Pertemuan 1 - Banking and financial intermediaries -micro ... · the sums required. It would also...

61

Transcript of Pertemuan 1 - Banking and financial intermediaries -micro ... · the sums required. It would also...

Pertemuan 1 - Banking and financial intermediaries -micro & macro perspective

Financial intermediation

is a process which involves surplus units depositing funds with financial

institutions who in turn lend to deficit units.

can be distinguished by four criteria:

Their liabilities -i.e., deposits- are specified for a fixed sum which is not

related to the performance of their portfolio

Their deposits are of a short-term nature and always of a much shorter

term than their liabilities

A high proportion of their liabilities are chequeable.

Neither their liabilities nor assets are in the main transferable. This aspect

must be qualified by the existence of certificates of deposit and

securitization.

Different Requirements of Borrowers & Lenders

Borrowers need large quantities of funds whereas the lender only have smaller

amounts of surplus funds; in other words, the capacity of the lender is less than

the size of the investment project.

bank will collect a number of smaller deposits, parcel them together and

lend out a larger sum ‗size transformation‘.

the lender usually wants to be able to have access to his funds in the event of an

emergency; that is, he/she is wary of being short of liquidity.

Banks can fulfil this gap by offering short-term deposits and making loans

for a longer period maturity transformation

Lenders will prefer assets with a low risk whereas borrowers will use borrowed

funds to engage in risky operations risk transformation

Why „they‟ deal through financial intermediaries?

Transaction costs the nature of costs involved in transferring funds from

surplus to deficit units:

Liquidity insurance the financial intermediary acts as an insurance agent.

Asymmetry of information

moral hazard

Assymetric information

1. TRANSACTION COSTS

Search costs

these involve transactors searching out agents willing to take an opposite

position; e.g., a borrower seeking out a lender(s) who is willing to provide

the sums required. It would also be necessary for the agents to obtain

information about the counterparty to the transaction and negotiating and

finalizing the relevant contract.

Verification costs

Cost of the lender to evaluate the proposal for which the funds are

required.

Monitoring costs.

Cost to monitor the progress of the borrower and ensure that the funds are

used in accordance with the purpose agreed.

To prevent moral hazard in miss alocate the funds

Enforcement costs.

Such costs will be incurred by the lender if the borrower violate any of the

contract conditions.

2. Liquidity insurance

the existence of banks enables consumers to alter the pattern of their

consumption (C1, C2) The value of this service permits a fee to be earned by

the financial intermediary.

bank offering fixed money claims overcomes this problem by pooling resources

and making larger payments to early consumers and smaller payments to later

consumers

3. ASYMMETRY OF INFORMATION

Borrower have more information about the project that is the subject of a loan

than the lender

Moral hazard is the risk that the borrower may engage in activities that reduce

the probability of the loan being repaid.

Before loan: Business proposal bout big profit, minim failure

After loan: engage in risky activities

Adverse selection: the lender is not sure of the precise circumstances

surrounding the loan and associated project salah pilih borrower, salah pilih

proyek

Cara bank mengatasi informasi asimetris

the banks are subject to scale economies in the borrowing/lending activity so that

they can be considered information-sharing coalitions;

banks monitoring the firms that they finance, i.e. delegated (representative)

monitoring of borrowers

Banks‘ provision of a commitment to a long-term relationship

1. INFORMATION-SHARING COALITIONS

problem information is costly to obtain and that it is in the nature of a ‗public

good‘.

Resolve it through an intermediary which uses information to buy and hold assets

in its portfolio

can provide information about its project is by way of offering collateral security,

coalition of borrowers‘ (i.e., the bank) can do better than any individual borrower

2. BANKS‟ ROLES IN DELEGATED MONITORING

Screening application of loans so as to sort out the good from the bad, thus

reducing the chance of financing excessively risky loans.

Examining the firm‘s creditworthiness.

Seeing that the borrower follow to the terms of the contract.

3. A MECHANISM FOR COMMITMENT

Japanese and German banks do have a close relationship with their clients and

in many cases are represented on the firms‘ governing bodies.

This enables the bank to have good information about investment prospects and

the future outlook for the firm and to take remedial actions other than foreclosure

in the event of the firm experiencing problems.

This close relationship may help to fix the twin problems of moral hazard and

adverse selection.

Hoshi et al. (1991) provide supportive evidence that firms with close banking ties

appear to invest more and perform more efficiently than firms without such ties.

Fractional Reserve Banking-Intro to Macro

Modern banks produce fiat money on the basis fractional reserves

Money has value because universal acceptance as money

The acceptance of money = social convention + legal system money as

instrument for the legal discharge of debts

Seigniorage rightfully belongs to the community at large & should not be

appropriable by private interest

Fractional Reserve Banking (FRB)

Fund themselves with liabilities that are convertible into cash on demand

But they hold only a fraction of liabilities in the form of cash assets

Result: withdrawals > available cash

Evolution of monetary & banking systems

From commodity money (gold, silver, etc) to more abstract forms of money

From warehouses (or 100% reserves banks) to more modern fractional reserve

banks

The substitution of fiat for commodity money concentrates enormous

economic power in the hands of monetary authority

FRB enormous power in the hands of individual bankers jeopardize the

stability of banking system in the pursuit of personal gain

The evolution of the primitive goldsmith into a bank

Gold as money means of payment, med of exchange

Debts & purchase are paid with gold

Problem holding & transporting gold security & convenience

Market response provide warehouse for gold emergence of the goldsmith

The owner receive a receipt to redeem the gold from goldsmith

From gold to the piece of paper

Repeated trips (both, seller/buyer) to goldsmith is wasteful

Willingness to accept warehouse receipt as mean of payment believe that the

gold is available on demand

Receipts totally displace gold, the inventory of gold unchanged (except newly

mined gold into system)

No need gold for outstanding receipts

Issue more receipts > had gold bcoz no one withdraw gold (exploitation of owner

by goldsmith begin)

The naughty possibility of printing extra receipts changed the world

Instability of fractional reserves bank

As means of payment, “Extra” receipts = authentic receipts

The “extra” loaned + earned interest

Loan are illiquid (must be held to maturity)

Goldsmith provide liquidity transformation

by issue liquid claims

Transformation of pedestrian goldsmith from warehouse clerk

into banker

Liability > capability (bcoz loan are illiquid) insolvency risk of

ruin is endogenous

Temptation from Prob of solvency print extra + make more

loans

Promise to pay on demand not sure

(liquidity issue)

That essence of FRB & its vulnerable +

maximizing behavior part of rational economic agent

Need way out to avoid periodic collapse.. From FRB to CB..

The illiquidity loans (assets) could be liquefied

Need ―bank for goldsmiths‖ to against infrequent redemption the collateral‘s loan

19th century Commercial Bank Clearing House (CBHS) in US banks agreed

to put their resources to unanticipated liquidity drains

Rationale to build central bank this private arrangements did not possess

unlimited capacity so need a ―central‖ as lender of last resort to the community

bankers

Here are come the regulation..

To avoid goldsmith make a huge loans CB will charges very high interest rate

for emergency borrowings

CB imposing cash asset reserve requirements to limit the volume of lending on

the basis of its cash assets

They said it is the most basic prudential regulation but this is a moral hazard

(save a little, get more but secure)

Un convenience of commodity money FRB CB moral hazard

regulation

A model of banks & regulations

n (depositor) = 1

j (bank) = 1

S = y-c

bank fee

Save for only 1 period, c the next period = + y the 2nd period

Interest on deposit =

Negative interest bank cant make loans + charge cost to the depositor

The macroeconomic implications of FRB: The Fixed Coefficient Model (FCM)

FCM = the standard textbook description of the banking firm and industry; it

emphasizes the asset-transformation function of financial intermediaries.

R = Reserves (from deposit)

M = earning asset (from loans)

D = deposit (s x n)

E = equity

r = legal reserve requirement

e = fix prop of capital reserves

Illustration: w/out equity (e=0, r=0.2)

FCM & monetary policy

3 major tools of monetary policy to influence the stock of money & interest rate

OMO = sales & purchases of govt securities (T-bonds) affect amount of

reserves (lending also) buy = lending rise, sale =lending fall

rr changes contractionary monetary policy (to cool down inflation) it

raise rr, to stimulate economy lower rr

Discount rate changes: the rate charged by the Fed to member banks for

short-term borrowings from the Fed

disc rate rise, costly for banks to borrow and build up reserves,

reduces the reserves available to banks & this reduces lending.

discount rate lower increased lending

Large Financial Intermediaries

Brokerage as a Natural Monopoly

Broker = information producer

Problem how customers know that the information the broker provides

is accurate and reliable?

Need higher reputation broker by comparing info from other resources

If single info producer, costly to ensure reliable info

Little less if info from team member of producer

Effective mechanism as long as nobody get free ride

Size of team grows (broker get larger), benefit keep growing

That is brokerage is a natural monopoly

Another ec. benefit from growing large

information reusability

can be reused by a greater number producers within the intermediary, and

yet the cost incurred only once.

Benefited to investment banks, financial newsletters, credit-rating

agencies, and other information producers

Large Financial Intermediaries contd

Asset Transformation as a Natural Monopoly

Bank as asset transformer borrows money from depositors and makes

loans.

Its advantage in being large comes from two sources:

multiple depositors are needed to finance a single bank borrower

and the borrower‘s creditworthiness has to be established through

costly credit analysis. So bank perform this credit analysis once

compared to a situation in which all the depositors engage in costly

screening of the borrower. That is, a bank eliminates duplicated

screening.

the depositors‘ payoff is a debt contract, so they behave risk

averse, by get lower interest rate on deposits. The bank can do this

by diversifying its risk across many different borrowers. And,

because the benefit of diversification keeps growing with size, the

bank is a natural monopoly.

How Banks Can Help Nonbank Financial Contracting More Efficient

bank loans reduce duplication in borrower evaluation by multiple creditors

Bank loan is short maturities periodically renewed bank evaluation of

the borrower‘s ability to meet fixed payment obligations

renews the loan positive signal about the firm to its other creditors so

no need to expend their own resources to duplicate the bank‘s evaluation

Simple example: dokumen yg sdh masuk bank legally secure

How Banks Can Help Nonbank Financial Contracting More Efficient

Banks have a cost advantage in making loans to depositors

The ongoing history of a borrower = borrower‘s cash management

activities

This permits the bank to assess risks of loans to depositors and to monitor

these loans at lower cost than other (competing) lenders.

This consideration is particularly important in short-term loans that are

rolled over because of the relatively more frequent borrower assessments.

This hypothesis has empirical validity in the observation that most short-

term debt is in the form of bank loans.

The Borrower‟s Choice of Finance Source: go to venture capitalist if..

Two very young characteristics.

the entrepreneur in charge may be unsure of his own management

expertise, so that approaching financial intermediary that can provide this

expertise is beneficial.

the borrower has few tangible assets to offer as collateral.

collateral is useful in controlling moral hazard

In the absence of collateral, the lender could use equity participation as a way of

addressing moral hazard.

Thus, it is in the borrower‘s interest to seek a lender who can take an equity

position and thus be able to offer capital at a ‗‗reasonable‘‘ price.

Both factors suggest that such firms should go to venture capitalists not bank

U should go to bank if..

Bank can lend to borrowers because they can offer collateral to secure their debt.

all moral hazard will not be eliminated by collateral, so that there will be an

important role for bank monitoring.

bank loans tend to be of short maturities, thereby generating periodic information

through reassessments of the borrower.

This information is refflected both in the bank‘s decision to renew/terminate the

loan as well as in the new contract terms offered, in combination with information

produced by rating agencies.

This helps to reduce duplication in information production by other creditors of

the firm, thereby diminishing overall contracting costs.

go to banks than venture capitalists because banks can fund their loans with

insured deposits, the borrower is able to obtain a loan at a lower price.

U go to capital market if..

when the firm is well-established and mature, it has a good track record for

repaying its debts.

This reputation can be valuable because it permits the firm to borrow at

preferential rates.

Consequently, bank monitoring to combat moral hazard is less important for such

borrowers, and this permits them to directly access the capital market where

borrowing costs are lower; capital market access would mean that the borrower

would not have to pay the bank its intermediation rents.

Of course, such firms still confront problems of asymmetric information , so that

nondepository financial intermediaries such as investment banks (or credit-rating

agencies) play an important role in the transfer of capital from investors to such

firms. This is because they make information about firms available to investors at

a lower cost than they could acquire themselves.

The venture capitalist provides financing, monitoring, and management

expertise; the bank provides financing and monitoring; and the capital market

provides mainly financing.

Pertemuan 2 - Banking industry

Sejarah industri perbankan

Asal mula Perbankan

1690 di Eropa bank pertama berdiri berbentuk firma

Kebutuhan kerajaan Inggris untuk membangun armada laut tapi tidak ada

dana

Dibangun lembaga intermediasi untuk memenuhi dana tsb.

Kemudian berkembang ke benua lain dibawa oleh bangsa Eropa saat

menjajah.

Jasa penukaran uang jasa penitipan uang jasa peminjaman uang

Evolution of the Banking Industry

Financial innovation is driven by the desire

to earn max profits tranformed the entire financial system

A change in the financial environment will stimulate a search by financial

institutions for innovations that are likely to be profitable

3 basic types of financial innovation

Responses to change in demand conditions

Responses to changes in supply conditions

Avoidance of regulations

Lobbying to channge regulations

Responses to changes in demand conditions

Interest rate volatility

1950s: 1-3.5%; 1970s: 4-11.5%; 1980s: 5-15%

Adjustable-rate mortgages

Lending more attractive if interest rate risk is lower

So, give lower rate and volatile after (adjust to market rate)

Financial derivatives

Born in 1975

Future contracts, their payoffs derived from previously issued

securities, used to hedge risk

Responses to changes in supply conditions

Information technology

- Lowered the cost of processing financial transcactions

- Easier for investors to acquire information

- easier for firms to issue securities

Bank credit & debit cards

Since before WW 2

Individual store (Sears, Macy‘s, Goldwater‘s) provide CC to

purchase w/out cash

1960s, improved computer technology: BankAmericard by Bank of

America Visa; Mastercharge by Interbank Card Association

Mastercard

Issued 200 million cards to purchase & to take loan out easily

Electronic banking

ATM: 24 hours/day cheaper transactions, convenience for

costumer

Home banking by telephone or PC linked up with the bank‘s

computer

Automated banking machine (ABM) combines in 1 location:

ATM, internet connection to the banks‘s website, telephone link to

CS

Virtual bank bank in cyberspace

Junks bonds (BB lower)

Easier screening, investor willing to buy LT debt sec from les-well

corp with lower credit ratings

Commercial paper market

S/T debt sec by large banks & corp

Securitization

Process of transformingilliquid financial assets (mortgages, auto

loans, CC receivables) of banking inst into cap mkt

Financial Engineering

1960s FI confronted drastic changes in the economic environment: inflation &

interest rate climbed sharply & harder to predict changed demand conditions

The rapid advance in computer technology changed supply conditions

Doing business old ways no longer profitable

Financial services & products were not sold

To survive in the new economic environment, FI had to research & develop new

products & services that would meet customer need & profitable, the process

Financial Engineering

Financial Innovation & the Growth of the “Shadow Banking System” (SBS)

Traditional banking business of making loans that are funded by deposits has

been in decline

Lending has been replaced by lending via the securities markets

Non-bank FI provide services similar to traditional commercial banks but less

regulation

SBS buildup systemic risk interelated with the traditional banking system via

credit intermediation chains

SBS do not have deposit insurance, lender of last resort

High level of financial leverage by transforming the maturity of credit (LT to ST)

real estate bubbles

SBS was primary factor in the subprime mortgage crisis of 2007-2008 & global

recession Morgan Stanley & Goldman Sachs merger, Merryll Lynch & Bear

Stearns acquired, Lehman Brothers Bankrupt

Banking business model

Investment Banking/ merchant bank / money market corporations

intermediasi keuangan yang melakukan fungsi khusus investasi, tidak menerima

saving & menyalurkan kredit

Customer segment: korporasi, pemerintah dan investor individual (High Net

Worth Individual) BCG >5jt USD, Merryl Lynch >1jt USD

Fungsi: underwriting securities (penerbitan saham/obligasi) & corporate advisory

services (konsultasi, corp finance, konsultasi mgt M&A, restrukturasi aset),

perdagangan surat berharga dan produk derivatif atas nama client/nasabah,

investment research, brokerage analyst, finance, asset management, & produk

derivatif atas nama perusahaan secara pribadi (proprietary trading), principal

investment

Ex: KFH dengan Liquidity Mgt House

Commercial Banking

Saving & credit

normal banking services at either or both retail and/or wholesale levels

Customer Segment: semua orang atau entitas yang membutuhkan layanan

perbankan mulai dari tabungan, pinjaman, jasa-jasa pembayaran dan

perdagangan luar negeri serta layanan-layanan yang lain business (small and

medium-sized businesses) dan individual customer

Produk: Bank Akseptasi, Pinjaman Konsumen sperti KPR, KKB, multiguna dan

produk investasi umum seperti Rekening Tabungan, Deposito.

Ada 2 jenis fungsi layanan yang diberikan oleh bank komersial yaitu:

Primary Banking: Fungsi pendanaan dan pembiayaan Menghimpun dana

dari masyarakat dalam bentuk simpanan berupa giro, deposito berjangka,

sertifikat deposito, tabungan , dan/atau bentuk lainnya yang dipersamakan

dengan itu

Secondary Banking: Fungsi agency dimana pendapatan bank diperoleh

dari fee based income

Universal Banking

kombinasi antara investment banking dan commercial banking

Customer Segment: berbagai segmen dari perorangan (dengan berbagai latar

belakang ekonomi), entitas bisnis (kecil,besar/korporasi), pemerintah, dan semua

entitas yang membutuhkan layanan jasa keuangan/ financial services.

penyediaan produk dan layanan yang lengkap akan memberikan economic of

scale sehingga lebih efisien dalam biaya opeasional sehingga biaya yang

dibebankan kepada nasabah juga lebih rendah.

Costumer relationship: cust priority, special rate/pricing

Consumer/retail/personal/B2C (Business to Customer) banking

untuk memenuhi kebutuhan nasabah individual/ bisnis dengan tingkat

pendapatan yang stabil.

Keunggulan: kelengkapan produk konsumsi yang ditawarkan dengan proses

yang mudah & sederhana.

revenue streams: margin antara suku bunga tabungan & pinjaman, fee dari

services

Produk: margin antara suku bunga tabungan dan suku bunga pinjaman serta

sebagian kecil fee atau komisi yang berasal dari layanan tambahan seperti

layanan investasi atas permintaan nasabahnya dll.

Partner: merchant berupa supermarket, dealer, perusahaan properti

Retail Banking

memfokuskan diri untuk memberikan pelayanan terutama kepada nasabah

individu dan sektor usaha kecil dan menengah.

Undang- Undang Nomor 20 Tahun 2008 tentang UMKM

Corporate/wholesale/B2B Banking

bank yang melayani kebutuhan-kebutuhan korporasi untuk menunjang

operasional bisnis mereka.

Manajemen cash dan layanan banking yang lain yang biasanya menyesuaikan

(customized) dengan kebutuhan korporasi.

Produk: secure dan unsecured loan, struktur transaksi keuangan yang sangat

canggih dengan melibatkan banyak bank berbeda atau sindikasi dalam

transaksi; deposits & loans from corporations dan large businesses, pembiayaan

alat berat bagi operasional korporasi, pembiayaan infrastruktur pemerintah, resi

gudang, cash management, trade service seperti L/C, kustodian dan

perdagangan mata uang (foreign exchange) untuk kebutuhan korporasi.

Community Banking

berukuran kecil dan hampir semua aktivitasnya diperuntukkan untuk komunitas

lokal

Costumer segment: small business dan sektor pertanian, komunitas lokal

untuk mempertahankan loyalitas nasabah: pendampingan usaha, special

rate/diskon suku bunga bagi nasabah yang sering melakukan transaksi bisnis

Development Banking

No saving

MT & ST financing proyek pembangunan & infrastruktur pemerintah, serta

industry strategis perusahaan swasta dan perusahaan pemerintah.

multipurpose financial institution, bantuan dana baik untuk insitusi swasta/publik.

gap filler ketika bantuan dana / managerial dari sumber lain tidak mampu

memenuhinya

meng-akselerasi pembangunan/pertumbuhan nasional.

Membantu industrialisasi (khusus) dan pertumbuhan ekonomi (umum).

memenuhi kepentingan public/pelayanan public bukan memaksimalkan

keuntungan.

merespon kebutuhan sosial ekonomi.

Ex: Bank Pembangunan Filipina 1958

Agricultural Banking

Development Financial Institution (DFIs) yang ditunjuk atau dimandatkan oleh

pemerintah untuk memberikan pinjaman/pendanaan sektor pertanian guna

mendukung ketahanan pangan nasional.

Tingkat suku bunga yang lebih rendah

Customer relationship: diskon suku bunga/special rate untuk retention lending &

technical assistance

Revenue: bunga, subsidi pemerintah

Ex: Bank for Agriculture and Agricultural Cooperatives (BAAC) di Thailand

(support by Bank Sentral Bank Of Thailand) dan Agriculture Bank of Iran

Cooperative Banking

muncul dengan latar belakang terjadinya krisis yang menimpa bank di berbagai

negara dengan tagline Bigger is not always better terutama dalam soal biaya

model bisnis bank ini memanfaatkan konsep economies of scale

beroperasi berdasarkan prinsip koperasi (kekeluargaan dan kegotongroyongan)

ada anggota dengan simpanan dan iuran anggota (local residents dan small and

medium-sized enterprises (SME)

skema kredit mudah dan sederhana

penghimpunan & penyaluran dana dari & ke anggotanya dan non anggota untuk

keperluan bisnis dan konsumsi serta menyediakan jasa-jasa: leasing, factoring,

insurance & investment funds.

Ex: Rabo bank-Belanda Jumlah anggota:1,9 juta jiwa di seluruh

Belanda,sedangkan jumlah SDM yang saat ini 59,670 orang.

Islamic Cooperative Bank of Malaysia ( ICBM)y ang didirikan oleh Angkatan

Koperasi Kebangsaan Malaysia (Angkasa) asosiasi/perkumpulan koperasi di

seluruh Malaysia dengan anggota 560 koperasi kredit dan 4 juta anggota serta

beberapa asosiasi koperasi non profit seperti koperasi pertanian, pada tanggal

27 November 2010 dengan modal awal/minimum paid in capital (modal disetor)

sebesar RM 300 juta/US$ 97 juta.

Social/ethical Banking

bank yang beroperasi untuk tujuan sosial dan atau lingkungan dari proyek-

proyek yang dibiayai.

menonjolkan prinsip-prinsip transparasi, keadilan, konsumerisme etis memiliki

tata nilai (code) yang komprehensif.

Ex: Islamic Banking

Customer segment: korporasi/perusahaan yg tidak memiliki reputasi negatif

terkait efek lingkungan yang ditimbulkan oleh usahanya.

financial Inclusion, meningkatkan taraf hidup masyarakat miskin karena

kemampuannya untuk menjangkau masyarakat yang unbankable, skema kredit

yang mudah/simple serta bunga rendah. seperti yang dilakukan oleh Grameen

bank di Bangladesh.

cust relationship: personal touch, technical assistance

Revenu: intangible brand image bank peduli thd social problem

Green Banking

Bank bekerjasama dengan multistakeholder pemerintah, LSM, International

Financial Institution (IFI)/International Government Organization (IGOs),Bank

Sentral, komunitas nasabah dan komunitas bisnis untuk mencapai tujuan-tujuan

green banking, meliputi manajemen lingkungan internal, pembiayaan

lingkungan/produk ekologi,pengungkapan/audit lingkungan dan pelaporannya,

merumuskan dan mengadopsi prinsip-prinsip green banking dan

mempromosikannya pemangku kepentingan lainnya

environmental-friendly: e-banking paperless, online system utk paying bills,

opening up CDs dan money market accounts

Cust: perusahaan yang memiliki sertifikasi ramah lingkungan dalam operasional

bisnisnya, ex: First Green Bank, Florida Amerika Serikat membiayai perusahaan

yang memiliki sertifikasi Leadership in Energy and Environmental Design

(LEED) seperti sertifikasi (AMDAL)

Cust relation: personal touch, technical assistance

Ex: Bank of Eustis, Florida feb 2009 bank pertama yang mendorong

dampak positif bagi lingkungan dan tanggungjawab sosial sementara bank tetap

beroperasi dalam fungsi tradisional bank dengan layanan execellent bagi

investor dan nasabah

Subsidiary Banking

Bank anak dari bank besar di luar negeri, untuk ekspansi bisnis & menjangkau

nasabah di luar negeri

Follow the regulation from host country, kalo branch banking follow regulation

from the origin country

Tdk dipengaruhi jumlah aset bank induk, sdgkan branch banking dipengaruhi shg

bisa menyalurkan lebih banyak

Cust relation: personal touch, special rate, special pricing

Window Banking

usaha yang dilakukan oleh bank komerasial untuk melakukan penetrasi pasar

dengan memberikan layanan perbankan dan keuangan kepada nasabah yang

tidak bisa dilayani oleh operasional bank komersial yang ada sekarang misalnya

terbentur oleh peraturan dan prinsip-prinsip yang dianut oleh nasabah.

Ex: UUS oleh BU untuk melayani produk syariah

Linkage Banking

Linkage dari bank komersial untuk dapat memberikan layanan keuangan

kepada neglected section of the population (poor dan unbankanble) melalui

Microfinance Institution (MFIs) dan Rural Saving and Credit Cooperatives

(RUSACCOs) untuk mencapai target MDGs.

Mereka unbankable karena tidak memenuhi persyaratan seperti

jaminan/collateral, credit rationing, preferensi mereka terhadap nasabah

berpenghasilan tinggi dan meminjam dalam jumlah besar, prosedur birokrasi dan

lamanya prosedur dalam pencairan pinjaman.

Branchless Banking

konsep penyediaan layanan perbankan di luar bentuk konvensional bank pada

umumnya baik dengan menggunakan layanan ICT maupun melalui keterlibatan

pihak ketiga Business Correspondents.

Ex: Easypaisa di Pakistan, EKO di India, Vodaphone M-Pesa di Tanzania.

Desember 2008, operator terbesar kedua Pakistan, Telenor (22% market share)

membeli 51% saham Tameer Microfinance Bank. Kedua institusi tersebut

membentuk joint venture untuk dan mendirikan branchless bank easypaisa.

Easypaisa menawarkan baik Over The Counter (OTC) bill payment dan layanan

transfer uang sebaik mobile wallet dimana nasabah dapat melakukan berbagai

macam transaksi termasuk deposit, transfer, bill payment, airtime top-ups dan

penarikan. Telenor meng-handle kampanye marketing dari easy paisa. Pertama

yang dilakukan,EasyPaisaTC menggunakan tool umum untuk membangun

brand dilengkapi dengan fungsional adevertising yang menerangkan tentang

produk.

International Banking

Rapid growth

Growth in international trade and multinational corporations

Global investment banking is very profitable

Ability to tap into the Eurodollar market

Reason the growth of international bank

1. The general relaxation of controls on international capital movements permit

banks to engage in overseas business.

2. Banks seek to maximize profits, so it is quite natural for them to seek

additional profit opportunities through dealing in foreign currency deposits and

overseas transactions.

3. Some banks may themselves have superior techniques, so that expansion in

multinational business offers them the chance to exploit their comparative

advantage in other countries. oversea sacquisitions, increasing their

competitive edge in domestic markets.

4. Banks desire to follow their clients, so that if important clients have overseas

business the banks will also engage in such business. by establishing its own

overseas operations, a bank may be able to monitor more thoroughly the

overseas operations of clients.

5. long-run cost curve of banks is relatively flat and that economies of scale are

quite quickly eliminated. This reduces or eliminates the advantage of having one

large o/ce as against dispersed o/ces. This is reinforced by the relatively low

salaries accompanied by satisfactory levels of expertise in certain overseas

countries. The migration of banking services to Asia and India

6. Regulation. Basle agreements once a centre has attracted banking

facilities, they will tend to remain in that centre even after the initial bene¢t has

been eliminated because of the acquired advantages, such as expertise,

quali¢ed staff, etc.

7. Portfolio theory diversification leads to lower risk suggests that banks

should diversify their operations both as to currency type and geographical area.

Pertemuan 3 - Teori dan Perilaku Perusahaan Perbankan

The SCP hypothesis

the level of concentration in a banking market influences banks‘ conduct (bearing

on loan and deposit quantities, qualities, interest rates, and other market

outcomes) that determine consumer welfare.

greater concentration gives banks more market power, which in turn leads to

fewer loans and deposits and higher loan rates and lower deposit rates, all of

which reduce consumer welfare

cost conditions faced by banks play a crucial role in determining the optimal

scale of individual banking organizations and the appropriate scope of banking

activities.

Efficient-Structure Theory

costs efficiencies resulting from expansions of scale and/or scope expansions

in loans and deposits lower loan rates and higher deposit rates

regulators contemplating applications for new banking licenses or, proposed

bank mergers and acquisitions have focused considerable attention on a

perceived trade-off between resulting increases in market power vs cost-

efficiency gains.

The SCP Hypothesis with Identical Banks

suggests that a reduction in the number of loan and deposit-market

competitors—that is, a rise in concentration in bank loan and deposit markets—

generates imperfectly competitive conduct that results in higher market loan rates

and lower market deposit rates.

Loan and deposit quantities decline with greater concentration, which results in

decreases in consumer and producer surpluses obtained by banks‘ customers

and increases in deadweight losses.

Consequently, increased concentration ultimately results in poorer market

performance.

Structural Asymmetry, Dominant Banks, and the SCP Paradigm

symmetric market environment doesnt real

banks with differing costs compete side by side and operate at different scales

The identical-bank SCP hypothesis: dominant-bank model takes into the

potential for more cost-efficient, larger banks to engage in market rivalry with less

efficient.

A Dominant-Bank Model

Strategic Entry Deterrence / Barriers

If fringe entry costs are relatively low fundamental danger faced by bank i

one or more of its fringe rivals may, in the process of learning by doing,

discover how to replicate the technology that provides bank i with its

market edge.

Bank i might engage in strategies aimed at raising the costs of its potential

fringe rivals

bank i could utilize its existing technological edge to engage in predatory (or limit)

pricing.

bank i could set its loan rate just below rDL.

As long as this loan rate > ACL profit-maximizing quantity of loans

the expected discounted stream of profits under this entry-deterrence

strategy > the discounted profit stream from pursuing a loan-pricing policy

that permits entry (Rdl)

This strategy maximizes short-term profits at the expense of future

economic profits.

the SCP Paradigm to the Banking Industry

The SCP hypothesis suggests that

in more concentrated banking markets, ceteris paribus, observed industry

quantities of loans and deposits should be smaller.

In addition, market loan rates should be higher, and market deposit rates should

be lower.

These quantity and interest-rate adjustments, of course, imply higher industry

profits, reduced levels of consumer surplus received by borrowers in loan

markets, and lower accruals to depositors of producer surplus in deposit markets.

The Conduct and Relative Performances of Large and Small Banks

The dominant-bank model utilized by proponents of the SCP paradigm offers:

1. asymmetric competition cannot exist unless a dominant bank possesses a

technological edge over its fringe rivals.

dominant banks operating at lower costs than smaller rivals.

large banks tend to be more efficient than smaller competitors.

2. if entry costs faced by fringe banks are substantial, then the existence of a cost

advantage enables dominant banks to set their loan rate independently and experience

positive economic profits even when some fringe entry occurs.

If fringe entry cost low dominant bank must respond by expanding its

lending and reducing its loan rate markup

3. fringe banks that enter a dominant bank‘s loan market should charge the same loan

rate as dominant banks.

If fringe banks‘ loan rates > their ACL positive economic profits.

fringe bank‘s profitability < the profitability of dominant banks smaller

scale of lending and the higher AC faces by a fringe bank

4. dominant bank can prevent entry by fringe competitors by setting its loan rate lower

than the minimum LRAC of potential fringe entrants.

This reduces the dominant bank‘s short run profits

enable the bank to maintain the technological edge that it possesses over

potential entrants.

the bank might be able to maintain a steady stream of positive economic

profits over a longer horizon

Market Structure and Bank–Customer Relationships

Potential barriers to entry in banking:

leverage — assets capitalization—advantage

absolute cost advantage produce at lower cost/unit than other

product differentiation barrier

Customer relationship:

close and continued interaction

may provide a lender with sufficient information

overcome adverse selection problems by maintain relationships

with successful borrowers

Basic Market-Structure Implications of Bank–Customer Relationships

the bank will set a lower loan rate and higher deposit rate in the first period

reduces the bank‘s profits but enables it to attract more loans and deposits in the

first period, which through its customer relationships will, ceteris paribus,

generate higher loan demand and deposit supply in the second period.

in the second period, the bank can set a higher loan rate and a lower deposit,

thereby boosting its second-period profits bank–customer relationship.

the bank will be more willing to trade off fewer profits in the present for greater

profits in the future

Current profits of incumbents will be lower, reducing the incentive for entry to

occur and resulting in a more concentrated banking industry, ceteris paribus.

Evidence on Bank–Borrowers Relationships

banks develop reputations through implicit contracts.

Maintaining these contracts enables banks to acquire private information

about borrowers and thereby take advantage of captive customers in

order to earn rents

Impacts

reduce monitoring cost lower loan rates to customers with which banks

have close relationships

Evidence on Bank–Depositor Relationships

banks tend to offer higher deposit rates within areas and over times in which

there was greater market inmigration, presumably reflecting a greater incentive to

offer more appealing deposit rates in an effort to attract new depositors

In contrast, in areas and times in which there was greater out-migration,

consistent with the hypothesis that banks in such markets anticipate less durable

relationships, evidence of lower deposit rates.

Competition & relationship lending

Relationship lending as barrier to entry: access to inelastically supplied core

transaction and savings deposits that enable a bank to provide borrowers with

insurance against exogenous shocks.

the length of tenure of lending, Lower of loan rate

Loan rates increase with the duration of the bank‘s lending relationships.

Highly concentrated markets, less competition fosters relationship lending

Competition in lending because the absence of relationship lending

The Efficient Structure (ES) Theory

the basis for the ES: economies of scale and scope could have implications for

the relationship between bank market structure, conduct, and performance for

the existence of relatively large banking organizations.

contrast to the SCP hypothesis, the ES theory proposes that a consequence of

cost advantages due to scale or scope is lower.

higher profits observed at larger institutions would result from the efficiency

advantages they possess rather than from predatory conduct aimed at precluding

entry

the intensity of market competition and market concentration are not necessarily

negatively related

Banking Efficiency and Costs

Concentrated attention to new developments in financial IT improved technical

efficiency in banking.

cost efficiency improvements from technological change rather than changes in

output scale or convergence to an efficient production frontier.

main source of cost inefficiencies derived from failure to utilize the least-cost

production technology or the least-cost mix of inputs—X-inefficiencies—> gap

between efficient behave by theory with observed behave in practice

Others inefficiencies: organizational form, market characteristics, and regulation

ES Theory and Bank Performance

higher profits accrue to the more cost-efficient banks.

support of the SCP dominant-bank model‘s prediction that large banks are able

to boost their profits through exercise of market power as well as cost-efficiency

advantages

decreases in banks‘ costs lower market loan rates

more efficient banks grow and prosper at the expense of less efficient banks.

greater efficiency of larger banks allows them to act as dominant market

participants along lines of the SCP dominant-bank model but that observed

higher profits earned by the larger banks result from greater efficiency rather than

market power.

Pertemuan 4 - Credit Rationing and Securitization

The availability doctrine

The doctrine the price of credit was not the important determinant of credit but

the availability of credit.

Background the doctrine:

regulatory restrictions (BMPK),

usury laws (regulations governing the amount of interest that can be

charged on loan)

asset management methods

weak relationship between the r and the ADL

Government and central banks were able to effectively control the flow of

credit through OMO at the prevailing rate of interest.

When OMO, Bank do asset mgt Gov‘t bond over, private loan under

tightening or loosening of monetary policy by OMO increased or

decreased gov‘t bond increase or decrease in bank lending to the

private sector.

microeconomic perspective of the doctrine the role of non price factors in the

determination of a loan contract.

Theories of credit rationing

expected profit for the bank increases as the rate of interest rises, because 2

effects of rising rate of interest

1. expected revenue increases because of the increase in price (assuming

loan demand is interest-inelastic r rise, Loan decrease insignificant)

2. a fall in expected revenue as the risk of default increases.

1>2 total expected revenue/profits will incline.

theory of endogenous credit rationing Hodgman (1960)

The bank‘s risk of loss (risk of default) is positively related to loan exposure

Components bank‘s expected return:

minimum return in the event of default

in the absence of default, the full return given by the loan rate less the cost

of raising deposits on the money market.

For very small loans the probability of default is virtually zero.

As the loan size increases after a certain point the probability of default

rises so that the profit on the loan starts to decrease such that the loan

offer curve bends backwards.

ASYMMETRIC INFORMATION AND ADVERSE SELECTION

Elements of endogenous rationing models:

Asymmetric information the possibility that both sides to the transaction

do not possess the same amount/quality of info.

the borrower have more information about the project than the

bank.

Adverse selection When the bank may select the wrong candidate, in

the sense of the person more likely to default out of a series of loan

applications.

Adverse incentives When the contracted interest rate creates an

incentive for the borrower to take on greater risk than they otherwise

would, so that the higher interest rate can be paid.

Moral hazard A situation when one of the parties to an agreement has

an incentive to behave in a way that brings benefits to them but at the

expense of the counterparty.

ADVERSE INCENTIVE

The negative effect of interest rate:

the interest rate charged affects the riskiness of the loan, which is the

adverse selection effect.

the higher the rate of interest charged, the greater the incentive to take on

riskier projects, which is the adverse incentive effect.

SCREENING vs RATIONING

Type of borrowers:

Honest borrowers will not borrow if they cannot repay,

dishonest borrowers will borrow knowing they would not repay.

Screening them with: collateral & interest rate

National Economic Research Associates (1990) shows that collateral is a

good signal/the riskiness of project success

The default rate for borrowers who had not offerred collateral was 40%

compared with 14% for those who had.

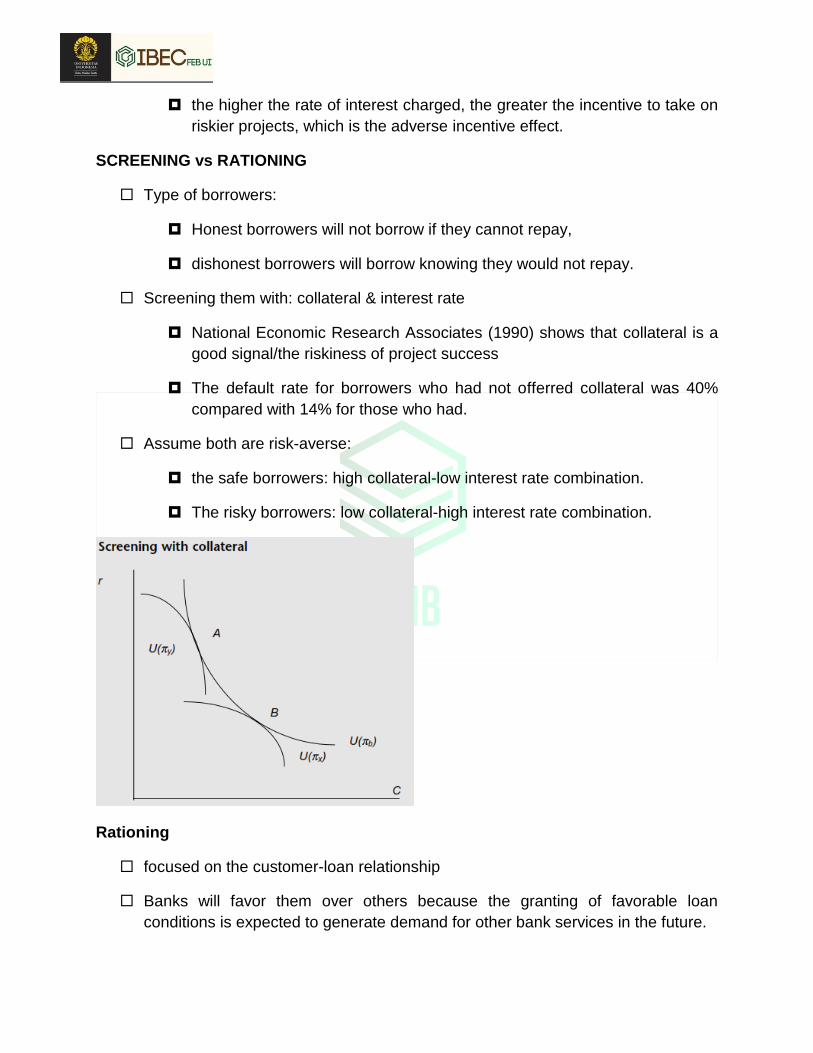

Assume both are risk-averse:

the safe borrowers: high collateral-low interest rate combination.

The risky borrowers: low collateral-high interest rate combination.

Rationing

focused on the customer-loan relationship

Banks will favor them over others because the granting of favorable loan

conditions is expected to generate demand for other bank services in the future.

Overcome Principal-agent problem with equilibrium risk-sharing arrangement by

offerring fixed rate (or slowly adjusting) rates than spot market rates.

SECURITIZATION

as the process of ‗matching up of borrowers and savers wholly or partly by way

of financial markets:

(i) the issuing of financial securities by firms as opposed to raising loans;

(ii) deposits organized via the banking system; and

(iii) asset-backed securities -i.e., sales of financial securities- which are

themselves backed by financial securities.

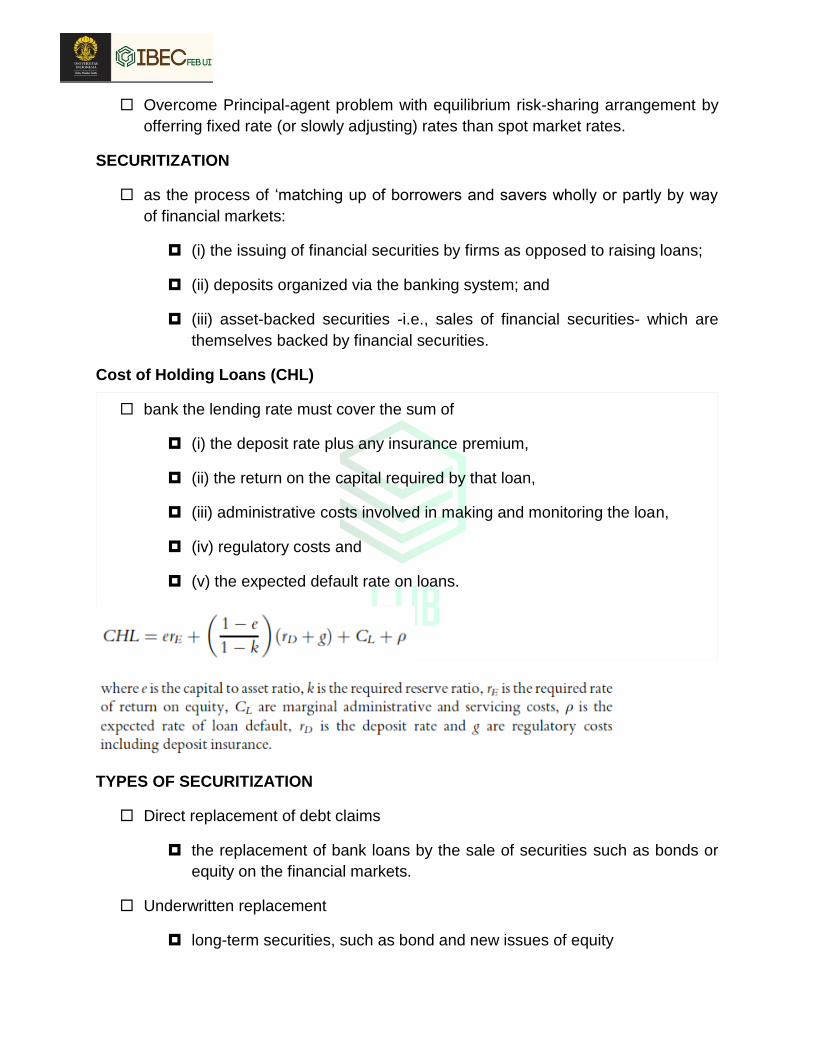

Cost of Holding Loans (CHL)

bank the lending rate must cover the sum of

(i) the deposit rate plus any insurance premium,

(ii) the return on the capital required by that loan,

(iii) administrative costs involved in making and monitoring the loan,

(iv) regulatory costs and

(v) the expected default rate on loans.

TYPES OF SECURITIZATION

Direct replacement of debt claims

the replacement of bank loans by the sale of securities such as bonds or

equity on the financial markets.

Underwritten replacement

long-term securities, such as bond and new issues of equity

deposit replacement

Certificates of Deposit (CDs)

Retail savers tend to hold claims on banks in the form of deposits and

institutional savers in a wide range of bank claims including subordinated

debt and equity as well as deposits.

ASSET BACKED SECURITIZATION (ABS)

a process whereby illiquid assets are pooled together and sold off to investors as

a composite financial security which includes the future cash proceeds.

Sold by banks financial institutions and private individuals

include Collateralized Debt Obligations (CDOs):

Collateralized Loan Obligations (CLOs)

Collateralized Bond Obligations (CBOs);

credit card obligations;

auto loans;

consumer loans;

mortgages.

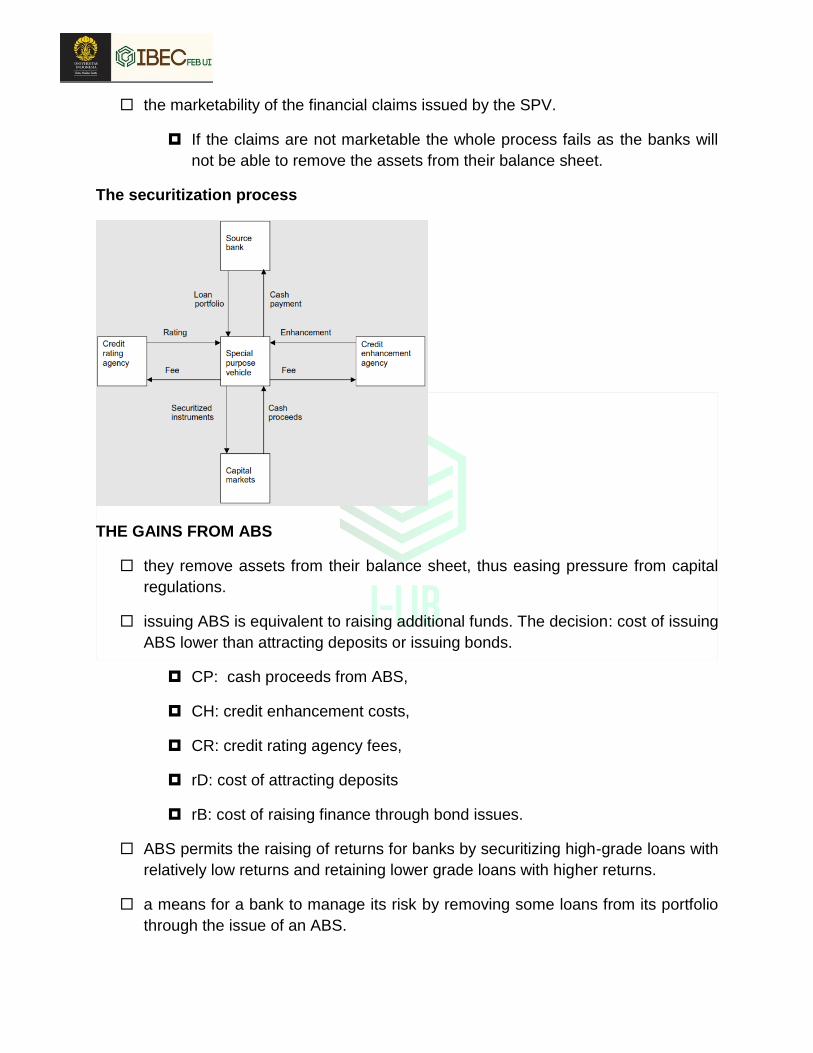

THE PROCESS OF ABS

forming by the originator

A special entity is set up specifically for the transaction Special Purpose

Vehicle (SPV), or Special Purpose Entity (SPE) or, if the special entity is a

company, a Special Purpose Company (SPC).

This entity is completely separate from the bank and is set up with capital

provided by the loan originator, though the SPV may raise capital on its

own behalf.

The SPV then buys the ABS tranche from the originator and then sells securities

(typically Floating Rate Notes/FRNs) to finance the purchase of the securities,

which it holds in trust on their behalf.

These securities receive credit enhancement in the form of a guarantee from a

bank (this may be the originator) or insurance company.

the marketability of the financial claims issued by the SPV.

If the claims are not marketable the whole process fails as the banks will

not be able to remove the assets from their balance sheet.

The securitization process

THE GAINS FROM ABS

they remove assets from their balance sheet, thus easing pressure from capital

regulations.

issuing ABS is equivalent to raising additional funds. The decision: cost of issuing

ABS lower than attracting deposits or issuing bonds.

CP: cash proceeds from ABS,

CH: credit enhancement costs,

CR: credit rating agency fees,

rD: cost of attracting deposits

rB: cost of raising finance through bond issues.

ABS permits the raising of returns for banks by securitizing high-grade loans with

relatively low returns and retaining lower grade loans with higher returns.

a means for a bank to manage its risk by removing some loans from its portfolio

through the issue of an ABS.

Dis/Advantages

the possible requirement of the borrower‘s permission

the relationship between the bank and the customer may be damaged by

the transfer of the loan

the costs incurred in the time and expenses involved in designing the issues

unattractive for banks with low funding costs.

the process of ABS connects the financial markets with the capital market

reduce agency and intermediary costs by providing investors with a wider

range of securities and enabling cheaper raising of funds.

Credit facilities have been increased.

This is beneficial during periods of faster growth of an economy

could lead to increased financial distress once a downturn occurs.

the volatility of the economy may have been increased.

Pertemuan 5- Struktur Perbankan

Structure-Conduct-Performance

(market) structure interaction D & S

Conduct number of competing firms and customers, and barriers to entry

performance/output combination of these two factors

MEASUREMENT OF OUTPUT

Output of bank? Difficult to measure

Ex: ATM improve quality of services

2 sides of ATM: operating cost reduction per transaction but rise in total costs if

the number of withdrawals increases

2 sides of closure of branches increased costs and inconvenience for

customers but lower costs for the banks.

measuring output: intermediation methods

the bank as an intermediary

output = the value of loans and investments + off-balance-sheet income +

payments made to factors of production (interest)

deposits may be treated as inputs or outputs

point of view of bank managers, deposits are inputs essential to obtain

profits through the purchase of earning assets such as loans and

investments.

point of view of the customer, are outputs since they create value for the

customer in the form of payment, record-keeping and security facilities.

focus on income with net interest income and noninterest income being declined

as output with the corresponding expenses declined as input.

measuring output: production methods

regard banks as firms that use factors of production (labour and capital) to

produce different categories of loans and deposit accounts.

The number of transactions, either in total or per account, are treated as a flow.

One problem interest costs are ignored.

Merger & Akuisisi (PP No. 28/99)

Merger penggabungan dari 2 (dua) Bank/lebih, dengan cara tetap

mempertahankan berdirinya salah satu Bank dan membubarkan Bank-bank

lainnya tanpa melikuidasi terlebih dahulu;

Lippo-Niaga CIMB-Niaga

Konsolidasi penggabungan dari 2 (dua) Bank atau lebih, dengan cara

mendirikan Bank baru dan membubarkan Bank-bank tersebut tanpa melikuidasi

terlebih dahulu;

BBD, Bank Bapindo, Bank Dagang Negara, Bank Exim Bank Mandiri.

Akuisisi pengambilalihan (take-over) kepemilikan suatu Bank yang

mengakibatkan beralihnya pengendalian terhadap Bank;

Bank Agroniaga diakuisisi BRI

REASONS FOR THE GROWTH OF MERGERS AND ACQUISITIONS

(i) increased technical progress,

increased the scope for economies of scale.

Ex: use of IT & fonancial innovation derivative contracts and off-

balance-sheet business, ATMs and online banking

increasing competition from other FIs.

(ii) improvements in financial conditions increase profitability extra funds to

finance acquisitions.

(iii) excess capacity because there are competition from Fis incentive to

rationalize via mergers

Financing from capital market n nonbank, saving from investment trust

(iv) international consolidation of financial markets increased globalization of

financial services

(v) enhance shareholder value

(vi) deregulation

PP No 28/1999 merger, konsolidasi dan akuisisi

Landasan Hukum Merger antar Bank Umum di Indonesia

UU No. 7 Th. 1992 tentang Perbankan jo UU No. 10 Th. 1998

UU No. 21 Th. 2008 tentang Perbankan Syariah

PP No. 28 Th. 1999 tentang Merger, Konsolidasi dan Akuisisi Bank

PP No. 29 Tahun 1999 tanggal 7 Mei 1999 tentang Pembelian Saham Bank

Umum.

SK Direksi BI No.32/50/KEP/DIR tgl.14 Mei 1999 tentang Persyaratan & Tata

Cara Merger Pembelian Saham Bank Umum

SK Direksi BI No.32/51/KEP/DIR tgl.14 Mei 1999 tentang Persyaratan & Tata

Cara Merger, Konsolidasi & Akuisisi Bank Umum

SK Direksi BI No.32/52/KEP/DIR tgl.14 Mei 1999 tentang Persyaratan & Tata

Cara Merger, Konsolidasi & Akuisisi Bank Perkreditan Rakyat

PBI No.2/27/PBI/2000 tanggal 15 Desember 2000 tentang Bank Umum.

SK Dir BI No. 32/34/KEP/DIR tgl 12 Mei 1999 tentang Bank Umum Syariah.

SK Dir BI No. 32/35/KEP/DIR tanggal 12 Mei 1999 tentang BPR;

SK Dir BI No. 32/36/KEP/DIR tanggal 12 Mei 1999 tentang BPR Syariah

Prioritas pembagian Aset Bersih hasil Likuidasi

1. Pajak (Pasal 21 : 7 UU No. 9/1994 tentang Pajak Penghasilan)

2. Upah buruh (pasal 110 UU No. 25/1997 tentang Perburuhan)

3. Biaya perkara sebagaimana diatur dalam Pasal 1139 butir 1 dan Pasal 1149

butir 1 Kitab Undang-Undang Hukum Perdata

4. Pemegang Hak Tanggungan dan Gadai

5. Para Berpiutang yang diistimewakan sebagaimana yang tercantum dalam

Pasal 1139 dan Pasal 1149 Kitab Undang-Undang Hukum Perdata (kecuali

yang disebutkan dalam butir 2 dan 3 di atas)

6. Para kreditur yang tidak memiliki jaminan.

ALASAN M & A

Pertumbuhan cepat atau diversifikasi usaha

•Mengurangi persaingan

Sinergi (esp dlm bisnis yg sama efisiensi labor)

•EOS OHC tetap, Income naik

Meningkatkan dana dgn low cost

•Joint with high liquidity firm Leverage naik, liabilities turun

Menambah ketrampilan manajemen atau teknologi

•Niaga with CIMB

Pertimbangan pajak

•Menutupi kerugian pajak

Meningkatkan likuiditas pemilik

•Big company more liquid than small one IPO, listing in capital mkt

Melindungi diri dari pengambilalihan

Dis / advantage M&A

Empirical Evidence M & A in the banking industry, based on 5 different types of

analysis

+ low cost

- Take time to get agreement from stock holder

Merger + no need RUPS

+ tender offer dgn stock holder tanpa persetujuan mgt/komisaris perusahaan

+ hostile takeover

- Cancel if majority stockholder dont agree (67%)

- Untuk akuisisi aset high legal cost balik nama

Akuisisi

saham

The analysis to evaluate M&A

static studies do not consider the behaviour of the merged firms before and

after the merger

production functions,

cost functions,

the efficient frontier

approach

dynamic studiesconsider the behaviour of the firms before & after the merger

use of accounting

data,

event studies

PRODUCTION FUNCTION APPROACH

output as a function of inputs

Cobb-Douglas

Q = book value of commercial assets

L = labour input (number of full-time employees)

K1, K2 = fixed and liquid assets

Merger = years 1 to 5 after the merger

Problem = differ form of prod function different result

THE COST FUNCTION APPROACH

estimating a cost function for the banks and, then, examining how the cost

function behaves over time.

single output (Q) with two inputs (L and K), the translog cost function:

only assesses the efficacy of mergers by examining scope for economies of

scale banking firms grow larger through mergers

Question:

potential economies of scale (cost per output decreasing) ambiguous from

the point of view of cost studies.

the translog cost function is the best vehicle for analysing the behaviour of

costs?

THE ACCOUNTING APPROACH

• domestic mergers between equal-sized

partners increase the efficiency of the merged banks.

• Cross-border acquisitions slight but insigni¢cant improvement in

performance

another factor: defensive motives & managerial preferences.

use of key financial ratios ROA/ROE (net income before/after tax), loans/OHC

to total asset cash flows.

Others variable: bank size, the ratio of loans to assets, asset utilization

THE EFFICIENT FRONTIER APPROACH

Data Envelopment Analysis (DEA) by Charnes, Cooper, Rhodes (1978)

pengukuran efisiensi

teknik pemrograman matematis untuk mengevaluasi efisiensi relatif dari decision

making unit/DMUs dlmmengelola input menjadi output.

nonparametric approach:

Stochastic Frontier Analysis (SFA)

function for cost, profit or production so as to determine the frontier

and treats the residual as a composite error comprising Random

error & Inefficiency

Distribution Free Approach (DFA)

Inefficiency=Average residual of the individual firm -Average

residual for the firm on the frontier

8

ROE Breakdown

ROE

xROA EM

• Return on equity depends on

– Asset Utilization (AU)

– Profit Margin (PM)

– Equity Multiplier (EM)43

xAU PM x EM

ROE Breakdown Over Time

Variable 2010 2009 2008

ROE 8.02% 7.69% 7.52%

EM 7 71 7 18 6 71

44

EM 7.71 7.18 6.71

ROA 1.04% 1.07% 1.12%

AU 7.31% 7.33% 7.37%

PM 14.23% 14.60% 15.20%

ROE Breakdown Over Time

Variable 2010 2009 2008

ROE 8.02% 7.69% 7.52%

EM 7 71 7 18 6 71

45

EM 7.71 7.18 6.71

ROA 1.04% 1.07% 1.12%

AU 6.85% 7.00% 7.37%

PM 15.18% 15.29% 15.20%

ROA Breakdown Versus Peer Group

Case 1 Bank PG

ROA 1.04% 0.87%

AU 7.31% 5.73%

PM 14.23% 15.18%

46

Case 2 Bank PG

ROA 1.04% 0.87%

AU 7.31% 7.55%

PM 14.23% 11.52%

What are different implications?

Income Statement

Interest Income

- Interest Expense

Net Interest Income

Revenue − ExpenseNet Income =

Net Interest Income

- Provision for Loan Losses

+ Noninterest Income

- Noninterest Expense

+ Gains/Losses on Secs

Pretax Earnings

- Taxes

Net income

47

Asset Utilization

AU

48

Int Inc

TA

G/L

TA+ +

Non Int Inc

TA

Thick Frontier Approach (TFA)

A functional form is specified to determine the frontier based on the

performance of the best firms

Pertemuan 6 - Makroekonomi Perbankan

INTRODUCTION

domain of a central bank: the control of the macroeconomy through the operation

of monetary policy.

The modern central bank maintaining the value of the currency by maintaining a

low rate of inflation, stabilizing the macroeconomy (debt, r, trade balance) and

ensuring the stability of the financial system.

The conduct of monetary policy also has effects on the banking system itself in

its role of the provision of finance and the money supply.

the relationship between monetary policy is a two-way one with the banks

affecting the conduct of monetary policy and the conduct of monetary policy

affecting the banks.

THE ECONOMICS OF CENTRAL BANKING: A HISTORY..

oldest central banks: Bank of England (1694)

as a joint stock company following a loan of 12m pounds by a syndicate of

wealthy individuals to the government of King William and Queen Mary

1688-1815 Britain need funding war by issue bank notes

A rise in gold prices at the beginning of the 19th century sparked a debate about

the role of the Bank

two schools of thought the role of Bank to stabilization currency

The Currency School

precursor of modern-day monetarists

stabilization of the value of the currency can only be ensured by strictly

linking note issue to the Bank‘s gold deposits

The Banking School

precursor of the Keynesian-Radcliffe view

Currency stability depended on all of the Bank‘s liabilities and not just its

gold deposits.

The 1844 Bank Charter Act: split the Bank into

The issue department

Role: to ensure convertibility by backing currency issue by gold

The banking department

Normal commercial bank

The Act also gave the Bank of England de facto monopoly of the note issuethe

Bank of England became the bank to the banks lender of last resort to the

banking system.

The Bank of England Act of 1946

Bank become public ownership

important issue under the Bretton Woods System.

dual goal:

assisting the target of full employment

maintaining the exchange rate to the US dollar by imposing quantitative

controls on bank lending.

i naik/turun Loan turun/naik MS turun/naik ER

apresiasi/depresiasi

system of fixed exchange rates broke down in the early 1970s, the Bank was

pushed into an even closer relationship with the government.

The Bank of England Act of 1998

gave the Bank operational independence in meeting the inflation targets set by

the government.

upper bound of 2.5% and a lower bound of 1%.

MONETARY POLICY

the central bank controls the supply of base money

central banks can alter the required reserve ratio to control bank lending and the

money supply

Required reserve ratio rise CB creates a shortage of reserves for the banking

system banks raise interest rates to reduce loan demand.

CB use the discount rate to control MS

discount rate is the rate of interest at which the central bank is willing to

lend reserves to the commercial banks

The CB exercises control on the banking system by exploiting the scarcity of

reserves

One simple way for the commercial banks to meet their liquidity needs is

to run down any excess reserves they hold.

CENTRAL BANK INDEPENDENCE

argument: monetary policy is cushioned from political interference and is

removed from the temptation to cheat on a low-inflation environment by

engineering some unexpected inflation prior to an election.

An independent central bank gives credibility to an announced monetary policy

that underpins low inflation.

Goal independence CB sets the goals of monetary policy.

Operational independence CB that has freedom to achieve the ends which are

themselves set by the government.

WHAT TYPE OF CENTRAL BANK?

The theory of central banking the central bank should have policy aims - i.e.,

an objective function- that includes output stabilization, but gives output stability a

lower weight than what the government would wish and inflation a higher weight

than what the government would want.

Therefore, the central bank should be conservative in the sense that it places a

high priority on low inflation, but not completely to the detriment of output

output down

FINANCIAL INNOVATION AND MONETARY POLICY

financial innovation weaken the effectiveness of monetary policy

switch from asset management to liability management the

development of interest-bearing sight deposits.

the conventional money demand function with the development of interest-

bearing sight deposits:

substitution between money and nonmoney liquid assets will depend on

the margin between the interest on nonmoney liquid assets and deposits

FINANCIAL INNOVATION AND MONETARY POLICY

Interest rates risebanks will also raise interest rates on deposits the rate of

interest on liquid assets will have to rise even more to generate a unit substitution

from money to nonmoney liquid assets.

The implication for monetary policy

The relationship between income and money is changed.

Control of the MS becomes difficult for CB if banks compete with

the government for savings, so that banks will raise interest rates

on deposits in response to a general rise in interest rates caused by

a rise in the CB rate of interest.

The reduction in the response of MD to a change in the rate of

interest on nonmoney liquid assets can be thought of as a fall in the

interest elasticity of MD

Financial-innovation-induced fall in the interest elasticity of demand for money

Poole (1970) an economy that is dominated by IS shocks should target the

money supply and an economy dominated by monetary shocks should target the

rate of interest.

also explain why central banks have gradually moved away from monetary

targets to inflation targets using the rate of interest as the primary instrument of

control.

Conclusion

The Bank for International Settlements report on Financial Innovation (BIS, 1985)

as a result of financial innovation:

the money supply would be an unreliable guide to monetary conditions.

the effectiveness of the rate of interest as the instrument of monetary

policy is greatly increased.

INFLATION TARGETING

Combined with a higher frequency of monetary shocks than real shocks, central

banks have abandoned monetary targets and adopted inflation targets

monetary policy can do to support long-term growth of the economy is to

maintain price stability

using the central bank rate of interest as short-term monetary instrument

raising interest rates usually cools the economy to reign in inflation; lowering

interest rates usually accelerates the economy, thereby boosting inflation.

BANK CREDIT AND THE TRANSMISSION MECHANISM

monetary transmission mechanism separates the effect of monetary policy on the

economy into an indirect route and a direct route.

The direct route: the direct effect of money on spending, through:

the real balance effect of Patinkin (1965): determinants of consumption by

the real value of money (i.e., real balance)

the wealth effect of Pigou (1947): real value of money+weatlh

MS increase (in excess of the level demanded), as implied by some

equilibrium level of real balances, generates an increase in

spending

The indirect route through the effect of interest rates and asset prices on the

real economy.

A fall in the rate of interest (both real and nominal) and/or an increase in

asset price inflation results in a fall in the cost of capital (Tobin‘s q) and an

increase in investment and consumer durables spending (including real

estate purchases)

asset price inflation: rise in price financial asset such as bonds,

shares, derivatives

further transmission effect of monetary policy

Comes from the ‗expectations effect‘ rational expectations make choices

based on rational outlook, available info, past experiences

An anticipated tightening of monetary policy (r naik / MS turun) faster ultimate

effects on the economy than an unanticipated tightening of monetary policy

r riseincrease of borrowing reduce its attractivenes

The real effects are weaker in the case of an anticipated change in monetary

policy than an unanticipated one.

credit channel

alternative to the orthodox transmission mechanism

is a mechanism for enhancing and amplifying (memperkuat) the effects of the

textbook monetary channel.

The credit channel works by amplifying the effects of interest rate changes by

endogenous changes in the external finance premium.

The external finance premium is the gap between the cost of funds raised

externally (equity or debt) and the cost of funds raised internally (retained

earnings).

Changes in monetary policy change the external finance premium. It works

through two channels:

1. The balance sheet channel.

2. Bank lending channel.

The balance sheet channel

based on the notion that the external finance premium facing a borrower should

depend on the borrower‘s net worth (liquid assets less short-term liabilities).

In the face of asymmetric information, the supply of capital is sensitive to shocks

that have persistence on output.

Bernanke and Gertler (1989) show that the net worth of entrepreneurs is an

important factor in the transmission mechanism.

A strong financial position translates to higher net worth and enables a borrower

to reduce dependence on the lender.

A borrower is more able to meet collateral requirements and or self-finance

The bank lending channel

recognizes that monetary policy also alters the supply of bank credit.

If bank credit supply is withdrawn, medium or small businesses incur costs in

trying to find new lenders

Thus shutting of bank credit increases the external finance premium.

The implication of the two channels

the availability of credit or otherwise has short-term real effects.

For example, a negative monetary shock to the economy can reduce the net

worth of businesses and reduce corporate spending, shifting the IS curve to the

left.

In the context of the macroeconomic IS=LM model, Bernanke and Blinder (1988)

argue that negative shocks to net worth caused by adverse monetary shocks

cause reinforcing shifts in the IS curve.

Blinder (1987) suggests that this also causes additional constraints on supply,

which leads to a reinforcing contraction in aggregate supply.

the effect of a positive monetary shock in the credit channel framework

A positive monetary shock (a relaxation in monetary policy) results in a strengthening of

corporate balance sheets which causes a reinforcing rightward shift of the IS curve.

Pertemuan 7 - Analisis Ekonomi Regulasi Perbankan

a “need” for bank regulation

the justification for any regulation usually stems from a market failure such as

externalities, market power, or asymmetry of information between buyers and

sellers.‖

―in the case of banking, there is still no consensus on whether banks need to be

regulated‖

Regulation need if banking failure has a large impact incentives to take risks

are high, and the social cost of failure is high

the fundamental rationales behind regulation the potential instability of the

banking system and the need for consumer protection

So, the analysis the implication of regulation include public interest rationale

Public Choice Motivations for Bank Regulation, in a real world..

motivations for regulating firms nothing to do with aiming to correct market

failures.

Stigler (1971) ―capturing‖ regulatory officials who will have the power to protect

firms from competition from prospective new entrants.

Viscussi (2005) ―the key reason why normative analysis as positive theory has

lacked supporters...‖ because ―many industries have been regulated for which

there is no efficiency rationale‖ and ―in many cases, firms supported or even

lobbied for regulation.‖ ex: IIA

Viscusi et al. also contend that even a common reformulation of theory of

regulation purely in the public interest—that regulation initially is established to

correct a market failure but then often is mismanaged by the agency charged

with performing such regulation—still fails to square with the evidence.

Posner (1974), ―theoretical and empirical research...[has] demonstrated that

regulation is not positively correlated with the presence of external economies or

diseconomies or with monopolistic market structure.‖

Applying the Economic Theory of Regulation to the Banking Industry

A regulatory optimum

The preferences of the regulator depend on industry profits and on the loan rate.

Higher profits = healthier/more satisfied firms and positive utility to

the regulator.

A lower loan rate increased level of credit at better terms

(approval by consumers, non financial firms, DPR/pemerintah)

banking industry structure desire by regulator between the extremes of perfect

competition and monopoly

If equil at point near R*: little incentive to regulate

If equil at point near M: incentive to press for industry regulation because

R* closer their preference point C: lowest loan rate and the level of credit

greatest.

If equil at point near C: industry has incentive to lobby for regulation,

because R * is closer to banks‘ preferred, M

Assessing the Implications of the Economic Theory of Regulation

The economic theory of regulation:

once a bank regulatory regime is put into place, actual profit and loan rate

(and aggregate credit) outcomes will depend on the preferences of the

regulator (figure)

But based on some theories and a limited empirical evidence suggesting that

risks of banking failure may rise with increased competition, so regulator choose

panel b by assuring bank profitability that helps limit the scope for failures

It should be real evidence relationship between bank competition & risk

Differences in regulator preferences

U steep: regulator accept significant swings in bank profits in exchange for slight

changes in the loan rate regulatory optimum R* must be close to the competitive limit

public interest need

U flat: the regulator desires to maintain industry profits, wide variations in the loan rate

(and aggregate credit) regulatory optimum is nearer to the monopoly limit industry

wants

The Political Economy of Banking Supervision

Bank face problem: risky project, bank run, adverse selection, moral hazard

so poorly designed or improperly managed regulatory frameworks can

deliver social welfare losses even more

The public choice perspective on regulation of industry emphasizes that the

preferences of regulators are crucial in shaping the structure of an industry

supervisory regime

regulator‘s preferences influence its supervisory actions

Regulatory Preferences and Bank Closure Policies

Boot and Thakor (1993): a two-period game-theoretic model in which the private

payoff of the regulator depends on his monitoring reputation.

A regulator charged with monitoring and closing banks can either respond

to a sub-optimal first-period risk choice by requesting a better risk choice

the next period or closing the bank.

Result: equilibrium policy that emerges from this principal (society)-agent

(regulator) problem is socially sub-optimal, because imperfectly informed agents