Pillar 3 Disclosure 2019 - Nationwide Building Society › ... › Pillar-3-2019.pdf · Nationwide...

114

Pillar 3 Disclosure 2019 Your Society. Strong today, investing for tomorrow. Jade, member since 2013 Sienna, member since 2016 Jeanette, member since 2013

Transcript of Pillar 3 Disclosure 2019 - Nationwide Building Society › ... › Pillar-3-2019.pdf · Nationwide...

Pillar 3 Disclosure 2019Your Society. Strong today, investing for tomorrow.

Jade, member since 2013 Sienna, member since 2016Jeanette, member since 2013

Nationwide Pillar 3 Disclosure 2019

2

Contents

1 Executive Summary ....................................................................................................................... 6

1.1 Introduction ................................................................................................................................................................... 6

1.2 Summary of key metrics ............................................................................................................................................... 6

2 Introduction .................................................................................................................................... 9

2.1 Background ................................................................................................................................................................... 9

2.2 Scope ............................................................................................................................................................................. 9

2.3 Risk appetite ................................................................................................................................................................ 10

2.4 Individual (Solo) consolidation .................................................................................................................................... 10

2.5 Reporting ...................................................................................................................................................................... 10

2.6 Changes to disclosure requirements .......................................................................................................................... 10

2.7 Location ........................................................................................................................................................................ 10

2.8 Policy, verification and sign off ................................................................................................................................... 10

3 Capital resources .......................................................................................................................... 11

3.1 Total available capital .................................................................................................................................................. 11

3.2 Common Equity Tier 1 capital ..................................................................................................................................... 11

3.3 Tier 1 capital ................................................................................................................................................................. 11

3.4 Tier 2 capital................................................................................................................................................................. 11

3.5 Leverage ratio .............................................................................................................................................................. 15

4 Capital requirements .................................................................................................................... 18

4.1 Introduction .................................................................................................................................................................. 18

4.2 Pillar 1 ........................................................................................................................................................................... 18

Credit risk ......................................................................................................................................................................... 18

Operational risk ................................................................................................................................................................ 18

Market risk ........................................................................................................................................................................ 19

Overview of Pillar 1 RWAs and capital requirements .................................................................................................... 19

Changes in value of minimum capital requirements ................................................................................................... 20

4.3 Pillar 2 .......................................................................................................................................................................... 20

Introduction ...................................................................................................................................................................... 20

Internal Capital Adequacy Assessment Process (ICAAP) ............................................................................................. 20

Pillar 2A .............................................................................................................................................................................. 21

Stress testing ..................................................................................................................................................................... 21

4.4 Regulatory capital buffers .......................................................................................................................................... 22

4.5 Countercyclical capital buffer .................................................................................................................................... 22

4.6 Future regulatory developments ............................................................................................................................... 23

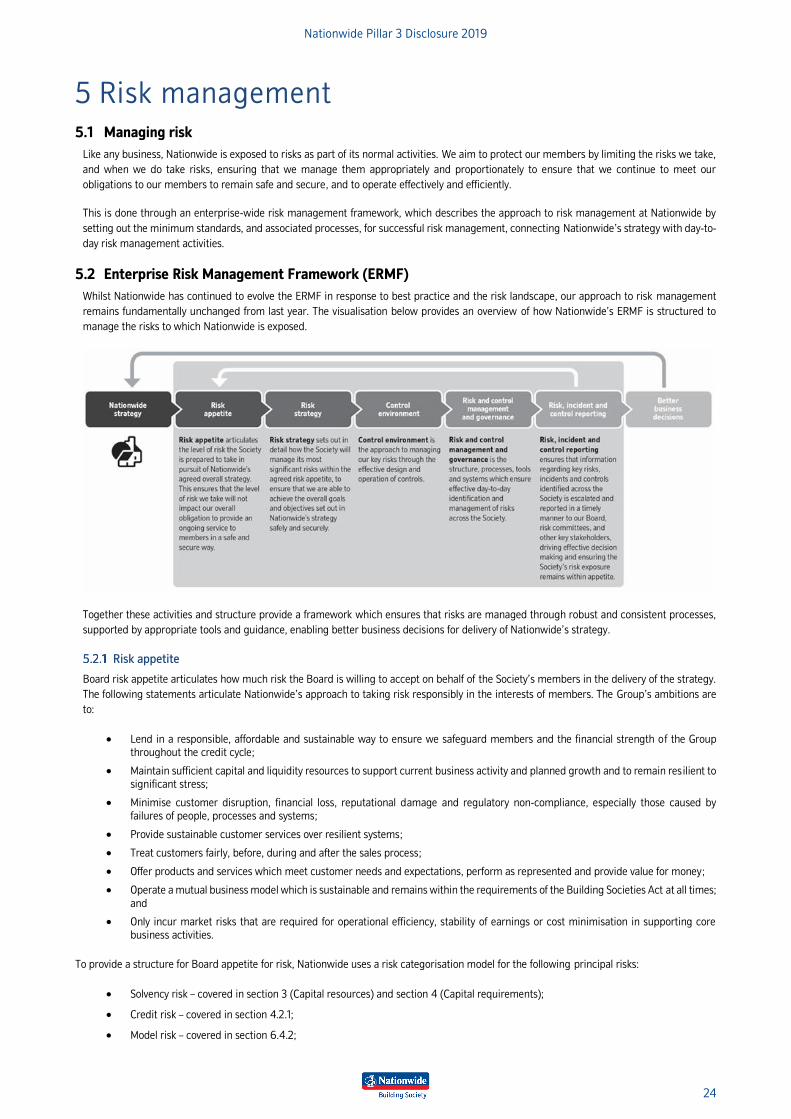

5 Risk management ........................................................................................................................ 24

5.1 Managing risk .............................................................................................................................................................. 24

5.2 Enterprise Risk Management Framework (ERMF) ................................................................................................... 24

Risk appetite ..................................................................................................................................................................... 24

Risk strategy ..................................................................................................................................................................... 25

Nationwide Pillar 3 Disclosure 2019

3

Control environment ........................................................................................................................................................ 25

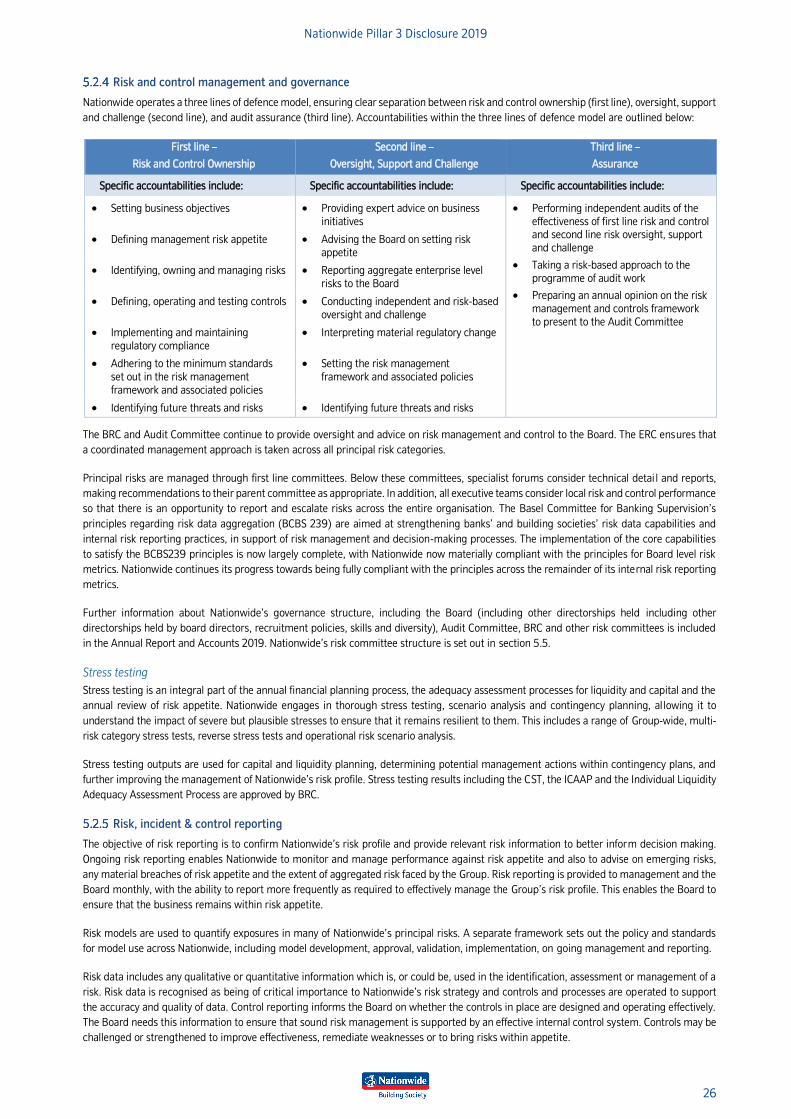

Risk and control management and governance ........................................................................................................... 26

Risk, incident & control reporting .................................................................................................................................. 26

Risk culture ....................................................................................................................................................................... 27

5.3 Effectiveness of risk management arrangements ..................................................................................................... 27

5.4 Coverage of risks .......................................................................................................................................................... 27

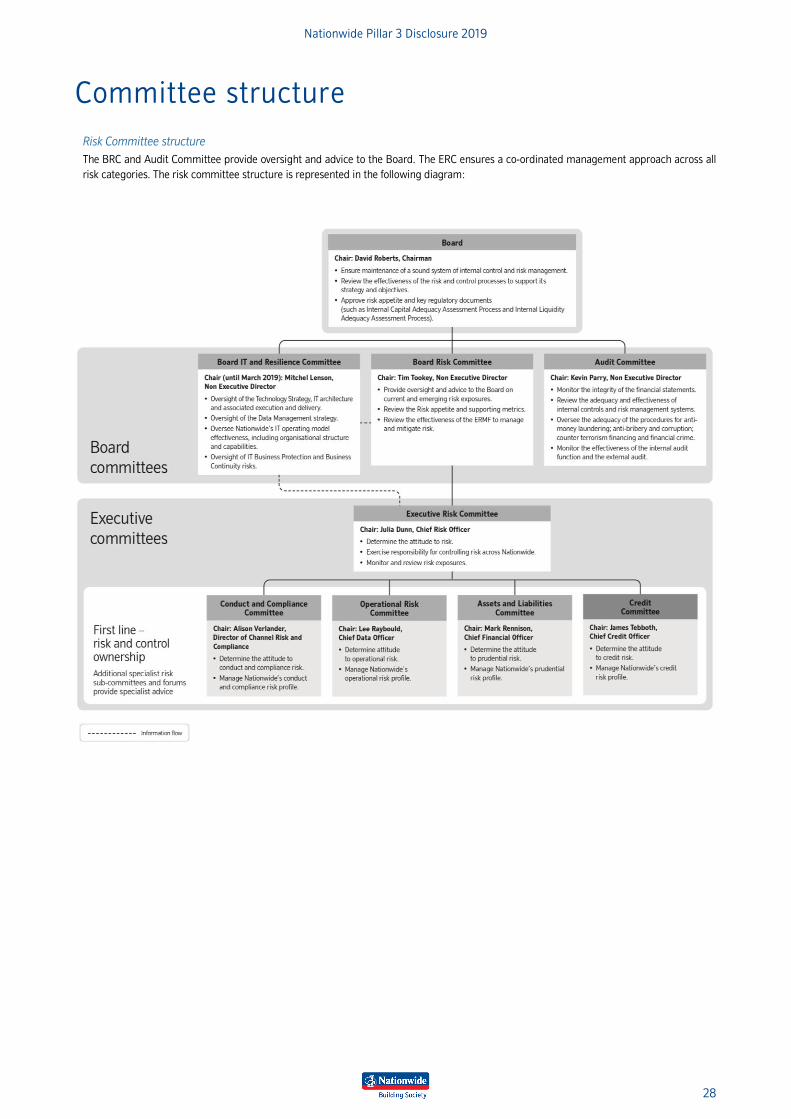

5.5 The Group’s risk committee structure and responsibilities ...................................................................................... 27

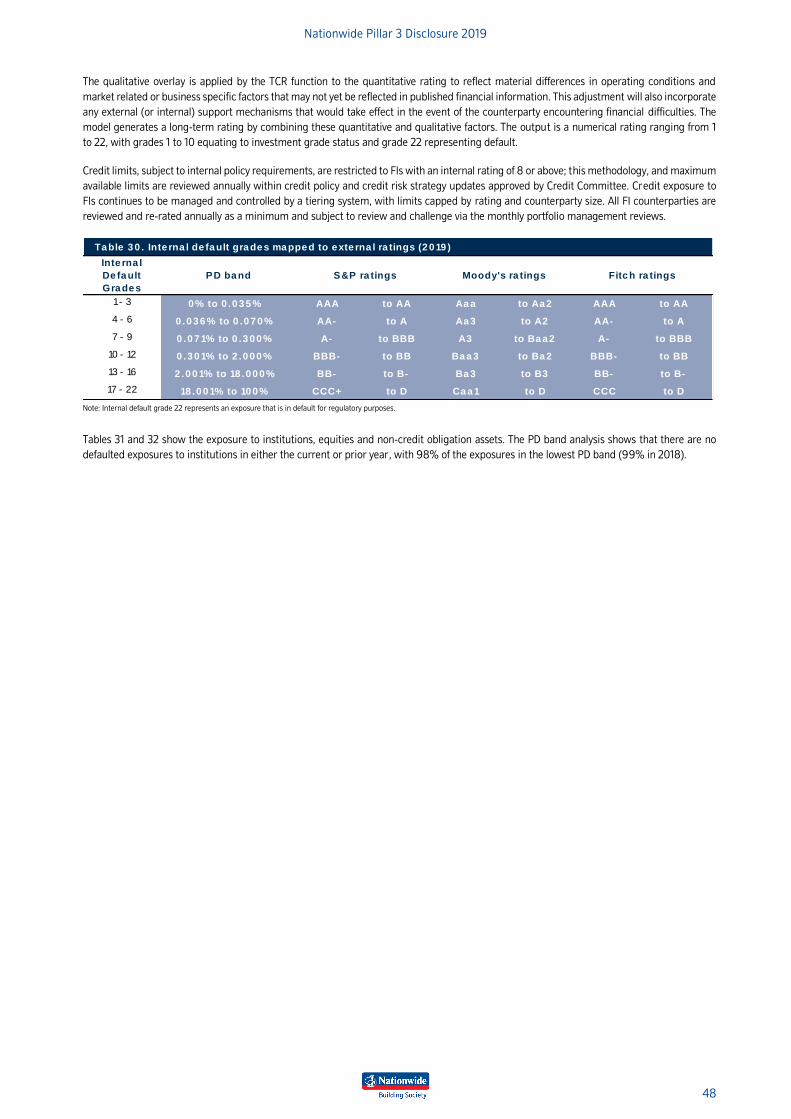

6 Credit risk ..................................................................................................................................... 29

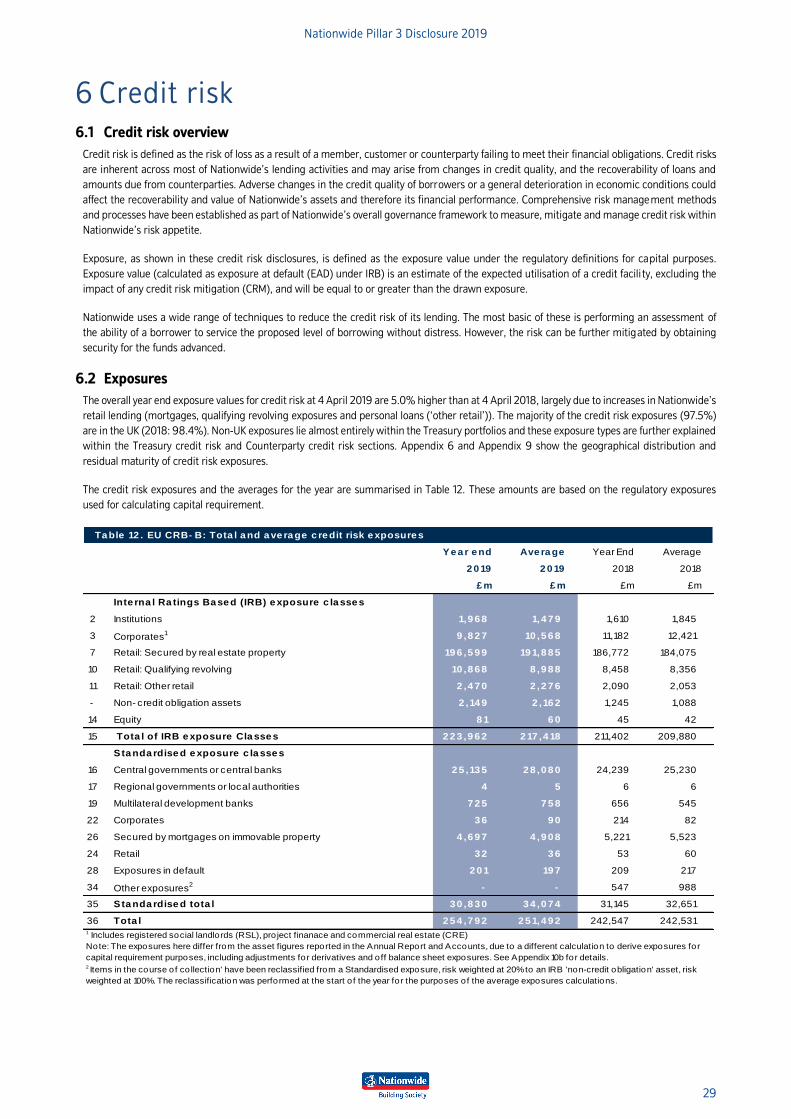

6.1 Credit risk overview .................................................................................................................................................... 29

6.2 Exposures .................................................................................................................................................................... 29

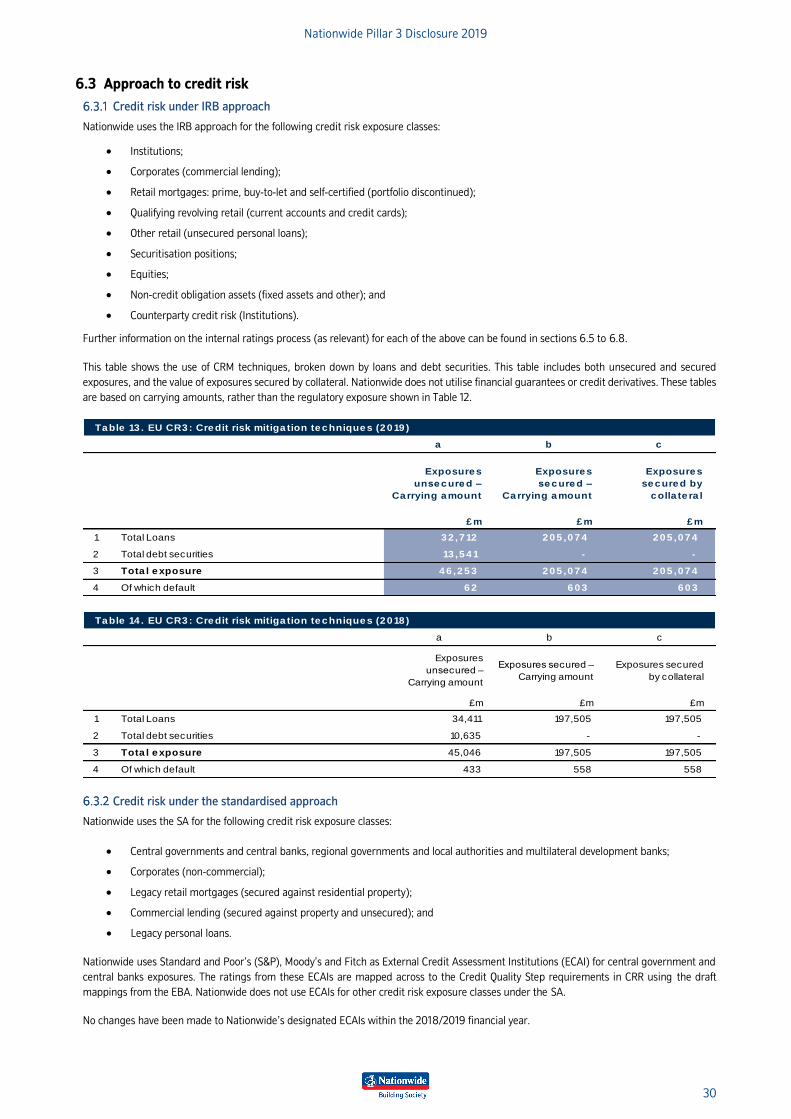

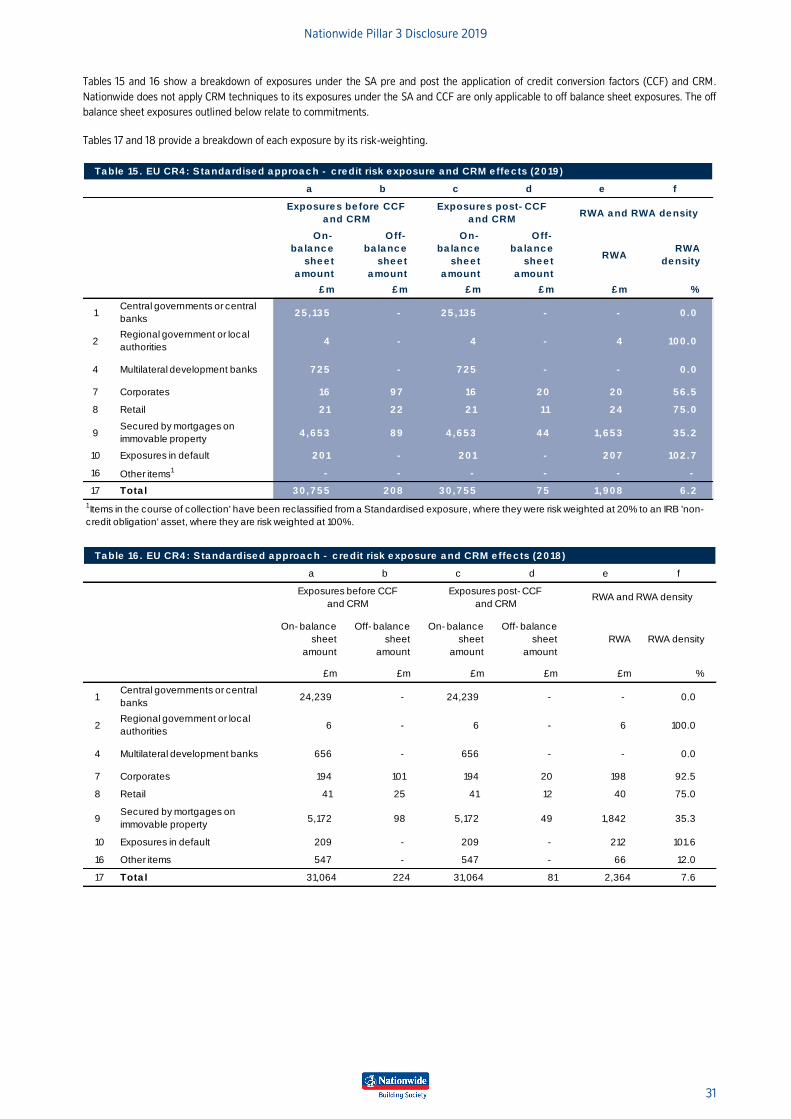

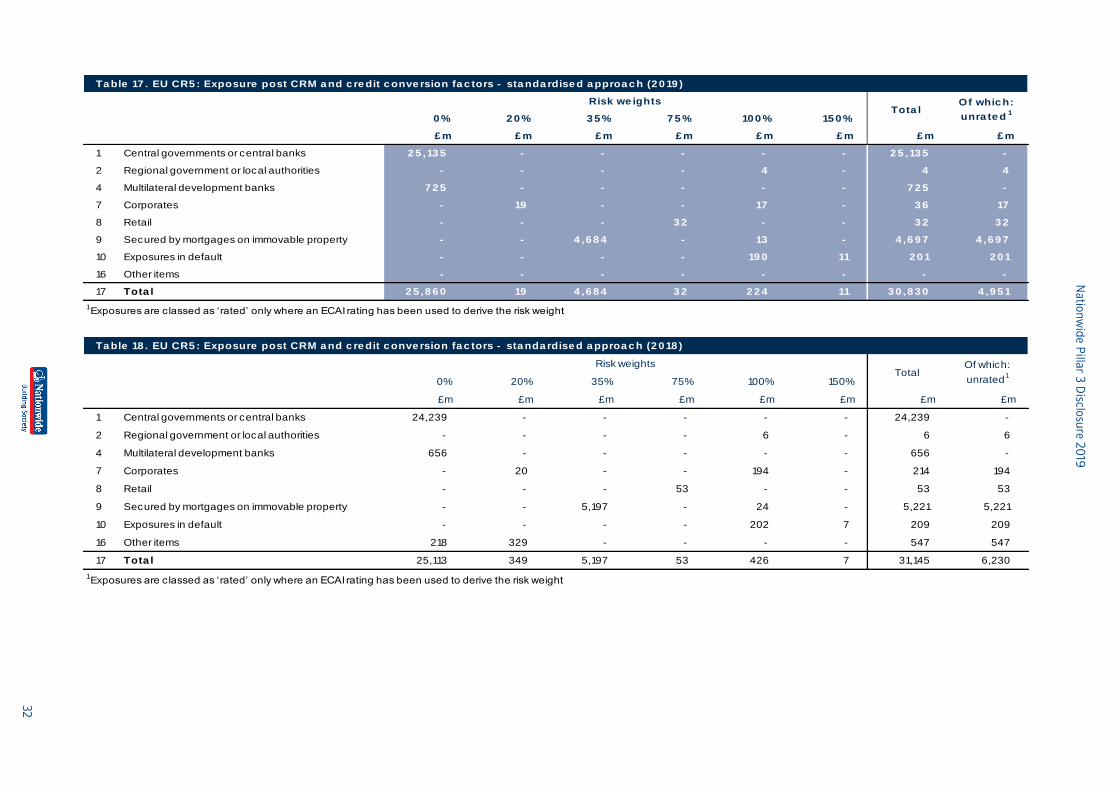

6.3 Approach to credit risk ............................................................................................................................................... 30

Credit risk under IRB approach ...................................................................................................................................... 30

Credit risk under the standardised approach ............................................................................................................... 30

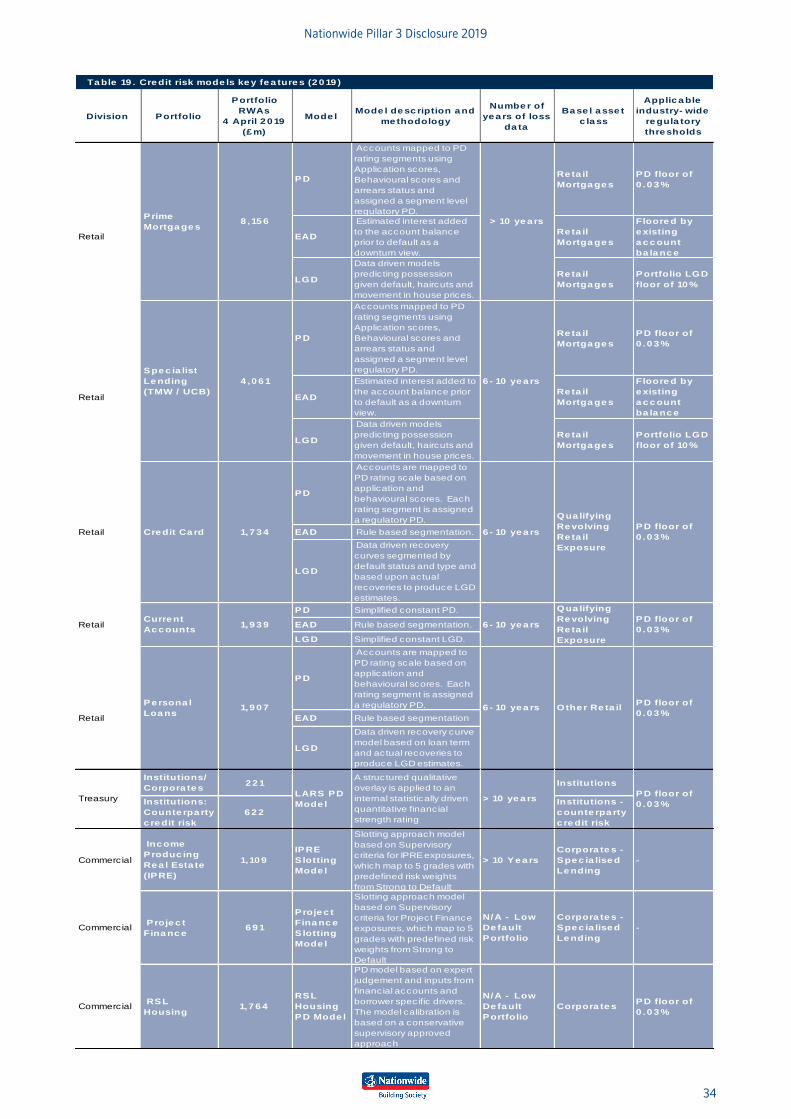

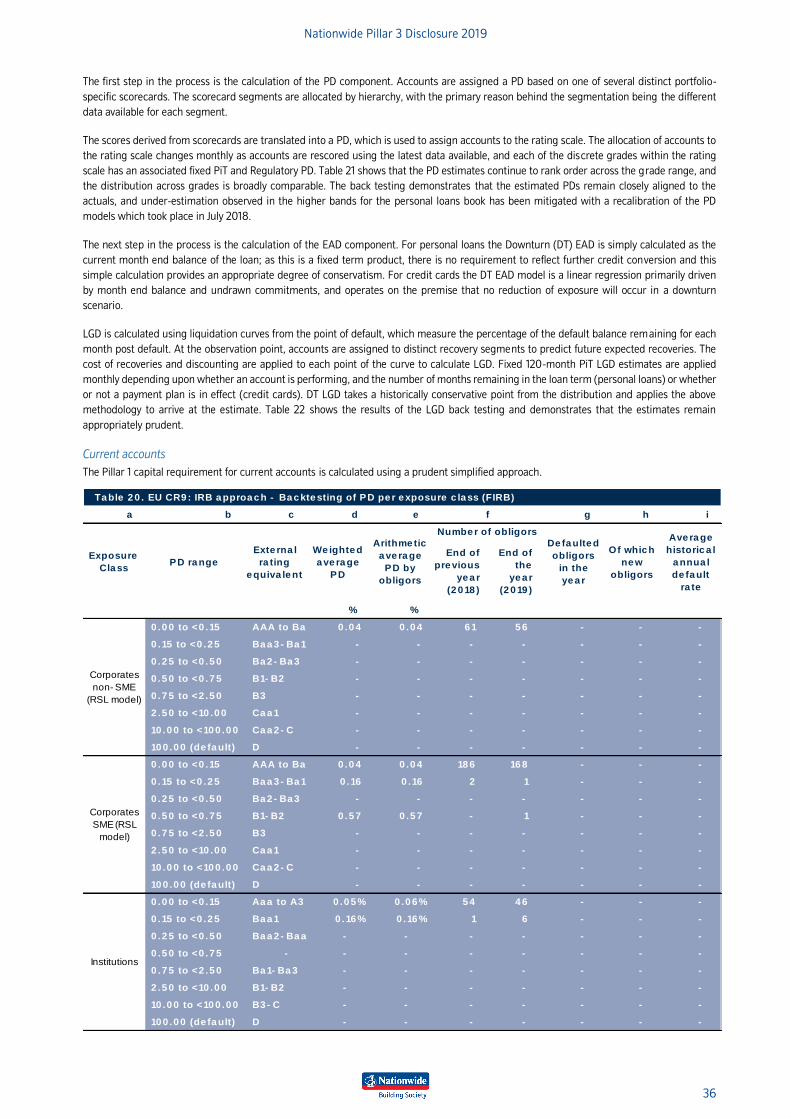

6.4 IRB models .................................................................................................................................................................. 33

IRB models overview ....................................................................................................................................................... 33

Model risk management of IRB risk ratings systems ................................................................................................... 33

IRB credit risk model performance ................................................................................................................................. 35

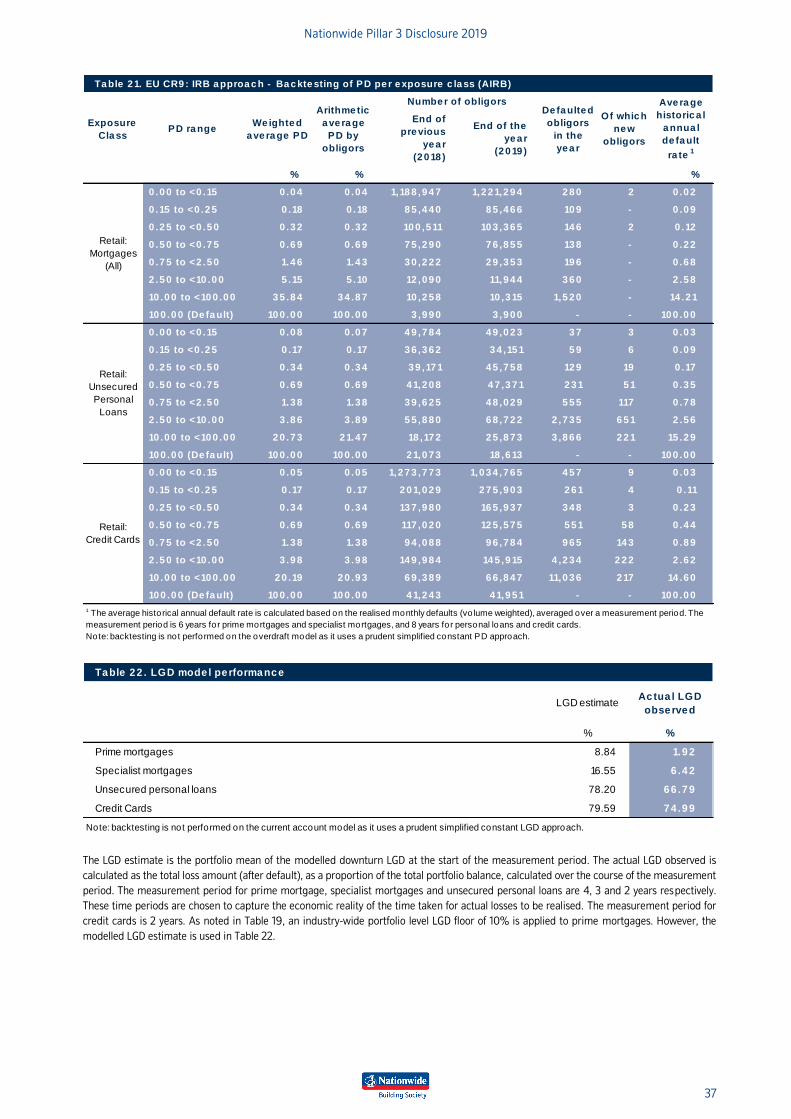

6.5 Retail credit risk ........................................................................................................................................................... 41

Management of retail credit risks................................................................................................................................... 41

Credit risk concentration ................................................................................................................................................. 41

Credit risk mitigation ....................................................................................................................................................... 41

6.6 Commercial credit risk ................................................................................................................................................ 41

Overview ........................................................................................................................................................................... 41

Credit risk concentration ................................................................................................................................................. 47

Credit risk mitigation ....................................................................................................................................................... 47

6.7 Treasury credit risk ..................................................................................................................................................... 47

Introduction ...................................................................................................................................................................... 47

Credit risk concentration .................................................................................................................................................. 51

Credit risk mitigation ........................................................................................................................................................ 51

6.8 Equities ......................................................................................................................................................................... 51

6.9 Impairment of financial assets held at amortised cost or FVOCI .............................................................................. 51

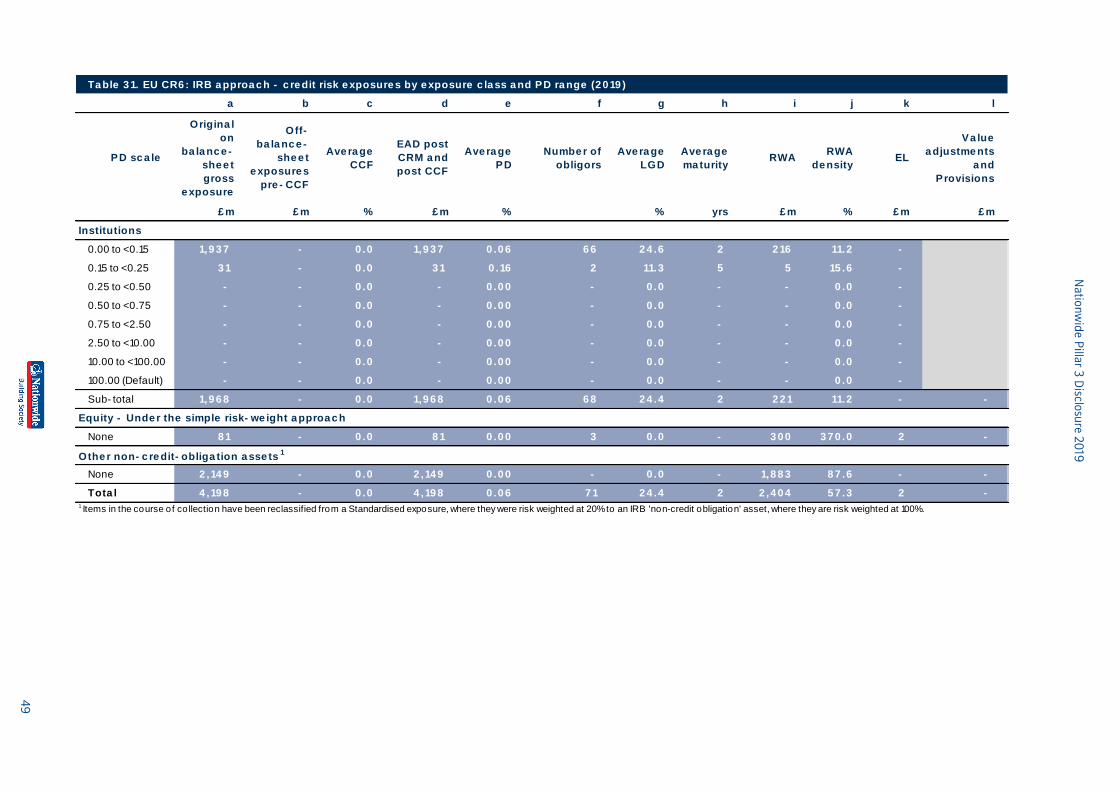

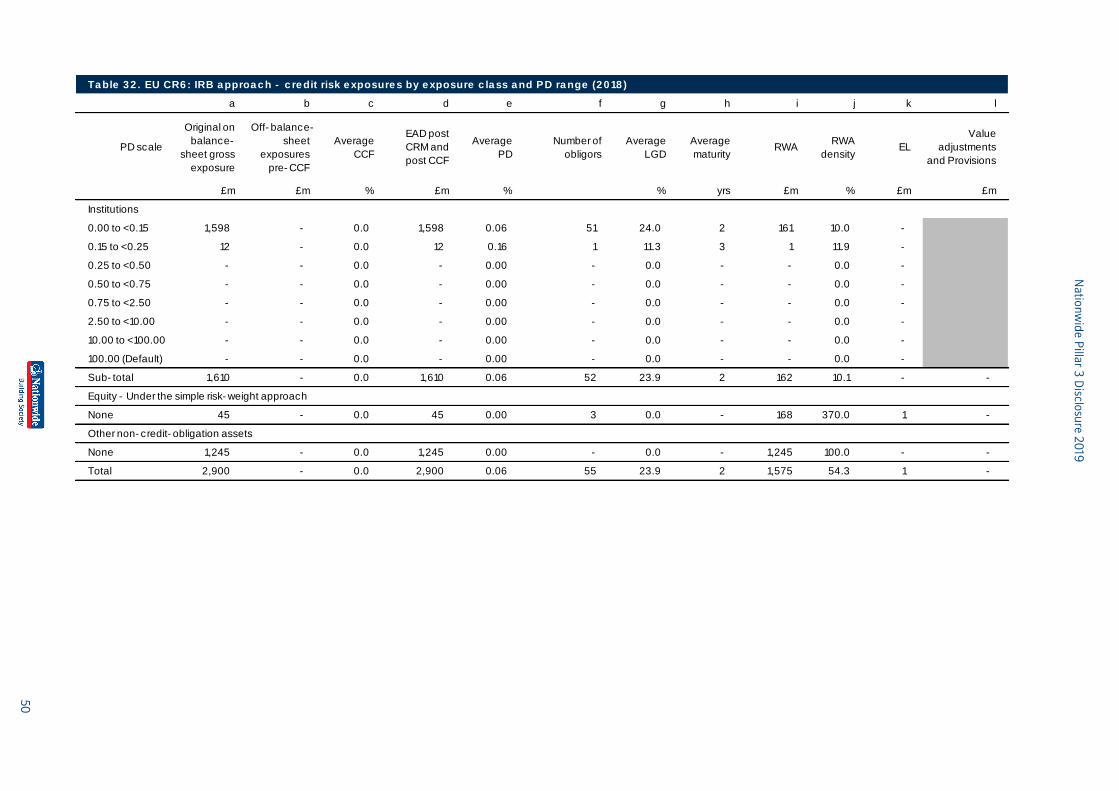

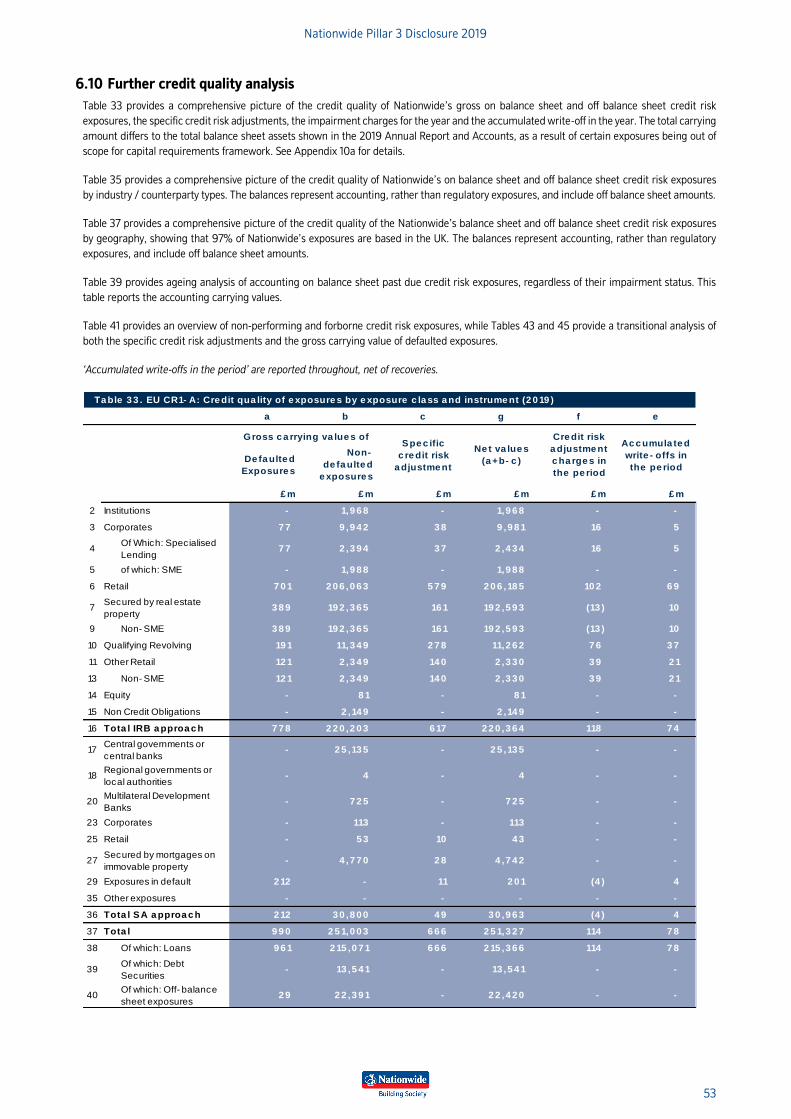

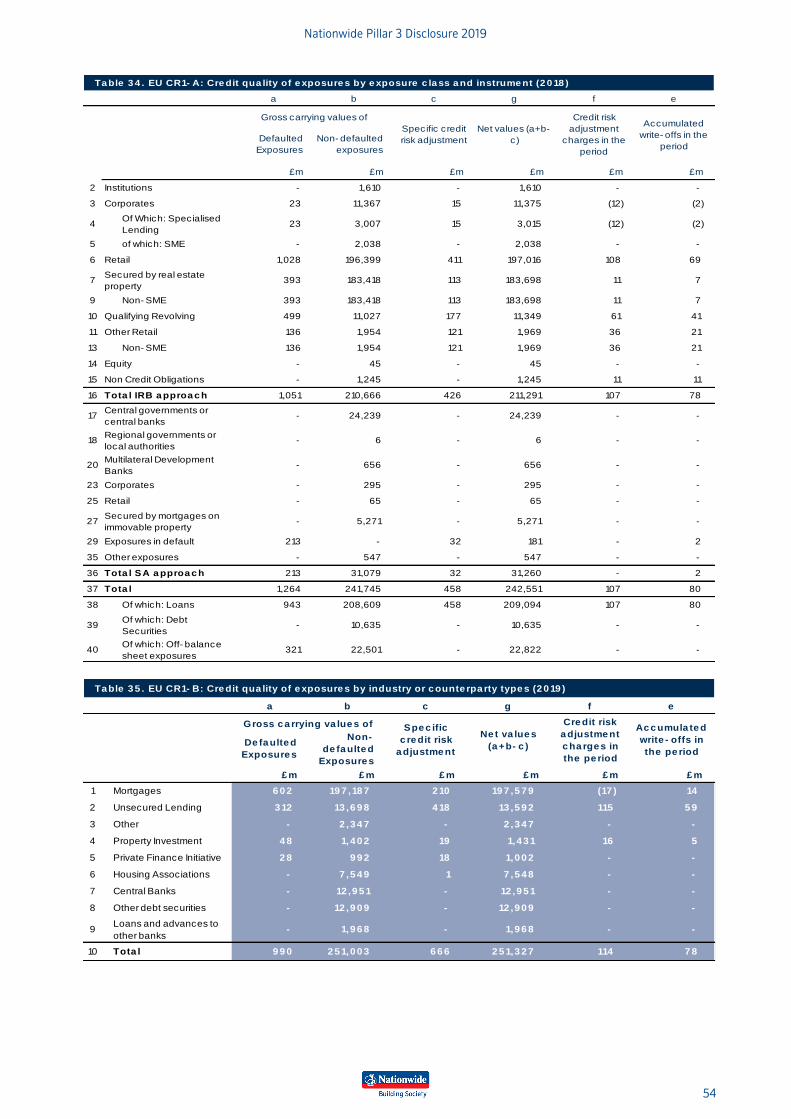

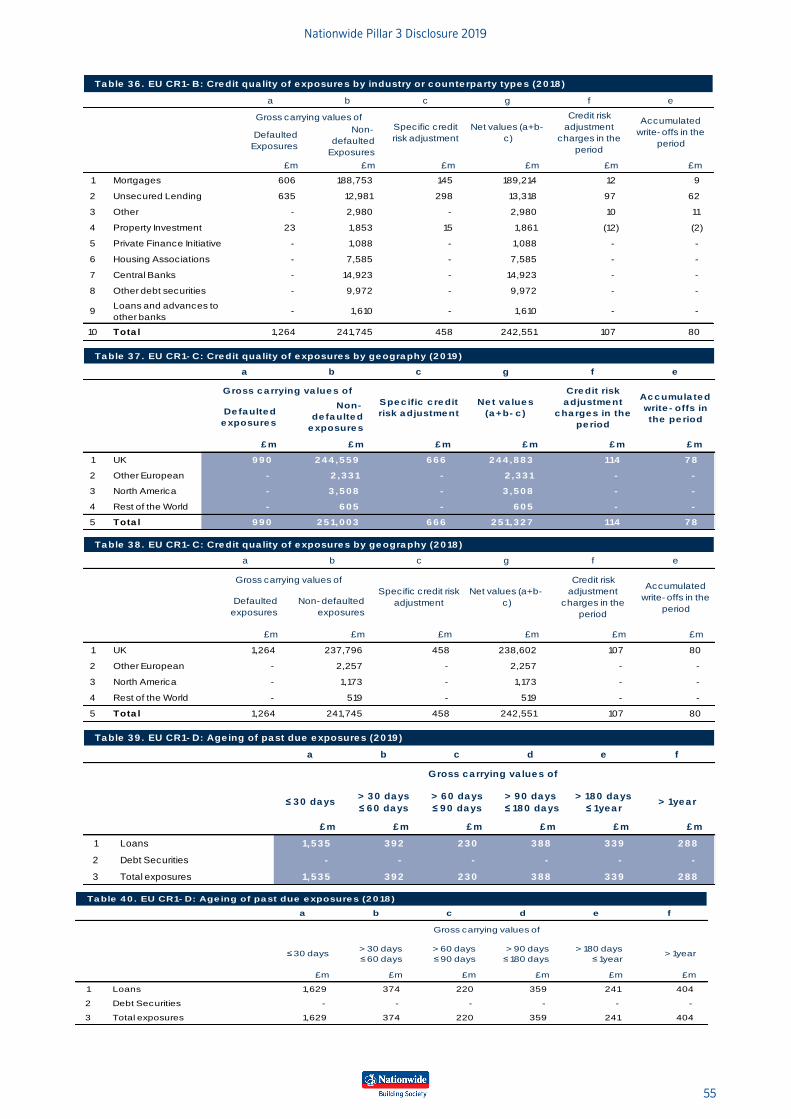

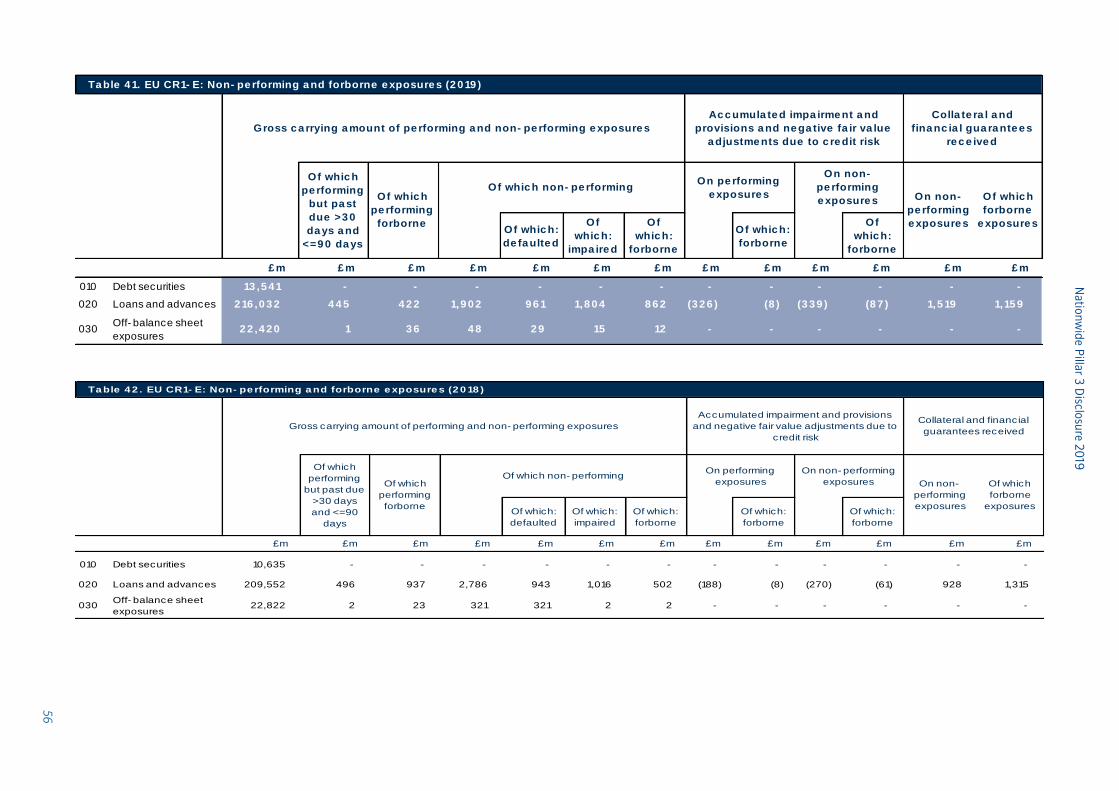

6.10 Further credit quality analysis ................................................................................................................................... 53

7 Counterparty credit risk .............................................................................................................. 58

8 Securitisations .............................................................................................................................. 62

9 Operational risk ............................................................................................................................ 65

9.1 Operational risk profile ............................................................................................................................................... 65

9.2 Operational risk framework........................................................................................................................................ 65

9.3 Operational risk governance ...................................................................................................................................... 65

9.4 Risk measurement ...................................................................................................................................................... 65

10 Market Risk ................................................................................................................................... 66

Nationwide Pillar 3 Disclosure 2019

4

10.1 Introduction ................................................................................................................................................................. 66

10.2 Market risk management ........................................................................................................................................... 66

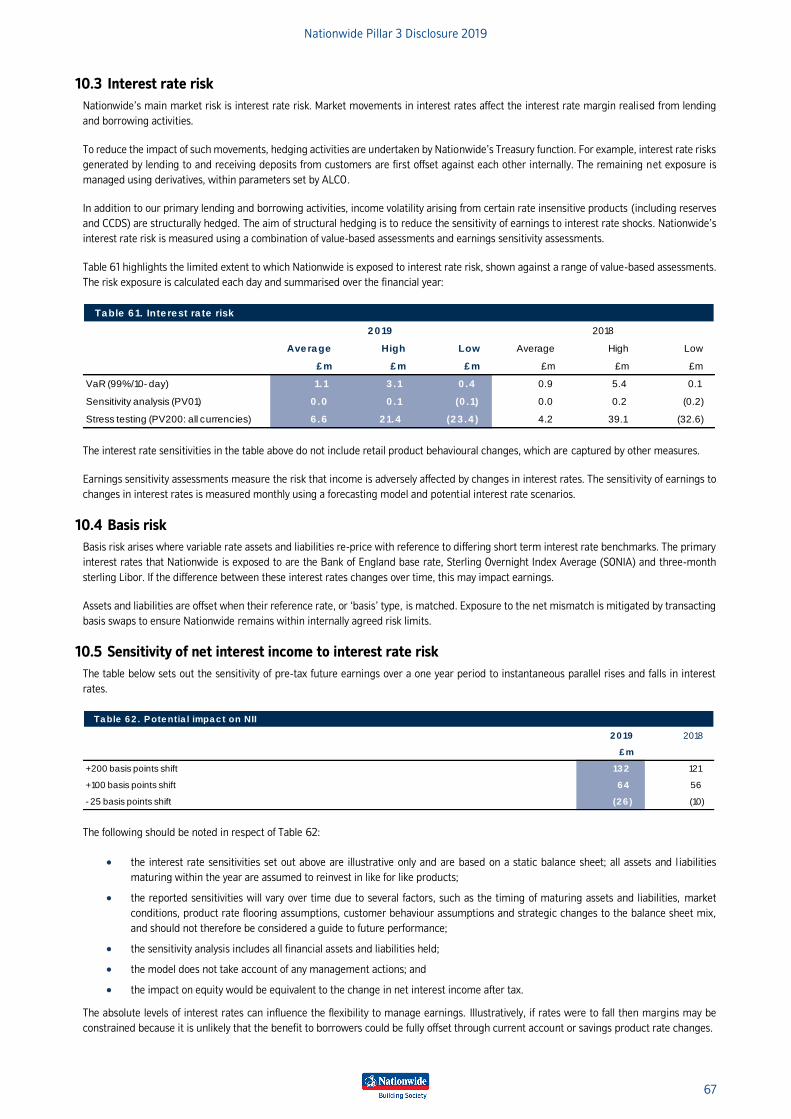

10.3 Interest rate risk ......................................................................................................................................................... 67

10.4 Basis risk ...................................................................................................................................................................... 67

10.5 Sensitivity of net interest income to interest rate risk ............................................................................................. 67

10.6 Other market risks ...................................................................................................................................................... 68

11 Other principal risks .................................................................................................................... 69

11.1 Business risk ................................................................................................................................................................ 69

11.2 Conduct and compliance risk ..................................................................................................................................... 69

11.3 Liquidity and funding risk ........................................................................................................................................... 69

11.4 Pension risk .................................................................................................................................................................. 71

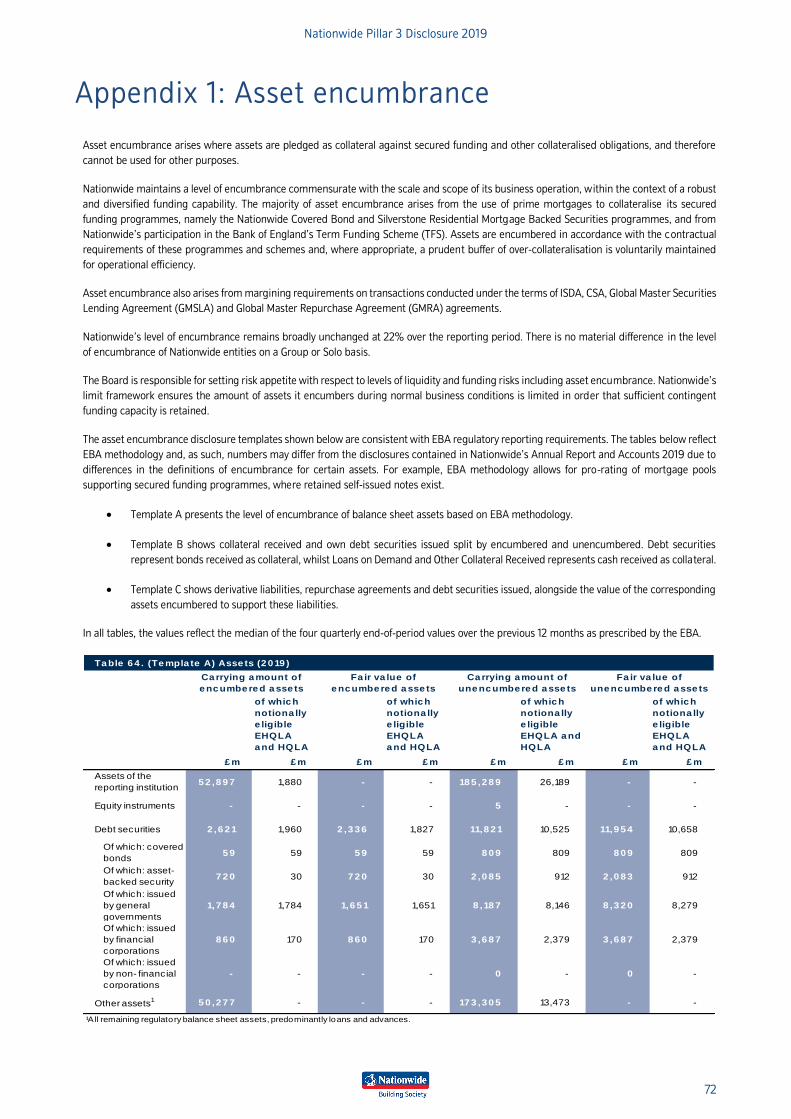

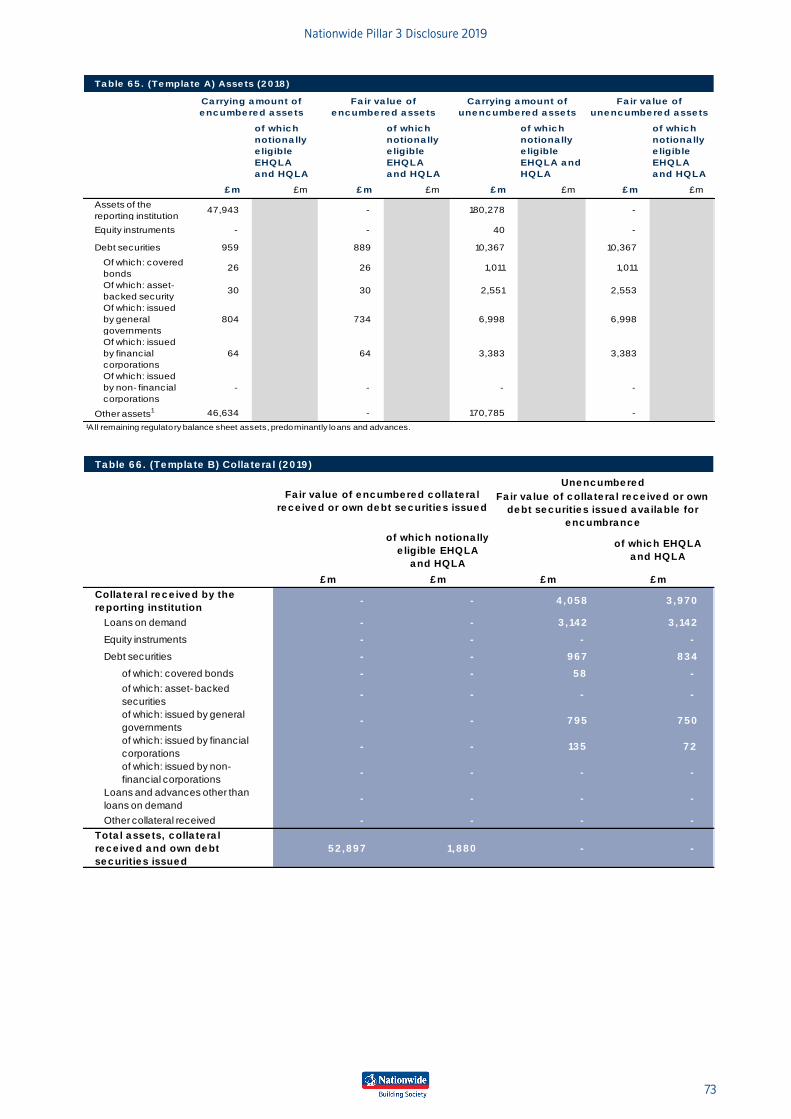

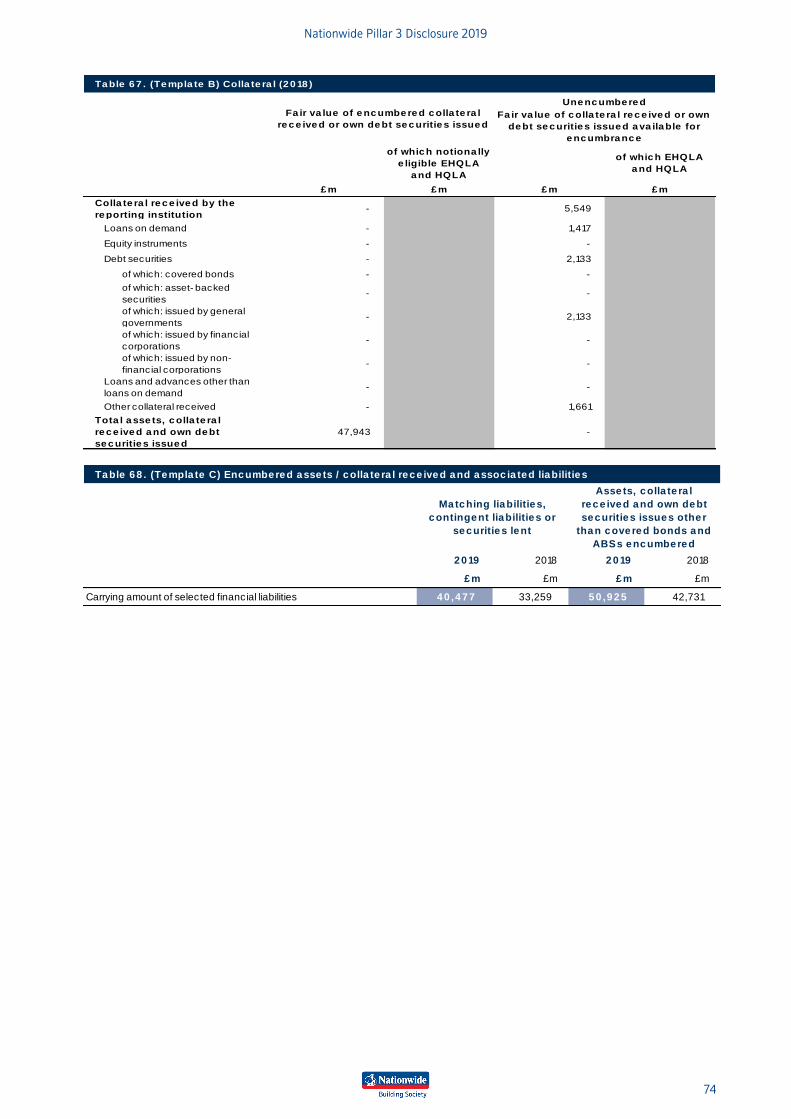

Appendix 1: Asset encumbrance ......................................................................................................... 72

Appendix 2: Remuneration ................................................................................................................. 75

Appendix 3: EBA own funds disclosure template ............................................................................... 81

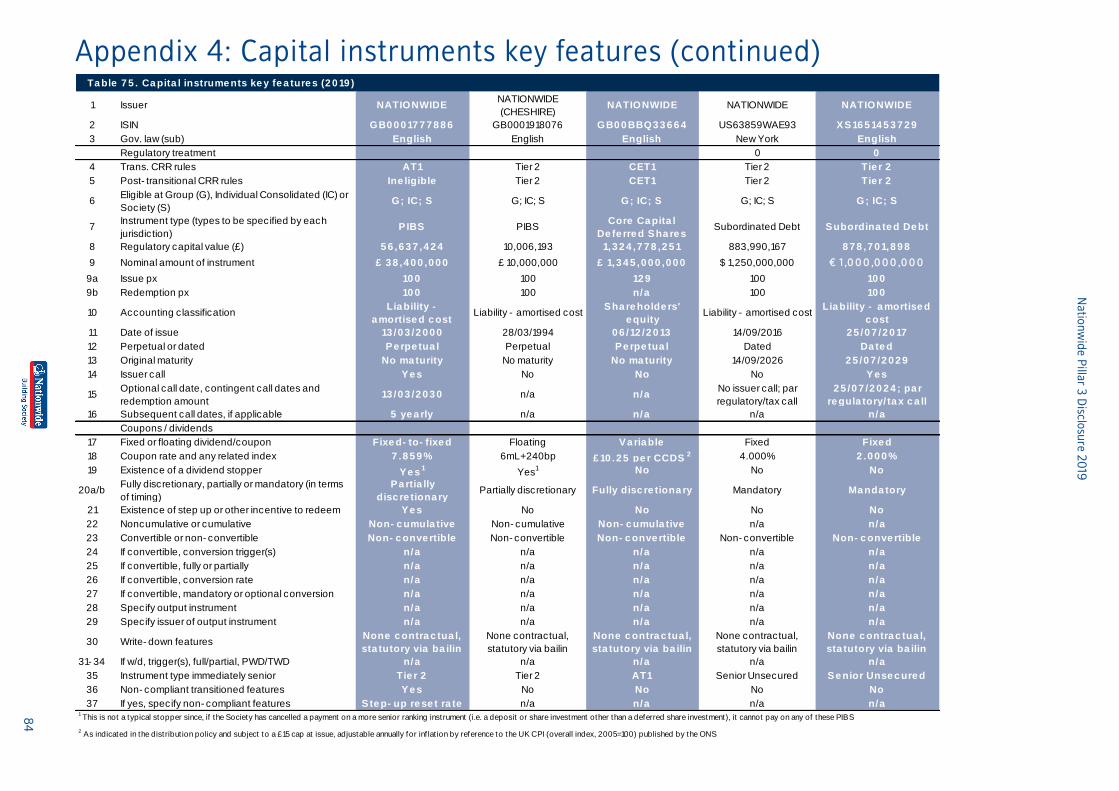

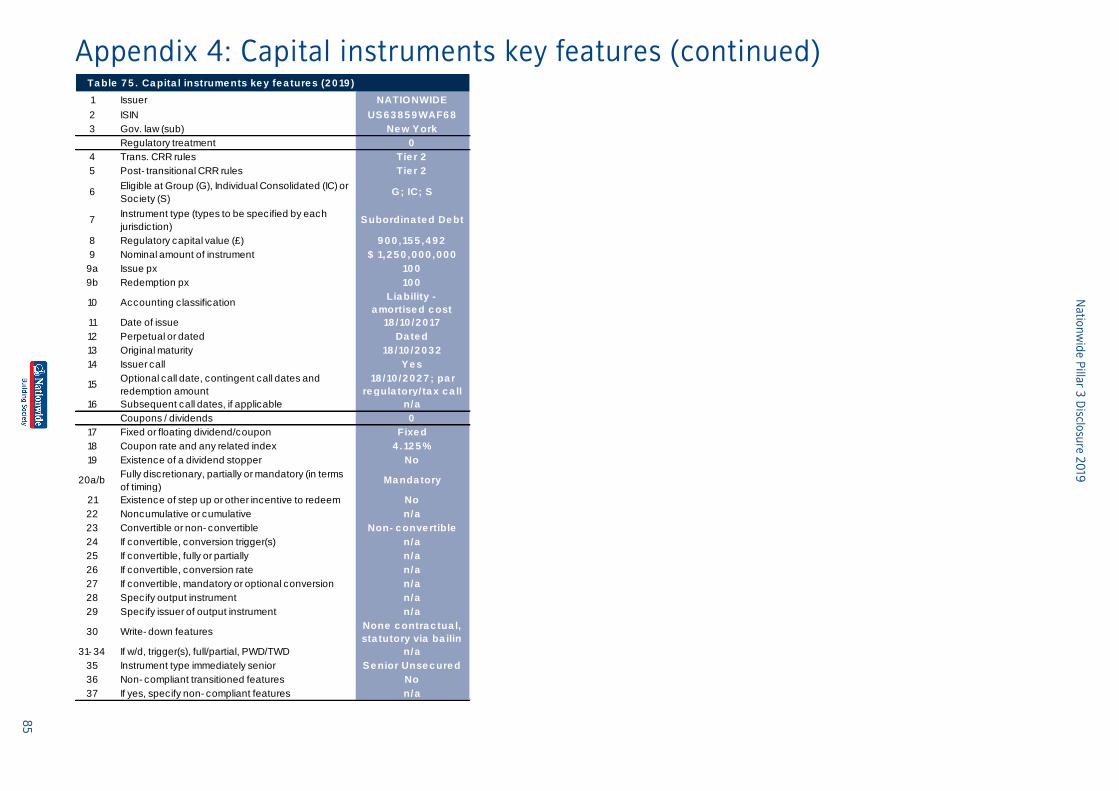

Appendix 4: Capital instruments key features ................................................................................... 83

Appendix 5: EAD, RWAs and requirements by exposure class and approach ................................. 86

Appendix 6a: Geographical breakdown of exposures (2019) ........................................................... 87

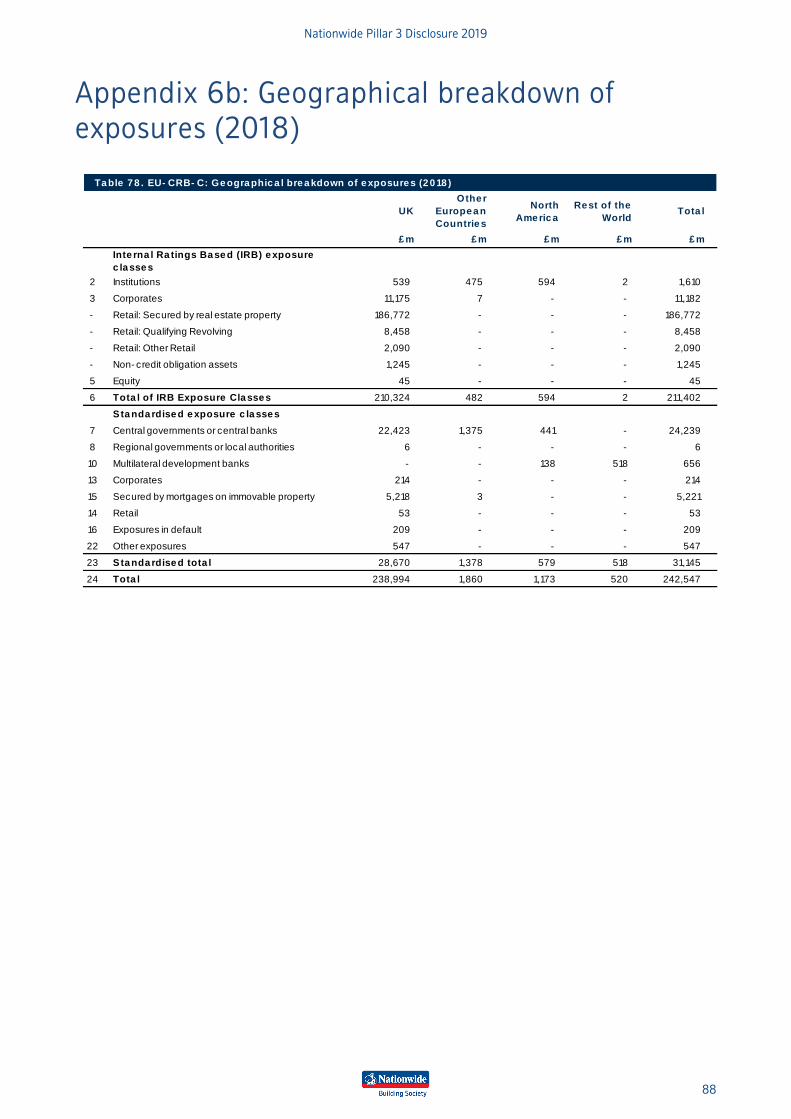

Appendix 6b: Geographical breakdown of exposures (2018) ........................................................... 88

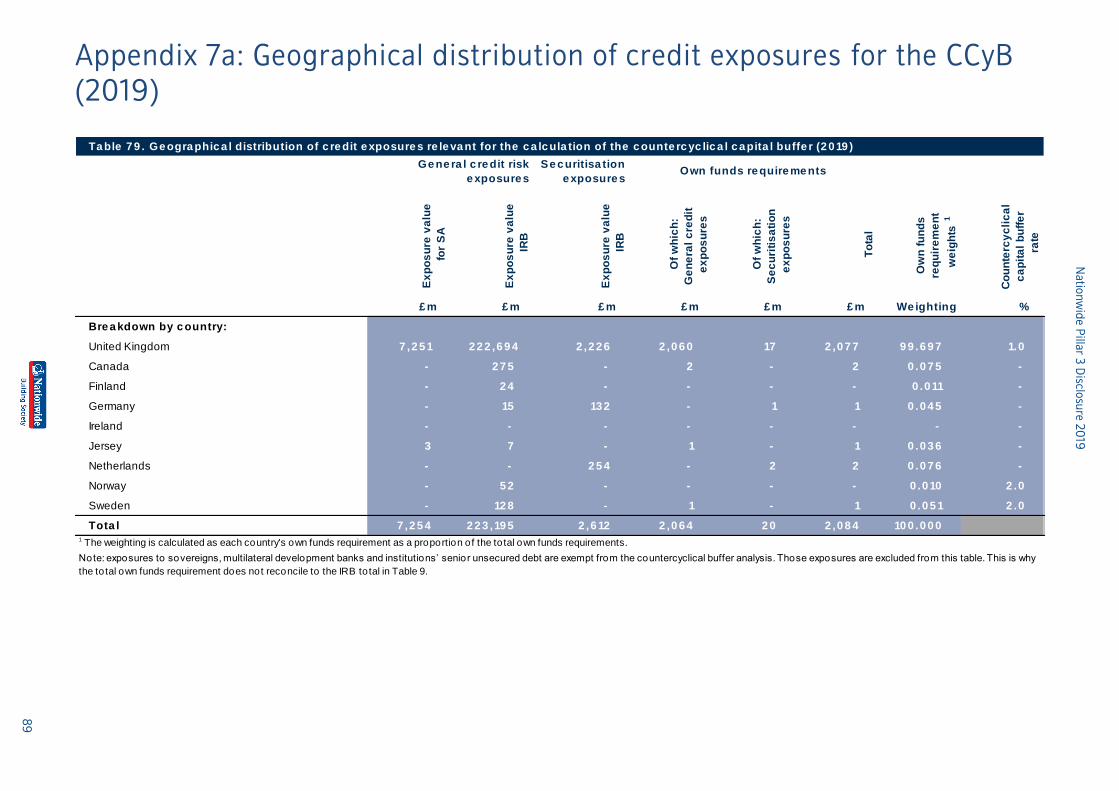

Appendix 7a: Geographical distribution of credit exposures for the CCyB (2019) .......................... 89

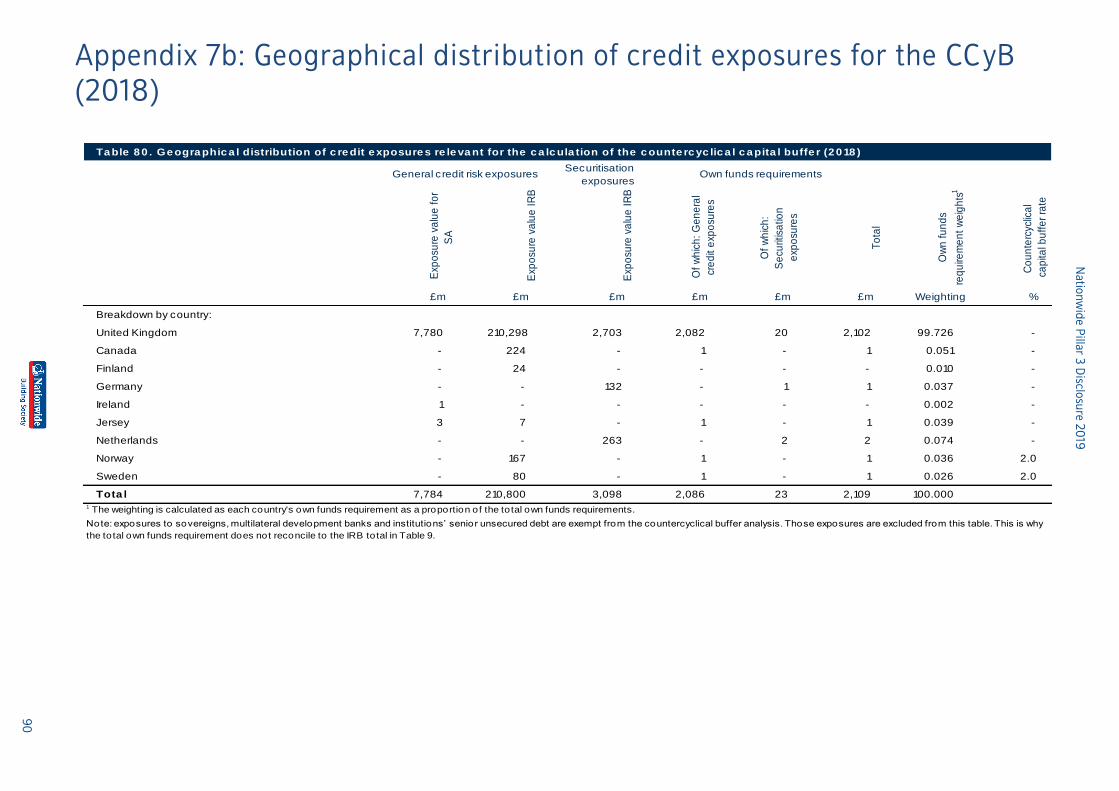

Appendix 7b: Geographical distribution of credit exposures for the CCyB (2018) .......................... 90

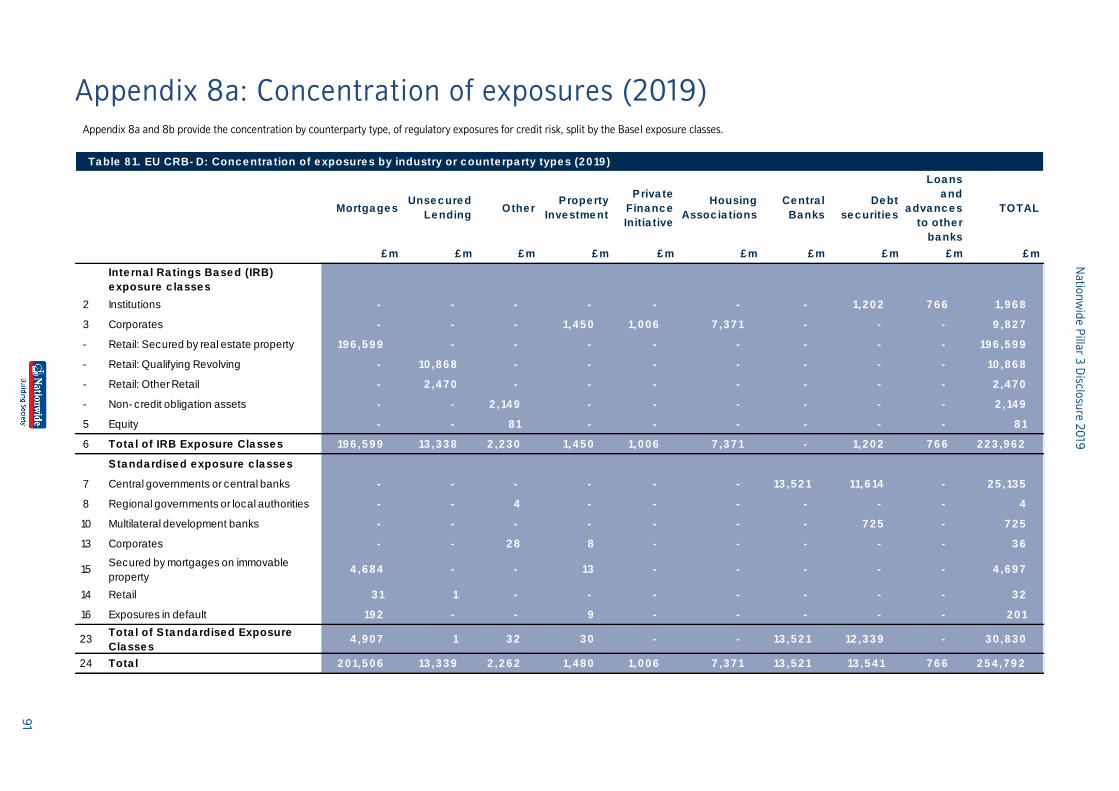

Appendix 8a: Concentration of exposures (2019) .............................................................................. 91

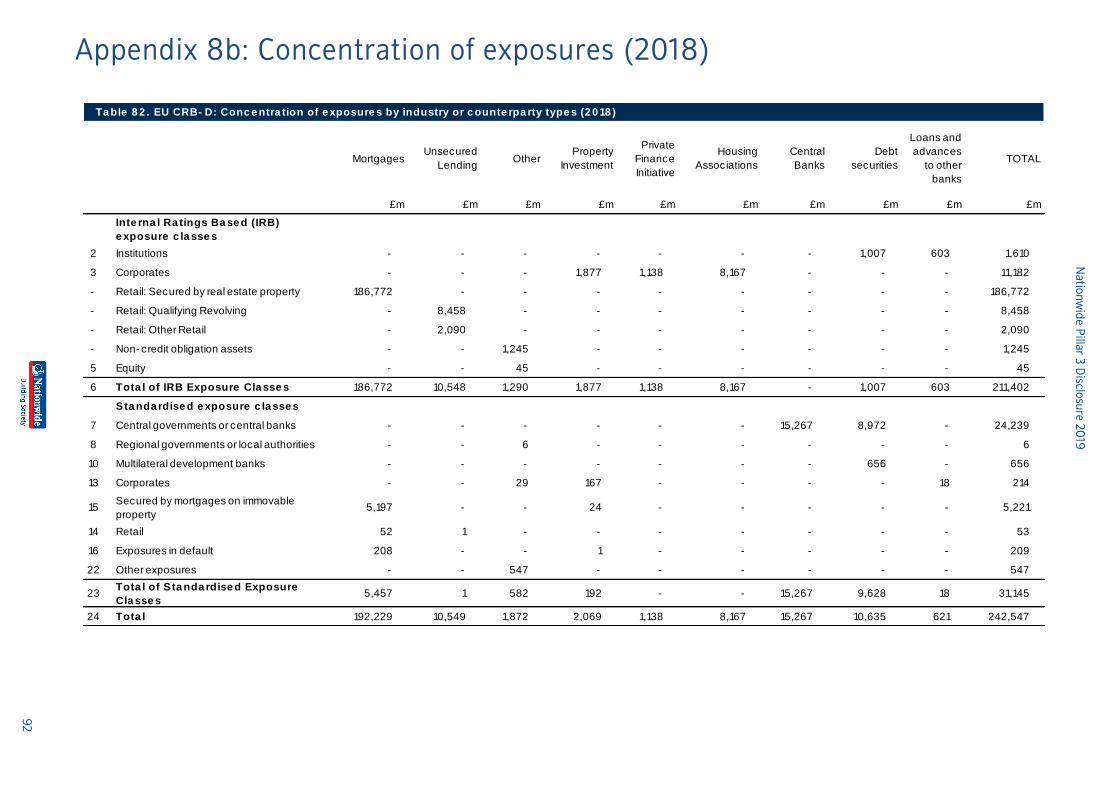

Appendix 8b: Concentration of exposures (2018) ............................................................................. 92

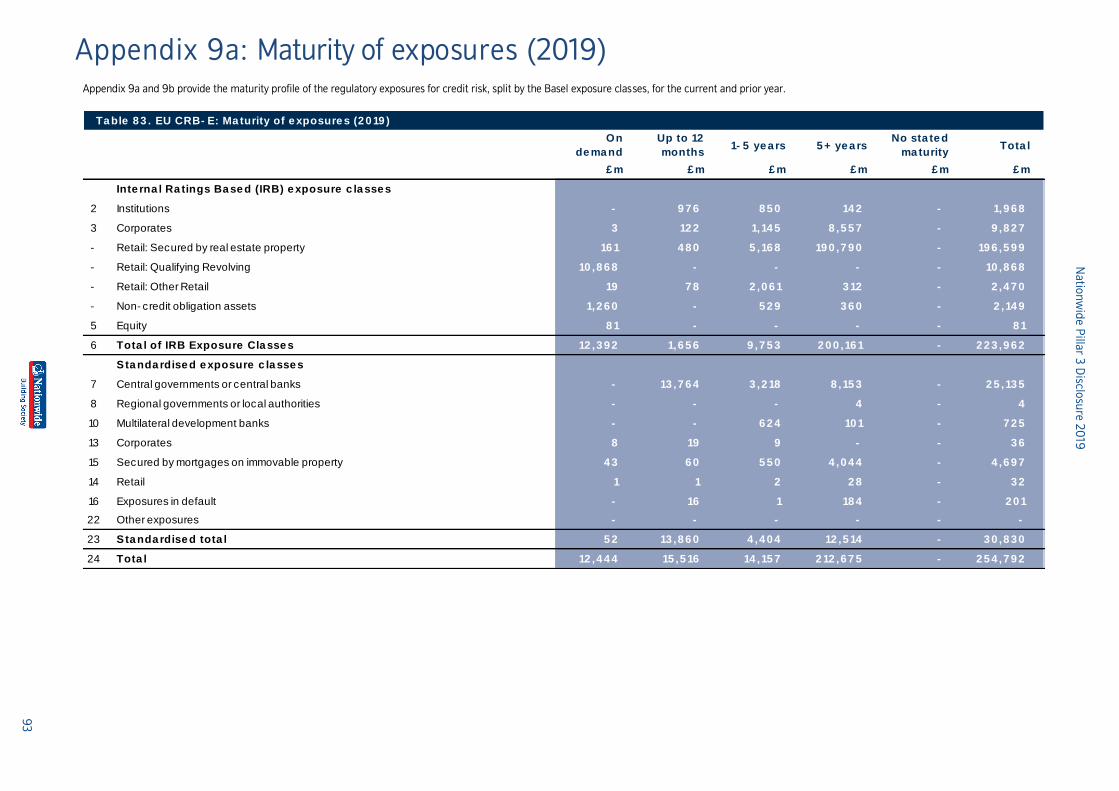

Appendix 9a: Maturity of exposures (2019) ......................................................................................... 93

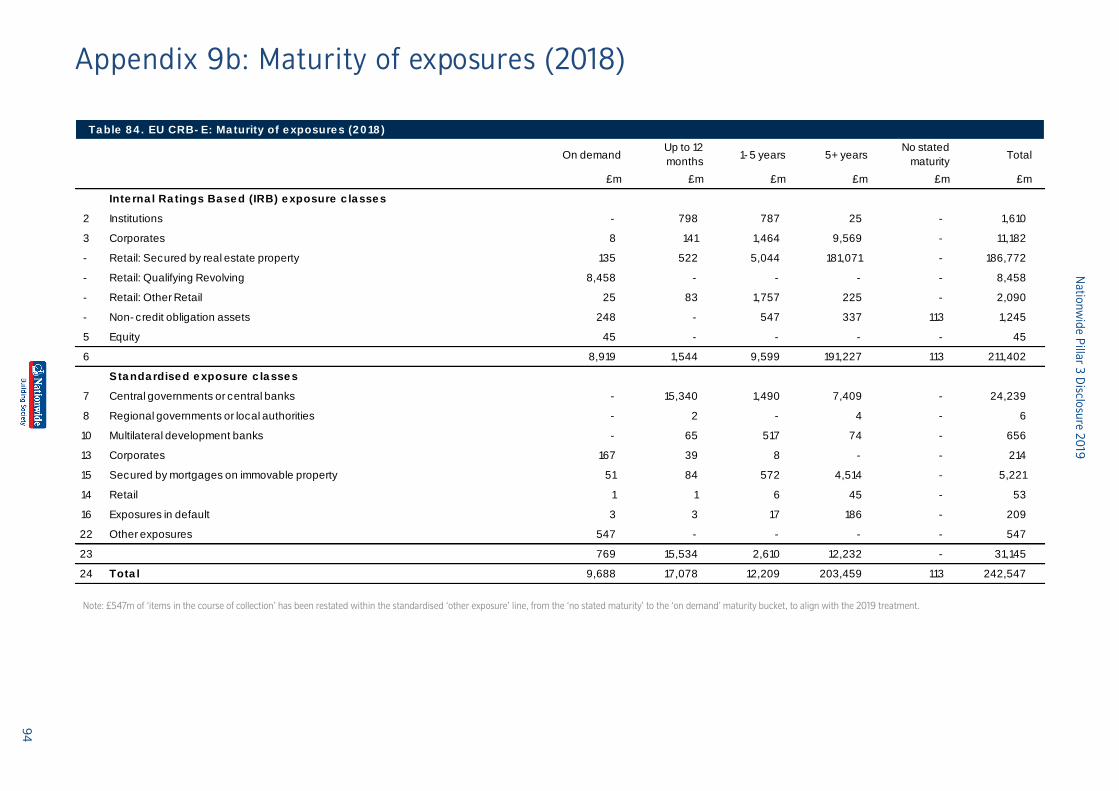

Appendix 9b: Maturity of exposures (2018) ....................................................................................... 94

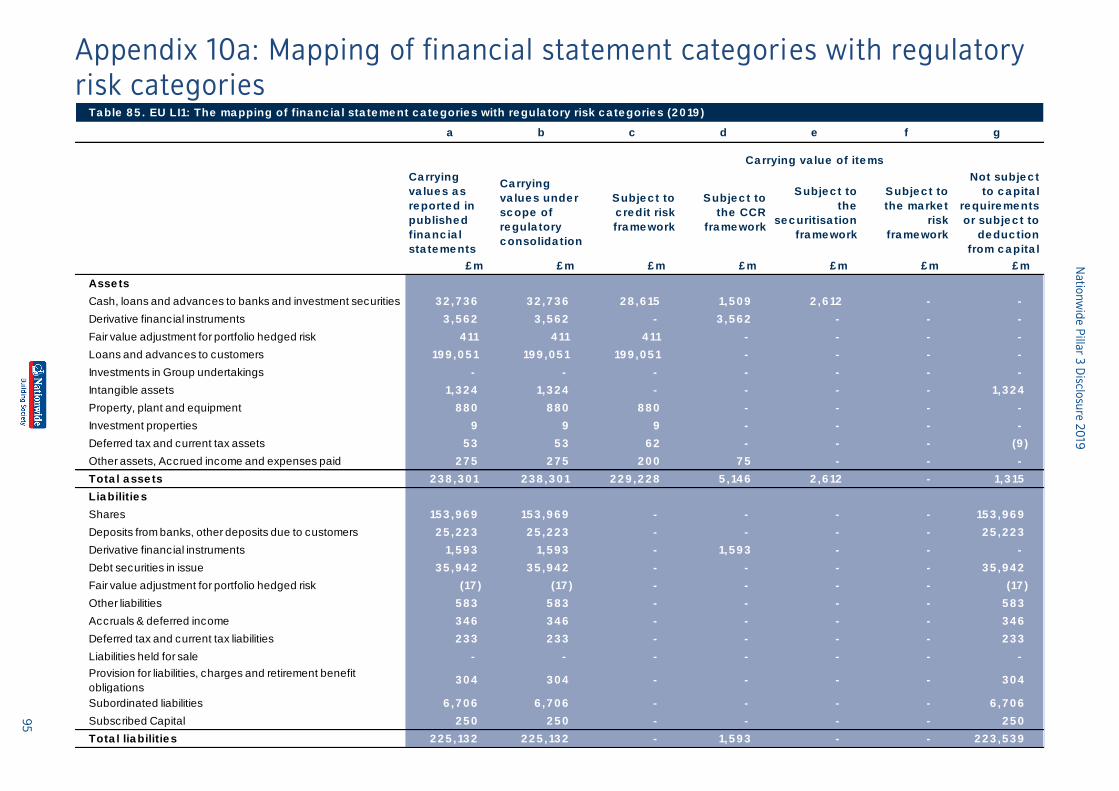

Appendix 10a: Mapping of financial statement categories with regulatory risk categories ........... 95

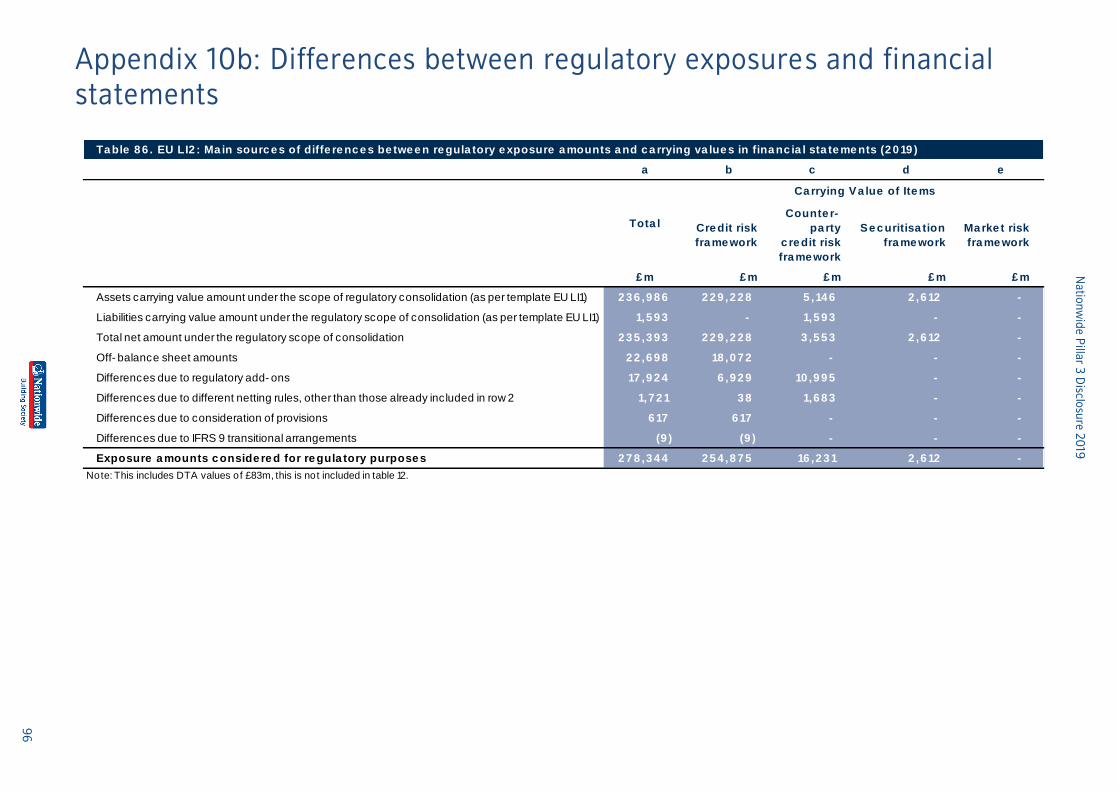

Appendix 10b: Differences between regulatory exposures and financial statements ..................... 96

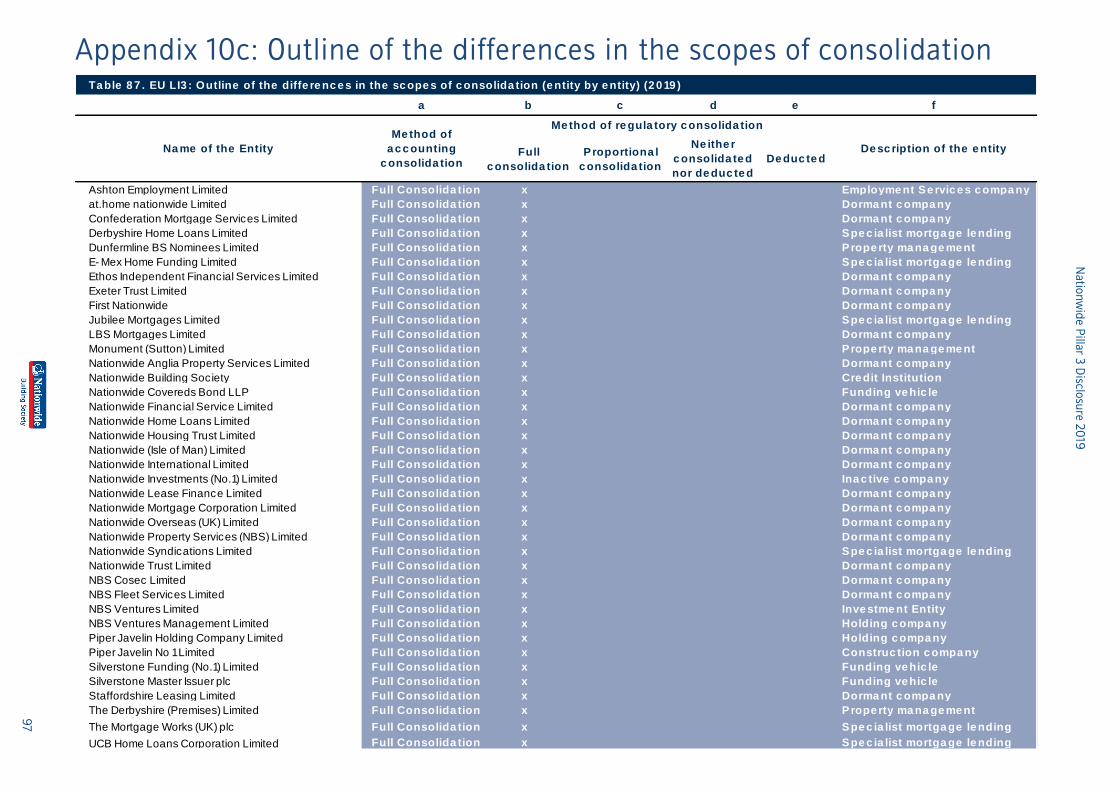

Appendix 10c: Outline of the differences in the scopes of consolidation ........................................ 97

Appendix 11: Compliance appendix .................................................................................................... 98

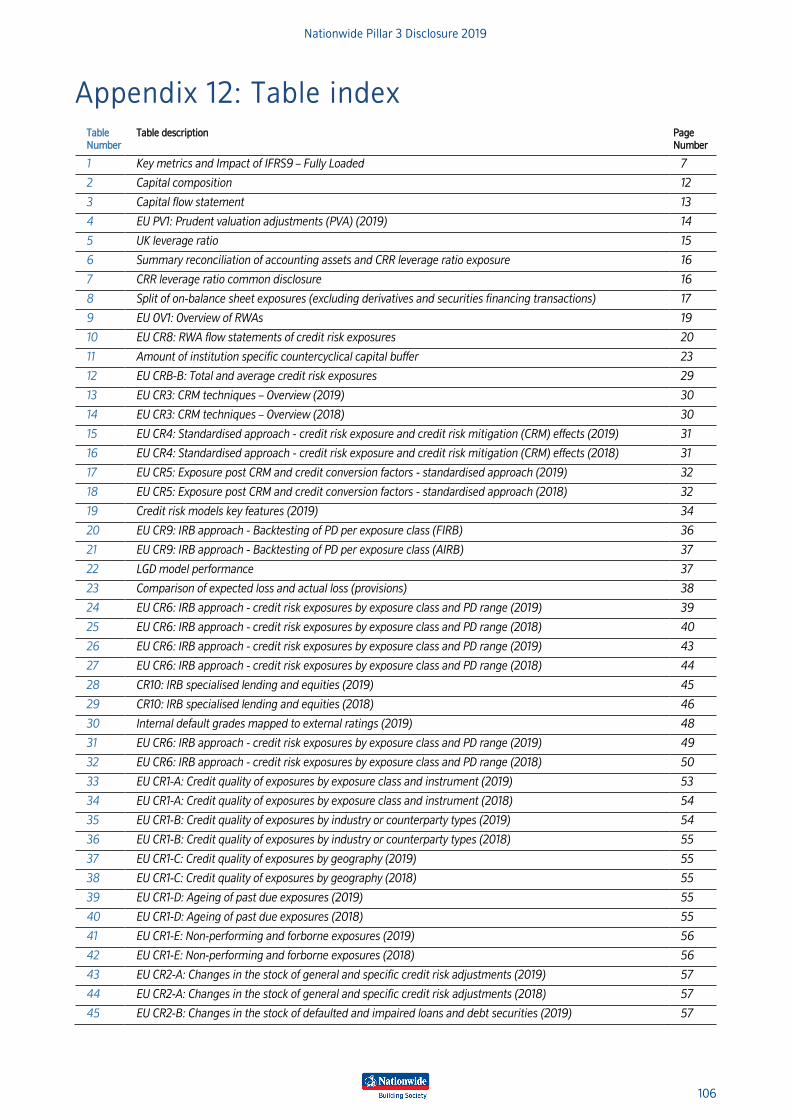

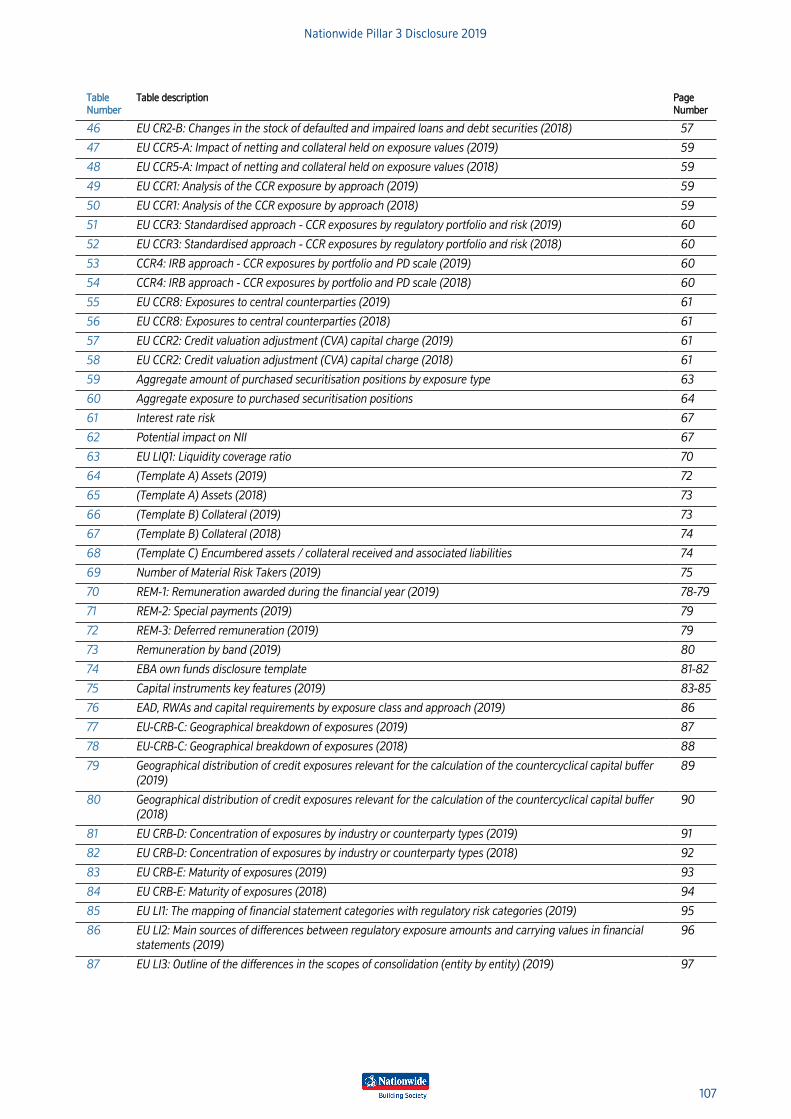

Appendix 12: Table index .................................................................................................................. 106

Glossary .............................................................................................................................................. 108

Abbreviations ...................................................................................................................................... 114

Nationwide Pillar 3 Disclosure 2019

5

Contacts

Sara Batchelor – Media Relations

T: 01793 657770

Alexander Wall – Treasury Investor Relations

T: 0207 2616568

Certain statements in this document are forward looking with respect to plans, goals and expectations relating to the future financial position,

business performance and results of Nationwide. Although Nationwide believes that the expectations reflected in these forward looking statements

are reasonable, Nationwide can give no assurance that these expectations will prove to be an accurate reflection of actual results. By their nature,

all forward looking statements involve risk and uncertainty because they relate to future events and circumstances that are beyond the control of

Nationwide including, amongst other things, UK domestic and global economic and business conditions, market related risks such as fluctuation

in interest rates and exchange rates, inflation/deflation, the impact of competition, changes in customer preferences, risks concerning borrower

credit quality, delays in implementing proposals, the timing, impact and other uncertainties of future acquisitions or other combinations within

relevant industries, the policies and actions of regulatory authorities, the impact of tax or other legislation and other regulations in the jurisdictions

in which Nationwide operates. The economic outlook also remains unusually uncertain due to Brexit. As a result, Nationwide’s actual future

financial condition, business performance and results may differ materially from the plans, goals and expectations expressed or implied in these

forward-looking statements. Due to such risks and uncertainties Nationwide cautions readers not to place undue reliance on such forward-looking

statements.

Nationwide undertakes no obligation to update any forward-looking statements whether as a result of new information, future events or otherwise.

This document does not constitute or form part of an offer of securities for sale in the United States. Securities may not be offered or sold in the

United States absent registration or an exemption from registration. Any public offering to be made in the United States will be made by means

of a prospectus that may be obtained from Nationwide and will contain detailed information about Nationwide and management as well as

financial statements.

Nationwide Pillar 3 Disclosure 2019

6

1 Executive Summary 1.1 Introduction

Our building society was founded 135 years ago to help people save and buy homes of their own. We were driven by our social purpose, and

our focus on building society is as important to us today as it was then.

We do many of the things that banks do, but we’re owned by, and run for, our members: people who have their mortgages, savings or current

accounts with us. And we measure our success through the things that matter to them: service, value and financial strength.

We need to be profitable to make sure that Nationwide and our members’ money are safe and secure, but – as a building society – we don’t

need to pursue profits to pay ever higher dividends or put shareholders’ needs above those of our members.

This document provides a detailed view of Nationwide’s capital resources, the components of solvency risk and the risk management strategy.

Nationwide targets strong capital ratios relative to regulatory requirements, helping to ensure that Nationwide is built to last.

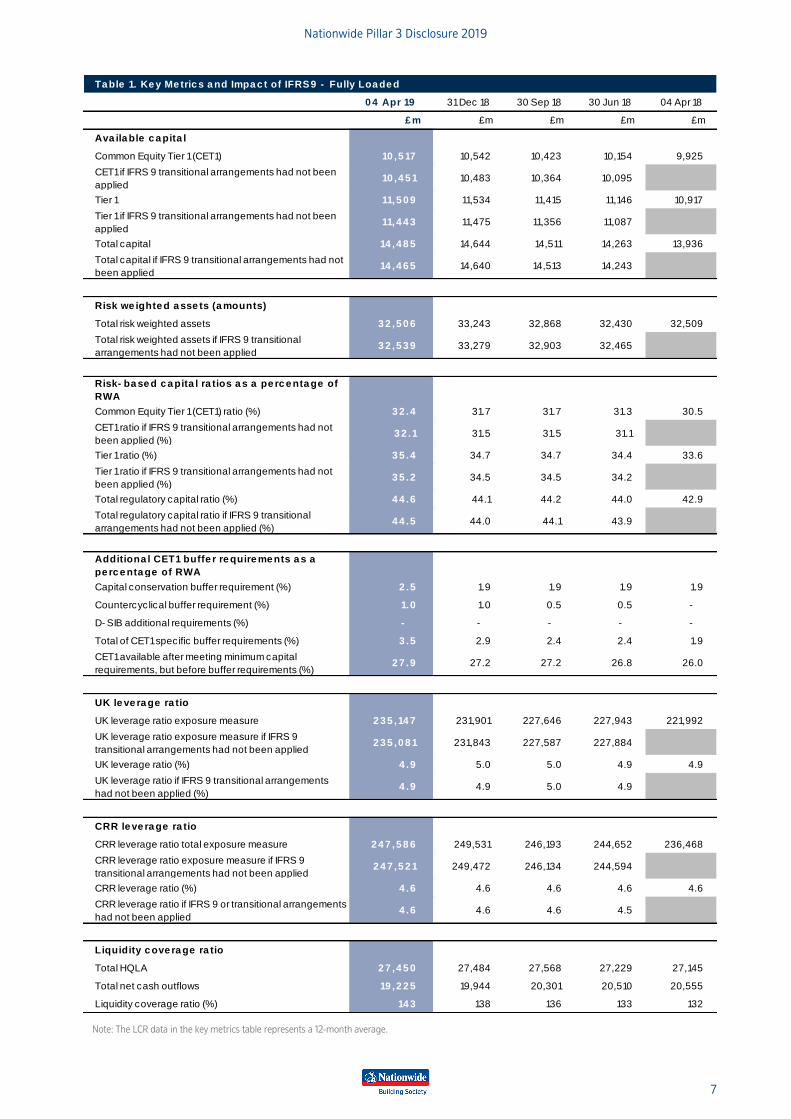

1.2 Summary of key metrics

The capital disclosures included in this report are on a Capital Requirements Directive IV (CRD IV) end-point basis, unless otherwise stated.

This assumes that all CRD IV requirements are in force during the period, with no CRD IV transitional provisions permitted1. The disclosures

are on a consolidated Group basis, including all subsidiary entities, unless otherwise stated.

Our capital position has strengthened during the period with our CET1 ratio increasing to 32.4% (2018: 30.5%) whilst our UK leverage ratio

remained stable at 4.9% (2018: 4.9%). Both ratios remain in excess of the regulatory capital requirements of 13.2% and 4.0% respectively,

which include the incumbent CRD IV buffers and the updated systemic risk buffer (SRB) that is applicable from August 20192.

CET1 capital resources have increased over the year by £0.6 billion, mainly due to profit after tax for the period of £0.6 billion. Risk weighted

assets (RWAs) remained stable, with increased retail lending and treasury related RWAs offset by run-off in the commercial book and legacy

mortgage portfolios, and the implementation of a new credit card Internal Ratings Based (IRB) model.

The UK leverage ratio remained stable at 4.9% (2018: 4.9%), with an increase in Tier 1 capital driven by profits after tax of £0.6 billion offset

by an increase in UK leverage exposure of £13 billion. The increased leverage exposure was driven by increased net retail lending of £9 billion,

increased treasury exposures (including counterparty credit risk) of £5 billion, increase in other assets of £1 billion, offset by run-off in the

commercial book of £2 billion. On 24 April 2019, Nationwide notified investors of its intention to redeem its outstanding AT1 capital instrument

in full, on 20 June 2019. This will reduce Tier 1 capital resources by £992m, resulting in a 0.4% reduction in the UK leverage ratio, to 4.5%,

based on the year-end balance sheet. The redemption will have no impact on the CET1 ratio.

The total regulatory capital ratio has increased to 44.6% (2018: 42.9%), driven primarily by the additional CET1 resources outlined above.

There has been no issuance or redemption of any capital instruments during the year.

Nationwide has submitted its new hybrid IRB mortgage models to the Prudential Regulatory Authority (PRA) for approval with the expectations

that these will be implemented during 2020, in line with the deadline set out in PS13/17. Our current estimate is that the impact of these

models will be to reduce our reported CET1 ratio by around a third, given the material increase in RWAs, however we expect UK leverage

requirements to continue to be the binding capital constraint.

The Basel Committee published their final reforms to the Basel III framework in December 2017. The amendments include changes to the

standardised approach (SA) for credit and operational risks and the introduction of a new RWA output floor. The rules are subject to a lengthy

transitional period from 2022 to 2027. These reforms will lead to a significant increase in the Group’s risk weights over time. We currently

expect the consequential impact on the reported CET1 ratio to ultimately be a reduction of approximately half relative to the current position.

The change relates to the application of standardised floors which override IRB model outputs. Organic earnings through the transition will

mitigate this impact such that the reported CET1 ratio will in practice remain well in excess of the proforma levels implied by this change, and

leverage requirements will remain the binding constraint based on latest projections. These reforms represent a re-calibration of regulatory

requirements with no underlying change in the capital resources held or the risk profile of assets. Final impacts are subject to uncertainty for

future balance sheet size and mix, and because the final detail of some elements of the regulatory changes remain at the PRA’s discretion.

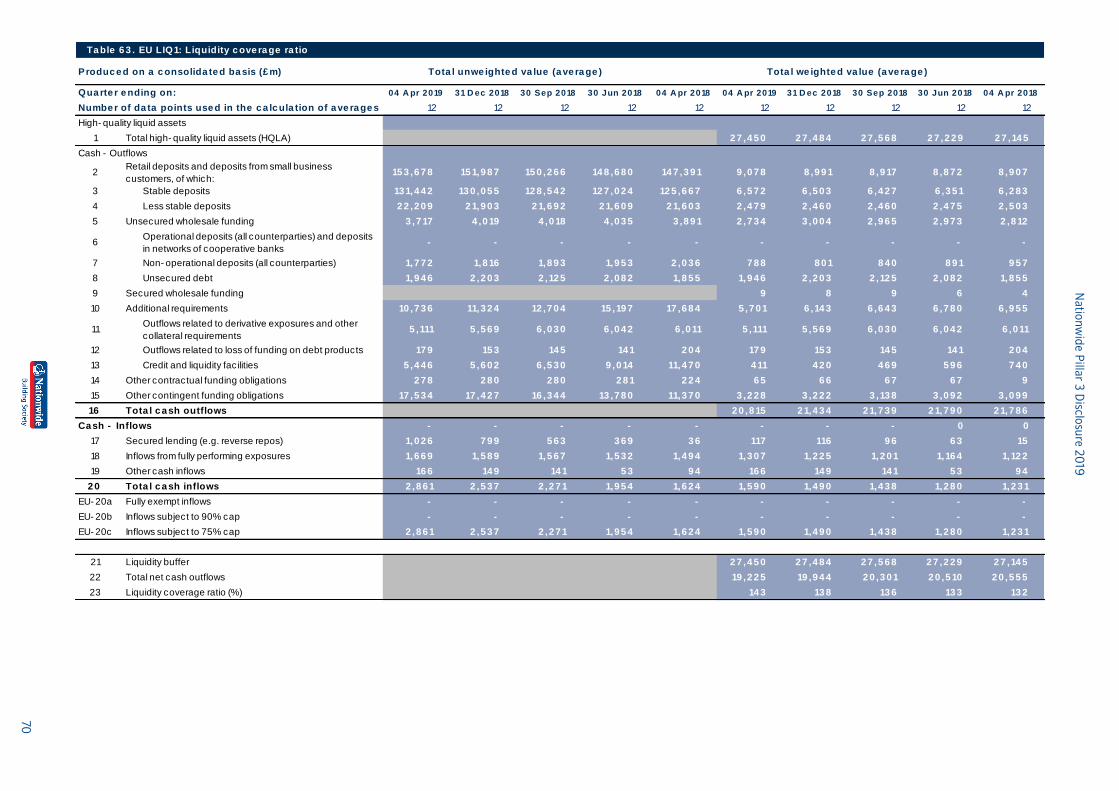

At 4 April 2019, Nationwide’s Liquidity Coverage Ratio (LCR) was 150% (2018: 130%), which exceeds the 100% regulatory minimum. The

average LCR based on 12 monthly data points was 143% (2018: 132%).

1 Note: IFRS 9 transitional provisions have been applied to the end-point disclosures. See section 3.1 for details. 2 See sections 4.4 and 4.5 for more information on regulatory buffer requirements.

Nationwide Pillar 3 Disclosure 2019

7

Ta ble 1. Ke y Me tric s a nd Impa c t of IFRS9 - Fully Loa de d

0 4 Apr 19 31 Dec 18 30 Sep 18 30 Jun 18 04 Apr 18

£ m £m £m £m £m

Ava ila ble c a pita l

Common Equity Tier 1 (CET1) 10 ,5 17 10,542 10,423 10,154 9,925

CET1 if IFRS 9 transitional arrangements had not been

applied 10 ,4 5 1 10,483 10,364 10,095

Tier 1 11,5 0 9 11,534 11,415 11,146 10,917

Tier 1 if IFRS 9 transitional arrangements had not been

applied11,4 4 3 11,475 11,356 11,087

Total capital 14 ,4 8 5 14,644 14,511 14,263 13,936

Total capital if IFRS 9 transitional arrangements had not

been applied14 ,4 6 5 14,640 14,513 14,243

Risk we ighte d a sse ts (a mounts)

Total risk weighted assets 3 2 ,5 0 6 33,243 32,868 32,430 32,509

Total risk weighted assets if IFRS 9 transitional

arrangements had not been applied3 2 ,5 3 9 33,279 32,903 32,465

Risk- ba se d c a pita l ra tios a s a pe rc e nta ge of

RWA

Common Equity Tier 1 (CET1) ratio (%) 3 2 .4 31.7 31.7 31.3 30.5

CET1 ratio if IFRS 9 transitional arrangements had not

been applied (%)3 2 .1 31.5 31.5 31.1

Tier 1 ratio (%) 3 5 .4 34.7 34.7 34.4 33.6

Tier 1 ratio if IFRS 9 transitional arrangements had not

been applied (%)3 5 .2 34.5 34.5 34.2

Total regulatory capital ratio (%) 4 4 .6 44.1 44.2 44.0 42.9

Total regulatory capital ratio if IFRS 9 transitional

arrangements had not been applied (%)4 4 .5 44.0 44.1 43.9

Additiona l CET1 buffe r re quire me nts a s a

pe rc e nta ge of RWA

Capital conservation buffer requirement (%) 2 .5 1.9 1.9 1.9 1.9

Countercyclical buffer requirement (%) 1.0 1.0 0.5 0.5 -

D- SIB additional requirements (%) - - - - -

Total of CET1 specific buffer requirements (%) 3 .5 2.9 2.4 2.4 1.9

CET1 available after meeting minimum capital

requirements, but before buffer requirements (%)2 7 .9 27.2 27.2 26.8 26.0

UK le ve ra ge ra tio

UK leverage ratio exposure measure 2 3 5 ,14 7 231,901 227,646 227,943 221,992

UK leverage ratio exposure measure if IFRS 9

transitional arrangements had not been applied2 3 5 ,0 8 1 231,843 227,587 227,884

UK leverage ratio (%) 4 .9 5.0 5.0 4.9 4.9

UK leverage ratio if IFRS 9 transitional arrangements

had not been applied (%)4 .9 4.9 5.0 4.9

CRR le ve ra ge ra tio

CRR leverage ratio total exposure measure 2 4 7 ,5 8 6 249,531 246,193 244,652 236,468

CRR leverage ratio exposure measure if IFRS 9

transitional arrangements had not been applied2 4 7 ,5 2 1 249,472 246,134 244,594

CRR leverage ratio (%) 4 .6 4.6 4.6 4.6 4.6

CRR leverage ratio if IFRS 9 or transitional arrangements

had not been applied4 .6 4.6 4.6 4.5

Liquidity c ove ra ge ra tio

Total HQLA 2 7 ,4 5 0 27,484 27,568 27,229 27,145

Total net cash outflows 19 ,2 2 5 19,944 20,301 20,510 20,555

Liquidity coverage ratio (%) 14 3 138 136 133 132

Note: The LCR data in the key metrics table represents a 12-month average.

Nationwide Pillar 3 Disclosure 2019

8

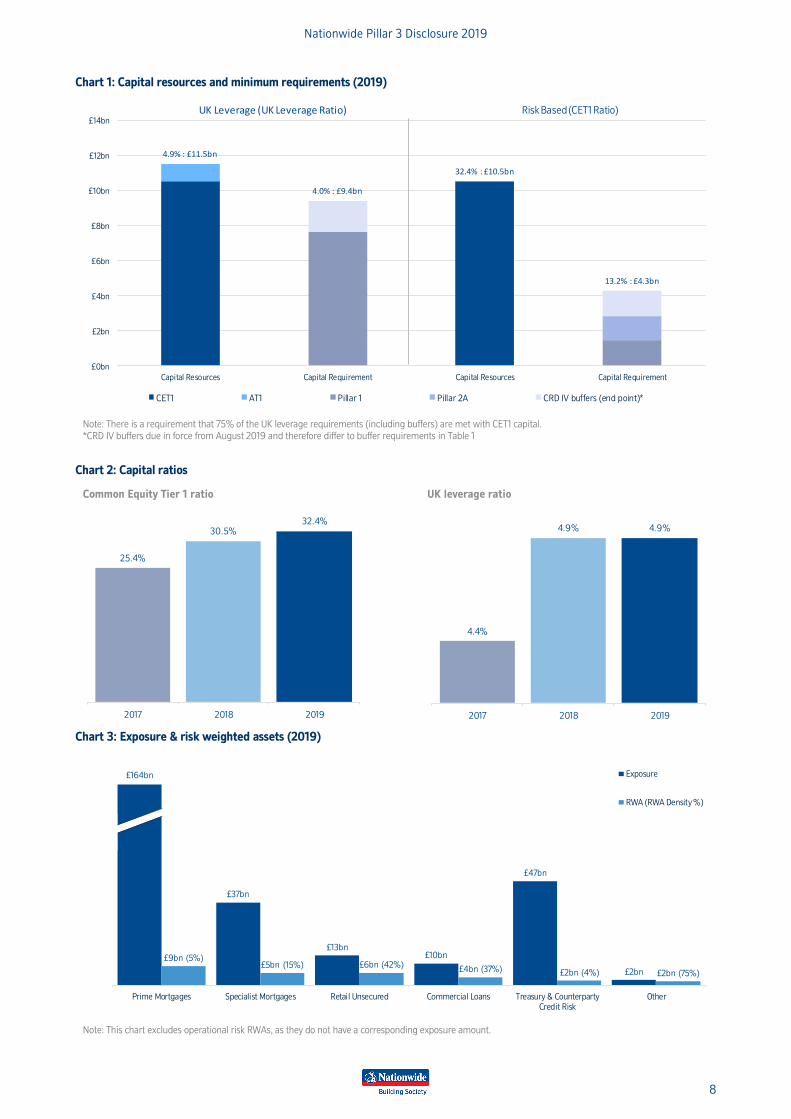

Chart 1: Capital resources and minimum requirements (2019)

4.9% : £11.5bn

4.0% : £9.4bn

32.4% : £10.5bn

13.2% : £4.3bn

£0bn

£2bn

£4bn

£6bn

£8bn

£10bn

£12bn

£14bn

Capital Resources Capital Requirement Capital Resources Capital Requirement

CET1 AT1 Pillar 1 Pillar 2A CRD IV buffers (end point)*

Risk Based (CET1 Ratio)UK Leverage (UK Leverage Ratio)

Note: There is a requirement that 75% of the UK leverage requirements (including buffers) are met with CET1 capital.

*CRD IV buffers due in force from August 2019 and therefore differ to buffer requirements in Table 1

Chart 2: Capital ratios

Common Equity Tier 1 ratio

25.4%

30.5%32.4%

2017 2018 2019

UK leverage ratio

4.4%

4.9% 4.9%

2017 2018 2019

Chart 3: Exposure & risk weighted assets (2019)

£37bn

£13bn£10bn

£47bn

£2bn

£9bn (5%)£5bn (15%) £6bn (42%)

£4bn (37%) £2bn (4%) £2bn (75%)

£0bn

£10bn

£20bn

£30bn

£40bn

£50bn

£60bn

£70bn

£80bn

£90bn

£100bn

Prime Mortgages Specialist Mortgages Retail Unsecured Commercial Loans Treasury & CounterpartyCredit Risk

Other

Exposure

RWA (RWA Density %)

£164bn

Note: This chart excludes operational risk RWAs, as they do not have a corresponding exposure amount.

Nationwide Pillar 3 Disclosure 2019

9

2 Introduction 2.1 Background

The European Union Capital Requirements Directive came into effect on 1 January 2007. This introduced consistent capital adequacy standards

and an associated supervisory framework in the EU based on the Basel II accord. Following publication of the Basel III accord, this was replaced

by the Capital Requirements Regulation (CRR) and the Capital Requirements Directive (together referred to as CRD IV) which came into force

on 1 January 2014 and is enforced in the UK, together with local implementing rules and guidance, by the PRA. The rules include disclosure

requirements known as ‘Pillar 3’ which apply to banks and building societies. These are designed to promote market discipline through the

disclosure of key information about risk exposures and risk management processes. See section 2.6 for details on how these disclosure rules

are evolving.

In May 2008, the Financial Services Authority (FSA) granted Nationwide permission to use IRB approaches for credit risk and capital

management. This permission was updated to become a CRR IRB permission from 1 January 2014. The disclosures in this document are based

on IRB approaches for most portfolios, including the majority of prime mortgages, specialist mortgages, personal loans, credit cards and

overdrafts. The SA is used for the remainder of credit risk and operational risk, as detailed in section 4.2.

As a building society subject to the Building Societies Act, Nationwide is required to maintain at least 75% of its ‘business assets’ (total assets

less fixed assets and liquid assets) in loans that are fully secured on residential property. For this reason, a higher proportion of Nationwide’s

lending is in the form of residential mortgages, when compared with many of the high-street plc banks. As a building society, Nationwide

cannot maintain a trading book and may only use derivatives to hedge risk. For this reason, Nationwide does not maintain RWAs for market

risk, as exposures are below the de minimis threshold in the CRR.

2.2 Scope

Nationwide’s structure

Nationwide is a European Economic Area (EEA) parent institution that is regulated by the PRA and Financial Conduct Authority (FCA). The

CRD IV framework therefore applies to Nationwide Building Society and its subsidiary undertakings (together, the ‘Group’).

There is a requirement to calculate and maintain regulatory capital ratios on both a Group basis and on an individual consolidation (or Solo)

basis. There are no differences between the basis of consolidation of the Group for accounting and prudential purposes. Full details of the

principal subsidiary undertakings are included in the Annual Report and Accounts 2019, Note 33 to the financial statements.

The subsidiaries included on the Individual consolidation basis are:

• The Mortgage Works (UK) plc;

• UCB Home Loans Corporation Limited;

• Derbyshire Home Loans Limited;

• E-Mex Home Funding Limited; and

• Nationwide Syndications Limited.

Unless otherwise stated, all subsidiary undertakings are included in the data provided in our Pillar 3 disclosures, this is referred to throughout

as the ‘Group’ position. Any reference to ‘Nationwide’ also refers to the Group position.

The Group does not see any practical or legal impediments to the transfer of capital resources or the repayment of liabilities within the Group.

Basis and frequency of disclosure

This document sets out the 2019 Pillar 3 disclosures for Nationwide. The purpose of these disclosures is to give information on the basis of

Basel III capital requirements and on the management of risks faced by Nationwide. Disclosures and bases of measurement are therefore in

accordance with the rules laid out in the CRR (Part 8). The disclosures may differ from similar information in the Annual Report and Accounts

2019 which is prepared in accordance with International Financial Reporting Standards (‘IFRS’). Therefore, the information in these disclosures

may not be directly comparable with that information.

Unless otherwise stated, all figures and narrative are as at 4 April 2019, Nationwide’s financial year end, with comparative figures for 4 April

2018 where relevant. Full Pillar 3 disclosures are published annually, and concurrently with the Annual Report and Accounts , in accordance

with regulatory guidelines. Summary Pillar 3 disclosures are published quarterly and semi-annually.

Regulatory balance sheet

There are no entities that are derecognised from the accounting balance sheet for regulatory purposes. For further information please see

Appendix 10.

Nationwide Pillar 3 Disclosure 2019

10

2.3 Risk appetite

A number of tools are employed to support the management of solvency risk. The Board is responsible for setting risk appetite with respect to

solvency risk, which is articulated through its risk appetite statements, and it defines minimum levels for capital ratios, including leverage, that

it is willing to operate with. These are translated into specific risk metrics, which are monitored by the BRC, Executive Risk Committee (ERC)

and Assets and Liabilities Committee (ALCO).

The capital structure is managed to ensure that minimum regulatory requirements are met, based on actuals and forecast stressed

performance, as well as meeting the expectations of key stakeholders and maintaining a robust financial position to protect our members. Any

planned changes to the balance sheet, potential regulatory developments and other factors (such as trading outlook) are all considered.

2.4 Individual (Solo) consolidation

Nationwide calculates capital requirements on a Group and Solo basis. The Solo consolidation includes entities that meet certain criteria as set

out in CRD IV and for Nationwide represent only lending entities. The differences between the Group and Solo consolidations relate primarily

to reserves held by entities that sit outside of the scope of Solo consolidation that are included in the Group consolidation, and a small impact

from the RWAs of these entities. The only Solo disclosures within this document are included in Tables 2 and 74.

2.5 Reporting

Key aspects of Nationwide’s capital position are reported monthly to the Board in Nationwide’s Bus iness Performance Pack. More detailed

reports of capital and risk are considered monthly by ALCO.

A range of Key Risk Indicators and Key Performance Indicators are routinely monitored (in both actual and forecast terms) by management,

and by the Board and its sub-committees (primarily BRC), to ensure that appropriate actions can be taken should triggers be breached.

2.6 Changes to disclosure requirements

This Pillar 3 disclosure includes 2 new tables, resulting from the introduction of a full Advanced Internal Ratings Based (AIRB) model for credit

cards in the year (Table 21) and the implementation of IFRS 9 transitional arrangements (Table 1). A summary of all tables within the document

is included in Appendix 12.

2.7 Location

These disclosures are located on Nationwide’s website: nationwide.co.uk

2.8 Policy, verification and sign off

Nationwide’s Pillar 3 disclosures have been verified and approved through internal governance procedures in line with Nationwide’s Pillar 3

Disclosure Standard. The Pillar 3 Disclosure Standard requires that:

• Solvency data is produced under the Capital Reporting Controls Framework (CRCF), which provides assurance over its accuracy,

integrity and completeness;

• Data outside of the CRCF is subject to appropriate senior review and approval;

• Appropriate reconciliations are performed on the disclosures;

• Narrative content is subject to appropriate senior review and approval;

• Compliance with regulatory requirements, as set out in Part 8 of the CRR, is documented and met;

• Risk-based review activities are performed across the three lines of defence, to provide assurance over the disclosures; and

• The BRC reviews and approves the disclosures.

“We attest that, to the best of our knowledge, Nationwide’s Pillar 3 disclosures have been prepared in accordance with Nationwide’s Pillar 3

Disclosure Standard and the internal controls framework described within it.”

Mark Rennison Julia Dunn

Chief Financial Officer Chief Risk Officer

Nationwide Pillar 3 Disclosure 2019

11

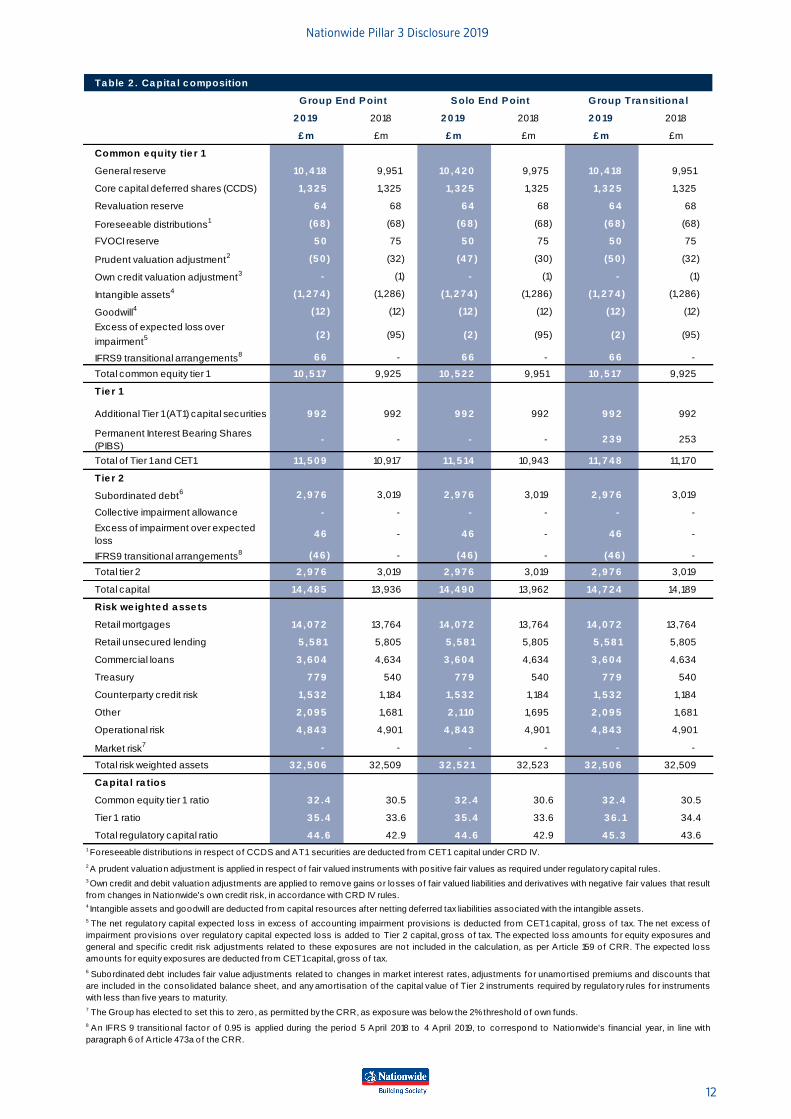

3 Capital resources 3.1 Total available capital

At 4 April 2019 and throughout the financial year, Nationwide complied with the capital requirements that were in force as set out by European

and national legislation. Nationwide continues to use an IRB approach, using its IRB models to calculate capital requirements. The PRA has

confirmed that the original 2008 permission transferred to a CRR IRB permission from 1 January 2014. Section 4.2 outlines the scope of

Nationwide’s IRB permission and which portfolios are calculated under the SA.

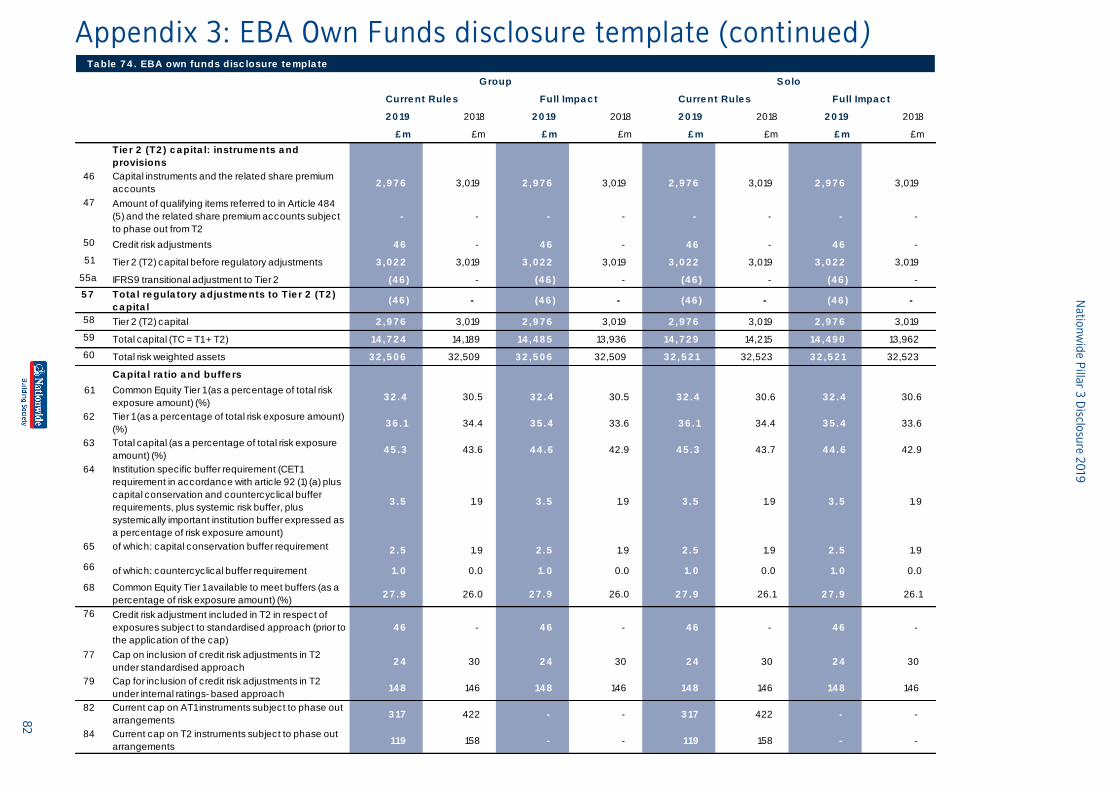

All disclosures are on an end-point basis unless otherwise stated as the transitional provisions only relate to grandfathered AT1 and Tier 2

capital. The impact of these can be seen in Table 2, which shows the comparison between the end-point and transitional arrangements. Our

Solo position can also be seen in Table 2.

With effect from 5 April 2018, Nationwide has adopted the IFRS 9 accounting standard. Management have chosen to apply the transitional

arrangements permitted by EU Regulation (2017/2395), which allows relief to capital ratios to reduce the impact of IFRS 9 ECLs. Whilst the

Day 1 impact of IFRS 9 was small from a CET1 perspective, the transitional arrangements have been applied because they provide relief during

the annual Concurrent Stress Testing (CST) exercise. The transitional adjustment is applied by adding back to CET1 capital resources, on a

reducing basis over the five years, the impact of IFRS 9 ECLs and then adjusting any related deferred tax assets and Tier 2 provisions. The

adjustment to CET1 resources at 4th April 2019 was an addback of £66 million, and a reduction of Tier 2 resources of £46 million, based on a

95% factor for year 1 of the IFRS 9 transition.

3.2 Common Equity Tier 1 capital

CET1 capital comprises:

• Core Capital Deferred Shares (CCDS);

• General reserve;

• Revaluation reserve;

• Fair value through other comprehensive income (FVOCI) reserve; and

• Adjustments as set out by the regulatory requirements governing capital resources.

The general reserve represents accumulated accounting profits as well as deductions relating to any pension fund deficit. General Reserves

have increased by £0.5 billion, driven predominantly by profit after tax.

3.3 Tier 1 capital

Tier 1 capital comprises:

• Permanent Interest Bearing Shares (PIBS) - CRD IV transitional basis only; and

• AT1 capital.

On 24 April 2019, Nationwide notified investors of its intention to redeem the outstanding AT1 capital instrument in full, on 20 June 2019. This

will reduce Tier 1 capital resources by £1 billion. These disclosures have been prepared based on the balance sheet position at 4 April 2019,

with the inclusion of the AT1 capital instrument.

3.4 Tier 2 capital

Tier 2 capital comprises:

• Qualifying subordinated notes;

• Qualifying PIBS; and

• Adjustments as set out by the regulatory requirements governing capital resources.

Subordinated notes are unsecured and rank behind the claims of all depositors, creditors and investing members (other than holders of PIBS,

AT1 securities and CCDS) of the Group. More details of the subordinated notes are included in the Annual Report and Accounts 2019, Note 19

to the financial statements.

Overall Tier 2 capital has been maintained at £3 billion. Future liability management options and decisions with respect to capital calls may be

made at Nationwide’s discretion in light of prevailing market, economic and regulatory conditions.

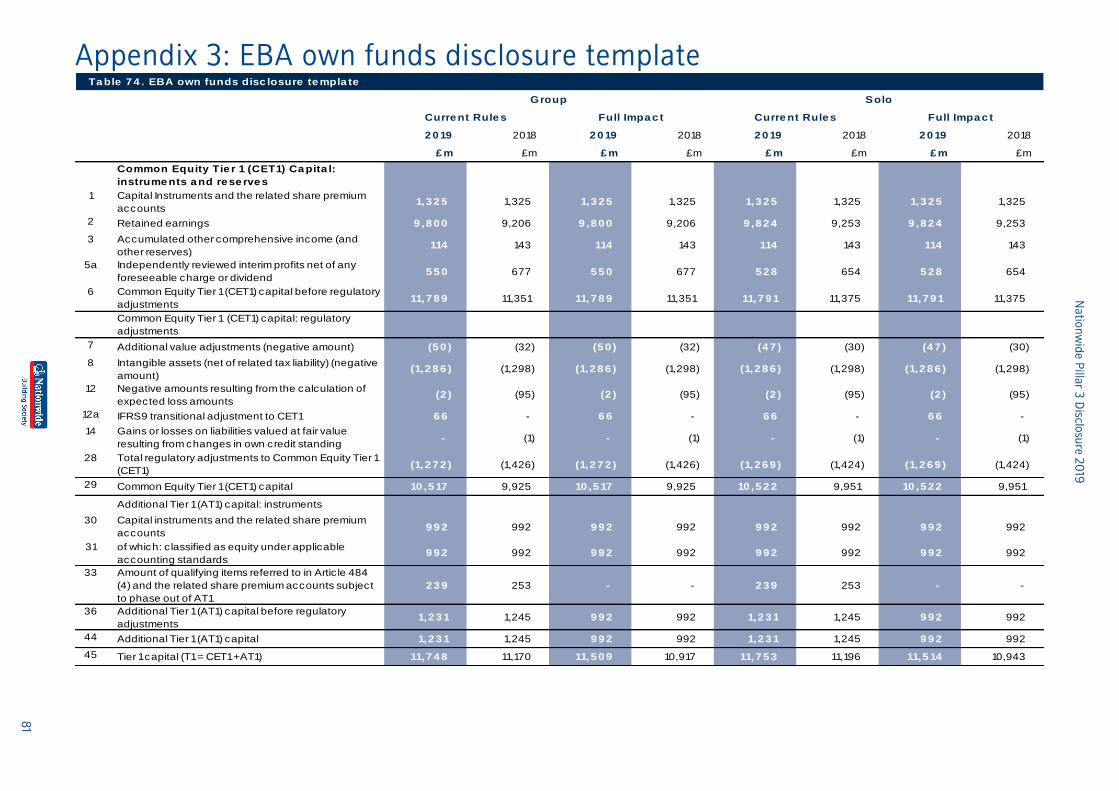

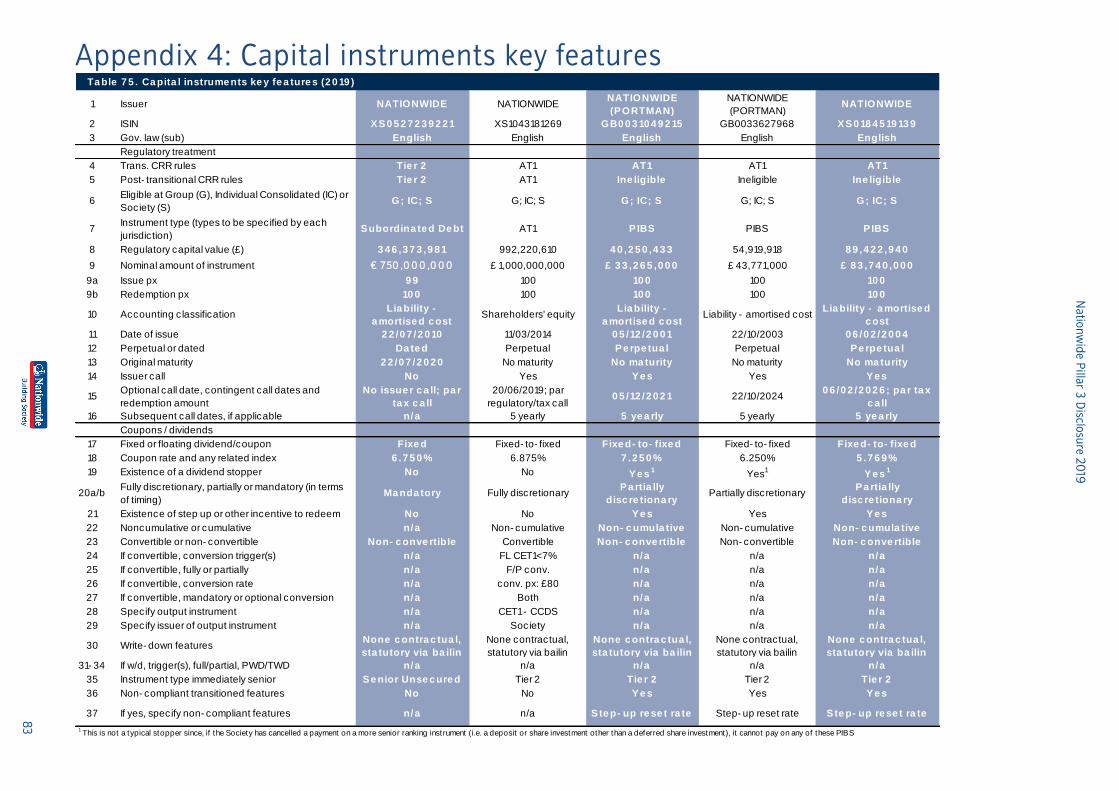

Appendix 4 shows the key features of the capital instruments issued by the Group, and more information can be found in the Annual Report

and Accounts 2019, Notes 19, 20, 31 and 32 to the financial statements.

Nationwide Pillar 3 Disclosure 2019

12

Ta ble 2 . Ca pita l c omposition

2 0 19 2018 2 0 19 2018 2 0 19 2018

£ m £m £ m £m £ m £m

Common e quity tie r 1

General reserve 10 ,4 18 9,951 10 ,4 2 0 9,975 10 ,4 18 9,951

Core capital deferred shares (CCDS) 1,3 2 5 1,325 1,3 2 5 1,325 1,3 2 5 1,325

Revaluation reserve 6 4 68 6 4 68 6 4 68

Foreseeable distributions1 (6 8 ) (68) (6 8 ) (68) (6 8 ) (68)

FVOCI reserve 5 0 75 5 0 75 5 0 75

Prudent valuation adjustment2 (5 0 ) (32) (4 7 ) (30) (5 0 ) (32)

Own credit valuation adjustment3 - (1) - (1) - (1)

Intangible assets4 (1,2 7 4 ) (1,286) (1,2 7 4 ) (1,286) (1,2 7 4 ) (1,286)

Goodwill4 (12 ) (12) (12 ) (12) (12 ) (12)

Excess of expected loss over

impairment5 (2 ) (95) (2 ) (95) (2 ) (95)

IFRS9 transitional arrangements8 6 6 - 6 6 - 6 6 -

Total common equity tier 1 10 ,5 17 9,925 10 ,5 2 2 9,951 10 ,5 17 9,925

Tie r 1

Additional Tier 1 (AT1) capital securities 9 9 2 992 9 9 2 992 9 9 2 992

Permanent Interest Bearing Shares

(PIBS)- - - - 2 3 9 253

Total of Tier 1 and CET1 11,5 0 9 10,917 11,5 14 10,943 11,7 4 8 11,170

Tie r 2

Subordinated debt6 2 ,9 7 6 3,019 2 ,9 7 6 3,019 2 ,9 7 6 3,019

Collective impairment allowance - - - - - -

Excess of impairment over expected

loss4 6 - 4 6 - 4 6 -

IFRS9 transitional arrangements8 (4 6 ) - (4 6 ) - (4 6 ) -

Total tier 2 2 ,9 7 6 3,019 2 ,9 7 6 3,019 2 ,9 7 6 3,019

Total capital 14 ,4 8 5 13,936 14 ,4 9 0 13,962 14 ,7 2 4 14,189

Risk we ighte d a sse ts

Retail mortgages 14 ,0 7 2 13,764 14 ,0 7 2 13,764 14 ,0 7 2 13,764

Retail unsecured lending 5 ,5 8 1 5,805 5 ,5 8 1 5,805 5 ,5 8 1 5,805

Commercial loans 3 ,6 0 4 4,634 3 ,6 0 4 4,634 3 ,6 0 4 4,634

Treasury 7 7 9 540 7 7 9 540 7 7 9 540

Counterparty credit risk 1,5 3 2 1,184 1,5 3 2 1,184 1,5 3 2 1,184

Other 2 ,0 9 5 1,681 2 ,110 1,695 2 ,0 9 5 1,681

Operational risk 4 ,8 4 3 4,901 4 ,8 4 3 4,901 4 ,8 4 3 4,901

Market risk7 - - - - - -

Total risk weighted assets 3 2 ,5 0 6 32,509 3 2 ,5 2 1 32,523 3 2 ,5 0 6 32,509

Ca pita l ra tios

Common equity tier 1 ratio 3 2 .4 30.5 3 2 .4 30.6 3 2 .4 30.5

Tier 1 ratio 3 5 .4 33.6 3 5 .4 33.6 3 6 .1 34.4

Total regulatory capital ratio 4 4 .6 42.9 4 4 .6 42.9 4 5 .3 43.6

8 An IFRS 9 transitional factor of 0.95 is applied during the period 5 April 2018 to 4 April 2019, to correspond to Nationwide's financial year, in line with

paragraph 6 of Article 473a of the CRR.

7 The Group has elected to set this to zero, as permitted by the CRR, as exposure was below the 2% threshold of own funds.

6 Subordinated debt includes fair value adjustments related to changes in market interest rates, adjustments for unamortised premiums and discounts that

are included in the consolidated balance sheet, and any amortisation of the capital value of Tier 2 instruments required by regulatory rules for instruments

with less than five years to maturity.

5 The net regulatory capital expected loss in excess of accounting impairment provisions is deducted from CET1capital, gross of tax. The net excess of

impairment provisions over regulatory capital expected loss is added to Tier 2 capital, gross of tax. The expected loss amounts for equity exposures and

general and specific credit risk adjustments related to these exposures are not included in the calculation, as per Article 159 of CRR. The expected loss

amounts for equity exposures are deducted from CET1 capital, gross of tax.

Group End Point Solo End Point Group Tra nsitiona l

1 Foreseeable distributions in respect o f CCDS and AT1 securities are deducted from CET1 capital under CRD IV.

2 A prudent valuation adjustment is applied in respect o f fair valued instruments with positive fair values as required under regulatory capital rules.

3 Own credit and debit valuation adjustments are applied to remove gains or losses of fair valued liabilities and derivatives with negative fair values that result

from changes in Nationwide's own credit risk, in accordance with CRD IV rules.4 Intangible assets and goodwill are deducted from capital resources after netting deferred tax liabilities associated with the intangible assets.

Nationwide Pillar 3 Disclosure 2019

13

Table 2 shows the composition of capital resources for the Group as at 4 April 2019 on a CRD IV basis, comparing this against the end point

basis for Group and Solo (i.e. assuming all CRD IV requirements were in force in full, with no transitional provisions permitted). See Appendix

3 for the full CRD IV disclosure template as published in the Official Journal of the European Union, 1423/2013.

There are no transitional provisions which apply to Nationwide’s common equity capital, so the CET1 ratio remains the same on a transitional

and end point basis at 32.4% (2018: 30.5%). The total Tier 1 capital ratio and total regulatory capital ratio are 36.1% (2018: 34.4%) and 45.3%

(2018: 43.6%) respectively on a transitional basis, as PIBS qualify under grandfathering provisions under CRD IV.

The CET1 ratio on an individual (Solo) consolidated basis at 4 April 2019 is 32.4% (2018: 30.6%) in line with the Group’s CET1 ratio. The

difference in RWAs is caused by the treatment of derivative instruments, some of which sit outside of the solo consolidation. Hedge accounting

results in differences in the Solo general reserves and solo cash flow hedge reserve, the latter of which is not included in CET1 capital. The Solo

general reserve was £2 million higher at 4 April 2019 (2018: £24 million higher).

The CET1 ratio improved due to an increase in CET1 capital resources, while RWAs remained stable. Table 3 provides an analysis of capital flows

and shows that CET1 capital resources have increased over the year by £0.6 billion, mainly due to profit after tax for the period. AT1 and Tier 2

capital has remained stable over the year. Other than two small redemptions of PIBS instruments for £12 million (which are not shown in Table

3 due to the table being on an end-point basis), no other capital instruments were issued or redeemed during the year.

RWAs remained stable, with increased retail lending and treasury related RWAs offset by run-off in the commercial book and the

implementation of a new credit card IRB model.

Table 9 and table 10 provide an analysis of the RWA movements, including the credit risk and counterparty credit risk components.

Ta ble 3 . Ca pita l flow sta te me nt

Group

£ m

Common e quity tie r 1 c a pita l a s a t 4 April 2 0 18 9,925

Issuance of CCDS -

Profit for the year 6 18

Other comprehensive income recognised directly in the general reserve (15 1)

Foreseeable distributions -

Revaluation reserve (4 )

FVOCI reserve (2 5 )

Capital adjustments:

Prudential valuation adjustment (18 )

Own credit valuation adjustment 1

Intangible assets 12

Excess of expected loss over impairment 9 3

IFRS 9 transitional arrangements 6 6

Common e quity tie r 1 c a pita l a s a t 4 April 2 0 19 10 ,5 17

Additiona l tie r 1 c a pita l a s a t 4 April 2 0 18 a nd 2 0 19 9 9 2

Tota l tie r 1 c a pita l a s a t 4 April 2 0 19 11,5 0 9

Tie r 2 c a pita l a s a t 4 April 2 0 18 3,019

Amortisation of subordinated debt (14 3 )

Fair value adjustments of subordinated debt 10 0

Excess of impairment provisions over regulatory expected losses 4 6

IFRS 9 transitional arrangements (4 6 )

Tie r 2 c a pita l a s a t 4 April 2 0 19 2 ,9 7 6

Tota l re gula tory c a pita l a s a t 4 April 2 0 18 13,936

Tota l re gula tory c a pita l a s a t 4 April 2 0 19 14 ,4 8 5

Na

tion

wid

e P

illar 3

Disclo

sure

20

19

14

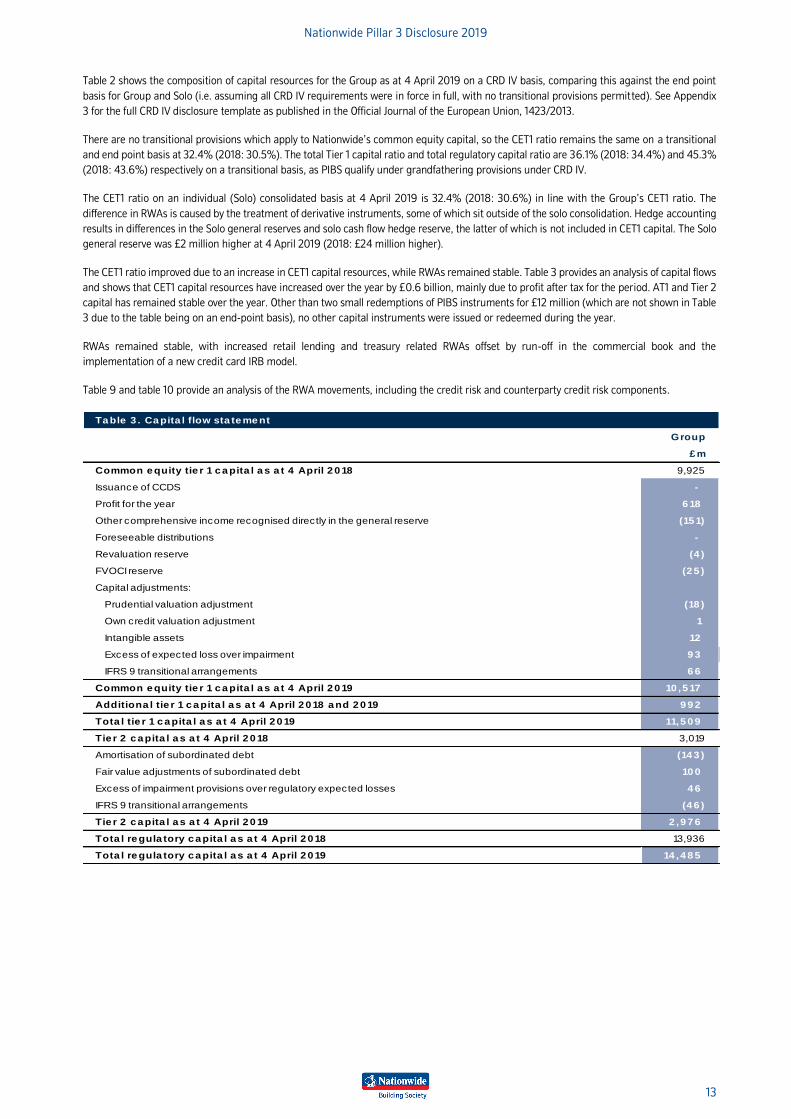

Table 4 is a breakdown of the constituent elements of the Group’s Prudent Valuation Adjustments (PVA) according to the requirements of paragraphs 698 to 701 of Basel II (comprehensive version, June 2006),

taking into account the guidance set out in Supervisory guidance for assessing banks’ financial instrument fair value practices, April 2009 (in particular Principle 10).

Ta ble 4 . EU PV1: Prude nt va lua tion a djustme nts (PVA) (2 0 19 )

a b c d f h

Equity Inte re st ra te s FX Cre dit Tota l

Of whic h:

In the ba nking

book

(£ m) (£ m) (£ m) (£ m) (£ m) (£ m)

1 Closeout uncertainty, of which: - 4 16 1 2 1 2 1

2 Mid- market value - 4 16 1 2 1 2 1

3 Closeout cost - - - - - -

4 Concentration - - - - - -

5 Early termination - - - - - -

6 Model risk 2 0 2 - 6 2 8 2 8

7 Operational risk - - 1 - 1 1

8 Investing and funding costs - - - - - -

9 Unearned credit spreads - - - - - -

10 Future administrative costs - - - - - -

11 Other - - - - - -

12 Tota l Adjustme nt 2 0 6 17 7 5 0 5 0

Note: Nationwide does not calculate closeout costs, concentration or future administration cost adjustments because the mid-market value adjustments assume exiting the full positions within a prudent exit

period. No early termination adjustments are calculated because these refer to potential losses arising from the non-contractual early termination of client trades and Nationwide does not provide client trades in

this context. No investing and funding cost nor unearned credit spread adjustments are calculated because valuations do not include funding costs nor expected losses due to counterparty default.

The majority of the PVA comprises of closeout uncertainty for interest rates and foreign exchange (FX), and model risk for equity. The closeout uncertainty for interest rates relates to the portfolio of interest rate

derivatives and fixed rate bonds held for liquidity purposes. The closeout uncertainty for FX is linked to derivatives used to manage currency risk, mainly for Euro and US Dollar debt issuances. The model risk for

equity adjustment relates to the valuation uncertainty of preferred stock in Visa Inc.

Nationwide Pillar 3 Disclosure 2019

15

3.5 Leverage ratio

Overview

Under CRD IV, firms are required to calculate a leverage ratio, which is not risk sensitive, to complement risk-based capital requirements. The

leverage ratio measures the relationship between a firm’s Tier 1 capital resources and its leverage exposure (total assets, plus certain off balance

sheet exposures). Monitoring and requiring firms to manage this metric allows regulators to limit the accumulation of excessive leverage.

UK leverage framework

Following recommendations from the Financial Policy Committee (FPC) in 2016 the PRA introduced the UK leverage ratio to the leverage

framework. It is calculated in the same way as the CRR leverage ratio, as outlined below, but excludes eligible central bank reserves from the

calculation of the leverage exposure measure. Nationwide has been granted permission to report a UK leverage ratio on the basis of

measurement announced by the PRA in August 2016.

In 2017 the PRA updated the UK leverage ratio framework following recommendations from the FPC. The update allowed for the exclusion of

certain central bank claims from the leverage exposure measure (previously excluded by ‘modification’ by the PRA in June 2016), increasing

the minimum leverage requirement to 3.25%, from 3%, and updating leverage reporting and disclosure requirements. It is calculated using

the CRR definition of Tier 1 for the capital amount.

A firm specific additional leverage ratio buffer will come into effect in August 2019, linked to the individual SRB requirement, which will be set

at 0.35%. In addition, the FPC can set a countercyclical leverage buffer up to 0.9% of leverage exposure for UK exposures; which is currently

set at 0.4%. Therefore, the minimum leverage ratio requirement is 4.0%. Nationwide is confident it is in a strong position to continue to meet

the minimum requirements.

The UK leverage ratio is also a hurdle rate in the annual CST exercise. Management calibrates Nationwide’s risk appetite to ensure our leverage

resources are enough to manage through a severe but plausible stress test. See section 4.3.4 for further detail on Nationwide’s approach to

stress testing.

Given that Nationwide’s balance sheet is focused on residential mortgage lending, it is considered that the risk of material unexpected

movements in the leverage exposure measure is limited, due to the relative stability of mortgage balances. Regular stress tests are undertaken,

which assess the sensitivity of the leverage ratio to stress conditions relative to risk-based capital metrics, which forms part of the risk appetite

framework.

Nationwide maintains a long-run strategic target for the UK leverage ratio of at least 4.5%. On 24 April 2019, Nationwide notified investors of

its intention to redeem its outstanding AT1 capital instrument in full, on 20 June 2019. This will reduce Tier 1 capital resources by £992m,

resulting in a 0.4% reduction in the UK leverage ratio, to 4.5%, based on the year-end balance sheet. Given Nationwide's historic financial

performance, Management remains confident that earnings accretion will be sufficient to meet projected balance sheet growth, such that

Nationwide can continue to meet its long-run strategic target for the UK leverage ratio.

If the leverage ratio were to fall below a defined level, Nationwide may take actions to restore its capital position, which may include actions to

increase capital resources or to reduce the size of the balance sheet based on a timescale deemed appropriate to the situation.

Table 5 . UK leverage ra tio

2019 2018

£m / % £m / %

Tier 1 capital 11,509 10,917

UK leverage exposure measure 235 ,147 221,992

UK leverage ratio 4 .9 4.9

The UK leverage ratio remained stable at 4.9% (2018: 4.9%), with an increase in Tier 1 capital, driven by profits after tax of £0.6 billion, offset

by an increase in UK leverage exposure of £13 billion. The increased leverage exposure was driven by increased net retail lending of £9 billion,

increased treasury exposures (including counterparty credit risk) of £5 billion, and an increase in other assets of £1 billion, offset by run-off in

the commercial book of £2 billion.

The average UK leverage ratio calculated over the quarter since 31 December 2018 was 4.9%.

CRR leverage framework

The CRR leverage ratio is calculated as Tier 1 capital / total exposures, defined as:

• Capital: Tier 1 capital defined according to CRD IV on an end-point basis (assuming the full impact of CRD IV requirements on Tier 1

capital were in force with no transitional provisions). See Table 2.

• Exposures: Total on and off balance sheet exposures (subject to credit conversion factors) as defined in the Delegated Act amending

CRR Article 429 (Calculation of the Leverage Ratio), which includes deductions applied to Tier 1 capital.

Nationwide Pillar 3 Disclosure 2019

16

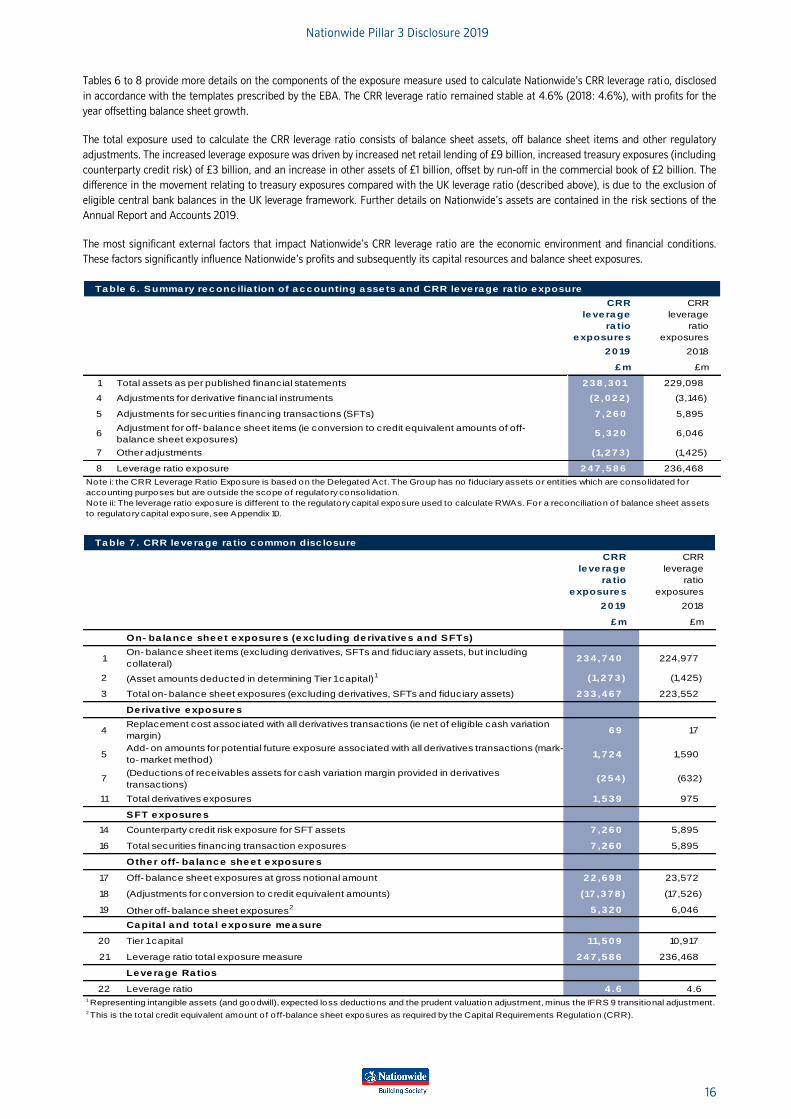

Tables 6 to 8 provide more details on the components of the exposure measure used to calculate Nationwide’s CRR leverage ratio, disclosed

in accordance with the templates prescribed by the EBA. The CRR leverage ratio remained stable at 4.6% (2018: 4.6%), with profits for the

year offsetting balance sheet growth.

The total exposure used to calculate the CRR leverage ratio consists of balance sheet assets, off balance sheet items and other regulatory

adjustments. The increased leverage exposure was driven by increased net retail lending of £9 billion, increased treasury exposures (including

counterparty credit risk) of £3 billion, and an increase in other assets of £1 billion, offset by run-off in the commercial book of £2 billion. The

difference in the movement relating to treasury exposures compared with the UK leverage ratio (described above), is due to the exclusion of

eligible central bank balances in the UK leverage framework. Further details on Nationwide’s assets are contained in the risk sections of the

Annual Report and Accounts 2019.

The most significant external factors that impact Nationwide’s CRR leverage ratio are the economic environment and financial conditions.

These factors significantly influence Nationwide’s profits and subsequently its capital resources and balance sheet exposures.

Ta ble 6 . Summa ry re c onc ilia tion of a c c ounting a sse ts a nd CRR le ve ra ge ra tio e xposure

CRR

le ve ra ge

ra tio

e xposure s

CRR

leverage

ratio

exposures

2 0 19 2018

£ m £m

1 Total assets as per published financial statements 2 3 8 ,3 0 1 229,098

4 Adjustments for derivative financial instruments (2 ,0 2 2 ) (3,146)

5 Adjustments for securities financing transactions (SFTs) 7 ,2 6 0 5,895

6Adjustment for off- balance sheet items (ie conversion to credit equivalent amounts of off-

balance sheet exposures)5 ,3 2 0 6,046

7 Other adjustments (1,2 7 3 ) (1,425)

8 Leverage ratio exposure 2 4 7 ,5 8 6 236,468

Note i: the CRR Leverage Ratio Exposure is based on the Delegated Act. The Group has no fiduciary assets or entities which are consolidated for

accounting purposes but are outside the scope of regulatory consolidation.

Note ii: The leverage ratio exposure is different to the regulatory capital exposure used to calculate RWAs. For a reconciliation of balance sheet assets

to regulatory capital exposure, see Appendix 10.

Ta ble 7 . CRR le ve ra ge ra tio c ommon disc losure

CRR

le ve ra ge

ra tio

e xposure s

CRR

leverage

ratio

exposures

2 0 19 2018

£ m £m

On- ba la nc e she e t e xposure s (e xc luding de riva tive s a nd SFTs)

1On- balance sheet items (excluding derivatives, SFTs and fiduciary assets, but including

collateral)2 3 4 ,7 4 0 224,977

2 (Asset amounts deducted in determining Tier 1 capital)1 (1,2 7 3 ) (1,425)

3 Total on- balance sheet exposures (excluding derivatives, SFTs and fiduciary assets) 2 3 3 ,4 6 7 223,552

De riva tive e xposure s

4Replacement cost associated with all derivatives transactions (ie net of eligible cash variation

margin)6 9 17

5Add- on amounts for potential future exposure associated with all derivatives transactions (mark-

to- market method)1,7 2 4 1,590

7(Deductions of receivables assets for cash variation margin provided in derivatives

transactions)(2 5 4 ) (632)

11 Total derivatives exposures 1,5 3 9 975

SFT e xposure s

14 Counterparty credit risk exposure for SFT assets 7 ,2 6 0 5,895

16 Total securities financing transaction exposures 7 ,2 6 0 5,895

Othe r off- ba la nc e she e t e xposure s 1

17 Off- balance sheet exposures at gross notional amount 2 2 ,6 9 8 23,572

18 (Adjustments for conversion to credit equivalent amounts) (17 ,3 7 8 ) (17,526)

19 Other off- balance sheet exposures2 5 ,3 2 0 6,046

Ca pita l a nd tota l e xposure me a sure

20 Tier 1 capital 11,5 0 9 10,917

21 Leverage ratio total exposure measure 2 4 7 ,5 8 6 236,468

Le ve ra ge Ra tios

22 Leverage ratio 4 .6 4.6 1 Representing intangible assets (and goodwill), expected loss deductions and the prudent valuation adjustment, minus the IFRS 9 transitional adjustment.2 This is the to tal credit equivalent amount o f o ff-balance sheet exposures as required by the Capital Requirements Regulation (CRR).

Nationwide Pillar 3 Disclosure 2019

17

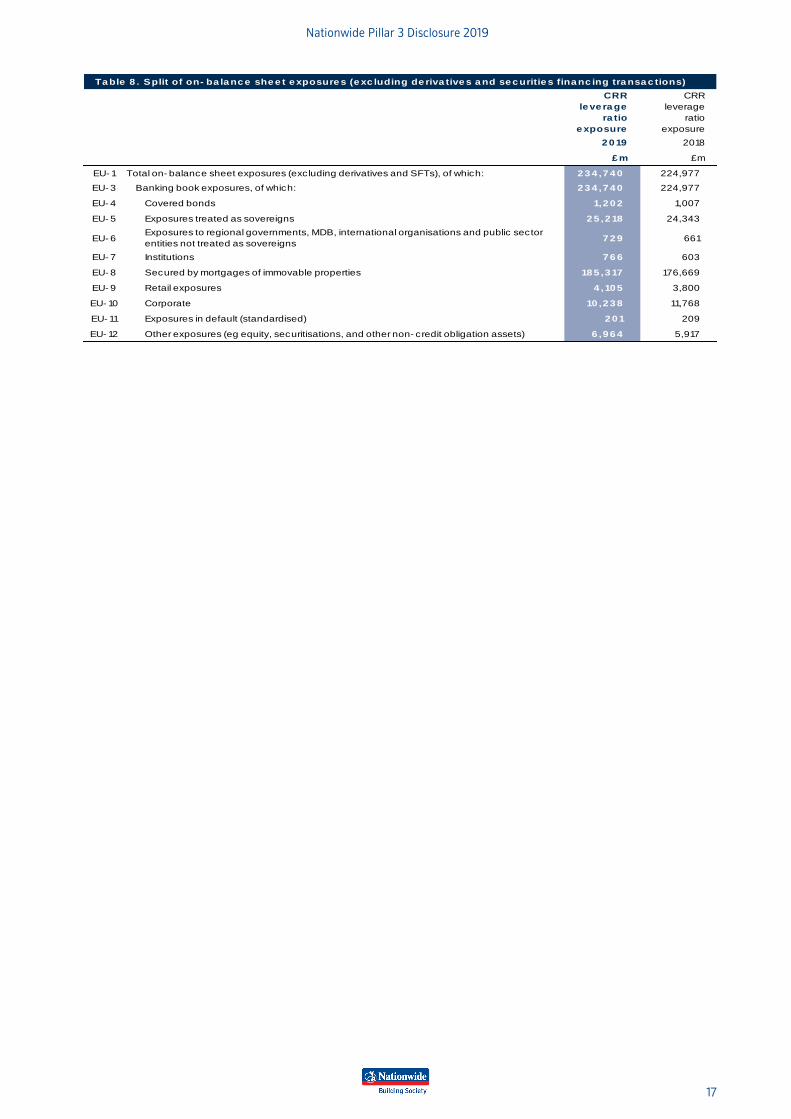

Ta ble 8 . Split of on- ba la nc e she e t e xposure s (e xc luding de riva tive s a nd se c uritie s fina nc ing tra nsa c tions)

CRR

le ve ra ge

ra tio

e xposure

CRR

leverage

ratio

exposure

2 0 19 2018

£ m £m

EU- 1 Total on- balance sheet exposures (excluding derivatives and SFTs), of which: 2 3 4 ,7 4 0 224,977

EU- 3 Banking book exposures, of which: 2 3 4 ,7 4 0 224,977

EU- 4 Covered bonds 1,2 0 2 1,007

EU- 5 Exposures treated as sovereigns 2 5 ,2 18 24,343

EU- 6Exposures to regional governments, MDB, international organisations and public sector

entities not treated as sovereigns7 2 9 661

EU- 7 Institutions 7 6 6 603

EU- 8 Secured by mortgages of immovable properties 18 5 ,3 17 176,669

EU- 9 Retail exposures 4 ,10 5 3,800

EU- 10 Corporate 10 ,2 3 8 11,768

EU- 11 Exposures in default (standardised) 2 0 1 209

EU- 12 Other exposures (eg equity, securitisations, and other non- credit obligation assets) 6 ,9 6 4 5,917

Nationwide Pillar 3 Disclosure 2019

18

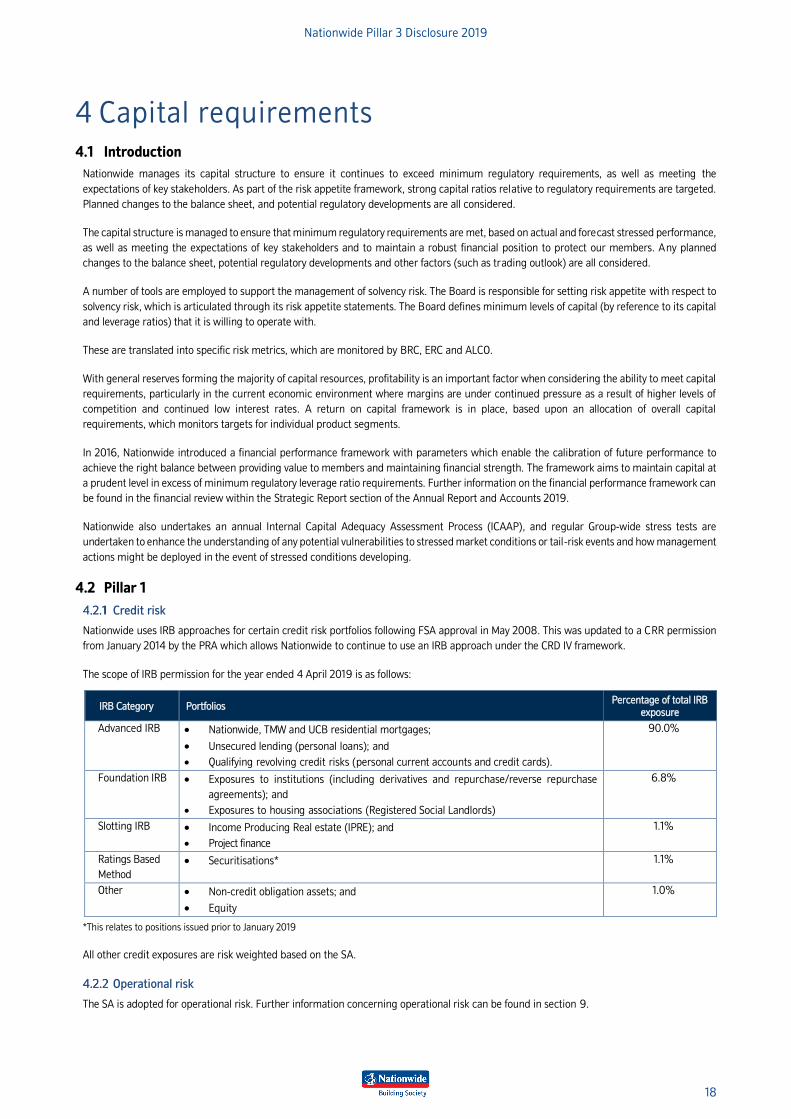

4 Capital requirements 4.1 Introduction

Nationwide manages its capital structure to ensure it continues to exceed minimum regulatory requirements, as well as meeting the

expectations of key stakeholders. As part of the risk appetite framework, strong capital ratios relative to regulatory requirements are targeted.

Planned changes to the balance sheet, and potential regulatory developments are all considered.

The capital structure is managed to ensure that minimum regulatory requirements are met, based on actual and forecast stressed performance,

as well as meeting the expectations of key stakeholders and to maintain a robust financial position to protect our members. Any planned

changes to the balance sheet, potential regulatory developments and other factors (such as trading outlook) are all considered.

A number of tools are employed to support the management of solvency risk. The Board is responsible for setting risk appetite with respect to

solvency risk, which is articulated through its risk appetite statements. The Board defines minimum levels of capital (by reference to its capital

and leverage ratios) that it is willing to operate with.

These are translated into specific risk metrics, which are monitored by BRC, ERC and ALCO.

With general reserves forming the majority of capital resources, profitability is an important factor when considering the ability to meet capital

requirements, particularly in the current economic environment where margins are under continued pressure as a result of higher levels of

competition and continued low interest rates. A return on capital framework is in place, based upon an allocation of overall capital

requirements, which monitors targets for individual product segments.

In 2016, Nationwide introduced a financial performance framework with parameters which enable the calibration of future performance to

achieve the right balance between providing value to members and maintaining financial strength. The framework aims to maintain capital at

a prudent level in excess of minimum regulatory leverage ratio requirements. Further information on the financial performance framework can

be found in the financial review within the Strategic Report section of the Annual Report and Accounts 2019.

Nationwide also undertakes an annual Internal Capital Adequacy Assessment Process (ICAAP), and regular Group-wide stress tests are

undertaken to enhance the understanding of any potential vulnerabilities to stressed market conditions or tail-risk events and how management

actions might be deployed in the event of stressed conditions developing.

4.2 Pillar 1

Credit risk

Nationwide uses IRB approaches for certain credit risk portfolios following FSA approval in May 2008. This was updated to a CRR permission

from January 2014 by the PRA which allows Nationwide to continue to use an IRB approach under the CRD IV framework.

The scope of IRB permission for the year ended 4 April 2019 is as follows:

IRB Category Portfolios Percentage of total IRB

exposure

Advanced IRB • Nationwide, TMW and UCB residential mortgages;

• Unsecured lending (personal loans); and

• Qualifying revolving credit risks (personal current accounts and credit cards).

90.0%

Foundation IRB • Exposures to institutions (including derivatives and repurchase/reverse repurchase

agreements); and

• Exposures to housing associations (Registered Social Landlords)

6.8%

Slotting IRB • Income Producing Real estate (IPRE); and

• Project finance

1.1%

Ratings Based

Method

• Securitisations* 1.1%

Other • Non-credit obligation assets; and

• Equity

1.0%

*This relates to positions issued prior to January 2019

All other credit exposures are risk weighted based on the SA.

Operational risk

The SA is adopted for operational risk. Further information concerning operational risk can be found in section 9.

Nationwide Pillar 3 Disclosure 2019

19

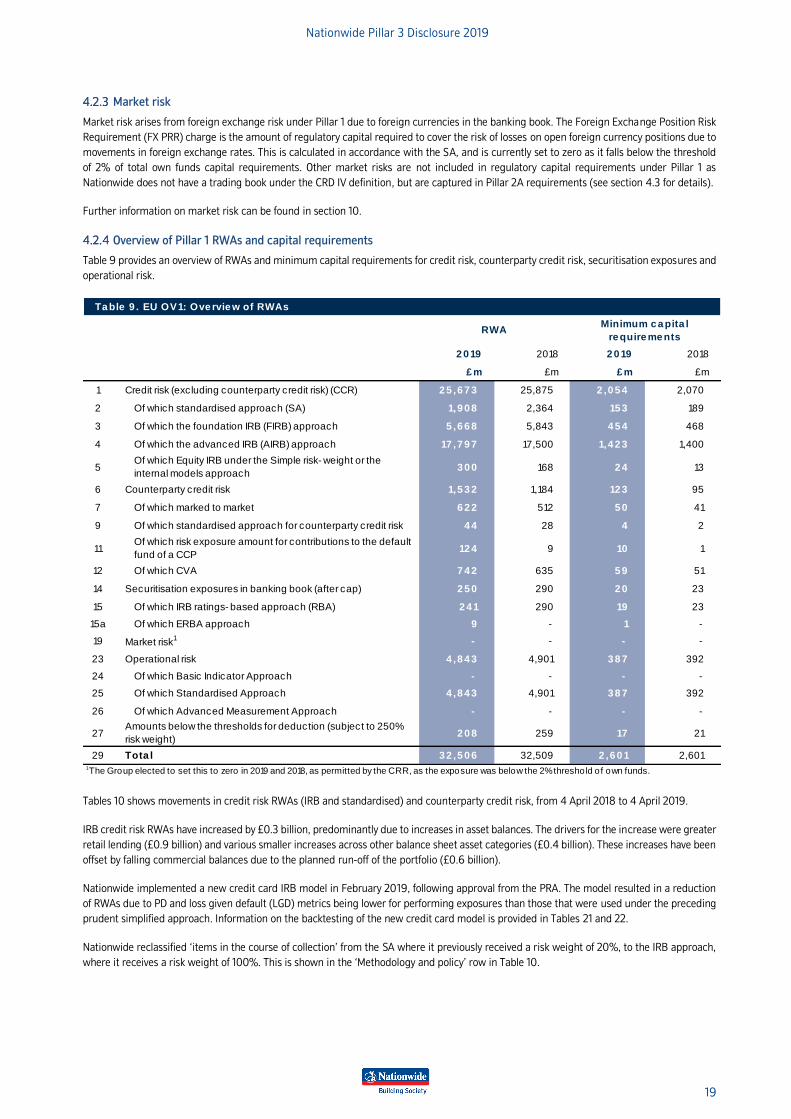

Market risk

Market risk arises from foreign exchange risk under Pillar 1 due to foreign currencies in the banking book. The Foreign Exchange Position Risk

Requirement (FX PRR) charge is the amount of regulatory capital required to cover the risk of losses on open foreign currency positions due to

movements in foreign exchange rates. This is calculated in accordance with the SA, and is currently set to zero as it falls below the threshold

of 2% of total own funds capital requirements. Other market risks are not included in regulatory capital requirements under Pillar 1 as

Nationwide does not have a trading book under the CRD IV definition, but are captured in Pillar 2A requirements (see section 4.3 for details).

Further information on market risk can be found in section 10.

Overview of Pillar 1 RWAs and capital requirements

Table 9 provides an overview of RWAs and minimum capital requirements for credit risk, counterparty credit risk, securitisation exposures and

operational risk.

Ta ble 9 . EU OV1: Ove rvie w of RWAs

2 0 19 2018 2 0 19 2018

£ m £m £ m £m

1 Credit risk (excluding counterparty credit risk) (CCR) 2 5 ,6 7 3 25,875 2 ,0 5 4 2,070

2 Of which standardised approach (SA) 1,9 0 8 2,364 15 3 189

3 Of which the foundation IRB (FIRB) approach 5 ,6 6 8 5,843 4 5 4 468

4 Of which the advanced IRB (AIRB) approach 17 ,7 9 7 17,500 1,4 2 3 1,400

5Of which Equity IRB under the Simple risk- weight or the

internal models approach3 0 0 168 2 4 13

6 Counterparty credit risk 1,5 3 2 1,184 12 3 95

7 Of which marked to market 6 2 2 512 5 0 41

9 Of which standardised approach for counterparty credit risk 4 4 28 4 2

11Of which risk exposure amount for contributions to the default

fund of a CCP12 4 9 10 1

12 Of which CVA 7 4 2 635 5 9 51

14 Securitisation exposures in banking book (after cap) 2 5 0 290 2 0 23

15 Of which IRB ratings- based approach (RBA) 2 4 1 290 19 23

15a Of which ERBA approach 9 - 1 -

19 Market risk1 - - - -

23 Operational risk 4 ,8 4 3 4,901 3 8 7 392

24 Of which Basic Indicator Approach - - - -

25 Of which Standardised Approach 4 ,8 4 3 4,901 3 8 7 392

26 Of which Advanced Measurement Approach - - - -

27Amounts below the thresholds for deduction (subject to 250%

risk weight)2 0 8 259 17 21

29 Tota l 3 2 ,5 0 6 32,509 2 ,6 0 1 2,601

RWAMinimum c a pita l

re quire me nts

1The Group elected to set this to zero in 2019 and 2018, as permitted by the CRR, as the exposure was below the 2% threshold of own funds.

Tables 10 shows movements in credit risk RWAs (IRB and standardised) and counterparty credit risk, from 4 April 2018 to 4 April 2019.

IRB credit risk RWAs have increased by £0.3 billion, predominantly due to increases in asset balances. The drivers for the increase were greater

retail lending (£0.9 billion) and various smaller increases across other balance sheet asset categories (£0.4 billion). These increases have been

offset by falling commercial balances due to the planned run-off of the portfolio (£0.6 billion).

Nationwide implemented a new credit card IRB model in February 2019, following approval from the PRA. The model resulted in a reduction

of RWAs due to PD and loss given default (LGD) metrics being lower for performing exposures than those that were used under the preceding

prudent simplified approach. Information on the backtesting of the new credit card model is provided in Tables 21 and 22.

Nationwide reclassified ‘items in the course of collection’ from the SA where it previously received a risk weight of 20%, to the IRB approach,

where it receives a risk weight of 100%. This is shown in the ‘Methodology and policy’ row in Table 10.

Nationwide Pillar 3 Disclosure 2019

20

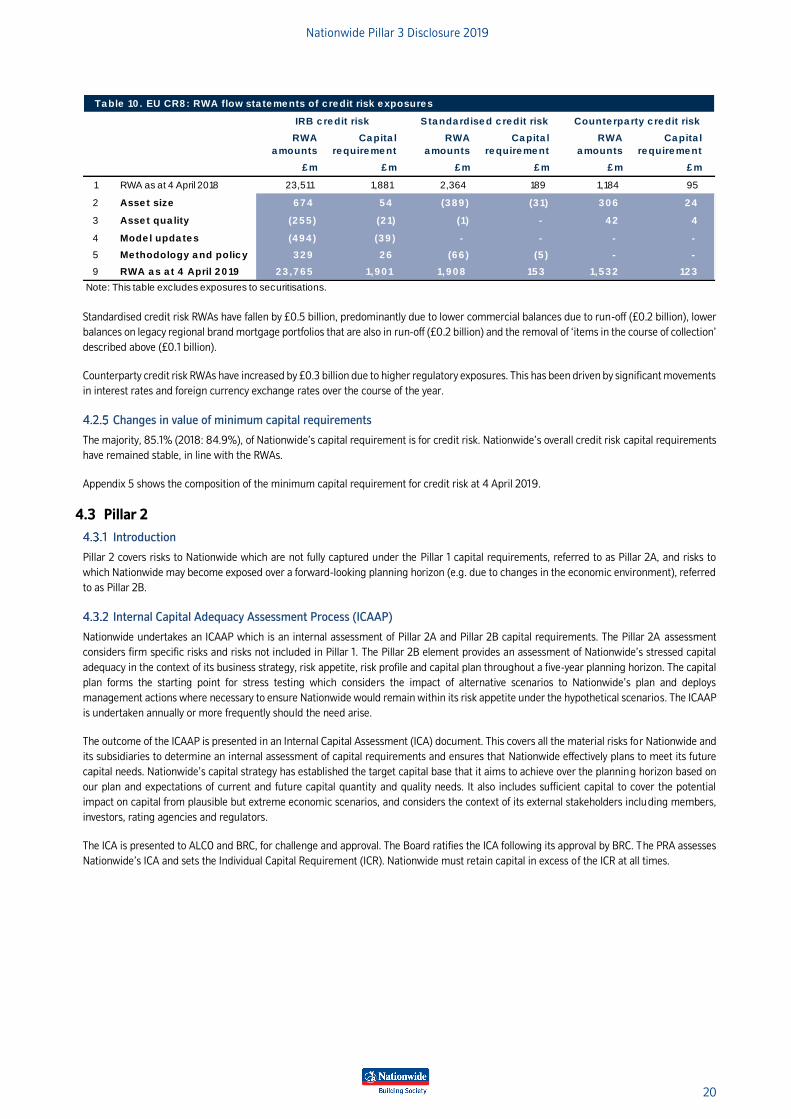

Ta ble 10 . EU CR8 : RWA flow sta te me nts of c re dit risk e xposure s

RWA

a mounts

Ca pita l

re quire me nt

RWA

a mounts

Ca pita l

re quire me nt

RWA

a mounts

Ca pita l

re quire me nt

£ m £ m £ m £ m £ m £ m

1 RWA as at 4 April 2018 23,511 1,881 2,364 189 1,184 95

2 Asse t size 6 7 4 5 4 (3 8 9 ) (3 1) 3 0 6 2 4

3 Asse t qua lity (2 5 5 ) (2 1) (1) - 4 2 4

4 Mode l upda te s (4 9 4 ) (3 9 ) - - - -

5 Me thodology a nd polic y 3 2 9 2 6 (6 6 ) (5 ) - -

9 RWA a s a t 4 April 2 0 19 2 3 ,7 6 5 1,9 0 1 1,9 0 8 15 3 1,5 3 2 12 3

Note: This table excludes exposures to securitisations.

IRB c re dit risk Sta nda rdise d c re dit risk Counte rpa rty c re dit risk

Standardised credit risk RWAs have fallen by £0.5 billion, predominantly due to lower commercial balances due to run-off (£0.2 billion), lower

balances on legacy regional brand mortgage portfolios that are also in run-off (£0.2 billion) and the removal of ‘items in the course of collection’

described above (£0.1 billion).

Counterparty credit risk RWAs have increased by £0.3 billion due to higher regulatory exposures. This has been driven by significant movements

in interest rates and foreign currency exchange rates over the course of the year.

Changes in value of minimum capital requirements

The majority, 85.1% (2018: 84.9%), of Nationwide’s capital requirement is for credit risk. Nationwide’s overall credit risk capital requirements

have remained stable, in line with the RWAs.

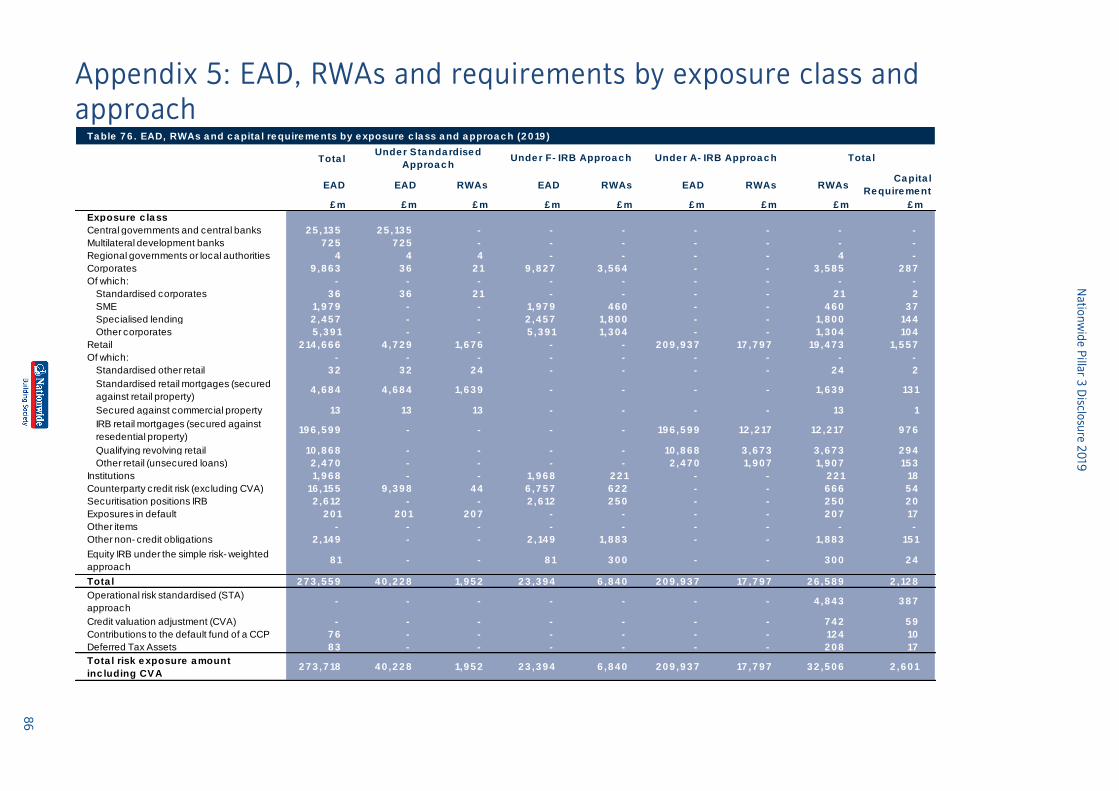

Appendix 5 shows the composition of the minimum capital requirement for credit risk at 4 April 2019.

4.3 Pillar 2

Introduction

Pillar 2 covers risks to Nationwide which are not fully captured under the Pillar 1 capital requirements, referred to as Pillar 2A, and risks to

which Nationwide may become exposed over a forward-looking planning horizon (e.g. due to changes in the economic environment), referred

to as Pillar 2B.

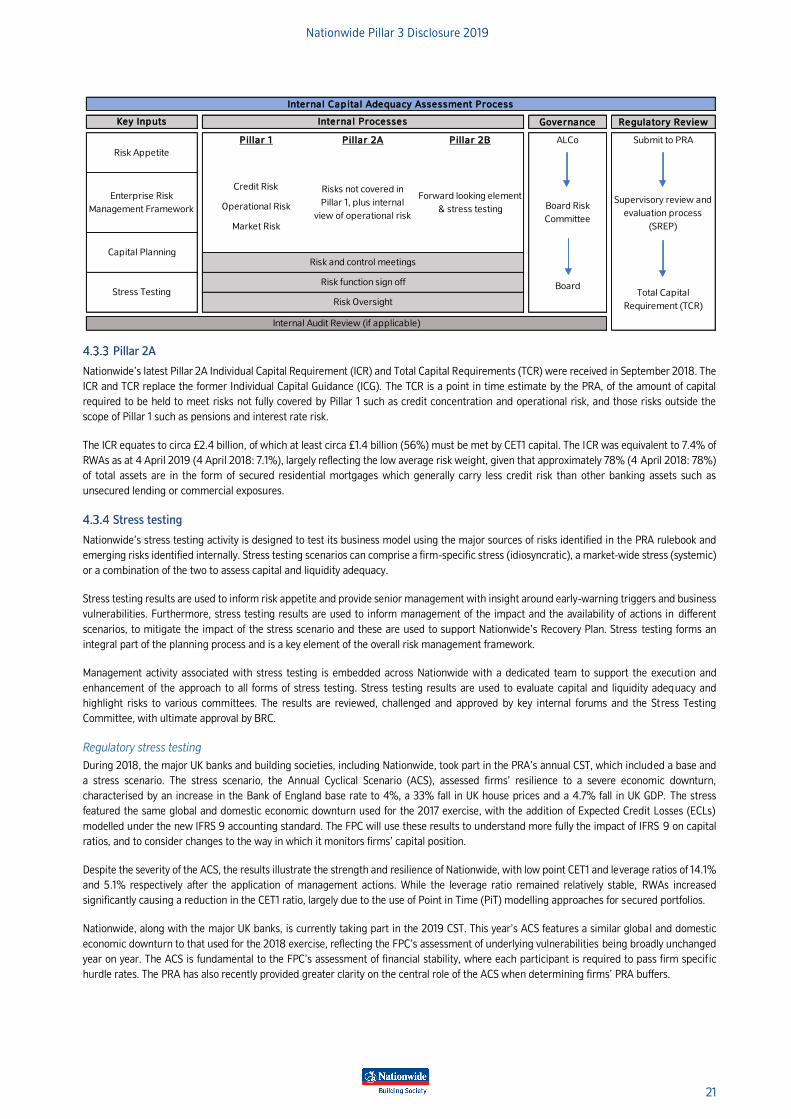

Internal Capital Adequacy Assessment Process (ICAAP)

Nationwide undertakes an ICAAP which is an internal assessment of Pillar 2A and Pillar 2B capital requirements. The Pillar 2A assessment

considers firm specific risks and risks not included in Pillar 1. The Pillar 2B element provides an assessment of Nationwide’s stressed capital

adequacy in the context of its business strategy, risk appetite, risk profile and capital plan throughout a five-year planning horizon. The capital

plan forms the starting point for stress testing which considers the impact of alternative scenarios to Nationwide’s plan and deploys

management actions where necessary to ensure Nationwide would remain within its risk appetite under the hypothetical scenarios. The ICAAP

is undertaken annually or more frequently should the need arise.

The outcome of the ICAAP is presented in an Internal Capital Assessment (ICA) document. This covers all the material risks for Nationwide and

its subsidiaries to determine an internal assessment of capital requirements and ensures that Nationwide effectively plans to meet its future

capital needs. Nationwide’s capital strategy has established the target capital base that it aims to achieve over the planning horizon based on

our plan and expectations of current and future capital quantity and quality needs. It also includes sufficient capital to cover the potential

impact on capital from plausible but extreme economic scenarios, and considers the context of its external stakeholders including members,

investors, rating agencies and regulators.

The ICA is presented to ALCO and BRC, for challenge and approval. The Board ratifies the ICA following its approval by BRC. The PRA assesses

Nationwide’s ICA and sets the Individual Capital Requirement (ICR). Nationwide must retain capital in excess of the ICR at all times.

Nationwide Pillar 3 Disclosure 2019

21

Governance Regulatory Review

Pillar 1 P illar 2A Pillar 2B ALCo Submit to PRA

Credit Risk

Operational Risk

Market Risk

Board

Supervisory review and

evaluation process

(SREP)

Internal Audit Review (if applicable)

Total Capital

Requirement (TCR)

Interna l Cap ita l Adequacy Assessment Process

Forward looking element

& stress testing

Capital PlanningRisk and control meetings

Risk function sign off

Risk OversightStress Testing

Board Risk

Committee

Interna l ProcessesKey Inp uts

Risk Appetite

Enterprise Risk

Management Framework

Risks not covered in

Pillar 1, plus internal

view of operational risk

Pillar 2A

Nationwide’s latest Pillar 2A Individual Capital Requirement (ICR) and Total Capital Requirements (TCR) were received in September 2018. The

ICR and TCR replace the former Individual Capital Guidance (ICG). The TCR is a point in time estimate by the PRA, of the amount of capital

required to be held to meet risks not fully covered by Pillar 1 such as credit concentration and operational risk, and those risks outside the

scope of Pillar 1 such as pensions and interest rate risk.

The ICR equates to circa £2.4 billion, of which at least circa £1.4 billion (56%) must be met by CET1 capital. The ICR was equivalent to 7.4% of