PHILEX MINING CORPORATION · Re: Definitive ... and endorsed the appointment of Sycip Gorres Velayo...

182

COVER SHEET D.JTITIilI] S.E.C. Registration Number PHILEX MINING COR P 0 RAT ION 2 (Compa ny' s Full Name) E (Business Address: No. Street City /Town Province) Atty. Barbara Anne C. Migall os Atty. Salvador Paolo A. Panelo, Jr. Co ntac t Pe r son 8%-9357 to 59 Tel ephone Number of the Contact Person Articl e third ] A mend ed Articles Number/Secti on ______-'T"o" ta "' l'-' Amo unt of Borrowings --::------,--_ _ 1 1 _ Domestic Foreign Month Day Fiscal Year Annual Mee ting Dept. Requiring this Doc. I 1 Total No. of Stoc khol de rs SEC z o- is Definitive Information Stat ement FORM TYPE 1 N{A I Secondary license Type, U Applicable Any da y in June Month Day To be accomplished by SEC Personnel concerned CCI:ITTTTJ File Number Document LD. STAMPS LCU Cashier R emarks « PIs . use black ink for scanning purposes C1\'i1·C_"'-' nmno''' ... I5J'i'f'74/,kon

Transcript of PHILEX MINING CORPORATION · Re: Definitive ... and endorsed the appointment of Sycip Gorres Velayo...

COVER SHEET

D.JTITIilI]S.E.C. Registration Number

PHILEX MINING COR P 0 RAT ION

2

(Company' s Full Name)

E

(Business Address: No. Street City/Town Province)

Atty. Barbara Anne C. MigallosAtty. Salvador Paolo A. Panelo, Jr.

Contact Person

8%-9357 to 59

Telephone Number of the Contact Person

Article third ]

Amended Articles Number/Section

______-'T"o"ta"'l'-'Amount of Borrowings--::------,--_ _ 1 1 _

Domestic Foreign

Month Day

Fiscal YearAnnual Mee ting

~Dept. Requiring this Doc.

I 1Total No. of Stockholders

SEC zo-isDefinitive Information Statement

FORM TYPE

1 N{A I

Secondary license Type, U Applicable

Any dayin June

Month Day

To be accomplished bySEC Personnel concerned

CCI:ITTTTJFile Number

Document LD.

STAMPS

LCU

Cashier

Remarks « PIs. use black ink for scanning purposesC1\'i1·C_"'-' nmno'''... I5J'i'f'74/,kon

Migallos 'LunaLaw

MIGALl OS .. LUNA LAW OFfiCES.,.~ 1hf PHlNMA Plaza. 39 Plaza DrMRock'AtlI (tritt!", Matati (ity1210 Philipplnts

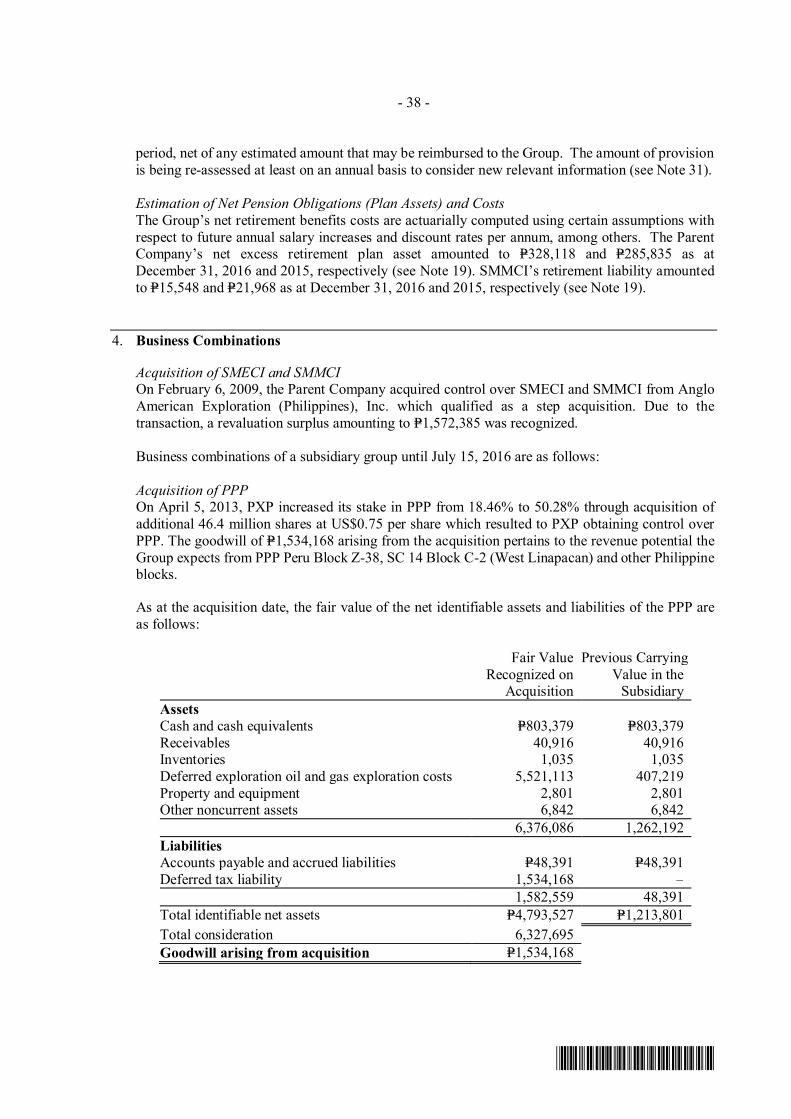

Barbara Annt C. MigallosTroy A. tuna

Ma. (ollCepcion Z. 5.'lfldo\oalSalvador Paolo A. Palltlo. Jr.

DanN IsbIIf F. PaladMa_ ~~ C~

wilt Angtla 1. Basula

SECURITIES AND EXCHANGE COMMISSIONMarkets and Securities RegUlation Departme ntSecretariat Building , PICC Complex,Roxas Boulevard . Metro Manila

P.o. BOI 1116, MCPO 12SO Mal::ati CityT,...,k!int Numb«: (6311 896-9357 to 59Facsimile: 16321 899·1833E-III.1Il: parmersOmigalmiunalaw.comWebsite: www.migalloslunalaw.com

SECURITIES AND E '

mCOMM/SS X.Cf.JANU·'n Tfi1J~~''':'''' lor..; 1:

j J ~ lj>r-,. ...~.-. 1, r:\

\ I 5 20:1 I I ) I

;}1 5 ~ 2017~ I ... /

B' ~"[GUlA TJO· -z...lj,d;_ _ N-'F?r

. - "ME~!Y!i=

Attention: DIRECTOR VICENTE GRACIANO P. FELlZMENO, JR.

MR. EDWIN ARCEO

Re: Defin itive Infonnation Sta teme nt for th e 2017 AnnualStockholders' Meeting of Philex Mining Corporation

Gentlemen :

On behalf of our client. PHILEX MINING CORPORATION (the "Company"),enclosed IS the Detmmve tntormanon Statement (' IS") for the Company's 2017 Annua lStockholders' Meeting ("ASM") to be held on 28 June 2017.

Changes and updates from the Preliminary IS filed by the Company on 9 May2017 are underscored in the enclosed Definitive IS for easy reference. The Definit ive ISalso complies with the comments and requirements of this Honorable Commission in itsletter dated 10 May 2017, as follows:

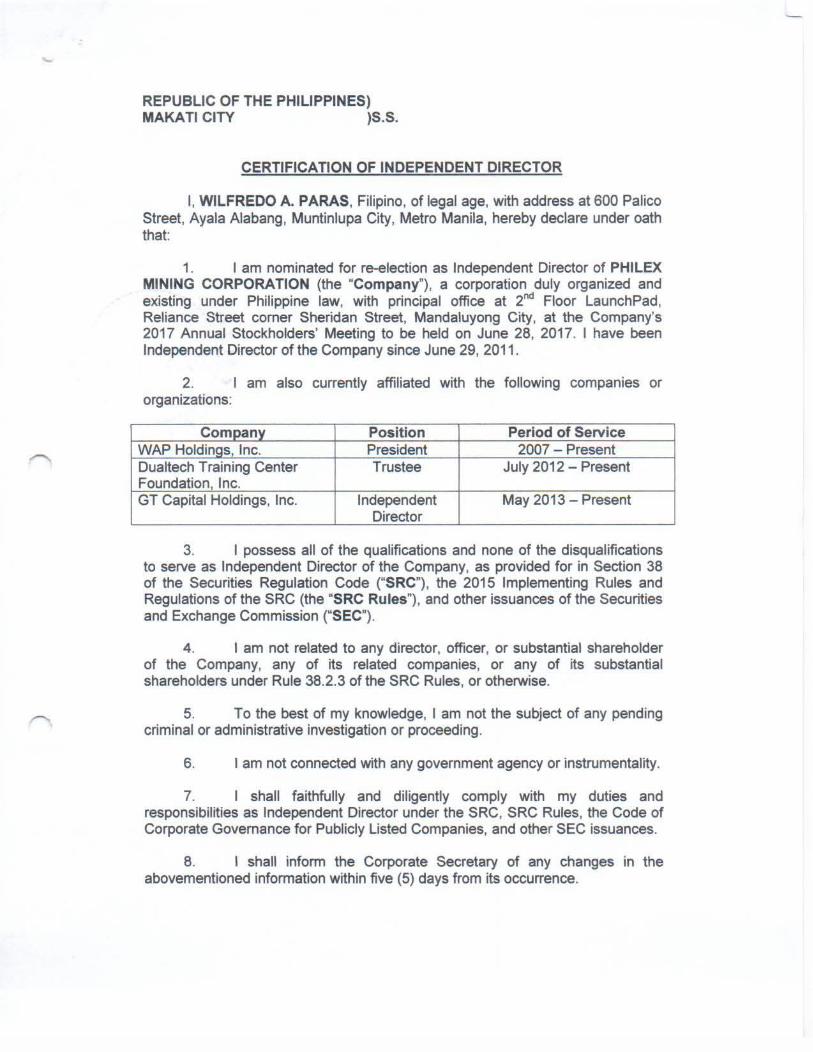

Th e Company was required to submitJ Responsecomoly with the following:1. Certifica te of Qualification of The Certificates of Qualification ofIndependent Director pursuant to SEC Messrs. Oscar J . Hilado and Wi~redo

Memorandum Circular No.5, Series of 2017. A. Paras. nominees for election asIndepend ent Director at the ASM areattached to the Deflnitive IS.

2. Statement of Management Rcsponsjbility The said Statement of Managementon the Financial Statements as prescribed by Responsibility is attached to theSRC Rule 68, as amended by Financial Definitive IS.Reporting Bulletin No. 20.

We trust that you will find the enclosed Definitive IS in order. Should you haveany questions, please contact our Atty. Salvador Paolo A. Panelo, Jr. at 8969357 to 59.

Very truly yours,

a ,JR.

PHILEX MINING CORPORATION

Notice of Annual Meeting of Stockholders

TO OUR STOCKHOLDERS: Please be informed that the Annual Meeting of the Stockholders of PHILEX MINING CORPORATION will be held on June 28, 2017 (Wednesday) at 2:30 p.m. at the Marco Polo Ortigas Manila, Meralco Avenue and Sapphire Street, Ortigas Centre, Pasig City, Metro Manila 1600 (the “Annual Stockholders’ Meeting”). The order of business thereat will be as follows:

1. Call to Order 2. Proof of Required Notice of the Meeting 3. Certification of Quorum 4. Reading and Approval of the Minutes of the June 29, 2016

Stockholders’ Meeting and Action Thereon 5. Presentation of Annual Report and Audited Financial Statements for

the Year Ended December 31, 2016 and Action Thereon 6. Ratification and approval of the acts of the Board of Directors and

Executive Officers during the corporate year 2016 – 2017 7. Approval of the amendment of Article Third of the Company’s Articles

of Incorporation re: the Company’s Principal Place of Business 8. Appointment of Independent Auditors 9. Appointment of election inspectors to serve until the close of the next

annual meeting 10. Election of Directors, including Independent Directors 11. Other Matters A brief statement of the rationale and explanation for each Agenda item which

requires shareholders’ approval is contained in Annex “A” of this Notice. The Information Statement accompanying this Notice contains more detail regarding the rationale and explanation for each of such Agenda items.

For the purpose of the Meeting, only stockholders of record at the close of business of April 10, 2017 will be entitled to vote. Stockholders are requested to bring some form of identification such as passport, driver’s license, or company I.D. in order to facilitate registration, which will start at 1:00 p.m. Shareholders who cannot attend the Meeting may accomplish the Proxy Form enclosed with the Information Statement. Shareholders are requested to indicate their vote (Yes, No, Abstain) for each item in the said Proxy Form, and submit the same on or before June 19, 2017 to the Office of the Corporate Secretary at the Company’s principal office. Secured electronic or online voting will also be available for certificated shareholders. Certificated shareholders who wish to vote online can log on to http://www.philexmining.com.ph/investor-relations/vote-online to cast their online ballots. Online voting instructions are attached to this Notice as Annex “B”.

Copies of the Minutes of the previous stockholders’ meetings are available on

the Company’s website (www.philexmining.com.ph) and will be available for examination during office hours at the office of the Corporate Secretary.

BARBARA ANNE C. MIGALLOS Corporate Secretary

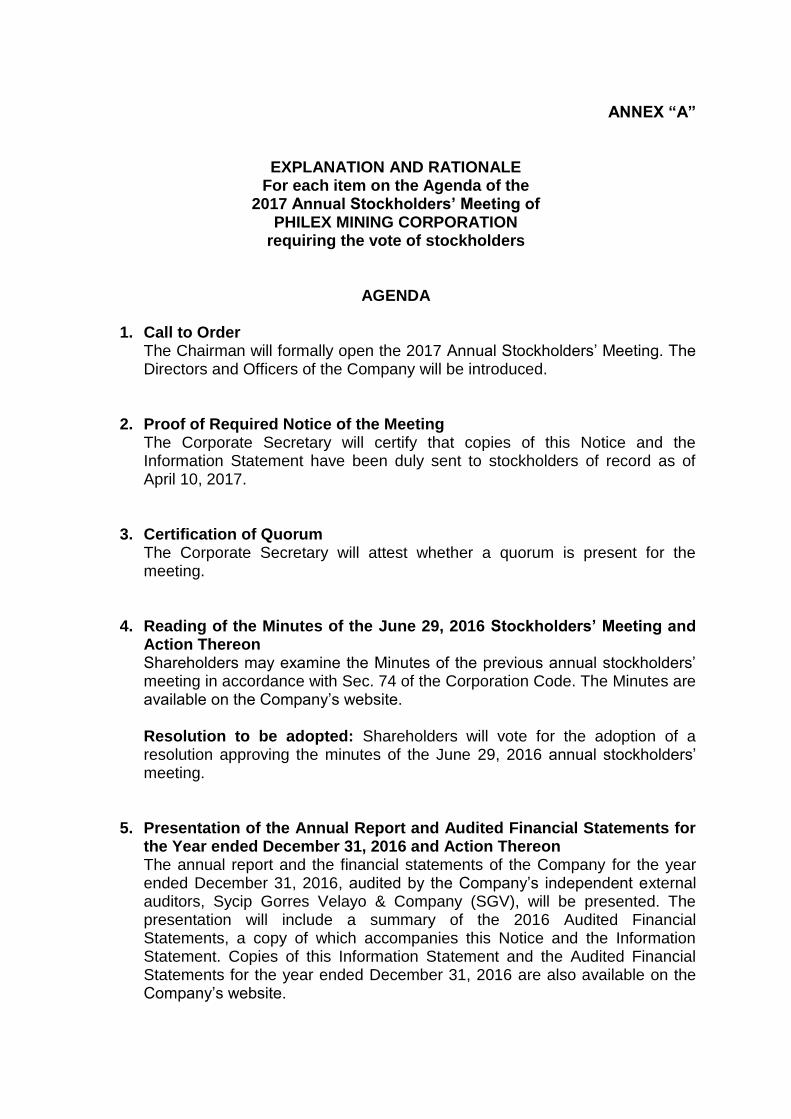

ANNEX “A”

EXPLANATION AND RATIONALE For each item on the Agenda of the

2017 Annual Stockholders’ Meeting of PHILEX MINING CORPORATION

requiring the vote of stockholders

AGENDA

1. Call to Order

The Chairman will formally open the 2017 Annual Stockholders’ Meeting. The Directors and Officers of the Company will be introduced.

2. Proof of Required Notice of the Meeting The Corporate Secretary will certify that copies of this Notice and the Information Statement have been duly sent to stockholders of record as of April 10, 2017.

3. Certification of Quorum The Corporate Secretary will attest whether a quorum is present for the meeting.

4. Reading of the Minutes of the June 29, 2016 Stockholders’ Meeting and Action Thereon Shareholders may examine the Minutes of the previous annual stockholders’ meeting in accordance with Sec. 74 of the Corporation Code. The Minutes are available on the Company’s website. Resolution to be adopted: Shareholders will vote for the adoption of a resolution approving the minutes of the June 29, 2016 annual stockholders’ meeting.

5. Presentation of the Annual Report and Audited Financial Statements for the Year ended December 31, 2016 and Action Thereon The annual report and the financial statements of the Company for the year ended December 31, 2016, audited by the Company’s independent external auditors, Sycip Gorres Velayo & Company (SGV), will be presented. The presentation will include a summary of the 2016 Audited Financial Statements, a copy of which accompanies this Notice and the Information Statement. Copies of this Information Statement and the Audited Financial Statements for the year ended December 31, 2016 are also available on the Company’s website.

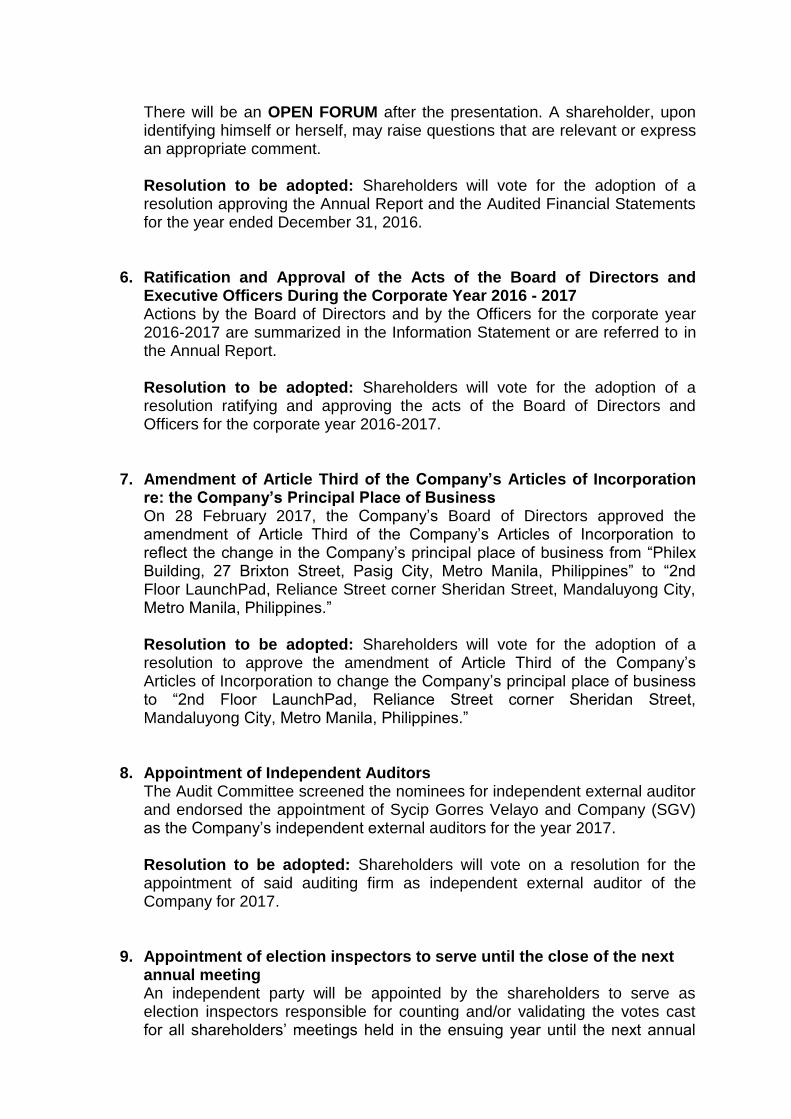

There will be an OPEN FORUM after the presentation. A shareholder, upon identifying himself or herself, may raise questions that are relevant or express an appropriate comment. Resolution to be adopted: Shareholders will vote for the adoption of a resolution approving the Annual Report and the Audited Financial Statements for the year ended December 31, 2016.

6. Ratification and Approval of the Acts of the Board of Directors and Executive Officers During the Corporate Year 2016 - 2017 Actions by the Board of Directors and by the Officers for the corporate year 2016-2017 are summarized in the Information Statement or are referred to in the Annual Report. Resolution to be adopted: Shareholders will vote for the adoption of a resolution ratifying and approving the acts of the Board of Directors and Officers for the corporate year 2016-2017.

7. Amendment of Article Third of the Company’s Articles of Incorporation re: the Company’s Principal Place of Business On 28 February 2017, the Company’s Board of Directors approved the amendment of Article Third of the Company’s Articles of Incorporation to reflect the change in the Company’s principal place of business from “Philex Building, 27 Brixton Street, Pasig City, Metro Manila, Philippines” to “2nd Floor LaunchPad, Reliance Street corner Sheridan Street, Mandaluyong City, Metro Manila, Philippines.” Resolution to be adopted: Shareholders will vote for the adoption of a resolution to approve the amendment of Article Third of the Company’s Articles of Incorporation to change the Company’s principal place of business to “2nd Floor LaunchPad, Reliance Street corner Sheridan Street, Mandaluyong City, Metro Manila, Philippines.”

8. Appointment of Independent Auditors The Audit Committee screened the nominees for independent external auditor and endorsed the appointment of Sycip Gorres Velayo and Company (SGV) as the Company’s independent external auditors for the year 2017. Resolution to be adopted: Shareholders will vote on a resolution for the appointment of said auditing firm as independent external auditor of the Company for 2017.

9. Appointment of election inspectors to serve until the close of the next annual meeting An independent party will be appointed by the shareholders to serve as election inspectors responsible for counting and/or validating the votes cast for all shareholders’ meetings held in the ensuing year until the next annual

meeting. In 2016 and in previous years, representatives of the independent external auditor were appointed. This practice will be followed this year. Resolution to be adopted: Shareholders will vote on a resolution approving the appointment of election inspectors to serve until the close of the next annual meeting.

10. Election of Directors, including Independent Directors

The Final List of Candidates for election as directors, as prepared by the Nominations Committee in accordance with the Company’s By-Laws and Manual on Corporate Governance, will be presented to the shareholders, and the election of directors will be held.

11. Other Matters Matters that are relevant to and appropriate for the annual stockholders’ meeting may be taken up. No resolution, other than the resolutions explained in the Notice and the Information Statement, will be submitted for voting by the shareholders.

12. Adjournment

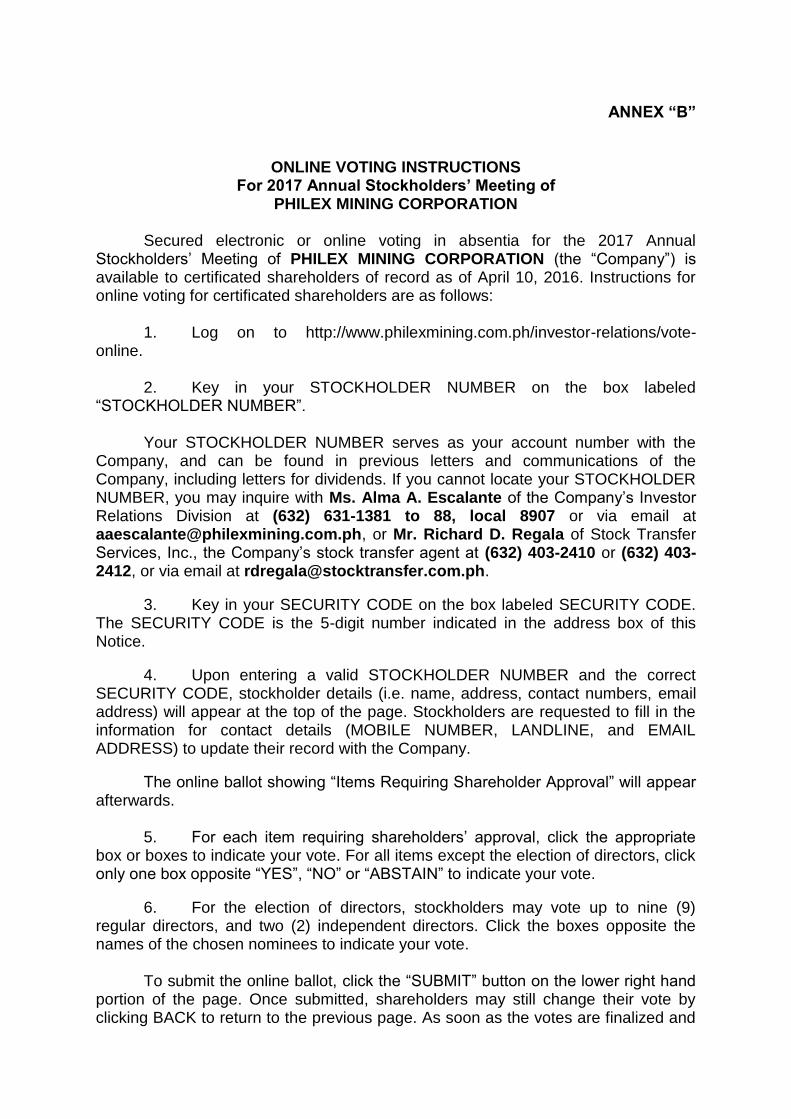

ANNEX “B”

ONLINE VOTING INSTRUCTIONS For 2017 Annual Stockholders’ Meeting of

PHILEX MINING CORPORATION Secured electronic or online voting in absentia for the 2017 Annual Stockholders’ Meeting of PHILEX MINING CORPORATION (the “Company”) is available to certificated shareholders of record as of April 10, 2016. Instructions for online voting for certificated shareholders are as follows:

1. Log on to http://www.philexmining.com.ph/investor-relations/vote-online.

2. Key in your STOCKHOLDER NUMBER on the box labeled

“STOCKHOLDER NUMBER”.

Your STOCKHOLDER NUMBER serves as your account number with the Company, and can be found in previous letters and communications of the Company, including letters for dividends. If you cannot locate your STOCKHOLDER NUMBER, you may inquire with Ms. Alma A. Escalante of the Company’s Investor Relations Division at (632) 631-1381 to 88, local 8907 or via email at [email protected], or Mr. Richard D. Regala of Stock Transfer Services, Inc., the Company’s stock transfer agent at (632) 403-2410 or (632) 403-2412, or via email at [email protected].

3. Key in your SECURITY CODE on the box labeled SECURITY CODE. The SECURITY CODE is the 5-digit number indicated in the address box of this Notice.

4. Upon entering a valid STOCKHOLDER NUMBER and the correct SECURITY CODE, stockholder details (i.e. name, address, contact numbers, email address) will appear at the top of the page. Stockholders are requested to fill in the information for contact details (MOBILE NUMBER, LANDLINE, and EMAIL ADDRESS) to update their record with the Company.

The online ballot showing “Items Requiring Shareholder Approval” will appear afterwards.

5. For each item requiring shareholders’ approval, click the appropriate

box or boxes to indicate your vote. For all items except the election of directors, click only one box opposite “YES”, “NO” or “ABSTAIN” to indicate your vote.

6. For the election of directors, stockholders may vote up to nine (9) regular directors, and two (2) independent directors. Click the boxes opposite the names of the chosen nominees to indicate your vote.

To submit the online ballot, click the “SUBMIT” button on the lower right hand

portion of the page. Once submitted, shareholders may still change their vote by clicking BACK to return to the previous page. As soon as the votes are finalized and

the SUBMIT button is clicked, a confirmation message “Thank you for Voting” will appear.

7. Online ballots will be accepted until 12:00 p.m. on June 27, 2017, the

day before the 2017 Annual Stockholders’ Meeting on June 28, 2017. 8. Online ballots will be tabulated at the Meeting together with ballots

filled out during the said Meeting. Results of the voting by shareholders will be announced for each item on the Agenda requiring the vote of shareholders, and shall be duly disclosed and shall be made available on the Company’s website on the business day following the meeting.

For any questions or concerns, kindly contact Mr. Rolando S. Bondoy, Division Manager - Investor Relations, at (632) 631-1381 to 88, or via email at [email protected].

C2357 PX 2017 ASM Notice with Agenda and Online Voting Instructions – Definitive IS CLEAN (17MAY17) spp74

SECURITIES AND EXCHANGE COMMISSION

SEC FORM 20-IS

INFORMATION STATEMENT PURSUANT TO SECTION 20 OF THE SECURITIES REGULATION CODE

1. Check the appropriate box:

[ ] Preliminary Information Statement [x] Definitive Information Statement

2. Name of Registrant as specified in its charter: PHILEX MINING CORPORATION 3. Province, country or other jurisdiction of incorporation or organization: Metro Manila,

Philippines 4. SEC Identification Number: 10044 5. BIR Tax Identification Code: 000-283-731-000 6. Address of principal office: 2nd Floor LaunchPad, Reliance Street corner Sheridan

Street, Mandaluyong City, Metro Manila1 7. Registrant’s telephone number, including area code: (632) 631-1381 to 88 8. Date, time and place of the meeting of security holders: Date : June 28, 2017 Time : 2:30 p.m.

Place : Marco Polo Ortigas Manila, Meralco Avenue and Sapphire Street, Ortigas Centre, Pasig City, Metro Manila 1600

9. Approximate date on which the Information Statement is first to be sent or given to

security holders: May 26, 2017, and in no case later than May 30, 2017. 10. In case of Proxy Solicitations:

Name of Person Filing the Statement/Solicitor: Philex Mining Corporation

Address and Telephone Number:

Philex Building, 27 Brixton Street, Pasig City, Metro Manila, Philippines 1600 (632) 631-1381 to 88

1 On February 28, 2017, the Company’s Board of Directors approved the amendment of Article Third of the

Company’s Articles of Incorporation to reflect the change in the Company’s principal place of business from “Philex Building, 27 Brixton Street, Pasig City, Metro Manila” to “2

nd Floor LaunchPad, Reliance Street corner

Sheridan Street, Mandaluyong City, Metro Manila.” The said amendment shall be presented for approval of shareholders at the Company’s 2017 Annual Stockholders’ Meeting on June 28, 2017.

2

11. Securities registered pursuant to Sections 8 and 12 of the Code or Sections 4 and 8 of the RSA (information on number of shares and amount of debt is applicable only to corporate registrants):

Number of Shares of Common Stock Issued 4,940,399,068 (as of March 31, 2017) Amount of Debt Outstanding P9,675,494,423 (as of December 31,

2016)

12. Are any or all of registrant’s securities listed on a stock exchange? ( x ) Yes ( ) No If so, disclose name of Exchange: Philippine Stock Exchange, Inc.

PART I.

INFORMATION REQUIRED IN INFORMATION STATEMENT

A. GENERAL INFORMATION Item 1. Date, Time and Place of Meeting of Security Holders The Annual Meeting of the Stockholders of PHILEX MINING CORPORATION (the “Company”), a corporation organized and existing under the laws of the Philippines with office address at the 2nd Floor, LaunchPad, Reliance Street corner Sheridan Street, Mandaluyong City, Metro Manila,2 will be held on June 28, 2017 (Wednesday) at 2:30 p.m. at Marco Polo Ortigas Manila, Meralco Avenue and Sapphire Street, Ortigas Centre, Pasig City, Metro Manila 1600 (the “Annual Stockholders’ Meeting” or the “Meeting”). The Agenda of the Meeting, as indicated in the accompanying Notice of Annual Meeting of Stockholders, is as follows:

1. Call to Order 2. Proof of Required Notice of the Meeting 3. Certification of Quorum 4. Reading and Approval of the Minutes of the June 29, 2016 Stockholders’ Meeting

and Action Thereon 5. Presentation of Annual Report and Audited Financial Statements for the Year

Ended December 31, 2016 and Action Thereon 6. Ratification and Approval of the Acts of the Board of Directors and Executive

Officers During the Corporate Year 2016 – 2017 7. Approval of the Amendment of Article Third of the Company’s Articles of

Incorporation re: the Company’s Principal Place of Business 8. Appointment of Election Inspectors to serve until the close of the next annual

meeting 9. Election of Directors, including Independent Directors 10. Other Matters

2 See Footnote 1

3

As in previous years, there will be an OPEN FORUM before the approval of the Annual Report and Audited Financial Statements for the year ended December 31, 2016 is submitted to the vote of the shareholders. Questions will likewise be entertained for other items in the agenda as appropriate and consistent with orderly proceedings. The Audited Financial Statements and Management Report for the year ended December 31, 2016, and the interim financial statements for the period ended March 31, 2017 on Securities and Exchange Commission (SEC) Form 17-Q, are attached to this Information Statement. The Annual Report under SEC Form 17-A is available on the Company’s website (www.philexmining.com.ph). Upon written request of a shareholder, the Company shall furnish such shareholder with a copy of the said Annual Report on SEC Form 17-A as filed with the SEC, free of charge. The contact details for obtaining such copy are on page 29 of this Information Statement. For the purpose of the Meeting, only stockholders of record at the close of business of April 10, 2017 will be entitled to vote. Stockholders are requested to bring some form of identification such as passport, driver’s license, or company I.D. in order to facilitate registration, which will start at 1:00 p.m. Shareholders who cannot attend the Meeting may accomplish the Proxy Form to be distributed to shareholders together with the Definitive Information Statement. Shareholders are requested to indicate their vote (Yes, No, Abstain) for each item in the said Proxy Form, and submit the same on or before June 19, 2017 to the Office of the Corporate Secretary at the Company’s principal office. Secured electronic or online voting will also be available for certificated shareholders at http://www.philexmining.com.ph/investor-relations/vote-online. Online voting instructions are attached to the Notice accompanying this Information Statement. Proxies will be validated by a special committee composed of the Company’s Corporate Secretary, Compliance Officer, and a representative of the Company’s stock transfer agent, Stock Transfer Services, Inc. (“STSI”) on June 22, 2017. The said committee will submit a report to the representative of Sycip Gorres Velayo & Co. elected by shareholders as independent election inspector at the 2016 Annual Stockholders’ Meeting. Voting procedures are contained in Item 19 (pages 27-28) of this Information Statement and will be announced at the start of the Meeting. Cumulative voting is allowed; please refer to Item 4 (page 5) and Item 19 (pages 27-28) for an explanation of cumulative voting. Further information and explanation regarding specific agenda items, where appropriate, are contained in various sections of this Information Statement. This Information Statement constitutes notice of the resolutions to be adopted at the Meeting. The Definitive Information Statement and Proxy Form shall be sent to stockholders of record as of April 10, 2017 on May 26, 2017, and in no case later than May 30, 2017, after the approval thereof by the SEC. Item 2. Dissenters' Right of Appraisal

There are no corporate matters or action to be taken during the Meeting that will entitle a stockholder to a Right of Appraisal as provided in Title X of the Corporation Code of the Philippines (Batas Pambansa [National Law] No. 68).

4

For the information of stockholders, any stockholder of the Company shall have a right to dissent and demand payment of the fair value of his shares in the following instances, as provided in the Corporation Code of the Philippines:

1. In case any amendment to the articles of incorporation has the effect of changing

or restricting the rights of any stockholder or class of shares, or of authorizing preferences in any respect superior to those of outstanding shares of any class, or of extending or shortening the term of corporate existence (Section 81);

2. In case of sale, lease, exchange, transfer, mortgage, pledge or other disposition of all or substantially all of the corporate property and assets (Section 81);

3. In case of merger or consolidation (Section 81); and

4. In case of investments in another corporation, business or purpose (Section 42).

The Corporation Code of the Philippines (at Section 82) provides that the appraisal right may be exercised by any stockholder who shall have voted against the proposed corporate action, by making a written demand on the corporation within thirty (30) days after the date on which the vote was taken, for payment of the fair value of his shares: provided, that failure to make the demand within such period shall be deemed a waiver of the appraisal right. A stockholder must have voted against the proposed corporate action in order to avail himself of the appraisal right. If the proposed corporate action is implemented or effected, the corporation shall pay to such stockholder, upon surrender of his certificate(s) of stock representing his shares, the fair value thereof as of the day prior to the date on which the vote was taken, excluding any appreciation or depreciation in anticipation of such corporate action. If within a period of sixty (60) days from the date the corporate action was approved by the stockholders, the withdrawing stockholder and the corporation cannot agree on the fair value of the shares, it shall be determined and appraised by three (3) disinterested persons, one of whom shall be named by the stockholder, another by the corporation and the third by the two thus chosen. The findings of the majority of appraisers shall be final, and their award shall be paid by the corporation within thirty (30) days after such award is made; provided, that no payment shall be made to any dissenting stockholder unless the corporation has unrestricted retained earnings in its books to cover such payment; and provided, further, that upon payment by the corporation of the agreed or awarded price, the stockholder shall forthwith transfer his shares to the corporation. Item 3. Interest of Certain Persons in or Opposition to Matters to be Acted Upon No director, nominee for election as director, associate of the nominee or executive officer of the Company at any time since the beginning of the last fiscal year, has any substantial interest, direct or indirect, by security holdings or otherwise, in any of the matters to be acted upon in the meeting, other than election to office. No incumbent director has informed the Company in writing of an intention to oppose any action to be taken at the meeting.

5

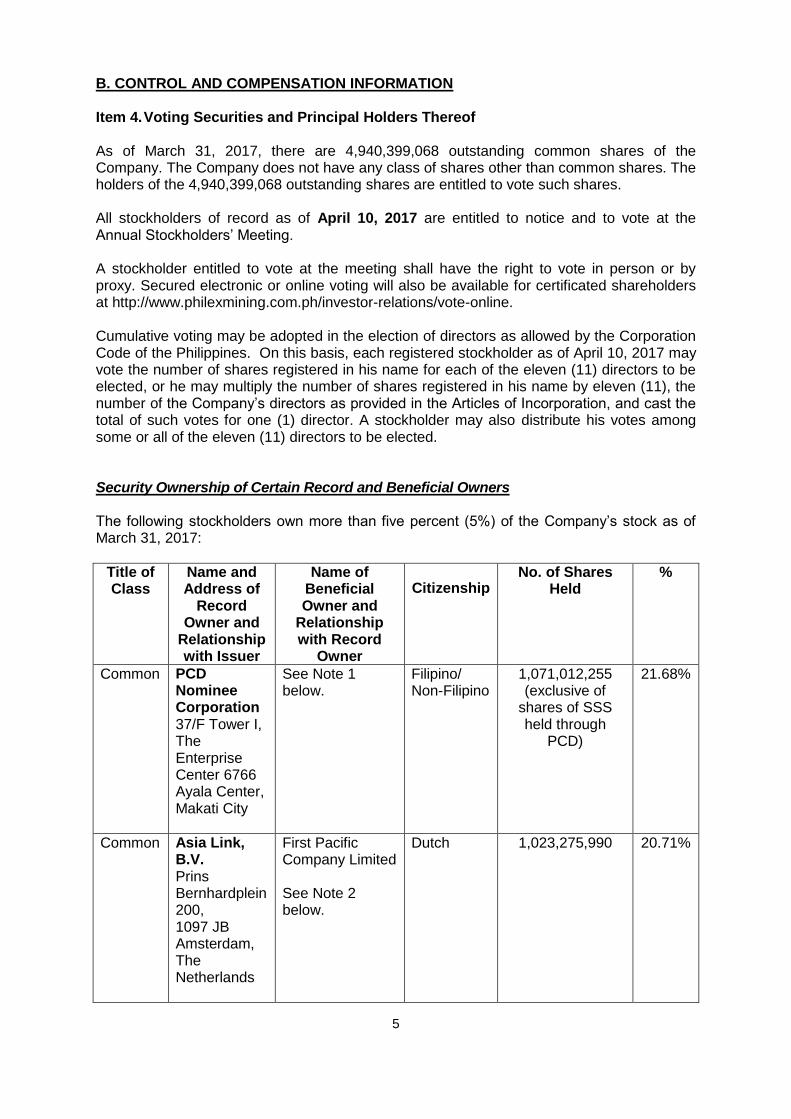

B. CONTROL AND COMPENSATION INFORMATION Item 4. Voting Securities and Principal Holders Thereof As of March 31, 2017, there are 4,940,399,068 outstanding common shares of the Company. The Company does not have any class of shares other than common shares. The holders of the 4,940,399,068 outstanding shares are entitled to vote such shares. All stockholders of record as of April 10, 2017 are entitled to notice and to vote at the Annual Stockholders’ Meeting. A stockholder entitled to vote at the meeting shall have the right to vote in person or by proxy. Secured electronic or online voting will also be available for certificated shareholders at http://www.philexmining.com.ph/investor-relations/vote-online. Cumulative voting may be adopted in the election of directors as allowed by the Corporation Code of the Philippines. On this basis, each registered stockholder as of April 10, 2017 may vote the number of shares registered in his name for each of the eleven (11) directors to be elected, or he may multiply the number of shares registered in his name by eleven (11), the number of the Company’s directors as provided in the Articles of Incorporation, and cast the total of such votes for one (1) director. A stockholder may also distribute his votes among some or all of the eleven (11) directors to be elected. Security Ownership of Certain Record and Beneficial Owners The following stockholders own more than five percent (5%) of the Company’s stock as of March 31, 2017:

Title of Class

Name and Address of

Record Owner and

Relationship with Issuer

Name of Beneficial Owner and

Relationship with Record

Owner

Citizenship No. of Shares

Held %

Common PCD Nominee Corporation 37/F Tower I, The Enterprise Center 6766 Ayala Center, Makati City

See Note 1 below.

Filipino/ Non-Filipino

1,071,012,255 (exclusive of

shares of SSS held through

PCD)

21.68%

Common Asia Link, B.V. Prins Bernhardplein 200, 1097 JB Amsterdam, The Netherlands

First Pacific Company Limited See Note 2 below.

Dutch 1,023,275,990 20.71%

6

Common Social Security System c/o Loan and Investment Office, 7/F SSS Building, Diliman, Quezon City

Social Security System See Note 3 below.

Filipino 982,434,729 19.89%

Common Two Rivers Pacific Holdings Corporation 10/F MGO Building, Legaspi cor. Dela Rosa Sts., Legaspi Village, Makati City

Two Rivers Pacific Holdings Corporation See Note 4 below.

Filipino 738,871,510

14.96%

1 PCD Nominee Corporation (“PCD Nominee”), the nominee of the Philippine Depository & Trust Corp., is the registered owner of the shares in the books of the Company’s transfer agent. The beneficial owners of such shares are PCD Nominee’s participants who hold the shares on their own behalf or in behalf of their clients. The 1,071,012,255 shares shown above as of March 31, 2017 are exclusive of the 117,989,799 shares owned by SSS which shares were included as part of the total holdings of SSS indicated above. PCD Nominee is a private company organized by the major institutions actively participating in the Philippine capital markets to implement an automated book-entry system of handling securities transaction in the Philippines.

2 Asia Link B.V., a wholly-owned subsidiary of First Pacific Company Limited

(“First Pacific”), is the registered owner of 1,023,275,990 shares. In its SEC Form 23-A dated December 3, 2009, First Pacific disclosed that it beneficially owns 1,542,589,352 shares of the Company, inclusive of the shares held by Asia Link B.V. First Pacific is represented on the Company’s Board of Directors by Messrs. Manuel V. Pangilinan, Robert C. Nicholson and Edward A. Tortorici.

3 Mr. Michael G. Regino, Mr. Jose Gabriel M. La Viña, and Ms. Anita Bumpus

Quitain currently represent the Social Security System (“SSS”) in the Company’s Board of Directors. Of the 982,434,729 shares of SSS, 117,989,799 shares are held by SSS through the PCD Nominee Corporation.

4 Two Rivers Pacific Holdings Corporation is represented by Ms. Marilyn A.

Victorio-Aquino and Mr. Eulalio B. Austin, Jr. on the Company’s Board of Directors.

7

To the best knowledge of the Company, there are no participants under the PCD account who own more than 5% of the Company’s voting securities as of March 31, 2017. Proxies of the foregoing record owners for the Annual Stockholders’ Meeting have not yet been received by the Company. The deadline set by the Board of Directors for submission of proxies is on June 19, 2017. Security Ownership of Management The beneficial ownership of the Company’s directors and executive officers as of March 31, 2017 is as follows:

Title of Class

Name of Beneficial Owner

Nature of Ownership

Amount of Beneficial Ownership

Citizenship %

Common Manuel V. Pangilinan Direct 4,655,000 Filipino 0.09

Common Eulalio B. Austin, Jr. Direct 1,360,937 Filipino 0.03

Common Robert C. Nicholson Direct 1,250 British 0.00

Common Marilyn A. Victorio-Aquino Direct 500,100 Filipino 0.01

Common Edward A. Tortorici Direct 3,285,100 American 0.07

Common Oscar J. Hilado Direct 173 Filipino 0.00

Common Wilfredo A. Paras Direct 1 Filipino 0.00

Common Michael G. Regino Direct 1 Filipino 0.00 Common Jose Gabriel M. La Viña Direct 1 Filipino 0.00 Common Anita Bumpus Quitain Direct 1 Filipino 0.00

Common Barbara Anne C. Migallos Direct 203,875 Filipino 0.00

Common Danny Y. Yu Direct 40,000 Filipino 0.00

Common Manny A. Agcaoili Direct 0 Filipino 0.00

Common Michael T. Toledo Direct 0 Filipino 0.00

Common Redempta P. Baluda Direct 20 Filipino 0.00

Common Victor A. Francisco Direct 50,000 Filipino 0.00

Common Joan A. De Venecia Direct 0 Filipino 0.00

Directors and Officers as a Group 10,096,459 0.20

Security Ownership of Non-Filipinos

The chart below shows the ownership of non-Filipinos as of March 31, 2017:

Total Outstanding

Shares

Shares Allowed to Foreigners

% Allowed to Foreigners

Shares Owned by Foreigners

% Owned by Foreigners

4,940,399,068 1,976,159,627 40% 1,928,084,936 39.03%

Voting Trust Holders/Changes in Control There are no voting trust holders of 5% or more of the Company’s stock. There are no arrangements that may result in a change of control of the Company.

8

Item 5. Directors and Executive Officers DIRECTORS The following are the present directors of the Company whose terms of office are for one year or until their successors are elected and qualified: 1. MANUEL V. PANGILINAN, Chairman, Non-Executive Director.

Age: 70 Date of First Election: November 28, 2008 Academic Background: Mr. Pangilinan graduated Cum Laude from the Ateneo de Manila University with a Bachelor of Arts degree in Economics. He received his Master of Business Administration degree from Wharton School of the University of Pennsylvania in 1968. Business and Professional Background/ Experience: Mr. Pangilinan founded First Pacific Company Limited, a corporation listed on the Hong Kong Stock Exchange, in May 1981. He served as Managing Director of First Pacific since its founding in 1981 until 1999. He was appointed Executive Chairman until June 2003, after which he was named Managing Director and Chief Executive Officer. In May 2006, the Office of the President of the Philippines awarded Mr. Pangilinan the Order of Lakandula, rank of Komandante, in recognition of his contributions to the country. He was named Management Man of the Year 2005 by the Management Association of the Philippines. Mr. Pangilinan was awarded Honorary Doctorates in Science by Far Eastern University in 2010; in Humanities by Holy Angel University in 2008; by Xavier University in 2007; and by San Beda College in 2002 in the Philippines. He was formerly Chairman of the Board of Trustees of the Ateneo de Manila University and was a member of the Board of Overseers of the Wharton School. He is a member of the ASEAN Business Advisory Council. Mr. Pangilinan has been a Director of the Company and Philex Gold Philippines, Inc. (PGPI) since November 2008, and most recently re-elected on June 29, 2016. He is also Managing Director and Chief Executive Officer of First Pacific, and Chairman of the PLDT Inc. (PLDT) since 2004, after serving as its President and Chief Executive Officer (CEO) since 1998. He reassumed the position of President and CEO of PLDT effective December 2015. He is also Chairman of Smart Communications, Inc., PLDT Communications and Energy Ventures, Inc. (Digitel), Metro Pacific Investments Corporation, Silangan Mindanao Mining Co., Inc., Landco Pacific Corporation, Medical Doctors Inc. (Makati Medical Center), Colinas Verdes Corporation (Cardinal Santos Medical Center), Asian Hospital, Inc., Davao Doctors, Inc., Riverside Medical Center Inc., Our Lady of Lourdes Hospital, Central Luzon Doctors’ Hospital, Inc., Maynilad Water Services Corporation, Mediaquest, Inc., Associated Broadcasting Corporation (TV5) and Manila North Tollways Corporation. Mr. Pangilinan is also Chairman of the Manila Electric Company (MERALCO), after serving as its President and Chief Executive Officer from July 2010 to May 2012. Mr. Pangilinan is also Vice Chairman of Roxas Holdings, Incorporated, the largest sugar producer in the Philippines. Directorship in other Listed Companies in the Philippines: 1. PLDT Inc. - Chairman 2. Metro Pacific Investments Corporation - Chairman

9

3. Roxas Holdings, Inc. - Vice Chairman and Non-Executive Director 4. Manila Electric Company – Chairman 5. PXP Energy Corporation - Chairman

2. EULALIO B. AUSTIN, JR. President & Chief Executive Officer, Executive Director.

Age: 55 Date of First Election: June 29, 2011 Academic Background: Mr. Austin graduated from Saint Louis University-Baguio City, with a Bachelor of Science degree in Mining Engineering and placed eight in the 1982 Professional Board Examination for mining engineers. He took his Management Development Program at the Asian Institute of Management in 2005, and his Advance Management Program at Harvard Business School in 2013. Business and Professional Background/ Experience: Mr. Austin has been a Director of the Company and PGPI since June 29, 2011 and was most recently re-elected on June 29, 2016. He became President and Chief Operating Officer on January 1, 2012 and President and Chief Executive Officer of the Company on April 3, 2013. He previously served the Company as its Senior Vice President for Operations and Padcal Resident Manager in 2011, Vice President & Resident Manager for Padcal Operations from 2004 to 2010, Mine Division Manager (Padcal) from 1999 to 2003, Engineering Group Manager in 1998, and Mine Engineering & Draw Control Department Manager from 1996 to 1998. Mr. Austin concurrently serves as Director of PXP Energy Corporation and Silangan Mindanao Mining Co., Inc. He likewise sits on the Board of the Chamber of Mines of the Philippines and Philippine Mineral Safety and Environmental Association (PMSEA) and was Founding President of PSEM’s Philex Chapter. He was recently awarded as the CEO of the Year in Mining by The Asset in December 2015. He was also a recipient of Asia Pacific Entrepreneur Award (APEA) for the Mining Industry by Enterprise Asia in 2016. He was also recognized by the Philippine Society of Mining Engineers as the Most Outstanding Engineer in Mine Management in June 2016. Directorship in other Listed Companies in the Philippines: 1. PXP Energy Corporation - Non - Executive Director

3. ROBERT C. NICHOLSON, Non-Executive Director.

Age: 61 Date of First Election: November 8, 2008 Academic Background: Mr. Nicholson graduated from the University of Kent in 1976, and is qualified as a solicitor in England and Wales, and in Hong Kong. Business and Professional Background/ Experience Mr. Nicholson has been a Director of the Company and PGPI since November 28, 2008, and was most recently re-elected on June 29, 2016. He is Executive Chairman of Forum Energy Plc, Chairman of Goodman Fielder Pty Limited (since March 2015), and Commissioner of PT Indofood Sukses Makmur Tbk. He is also Director of Metro

10

Pacific Investments Corporation, PXP Energy Corporation, and Silangan Mindanao Mining Co, Inc., Executive Director of Pitkin Petroleum Plc and Pacific Light Power Pte. Ltd., all of which are First Pacific subsidiaries or associates. Mr. Nicholson is also an Independent Non-executive Director of Pacific Basin Shipping Limited and Lifestyle Properties Development Limited. Previously, he was a senior partner of Reed Smith Richards Butler from 1985 to 2001 where he established the corporate and commercial department, and senior advisor to the board of directors of PCCW Limited between August 2001 and September 2003. Mr. Nicholson has wide experience in corporate finance and cross-border transactions, including mergers and acquisitions, regional telecommunications, debt and equity capital markets, corporate reorganizations and privatizations in China. Directorship in other Listed Companies in the Philippines 1. PXP Energy Corporation - Non-Executive Director 2. Metro Pacific Investment Corporation - Non-Executive Director

4. EDWARD A. TORTORICI, Non-Executive Director. Age: 77 Date of First Election: December 7, 2009 Academic Background Mr. Tortorici received his Bachelor of Science degree from New York University, and a Master of Science degree from Fairfield University. Business and Professional Background/ Experience Mr. Tortorici has been a Director of the Company and PGPI since December 7, 2009, and was last re-elected on June 29, 2016. Mr. Tortorici has served in a variety of senior and executive management positions, including Corporate Vice President for Crocker Bank, and Managing Director positions at Olivetti Corporation of America and Fairchild Semiconductor Corporation. Mr. Tortorici subsequently founded EA Edwards Associates, an international management and consulting firm specializing in strategy formulation and productivity improvement with offices in USA, Europe and Middle East. In 1987, Mr. Tortorici joined First Pacific as an Executive Director for strategic planning and corporate restructuring, and launched the Group’s entry into the telecommunications and technology sectors. Presently, he oversees corporate strategy for First Pacific and guides the Group’s strategic planning and corporate development activities. Mr. Tortorici is Commissioner of PT Indofood Sukses Makmur Tbk, and Director of Metro Pacific Investments Corporation, Maynilad Water Services, Inc., and FEC Resources Inc. of Canada. He previously served as Director of AIM-listed Forum Energy Plc. Mr. Tortorici is Trustee of the Asia Society Philippines, and is on the Board of Advisors of the Southeast Asia Division of the Center for Strategic and International Studies, a Washington D.C. non-partisan think tank. He also served as Commissioner of the U.S. ASEAN Strategy Commission. Directorship in Other Listed Companies in the Philippines 1. Metro Pacific Investment Corporation - Non-Executive Director

11

5. MARILYN A. VICTORIO-AQUINO, Non-Executive Director.

Age: 61 Date of First Election: December 7, 2009 Academic Background: Ms. Victorio-Aquino graduated Cum Laude (class salutatorian) from the University of the Philippines College of Law in 1980, and placed second in the 1980 Philippine Bar Examinations. Business and Professional Background/ Experience: She has been a Director of the Company and PGPI since December 7, 2009, and was most recently re-elected on June 29, 2016. She is an Assistant Director of First Pacific Co. Ltd. since July 2012, following her 32-year law practice at SyCip Salazar Hernandez and Gatmaitan Law Offices, where she was Partner from 1989 to 2012. She is also a Director of Philippine Indofood Distribution Corporation since August 2014, of Light Rail Manila Corporation since July 2014, of Silangan Mindanao Mining Co., Inc., and Lepanto Consolidated Mining Company since October 2012, and of Maynilad Water Services Corporation since December 2012. Directorship in Other Listed Companies in the Philippines: 1. PXP Energy Corporation - Non-Executive Director 2. Lepanto Consolidated Mining Company – Non-Executive Director

6. OSCAR J. HILADO, Independent Director.

Age : 79 Date of First Election: December 7, 2009 Academic Background: Mr. Hilado, a Certified Public Accountant, completed his undergraduate studies at the De La Salle College-Bacolod in 1958, and obtained his Master’s in Business Administration from the Harvard School of Business Administration (Smith Mundt/Fulbright Scholar) in 1962. He received a Doctorate in Business Management, Honoris Causa, from the De La Salle University, and a Doctorate of Laws, Honoris Causa, from the University of St. La Salle in 1992. Business and Professional Background/ Experience: Mr. Hilado has been an Independent Director of the Company since December 7, 2009, and was most recently re-elected on June 29, 2016. He was the Chairman & Chief Executive Officer of Philippine Investment Management (PHINMA), Inc. (January 1994 to August 2005), and currently Chairman of the Board. He is currently also Chairman of PHINMA Corporation, PHINMA Property Holdings Corp., Vice Chairman of PHINMA Energy Corporation, Trans-Asia Power Generation Corporation, and Union Galvasteel Corporation, and Director of Trans Asia Renewable Energy Corporation and publicly listed Trans-Asia Petroleum Corporation. Mr. Hilado is an Independent Director of publicly listed corporations Smart Communications, Inc., First Philippine Holdings Corporation, A. Soriano Corporation, and Rockwell Land Corporation, and private corporation Digital Telecommunications Phils., Inc, and the publicly listed corporations. He is also a Director of United Pulp and Paper Company, Inc., Beacon Property Ventures, Inc., Manila Cordage Company, Pueblo de Oro Development Corporation, Seven Seas

12

Resorts and Leisure, Inc., Asian Eye Institute, Southwestern University, Araullo University, Cagayan de Oro College, University of Iloilo, University of Pangasinan, Microtel Inns & Suites (Pilipinas) Inc. Directorship in Other Listed Companies in the Philippines : 1. PHINMA Corporation - Chairman 2. PHINMA Energy Corporation (Chairman), and its subsidiary, Trans Asia

Petroleum Corporation (Vice Chairman) 3. A. Soriano Corporation - Non-Executive Director 4. First Philippine Holdings Corp. -Independent Director 5. Rockwell Land Corporation – Independent Director 6. Roxas Holdings, Inc. – Independent Director

7. WILFREDO A. PARAS, Independent Director.

Age : 70 Date of First Election: June 29, 2011 Academic Background Mr. Paras completed his undergraduate studies at the University of the Philippines in 1969 with a Bachelor of Science degree in Industrial Pharmacy, and his Master in Business Administration at the De La Salle University in 1991. He also completed an Executive Program at the University of Michigan at Ann Arbor, Michigan, USA. Business and Professional Background/ Experience Mr. Paras has been an Independent Director of the Company since June 29, 2011, and was last re-elected on June 29, 2016. He has also been Independent Director of GT Capital Holdings, Inc. since May 2013, and President of WAP Holdings, Inc. He is also a member of the Board of Trustees of Dualtech Training Foundation Inc. Mr. Paras was previously the Executive Vice President, Chief Operating Officer and Director of JG Summit Petrochemical Corporation, President and Director of PT Union Carbide Indonesia, Managing Director of Union Carbide Singapore, and Business Director for Union Carbide Asia Pacific. Directorship in Other Listed Companies in the Philippines 1. GT Capital Holdings, Inc. - Independent Director

8. BARBARA ANNE C. MIGALLOS Corporate Secretary , Executive Director.

Age: 62 Date of First Election: June 26, 2013 Academic Background: Ms. Migallos graduated Cum Laude from the University of the Philippines, with a Bachelor of Arts degree, and finished her Bachelor of Laws degree as Cum Laude (salutatorian) also at the University of the Philippines. She placed third in the 1979 Philippine Bar Examination. Business and Professional Background/ Experience Ms. Migallos was first elected to the Board of Directors of the Company and PGPI on June 26, 2013, and was most recently re-elected on June 29, 2016. She has been

13

the Company’s Corporate Secretary since July 1998. She is also Director and Corporate Secretary of PXP Energy Corporation, and Corporate Secretary of Silangan Mindanao Mining Co., Inc. She is the Managing Partner of the Migallos & Luna Law Offices. Ms. Migallos is also Director of Mabuhay Vinyl Corporation since 2000, and Philippine Resins Industries since 2001, and Corporate Secretary of Eastern Telecommunications Philippines, Inc. since 2005 and Nickel Asia Corporation since 2010. She is a professorial lecturer in Corporations Law, Insurance, Securities Regulation and Credit Transactions at the De La Salle University College of Law. She was a Senior Partner of Roco Kapunan Migallos and Luna Law Offices from 1988 to 2006. Directorship in other Listed Companies in the Philippines 1. PXP Energy Corporation - Executive Director 2. Mabuhay Vinyl Corporation - Non-Executive Director

9. JOSE GABRIEL M. LA VIÑA, Non-Executive Director.

Age: 59 Date of First Election: February 28, 2017. Academic Background: Mr. La Viña graduated at the Ateneo de Manila University with a Bachelor of Arts degree in Philosophy (Magna Cum Laude), and where he was an Ateneo Full Scholar & Insular Life Educational Foundational Scholar. He was also an AFS Scholar, Master in Entrepreneurship (Superior Performance) at the Asian Institute of Management; a Valedictorian at Corona del Mar High School, Newport Beach, California, Xavier University High School, and Xavier University Grade School. Business and Professional Background/ Experience: Mr. La Viña was appointed Commissioner of the Social Security System (SSS) on November 2016. He was elected to the Company’s Board of Directors on February 28, 2017. Prior to his appointment to the SSS, he was Social Media Director of the Duterte 2016 Presidential Campaign, and a member of its Media Central & Communications Group. Mr. La Viña has 32 years of experience as Founder & CEO in various industries, including Home Mortgage Brokerage, Real Estate, Cooperative Banking, Technology, Auto Sales, Supply Chain Management, Hospitality and Music Entertainment. He was elected to the Board of Directors of the Alumni Association of the Asian Institute of Management in February 2016. Mr. La Viña was Treasurer & Trustee of AFS Intercultural Services, which sends around 30 to 40 Filipino Muslim youth scholars to the United States every year under the Kennedy-Lugar Youth Exchange and Study program funded by the U.S. State Department. As a composer, Mr. La Viña’s songs have been recorded by Lea Salonga, Chad Borja, Joey Albert, Iza Calzado, Gino Padilla, Anna Fegi, Renz Verano, Jinky Llamanzares, Kaye Abad, Toti Fuentes, Raymond Lauchenco, Iwi Laurel, Tillie Moreno, Louie Reyes, Eugene Villaluz, Teresa Loyzaga, and other Filipino and international artists. One of his compositions won Third Prize in the Metro Manila Popular Music Festival in 1984, and two other received Honorable Mention at the 10th Billboard International Song Contest, 2002. Directorship in Other Listed Companies in the Philippines: None

14

10. MICHAEL G. REGINO, Non-Executive Director.

Age: 59 Date of First Appointment : February 28, 2017 Academic Background: Mr. Regino graduated Cum Laude and Salutatorian from Ateneo de Zamboanga University in 1981, with a degree of Bachelor of Science, Major in Economics. He obtained his Master’s in Business Administration in 1985 from Ateneo de Manila University. Business and Professional Background/ Experience: Mr. Regino has more than 30 years of corporate experience in organizing, developing and successfully operating enterprises in the following fields: real estate and construction, ready mix concrete operations, crushing plant operations, heavy equipment, cable television operations, property management, non-life insurance brokerage and risk management, and memorial parks development. He is also President and Director of San Agustin Services, Inc., Agata Mining Ventures, Inc., and Exploration Drilling Corp.; Senior Vice President and Chief Operating Officer of St. Augustine Gold and Copper Ltd.; and Executive Director of TVI Resources Development Phils., Inc. He likewise sits in the Board of Directors of Nationwide Development Corporation, as well as of KingKing Mining Corp., where he is in charge of Davao Operations. He was elected to the Company’s Board of Directors on February 28, 2017. Mr. Regino previously worked as President of Golden Haven Memorial Parks, Inc., Camella Homes, and MGS Group of Companies. He was also with Northern Foods, Corp., Kilusang Kabuhayan at Kaunlaran, and Ateneo de Zamboanga University, where he served as Finance and Treasury Manager, Chief Financial Specialist, and Instructor in Economics, respectively. Directorship in Other Listed Companies in the Philippines: None

11. ANITA BUMPUS QUITAIN, Non-Executive Director.

Age: 70 Date of First Appointment: February 28, 2017 Academic Background: Ms. Quitain has a BSE Education Degree from the University of Mindanao in Davao City, and Bachelor of Science Degree in Commerce, Major in Accounting. She has also completed two (2) years of Masters in Public Administration (37 units) for her Career Civil Service Eligibility. Business and Professional Background/ Experience: As newly-appointed SSS Commissioner, Ms. Quitain voted for the approval of the increase of the pension of SSS pensioners. As an employee of the SSS (for 31 years) assigned to the Main Office of Region 09 in Davao City, one of her major achievements was taking charge of the operations of

15

the then newly-opened SSS Representative Office in Digos City, Davao del Sur as Office-in-Charge. She stayed there for five (5) years where she conducted seminars and coverage drives, especially in rural areas, aside from discharging management and leadership functions in the Representative Office. As a BSE Education Degree holder, she worked with the Department of Education as an elementary classroom teacher for ten (10) years and was a teacher at the Philippine Women’s College of Davao. After this, she moved to SSS office in Region 09, Davao City, where she eventually retired in July, 2009 after 31 years of dedicated service. Ms. Quitain, at one time or another, headed different sections of SSS Region 09, namely: Membership, Real Estate, Operations Accounting, Member Assistance Center, and Sickness, Maternity and Disability Sections. Directorship in Other Listed Companies in the Philippines: None.

Process and Criteria for Selection of Nominees for Directors The Board of Directors set April 21, 2017 as the deadline for the submission of nominations to the Board of Directors. The deadline was duly announced and disclosed on March 1, 2017. The Nominations Committee composed of Manuel V. Pangilinan (Chairman), Robert C. Nicholson, Marilyn A. Victorio-Aquino, Wilfredo A. Paras (Independent Director) and Jose Gabriel M. La Viña screened the nominees for election to the Board of Directors in accordance with the Company’s Manual on Corporate Governance. The Committee assessed the candidates’ background, educational qualifications, work experience, expertise and stature as would enable them to effectively participate in the deliberations of the Board. In the case of the independent directors, the Committee further reviewed their business relationships and activities to ensure that they have all the qualifications and none of the disqualifications for independent directors as set forth in the Company’s Manual of Corporate Governance, the Securities Regulation Code (SRC), the 2015 SRC Implementing Rules and Regulations, and SEC Memorandum Circular No. 19, series of 2016 or the "Code of Corporate Governance for Publicly-Listed Companies." Nominees for Election at Annual Stockholders’ Meeting on June 28, 2017 The Nominations Committee screened the nominees to determine whether they have all of the qualifications and none of the disqualifications for election to the Company’s Board of Directors, and prepared the Final List of Candidates for election to the Board of Directors at the Annual Stockholders’ meeting. The following have been nominated for election to the Company’s Board of Directors:

1. Manuel V. Pangilinan 2. Eulalio B. Austin, Jr. 3. Robert C. Nicholson 4. Edward A. Tortorici 5. Marilyn A. Victorio-Aquino 6. Barbara Anne C. Migallos 7. Michael G. Regino 8. Jose Gabriel M. La Viña 9. Anita Bumpus Quitain 10. Oscar J. Hilado (Independent Director)

16

11. Wilfredo A. Paras (Independent Director) The experience and background of Messrs. Pangilinan, Austin, Nicholson, Tortorici, Regino, La Viña, Hilado and Paras, and of Mses. Aquino, Migallos and Quitain are contained in pages 8 to 15 of this Information Statement. The Company complied with the guidelines on the nomination and election of independent directors prescribed in Rule 38 of the SRC Rules, and the Code of Corporate Governance for Publicly Listed Companies. Mr. Oscar J. Hilado was nominated by Mr. Pangilinan. Mr. Wilfredo A. Paras was nominated by Ms. Migallos. Both nominees have accepted their nominations in writing. There are no relationships between the foregoing nominees for independent director and the persons who nominated them. Messrs. Hilado and Paras were first elected as independent directors on December 7, 2009 and June 29, 2011, respectively. Both Messrs. Hilado and Paras have each served less than the maximum cumulative nine (9) year term recommended by the Code of Corporate Governance for Publicly Listed Companies. The Certificates of Qualification as Independent Director of Messrs. Hilado and Paras are attached to this Information Statement. No director has resigned or declined to stand for re-election to the Board of Directors due to disagreement on any matter. Executive Officers The following persons are the present executive officers of the Company: EULALIO B. AUSTIN, JR. – 55, Filipino citizen. Mr. Austin has been a Director of the Company and PGPI since June 29, 2011 and was most recently re-elected on June 29, 2016. He became President and Chief Operating Officer on January 1, 2012 and President and Chief Executive Officer of the Company on April 3, 2013. He previously served the Company as its Senior Vice President for Operations and Padcal Resident Manager in 2011, Vice President & Resident Manager for Padcal Operations from 2004 to 2010, Mine Division Manager (Padcal) from 1999 to 2003, Engineering Group Manager in 1998, and Mine Engineering & Draw Control Department Manager from 1996 to 1998. Mr. Austin concurrently serves as Director of PXP Energy Corporation and Silangan Mindanao Mining Co., Inc. He likewise sits on the Board of the Chamber of Mines of the Philippines and Philippine Mineral Safety and Environmental Association (PMSEA) and was Founding President of PSEM’s Philex Chapter. He was recently awarded as the CEO of the Year in Mining by The Asset in December 2015. He was also a recipient of Asia Pacific Entrepreneur Award (APEA) for the Mining Industry by Enterprise Asia in 2016. He was also recognized by the Philippine Society of Mining Engineers as the Most Outstanding Engineer in Mine Management in June 2016. Mr. Austin graduated from Saint Louis University-Baguio City, with a Bachelor of Science degree in Mining Engineering and placed eight in the 1982 Professional Board Examination for mining engineers. He took his Management Development Program at the Asian Institute of Management in 2005, and his Advance Management Program at Harvard Business School in 2013. BARBARA ANNE C. MIGALLOS – 62, Filipino citizen. Ms. Migallos was first elected to the Board of Directors of the Company and PGPI on June 26, 2013, and was most recently re-elected on June 29, 2016. She has been the Company’s Corporate Secretary since July

17

1998. She is also Director and Corporate Secretary of PXP Energy Corporation, and Corporate Secretary of Silangan Mindanao Mining Co., Inc. She is the Managing Partner of the Migallos & Luna Law Offices. Ms. Migallos is also Director of Mabuhay Vinyl Corporation since 2000, and Philippine Resins Industries since 2001, and Corporate Secretary of Eastern Telecommunications Philippines, Inc. since 2005 and Nickel Asia Corporation since 2010. She is a professorial lecturer in Corporations Law, Insurance, Securities Regulation and Credit Transactions at the De La Salle University College of Law. She was a Senior Partner of Roco Kapunan Migallos and Luna Law Offices from 1988 to 2006. Ms. Migallos graduated Cum Laude from the University of the Philippines, with a Bachelor of Arts degree, and finished her Bachelor of Laws degree as Cum Laude (salutatorian) also at the University of the Philippines. She placed third in the 1979 Philippine Bar Examination. DANNY Y. YU. – 55, Filipino citizen. Mr. Yu was appointed Senior Vice President for Finance and Chief Financial Officer (“CFO”) on September 2, 2013. He is also the Company’s Compliance Officer and Corporate Governance Officer. Prior to joining the Company, Mr. Yu was CFO of Digitel Communications, Inc. (subsidiary of PLDT) and of Digitel Mobile Philippines, Inc. (Sun Cellular) from November 2011 to July 2013. He was also Group CFO of ePLDT, Inc. and subsidiaries (November 2010 to December 2011); CFO of PLDT Global Corporation (June 2004 to November 2010) and of Mabuhay Satellite Corporation (March 1999 to May 2004). Mr. Yu was also Vice President-Corporate Development of Fort Bonifacio Development Corporation (March 1997 to March 1999). A Certified Public Accountant, he was previously connected with Sycip, Gorres and Velayo & Co. Last year, Mr. Yu was named as the 2016 ING Finex CFO of the Year. Mr. Yu obtained a Bachelor of Science Degree in Commerce, Major in Accounting (Magna Cum Laude) from the San Carlos University in Cebu City. In 1995, he completed a Master’s degree in Management at the Asian Institute of Management. MANUEL A. AGCAOILI – 60, Filipino citizen. Mr. Agcaoili joined the Company as Senior Vice President and Padcal Resident Manager on January 15, 2014. He was previously with MBMI Resources, Inc. (Vancouver, Canada) as Director and President from 2004 to 2014 and Senior Philippine Representative, Narra Nickel Mining and Development Corporation, Tesoro Mining and Development Corporation, and McArthur Mining, Inc. as Director and President from 2006 to 2008, and Lafayette Philippines, Inc. as Director also from 2006 to 2008. He was also previously connected with the Philippine Associated Smelting and Refining Corporation. Mr. Agcaoili graduated with a Bachelor of Science Degree in Metallurgical Engineering at the University of the Philippines in 1980. He also completed a Master’s degree in Business Administration from the Ateneo De Manila University Graduate School of Business in 2002. MICHAEL T. TOLEDO – 56, Filipino citizen. Mr. Toledo has been Senior Vice President for Public and Regulatory Affairs since February 15, 2012. He also heads the Media Bureau of the MVP group of companies. Before joining the Company, he was President and Chief Executive Officer of the Weber Shandwick Manila office since 2006, and was Director and/or Legal and Financial Consultant for various government owned and controlled corporations. Mr. Toledo was also Press Secretary and Presidential Spokesperson for former President Joseph Ejercito Estrada. Mr. Toledo finished a Bachelor of Arts Degree in Philosophy in 1981, and completed a Bachelor of Laws Degree in 1985, both at the University of the Philippines. In 1994, he obtained a Masters of Law degree at the London School of Economics and Political Science.

18

REDEMPTA P. BALUDA – 61, Filipino citizen. Ms. Baluda has been Vice President for Exploration since January 2, 2009. She was formerly Assistant Vice President for Exploration from 2007 to 2009, Division Manager for Environment and Community Relations and Geology for Padcal Operations from 1998 to 2007 and Department Manager for Geology from 1996 to 1998. Ms. Baluda graduated with a Bachelor of Science Degree in Geology at the University of the Philippines in 1976. She also completed the academic units for a Master’s degree in Environment & Natural Resource Management at the University of the Philippines campus in Los Baños, Laguna in 2007. VICTOR A. FRANCISCO – 52, Filipino citizen. Mr. Francisco has been Vice President for Environment and Community Relations since January 2, 2009. He was previously Group Manager for Corporate Environment and Community Relations in 2007, Department Manager – Corporate Environment and Community Relations in 1999, and Assistant Manager – Corporate Environmental Affairs in 1997. Mr. Francisco completed a Bachelor of Science Degree in Community Development at the University of the Philippines in 1987. He also obtained a Masters degree in Environmental Science and Management at the University of the Philippines campus in Los Baños, Laguna in 1995. JOAN A. DE VENECIA – 36, Filipino citizen. Atty. De Venecia has been Vice President and General Counsel of the Company since August 2015. Prior to this, Ms. De Venecia was the Vice President for the Public Relations and Information Services Group at Pag-IBIG Fund, a government owned and controlled corporation. Before joining public service, Ms. De Venecia was a senior associate at SyCip Salazar Hernandez & Gatmaitan. She obtained her Master of Laws in International Legal Studies degree (Hugo Grotius scholar & Fulbright scholar, 2010) from the New York University School of Law; Bachelor of Laws degree (Valedictorian, Cum Laude, Academic Excellence awardee, 2005) from the University of the Philippines College of Law; and BS–Legal Management (hon. mention, 2001) from the Ateneo de Manila University. She ranked 1st in the 2005 Bar Examinations. She teaches law at the UP College of Law, and is a regular Mandatory Continuing Legal Education lecturer on Investor-State Arbitration. Significant Employees No single person is expected to make a significant contribution to the business since the Company considers the collective efforts of all its employees as instrumental to the overall success of the Company’s performance. Family Relationships There are no family relationships up to the fourth civil degree either of consanguinity or affinity among any of the directors, executive officers and persons nominated or chosen to become directors or executive officers. Involvement in Certain Legal Proceedings None of the directors, nominees for election as a director, executive officers or control persons of the Company have been involved in any legal proceeding, including without limitation being the subject of any:

19

a. bankruptcy petition filed by or against any business of which such person was a general partner or executive officer either at the time of the bankruptcy or within two (2) years prior to that time;

b. conviction by final judgment, including the nature of the offense, in a criminal proceeding, domestic or foreign, or being subject to a pending criminal proceeding, domestic or foreign, excluding traffic violations and other minor offenses;

c. order, judgment or decree, not subsequently reversed, suspended or vacated, of any court of competent jurisdiction, domestic or foreign, permanently or temporarily enjoining, barring, suspending or otherwise limiting his involvement in any type of business, securities commodities or banking activities; and

d. order or judgment of a domestic or foreign court of competent jurisdiction (in a civil action), the Commission or comparable foreign body, or a domestic or foreign Exchange or other organized trading market or self-regulatory organization finding him/her to have violated a securities or commodities law or regulation,

for the past five (5) years up to the latest date, that is material to the evaluation of ability or integrity to hold the relevant positions in the Company. Note 31 of the Notes to the Company’s Consolidated Financial Statements as of December 31, 2016, attached hereto, is incorporated by reference. Certain Relationships and Related Transactions

The Company’s significant related party transactions as of March 31, 2017, and as of December 31, 2016, which are under terms that are no less favorable than those arranged with third parties, and account balances are as follows:

a) Advances from the Company to Silangan Mindanao Mining Co., Inc. (SMMCI) and Silangan Mindanao Exploration Co., Inc. (SMECI) The Company, which owns directly and indirectly 100% of SMMCI and SMECI, provides the funds to SMMCI, through SMECI since 2011, and directly to SMMCI thereafter, for the Silangan Project’s expenditures since the Company’s acquisition of Anglo American’s interest in the Silangan Project in 2009. These advances, which are intended to be converted into equity, amounted to P650.6 million as of March 31, 2017, the same as of December 31, 2016.

b) Advances from the Company to PXP Energy Corporation (PXP) The Company made cash advances to PXP for its additional working capital requirements, and for the acquisition of equity in Forum Energy Plc, PetroEnergy Resources Corporation (PERC) and Pitkin Petroleum Plc. As of March 31, 2017 and December 31, 2016, advances from the Company amounted to P2.167 billion and P2.194 billion, respectively. On August 17, 2015, PX and PXP entered into a pledge agreement to secure the advances against certain shares of stocks owned by PXP. In 2017, the Company received partial payment from PXP amounting to P25.1 million (US$ 0.5 million).

c) Issuance of Convertible Bonds to First Pacific and SSS by SMECI In December 2014, SMECI and the Company, as co-issuer, issued 8-year convertible bonds with a face value of P7.2 billion at 1.5% coupon rate p.a. payable semi-annually. The bonds are convertible into 400,000 common shares of SMECI at P18 per share 12 months after the issue date (“Standstill Period”). On the last day of the

20

Standstill Period, the Issuer shall have a one-time right to redeem the bonds from the holders in whole or in part. After the Standstill Period, the noteholders may exercise the conversion right, in whole but not in parts, at any time but no later than the maturity date. At redemption/maturity date, the bonds can be redeemed together with the principal or face value of the bonds at a premium, payable at a rate of 3% per annum compounded semi-annually based on the face value of the bonds and unpaid accrued interest (if there be any). The proceeds of the bonds were used to repay the SMECI’s advances from the Company and fund further exploration works of SMMCI. The carrying value of loans payable amounted to P6.668 billion and P6.593 billion as of March 31, 2017 and December 31, 2016, respectively.

Note 14 and 24 of the Notes to Consolidated Financial Statements on Related Party Transactions, are incorporated hereto by reference.

Item 6. Compensation of Directors and Executive Officers There are no arrangements for additional compensation of Directors other than that provided in the Company’s by-laws which provides that the Board at its discretion may determine and apportion as it may deem proper, an amount of up to one and a half (1½%) percent of the Company’s net income before tax of the preceding year. Payments made in 2016, 2015 and 2014 amounted to P12.7 million, P10.5 million, and P10.6 million, respectively. In 2016, 2015 and 2014, the payments represented only 1% of the Company’s net income before tax. Effective March 2015, the Directors’ per diem increased to P40,000 per board meeting attendance, and P30,000 per committee participation, and are deductible from the annual directors’ compensation provided under Section 7 of the Company’s By-laws. Previously, the rate per attendance for both board and committee meetings was P8,000. In the event that financial results warrant the payment of the annual directors’ compensation under the Company’s by-laws, such directors’ compensation shall be inclusive of the annual total per diem paid to directors. There is no executive officer with contracts or with compensatory plan or arrangement having terms or compensation significantly dissimilar to the regular compensation package, or separation benefits under the Company’s group retirement plan, for the managerial employees of the Company. On June 23, 2006, the Company’s stockholders approved the stock option plan of the Company which was thereafter duly approved by the Securities and Exchange Commission on March 8, 2007. This Plan and all outstanding option shares granted under this plan expired in 2016. On June 29, 2011, the Company’s stockholders approved a new stock option plan covering up to 246,334,118 shares equivalent to 5% of the Company’s outstanding shares of 4,926,682,368 as of June 29, 2011. This plan was approved by the SEC on February 22, 2013, which approval was received by the Company on March 5, 2013. Note 27 of the Notes to Consolidated Financial Statements of the Exhibits in Part V, Item 14 on the Company’s Stock Option Plan is hereby incorporated for reference. The following table shows the compensation of the directors and officers for the past three years and estimated to be paid in the ensuing year. Starting 2008, stock option exercises of the Company’s non-management directors, consisting of the difference between the market and exercise prices at the time of option exercise, are considered as director’s fee for purposes of the table.

21

SUMMARY OF COMPENSATION TABLE

(In Thousands)

DIRECTORS

Year Directors' Fee

2017 (Estimated) P 22,790

2016 P 11,666

2015 P 13,544

2014 P 10,461

CEO AND FOUR MOST HIGHLY COMPENSATED OFFICERS

Year Salary Bonus/Others

2017 (Estimated) P 62,649 P 5,221

2016 P 67,544 P 17,553

2015 P 60,918 P 14,774

2014 P 64,499 P 21,992

Total Officers'

Year Salary Bonus/Others

2017 (Estimated) P 74,317 P 6,193

2016 P 76,754 P 22,101

2015 P 77,938 P 29,971

2014 P 84,829 P 27,669

ALL DIRECTORS & OFFICERS AS A GROUP

Year Total Amount

2017 (Estimated) P 103,300

2016 P 110,521

2015 P 121,453

2014 P 122,959

The aggregate amount of compensation paid in 2016, 2015 and 2014 and estimated amount expected

to be paid in 2017 as presented in the above table are for the following executive officers:

2017 (Estimate) - Eulalio B. Austin, Jr. (CEO), Danny Y. Yu, Manuel A. Agcaoili, Michael T.

Toledo and Redempta P. Baluda

2015 - Eulalio B. Austin, Jr. (CEO), Danny Y. Yu, Manuel A. Agcaoili, Michael T. Toledo

and Redempta P. Baluda

2014 - Eulalio B. Austin, Jr. (CEO), Danny Y. Yu, Manuel A. Agcaoili, Michael T. Toledo

and Benjamin R. Garcia

2016 - Eulalio B. Austin, Jr. (CEO), Danny Y. Yu, Manuel A. Agcaoili, Michael T. Toledo

and Redempta P. Baluda

22

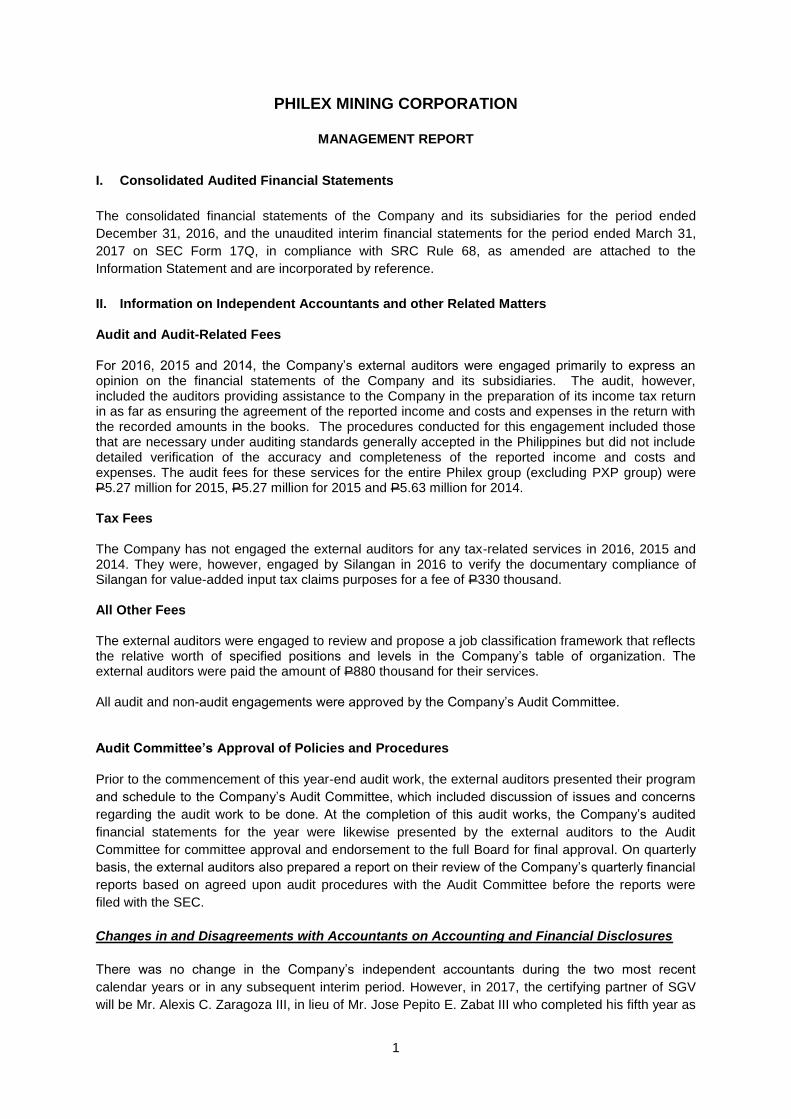

Item 7. Independent Public Auditor The appointment, approval or ratification of the Company’s independent public auditor or independent external auditor for 2017 will be submitted to the shareholders for approval at the Annual Stockholders’ Meeting on June 28, 2017. The Audit Committee has recommended, and the Board of Directors has approved, the reappointment of the auditing firm of SyCip Gorres Velayo & Co (SGV). SGV has been the Company’s independent auditor since 1981. Mr. Alexis C. Zaragoza III will be the certifying partner for SGV for 2017, and will be primarily responsible for the audit of the Company’s financial accounts. Mr. Zaragoza replaces Mr. Jose Pepito E. Zabat III who completed his fifth year as SGV certifying partner in 2016. The certifying partner of the Company’s independent external auditor is rotated at least once every five (5) years, with a two (2) year cooling off period as applicable, in accordance with SRC Rule 68, Part 3(b)(iv)(ix). The Company’s Audited Financial Statements for 2016 as certified by Mr. Zabat is attached to this Information Statement. The Company has been advised that the SGV auditors assigned to render audit-related services have no shareholdings in the Company, or a right, whether legally enforceable or not, to nominate persons or to subscribe to the securities of the Company, consistent with the professional standards on independence set by the Board of Accountancy and the Professional Regulation Commission. Representatives of SGV will be present at the scheduled stockholders meeting. They will have the opportunity to make a statement should they desire to do so and will be available to respond to appropriate questions. External Audit Fees and Services Audit and Audit-Related Fees For 2016, 2015 and 2014, SGV was engaged primarily to express an opinion on the financial statements of the Company and its subsidiaries. The audit, however, included SGV providing assistance to the Company in the preparation of its income tax return in as far as ensuring the agreement of the reported income and costs and expenses in the return with the recorded amounts in the books. The procedures conducted for this engagement included those that are necessary under auditing standards generally accepted in the Philippines but did not include detailed verification of the accuracy and completeness of the reported income and costs and expenses. The audit fees for these services for the entire Philex group (excluding PXP group) were P5.27 million for 2015, P5.27 million for 2015 and P5.63 million for 2014. Tax Fees The Company has not engaged SGV for any tax-related services in 2016, 2015 and 2014. They were, however, engaged by SMMCI in 2016 to verify its documentary compliance for value-added input tax claims purposes for a fee of P330 thousand. All Other Fees SGV were engaged to review and propose a job classification framework that reflects the relative worth of specified positions and levels in the Company’s table of organization. The external auditors were paid the amount of P880 thousand for their services.

23

All audit and non-audit engagements were approved by the Company’s Audit Committee. Audit Committee’s Approval of Policies and Procedures Prior to the commencement of the 2016 year-end audit work, SGV presented their program and schedule to the Company’s Audit Committee, which included discussion of issues and concerns regarding the audit work to be done. After completion of said audit work, the Company’s audited financial statements for the year were presented by the external auditors to the Audit Committee for committee approval and endorsement to the full Board for final approval.

Changes in and Disagreements with Accountants on Accounting and Financial Disclosures

There was no change in the Company’s independent accountants during the two most recent calendar years or in any subsequent interim period, but as noted above, the certifying partner of SGV for 2017 will be Mr. Zaragoza in lieu of Mr. Zabat who completed the 5 year limit of service in 2016.

There has been no disagreement with the independent accountants on accounting and financial disclosure. Item 8. Compensation Plans No action is to be taken by the shareholders at the Meeting with respect to any plan pursuant to which cash or non-cash compensation may be paid or distributed. Item 9. Authorization or Issuance of Securities Other than for Exchange No action is to be taken at the Meeting with respect to the authorization or issuance of any securities otherwise than for exchange for outstanding securities of the Company. Item 10. Modification or Exchange of Securities No action is to be taken at the Meeting with respect to the modification of any class of securities of the Company, or the issuance or authorization for issuance of one class of securities of the Company in exchange for outstanding securities of another class. Item 11. Financial and Other Information related to Items 9 and/or 10 As stated above, no action is to be taken at the Meeting with respect to the matters under Items 9 (Authorization or Issuance of Securities Other than for Exchange) and 10 (Modification or Exchange of Securities). Item 12. Mergers, Consolidations, Acquisitions and Similar Matters No action is to be taken at the Meeting with respect to any transaction involving the following:

a) the merger or consolidation of the Company into or with any other person or of any other person into or with the Company;

24

b) the acquisition by the Company or any of its security holders of securities of