Phillips Carbon Black Ltd. - Myirisbreport.myiris.com/SKPSEC/PHICARBL_20121010.pdfPhillips Carbon...

14

October 10, 2012 Phillips Carbon Black Ltd. On a recovery path... CMP INR 106.0 Target INR 148.0 Initiating Coverage - BUY SKP Securities Ltd www.skpmoneywise.com Page 1 of 14 Key Share Data Face Value (INR) 10.0 Equity Capital (INR Mn) 344.7 52 Week High/Low (INR) 145.2 / 76.1 6 months Avg. Daily Volume (NSE) 73,461 BSE Code 506590 NSE Code PHILIPCARB Reuters Code PHIL.BO Bloomberg Code PHCB IN Shareholding Pattern (as on 30th Jun. 2012) Promoter 52.26% FII's, 10.68% Others, 29.65% DII's, 7.41% Source: Company Particulars FY11 FY12 FY13E FY14E Net Sales 16,957.2 21,867.8 23,861.1 27,418.2 Growth (%) 37.6% 29.0% 9.1% 14.9% EBITDA 2,213.2 2,071.6 2,247.7 2,648.6 PAT 1,127.0 856.1 851.8 1,098.3 Growth (%) -7.8% -24.0% -0.5% 28.9% EPS (INR) 34.3 25.4 24.7 31.9 BVPS (INR) 155.2 176.2 196.2 222.2 Key Financials (INR Million) Particulars FY11 FY12 FY13E FY14E P/E (x) 4.3 4.4 4.3 3.3 P/BVPS (x) 0.9 0.6 0.5 0.5 Mcap/Sales (x) 0.3 0.2 0.2 0.1 EV/EBITDA (x) 3.9 5.0 4.8 4.5 ROCE (%) 19.1% 13.4% 12.0% 13.0% ROE (%) 26.9% 15.3% 13.3% 15.2% EBITDA Mar (%) 13.1% 9.5% 9.4% 9.7% PAT Mar (%) 6.6% 3.9% 3.6% 4.0% Debt - Equity (x) 0.9 1.1 1.1 1.1 Key Financials Ratios Source: Company, SKP Research 1 Yr price performance PCBL vis-à-vis BSE Small Cap -60% -45% -30% -15% 0% 15% Oct-11 Dec-11 Mar-12 May-12 Jul-12 Oct-12 PCBL BSE Small Cap Company Background Phillips Carbon Black Ltd (PCBL) incorporated in 1960, is a part of RP- Sanjiv Goenka Group. The company is engaged in the manufacturing of carbon black having a capacity of 422,000 MT along with power generation capacity of 76 MW. Columbian Chemical Corporation, US, a leading international producer of rubber blacks is the technical collaborator of the company. Investment Rationale Strategic plant location with dominant market share PCBL enjoys a Pan India presence with four manufacturing plants, which are strategically located to cater to the tyre demands of the respective regions, thereby reducing the cost of freight. The domestic industry is consolidated with five players with PCBL having a market share of ~46 percent in FY12, in terms of production. Growth in the Automobile Industry to drive volumes To meet the growing demand (OEM & Replacement markets), majority of the tyre manufacturers are in the process of capacity expansion especially in the radials segment which would lead to utilisation of newer capacities of carbon black. Going forward, the radialization in truck segment is expected to reach ~35 percent (next 3 years) owing to infrastructure thrust and OE thrust, leading to an increase in the demand for tyres. Capacity expansion plan to propel growth PCBL is implementing a Greenfield expansion of 140,000 MT carbon black plant at Chennai along with 25 MW CPP at a total cost of INR 4,000 million which is expected to get commissioned in FY15. It is also setting up of a new coal tar distillation plant in Orissa with capacity of 1,50,000 mtpa coal tar processing and 50,000 mtpa soft pitch processing at an investment of INR 1,800 million. The 1,50,000 mtpa coal tar processing plant is expected to get commissioned in FY14 while 50,000 mtpa soft pitch processing will get commissioned in FY15. Surplus power sales to maintain margins With increase in the power generation capacity from 68 MW in FY12 to 84 MW by Oct. ’12, the share of revenues from power sale is expected to increase to ~4.5 percent by FY14E from current 3.8 percent. The power business enjoys EBITDA margins of ~90 percent in the absence of raw material cost. Valuation We rate a BUY rating on PCBL with a price target of INR148/share, implying an upside potential of 39.6 percent from current levels. Our target price is based on PCBL’s FY14E EV/EBITDA multiple of 5x. Analyst: Nikhil Saboo Ph: +91 33 4007 7027, M: +91 9330186643 Email: n[email protected]om

-

Upload

truongkhuong -

Category

Documents

-

view

217 -

download

2

Transcript of Phillips Carbon Black Ltd. - Myirisbreport.myiris.com/SKPSEC/PHICARBL_20121010.pdfPhillips Carbon...

October 10, 2012

Phillips Carbon Black Ltd.

On a recovery path...

CMP INR 106.0 Target INR 148.0 Initiating Coverage - BUY

SKP Securities Ltd www.skpmoneywise.com Page 1 of 14

Key Share Data

Face Value (INR) 10.0

Equity Capital (INR Mn) 344.7

52 Week High/Low (INR) 145.2 / 76.1

6 months Avg. Daily Volume (NSE) 73,461

BSE Code 506590

NSE Code PHILIPCARB

Reuters Code PHIL.BO

Bloomberg Code PHCB IN

Shareholding Pattern (as on 30th Jun. 2012)

Promoter 52.26%

FII's, 10.68%

Others, 29.65%

DII's, 7.41%

Source: Company

Particulars FY11 FY12 FY13E FY14E

Net Sales 16,957.2 21,867.8 23,861.1 27,418.2

Growth (%) 37.6% 29.0% 9.1% 14.9%

EBITDA 2,213.2 2,071.6 2,247.7 2,648.6

PAT 1,127.0 856.1 851.8 1,098.3

Growth (%) -7.8% -24.0% -0.5% 28.9%

EPS (INR) 34.3 25.4 24.7 31.9

BVPS (INR) 155.2 176.2 196.2 222.2

Key Financials (INR Million)

Particulars FY11 FY12 FY13E FY14E

P/E (x) 4.3 4.4 4.3 3.3

P/BVPS (x) 0.9 0.6 0.5 0.5

Mcap/Sales (x) 0.3 0.2 0.2 0.1

EV/EBITDA (x) 3.9 5.0 4.8 4.5

ROCE (%) 19.1% 13.4% 12.0% 13.0%

ROE (%) 26.9% 15.3% 13.3% 15.2%

EBITDA Mar (%) 13.1% 9.5% 9.4% 9.7%

PAT Mar (%) 6.6% 3.9% 3.6% 4.0%

Debt - Equity (x) 0.9 1.1 1.1 1.1

Key Financials Ratios

Source: Company, SKP Research

1 Yr price performance PCBL vis-à-vis BSE Small Cap

-60%

-45%

-30%

-15%

0%

15%

Oct-11 Dec-11 Mar-12 May-12 Jul-12 Oct-12

PCBL BSE Small Cap

Company Background

Phillips Carbon Black Ltd (PCBL) incorporated in 1960, is a part of RP-Sanjiv Goenka Group. The company is engaged in the manufacturing of carbon black having a capacity of 422,000 MT along with power generation capacity of 76 MW. Columbian Chemical Corporation, US, a leading international producer of rubber blacks is the technical collaborator of the company.

Investment Rationale

Strategic plant location with dominant market share

� PCBL enjoys a Pan India presence with four manufacturing plants, which are strategically located to cater to the tyre demands of the respective regions, thereby reducing the cost of freight.

� The domestic industry is consolidated with five players with PCBL

having a market share of ~46 percent in FY12, in terms of production.

Growth in the Automobile Industry to drive volumes

� To meet the growing demand (OEM & Replacement markets), majority of the tyre manufacturers are in the process of capacity expansion especially in the radials segment which would lead to utilisation of newer capacities of carbon black.

� Going forward, the radialization in truck segment is expected

to reach ~35 percent (next 3 years) owing to infrastructure thrust and OE thrust, leading to an increase in the demand for tyres.

Capacity expansion plan to propel growth

� PCBL is implementing a Greenfield expansion of 140,000 MT carbon black plant at Chennai along with 25 MW CPP at a total cost of INR 4,000 million which is expected to get commissioned in FY15.

� It is also setting up of a new coal tar distillation plant in Orissa with

capacity of 1,50,000 mtpa coal tar processing and 50,000 mtpa soft pitch processing at an investment of INR 1,800 million. The 1,50,000 mtpa coal tar processing plant is expected to get commissioned in FY14 while 50,000 mtpa soft pitch processing will get commissioned in FY15.

Surplus power sales to maintain margins

� With increase in the power generation capacity from 68 MW in FY12 to 84 MW by Oct. ’12, the share of revenues from power sale is expected to increase to ~4.5 percent by FY14E from current 3.8 percent. The power business enjoys EBITDA margins of ~90 percent in the absence of raw material cost.

Valuation

We rate a BUY rating on PCBL with a price target of INR148/share, implying an upside potential of 39.6 percent from current levels. Our target price is based on PCBL’s FY14E EV/EBITDA multiple of 5x.

A Analyst: Nikhil Saboo

Ph: +91 33 4007 7027, M: +91 9330186643

Email: [email protected]

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 2 of 14

The domestic industry is globally

competitive, as most of the capacity

in modern and product quality

matches international standards

Environmental issue have made it

difficult to produce carbon black in

major developed countries as a result

of which production is shifting to

emerging countries

Industry Overview

� Carbon black is a form of amorphous carbon that has an extremely

high surface area to volume ratio and it is one of the first nano-

materials to find common use. Carbon black is a material, usually

produced by the incomplete combustion of petroleum products.

� Carbon black is used in the tyre industry as well as in the non-tyre

sector as reinforcing filler in rubber products and in the printing ink

and paint industry. The tyre industry accounts for about 65 percent

of carbon black demand in India followed by 15 percent in rubber

and 20 percent is utilized by ink, printing, belts & hoses and other

speciality chemicals etc. Carbon black helps in conducting heat

away from the tread and belt area of the tyre, reducing thermal

damage and increasing the durability of the tyre.

Exhibit: Sector Wise Utilization of Carbon Black

Source: Company, SKP Research

65.0%

15.0%

10.0%

10.0%

Tyre Rubber Belts & Hoses Printing, Ink & Other Speciality

� During 2011, the global demand for carbon black rose by 5.8

percent from 10.2 million MT to 10.8 million MT, while global

capacity and utilization stood at 13.9 million MT and 77 percent

respectively. The demand growth was led by regions like North

America (9.0 percent), European Union (11.0 percent) and Eastern

Europe (14.7 percent), while Asia (excluding China) saw a modest

growth of 5.2 percent compared to last year y-o-y growth of 18

percent.

Particulars CY09 CY10 CY11

Capacity 12.7 13.4 13.9

Growth (%) - 5.5% 3.7%

Capacity Utilization (%) 71% 76% 77%

Demand 8.9 10.2 10.8

Source: Company, SKP Research

Exhibit: Global Carbon Black Scenario Figs. in Million MT

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 3 of 14

The domestic carbon black industry

was impacted by a slowdown within

the automobile sector as well as by

the increasing dumping of carbon

black into India by China and other

countries

Around 40 percent of the tyre

demand is led by the OEM segment

while 60 percent is from the

replacement segment (by revenue)

Demand growth for carbon black

continues to be robust with the global

demand expected to grow at a CAGR

of 4.6 percent from 2010 to 2015

� In India, the demand for carbon black during FY12 was 657,000 MT

witnessing a y-o-y growth of 2.5 percent. Total production during

FY12 was 694,000 MT, which is at the same level as FY11. The

total capacity of the Indian carbon black industry stood at 935,000

MT, with capacity utilization of 74 percent.

Particulars FY10 FY11 FY12

Capacity 0.700 0.790 0.935

Growth (%) - 12.9% 18.4%

Production 0.633 0.693 0.694

Capacity Utilization (%) 90% 88% 74%

Demand 0.605 0.641 0.657

Source: Company, SKP Research

Exhibit: India Carbon Black Scenario Figs. in Million MT

� Domestic tyre production is expected to get a boost from the high

OEM and replacement demand from the tyre and automobile

industry. Around 40 percent of the tyre demand is led by the OEM

segment while 60 percent is from the replacement segment (by

revenue). Furthermore, a number of international car makers are

increasingly focusing on the Indian automobile industry and

ramping up investment. In view of this, tyre manufacturers have

lined-up capacity expansion plans in the near future, which are

expected to benefit the domestic carbon black industry.

� The industry sold about 122.8 million tyres in various segments in

FY12 compared to 118.1 million tyres sold in FY11. Demand

growth for carbon black continues to be robust with the global

demand expected to grow at a CAGR of 4.6 percent from 2010 to

2015. Domestic demand for carbon black is expected to grow at

~7-8 percent during FY13. Exhibit: Domestic Auto Sales Volumes

Source: Industry, SKP Research

9.9 10.7 11.6 11.7 13.6 14.7 14.43.1 3.3 3.7 3.7 4.3 4.6 513.6 14.2 16.8 18.8

22.529.3 30.3

3 3.83.8 3.8

4.9

5.4 5.6

30.335.2

38.7 40.1

48.4

61.965.2

2.22.4

2.72.4

2.3

2.22.3

0

10

20

30

4050

60

70

80

90100

110

120

130

FY06 FY07 FY08 FY09 FY10 FY11 FY12

Fig

s. in

Mill

ions

Truck/Bus Light Trucks Pasng. Cars Farm Two Wheelers Others

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 4 of 14

PCBL is the leading carbon black

manufacturer in the country and

seventh largest player across the

globe

The strategic location of four plants in

different parts of India facilitate PCBL

to optimize logistic costs within India

and outside

Company Profile

� Phillips Carbon Black Limited (PCBL), incorporated in 1960, is a

part of RP-Sanjiv Goenka Group. The company is engaged in the

manufacturing of carbon black and power generation. It is the

leading carbon black manufacturer in the country and seventh

largest player across the globe. Columbian Chemical Corporation,

US, a leading international producer of rubber blacks is the

technical collaborator of the company.

Source: Company, SKP Research

Exhibit: Key Milestones

Started with Phillips Petroleum Co, USA at Durgapur with 14,000 MT.

Collaboration with Columbian Chemical, Acquisition of CB division of

Gujarat Carbon & Carbon & Chemicals, Ltd, Kochi etc.

1960 -

2004:

2005: Durgapur capacity increased to 1,40,000 MT & 12 MW CPP commissioned at

2007: Signed a MOU for plant in Vietnam

2008: 30 MW CPP commissioned at Durgapur

2009: 90000 MT & 16 MW CPP commissioned at Mundra

2011: 10 MW CPP commissioned at Kochi

2012: Mundra & Durgapur capacity increased to 1,40,000 & 1,52,000 MT

Q1FY13: 8 MW CPP commissioned at Mundra

� The company has four manufacturing facilities in India with total

installed carbon black manufacturing capacity of 422,000 MT and

power generation capacity of 76 MW. Its plant is located at

Durgapur (West Bengal), Palej & Mundra (Gujarat) and Kochi

(Kerala). PCBL is setting up a green field carbon black plant at

Chennai and carbo chemical plant at Orissa, which going forward

will further strengthen its geographical reach.

Location Carbon Black Capacity Power Capacity

Durgapur, West Bengal 1,52,000 MT 30 MW

Palej, Gujarat 90,000 MT 12 MW

Mundra, Gujarat 1,40,000 MT 24 MW

Kochi, Kerala 40,000 MT 10 MW

Total 4,22,000 MT 76 MW

Exhibit: Current Plant Overview

Source: Company, SKP Research

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 5 of 14

PCBL products are exported to more

than 20 countries, which contribute

~30 percent of its revenue.

PCBL is setting up a green field

carbon black plant at Chennai, which

going forward will further strengthen

its geographical reach

� Multi-locational production facilities along with focus on product

innovation and global technological alliance helps, PCBL to cater

the demand of its customers across India. Its products are exported

to more than 20 countries, which contribute ~30 percent of its

revenue. PCBL manufacturers ~20-25 grades of carbon black

which is supplied to the tyre industry, non-tyre industry and

specialty chemicals sector.

Investment Rationale

Strategic plant location with dominant market share

� PCBL is the only player in the carbon black industry with a Pan

India presence. It has four manufacturing plants in India which are

strategically located to cater to the tyre demands of the respective

regions, thereby reducing the cost of freight. Further, PCBL is

setting up a green field carbon black plant at Chennai, which going

forward will further strengthen its geographical reach.

LocationCapacity

(FY12)

Capacity

(FY14E) *

Mundra140000 MT +

16 MW

140000 MT +

24 MW

Palej90000 MT +

12 MW

90000 MT +

20 MW

Kochi40000 MT +

10 MW

90000 MT +

10 MW

Orissa - 150000 MT

Durgapur152000 MT +

30 MW

152000 MT +

30 MW

Exhibit: Strategic Plant Locations

Note: * Chennai capacity of 140000 MT &

25 MW power plant is expected to get

commissioned in FY15. Also excluding

Vietnam project of 115000 MT & 18 MW

power plant.

Source: Company, SKP Research

Mundra

Orissa

Chennai

Palej

Kochi

Durgapur

Carbon Black Plants

Carbo Chemical Plants

MRF Tyres

Apollo Tyres

JK Tyres

0Ceat Tyres

� The domestic carbon black industry is consolidated with five

players, accounting for the entire carbon black capacity. PCBL is

the largest player in the domestic market having a market share of

~46 percent in FY12, in terms of production while globally it is

ranked seventh. It takes around ~20-24 months to build a new

carbon black manufacturing facility; hence, PCBL is well placed to

take advantage of the expansions in the industry.

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 6 of 14

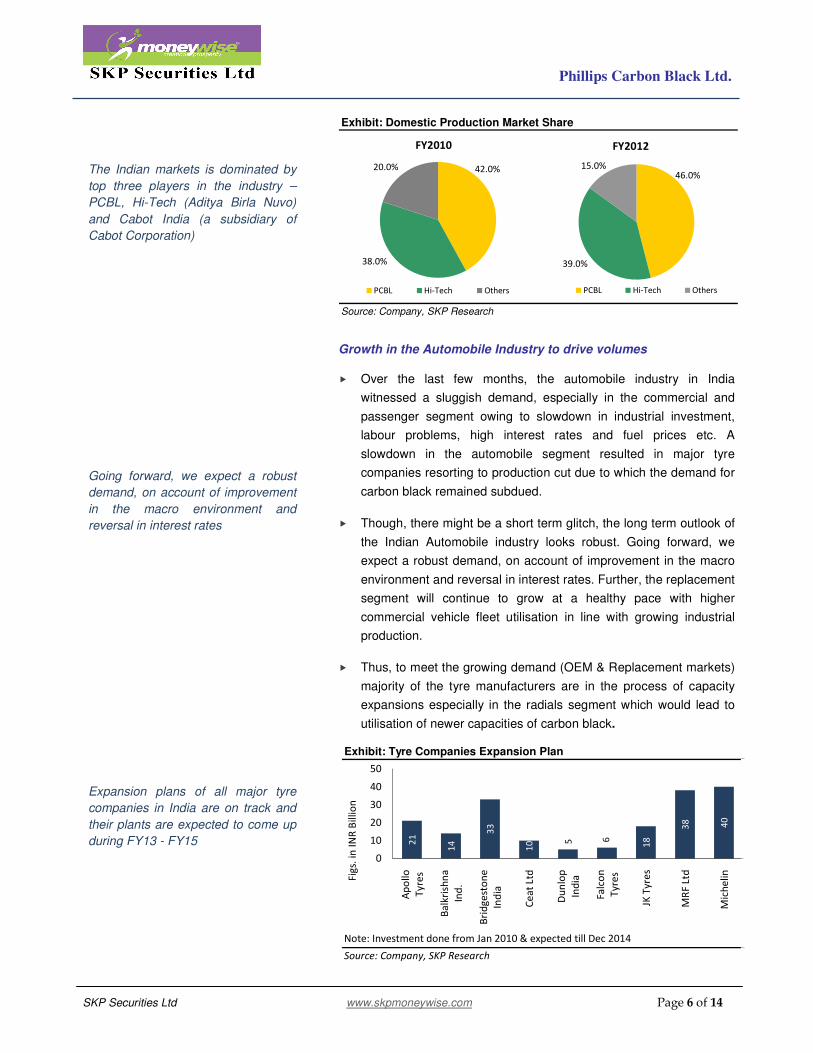

The Indian markets is dominated by

top three players in the industry –

PCBL, Hi-Tech (Aditya Birla Nuvo)

and Cabot India (a subsidiary of

Cabot Corporation)

Going forward, we expect a robust

demand, on account of improvement

in the macro environment and

reversal in interest rates

Expansion plans of all major tyre

companies in India are on track and

their plants are expected to come up

during FY13 - FY15

Exhibit: Domestic Production Market Share

Source: Company, SKP Research

42.0%

38.0%

20.0%

FY2010

PCBL Hi-Tech Others

46.0%

39.0%

15.0%

FY2012

PCBL Hi-Tech Others

Growth in the Automobile Industry to drive volumes

� Over the last few months, the automobile industry in India

witnessed a sluggish demand, especially in the commercial and

passenger segment owing to slowdown in industrial investment,

labour problems, high interest rates and fuel prices etc. A

slowdown in the automobile segment resulted in major tyre

companies resorting to production cut due to which the demand for

carbon black remained subdued.

� Though, there might be a short term glitch, the long term outlook of

the Indian Automobile industry looks robust. Going forward, we

expect a robust demand, on account of improvement in the macro

environment and reversal in interest rates. Further, the replacement

segment will continue to grow at a healthy pace with higher

commercial vehicle fleet utilisation in line with growing industrial

production.

� Thus, to meet the growing demand (OEM & Replacement markets)

majority of the tyre manufacturers are in the process of capacity

expansions especially in the radials segment which would lead to

utilisation of newer capacities of carbon black. Exhibit: Tyre Companies Expansion Plan

Source: Company, SKP Research

Note: Investment done from Jan 2010 & expected till Dec 2014

21

14

33

10 5 6

18

38 40

0

10

20

30

40

50

Ap

oll

o

Ty

res

Ba

lkri

shn

a

Ind

.

Bri

dg

est

on

e

Ind

ia

Ce

at

Ltd

Du

nlo

p

Ind

ia

Fa

lco

n

Ty

res

JK T

yre

s

MR

F L

td

Mic

he

lin

Fig

s. i

n I

NR

Bil

lio

n

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 7 of 14

Going forward, the radialization in

truck segment is expected to reach

~35 percent (next 3 years) owing to

infrastructure and OE thrust, leading

to an increase in the demand for

tyres

PCBL is implementing a Greenfield

expansion of 140,000 MT carbon

black plant at Chennai along with 25

MW CPP at a total cost of INR 4,000

million which is expected to get

commissioned in FY15

� The radialization of truck tyres is still at extremely low levels in India

and offers huge opportunity for tyre companies. Going forward, the

radialization in truck segment is expected to reach ~35 percent

(next 3 years) owing to infrastructure and OE thrust, leading to an

increase in the demand for tyres, thereby boosting the demand for

carbon black.

Source: Industry Sources, SKP Research

Exhibit: Radialisation in Truck Segment

100%

96%

95%

72%

68%

65%

52%

27%

21%

0% 20% 40% 60% 80% 100% 120%

Western Europe

North America

Central Europe

Africa/Middle East

World

South America

Asia

Eastern Europe

India

Capacity expansion plan to propel growth

� To meet the growing demand of carbon black, PCBL had

undertaken significant capacity addition across all its manufacturing

plants over the last two years as well increased its co-generation

power capacity. In FY12, PCBL completed expansion of carbon

black plant of 50,000 MT at Mundra, 11,000 MT at Durgapur along

with 10 MW captive power plant (CPP) plant at Kochi. During

Q1FY13, PCBL commissioned its 8 MW CPP at Mundra, and is

underway to commission 50,000 MT of carbon black capacity at

Cochin plant and 8 MW CPP at Palej, Gujarat (expected by

September 2012), thereby taking the total carbon black capacity to

472,000 and co-generation power capacity to 84 MW.

� The company is implementing a Greenfield expansion of

140,000 MT carbon black plant at Chennai along with 25 MW

CPP at a total cost of INR 4,000 million which is expected to

get commissioned in FY15. The funding for the same will be done

through a mix of debt and internal accruals in the ratio of 2:1. PCBL

has already signed Memorandum of Understanding (MoU) with the

Tamil Nadu Government and is in the process of obtaining all

approvals for the same.

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 8 of 14

In order to partially offset its volatility,

PCBL has planned to use coal tar as

its raw material. Coal Tar is a by-

product generated through the

processing of coal into coke for use

in steel manufacturing

The entire Vietnam projects have

been kept under review on account

of slowing demand scenario

Waste gases from plants being used

to produce electricity, Surplus power

sold to grid at an average realization

of INR 3.2 – 3.3/unit

� The key raw material for PCBL is Carbon Black Feed Stock

(CBFS), which is directly linked to the international crude oil prices

and is imported from USA. In order to partially offset its volatility,

PCBL has planned to use coal tar as its raw material. Coal Tar is a

by-product generated through the processing of coal into coke for

use in steel manufacturing. PCBL is setting up of a new coal tar

distillation plant (Carbo Chemical business) in Orissa with capacity

of 1,50,000 mtpa coal tar processing and 50,000 mtpa soft pitch

processing at an investment of INR 1,800 million. The 1,50,000

mtpa coal tar processing plant is expected to get

commissioned in FY14 while 50,000 mtpa soft pitch

processing will get commissioned in FY15.

� PCBL planned to set up 115,000 MT carbon black plant at Vietnam

along with 18 MW CPP in two phases at an investment of USD 84

million, which was to be funded through a debt equity ratio of 2:1.

The first phase of 60,000 MT carbon black along with 12 MW CPP

was expected to get commissioned in FY13 while the second

phase consisting of 55,000 MT carbon black and 21 MW was

scheduled to get commissioned in FY14. Though, the entire

Vietnam projects have been kept under review on account of

slowing demand scenario. Till date, investments in Vietnam

projects stand at ~USD 5-7 million.

Surplus power sales to maintain margins

� The process of manufacturing of carbon black results in generation

of lean gases which have both sensible heat and low calorific

value. Instead of wasting the energy, PCBL has installed extremely

specialized and state of the art 30 MW CPP at Durgapur, 12 MW

CPP at Palej, 24 MW CPP at Mundra and 10 MW CPP at Kochi.

� The entire lean gas is used to generate power for meeting the

entire internal process requirements for production of carbon black

as well as surplus is sold to the grid. At present, about 35-40

percent of power produced is used for own captive consumption

while rest is sold to the grid at an average realization of INR 3.2-

3.3/unit.

� During FY12, 3.8 percent of the revenues accrue from the sale of

power. With the increase in the power generation capacity from 68

MW in FY12 to 84 MW by October 2012, the share of revenues

from power sale is expected to increase to ~4.5 percent in the

next two years.

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 9 of 14

The power business enjoys EBITDA

margins of ~90 percent in the

absence of raw material cost

With the increase in the power

generation capacity from 68 MW in

FY12 to 84 MW by October 12, the

share of revenues from power sale is

expected to increase to ~4.5 percent

in the next two years

Source: Company, SKP Research

Exhibit: Co-Generation Power

Earlier

Waste Gas

generated at the

Carbon Black Plant

Waste Gas

Incineration

Waste Gas Co- Electricity

Internal Plant

Requirement

Surplus

power sold to

76 MW green power generating capacity

� The power business enjoys EBITDA margins of ~90 percent in the

absence of raw material cost. Its increasing presence in PCBL’s

revenue profile is likely to provide a cushion to the overall EBITDA

margins and reduce the dependence of PCBL’s earnings from

carbon black.

Source: Company, SKP Research

Exhibit: Revenue & EBIT Breakup

95.9%

3.8%

Revenue Split (FYRevenue Split (FYRevenue Split (FYRevenue Split (FY12121212))))

Carbon Black Power

59.4%40.6%

EBIT Split (FYEBIT Split (FYEBIT Split (FYEBIT Split (FY12121212))))

Carbon Black Power

Strong clientele base

� The carbon black industry typically has a product mix of 70:30 for

Tyre: Non-Tyre customers. Being present for over five decades in

the industry has enabled PCBL to develop long standing customer

relationship.

� It has a wide range of customers which comprises of prominent and

growing companies like MRF, Apollo Tyres, CEAT Tyres, Good

Year, Bridgestone, Loadstar etc. Long-established relationship with

its clients and diversified client profile helps PCBL to get repeat

orders and also reduces customer concentration risk.

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 10 of 14

Any unfavourable movement in

CBFS prices vis-à-vis carbon black

prices and inability to completely

pass it on to the end consumers will

have an adverse impact on the

PCBL’s margins

Exhibit: Clientele Base

Source: Company, SKP Research

Domestic

Customers

International

Customers

Key Concerns

� CBFS which is the key raw material for PCBL is directly linked to

the international oil prices and is imported from USA. Over the last

couple of year’s international oil prices is on an uptrend and is

subject to frequent volatility while the prices of finished carbon

black are revised every quarter. In order to partially offset its

volatility, PCBL has planned to use coal tar as its raw material.

Though, this might take time as plant is expected to get

commissioned in FY14-15 only. Therefore, any unfavourable

movement in CBFS prices and inability to completely pass it on to

the end consumers will have an adverse impact on the PCBL’s

margins.

Exhibit: CBFS Expense as a %age of Sales

Source: Company, SKP Research

60%

65%

70%

75%

80%

0

3

6

9

12

15

18

FY09 FY10 FY11 FY12

Fig

s in

IN

R B

illio

n

CBFS Expense CBFS Expense as a %age of Sales

� Despite anti-dumping duty on carbon black, import has been

increasing over the past few years. Total imports of carbon black in

India rose to 117,000 MT during FY12 from 70,000 MT in the

earlier year, and the major chunk of imports was from China, at

83,000 MT. As a result, domestic companies resorted to production

cuts during FY12. Thus, the threat of cheap imports always

remains high which may prove detrimental to the interest of PCBL.

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 11 of 14

We maintain a BUY rating with a

price target of INR 148.0/share,

reflecting an upside potential of 39.6

percent from current levels

PCBL historically traded in a narrow

band of 3x to 6x on the one year

forward EV/EBITDA basis, despite

high volatility in earnings on account

of CBFS prices

� The carbon black industry is treated as high pollution emitting

industry by the Ministry of Environment and Forest (GOI). The

Central Pollution Control Board has categorized the carbon black

industry under the highly polluting industry (red category) and

companies need to comply with the norms in this regard. Any

negative impact on the same would impact PCBL growth going

forward.

Valuations

At current market price of INR 106/share, PCBL is trading at an

EV/EBITDA of 4.81x and 4.45x FY13E and FY14E EBITDA

respectively. We valued PCBL’s business at FY14E EV/EBITDA

multiple of 5x. Thus, we arrived at a price target of INR 148/share,

implying an upside potential of 39.6 percent in 18 months.

Target EV/EBITDA Multiple 5.0 x

FY14E EBITDA (INR Million)

Target Enterprise Value (INR Million)

Less: FY14E Debt (INR Million)

Less: Minority Interest (INR Million)

Add: FY14E Cash (INR Million)

Target Market Cap (INR Million)

No of Shares (Million)

Target Price Per Share (INR)

67.1

Exhibit: Value based on FY14E EV/EBITDA

Source: SKP Research

148.0

34.5

5,099.8

295.8

8,371.9

13,243.0

2,648.6

One Year Forward EV/EBITDA Band

Exhibit: One Year Forward EV/EBITDA Band

Source: Company, SKP Research

3

5

7

9

11

13

15

17

19

21

Mar-

09

Jul-09

Oct-

09

Jan-1

0

Apr-

10

Jul-10

Oct-

10

Jan-1

1

Apr-

11

Jul-11

Oct-

11

Jan-1

2

Apr-

12

Jul-12

Oct-

12

Jan-1

3

Fig

s. In

IN

R B

illio

n

7x 6x 5x 4x 3x

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 12 of 14

At CMP, PCBL is trading at 0.54x

and 0.48x its FY13E and FY14E

book value, respectively

At CMP, the stock is trading at 4.3x

and 3.3x its FY13E and FY14E

earnings, respectively

The company is likely to fund most of

its expansion through internal

accruals

One Year Forward P/Bv Band

Exhibit: One Year Forward P/BV Band

Source: Company, SKP Research

0

50

100

150

200

250

300

Mar-

09

Jul-

09

Oct-

09

Jan-1

0

Apr-

10

Jul-

10

Oct-

10

Jan-1

1

Apr-

11

Jul-

11

Oct-

11

Jan-1

2

Apr-

12

Jul-

12

Oct-

12

Jan-1

3

1.2x 1x 0.8x 0.6x 0.4x

One Year Forward P/E Band

Exhibit: One Year Forward P/E Band

Source: Company, SKP Research

0

50

100

150

200

250

300

Mar-

09

Jul-09

Oct-

09

Jan-1

0

Apr-

10

Jul-10

Oct-

10

Jan-1

1

Apr-

11

Jul-11

Oct-

11

Jan-1

2

Apr-

12

Jul-12

Oct-

12

Jan-1

3

6x 5x 4x 3x 2x

Financial Outlook

To fund most of its expansion through internal accruals

Exhibit: CFO & D/E Ratio

Source: Company, SKP Research

0.30.40.50.60.70.80.91.01.11.2

-2.0

-1.0

0.0

1.0

2.0

3.0

FY

11

FY

12

FY

13E

FY

14E

Fig

s. in

IN

R B

illio

n

Cash Flow from Operations (CFO) D/E (x)

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 13 of 14

Exhibit: Balance Sheet

Particulars FY11 FY12 FY13E FY14E Particulars FY11 FY12 FY13E FY14E

Net Sales 16,957.2 21,867.8 23,861.1 27,418.2 Share Capital 332.2 344.7 344.7 344.7

Growth (%) 37.6% 29.0% 9.1% 14.9% Reserve & Surplus 4,760.8 5,727.8 6,418.3 7,315.0

Expenditure 14,744.0 19,796.3 21,613.4 24,769.6 Share Warrants 61.25 - - -

Material Consumed 12,281.7 17,018.0 18,241.8 20,725.4 Shareholders Funds 5,154.2 6,072.4 6,763.0 7,659.7

Power & Fuel Cost 131.1 175.6 179.0 205.6 Secured Loan 3,936.4 4,913.9 5,646.9 6,731.9

Employee Cost 478.2 528.5 596.5 712.9 Unsecured Loan 508.8 1,640.0 1,640.0 1,640.0

Freight Cost 331.1 352.3 400.9 479.8 Total Debt 4,445.2 6,553.9 7,286.9 8,371.9

Admin & Other Exp. 1,521.9 1,721.8 2,195.2 2,645.9 Minority Interest 55.00 67.13 67.13 67.13

EBITDA 2,213.2 2,071.6 2,247.7 2,648.6 Deferred Tax Liability 569.0 728.7 728.7 728.7

EBITDA Margin (%) 13.1% 9.5% 9.4% 9.7% Total Liabilities 10,223.3 13,422.1 14,845.6 16,827.3

Depreciation 385.8 492.5 549.4 586.6

EBIT 1,827.4 1,579.0 1,698.3 2,062.0 Net Block inc Capital WIP 7,847.0 8,444.1 9,675.7 10,181.1

Other Income 209.5 112.1 122.0 131.7 Investments 385.0 376.5 406.6 439.1

Interest Expense 437.5 676.3 692.0 743.8 Current Assets 8,989.2 12,114.4 12,758.6 14,941.6

Profit Before Tax (PBT) 1,599.4 1,014.9 1,128.2 1,449.9 Inventories 2,553.3 3,603.4 3,852.1 4,535.9

Income Tax 480.7 163.1 276.4 351.6 Sundry Debtors 3,625.5 5,473.4 5,542.0 6,477.0

Minority Interest 8.3 4.3 0.0 0.0 Cash & Bank Balance 657.2 152.2 202.9 295.8

Profit After Tax (PAT) 1,127.0 856.1 851.8 1,098.3 Other Current Assets 294.9 188.4 238.6 274.2

Growth (%) -7.8% -24.0% -0.5% 28.9% Loans & Advances 1,858.3 2,697.0 2,923.0 3,358.7

PAT Margins (%) 6.6% 3.9% 3.6% 4.0% Current Liabilities & Prov 6,997.8 7,512.9 7,995.2 8,734.4

Diluted EPS 34.3 25.4 24.7 31.9 Total Assets 10,223.3 13,422.1 14,845.6 16,827.3

Particulars FY11 FY12 FY13E FY14E Particulars FY11 FY12 FY13E FY14E

PBT 1,599.4 1,014.9 1,128.2 1,449.9 Earning Ratios (%)

Depreciation 385.8 492.5 549.4 586.6 EBITDA Margin (%) 13.1% 9.5% 9.4% 9.7%

Interest Provided 356.6 582.8 692.0 743.8 PAT Margins (%) 6.6% 3.9% 3.6% 4.0%

Chg. in Working Capital (213.9) (2,781.8) (111.1) (1,350.8) ROCE (%) 19.1% 13.4% 12.0% 13.0%

Direct Taxes Paid (243.3) (199.8) (276.4) (351.6) ROE (%) 26.9% 15.3% 13.3% 15.2%

Other Non Cash Charges (14.9) (21.6) - - Per Share Data (INR)

Operating Cash Flows 1,869.7 (913.0) 1,982.2 1,077.9 Diluted EPS 34.3 25.4 24.7 31.9

Capital Expenditure (1,546.8) (938.5) (1,781.0) (1,092.0) Cash EPS (CEPS) 45.3 39.0 40.7 48.9

Investments 0.4 - (30.1) (32.5) BVPS 155.2 176.2 196.2 222.2

Others 61.6 60.8 - - Valuation Ratios (x)

Investing Cash Flows (1,484.9) (877.7) (1,811.1) (1,124.5) P/E 4.3 4.4 4.3 3.3

Inc / (Dec) in Debt (782.8) 1,044.9 733.0 1,085.0 Price/BVPS 0.9 0.6 0.5 0.5

Dividend Paid (inc tax) (192.3) (192.1) (161.3) (201.6) EV/Sales 0.5 0.5 0.5 0.4

Interest Paid (443.3) (596.7) (692.0) (743.8) EV/EBITDA 3.9 5.0 4.8 4.5

Others 1,360.6 1,029.2 - - Dividend Yield (%) 3.4% 3.6% 3.8% 4.7%

Financing Cash Flows (57.9) 1,285.4 (120.3) 139.6 Balance Sheet Ratios

Chg. in Cash & Cash Eqv 326.9 (505.4) 50.7 93.0 Debt - Equity 0.9 1.1 1.1 1.1

Opening Cash Balance 330.3 657.2 152.2 202.9 Current Ratio 1.3 1.7 1.6 1.8

Closing Cash Balance 657.2 151.8 202.9 295.8 Fixed Asset Turn. Ratios 2.8 3.2 3.1 3.3

Source: Company Data, SKP Research

Exhibit: Income Statement Figures in INR Million Figures in INR Million

Exhibit: Cash Flow Statement Figures in INR Million Exhibit: Ratio Analysis

Phillips Carbon Black Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 14 of 14

The above analysis and data are based on last available prices and not official closing rates. SKP Research is also available on Bloomberg, Thomson

First Call & Investext Myiris, Moneycontrol, Ticker plant and ISI Securities.

DISCLAIMER: This document has been issued by SKP Securities Ltd (SKP), a stock broker registered with and regulated by Securities & Exchange Board of

India, for the information of its clients/potential clients and business associates/affiliates only and is for private circulation only, disseminated and available

electronically and in printed form. Additional information on recommended securities may be made available on request. This document is supplied to you solely

for your information and no matter contained herein may be reproduced, reprinted, sold, copied in whole or in part, redistributed or passed on, directly or

indirectly, to any other person for any purpose, in India or into any other country without prior written consent of SKP. The distribution of this document in other

jurisdictions may be strictly restricted and/ or prohibited by law, and persons into whose possession this document comes should inform themselves about such restriction and/ or prohibition, and observe any such restrictions and/ or prohibition. If you are dissatisfied with the contents of this complimentary document or

with the terms of this Disclaimer, your sole and exclusive remedy is to stop using the document and SKP shall not be responsible and/ or liable in any manner.

Neither this document nor the information or any opinion expressed therein should be construed as an investment advice or offer to anybody to acquire, subscribe, purchase, sell, dispose of, retain any securities or derivatives related to such securities or an offer to sell or the solicitation of an offer to purchase or subscribe for

any investment or as an official endorsement of any investment. Any recommendation or view or opinion expressed on investments in this document is not intended to constitute investment advice and should not be intended or treated as a substitute for necessary review or validation or any professional advice. The

views expressed in this document are those of the analyst which are subject to change and do not represent to be an authority on the subject. SKP may or may not

subscribe to any and/ or all the views expressed herein. It is the endeavor of SKP to ensure that the analyst(s) use current, reliable, comprehensive information and obtain such information from sources, which the analyst(s) believes to be reliable. However, such information may not have been independently verified by SKP

or the analyst(s). The information, opinions and views contained within this document are based upon publicly available information, considered reliable at the

time of publication, which are subject to change from time to time without any prior notice. The Document may be updated anytime without any prior notice to anybody. SKP makes no guarantee, representation or warranty, express or implied; and accepts no responsibility or liability as to the accuracy or completeness or

correctness of the information in this Report. SKP, its Directors, affiliates and employees do not accept any liability whatsoever, direct or indirect, that may arise

from the use of the information or recommendations herein. Please note that past performance is not necessarily a guide to evaluate future performance. SKP or its

affiliates, may, from time to time render advisory and other services to companies being referred to in this document and receive compensation for the same. SKP

and/or its affiliates, directors and employees may trade for their own account or may also perform or seek to perform investment banking or underwriting services

for or relating to those companies and may also be represented in the supervisory board or on any other committee of those companies or may sell or buy any

securities or make any investment, which may be contrary to or inconsistent with this document. This document should be read and relied upon at the sole

discretion and risk of the reader. The value of any investment made at your discretion based on this document or income there from may be affected by changes in

economic, financial and/ or political factors and may go down as well as up and you may not get back the full or the expected amount invested. Some securities and/ or investments involve substantial risk and are not suitable for all investors. Neither SKP nor its affiliates or their directors, employees, agents or

representatives/associates, shall be responsible or liable in any manner, directly or indirectly, for information, views or opinions expressed in this document or the

contents or any errors or discrepancies herein or for any decisions or actions taken in reliance on the document or inability to use or access our service or this document or for any loss or damages whether direct or indirect, incidental, special or consequential including without limitation loss of revenue or profits or any

loss or damage that may arise from or in connection with the use of or reliance on this document or inability to use or access our service or this document.

SKP Securities Ltd

Contacts Research Sales

Mumbai Kolkata Mumbai Kolkata

Phone 022 2281 9012 033 4007 7000 022 2281 1015 033 4007 7400

Fax 022 2283 0932 033 4007 7007 022 2283 0932 033 4007 7007

E-mail [email protected] [email protected] [email protected]

Member: NSE BSE NSDL CDSL NCDEX* MCX* MCX-SX FPSB *Group Entities

INB/INF: 230707532, BSE INB: 010707538, CDSL IN-DP-CDSL-132-2000, DPID: 021800, NSDL IN-DP-NSDL: 222-2001, DP ID: IN302646, ARN: 0006, NCDEX: 00715, MCX: 31705, MCX-SX: INE 260707532

![Florida Star. (Titusville, Florida) 1902-04-04 [p 8].ufdcimages.uflib.ufl.edu/UF/00/07/59/01/00620/00204.pdfPhillips position MELBOURNE directions enjoyed reason con-tributed enjoyed](https://static.fdocuments.us/doc/165x107/5fbb3dead70908426903e60e/florida-star-titusville-florida-1902-04-04-p-8-phillips-position-melbourne.jpg)