committee recommends to the Board of Directors the risk undertaking and capital

management strategy which corresponds to the business objectives of the Bank. The Risk Management Committee evaluates on an annual basis or more frequently, if necessary:

4

• the adequacy and effectiveness of the risk management policies of the Bank and in particular the compliance with the specified risk tolerance level,

• the appropriateness of limits, the adequacy of provisions and the overall capital adequacy in relation to the amount and type of risks undertaken based.

Furthermore, the Risk Management Committee evaluates the adequacy and effectiveness of the risk management policy and procedures of the Bank specifically in terms of the:

• undertaking, monitoring, and management of risks (market, credit, interest rate, liquidity, operational, other substantial risks) per category of transactions and customers per risk level (i.e. country, profession, and activity).

• determination of the applicable maximum risk appetite on an aggregate basis for each type of risk and further allocation of each of these limits per country, sector, currency, business unit, etc.

• establishment of stop-loss limits or of other corrective actions.

The Risk Management Committee drafts minutes which are submitted to the Board of Directors.

2 Capital Adequacy Framework Alpha Bank Romania implemented the so called Basel III framework, enhancing the former European Directives on

capital adequacy, which consists of the three fundamental pillars of supervision:

• Pillar I specifying the calculation of minimum capital requirements (8% for Total Capital Adequacy ratio, 4.5% for CET 1 ratio). Alpha Bank reports to the National Bank of Romania its capital requirements on a solo basis according to the adopted by the Commission of the Implementing Technical Standards developed by EBA

• Pillar II that sets the principles, criteria and processes required for assessing capital adequacy and risk management systems of the credit institutions.

• Pillar III, aiming at increasing transparency and market discipline, sets the disclosure requirements of key information regarding the exposure of financial institutions to key risks as well as the processes applied for managing them.

The Capital Adequacy framework, apart from the above, defines the regulatory own funds of credit institutions and

addresses other regulatory issues such as monitoring and control of large exposures, open foreign exchange position, concentration risk and the liquidity ratios, the internal audit system, including risk management and regulatory reporting and disclosures.

The methodologies that are adopted for the calculation of the capital requirements are determined by the nature and type of risks the Bank undertakes, the level and the complexity of the Bank’s business and other factors, such as the degree of readiness of the information and software systems.

2.1 Alpha Bank’s approach to Pillar I Alpha Bank calculates Capital Requirements using the following approaches:

• Credit Risk: The Bank follows the Standardized Approach (STA). The calculations are performed using the BWCM system of SUNGARD;

• Operational Risk: The Bank follows the Basic Indicator Approach aiming at using the Advanced Measurement Approach (AMA);

• Market Risk: The Bank uses the Standardized approach.

2.2 Pillar II

The Pillar II assessment consists of the Internal Capital Adequacy Assessment Process (ICAAP), which is conducted by the credit institution.

The ICAAP process is aligned with the general principles and requirements set by CRD IV and National Bank of Romania Regulation 5/2013. In particular, its main aims are:

• The identification, analysis, monitoring and the overall assessment of risks, • The improvement of various systems/ procedures/ policies related to the assessment and management of risks and • The estimation of the necessary level of Internal Capital required for the coverage of all risks and for Capital

planning purposes as well.

The level of the internal capital required according to the business plan to cover the risks which the Bank is willing to undertake in one year’s horizon (base case scenario). Additionally the bank is applying severe but plausible shocks in order to estimate its resilience to extreme systemic or market stress scenarios, should these occur.

The Key principles on which the ICAAP framework is based are responsibility, proportionality, risks’ materiality and forward looking stance.

The main risks addressed in the ICAAP are the following:

• Credit Risk including concentration risk, residual risk , currency risk and specialized lending Market risk: • Operational risk Liquidity risk

• Reputational risk • Business and Strategic risk • Interest Rate Risk in the Banking

5

• Book Compliance risk The Bank’s ICAAP report mainly includes:

• The macro overview and recent market developments. • The business plan/ model. • The ICAAP framework and procedures. • The analysis of risks and respective controls (including definition, identification, assessment, measurement,

monitoring, reviewing, reporting, capital impact). • The internal capital overview. • The capital planning and allocation. • Stress testing.

Besides ICAAP report, Alpha Bank Romania is currently working on the preparation of the first Internal Liquidity

Adequacy Assessment Process (ILAAP). ILAAP, which has been introduced by Article 86 of Directive 2013/36/EU, refers to the internal process that should be developed by the Bank in order to identify, measure, manage and monitor its liquidity and funding risks.

2.3 Own Funds

2.3.1 Own Funds structure

The Bank Capital Strategy commits to maintain sound capital adequacy both from economic and regulatory perspective. It aims at monitoring and adjusting capital levels, taking into consideration capital markets’ demand and supply, in an effort to achieve the optimal balance between the economic and regulatory considerations.

The overall Bank Risk and Capital Strategy sets specific risk limits, based on management’s risk appetite, as well

as thresholds to monitor whether actual risk exposure deviates from the desired optimum. The Bank’s capital is totally owned by the Group ALPHA Bank. The 65% of the total capital as of 31.12.2014

represents Common Equity Tier 1 (CET1) while the rest represents a headquarters’ subordinated debt. The above capital level will be positively affected by the full implementation of Basel III (in 5 years’ time). More specifically the respective transitional provisions regarding regulatory adjustments are the following:

• Period loss. • Intangible Assets (20% of intangible assets is deducted from CET1 due to transitional provisions, the remaining

80% is deducted from Tier I capital). • Prudential Filter - according to transitional provisions of CRR 575/2013, as well as NBR Regulation no.5/2013,

prudential filter represents 80% from the difference between former RAS provision determined according to NBR regulations and IFRS provision, which is deducted from own funds as follows: ½ of prudential filter amount is deducted from Tier 1, while the other ½ of the amount is deducted from Tier 2

• Adjustments applied to CET1 due to insufficient Additional Tier I to cover corresponding deductions (e.g. the 80% of intangible assets that would be deducted from Tier I). As already mentioned above the positive effect of the reversal of regulatory provisions is quite high, oversubscribing the minimal negative impact of the other regulatory adjustments.

Further details of the characteristics of the aforementioned instruments are provided in note 23 of the Financial

Statements as of 31 December 2014. All the amounts are expressed in EUR thousand (EUR '000) using NBR exchange rate at 31 December 2014, unless

otherwise stated (4.4821 EUR/RON).

The following table presents the analysis of own funds capital structure, as defined in CRR 575/2013:

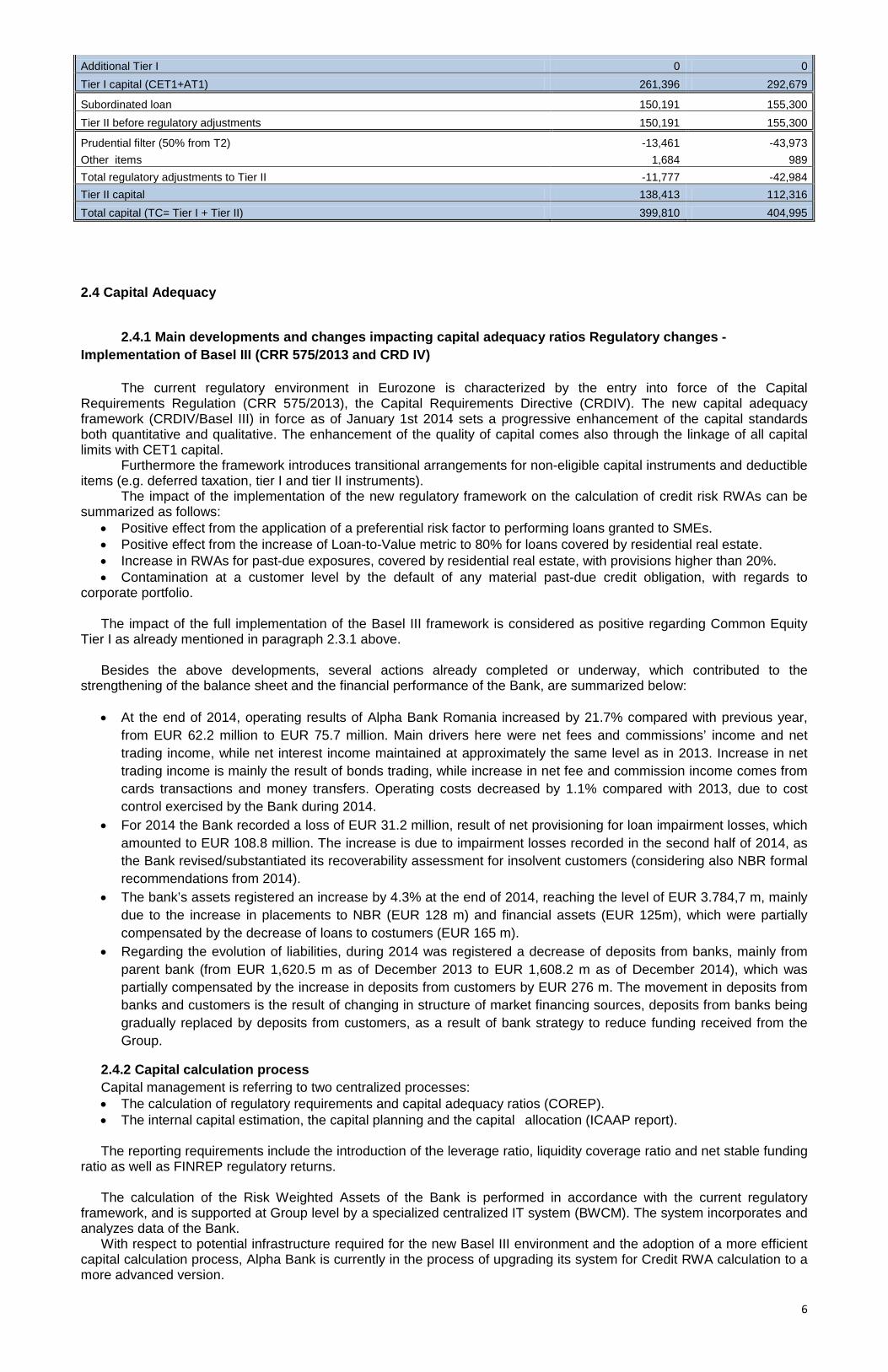

Own funds synthesis '000 EUR

Type 31.12.2014 31.12.2013

Share capital 218,360 218,233 Retained earnings 40,344 32,884 Accumulated other comprehensive income (AFS reserves) -28,290 0 Other reserves 78,543 78,940

Common equity Tier I capital before regulatory adjustments 308,956 330,057

Period loss/profit -31,159 7,437 Intangible assets (20% in 2014, 100% in 2013) -107 -604 Other deductible items -2,265 -236

Regulatory adjustments applied to Common Equity Tier I due to insufficient Additional Tier I to cover deductions -14,029 -43,973 Total regulatory adjustments to Common Equity Tier I -47,560 -37,377 Common Equity Tier I capital (CET1) 261,396 292,679 Additional Tier I before regulatory adjustments 0

Intangible assets (80% in 2014)-deductible from CET1 -428 0 Prudential filter (50% form AT1) - deductible from CET1 -13,461 -43,973 Other deductions - deductible from CET1 -141 0 Total regulatory adjustments to Additional Tier I -14,029 -43,973

6

Additional Tier I 0 0 Tier I capital (CET1+AT1) 261,396 292,679

Subordinated loan 150,191 155,300 Tier II before regulatory adjustments 150,191 155,300

Prudential filter (50% from T2) -13,461 -43,973 Other items 1,684 989 Total regulatory adjustments to Tier II -11,777 -42,984 Tier II capital 138,413 112,316 Total capital (TC= Tier I + Tier II) 399,810 404,995

2.4 Capital Adequacy

2.4.1 Main developments and changes impacting capital adequacy ratios Regulatory changes - Implementation of Basel III (CRR 575/2013 and CRD IV)

The current regulatory environment in Eurozone is characterized by the entry into force of the Capital Requirements Regulation (CRR 575/2013), the Capital Requirements Directive (CRDIV). The new capital adequacy framework (CRDIV/Basel III) in force as of January 1st 2014 sets a progressive enhancement of the capital standards both quantitative and qualitative. The enhancement of the quality of capital comes also through the linkage of all capital limits with CET1 capital.

Furthermore the framework introduces transitional arrangements for non-eligible capital instruments and deductible items (e.g. deferred taxation, tier I and tier II instruments).

The impact of the implementation of the new regulatory framework on the calculation of credit risk RWAs can be summarized as follows:

• Positive effect from the application of a preferential risk factor to performing loans granted to SMEs. • Positive effect from the increase of Loan-to-Value metric to 80% for loans covered by residential real estate. • Increase in RWAs for past-due exposures, covered by residential real estate, with provisions higher than 20%. • Contamination at a customer level by the default of any material past-due credit obligation, with regards to

corporate portfolio.

The impact of the full implementation of the Basel III framework is considered as positive regarding Common Equity Tier I as already mentioned in paragraph 2.3.1 above.

Besides the above developments, several actions already completed or underway, which contributed to the strengthening of the balance sheet and the financial performance of the Bank, are summarized below:

• At the end of 2014, operating results of Alpha Bank Romania increased by 21.7% compared with previous year, from EUR 62.2 million to EUR 75.7 million. Main drivers here were net fees and commissions’ income and net trading income, while net interest income maintained at approximately the same level as in 2013. Increase in net trading income is mainly the result of bonds trading, while increase in net fee and commission income comes from cards transactions and money transfers. Operating costs decreased by 1.1% compared with 2013, due to cost control exercised by the Bank during 2014.

• For 2014 the Bank recorded a loss of EUR 31.2 million, result of net provisioning for loan impairment losses, which amounted to EUR 108.8 million. The increase is due to impairment losses recorded in the second half of 2014, as the Bank revised/substantiated its recoverability assessment for insolvent customers (considering also NBR formal recommendations from 2014).

• The bank’s assets registered an increase by 4.3% at the end of 2014, reaching the level of EUR 3.784,7 m, mainly due to the increase in placements to NBR (EUR 128 m) and financial assets (EUR 125m), which were partially compensated by the decrease of loans to costumers (EUR 165 m).

• Regarding the evolution of liabilities, during 2014 was registered a decrease of deposits from banks, mainly from parent bank (from EUR 1,620.5 m as of December 2013 to EUR 1,608.2 m as of December 2014), which was partially compensated by the increase in deposits from customers by EUR 276 m. The movement in deposits from banks and customers is the result of changing in structure of market financing sources, deposits from banks being gradually replaced by deposits from customers, as a result of bank strategy to reduce funding received from the Group.

2.4.2 Capital calculation process Capital management is referring to two centralized processes: • The calculation of regulatory requirements and capital adequacy ratios (COREP). • The internal capital estimation, the capital planning and the capital allocation (ICAAP report).

The reporting requirements include the introduction of the leverage ratio, liquidity coverage ratio and net stable funding

ratio as well as FINREP regulatory returns.

The calculation of the Risk Weighted Assets of the Bank is performed in accordance with the current regulatory framework, and is supported at Group level by a specialized centralized IT system (BWCM). The system incorporates and analyzes data of the Bank.

With respect to potential infrastructure required for the new Basel III environment and the adoption of a more efficient capital calculation process, Alpha Bank is currently in the process of upgrading its system for Credit RWA calculation to a more advanced version.

7

2.4.3 Capital requirements As mentioned above, Alpha Bank has undertaken several actions in order to enhance its balance-sheet and

financial performance as well. These actions have also contributed to the reduction of the RWAs and the strengthening of the capital adequacy ratios.

The corresponding capital requirements for Credit (per portfolio based on the standardized approach), Market (standardized approach) and Operational (BIA) Risks are presented in the following table. Capital requirements for Credit, Market and Operational Risk (in EUR ‘000)

Exposure Type Dec 14 Dec 13

Central governments and Central Banks/Regional governments and local authorities

2,192

2,967

Financial Institutions 17,435 19,348

Corporate 33,744 98,957

Retail 35,855 31,423

Secured by Immovable Property 36,839 11,016

Default/Past due items 24,635 4,083

Equity and Other Items 17,559 3,022

Total Capital Requirement for Credit Risk 168,259 170,816

Total Capital Requirement for Market Risk 5,781 1,002

Total Capital Requirement for Operational Risk 22,863 25,178

2.4.4 Capital ratios The following table presents the analysis of capital ratios, at the end of 2014:

Own funds synthesis (in EUR ‘000)

Type Dec 14 Dec 13

CET I 261,396 -

Tier I Capital 261,396 292,679

Tier II Capital 138,414 112,316

Total Regulatory Capital for C.A.R calculation 399,810 404,995

Risk Weighted Assets 2,103,235 2,462,457

CET I Ratio 10.62%

Tier I Ratio 10.62% 11.89%

Total Capital Adequacy Ratio (Tier I + Tier II) 16.24% 16.45%

3 Risk Management

3.1 Risk Management Framework and Principles

Alpha Bank thorough and prudent risk management framework is evolved over time and implemented in a coherent and effective manner in the conduct of the day-to-day business so as to strengthen its sound corporate governance under the current challenging macroeconomic and financial environment, taking into account the common European legislation and banking system rules, the regulatory principles and supervisory guidance and the best international practices.

The Bank’s focus throughout 2014 was to maintain the highest operating standards, ensure compliance with regulatory risk rules and retain confidence in the conduct of its business activities through sound and robust provision of financial services.

Taking also into consideration the new regulatory (Basel III implementation) Alpha Bank risk governance framework, including risk management strategy and business model, is further enhanced with a view to comply with the heightened standards and extensive guidelines covering risk data governance, aggregation, and reporting and is evolved around the following three lines of defense, operating independently and structured accordingly with the Bank’s nature, size and complexity as well as the risk profile of its activities:

• The business line; the first line of defense with “ownership” of risk whereby it acknowledges and manages the risk that it incurs in conducting its activities.

8

• The risk management function and the compliance function, independent from the first line of defense; the second line of defense that complements the business line’s risk activities through its monitoring and reporting responsibilities.

• The internal audit function independent from the first and second lines of defense; the third line of defense that conducts risk-based and general audits and reviews to provide assurance to the board that the overall governance framework, including the risk governance framework, is effective and that policies and processes are in place and consistently applied.

The Risk Management Framework, as a structural part of the Bank’s corporate and risk governance framework, is

based upon the following guiding principles: • Development of a sound risk culture that incorporates risk awareness, risk taking and risk management and control

in the decisions of management and employees during the day-to-day activities taking into account their impact on the risks they assume.

• Definition of the risk appetite framework, which establishes the individual and aggregate levels and types of risk that the Bank is willing to assume in advance of and in order to achieve its strategic business activities within its risk capacity.

• Definition of the risk policy that is adherent to the risk appetite and is supported by appropriate control procedures and processes.

• Development of the processes to ensure that all material risks and associated risk concentrations are identified, measured, limited, controlled, mitigated and reported on a timely and comprehensive basis.

• Monitoring of risk limits with alignment to the business goals. • Transparency promoted through clear communication lines. • Contributing staff has an active role in Risk Management, is equipped with all the necessary skills and means

which are necessary for effective Risk Management and understands its roles and responsibilities related to the Risk Management Framework.

• Documentation of all processes related to risk identification, measurement, monitoring, reporting and control/mitigation.

• Providing adequate information to Bank and Business Unit Management.

3.2 Risk Governance Structure

The Board of Directors of the Bank and the Executive Management have separate and distinct roles in providing the final and ultimate levels of defense ensuring the effective implementation of the risk management framework and policies within the Bank.

The Board has the overall responsibility for the Bank’s business strategy and financial soundness, internal organization and overall corporate governance structure and practices as well as the oversight of the Risk Management framework and the compliance with the regulatory requirements.

To this end, it ensures that the executive management carries out appropriately and effectively the Bank’s activities in a manner consistent with the business strategy, the risk profile and the risk appetite, while at the same time it oversees that the management is escalating risk issues and involves the appropriate board committees in a timely manner.

The Risk Management Division has been assigned with the responsibility of implementing the Risk Management Framework, according to the directions of the Risk Management Committee and operates independently from any executing processes.

The Risk Management Committee recommends to the Board of Directors the risk undertaking and capital management strategy which corresponds to the business objectives of the Bank; monitors and checks its implementation.

The main responsibilities of the committee are the following: • Define the principles for managing risk with regard to identifying, forecasting, measuring, monitoring and controlling

risk while focusing on forward-looking, emerging risks. • Evaluate and periodically review the adequacy and effectiveness of the risk management policy and procedures of

the Bank, in terms of the undertaking, monitoring, and management of risks on both an aggregated basis and by type of risk

• Determine the maximum risk appetite on an aggregate basis for each type of risk and further allocation of each of these limits per country, sector, currency, business unit, etc.

• Establish stop-loss limits or of other corrective actions.

Furthermore, the risk management functions that provide an overarching risk control framework for a more comprehensive and effective identification and handling of all risk types linked to the Bank’s risk appetite are supported by the following Committees: the Assets-Liabilities Management Committee and the Risk Management Committee.

Under the supervision of the Risk Vice-president operates the Risk Management Division. The RMD has been assigned with the responsibility of implementing the risk management framework, according to the directions of the Risk Management Committee.

3.3 Risk Profile

Alpha Bank, based on its strong reputation, its excellent organization, its well trained staff, its longstanding relationships with its customer base and its conservative Risk Policy, is successfully operating up to date adjusting itself to the prevailing circumstances.

The Bank’s focus throughout 2014 was to maintain its risk profile in line with its risk strategy at the moderate level, ensuring the safe and sound functioning of the daily business operations and supporting the strategic management initiatives with a view on a balanced risk-return approach.

9

3.4 Risk Management Policies

Bank Risk Strategy is based on the Risk Policies defined by the Risk Management Committee and approved by the Board of Directors.

Bank’s Risk Policies & Procedures framework include all central rules of conduct for handling risks and are set out in specific Manuals. The framework is reviewed regularly.

Internal Audit is responsible for providing an independent review of the integrity of the overall risk management processes and ensuring the appropriateness and effectiveness of the controls applied.

4 Credit Risk

4.1 General information

Credit risk is the risk that a borrower or counterparty fails to meet their contractual obligations in a timely manner, thus resulting to a financial loss for the Bank.

The definition of assets and other exposures a) past due and b) non-performing are described in note 3 item i) and in note 4 of Financial Statements as of 31.12.2014.

According to the CRR 575/2013 definition, any of the following events triggers a default status: • The institution considers that the obligor is unlikely to pay its credit obligations to the institution. • The obligor is past due more than 90 days on any material credit obligation to the institution.

The Bank constantly assesses whether there is evidence of impairment in accordance with the general principles and

methodology set out in IAS 39 and the relevant implementation guidance.

If there is objective evidence that an impairment loss on loans and receivables carried at amortized cost has been incurred, the amount of the loss is measured as the difference between the asset's carrying amount and the present value of estimated future cash flows discounted at the financial asset's original effective interest rate.

The Bank considers evidence of impairment for loans and advances to customers at both a specific asset and collective level.

Wholesale Portfolio For the Wholesale portfolio, an impairment test may be performed for obligors with one of the following trigger events:

• Significant financial difficulty of the borrower or issuer (Clients with rating D, D0, D1, D2 and E (default zone) and clients with Rating CC- and C (high risk zone)).

• Breach of contractual terms and conditions • The lender, for economic or legal reasons relating to the borrower's financial difficulty, is granting to the borrower a

concession that the lender would not otherwise consider such as the rescheduling of the interest or principal payments;

• Indications that a borrowers or issuer will enter bankruptcy • Significant deterioration in the industry outlook in which the borrower operates. • Derogatory items (e.g. payment orders, bounced cheques, auctions, bankruptcies, overdue payments to the State,

to Social Security Funds, or to employees). • Occurrence of unexpected, extreme events such as natural disasters, fraud, etc. • Interventions and actions by regulatory bodies/local authorities against the borrower, with possible significant

adverse impact on borrower’s cash flows • Adverse changes in the shareholders’ structure or the management of the company or serious management

issues/ problems. • Significant adverse changes in cash flows potentially due to ceased cooperation with a key/major customer,

significant reduction in demand of a main product or service, ceased cooperation with a key/major supplier or suppliers cut credit, etc.

The Bank includes in the individual assessment exposures that exceed the established threshold, which as of 31

December 2014 amounts to EUR 450,000 or equivalent and for which evidence of impairment exists (e.g. past due amounts, restructured facilities, significant deterioration of client’s financial standing etc.). If no objective evidence of impairment existed for the individually assessed assets, these assets have been included in the collective impairment assessment for any impairment that has been incurred but not yet identified.

Furthermore, the Bank assesses whether objective evidence for individual assessment for impairment exists. Customers who have been assessed individually but the impairment allowance estimated was zero, are consequently assessed for impairment on a collective basis, once grouped in pools based on common credit risk characteristics. Customers with no trigger events and hence, who are not individually assessed, are assessed collectively in pools formed based on similar credit risk characteristics. Indicatively, some categories in terms of credit risk characteristics are the estimated default probabilities or credit ratings, the collateral coverage and type of coverage, days in arrears, etc.

The Bank assesses for collective impairment the restructured loans in separate categories for companies and retail

loans. Each category presented above is further detailed in buckets of overdue days. For impairment computation the collective assessment factors (PD and LGD) are estimated on the basis of historical

loss experience for loans with credit risk characteristics. The loan impairment assessment considers the visible effects on current market conditions on the individual / collective assessment of loans and advances to customers’ impairment.

The pre-condition that there is need to be objective evidence in order for the loss to be recognized and effectively the

impairment loss to be assumed on individual loans, may lead to a delay in the recognition of a loan’s impairment, which

10

has already taken place. Within this context and in accordance with IAS39, it would be appropriate to recognize impairment losses for those losses "which have been incurred but have not yet been reported» (Incurred But Not Reported - IBNR).

Provisions for loss events that have occurred but have not yet been reported ("IBNR provisions") are calculated on a

collective basis for the wholesale portfolio. For IBNR provisioning purposes, loans are grouped based on similar credit risk characteristics. The characteristics selected are based on the estimation of future cash flows for groups of such loans showing the debtors' ability to pay all amounts due, according to the contractual terms and conditions.

Retail Portfolio

The Bank includes in the individual assessment exposures that exceed the established threshold, which as of 31 December 2014 amounts to EUR 450,000 or equivalent and for which evidence of impairment exists (e.g. past due amounts, restructured facilities, significant deterioration of client’s financial standing etc.). If no objective evidence of impairment existed for the individually assessed assets, these assets have been included in the collective impairment assessment for any impairment that has been incurred but not yet identified. Further details on impairment calculations are described in note 3 item n) of Financial Statements as of 31.12.2014.

Individuals • Customers over 90 days in arrears. • Customers 30-89 days delinquent. • Customers with forborne products. • Unemployed Customers. • Deceased Customers. • Unforeseen, extreme events such as fraud, natural disasters, etc. • Customers who are freelancers or personal company holders and stop their business activity due to retirement. • Customers who are freelancers or personal company holders and have suffered a significant deterioration of their

financial situation, either due to poor management or because of bad reputation, either due to termination of important business partnerships or because of

• Customers who are representatives of the company and their business are over 90 days in arrears (rating D, D0 or D1 or D2 or E) or CC- or C rating.

• Customers who are representatives of the company and their business have detrimental (e.g. payment orders, denounced checks, auctions, bankruptcies, overdue amounts to the State, overdue amounts to Social Security or employees - work lien).

• Customers who are representatives of the company and there are interventions and actions from the regulatory authorities over their companies

• Customers who are representatives of the company and in their companies are observed significant negative changes in the cash flows, which may be due to e.g. termination of cooperation with key customers, a significant reduction in demand of commodities or services, discontinuation of credit from suppliers, etc.

• Customers who are representatives of the company and their companies operate in industries where there is observed significant deterioration in the prospects of the industry (considering the five sectors with the most significant annual deterioration according to the risk sector classification from the Risk Analyst).

• Customers with impairment in the previous control, for whom any of the above criteria applies. • Customers with detrimental (e.g. payment orders, denounced checks, auctions, bankruptcies, overdue amounts to

the State, overdue amounts Social Security or employees - work lien).

Small businesses • significant financial difficulty of the borrower or issuer (Clients with rating D, D0, D1, D2 and E (default zone) and

clients with Rating CC- and C (high risk zone)). • Breach of contractual terms and conditions • the lender, for economic or legal reasons relating to the borrower's financial difficulty, is granting to the borrower a

concession that the lender would not otherwise consider such as the rescheduling of the interest or principal payments;

• Indications that a borrowers or issuer will enter bankruptcy • Significant deterioration in the industry outlook in which the borrower operates. • Derogatory items (e.g. payment orders, bounced cheques, auctions, bankruptcies, overdue payments to the State,

to Social Security Funds, or to employees). • Occurrence of unexpected, extreme events such as natural disasters, fraud, etc. • Interventions and actions by regulatory bodies/local authorities against the borrower with possible significant

adverse impact on borrower’s cash flows • Adverse changes in the shareholders’ structure or the management of the company or serious management

issues/ problems. • Significant adverse changes in cash flows potentially due to ceased cooperation with a key/major customer,

significant reduction in demand of a main product or service, ceased cooperation with a key/major supplier or suppliers cut credit, etc.

Collective Impairment Assessment is applied to loans which do not meet the conditions for individual assessment once

they are classified based on similar credit risk characteristics. In addition, exposures for which there has not been calculated any loss during the individual assessment, are assessed on a collective basis, once they are incorporated into groups based on similar credit risk characteristics.

In order to effectively manage credit risk, the Bank has developed specific methodologies and credit risk measurement

systems in accordance with regulatory and Basel III requirements while incorporating banking industry best practices. These methodologies and systems are continuously evolving to provide the Business Units with timely and effective support in the decision making process and to avoid possible adverse consequences for the Bank.

11

The Risk Management Committee assesses the adequacy and the efficiency of the credit risk management policy and procedures as regards undertaking, monitoring and management of credit risk per business line, geographic area, product, activity, sector, etc., and resolves on the planning of the required corrective actions.

4.2 Disclosures with respect to Credit Risk and Asset Quality of Bank’s exposures The tables below show the Bank's credit exposures, impairment losses and non-performing loans that are over 90

days past-due per portfolio, as disclosed for IFRS purposes as well as the average balances:

Table 4a: Loans and Advances to Customers, Impaired Loans and Impairment Allowance by Product Line, Industry and Geographical Region (in Euro '000) 31.12.2014

ALPHA BANK ROMANIA Greece Romania

Gross Amount

Impaired Amount

Impairment Allowance Gross Amount Impaired

Amount Impairment Allowance

Retail Lending 149 1 1 1,172,023 124,465 90,983 Mortgage 110 - - 882,579 48,793 30,739 Consumer 26 1 1 265,522 71,553 56,457 Credit Card 13 - - 23,618 4,120 3,783 Other (incl. SBL) - - - 304 - 4 Corporate Lending - - - 1,462,078 399,013 218,138 Financial Institutions - - - 52,094 1,383 1,197 Manufacturing - - - 110,614 33,058 23,828 Real Estate Development - - - 308,662 100,629 38,550 Construction - - - 466,981 114,374 50,385 Whole sale and retail trade - - - 210,889 56,600 41,034 Transportation - - - 25,198 10,969 5,826 Shipping - - - 523 - 6 Hotels / Tourism - - - 45,112 19,044 11,568 Services - - - 69,003 31,214 18,190 Other sectors - - - 173,001 31,743 27,555 Public Sector - - - 15,172 - 165 Total 149 1 1 2,649,273 523,478 309,285

Table 4b: Loans and Advances to Customers, Impaired Loans and Impairment Allowance by Product Line, Industry and Geographical Region (in Euro '000) 31.12.2013

ALPHA BANK ROMANIA Greece Romania

Gross Amount

Impaired Amount

Impairment Allowance Gross Amount Impaired

Amount Impairment Allowance

Retail Lending 10 1 1 1,155,235 125,235 89,542 Mortgage - - - 835,593 47,188 25,619 Consumer 10 1 1 293,023 73,533 59,481 Credit Card - - - 25,754 4,515 4,411 Other (incl. SBL) - - - 864 - 32

Corporate Lending - - - 1,648,649 474,640 226,662 Financial Institutions - - - 35,522 1,724 857 Manufacturing - - - 147,460 74,874 38,159 Real Estate Development - - - 359,740 105,987 39,211 Construction - - - 566,944 120,295 56,762 Whole sale and retail trade - - - 250,796 70,928 50,084 Transportation - - - 21,725 10,033 2,193 Shipping - - - 632 - - Hotels / Tourism - - - 52,315 19,946 5,396 Services - - - 83,900 37,184 17,215 Other sectors - - - 129,616 33,669 16,786

Public Sector - - - 17,208 - - Total 10 1 1 2,821,092 599,876 316,205

12

Table 5a: Impaired and Past-due Loans and Advances to Customers by Business Line (in Euro '000) 31.12.2014

ALPHA BANK ROMANIA

Non impaired L&As Impaired L&As Total Gross

amount Neither past due nor impaired

Past due but not impaired

Individually assessed

Collectively assessed

Retail Lending 921,950 125,756 47,231 77,235 1,172,172 Mortgage 749,561 84,335 28,514 20,279 882,689 Consumer 155,121 38,873 18,679 52,874 265,548 Credit Card 16,964 2,547 38 4,082 23,631 Other (Incl. SBL) 304 - - - 304 Corporate Lending 1,055,108 7,957 389,782 9,231 1,462,078 Large 993,729 4,764 366,323 1,736 1,366,552 SMEs 61,379 3,193 23,459 7,495 95,526 Public Sector 14,653 520 - - 15,172 Greece - - - - - Other Countries 14,653 520 - - 15,172

Total 1,991,710 134,233 437,013 86,466 2,649,422

Table 5b: Impaired and Past-due Loans and Advances to Customers by Business Line (in Euro '000) 31.12.2013

ALPHA BANK ROMANIA

Non impaired L&As Impaired L&As Total Gross

amount Neither past due nor impaired

Past due but not impaired

Individually assessed

Collectively assessed

Retail Lending 901,368 128,641 17,635 107,601 1,155,245 Mortgage 709,077 79,328 11,792 35,396 835,593 Consumer 172,965 46,535 5,843 67,690 293,033 Credit Card 18,462 2,778 - 4,515 25,754 Other (Incl. SBL) 864 - - - 864 Corporate Lending 1,169,883 4,127 413,680 60,960 1,648,649 Large 1,108,161 2,170 395,391 42,817 1,548,540 SMEs 61,722 1,956 18,288 18,143 100,110 Public Sector 17,208 - - - 17,208 Greece - - - - - Other Countries 17,208 - - - 17,208 Total 2,088,458 132,767 431,315 168,561 2,821,102

Table 6: Credit Exposure, non-performing loans, impairment losses (in Euro '000)

ALPHA BANK ROMANIA 31.12.2014 31.12.2013

Gross Loans 2,649,422 2,821,102 Mortgages 882,689 835,593 Consumer Credit 289,483 319,652 Businesses 1,477,250 1,665,857 NPL Ratio 11.70% 13.34% Impairment Losses 309,286 316,205

13

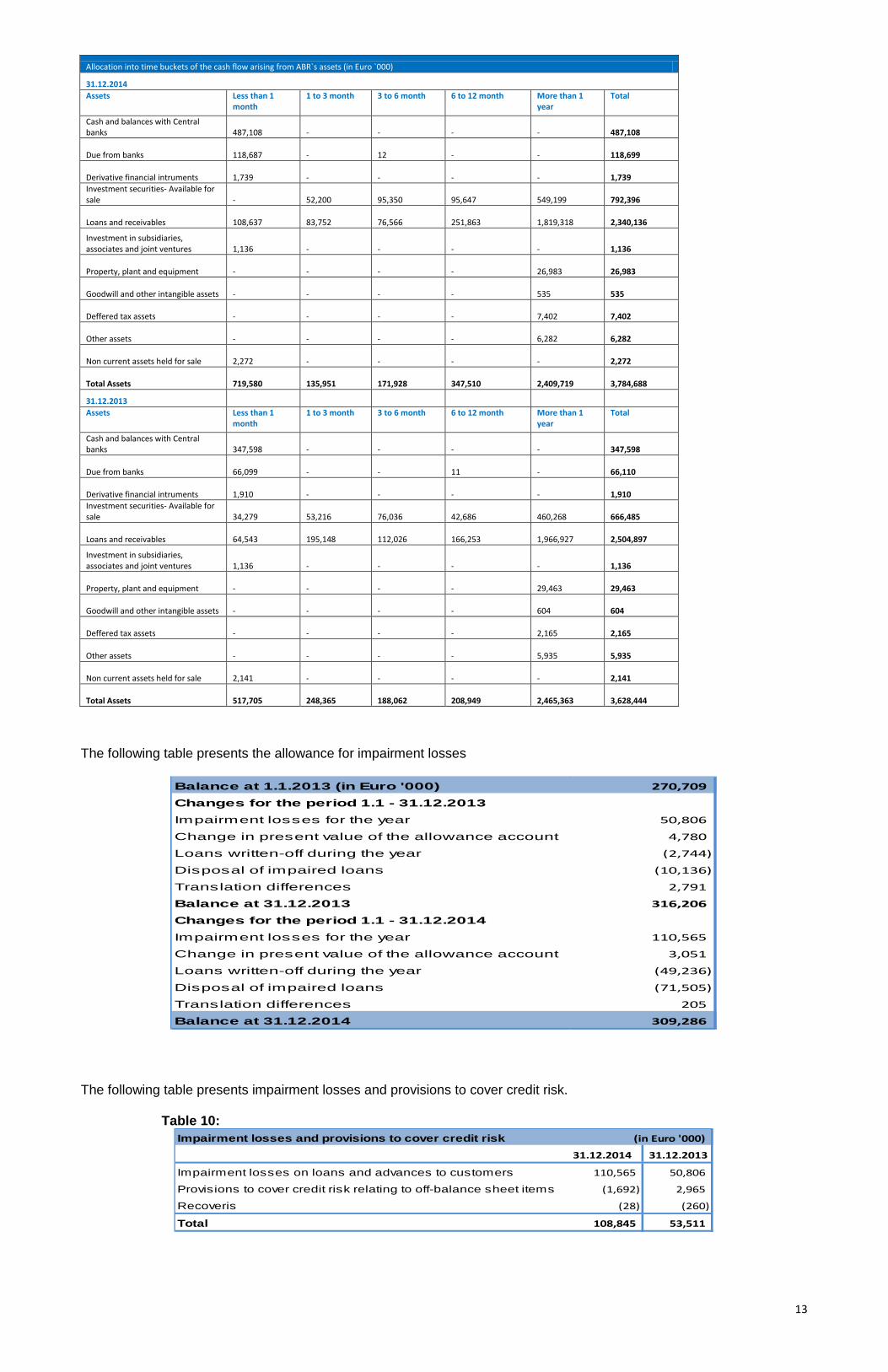

Allocation into time buckets of the cash flow arising from ABR`s assets (in Euro `000)

31.12.2014 Assets Less than 1

month 1 to 3 month 3 to 6 month 6 to 12 month More than 1

year Total

Cash and balances with Central banks

487,108

-

-

-

-

487,108

Due from banks 118,687

-

12

-

-

118,699

Derivative financial intruments 1,739

-

-

-

-

1,739

Investment securities- Available for sale

-

52,200

95,350

95,647

549,199

792,396

Loans and receivables 108,637

83,752

76,566

251,863

1,819,318

2,340,136

Investment in subsidiaries, associates and joint ventures

1,136

-

-

-

-

1,136

Property, plant and equipment -

-

-

-

26,983

26,983

Goodwill and other intangible assets -

-

-

-

535

535

Deffered tax assets -

-

-

-

7,402

7,402

Other assets -

-

-

-

6,282

6,282

Non current assets held for sale 2,272

-

-

-

-

2,272

Total Assets 719,580

135,951

171,928

347,510

2,409,719

3,784,688

31.12.2013 Assets Less than 1

month 1 to 3 month 3 to 6 month 6 to 12 month More than 1

year Total

Cash and balances with Central banks

347,598

-

-

-

-

347,598

Due from banks 66,099

-

-

11

-

66,110

Derivative financial intruments 1,910

-

-

-

-

1,910

Investment securities- Available for sale

34,279

53,216

76,036

42,686

460,268

666,485

Loans and receivables 64,543

195,148

112,026

166,253

1,966,927

2,504,897

Investment in subsidiaries, associates and joint ventures

1,136

-

-

-

-

1,136

Property, plant and equipment -

-

-

-

29,463

29,463

Goodwill and other intangible assets -

-

-

-

604

604

Deffered tax assets -

-

-

-

2,165

2,165

Other assets -

-

-

-

5,935

5,935

Non current assets held for sale 2,141

-

-

-

-

2,141

Total Assets 517,705

248,365

188,062

208,949

2,465,363

3,628,444

The following table presents the allowance for impairment losses

The following table presents impairment losses and provisions to cover credit risk.

Table 10:

Balance at 1.1.2013 (in Euro '000) 270,709

Changes for the period 1.1 - 31.12.2013Impairment losses for the year 50,806

Change in present value of the allowance account 4,780

Loans written-off during the year (2,744)

Disposal of impaired loans (10,136)

Translation differences 2,791

Balance at 31.12.2013 316,206

Changes for the period 1.1 - 31.12.2014Impairment losses for the year 110,565

Change in present value of the allowance account 3,051

Loans written-off during the year (49,236)

Disposal of impaired loans (71,505)

Translation differences 205

Balance at 31.12.2014 309,286

Impairment losses and provisions to cover credit risk31.12.2014 31.12.2013

Impairment losses on loans and advances to customers 110,565 50,806

Provisions to cover credit risk relating to off-balance sheet items (1,692) 2,965

Recoveris (28) (260)

Total 108,845 53,511

(in Euro '000)

14

4.3 Disclosures for portfolios subject to Standardized Approach

Alpha Bank Romania uses the available credit ratings from Moody’s Investors Service, Standard & Poor’s Ratings Services and Fitch Ratings, which have been approved by National Bank of Romania as eligible External Credit Assessment Institutions (ECAIs) for the use of their credit ratings in regulatory capital calculation.

Credit ratings are assigned to credit quality bands. Then, credit quality bands are assigned to the corresponding risk

weights per portfolio type. Assignment of the credit ratings of the eligible ECAI’s to credit quality steps

Credit Quality Band Standard & Poor's Ratings

Service Moody's Investor Services Fitch Ratings

1 AAA to AA- Aaa to Aa3 AAA to AA-

2 A+ to A- A1 to A3 A+ to A-

3 BBB+ to BBB- Baa1 to Baa3 BBB+ to BBB-

4 BB+ to BB- Ba1 to Ba3 BB+ to BB-

5 B+ to B- B1 to B3 B+ to B-

6 CCC+ and below Caa1 and below CCC+ and below

The asset classes for which ECAIs ratings are used are the following:

• Exposures to Central Governments and Central Banks; • Exposures from securities to Financial Institutions and companies;

For all other asset classes there are not available credit ratings and credit quality bands are assigned to the

corresponding risk weights per portfolio type. The table below shows the Bank's credit exposures after subtracting provisions and before any credit risk mitigation.

Credit exposures before any credit risk mitigation (in EUR ‘000 )

Exposure Type Dec-14 Dec-13 Central governments and Central Banks/Regional governments and local authorities

613,414 765,334

Financial Institutions 353,497 318,649

Corporate 1,612,005 635,411

Retail 741,032 1,037,153

Secured by mortgages on immovable property 397,933 752,750

Default/Past due items 52,781 273,721

Equity and Other Items 72,447 271,686 Total 3,843,109 4,054,704

Credit exposures for regulatory purposes before any credit risk mitigation are differentiated from equivalent balances

presented in IFRS balance sheet, due to integration of the off-balance sheet exposures (e.g. non-utilized, uncommitted undrawn facilities) and potential future exposures for derivative financial instruments.

The table below presents the credit exposures, after credit risk mitigation broken down by supervisory risk weights.

Exposures broken down by supervisory risk weighs according to credit quality steps (in Euro '000) Dec 2014

Exposure Type 0% 20% 35% 50% 75% 100% 150% Total

Central governments and Central Banks

918,368 0 0 0 0 19,939 0 938,307

Regional gov. and local authorities 0 9,489 0 0 0 5,560 0 15,048

Financial Institutions 29,383 125,295 0 273 0 70,568 93,338 318,855

Corporate 129,679 645 0 0 0 505,458 0 635,782

Retail 5,837 191 0 0 716,444 0 0 722,473

Secured by Immovable Property 0 0 434,526 0 0 318,661 0 753,187

Default 127,552 736 0 0 0 203,834 69,305 401,428

Equity 0 0 0 0 0 182,451 0 182,451

Other Items 47,060 6,617 0 0 0 35,715 0 89,392

Total 1,257,879 142,972 434,526 273 716,444 1,342,186 162,643 4,056,924

15

Exposures broken down by supervisory risk weighs according to credit quality steps (in Euro '000) Dec 2013

Exposure Type 0% 20% 35% 50% 75% 100% 150% Total

Central governments and Central

Banks/Regional gov. and local authorities

740,535 - - - - 37,086 - 777,621

Financial Institutions 284,936 70,107 - 100,359 - 29,799 98,566 583,767

Corporate Customers 6,264 68 - - - 1,102,189 89,842 1,198,364

Retail Customers 7,393 513 - - 523,583 - - 531,489

Secured by Real Estate Property

- - 393,427 - - - - 393,427

Past due items - - - 2,589 - 47,391 1,567 51,547

Other Items 34,626 - - - - 37,779 - 72,405

Total 1,073,755 70,688 393,427 102,948 523,583 1,254,244 189,975 3,608,620

5 Credit risk mitigation Credit risk mitigation techniques reduce exposure value and expected loss. According to CRR 575/2013, only specific

types of credit risk mitigation are eligible for capital adequacy calculation purposes.

5.1 Collateral valuation and management policies and procedures Collateral can be used in order to hedge the Credit Risk created in case a customer or counterparty to a financial

instrument fails to meet their contractual obligations. Collaterals are holdings or rights of every type provided to the Bank by its debtors or third parties to be used as additional funding sources in case of claim liquidation.

The main collateral types held for retail customers are mortgages, cash, mutual funds and sovereign securities.

Additionally, in case of real estate loans maximum Loan to Value (LTV: loan amount to property commercial value) limits have been set, depending upon loan purpose and collateral. The amount the customer contributes to the asset being financed is a very important factor during the loan approval process since it directly affects customer’s repayment ability.

As far as wholesale customers are concerned, loan repayment depends upon the viability and growth perspectives of

the company, the servicing ability of the company and its owners, the circumstances prevailing at the sectors and markets they are active in, as well as unexpected factors, positively or negatively affecting their operation.

The Bank estimates collateral value based upon the potential cash flows which will be received in case of liquidation.

During the estimation process the following are taken into consideration: • Asset quality. • Commercial / market value. • Potential difficulties in liquidation. • Time required for liquidation. • Liquidation associated costs. • Existing weights on real estate properties (mortgages, confiscations). • Potential senior claims which might occur during the liquidations of corporate assets (government, state

organizations, and employees).

The above parameters are taken into consideration while estimating collateral value factors, expressed as a percentage of the market, nominal or weighted collateral value, depending upon collateral type.

Real estate property and equipment valuation is carried out through the Evaluation department of the Bank or other,

approved, companies.

5.2 Description of the main collateral types eligible for Pillar I calculations There are two broad categories of collateral: guarantees / credit derivatives and financial collateral. Guarantees are the most common collateral type of the first category. A guarantee is a legally enforceable relationship

between the Bank and the borrower, through which the guarantor assumes the responsibility of paying the debt. It is documented and presupposes the existence of another legally enforceable relationship between the Bank and the borrower (loan).

The most common types of guarantors are: private individuals, companies, financial institutions, State and SME Guarantee Fund.

The following table presents the exposure value covered through eligible financial collateral and guarantees / credit

derivatives for each asset class, based on regulatory standards:

16

Market Value of eligible physical collateral and guarantees / credit derivatives (in Euro '000)

Total exposure value covered through eligible financial collateral and guarantees / credit derivatives (in EUR ‘000) Dec 2014

Exposure type Exposure amount Covered through financial collateral

Covered through guarantees

Central governments and central banks 750,729

Regional governments and local authorities 15,213

Financial Institutions 318,959 32,529

Corporate 637,614 130,322

Retail 1,048,853 134,189 187,122

Secured by immovable property 753,187

Default 592,743 150 591

Equity 182,451

Other Items 89,392

Total 4,389,141 297,190 187,713

Total exposure value covered through eligible financial collateral and guarantees / credit derivatives (in EUR ‘000) Dec 2013

Exposure type Exposure amount Covered through financial collateral

Covered through guarantees

Central governments and central banks/Regional governments and local authorities 613,059

Financial Institutions 353,292 42,691 15,148

Corporate Customers 1,686,485 257,798 2,276

Retail Customers 770,800 8,391 165,728

Secured by real estate property 397,703

Past due items 352,683 14 1,190

Other Items 72,405

Total 4,246,426 308,892 184,342

6. Counterparty credit risk (CCR)

Counterparty credit risk is the risk that a counterparty could default before the final settlement of all existing transactions’ cash flows. An economic loss would occur if the portfolio of transactions with the counterparty has a positive economic value to the Bank at the time of counterparty default. According to CRR 575/2013 the term transaction refers to:

• Over the counter (OTC) derivative transactions, such as FX or interest rate derivative transactions. • Repurchase transactions, securities or commodities lending or borrowing transactions or margin lending

transactions. • Long settlement transactions.

In principle, Alpha Bank only has the first two types of transactions. The exposures generating counterparty credit risk are monitored on a daily basis. The Bank has set limits per

counterparty group, per counterparty and per product. As far as repos and reverse repos are concerned, where Alpha Bank exchanges securities for cash for a specific

period of time, they are included in counterparty limits as they involve counterparty credit risk. The maximum potential loss of the Bank is capped by the difference between the market value of securities held (or assigned) and the respective interbank transaction.

As far as the derivative transactions with other (non-financial institution) counterparties are concerned, the resulting

risk exposure is taken into account as part of the Credit exposure against the customer according to the Credit Policy in force.

17

As of December 31, 2014 Alpha Bank had limited OTC derivative exposure only with the parent company and no outstanding repo or securities lending/ borrowing transactions.

Alpha Bank has adopted the Mark to Market Method, according to which, as described in article 274, section 3 of

CRR 575/2013, the exposure value of each contract is calculated as the sum of the current replacement cost of the contract, given it is positive, and the potential future exposure. The potential future exposure is estimated after multiplying the nominal value with a weight, the size of which depends upon the contractual remaining maturity and the underlying asset.

According to CRR 575/2013 Article 381, financial institutions are required to calculate the own funds requirements for Credit Valuation Adjustment (CVA Risk).

The CVA reflects the current market value of the counterparty credit risk to the institution. Own Funds requirements for CVA risk, are calculated for all OTC derivative instruments but excluding credit derivatives.

7. Market Risk

Market risk is the risk of reduction in economic value arising from unfavorable changes in the value or volatility of interest rates, foreign exchange rates, stock exchange indices, equities and commodities.

Market risk management is conducted in accordance with policies and procedures that have been developed and are

implemented by the Bank. Risk Management Committee recommends the market risk management strategy to the Executive Committee. Risk Management Committee is responsible for supporting and supervising the Market Risk management framework

and ensuring the application of all the necessary measures to identify, assess, monitor and control this type of risk. The Board of Directors is responsible for approving the guidelines, the strategy and the organizational structure as far as Market Risk is concerned.

Market Risk is controlled through the establishment and implementation of a well-structured set of transaction limits,

according to the risk tolerance while satisfying the relevant customer needs. The Standardized approach is used for the calculation of market risk regulatory capital. The Trading portfolio consists

mainly of the open FX position. In order to investigate any extreme market situations, market risk stress tests are performed on the Trading and

Available for Sale (AFS) portfolios. Stress Tests are performed by creating scenarios (‘what if’ hypothesis) to estimate the losses that may occur on the positions from potential unfavorable substantial movements/shocks in the market and in order to identify potential concentration risk within the portfolios.

Stress Tests may be carried out at any time on any position, however they are carried out on a regular basis at the end of every month and the results are reported to the ALCO and Risk Management Committee.

Typical stress scenarios consider the following changes in risk factors:

Yield curves: For sensitivity –market risk

Parallel shift by +100bp for all AFS financial securities portfolio. For sensitivity – specific risk (issuer risk)

The stress is applied depending on the counterparty external rating as follows: • For Bonds with ratings AAA+ to AAA- no scenario to be considered. • For Bonds with ratings AA+ to A- a 10 basis points increase in credit spreads to be considered. • For Bonds with ratings BBB+ to BBB- a 60 basis points increase in credit spreads to be considered. • For Bonds with ratings bellow BBB- and unrated Bonds a 100 basis points increase in the credit spreads to be

considered FX rates:

Appreciation/Depreciation of local currency vs. each other currency by 10% (unfavorable direction depending on current position).

Prices (e.g. equities and indices):

Equity Prices: Decrease by 10%.

8. Operational Risk

The Bank acknowledges the need for managing the operational risk that stems from its business activities, as well as

the need for holding adequate capital, in order to absorb potential losses related with this type of risk. Operational risk is the risk of loss due to failure or inadequacy of internal processes, people and systems or external

events, also including legal risk. Operational risk management is conducted in accordance to Policies and procedures designed and implemented

within the Bank and compliant with the Group’s methodologies and guidelines.

18

Within this context and in order to achieve effective operational risk management, the Bank has adopted and implemented an Operational Risk Framework which focuses on the following areas:

• Operational risk events management and collection, including management of Lawsuits against the Bank. • Operational risk identification and assessment through Risk and Control Self Assessment exercises (RCSA). • Definition and monitoring of Key Risk Indicators. • Operational Risk Reporting. • Operational risk mitigation approaches, including the implementation of Action Plans that improve the existing

internal control environment. The Operational Risk Committee is responsible of supporting and supervising this Operational Risk Management

Framework and ensuring the application of all the necessary processes as to identify, assess, monitor and control this type of risk.

The Framework is also supported by an appropriate organizational structure, with clear roles and responsibilities,

under the core assumption that the prime responsibility for Operational Risk management and mitigation plans application remains with the Business Units throughout the Bank.

The Risk Management Division is responsible among others, for the collection, the control and the assessment of Key

Risk Indicators, the Risk and Control Self Assessment exercises (RCSAs), Loss Data collection, as well as Reporting. This Framework is continuously reviewed and various initiatives have been introduced in order to improve it.

Indicatively, during 2014, the Policy and Procedures for Fraud Risk Management have been updated and the procedures for Managing Lawsuits against the Bank have been revised.

The calculation of capital requirements for operational risk is performed in accordance with the Basic Indicator

Approach. BIA requires capital of 15% of the average over the previous three year of positive annual gross income. The bank is planning to switch to the Advanced Measurement Approach.

9. Interest Rate Risk in the Banking Book

9.1 Interest Rate Risk Definition There are four main sources of interest rate risk which can have an impact on Alpha Bank’s earnings and economic

value: • Re-pricing risk that arises from timing differences in the maturity and re-pricing of Alpha Bank’s assets, liabilities

and off balance sheet positions. • Yield curve risk that arises when unexpected shifts of the yield curve have adverse effects on Alpha Bank’s

earnings and underlying economic value. • Basis risk that arises from imperfect correlation in the adjustment of the interest rates paid for and received from

different instruments with otherwise similar repricing characteristics. • Optionality that arises from embedded options in Alpha Bank’s assets and liabilities or off balance sheet positions.

9.2 Interest Rate Risk Framework The Bank aims to maximize its profitability in line with its risk appetite and business objectives. Therefore, it recognizes

the need to provide a sound framework for the identification, estimation, monitoring, controlling and reporting of interest rate and foreign exchange risks in the Banking Book, in a consistent manner across the Bank.

Interest rate risk management for the Banking Book is performed on a monthly basis and according to the Bank Risk

Management Strategy and Policy that have been developed and adopted. Interest rate and Foreign Exchange risk management for the Banking Book is performed through effective and timely

identification and the estimation of their effects on Bank’s earnings and economic value.

9.3 Interest Rate Risk Identification and Assessment For interest rate risk assessment the following estimation techniques are used: • Gap analysis for each currency. • Scenario analysis for each currency.

When performing Interest Rate Gap Analysis, bank assets and liabilities are allocated into time bands according to

their re-pricing date for variable interest rate instruments, or according to their maturity date for fixed rate instruments. In particular, sight deposits and savings are grouped into time bands according to their transactional behavior.

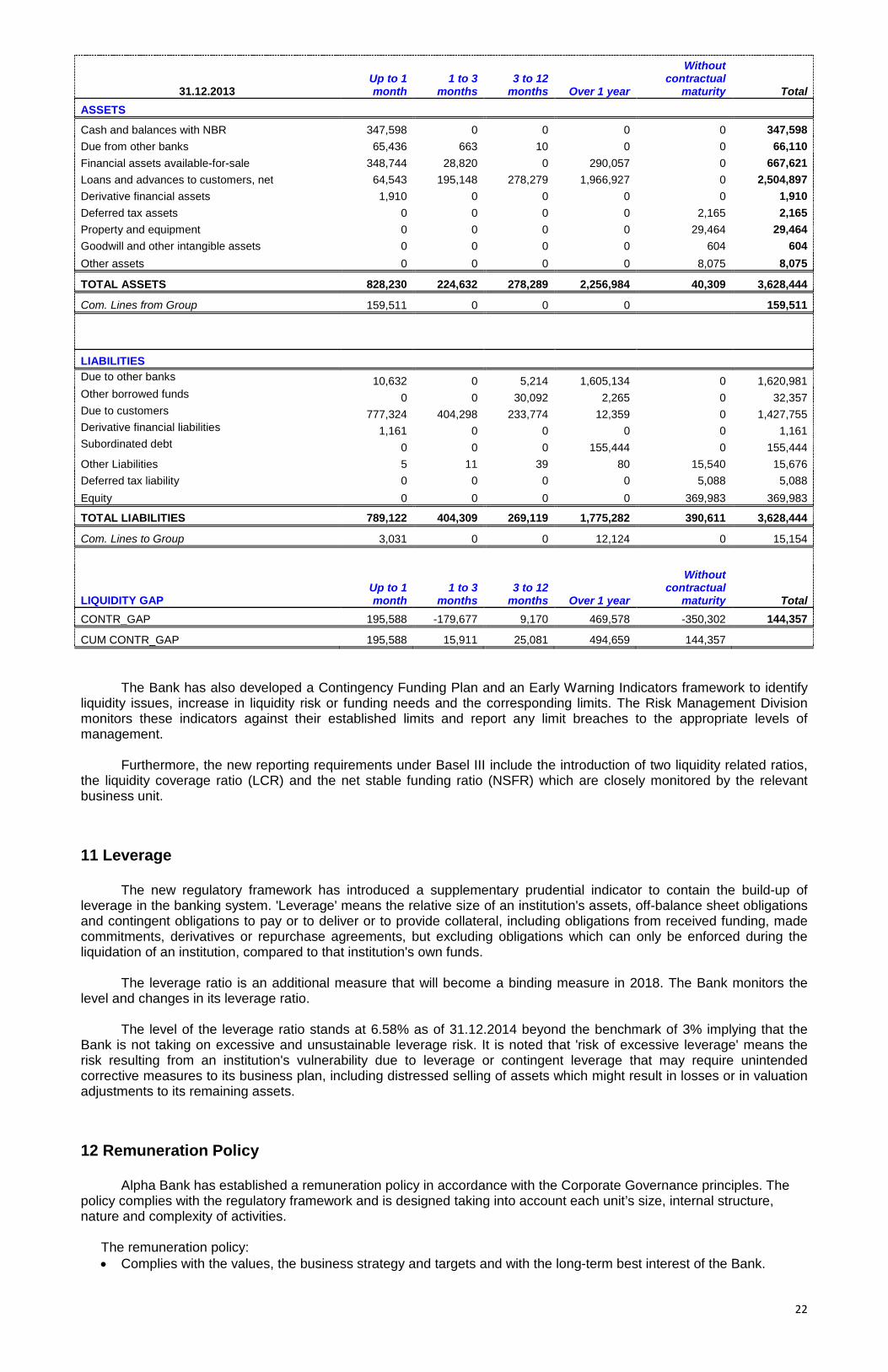

Bank Interest Rate Gap Analysis results at 31.12.2014 and 31.12.2013 below.

19

31.12.2014 Interest Rate Gap Analysis (in Euro `000) Up to 1 1 to 3 3 to 12 Over 1 Without

month

months months Year interest

rate Total

Assets Cash and balances with National Bank of Romania 441,173 0 0 0 45,935 487,108

Due from other banks 118,687 0 12 0 0 118,699

Financial assets available-for-sale 43,280 170,288 197,744 381,084 1,136 793,532

Loans and advances to customers 1,692,100 43,400 92,237 512,399 0 2,340,136

Property and equipment 0 0 0 0 26,983 26,983

Intangible fixed assets 0 0 0 0 535 535

Derivatives financial assets 1,739 0 0 0 0 1,739

Deferred tax assets 0 0 0 0 7,402 7,402

Other assets 0 0 0 0 8,554 8,554

Total assets 2,296,979 213,689 289,993 893,483 90,545 3,784,688

Liabilities

Due to other banks 481,349 1,113,881 0 13,877 0 1,609,107

Due to customers 965,685 479,085 258,651 732 0 1,704,153

Other borrowed funds 1,962 0 0 0 0 1,962

Subordinated loan 50,000 105,382 0 0 0 155,382

Other liabilities 0 80 0 0 12,989 13,069

Derivatives financial liabilities 1,959 0 0 0 0 1,959

Deferred tax liabilities 0 0 0 0 666 666

Total liabilities 1,500,954 1,698,428 258,651 14,609 13,655 3,486,297

Equity 0 0 0 0 298,390 298,390

Total liabilities and equity 1,500,954 1,698,428 258,651 14,609 312,045 3,784,688

Marginal Gap 796,025 -1,484,739 31,342 878,873 -221,501 0

Cummulative Gap 796,025 -688,714 -657,372 221,501 0 0

20

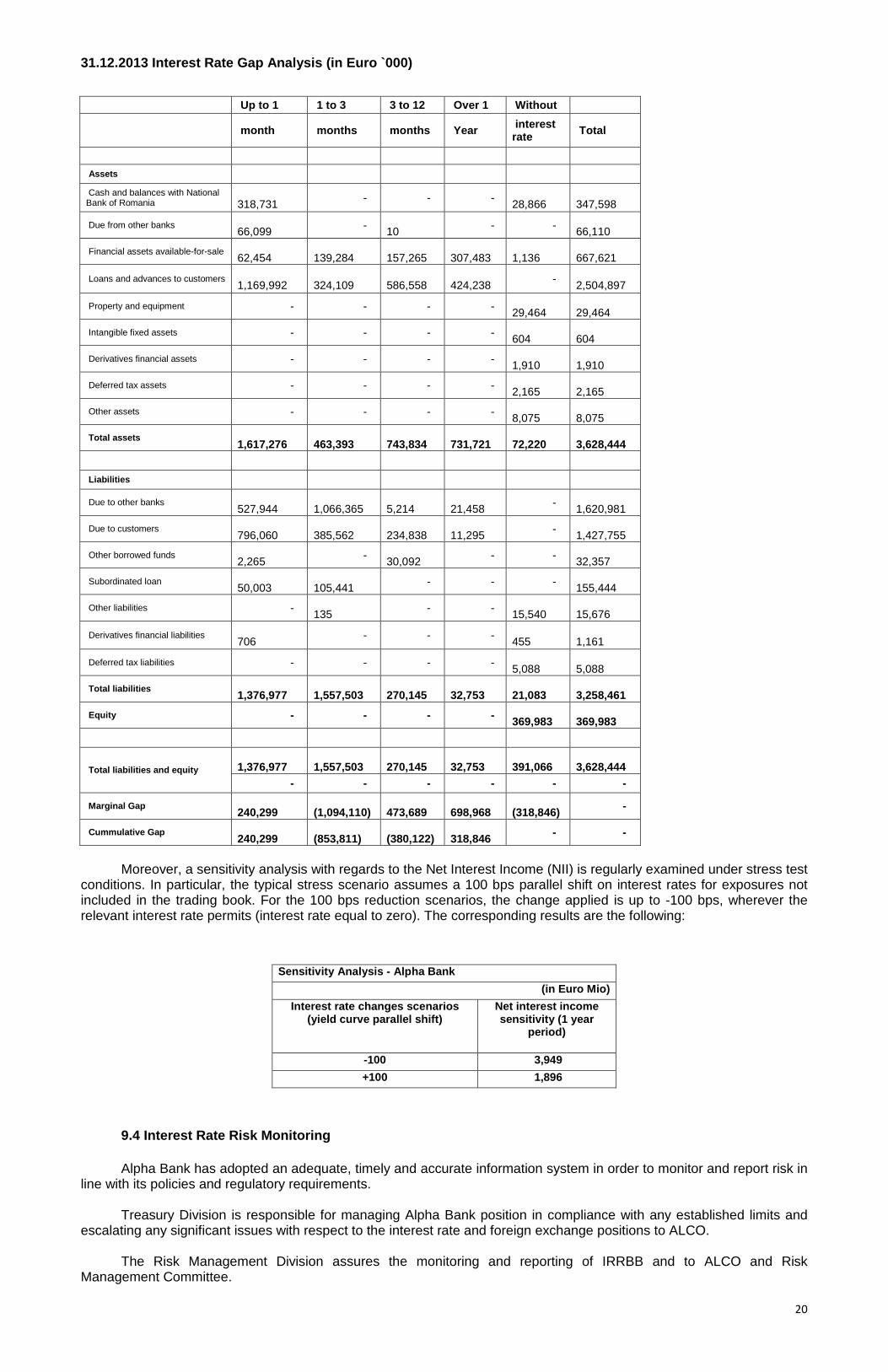

31.12.2013 Interest Rate Gap Analysis (in Euro `000)

Up to 1 1 to 3 3 to 12 Over 1 Without

month months months Year interest rate Total

Assets Cash and balances with National Bank of Romania

318,731 - - -

28,866 347,598

Due from other banks 66,099 -

10 - - 66,110

Financial assets available-for-sale 62,454

139,284

157,265

307,483

1,136

667,621

Loans and advances to customers 1,169,992

324,109

586,558

424,238 -

2,504,897

Property and equipment - - - - 29,464

29,464

Intangible fixed assets - - - - 604

604

Derivatives financial assets - - - - 1,910

1,910

Deferred tax assets - - - - 2,165

2,165

Other assets - - - - 8,075

8,075

Total assets 1,617,276

463,393

743,834

731,721

72,220

3,628,444

Liabilities

Due to other banks 527,944

1,066,365

5,214

21,458 -

1,620,981

Due to customers 796,060

385,562

234,838

11,295 -

1,427,755

Other borrowed funds 2,265 -

30,092 - - 32,357

Subordinated loan 50,003

105,441 - - -

155,444

Other liabilities - 135 - -

15,540 15,676

Derivatives financial liabilities 706 - - -

455 1,161

Deferred tax liabilities - - - - 5,088

5,088

Total liabilities 1,376,977

1,557,503

270,145

32,753

21,083

3,258,461

Equity - - - - 369,983

369,983

Total liabilities and equity 1,376,977

1,557,503

270,145

32,753

391,066

3,628,444

- - - - - -

Marginal Gap 240,299

(1,094,110)

473,689

698,968

(318,846) -

Cummulative Gap 240,299

(853,811)

(380,122)

318,846 - -

Moreover, a sensitivity analysis with regards to the Net Interest Income (NII) is regularly examined under stress test

conditions. In particular, the typical stress scenario assumes a 100 bps parallel shift on interest rates for exposures not included in the trading book. For the 100 bps reduction scenarios, the change applied is up to -100 bps, wherever the relevant interest rate permits (interest rate equal to zero). The corresponding results are the following:

Sensitivity Analysis - Alpha Bank (in Euro Mio)