Pillar 3 Disclosure report BNG Bank 2017 BNG Bank... · 2018-05-09 · liquidity and operational...

130

BANK Pillar 3 Disclosure report BNG Bank 2017

Transcript of Pillar 3 Disclosure report BNG Bank 2017 BNG Bank... · 2018-05-09 · liquidity and operational...

BANK

Pillar 3 Disclosure reportBNG Bank 2017

2

Contents

CONTENTS

Preliminary remarks 5

Frequency and means of disclosure (articles 433 and 434 CRR) 6

Risk management objectives and policies (article 435 CRR) 8

General information 8

Credit risk 16

Market risk 23

Liquidity risk and funding risk 28

Operational risk 33

Strategic risk 37

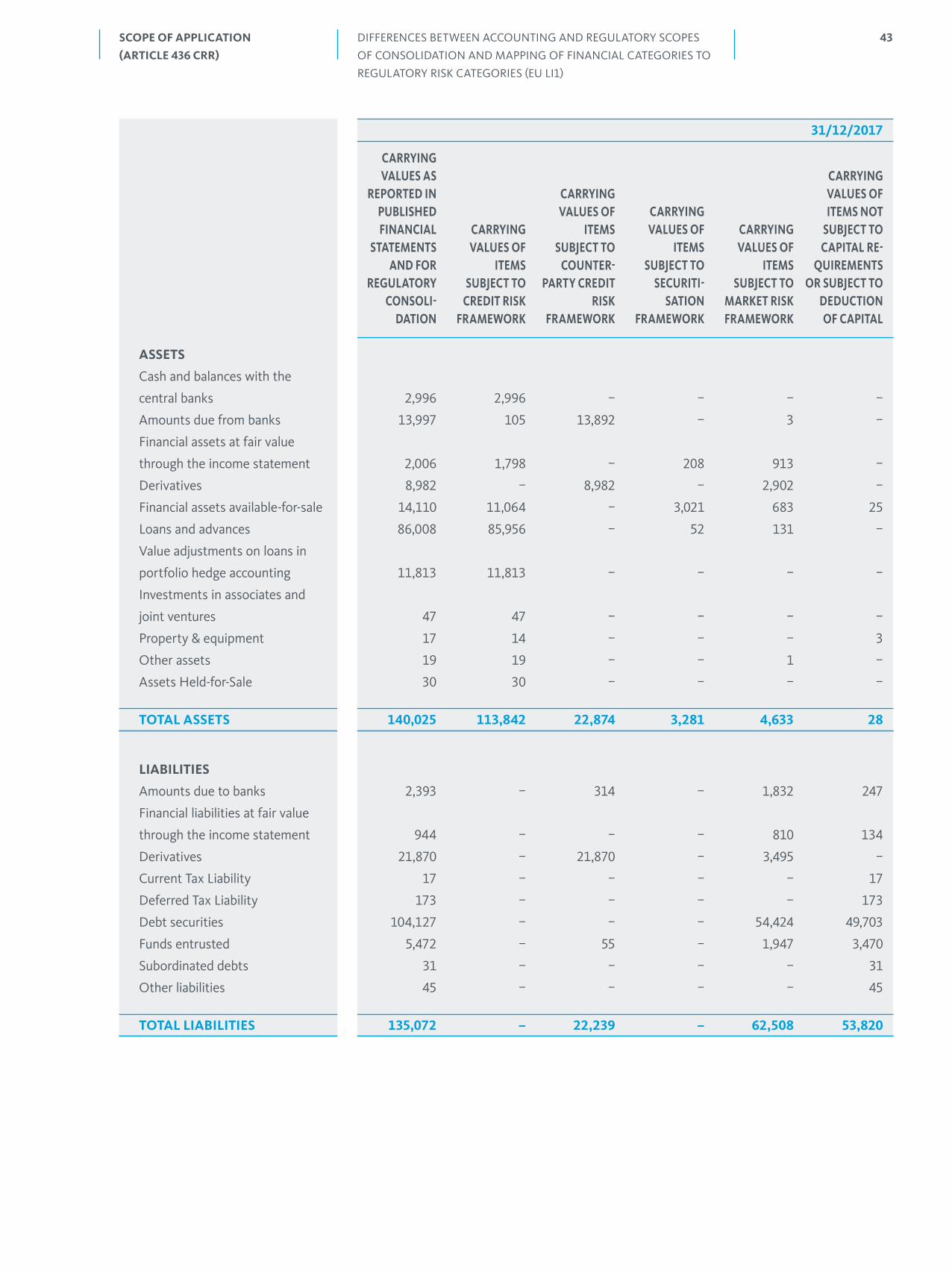

Scope of application (article 436 CRR) 41

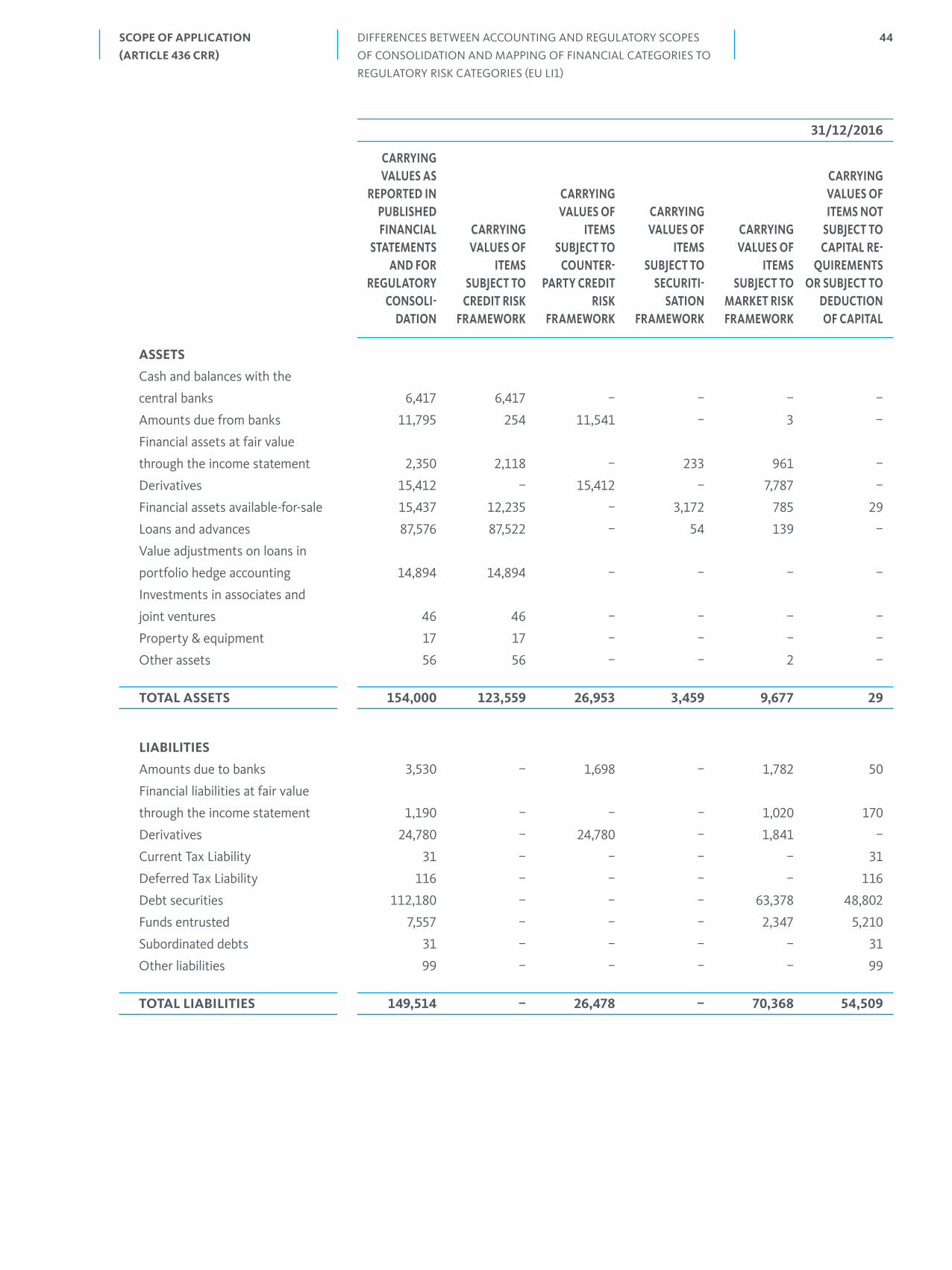

Differences between accounting and regulatory scopes of consolidation and mapping of financial categories to regulatory risk categories (EU LI1) 42

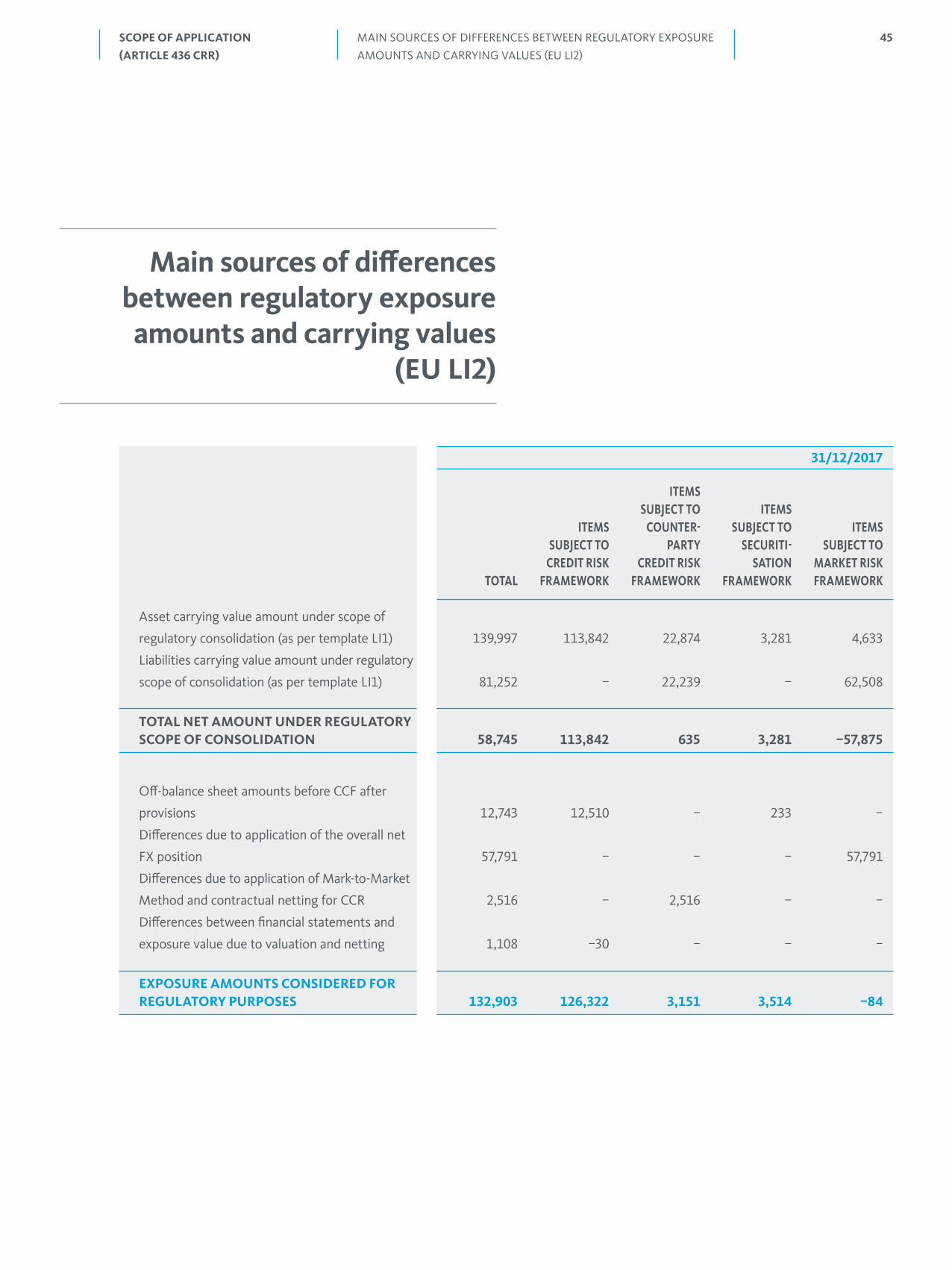

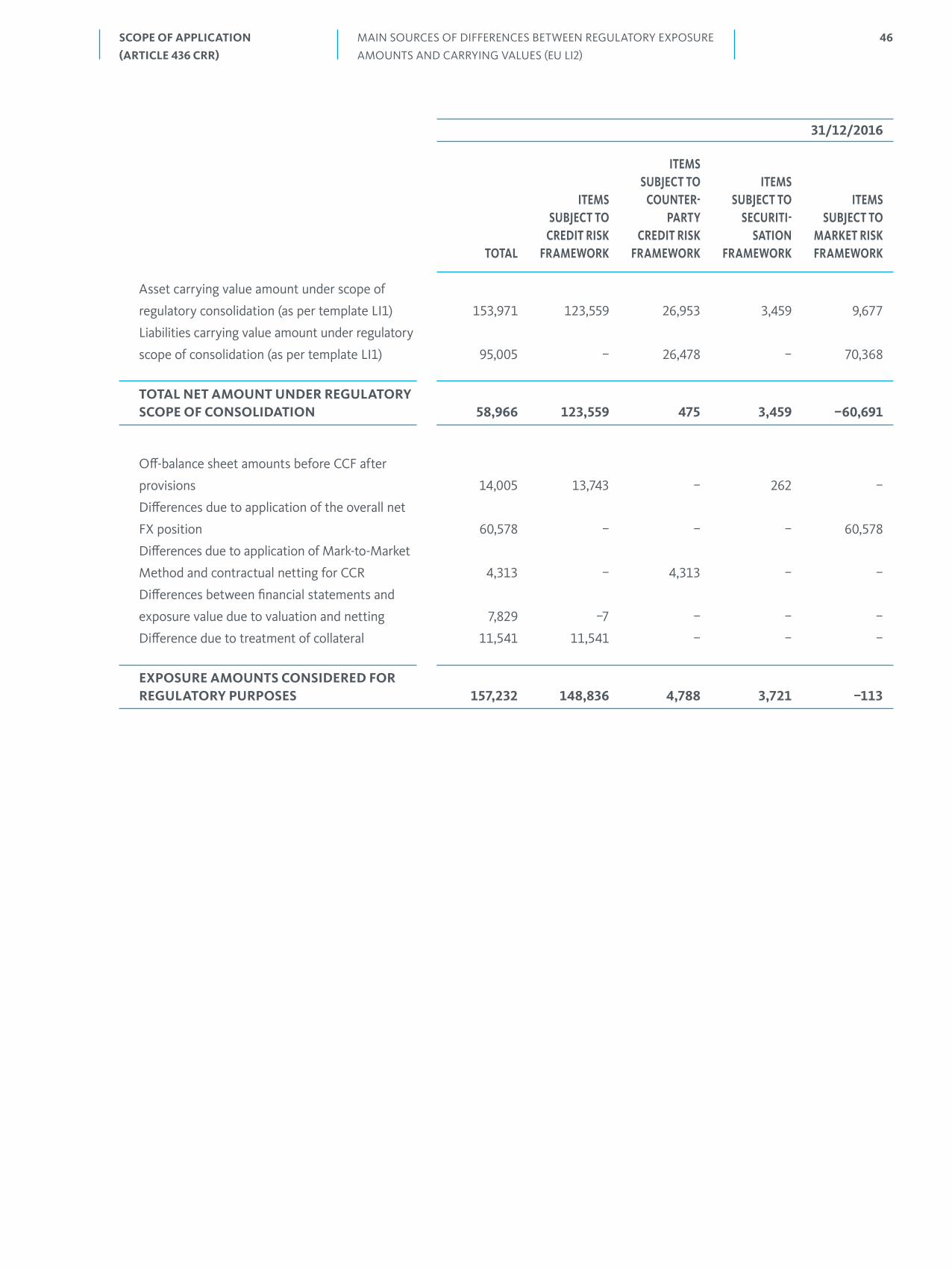

Main sources of differences between regulatory exposure amounts and carrying values (EU LI2) 45

Explanations of differences between accounting and regulatory exposure (EU LIA) 47

Outline of the differences in the scopes of consolidation (EU LI3) 48

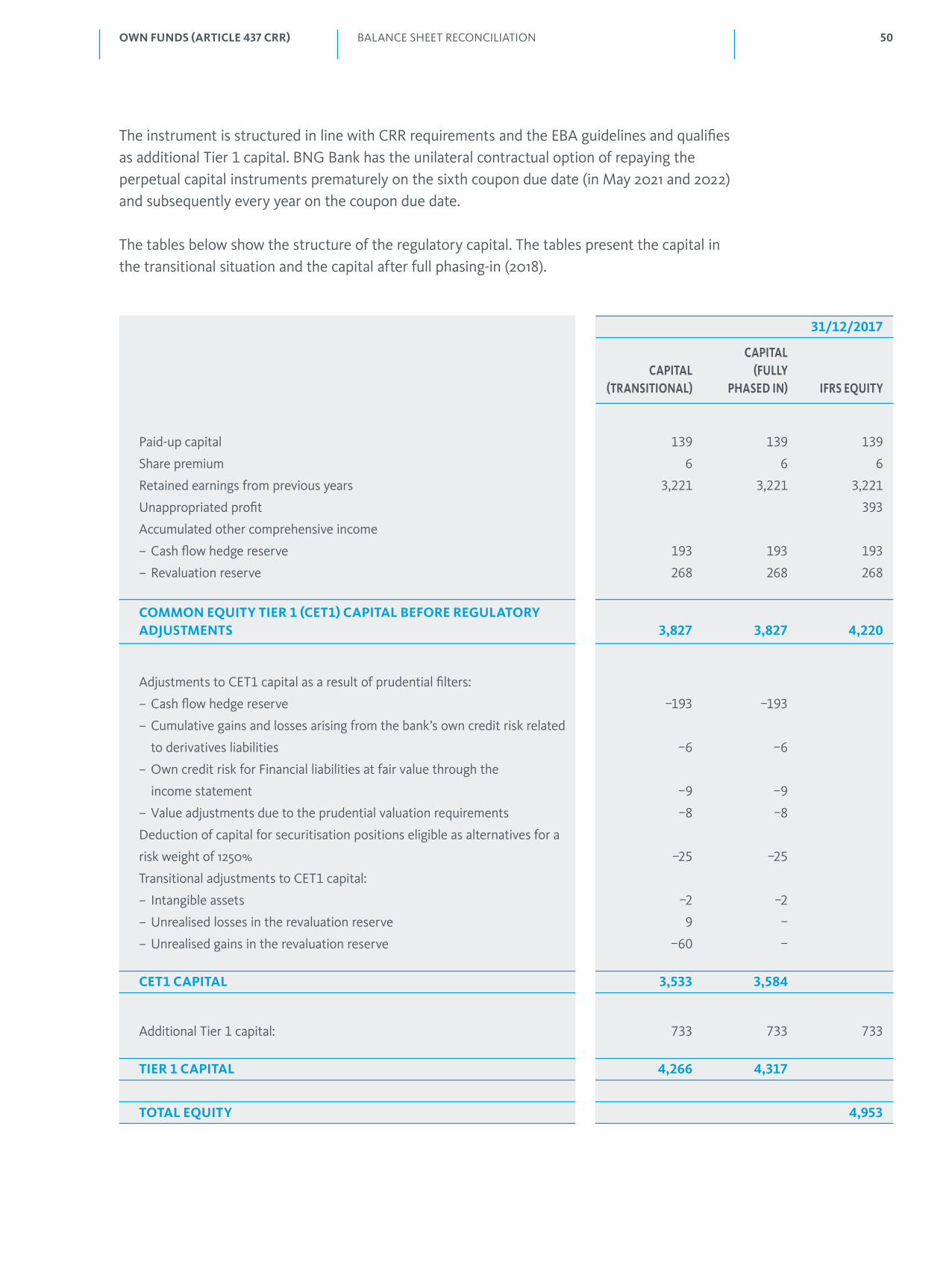

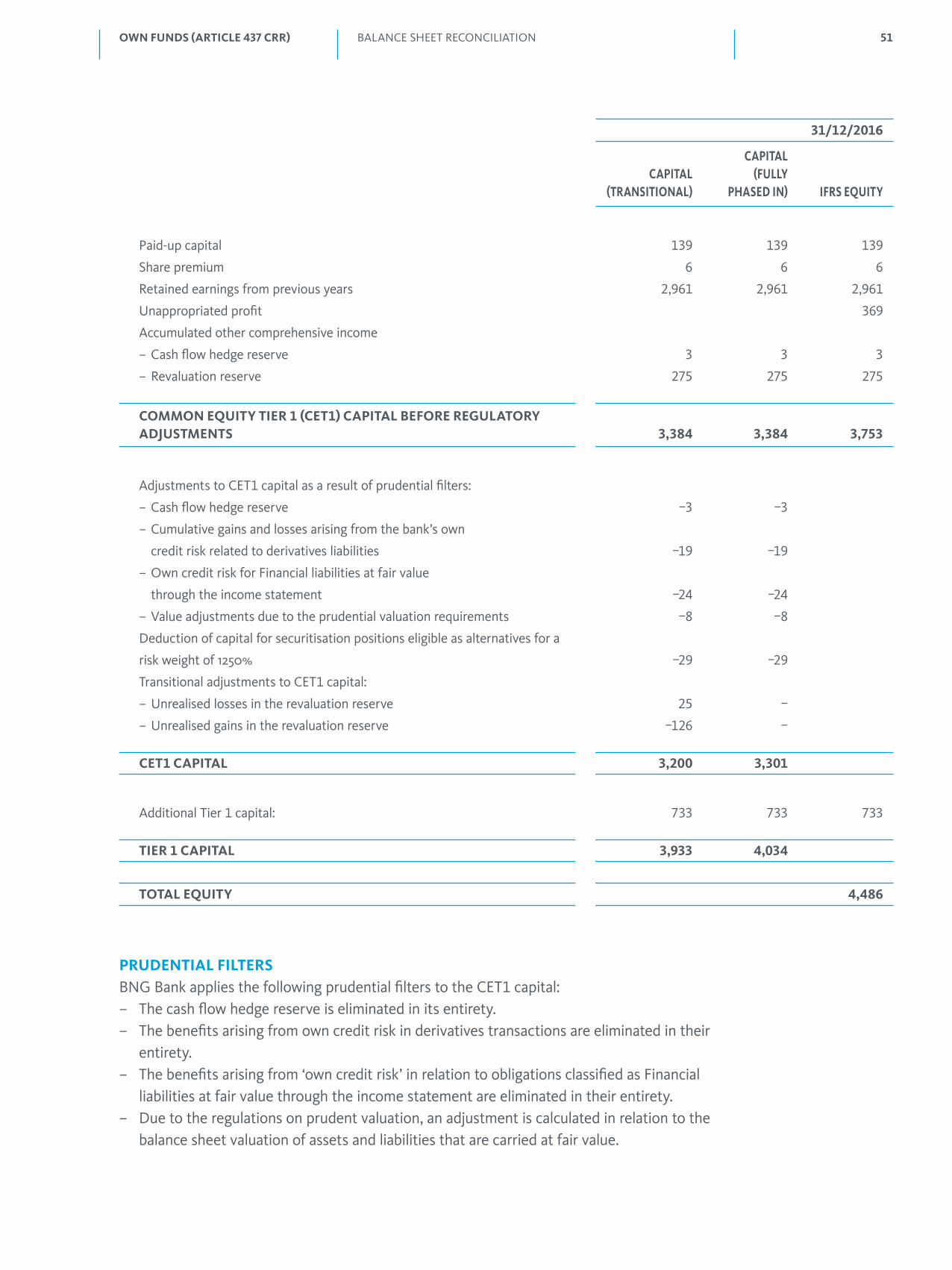

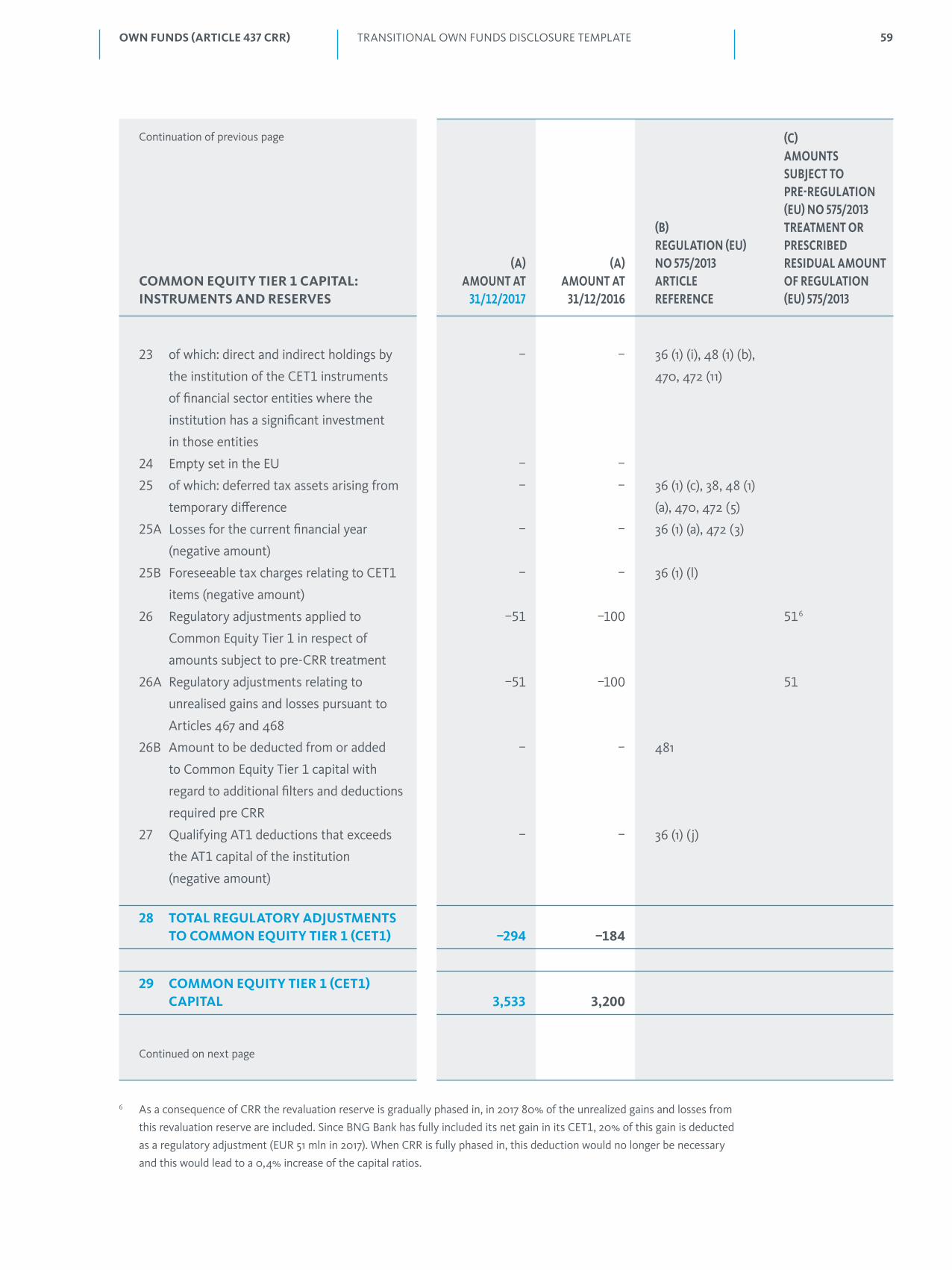

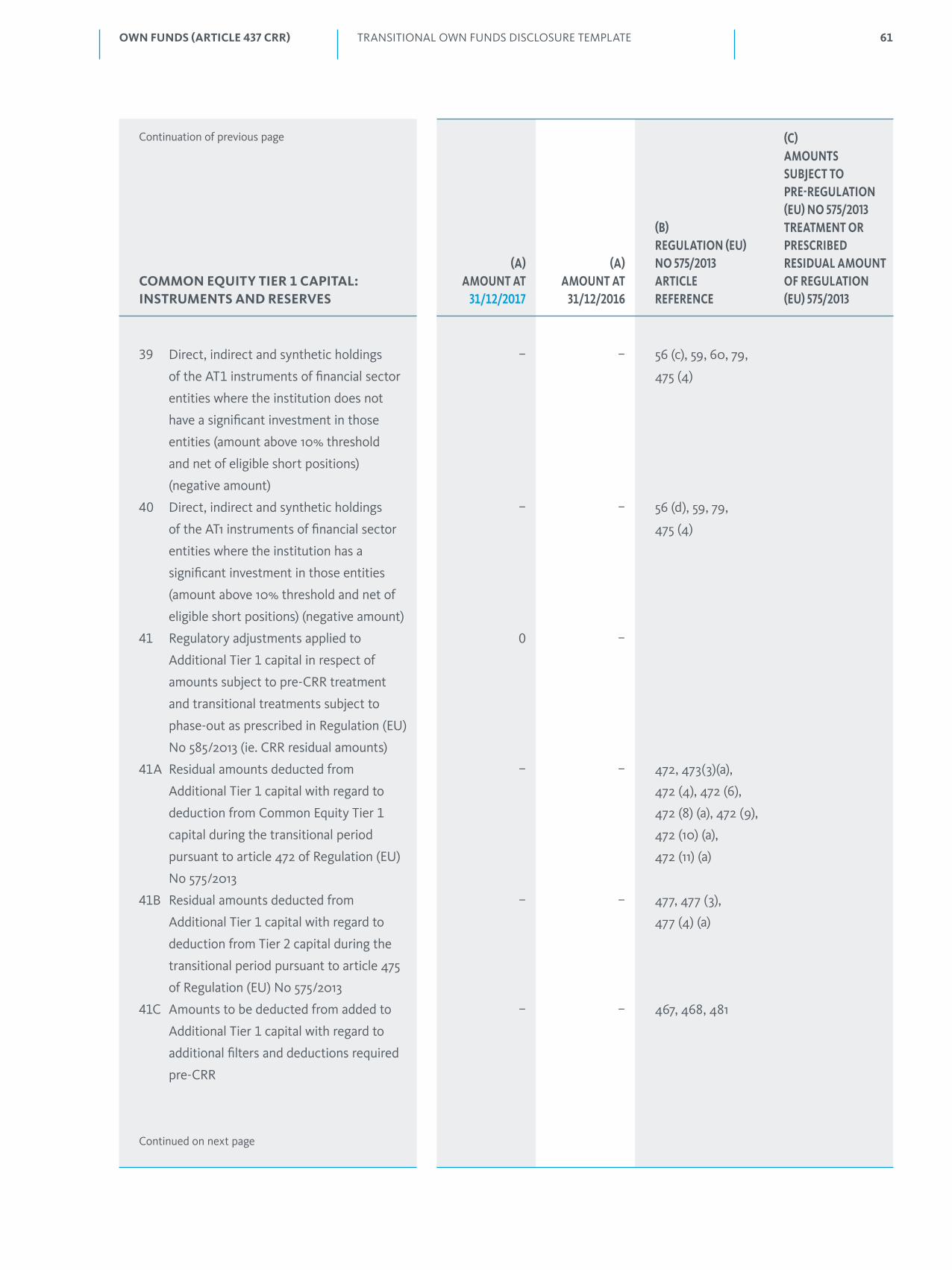

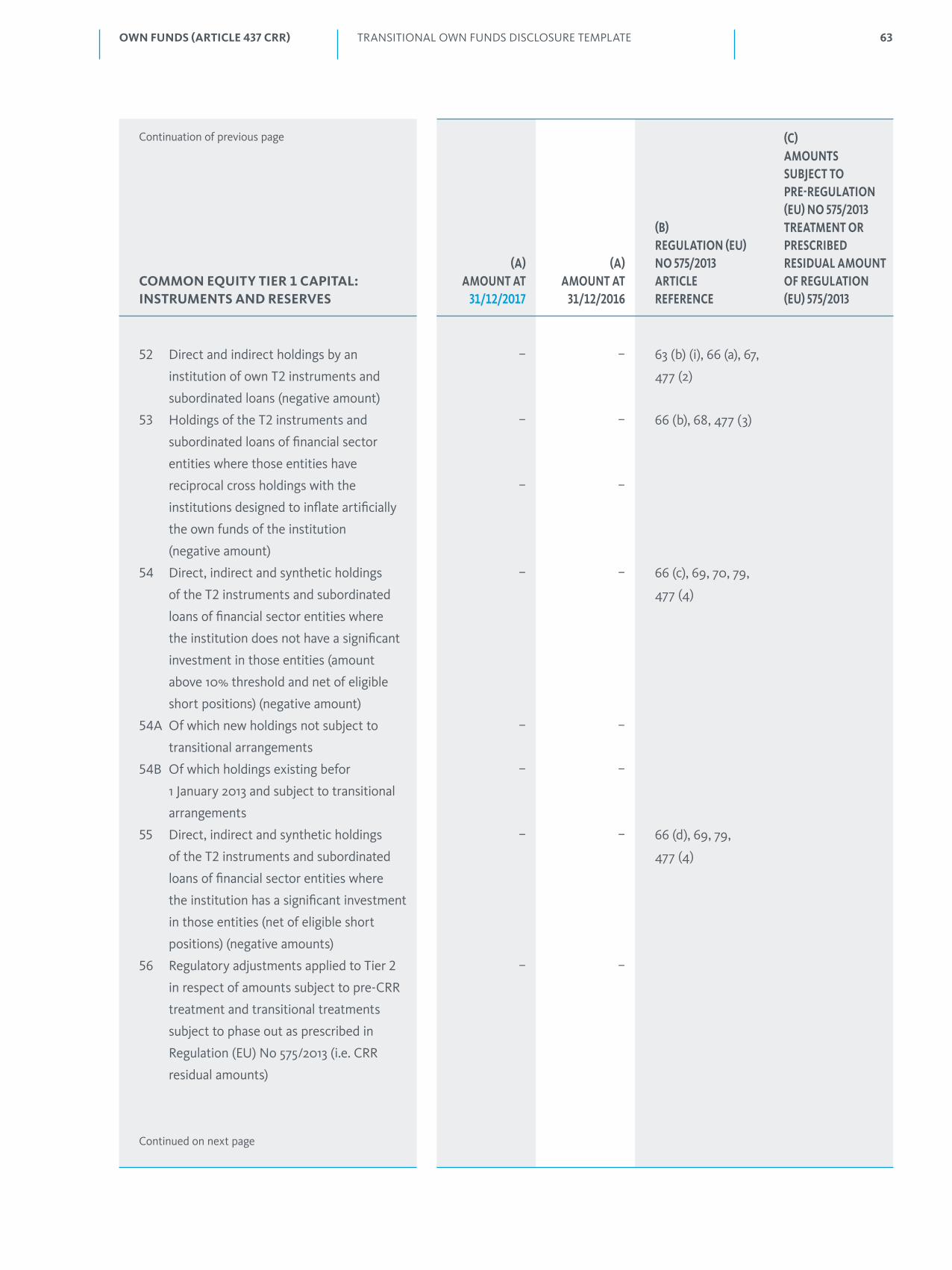

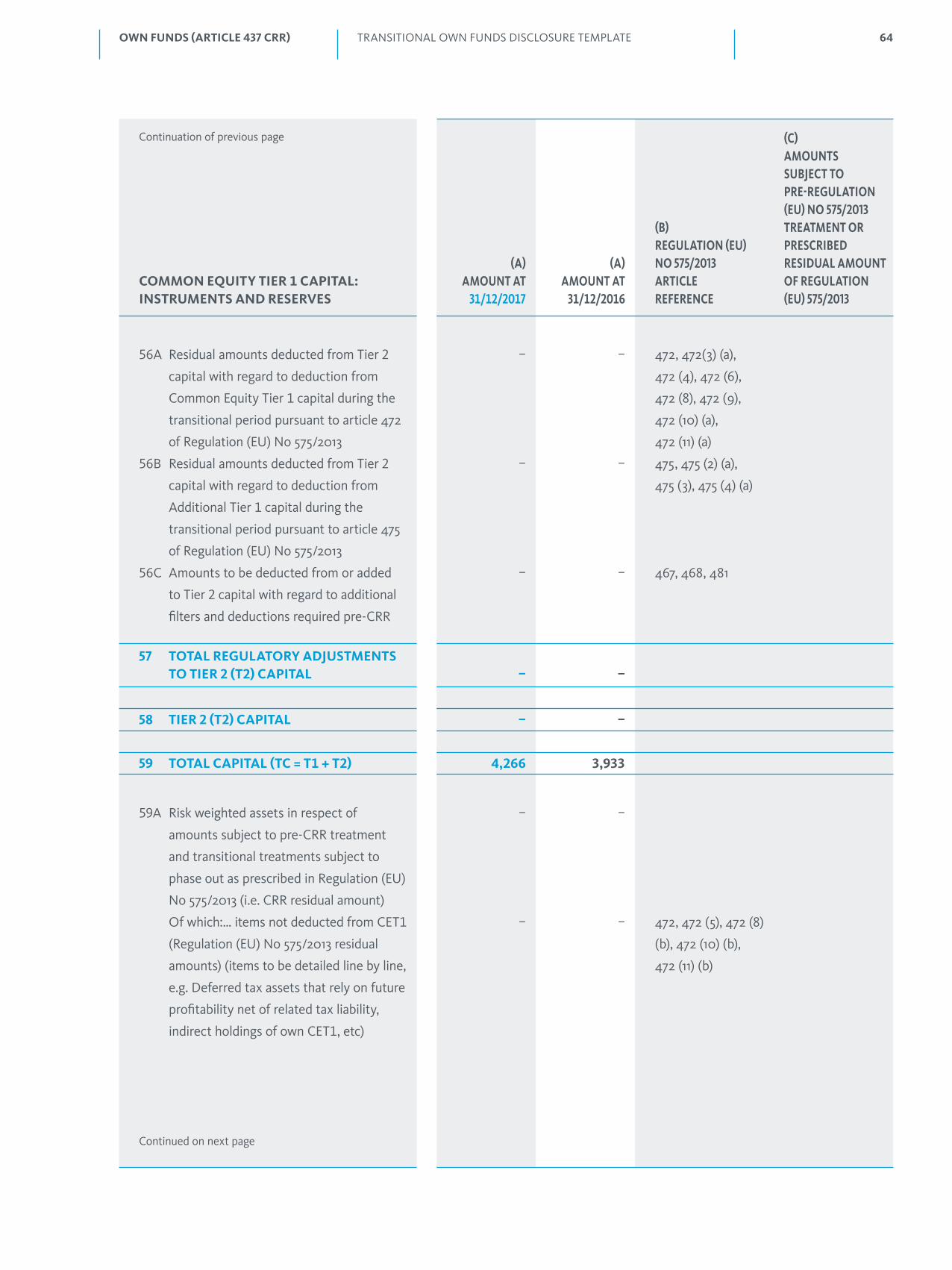

Own funds (article 437 CRR) 49

Balance Sheet Reconciliation 49

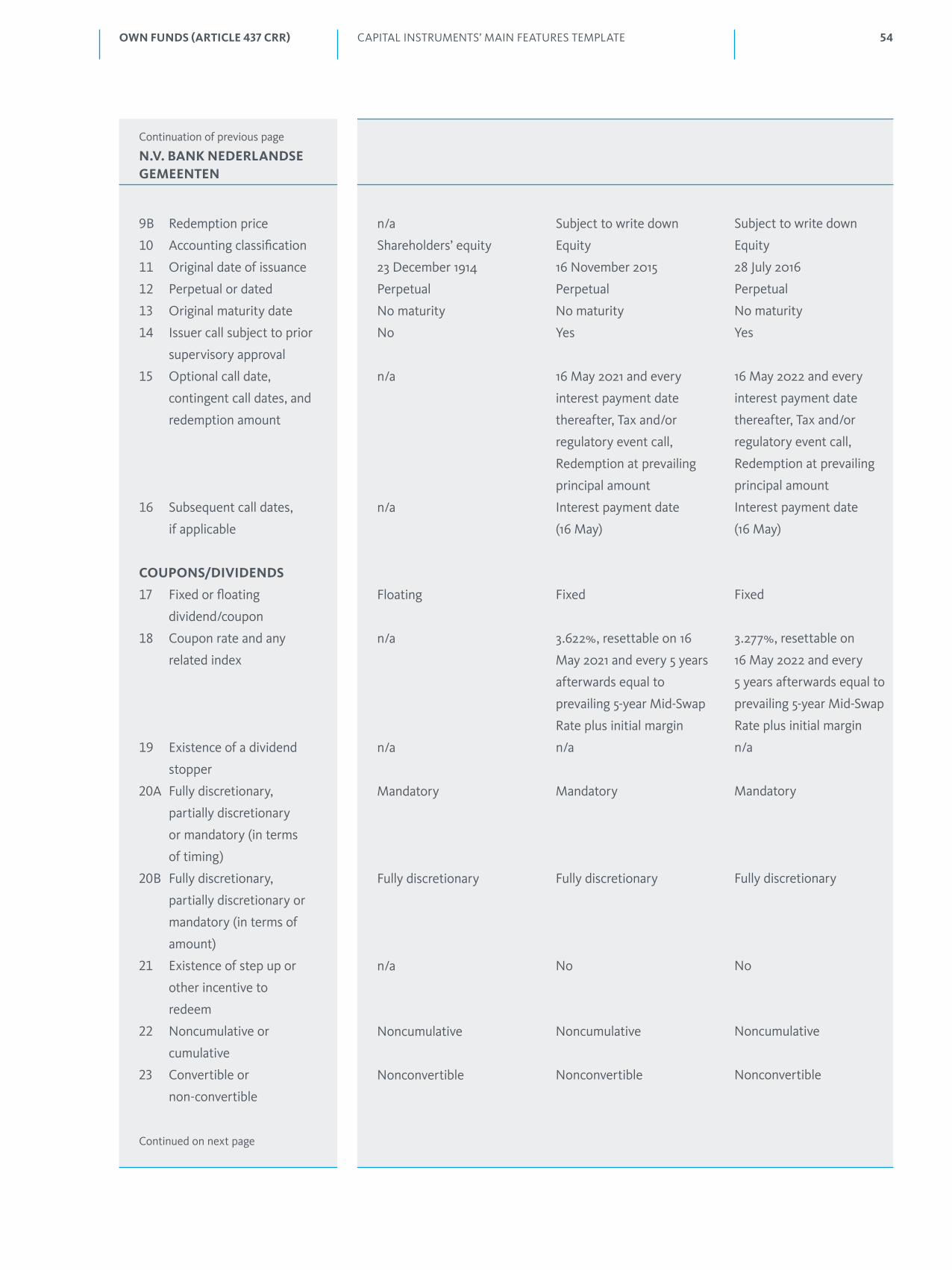

Capital instruments’ main features template 53

Transitional own funds disclosure template 56

3

Capital requirements (article 438 CRR) 69

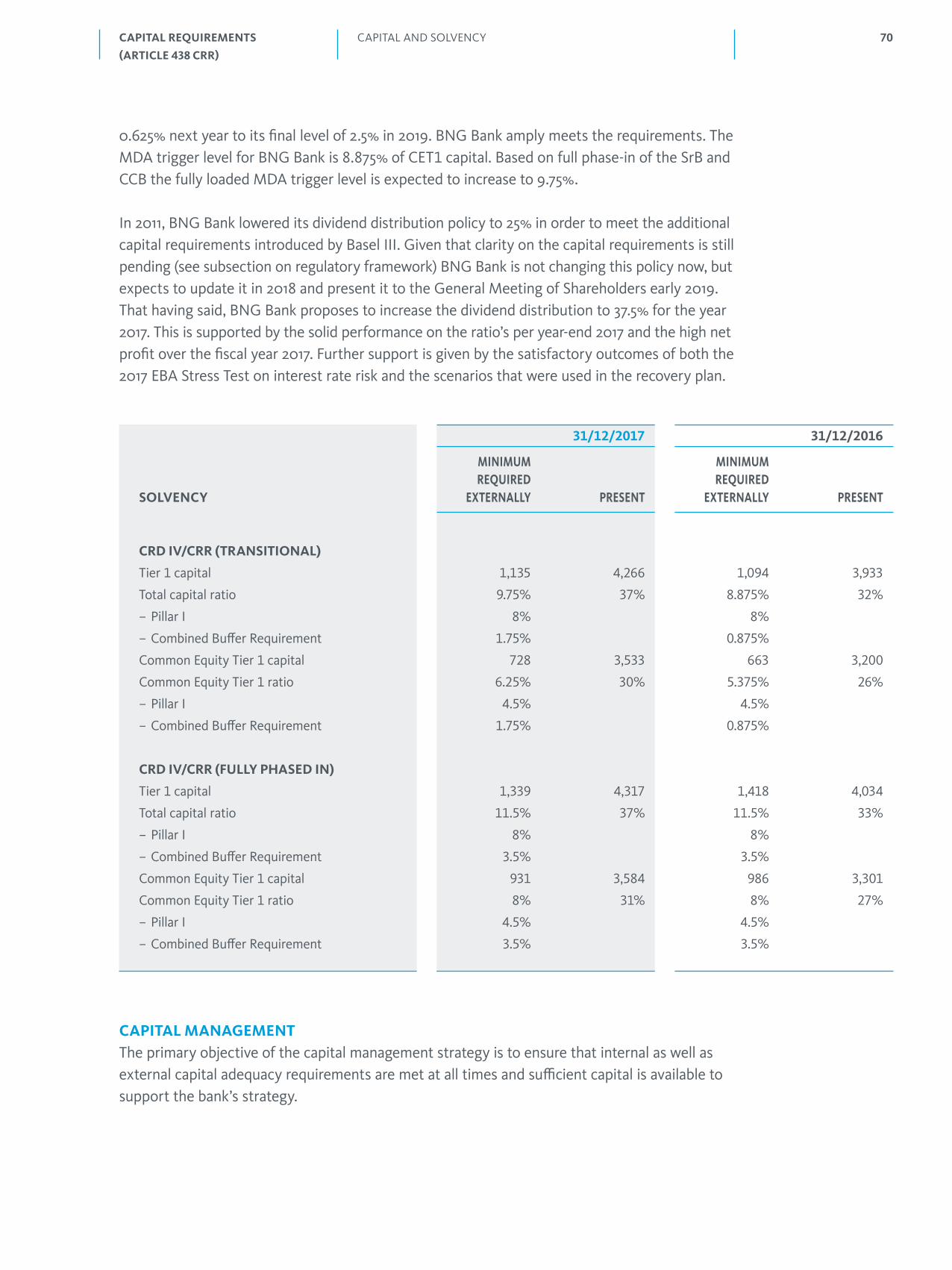

Capital and Solvency 69

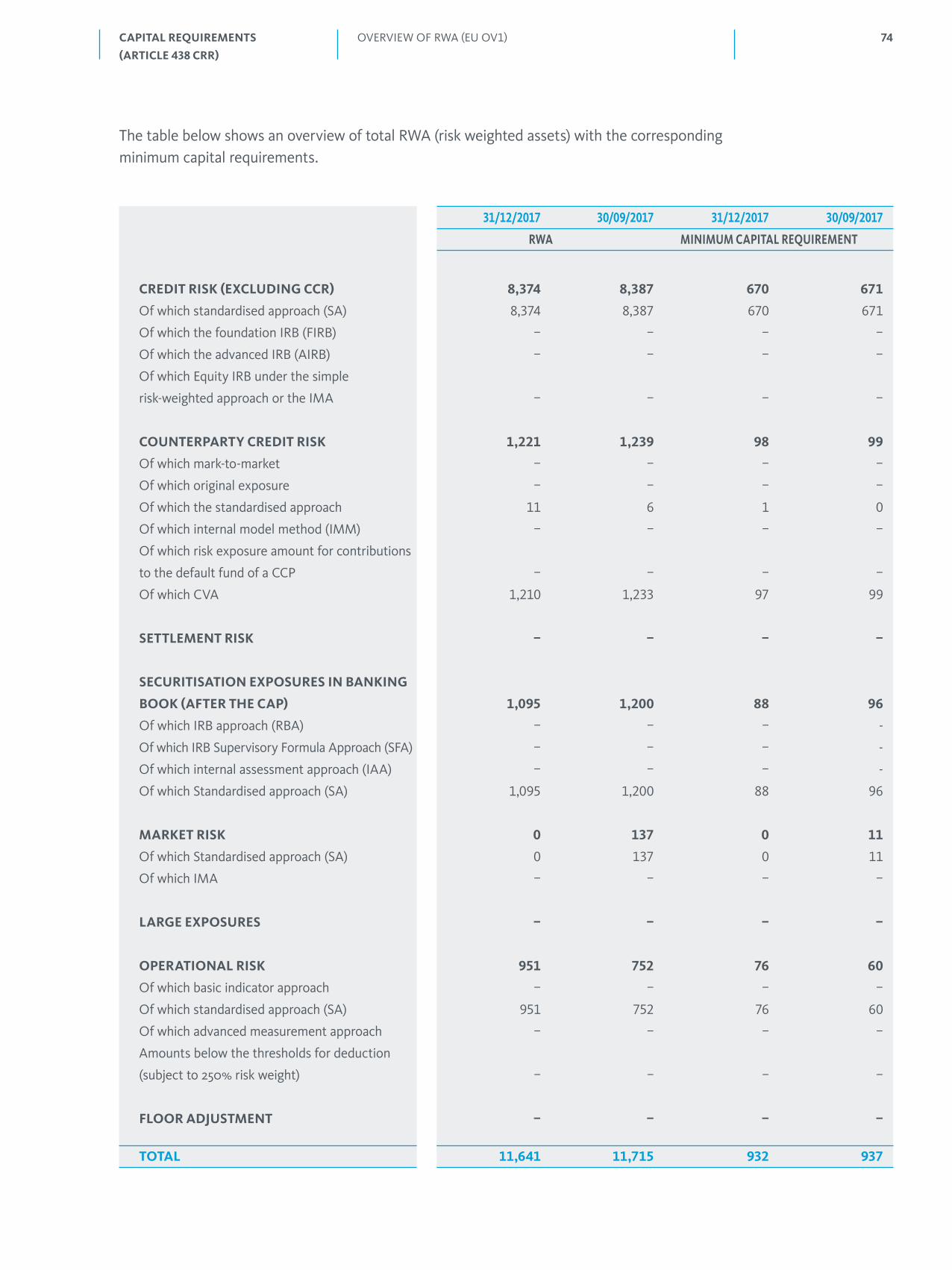

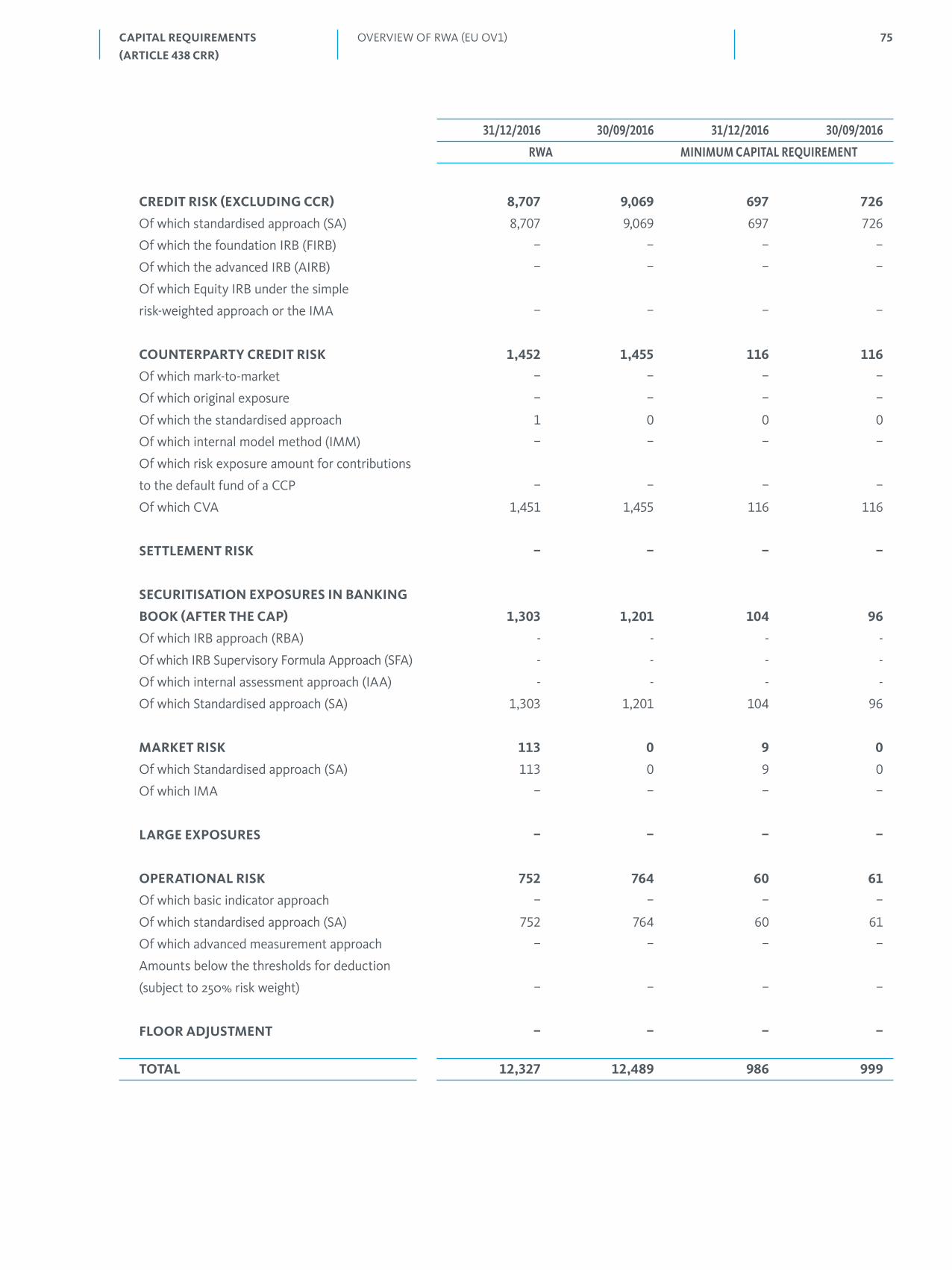

Overview of RWA (EU OV1) 73

Credit risk and credit risk mitigation (article 442 en 453 CCR) 76

Credit quality assets 77

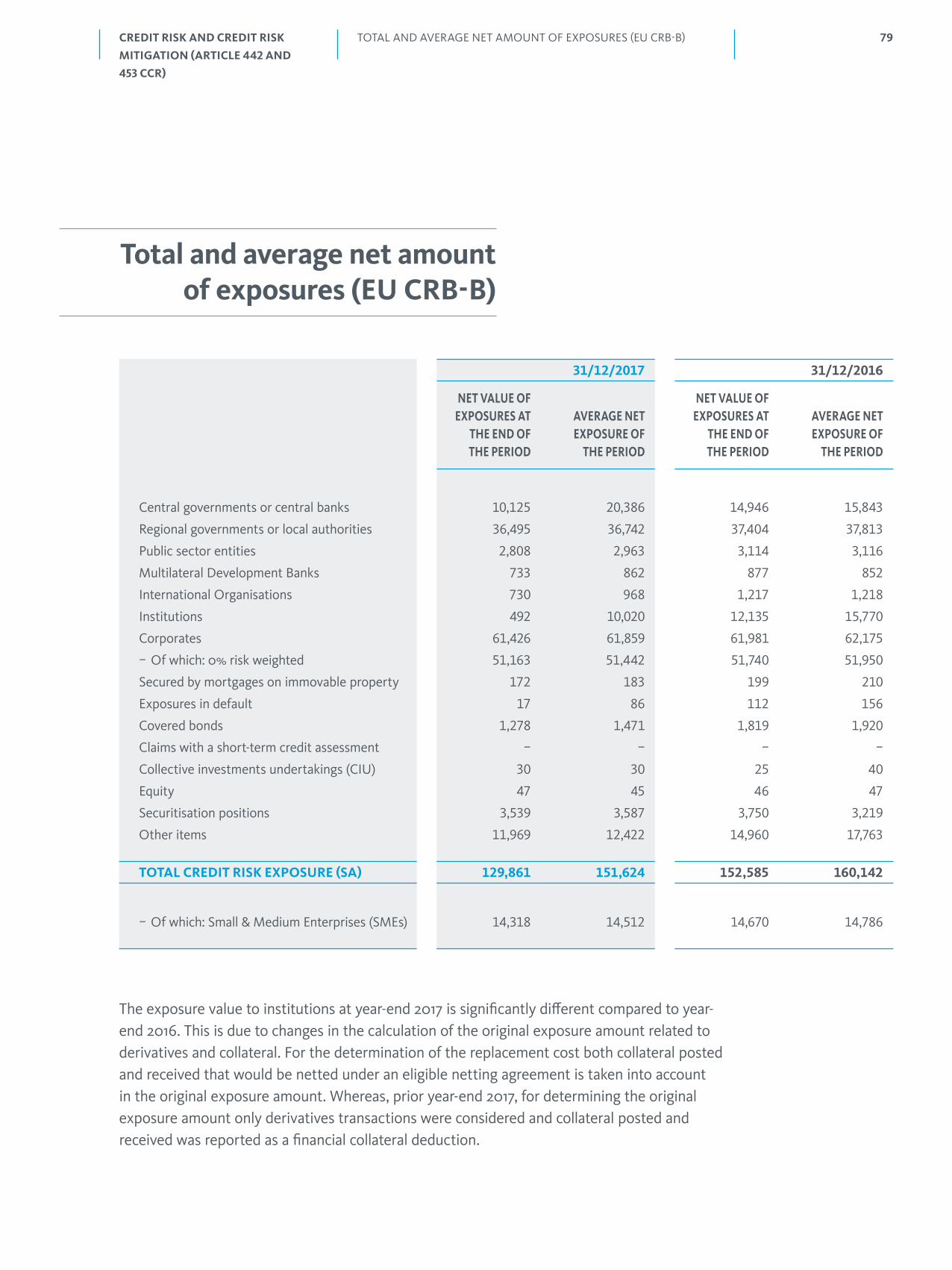

Total and average net amount of exposures (EU CRB-B) 79

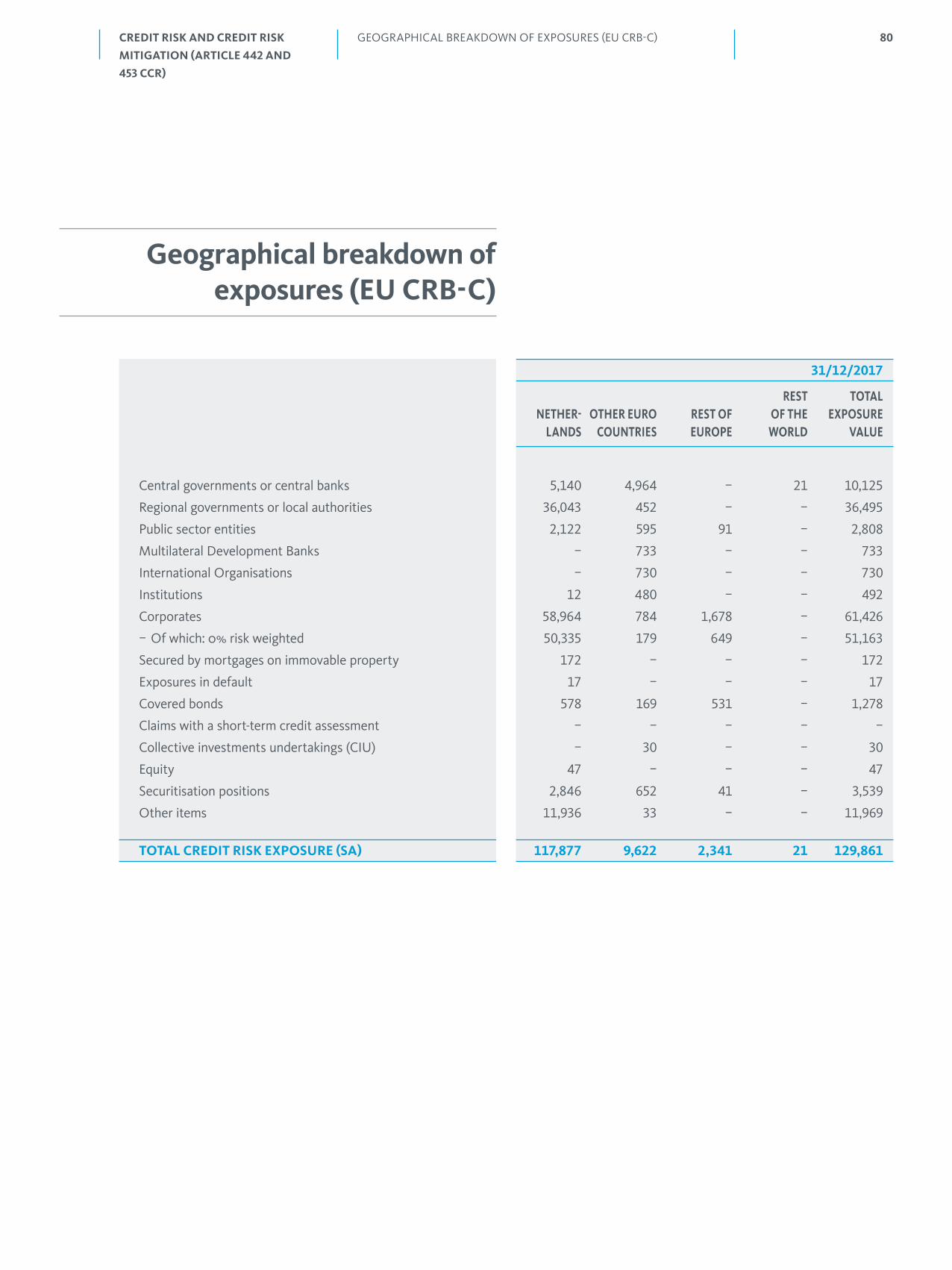

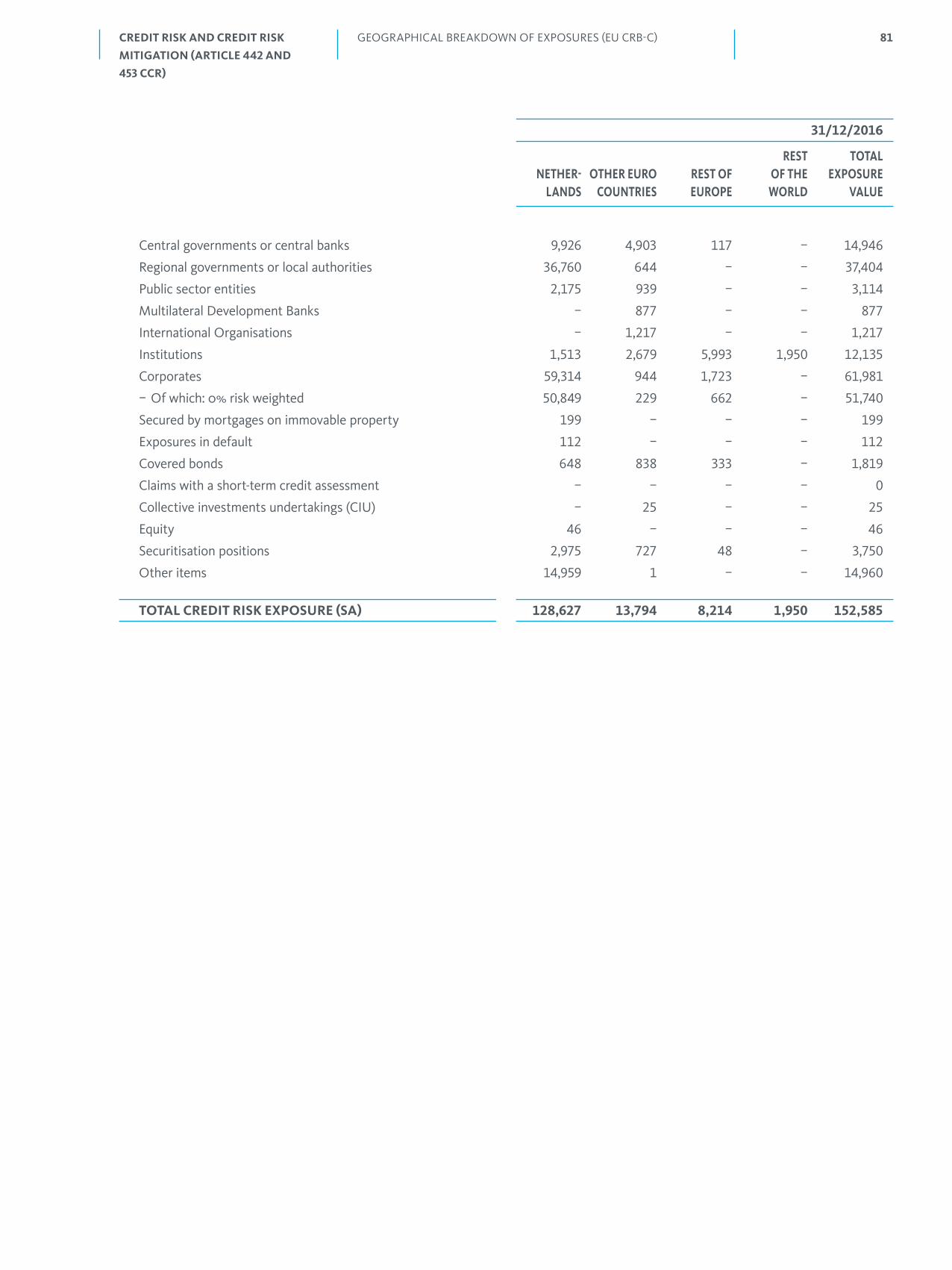

Geographical breakdown of exposures (EU CRB-C) 80

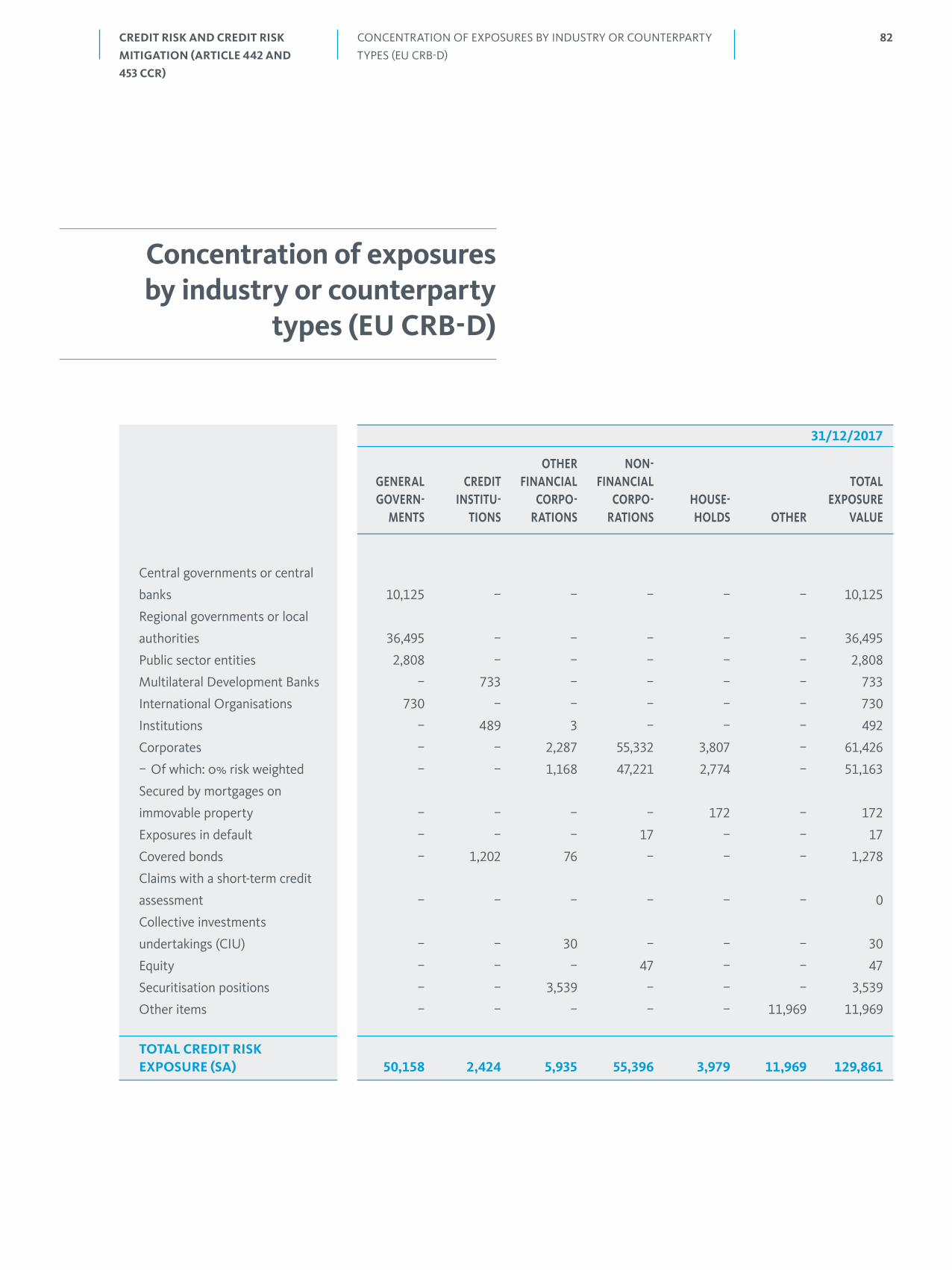

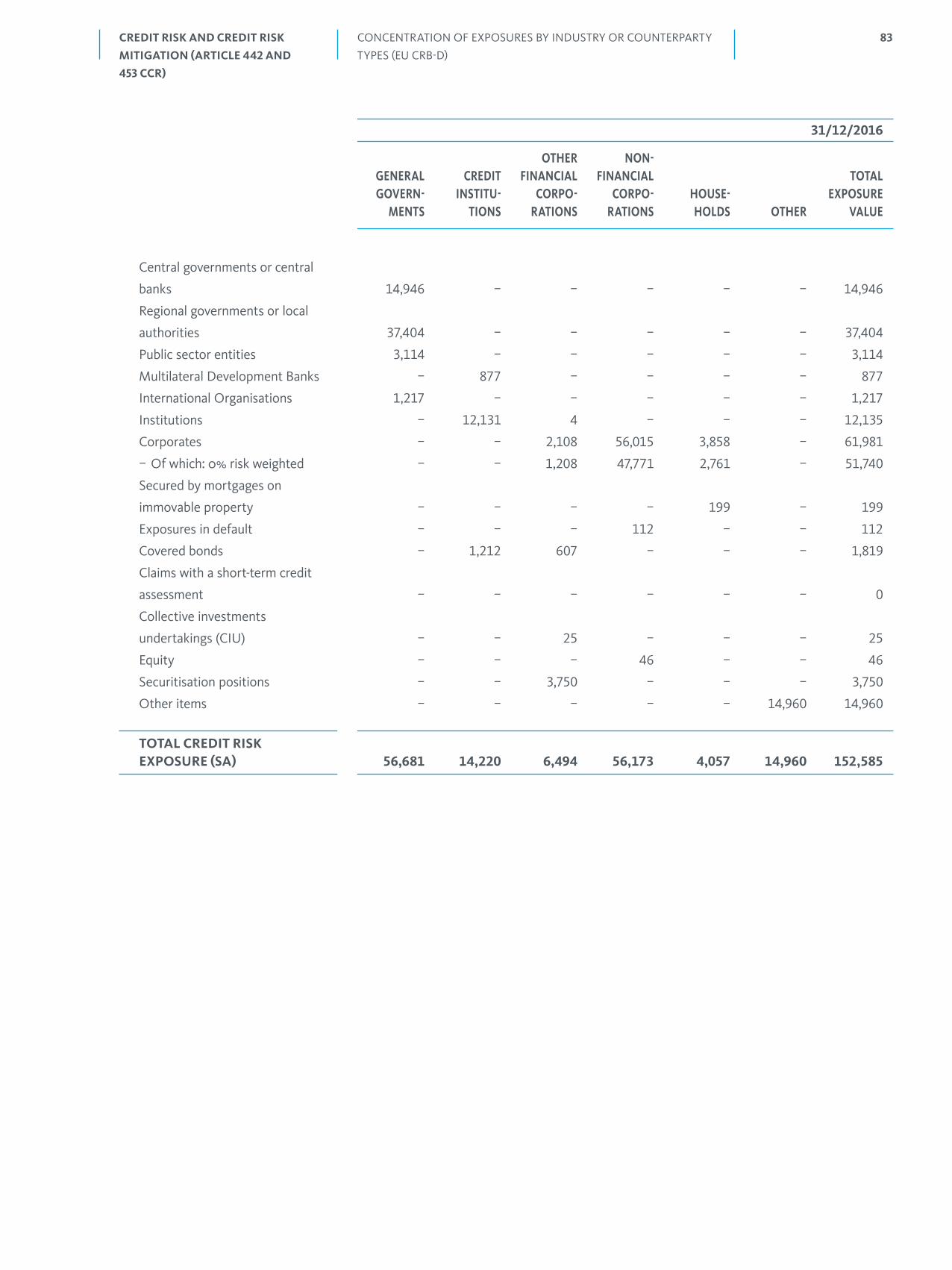

Concentration of exposures by industry or counterparty types (EU CRB-D) 82

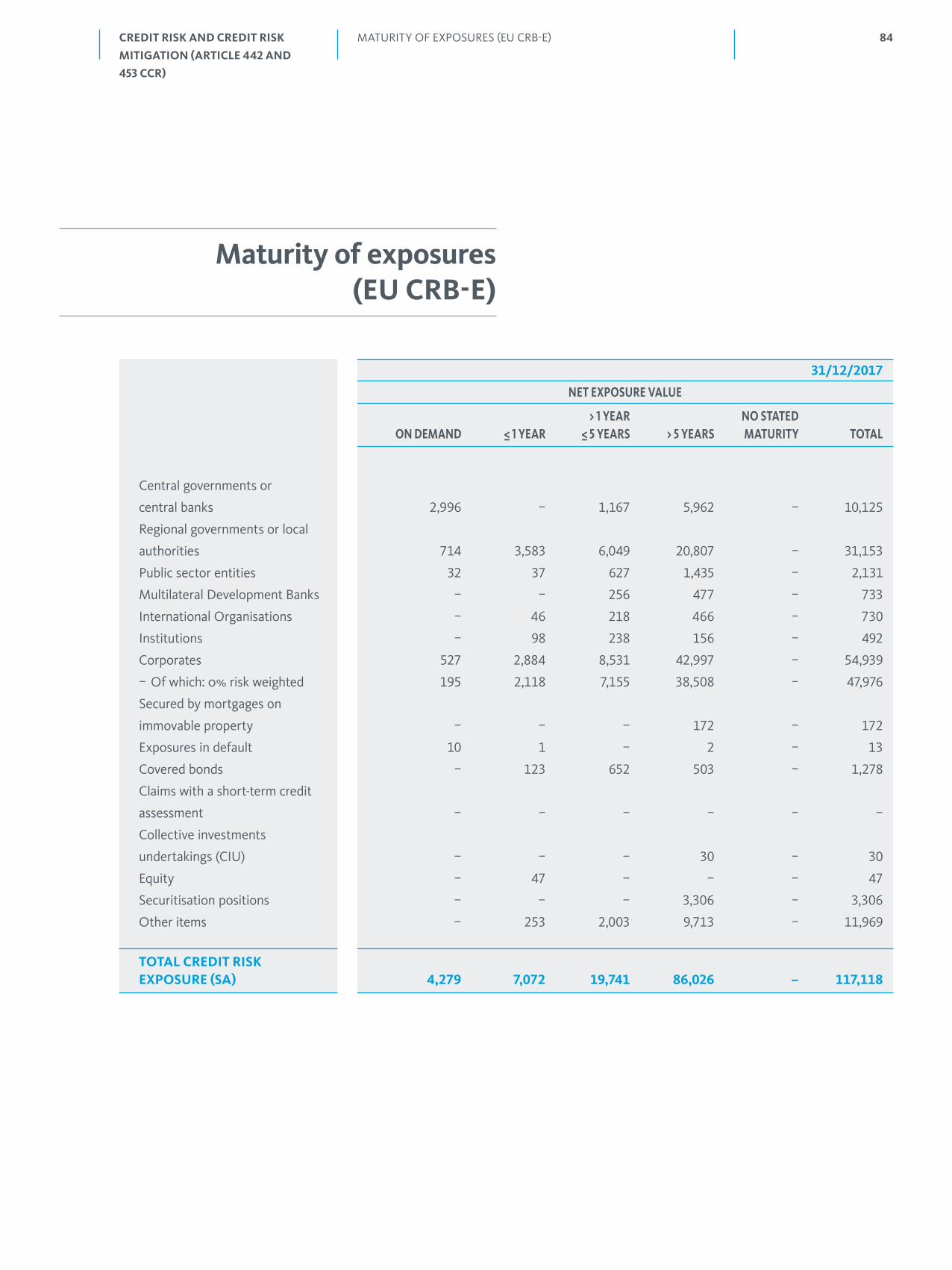

Maturity of exposures (EU CRB-E) 84

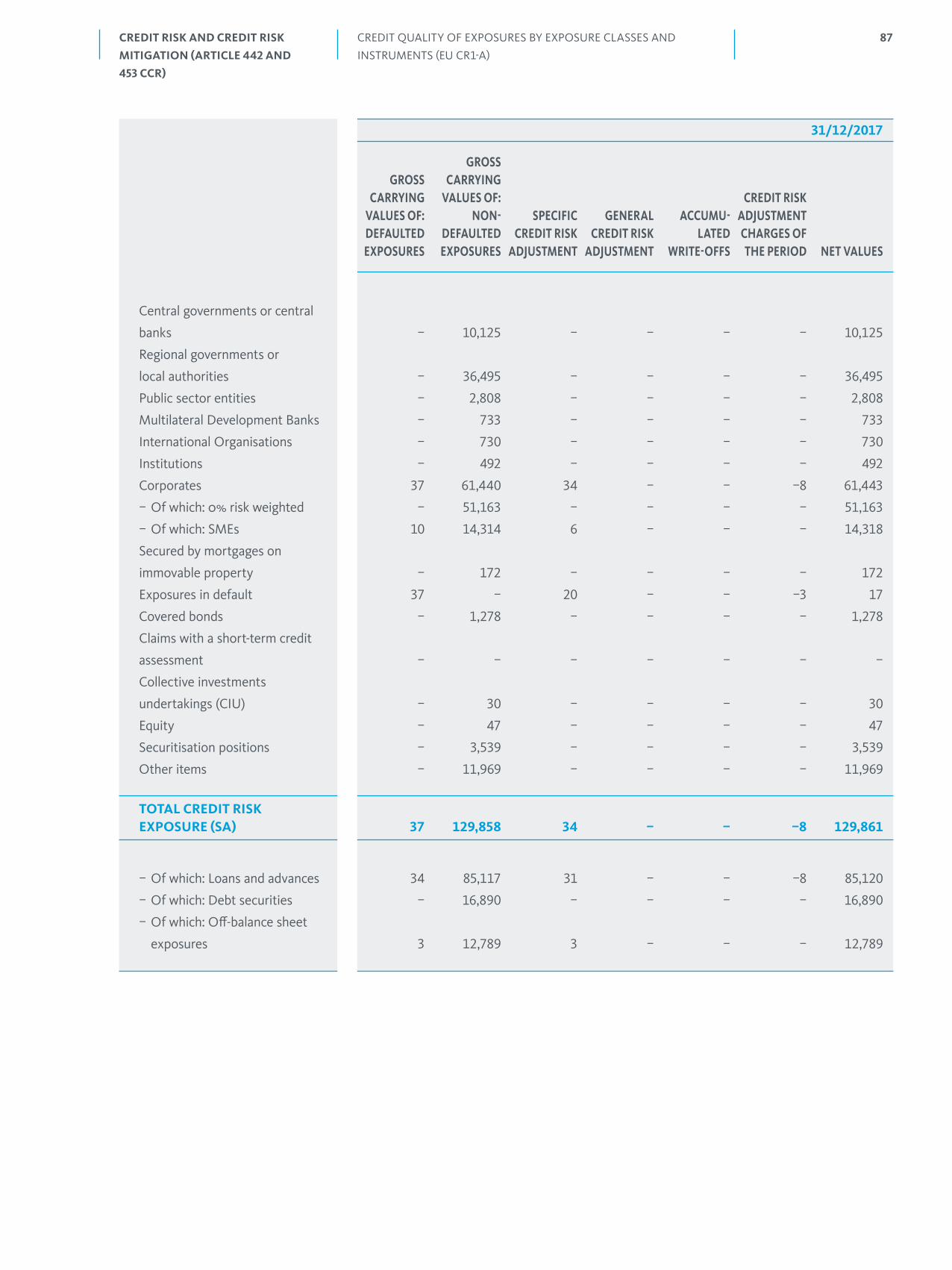

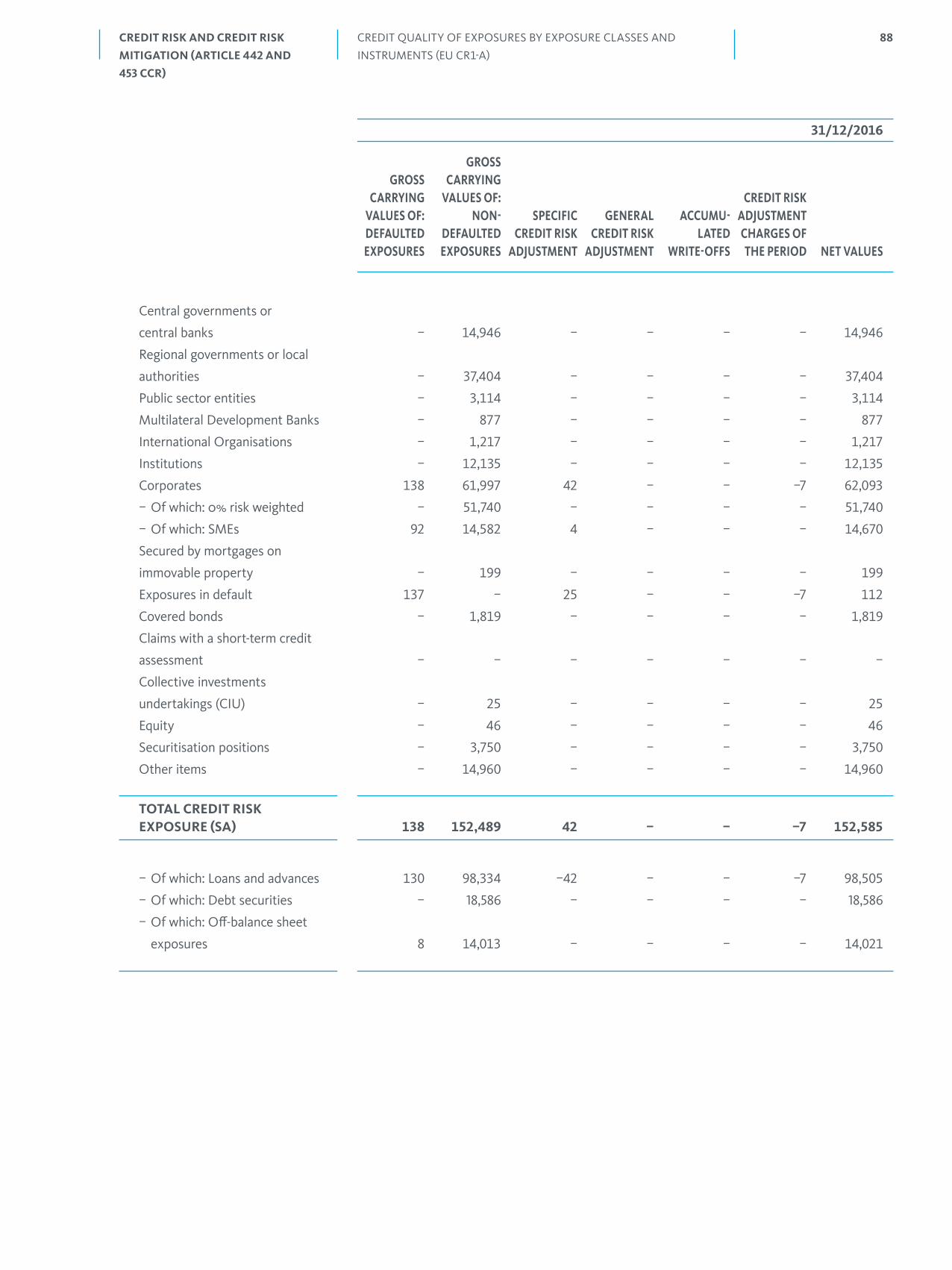

Credit quality of exposures by exposure classes and instruments (EU CR1-A) 86

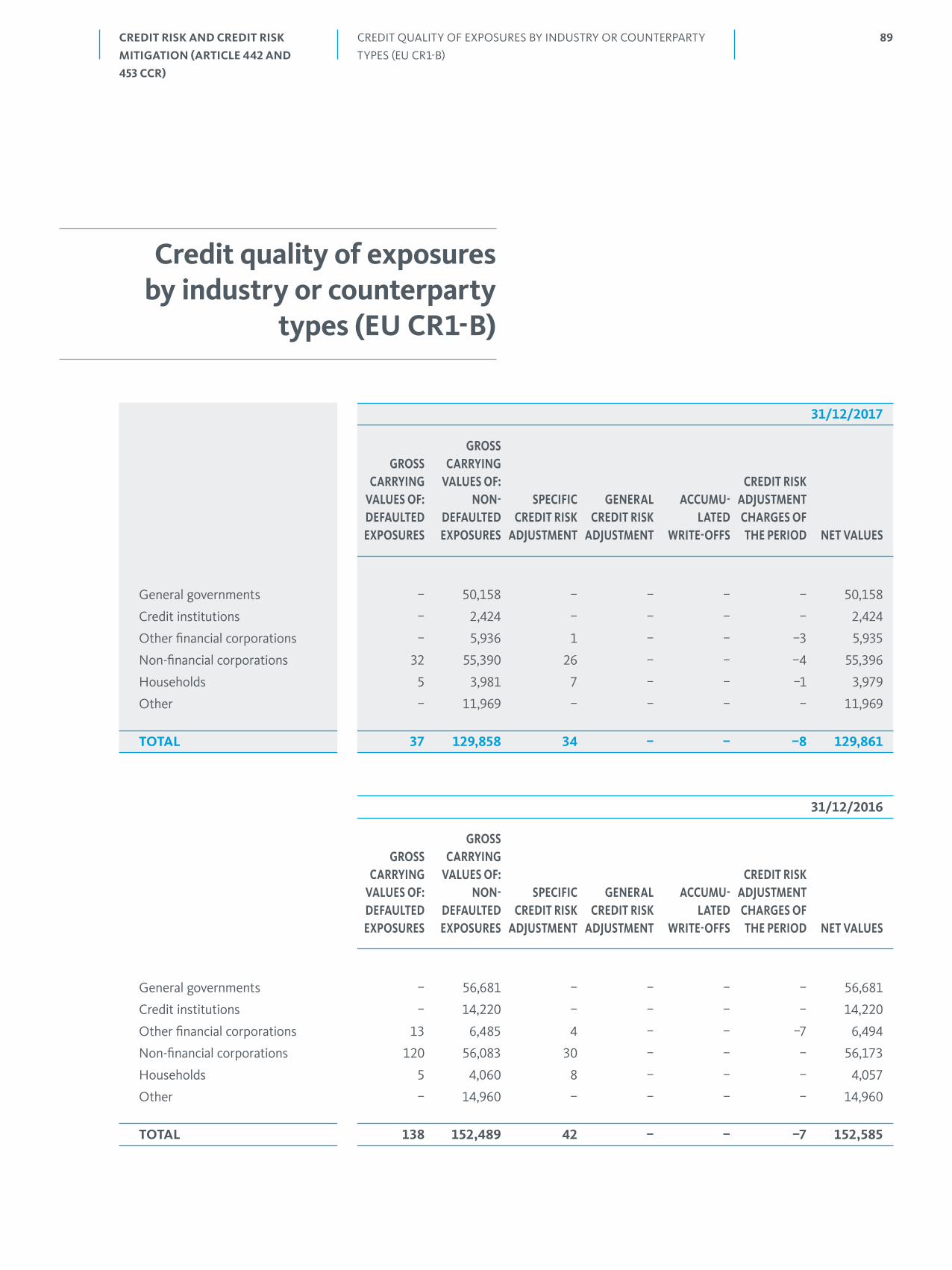

Credit quality of exposures by industry or counterparty types (EU CR1-B) 89

Credit quality of exposures by geography (EU CR1-C) 90

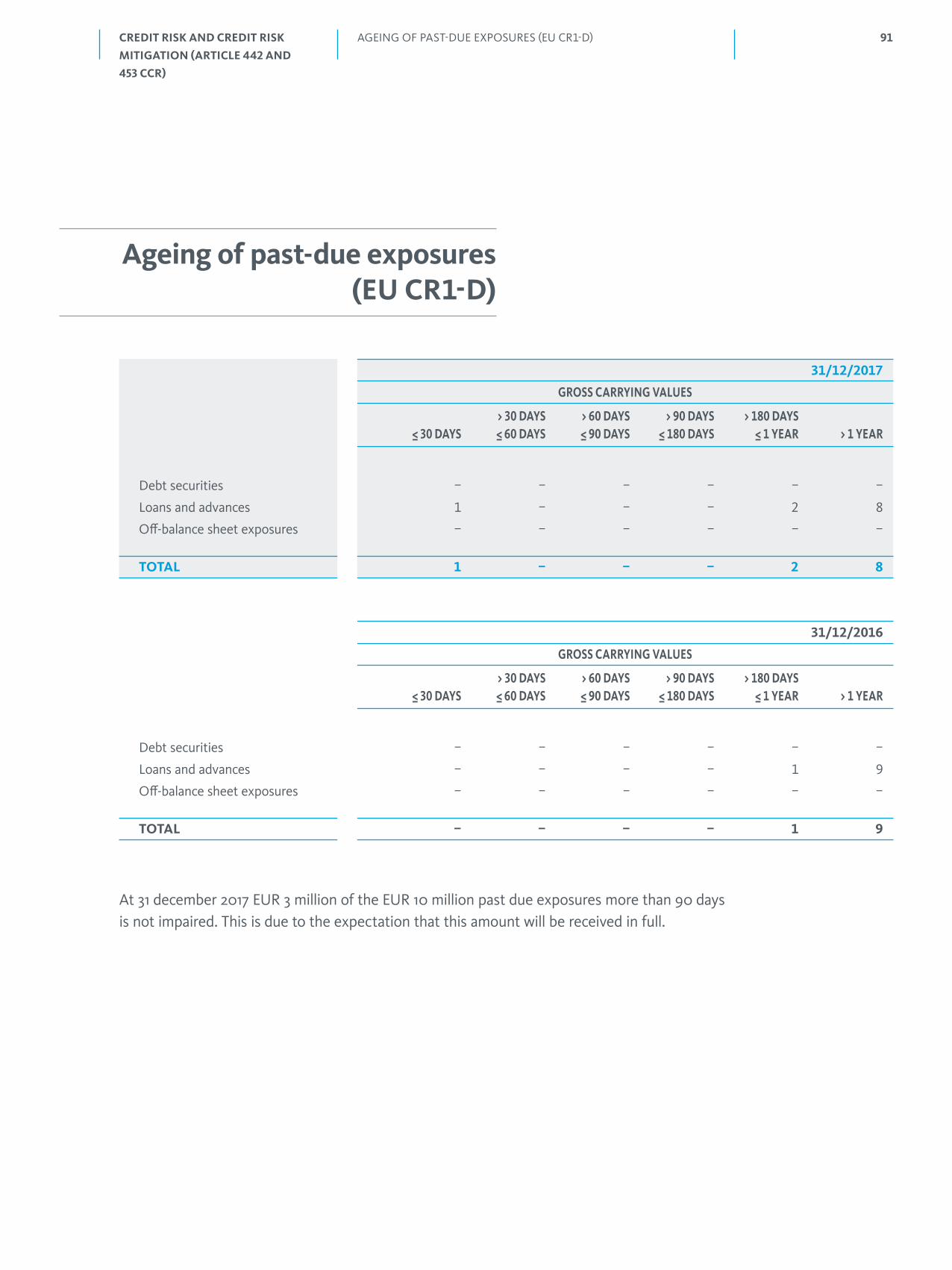

Ageing of past-due exposures (EU CR1-D) 91

Non-performing and forborne exposures (EU CR1-E) 92

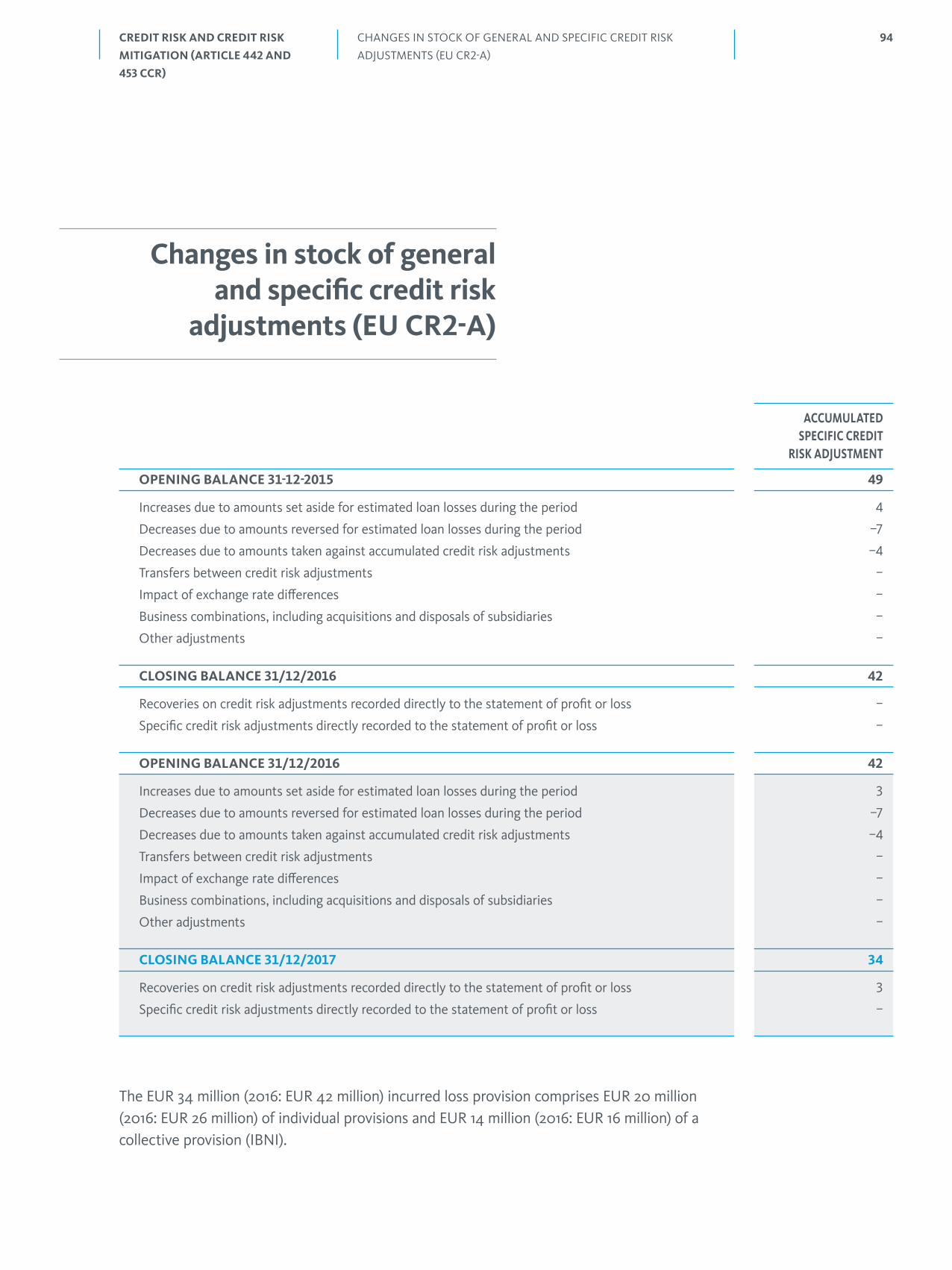

Changes in stock of general and specific credit risk adjustments (EU CR2-A) 94

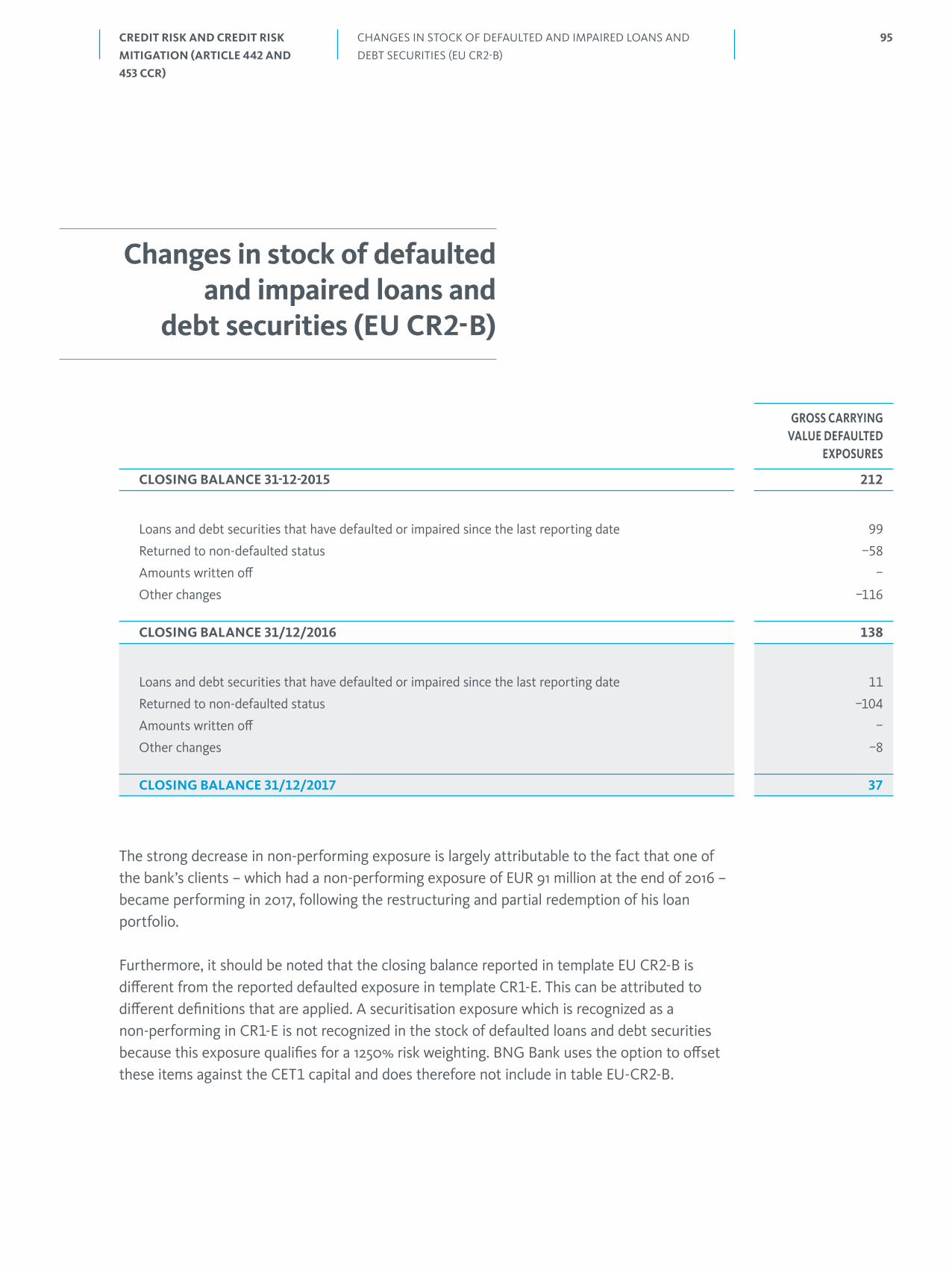

Changes in stock of defaulted and impaired loans and debt securities (EU CR2-B) 95

Credit risk mitigation techniques – overview (EU CR3) 96

Standardised approach – credit risk exposure and Credit Risk Mitigation (CRM) effects (EU CR4) 97

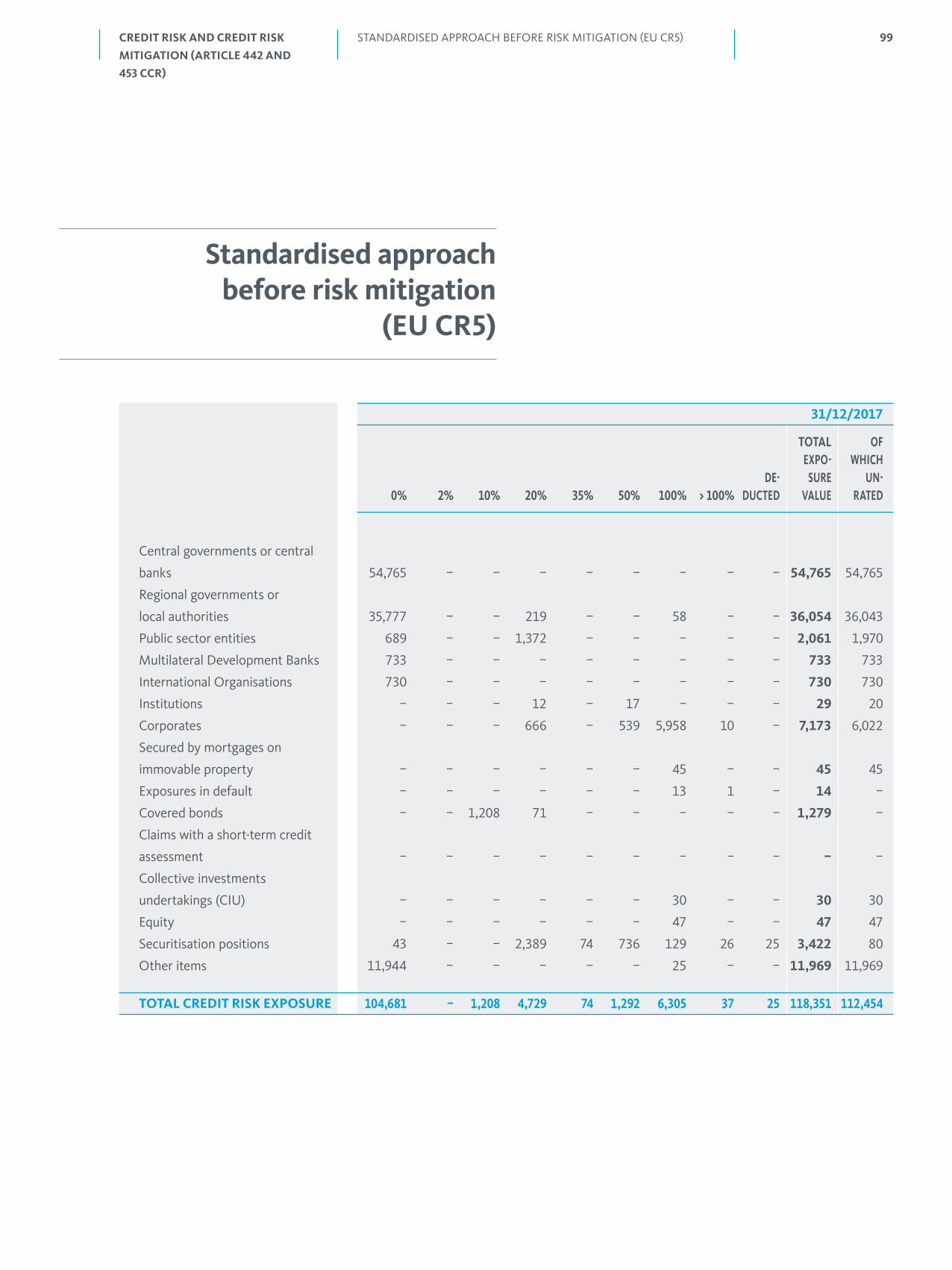

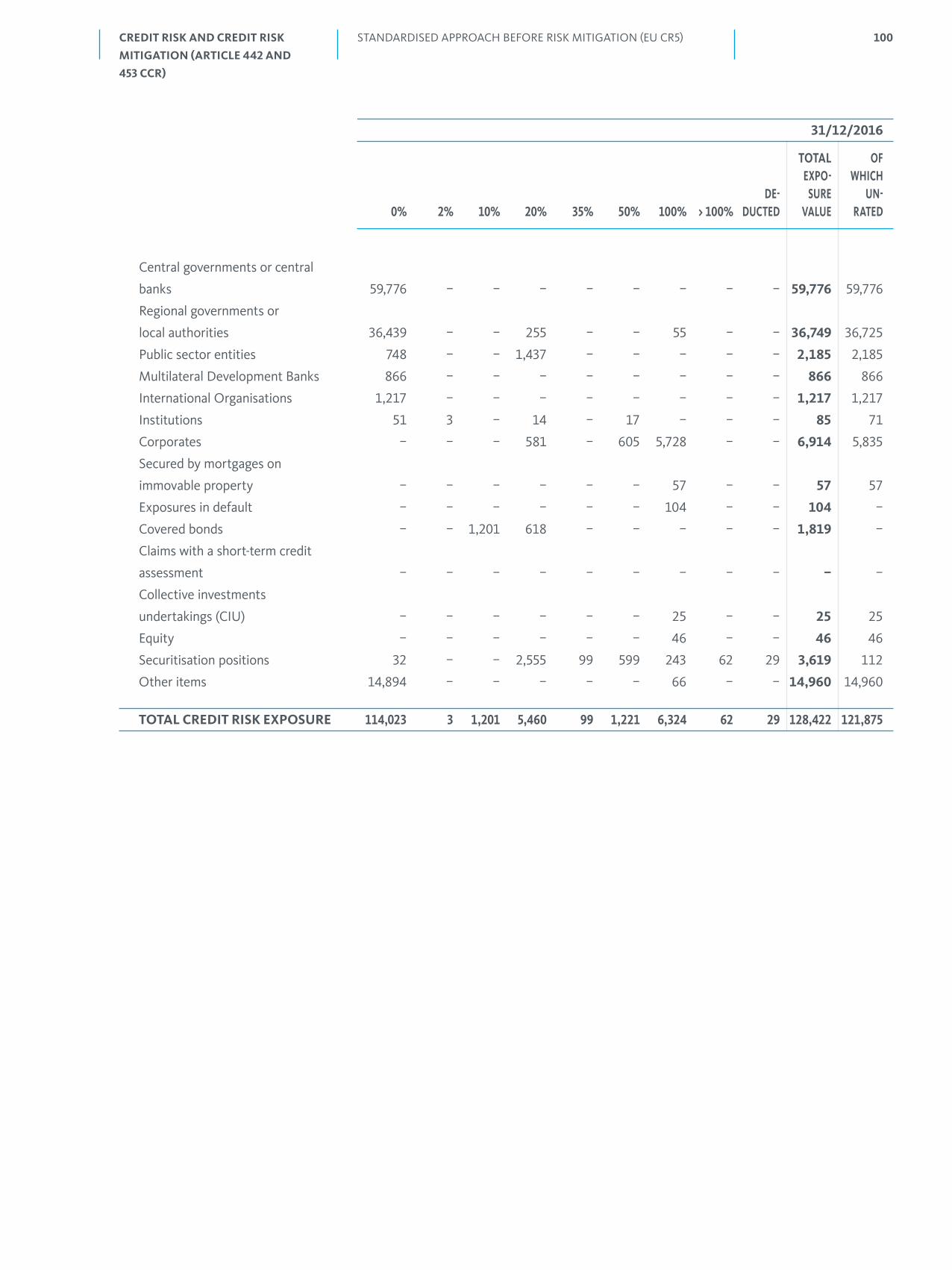

Standardised approach before risk mitigation (EU CR5) 99

Counterparty credit risk (article 439 CRR) 101

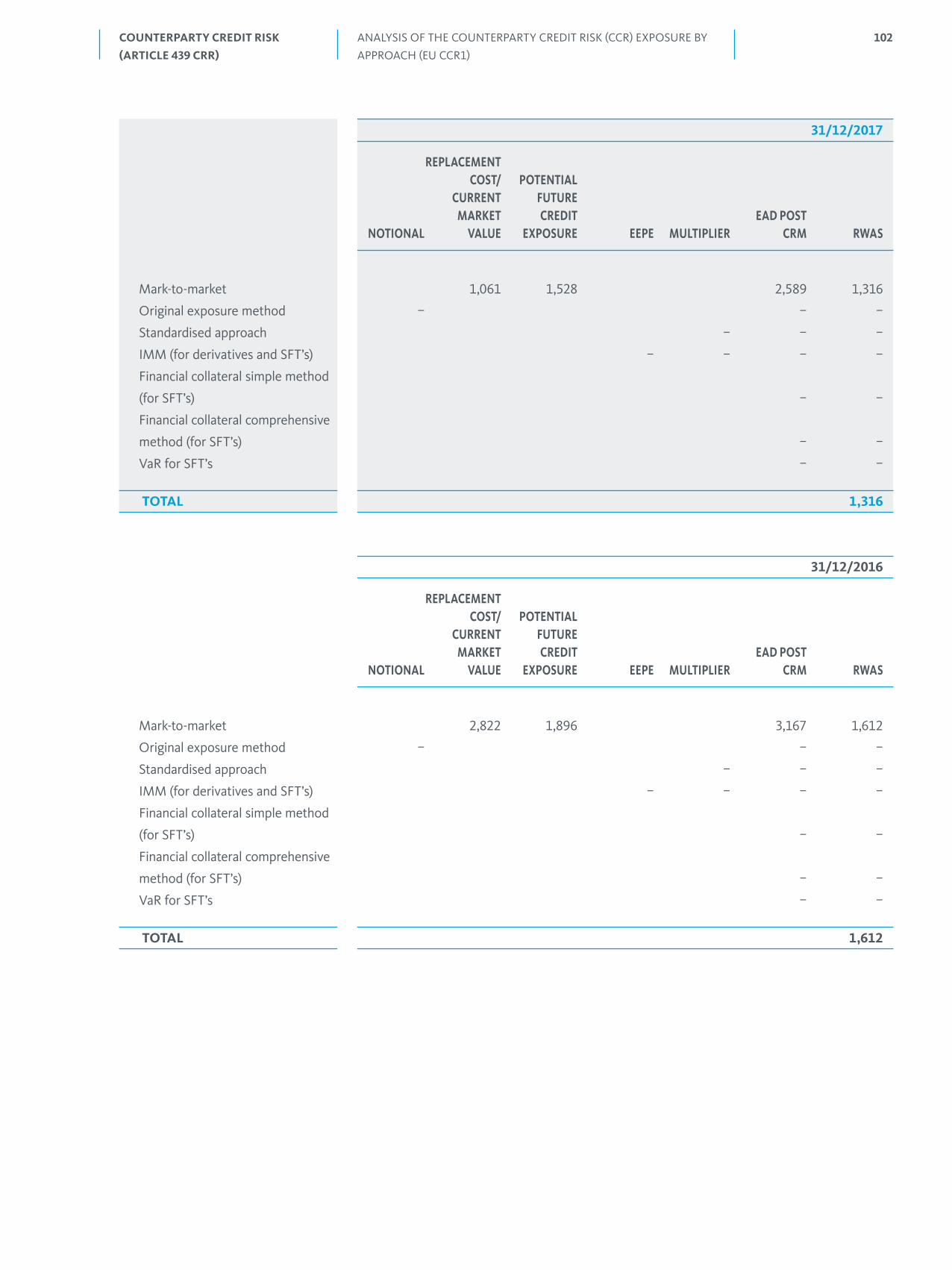

Analysis of the counterparty credit risk (CCR) exposure by approach (EU CCR1) 101

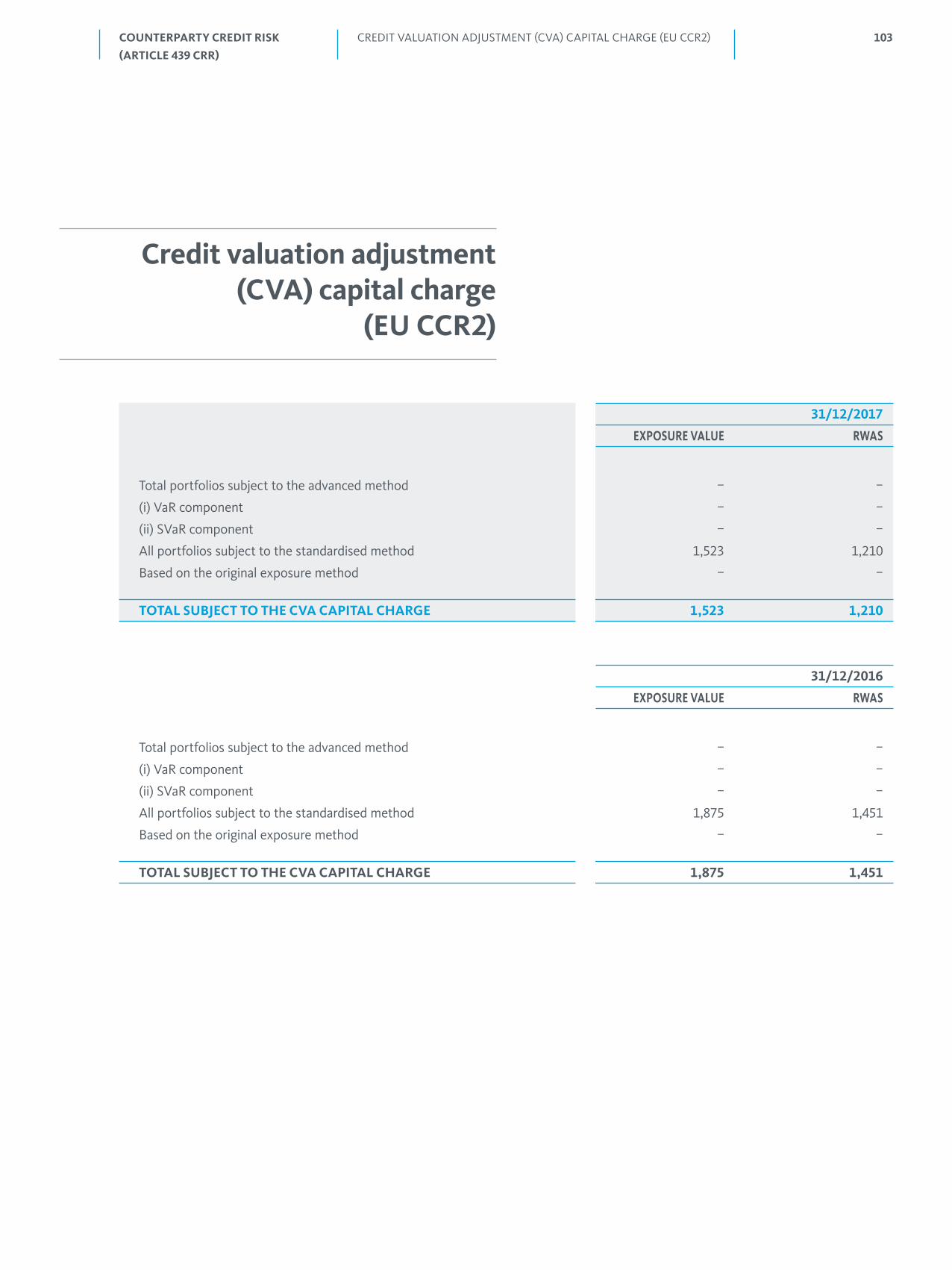

Credit valuation adjustment (CVA) capital charge (EU CCR2) 103

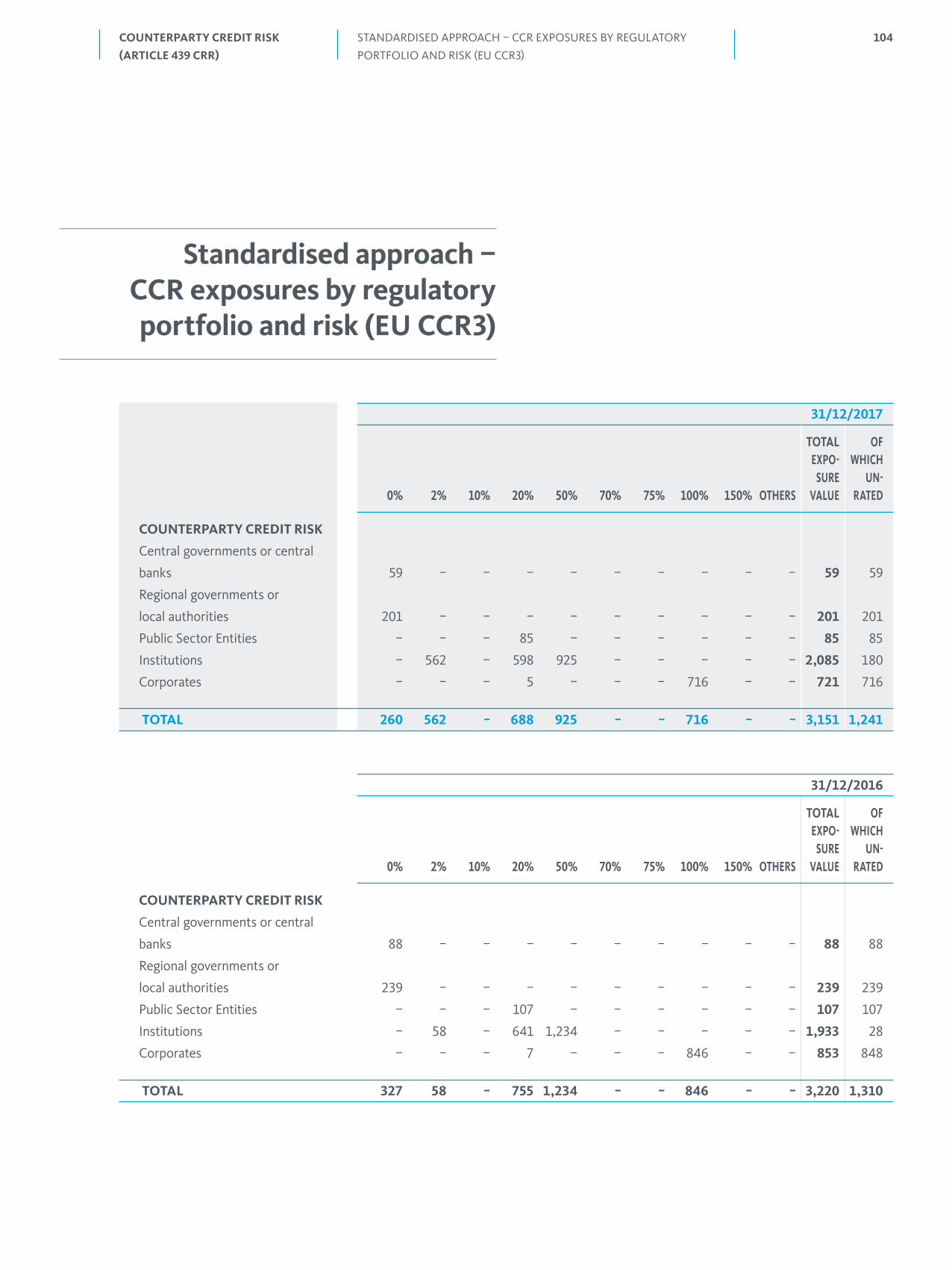

Standardised approach – CCR exposures by regulatory portfolio and risk (EU CCR3) 104

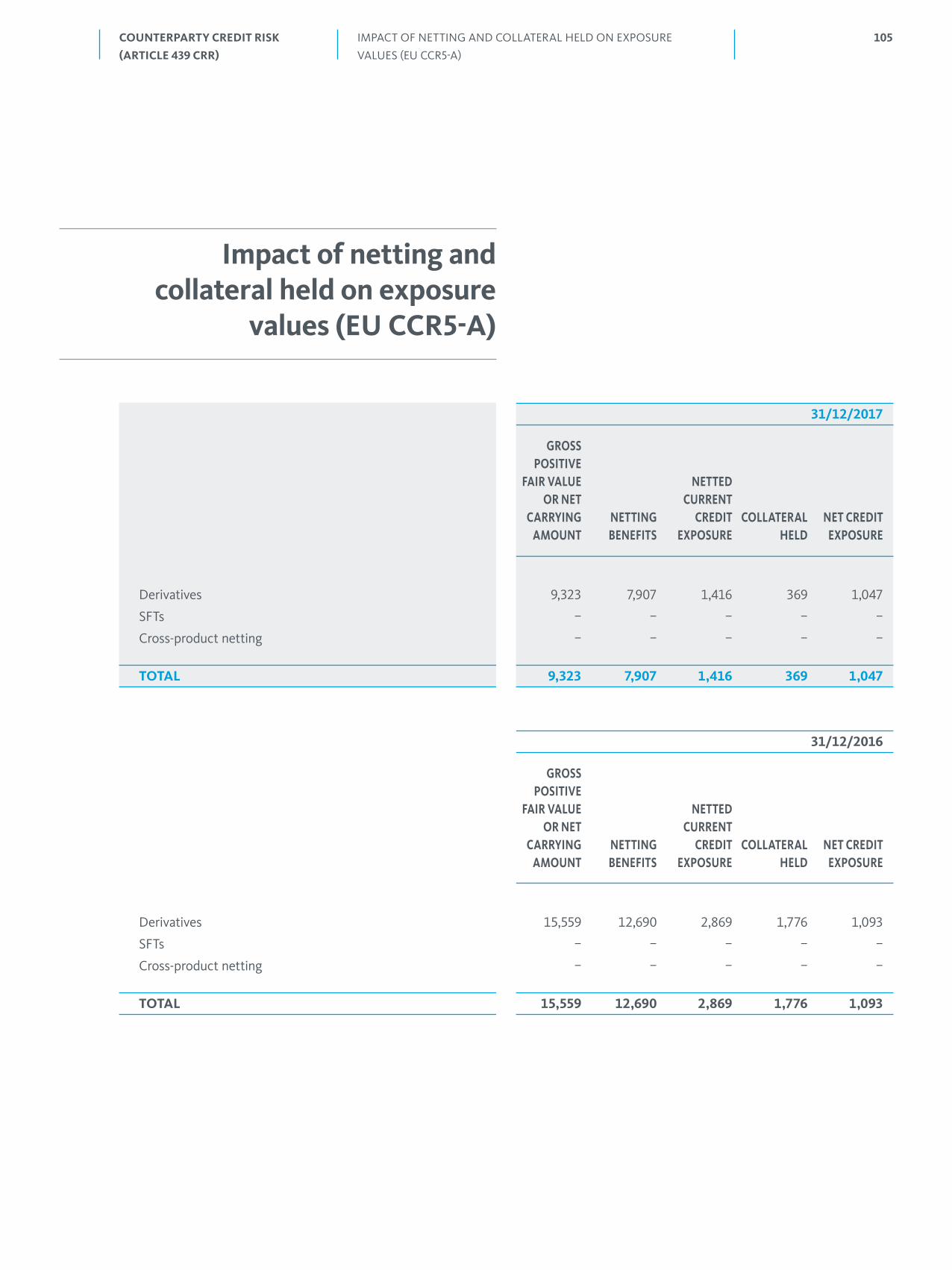

Impact of netting and collateral held on exposure values (EU CCR5-A) 105

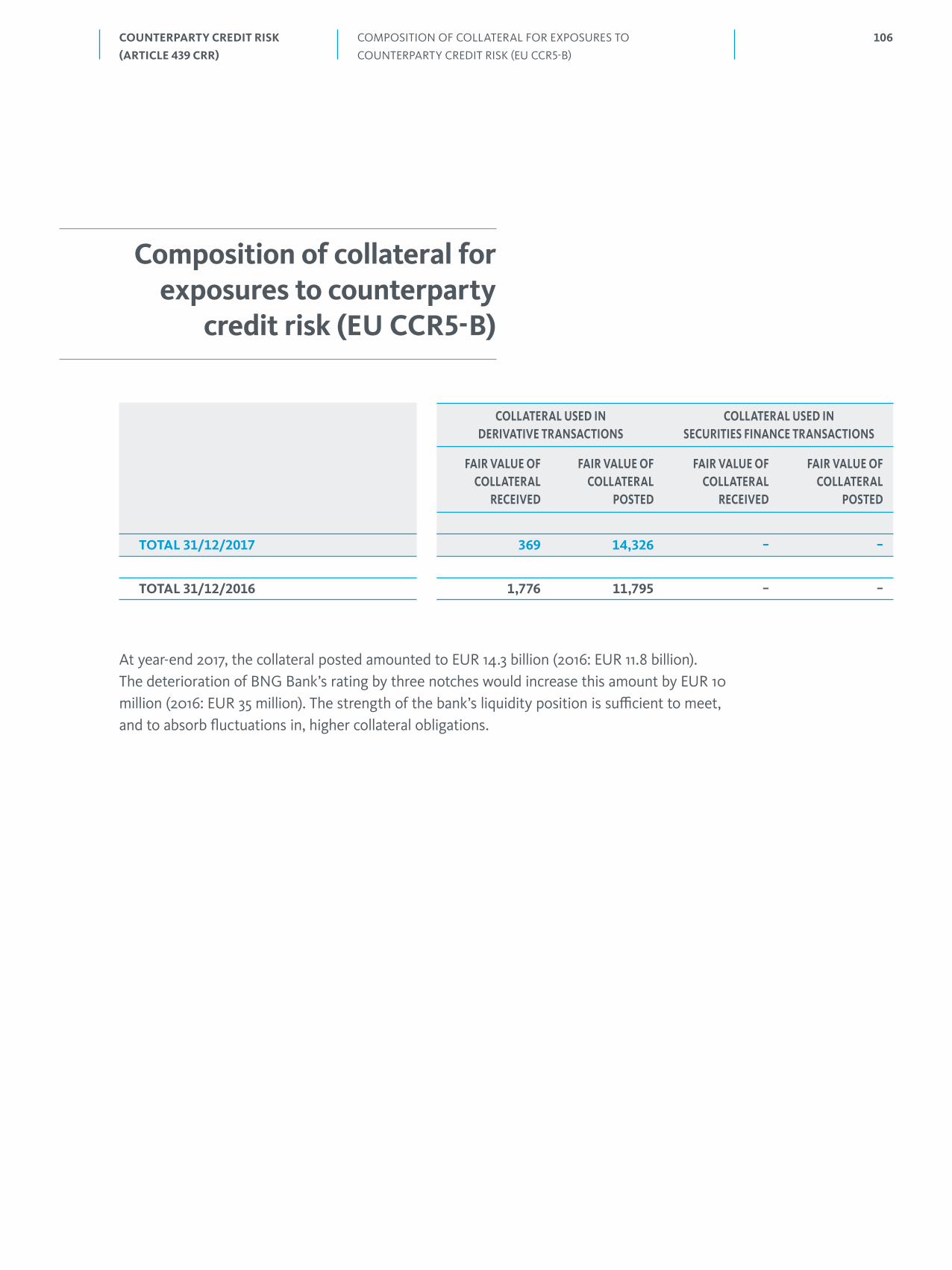

Composition of collateral for exposures to counterparty credit risk (EU CCR5-B) 106

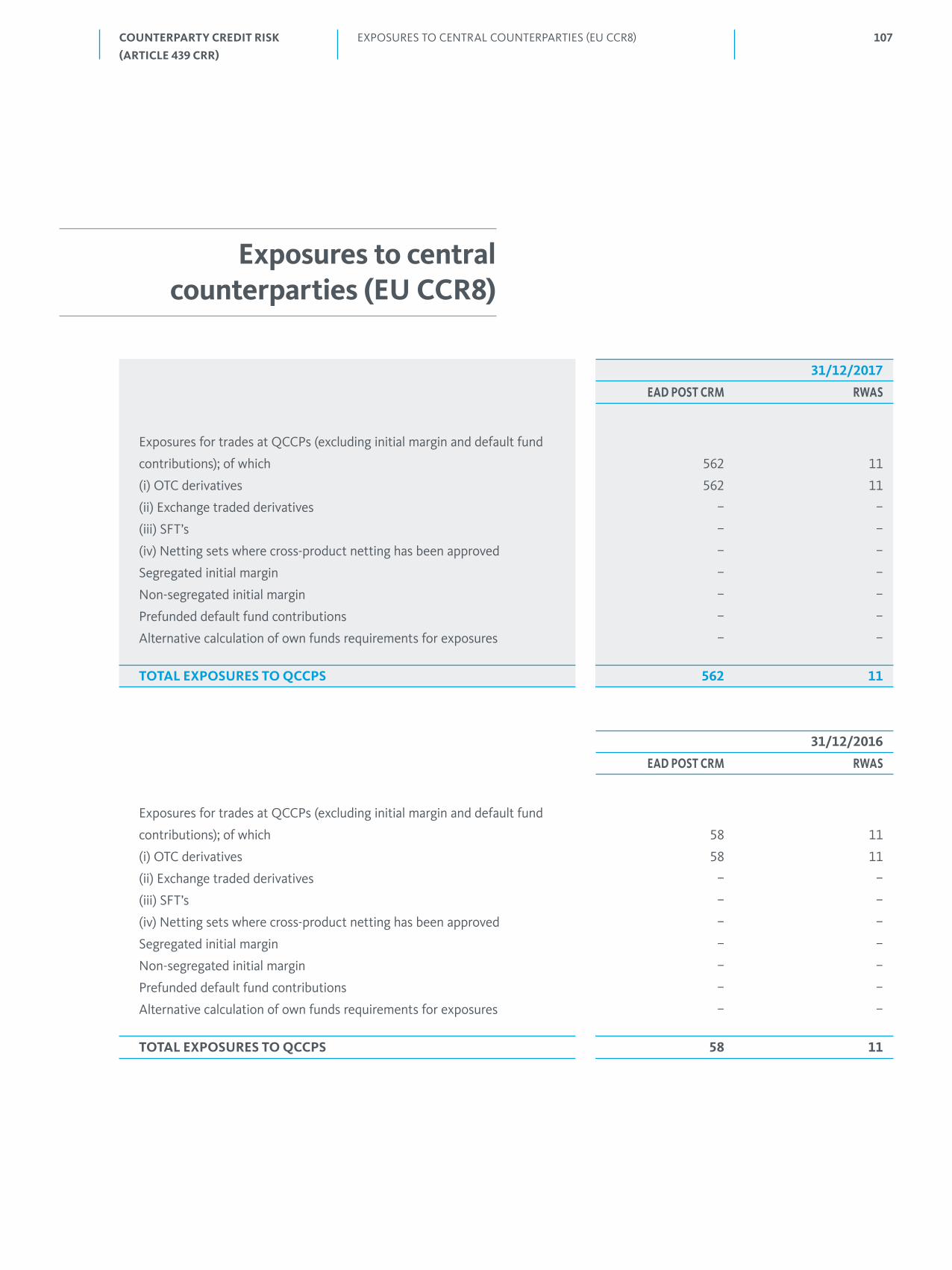

Exposures to central counterparties (EU CCR8) 107

CONTENTS

4

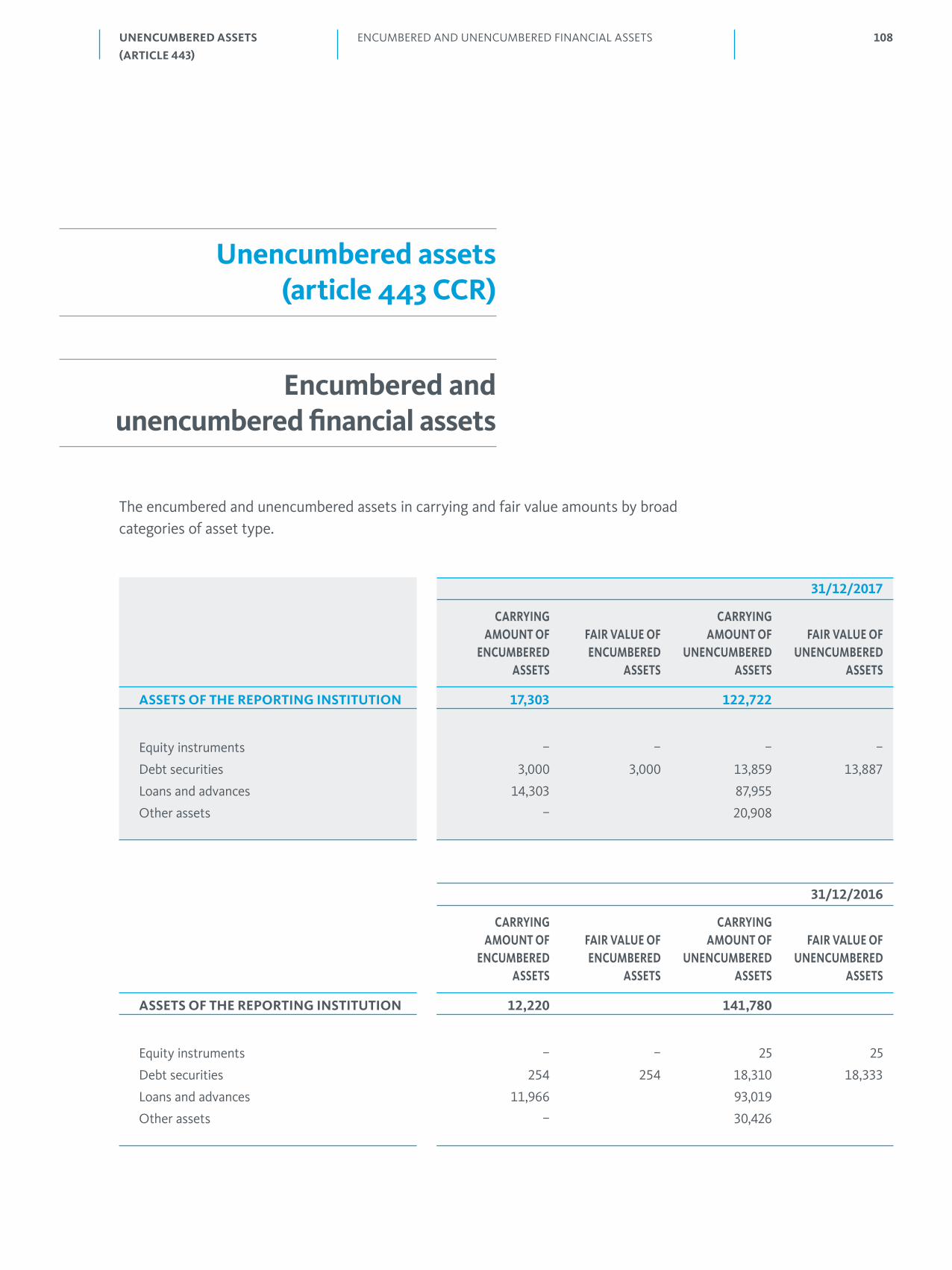

Unencumbered assets (article 443 CRR) 108

Encumbered and unencumbered financial assets 108

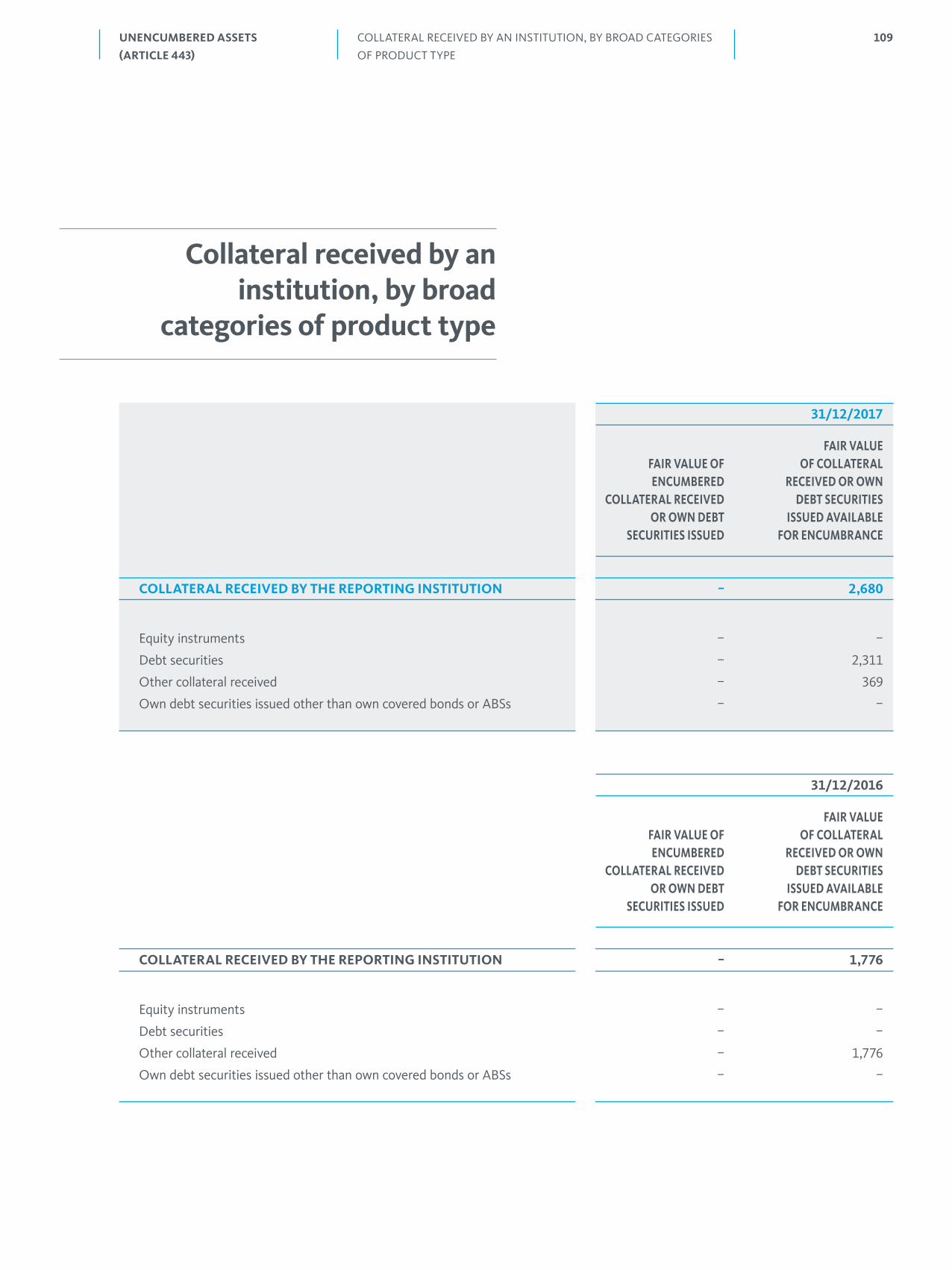

Collateral received by an institution, by broad categories of product type 109

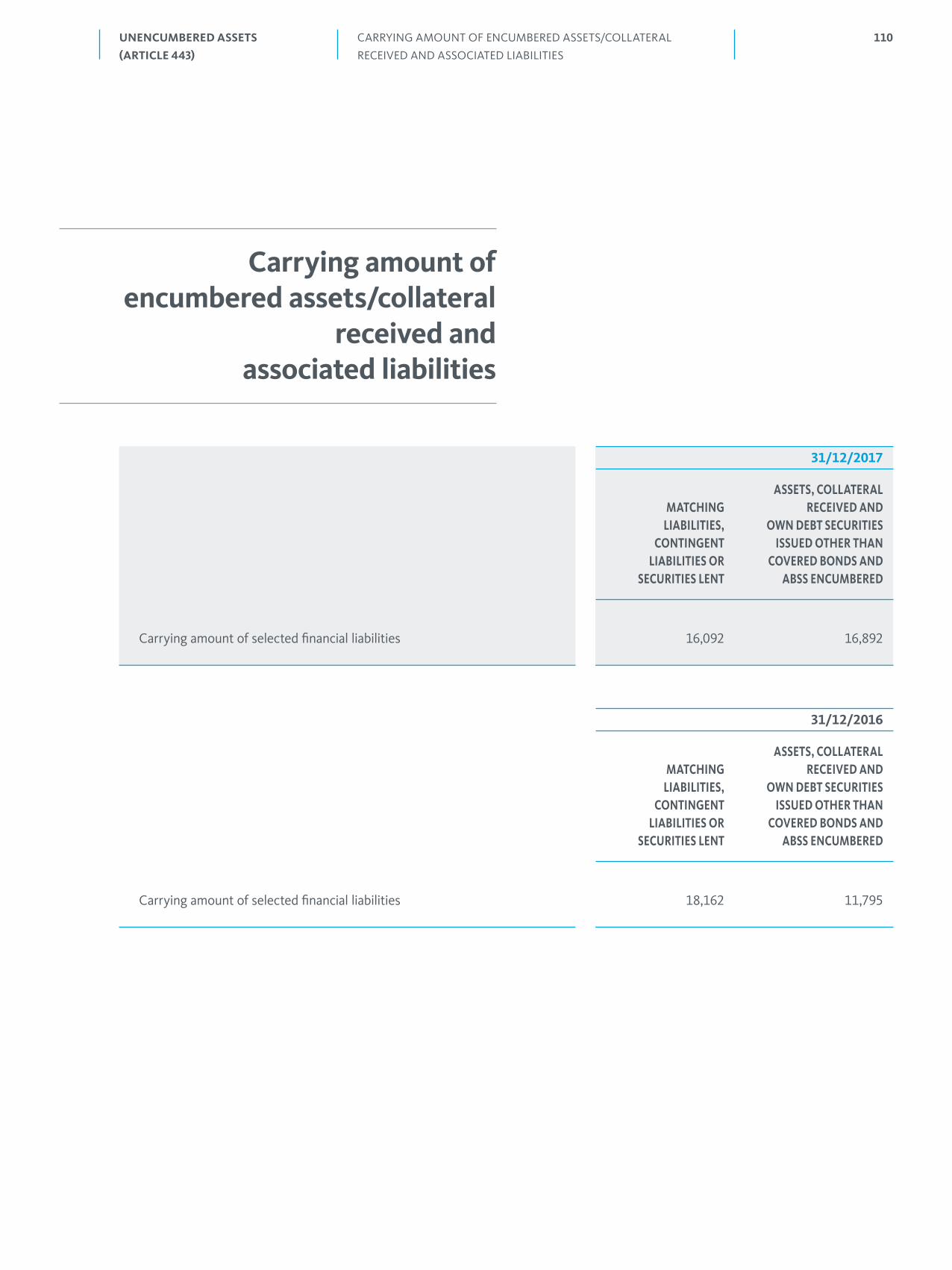

Carrying amount of encumbered assets/collateral received and associated liabilities 110

Narrative information on the importance of asset encumbrance for an institution 111

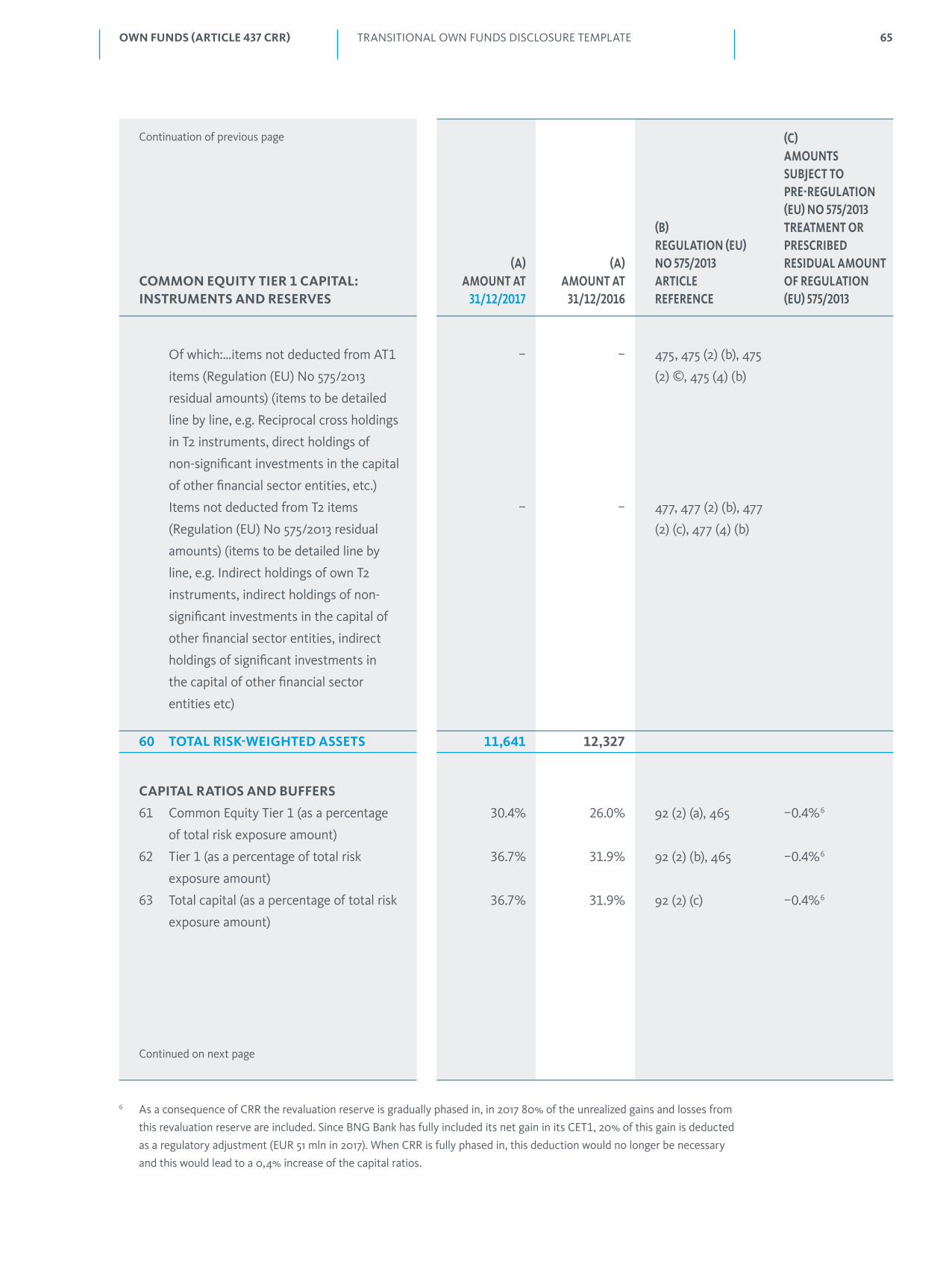

Market risk (article 445 CRR) 112

Market risk under the standardised approach (EU MR1) 112

Remuneration (article 450 CRR) 113

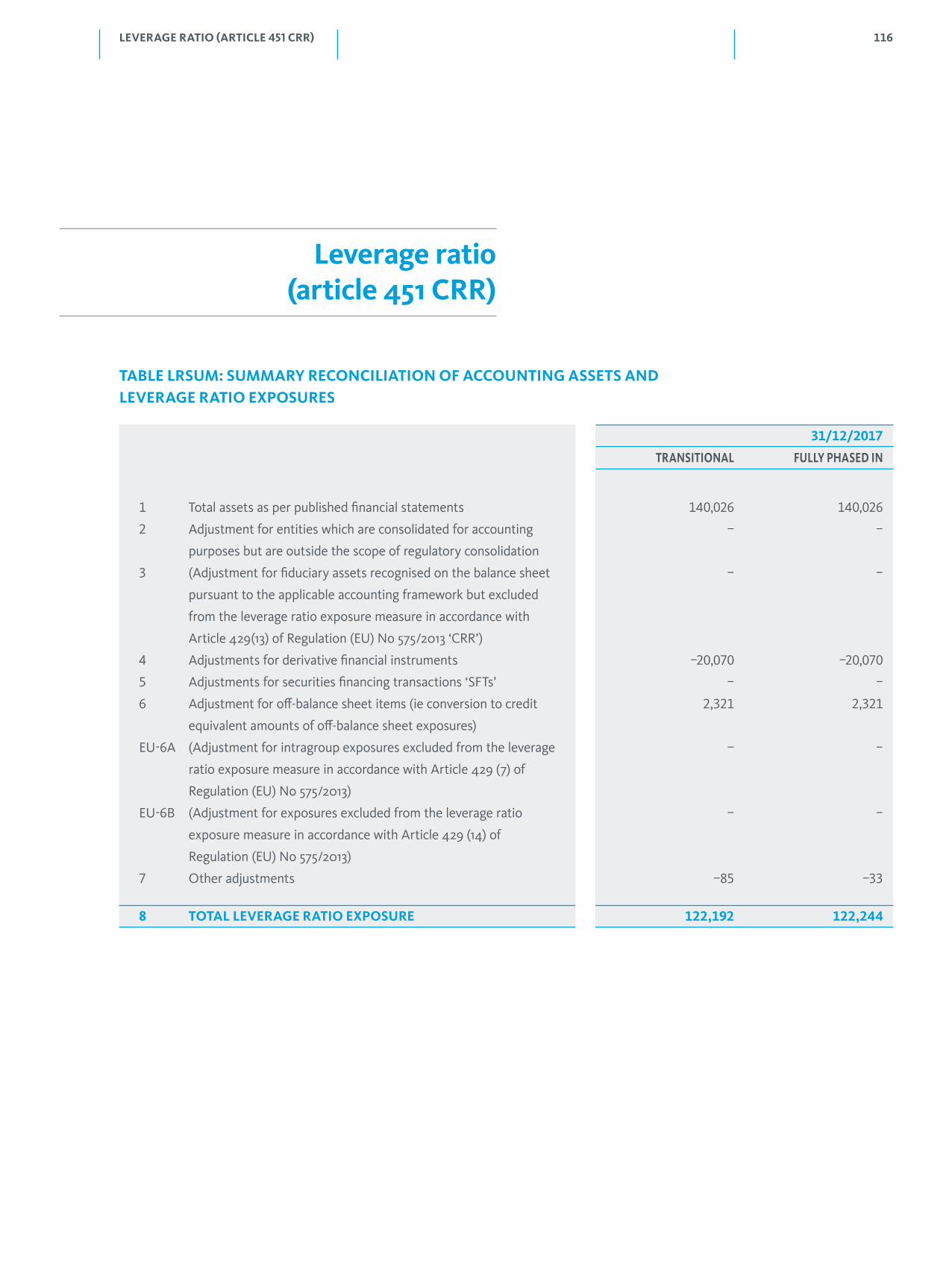

Leverage ratio (article 451 CRR) 116

Exposures in equities not included in the trading book (article 447 CRR) 120

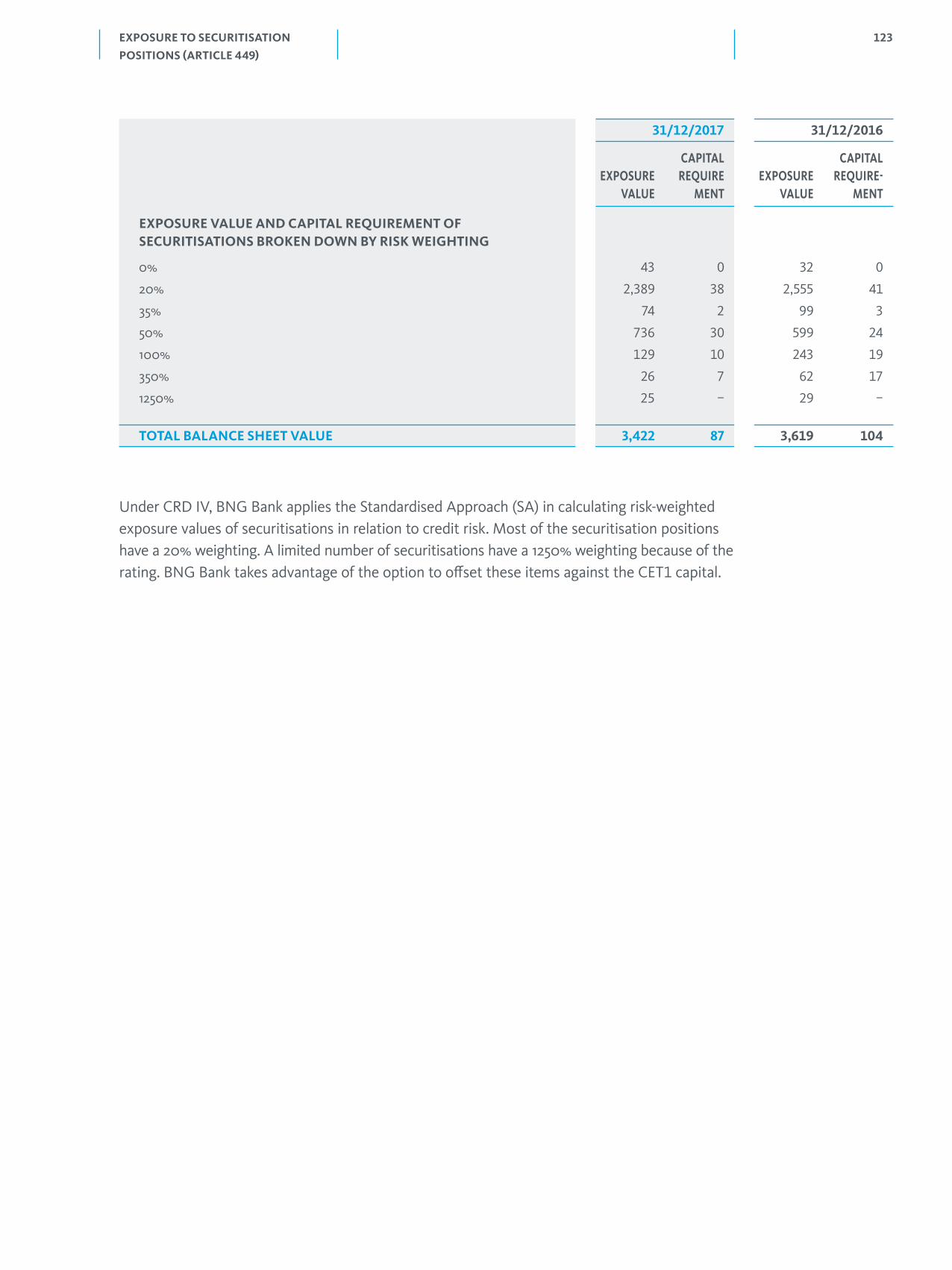

Exposure to securitisation positions (article 449 CRR) 122

Mapping of regulatory requirements 124

CONTENTS

5

Preliminary remarks

The current international regulatory framework for banks consists of a comprehensive set of measures developed by the Basel Committee on Banking Supervision (known as Basel III). Basel III has been implemented in the European Union through the Capital Requirements Directive IV (CRD IV) and is applicable as of January 1st 2014. CRD IV is formed by two legal acts (a Directive and a Regulation) and includes various transitional provisions which allow for a gradual phasing in of the new requirements.

The Basel framework (and thus CRD IV) is based upon three pillars:– The first pillar consists of minimum capital requirements for three main categories of risk:

credit risk, market risk and operational risk.– The second pillar provides a framework for banks to review their capital (and liquidity)

adequacy for both the risks identified in Pillar 1 as well as all other risks (e.g. concentration risk, strategic risk, etc.). This internal review by banks is known as the Internal Capital/Liquidity Adequacy Assessment Process (ICAAP/ILAAP). Supervisors independently assess these processes in their Supervisory Review and Evaluation Process (SREP).

– Finally the third pillar aims to introduce market discipline to complement the capital and liquidity requirements from the first and second pillar. Therefore Basel III (and CRD IV) contains a set of disclosure requirements which will allow market participants to have a sufficient understanding of a bank’s activities, the risks that are involved and the controls that are implemented to manage these risks.

This report is drafted in response to the last pillar. The Pillar 3 disclosure provides a comprehensive overview of the risk profile of BNG Bank. Central to the Pillar 3 disclosure requirements is to promote the transparency of financial institutions and provide market participants with an adequate and comparable picture of the risks of a financial institution. This contributes to a proper functioning of financial markets, improves efficiency of market discipline and helps in building trust between market participants.

PRELIMINARY REMARKS

6

Frequency and means of disclosure (articles 433 CRR

and 434 CRR)

The Pillar 3 disclosure of BNG Bank is published annually. This Pillar 3 Report is published on the website of BNG Bank shortly after the publication of the Annual Report.

In previous years the Pillar 3 Disclosure report mainly served as a reference guide to clearly indicate where relevant information could be found in the financial statements. However, as of 31 December 2017 the EBA guidelines on diclosure requirements1 are applicable to the disclosure of financial insitutions (as defined in Artilcle 4(1) of Regulation (EU) No 1093/2010). These guidelines prescribe in detail the tables and templates through which the Pillar 3 information needs to be disclosed.

These tables and templates do not fully align with the information that is disclosed in the financial statements of BNG Bank as these statements are based on IFRS accounting principles. Therefore, this year a Pillar 3 Disclosure report has been drafted that contains the required Pillar 3 information separately and can be read on its own. On the other hand, a part of the information is already included in the financial statements. This is especially true for the qualitative information in the risk section of the financial statements. This information is reproduced in this report.

In this respect the report can be divided in two parts. The first section provides a comprehensive qualitative overview on the management of risks by BNG Bank and is derived mostly from the risk section of the financial statements. Where possible quantitative information from this risk section is, however, omitted as the second part of this report contains all templates for disclosing the relevant quantitative information as provided for by the European Banking Authority (EBA)2. The order of these different sections has been aligned with those EBA guidelines and standards. For the sake of completeness, the last section includes a overview of the regulatory requirements regarding Pillar 3 disclosure and the location where the information can be found.

FREQUENCY AND MEANS OF

DISCLOSURE (ARTICLES 433 AND

434 CRR)

1 EBA/GL/2016/11, Guidelines on disclosure requirements under Part Eight of Regulation (EU) No 575/20132 Templates and tables are described in detail in EBA/GL/2016/11, Guidelines on disclosure requirements under Part Eight of

Regulation (EU) No 575/2013

7

Following relevant EBA guidelines on the frequency of disclosure3 BNG Bank has assessed the need to publish information more frequently than annually. An annual publication of a comprehensive Pillar 3 disclosure report is deemed sufficient despite the designation of BNG Bank as an other systemically important institution (O-SII). BNG Bank is characterized by a stable business model with a limited range of activities and exposures. The resulting risk profile of BNG Bank is not prone to any rapid changes. And in general, the information, that would qualify for more frequent disclosure, does normally not exhibit any sudden changes either. An annual disclosure suffices therefore.

In addition, BNG Bank does publish an interim report on its website which is reviewed by an external auditor. Any sudden changes in the financial position or in the markets in which BNG Bank operates will be addressed in this interim report. If these circumstances would lead to material changes in the risk profile of BNG Bank an additional disclosure of some or all of the Pillar 3 requirements will be contemplated.

Finally, it should be noted that information in this report has not been audited. However, the appropriateness of the disclosed information is approved by the Executive Board of BNG Bank. Information that is considered to be proprietary or confidential will not be published, but is disclosed in a more general manner. The Annual Report itself is audited by an external auditor.

3 EBA/GL/2014/14, Guidelines on materiality, proprietary and confidentiality and on disclosure frequency under Articles

432(1), 432(2) and 433 of the CRR

FREQUENCY AND MEANS OF

DISCLOSURE (ARTICLES 433 AND

434 CRR)

8

General information

INSTITUTION RISK MANAGEMENT APPROACH The process of accepting and controlling risks is inherent to the day-to-day operations of any bank. In order to conduct its operations, a bank must accept a certain amount of credit, market, liquidity and operational risk. On top of this, there is strategic risk. BNG Bank only has a banking book and does not have a trading book. BNG Bank’s risk management strategy is aimed at maintaining its safe risk profile, which is expressed in its high external credit ratings. For this reason, BNG Bank employs a strict capitalisation policy.

RISK APPETITE STATEMENTThe bank has prepared a Risk Appetite Statement (RAS) describing its risk appetite, which sets out the types and degree of risk the bank is willing to assume, decided in advance and within its risk capacity, to achieve its strategic objectives and business plan. The risk appetite falls within the risk capacity, which is the maximum risk level that the bank is able to assume given its capital base, risk management and control capabilities as well as its regulatory constraints and at which the bank is still able to meet its obligations towards its clients, investors, shareholders and other stakeholders. The bank has a mission, a strategy and core values, which jointly influence the risk culture. The bank balances the interests of the various stakeholders when fulfilling the mission and executing the strategy. To facilitate this, a stakeholders model is used which is represented in the next figure.

GENERAL INFORMATIONRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

Risk management objectives and policies (article 435 CRR)

9

Formulating a risk appetite also requires definitions of risks to ensure everyone speaks the same language. BNG Bank recognises the financial risks of credit risk, market risk and liquidity risk, as well as the non-financial risks of operational risk and strategic risk in this regard. Finally, several components are defined that form the core of the bank’s operations and constitute the framework within which the risk appetite is formulated. In the case of a bank, the components (1) Profitability, (2) Solvency and (3) Liquidity are most obvious. These are widely used concepts for assessing the security and hence the risk profile of a bank. Besides those components, BNG Bank has also opted for (4) Reputation and Brand as BNG Bank has always placed great value on an impeccable reputation. The risk appetite is evaluated annually and adjusted where necessary in order to ensure that it remains in line with BNG Bank’s strategic objectives:– substantial market shares in the Dutch public sector and semi-public domain;– generate a reasonable return for its shareholders.

And satisfies the conditions identified in this context:– an excellent credit rating and adequate risk management;– an excellent funding position;– effective and efficient operations.

In translating these strategic objectives and conditions into the risk appetite, the bank identifies the interests and expectations of all its stakeholders. This subsequently results in the formulation of objectives with regard to profitability, solvency, liquidity and reputation & brand in the form of the RAS. The RAS is laid down by both the Executive Board and the Supervisory Board. Once the risk appetite has been established, it is translated to the different risks, namely the financial risks of credit risk, market risk and liquidity risk, and the non-financial risks of operational risk and strategic risk.

PROFITABILITY SOLVENCY LIQUIDITY

COMPONENTS

REPUTATION & BRAND

MISSION, STRATEGY, RISK CULTURE

RISK APPETITEFRAMEWORK

EXPECTATIONS & INTERESTS

STAKEHOLDERS

SHAREHOLDERS

INVESTORS

CLIENTS

FINANCIAL COUNTERPARTIES

GOVERNMENT

EMPLOYEES

SUPERVISORY AUTHORITIES

RATING AGENCIES

RISKS

CREDIT RISK

MARKET RISK

LIQUIDITY RISK

OPERATIONAL RISK

STRATEGIC RISK

GENERAL INFORMATIONRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

10

PROFITABILITY

BNG Bank aims to minimise charges for the public sector, and hence does not seek to maximise profits. For its shareholders the

bank’s objective is to achieve a reasonable return. Relative stability of the annual results is also important to different stakeholders,

including regulatory authorities and rating agencies. ‘Relative’ in this context refers to a maximum percentage of deviation relative

to the previous annual result.

SOLVENCY

BNG Bank aims expressly to stand out in the financial markets in terms of the size and quality of its capital. This is expressed in the

desired rating profile: a rating at the same level as that of the Dutch State. To realise this, BNG Bank’s capital must be significantly

greater than the criteria applied by the regulatory authorities and significantly greater than (the majority of) other banks to ensure

favourable funding rates. This relates to domestic Dutch banks as well as foreign banks.

LIQUIDITY

BNG Bank intends to use its position to maintain a lasting and stable presence in the market for the public sector and continue to

meet the demand for lending even in difficult times. It also aims for a prudent liquidity position, with due regard for the principles

that it is always able to meet its short-term obligations and also adequately mitigates its refinancing risk. In this context, continuous

access to funding is crucial and hence continuous maintenance of an attractive, varied issuance programme of sufficient volume for

investors. In addition, it is important to have sufficient collateral lodged with the ECB to ensure short-term funding can be raised

with the ECB in times of need.

REPUTATION & BRAND

BNG Bank aims to retain the perception its stakeholders have of it as a quasi-public sector body, with excellent creditworthiness

and a fine reputation and integrity profile. The bank wants to retain the status of promotional bank. The nature and size of financial

losses should be aligned with the perception of its stakeholders and not include any unexpected elements. The bank is not willing

to assume any risks for which it may reasonably be presumed that the risk can harm its integrity and/or reputation. BNG Bank

aims to exercise due care in the provision of services and to observe a duty of care towards its clients, and endeavours to provide

tailored products and services at competitive rates.

The risk appetite for the four components is reflected in the following objectives:

RISKS ACCEPTED BY BNG BANKIn order to achieve its goals, the bank has identified the types of risks it is prepared to accept as a consequence of its strategy and business operations. Three important principles in this respect are: – BNG Bank aims to provide the best possible services to its stakeholders, now and in the future.

The return required by its principal shareholder takes account of the bank’s risk profile. This means that the required return should not result in the bank taking such considerable risk as to jeopardise its ratings and funding position, as a consequence of which it would no longer be able to fulfil its mission in the long term. Subject to certain conditions, the bank seeks a higher return than this external return requirement.

– In addition to a reasonable return for shareholders, low prices are the major focus. BNG Bank is willing to assume the necessary risks, in a controlled manner, that go hand in hand with lending to clients. The bank is furthermore willing to assume certain additional risks for activities that support lending to clients. Achieving an additional return (based on considerations of risk and return) makes lower prices for clients possible now and in the

GENERAL INFORMATIONRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

11

future. Again, this may not be at the expense of the external ratings and excellent funding position, since that would jeopardise the bank’s mission.

– In the public sector there is a distinction between lending not subject to solvency requirements (zero risk weighted) and lending that is subject to solvency requirements (non zero risk weighted), whether this is caused by guarantees or otherwise. The largest share of the bank’s lending (loans and advances) is not subject to solvency requirements. In order to facilitate this lending at the lowest possible rates, it is essential that the bank retains its competitive funding position. This in turn is dependent on the high ratings, forcing the bank to impose restrictions on lending subject to solvency requirements, in view of the related credit risks.

As a result of the foregoing, the bank is prepared to accept the following risks.

CREDIT RISK– Counterparty risk associated with lending subject to solvency requirements to clients.

Certain non solvency free parties belong to the public sector and hence are covered by the bank’s mission. Additionally, the return on lending subject to solvency requirements can support the competitive rates charged for lending not subject to solvency requirements.

– Risks in terms of financial counterparties associated with activities that support lending (including the hedging of market risks through derivatives).

– Concentration risk in relation to the Dutch public sector is inherent to the business model. A sizeable part of the associated exposure relates to public sector real estate. For the most part, this risk is mitigated by the guarantee funds in the Social Housing sector and Healthcare sector, resulting ultimately in a risk exposure to the Dutch State.

– Investments that support lending to clients.

MARKET RISK– BNG Bank hedges the interest rate risks arising from lending (loans and advances) and

borrowing. However, the bank is willing to assume a certain degree of interest rate risk. On the one hand, a certain maturity mismatch, related to the bank’s capital base, is a common source of income for banks (longer lending term than borrowing term). Additionally, BNG Bank strives to achieve additional return with an active interest rate position policy. With regard to (tenor) basis risk the bank assumes a limited position arising from regular funding and lending.

– It is the banks policy to hedge any option positions, unless they support the active interest rate position policy.

It should be noted that BNG Bank is not willing to assume any exposures to foreign exchange risk. Foreign exchange risks are therefore hedged, including FX basis risk. Furthermore, BNG Bank has no trading book and, consequently, does not assume any market risk in connection with trading portfolios.

LIQUIDITY RISK– As BNG Bank wishes to meet its payment obligations at all times, short-term liquidity risks

are only assumed if they are matched by sufficient capital buffers capable of meeting these short-term obligations.

– The public sector consists largely of institutions with a long-term investment horizon. This means that assets frequently have long maturities that can run into decades. As BNG Bank is unable to raise funding for these maturities, a funding mismatch is assumed, provided there are sufficient buffers to be able to refinance at acceptable cost with a high degree of

GENERAL INFORMATIONRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

12

probability also in times of stress. The Bank is also willing to assume the refinancing risk arising from the liquidity requirement related to activities other than lending to its clients, as is the case with investments. The ensuing additional liquidity requirement may not jeopardize the bank’s mission.

OPERATIONAL RISK– Operational risk is inherent in operating a business. BNG Bank accepts that providing tailored

services entails additional inherent operational risks with regard to standard products.– Operational risks are mitigated by weighing the costs against the economic benefits, except

in case of compliance with legal and regulatory requirements and duty of care and proper conduct issues, where the risks should be minimised.

– In addition to lending, BNG Bank also provides its clients with other products, such as current account and payment transaction services. Clients benefit considerably from this broader range of services, and this also promotes client loyalty to the bank even if it can be argued that payment transaction services do not significantly contribute to minimising public sector financing costs. The bank is willing to assume operational risks also for these additional products, provided they do not jeopardize its mission.

STRATEGIC RISKIn the case of strategic risk it is more difficult to determine the extent to which risks are assumed, since they are driven by external factors in particular and hence are less easily influenced. However, BNG Bank needs to address the risks that emerge from changes in its environment. It is essential that the bank remains relevant for its clients and is therefore responsive to political and social developments. Sustainability e.g. is a major issue for the bank’s clients. A failure to satisfy clients’ expectations can adversely affect the bank’s market position. BNG Bank actively advances the message that it wishes to partner with clients in relation to sustainability. This carries the reputational risk that it will be unable to adequately fulfil this publicly issued commitment.

In a yearly cycle the RAS is updated based on external as well as internal developments. It is subsequently cascaded into these limits, targets and information figures. These are subject to a monitoring program that is conducted each quarter to determine whether the bank is still within the limits of its risk appetite. The outcomes are reported to the Management Board and Supervisory Board as part of the quarterly Risk Report. Examples of further tools to monitor compliance to the risk of the bank are the yearly In Control Statements by senior management and reports by internal and external auditors. In 2017, the bank operated comfortably within its own risk appetite for market risk, credit risk and liquidity risk. With regard to capital, in 2017, the bank achieved the expected legal requirement including an internally desired buffer. With regard to operational risk, the bank remained well within the internal norms for operational incidents. The tools available for monitoring operational risk have been improved and development will continue in 2018. In monitoring its strategic risk the bank decided to follow an approach aimed at systematically examining the most important strategic risks in a qualitative way.

GENERAL INFORMATIONRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

13

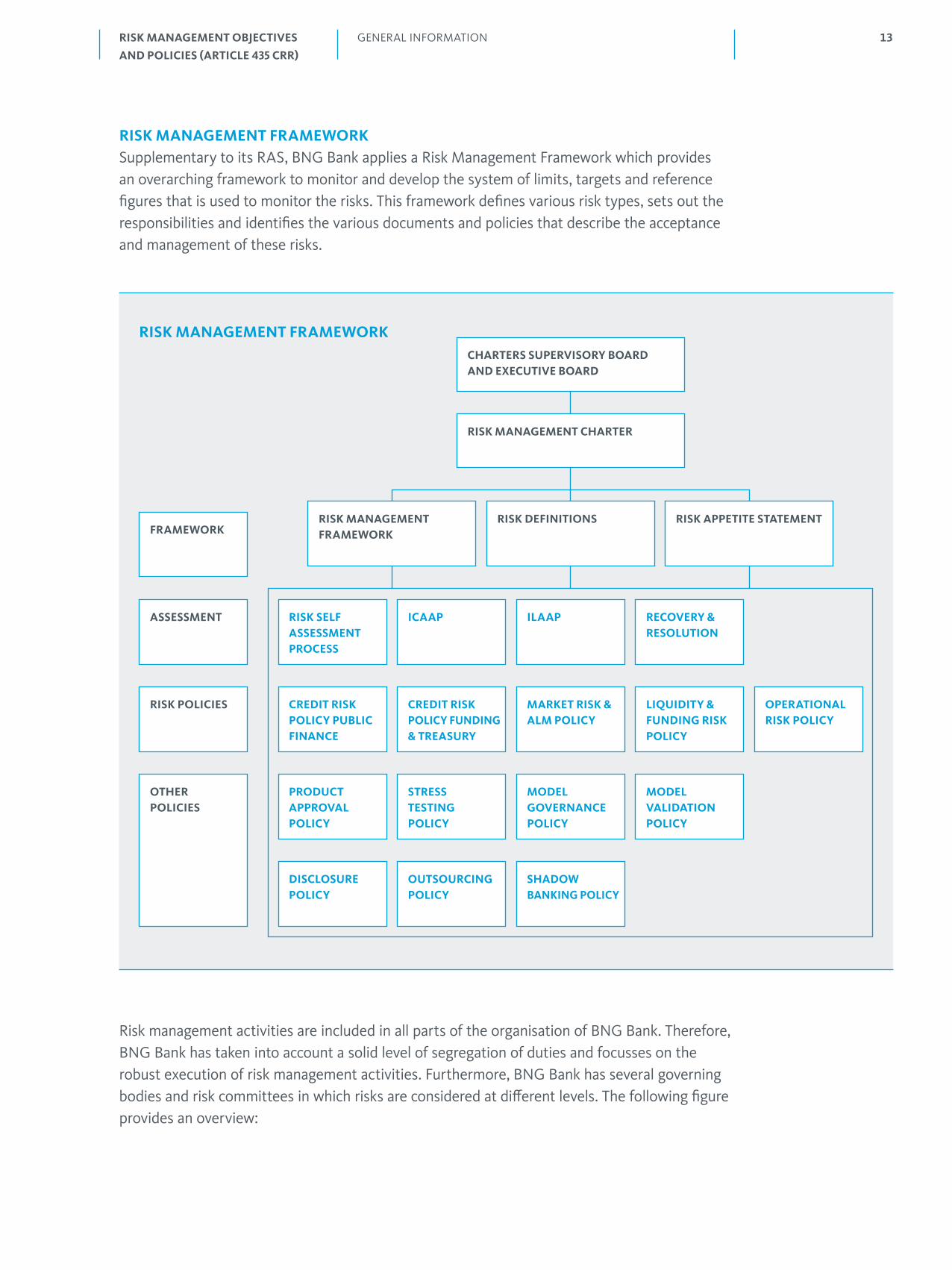

RISK MANAGEMENT FRAMEWORKSupplementary to its RAS, BNG Bank applies a Risk Management Framework which provides an overarching framework to monitor and develop the system of limits, targets and reference figures that is used to monitor the risks. This framework defines various risk types, sets out the responsibilities and identifies the various documents and policies that describe the acceptance and management of these risks.

GENERAL INFORMATIONRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

CHARTERS SUPERVISORY BOARDAND EXECUTIVE BOARD

FRAMEWORK

ASSESSMENT

RISK POLICIES

OTHER POLICIES

RISK SELF ASSESSMENT PROCESS

CREDIT RISK POLICY PUBLIC FINANCE

PRODUCT APPROVAL POLICY

DISCLOSURE POLICY

ICAAP

CREDIT RISK POLICY FUNDING & TREASURY

STRESS TESTING POLICY

OUTSOURCING POLICY

ILAAP

MARKET RISK & ALM POLICY

MODEL GOVERNANCE POLICY

SHADOW BANKING POLICY

RECOVERY & RESOLUTION

LIQUIDITY & FUNDING RISK POLICY

MODEL VALIDATION POLICY

OPERATIONAL RISK POLICY

RISK MANAGEMENT FRAMEWORK

RISK MANAGEMENT CHARTER

RISK MANAGEMENT FRAMEWORK

RISK DEFINITIONS RISK APPETITE STATEMENT

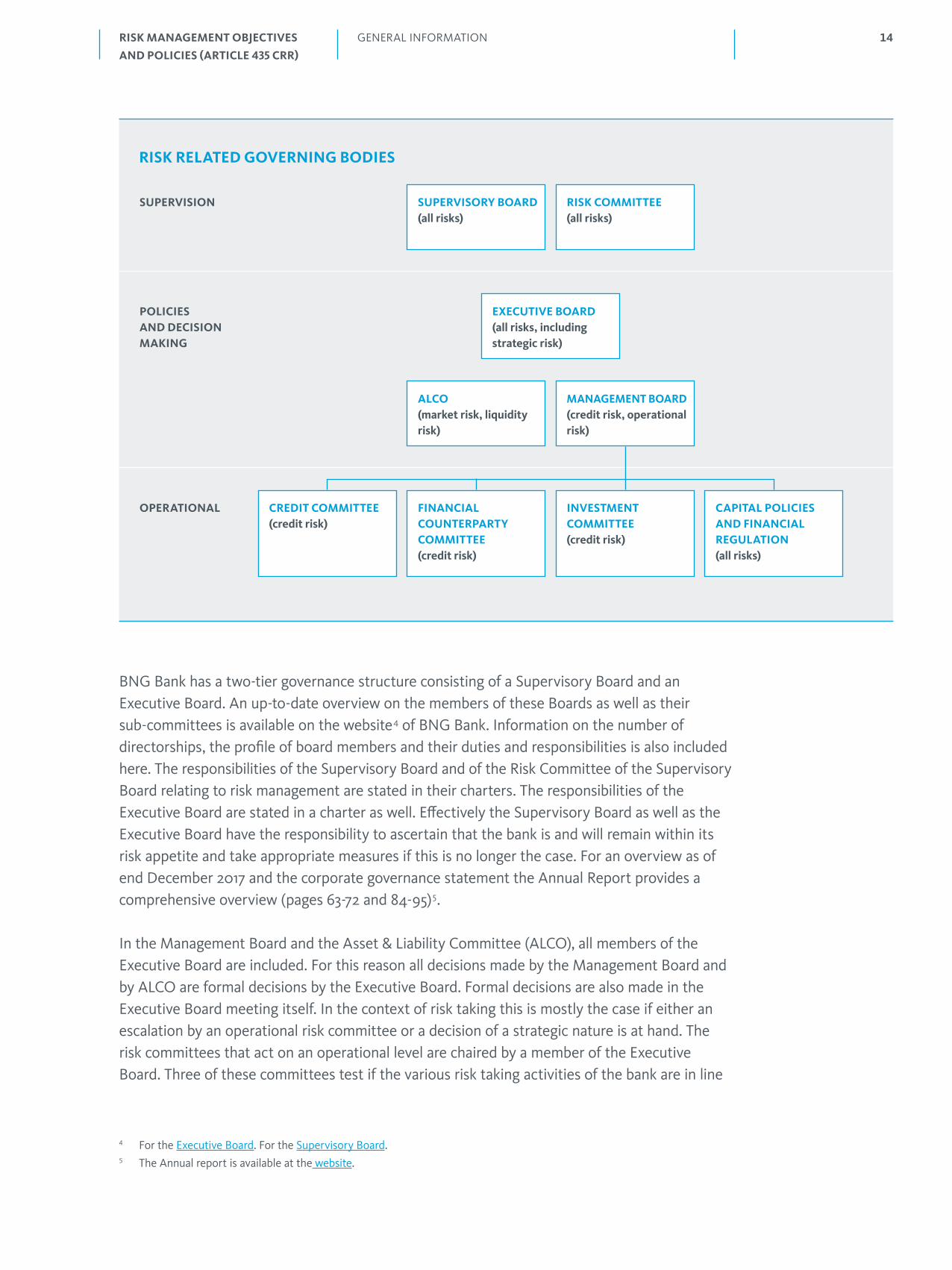

Risk management activities are included in all parts of the organisation of BNG Bank. Therefore, BNG Bank has taken into account a solid level of segregation of duties and focusses on the robust execution of risk management activities. Furthermore, BNG Bank has several governing bodies and risk committees in which risks are considered at different levels. The following figure provides an overview:

14

SUPERVISION

POLICIES AND DECISION MAKING

OPERATIONAL

EXECUTIVE BOARD (all risks, including strategic risk)

ALCO(market risk, liquidity risk)

CREDIT COMMITTEE(credit risk)

MANAGEMENT BOARD(credit risk, operational risk)

FINANCIAL COUNTERPARTY COMMITTEE(credit risk)

INVESTMENT COMMITTEE(credit risk)

CAPITAL POLICIES AND FINANCIAL REGULATION(all risks)

RISK RELATED GOVERNING BODIES

SUPERVISORY BOARD (all risks)

RISK COMMITTEE(all risks)

BNG Bank has a two-tier governance structure consisting of a Supervisory Board and an Executive Board. An up-to-date overview on the members of these Boards as well as their sub-committees is available on the website4 of BNG Bank. Information on the number of directorships, the profile of board members and their duties and responsibilities is also included here. The responsibilities of the Supervisory Board and of the Risk Committee of the Supervisory Board relating to risk management are stated in their charters. The responsibilities of the Executive Board are stated in a charter as well. Effectively the Supervisory Board as well as the Executive Board have the responsibility to ascertain that the bank is and will remain within its risk appetite and take appropriate measures if this is no longer the case. For an overview as of end December 2017 and the corporate governance statement the Annual Report provides a comprehensive overview (pages 63-72 and 84-95)5.

In the Management Board and the Asset & Liability Committee (ALCO), all members of the Executive Board are included. For this reason all decisions made by the Management Board and by ALCO are formal decisions by the Executive Board. Formal decisions are also made in the Executive Board meeting itself. In the context of risk taking this is mostly the case if either an escalation by an operational risk committee or a decision of a strategic nature is at hand. The risk committees that act on an operational level are chaired by a member of the Executive Board. Three of these committees test if the various risk taking activities of the bank are in line

4 For the Executive Board. For the Supervisory Board.5 The Annual report is available at the website.

GENERAL INFORMATIONRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

15

with the policies. The fourth committee, Capital Policy and Financial Regulations Committee, advises the Management Board on the capital policy and the allocation of capital to the bank’s various business units. In addition, the committee advices on the introduction of new regulations concerning solvency and liquidity as well as on technical financial issues. The committees also advise the Management Board and the ALCO on changes in policies. The operational committees have no mandate to approve policy changes themselves.

The following departments support the Executive Board and the committees in implementing risk policy:– The Risk Management department qualifies, quantifies and monitors risks, and reports to the

responsible committees. These risks consist of credit risk, market risk, liquidity risk, operational risk and other risks. The department has a supporting role as regards strategic risk. The department manages the risk policy documents and the Risk Management Framework. The Risk Management Department participates in the internal risk committees as well as in the Risk Committee of the Supervisory Board.

– The Credit Risk Assessment department provides independent assessments and advice on risks relating to credit and review proposals for clients and financial counterparties. It also formulates policies with respect to credit risk. As part of the operational lending process it is represented in the bank’s Credit Committee, the Financial Counterparties Committee and the Investment Committee. This department is also responsible for the bank’s Special Management activities – being the supervision, management and processing of distressed credits.

– The Internal Audit Department (IAD) periodically conducts operational audits in order to evaluate the structure and performance of the bank’s risk management systems and assess compliance with the applicable legislation. The IAD functions as an independent entity within the bank and reports to the Executive Board. The IAD also has a reporting line to the Supervisory Board.

– Where necessary, the Compliance & Integrity department is engaged in connection with conduct-related issues. This department monitors compliance with all relevant laws and regulations. The duties, position and authorities of this compliance function are laid down in the BNG Bank Compliance Charter. The Compliane officer reports to the Executive Board and has a reporting line to the Supervisory Board.

The Capital Management department also reports directly to the Executive Board. Apart from managing capital policy and allocation the department also actively monitors and analyses upcoming legislative changes.

GENERAL INFORMATIONRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

16

Credit risk

DEFINITIONS Credit risk is defined as the chance of losses if and when a counterparty is unable to meet its financial and/or other obligations and includes settlement risk, counterparty risk and concentration risk.– Counterparty risk: The risk of losses if a party fails to make payments that result from a

financial transaction, at the moment those payments are due.– Concentration risk: The overall spread of a bank’s exposures over the number or variety of

debtors to whom the bank has lent money.– Settlement risk: The risk that one party will fail to deliver the terms of a contract (or a group

of contracts) with another party at the time of settlement.

GOVERNANCEBNG Bank has an internal risk management organisation that serves to control its credit risks. This organisation is in line with the diversity and complexity of the bank’s lending activities and is structured as follows:– The Executive Board determines the relevant lending parameters and policies, facilitated

by the Management Board.– The Credit Committee decides on loans and advances subject to solvency requirements.

In some cases, this authority is delegated.– The Financial Counterparties Committee decides on limits for transactions with financial

institutions.– The Investment Committee decides on proposals for investment in interest-bearing securities.– The Client Acceptance Committee assesses whether potential clients are suitable under the

bank’s Articles of Association, whether they fit in the bank’s commercial policy and whether they constitute an integrity risk.

The Credit Risk Assessment department and the Risk Management department (at portfolio level) are responsible for assessing, quantifying and reporting the credit risk. In the organisation, these departments operate independently from the Public Finance and Treasury directorates, which are responsible for contracts that include credit risk. The Risk Management department is internally responsible for all Credit Risk policies.

DEVELOPMENTSBecause of IFRS 9, financial institutions needed to develop an impairment model in order to recognize credit losses before an actual credit event occurs. The impairment model is based on a three-stage process which is intended to reflect deterioration in credit risk. BNG Bank assumes that the credit risk on a financial asset has not increased significantly since initial recognition if

CREDIT RISKRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

17

the asset is determined to have low credit risk at the reporting date. In that case, the bank measures impairment under 12-month expected credit losses (ECL). Otherwise, the ECL of an asset is either determined on a 12-month or lifetime basis depending on whether a significant increase in credit risk occurred. On top of the existing internal Probability of Default (PD) models, BNG Bank developed an overlay model that calculates an add-on for the PD’s by using forward looking information (FLI) based on forecasts on macroeconomic variables. By incorporating this add-on, the resulting point-in-time PD has a cyclical component. For its internal capital calculations, BNG Bank assigns a Loss Given Default (LGD) percentage to exposures based on values from the Standardized Approach because statistical data is practically unavailable for its client exposures. Since this is not allowed under IFRS 9, an LGD percentage is calculated based on the very little internal and some available relevant external statistical data. The bank applies a cash flow model to calculate the estimated exposure at each future year-end. BNG Bank employs different techniques and judgements in the staging assessment. The techniques or ‘triggers’ differ in nature, being quantitative, qualitative or a backstop indicator. IFRS 9 will be effective as from 1 January 2018.

In 2017 the lean way of working was introduced in the lending process. This led to several organisational changes like working in teams instead of in separate departments. For these organisational changes, separation of duties was monitored by the IAD. The introduction of lean working did not result in significant changes in formal credit risk policies. Any changes in credit risk policies were facilitated by the Risk Management department and approved by the Executive Board.

COUNTERPARTY RISKThe bank is exposed to counterparty risk in relation to public sector entities (loans and advances), financial counterparties (derivatives) and issuers of interest-bearing securities (IBS) in which the bank has invested. BNG Bank applies the following credit risk mitigation measures:– Because loans subject to solvency requirements are often extended under (partial) guarantees

or suretyships, on balance the loan remains (partly) solvency-free for BNG Bank (see the section on statutory market parties). The guarantees are provided by a central or local authority or by the guarantee funds WSW (Social Housing) and WfZ (Healthcare).

– Other forms of security, such as pledges and mortgages are used to minimise possible losses due to credit risks. The potential risk reducing effect, however, is not used in the calculation of the regulatory capital requirement.

– Bilateral netting and collateral agreements based on a daily collateral exchange with financial counterparties. See also the section ‘Financial counterparties’.

STATUTORY MARKET PARTIESThe bank’s Articles of Association limit lending to parties subject to some form of government involvement. As a result, the credit portfolio is largely comprised of solvency-free loans and advances, provided to or guaranteed by the government. In the case of the guarantee funds WSW and WfZ, the credit risk assessment of guaranteed institutions is carried out expressly by the guarantee fund concerned next to the abovementioned assessment by the bank. BNG Bank actively follows the developments within the sectors in which it operates. This also applies to (the operation of) the institutions issuing the individual guarantees or suretyships. In addition, BNG Bank maintains contacts with relevant parties through a variety of channels, including conferences, seminars and bilateral talks. Lending subject to solvency requirements are preceded by an extensive creditworthiness analysis. The responsible team within Public Finance draws up the credit proposal. This contains a detailed assessment of the creditworthiness of the client

CREDIT RISKRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

18

concerned, based in part on the bank’s own internal rating model. The greater the degree of tailoring involved in a transaction, the more intensive the operational risk procedure is followed. To that end, the bank has implemented a tailor-made assessment process in order to keep the complexity manageable for both the client and the bank.– The Credit Risk Assessment department prepares an independent second opinion on the

credit proposal.– The intensity of the decision-making process is determined based on the proposed rating

and the size of the loan. The bank’s risk appetite also determines the level of maximum credit risk the bank is prepared to accept for the client in question. The credit proposal must be in accordance with this maximum risk.

– The Credit Committee decides whether the credit can be accepted. The Credit Committee is chaired by a member of the Executive Board and includes representation from the Public Finance directorate, the Credit Risk Assessment department and – where applicable – the Treasury department. If the Credit Committee is unable to form a unanimous opinion, the decision on the proposal is escalated to the Executive Board. A delegation model applies to loans and advances of limited scale or risk, in which authority to make decisions lies with the Director of Public Finance and the Credit Risk Assessment Manager.

Following the approval of a credit proposal and its acceptance by the client, the credit management process starts. This includes the following elements:– The file is completed with relevant documentation by the Public Finance Teams.– The Public Finance Teams are responsible for the file management, including monitoring

securities and covenants.– The creditworthiness is reviewed at least once a year. This involves an updating of the internal

rating. The Credit Committee evaluates these reviews. A delegation model applies here as well. Loans and advances whose credit quality (rating) has fallen below a specific level (see the table below) are subject to increased management scrutiny and, if necessary, transferred to the Special Management group within the Credit Risk Assessment department.

Despite the virtual absence of credit risk within this solvency-free portfolio, in 2016 the bank has set up an additional process for the assessment and review of the creditworthiness of parties that have only been granted loans and advances that are directly or indirectly guaranteed by the Dutch State. The bank’s internal rating models have been adapted to facilitate these assessments, thus providing consistency with the existing assessment for non solvency free lending. During 2017 these assessments have taken place and a process of fine tuning of policies and processes is in its final stage.

CREDIT MODELSMost of BNG Bank’s clients do not have an external rating. The bank makes their creditworthiness transparent using internally developed rating models. Given the ‘low default’ character of the loan portfolio, expert models are utilised. The models are used for internal assessment of creditworthiness, but not for capital calculations under Pillar I, where the bank uses the Standardised Approach. Models are in use for the following sectors:– Public housing;– Healthcare and Education;– DBFMO (Design Build Finance Maintain Operate, project financing);– Area development;– Financial institutions;– Energy, water, telecom, transport, logistics and the environment.

CREDIT RISKRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

19

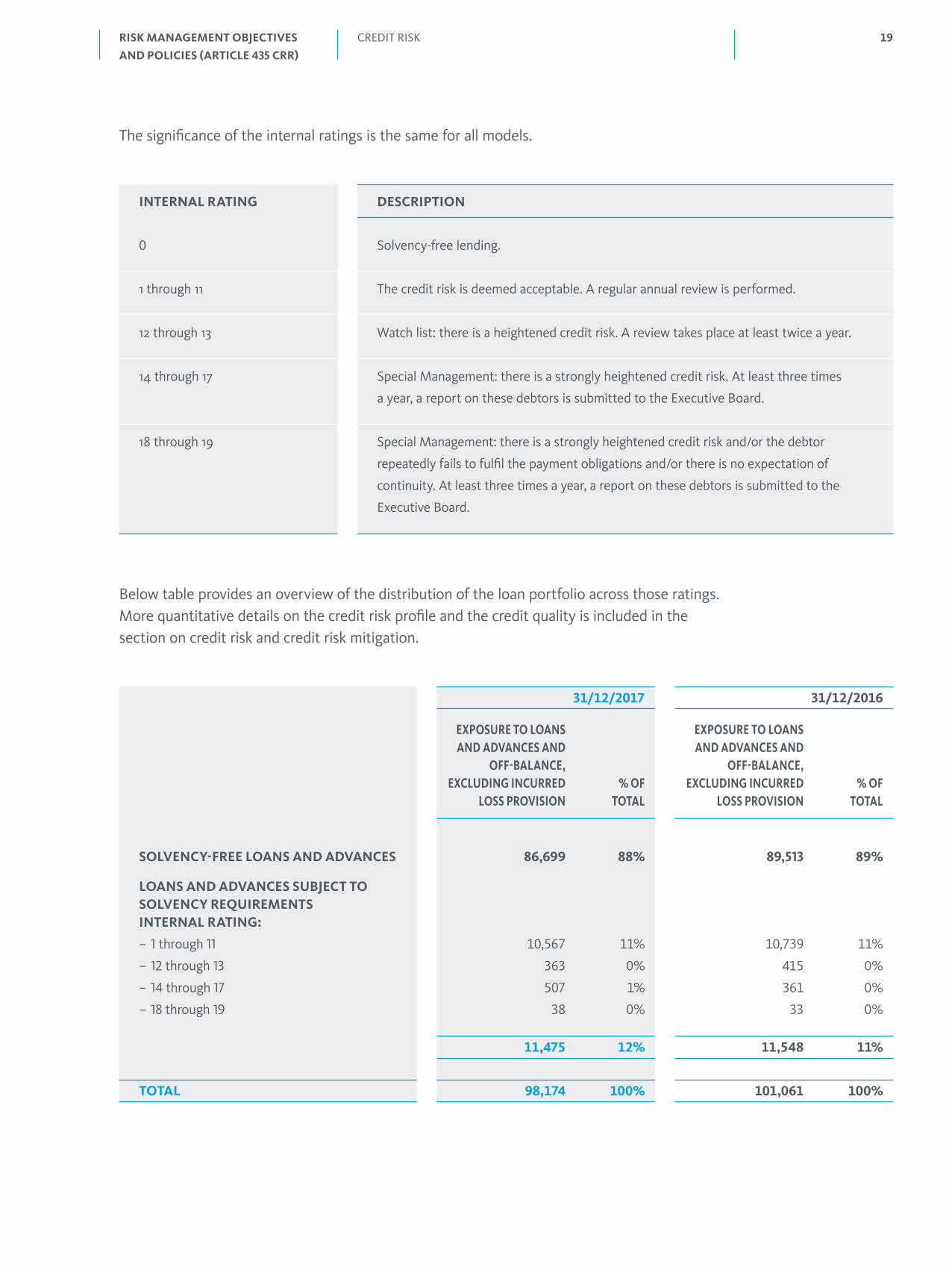

The significance of the internal ratings is the same for all models.

Below table provides an overview of the distribution of the loan portfolio across those ratings. More quantitative details on the credit risk profile and the credit quality is included in the section on credit risk and credit risk mitigation.

CREDIT RISKRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

INTERNAL RATING DESCRIPTION

0 Solvency-free lending.

1 through 11 The credit risk is deemed acceptable. A regular annual review is performed.

12 through 13 Watch list: there is a heightened credit risk. A review takes place at least twice a year.

14 through 17 Special Management: there is a strongly heightened credit risk. At least three times

a year, a report on these debtors is submitted to the Executive Board.

18 through 19 Special Management: there is a strongly heightened credit risk and/or the debtor

repeatedly fails to fulfil the payment obligations and/or there is no expectation of

continuity. At least three times a year, a report on these debtors is submitted to the

Executive Board.

31/12/2017 31/12/2016

EXPOSURE TO LOANS EXPOSURE TO LOANS AND ADVANCES AND AND ADVANCES AND OFF-BALANCE, OFF-BALANCE, EXCLUDING INCURRED % OF EXCLUDING INCURRED % OF LOSS PROVISION TOTAL LOSS PROVISION TOTAL

SOLVENCY-FREE LOANS AND ADVANCES 86,699 88% 89,513 89%

LOANS AND ADVANCES SUBJECT TO SOLVENCY REQUIREMENTSINTERNAL RATING:

– 1 through 11 10,567 11% 10,739 11%

– 12 through 13 363 0% 415 0%

– 14 through 17 507 1% 361 0%

– 18 through 19 38 0% 33 0%

11,475 12% 11,548 11%

TOTAL 98,174 100% 101,061 100%

20

EXTERNAL RATINGBNG Bank uses the external ratings awarded by rating agencies, specifically S&P, Moody’s, Fitch and DBRS. In determining the capital requirement, the bank uses the ratings of these four agencies if such ratings are available. Where possible, this applies to exposures to financial counterparties and investments in listed securities. The ratings relate to the counterparties themselves or specifically to the securities purchased.

FINANCIAL COUNTERPARTIESThe bank only conducts business with financial counterparties that have been rated by an external agency. Financial counterparties are periodically assessed for creditworthiness. This analysis includes an assessment of the internal rating. A limit is subsequently set or adjusted accordingly. The market risks associated with these parties are mitigated primarily through derivative transactions.

In order to reduce credit risk, netting agreements are agreed upon with financial counterparties with which BNG Bank actively concludes derivatives transactions. In addition, collateral agreements are concluded. These ensure that market value developments are mitigated on a daily basis by collateral. The agreements are updated where necessary in response to changing market circumstances, market practices and regulatory changes

COUNTERPARTIES WITH INVESTMENTS IN INTEREST-BEARING SECURITIES (IBS)BNG Bank’s IBS portfolio is held primarily for liquidity management purposes. The portfolio is composed of high-quality bonds, the majority of which are accepted as collateral by the central bank. BNG Bank’s total IBS portfolio can be subdivided into a liquidity portfolio and an ALM (Asset & Liability Management) portfolio. The liquidity portfolio consists exclusively of highly negotiable securities and is subdivided according to the various Liquidity Coverage Ratio (LCR) levels. The ALM portfolio is subdivided according to type of security. Each month, the development of the portfolio is reported to and discussed by the Investment Committee. Using factors such as external ratings and – in part – internal ratings, the bank monitors the development on an individual basis. The securities qualifying in accordance with the Delegated Act are subjected to a due diligence review process. The assets within these portfolios undergo an impairment analysis twice a year.

CONCENTRATION RISKRegarding of concentration risk, the bank differentiates between:– country risk with a distinction between domestic and foreign risk;– sector risk;– risk for individual parties with a distinction between clients and financial counterparties. Concentration risk is monitored by the first line as well as independently by the second line Risk Management department. Reports are submitted to the various committees and to the Management Board as the overarching authority. All policy decisions are taken by the Management Board, usually based on a recommendation by one of the sub-committees.

Alongside the risk concentration for solvency-free lending to the Dutch and other European governments, risk concentrations also exist in the market segments with exposures subject to solvency requirements, e.g. university hospitals. Almost all exposures to public sector entities subject to solvency requirements are secured by means of collateral or other securities. The other exposures subject to solvency requirements relate to financial institutions. Regarding

CREDIT RISKRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

21

concentration risk, three (2016: five) of these financial institutions together represent an exposure of more than 10% of the Tier 1 capital.

DOMESTIC COUNTRY RISKA considerable degree of concentration risk to the Netherlands is inherent to BNG Bank’s mission: financing the Dutch public sector. A considerable portion of the exposure is indirectly related to public sector property. However, these risks are generally mitigated by government guarantees on lending and by the WSW and WfZ guarantee funds. These guarantees result in a concentration risk in relation to public authorities and guarantee funds. The guarantee funds are guaranteed by the government via backstop constructions. What results on balance is therefore a risk in relation to the Dutch State. The concentration of this risk is high, but inextricably linked to BNG Bank’s business model and to its place in the Dutch social system.

FOREIGN COUNTRY RISKThe bank is exposed to foreign country risk as a result of transactions with financial counterparties to hedge the market risks arising from lending activities, as a result of its liquidity portfolio and, to a limited extent, in the context of lending and investments in the public sector abroad. The bank consciously purchases foreign securities for its liquidity portfolio because the majority of its loan portfolio relates to the Netherlands. Foreign lending is in most cases directly or indirectly guaranteed by the relevant governments.

All foreign exposures fall within limits set for each country. These limits mainly depend on the credit quality of the country in question. Moreover, a general limit of 15% of the balance sheet total applies to the total of all foreign exposures.

After the creditworthiness of certain countries in the Eurozone deteriorated, the bank has gradually reduced its positions in these countries. This was mainly realised by expiration of exposures without replacing them with new exposures. At the end of 2017, the bank’s foreign exposure (expressed in balance sheet value) totalled EUR 24.1 billion (2016: EUR 23.8 billion), of which EUR 11.6 billion consisted of long-term exposures (2016: EUR 13.1 billion). This represents 8.3% of the balance sheet total (2016: 8.5%).

SECTOR RISKSector-specific policies and annual internal targets are used for lending without direct or indirect guarantees from the Dutch State. These sector targets relate to both maximum concentrations on the balance sheet and commercial targets for new transactions according to the bank’s Annual Plan. Active portfolio management is positioned within the Public Finance department. Realisation of the risk targets as well as the commercial targets is reported to the Management Board on a quarterly basis by the Risk Management department. The concentration risk per sector is also part of the Risk Management economic capital model used to assess the capital adequacy allocation.

INDIVIDUAL STATUTORY MARKET PARTIESIn terms of exposures to individual parties without direct or indirect guarantees from the Dutch State, maximum amounts apply to all parties that, regardless of individual credit quality, are much lower than the amounts permitted under the Large Exposure Regulation. These limits take into account the degree to which sectors are anchored in the public sector. Further limits are also established based on the party’s individual internal rating.

CREDIT RISKRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

22

INDIVIDUAL FINANCIAL COUNTERPARTIESTransactions with these parties primarily consist of interest rate and currency swaps that are undertaken to mitigate market risks. Money market exposures can also apply. BNG Bank sets requirements for the minimum ratings of the financial counterparties with which it is willing to transact. This limits the number of available parties. As a consequence, the number of transactions with approved parties is high. Daily exchange of collateral helps to mitigate the credit risk from these parties with respect to derivatives in terms of market value, resulting in some operational risks. Default can also lead to market risks. Although the derivatives are measured at market value and the value of the collateral in this type of situation will be equal or close to the market value, the market is subject to fluctuations while the derivatives need to be rearranged with another party. The Financial Counterparties Committee limits and monitors positions with financial counterparties. Since 2016 the bank is clearing parts of its derivatives centrally. The bank uses five clearing members for this purpose. Central clearing has resulted in a shift in concentration risk from individual financial counterparties to the clearing members.

SETTLEMENT RISKExposure to settlement risks is limited to transactions with financial counterparties. Settlement risk is potentially high for those parties because of the relatively large size of the bank’s benchmark issues in foreign currencies. Netting and collateral agreements concluded with those parties serve to limit settlement risks resulting from the mutual offsetting of payments. Control measures throughout the operational process serve to further mitigate the settlement risk. The Bank Recovery and Resolution Directive (BRRD) that was introduced in Dutch law in November 2015, has included protection for settlement and payment systems in case of resolution of a bank, effectively reducing the settlement risk in parts of the financial system. An extensive review of the internal control measures was launched in 2016. Several follow up actions to improve practical mitigation have been implemented in 2017 and evaluation of further possible actions will continue in 2018. Capital allocation for settlement risk is based on an assessment of the likelihood of a possible loss from settlement risk and is updated yearly as part of the Internal Capital Adequacy Assessment Process.

CREDIT RISKRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

23

Market risk

DEFINITIONSMarket risk is defined as existing or future threats to the institution’s capital and results as a result of market price fluctuations. There are several forms of market risk: interest rate risk, foreign exchange risk, volatility risk and spread risk.– Interest rate risk: The current or prospective risk to earnings and capital arising from adverse

movements in interest rates. – Foreign exchange: The risk to annual results and capital arising from unfavourable exchange

rate fluctuations.– Volatility risk: The risk to annual results and capital arising from adverse movements in the

implied volatility of market interest rates or currencies. This risk only applies to products with types of optionality, such as caps and floors.

– Spread risk: The risk to annual results and capital arising from unfavourable credit risk spread fluctuations and unfavourable liquidity risk spread fluctuations.

GOVERNANCEThe Treasury and Capital Markets directorate is the ‘first line of defence’ and responsible for day-to-day market risk management. This directorate is responsible for hedging the market risks resulting from commercial activities. Additionally, the Treasury department has a mandate to adopt an interest rate risk position within the limits imposed by the Asset & Liability Committee (ALCO). The mandate for the ALCO to set limits is restricted by the capital that is explicitly allocated for this purpose. Stress scenarios are used to assess continuously whether this capital is sufficient.

The Risk Management Department is the ‘second line of defence’ and responsible for the independent monitoring of market risk and checks daily whether the risk positions are within their limits. The department prepares reports for the ALCO and the Treasury department and provides risks analyses and advice, both proactively and on request. By participating in the product approval process it also plays an important role in decisions to assume new market risks caused by new activities.

The ALCO is responsible for implementing the market risk policy. The ALCO consists of the Executive Board members, the Managing Director of Treasury and Capital Markets, the Head of Risk Management, the Company Secretary and the Senior economist, supplemented with other participators depending on the agenda.

MARKET RISKRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

24

DEVELOPMENTSThe bank opted for a restrictive interest rate risk position in 2017. Because of an expected rise in interest rates, the interest rate position, measured in basis point sensitivity, was lower throughout the year compared to the long-term benchmark applied by the bank. The actual interest rate risk position took into account that the likelihood of an additional return in terms of market value due to a stable trend or further decline in interest rates did not sufficiently compensate for the possibly much larger loss of market value if interest rates would rise.

The benchmark reflects a continuously neutral investment of equity position in 10 years Dutch Government Bonds, which is in line with the required return of the shareholders. Compared to this the bank’s interest rate risk position in terms of mark to market outperformed the benchmark because the interest rates rose as expected.

Regarding its interest rate risk framework, the bank improved the measurement and monitoring of the credit spread risk. Furthermore, an interest rate gap analysis was designed and implemented in 2017, to complement the existing interest rate risk measures. Finally, a reverse stress scenario was added to the current parallel and non-parallel stress scenarios to determine under which circumstances the market risk limits set by the ALCO would be breached. In February the bank participated in the Interest Rate Risk in the Banking Book sensitivity exercise that was conducted by the ECB. The conclusion was that the bank was well capitalised to survive this stress scenario.

–0.2

–0.4

0

0.2

0.4

0.6

0.8

1.0

1.2

(in %

)

EUR Swap 2 years DifferenceEUR Swap 10 years

Janu

ary

2017

Febr

uary

017

Mar

ch 2

017

Apr

il 20

17

May

20

17

June

20

17

July

20

17

Aug

ust 2

017

Sept

embe

r 20

17

Oct

ober

20

17

Nov

embe

r 20

17

Dec

embe

r 20

17

EUROPEAN SWAP CURVE

MARKET RISKRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

25

INTEREST RATE RISKThe bank’s interest rate risk position is determined based on interest rates excluding credit and liquidity risk spreads and discounts. This means that changes in these spreads and discounts are not taken into account. The interest rate position in the banking book is internally managed in books for the Treasury department and the ALCO. The interest rate risk within the margin books (containing the lending and funding activities) and ALCO book (containing the active position) are transferred to the Treasury book by using internal swaps. The net interest rate risk in the Treasury book is externally hedged. Working on the basis of market forecasts from the departments Treasury and Economic Research, the ALCO periodically determines the bank’s interest rate outlook and defines – within the predetermined frameworks – the interest rate position and the limits and early warnings (target) levels within which the Treasury and Capital Markets directorate must operate.

The bank manages its interest rate position by using principal risk measures, which are monitored by the Risk Management department. The principal risk measure to monitor and manage interest rate risk applied by BNG Bank is the sensitivity (delta) of the economic value of the bank’s equity to changes in the interest-rate curve. The delta is determined for several maturity intervals on the interest rate curve and is reported daily. The ALCO manages the interest rate risk position based on the delta for each maturity interval.

In addition, the bank carries out daily and monthly scenario analyses on the economic value of the bank’s equity. These parallel and non-parallel stress scenario analyses are performed to cover both external requirements as well internal required levels.

Furthermore, BNG Bank analyses the basis risk between tenors and now uses an interest rate gap report. Next to that, the impact of interest rate stress scenarios on the interest results (Earnings at Risk) of the bank is monitored. All these interest rate risk measures complement each other and ensure the transparency and manageability of risks.

Any breach of a limit must be reported to the ALCO. The ALCO decides whether action should be taken immediately to adjust the interest rate position to a position within the limit or to authorize the limit breach for a certain period of time. Limits are set for the delta of the economic value per maturity interval and the scenario analysis outcomes. Early warning levels are set for the internal Earnings at Risk scenarios; the (tenor) basis risks and the interest rate gap analysis for which no direct action from the ALCO is required. The bank also sees to it that the outlier criterion is not exceeded, by applying an internal threshold value which serves as an early warning. The outlier criterion is prescribed by the Basel regulations, where it is used to express the maximum relationship between market risk and equity. In this context, the interest rate risk is measured under extreme conditions with an instantaneous parallel interest rate shock of plus or minus 200 basis points. The limits with respect to interest rate risk were not breached in 2017.

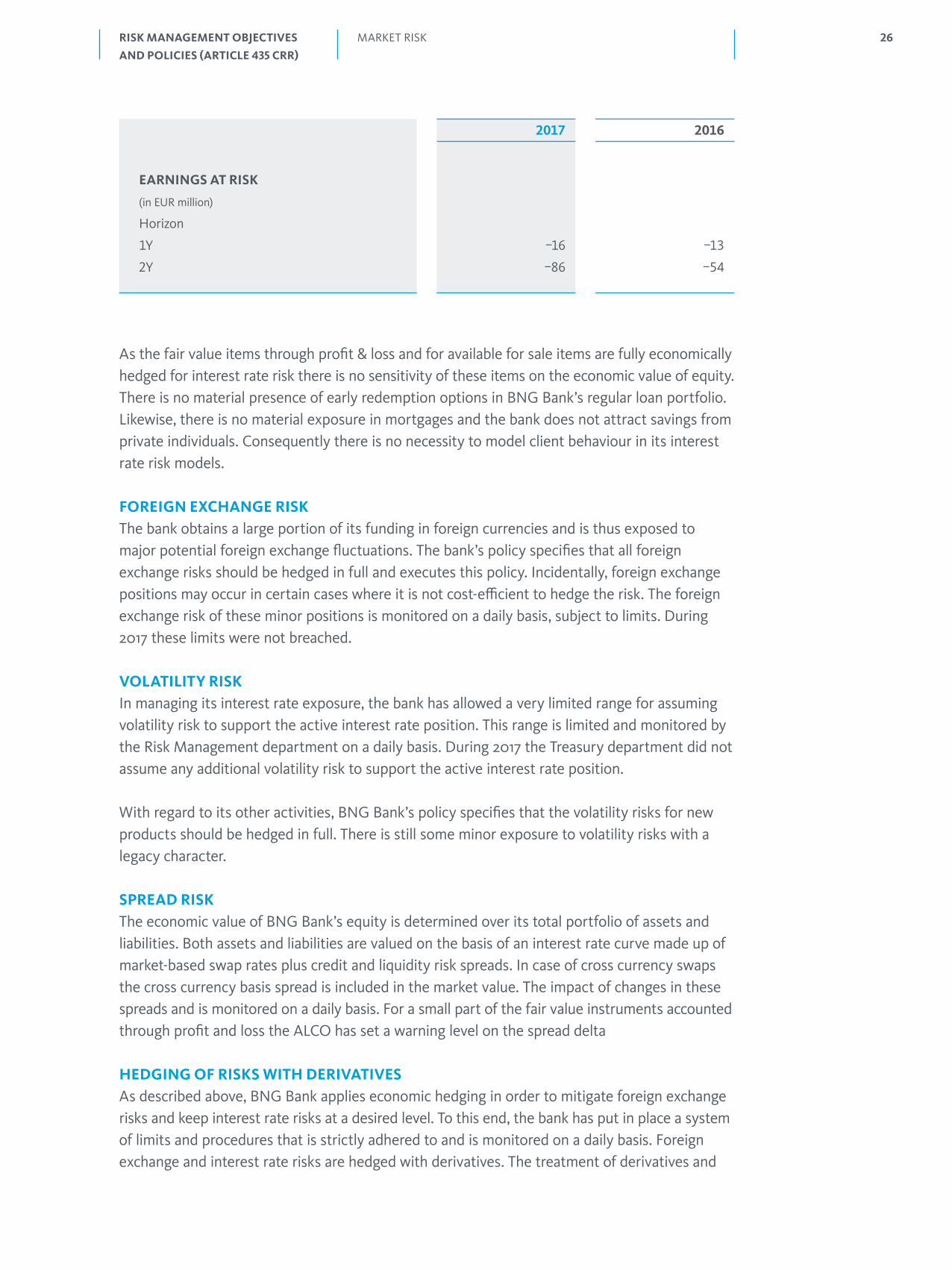

BNG Bank measures the sensitivity of its interest rate result using the Earning at Risk (EAR) measure. The EAR is for BNG Bank an appropriate measure because it monitors the effect of an interest rate shock scenario on an accrual basis. The table below outlines the effect of a minus 180 basis points gradual parallel interest rate shock for the 1 year and 2 year horizon at the end of 2017.

MARKET RISKRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

26MARKET RISKRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

As the fair value items through profit & loss and for available for sale items are fully economically hedged for interest rate risk there is no sensitivity of these items on the economic value of equity.There is no material presence of early redemption options in BNG Bank’s regular loan portfolio. Likewise, there is no material exposure in mortgages and the bank does not attract savings from private individuals. Consequently there is no necessity to model client behaviour in its interest rate risk models.

FOREIGN EXCHANGE RISKThe bank obtains a large portion of its funding in foreign currencies and is thus exposed to major potential foreign exchange fluctuations. The bank’s policy specifies that all foreign exchange risks should be hedged in full and executes this policy. Incidentally, foreign exchange positions may occur in certain cases where it is not cost-efficient to hedge the risk. The foreign exchange risk of these minor positions is monitored on a daily basis, subject to limits. During 2017 these limits were not breached.

VOLATILITY RISKIn managing its interest rate exposure, the bank has allowed a very limited range for assuming volatility risk to support the active interest rate position. This range is limited and monitored by the Risk Management department on a daily basis. During 2017 the Treasury department did not assume any additional volatility risk to support the active interest rate position.

With regard to its other activities, BNG Bank’s policy specifies that the volatility risks for new products should be hedged in full. There is still some minor exposure to volatility risks with a legacy character.

SPREAD RISKThe economic value of BNG Bank’s equity is determined over its total portfolio of assets and liabilities. Both assets and liabilities are valued on the basis of an interest rate curve made up of market-based swap rates plus credit and liquidity risk spreads. In case of cross currency swaps the cross currency basis spread is included in the market value. The impact of changes in these spreads and is monitored on a daily basis. For a small part of the fair value instruments accounted through profit and loss the ALCO has set a warning level on the spread delta

HEDGING OF RISKS WITH DERIVATIVESAs described above, BNG Bank applies economic hedging in order to mitigate foreign exchange risks and keep interest rate risks at a desired level. To this end, the bank has put in place a system of limits and procedures that is strictly adhered to and is monitored on a daily basis. Foreign exchange and interest rate risks are hedged with derivatives. The treatment of derivatives and

2017 2016

EARNINGS AT RISK

(in EUR million)

Horizon

1Y –16 –13

2Y –86 –54

27

hedged items in the balance sheet and income statement is such that they are aligned as much as possible with the actual economic hedging. For accounting purposes, BNG Bank processes this hedging relationship under IFRS by applying micro and portfolio fair value hedging, as well as cash flow hedging.

Micro fair value hedging (MH) is applied to individual transactions involved in an economic hedge relationship to offset interest rate risks. This form of hedging is applied to nearly all debt securities issued. The foreign exchange and interest rate risks are hedged by means of derivatives, mainly (cross-currency) interest rate swaps. The issues are fully offset against the derivatives so that, on a net basis, the fixed coupons of the issues are converted into variable interest amounts in euros. Both the issues and the accompanying derivatives can contain structures, such as options, which are also fully offset. The revaluation effect of hedged MH transactions with regard to fair value hedging is accounted for in the same balance sheet item as the hedged items.

BNG Bank applies (micro) cash flow hedge accounting to virtually all long-term funding transactions in foreign currencies in order to protect the bank’s result against possible variability in future cash flows due to exchange rate fluctuations. The basis swap spread is an important building block of the value of a cross-currency (interest rate) swap. Therefore, if seen as a separate financial instrument, the fair value of these swaps is influenced by the change in the basis swap spread. However, this change has no economic effect on the bank and it, in principle, never will, as the bank will generally retain the contracts until their maturity. With the exception of voluntary early redemption of funding in foreign currencies or an immediate and complete withdrawal from the banking business, there are no circumstances under which these negative revaluations can lead to a realised result.

In portfolio fair value hedging (PH), the interest rate risks of a group of transactions are hedged by means of a group of derivatives. The hedging relationship is constructed and controlled at an aggregate level, thus precluding relationships with individual transactions. Within BNG Bank, portfolio hedging, like micro hedging, has been highly effective in recent years. Any ineffectiveness that occurs is recognised in the income statement.

Although BNG Bank uses derivatives for economic hedging purposes, it is not possible in all cases to include these in a hedge accounting relationship, as permitted by IFRS. For the derivatives that are not involved in a hedge accounting relationship, in virtually all cases there is an economic hedged position which is also recognised at fair value through the income statement so that, in total, the volatility of the result due to interest rate and foreign exchange risks is limited.

MARKET RISKRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

28

Liquidity risk and funding risk

DEFINITIONSLiquidity risk is defined as the existing or future threat to the institution’s capital and results due to the possibility that at any moment it will not be able to fulfil its payment obligations without incurring any unacceptable costs or losses.− Short-term liquidity risk: The risk that the bank will not be able to attract sufficient funds to

meet its payment obligations.− Refinancing or long-term liquidity: The risk that the bank will not, as a result of its own

creditworthiness, be able to attract any (or sufficient) funds against prices that won’t jeopardise its continuity.

GOVERNANCEThe Treasury and Capital Markets directorate is the ‘first line of defence’ and responsible for the day-to-day liquidity and funding risk management. They are responsible to attract funding resulting from commercial activities. The Treasury department is mandated to adopt a liquidity risk position within the limits and triggers imposed by the ALCO. Stress scenarios are used to continually assess the liquidity risks, in order to determine whether the liquidity and funding is sufficient.

The Risk Management department is the ‘second line of defence’ and responsible for the independent monitoring of liquidity risk and daily checks whether the bank remains within its limits and triggers set by the ALCO. The Risk Management department independently reports to the ALCO and to the Treasury department on the use of predetermined limits and provides risks analyses and advice, both proactively and on request. Liquidity and funding risk measures such as liquidity gap analysis, contingency funding plan, and stress scenarios regarding the survival period are monitored against limits or triggers, both short term and long term. The Risk management department is also instrumental in the decision to accept liquidity and funding risks as part of the product approval process.

If liquidity limits or triggers are breached, the Contingency Funding Plan is enforced. Additional ALCO meetings, temporary procedures for more intensive liquidity management and temporary control of liquidity management by the liquidity contingency team are the main elements of this plan.

LIQUIDITY RISK AND FUNDING RISKRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

29

DEVELOPMENTSIn the last quarter of 2017, BNG Bank decided to continue long term prefunding, by exceeding the funding target for 2017 of EUR 15.6 billion by EUR 1.3 billion. The main reasons are funding of collateral and attractive pricing of liquidity. Regarding alternative funding, negotiations on a new Global Loan Facility were finalised in during the last quarter. This Global Loan of EUR 300 million is provided by Council of Europe.

In 2017 BNG Bank has improved the Internal Liquidity Adequacy Assessment Process stress scenarios by adding more scenarios including a reverse stress scenario, remodelling collateral outflows and fine-tuning other input parameters to get a better insight in the bank’s liquidity position.

In addition, ALCO reporting was improved by implementing a monthly liquidity risk dashboard. Furthermore, the bank improved the measurement, reporting and monitoring of the funding spread risk. Funding spread risk is the accrual margin change due to increased funding spreads which cannot be passed through to the spreads of new assets. This risk is caused by the liquidity mismatch between assets and liabilities. The ALCO has set an early warning level for the 1 year horizon funding spread risk.

Finally, the bank is working on a forward-looking model to monitor the Net Stable Funding Ratio (NSFR) more closely.

LIQUIDITYBNG Bank wants to provide a constant and stable presence in the market and want to continue to meet the demand for credit, even in difficult times. It also pursues a prudent liquidity position to ensure that it can meet its obligations at all times. In this context, ongoing access to the money and capital markets is essential, and with it, the ongoing maintenance of attractive, varied and sufficiently large issue programmes for investors. In addition, buffers are required in order to have access to liquidity in times of stress. One such buffer is formed by assets held explicitly for liquidity purposes, known as the liquidity portfolio. The management of the size and composition of this portfolio is one of the liquidity measures to comply with the requirement under the CRR to have an LCR of at least 100%. BNG Bank also holds an ample quantity of collateral with the central bank, which enables it to obtain short-term funding immediately. Since most of the banks assets could serve as collateral, this collateral may be further extended in the event of prolonged stress.

The limits on funding deficits in the short term and in the long term are an explicit part of the risk appetite and directly determine the level of the principal liquidity limits. BNG Bank also calculates survival periods. The survival period is the period in which the standard liquidity buffers are sufficient for absorbing the consequences of a stress scenario. Survival periods are determined under a range of stress scenarios. During 2017, the survival periods indicated by the stress tests met the requirement laid down in the risk appetite to be able to endure nine months without access to capital market funding. During this period, the bank is also capable to provide its core client groups with liquidity, fulfilling its ambition to assist its clients even in difficult times.

The bank believes that during 2017 its liquidity management was adequate and that the strength of the bank’s liquidity position is both amply sufficient and in compliance with the regulatory standards and limits set by the ALCO.

LIQUIDITY RISK AND FUNDING RISKRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

30

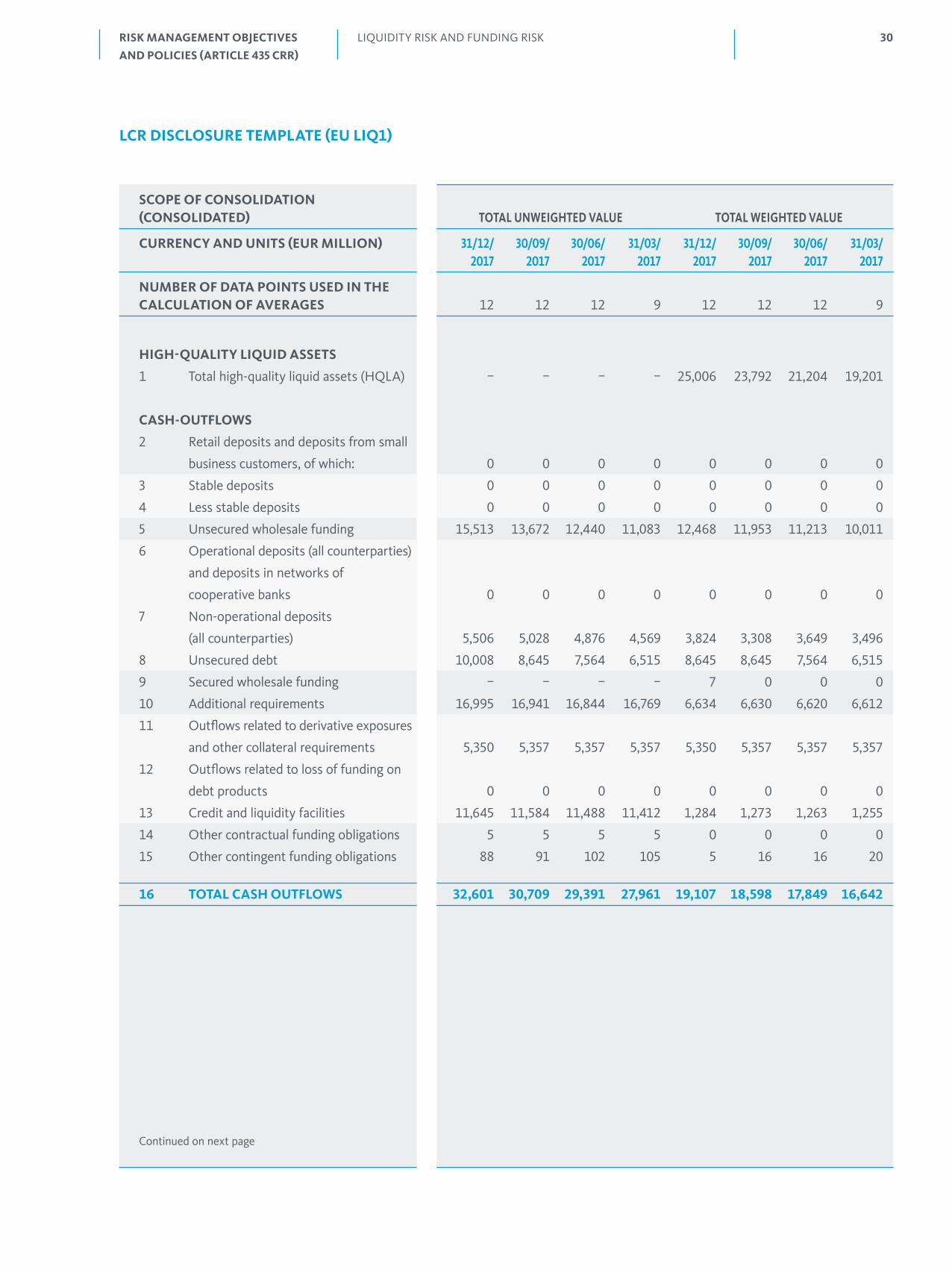

LCR DISCLOSURE TEMPLATE (EU LIQ1)

LIQUIDITY RISK AND FUNDING RISKRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

SCOPE OF CONSOLIDATION (CONSOLIDATED) TOTAL UNWEIGHTED VALUE TOTAL WEIGHTED VALUE

CURRENCY AND UNITS (EUR MILLION) 31/12/ 30/09/ 30/06/ 31/03/ 31/12/ 30/09/ 30/06/ 31/03/ 2017 2017 2017 2017 2017 2017 2017 2017

NUMBER OF DATA POINTS USED IN THE CALCULATION OF AVERAGES 12 12 12 9 12 12 12 9

HIGH-QUALITY LIQUID ASSETS

1 Total high-quality liquid assets (HQLA) – – – – 25,006 23,792 21,204 19,201

CASH-OUTFLOWS

2 Retail deposits and deposits from small

business customers, of which: 0 0 0 0 0 0 0 0

3 Stable deposits 0 0 0 0 0 0 0 0

4 Less stable deposits 0 0 0 0 0 0 0 0

5 Unsecured wholesale funding 15,513 13,672 12,440 11,083 12,468 11,953 11,213 10,011

6 Operational deposits (all counterparties)

and deposits in networks of

cooperative banks 0 0 0 0 0 0 0 0

7 Non-operational deposits

(all counterparties) 5,506 5,028 4,876 4,569 3,824 3,308 3,649 3,496

8 Unsecured debt 10,008 8,645 7,564 6,515 8,645 8,645 7,564 6,515

9 Secured wholesale funding – – – – 7 0 0 0

10 Additional requirements 16,995 16,941 16,844 16,769 6,634 6,630 6,620 6,612

11 Outflows related to derivative exposures

and other collateral requirements 5,350 5,357 5,357 5,357 5,350 5,357 5,357 5,357

12 Outflows related to loss of funding on

debt products 0 0 0 0 0 0 0 0

13 Credit and liquidity facilities 11,645 11,584 11,488 11,412 1,284 1,273 1,263 1,255

14 Other contractual funding obligations 5 5 5 5 0 0 0 0

15 Other contingent funding obligations 88 91 102 105 5 16 16 20

16 TOTAL CASH OUTFLOWS 32,601 30,709 29,391 27,961 19,107 18,598 17,849 16,642

Continued on next page

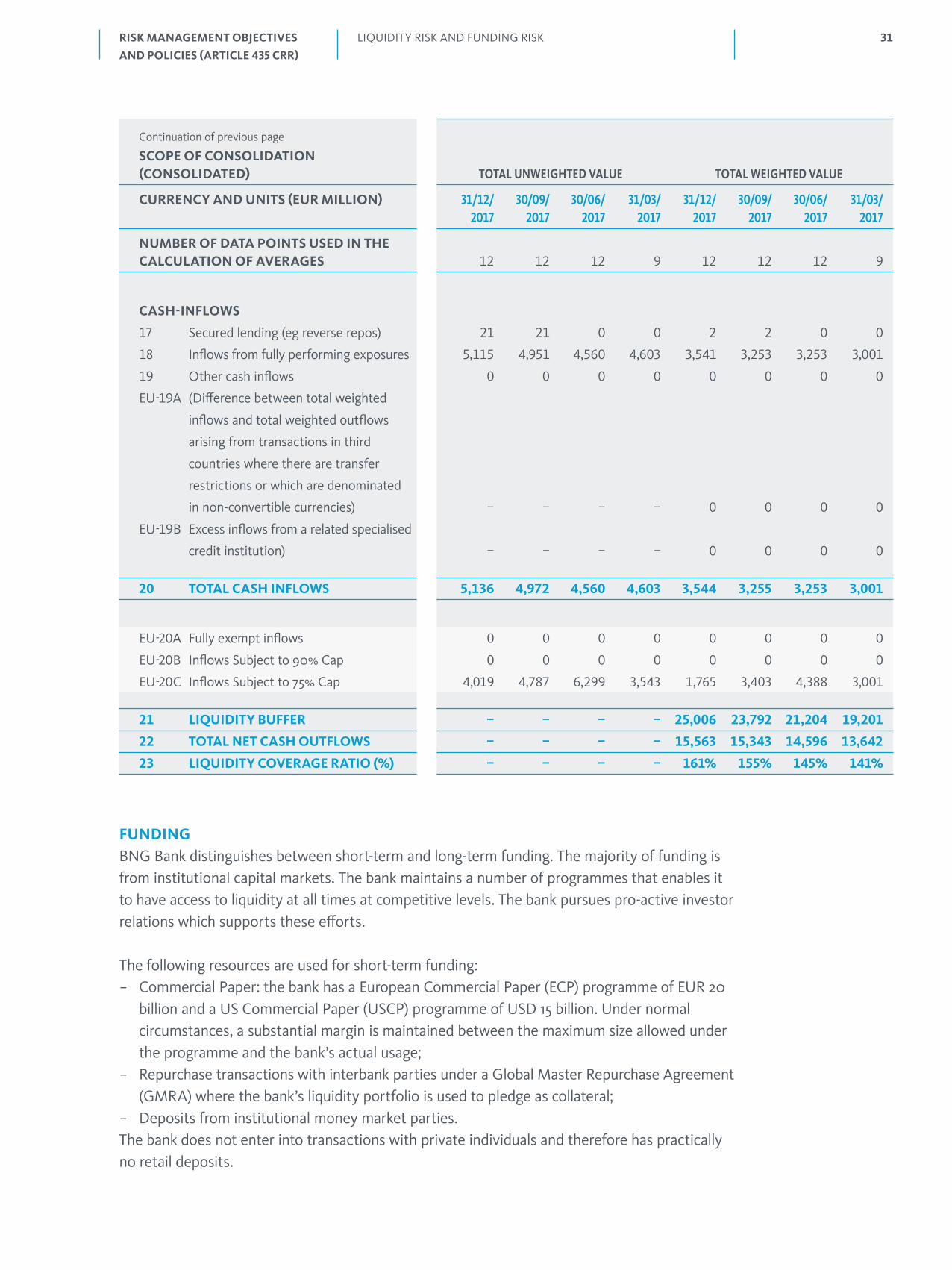

31LIQUIDITY RISK AND FUNDING RISKRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

Continuation of previous page

SCOPE OF CONSOLIDATION (CONSOLIDATED) TOTAL UNWEIGHTED VALUE TOTAL WEIGHTED VALUE

CURRENCY AND UNITS (EUR MILLION) 31/12/ 30/09/ 30/06/ 31/03/ 31/12/ 30/09/ 30/06/ 31/03/ 2017 2017 2017 2017 2017 2017 2017 2017

NUMBER OF DATA POINTS USED IN THE CALCULATION OF AVERAGES 12 12 12 9 12 12 12 9

CASH-INFLOWS

17 Secured lending (eg reverse repos) 21 21 0 0 2 2 0 0

18 Inflows from fully performing exposures 5,115 4,951 4,560 4,603 3,541 3,253 3,253 3,001

19 Other cash inflows 0 0 0 0 0 0 0 0

EU-19A (Difference between total weighted

inflows and total weighted outflows

arising from transactions in third

countries where there are transfer

restrictions or which are denominated

in non-convertible currencies) – – – – 0 0 0 0

EU-19B Excess inflows from a related specialised

credit institution) – – – – 0 0 0 0

20 TOTAL CASH INFLOWS 5,136 4,972 4,560 4,603 3,544 3,255 3,253 3,001

EU-20A Fully exempt inflows 0 0 0 0 0 0 0 0

EU-20B Inflows Subject to 90% Cap 0 0 0 0 0 0 0 0

EU-20C Inflows Subject to 75% Cap 4,019 4,787 6,299 3,543 1,765 3,403 4,388 3,001

21 LIQUIDITY BUFFER – – – – 25,006 23,792 21,204 19,201

22 TOTAL NET CASH OUTFLOWS – – – – 15,563 15,343 14,596 13,642

23 LIQUIDITY COVERAGE RATIO (%) – – – – 161% 155% 145% 141%

FUNDINGBNG Bank distinguishes between short-term and long-term funding. The majority of funding is from institutional capital markets. The bank maintains a number of programmes that enables it to have access to liquidity at all times at competitive levels. The bank pursues pro-active investor relations which supports these efforts.

The following resources are used for short-term funding:− Commercial Paper: the bank has a European Commercial Paper (ECP) programme of EUR 20

billion and a US Commercial Paper (USCP) programme of USD 15 billion. Under normal circumstances, a substantial margin is maintained between the maximum size allowed under the programme and the bank’s actual usage;

− Repurchase transactions with interbank parties under a Global Master Repurchase Agreement (GMRA) where the bank’s liquidity portfolio is used to pledge as collateral;

− Deposits from institutional money market parties.The bank does not enter into transactions with private individuals and therefore has practically no retail deposits.

32

The following programmes are available for long-term funding:− the Debt Issuance Programme (DIP) of EUR 100 billion. Socially Responsible Investing (SRI)

bonds are also issued under this programme;− the Kangaroo-Kauri Programme, specifically for the Australian and New Zealand market, of

AUD 10 billion;− the Samurai shelf registration and Uridashi shelf registration, specifically for Japanese investors;− the Namen-Schuld-Verschreibungen (NSV), under German Law;− and Private loan agreements.

For reasons of diversification, the bank also uses the following alternative funding sources in order to finance its activities:− Global loans from the European Investment Bank and the Council of Europe development

Bank;− Guaranteed Investment Contracts (GICs).

The bank has a funding plan in which the desired funding mix is described in more detail. Part of the funding plan is the annual issuance in benchmark size. These large-scale issues ensure that the bank has a high profile among investors, allowing it to retain access to investors even in times of market stress. The actual realisation of this desired funding mix or the reason for diverging from it is monitored and reported to the ALCO.

LIQUIDITY RISK AND FUNDING RISKRISK MANAGEMENT OBJECTIVES

AND POLICIES (ARTICLE 435 CRR)

33

Operational risk