Petrobras Investments Webcast Pn 2010 2014

38

1 STRATEGIC PLAN PETROBRAS 2020 BUSINESS PLAN 2010 BUSINESS PLAN 2010 - - 2014 2014 Webcast Webcast Jos Jos é é Sergio Sergio Gabrielli Gabrielli – – CEO CEO Almir Almir Barbassa Barbassa – – CFO CFO

-

Upload

joaquim-leao -

Category

Business

-

view

3.602 -

download

2

Transcript of Petrobras Investments Webcast Pn 2010 2014

1

STRATEGIC PLAN PETROBRAS 2020

BUSINESS PLAN 2010 BUSINESS PLAN 2010 -- 20142014WebcastWebcast

JosJoséé Sergio Sergio GabrielliGabrielli –– CEOCEOAlmir Almir BarbassaBarbassa –– CFOCFO

2

STRATEGIC PLAN PETROBRAS 2020

DISCLAIMERDISCLAIMER

FORWARD-LOOKING STATEMENTS:

DISCLAIMER

The presentation may contain forward-looking statements about future events within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, that are not based on historical facts and are not assurances of future results. Such forward-looking statements merely reflect the Company’s current views and estimates of future economic circumstances, industry conditions, company performance and financial results. Such terms as "anticipate", "believe", "expect", "forecast", "intend", "plan", "project", "seek", "should", along with similar or analogous expressions, are used to identify such forward-looking statements. Readers are cautioned that these statements are only projections and may differ materially from actual future results or events. Readers are referred to the documents filed by the Company with the SEC, specifically the Company’s most recent Annual Report on Form 20-F, which identify important risk factors that could cause actual results to differ from those contained in the forward-looking statements, including, among other things, risks relating to general economic and business conditions, including crude oil and other commodity prices, refining margins and prevailing exchange rates, uncertainties inherent in making estimates of our oil and gas reserves including recently discovered oil and gas reserves, international and Brazilian political, economic and social developments, receipt of governmental approvals and licenses and our ability to obtain financing.

We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information or future events or for any other reason. Figures for 2010 on are estimates or targets.

All forward-looking statements are expressly qualified in their entirety by this cautionary statement, and you should not place reliance on any forward-looking statement contained in this presentation.

NON-SEC COMPLIANT OIL AND GAS RESERVES:

CAUTIONARY STATEMENT FOR US INVESTORS

We present certain data in this presentation, such as oil and gas resources, that we are not permitted to present in documents filed with the United States Securities and Exchange Commission (SEC) under new Subpart 1200 to Regulation S-K because such terms do not qualify as proved, probable or possible reserves under Rule 4-10(a) of Regulation S-X.

3

STRATEGIC PLAN PETROBRAS 2020

CHALLENGES TO WORLD OIL SUPPLYCHALLENGES TO WORLD OIL SUPPLYNatural decline requires finding new reserves to meet world demaNatural decline requires finding new reserves to meet world demandnd

20

30

40

50

60

70

80

90

100

110

120

2000 2005 2010 2015 2020 2025 2030

2020: 43 – 48 MM bpd

2030: 65 – 78 MM bpdProjected Decline

Required Addition to CapacityScenario: Sustainable Development

Scenario: Business as Usual

28%

59%

13%

Source: Estimates using WoodMackenzies’ data

Production from revaluation of existing reserves (increases to Oil in Place or the recovery factor )

Production from reserves not yet discovered or without a development plan

Production currently developed with operations in short and medium term

87% of needed supply must come from re-valuing existing reserves, or from reserves not yet discovered or declared commercial

4

STRATEGIC PLAN PETROBRAS 2020

PRIMARY DEMAND FOR ENERGYPRIMARY DEMAND FOR ENERGYDespite growth of alternatives, oil will maintain its importanceDespite growth of alternatives, oil will maintain its importance

2008 20302008 2030

28%

22%

28%

6%7%2%7%

1%

2008 2030

0.4%0.5%

33%

22%

26%

6%6%7%

29%

22%

29%

6%

7%1%

6%1%

Average Annual Change

+5.2% p.y.

+4.2% p.y.

Traditional Biomass

Other Renewable sourcesBiofuels

Hydro

Nuclear

Coal

Gas

Oil

MM

TOE

* Aeolian, Solar and Geothermal

1.32%1.30%

17,32417,236

12,974

Sustainable Development

Business as Usual

+6.1% p.y.

+7.8% p.y.

Sustainable Development

Business as Usual

Aggressive growth in biofuels will only slow the rate of growth in the consumption of Petroleum products

5

STRATEGIC PLAN PETROBRAS 2020

Per capita petroleum consumption

DEMAND FOR PETROLEUMDEMAND FOR PETROLEUMDeveloping country demand should exceed reduced OECD demandDeveloping country demand should exceed reduced OECD demand

-2 0 2 4 6 8

Transport Eletrical Generation Others

Petroleum demand – 2009-2030 (variation million bpd)

USA

China

India

Middle East

OECD Europe

Brazil

•Considering France, Germany, Italy and UK

0

5

10

15

20

25

30

per c

apita

- ba

rrel

s pe

r yea

r

US Japan OECD* Brazil China India

1980 2000 2009

Source: BP

6

STRATEGIC PLAN PETROBRAS 2020

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

6000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Source: PFC Energy and Company reports

OIL AND GAS PRODUCTION TARGETS: SUPERMAJORS AND PETROBRASOIL AND GAS PRODUCTION TARGETS: SUPERMAJORS AND PETROBRASPetrobras has the highest growth rate target of the industryPetrobras has the highest growth rate target of the industry

ExxonMobil: Productiongrowth rate ~3-4% in 2010; ~2-3% p.y. up to 2013

BP: Production growth rate ~1-2% p.y. up to 2015

Shell: ~3.5 MM boe/d in 2012 and ~3.7 MM boe/d in 2014

Petrobras: 3.9 MM boe/d in 2014 and 5.4 MM boe/d in 2020

thou

sand

boe

/d

Chevron: production growthrate ~1% p.y. between 2010-2014 and 4.5% p.y. between 2014-2017

7

STRATEGIC PLAN PETROBRAS 2020

PETROBRAS CORPORATE STRATEGY to 2020PETROBRAS CORPORATE STRATEGY to 2020Integrated, profitable growth, on a sustainable basisIntegrated, profitable growth, on a sustainable basis

Commitment to Sustainable Development

Integrated Growth

Expand operations in target markets for oil, oil products, petrochemicals, gas and energy, biofuels and distribution and to be recognized as a benchmark among integrated energy companies

Cor

pora

te S

trat

egy

Bus

ines

s Se

gmen

ts

Grow oil and gas production in a sustainable manner, becoming one of the five largest oil producers in the world

Expand refining in Brazil, ensuring sufficiency in domestic supply and leadership in distribution, while developing export markets for products, with emphasis in the Atlantic basin

Consolidate leadership in the Brazilian natural gas market, and establishing an international presence and increasing the domestic electricity generation business and gas chemical, emphasizing fertilizers

Operate in the petrochemical sector in activities that are integrated manner with the other businesses of the Petrobras system

Operate in Brazil and abroad in the biofuels sector in activities that are integrated with the Petrobras system, and to do so on a sustainable basisl

Operational excellence, in management, in energy efficiency, in human resources and in technology

E&P Downstream

(RTC)

Gas and Energy Petrochemicals BiofuelsDistribution

Social and Environmental ResponsibilityProfitability

8

STRATEGIC PLAN PETROBRAS 2020

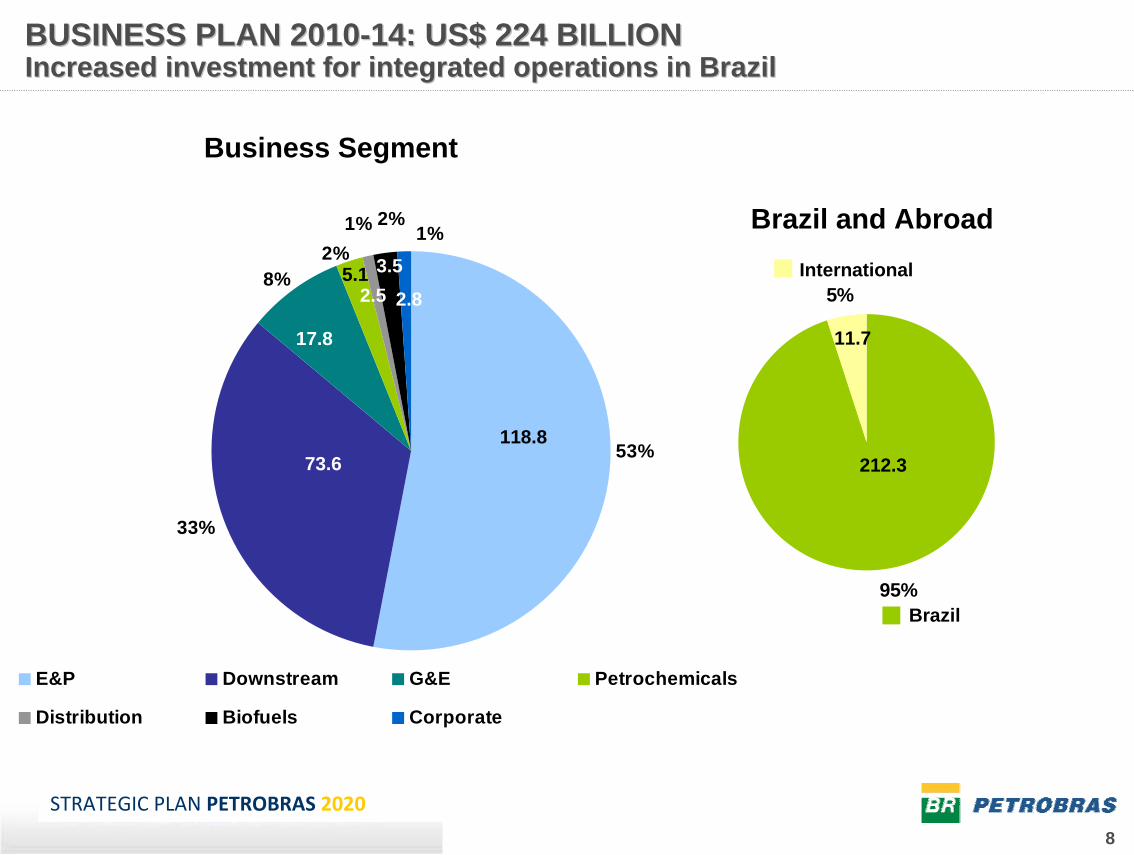

BUSINESS PLAN 2010BUSINESS PLAN 2010--14: US$ 224 BILLION14: US$ 224 BILLIONIncreased investment for integrated operations in BrazilIncreased investment for integrated operations in Brazil

95%

5%International

Brazil

212.3

Brazil and Abroad

11.7

Business Segment

33%

53%

1%2%

8%

2%1%

E&P Downstream G&E Petrochemicals

Distribution Biofuels Corporate

118.873.6

5.13.5

2.8

17.8

3.52.5

9

STRATEGIC PLAN PETROBRAS 2020

ADJUSTMENTS TO THE 2010ADJUSTMENTS TO THE 2010--2014 PORTFOLIO2014 PORTFOLIOIncreased spending on infrastructure, logistics, value chain in Increased spending on infrastructure, logistics, value chain in BrazilBrazil

• New projects for pre-salt, logistics, increased utilization of domestic oil, and monetization of natural gas.

• Change in partnership participation reflecting uncertainty about participation of partners in downstream projects

E&P

Downstream

Gas & Energy

Corporate

0.3

6.5

5.1 19.7

62%16%

21%1%

5.1 19.7

6.50.3

CAPEX 2010-2014 in 2009-2013

Business Plan

2010-2014 Business Plan

New Projects

Projects Excluded

Change in project timeline

Change in project design and cost

Change in Stake

186.6

31.6 (17.0) (6.8) 19.210.3

224

10

STRATEGIC PLAN PETROBRAS 2020

APPROVAL STATUS OF 2010APPROVAL STATUS OF 2010--2014 PORTFOLIO2014 PORTFOLIOFlexibility to adjust Flexibility to adjust CapexCapex for projects in Phases I and IIfor projects in Phases I and II

Phase I – Identification of OpportunityPhase II – In Conceptual PhasePhase III – In Basic ProjectPhase IV+ ‐ Authorization for Execution/Implementation/Operations

0,9

US$ 224 Billion686 projects

23.6

17.5

0.9

122.6

10.5%

54.7%

0.4%

7.9%

26.5%Phase I

Phase II

Phase III

Phase IV +

Aquisitions23.6

17.5

59.4

0,9

122.6

11

STRATEGIC PLAN PETROBRAS 2020

LOCAL CONTENT PARTICIPATION 2010LOCAL CONTENT PARTICIPATION 2010--20142014Brazilian suppliers expected to provide nearly 70% of total needBrazilian suppliers expected to provide nearly 70% of total needss

• Petrobras purchases in Brazil of approximately $28 billion per year (versus $20 billion per year in prior plan)

Capex in Brazil (US$ billion)

Brazilian Content0 %

40 %

60 %

80 %

100 %

20 %

E&P(53%)

Gas & Energy (82%)

Distribution and Biofuels (100%)

Downstream and

Corporate (80%)

100%2.32.3Biofuels

82%14.417.6Gas & Energy

100%2.32.3Distribution

80%2.63.3Corporate

Total

RTM and Petrochem

E&P

Business unit

67%

80%

53%

Braziliancontent

(%)

142.2

62.8

57.8

Purchased inBrazilianMarket

Investmentsin Brazil

212.3

78.6

108.2

+US$ 46.4 billion from Partners

12

STRATEGIC PLAN PETROBRAS 2020

Goals and Principal ProjectsGoals and Principal Projects

STRATEGIC PLAN PETROBRAS 2020

13

STRATEGIC PLAN PETROBRAS 2020

OIL AND GAS PRODUCTION TARGETS 2010OIL AND GAS PRODUCTION TARGETS 2010--20202020Domestic targets unchanged, international targets reducedDomestic targets unchanged, international targets reduced

(Tho

us. b

oe/d

ay)

1,500 1,540 1,493 1,684 1,778 1,792 1,855 1,971 2,100

2,980

3,950252 251 265

274 277 273 321 316384

623

1109

35 161 168163 142 126 124 141

146

176

203

85 94 96 101 110 100 9793

128

120

22

2002 2003 2004 2005 2006 2007 2008 2009 2010 2014 2020

Oil Production - Brazil Gas Production - Brazil Oil Production - International Gas Production - International

2,4002,3012,2972,2172,0202,0371,810

2,525

4.9% p.y.

2,723

5,382

3,9077.1% p.y.

9.4% p.y.

1.183152

Pre-Salt241

1, 078

• Production curve for domestic oil gas production consistent with prior Business Plan

• Projected international production reduced as a result of decrease in investment

• Production curve does not currently assume any contribution from Transfer of Rights

14

STRATEGIC PLAN PETROBRAS 2020

2,980

2,100

1200

1600

2000

2400

2800

2010 2011 2012 2013 2014

Tupi NE EWT30.000 bpd

Tupi NE EWT30.000 bpdGuará EWT

Dynamic Producer30,000 bpd

Guará EWTDynamic Producer

30,000 bpd

Th. bpd

Tupi PilotCidade de Angra dos

Reis100,000 bpd

Tupi PilotCidade de Angra dos

Reis100,000 bpd

Cachalote eBaleia Franca

FPSO Capixaba100,000 bpd

Cachalote eBaleia Franca

FPSO Capixaba100,000 bpd

Marlim Sul

SS P-56Module 3

100,000 bpd

Marlim Sul

SS P-56Module 3

100,000 bpd

JubarteFPSO P-57180,000 bpd

JubarteFPSO P-57180,000 bpd

Antecipation of Baleia Azul

FPSO Espadarte100,000 bpd

Antecipation of Baleia Azul

FPSO Espadarte100,000 bpd

RoncadorFPSO P-62Module 4

180,000 bpd

RoncadorFPSO P-62Module 4

180,000 bpd

RoncadorSS P-55Module 3

180,000 bpd

RoncadorSS P-55Module 3

180,000 bpd

Papa-Terra TLWP P-61 &FPSO P-63150,000 bpd

Papa-Terra TLWP P-61 &FPSO P-63150,000 bpd

Guará Pilot FPSO120,000 bpd

Guará Pilot FPSO120,000 bpd

Pre‐salt

Whales ParkFPSO P-58180,000 bpd

Whales ParkFPSO P-58180,000 bpd

Tupi NE Pilot FPSO

120,000 bpd

Tupi NE Pilot FPSO

120,000 bpd

Tiro/SidonFPSO

100,000 bpd

Tiro/SidonFPSO

100,000 bpd

Aruanã EWTCidade Rio das Ostras

15,000 bpd

Aruanã EWTCidade Rio das Ostras

15,000 bpd

Tiro EWTSS-11

30,000 bpd

Tiro EWTSS-11

30,000 bpd

MexilhãoNG

MexilhãoNG

AruanãFPSO

100,000 bpd

AruanãFPSO

100,000 bpd

GuaiamáFPSO

100,000 bpd

GuaiamáFPSO

100,000 bpd

Uruguá/TambaúFPSO Cidade de Santos

NG/35,000bpd

Uruguá/TambaúFPSO Cidade de Santos

NG/35,000bpd

Natural Gas

PRINCIPAL PROJECTS SCHEDULED DURING 2010PRINCIPAL PROJECTS SCHEDULED DURING 2010--20142014Updated business plan added new projectsUpdated business plan added new projects

Oil

4 EWTPre-salt4 EWTPre-salt

4 EWTPre-salt4 EWTPre-salt

3 EWTPre-salt3 EWTPre-salt

2 EWTPre-salt2 EWTPre-salt

EWT = Extended Well Test

15

STRATEGIC PLAN PETROBRAS 2020

E&PE&P--BRAZIL INVESTMENTS 2010BRAZIL INVESTMENTS 2010--2014 2014 Continued emphasis on PostContinued emphasis on Post--Salt acreage, growing spending on PreSalt acreage, growing spending on Pre--SaltSalt

Exploration Development Infrastructure

• Annual expenditures for exploration of more than US$4 billion annually

• Development capex in Pre-salt approaching 50% of Post-salt spending

27.8

0.9

4.3

84%

3%13%

Pre-Salt

US$ 33.0 Billion

Post-Salt

US$ 75.2 Billion

50.1

11.413.7

15% 18%

67%

16

STRATEGIC PLAN PETROBRAS 2020

NEW VESSELS AND PURCHASE OF NEW EQUIPMENTSNEW VESSELS AND PURCHASE OF NEW EQUIPMENTSPetrobras critical resources demand will drive Brazilian and intPetrobras critical resources demand will drive Brazilian and international industryernational industry

26 RIGS CONTRACTED, 28 MORE TO BE BUILT BY 2020:26 RIGS CONTRACTED, 28 MORE TO BE BUILT BY 2020:o Until 2013: 13 rigs contracted before 2008 and 1 rig relocated from international operations*;

+12 new rigs contracted in 2008 , through international bidding;o 2013-2020: Bidding process in progress, to contract 28 rigs to be built in Brazil.

By 2013

79

41

254

5

Current Situation(Dec/09)

Others (Jacket and TLWP)

Production Platforms SS e FPSO

Supply and Special Vessel

Drilling Rigs Water Depth Above 2.000 m

Critical ResourcesDelivery Plan (to be contracted)

Accumulated Value

By 2015 By 2020

26 31 53*

465 491 504

53 63 84

81 83 85

Production

Platform (FPSO)Drilling RigsSupply Vessel

* The rig reallocated from international operations, expire in 2015, so it is not considered in the 2020 accumulated value

17

STRATEGIC PLAN PETROBRAS 202017

RTM

(Refining, Transportation and Marketing)

and PETROCHEMICALS

Market Demand, Goals and Principal ActivitiesMarket Demand, Goals and Principal Activities

BUSINESS PLAN PETROBRAS 2020STRATEGIC PLAN PETROBRAS 2020

18

STRATEGIC PLAN PETROBRAS 2020

2,7943,196

3,9502,356

2,260

2,980

1,9331,791

1,971

1,0361,393

181

2009 2014E 2020E

kbpd

110%

132%

• Oil Production and the Brazilian market demand currently exceed refining capacity

• By 2014, exports are projected to reach nearly 1 million bpd, even as refining capacity is expanded to process Brazilian production to meet demand

BRAZILIAN PRODUCTION, REFINING AND DEMANDBRAZILIAN PRODUCTION, REFINING AND DEMANDLong term plans to achieve greater balance and integrationLong term plans to achieve greater balance and integration

ThroughputProduction Oil Product Demand

124%

1980

13%

Production as a % of refining

19

STRATEGIC PLAN PETROBRAS 2020

BRAZILIAN DEMAND AND REFINING CAPACITYBRAZILIAN DEMAND AND REFINING CAPACITYStrong Brazilian GDP growth projected to increase demand 3.4% Strong Brazilian GDP growth projected to increase demand 3.4% p.yp.y..

• Domestic production will represent 91% of refinery throughput by 2020

• Comperj’s first phase is now a new refinery

403

769937

826

452338

1,187

1,155

1,016

0

1000

2000

3000

Thousand bpd

1,933

PREMIUM I(1ª phase)

300 thou. bpd(2014)

2,356

1,831

2,260REPLANRevamp

U200+PAM33 thous. bpd

(2010)

COMPERJ(1º phase)

165 thous. bpd(2013)

RNE230 thous. bpd

(2013)

2020

...

3,196

2,794

2009 20142010

Gasoline Diesel Others

PREMIUM I(2ª fase)

300 thous. bpd

(2016)

...

COMPERJ(2º phase)

165 thous. bpd(2018)

Throughput

Clara Camarão

2010

PREMIUM II300 thous.

bpd(2017)

20

STRATEGIC PLAN PETROBRAS 2020

50%

29%

11%

6% 3%1%

Additional capacity Quality and conversionOperational Improvement Fleet expansionLogistics for oil International

RTM AND PETROCHEMICALS INVESTMENTS 2010RTM AND PETROCHEMICALS INVESTMENTS 2010--20142014New refineries, fuel quality, and modernization account for 70% New refineries, fuel quality, and modernization account for 70% of capexof capex

• Additional capacity:• Refinery NE• Premium I• Comperj

• Quality and conversion• Sulfur removal• Modernization• Upgrading (coker)

• Operating improvement and logistics:• Maintenance• HSE• Logistics for oil and biofuels

US$ 73.6 Billion

• Investments of US$ 5.1 Billion in Petrochemical (includes acquisition of Quattor)

21

STRATEGIC PLAN PETROBRAS 2020BUSINESS PLAN PETROBRAS 2020

Demand, Goals and Principal ActivitiesDemand, Goals and Principal Activities

GAS, ENERGY AND GASCHEMICAL

STRATEGIC PLAN PETROBRAS 2020

22

STRATEGIC PLAN PETROBRAS 2020

NATURAL GAS MARKET AND POWER CAPACITY NATURAL GAS MARKET AND POWER CAPACITY Growth in natural gas demand, consolidation in Thermo Power capaGrowth in natural gas demand, consolidation in Thermo Power capacitycity

41

32

53

5.324.32.0

4

14.4

2009 2014

Electrical Generation Industrial Fertilizers Other uses

137 365

1,090 1,093

6,437 5,997

2010 2014International Thermoelectrical and Co-generation Renewables Sources

Installed Capacity of Electrical Energy Generation (MW)

+9%7,227 7,892

* 2014 – Thermooelectrical generationa refers to full and simultaneous dispatch of plants

Natural Gas Demand

46

130*

Mill

ion

m3/

day

23

STRATEGIC PLAN PETROBRAS 2020

NATURAL GAS BASED FERTILIZERSNATURAL GAS BASED FERTILIZERSFertilizer plants to take advantage of available gas and infrastFertilizer plants to take advantage of available gas and infrastructureructure

• Manage total demand for gas by transforming natural gas into fertilizers needed by Brazilian agriculture (substituting demand that is currently imported)

8441,076

2,104

807

298274

2010 2014 2015Ammonia Urea

+160%

Th. t

on/y

ear 1,374

2,911

1,118

UFN III (sep/14)Ammonia:

81th. ton/yearUrea 1.210 th.

ton/year

UFN IV (dec/15)

Urea 763 th. ton/year

Ammonia Plant(Dec/14)519 th.

ton/year

24

STRATEGIC PLAN PETROBRAS 2020

15%

23%

32%

30%

GAS, POWER AND GAS CHEMICAL INVESTMENTS 2010GAS, POWER AND GAS CHEMICAL INVESTMENTS 2010--20142014Transition from investment in infrastructure to gas demand flexiTransition from investment in infrastructure to gas demand flexibilitybility

LNG Pipeline network

Electrical Energy Chemical Gas Facilities (Fertilizers, ammonia)

Investments 2010Investments 2010--1414US$ 17.8 US$ 17.8 billionbillion

• Completion of the natural gas transport and processing infrastructure

• Consolidating investment in power generation: thermo-electric, wind, biomass

• Presence in LNG chain for transport and distribution of pre-salt gas

• Major investments in the conversion of natural gas in to Urea and Ammonia

5.7

4.1

2.75.3

25

STRATEGIC PLAN PETROBRAS 2020

Goals and Main Projects Goals and Main Projects

INTERNATIONALDISTRIBUTION

BUSINESS PLAN PETROBRAS 2020STRATEGIC PLAN PETROBRAS 2020

BIOFUELS

26

STRATEGIC PLAN PETROBRAS 2020

BR market share in the total and automotive market (%)

Distribution CAPEX – Brazil

30.438.6 40.0

22.430.6 33.6

2004 2009 2014

BR market share in total market in Brazil (%) BR market share in automotive market in Brazil (%)

US$ 2.5 BillionUS$ 2.5 Billion

DISTRIBUTION INVESTMENTS 2010DISTRIBUTION INVESTMENTS 2010--20142014Leading the Brazilian market for distribution, increasing the maLeading the Brazilian market for distribution, increasing the market sharerket share

• 8 p.p. increase in the global and automotive market share in the last 5 years.

• We intend to continue leading the Brazilian distribution market of oil products and biofuels, increasing our share in the market.

27%

26%24%

23%Gas station

Wholesales consumers

Operation and Logistics

Liquigás + Others

27

STRATEGIC PLAN PETROBRAS 2020

INTERNATIONAL STRATEGYINTERNATIONAL STRATEGYReduced allocation of Reduced allocation of capexcapex, with focus on upstream, with focus on upstream

Ramp up of existing developments, stable production in long term

Reduced investment and production a reflection of greater opportunities in Brazil

• Development focus: Gulf of Mexico, West Coast of Africa and Latin America

• Exploration focus: Atlantic Project, West coast of Africa, aligned with domestic E&P

• Reduced emphasis on refining

• Reduced emphasis on LNG, alignment with domestic Gas and Power segment

RTCP615 5%

E&P10,330 90%

CORPORATE123 1%G&E

186 2%

DISTRIBUTION221 2%

INTERNATIONAL PRODUCTION OF OIL AND GASINTERNATIONAL PRODUCTION OF OIL AND GASBP 2010 BP 2010 -- 20142014

INVESTMENTS 2010INVESTMENTS 2010--2014: 2014: US$ 11.5 biUS$ 11.5 bi

Thousand bpd

239 304

146 176 20393 128 120

0

200

400

600

800

2010 2014 2020

Oil and NGL Natural Gas BP 2009-2013 Target

323

632BP 2009-2013

Target

- 49%

28

STRATEGIC PLAN PETROBRAS 2020

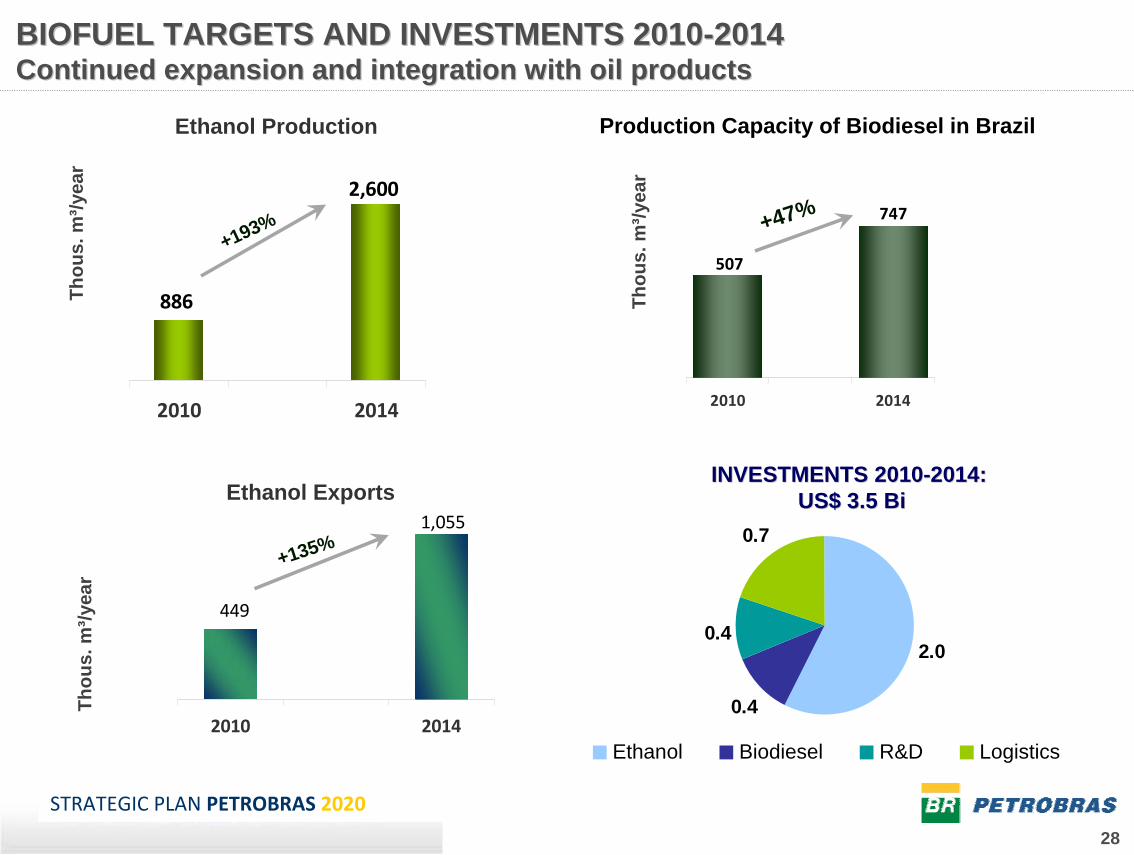

BIOFUEL TARGETS AND INVESTMENTS 2010BIOFUEL TARGETS AND INVESTMENTS 2010--20142014Continued expansion and integration with oil productsContinued expansion and integration with oil products

2,600

886

2010 2014

+193%

Thou

s. m

³/yea

r

Ethanol Production

747

507

2010 2014

Production Capacity of Biodiesel in Brazil

+47%

2.0

0.4

0.4

0.7

Ethanol Biodiesel R&D Logistics

INVESTMENTS 2010INVESTMENTS 2010--2014:2014:US$ 3.5 BiUS$ 3.5 Bi

Thou

s. m

³/yea

r

Thou

s. m

³/yea

r

1,055

449

2010 2014

Ethanol Exports

+135%

29

STRATEGIC PLAN PETROBRAS 2020

Targets and Goals, HSE, Technology, and Research Targets and Goals, HSE, Technology, and Research and Developmentsand Developments

BUSINESS PLAN PETROBRAS 2020STRATEGIC PLAN PETROBRAS 2020

RESEARCH & DEVELOPMENT

30

STRATEGIC PLAN PETROBRAS 2020

Other Renewable sources Energy

Maximizing recovery factor

Developing Production,

Operation and Pre Salt Logistic

Operational Optimization

Solutions for Natural Gas

logistic in harsh environments

New Exploratory Frontier

CO2 and other gas management Energetic

Efficiency

TECNOLOGICAL CHANGESTECNOLOGICAL CHANGES3 Key pillars3 Key pillars

Middle distillate Maximization

Petrochemicals Gas Chemic

Fuel, Lubricants and special

products innovation Biofuels

Sediments and other fuels

characterization of the pre salt

and other complex

reservoirs

Development of new generation Sea and Subsea

Systems

Expanding Limits

Sustainability

Adding value and Diversifying Products

Water management

31

STRATEGIC PLAN PETROBRAS 2020

Reduction in the complexity of the projects, using standard solutions

Contributing for the consolidation of Brazil as a supplying hub with international competitive level

Using international engineering patterns and metrics in our facility projects

ENGINEERING CHALLENGESENGINEERING CHALLENGES

Simplification and Standardization

Competitiveness/ Sustainability

Brazilian ContentTechnological & Engineering

Drivers

32

STRATEGIC PLAN PETROBRAS 2020

ESTRUTURA CORPORATIVA DE RESPOSTA CDA / BASES AVANÇADAS / EDR&D INVESTMENTS ALLOW TECHNOLOGICAL LEADERSHIP WITH R&D INVESTMENTS ALLOW TECHNOLOGICAL LEADERSHIP WITH FOCUS IN HSEFOCUS IN HSE

Investments in HSE, IT and R&D

US$ 11.4 Billion

29%

25%

46% HSE

IT

R&D

• Continued spending of $1 billion per year on Research and Development

• Continued focus on Health, Safety and Environment

33

STRATEGIC PLAN PETROBRAS 2020

Cash generation and Funding needsCash generation and Funding needs

BUSINESS PLAN PETROBRAS 2020STRATEGIC PLAN PETROBRAS 2020

PLAN FINANCING

34

STRATEGIC PLAN PETROBRAS 2020

FORECASTED OIL PRICE VERSUS Business PLAN 2010FORECASTED OIL PRICE VERSUS Business PLAN 2010--20142014Petrobras base case planning price at lower end of forecast rangPetrobras base case planning price at lower end of forecast rangee

3629

2723 21 22 26 24

1622

34 29 2933

42

59

6975

78

72

84

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

1990 1995 2000 2005 2010 2015 2020 2025 2030

Forecasts: CERA, PIRA, WoodMackenzie, EIA e IEA.

Petrobras budget price62

98

35

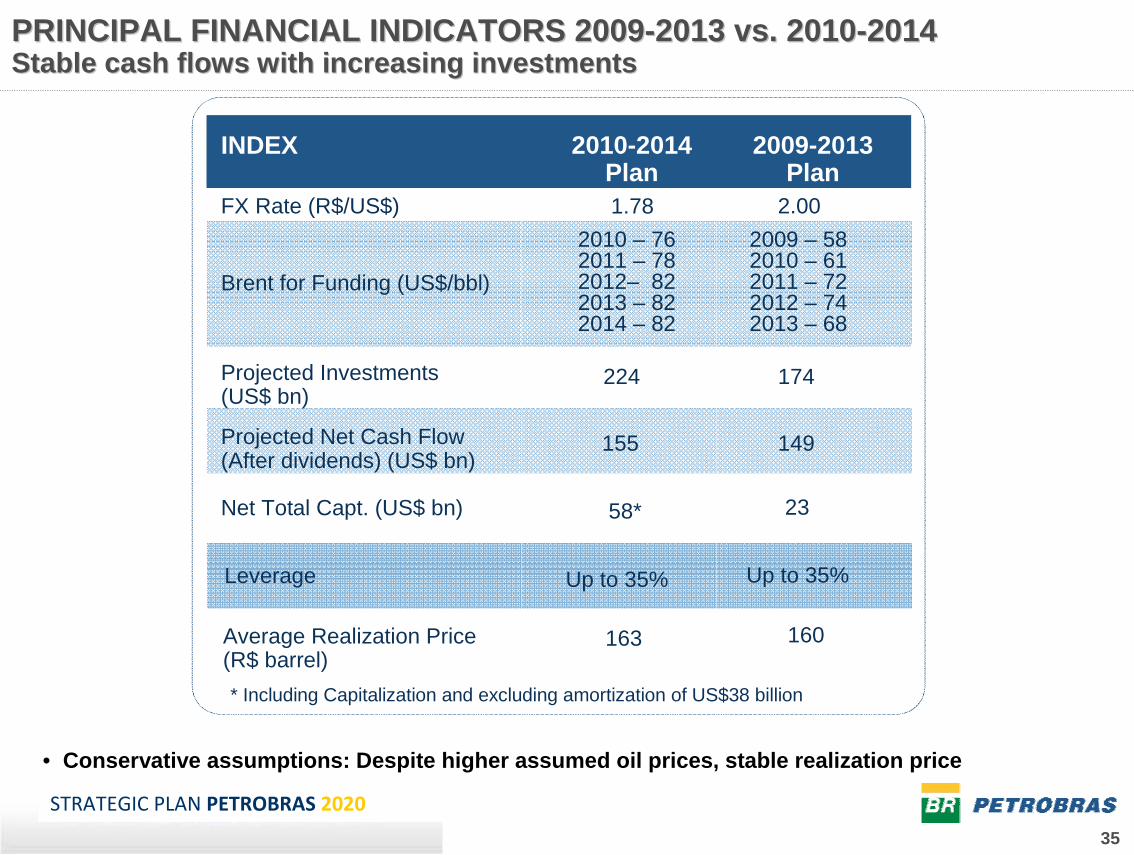

STRATEGIC PLAN PETROBRAS 2020

PRINCIPAL FINANCIAL INDICATORS 2009PRINCIPAL FINANCIAL INDICATORS 2009--2013 vs. 20102013 vs. 2010--20142014Stable cash flows with increasing investmentsStable cash flows with increasing investments

• Conservative assumptions: Despite higher assumed oil prices, stable realization price

INDEX 2009-2013 Plan

2010-2014 Plan

FX Rate (R$/US$) 2.00

Brent for Funding (US$/bbl)

Projected Investments (US$ bn)

174

Projected Net Cash Flow (After dividends) (US$ bn)

149

Net Total Capt. (US$ bn) 23

Leverage Up to 35%

1.78

224

155

58*

Up to 35%

2010 – 762011 – 782012– 822013 – 822014 – 82

2009 – 582010 – 612011 – 722012 – 742013 – 68

Average Realization Price (R$ barrel)

163 160

* Including Capitalization and excluding amortization of US$38 billion

36

STRATEGIC PLAN PETROBRAS 2020

CASH GENERATION AND INVESTMENTCASH GENERATION AND INVESTMENTProfitable investments funded with cash flow, debt and equity caProfitable investments funded with cash flow, debt and equity capitalpital

• Plan requires additional debt and equity capital

• Return on portfolio of approximately 14% on the aggregate of projects in the Plan substantially exceeds cost of capital

PROJECTED Operating Cash Flow(2010 – 2014)

OCF(after dividends)US$ 155 billion

Funding(debt + equity)US$ 96 billion

InvestmentsUS$ 224 billion

Sources Uses

CashUS$ 11 billion

AmortizationUS$ 38 billion

37

STRATEGIC PLAN PETROBRAS 2020

CHALLENGESCHALLENGES

•• Capacity to execute a huge portfolio projectCapacity to execute a huge portfolio project

•• Strength and reliability of supply chainStrength and reliability of supply chain

•• Resource management and efficiencyResource management and efficiency

•• Human Resources challengesHuman Resources challenges

•• Funding requirements Funding requirements

38

STRATEGIC PLAN PETROBRAS 2020

Thank youThank you