Pharma Mrp 1

90

- 1 - A MANAGEMENT RESEARCH PROJECT ON PHARMACEUTICAL INDUSTRY

Transcript of Pharma Mrp 1

- 1 -

A

MANAGEMENT RESEARCH PROJECT

ON

PHARMACEUTICAL

INDUSTRY

- 2 -

CHAPTER-1

INTRODUCTION OF PHARMACEUTICAL INDUSTRY

1.1 About Pharmaceutical Industry. 1.2 Bulk Drugs and Formulation.

1.3 Research & Development.

- 3 -

ABOUT PHARMACEUTICALS:

Pharmaceuticals are medicinally effective chemicals, which are converted to dosage forms suitable for patients to imbibe. In its basic chemical form, pharmaceuticals are called bulk drugs and the final dosage forms are known as formulations. Bulk drugs are derived from 4 types of intermediates (raw materials), namely

• Plant derivatives (herbal products) • Animal derivatives e.g. Insulin extracted from bovine pancreas • Synthetic chemicals • Biogenetic (human) derivatives e.g. Human insulin

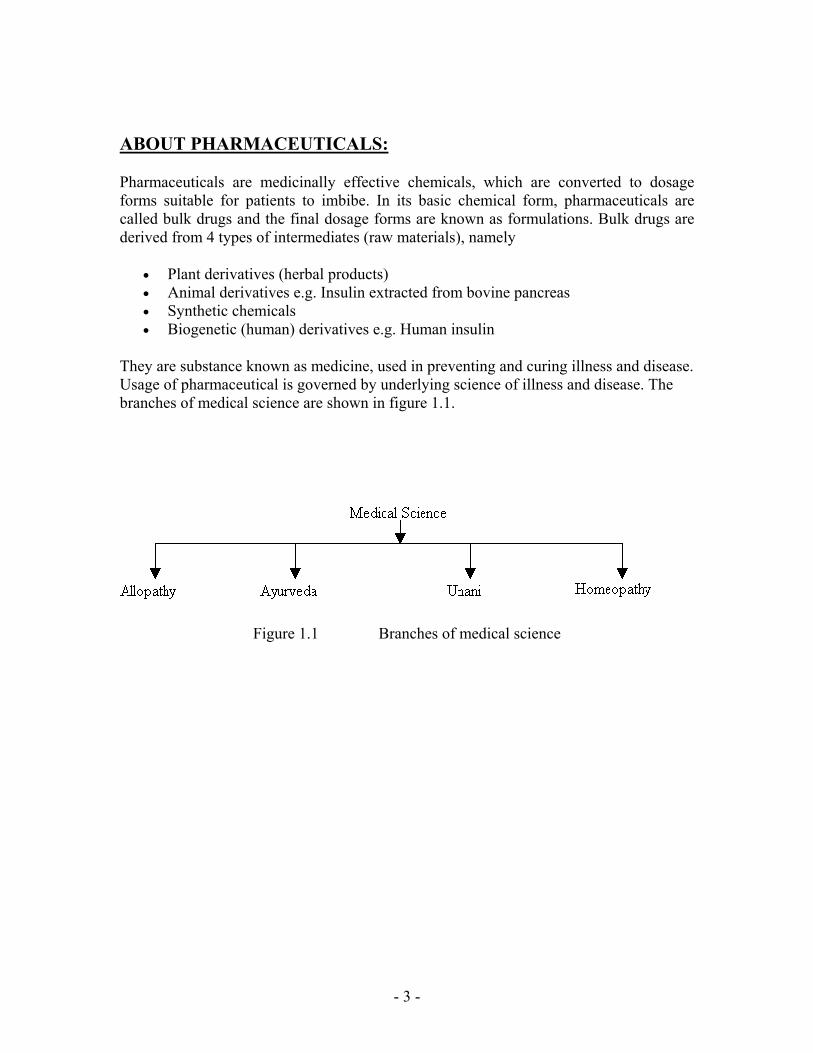

They are substance known as medicine, used in preventing and curing illness and disease. Usage of pharmaceutical is governed by underlying science of illness and disease. The branches of medical science are shown in figure 1.1.

Figure 1.1 Branches of medical science

- 4 -

1) Allopathy: It is known as the modern medicine and world over the pharmaceutical industry is focused upon it.

2) Ayurveda: It is an ancient Indian medical science and mainly uses herbal remedies. It is gaining importance in pharmaceutical market particularly in United States.

3) Unani: It has its origin in China and is prevalent in South East Asia.

4)Homeopathy: It was founded by a German physician and was fairly popular in 19th century. It is still prevalent in third world countries.

- 5 -

BULK DRUGS AND FORMULATION: In basic form, pharmaceutical are called bulk drugs. They are derived from intermediate raw material, namely

1) Plant derivatives

2) Animal derivatives

3) Synthetic chemicals

Formulation:

Bulk drugs in their raw form cannot be used as medicine and they have to be converted in to form in which human can use them as medicine. This type of final dosage form is known as formulations. Formulations can be classified into two types namely,

1) Ethical products These types of formulations are available only under medical prescription to prevent

misuse. Doctors, to cure a disease in the patient primarily prescribe ethical formulations. Generally, for ethical products direct advertisements to users is prohibited.

2) Over the Counter products: These types of formulation known as OTC can be purchased by users directly, for example pain balms, health tonics etc. For over the counter product direct advertisements to user can be used to promote product under certain conditions.

Formulations can be categorized as per the route of administration to patients, namely, 1) Oral: They are taken internally by patients, for example tablets, syrup, capsules, powders etc. 2) Topical: They are applied on skin, for example creams, ointments, liquids, aerosol etc. 3) Parenterals: They are injected in an intravenous and intramuscularly fashion. 4) Others: It includes eye drops, surgical dressings etc.

- 6 -

Research and Development Four types of research are conducted in the pharmaceutical industry:

1. Fundamental or Basic Research: This involves discovering new molecules from scratch. No Indian company does basic research, simply because it is far too expensive. Indian drug companies don’t make the kind of profits required for automation. In the West, compounds are screened by robots or hi-tech equipments and the equipment can cost up to 2 billion pounds (Rs 13,800 crores).

2. Process Research or Reverse Engineering: Here, a company copies a molecule

(Indian patent law covers process patents, not product patents). Reverse engineering by Indian companies has been very cost effective and efficient. However, Western companies regard this as a violation of intellectual property rights (IPR). A new patent law will, obviously, not permit reverse engineering.

3. Analogue or Discovery Research: Companies modify an existing molecule (or a

new one that hasn’t yet been commercialized), after accessing international patent databases, to arrive at a new molecule. Some of the bigger Indian companies (Ranbaxy, Dr Reddy’s, Torrent, Sun pharma) are either conducting discovery research or plan to do so.

4. Genetic Research: It aims at establishing the link between genes and diseases and

could one day determine the best drugs for individuals based on their genetic makeup. No Indian company does this kind of research, but several government or academic institutions (National Institute of Immunology and Jawaharlal Nehru University in New Delhi, Center for Microbiology in Hyderabad) have begun work in this area.

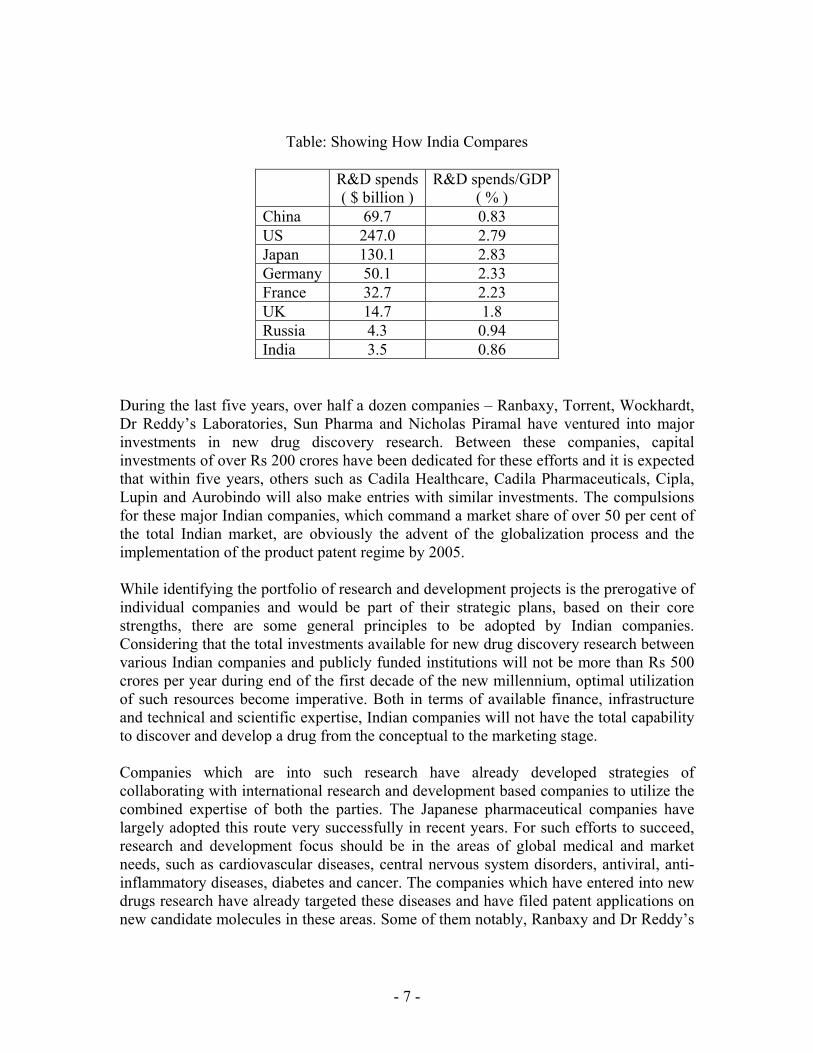

Few doubt that India has the potential to emerge as a global research and development base in sectors like pharmaceuticals and software. But that does not necessarily mean that it will. The key lies in the country’s ability to scale up its research and development expenditure. At last count, India’s research and development expenditure stood at 0.86 per cent of the GDP, which is much lower than that 0of developed countries such as the US (2.79 per cent), Japan (2.83 per cent) and Germany (2.33 per cent). Similarly, if India has to realize its potential of becoming a leading supplier of generic drugs, the pharma sector will need to increase its R&D spend almost five-fold in the next five years- from Rs 320 to 1,500 crores.

- 7 -

Table: Showing How India Compares

R&D spends( $ billion )

R&D spends/GDP( % )

China 69.7 0.83 US 247.0 2.79 Japan 130.1 2.83 Germany 50.1 2.33 France 32.7 2.23 UK 14.7 1.8 Russia 4.3 0.94 India 3.5 0.86

During the last five years, over half a dozen companies – Ranbaxy, Torrent, Wockhardt, Dr Reddy’s Laboratories, Sun Pharma and Nicholas Piramal have ventured into major investments in new drug discovery research. Between these companies, capital investments of over Rs 200 crores have been dedicated for these efforts and it is expected that within five years, others such as Cadila Healthcare, Cadila Pharmaceuticals, Cipla, Lupin and Aurobindo will also make entries with similar investments. The compulsions for these major Indian companies, which command a market share of over 50 per cent of the total Indian market, are obviously the advent of the globalization process and the implementation of the product patent regime by 2005. While identifying the portfolio of research and development projects is the prerogative of individual companies and would be part of their strategic plans, based on their core strengths, there are some general principles to be adopted by Indian companies. Considering that the total investments available for new drug discovery research between various Indian companies and publicly funded institutions will not be more than Rs 500 crores per year during end of the first decade of the new millennium, optimal utilization of such resources become imperative. Both in terms of available finance, infrastructure and technical and scientific expertise, Indian companies will not have the total capability to discover and develop a drug from the conceptual to the marketing stage. Companies which are into such research have already developed strategies of collaborating with international research and development based companies to utilize the combined expertise of both the parties. The Japanese pharmaceutical companies have largely adopted this route very successfully in recent years. For such efforts to succeed, research and development focus should be in the areas of global medical and market needs, such as cardiovascular diseases, central nervous system disorders, antiviral, anti-inflammatory diseases, diabetes and cancer. The companies which have entered into new drugs research have already targeted these diseases and have filed patent applications on new candidate molecules in these areas. Some of them notably, Ranbaxy and Dr Reddy’s

- 8 -

Laboratories have already entered into licensing arrangements with international companies. Besides these areas, it is also imperative that Indian companies involve themselves in research and development for the discovery of new drugs for diseases which are largely endemic to the developing countries. Many of these diseases have not been properly addressed by the multinational corporations in view of the small market and the low buying power of the patients. In such cases, since they largely belong to the orphan drug category, with potentially very low commercial returns, government and international agencies should subsidies the companies by providing funds for carrying out research in those areas. While fixing targets for outcomes from research and development inputs is risky, it is fair to assume that with annual investments reaching Rs. 500 crores per year by 2010, form all sources, Indian industry should be able to discover and develop at least three new molecular entities per year for various disease conditions. It is also expected that around 50 new patents will be issued or applied for, based on Indian research efforts. A part form the above investments by Indian companies, multinational companies will also invest in basic research in India, including clinical research, both on their own and through contract research organizations. Considering the variety and quantum of intellectual capital available and low overhead costs, it is fair to assume that international companies will do well to establish research and development centers here. Other areas which have the potential to be major targets for attention in India are research and development efforts in innovative and patentable new drug delivery systems for established drugs, a relook at racemic molecules with reference to the potential for developing new chiral drugs, biotechnology products and development of new clinical indications for drugs in current use. Most importantly, an area of great relevance to India is the area of drugs based on the Indian traditional system of medicine. General Insurance Company (GIC) is the sole medical insurance provider in the country, covering only 4 per cent of the population. There could be significant opportunities for pharma companies when the health insurance sector opens up to private sector. By forming exclusive alliances with insurance companies, pharma companies could potentially increase penetration of their products within the insurer’s customer base. Based on patient’s medical records from insurance companies, they could undertake customized marketing and distribution programs to increase sales and build loyalty.

- 9 -

Recognizing the importance and strengths of the Indian pharmaceutical industry, the Government of India has made conscious efforts to assist its overall development to meet the challenges of the post 2005 era. The two committees which have been constituted for this purpose have come out with very positive recommendations to create an ambience conducive to the development of a strong research and development based drug industry supported by appropriate fiscal measures. At this stage, the Indian industry needs this support and its success will depend only on the concerted efforts of all parties concerned with healthcare in this country.

- 10 -

CHAPTER -2 INRODUCTION OF INDIAN PHARMACEUTICAL

INDUSTRY 2.1 – Overview 2.2- History and Development 2.3- Major Therapeutic Segments 2.4- Growth drivers of the Indian

Pharmaceutical Industry.

- 11 -

2.1 OVERVIEW:

• The pharmaceutical industry is a lifeline industry which plays a very crucial role in building a strong human capital of a country and is very essential for economic growth and development.

• Today, it is at the top end of India's science-based industries with wide ranging capabilities in the complex field of drug manufacture and technology. The contribution of the pharmaceutical industry towards a nation’s growth cannot be undermined.

• The Pharmaceutical industry in India is one of the largest and most advanced among the developing countries.

• Today it is in the front rank of India’s science-based industries with wide ranging capabilities in the complex field of drug manufacturing and technology.

• The Indian pharmaceutical industry is highly fragmented, but has grown rapidly due to the friendly patent regime and low cost manufacturing structure.

• Globally, the output of Indian pharmaceutical industry ranks 4th in terms of volume and 13th in terms of value.

• Intense competition, high volumes and low prices characterize the Indian domestic market. Exports have been rising at around 30% CAGR over last five years.

• In India, medicines account for 2.5% in hospitalization and 0.5% in domiciliary treatment cost.

• There could be sharp dip in the growth rate in the population in India, which is already down to about 1.7% year and is projected to go down further to about 1.5% by the turn of the century and to roughly 1% by2010.

• Indian’s per capita expenditure for healthcare remains Rs.115.5 compared to the US (Rs.6876.00) and Japan (Rs.14, 832).

• In India the values for pharmaceutical production of bulk drugs and formulations in 2001-02 were Rs.5439 Crores and Rs. 21104 corers respectively.

• The Indian Pharmaceutical market ranks about 20th in the world and accounts for less than 1% of world market. It is expected by 2003; the market could be worth of $ 7-9 billion (Rs.280 billion to Rs.360 billion).

• India accounts for 6% of all bulk drugs export. There are about 250 large/medium units and about 8000 small-scale units in operations, which form the core of the industry. There are about 350 bulk drugs i.e. active pharmaceutical molecules having therapeutic values and used for production of pharmaceuticals, which accounts for, majority of formulations produced in the country.

• During the year ending March 1998, pharmaceutical companies for various bulk drugs, formulations and intermediates filed 265 IEMs. These IEMs are expected to generate employment for about 19000 people and there would be an investment of approximately Rs.4.1 billion on these projects. During the same period foreign investment proposal worth approx. Rs.1.6 billion were approved.

• Between August 1991 and March 1998, Gujarat received 5174 proposals for the projects and topped the list in terms of value of investment, which was estimated

- 12 -

to be Rs.1379 billion during that period. Next to Gujarat was Maharashtra and other States receiving more than 5% of the investment proposal are Tamil Nadu, Andhra Pradesh, Karnataka, Uttar Pradesh, Punjab and Madhya Pradesh.

• The top 12 companies in India together will have a turnover of around 50 billion in the domestic market by 2005, or approximately 25% of industry turnover. About half a dozen companies with a turnover of Rs.35 billion by 2005 will be able to spend about 8% of their turnover on research.

• The Drug Pricing Control Order (DPCO) has severely restricted profitability and hence innovation. However, the government has been relaxing controls in a slow but progressive manner. The span of control of DPCO has come down from 90% in 1980s to 50% in 1995 and is likely to be further reduced as per the latest proposed changes.

• In the domestic market, old and mature categories like anti- infectives, vitamins, analgesics are degrading or stagnating while new lifestyle categories like cardiovascular, CNS, anti diabetic are growing at double-digit rates. The growth of a company in the domestic market is thus critically dependent on its therapeutic presence.

• The growth in the Indian pharmaceuticals:

Industry at around 15% p.a. compares well with the industry’s growth of 14% per annum in North American Region. India is ranked 5th in the World, and accounts for 8% of the worlds production of drugs and pharmaceuticals by volume.

• Globally, the output of Indian pharmaceutical industry ranks 4th in terms of volume and 13th in terms of value.

• In FY02, the domestic Indian pharma market was valued at $4.5bn, representing 1.6% of the global market, and is growing at an annual rate of 8 to 9%.

• The industry produces about 60,000 finished medicines and roughly 400 bulk drugs, which are used in formulations.

• At the end of FY01, the Indian pharmaceutical industry had over 23,000 units, although this number cannot be authenticated. Around 260 players constituted the organized sector while 6,000-8,000 players existed in the small scale sector.

• The industry is highly fragmented, with the largest formulation players having a market share of less than 6%.

• The top ten players account for 36% of the formulation market in contrast with the global scenario where the top ten players account for 49% of the Pharmaceutical market.

• In FY01, the total output of the Indian pharmaceutical industry was Rs 229 bn, which grew by 16% yoy. In FY02, it was above Rs. 260 bn, of which bulk drugs accounted for Rs. 54 bn (21%) and formulations Rs 210 bn (79%).

• The demand for the industry is mainly from urban areas (74%).

- 13 -

• Urban areas witnessed a 15% increase in sales in FY02 as against 13% in FY01. • The industry grew at 2.6% yoy during Oct 2002 and 9% during Jan to Oct 2002. • In FY03, the industry would have grown by 10-15% increase in sales, production

and exports, despite adverse global conditions. • The odd 400 bulk drugs make up 20% of total drug production. During FY91-

FY01, the production of bulk drugs increased at a compounded annual growth rate (CAGR) of 20%.

• On the other hand, formulations, which are the end product of the medicine manufacturing process, had a CAGR of 17% during FY91-FY01. Most of the domestic demand for formulations is met by the domestic industry.

- 14 -

2.2 HISTORY AND DEVLOPMENT:

History of pharmaceutical industry in India:

• India’s traditions in the science of health and healing go back to the halcyon days of Susruta, Vaghatta and Charska. Our systems of medicine like Ayurveda were well established and schools and hospitals with treatises and instructions manual were in wide use.

• The establishment of a modern pharmaceutical industry in India may be and to have commenced with the setting up of Bengal Chemicals by Acharya P.C. Ray in Calcutta and of Alembic Chemicals in Baroda, by B.D. Amin. Significant who helped the indigenous drug industry were the establishment of the Haffkine Institute in Bombay, the King Institute in Madras in 1904 and the Pasteur Institute in Coonoor in 1907.

The Early Years

• The industry received a fillip during World War I as the local demand for allopathic medicines increased steeply and imports were almost completely cut off. The outbreak of World War II proved to be a shot in the arm for the industry. A number of products in the category of phyto-chemicals, based on indigenous raw materials and several synthetic drugs and biological were manufactured during the war period. The immediate post-war years (1945-1947) experienced a continued shortage of drug and pharmaceuticals throughout the world. The industry in India had, therefore, no difficulty in maintaining its tempo of growth.

Post Independence Development

• In the post-independence years, several international pharmaceutical companies have set up manufacturing facilities in the country. Public sector units like HAL and IDPL were also set up. The diversified character of the industry's growth is reflected in the range and variety of products manufactured. These cover a wide therapeutic spectrum ranging from antibiotics to vitamins. The following table gives us a picture of the progress of drug industry in India.

In Financial year 2002:

• Several out licensing deal have been entered into pharma majors in the last few months and many more are ripe. This is a strong pointer to the fact that the country is gearing up for the patent regime (post 2005). Dr. Reddy’s anti-diabetic molecule out licensed to Novo-Nordisk entered the last stage of clinical trials before it enters commercial.

• The domestic industry recorded a 9% growth rate, falling short of historic double-digit growth rates. The primary reason for the same is due to the fact that domestic market continues to remain price sensitive and premium pricing of product is extremely difficult to maintain.

- 15 -

• MNC’s continued to under perform their domestic peers for the second consecutive year in succession. While the top 5 domestic companies recorded a revenue growth of more than 20% last year, consolidated MNC pharma growth was less than 3% with margins at half the average of domestic majors. However, MNC’s have been quick in responding to this trend with most companies intensively restructuring their operations in a bid to bounce back. Post restructuring, MNC pharma majors are expected to record healthy growth rates though growth rates are still expected to be lower than the domestic majors.

• The pharma industry is expected to have grown by 8-9% in FY01. While top 5 domestic companies have grown at 14% in FY01, top 5 MNC’s have grown at a slower rate of 7.2%. The slow growth in sales of MNC’s is because of their relatively older product portfolio. As in the past MNC’s continued to shy away from launching new products in the domestic markets.

• Growth in traditional therapeutic segments such as antibiotics is stagnating and competition is increasingly getting stiffer. The price war is so intense that companies have in-fact started promoting unbranded versions of formulations (alternatively called as “generic generics”) against their own branded formulations, to generate growth. However, life style segments such as cardiovascular, anti-diabetes, anti-ulcer and anti-depressants are lucrative and fast growing. Growth in domestic sales in the future will depend on the ability of companies to launch/shift products in relatively fast-growing therapeutic segments. These are likely to be the key earnings drivers. Volumes may, however, continue to come from traditional segments such as anti-invectives, vitamins, tonics and mineral supplements.

• A committee, formed to recommend measures for legitimizing the OTC business in India, has suggested that some 67 brands be sold through OTC. This will help in expanding the size of the market, as companies will be permitted to advertise via mass media and increase availability of these products.

• A new concept that is gaining momentum in the pharma industry is contract research apart from contract manufacturing. Given the low cost high quality advantage Indian companies are poised to benefit from contract research business on behalf of multinationals. As for contract manufacturing, large global pharmaceutical companies are finding it profitable to outsource production. To cash on these opportunities many large production houses in the country are becoming US FDA compliant.

• The expiry of patents going off patent in the next few years is opening up big opportunity for domestic companies to capture the consequent generic market in the US and the Europe. The US generic market is projected to be US $ 15 bn by 2004. Though generic is low margin business, Indian company’s skills in reverse engineering and cost effective production enables them to yield better realisations. Indian Pharma companies like Sun Pharma, Dr. Reddy, Ranbaxy are aggressively trying to cash in on this opportunity.

• The government has recently allowed 100% Foreign Direct Investment Pharma FDI in drugs and pharmaceutical companies. This is expected to open floodgates of contract research work in the country. However, technology transfer by MNC’s even to 100% subsidiaries seems quite unlikely before 2005 deadline.

- 16 -

• The penetration of health insurance is abysmally low in the country. The entry of private players would not only bring in quantum leap in the health insurance business but also increase capital inflows into this sector. It would also bring in the concept of managed healthcare in the country. These would finally lead to overall increase in per capita usage of drugs.

- 17 -

2.3 MAJOR THERAPEUTIC SEGMENTS:

This section gives an overview of the major therapeutic segments in the Indian pharmaceuticals sector. These segments account for nearly 85% of the domestic formulation market

Indian TherapeuticSegments

Market Share (%)

Growth

Systemic Antibiotics 15.7 5.9 Cardiovascular 6.9 17.4 CNS 6.5 11.5 Vitamins 6.1 8.7 Anti-Inflammatory 6 12.9 Cough and Cold Preparations 5.3 1.7 Antacid and anti-Ulcerants 4.3 15 Anti-TB 2.5 -3.1 Anti-anemic 2.8 10.7 Anti-diabetic 2.7 34.1 Analgesic 3.10 15 General nutrients 1.80 -1. Anti parasitic & antifungal 3.9 19

- 18 -

1. Analgesics & anti-pyretics:

• They are used for relief in pain/ fever. In this segment, most of the popular drugs like Aspirin, Analgin and Paracetamol are off patent.

• Yet, DPCO coverage is high hence, margins are low. In case of formulations, including OTC brands and anti-spasmodic combinations, the market size is around Rs. 3.1 bn and is growing 15% yoy.

• But, a large number of local players result in keen competition, while volumes drive sales.

• Major players in formulations are Burroughs Wellcome, SmithKline Beecham, Hoechst and Wockhardt. Paracetamol and Analgin formulations also have large export markets.

2. Antacids and anti-ulcerants

• This segment has large number of new under-patent molecules, due to ongoing R&D on developing more effective ways to combat acidity/ ulcers.

• DPCO coverage is high as it encompasses the major drug Ranitidine. But, as this globally popular anti-ulcer drug has gone off patent in Jul ’97, there are good export opportunities.

• The domestic formulations market for antacids is estimated to be Rs 4.3 bn, growing 15% yoy.

• Major players are Knoll and Parke Davis. For anti-ulcer formulations, market size is Rs2.3bn growing at 17-18% yoy, with major growth in Omeprazole based formulations.

• Major players are Glaxo, Cadila, Ranbaxy, and Dr Reddy’s Labs etc.

3. Antibiotics:

• They are a vast range of drugs. The earlier generation drug groups such as Penicillins (e.g. Amoxycillin) and Macrolides (e.g. Erythromycin) have mostly gone off patent. Newer generation groups like Quinolones (e.g. Ciprofloxacin) and Cephalosporins (e.g. Ceftriaxone) are still largely under patent.

• DPCO mostly encompasses the latest generation drugs. Penicillin-G, itself an antibiotic drug, is a common intermediate for many other antibiotics.

• Total domestic formulations market is estimated to be Rs 15.7 bn and is growing at 5.9% yoy. Of this, 27% is accounted by semi-synthetic Penicillins. The fastest growing major subgroup is Cephalosporins at 23.9% yoy.

• Major players are Glaxo, Ranbaxy, Cipla, Hoechst, Alembic, Burroughs Wellcome, and Ambalal Sarabhai etc.

• Antibiotics also have a large export market, especially off-patent drugs like Amoxycillin, Ampicillin, Sulphamethoxazole and Cephalexin. Cephalosporins, which will be going off patent in near future, have a high export potential.

- 19 -

4. Anti-tuberculosis:

• These products find greater application in developing nations due to tropical concentration of the disease incidence. All popularly used drugs are off patent

• DPCO continues to cover the main drug Rifampicin. • The dominant player in both bulk drugs and formulations is Lupin. The domestic

formulations market is estimated to be Rs 2.5 bn, losing 3.1% yoy. • Other major players are Hind. Ciba and Cadila. MNCs like Glaxo and Hoechst are

increasing their presence in this segment. Export opportunities may grow manifold if the spread of AIDS leads to large-scale resurgence of TB in developed nations.

5. Cardiac therapy:

• It is the world’s top therapeutic segment and new drugs are continually introduced by MNCs abroad.

• However, most of the drugs popularly used in India are off patent. DPCO coverage is also low.

• Domestic formulations market size, estimated to be Rs 6.9 bn is growing 17-18% pa.

• The leading players are mostly local companies like Sun Pharma, Torrent, Cadila, ICI etc. Share of MNCs is relatively low. With increasing level of urbanization in India, heart trouble is on the rise. Also, cardiac care is a long-term therapy, providing a good market for the players.

6. Anti-rheumatics:

• These products relieve inflammation/ joint pain and also have analgesic/ anti-pyretic properties.

• All major drugs used in India are off patent yet DPCO coverage is high especially due to inclusion of major drug Ibuprofen under price control. However, DPCO ’95 excluded another major drug Diclofenac Sodium. The domestic formulations market is estimated to be Rs 6 bn, growing at 12.9 %yoy. The growth is again hampered by DPCO coverage, while volumes largely drive sales.

• Major players are MNCs like Knoll, Roussel, Hind Ciba, and Pfizer etc. Local players have higher presence in topical formulations. A large global market for anti-rheumatics makes Ibuprofen the top pharmaceutical product exported from India. But, even here multiple players has kept margins low.

- 20 -

7. Respiratory system:

• Ailments like cough and are common occurrences, especially among children. Asthma is often chronic, providing assured long-term demand for medication. Patent coverage is very low.

• Also, as DPCO has excluded most popular anti-cough drugs, there have been price hikes and high sales growth.

• The domestic cough & cold formulations market is estimated to be Rs 5.3 bn, growing 1.7% yoy.

• Of this 75% are anti-cough preparations, wherein major players are MNCs like Pfizer, Parke Davis, Rhone Poulenc. In anti-cold formulations, key players are Burroughs, Alembic etc. The anti-asthmatics market is Rs2bn, growing 15.5% yoy. The dominant leader here is Cipla.

8. General Nutrients:

• They are taken mostly in case of deficiencies in India. Globally, the trend is towards imbibing them as a tonic.

• So, if such a fad catches on, the Rs 1.8 bn domestic market losing 1% yoy, would notch good growth in future.

• All drugs are off patent but DPCO coverage is very high. • Leading players are MNCs like E-Merck, Pfizer, Glaxo, Abbott etc. Local players

have very poor presence in the segment, probably deterred by the high DPCO coverage which limits margins.

9. Other therapeutic segments:

• This covers segments like Anti-anemic, Anti-diabetes, Anti-emetic, Anti-histamine, Anti-malarial, CNS & Psychiatric therapy, Gynecological, Nutrients & Mineral Supplements.

• The major group is a Psychiatric product, which has Rs 6.5 bn market, growing 11.5% yoy. All other groups range between Rs 1-2 bn in size.

• The antidiabetic market is growing at the rate of 34% in present environment.

- 21 -

2.4 GROWTH DRIVERS OF THE INDIAN PHARMACEUTICAL INDUSTRY:

Indian pharmaceutical industry, which is highly fragmented due to various therapeutic segments and specialty of individual firm in each segment, drive it due to following growth drivers in the present era.

• Industry’s entrepreneurship and its scientific and technological skills:- Unique blend of this two key elements with innovative marketing strategies gave cutting edge to the Indian companies in the market.

• Low manufacturing cost base: The cost of manufacturing is lower in India due to low labor costs and lower equipments cost.

• High process development skills: Specialization of the companies by reverse engineering enables them to develop cost effective and non-infringing processed for product going generic. India has a history of developing such processes due to the prevalence of process patents.

• Business Environment: The government has recently allowed 100% Foreign Direct Investment Pharma FDI in drugs and pharmaceutical companies. This is expected to open floodgates of contract research work in the country.

• Innovative Scientific manpower & competent workforce: India has a pool of personnel with high managerial and technical competence as also skilled workforce. It has an educated work force and English is commonly used. Professional services are easily available.

• Friendly Patent regime: The current Patent law in India relating to Pharmaceuticals provides for only process patent which encourage various small scale companies to go for reverse engineering and make the profit.

- 22 -

Chapter 3

Emergence of Indian Pharma MNCs

3.1 Global MNCs

3.2 R&D in MNCs

3.3 Emerging Indian Pharmaceutical Industry

3.4 Emerging global generic market

- 23 -

Global MNCs: Global leaders of the pharma industry which dominate all components of business and industrial activity in drugs, including R & D, production and marketing are the MNCs located primarily in the US, Western Europe and Japan. MNCs are defined as ‘Large Business Companies which operate in many countries’. These highly visible corporations which are generally regarded as products of the capitalists and free trade societies of the Western world, gained their dominance during the second half of the last century. Today they control the markets as well as the economies of not only the countries where they are based, but also of many other countries in the developed and developing world. In the pharmaceutical industry the top twenty companies of the western world command over 60% of the global markets and due to various compulsions, these companies are getting to be more and more dominant through arrangements between them. The global MNCs have some special characteristics, even though, even within them, there are wide disparities. For example, the US MNCs have over 60% of their global sales coming from their domestic market, while the MNCs of the smaller European countries such as Switzerland, Sweden, Denmark etc. sell over 90% of their global production abroad. The third category of MNCs is illustrated by the case of Japan, which has over the last half a century adopted a policy of licensing their products to western MNCs for development and marketing in territories outside Japan. R&D in MNCs: Over 90% of the drugs available today have been discovered and developed by the R & D based MNCs, the majority of them from the USA. These US companies together had a turn-over of around $178 billion ($130 billion in USA and $48 billion abroad) in 2001. as a percent of sales, their average R & D spend within the US in 2001 was around 13.8% and abroad around 3.5%. Over 60% of their total R & D expenditure is currently in areas of cancer (18.5%), infections (12.7%), and cardiovascular system disease (11%). Outside the US, R & D activities of US MNCs are largely in Western Europe (52%), Japan (12%), Canada (5.3%) and Central & Eastern Europe (5.2%). It is significant that R & D spending by MNCs of Us origin in the Asia-Pacific region is as low as 0.9% of their total investment in R & D. Global MNCs in most cases market their products in over 100 countries of the world, directly or through their fully or partly owned subsidiaries. Yet another characteristic of their operations is that they, as a rule, set up manufacturing and R & D bases in locations which provide maximum benefits to them in terms of costs of production. Critics of MNCs feel that these companies have no allegiance to the countries where they operate

- 24 -

and have little regard for the economic or societal problems of the countries where they are domiciled. The three major trade blocks, the European Community (EC), the North American Free Trade Agreement (NAFTA) and the Asian-Pacific Economic Conference (APEC), as well as the General Agreement for Tariffs and Trade (GATT), have further provided the impetus for MNCs to freely roam the world at their pleasure and sweet will. The MNCs have also mastered the science of transfer pricing as a valuable tool to maximize profits form global business, across countries. Emerging Indian Pharmaceutical MNCs: Indian pharma companies need to satisfy the following conditions if they are to graduate to the status of multinational corporations (MNCs):

• A product range of relevance to major markets abroad.

• Access to these markets with generic (patent expired or non patented) products.

• Costs and price advantages.

• Production as per the regulatory requirements, such as adherence to Good Laboratory, Good Manufacturing and Good Clinical Practices.

• R & D capability for discovery and total or partial development of drugs relevant

to other markets.

• Marketing facilities through subsidiaries or through tie-ups with local companies.

• Ability to get Abbreviated New Drug Application (ANDA) approvals to enable early marketing of generic versions of patented drugs.

Indian Companies with Potential to be Drug MNCs: It is significant that in the US and Western Europe, the largest MNCs are those which are research based companies, each one of them investing over $1 billion annually in R & D mostly on new drugs research. While the US companies spend bulk of the R & D budget within the US, they increasingly carry out or outsource R & D from companies abroad. For example, while the growth in domestic R & D by these companies was 11.8% in 2001 over 2000, the corresponding figure for R & D abroad was 33.8%. The companies in India which have invested in New Drugs Discovery Research include Ranbaxy, Dr Reddy’s Laboratories, Torrent, Wockhardt, Zydus Cadila, Cadila Pharma, Lupin, Sun Pharma, Cipla, Nicholas Piramal, US Vitamins, Orchid, Aurobindo, Glenmark, Kopran and Unichem.

- 25 -

Like the US association of PhRMA, 12 of these companies have formed a new association, termed the Indian Pharma Alliance, whose members account for 90% of the total expenditure on new drug research in India. Their total sales top $1 billion, constituting 30% of the exports from India. Within the short period of 5-8 years over half a dozen Investigational New Drug Application (INDA) of these companies have been approved by the Indian drug control authorities in areas as diverse as Benign Prostatic Hyperplasia (BPH), diabetes, microbial and fungal infections, asthma cardiovascular diseases and cancer. Some of these products under development have been licensed out to MNCs such as Novo Nordisk, Novartis, Bayer etc. other Indian companies which also have candidate drugs for development are Dabur, Glenmark and Kopran. The strategy adopted by all these companies has been to initiate discovery programme in chosen therapeutic areas, identity candidate molecules, file international patents and license them to global pharma companies for development and marketing on terms which will include milestone and royalty payments. Examples of success in new drug research in India include the discovery of eight candidate molecules by Dr Reddy’s Laboratories, three for type II diabetes, three for cancer, one each for inflammation and elevated cholesterol and seven from Ranbaxy, of which three are for BPH, two for additions to several new drug delivery systems, including the once daily formulation of Ciprofloxacin licensed to Bayer. While Wockhardt has three biogenetic molecules and two anti-infective in the pipeline, Cipla has been active in developing improved therapy for asthma, cardiac care and oncology, Torrent has in their pipeline, products for hypertension and diabetes, while Glenmark has candidate molecules for respiratory diseases, Kopran for gastro-intestinal disorders and Sun Pharma has a number of drug delivery systems and one product in human trials. Overall, considering the relatively low investments made by India companies, their track record should indeed be considered impressive. Entering Global Generic Markets: The 1970 Indian Patents Act enabled the Indian Companies to master the process technologies for the production of most of the bulk drugs used in formulations. Exports of these products however have been restricted to only countries where there are no valid patents for the products. The new strategies which Indian companies can adopt, include the manufacture and exports of generic drugs, which are outside patents for the global markets. Between 2002 and 2005, drugs currently valued at $40 billion are going off patents, in USA alone. For example, patents on several block-busters such as Prilosec for ulcers ($4bn), Claritine for allergy ($3.4bn) and Neurotin for epilepsy ($1.4bn) are expiring in

- 26 -

2002, Depakote for CNS disorders ($800mn), Accupril for hypertension ($600mn), and Ortho Cyclene for Contraception ($650mn), in 2003, Glucovance for diabetes ($2bn), Flovent for asthma ($1.6bn), Procrit for anemia ($1.5bn) and Diflucan for vaginal candidiasis ($1 bn) in 2004 and in 2005 , Provacid for Ulcer ( $ 3.75 bn ), Zoloft for depression ($3bn) & pravachol for hyper cholesterolemia ($1.7bn). India has the capacity to produce all of these bulk drugs and offer them at competitive for the global generic market. Already the leading companies have made considerable process in this direction, which calls for early approval, of Abbreviated New Drug Applications (ANDAs) to enable companies market the generic products immediately after the product expires, for example, Ranbaxy has over no ANDAs and over 30 drug master files (DMFs) filed in USA $ Europe, Dr. Reddy’s 7&35, Cipla over 40 DMFs, Wockhardt 5 ANDAs & 18 DMFs and Sun pharma 6ANDAs. Marketing strategies have involve direct selling and through subsidiaries as well as through major generic companies, such as Andrx, Ivax, Teva, Par, Warrick etc. the companies have been expediting their ANDAs so that benefit form the exclusivity for 180 days provided for , under the Hatch-Waxman Act is available to them ahead of other major products which have been target several blockbusters such as Fluoxetine, omeprazok, ciprofloxacin amlodipine, setraline, albendazole, metformin, and some of the biotechnology products such as erythropoietin, human insulin and hepatitis is vaccine . Conclusion It is obvious that top ten Indian pharma companies have the potential to become MNCs in the global context, even though in size and available resources, they will be mini MNCs. These companies will have annual sales ranging form $ 400 mn to $1.5 bn by 2010 and will spend 10% of their sales turn over on R&D, bulk of it, on new drug discovery These companies will be to 100 countries & belt them will be able to discover and develop 3 to5 new technology entities per year, out of which two will be relevant to the developing world, they will follow a collaborative mode including licensing co-development and/or marketing of their product with global MNCs. India thus will be the fourth largest pharma force in the world, next only to USA, western Europe and Japan , with around a dozed companies opening in all the major markets of the world.

- 27 -

CHAPTER-4

WTO & ITS IMPACT ON INDIAN PHARMACEUTICAL INDUSTRY

3.1 Impact of Global Regulation on Indian Pharmaceutical Industry

3.2 WTO & Indian Pharmaceutical Industry

- 28 -

Impact of Global Regulation on Indian Pharmaceutical Industry.

Globalization is a process which involves economic inter-dependence of countries world-wide removing all barriers for economic integration as if the whole world is a single village. Obviously, in this process, the rich nations with their superior financial power, control the scenario and the poor and the developing nations are forced to integrate surrendering their economic independence knowing fully well what they are forced to accept is really prejudicial to their own interest. In this process the world financial institutions like the World Bank, IMF and now the WTO advance the interest of the rich countries alone. The draconian policies of the World Bank and the IMF under the structural adjustment programme resulted in the net transfer of $178 billion between 1984 and 1990 from the poor countries to the commercial banks of rich nations. (UNDP Human Development Report, 1994). The Transnational Corporations (TNCs) of the rich nations are practically controlling the world finances. Today, the whole world is colonized by global finance and the TNCs supported by the neo-colonial structure including the World Bank, IMF and WTO are controlling the financial situation world-wide. The governments of third world countries are powerless against global finance and are unable to control its movement within their own national boundaries.

The situation of the world drug industry is no different. 'Operating at the behest of the Pharmaceutical Research and Manufacturers' Association (PhRMA) for a decade and a half, the U.S.Government has waged a ruthless crusade to force third world countries to adopt strait jacketing intellectual property rules at the expense of protecting public health', says the editorial comment in the June 1998 issue of Multinational Monitor, a journal published from Washington.

The structural adjustment programme introduced by the government of India at the behest of the IMF, World Bank and WTO created a serious impact on India's drug industry, health care system, on the workers engaged in the industry and ultimately on the people of the country. These reform policies are mainly the reduced role of the Government, cut in subsidy in the social sector, increase in administered prices, liberalization of trade by increasing tariff rates providing incentives for foreign investment, privatization of the public sector, equating foreign companies with Indian companies, de-regulating the labour market etc. This is aimed at the withdrawal of the state initiative from the social and welfare sectors like health, education, public distribution etc.

In this article I shall try to show how the workers of the drug industry and the people of our country are affected by the impact of globalization.

Drug industry situation prior to the Indian Patent Act, 1970

At the time of independence, the total drug production in our country was around Rs. 10 crores. At that time the MNCs taking the help of the colonial Patent and Designs Act, 1911 exploited the drug market of our country. They were engaged mainly in the import

- 29 -

of drugs from their country of origin. Between 1947-57, 99% of the 1704 drugs and pharmaceutical patents in India were held by foreign MNCs. During that time the MNCs who were controlling 80% of the market did not come forward with financial investment and technological help to establish drug production centers in India. Drug prices in India were amongst the highest in the world. In 1954, the first public sector drug company Hindustan Antibiotic Ltd. (HAL) was established with the help of WHO and UNICEF. The Indian Drugs and Pharmaceutical Limited (IDPL) was established in 1961 with help from the Soviet Union. The establishment of these two public sector units and the coming into force of the Drug Policy of 1978 had been mainly responsible for the availability of drugs and medicines at relatively lower prices in India. The country became almost self-sufficient in the production of drugs.

Indian Patent Act 1970

The Patent Bill was first introduced in Parliament in 1967, but the Patent Act, 1970 came into force only in 1972. The Indian Patent Act 1970 which is in operation in our country does not allow product patents on medicines, agricultural products and atomic energy. This is the most suitable patent act for the developing world. Here, process patents are allowed for 5-7 years. Mainly with the help of the Indian Patent Act 1970 India is today self-sufficient in the production of basic drugs covering various groups of drugs. Indian scientists developed new processes for 107 drugs. Indian companies are now among the world leaders in the production of bulk drugs from basic stages. At present, the prices of drugs in India are comparatively cheaper than many other countries. As per UNIDO, India is identified to produce its own drug needs with its own technology and manpower indigenously. After 1970, many new drug firms were established by Indian businessmen. At present, around 23 thousand small, big, and medium factories are producing drugs in India.

Attempts to change the Indian Patent Act 1970 are a part of this globalization programme. The imposition of an unequal trade treaty like the World Trade Organization (WTO) is a step towards globalization in favour of the MNCs of rich nations. With its help, the market of the developing nations is forced open for the developed countries. Most of the developing countries were forced to sign the WTO agreement without realizing its implication: as a result, the developed countries are the gainers. Already, at the dictates of the IMF, World Bank and WTO, the Government of India is slackening all checks and controls to invite the MNCs in all industries including the pharmaceutical industry. FERA and MRTP Acts have been amended. Customs duties and corporate taxes have been lowered. Relief, concessions and facilities have been extended to the MNCs as to Indian companies. All these, already, had an adverse impact on the indigenous drug industry. As per the requirement of WTO guidelines for the product patent regime, the availability of new drugs in our country may be delayed depending on the desire of the patent holders. As per the guidelines, a product patent is granted for 20 years and a process patent for another 20 years. At present, newer drugs are made available in our country within a 4-6 years period. Prices of drugs will go up by 5 to 10 times as it is evident from the prices of drugs in India and other countries like Pakistan, U.K. and U.S.A. where product patents are in force. Ranitidine is sold by Glaxo in India at Rs.

- 30 -

7.20. The same product is sold by the same company in Pakistan at Rs. 65 and in the U.S.A. at Rs. 545. Similarly, the anti-viral drug Aciclovir costs Rs. 33.75 in India while the same drug is sold in Pakistan at Rs. 363. There are many such examples. The drug prices in the U.S.A., U.K. and other developed countries have gone up so high that the health care expenditure in those countries is predominantly funded by insurance companies at a very high premium. In those countries people cannot think of treatment without insurance coverage. Product patent regime will definitely hamper India's drugs exports as countries will be forced to purchase from patent holders only.

Dilution of Drug Policy and Drug Price Increase

Unlike consumer goods, drugs are not purchased by the preference of a person, but on a doctors' prescription. Consumers have no choice of their own on this matter.

Prices of drugs are increasing by leaps and bounds along with the prices of other commodities in recent times. The drug manufacturers are flouting the Drug Price Control Order (DPCO). The DPCO was first introduced in 1970. In 1970 most of the drugs were under price control. In 1987 this was diluted and the number of drugs which were restricted declined to 347, in 1987 it was brought down to 163 drugs and in 1994 only 73 drugs were under DPCO. Even then industry is not happy; they want the control to be abolished totally. They have already demanded decontrol of 17 bulk drugs and further recommended full decontrol within 3 years time (Economic Times, 28th September, 1998). Many developed countries of Europe control drug prices directly. In the U.K., the government determines the profit level of drugs supplied by individual companies. A company has to reimburse excess profits to the Department of Health.

A recent study shows that the prices of many life-saving bulk drugs have gone up steeply. Drugs policies in our country are decided not by the need of our people, the pattern of diseases or by the purchasing capacity of the people, but by the profit motive of the industry and the Central Government are playing the role of a silent onlooker.

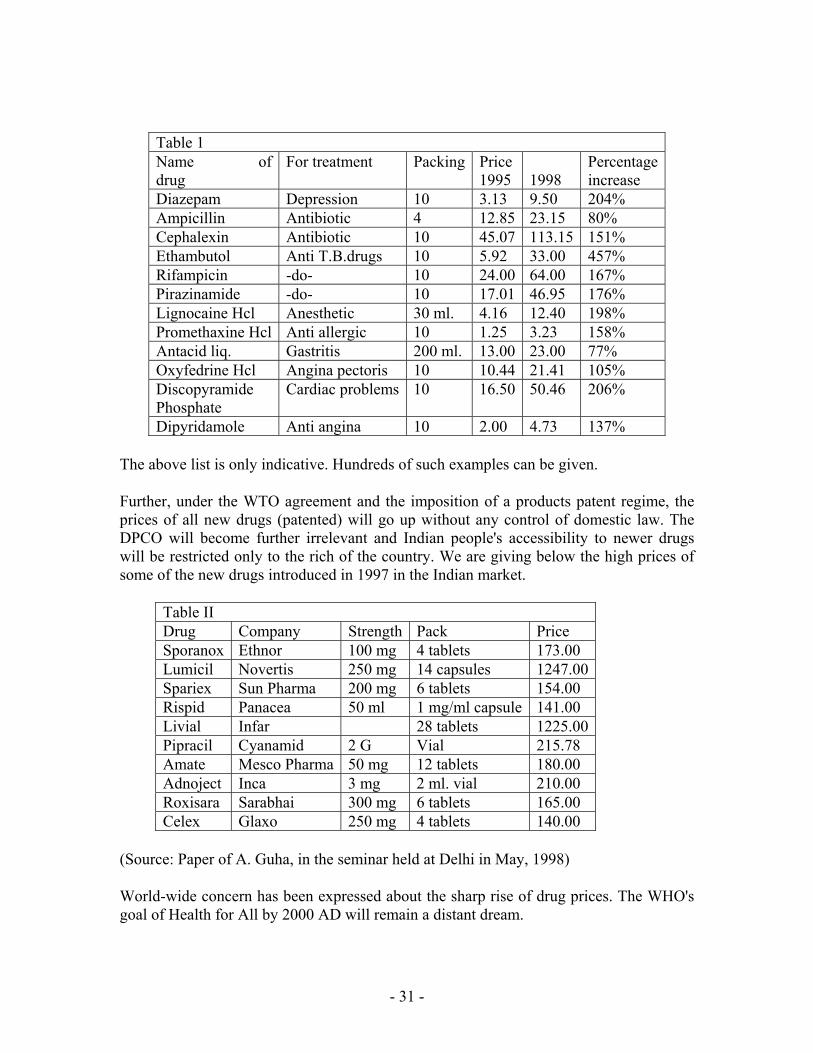

We are giving below the prices of twelve essential drugs before the liberal decontrol of DPCO in 1995 and today.

- 31 -

Table 1 Name of drug

For treatment Packing Price1995

1998

Percentageincrease

Diazepam Depression 10 3.13 9.50 204% Ampicillin Antibiotic 4 12.85 23.15 80% Cephalexin Antibiotic 10 45.07 113.15 151% Ethambutol Anti T.B.drugs 10 5.92 33.00 457% Rifampicin -do- 10 24.00 64.00 167% Pirazinamide -do- 10 17.01 46.95 176% Lignocaine Hcl Anesthetic 30 ml. 4.16 12.40 198% Promethaxine Hcl Anti allergic 10 1.25 3.23 158% Antacid liq. Gastritis 200 ml. 13.00 23.00 77% Oxyfedrine Hcl Angina pectoris 10 10.44 21.41 105% Discopyramide Phosphate

Cardiac problems 10 16.50 50.46 206%

Dipyridamole Anti angina 10 2.00 4.73 137%

The above list is only indicative. Hundreds of such examples can be given.

Further, under the WTO agreement and the imposition of a products patent regime, the prices of all new drugs (patented) will go up without any control of domestic law. The DPCO will become further irrelevant and Indian people's accessibility to newer drugs will be restricted only to the rich of the country. We are giving below the high prices of some of the new drugs introduced in 1997 in the Indian market.

Table II Drug Company Strength Pack Price Sporanox Ethnor 100 mg 4 tablets 173.00 Lumicil Novertis 250 mg 14 capsules 1247.00 Spariex Sun Pharma 200 mg 6 tablets 154.00 Rispid Panacea 50 ml 1 mg/ml capsule 141.00 Livial Infar 28 tablets 1225.00 Pipracil Cyanamid 2 G Vial 215.78 Amate Mesco Pharma 50 mg 12 tablets 180.00 Adnoject Inca 3 mg 2 ml. vial 210.00 Roxisara Sarabhai 300 mg 6 tablets 165.00 Celex Glaxo 250 mg 4 tablets 140.00

(Source: Paper of A. Guha, in the seminar held at Delhi in May, 1998)

World-wide concern has been expressed about the sharp rise of drug prices. The WHO's goal of Health for All by 2000 AD will remain a distant dream.

- 32 -

Moreover, with the rapid development in technology, a greater number of new drugs are being introduced. Experts say that very few of them are having therapeutic advantages over the existing drugs. 'Out of 348 new drugs introduced by 25 big US companies during 1981 to 1988 only 3 per cent made important potential contribution while 84 percent made little or no potential contribution' said the US federal authority. Hence the introduction of new costly drugs should be properly monitored by the central government.

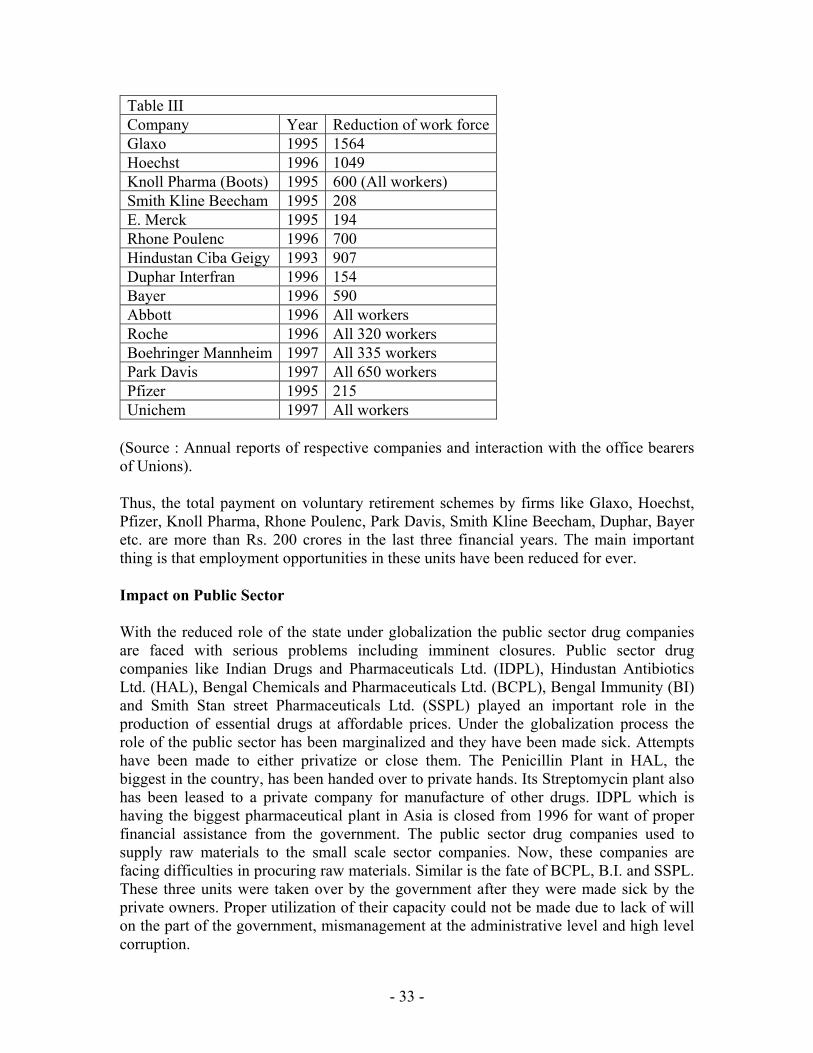

Mass Ending of Jobs

With the reduction of the customs duties on foreign imports many drugs manufactured in India have become unviable compared to the foreign goods in the Indian market. As a result, the owner of these factories are closing down their units and throwing the workers out of employment. Messrs. Boehringer Mannheim, and Parks Davis who were the lone producers of Chloramphenicol in India stopped their production as its prices in the international market were cheaper than the cost of production in India. M/s. Sarabhai Chemicals closed their Vitamin 'C' plant for a similar reason. Like Chloramphenicol and vitamin 'C' many other drugs like Paracetamol, Metronidazole, Ampicillin, Amoxycillin etc. are available at a cheaper price in our country from abroad because of the lowering of the customs duties so that Indian factories have closed and workers are on the streets. For the above drugs our country has became dependent on foreign supply.

In their attempt to shift the production to the third party manufacturing already, Hindustan Ciba Geigy, Roche, Abbot, Boehringer Mannheim, Boots, Park Davis, Unichem etc. have closed their factories and offered a voluntary retiring scheme to workers and they have sold the land of their factory premises at a premium price. Apart from these closures, Pfizer, Rhone Poulenc, Hoechst, Glaxo etc. have reduced their work force. Crores of rupees have been spent to give VRS. These companies are manufacturing their products with the help of loan licensees. Some of the companies have opened new smaller factories in new places and appointed workers with lower wages and more workload. More casual workers are being appointed. In the last two years in the Mumbai Thane region of Maharashtra around 30,000 workers have lost their jobs in the pharmaceutical industry.

Apart from the factory workers the distribution workers are gradually being replaced by Cost & Freight agency system. In this system, the original company does not have any responsibility for the workers. They are employed by agents with more workload and lower wages. In the last decade around 15 thousand distribution workers have lost their jobs in the pharmaceutical industry. Moreover, through the agency system the Government is deprived of sales tax.

In marketing also the field workers or the sales promotion employees are facing tremendous attacks in the name of franchise, co-marketing, appointment of communicators etc. many permanent sales promotion employees are losing their jobs. Many others are appointed in the name of so-called executives to remove them from the fold of the union. More casual and contractual workers are being recruited.

- 33 -

Table III Company Year Reduction of work forceGlaxo 1995 1564 Hoechst 1996 1049 Knoll Pharma (Boots) 1995 600 (All workers) Smith Kline Beecham 1995 208 E. Merck 1995 194 Rhone Poulenc 1996 700 Hindustan Ciba Geigy 1993 907 Duphar Interfran 1996 154 Bayer 1996 590 Abbott 1996 All workers Roche 1996 All 320 workers Boehringer Mannheim 1997 All 335 workers Park Davis 1997 All 650 workers Pfizer 1995 215 Unichem 1997 All workers

(Source : Annual reports of respective companies and interaction with the office bearers of Unions).

Thus, the total payment on voluntary retirement schemes by firms like Glaxo, Hoechst, Pfizer, Knoll Pharma, Rhone Poulenc, Park Davis, Smith Kline Beecham, Duphar, Bayer etc. are more than Rs. 200 crores in the last three financial years. The main important thing is that employment opportunities in these units have been reduced for ever.

Impact on Public Sector

With the reduced role of the state under globalization the public sector drug companies are faced with serious problems including imminent closures. Public sector drug companies like Indian Drugs and Pharmaceuticals Ltd. (IDPL), Hindustan Antibiotics Ltd. (HAL), Bengal Chemicals and Pharmaceuticals Ltd. (BCPL), Bengal Immunity (BI) and Smith Stan street Pharmaceuticals Ltd. (SSPL) played an important role in the production of essential drugs at affordable prices. Under the globalization process the role of the public sector has been marginalized and they have been made sick. Attempts have been made to either privatize or close them. The Penicillin Plant in HAL, the biggest in the country, has been handed over to private hands. Its Streptomycin plant also has been leased to a private company for manufacture of other drugs. IDPL which is having the biggest pharmaceutical plant in Asia is closed from 1996 for want of proper financial assistance from the government. The public sector drug companies used to supply raw materials to the small scale sector companies. Now, these companies are facing difficulties in procuring raw materials. Similar is the fate of BCPL, B.I. and SSPL. These three units were taken over by the government after they were made sick by the private owners. Proper utilization of their capacity could not be made due to lack of will on the part of the government, mismanagement at the administrative level and high level corruption.

- 34 -

It is not because of any inherent weakness but due to the lack of political will, deliberate efforts to destroy them, corruption and mismanagement that these public sector units have been rendered commercially unviable.

Moreover, the number of workers engaged in these units have been reduced drastically. When IDPL was established it had a strength of more than 15,000 workers. Today, it has been reduced to less than 7,000.

With the pharmaceutical industry taking a leap towards biotechnology development world-wide, only the public sector drug companies, with the backing of the Central Government, could have faced the challenge effectively from the MNCs in the new situation.

- 35 -

Mergers and Acquisitions

International and national level mergers, acquisitions and takeovers have now become a common phenomenon in the pharmaceutical industry. Internationally American Home Product merged with Cyanamid, SKB with Sterling, Rhone Poulenc took over Fashions, BSF with Boots, Glaxo with Burroughs Welcome, Ciba Geigy with Sandoz, Warner Hindustan with Parke Davis, Hoechst with Rhone Poulenc etc. are some of the examples of big take over. By mergers and acquisitions these companies became even larger with more financial power at their disposal over their competitors. (See Table IV for the top pharmaceuticals of the world).

In coming days, with the help of international financial companies the MNCs will capture and take control of Indian companies to control the Indian market.

To match the situation created by international mergers and takeovers, Indian companies are adopting the same path. For example Wockhardt took over Merind and Tata Pharma, Ranbaxy took over Croslands, Nicholas Piramal took over Roche, Boehringer, Sumitra Pharma. The inevitable results are job loss of workers. Because of overlapping of jobs large numbers of workers are declared surplus. After merger Glaxo-Welcome and Ciba-Sandoz announced a reduction of 15 thousand and 10 thousand of their work force respectively world-wide. Upjohn and Pharmacia decided to close 24 of their 57 plants in different countries after their merger.

Some countries are adopting the 'buy and grow' method. They are taking over some popular brands and increasing their business. SKB took over Crocin from Duphar, Ranbaxy took over 7 leading brands from Gufic, Dr. Reddy's Lab purchased 6 products of Dolphin and two each from Pfimex and SOL Pharma. Sun pharma purchased all leading brands of NATCO, after selling the popular brands the companies are becoming sick and closing their shutters throwing the workers on the street.

The governments permission to the MNCs to come to India with 100% equity have threatened the existing companies with the same origin and their workers.

Through the process of mergers, acquisitions and takeovers MNCs will gradually perpetuate their grip on the Indian industry by the creation of a limited number of mega companies having monopoly control and domination world wide. In the absence of competition people will have to pay any price as it happens in the sellers market.

- 36 -

CONCLUSION

The present government at the centre is bringing a bill in the winter session of Parliament to change the Indian Patent Act 1970. The change in the Act is not in the interest of the people of the country. Now patents have become an object of business instead of development. Considering the wide gap of industrial and technological development between developed and developing countries monopoly rights through the patent system should not be allowed to the rich nations. Today 85% of the patents are being controlled by the TNCs of the rich nations. 'Globalization is hurting poor people, not just the poor countries. In this process poor countries and poor people will become increasingly marginalized', says the 1997 world development report of UNDP.

The question is why this pressure and hurry? The main aim is to impose the conditionalities of WTO and to change the Indian Patent Act as MNCs need more markets and are eyeing Asia which is the largest continent of the world where 60% of the world population lives but contributes only 20% of the world pharmaceuticals business. With a high rate of population growth it is expected that the need of drugs will tremendously increase in the third world countries including India in the next millennium. India contributes 16.1% of the world population, but it produces only 1.2% of world drug production (See Table V). Hence the MNCs are trying to have more control over the pharmaceutical markets of the developing nations.

Developed countries are backing their own big companies to capture markets in other countries even at the cost of the interest of the people there. The United States has successfully battled for the inclusion of strict intellectual property rules in international trade agreements such as NAFTA and GATT. Often the U.S. position has literally been drafted by PhRMA. These trade agreements disregard public health considerations and have forced dramatic changes in the intellectual property rules the world over. Still PhRMA is not satisfied. And when PhRMA is not happy the office of U.S. Trade Representative (USTR) is not happy, says the editorial comment of Multinational Monitor.

The above comments clearly indicate the intention of the USA and other rich nations. Unfortunately, the Government of India is dancing to their tune. Against this, it is necessary to develop and launch broad-based movements everywhere with the active support of people hailing from all walks of life to force the government to change their stand.

- 37 -

TableIV Some top pharma company mergers in the world Company Merger Year of

merger Value of merged company

Dow Chemicals Marion Labs 1986 $ 6.21 bn. Bristol Myers Squibb Corp 1989 12.09 bn. Beecham group SmithKline & French 1989 7.9 bn. American Home Products American Cynamide 1994 9.7 bn. Hoffman La Roche Syntex Lab. 1994 5.3 bn. Eli Lyly PCS Health System 1994 4 bn. Sandoz Gerber 1994 3.7 bn. Smith Kline Beecham Sterling 1994 2.9 bn. Glaxo Burroughs Wellcome 1995 14.2 bn. Hoechst MMD Roussel 1995 7.2 bn. Pharmacia Upjohn 1995 7 bn. Rhone-Poulenc Rorers Fison 1995 2.7 bn. BASF Boots 1995 1.3 bn. Ciba Geigy Sandoz 1996 30.1 bn. Hoffman la Roche Comage Ltd. 1997 11 bn. Hoechst A.G. Rhone Poulenc 1998 Astra Zeneca 1998 67 bn.

(Source: Compilation from reports published in various news papers at different times)

Table:5 Percentage of drug production and world population in some countries Country % of world

drug production % of world population

USA 28.2% 4.7% Germany 7.7% 1.5% France 7.1% 1.1% U.K. 3.4% 1.1% Brazil 1.7% 2.8% India 1.2% 16.1%

(Source : Business Standard, February 19, 1997)

- 38 -

WTO AND INDIAN PHARMACEUTICAL INDUSTRY

Introduction Prior to 1970, Indian Pharmaceutical Industry was clearly dominated by foreign companies. This made the country exceedingly dependent on imports for bulk drugs and formulations. As a result drug prices were amongst the highest in the world. The burden to the society on account of exorbitant prices for medication was explicit. To bring down the burgeoning prices and to break the MNC domination, the government of the day introduced India Patents Act, 1970. Indian Patent Act, 1970 allowed for process patenting, which has fostered a self-reliant indigenous industry. Process patenting made new drugs available substantially cheaply and promoted import substitution by encouraging local companies to make copies of drugs, by developing their own processes, followed by bulk drug production. In a way, pharmaceutical industry in India was provided the protection much needed by it. WTO AND ITS RUB-OFF The world has awakened to a new global order. Though many efforts were made in the post-depression era to agglomerate world business through an inter-governmental treaty like GATT, it was not until the Uruguay Round resolution of the partner countries of GATT in end-1944 to establish a new trade order through the ensconcement of an international organization named World Trade Organization, did anything worthwhile materialize. The WTO, an organization of multilateral trading system has in fact become the main vehicle of a few industrialized, developed countries for organizing and enforcing global economic governance. It is serving the purpose of the big countries, which use it as a weapon to arm twist their way into the markets of developing countries. India has been amongst the first signatories to the WTO charter. An arrangement with WTO facilitates recourse to cross-retaliation for non-fulfillment of specific obligations. India which till today is minting money through export of drugs, courtesy its process patenting law would suffer a severe setback once it has to comply with the rules and provisions made in the TRIPs. According to the WTO Agreement, India has been given time up to year 2005 to amend its IPA to allow product patent instead of process patent. So new chemical entities introduced into India after this period have to be accorded. Some provisions of TRIPs with regards to pharmaceutical products that are of relevance to India are:

• The minimum patent term will be twenty years from filing. • Patent production is to be extended to pharmaceutical products. • Importation must be accepted as a working patent. • Compulsory licensing is relegated to special circumstances.

- 39 -

• In infringement suits over process patents, the ‘burden of proof’ is reversed. • Provide transitional arrangements – deferment of the acceptance of

pharmaceutical product patents by developing countries for ten years. • Limited exclusively is granted to developing countries for pharmaceutical

products whose patent applications are filed after the enforcement of the TRIPs agreement.

EMR ROUTE The EMR route is a backdoor method of granting monopoly rights. To ensure a smooth transition from process patent regime to a product patent one, WTO has granted India a grace period of ten years. During this period, all patent applications received by her would be put in a ‘black box’ for further future consideration. However, in the interim, pharmaceutical companies can apply for exclusive marketing rights (EMRs) for their products for a period of five years, even before India’s transition is fully phased. Any company that has been registered for a patent and has received marketing rights in any of the WTO member countries can avail the EMR route in India. EMR’S IMPLICATION A mere grant of a patent and exclusive marketing rights by any member country would automatically qualify a company to avail EMR in India for that product, for a minimum period of five years. This clause has a very serious implication. The company in question can happily experiment with the lives of poor Indians. If their experiment fails, the drug can be withdrawn and in the process endangering the lives of millions of Indians. However, if the drug proves successful, given the provision of the validity of a patent for twenty years, the company can take in enormous monopoly profits. THE CURRENT SCENARIO There are as many as 23,000 pharmaceutical firms in India, engaged in the production of 16,000 formulation and 700 bulk drugs. With over 28.60 lakhs of manpower employed in the sector, it is growing drastically. The year India became a member signatory of WTO, in 1995 its investment in pharmaceutical industry was Rs. 1380 crores in 1999-2000. These two indicators are proof enough to exhibit the panic in the industry. The industry is growing by leaps and bounds to ensure that post 2005 it takes on its TNC competitors head on. Individual companies like Ranbaxy, Dr. Reddy’s Laboratories, Cipla, Dabur, Aurobindo Pharma, Orchid Chemicals and others are setting the pace and defining industry standard. Ranbaxy with its presence in 40 countries, with operations in 24 and manufacturing facilities in 6 countries, with 7000 people across the globe is the harbinger of the coming of the age of the Indian industry. Incidentally it spends double the industry standards on its R & D efforts.

- 40 -

Capital expenditure of the tune of millions is being incurred by the industry to modernize plants and machinery. Global marketing alliance, mergers and acquisitions have taken the industry by storm. Some companies like Cipla are examining their future role in path-breaking areas of research such as genetics, hoping to open up unexplored venues of global alliance for the introduction of new therapeutic agents. DRL and Ranbaxy are doing collaborative work with companies such as Novo-Novordis and Bayer. Path-breaking work on agronomy and scientific development of traditional medicines is on. Companies are focusing on securing international patents for new processes, for novel drug delivery systems and innovative drug formulations. Indian pharmaceutical industry is growing at the rate of 12-15% per year as against the global industry growth rate of 8%. This can be attributed to healthcare cost-containment pressures, keeping pharmaceutical prices low, while export opportunities and low domestic per capita consumption have provided higher growth potential. Exports were 192% higher than imports in the year 1999-2000. annual drug per capita expenditure is only $3 as compared to Japan’s $412, Germany’s $222, United States’ 191, Canada’s $124 and United Kingdom’s $97. The pharmaceutical sector has undergone several policy changes in the past two years. It has largely benefited from the budget proposals made by the government. Some of the positive steps taken by the government apropos of, the industry are :

• Pharmaceutical industry has been recognized as a knowledge-based industry. • The government has plans to step up the R&D expenditure. Ironically, only 4.3%

of the projected Rs 1400 crores proposed investment in R&D as in the ninth five year plan has been made. Given a year’s time from now for the 5 year plan to give way to the tenth five year plan, this plan seems quite overdue.

• Rationalization of excise duty and reduction in interest rates in export financing. • Additional deductions under income tax laws for R&D expense. • Foreign direct investment permit up to 74% through automatic rout under powers

delegated to the RBI of by the government as the case may be. Automatic route for FDI and /of for technology collaboration would not be available to those who have had any previous joint venture of technology transfer / trademark agreement in the same of allied field in India.

PRE 2005 The phase of transition has taken over. Established national pharmaceutical majors are gobbling up smaller companies through consolidations, acquisitions and mergers. The very notion of the entry of TNCs into India post WTO has propped up Indian firms to follow the dictum: United we stand, Divided we fall. Consolidations have become a buzzword in the industry. Smaller players unable to bear the brunt of heavy competition are giving up to larger ones. With only three odd years in hand, Indian pharmaceutical firms are losing no time in extensive copying to reap full advantage of the laxity in the current policy, copying

- 41 -

though a cheap practice, yet given the policy of price control, Pharma firms are left with no option to invest in research and development . Price control is a non incentive for innovation. Lower drug prices might also imply increasing healthcare expenditure. On the one hand where global giants like Novartis and Hoechst have already set up 100% Indian subsidiaries, some are increasing their stakes in existing ventures and some restructuring their operations. Quite contrary to these optimists are some pessimists who still linger with the rear that their top of the line products would find no ready market in India given the amount of piracy and low product prices. Companies are increasingly investing in riskier, cutting edge technologies. SmithKline Beecham is one of the first such companies to leap into new technologies. Glaxo is also contemplating to develop broader portfolio of drugs. Indian pharmaceutical companies are in the process of building a strong distribution network and manufacturing facilities so that they can be in a better position to attract foreign partners post WTO. Also the would leverage their bargaining power. POST 2005 Indian pharmaceutical industry would be have to confront the reality of the implementations of TRIPs Agreement from the year 2005. The year would be a turning point, a defining one in India’s pharmaceutical trade. Post-2005 period would be characterized by many hectic business changes. Most transnational companies are likely to introduce there new-patented drug once the product patent becomes fully operational. Indian pharmaceutical would try to haggle with them and government might introduce compulsory licensing. This would lead to an increase in the bargaining power of the patent holder. Also it is likely that TNCs might not set up base in India but consider it as an assembly point of some drugs manufactured by them. However, new launches in the post –WTO period is a guaranteed fact. These new launches would primarily be high margin, low volume products. Competition is likely to increase in the domestic market due to due to the entry of transnational companies. This would whittle down many manufacturers and small and medium enterprises would slowly decimate. They would lose the benefits enjoyed so far and forced to compete with the foreign firms. Not only would they lose their significance, and their existence would be jeopardized with the implementation of the TRIPs agreement. The product sales of foreign transnational companies would increase at the expense of the local layers. Local players would increase their research and development expenditures and try to expand their business overseas to enter the generic market due to their cost efficiency. Imitation is cheaper then innovation. Post-2005, drug discovery would be a costlier affair that Indian pharma companies cannot afford. Joint ventures would become the order of the day. Prizes of drugs would shoot high. IPR rules would enable TCNs to jack up prizes of their products far beyond cost and earn monopoly rents and profits. Higher prices would mean higher cost on medicament. This would lead to

- 42 -