Latin American Panel Miami, 24 July 2003 “ POST PRESTIGE ” Peter M. Swift.

Upload

belinda-goodwinCategory

view

220download

2

Peter M. Swift, Propeller Club, London, 22 January 2001

For better or for worse – tanker owning today

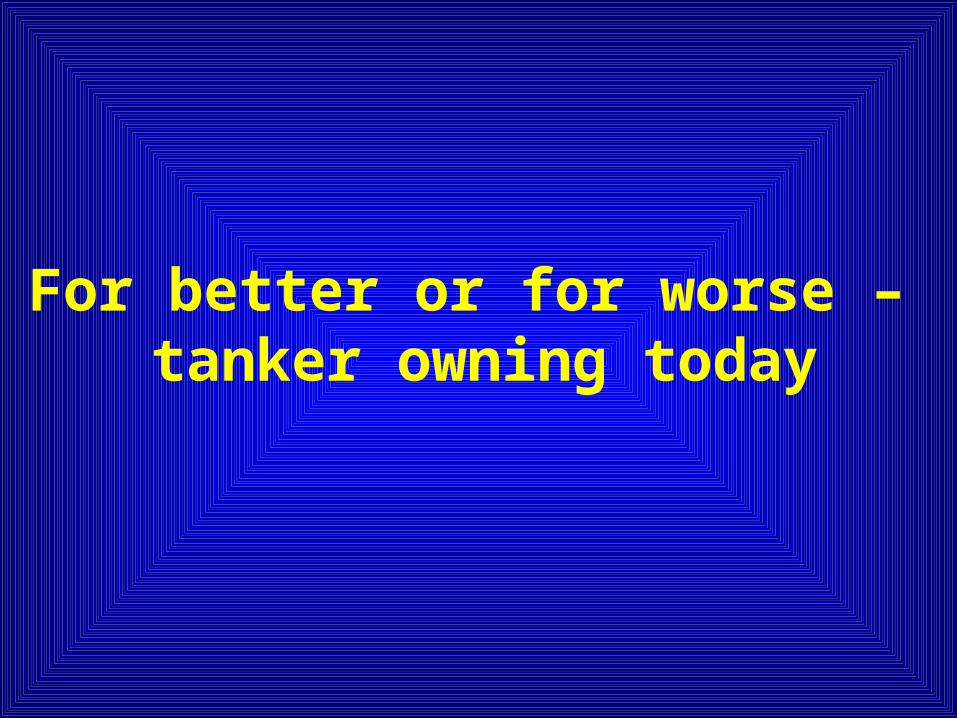

International Association of Independent Tanker OwnersInternational Association of Independent Tanker Owners

INTERTANKO INTERTANKO todaytoday

• 224343 Members Members• 2,2,046046 tankers tankers• 115858 million dwt million dwt • 4455 countries countries• 293 293 Associate MembersAssociate Members

Oslo London Singapore Washington

INTERTANKOINTERTANKOInternational Association of Independent Tanker OwnersInternational Association of Independent Tanker Owners

Safe TransportSafe TransportCleaner SeasCleaner Seas

Free CompetitionFree Competition

advocatingadvocating

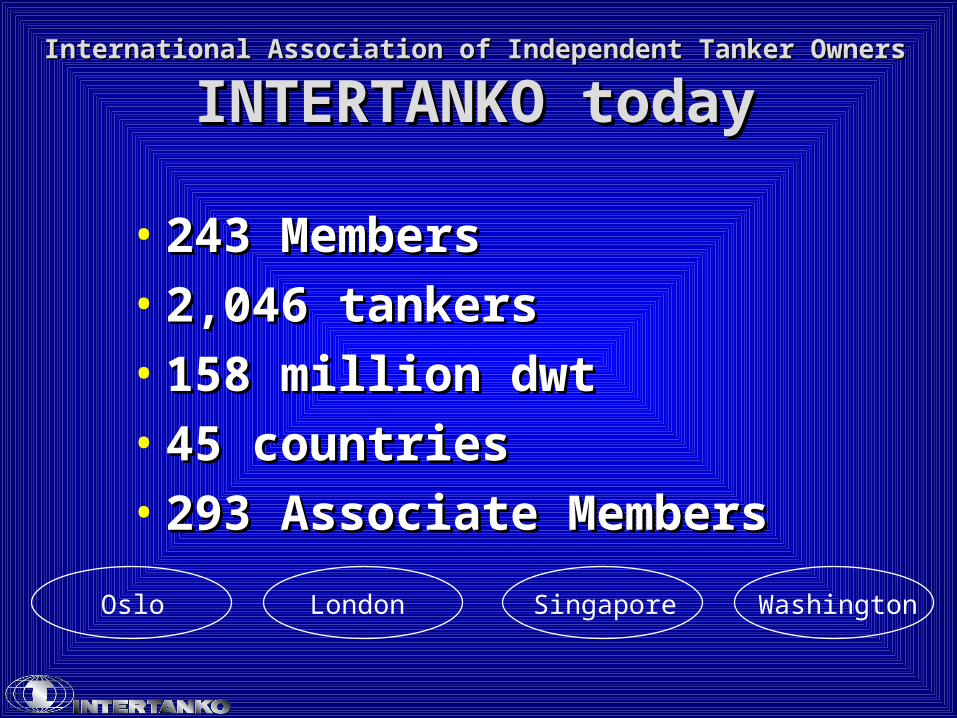

AS AN INDUSTRY WE MAY NOT BE LOVED BUT WE ARE NEEDED

• World Oil World Oil Consumption Consumption 3,590 mil ts3,590 mil ts

• Transported by sea Transported by sea 2, 0152, 015 mil tsmil ts

• 5757% transported by sea.% transported by sea.

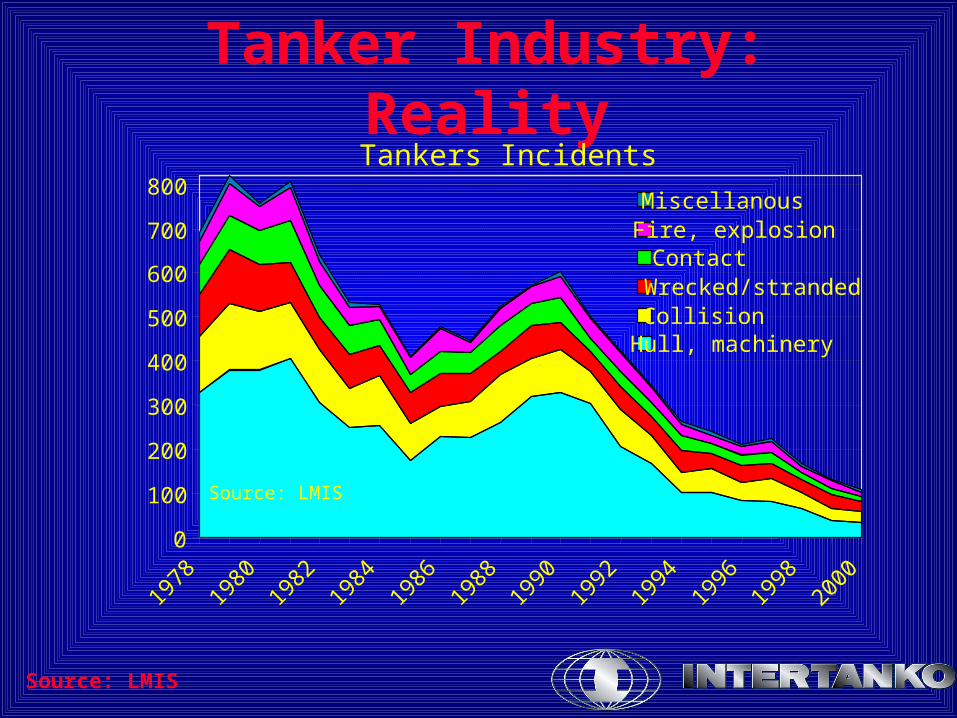

Tanker Industry: RealityTankers Incidents

0

100

200

300

400

500

600

700

800

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

MiscellanousFire, explosionContactWrecked/strandedCollisionHull, machinery

Source: LMIS

Source: LMIS

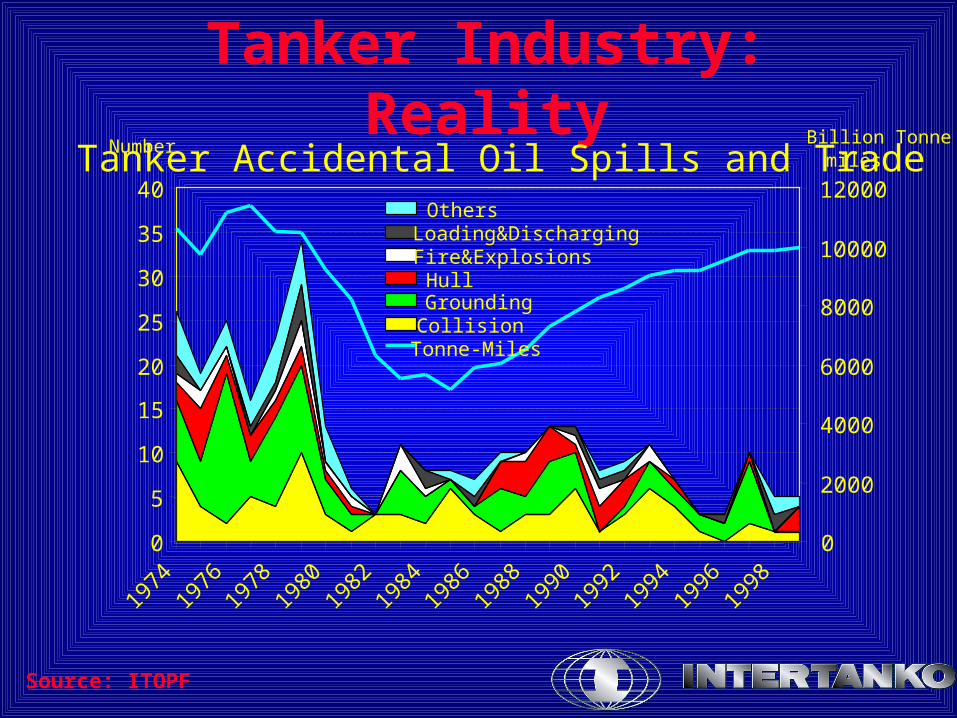

Tanker Industry: RealityTanker Accidental Oil Spills and Trade

0

5

10

15

20

25

30

35

40

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

0

2000

4000

6000

8000

10000

12000 Others Loading&Discharging Fire&Explosions Hull Grounding CollisionTonne-Miles

Number Billion Tonne miles

Source: ITOPF

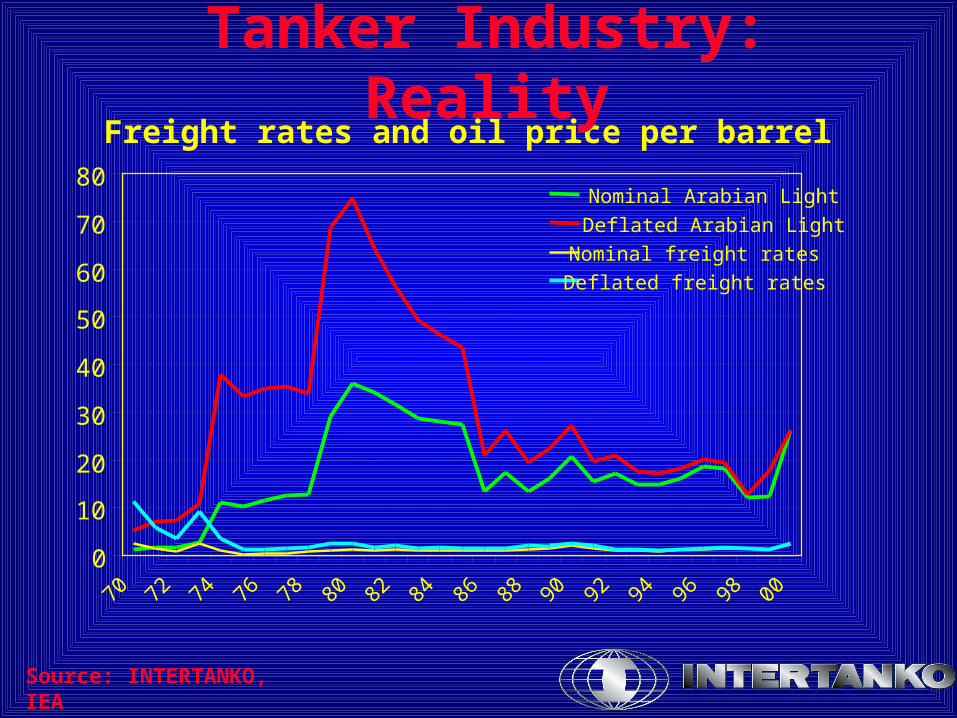

Freight rates and oil price per barrel

0

10

20

30

40

50

60

70

80

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00

Nominal Arabian Light

Deflated Arabian Light

Nominal freight rates

Deflated freight rates

Source: INTERTANKO, IEA

Tanker Industry: Reality

Tankers 39% DH

VLCCs Suezmaxes Aframaxes 60-80,000 20/30-60,0000%

20%

40%

60%

80%

100%

35% 44% 47% 36% 35%

Single Hull

Double Hull

Tanker Industry: Reality

Source: INTERTANKO

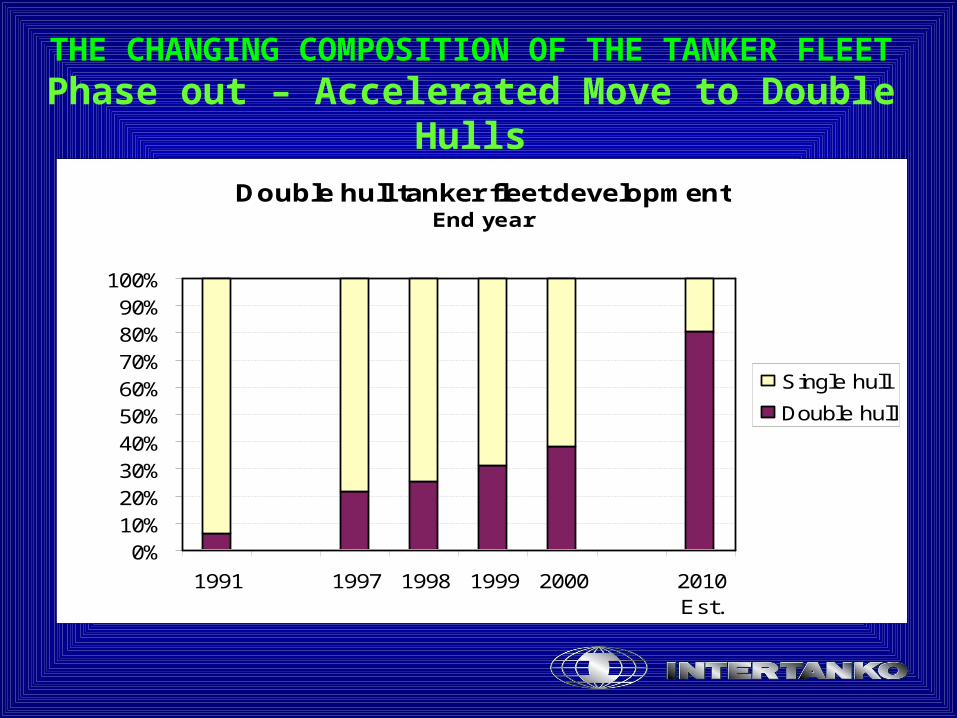

THE CHANGING COMPOSITION OF THE TANKER FLEETPhase out – Accelerated Move to Double Hulls

Double hull tanker fleet developmentEnd year

0%10%20%30%40%50%60%70%80%90%

100%

1991 1997 1998 1999 2000 2010Est.

Single hull

Double hull

The image

OWNER CHARTERER CLASS

IMAGE PROBLEM !

The Rogues of the Tanker Industry

SHIPBROKER

BUT EVEN WORSE IMAGE !

The world expects us to have 0 accidents.

99.97% safe transportation means that out of 1.000 tanker liftings 3 will have some problems.

That will not be accepted! It takes one accident to change the industry

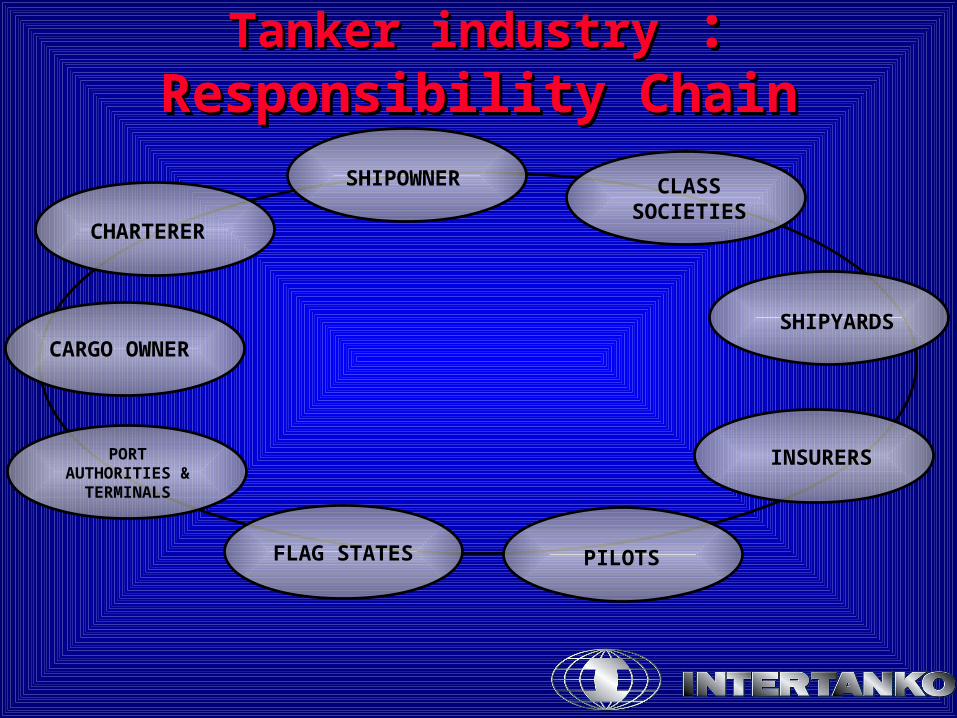

Tanker industryTanker industry : : Responsibility ChainResponsibility Chain

SHIPOWNER

SHIPYARDS

INSURERS

PILOTS

CARGO OWNER

CHARTERER

PORTAUTHORITIES &

TERMINALS

CLASSSOCIETIES

FLAG STATES

WEAKEST LINK: Consequences of WEAKEST LINK: Consequences of FailureFailure

Credibility with stakeholders damaged

Political Intervention/Regulations

instead of

Self Correction

Weaknesses in system exposed

FOR BETTER OF FOR WORSE

VICIOUS CIRCLE

CRACKDOWNON

WEAKNESSES

ADDITIONAL COSTS&

OFFHIRE TIME

EROSIONOF FRAGILE

PROFITABILITY

PRESSURE ONCOSTS &

STANDARDS

?

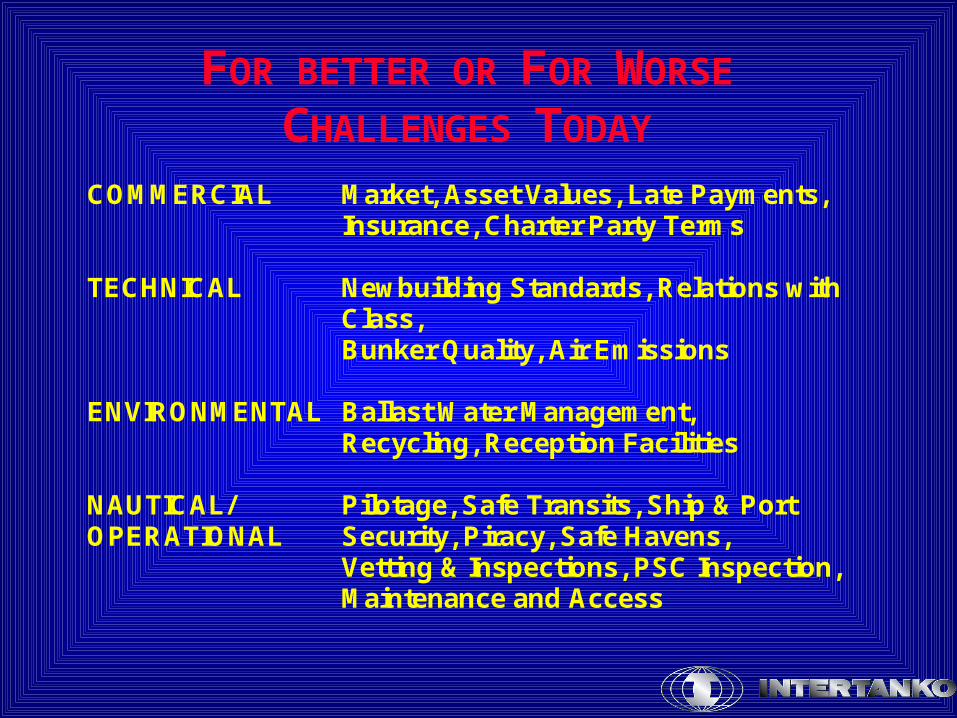

FOR BETTER OR FOR WORSE

CHALLENGES TODAY

COMMERCIAL Market, Asset Values, Late Payments, Insurance, Charter Party Terms

TECHNICAL Newbuilding Standards, Relations with Class, Bunker Quality, Air Emissions

ENVIRONMENTAL Ballast Water Management, Recycling, Reception Facilities

NAUTICAL/ OPERATIONAL

Pilotage, Safe Transits, Ship & Port Security, Piracy, Safe Havens, Vetting & Inspections, PSC Inspection, Maintenance and Access

FOR BETTER OR FOR WORSE

SOLUTIONS - TODAY

• ENACTMENT & ENFORCEMENT OF EXISTING

LEGISLATION

(UNIFORMITY & HARMONISATION ON GLOBALS BASIS)

• INCREASED TRANSPARENCY

• GREATER DIALOGUE AMONG PARTNERS

• MORE RESPECT FOR MARITIME PROFESSIONALISM

• BETTER UNDERSTANDING & ASSESMENT OF RISKS

• IMPROVED FEEDBACK & LEARNING MECHANISMS

• EFFECTIVE ACCIDENT INVESTIGATION

• MORE TRUST!