PERSONAL AND CORPORATE TAXATION882fe31f29e7fd8c9ada-b447e7f1eed2117ba41e7c09f22d2c1c.r12.cf3... ·...

15

PERSONAL AND PERSONAL AND CORPORATE CORPORATE TAXATION TAXATION J. E. Triay J. E. Triay Triay & Triay Triay & Triay 28, Irish Town 28, Irish Town Gibraltar Gibraltar

Transcript of PERSONAL AND CORPORATE TAXATION882fe31f29e7fd8c9ada-b447e7f1eed2117ba41e7c09f22d2c1c.r12.cf3... ·...

PERSONAL AND PERSONAL AND

CORPORATE CORPORATE

TAXATIONTAXATION

J. E. TriayJ. E. TriayTriay & TriayTriay & Triay28, Irish Town28, Irish Town

GibraltarGibraltar

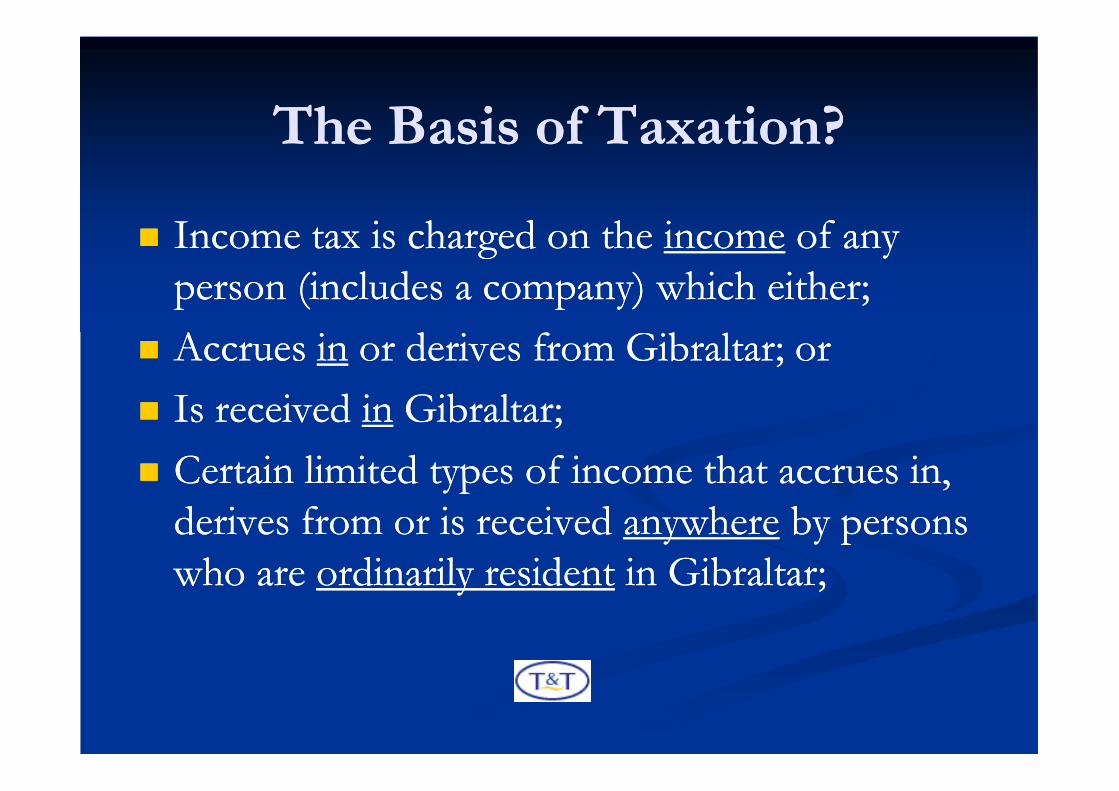

The Basis of Taxation?The Basis of Taxation?

�� Income tax is charged on the Income tax is charged on the incomeincome of any of any person (includes a company) which either;person (includes a company) which either;

�� Accrues Accrues inin or derives from Gibraltar; oror derives from Gibraltar; or

�� Is received Is received inin Gibraltar;Gibraltar;�� Is received Is received inin Gibraltar;Gibraltar;

�� Certain limited types of income that accrues in, Certain limited types of income that accrues in, derives from or is received derives from or is received anywhereanywhere by persons by persons who are who are ordinarily residentordinarily resident in Gibraltar;in Gibraltar;

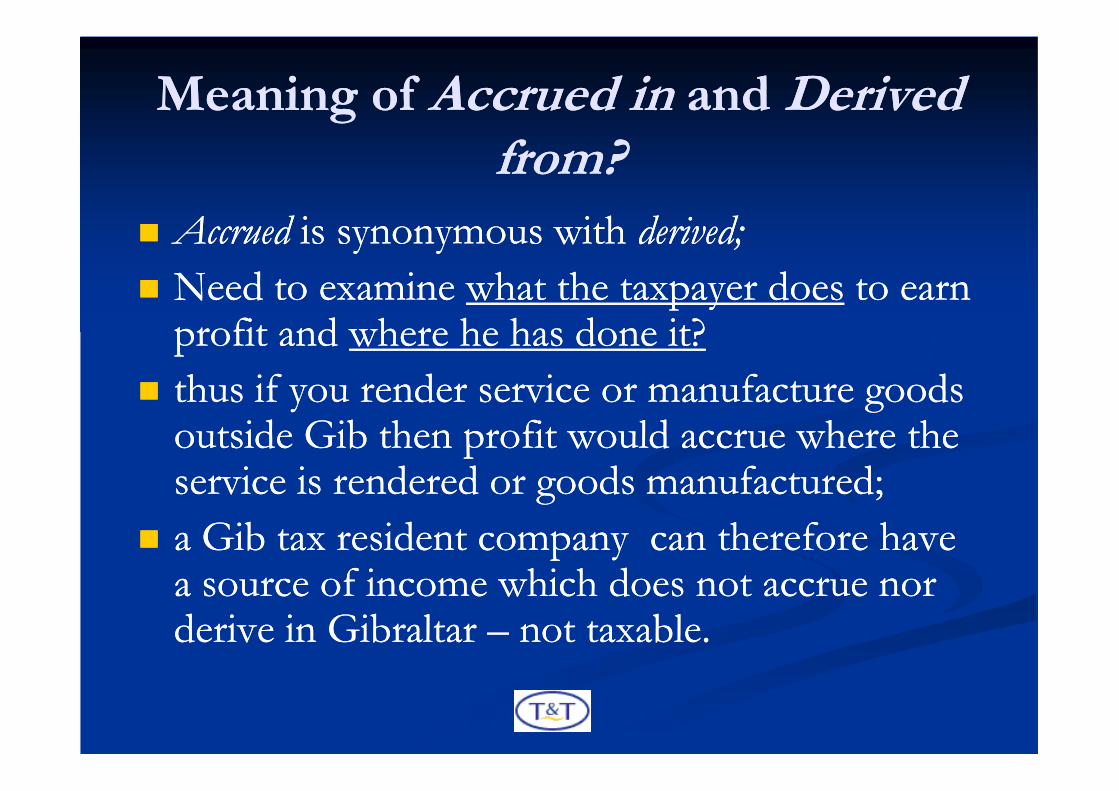

Meaning of Meaning of Accrued inAccrued in and and Derived Derived from?from?

�� AccruedAccrued is synonymous with is synonymous with derived;derived;

�� Need to examine Need to examine what the taxpayer doeswhat the taxpayer does to earn to earn profit and profit and where he has done it?where he has done it?

�� thus if you render service or manufacture goods thus if you render service or manufacture goods �� thus if you render service or manufacture goods thus if you render service or manufacture goods outside Gib then profit would accrue where the outside Gib then profit would accrue where the service is rendered or goods manufactured;service is rendered or goods manufactured;

�� a Gib tax resident company can therefore have a Gib tax resident company can therefore have a source of income which does not accrue nor a source of income which does not accrue nor derive in Gibraltar derive in Gibraltar –– not taxable.not taxable.

The Type of IncomeThe Type of Income

�� The Charge to income tax arises in respect;The Charge to income tax arises in respect;�� Gains or profits from any trade business, profession Gains or profits from any trade business, profession

or vocation;or vocation;

�� Gains or profits from employment including Gains or profits from employment including allowances perquisites or benefits in kind;allowances perquisites or benefits in kind;allowances perquisites or benefits in kind;allowances perquisites or benefits in kind;

�� Dividends, interest and discounts;Dividends, interest and discounts;

�� Any pension charge or annuity;Any pension charge or annuity;

�� Rents royalties, premiums and profits arising from Rents royalties, premiums and profits arising from property;property;

�� Income from occupation of property;Income from occupation of property;

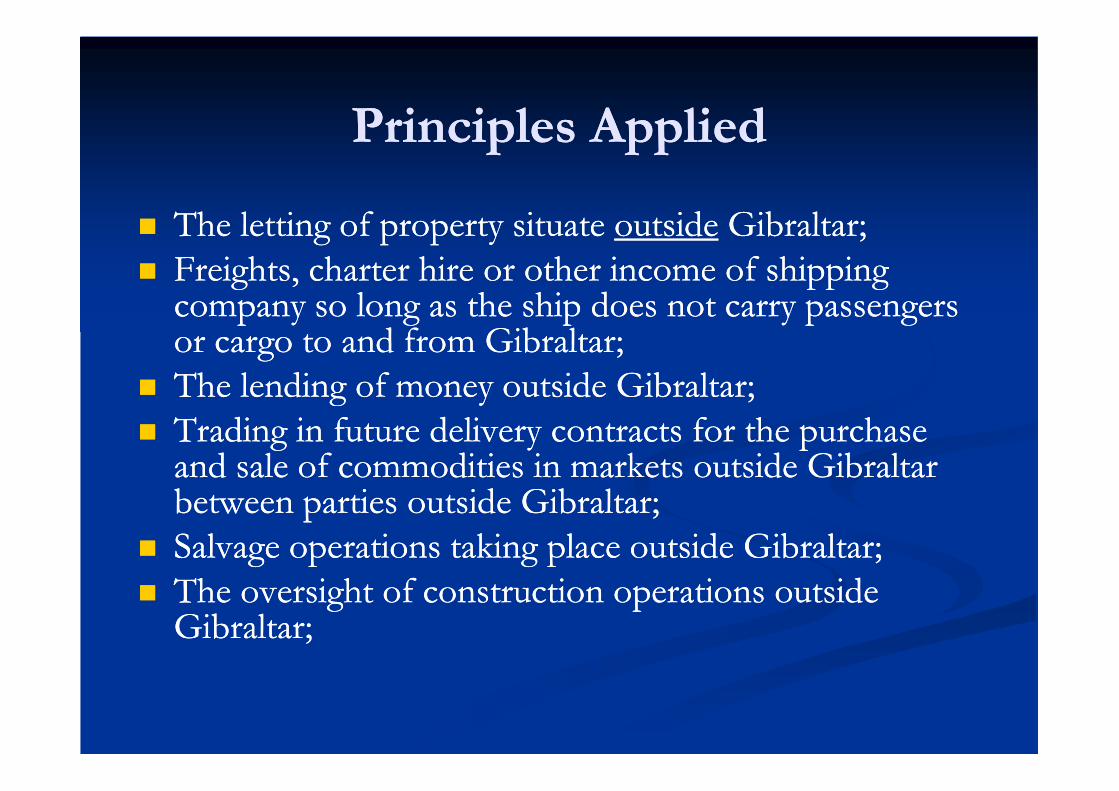

Principles AppliedPrinciples Applied

�� The letting of property situate The letting of property situate outsideoutside Gibraltar;Gibraltar;

�� Freights, charter hire or other income of shipping Freights, charter hire or other income of shipping company so long as the ship does not carry passengers company so long as the ship does not carry passengers or cargo to and from Gibraltar; or cargo to and from Gibraltar;

�� The lending of money outside Gibraltar;The lending of money outside Gibraltar;�� The lending of money outside Gibraltar;The lending of money outside Gibraltar;

�� Trading in future delivery contracts for the purchase Trading in future delivery contracts for the purchase and sale of commodities in markets outside Gibraltar and sale of commodities in markets outside Gibraltar between parties outside Gibraltar;between parties outside Gibraltar;

�� Salvage operations taking place outside Gibraltar;Salvage operations taking place outside Gibraltar;

�� The oversight of construction operations outside The oversight of construction operations outside Gibraltar; Gibraltar;

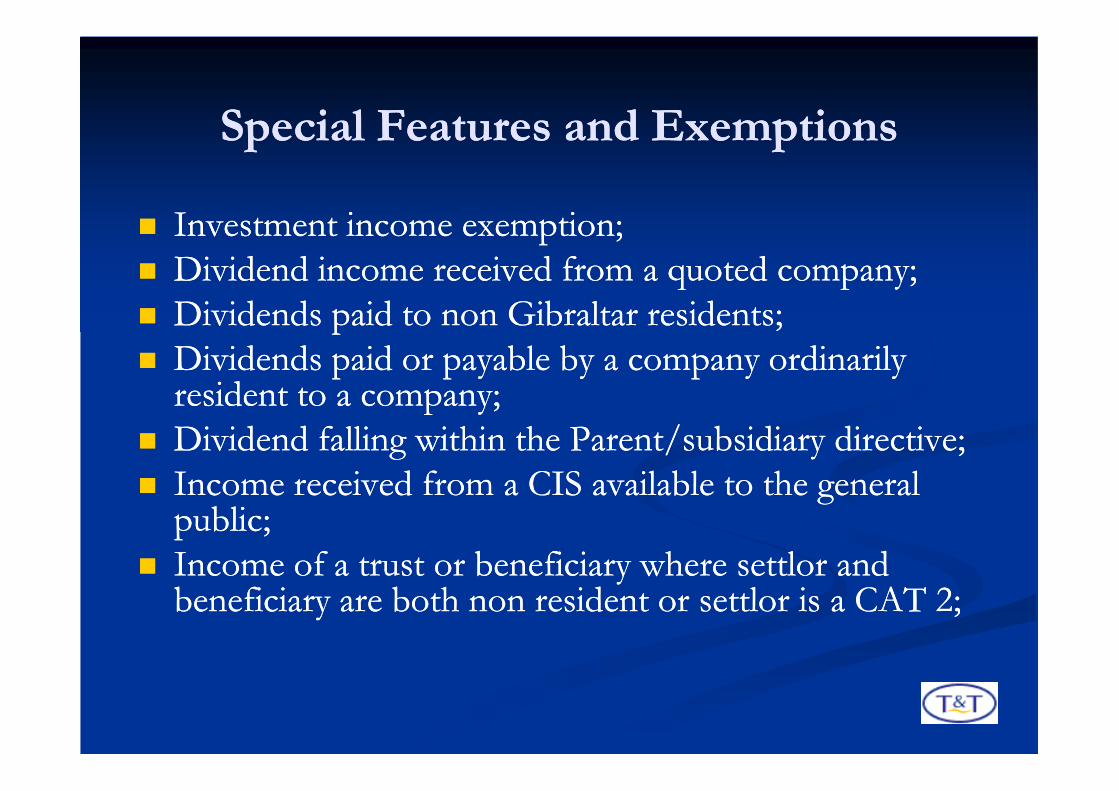

Special Features and ExemptionsSpecial Features and Exemptions

�� Investment income exemption;Investment income exemption;

�� Dividend income received from a quoted company;Dividend income received from a quoted company;

�� Dividends paid to non Gibraltar residents;Dividends paid to non Gibraltar residents;

�� Dividends paid or payable by a company ordinarily Dividends paid or payable by a company ordinarily resident to a company;resident to a company;resident to a company;resident to a company;

�� Dividend falling within the Parent/subsidiary directive;Dividend falling within the Parent/subsidiary directive;

�� Income received from a CIS available to the general Income received from a CIS available to the general public;public;

�� Income of a trust or beneficiary where settlor and Income of a trust or beneficiary where settlor and beneficiary are both non resident or settlor is a CAT 2;beneficiary are both non resident or settlor is a CAT 2;

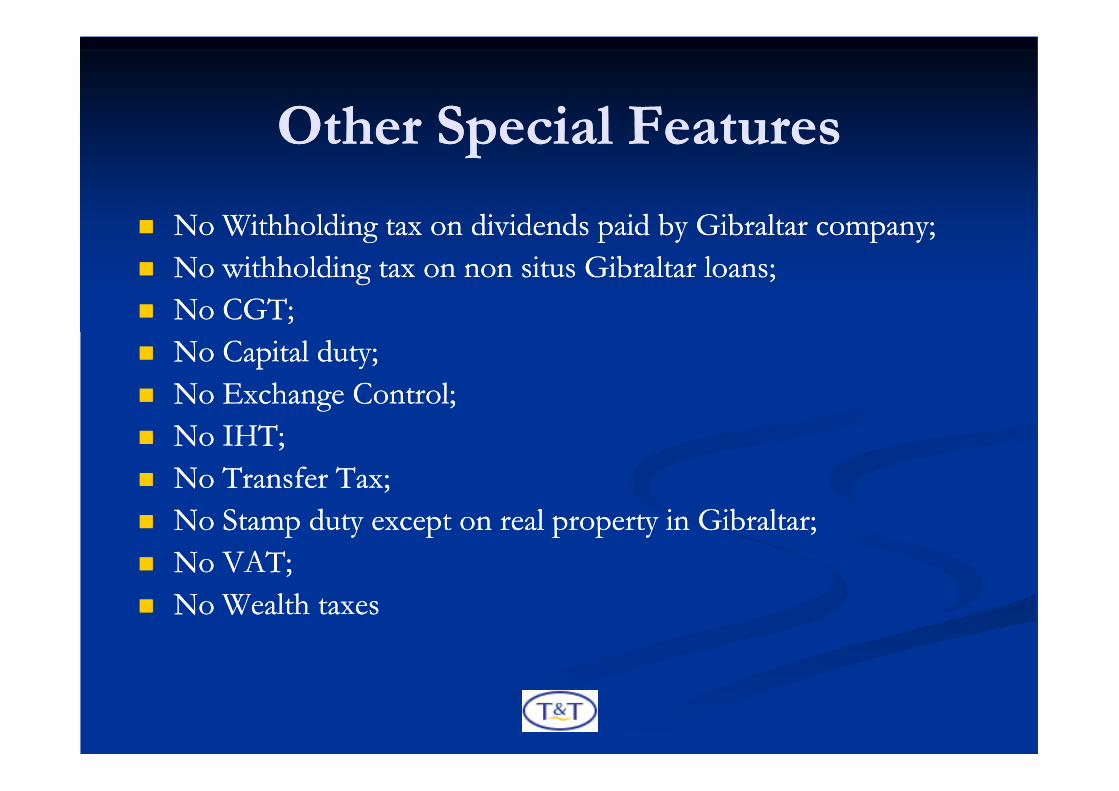

Other Special FeaturesOther Special Features

�� No Withholding tax on dividends paid by Gibraltar company;No Withholding tax on dividends paid by Gibraltar company;

�� No withholding tax on non situs Gibraltar loans;No withholding tax on non situs Gibraltar loans;

�� No CGT;No CGT;

�� No Capital duty;No Capital duty;

�� No Exchange Control;No Exchange Control;�� No Exchange Control;No Exchange Control;

�� No IHT;No IHT;

�� No Transfer Tax;No Transfer Tax;

�� No Stamp duty except on real property in Gibraltar;No Stamp duty except on real property in Gibraltar;

�� No VAT;No VAT;

�� No Wealth taxesNo Wealth taxes

Deductions and AllowancesDeductions and Allowances

�� In calculating assessable income, all outgoings In calculating assessable income, all outgoings and expenses and expenses wholly and exclusively incurredwholly and exclusively incurred in in and expenses and expenses wholly and exclusively incurredwholly and exclusively incurred in in the production of the income are deducted;the production of the income are deducted;

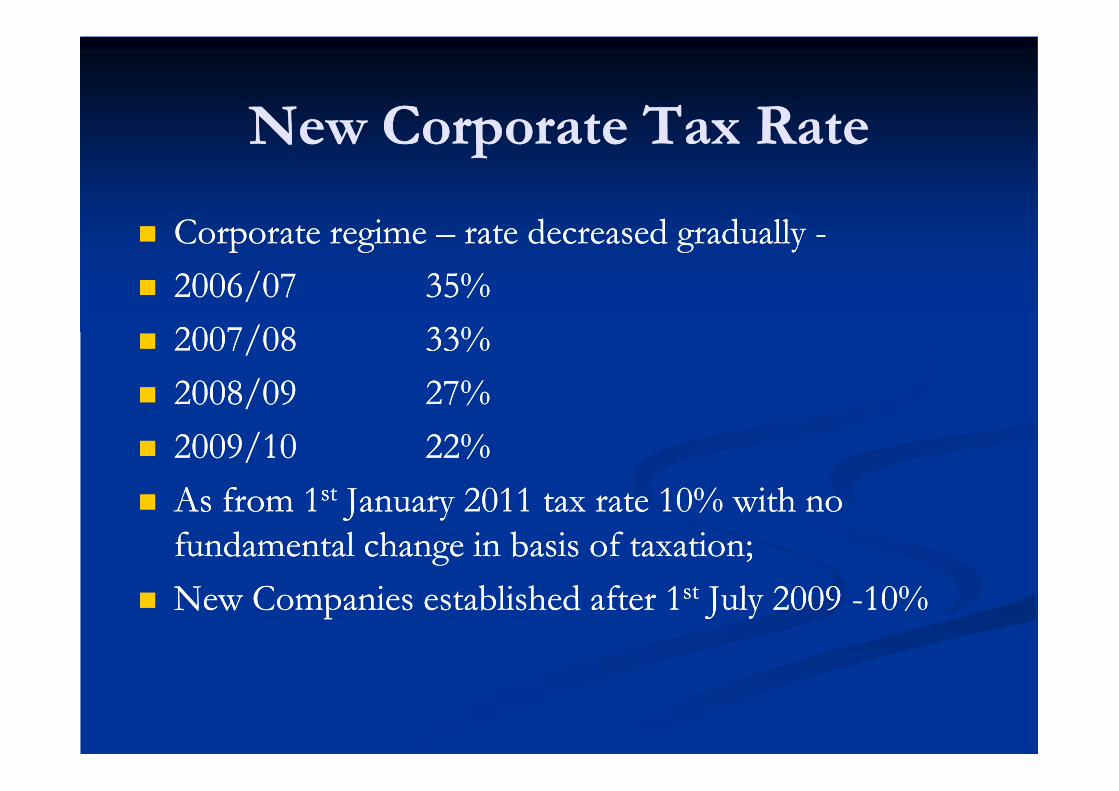

New Corporate Tax RateNew Corporate Tax Rate

�� Corporate regime Corporate regime –– rate decreased gradually rate decreased gradually --

�� 2006/072006/07 35%35%

�� 2007/082007/08 33%33%

�� 2008/092008/09 27%27%�� 2008/092008/09 27%27%

�� 2009/102009/10 22%22%

�� As from 1As from 1stst January 2011 tax rate 10% with no January 2011 tax rate 10% with no

fundamental change in basis of taxation;fundamental change in basis of taxation;

�� New Companies established after 1New Companies established after 1stst July 2009 July 2009 --10%10%

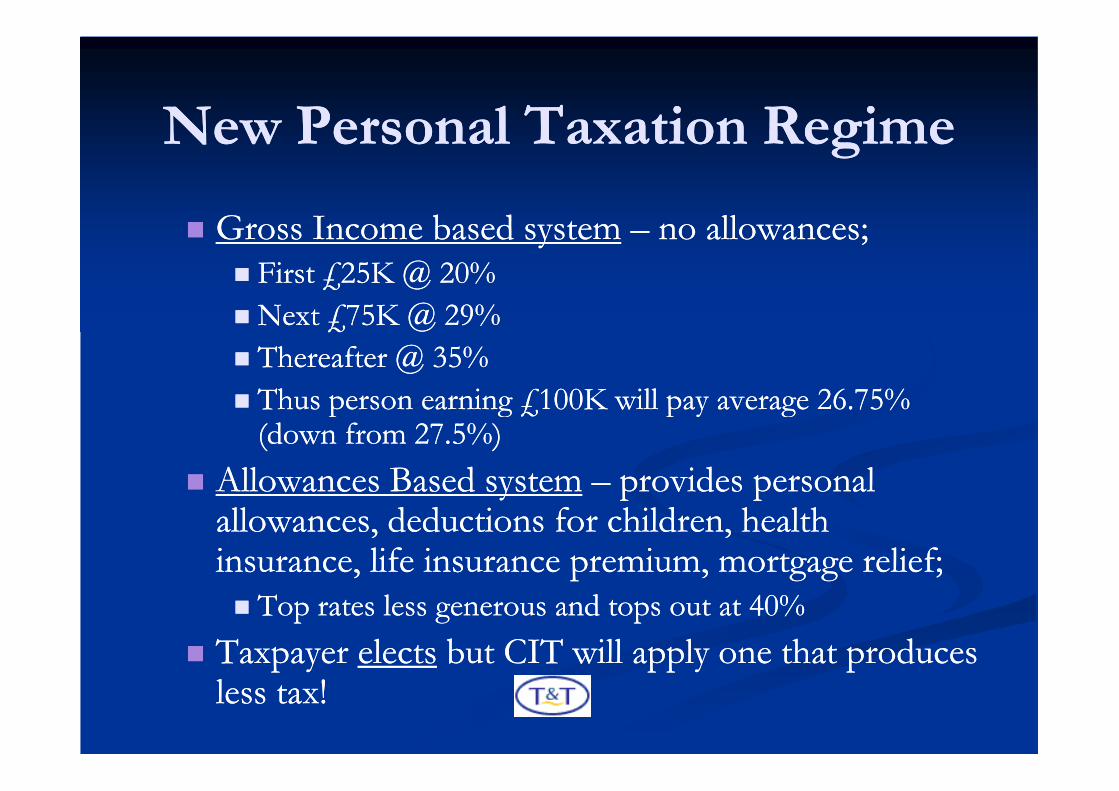

New Personal Taxation RegimeNew Personal Taxation Regime

�� Gross Income based systemGross Income based system –– no allowances;no allowances;�� First £25K @ 20%First £25K @ 20%

�� Next £75K @ 29%Next £75K @ 29%

�� Thereafter @ 35%Thereafter @ 35%

�� Thus person earning £100K will pay average 26.75% Thus person earning £100K will pay average 26.75% �� Thus person earning £100K will pay average 26.75% Thus person earning £100K will pay average 26.75% (down from 27.5%)(down from 27.5%)

�� Allowances Based systemAllowances Based system –– provides personal provides personal allowances, deductions for children, health allowances, deductions for children, health insurance, life insurance premium, mortgage relief;insurance, life insurance premium, mortgage relief;�� Top rates less generous and tops out at 40%Top rates less generous and tops out at 40%

�� Taxpayer Taxpayer electselects but CIT will apply one that produces but CIT will apply one that produces less tax!less tax!

Gibraltar Top rates ComparedGibraltar Top rates Compared

�� DenmarkDenmark 59%59% from from £40,250£40,250

�� SwedenSweden 56.7%56.7% £43,120£43,120

�� JapanJapan 50%50% £125,750£125,750

�� BritainBritain 50%50% £150,000£150,000

�� AustraliaAustralia 45%45% £87,750£87,750

�� ChinaChina 45%45% £10,020£10,020

�� GermanyGermany 45%45% £225,600£225,600

�� ItalyItaly 43%43% £67,600£67,600�� ItalyItaly 43%43% £67,600£67,600

�� FranceFrance 40%40% £62,600£62,600

�� GibraltarGibraltar 35%35% £100,000£100,000

�� USAUSA 35%35% £225,450£225,450

�� IndiaIndia 30%30% £6,850£6,850

�� BrazilBrazil 27.5%27.5% £13,305£13,305

�� SwitzerlandSwitzerland 22%22% £392,250£392,250

�� Hong KongHong Kong 17%17% £9,350£9,350

�� RussiaRussia 13%13% Flat rateFlat rate

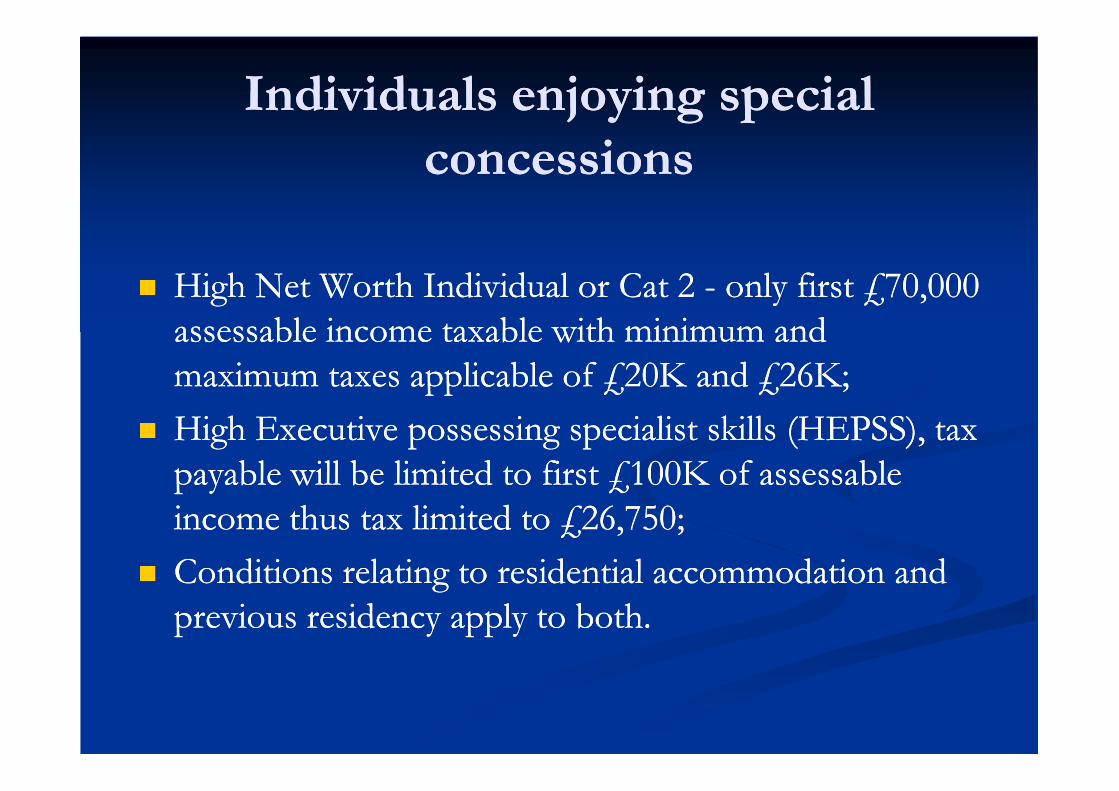

Individuals enjoying special Individuals enjoying special

concessionsconcessions

�� High Net Worth Individual or Cat 2 High Net Worth Individual or Cat 2 -- only first £70,000 only first £70,000

assessable income taxable with minimum and assessable income taxable with minimum and

maximum taxes applicable of £20K and £26K;maximum taxes applicable of £20K and £26K;maximum taxes applicable of £20K and £26K;maximum taxes applicable of £20K and £26K;

�� High Executive possessing specialist skills (HEPSS), tax High Executive possessing specialist skills (HEPSS), tax

payable will be limited to first £100K of assessable payable will be limited to first £100K of assessable

income thus tax limited to £26,750;income thus tax limited to £26,750;

�� Conditions relating to residential accommodation and Conditions relating to residential accommodation and

previous residency apply to both.previous residency apply to both.

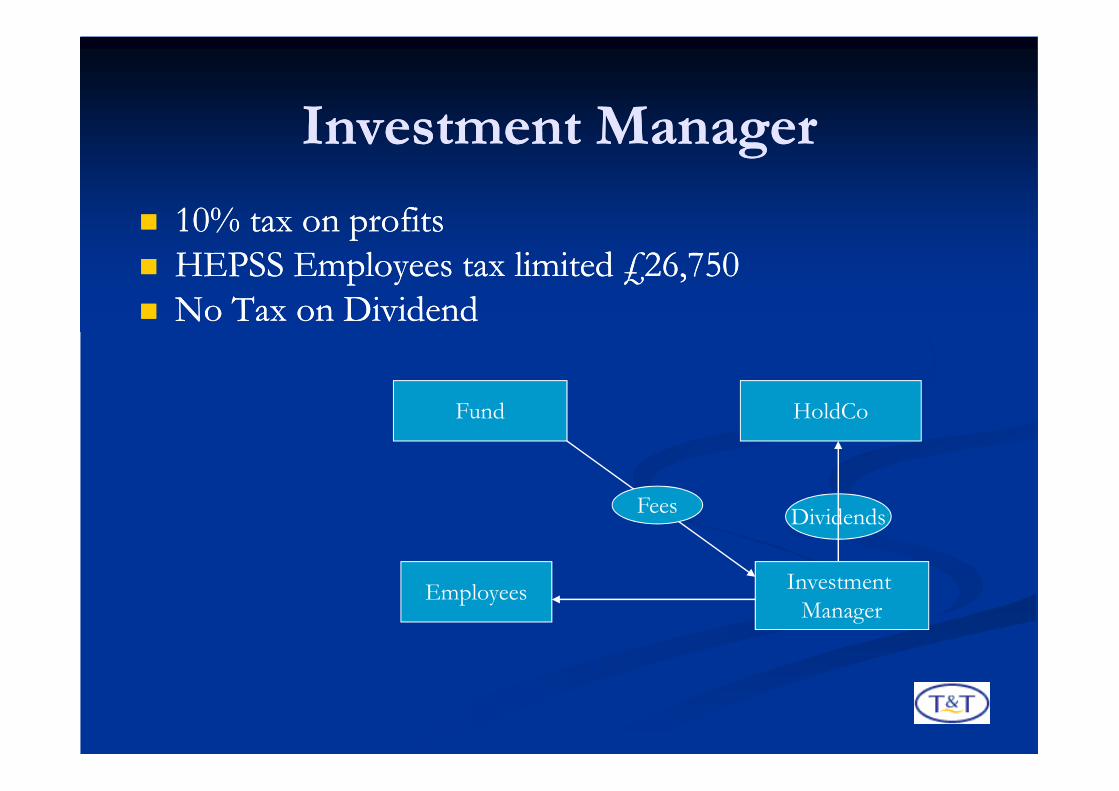

Investment ManagerInvestment Manager

�� 10% tax on profits10% tax on profits

�� HEPSS Employees tax limited £26,750HEPSS Employees tax limited £26,750

�� No Tax on DividendNo Tax on Dividend

Fund

Investment

Manager

Fees

Employees

HoldCo

Dividends

Private ClientPrivate Client

Cat 2 or

non resident settlor

Gib Trust(ee)Dividend

Dividend

Exempt

Exempt

Income

Rule 3(27)

Non-resident

beneficiaries or Cat 2

Gib Trust(ee)

Gib HoldCo

Property

outside GIb

Bank deposits,

investments

Stocks and shares

Rental Income – does

not accrue or derive in

Gibraltar -Not taxable Interest/InvestmentS6(8) Income Tax Act

Income exempt

Dividend

Exempt

S6(8)(j)

Exempt

S6(8)(a)

ConclusionsConclusions

�� Flexible, user friendly tax environment within Flexible, user friendly tax environment within Europe providing certainty;Europe providing certainty;

�� Attractive low rate of corporate tax;Attractive low rate of corporate tax;

�� Attractive tax provisions for individuals.Attractive tax provisions for individuals.