Philippine Strategy: Manufacturing a new growth driver · 2013-11-22 · Deutsche Bank Philippine...

24

Deutsche Bank Philippine Strategy: Manufacturing – a new growth driver Rafael Garchitorena [email protected] +63 2 894 6644 November 2012 All prices are those current at the end of the previous trading session unless otherwise indicated. Prices are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies. Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MICA(P) 072/04/2012.

Transcript of Philippine Strategy: Manufacturing a new growth driver · 2013-11-22 · Deutsche Bank Philippine...

Deutsche Bank

Philippine Strategy: Manufacturing – a new growth driver Rafael Garchitorena [email protected]

+63 2 894 6644

November 2012

All prices are those current at the end of the previous trading session unless otherwise indicated. Prices are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies. Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MICA(P) 072/04/2012.

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

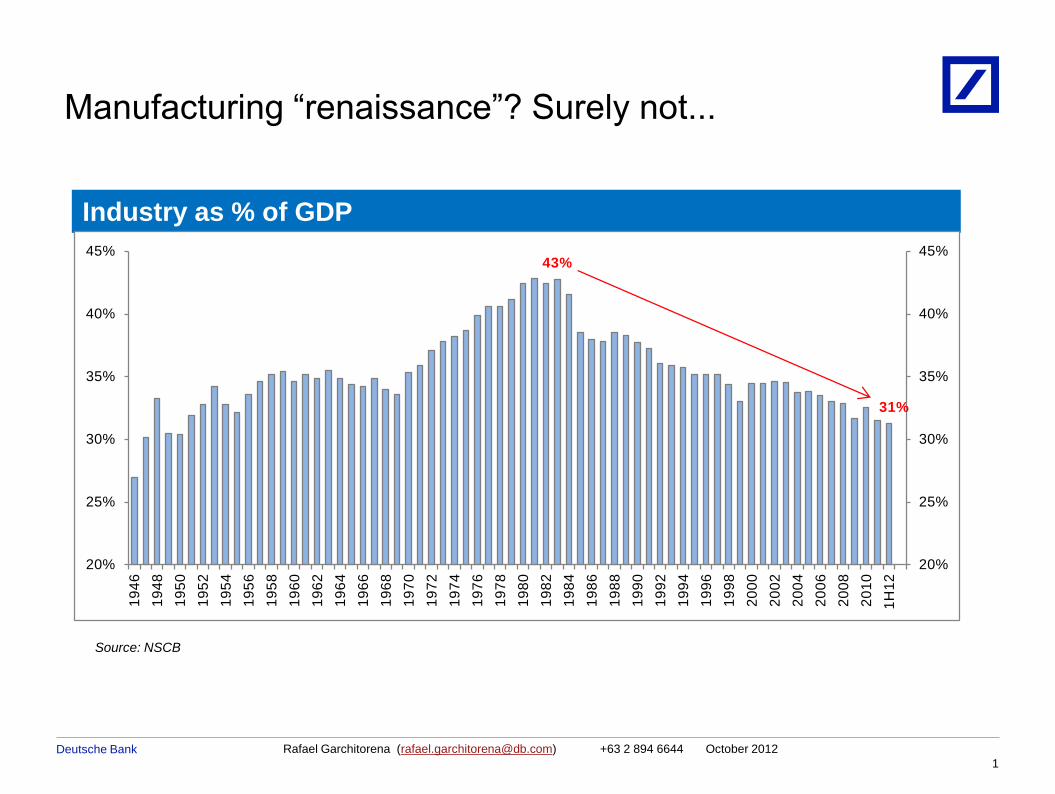

Manufacturing “renaissance”? Surely not...

11/23/2013 2010 DB Blue template

1

Source: NSCB

Industry as % of GDP

43%

31%

20%

25%

30%

35%

40%

45%

20%

25%

30%

35%

40%

45%

19

46

19

48

19

50

19

52

19

54

19

56

19

58

19

60

19

62

19

64

19

66

19

68

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

1H

12

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

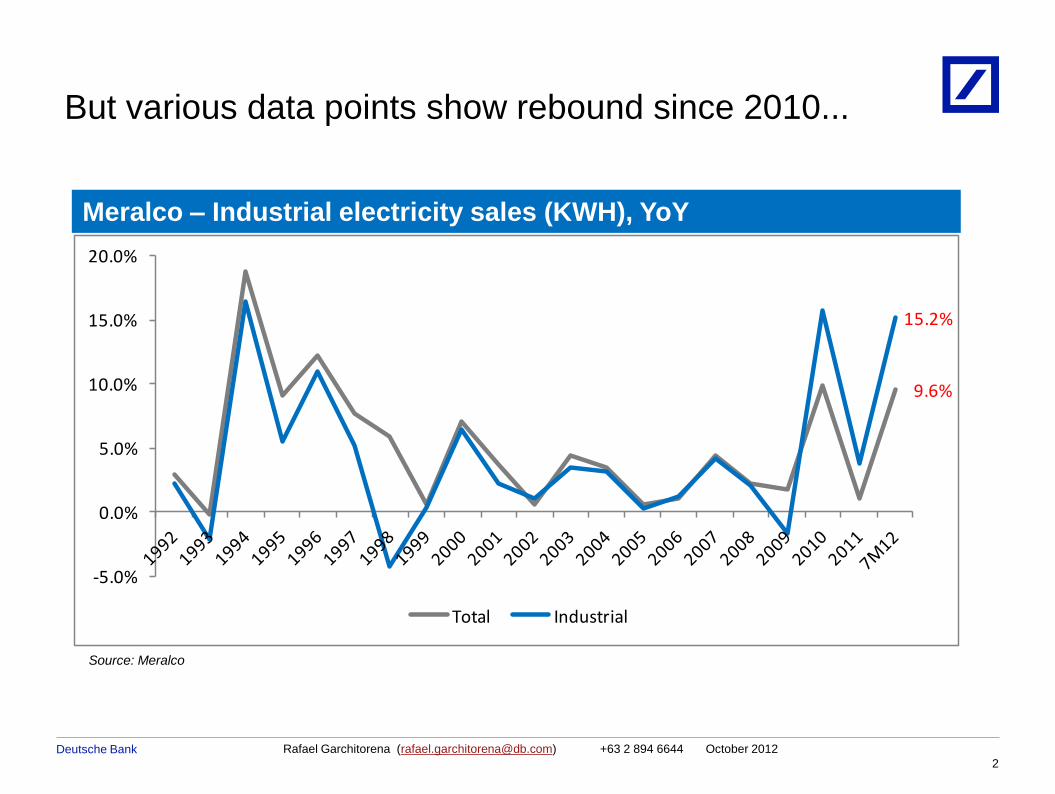

But various data points show rebound since 2010...

11/23/2013 2010 DB Blue template

2

Source: Meralco

Meralco – Industrial electricity sales (KWH), YoY

9.6%

15.2%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

Total Industrial

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

But various data points show rebound since 2010...

11/23/2013 2010 DB Blue template

3

Source: BSP

Manufacturing loan growth, YoY

(30.0)

(20.0)

(10.0)

0.0

10.0

20.0

30.0

40.0 Dec'11

+32%

Jul'12 +25%

Dec'10 +18%

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

But various data points show rebound since 2010...

11/23/2013 2010 DB Blue template

4

Source: NSO

Export growth, YoY

44%

12%7%

-7%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

2006 2007 2008 2009 2010 2011 9M12

Mfg, ex-electronics

Manufactured goods

Total exports

Electronics

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

But various data points show rebound since 2010...

11/23/2013 2010 DB Blue template

5

Source: MNTC

NLEX traffic growth, YoY

13%

5%

-1%

-10%

-5%

0%

5%

10%

15%

20%

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

Class 3

Class 2

Class 1

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

Scepticism despite the data...

11/23/2013 2010 DB Blue template

6

DB‟s Michael Spencer, in his comment on exports in Sept

“Philippine exports surprised to the upside... driven mainly by

manufactured goods”

“... but we don’t know why.”

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

IPA-approved investments at all-time high, particularly for manufacturing sector

11/23/2013 2010 DB Blue template

7

Source: NSCB

IPA-approved manufacturing investments

65

178

145

10385

4257

30

54

150 152

9576

106

215

257

0

50

100

150

200

250

300

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Impact to the economy to continue as commitments become capacity

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

• Yokohama tires

• Kao chemicals

• Murata ceramic capacitors

• Terumo Medical products

• Epson printers, projectors

• Austal catamarans, trimarans

• Canon, Brother printers

• Furkawa ignition wiring sets

• Fujifilm optical lenses

• Bandai toys

• B/E Aerospace airline galleys

• Li & Fung garments (??)

News flow in 2012 suggests continued investments

11/23/2013 2010 DB Blue template

8

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

(since Sept 2012 report)

• Sharp to expand Phils capacity (15 Sept)

• Isuzu to expand transmission production in PH (26 Sept)

• China vehicle firm (Foton) mulls PH as SEAsian hub (08 Oct)

• Nestlé allots P5 B for expansion (13 Oct)

• Korean manufacturers eye Phl operations (20 Oct)

• Foreign manufacturers raring to flock to Davao (06 Nov)

• Knowles sets up Cebu plant (09 Nov)

• P&G Plans $50-M Plant Expansion (14 Nov)

• Suzuki inaugurates new motorcycle plant in Laguna, to build

car plant (16 Nov)

News flow in 2012 suggests continued investments

11/23/2013 2010 DB Blue template

9

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

What‟s driving it? Chinese, Thai wage inflation

11/23/2013 2010 DB Blue template

10

Source: DOLE, CEIC

Minimum wage, daily

Daily

minimum

wage USD USD Phils prem USD Phils prem USD Phils prem USD Phils prem USD Phils prem USD Phils prem

2002 5.43 1.85 193% 3.83 42% 2.94 85% 2.47 120%

2003 5.17 2.23 132% 4.27 21% 3.13 65% 2.64 96%

2004 5.35 2.25 138% 4.37 23% 3.49 54% 2.91 84%

2005 5.90 2.35 151% 4.41 34% 3.83 54% 1.95 203% 2.28 159% 2.94 100%

2006 6.82 3.08 122% 5.19 31% 4.28 59% 3.03 125% 3.26 109% 3.73 83%

2007 7.84 3.30 138% 5.66 38% 5.04 56% 3.96 98% 3.99 97% 4.26 84%

2008 8.59 3.09 178% 5.84 47% 6.30 36% 5.08 69% 5.25 64% 5.84 47%

2009 8.02 4.07 97% 6.08 32% 6.39 25% 5.15 56% 5.32 51% 5.92 35%

2010 8.47 4.59 84% 6.85 24% 7.53 12% 6.39 33% 6.25 35% 6.79 25%

2011 9.84 4.96 98% 6.81 44% 9.02 9% 8.22 20% 7.90 25% 8.71 13%

2012 10.68 5.36 99% 9.72 10% 10.42 3% 8.91 20% 9.48 13% 9.41 14%

China (Hebei,

Jiangsu)

China (Xhejiang,

Tianjin)Indo

Phils

(Manila)

Thai

(Bangkok China (Shanghai)

China (Shandong,

Liaoning,

Indonesia also talking about 40% hike in minimum wages

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

What‟s driving it? Chinese, Thai wage inflation

11/23/2013 2010 DB Blue template

11

Source: DOLE, CEIC

Minimum wage, daily

More competitive by virtue of standing still

0

5

10

15

20

2010 2011 Current

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

.

• Financial Times (26 Sept)

“Mexico: China‟s unlikely challenger”

• DB Indonesia (27 Sept)

“Current Acct Deficit a consequence of investment”

• “Capital goods imports are dominated by machinery equipment.”

• “Even the textile sector... has started to see a resurgence in investment.”

• Time.com (02 Oct)

“Why China must push „reset‟”

• “The average wage for a shop-floor worker in the industry jumped 30% in

2011, to about $350 a month.”

This is a global phenomenon

11/23/2013 2010 DB Blue template

12

Even the US and UK are seeing a resurgence in manufacturing

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

Why Philippines? The investors speak

11/23/2013 2010 DB Blue template

13

Quality of labor

• English-speaking;

• Easy to train (8wks vs 16-24wks for others)

• Worker retention (loyalty), competency

• Quality control

Other factors

• Stable, efficient PEZA; availability and price of industrial land

• Good schools – local and international

• Golf courses

• Respect for intellectual property

• Thai flooding

• China actions re disputed islands

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

Groups pushing for more focused gov‟t policy

11/23/2013 2010 DB Blue template

14

Asian Development Bank

• 2012 report “Taking the right road to Inclusive growth –

Industrial upgrading and diversification in the Philippines”

Federation for Philippine Industry

• Nov 2011 paper, “The importance of the Philippine

Manufacturing Sector”

“Gov‟t Vows To Revive Manufacturing Sector; Crafts

Comprehensive Industrial Roadmap” (Manila Bulletin 21 Oct)

Can the Philippines get (more than) its fair share?

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

Power rates still the highest in the region

11/23/2013 2010 DB Blue template

15

Source: DOE

Industrial electricity tariffs (US$/KWH)

0

2

4

6

8

10

12

14

16

18

20

Philippines Japan Hong Kong Thailand Malaysia Taiwan Sabah Korea Indonesia

Philippines most likely light manufacturing hub

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

The fly in the ointment – strong Peso

11/23/2013 2010 DB Blue template

16

Source: Bloomberg Finance

Peso vs Asian currencies

.

80

85

90

95

100

105

110

80

85

90

95

100

105

110

KRW

CNYMYRPHP

SGD

JPY

80

85

90

95

100

105

110

115

120

125

80

85

90

95

100

105

110

115

120

125

INR

VND

IDR

THBTWS

PHP

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

Banks – as proxy to the investment cycle

• BDO

• Security Bank

• East West Bank

Power – volumes and price

• Meralco TOP PICK

• EDC

Property – industrial land, plus resi/retail support

• Ayala Land

• Filinvest

• Vista

Consumer – employment, spending power

• PureGold

• Alliance Global

The bull lives... even longer!

11/23/2013 2010 DB Blue template

17

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

How can DB and DB-Regis help?

11/23/2013 2010 DB Blue template

18

Debt capital markets – long-term instruments

• 25-yr USD Global sovereign bonds

• 7-15yr corporate debt issues

Access to financial and technical partners

• Global platform – identify technical and financial partners

• Familiarity with local practices to guide their investments

Equity market access

• Deutsche Regis #1 broker by market share

• Stock market at all-time high

No better time than now!

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

23/11/2013 05:52:37 2010 DB Blue template

Appendix 1 Important Disclosures Additional Information Available upon Request

Disclosure Checklist

Company Ticker Price Disclosure

Company number 1

Company number 2

Company number 3

Company number 4

Company number 5

DOUBLE CLICK IN

1. Within the past year, Deutsche Bank and/or its affiliate(s) has managed or co-managed a public or private offering for this company, for which it received fees.

2. Deutsche Bank and/or its affiliate(s) makes a market in securities issued by this company. 3. Deutsche Bank and/or its affiliate(s) acts as a corporate broker or sponsor to this company. 4. The research analyst(s) or an individual who assisted in the preparation of this report (or a member of his/her household) has a direct ownership position

in securities issued by this company or derivatives thereof. 5. The research analyst (or, in the US, a member of his/her household) is an officer, director, or advisory board member of this company. 6. Deutsche Bank and/or its affiliate(s) owns one percent or more of any class of common equity securities of this company. 7. Deutsche Bank and/or its affiliate(s) has received compensation from this company for the provision of investment banking or financial advisory services

within the past year. 8. Deutsche Bank and/or its affiliate(s) expects to receive or intends to seek compensation for investment banking services from this company in the next

three months. 10. Deutsche Bank and/or its affiliate(s) holds more than five percent of the share capital of the company whose securities are subject of the research,

calculated under computational methods required by German law (data as of the last trading day of the past month). 11. See footnote headed Special Disclosures for any other relevant disclosures. 14. Deutsche Bank and/or its affiliate(s) has received non-investment banking related compensation from this company within the past year. 15. This company has been a client of Deutsche Bank Securities Inc. within the past year, during which time it received non-investment banking securities-

related services. 16. A draft of this report was previously shown to the issuer (for fact checking purposes) and changes were made to the report before publication. 17. Deutsche Bank and or/its affiliate(s) has a significant Non-Equity financial interest (this can include Bonds, Convertible Bonds, Credit Derivatives and

Traded Loans) where the aggregate net exposure to the following issuer(s), or issuer(s) group, is more than 25m Euros.

For disclosures pertaining to recommendations or estimates made on securities other than the primary

subject of this research, please see the most recently published company report or visit our global

disclosure look-up page on our website at http://gm.db.com.

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

23/11/2013 05:52:37 2010 DB Blue template

Special Disclosures

Analyst Certification

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

23/11/2013 05:52:37 2010 DB Blue template

Buy: Based on a current 12-month view of total shareholder return

(TSR = percentage change in share price from current price to

projected target price plus projected dividend yield), we recommend

that investors buy the stock.

Sell: Based on a current 12-month view of total shareholder return,

we recommend that investors sell the stock.

Hold: We take a neutral view on the stock 12 months out and, based

on this time horizon, do not recommend either a Buy or Sell.

Notes:

1. Newly issued research recommendations and target prices always

supersede previously published research.

2. Ratings definitions prior to 27 January, 2007 were:

Buy: Expected total return (including dividends) of 10% or more

over a 12-month period

Hold: Expected total return (including dividends) between -10%

and 10% over a 12-month period

Sell: Expected total return (including dividends) of -10% or

worse over a 12-month period

Equity Rating Key

Equity Rating Dispersion and Banking

Relationships

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

23/11/2013 05:52:37 2010 DB Blue template

Regulatory Disclosures 1. Important Additional Conflict Disclosures Aside from within this report, important conflict disclosures can also be found at https://gm.db.com/equities under the “Disc losures Lookup” and “Legal” tabs. Investors are strongly encouraged to review this information before investing.

2. Short-Term Trade Ideas Deutsche Bank equity research analysts sometimes have shorter-term trade ideas (known as SOLAR ideas) that are consistent or inconsistent with Deutsche Bank‟s existing longer term ratings. These trade ideas can be found at the SOLAR link at http://gm.db.com.

3. Country-Specific Disclosures Australia & New Zealand: This research, and any access to it, is intended only for "wholesale clients" within the meaning of the Australian Corporations Act and New Zealand Financial Advisors Act respectively. Brazil: The views expressed above accurately reflect personal views of the authors about the subject company(ies) and its(their) securities, including in relation to Deutsche Bank. The compensation of the equity research analyst(s) is indirectly affected by revenues deriving from the business and financial transactions of Deutsche Bank. EU countries: Disclosures relating to our obligations under MiFiD can be found at http://www.globalmarkets.db.com/riskdisclosures. Japan: Disclosures under the Financial Instruments and Exchange Law: Company name – Deutsche Securities Inc. Registration number – Registered as a financial instruments dealer by the Head of the Kanto Local Finance Bureau (Kinsho) No. 117. Member of associations: JSDA, Type II Financial Instruments Firms Association, The Financial Futures Association of Japan, Japan Investment Advisers Association. Commissions and risks involved in stock transactions – for stock transactions, we charge stock commissions and consumption tax by multiplying the transaction amount by the commission rate agreed with each customer. Stock transactions can lead to losses as a result of share price fluctuations and other factors. Transactions in foreign stocks can lead to additional losses stemming from foreign exchange fluctuations. "Moody's", "Standard & Poor's", and "Fitch" mentioned in this report are not registered credit rating agencies in Japan unless “Japan” or “Nippon” is specifically designated in the name of the entity. Russia: This information, interpretation and opinions submitted herein are not in the context of, and do not constitute, any appraisal or evaluation activity requiring a license in the Russian Federation.

Rafael Garchitorena ([email protected]) +63 2 894 6644 October 2012

Deutsche Bank

Global Disclaimer The information and opinions in this report were prepared by Deutsche Bank AG or one of its affiliates (collectively "Deutsche Bank"). The information herein is believed to be reliable and has been obtained from public sources believed to be reliable. Deutsche Bank makes no representation as to the accuracy or completeness of such information.

Deutsche Bank may engage in securities transactions, on a proprietary basis or otherwise, in a manner inconsistent with the view taken in this research report. In addition, others within Deutsche Bank, including strategists and sales staff, may take a view that is inconsistent with that taken in this research report.

Opinions, estimates and projections in this report constitute the current judgement of the author as of the date of this report. They do not necessarily reflect the opinions of Deutsche Bank and are subject to change without notice. Deutsche Bank has no obligation to update, modify or amend this report or to otherwise notify a recipient thereof in the event that any opinion, forecast or estimate set forth herein, changes or subsequently becomes inaccurate. Prices and availability of financial instruments are subject to change without notice. This report is provided for informational purposes only. It is not an offer or a solicitation of an offer to buy or sell any financial instruments or to participate in any particular trading strategy. Target prices are inherently imprecise and a product of the analyst judgement.

As a result of Deutsche Bank‟s March 2010 acquisition of BHF-Bank AG, a security may be covered by more than one analyst within the Deutsche Bank group. Each of these analysts may use differing methodologies to value the security; as a result, the recommendations may differ and the price targets and estimates of each may vary widely.

In August 2009, Deutsche Bank instituted a new policy whereby analysts may choose not to set or maintain a target price of certain issuers under coverage with a Hold rating. In particular, this will typically occur for "Hold" rated stocks having a market cap smaller than most other companies in its sector or region. We believe that such policy will allow us to make best use of our resources. Please visit our website at http://gm.db.com to determine the target price of any stock.

The financial instruments discussed in this report may not be suitable for all investors and investors must make their own informed investment decisions. Stock transactions can lead to losses as a result of price fluctuations and other factors. If a financial instrument is denominated in a currency other than an investor's currency, a change in exchange rates may adversely affect the investment. Past performance is not necessarily indicative of future results. Deutsche Bank may with respect to securities covered by this report, sell to or buy from customers on a principal basis, and consider this report in deciding to trade on a proprietary basis.

Unless governing law provides otherwise, all transactions should be executed through the Deutsche Bank entity in the investor's home jurisdiction. In the U.S. this report is approved and/or distributed by Deutsche Bank Securities Inc., a member of the NYSE, the NASD, NFA and SIPC. In Germany this report is approved and/or communicated by Deutsche Bank AG Frankfurt authorized by the BaFin. In the United Kingdom this report is approved and/or communicated by Deutsche Bank AG London, a member of the London Stock Exchange and regulated by the Financial Services Authority for the conduct of investment business in the UK and authorized by the BaFin. This report is distributed in Hong Kong by Deutsche Bank AG, Hong Kong Branch, in Korea by Deutsche Securities Korea Co. This report is distributed in Singapore by Deutsche Bank AG, Singapore Branch, and recipients in Singapore of this report are to contact Deutsche Bank AG, Singapore Branch in respect of any matters arising from, or in connection with, this report. Where this report is issued or promulgated in Singapore to a person who is not an accredited investor, expert investor or institutional investor (as defined in the applicable Singapore laws and regulations), Deutsche Bank AG, Singapore Branch accepts legal responsibility to such person for the contents of this report. In Japan this report is approved and/or distributed by Deutsche Securities Inc. The information contained in this report does not constitute the provision of investment advice. In Australia, retail clients should obtain a copy of a Product Disclosure Statement (PDS) relating to any financial product referred to in this report and consider the PDS before making any decision about whether to acquire the product. Deutsche Bank AG Johannesburg is incorporated in the Federal Republic of Germany (Branch Register Number in South Africa: 1998/003298/10). Additional information relative to securities, other financial products or issuers discussed in this report is available upon request. This report may not be reproduced, distributed or published by any person for any purpose without Deutsche Bank's prior written consent. Please cite source when quoting.

Copyright © 2012 Deutsche Bank AG