Philippines Trarisport Sector Review - World Bank€¦ · Philippines Trarisport Sector Review...

74

Report No. 7098-PH Philippines Trarisport Sector Review March 31,1988 Intrastructure Division Country Department II Asia Region FOR OFFICiAL USEONLY Document of the World Bank This document hasa restricted distribution and may be usedby recipients only in the performance of their official duties. Its contents rnay not otherwise be disclosedwith out World Bankauthorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

vuonghuong -

Category

Documents

-

view

215 -

download

0

Transcript of Philippines Trarisport Sector Review - World Bank€¦ · Philippines Trarisport Sector Review...

Report No. 7098-PH

PhilippinesTrarisport Sector Review

March 31,1988

Intrastructure DivisionCountry Department IIAsia Region

FOR OFFICiAL USE ONLY

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents rnay not otherwisebe disclosed with out World Bank authorization.

Pub

lic D

iscl

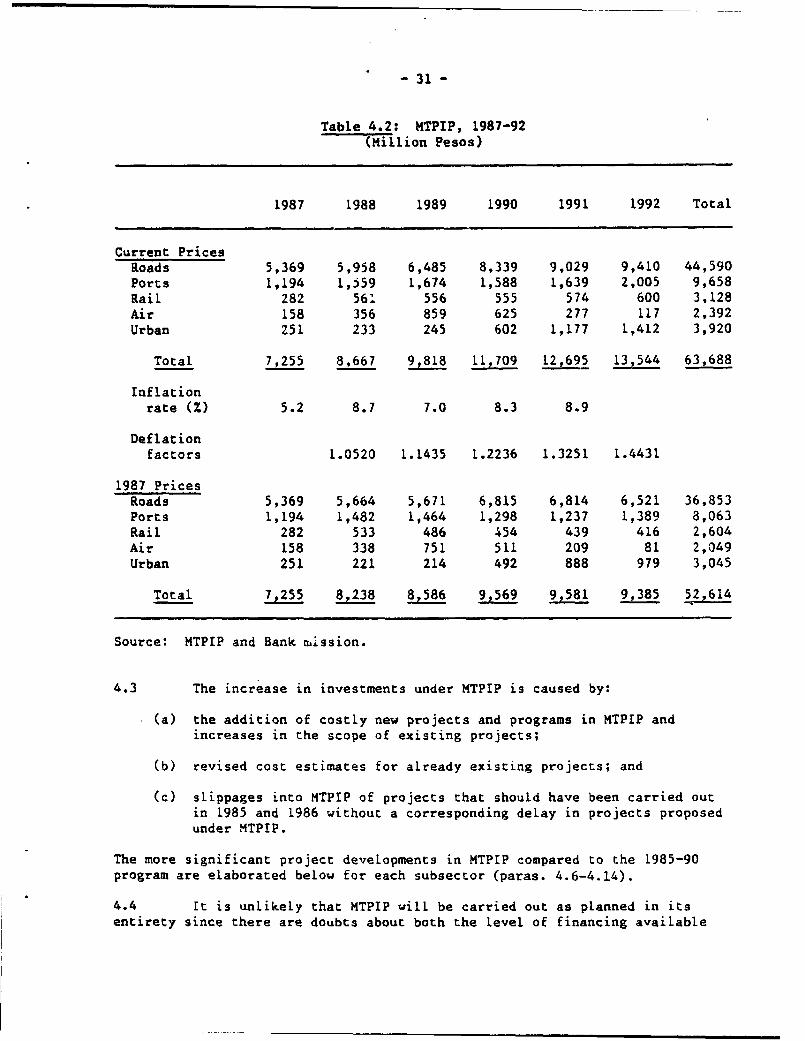

osur

e A

utho

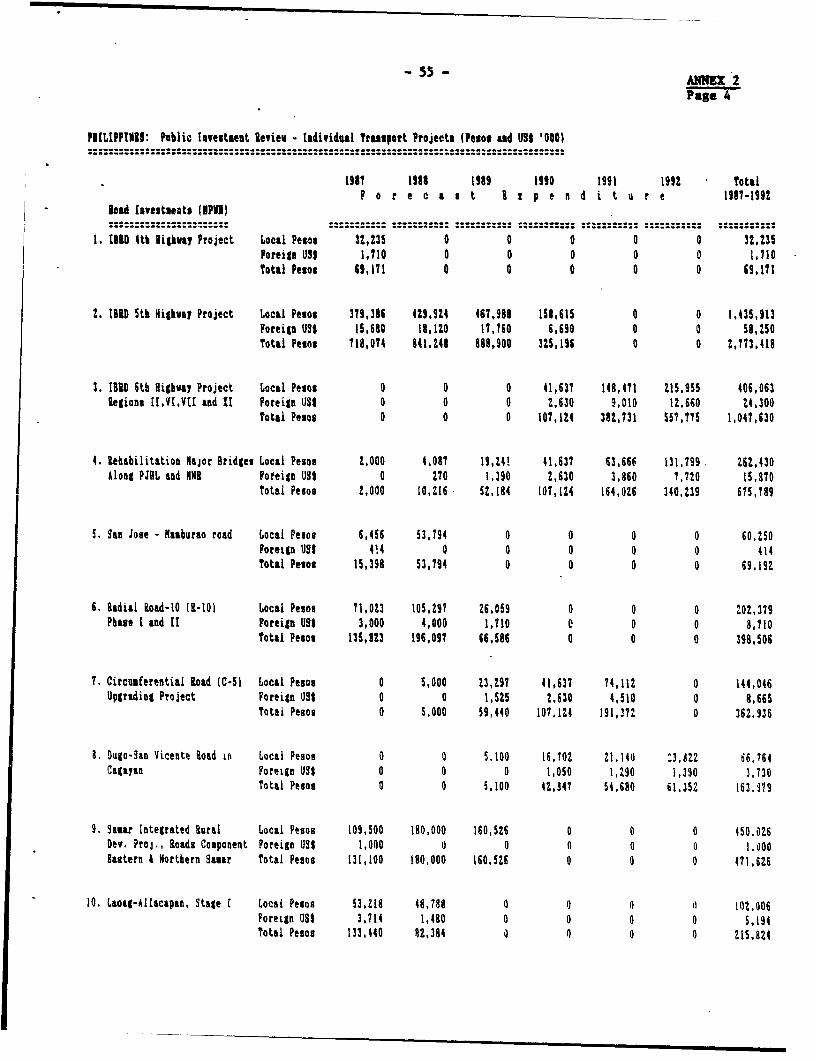

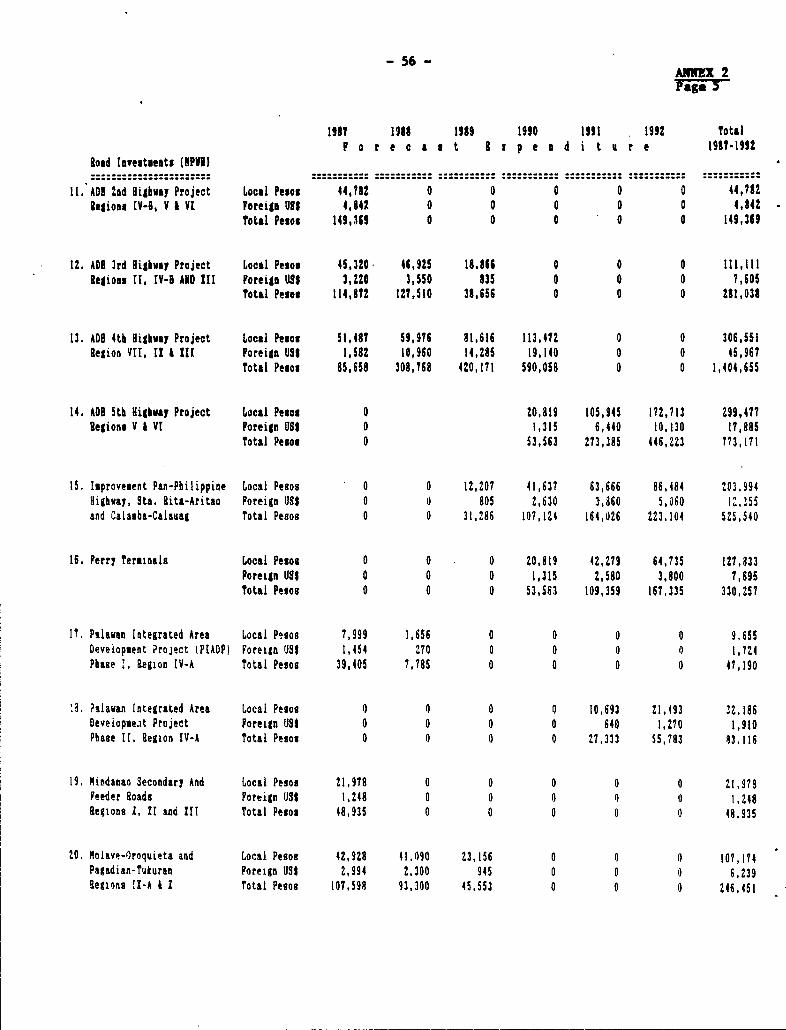

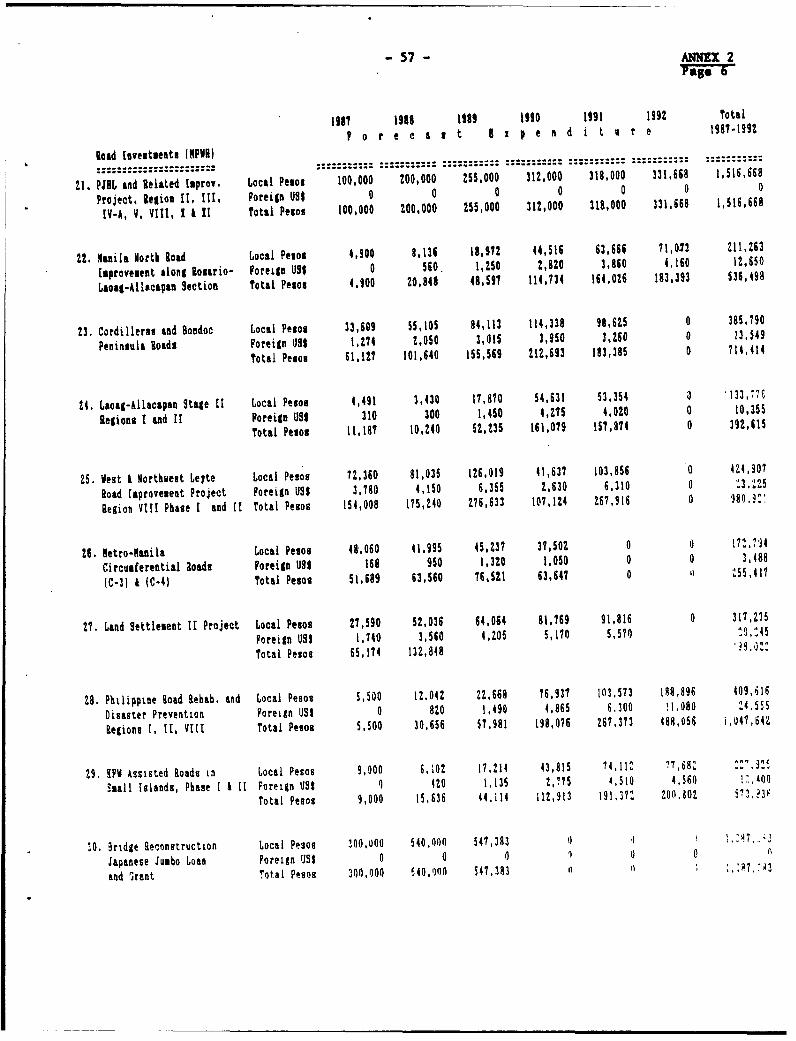

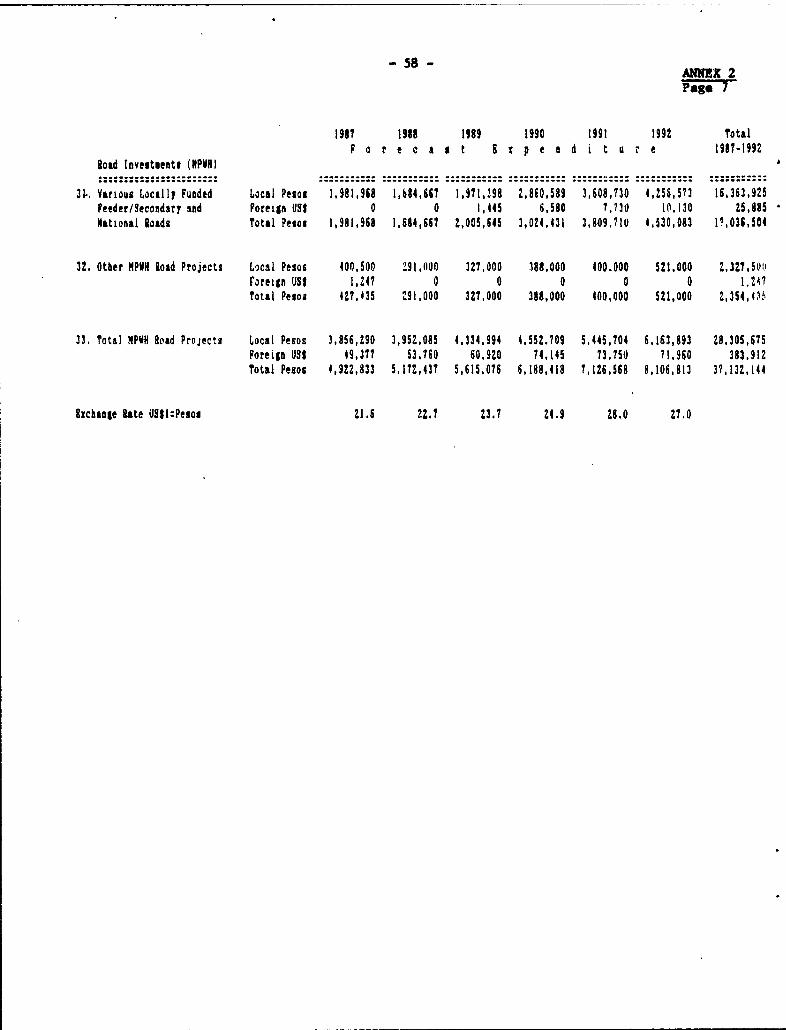

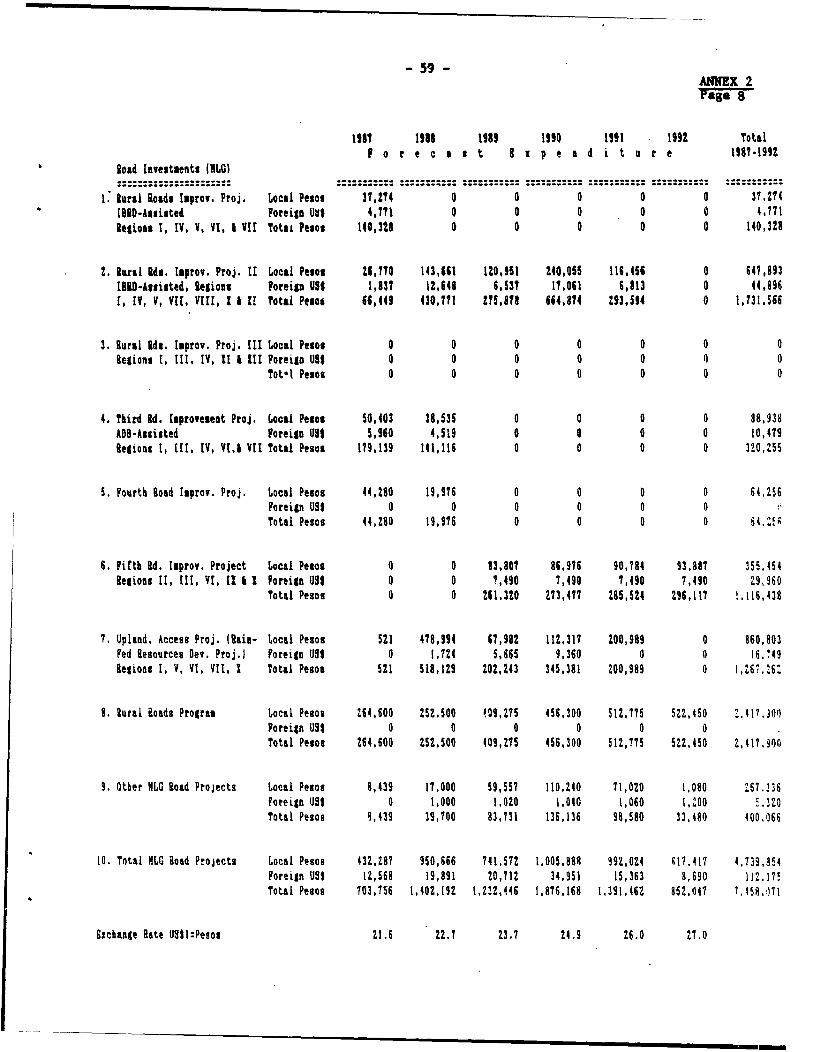

rized

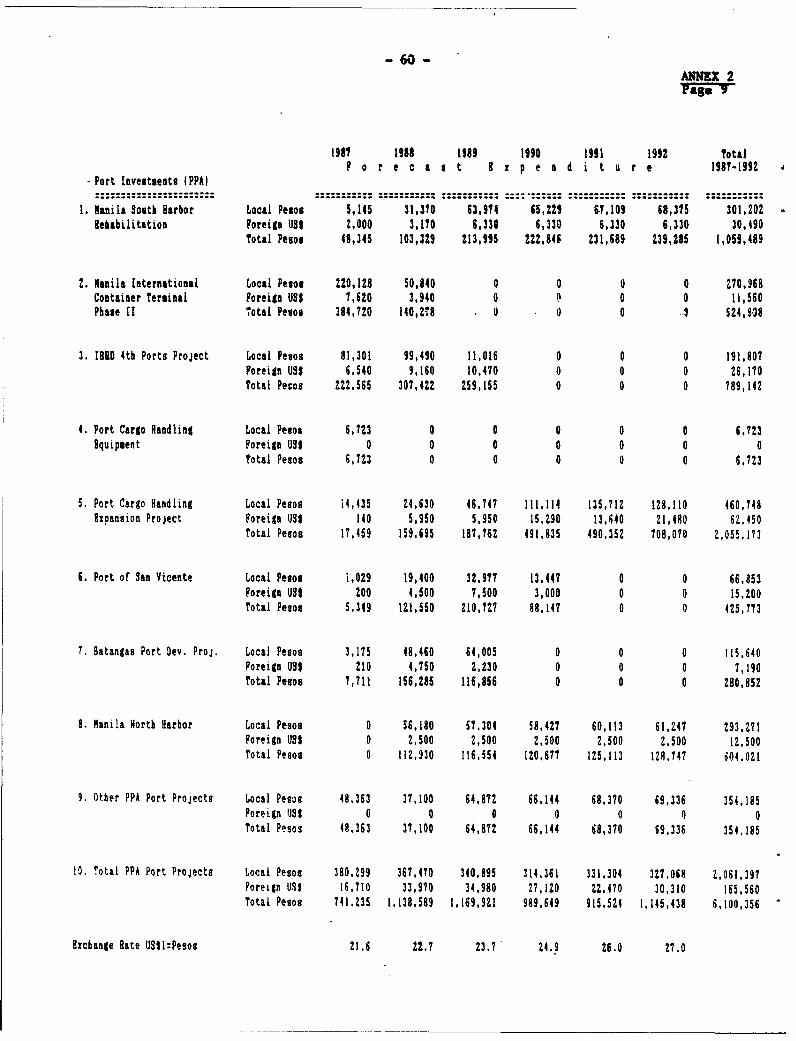

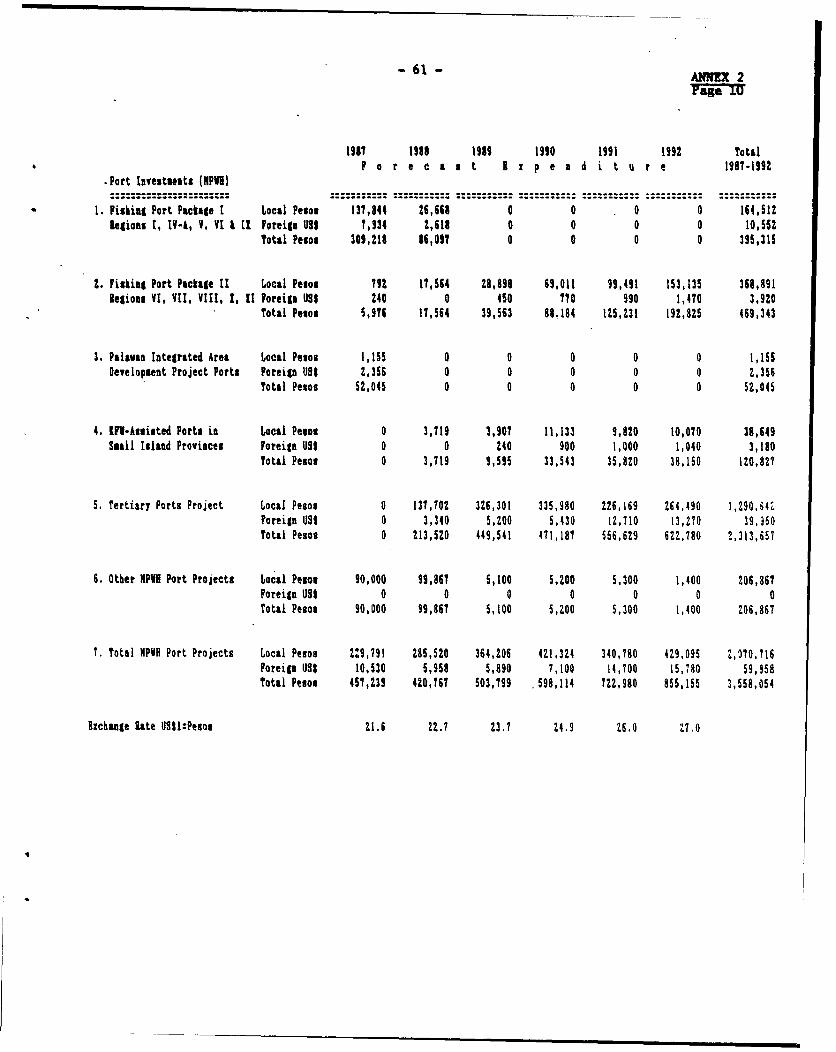

Pub

lic D

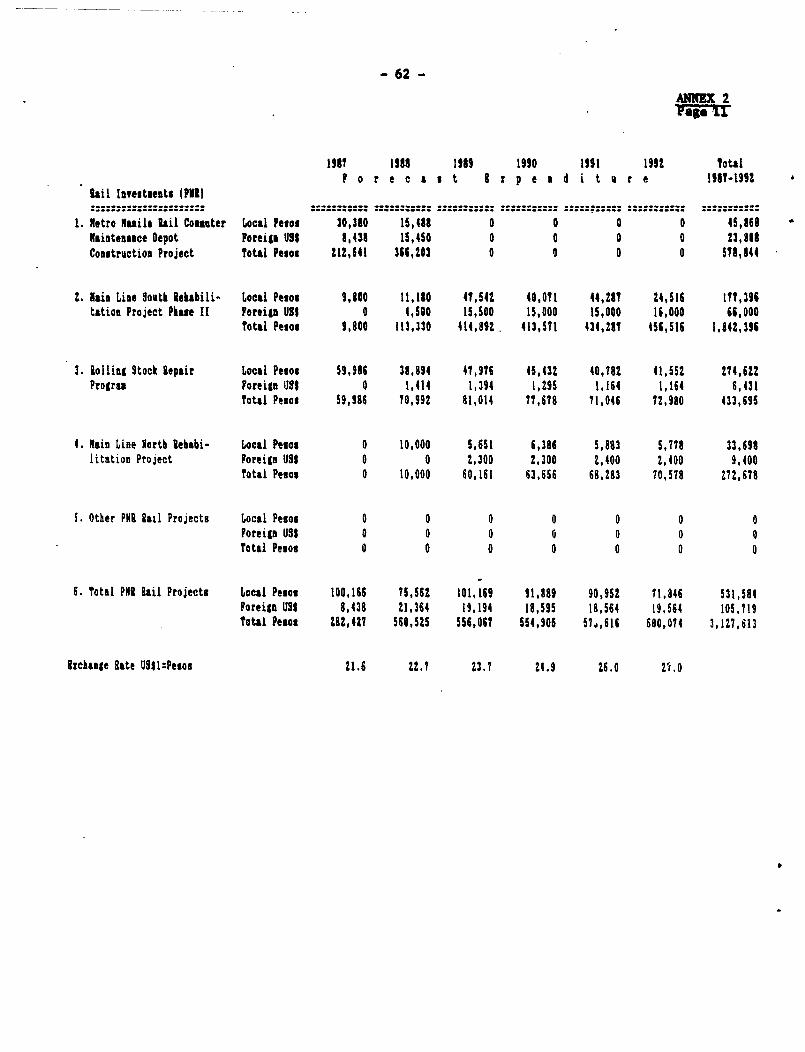

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Year Pesos (P) per US DolLar

1983 11.1

1984 16.7

1985 18.6

1986 20.4

ApriL 1987 20.5

ABBREVIAT IONS

BAT - Bureau of Air rransportation

CAB - Civil Aeronautics Bureau

CCT - Common Carrier Tax

COA - Commission on Audit

CTP - Commitcee on Transport Planning

DLG - Department of Local Government

DOTC - Department of Transport and Communications

DPWH - Department of Public Works and Highways

GVW - Gross Vehicle Weight

LRT(A) - Light Rail Transit (Authority)

LTC - Land Transportation Commission

MARINA - Maritime Industry Authority

MIA(A) - Manila International Airport (Authority)

MMC - Metro Manila Commission

MMTC - Metro Manila Transit Corporacion

MTPIP - Medium-Term Public Investment Program

NEDA - National Economic DeveLopment Authority

NTPP - National Transportation PLanning Project

O&M - Operation and Maintenance

PIP - Public Investment Program

PNR - Philippine National Railways

PPA - Philippine Ports Auchority

ICC - Traffic ControL Center

TRB - ToLl ReguLatory Board

'JRPO - Urban Roads PrK,ect Otfice

JR OMCILu USE ONLY

PHILIPPINES

TRANSPORT SECTOR REVIEW

Table of Contents

Page No.

EXECUTIVE SUMMARYIntroduction .... .... ... ........ ..*. i

Sector Issues and PoLicy Choices ...........................i

Institutional Aspects and Issues . . iv

Public Expenditure Programs in the Transport Sector ......... v

Recomnendations ............................. . vii

I. INTRODUCTION . . . 1

A. Role of the Transport Sector . ............. 1.............. I

B. Previous Bank Sector Work .............................. 2

C. Objectives of the Present Sector Review . . 2

II. SECTOR ISSUES AND POLICY CHOICES . ................... 3

A. Introduction ....... .............................. ....... 3

B. Road Transport .. 3

Optimum Road Transport Technology . . 3

Regulatory Policies ................................... 4

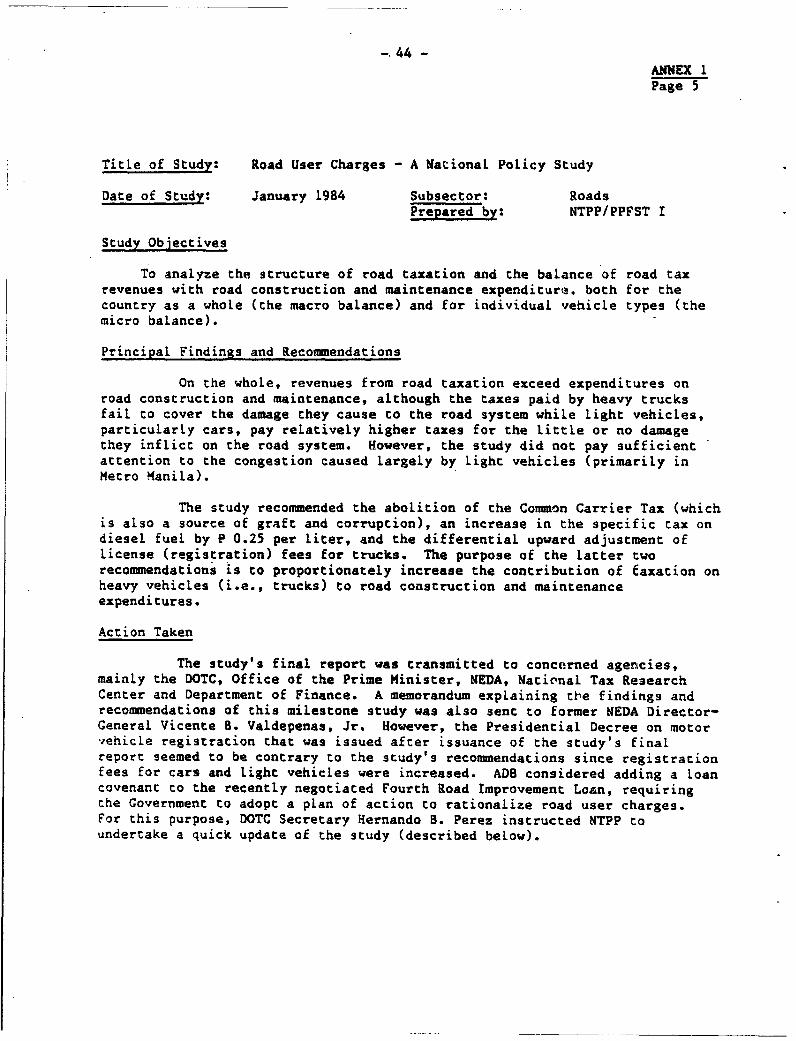

Road User Charges . ................................ 7

Cost Recovery from Road Users ......................... 11

C. Transport in Metro Manila . . .o ........................ 14

Traffic Congestion ... 14

Public Transport ... . ........... 15

D. Interisland Shipping ..... ............. .................. 16

Market Structure . . . 16

Cost and Price of Shipping Services . . . 1 ' 7

Fleet Modernization and Quality of Service ... 19

Maritime Safety . . . 19

Public Policy Recommendations ..... ................... 20

E. Other Modes . ............................................ 21

This report is based on the findings of a transport sector mission thac

visited the Philippines in May/June 1987 consisting of Lars Nordin (Mission

Leader), Clell Harral (Economist), Cerhard Menckhoff (Urban Transport

Specialist), Asif Faiz (Economist) and Mohua Mukherjee (YP Economist).

Contribution has also been made by Lily Uy (Researcher). The report has been

edited by Patricia Brereton-MilLer.

This document has a restricted distribution and may be used by recipients only in the performance

of their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

- ii -

Page No.

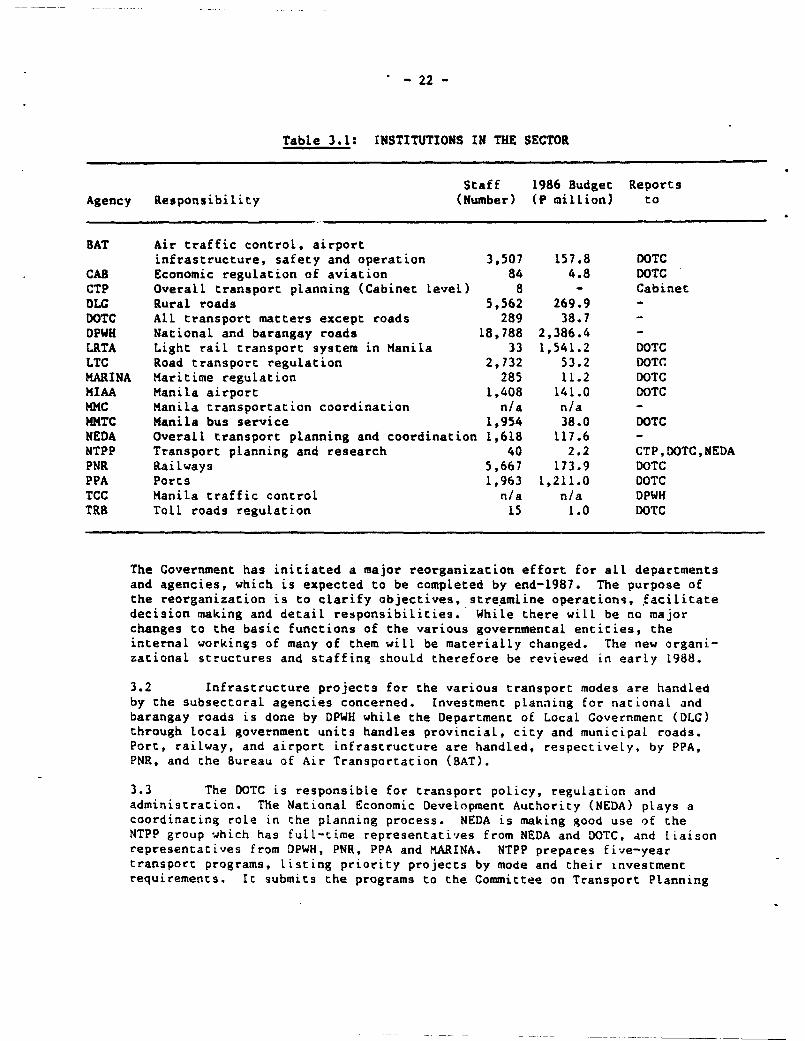

III. INSTITUTIONAL A SPECTS AND ISSUES ......... .......... 21

A. Organizational Setup ................. ....... .... ............. . 21

B. Major Sectorwide Issues ... .. ........ .......... . 23

C. Institutional Issues in the Subsectors .................... 25

Roads ......................... ................... * .......... 25

Urban . ......... , 25

Ports . ... 0.. ... 28

Railways ............... .... . .............................. 28

Aviation . ............ 29

IV. PUBLIC EXPENDITURE PROGRAMS IN fHE TRANSPORT SECTCR ........ .29

A. General ...... .... ..... ... ...... ............... 29

Investments . ................................... . 29

Operation and Maintenance..... ....................... 32

B. Roads ..... 33

Investments .............................. so. 33

Operation and Maintenance ................................ ................ 34

C. Ports ..... ....... o...... o ........ .............................. 34

Investments ........ -.............. ............ % ............ 34

Operation and Mainteadnc e ..................... ..... . 34

D. Railways .. .............. .. 35

E. Aviation ... 35

F. Urban .. ..................................... .......... 35

V. FUTURE ROLE OF THE BANK IN THE SECTOR . ... 35

ANNEXES

1. Sumnaries of Selected Transport Policy Studies

2. Public Investment Program

EXECUTIVE SUMMARY

Introduction

1. The purpose of this review is broadly to assess the impact of recent

economic and public policy developments on the role of the transport sector

in

the Philippine economy. The report particularly focuses on policy,

institu-

tional, and public expenditure developments in the sector that have occurred

since the previous Bank transport sector review in 1983.

2. In its consideration of sectoral policy issues, the report also

reviews key planning and policy studies which have been recently undertaken

by

the Government but which have not always been acted upon. The report

then

identifies those recommendations which are stilL worthwhile in the

current

climate of decentralization and privatization. It is hoped that these

recommendations will form the basis for a short- to medium-term action

plan

still to be developed. On the institutional side, the report identifies

institutional constraints and inadequacies which have arisen over the past

few

years and which prevent the system from functioning as it should.

Finally,

the report reviews the 1987-92 Public Investment Program. Such a review

is

particularly well-timed, given the change in government and the consequent

shift in priorities for public expenditures. The Philippine economy, despite

its scarce resources, appears ;o be poised for a recovery after the

difficult

phase since 1983. Certain public expenditure questions, such as the

balance

between investment and maintenance in the various subsectors, merit

atten-

tion. These issues are tackled in the third section of the report.

Sector Issues and Policy Choices

3. The objectives of public policy in the transport sector should be to

promote a diversity of transport services, responsive to market demands

and

technoLogical innovations in the industry, at as low a cost and price

as

possible. An additional objective is the reduction in economic disparities

across regions and income classes by proper pricing of transport services.

In

accordance with the Government's stated intentions, these objectives

should be

achieved through maximum reliance on the free market, with governmental

intervention limited to the establishment of a policy environment which

encourages the market to work mos; efficiently and to the provision

of

essential infrastructure which the private sector is not well placed

to

provide.

4. The existing policy environment comprises a mixture of diverse and

sometimes ill-conceived laws, regulations and practices accumulated from the

past, which, if rigorously enforced, would undermine the objectives stated

above. From an economic perspective it is fortunate that the existing

policies are often evaded. However, significant distortions exist and

there

is a danger that vested interests will seek enforcement of present

policies to

limit competition.

5. Despite a surprising dearth of quantitative information, a number

of

good sectoral policy studies have recently been completed. Their

recommenda-

tions, if implemented, should substantially improve the functioning of

transportation markets and lead to more efficient and less costly transporta-

tion services.

6. Road Transportation. The National Transportation Planning Project's

(NTPP's) "Study of Road Transportation Regulation" (December 1986) recommends

economic deregulation (i.e., elimination of present restrictions on r-arket

entry and regulation of prices) and emphasizes safety aspects. The present

regulatory restrictions not only pose an enforcement problem, but are also

economically inefficient. Furthermore, there is a clear risk that existing

vested interests in the industry will seek to enforce the regulations in order

to restrict entry and control as much of the market as possible. The Govern-

ment would best protect the public interest by moving gradually but decisively

to dismantle the existing franchise system.

7. Economies of scale in truck size and pavement construction warrant

the development of strong pavements and bridges instead of building weaker

infrastructure and legally restricting the size and axle loads of vehicles.

In addition, enforcement of such restrictions is difficult in almost all

countries. Fortunately in the Philippines, the majority of the primary roads

have been constructed with rigid concrete pavements of high bearing

strength. The proposal in the Department of Public Works and Highways'

(DPWH's) "Pavement and Axle Load Study" (July 1986) to raise legal, limits from

8 to 13 tons therefore appears reasonable.

8. With respect to road user taxation and financing, the conclusions

and recommendations of the NTPP "Road User Charges - National Policy Study"

(January 1984) and an updating report in February 1987 are well founded. The

methodology employed is consistent with the current state-of-the-art and

commonly accepted economic principles of cost recovery in the roads sector.

In the Philippines, it appears that two types of road users are paying less

than the marginal costs they occasion by their use of the roads: (a) 2- and

3-axle trucks, and (b) all vehicles under congested conditions. The proposals

of the study to increase the taxes (on ownership and usage) for 2- and 3-axle

trucks are sound. In addition to cost recovery objectives, these measures

would also contribute to improving efficiency of transport services by

encouraging selection and usage of appropriate vehicles.

9. Congestion pricing is widely endorsed in principle by transport

planners, but rarely applied due partly to practical administrative difficul-

ties and partly to political opposition. The principal exception is road

tolling, which is often implemented for financial reasons but also may serve

the economic purpose of charging for scarce road space. Private automobiles,

due to their numbers and low occupancy ratios, are major causes of conges-

tion. If more specific congestion pricing schemes are not feasible, and

because private automobiles may be viewed as "luxury goods," the current high

taxes on private automobiles should be maintained.

10. Maritime Transportation. The principal concerns in the maritime

sector, so important to economic integration of the country, are the high cost

of interisland shipping and the poor safety record. There appear to be two

principal causes for high shipping costs: (a) existing arrangements for

- iii -

freight handling at ports, and (b) the presence of a cartel in the liner

services indirectLy supported by governmental regulatory policies. The

present policy of the Philippine Ports Authority's (PPA's) acting as Landlord

and procuring stevedoring and Longshore ("arrastre") services by contract is

sound. However, the manner in which this policy has been implemented, in

effect granting quasi-monopolies, could be improved. PPA shouLd create a more

competitive market with alternative suppliers of such services in each port.

PPA port charges to non-PPA ports should also be related more closely to the

services rendered by PPA. As PPA's cost accounting system is improved,

consideration should also be given to gradually abandoning the uniform PPA

charges in all ports in favor of more cost-related port tariffs.

11. The other major factor tending to inflate the costs of inter-island

transport is the pricing practices of the Liner cartel. These are indirectly

supported by the Government's regulatory policies, which limit competition by

restricting market entry and price flexibility. In contrast to the

recommendations of NTPP's "Interisland Shipping Regulation Study" (December

1986), which recommends a form of "seLf-regulation" by the shipping cartel in

collaboration with the Maritime Industry Authority (MARINA) to restrict entry,

it appears that gradual deregulation of the industry, with essentially free

entry (subject only to safety requirements for vessels) and free market

pricing would best serve the interests of the Philippine economy. Reduction

in the various taxes imposed on the import of vessels would also serve to

stimulate innovation and reduce costs of interisland shipping.

12. Safety concerns may be less related to the age and type of vessel

thar to the size and the capabilities of the crews. Maritime safety is one of

the few areas which may need further study to identify the fundamental

determinants and appropriate governmental response.

13. RaiLways. The fundamental question of the financial viability of

the PhiLippine National Railways (PNR) continues to be of concern,

particularly in light of the extremely low volumes of traffic. At minimum, a

radical restructuring of PNR to address those few sectors where it might

possibly render a socially useful service at reasonably competitive costs

appears indicated. The opportunity costs of assets not needed for such

services should also be considered.

14. Urban Transport. The Government's general decentralization poLicy

will transfer many func~.ions from national agencies to the local level. While

the details of the new policy have yet to be worked out, local decision-making

on urban roads and transport regulations deserves support as it is likeLy to

be more responsive to the needs of the peopLe. In Metro Manila, the sheer

size of the population (equivalent to the next 30 largest cities in the

nation) has raised a different set of complex issues.

15. Manila's traffic congestion seems to have improved in recent

years. This is probabLy due to three major factors: (a) traffic engineering

schemes implemented by DPWH's Traffic Control Center, (b) economic recession

and a slight decline in private car ownership, and (c) the introduction of the

Light Rail Transit (LRT), a 16-km long elevated rail line which began opera-

tions in 1984-85. -With an economic recovery, the tra.fic situation could

- iv -

worsen if the pent up demand for cars results in a rapid increase of new car

registration. Moreover, while Metro Manila continues to grow, no major

capacity expansion of the transport system can be expected for at least the

next five years because of the lead time required for such works.

16. Another cause for concern is the weak financial situation of the

Government-owned transport services. It would appear that public transport

services could deteriorate substantially in the coming years if (a) the Metro

Manila Transit Corporation (MMTC) is unable to modernize its aging fleet due

to scarcity of funds; (b) private bus consortia continue to go out of

business, and (c) the moratorium on issuing jeepney licenses is maintained.

17. To avert possible public transport shortages in Manila, a three-

pronged approach should be considered. First, the current policy of bus and

jeepney franchising should be revised to permit new services where the passen-

ger market calls for them. The Department of Transport and Communications

(DOTC) has requested NTPP to prepare a report on this subject by December

1987. Second, the restructuring of bus services to make them commercially

more viable should be considered. Third, planning to substantially upgrade

public transport in at least one high-volume corridor requires urgent

attention. Since a study is currently envisaged for a second LRT line, this

might provide an opportunity to also look at lower-cost alternatives, such as

reserved bus/jeepney roads and, especially, separate busways which might

include short elevated sections to avoid bottlenecks in the street system.

SupporLt shuu'Ld aLso Ue given to the traffic engineering program and the

construction of new road links as envisaged under a proposed Manila Urban

Transport Project to be financed by the Japanese Government.

18. Effective coordination is required to implement a coherent transport

improvement program. At present, most policy and investment decisions are

taken independently by the individual urban agencies. Institutional coordina-

tion will therefore be one of the key issues that must be resolved with regard

to traffic and transport in Metro Manila.

Institutional Aspects and Issues

19. A multitude of institutions collectively provide transportation

services in the Philippines. It has become clear in recent years that a less-

than-efficiently functioning transport system can often be traced to institu-

tional constraints. These have been examined and are observed to fall broadly

into three categories: coordination problems, delays in the processing of

work, and inadequate staffing.

20. Coordination. Responsibility for construction and maintenance of

transport infrastructure is vested in agencies which are not directly

concerned with transport policy, regulation and administration. While there

are merits to such a division of responsibilities, it is important noc to lose

sight of the overall need for coherent planning. Although the National

Economic Development Authority (NEDA) is the key agency carrying out inter-

modal coordination between ports, railways, airports, highways and rural

roads, projects are initiated and evaluated at the agency level, without

regard to their impact on the development of other transport modes. At the

agency level, there is neither an incentive to coordinate activities nor a

built-in mechanism to ensure coordination during the project preparation

period. NEDA's function is, in effect, one of allocating resources for

already prepared projects in all sectors.

21. Delays. Project implementation is often impeded by delays in the

processing of contracts. This problem has be,:ome acute in recent years, when

contract prices have had to be adjusted and price escalations recalculated due

to currency devaluation and inflation. Approvals may take as long as two

years to pass through the government bureaucracy. Part of this problem is due

to a duplication of work by various agencies. The Commission on Audit (COA),

for example, has mandated a review of all feasibility studies for contracts

signed after March 1984, although the review is now done on a selective

basis. Delays are also caused by the sometimes weak quality and competence of

staff involved in the whole decision process. Some of the delays occur simpLy

due to lack of technical expertise at certain management levels to make an

appropriate decision within a reasonable length of time. Thus, the tendency

is to retain documents for longer than required while clarifications are being

sought.

22. Staffing. Staffing and management of the sector agencies is

uneven. While low government salaries make it difficult to recruit and retain

competent staff, this problem has been somewhat alleviated by the general

economic slowdown, which has reduced the "brain drain" toward the private

sector. As a result, working level staff have in large measure remained in

many agencies. On the other hand, and potentially more serious, the number of

managerial positions that have changed incumbents after the change in govern-

ment in February 1986 appears to threaten the proper functioning and conti-

nuity of some of the sector institutions. There is consequently a need for

the Government to strike a proper barance between political and professionaL

career appointments to remedy this situation.

23. Centralization of government authority has added to the inefficien-

cies in project implementation caused by slow contracting processing. While

this problem has been widely recognized, and Government has recently been

moving toward decentralization, success so far has been limiced, owing to a

number of factors. One important issue is the readiness of regional offices

to take over some of the delegated responsibilities and authority.

Decentralization will be successful only if local offices are adequately

staffed with qualified officials. A technical training program for local

staff should therefore be established at the regional/provincial Level. The

quality of local officials also varies greatLy, and many regionaL offices of

both the agencies and COA are reluctant co take on extra responsibiLities.

Public Expenditure Programs in the Transport Sector

24. The October 1986 Medium-Term Public Investment Program (MTPIP) for

1987-92 represents a massive build-up to support economic recovery and agro-

industrial development (82% in real terms) compared to the 1985-90 program,

which was evaluated by the Bank two years ago. The highway subsector would

receive the largest share of MTPIP funding, about 70%, followed by the ports

subsector with about 15%.

- vi -

25. While it is unlikely that MTPIP .will be carried out in its entirety

since there are doubts about both the level of financing available and the

implementation capacity of the respective agencies, the Plan is valuable in

setting implementation objectives. Many of the projects included have

feasibility studies completed, showing economic rates of return sometimes

substantially above the 15% level customarily used in the Philippines for

transport projects. The projects that have not yet uee-i evaluared have been

included in MTPIP based on prima facie viability which will be confirmed in

due course.

26. Operation and Maintenance. Actual operation and maintenance (O&M)

expenditures recorded by the Department of Budget for the period 1.982-86 and

estimated for 1987 show relatively stagnant O&M expenditures up to 1985

(declining in real terms) followed by a substantial 53% increase in 1986. The

Government's O&M expenditures in the transport sector account for about 35% of

total expenditures in 1986 and 1987 co.?ared to about 28% in previous years.

While this percentage increase in itself does not constitute a sufficient

indication that O&M expeneitures are adequate, it does show the increased

relative importance the Government attaches to maintenance. Since O&M expen-

ditures are also increasing in absolute amounts and assuming that the

increased levels can be maintained during the 1987-92 period, this would help

reduce the backlog of deferred maintenance in the sector.

27. Subsectoral Issues. The majority of investments proposed for the

road subsector seem justified. The only component to be watched is the

program for "various locally funded feeder/secondary and national roads,"

which would require 38% of the P 44,590.2 million requested for the road

program and is the principal reason for the large increase of MTPIP over the

1985-90 program. While the objectives are worthwhile, the concern is that

substantial funds may be spent without corresponding physical assets being

created due to capacity constraints in selecting, evaluating, designing and

implementing the huge number of small projects involved. The Covernment

intends to use reliable non-governmental organizations such as religious

groups and the Red Cross to augment its own implementation and monitoring

capabilities for this important program. If these efforts fail to produce the

intended results, the program should be reduced to more manageable levels, say

10-20% of the total road program.

28. The MTPIP port program includes three new projects with a total cost

representing 56% of the P 9,657.8 million port program. All three projects

should be reduced in scope. the projects at issue are (a) the Port Cargo

Handling Expansion Project, (b) the Manila South Harbor RehabiLitation

Project, and (c) the Tertiary Ports Project.

29. The PPA share of the MTPIP ports program also exceeds PPA*s present

investment projections and should be reduced accordingly. The port of San

Vicente (Port Irene) remains questionable and should be postponed until ics

justification has been established.

- vii -

30. PNR has embarked on a revitalization program to regain its opera-

tional levels of the middle 1970s. While the financial viability of the

railway is doubtful, the type of railway investments proposed under MTPIP,

i.e., rehabilitation of motive power, rolling stock and the permanent way,

seem appropriate if PNR's assets are to remain in operational condition.

Expenditures on the northern line should be limited to that part of the line

which is used for passengers commuting in and out of Manila. The rest of the

northern line should be closed. The investment amounts needed depend on how

much equipment can be saved as a result of general operational improvements

being carried out by PNR's new management. Care should be taken against

overinvesting in what has been and will likely continue to be a Loss-making

enterprise, but the risk of underinvesting is not negligible and should be

considered if the railways are indeed to remain in business. The alternative

use of the railways' real estate assets for busways and industrial development

should be an integral part of any discussion regarding the railways' future.

31. In the aviation subsector, the increase in investment is accounted

for by the new Cebu International Airport Development Project which wculd

provide better services for Cebu-bound traffic and would relieve Manila

International Airport of unnecessary transit traffic. While there is no

reason to question the project at this stage, its economic justification

should be established before implementation.

32. The proposed gubstantial. increase in urban investment is caused by

the inclusion in MTrIP of new investr.Lnts in the light rail transport (LRT)

system in Manila. Improvements to line I and design/construction of line 2

are understood to be included, subject to confirmation of their economic

viability. Any study of this matter should also consider the option of

providing lower-cost alternatives to upgrade public transport, such as

dedicated busways.

Recommendations

33. The main recommendations made in the report can be summarized as

follows:

Sectorwide

- Develop a short- to medium-term action plan for the sector

(para. 1.7)- Use explicit subsidies for essential, socially-justified services

racher than implicit subsidies provided by hidden taxes on other

services (para. 2.44)- Review the new sector organizational structure, which is currently

being changed, in early 1988 (para. 3.1)

- Institutionalize a capacity for transport planning and research

(para. 3.2)- Improve coordination among sector agencies (para. 3.4)

- Streamline procedures for approving contracts in order to eliminate

duplicate reviews (para. 3.7)- Improve staff capabilities by carrying out a technical training

program aimed particularly at the regional/provincial levels

(para. 3.9)

- viii -

- Balance political and professional career appointments (para. 3.Q)

The Roads Subsector

- Relate vehicLe taxation to the amount of road damage caused by a

vehicle (paras. 1.5, 2.6)- Increase legal axle load limits (paras. 2.5, 2.13(g))- Make adjustments in the road user tax structure (paras. 2.15, 2.18)

- Clarify responsibility for rural roads development and involve local

staff in maintenance activities (para. 3.11)- Reduce various road investment programs to manageable levels

(para. 4.6)

Road Transport Industry

- Discourage controlled supply of road transport passenger services

(para. 2.11)- Free entry into the road transport industry (para. 2.12)

- Abolish the distinction between own-account (T Licenses) and for-

hire (TH licenses) trucks (para. 2.12)- Decontrol prices of road transport services (para. 2.12)

- Formulate and pursue a program to deregulate the industry

(para. 2.13)- Encourage interisland road/ferry transport (paras. 1.4, 2.12)

- Abolish the Common Carrier Tax which also affects maritime

transport (paras. 2.15(e) and 2.43)

Ports and Maritime Transport

- Carry out a study of maritime safety (para. 2.3)

- Continue efforts to privatize PPA activities (para. 2.32)

- Consider abandoning uniform PPA charges in favor of cost-related

port tariffs (paras. 2.32, 2.42)} - Move gradually but decisively toward free entry into the shipping

industry and deregulation of prices (para. 2.42)- Introduce stricter inspection ot vessel sea worthiness (para. 2.39)

- Remove the Bureau of Customs from involvement in domestic shipping

(para. 2.42)- Review maritime freight rates and port charges (para. 3.22)

- Reduce three proposed port projects (para. 4.9)

The Railway

- Restructure PNR (para. 2.45)- Maintain separace accounts for railway and non-railway operations

(para. 3.24)- Restrict investments on PNR's north line (para. 4.12)

- ix -

Aviation

- Limit the responsibilities of the Manila International Airport

Authority to operation of the Manila Airport (para. 3.27)

- Establish the economic justification for the Cebu International

Airport Development Project (para. 4.13)

Urban Transport

- Carry out studies of congestion pricing for road traffic in urban

areas and of public transport in Manila (para. 2.3)- Expand the traffic engineering program for Metro Manila (para. 2.21)

- Introduce a pricing mechanism for vehicle use in congested areas of

Metro Manila (para. 2.21)- Maintain high cost of car ownership (para. 2.21)

- Coordinate the activities of the agencies responsible for traffic

management in Manila (para. 2.23)- Ease regulatory controls on bus and jeepney franchising and entry

into Manila's passenger transport market (para. 2.24)

- Restructure bus services to improve their financial viability

(para. 2.24)- Plan to upgrade public passenger services in at least one high-

volume traffic corridor in Manila (para. 2.24)- Clarify responsibilities for urban road construction and maintenance

among DPWH, the cities and barangays (para. 3.12)

- Strengthen traffic law enforcement in urban areas (para. 3.15)

- Revive TRANSEC, a recently dissolved transport coordination agency

for Metro Manila (para. 3.18)- Review the policy of giving public support to various bus companies

operating in Metro Manila (para. 3.19)- Review the organizational set up for Manila's Light Rail Transit

Authority and the Metro Manila Transit Corporation (para. 3.19)

- Study the use of dedicated busways to improve mass transit

(para. 4.14)

14. The task at hand is to establish priorities among the many possible

actions that could be taken. While setting of priorities is clearLy the

primary responsibility of the Government, the Bank would view the foLLowing as

major concerns. On economic grounds, the priority policy actions would be

expected to include the gradual deregulation of the trucking and interisland

shipping industries and the restructuring of road user charges. Deregulation

of trucking and shipping would lead to more efficient transport services which

would yield economic benefits to the overall economy. During the impLementa-

tion and adjustment phase, however, it would be necessary to protect both the

industries and their customers from violent swings in the pricing of transport

services.

35. As to priority institutional issues, measures are needed to:

(a) institutionalize a capacity for transport planning and research;

(b) clarify responsibilities for rural roads development;

(c) protect professional career appointments; and

(d) streamline administrative procedures.

Other policy and institutitional recommendations made in the report can be

dealt with simultaneously with or subsequently to the above, depending on the

relative difficulty of achieving the necessary national consensus and legis-

lative agenda.

36. During the next five years, efforts should be made to gradually

shift Bank assistance in the sector away from direct project loans and towards

annual transport sector loans to the Government, with an emphasis on policy

and institutional reform. Such annual sector loans would aLlow maximum

flexibility to include project components for financing as they are developed,

without having to wait for preparation of the next project loan cycle. The

Government and the Bank, in embarking on the proposed new approach to sector

cooperation, will use this report as a source document to catalyze and channel

the sector dialogue and sector development. The extent and timing of the

implementation of the report's recommendations would however, be subject to

the economic, social and political realities in the Philippines.

I. INTRODUCTION

A. Role of the Transport Sector

1.1 The Philippines transport system is composed of about 740 km of

railways, over 161,000 km of roads, 131 national ports, 256 private ports, and

some 400 toading points and 219 airports, of which 82 are national and 137

private. The system is basicaLLy bimodal. Road transport handles about 65X

of freight movement and 90% of passenger movement, while maritime transport

handles about 35% of freight and 7% of passengers. Air transport is very

limited and almost entirely passenger traffic, while railways traffic, both

passenger and freight, is negligible. Road and sea transport generally

complement rather than compete with each other.

1.2 During the 1970s, the transport sector grew at about 9% p.a., faster

than the GDP growth of about 6% p.a. As a result of the country's economic

recession, the GDP growth rate for the 1980s has been negative (-0.3% r..a.),

while the transport sector has been growing at only 1.0% p.a. Government

transport outlays have been about P 4.0 billion p.a.

1.3 The transportation sector plays a significant role in the

Government's macroeconomic goal of national economic integration. This is

refLected in the statement of objectives included in the Medium-Term

Philippine Development Plan (1986):

The transport sector shall support nationwide efforts to stimulate

agricultural production and increase rural incomes by orienting

transport infrastructure towards rural areas. It aims to reduce

interregional socioeconomic gaps and to strengthen interregional

linkages by providing for the more efficient movement of products

from excess production areas to deficit/market areas. A cransport

system that achieves a desired hierarchicaL pattern of growth

centers across the country shall be developed. Greater efficiency

in the use and safety of existing transport facilities shaH. -a.so oe

promoted. This includes a firmer commitment to maintenance activi-

ties and the adoption of low-cost schemes that will enabie the most

effective use of these facilities.

This is a sensible statement of public objectives in the transport sector.

How best to achieve these goals is the issue to be addressed.

1.4 As the Government Plan points out, a better functioning interisland

transportation system is needed for an economy dispersed over 7,000 isLands,

and a smoother movement of goods between farm and market is crucial for

regional development. Due to the development patterns of towns along road

corridors and the Government's poLicy of extending feeder roads to C>.e hinter-

lands, road transport is likely to continue as the dominant mode in the

foreseeable future. However, facilitating inter-island road and ferry trans-

port could make a major contribution to closer economic integration, and would

generate competitive pressures to weaken cartelization tendencies in the

maritime sector.

-2

B. Previous Bank Sector Work

1.5 The Bank's last review of the Philippine transport sector was issued

in September 1983, and the Government has, on its own initiative, implemented

several measures similar to those suggested in that review. In particular, in

the roads subsector, the Department of Public Works and Highways (DPWH) has

increased its maintenance budget from 25Z to 30% of its total expenditures.

In the railway subsector, the Philippine National Railway (PNR) has recently

appointed a strong management team, improved morale, and is making an orga-

nized marketing effort to attract passenger and freight traffic. Regarding

ports, recommendations in the earlier sector review on the rehabilitation and

development of secondary and tertiary ports will be implemented under the

Bank-financed Provincial Ports Project (Loan 2823-PH, 1987). Problems at the

Port of Manila will be addressed under an ADB-financed Second Manila Port

Project. Other areas highlighted under the previous report but still to be

corrected include Government's vehicle taxation system which fails to relate

taxation levels to the amount of damage vehicles inflict on the roads, govern-

ment regulation of the trucking industry which reduces the productivity of the

fleet, and the questionable financial viability of the railway's northern

line.

C. Objectives of the Present Sector Review

1.6 The purpose of the present review is broadly to assess the impact of

recent economic and public policy developments on the role of the transport

sector in the Philippine economy. The report focuses on transport sector

developments on three fronts--policy, institutional, and public expenditures--

that have occurred since the 1983 review.

1.7 In its three-part analysis, the report reviews the major transport

planning and policy studies which have been undertaken recently by the

Government but which have not always been acted upon. It then identifies the

recommendations of those reports which are relevant to the Government's

overall goals of decentralization and privatization. It is hoped that these

recommendations will form the basis for a short- to medium-term action plan

still to be deveLoped. On the institutional side, the report identifies the

key insticutional constraints and inadequacies which prevent the transport

system from functioning as foreseen. Finally, the report reviews the

Government's Public Investment Program in the light of recently emerging

priorities for public expenditures.

-3-

II. SECTOR ISSUES AND POLICY CHOICES

A. Introduction

2.1 As stated in the Medium-Term Philippine Development Plan, Govern-

ment's objectives in the transport sector are to promote a diversity of

transport services, responsive to market demands and technological innovations

in the industry, ac as low a cost and price as possible. An additional

objective is the reduction in income disparities across regions and income

classes. In accordance with the Government's stated intentions, these objec-

tives should be achieved through maximum reLiance on the free market, with

governmental intervention limited to the establishment of a policy environment

which encourages the market to work most efficiently and to the provision

of

essential infrastructure which the private sector is not weLl pLaced to

provide.

2.2 Government's current policies for the sector reflect a mixture of

diverse and sometimes ill-conceived laws, regulations and practices accumu-

lated from the past, which, if rigorously enforced, would undermine the

objectives stated above. From an economic perspective, it is fortunate that

the existing policies are often evaded. However, significant distortions

exist and there is a danger that vested interests will seek enforcement of

present policies to suppress competition wherever possible.

2.3 Despite a surprising dearth of quantitative information, a number of

good sectoral policy studies have recently been completed. Their recommenda-

tions, if implemented, should substantially improve the functioning of trans-

portation markets and lead to more efficient and less costly transportation

services. An annotated bibliography of the major policy studies carried

ouc

since 1982 is provided in Annex 1. Most of the nationwide studies have been

produced by the National Transportation Planning Project (NTPP), the

Government's chief organization for sectoral planning, and DPWH, which over-

sees the technical aspects of all sectoral projects. The studies focused on

Manila were generally prepared by Australian and Japanese consultants and by

the Department of Transportation and Communications (DOTC). In addition,

the

Philippine Chamber of Commerce and Industry has issued important commentaries

on the functioning of the transport system-which provide a valuable perspec-

tive independent of, and often at variance with, official government views.

While the studies provide a solid basis for prompt, decisive action in most

areas, further studies are still needed on: (a) maritime safety; (b) road use

pricing to reduce congestion; and (c) public transport pLanning in

Manila.

B. Road Transport

Optimum Road Transport Technology

2.4 Like studies in other countries (e.g., Sweden, the United States,

Australia and Indonesia), the DPWH "Pavement and Axle Load Study" (July 1986)

has found that, from the perspective of total costs to the society, it is

optimal to employ a range of vehicles, including very large, heavy trucks

operating over strong infrastructure. This is essentially due to economies

of

scale both in truck size and in the design and construction of pavements

and

-4-

bridges. Unlike many other countries, however, much of the existing infra-structure in the Philippines has already been dimensioned to a level which cansustain such heavy loadings. The DPWH estimates that, while the legal axle-load Limit is 8 tons, over 80% of inter-city freight in ton-km moves overinfrastructure which could accommodate axle loads of 13 tons.

2.5 The practice in the Philippines of building many roads with rigidconcrete pavements, to make use of the plentiful suppLy of local cement ratherthan importing asphalt, places the country in a good position to exploit theeconomies of large trucks without the necessity of large capital outlaysrequired for pavement strengthening. NevertheLess, some existing asphalticroads which carry high traffic volumes will need to be strengthened. Moderateoutlays for bridge deck replacement will also be needed, although the extracost necessary to accommodate very heavy vehicles is quite small. Conse-quently, support should be given to DPWH's proposal to increase legal axleload Limits from 8 to 13 tons for single axles, from 14.5 to 23 tons for dualtandem axles and to 30 tons for tridems, at least for high traffic densitycorridors (para. 2.13 (g)).

2.6 To some degree, this proposal merely legitimizes the existingsituation, since economic forces long ago overwhelmed nominal legal restric-tions on axle loads. To go beyond this and capture further benefits of truckfleet modernization, road vehicle taxes should be structured so as to providethe transport industry with the correct relative prices for road use bydifferent vehicLes (see paras. 2.14-2.17). With a change in taxation, themarket can be trusted to determine the optimum vehicle types, sizes and fleetconfiguration.

Regulatory Policies

2.7 Road Transportation. The NTPP's "Study of Road TransportationRegulation" (December 1986) recommends economic deregulation (i.e., elimina-tion of present restrictions on market entry and prices) and emphasizes safetyaspects. The present regulatory restrictions not only pose an enforcementproblem, but are also economically unsound. The market segments most affectedare pubLic passenger transport, petroleum distribution and interisland truck-ing using ferries. Since existing vested interests in the industry are orga-nizing to enforce the regulations in order to restrict entry and control asmuch of the market as possible, Government would best protect the publicinterest by moving gradually but decisively to dismantle the existing fran-chise system. At the same time, however, it should strengthen its safety andpollution regulations.

2.8 Road Freight Services. About 95,000 trucks were registered in thePhilippines in 1986, but less than lOZ held public utility (TH) licensesLegally entitling them to operate for hire. While most trucks haveT-licenses, which are officially valid only for own-account haulage, manyoperate illegal ('colorum') for-hire services. The NTPP "Road Industry Study"estimates that possibly 75Z of trucking services (including own-account) arecarried out by T license holders and 25% by TH licenses; the illegal 'colorum'operators are thought to provide perhaps half the public carrier services.This situation largely results from the distortionary effect of the CommonCarrier Tax, as discussed further in para. 2.15(e) below.

-5-

2.9 The official trucking tariff is currently fixed at P 2.20 per ton-

km, but rates are normally (though illegally) discounted substantially, with

actual rates on the main Luzon routes currently in the range of P 0.60-1.10,

i.e., half or Less of the official rates. Rates on the other islands are said

to be mostly higher, but usually well below the official rate. The official

rate is, however, applied for distribution of petroleum products, thus inflat-

ing fuel costs to all users. Overall average kilometers traveled per truck

are Low, about 40,000-50,000 km per year, reflecting in part the excessive

size of the own-account fleet.

2.10 Road Passenger Services. Passenger transport is provided by

(a) large buses (long-distance or urban services in Manila), (b) minibuses

(medium and Long distance), (c) jeepneys (omnipresent and used not only for

short hauls but also to connect with buses for Longer trips); and (d) motor-

tricycles. The total number of public utility buses and minibuses is esti-

mated at 11,000-12,000, predominantly large vehicles, of which about 7,000-

9,000 are in interurban service. The interurban bus services are operated by

some 1,500 provincial bus operators, of which more than 75% field three or

fewer units, although the 3% of bus operators who manage more than 20 units

account for about 45% of the fleet. Legally licensed for-hire jeepneys (PUJ)

outnumber buses by about 6:1, with PUJ licenses standing at about 66,000.

Moreover, an unknown but highly significant proportion of the privately regis-

tered jeepneys operate either 'colorum' or 'kabit' (by sharing a franchise)

for-hire services. About 130,000 tricycles are also registered to provide

for-hire services. They generally operate along fixed routes in small towns,

rural areas and selected zones in Large cities; they serve short-distance

trips and are commonly overloaded, with up to 10 passengers per vehicle.

2.11 The official tariff, which is tapered by distance, is the same for

buses, minibuses and jeepneys, although each clearly offers a different stan-

dard of service. rn reality, interurban fares charged are normally discounted

(the minibuses more than Large buses, and jeepneys the most discounted). On

some routes where large bus operators are able to agree with each other on

tariffs, there is less discounting. Few routes are cartelized, although fran-

chising practices (such as Route Measured Capacity) of the Government's Land

Transportation Commission (recently spLit into the Land Transportation Office

and the Land Transportation Franchising and Regualatory Board) have activeLv

encouraged such developments, e.g., the route 'rationalization' in East

Mindanao. This type of controlled supply should be discouraged in the future,

as it is contrary to the public interest and leads to sustained high fares.

2.12 Recommendation. The NTPP reports provide a convincing case tor

complete economic deregulation of the road transport industries (with the

possible exception of urban passenger transport which is now also being

studied by NTPP). By freeing market entry, abolishing the nominal distinction

between T and TH licenses, and completely decontrolling prices, substanciaL

gains to the Philippine economy should be realized from improvements in util-

ization of the road transport fleet and reductions in the cost and price of

-6-

transport. By also permitting nationwide operation and eliminating unwarran-

ted stevedoring and warehouse-related "arrastre" charges at ferry crossings,

it is likely that new interisland road services would emerge which could

promote economic and political integration, as well as provide needed competi-

tion in the area of interisland transport.

2.13 The Government would best promote the public interest by moving

gradually but decisively to dismantle the existing regulatory regime.

Although the Committee on Transport Planning (CTP) proposed that deregulation

should initially be Limited to a pilot area, this may give vested interests

the opportunity to marshall forces against deregulation. The Bank therefore

supports the recommendation of the Road Transportation Regulation Study to

implement deregulation nationwide. The key elements of any deregulation

program should be as follows:

(a) quantity licensing and route allocations on interurban bus routes

should be phased out;

(b) government-promulgated fares, rates, and tariffs should be decon-

trolLed and transporters allowed to set their own rates;

(c) entry into the road transport industry should be free and only

subject to a few qualitative requirements;

(d) the differentation in licensing requirements of for-hire (TH) and

own-account (T) trucks should be abolished, and all trucks should

pay the same registration and license fees and other road use taxes;

(e) the importation of vehicles, spare parts, and tires should be

liberalized;

(f) the new Land Transportation Franchising and Regulatory Board should

minimize its role in economic regulation of the road transport

industry. It may be entrusted with anti-trust functions to ensure

that cartels and monopolistic practices do not arise in the trans-

port industry. The key role of the new Land Transportation Office

should be to enhance safety regulations through inspection, testing,

and training programs; and

(g) the Government should review the existing vehicle weights and

dimensions and axle-Load regulations and raise the axle load Limits

progressively in order to more closely reflect actual traffic

Loading conditions. An 11-ton single axle load limit is recommended

for general application with provision of a 13 ton single axle load

Limit on designated high-density corridors with strong pavements and

adequate bridges.

Road User Charges

2.14 The term "road user charges" is used here to mean any indirect tax

or charge levied on the purchase, ownership, and operation of motor

vehi-

cles. It includes "taxes" aimed at generating general revenue for the

govern-

ment, and "road use fees" to recover the cost of road wear or congestion.

Road user charges in the Philippines may be divided into two broad classes

as

follows:

(a) taxes and fees on vehicle ownership--various registration and

license fees, import duties, and sales taxes; and

(b) taxes on use--primarily fuel and sales taxes and import/excise

duties on tires and spare parts.

In addition, a 3% Common Carrier's Tax (CCT) is levied on the revenue

of all

for-hire carriers, and tolls are collected on about 130 km of expressways near

Manila, constituting an additional tax on use.

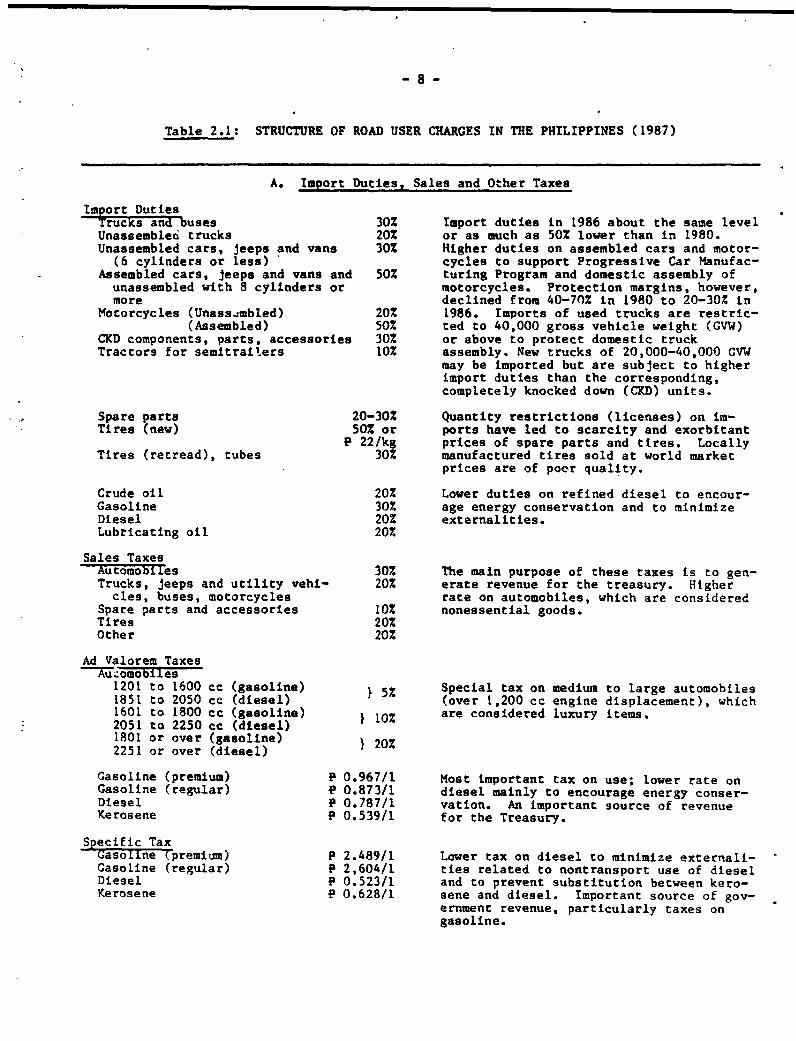

2.15 The structure of the main road user taxes is summarized in

Table 2.1. The various tax instruments serve a variety of objectives, includ-

ing general resource mobilization, energy conservation, income distribution,

and cost recovery from road users. Road user taxation in the Philippines

has

been guided by two primary objectives: raising general revenues for the

Covernment and energy conservation. Efficiency considerations such as

con-

trolling pavement damage and easing congestion are not explicitly considered

in the road user tax structure. Income distribution (ability to pay) and

equity considerations are reflected in automobile and gasoLine taxes,

which

also serve to discourage private car ownership. Some of the anomalous

features in the current road user tax structure are discussed beLow:

(a) The Government's policy of taxing gasoline substantiaLly more than

diesel has resulted in major shifts in the demand for these fuels

and in supply and demand imbalances. However, the current excess

production of gasoline and shortage of diesel can be corrected only

marginally by changes in production. Since the current fuel price

structure (Table 2.2) no longer reflects the relative scarcity of

each product, there is a need to reaLign the prices of automotive

fuels and to reduce the import of refined diesel fuel. In adjusting

its policies, Government should also consider that dieseL engines

have a higher initial cost and Life-cycle maintenance expenses which

to some degree offset their greater fuel economy.

(b) The structure of vehicle registration fees shows a generaL bias

against for-hire commercial vehicles which pay abouc 20-50% more in

annual registration fees than own-account commercial vehicles. This

difference may derive from a perception that for-hire vehicles are

used more intensively and therefore cause more road damage and

congestion than own-account vehicles. However, most own-account

trucks are used for-hire in any case, and there is no evidence that

they are used less intensively. On the other hand, utility vehicles

for private transport (pickups, vans) are taxed at a rate two to

-8-

Table 2.1: STRUCTURE OF ROAD USER CHARGES IN THE PHILIPPINES (1987)

A. Import Duties, Sales and Other Taxes

Import DutiesTrucks and ouses 30% Import duties in 1986 about the same levelUnassemble6 trucks 20% or as much as 50% lower than in 1980.Unassembled cars, jeeps and vans 30% Higher duties on assembled cars and motor-(6 cylinders or less) cycles to support Progressive Car Manufac-

Assembled cars, jeeps and vans and 50% turing Program and domestic assembly ofunassembled with 8 cylinders or motorcycles. Protection margins, however,more declined from 40-70% in 1980 to 20-30Z in

Motorcycles (Unassjmbled) 20% 1986. Imports of used trucks are restric-(Assembled) 50% ted to 40,000 gross vehicle weight (GVW)

CKD components, parts, accessories 30% or above to protect domestic truckTractors for semitrailers 10% assembly. New trucks of 20,000-40,000 GVW

may be imported but are subject to higherimport duties than the corresponding,completely knocked down (CKD) units.

Spare parts 20-30% Quantity restrictions (licenses) on im-Tires (new) 50% or ports have led to scarcity and exorbitant

P 22/kg prices of spare parts and tires. LocallyTires (retread), tubes 30% manufactured tires sold at world market

prices are of pocr quality.

Crude oil 20% Lower duties on refined diesel to encour-Gasoline 30% age energy conservation and to minimizeDiesel 20% externalities.Lubricating oil 20%

Sales TaxesAutomobiles 30% The main purpose of these taxes is to gen-Trucks, jeeps and utility vehi- 20% erate revenue for the treasury. Highercles, buses, motorcycles rate on automobiles, which are considered

Spare parts and accessories 10% nonessential goods.Tires 20%Other 20%

Ad Valorem TaxesAu omobiles1201 to 1600 cc (gasoline) } 5% Special tax on medium to large automobiles1851 to 2050 cc (diesel) (over 1,200 cc engine displacement), which1601 to 1800 cc (gasoline) } 10% are considered luxury items.2051 to 2250 cc (diesel)1801 or over (gasoline) 20%2251 or over (diesel)

Gasoline (premium) P 0.967/1 Most important tax on use; lower rate onGasoline (regular) P 0.873/1 diesel mainly to encourage energy conser-Diesel f 0.787/1 vation. An important source of revenueKerosene P 0.539/1 for the Treasury.

Specific TaxGasoline (premlum) P 2.489/1 Lower tax on diesel to minimize externali-Casoline (regular) P 2,604/1 ties related to nontransport use of dieselDiesel P 0.523/1 and to prevent substitution between kero-Kerosene P 0.628/1 sene and diesel. Important source of gov-

ernment revenue, particularly taxes ongasoline.

Table 2.1: (cont'd)

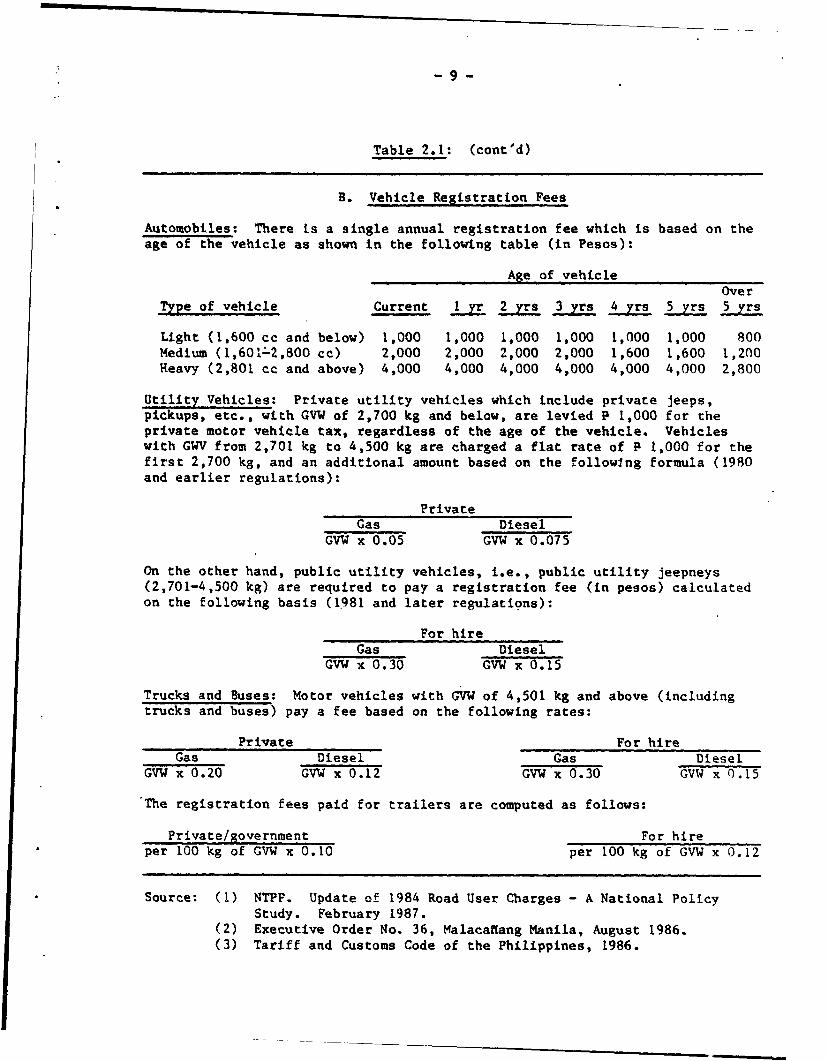

B. Vehicle Registration Fees

Automobiles: There is a single annual registration fee which

is based on the

age of the vehicle as shown in the following table (in Pesos):

Age of vehicleOver

Type of vehicle Current I yr 2 yrs 3 yrs 4 yrs 5 yrs 5 yrs

Light (1,600 cc and below) 1,000 1,000 1,000 1,000 1,000

1,000 800

Medium (1,601-2,800 cc) 2,000 2,000 2,000 2,000 1,600

1,600 1,200

Heavy (2,801 cc and above) 4,000 4,000 4,000 4,000 4,000

4,000 2,800

Utility Vehicles: Private utility vehicles which include private

jeeps,

pickups, etc., with GVW of 2,700 kg and below, are levied

P 1,000 for the

private motor vehicle tax, regardless of the age of the

vehicle. Vehicles

with GWV from 2,701 kg to 4,500 kg are charged a flat rate of

P 1,000 for the

first 2,700 kg, and an additional amount based on the following

formula (1980

and earlier regulations):

PrivateGas Diesel

GVW x 0.05 GVW x 0.075

On the other hand, public utility vehicles, i.e., public utility

jeepneys

(2,701-4,500 kg) are required to pay a registration fee (in

pesos) calculated

on the following basis (1981 and later regulations):

For hireGas Diesel

GVW x 0.30 GVW x 0.15

Trucks and Buses: Motor vehicles with GVW of 4,501 kg and above

(including

trucks and buses) pay a fee based on the following rates:

Private For hire

Gas Diesel Gas Diesel

GVW x 0.20 GVW x 0.12 GVW x 0.30 GVW x 0.15

The registration fees paid for trailers are computed as

follows:

Private/government For hire

per 100 kg of GVW x 0.10 per 100 kg of GVW x 0.12

Source: (1) NTPP. Update of 1984 Road User Charges -

A National Policy

Study. February 1987.

(2) Executive Order No. 36, Malacaffang Manila, August 1986.

(3) Tariff and Customs Code of the Philippines, 1986.

- 10 -

Table 2.2: PRICE BUILDUP FOR PETROLEUM PRODUCTS (FOR METRO MANILA)EFFECTIVE MARCH 1, 1987

(Pesos per liter)

Direct Ad Oil price Wholesalecompany Specific valorem stabiliza- posted Hauling Dealer's Pumprecovery tax tax tion fund price charge markup prices

Premium gas 3.8688 2.489 0.967 (0.709) 6.6158 0.0463 0.2343 6.90

Regular gas 3.4928 2.604 0.873 (0.714) 6.2558 0.0463 0.2249 6.53

AVTURBO 3.8968 2.567 0.974 (0.844) 6.5938

Kerosene 3.8498 0.628 0.539 (0.465) 4.5518 0.0463 0.2102 4.81

Diesel 3.5778 0.523 0.787 (0.404) 4.4838 0.0463 0.2299 4.76

Fuel oil 2.8895 0.511 0.202 (1.098) 2.5045

LP gas 2.5214 0.697 0.353 (0.005) 3.5664

Asphalts 3.3488 0.581 r.469 (0.752) 3.6468

Solvents 3.8118 2.472 0.953 (0.777) 6.4;94

Feedstock 2.8895 0.511 0.202 (1.098) 2.5045

Source: Board if Energy.

- 11 -

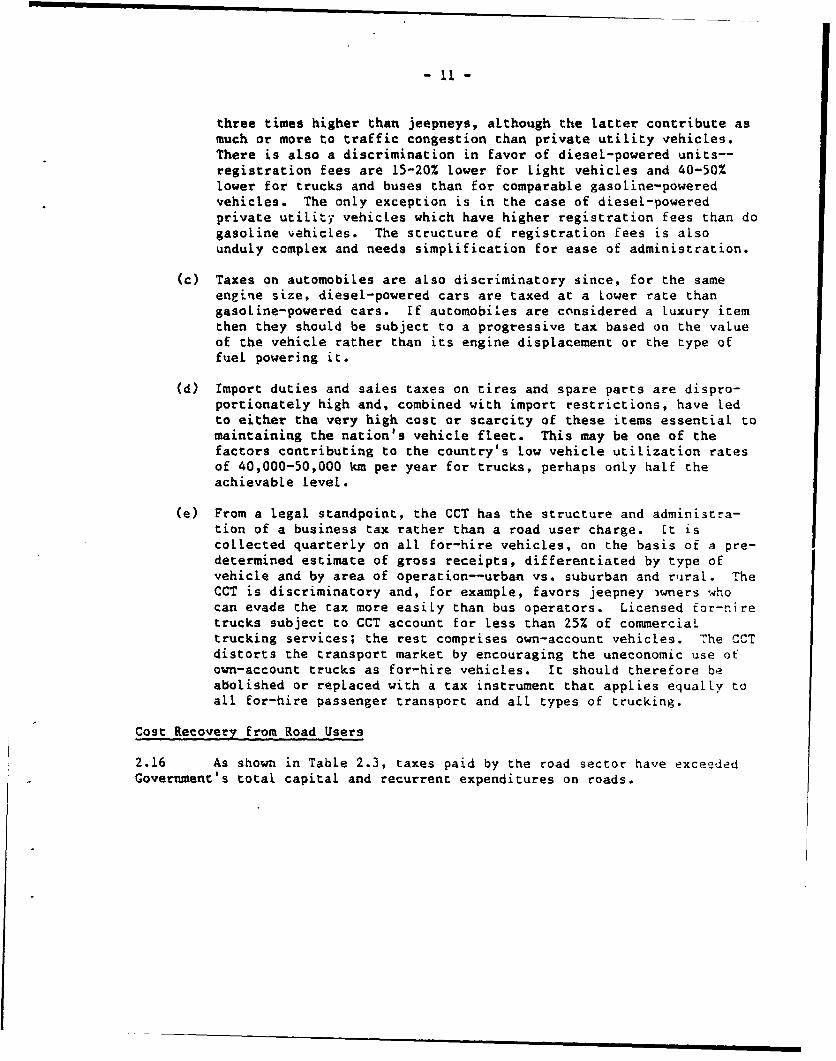

three times higher than jeepneys, although the latter contribute as

much or more to traffic congestion than private utility vehicles.

There is also a discrimination in favor of diesel-powered units--

registration fees are 15-20Z lower for light vehicles and 40-50%

lower for trucks and buses than for comparable gasoline-powered

vehicles. The only exception is in the case of diesel-powered

private utility vehicles which have higher registration fees than do

gasoline vehicLes. The structure of registration fees is also

unduly complex and needs simplification for ease of administration.

(c) Taxes on automobiles are also discriminatory since, for the same

engine size, diesel-powered cars are taxed at a Lower rate than

gasoline-powered cars. If automobiles are considered a Luxury item

then they should be subject to a progressive tax based on the vaLue

of the vehicle rather than its engine displacement or the type of

fuel powering it.

(d) Import duties and sales taxes on tires and spare parts are dispro-

portionately high and, combined with import restrictions, have Led

to either the very high cost or scarcity of these items essential to

maintaining the nation's vehicle fleet. This may be one of the

factors contributing to the country's low vehicle utilization rates

of 40,000-50,000 km per year for trucks, perhaps onLy half the

achievable level.

(e) From a legal standpoint, the CCT has the structure and administra-

tion of a business tax rather than a road user charge. It is

collected quarterly on all for-hire vehicles, on the basis of a pre-

determined estimate of gross receipts, differentiated by type of

vehicle and by area of operation--urban vs. suburban and ruraL. The

CCT is discriminatory and, for example, favors jeepney )wners who

can evade the tax more easiLy than bus operators. Licensed for-r.ire

trucks subject to CCT account for less than 25% of commercial

trucking services; the rest comprises own-account vehicles. The CCT

distorts the transport market by encouraging the uneconomic use ot

own-account trucks as for-hire vehicles. It shouLd therefore be

abolished or repLaced with a tax instrument that applies equalyv to

all for-hire passenger transport and alL types of trucking.

Cost Recovery from Road Users

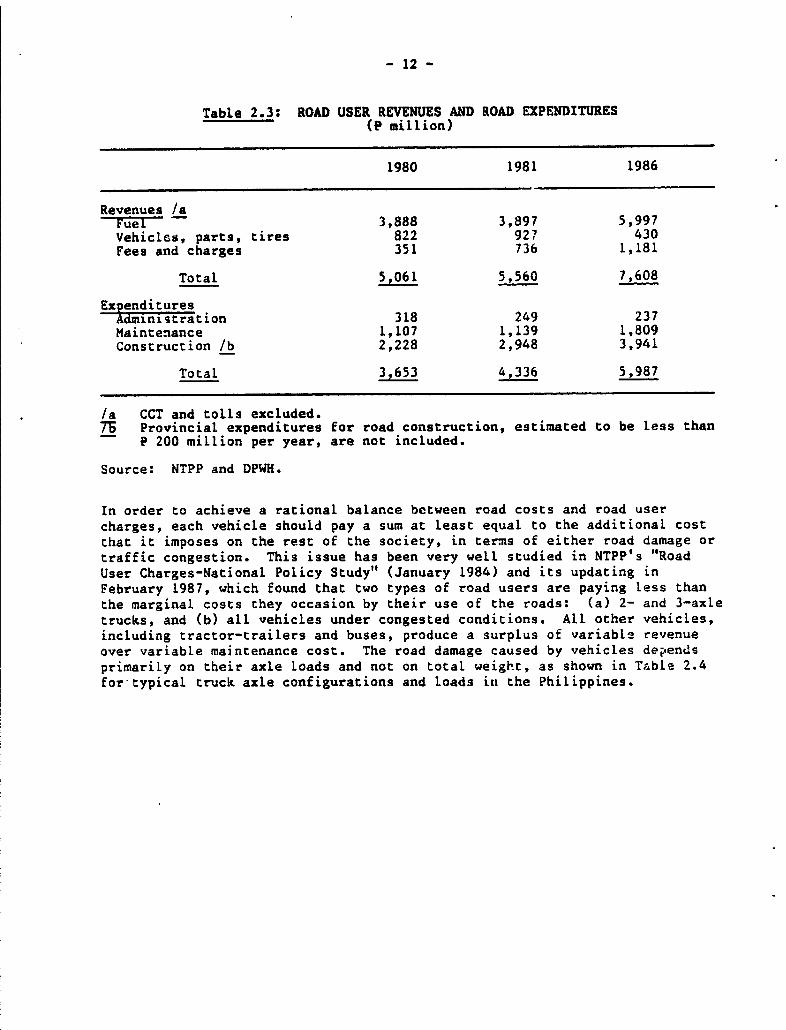

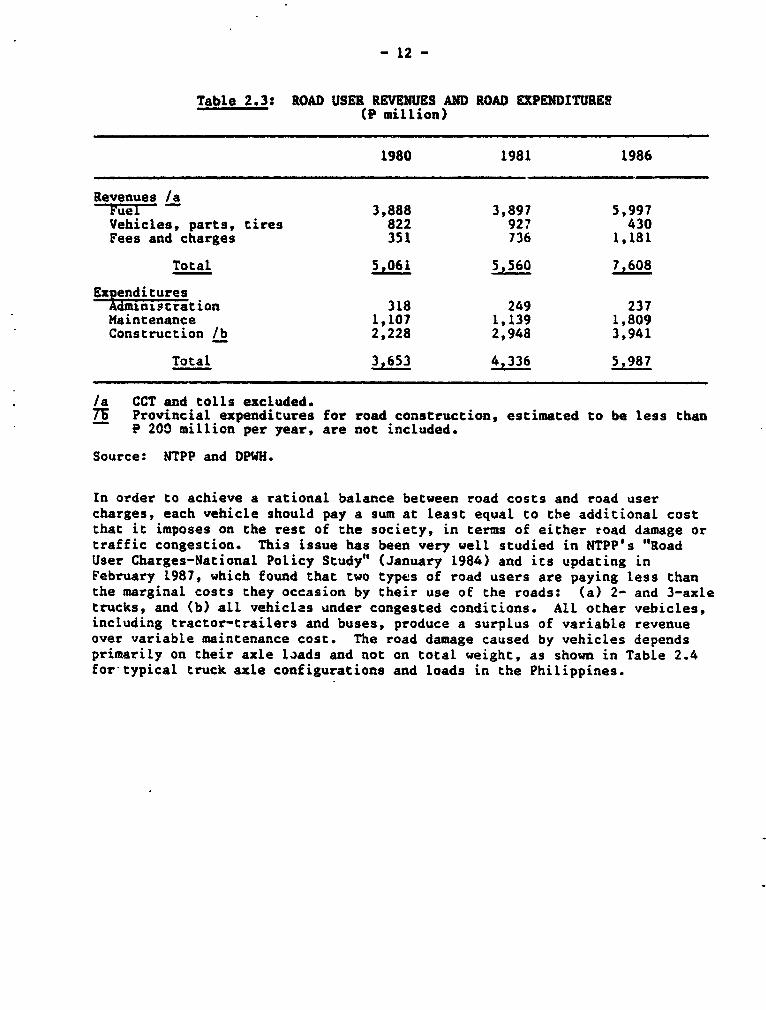

2.16 As shown in Table 2.3, taxes paid by the road sector have exceeded

Government's total capital and recurrent expenditures on roads.

- 12 -

Table 2.3: ROAD USER REVENUES AND ROAD EXPENDITURES(P million)

1980 1981 1986

Revenues /aFu-el 3,888 3,897 5,997Vehicles, parts, tires 822 927 430Fees and charges 351 736 1,181

Total 5,061 5,560 7,608

Ex endituresAdministration 318 249 237Maintenance 1,107 1,139 1,809Construction /b 2,228 2,948 3,941

Total 3,653 4,336 5,987

/a CCT and tolls excluded.7b Provincial expenditures for road construction, estimated to be less than

P 200 million per year, are not included.

Source: NTPP and DPWH.

In order to achieve a rational balance between road costs and road user

charges, each vehicle should pay a sum at least equal to the additional cost

that it imposes on the rest of the society, in terms of either road damage or

traffic congestion. This issue has been very well studied in NTPP's "Road

User Charges-National Policy Study" (January 1984) and its updating inFebruary 1987, which found that two types of road users are paying less than

the marginal costs they occasion by their use of the roads: (a) 2- and 3-axletrucks, and (b) all vehicles under congested conditions. All other vehicles,

including tractor-trailers and buses, produce a surplus of variable revenue

over variable maintenance cost. The road damage caused by vehicles dep'ends

primarily on their axle loads and not on total weight, as shown in Table 2.4

for typical truck axle configurations and loads in the Philippines.

- 12 -

Table 2.3: ROAD USER REVENUES AND ROAD EXPENDITURES(P million)

1980 1981 1986

Revenues /aFu-elr- 3,888 3,897 5,997Vehicles, parts, tires 822 927 430Fees and charges 351 736 1,181

Total 5.061 5,560 7,608

ExtendituresAdministration 318 249 237Maintenance 1,107 1,139 1,809Construction lb 2,228 2,948 3,941

Total 3,653 4,336 5,987

/a CCT and tolls excluded.7T Provincial expenditures for road construction, estimated to be less than

e 200 million per year, are not included.

Source: NTPP and DPWH.

In order to achieve a rational balance between road costs and road usercharges, each vehicle should pay a sum at least equal to tbe additional costthat it imposes on the rest of the society, in terms of either road damage ortraffic congestion. This issue has been very well studied in NTPP's "RoadUser Charges-National Policy Study" (January 1984) and its updating inFebruary 1987, which found that two types of road users are paying less thanthe marginal costs they occasion by their use of the roads: (a) 2- and 3-axletrucks, and (b) all vehiclas under congested conditions. All other vehicles,including tractor-trailers and buses, produce a surplus of variable revenueover variable maintenance cost. The road damage caused by vehicles dependsprimarily on their axle loads and not on total weight, as shown in Table 2.4for typical truck axle configurations and loads in the Philippines.

- 14 -

(b) the current structure of license fees based on GVW should be recali-

brated to an equivalent axle load (EAL) per ton scale, in line with

NTPP recommendations. The schedule of import duties and taxes

should also be modified to promote the use of multi-axle, articu-

lated trucks. Vehicle registration and license fees (road tax)

should be adjusted periodicaLly for inflation and price changes as

well as changes in the structure of the vehicle fleet. The tax rate

should be the same for both for-hire and private trucks;

(c) the structure of road tolls should be reviewed to ensure that toll

administration costs are reasonable and that tolls are contributing

to efficient use of road space;

(d) imports of spare parts and tires should be Liberalized (by removal

of quantity restrictions and Lowering of duties) to avoid distortion

of vehicle replacement choices and increases in vehicLe operation

and maintenance costs; and

(e) the rates of import duties and sales taxes on diesel-powered automo-

biles, pickups, and jeeps should be set higher than those for

comparable gasoline-powered units to minimize the switch from

gasoline to diesel-powered vehicles.

C. Transport in Metro Manila

2.19 The Government's general decentralization policy will transfer many

functions from national agencies to the local Level. While the details of the

new policy have yet to be worked out, local decision-making for urban roads

and transport regulations deserves support as it is LikeLy to be more respon-

sive to the needs of the people. In Metro Manila, the sheer size of the

population (7.3 million or 13Z of the national population and equivalent co

the next 30 largest cities) has raised some particularly complex issues.

Traffic Congestion

2.20 While regulations and institutional responsibilities Eor transport

in Metro Manila are similar to the national pattern, the sheer concentration

of people and activities poses unique problems such as severe traffic conges-

tion, and requires special solutions such as computerized craffic signals or

exclusive-use transitways like the recently compLeted Light Rail Transit

(LRT), a 16-km Long elevated rail line. Traffic congestion in Manila does

seem to have improved in recent years, due to (a) traffic engineering schemes

implemented by DPWH's Traffic Control Center, as well as the rehabilitation

and widening of some urban highways, W4) economic recession and a sLight

decline in private car registrations,- and (c) the introduction of LRT in

1984/85. However, with an economic recovery, traffic couLd easiLv worsen in

the coming years if the pent-up demand for cars results in a rapid increase of

new car registrations. Moreover, while Metro Manila continues to grow by

1/ From 36 cars per 1,000 inhabitants in 1983 to 32 in 1986.

- 15 ̂

about 200,000 persons per year, no major capacity expansion of the transport

system can be expected for at least the next five years because of the lead

* time required for such works.

2.21 To address the probable worsening of traffic conditions, support

should be given to expanding the successful traffic engineering program and

the construction of new road links as envisaged under a proposed Manila Urban

Transport Project to be financed by the Japanese Government. It would also be

timely to consider a pricing mechanism such as tolls or licensing schemes for

driving in congested times and areas, which would charge vehicle users for the

congestion they cause. Unfortunately, experience elsewhere has shown that it

is extremely difficult to gain public acceptance for congestion pricing on

urban streets and, although well-conceived s Pemes have been designed for

several major cities, only two such schemes - have actually been introduced

while the others have been shelved for the time being. Thus, while the con-

cept of pricing vehicle use should be actively pursued at the technical and

political levels (because of its enormous economic benefits), it is suggested

that, because private automobiles are the major causes of congestion due to

their numbers and low occupancy ratios and may be viewed as luxury goods,

traffic growth should be restrained through high pricing of car ownership, at

least until a major congestion pricing scheme is introduced in ManiLa.

Public Transport

2.22 Prospects for public transport in Manila are, under prevailing

conditions, not good. In 1986, LRT had a deficit of P 240 million, of which

about 75Z was interest charges, and the Metro Manila Transit Corporation

(MMTC), which operates the city's largest bus fleet, had an estimated operat-

ing loss of P 39 million (if bus depreciation is revalued to account for

exchange rate shifts since 1980 when the present fleet was acquired). In

addition, three of the ten private bus consortia operating at the beginning of

1987 have since gone out of business and others are expected to follow. It

thus appears that public transport services could deteriorate substantially in

the coming years if (a) MMTC is unable to modernize its aging fleet due to

scarcity of funds, (b) private bus consortia continue to withdraw services,

and (c) a current moratorium on issuing jeepney licenses is maintained and

enforced.

2.23 Transport in Manila is also constrained by the policy of jeepney

franchising which aims to balance supply with estimated passenger demand along

any given route. While the economic rationale for this regulation is unclear,

a restrictive franchising policy can be justified on the grounds that an

oversupply of relatively space-consuming jeepneys (compared to buses) should

be avoided to reduce traffic congestion. This would imply that franchising

should depend on the spare traffic capacity along any given thoroughfare--a

criterion that, surprisingly, is not currently considered in jeepney franchis-

. 2/ Operating since 1)75, the Singapore Area Licensing Scheme is widely

regarded as a major success. More recently, the city of Bergen, Norway,

has implemented a congestion pricing scheme.

- 16 -

ing regulations in Manila. At present, the emphasis is on the commercial

aspects of jeepney operation rather than jeepney-caused congestion. This is

due to a division in institutional responsibilities. DOTC regulates jeepneys,

as other vehicles, to achieve global objectives and is thus not well equipped

to investigate traffic congestion at the local level. DPWH is responsible for

providing an adequate road infrastructure and has therefore created its

Traffic Control Center which has been successful in checking Manila's traffic

congestion. An effective public transport policy requires close integration

of route franchising and traffic engineering, and thus a close coordination

(if not merging) of the agencies responsible for those functions.

2.24 To avert possible public transport shortages in Manila, a three-

pronged approach might be considered. First, revise the current policy of bus

and jeepney franchising, probably by easing the regulatory controls to perm;t

new services where the passenger market calls for them; DOTC has already

requested NTPP to prepare a report on this subject by December 1987. Second,

restructure the organizational and financial framework of bus services to make

them commercially more viable and reverse their current decline. Third, begin

pLanning for a substantial upgrading of public transport in at least one high-

volume corridor or preferably in a metropolitan system of such corridors. A

study currently envisaged for a second LRT line should be expanded to also

consider lower-cost alternatives, such as reserved bus/jeepney roads and, even

better, separate busways which might include short elevated sections to avoid

bottlenecks in the street system. Support should also be given to the traffic

engineering program and the construction of new road links as envisaged under

the proposed Manila Urban Transport Project.

D. Interisland Shipping

Market Structure

2.25 While data on interisland shipping are somewhat inadequate with

respect to the induscry's structure, scope and functioning, the key features

seem to be as follows. Scheduled liner services seem to account for about

half of total domestic freight movements by water. The remainder are carried

by the largely unreguLated, unscheduled contract carriers (trampers) and

private (own-account) bottoms. Large shippers can use the competitive

services, but smaller shippers must normally rely on the liners. The regu-

lated liner services also provide substantial passenger services, which in