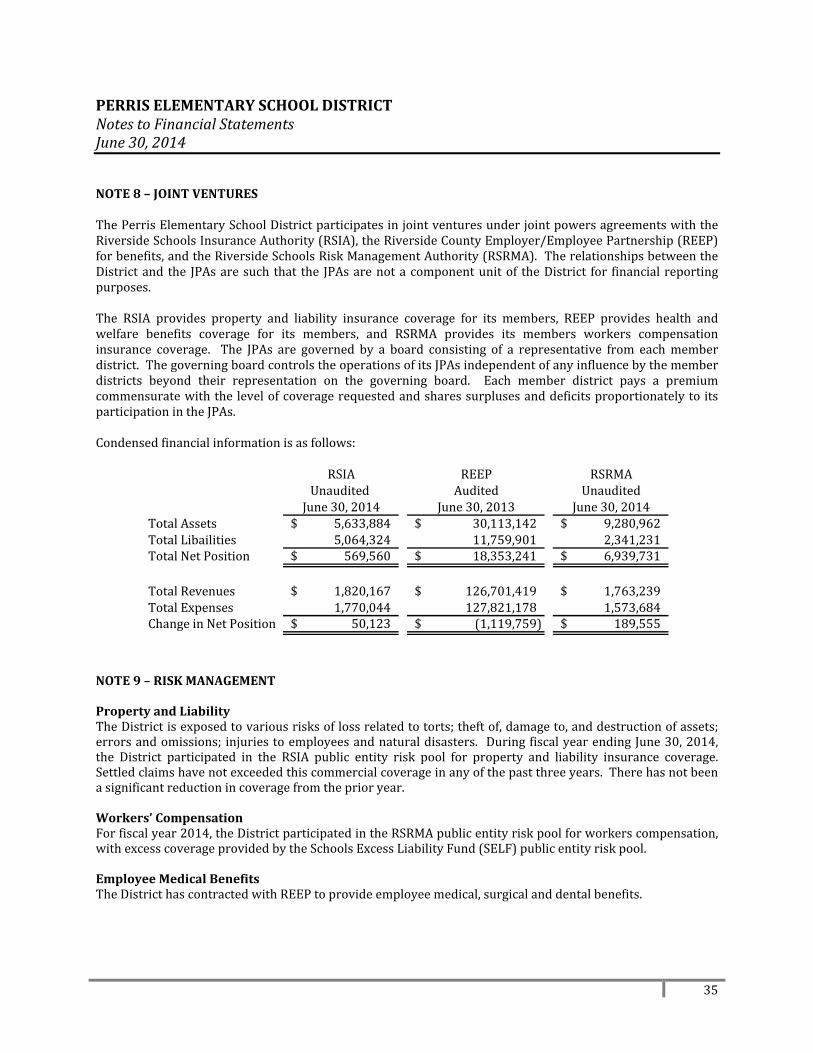

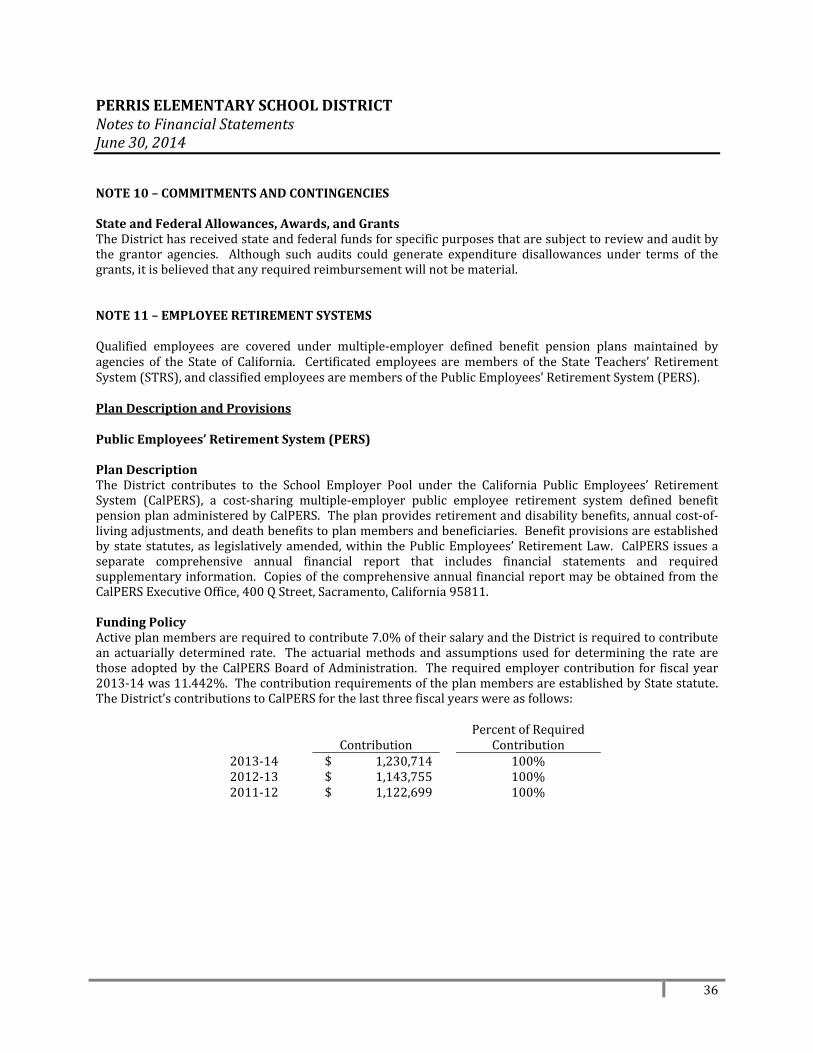

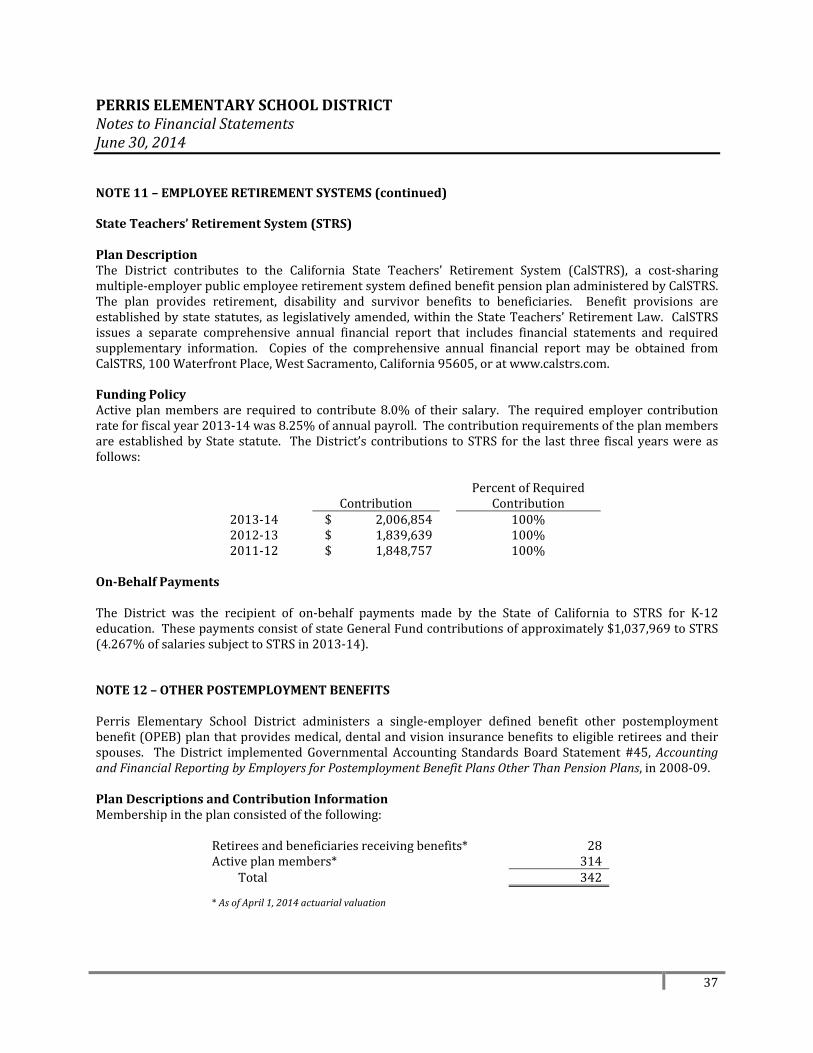

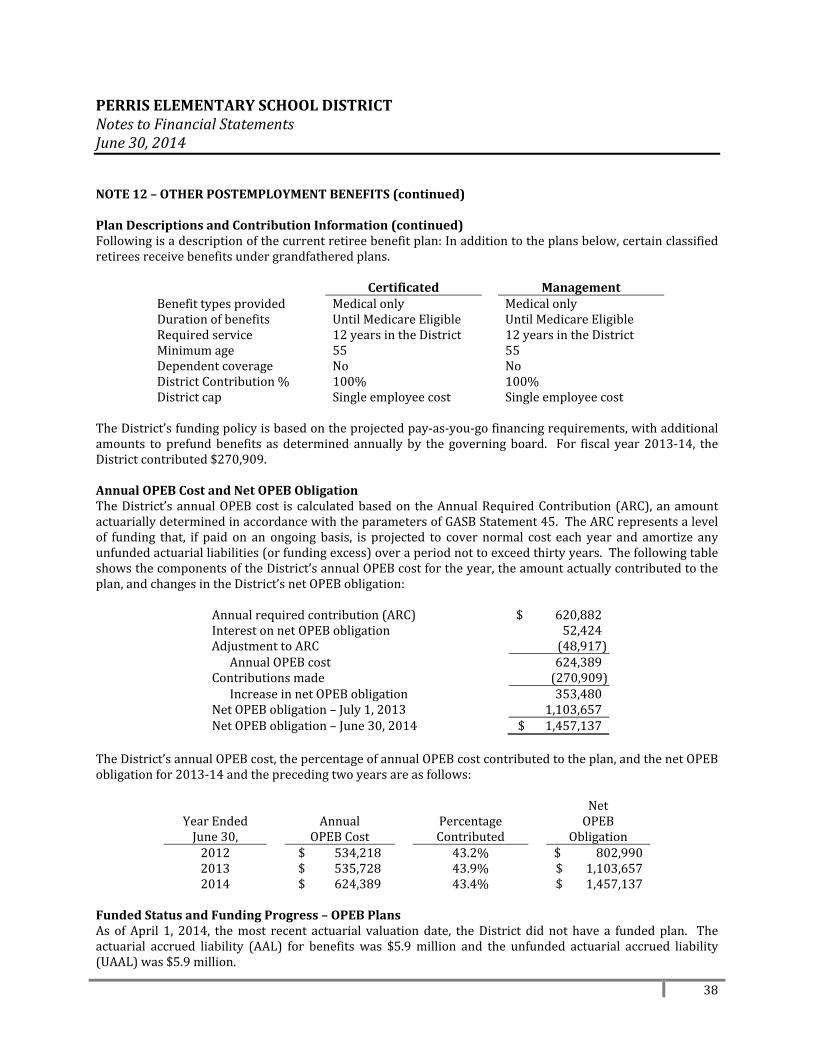

PERRIS ELEMENTARY SCHOOL DISTRICT AUDIT … ELEMENTARY SCHOOL DISTRICT For the Fiscal Year Ended...

80

PERRIS ELEMENTARY SCHOOL DISTRICT AUDIT REPORT For the Fiscal Year Ended June 30, 2014

Transcript of PERRIS ELEMENTARY SCHOOL DISTRICT AUDIT … ELEMENTARY SCHOOL DISTRICT For the Fiscal Year Ended...

PERRISELEMENTARYSCHOOLDISTRICT

AUDITREPORT

FortheFiscalYearEndedJune30,2014

PERRISELEMENTARYSCHOOLDISTRICTFortheFiscalYearEndedJune30,2014TableofContents

FINANCIALSECTION Page

IndependentAuditors’Report..................................................................................................................................................................1Management’sDiscussionandAnalysis...............................................................................................................................................3BasicFinancialStatements:

Government‐wideFinancialStatements:StatementofNetPosition...........................................................................................................................................................12StatementofActivities.................................................................................................................................................................13

GovernmentalFundsFinancialStatements:BalanceSheet...................................................................................................................................................................................14ReconciliationoftheGovernmentalFundsBalanceSheettothe

StatementofNetPosition....................................................................................................................................................15StatementofRevenues,Expenditures,andChangesinFundBalances.................................................................16ReconciliationoftheGovernmentalFundsStatementofRevenues,

ExpendituresandChangesinFundBalancestotheStatementofActivities................................................17FiduciaryFundFinancialStatement:StatementofFiduciaryNetPosition......................................................................................................................................18

NotestoFinancialStatements...............................................................................................................................................................19

REQUIREDSUPPLEMENTARYINFORMATIONBudgetaryComparisonSchedule–GeneralFund.........................................................................................................................41BudgetaryComparisonSchedule–CharterSchoolFund..........................................................................................................42ScheduleofFundingProgress...............................................................................................................................................................43NotestotheRequiredSupplementaryInformation....................................................................................................................44

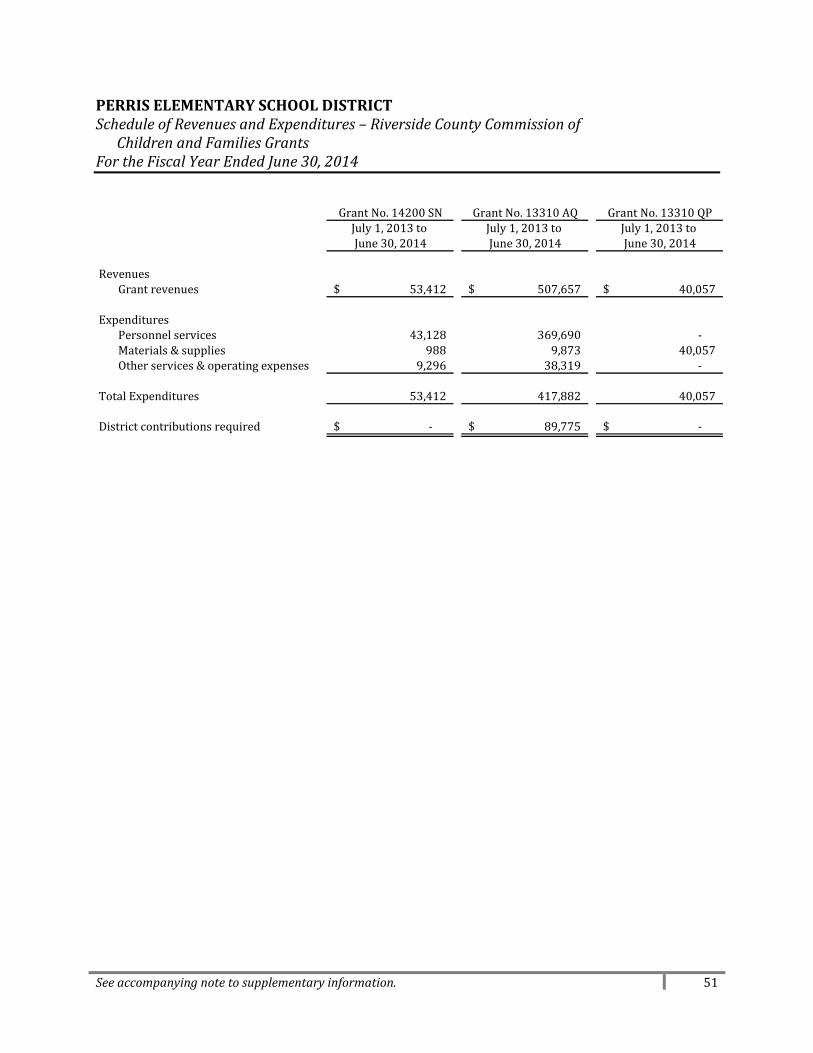

SUPPLEMENTARYINFORMATIONLocalEducationalAgencyOrganizationStructure.......................................................................................................................45ScheduleofAverageDailyAttendance..............................................................................................................................................46ScheduleofInstructionalTime.............................................................................................................................................................47ScheduleofFinancialTrendsandAnalysis......................................................................................................................................48ScheduleofExpendituresofFederalAwards.................................................................................................................................49ScheduleofCharterSchools...................................................................................................................................................................50ScheduleofRevenuesandExpenditures–RiversideCountyCommissionof

ChildrenandFamiliesGrants....................................................................................................................................................51ReconciliationofAnnualFinancialandBudgetReportwithAuditedFinancialStatements.....................................52NotetotheSupplementaryInformation...........................................................................................................................................53

PERRISELEMENTARYSCHOOLDISTRICTFortheFiscalYearEndedJune30,2014TableofContents

OTHERINDEPENDENTAUDITORS’REPORTS Page

IndependentAuditors'ReportonInternalControloverFinancialReportingandonCompliance andOtherMattersBasedonanAuditofFinancialStatementsPerformedinAccordancewith GovernmentAuditingStandards.....................................................................................................................................................54IndependentAuditors’ReportonStateCompliance...................................................................................................................56IndependentAuditors'ReportonComplianceForEachMajorFederalProgramandon InternalControlOverCompliance................................................................................................................................................58

FINDINGSANDQUESTIONEDCOSTS

ScheduleofAuditFindingsandQuestionedCosts: SummaryofAuditors’Results......................................................................................................................................................60 CurrentYearAuditFindingsandQuestionedCosts...........................................................................................................61 SummaryScheduleofPriorAuditFindings...........................................................................................................................65ManagementLetter....................................................................................................................................................................................66

FinancialSection

(Thispageintentionallyleftblank)

1

INDEPENDENTAUDITORS’REPORTGoverningBoardPerrisElementarySchoolDistrictPerris,CaliforniaReportontheFinancialStatementsWehaveauditedtheaccompanyingfinancialstatementsofthegovernmentalactivities,eachmajorfund,andtheaggregateremaining fund informationofPerrisElementarySchoolDistrict, asofand for the fiscalyearended June 30, 2014, and the related notes to the financial statements, which collectively comprise theDistrict'sbasicfinancialstatementsaslistedinthetableofcontents.Management’sResponsibilityfortheFinancialStatementsManagement is responsible for the preparation and fair presentation of these financial statements inaccordancewithaccountingprinciplesgenerallyaccepted in theUnitedStatesofAmerica; this includes thedesign,implementation,andmaintenanceofinternalcontrolrelevanttothepreparationandfairpresentationoffinancialstatementsthatarefreefrommaterialmisstatement,whetherduetofraudorerror.Auditors'ResponsibilityOurresponsibilityistoexpressopinionsonthesefinancialstatementsbasedonouraudit.WeconductedourauditinaccordancewithauditingstandardsgenerallyacceptedintheUnitedStatesofAmerica,thestandardsapplicabletofinancialauditscontainedinGovernmentAuditingStandards,issuedbytheComptrollerGeneralof theUnited States, andStandardsandProcedures forAuditsofCaliforniaK‐12LocalEducationalAgencies2013‐14. Thosestandardsrequirethatweplanandperformtheaudittoobtainreasonableassuranceaboutwhetherthefinancialstatementsarefreefrommaterialmisstatement.Anauditinvolvesperformingprocedurestoobtainauditevidenceabouttheamountsanddisclosuresinthefinancialstatements.Theproceduresselecteddependontheauditor’sjudgment,includingtheassessmentoftherisksofmaterialmisstatementofthefinancialstatements,whetherduetofraudorerror.Inmakingthoserisk assessments, the auditor considers internal control relevant to the entity’s preparation and fairpresentation of the financial statements in order to design audit procedures that are appropriate in thecircumstances,butnot for thepurposeofexpressinganopinionontheeffectivenessoftheentity’s internalcontrol. Accordingly,we express no suchopinion.An audit also includes evaluating the appropriatenessofaccountingpoliciesusedandthereasonablenessofsignificantaccountingestimatesmadebymanagement,aswellasevaluatingtheoverallpresentationofthefinancialstatements.Webelievethattheauditevidencewehaveobtainedissufficientandappropriatetoprovideabasisforourauditopinions.OpinionsInouropinion,thefinancialstatementsreferredtoabovepresentfairly,inallmaterialrespects,therespectivefinancial position of the governmental activities, each major fund, and the aggregate remaining fundinformationofPerrisElementarySchoolDistrict,asofJune30,2014,andtherespectivechangesinfinancialpositionthereofforthefiscalyearthenendedinaccordancewithaccountingprinciplesgenerallyacceptedintheUnitedStatesofAmerica.

2

EmphasisofMatterAsdiscussedinNote1.G.tothebasicfinancialstatements,theDistricthaschangeditsmethodforaccountingandreportingcertainitemspreviouslyreportedasassetsorliabilitiesduringfiscalyear2013‐2014duetotheadoptionofGovernmentalAccountingStandardsBoardStatementNo.65,"ItemsPreviouslyReportedasAssetsand Liabilities". The adoption of this standard required retrospective application resulting in a $493,381reductionofpreviouslyreportednetpositionatJuly1,2013.Ouropinionisnotmodifiedwithrespecttothismatter.OtherMattersRequiredSupplementaryInformationAccounting principles generally accepted in the United States of America require that the management’sdiscussionandanalysisonpages3through11,budgetarycomparisoninformationonpages41and42,andschedule of fundingprogress onpage43bepresented to supplement thebasic financial statements. Suchinformation,althoughnotapartofthebasicfinancialstatements,isrequiredbytheGovernmentalAccountingStandardsBoard,whoconsidersittobeanessentialpartoffinancialreportingforplacingthebasicfinancialstatements in anappropriateoperational, economic, orhistorical context. Wehaveapplied certain limitedprocedures to the required supplementary information in accordance with auditing standards generallyacceptedintheUnitedStatesofAmerica,whichconsistedofinquiriesofmanagementaboutthemethodsofpreparing the informationandcomparing the information forconsistencywithmanagement’s responses toourinquiries,thebasicfinancialstatements,andotherknowledgeweobtainedduringourauditofthebasicfinancialstatements.Wedonotexpressanopinionorprovideanyassuranceontheinformationbecausethelimitedproceduresdonotprovideuswithsufficientevidencetoexpressanopinionorprovideanyassurance.OtherInformationOur auditwas conducted for the purpose of forming opinions on the financial statements that collectivelycomprise Perris Elementary School District’s basic financial statements. The other supplementaryinformation listed in the table of contents is presented for purposes of additional analysis and is not arequiredpartofthebasicfinancialstatements.Theothersupplementaryinformationlistedinthetableofcontents,includingtheScheduleofExpendituresofFederal Awards, is the responsibility of management and was derived from and relates directly to theunderlyingaccountingandotherrecordsusedtopreparethebasicfinancialstatements.Suchinformationhasbeensubjected to theauditingproceduresapplied intheauditof thebasic financialstatementsandcertainadditional procedures, including comparing and reconciling such information directly to the underlyingaccounting and other records used to prepare the basic financial statements or to the basic financialstatements themselves, and other additional procedures in accordance with auditing standards generallyacceptedintheUnitedStatesofAmerica.Inouropinion,theothersupplementaryinformationisfairlystated,inallmaterialrespects,inrelationtothebasicfinancialstatementsasawhole.OtherReportingRequiredbyGovernmentAuditingStandardsInaccordancewithGovernmentAuditingStandards,wehavealsoissuedourreportdatedDecember11,2014on our consideration of the District's internal control over financial reporting and on our tests of itscompliancewithcertainprovisionsof laws,regulations,contracts,andgrantagreementsandothermatters.Thepurposeofthatreportistodescribethescopeofourtestingofinternalcontroloverfinancialreportingandcomplianceandtheresultsofthattesting,andnottoprovideanopiniononinternalcontroloverfinancialreporting or on compliance. That report is an integral part of an audit performed in accordance withGovernment Auditing Standards in considering the District's internal control over financial reporting andcompliance.

Murrieta,CaliforniaDecember11,2014

3

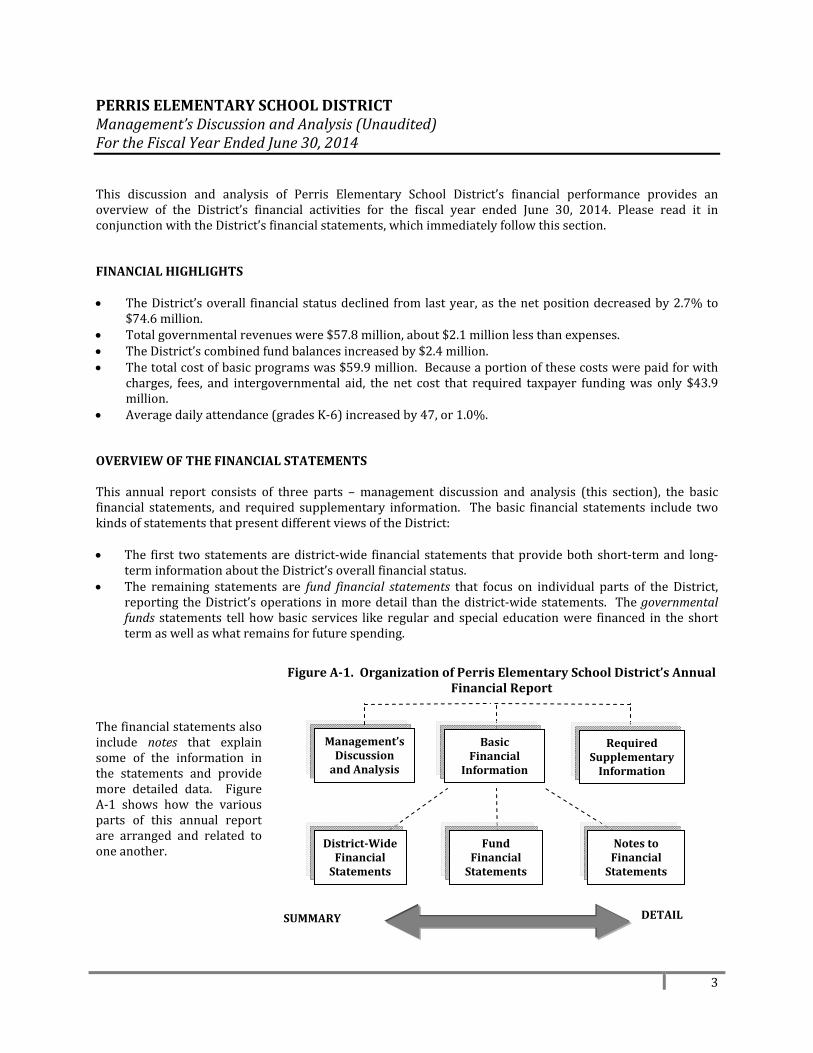

FigureA‐1.OrganizationofPerrisElementarySchoolDistrict’sAnnualFinancialReport

PERRISELEMENTARYSCHOOLDISTRICTManagement’sDiscussionandAnalysis(Unaudited)FortheFiscalYearEndedJune30,2014This discussion and analysis of Perris Elementary School District’s financial performance provides anoverview of the District’s financial activities for the fiscal year ended June 30, 2014. Please read it inconjunctionwiththeDistrict’sfinancialstatements,whichimmediatelyfollowthissection.FINANCIALHIGHLIGHTS TheDistrict’soverall financialstatusdeclinedfromlastyear,as thenetpositiondecreasedby2.7%to

$74.6million. Totalgovernmentalrevenueswere$57.8million,about$2.1millionlessthanexpenses. TheDistrict’scombinedfundbalancesincreasedby$2.4million. Thetotalcostofbasicprogramswas$59.9million.Becauseaportionofthesecostswerepaidforwith

charges, fees, and intergovernmental aid, the net cost that required taxpayer fundingwas only $43.9million.

Averagedailyattendance(gradesK‐6)increasedby47,or1.0%.OVERVIEWOFTHEFINANCIALSTATEMENTSThis annual report consists of three parts – management discussion and analysis (this section), the basicfinancial statements, and required supplementary information. The basic financial statements include twokindsofstatementsthatpresentdifferentviewsoftheDistrict: The first twostatementsaredistrict‐wide financial statements thatprovidebothshort‐termand long‐

terminformationabouttheDistrict’soverallfinancialstatus. The remaining statements are fund financial statements that focus on individual parts of the District,

reporting theDistrict’soperations inmoredetail thanthedistrict‐widestatements. Thegovernmentalfunds statements tell howbasic services like regular and special educationwere financed in the shorttermaswellaswhatremainsforfuturespending.

Thefinancialstatementsalsoinclude notes that explainsome of the information inthe statements and providemore detailed data. FigureA‐1 shows how the variousparts of this annual reportare arranged and related tooneanother.

Management’sDiscussionandAnalysis

BasicFinancial

Information

RequiredSupplementaryInformation

FundFinancialStatements

District‐WideFinancialStatements

NotestoFinancialStatements

SUMMARY DETAIL

4

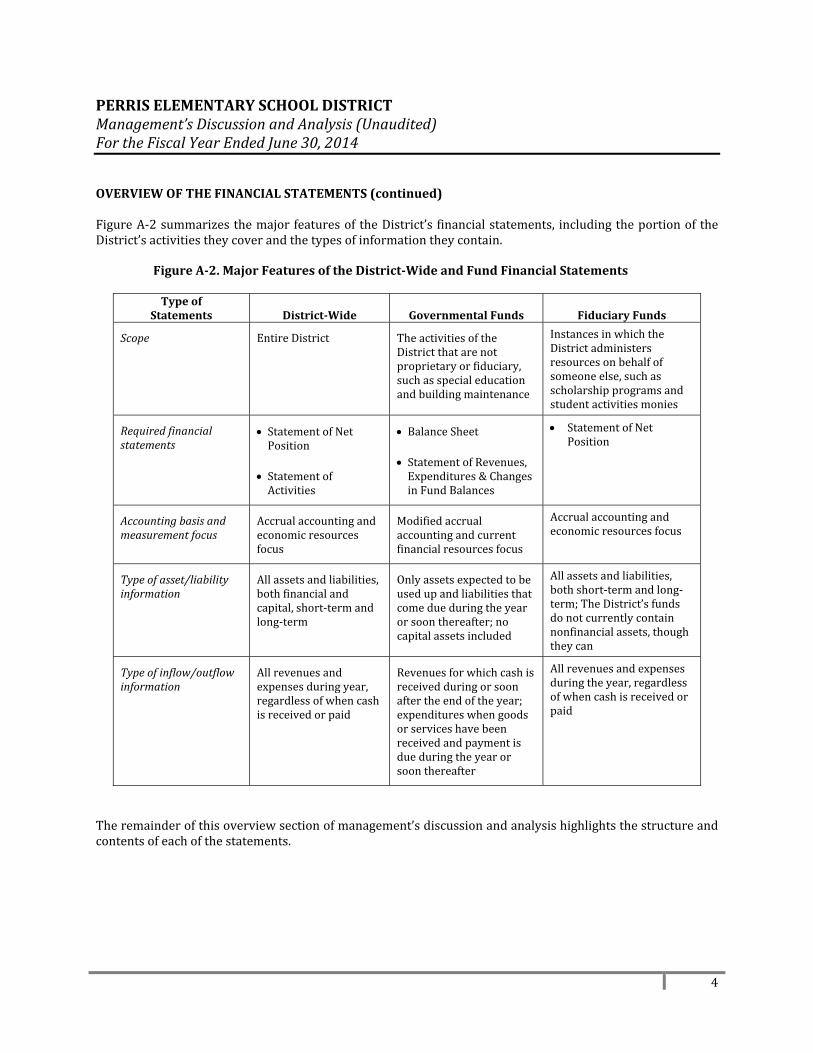

PERRISELEMENTARYSCHOOLDISTRICTManagement’sDiscussionandAnalysis(Unaudited)FortheFiscalYearEndedJune30,2014OVERVIEWOFTHEFINANCIALSTATEMENTS(continued)FigureA‐2summarizesthemajorfeaturesoftheDistrict’s financialstatements, includingtheportionoftheDistrict’sactivitiestheycoverandthetypesofinformationtheycontain.

FigureA‐2.MajorFeaturesoftheDistrict‐WideandFundFinancialStatements

TypeofStatements

District‐Wide

GovernmentalFunds

FiduciaryFunds

Scope EntireDistrict TheactivitiesoftheDistrictthatarenotproprietaryorfiduciary,suchasspecialeducationandbuildingmaintenance

InstancesinwhichtheDistrictadministersresourcesonbehalfofsomeoneelse,suchasscholarshipprogramsandstudentactivitiesmonies

Requiredfinancialstatements

StatementofNetPosition

StatementofActivities

BalanceSheet

StatementofRevenues,Expenditures&ChangesinFundBalances

StatementofNetPosition

Accountingbasisandmeasurementfocus

Accrualaccountingandeconomicresourcesfocus

Modifiedaccrualaccountingandcurrentfinancialresourcesfocus

Accrualaccountingandeconomicresourcesfocus

Typeofasset/liabilityinformation

Allassetsandliabilities,bothfinancialandcapital,short‐termandlong‐term

Onlyassetsexpectedtobeusedupandliabilitiesthatcomedueduringtheyearorsoonthereafter;nocapitalassetsincluded

Allassetsandliabilities,bothshort‐termandlong‐term;TheDistrict’sfundsdonotcurrentlycontainnonfinancialassets,thoughtheycan

Typeofinflow/outflowinformation

Allrevenuesandexpensesduringyear,regardlessofwhencashisreceivedorpaid

Revenuesforwhichcashisreceivedduringorsoonaftertheendoftheyear;expenditureswhengoodsorserviceshavebeenreceivedandpaymentisdueduringtheyearorsoonthereafter

Allrevenuesandexpensesduringtheyear,regardlessofwhencashisreceivedorpaid

Theremainderofthisoverviewsectionofmanagement’sdiscussionandanalysishighlightsthestructureandcontentsofeachofthestatements.

5

PERRISELEMENTARYSCHOOLDISTRICTManagement’sDiscussionandAnalysis(Unaudited)FortheFiscalYearEndedJune30,2014OVERVIEWOFTHEFINANCIALSTATEMENTS(continued)District‐WideStatementsThe district‐wide statements report information about the District as a whole using accounting methodssimilartothoseusedbyprivate‐sectorcompanies.ThestatementofnetpositionincludesalloftheDistrict’sassetsand liabilities. Allof thecurrentyear’srevenuesandexpensesareaccountedfor inthestatementofactivitiesregardlessofwhencashisreceivedorpaid.Thetwodistrict‐widestatementsreporttheDistrict’snetpositionandhowithaschanged.Netposition–thedifferencebetweentheDistrict’sassetsanddeferredoutflowsofresourcesandliabilitiesanddeferredinflowsofresources–isonewaytomeasuretheDistrict’sfinancialhealth,orposition. Overtime,increasesanddecreasesintheDistrict’snetpositionareanindicatorofwhetheritsfinancial

positionisimprovingordeteriorating,respectively. ToassesstheoverallhealthoftheDistrict,youneedtoconsideradditionalnonfinancial factorssuchas

changesintheDistrict’sdemographicsandtheconditionofschoolbuildingsandotherfacilities. In the district‐wide financial statements, the District’s activities are categorized as Governmental

Activities. Mostof theDistrict’sbasicservicesare includedhere,suchasregularandspecialeducation,transportation,andadministration.Propertytaxesandstateaidfinancemostoftheseactivities.

FundFinancialStatementsThefundfinancialstatementsprovidemoredetailedinformationabouttheDistrict’smostsignificantfunds–nottheDistrictasawhole.FundsareaccountingdevicestheDistrictusestokeeptrackofspecificsourcesoffundingandspendingonparticularprograms: SomefundsarerequiredbyStatelawandbybondcovenants. TheDistrictestablishesotherfundstocontrolandmanagemoneyforparticularpurposes(likerepaying

itslong‐termdebt)ortoshowthatitisproperlyusingcertainrevenues.TheDistricthastwotypesoffunds: Governmental funds – All of the District’s basic services are included in governmental funds, which

generallyfocuson(1)howcashandotherfinancialassetsthatcanreadilybeconvertedtocashflowinand out and (2) the balances left at year‐end that are available for spending. Consequently, thegovernmental funds statementsprovideadetailed short‐termview thathelpsyoudeterminewhethertherearemoreorfewerfinancialresourcesthatcanbespentinthenearfuturetofinancetheDistrict’sprograms. Becausethisinformationdoesnotencompasstheadditionallong‐termfocusofthedistrict‐widestatements,weprovideadditionalinformationonaseparatereconciliationpagethatexplainstherelationship(ordifferences)betweenthem.

Fiduciary funds – TheDistrict is the trustee, or fiduciary, for assets that belong to others, such as thestudentactivitiesfunds.TheDistrictisresponsibleforensuringthattheassetsreportedinthesefundsareusedonlyfortheirintendedpurposesandbythosetowhomtheassetsbelong.AlloftheDistrict’sfiduciary activities are reported in a separate statement of fiduciary net position. We exclude theseactivities from the district‐wide financial statements because the District cannot use these assets tofinanceitsoperations.

6

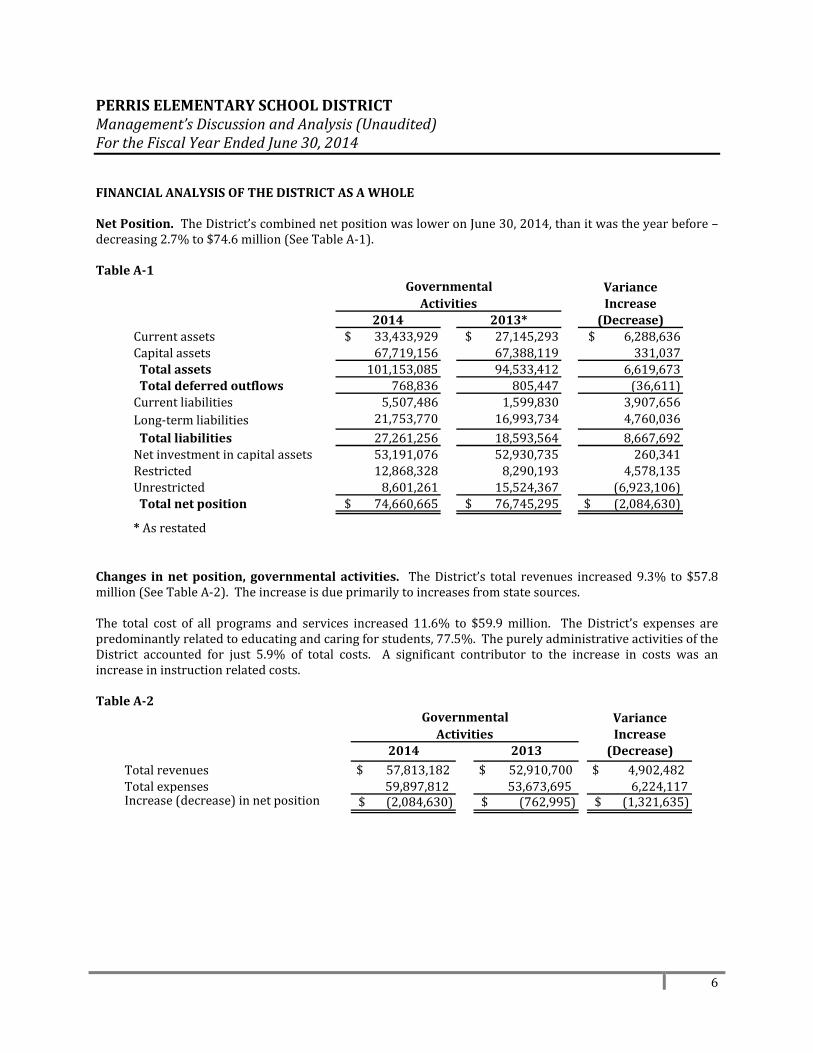

PERRISELEMENTARYSCHOOLDISTRICTManagement’sDiscussionandAnalysis(Unaudited)FortheFiscalYearEndedJune30,2014FINANCIALANALYSISOFTHEDISTRICTASAWHOLENetPosition.TheDistrict’scombinednetpositionwasloweronJune30,2014,thanitwastheyearbefore–decreasing2.7%to$74.6million(SeeTableA‐1).TableA‐1

VarianceIncrease

2014 2013* (Decrease)Currentassets $33,433,929 $27,145,293 $6,288,636Capitalassets 67,719,156 67,388,119 331,037Totalassets 101,153,085 94,533,412 6,619,673Totaldeferredoutflows 768,836 805,447 (36,611)Currentliabilities 5,507,486 1,599,830 3,907,656Long‐termliabilities 21,753,770 16,993,734 4,760,036Totalliabilities 27,261,256 18,593,564 8,667,692Netinvestmentincapitalassets 53,191,076 52,930,735 260,341Restricted 12,868,328 8,290,193 4,578,135Unrestricted 8,601,261 15,524,367 (6,923,106)Totalnetposition $74,660,665 $76,745,295 $(2,084,630)

*Asrestated

ActivitiesGovernmental

Changes innetposition,governmentalactivities. TheDistrict’s total revenues increased9.3% to $57.8million(SeeTableA‐2).Theincreaseisdueprimarilytoincreasesfromstatesources.The total cost of all programs and services increased 11.6% to $59.9million. The District’s expenses arepredominantlyrelatedtoeducatingandcaringforstudents,77.5%.ThepurelyadministrativeactivitiesoftheDistrict accounted for just 5.9% of total costs. A significant contributor to the increase in costs was anincreaseininstructionrelatedcosts.TableA‐2

VarianceIncrease

2014 2013 (Decrease)Totalrevenues $57,813,182 $52,910,700 $4,902,482Totalexpenses 59,897,812 53,673,695 6,224,117Increase(decrease)innetposition (2,084,630)$ (762,995)$ (1,321,635)$

ActivitiesGovernmental

7

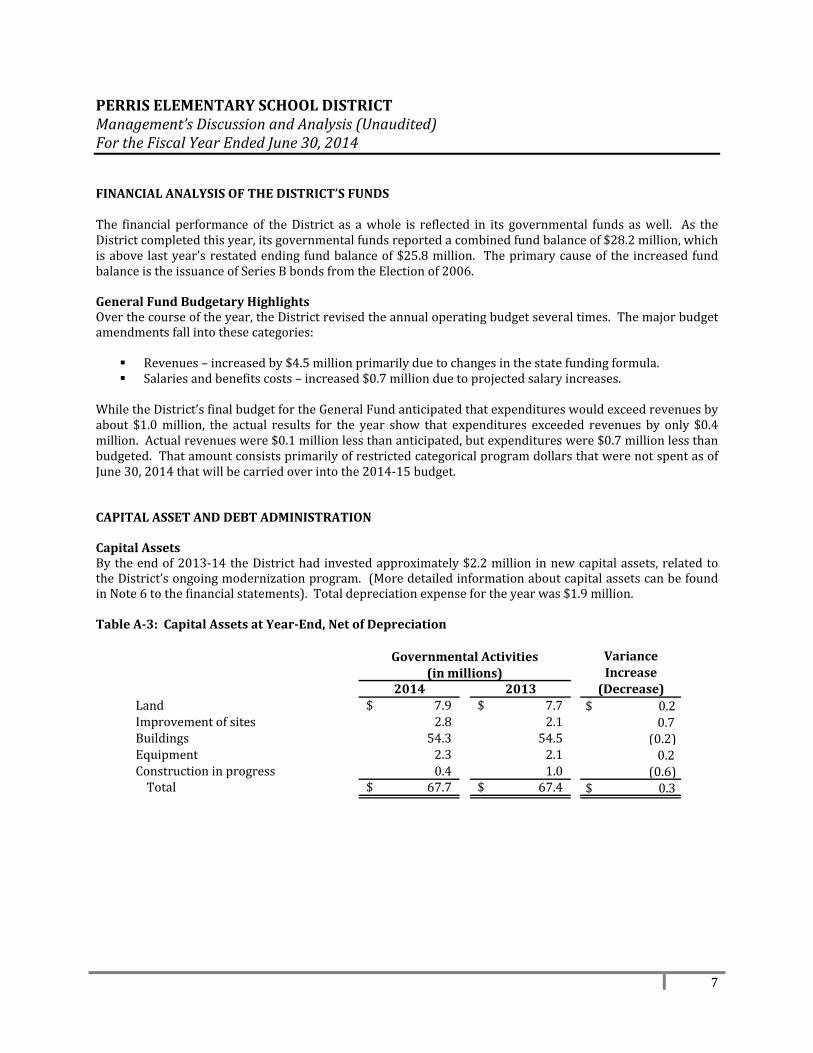

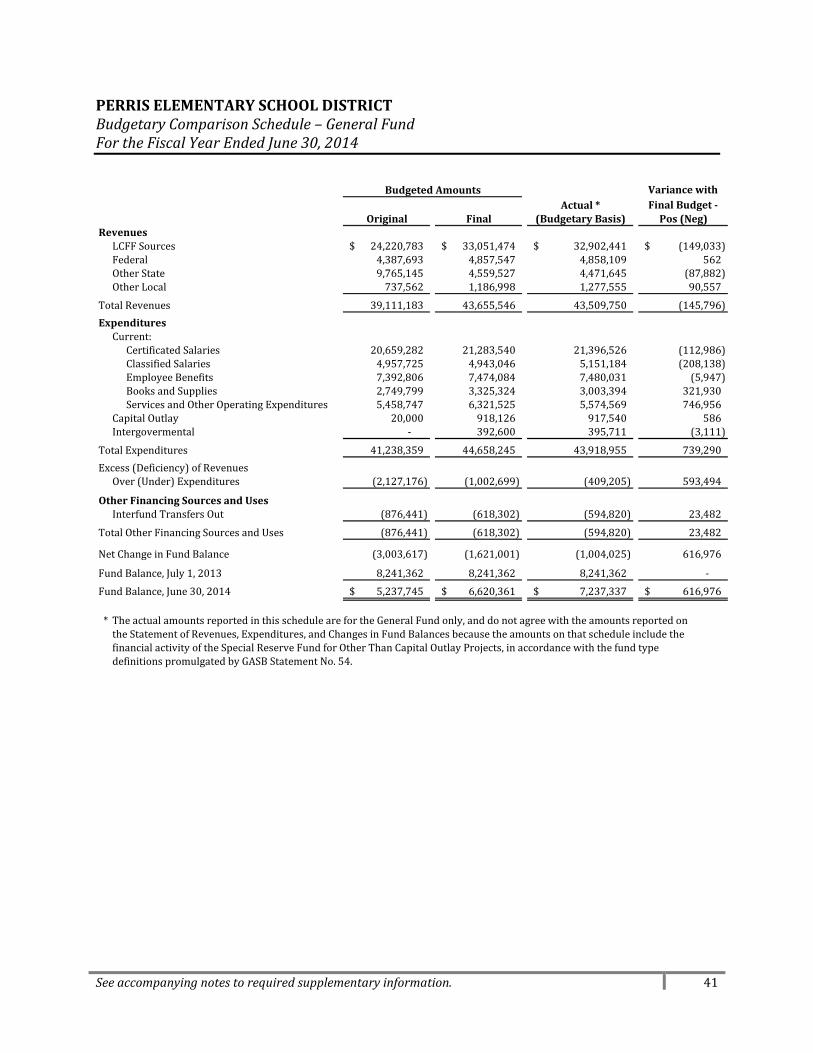

PERRISELEMENTARYSCHOOLDISTRICTManagement’sDiscussionandAnalysis(Unaudited)FortheFiscalYearEndedJune30,2014FINANCIALANALYSISOFTHEDISTRICT’SFUNDSThe financial performance of theDistrict as awhole is reflected in its governmental funds aswell. As theDistrictcompletedthisyear,itsgovernmentalfundsreportedacombinedfundbalanceof$28.2million,whichisabove lastyear’srestatedendingfundbalanceof$25.8million. Theprimarycauseofthe increasedfundbalanceistheissuanceofSeriesBbondsfromtheElectionof2006.GeneralFundBudgetaryHighlightsOverthecourseoftheyear,theDistrictrevisedtheannualoperatingbudgetseveraltimes.Themajorbudgetamendmentsfallintothesecategories:

Revenues–increasedby$4.5millionprimarilyduetochangesinthestatefundingformula. Salariesandbenefitscosts–increased$0.7millionduetoprojectedsalaryincreases.

WhiletheDistrict’sfinalbudgetfortheGeneralFundanticipatedthatexpenditureswouldexceedrevenuesbyabout $1.0million, the actual results for the year show that expenditures exceeded revenues by only $0.4million.Actualrevenueswere$0.1millionlessthananticipated,butexpenditureswere$0.7millionlessthanbudgeted.ThatamountconsistsprimarilyofrestrictedcategoricalprogramdollarsthatwerenotspentasofJune30,2014thatwillbecarriedoverintothe2014‐15budget.CAPITALASSETANDDEBTADMINISTRATIONCapitalAssetsBytheendof2013‐14theDistricthadinvestedapproximately$2.2millioninnewcapitalassets,relatedtotheDistrict’songoingmodernizationprogram.(MoredetailedinformationaboutcapitalassetscanbefoundinNote6tothefinancialstatements).Totaldepreciationexpensefortheyearwas$1.9million.TableA‐3:CapitalAssetsatYear‐End,NetofDepreciation

VarianceIncrease

2014 2013 (Decrease)Land 7.9$ 7.7$ $0.2Improvementofsites 2.8 2.1 0.7Buildings 54.3 54.5 (0.2)Equipment 2.3 2.1 0.2Constructioninprogress 0.4 1.0 (0.6)Total 67.7$ 67.4$ $0.3

(inmillions)GovernmentalActivities

8

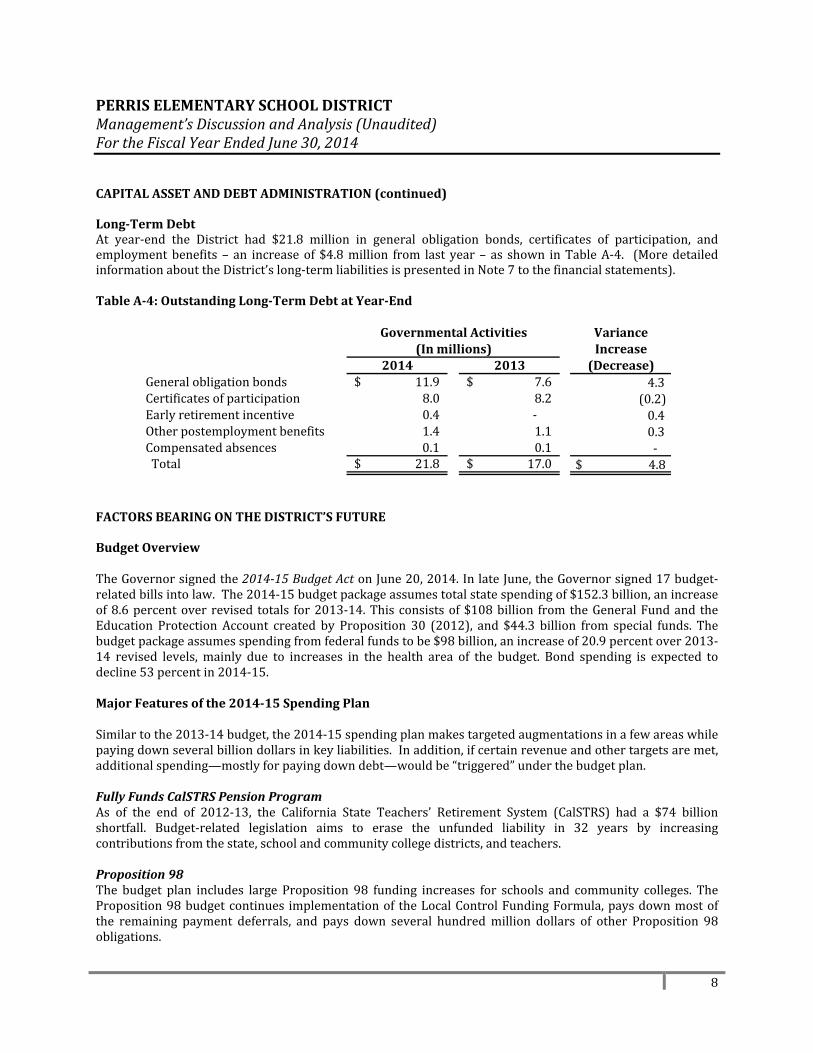

PERRISELEMENTARYSCHOOLDISTRICTManagement’sDiscussionandAnalysis(Unaudited)FortheFiscalYearEndedJune30,2014CAPITALASSETANDDEBTADMINISTRATION(continued)Long‐TermDebtAt year‐end the District had $21.8 million in general obligation bonds, certificates of participation, andemploymentbenefits – an increaseof $4.8million from last year– as shown inTableA‐4. (MoredetailedinformationabouttheDistrict’slong‐termliabilitiesispresentedinNote7tothefinancialstatements).

TableA‐4:OutstandingLong‐TermDebtatYear‐End

VarianceIncrease

2014 2013 (Decrease)Generalobligationbonds 11.9$ 7.6$ 4.3Certificatesofparticipation 8.0 8.2 (0.2)Earlyretirementincentive 0.4 ‐ 0.4Otherpostemploymentbenefits 1.4 1.1 0.3Compensatedabsences 0.1 0.1 ‐Total 21.8$ 17.0$ $4.8

(Inmillions)GovernmentalActivities

FACTORSBEARINGONTHEDISTRICT’SFUTUREBudgetOverviewTheGovernorsignedthe2014‐15BudgetActonJune20,2014.InlateJune,theGovernorsigned17budget‐relatedbillsintolaw.The2014‐15budgetpackageassumestotalstatespendingof$152.3billion,anincreaseof8.6percentover revised totals for2013‐14.Thisconsistsof$108billion fromtheGeneralFundand theEducation Protection Account created by Proposition 30 (2012), and $44.3 billion from special funds. Thebudgetpackageassumesspendingfromfederalfundstobe$98billion,anincreaseof20.9percentover2013‐14 revised levels, mainly due to increases in the health area of the budget. Bond spending is expected todecline53percentin2014‐15.MajorFeaturesofthe2014‐15SpendingPlanSimilartothe2013‐14budget,the2014‐15spendingplanmakestargetedaugmentationsinafewareaswhilepayingdownseveralbilliondollarsinkeyliabilities.Inaddition,ifcertainrevenueandothertargetsaremet,additionalspending—mostlyforpayingdowndebt—wouldbe“triggered”underthebudgetplan.FullyFundsCalSTRSPensionProgramAs of the end of 2012‐13, the California State Teachers’ Retirement System (CalSTRS) had a $74 billionshortfall. Budget‐related legislation aims to erase the unfunded liability in 32 years by increasingcontributionsfromthestate,schoolandcommunitycollegedistricts,andteachers.Proposition98The budget plan includes large Proposition 98 funding increases for schools and community colleges. TheProposition98budgetcontinues implementationof theLocalControlFundingFormula,paysdownmostofthe remaining payment deferrals, and pays down several hundredmillion dollars of other Proposition 98obligations.

9

PERRISELEMENTARYSCHOOLDISTRICTManagement’sDiscussionandAnalysis(Unaudited)FortheFiscalYearEndedJune30,2014

FACTORSBEARINGONTHEDISTRICT’SFUTURE(continued)SpendingChangesFundingforK‐14educationincreasessignificantlyunderthenewbudgetpackage.Inthesectionsthatfollow,wedescribehowtheStateisspendingthesefunds.DeferralPaymentsPaysDown$5.2BillioninOutstandingDeferralsThebudgetpackagepaysdown$5.2billioninoutstandingdeferrals($4.7billionforschoolsand$498millionforcommunitycolleges).Ofthetotalpaydown,$1.4billionisdesignatedas2012‐13spending,$3.1billionisdesignatedas2013‐14spending,and$662millionisdesignatedas2014‐15spending.Underthebudgetplan,$992million indeferrals ($897million for schools and$94million for community colleges)would remainoutstandingattheendof2014‐15.EliminatesRemainingDeferralsifMinimumGuaranteeExceedsEstimatesThe budget package pays down additional deferrals (potentially eliminating all outstanding deferrals) ifsubsequentestimatesofthe2013‐14and2014‐15minimumguaranteesarehigherthantheadministration’sMay2015estimates.Effectively,thebudgetplanearmarksthefirst$992millioninpotentialadditional2013‐14and2014‐15spendingfordeferralpaydowns.MandatesPaysDown$450MillioninOutstandingEducationMandateClaimsWe estimate the State currently has a backlog of more than $5 billion in unpaid claims for educationmandates.Thebudgetincludes$400milliontoreducethemandatebacklogforschools.(Ofthisamount,$287millionis2014‐15Proposition98fundingand$113millionisfromunspentprior‐yearfund.)Fundswillbedistributedtoschoolsandcommunitycollegesonaper‐studentbasis.AddsSeveralMandatestoSchoolandCommunityCollegeBlockGrantsTheCommissiononStateMandates recentlyapprovedsevennewreimbursableeducationmandates.Sixofthese mandates apply to schools, two apply to community colleges, and one applies to both schools andcommunity colleges. For schools, the budget adds to the block grant mandates related to (1) parentalinvolvementprocedures,(2)complianceactivitiesassociatedwiththeWilliamsv.Californiacase,(3)uniformcomplaintprocedures,(4)developerfees,(5)charterschooloversight,and(6)publiccontracts.EnergyGrantsStateProvidesSecond‐YearFundingforEnergyProjectsPassedbyvotersinNovember2012,Proposition39increasesstatecorporatetaxrevenuesandrequiresforafive‐yearperiod,starting in2013‐14, thataportionof theserevenuesbeusedto improveenergyefficiencyand expand the use of alternative energy in public buildings. The 2014‐15 budget provides $345millionProposition98GeneralFundforProposition39schoolandcommunitycollegeenergyprograms.Specifically,the budget provides $279 million for school grants, $38 million for community colleges grants, and $28millionfortherevolvingloanprogramforbothschoolsandcommunitycolleges.(EstimatesofProposition39revenuesare lower in2014‐15compared to2013‐14, resulting in lessprovided forschoolandcommunitycollegegrants.)Thebudgetalsoprovides$8millionnon‐Proposition98GeneralFundforProposition39job‐training programs administered by the California Conservation Corps ($5 million) and the CaliforniaWorkforceInvestmentBoard($3million).

10

PERRISELEMENTARYSCHOOLDISTRICTManagement’sDiscussionandAnalysis(Unaudited)FortheFiscalYearEndedJune30,2014

FACTORSBEARINGONTHEDISTRICT’SFUTURE(continued)Chapter751ObligationMakesFinal$410MillionPaymentonOutstandingProposition98ObligationsFrom2004‐05and2005‐06The2014‐15budgetmakesafinal$410millionpaymenttoretirethestate’sobligationsetforthinChapter751, Statutes of 2006 (SB 1133, Torlakson). Chapter 751 required the state to provide additional annualschool and community college payments until a total of $2.8 billion had been provided. Of the amountprovidedinthebudgetpackage,$316millionisforcontinuedfundingoftheQEIAprogram($268millionforschoolsand$48millionforcommunitycolleges)and$94millionistopaydownaseparatestateobligationrelatedtoschoolfacilityrepairs.K‐12EducationThelargestK‐12augmentationisforthesecond‐yearphaseinoftherecentlyadoptedLocalControlFundingFormula(LCFF).Thebudgetalsoincludesseveralotherschool‐specificaugmentations—someofwhichrelatetoschooloperationsandsomeofwhichrelatetoschoolinfrastructure.Inadditiontothesebudgetactions,theLegislature adopted trailer legislation relating to school district reserves and independent study (IS)programs.OperationalFundingProvides$4.7BillionforLCFFImplementationThebudgetplanincludes$4.7billioninadditionalfundingfortheschooldistrictLCFF—resultinginper‐pupilLCFF funding that is12percenthigher than2013‐14 levels.Theadditional funding issufficient toclose29percentofthegapbetweendistricts’2013‐14fundinglevelsandtheirtargetfundingrates.Weestimatethe2014‐15fundinglevelisapproximately80percentofthefullimplementationcost.Thebudgetalsoincludes$26millionfortheLCFFforcountyofficesofeducation(COEs).ThisincreaseissufficienttobringallCOEsuptotheirLCFFfundingtargetsin2014‐15.OtherNotableK‐12ActionsThebudgetprovides$54milliontocontinueimplementationofnewstudentassessmentsand$33milliontoprovideacost‐of‐livingadjustment(COLA)forseveralK‐12programs(includingspecialeducationandchildnutritionprograms).InfrastructureAllocates$189MillionforEmergencyRepairProgram(ERP)Chapter899,Statutesof2004(SB6,Alpert),createdtheERPto fundcriticalrepairprojectsatcertain low‐performingschools.Chapter899requiresthestatetocontributeatotalof$800millionfortheprogram.Thestatehasprovided$338milliontodate.Thebudgetprovides$189millionfortheERPin2014‐15.Allocates$27MillioninOne‐TimeFundsforSchoolInternetInfrastructureThe budget includes $27 million in one‐time Proposition 98 funding for schools to purchase Internetconnectivity infrastructure upgrades required to administer new computer‐based tests. Grantees are to beselectedbasedontheresultsofastatewideassessmentofschools’InternetconnectivityinfrastructuretobecompletedbytheK‐12High‐SpeedNetwork(HSN)byMarch1,2015.

11

PERRISELEMENTARYSCHOOLDISTRICTManagement’sDiscussionandAnalysis(Unaudited)FortheFiscalYearEndedJune30,2014

FACTORSBEARINGONTHEDISTRICT’SFUTURE(continued)ShiftsRemainingBondAuthorityAmongCertainSchoolFacilityProgramsThe budget package shifts remaining bond authority from the Career Technical Education (CTE) andHighPerformance Incentive (HPI) school facility programs to the New Construction andModernization facilityprograms.LocalReservesRequiresSchoolDistrictstoDiscloseandJustifyReservesChapter 32, Statutes of 2014 (SB 858, Committee on Budget and Fiscal Review), creates new disclosurerequirements effective beginning in 2015‐16 for districts that have reserves exceeding state‐specifiedminimums. If a district’s budget reserve exceeds the state minimum, Chapter 32 requires the district toidentify the amount of reserves that exceed the minimum and explain why the higher reserve levels arenecessary.ThedistrictmustdisclosethisinformationinapublicmeetingandeachtimeitsubmitsabudgettoitsCOE.CapsLocalReservesSomeYearsUnderProposition2Proposition2ontheNovember2014ballotsetforthnewconstitutionalprovisionsrelatingtostatereserves,including provisions relating to a new state reserve for schools. With the voters approvingProposition2,certainprovisionsofChapter32gointoeffect.Theseprovisionscapschooldistricts’reservelevelstheyearafterthestatemakesadepositintothenewstatereserveforschools.Thecapsformostdistrictswillrangefrom3percentto10percentofadistrict’sannualexpenditures.AllofthesefactorswereconsideredinpreparingthePerrisElementarySchoolDistrictbudgetforthe2014‐15fiscalyear.CONTACTINGTHEDISTRICT’SFINANCIALMANAGEMENTThis financial report is designed toprovideour citizens, taxpayers, customers, and investors and creditorswith a general overview of the District’s finances and to demonstrate the District’s accountability for themoney it receives. If you have any questions about this report or need additional financial information,contactTinaDaigneault,CBO,DistrictBusinessOfficeat(951)657‐3118.

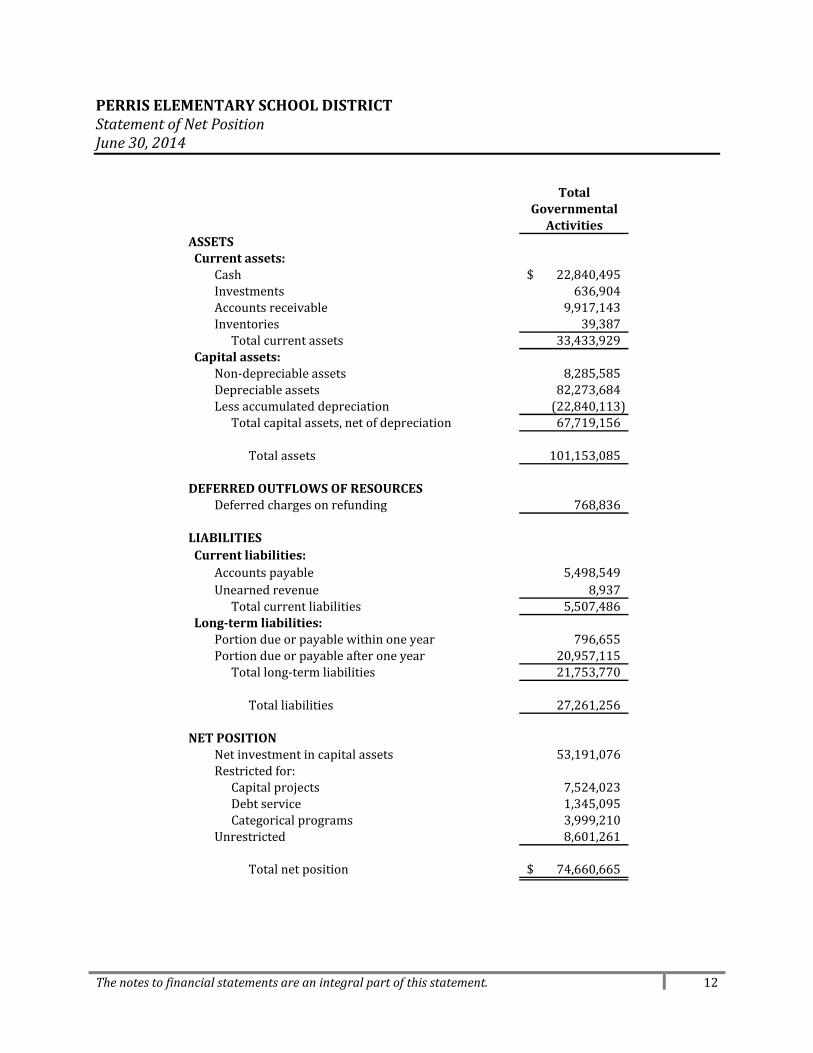

Thenotestofinancialstatementsareanintegralpartofthisstatement. 12

PERRISELEMENTARYSCHOOLDISTRICTStatementofNetPositionJune30,2014

TotalGovernmentalActivities

ASSETSCurrentassets:

Cash 22,840,495$Investments 636,904Accountsreceivable 9,917,143Inventories 39,387

Totalcurrentassets 33,433,929Capitalassets:

Non‐depreciableassets 8,285,585Depreciableassets 82,273,684Lessaccumulateddepreciation (22,840,113)

Totalcapitalassets,netofdepreciation 67,719,156

Totalassets 101,153,085

DEFERREDOUTFLOWSOFRESOURCESDeferredchargesonrefunding 768,836

LIABILITIESCurrentliabilities:

Accountspayable 5,498,549Unearnedrevenue 8,937

Totalcurrentliabilities 5,507,486Long‐termliabilities:

Portiondueorpayablewithinoneyear 796,655Portiondueorpayableafteroneyear 20,957,115

Totallong‐termliabilities 21,753,770

Totalliabilities 27,261,256

NETPOSITIONNetinvestmentincapitalassets 53,191,076Restrictedfor:

Capitalprojects 7,524,023Debtservice 1,345,095Categoricalprograms 3,999,210

Unrestricted 8,601,261

Totalnetposition 74,660,665$

Thenotestofinancialstatementsareanintegralpartofthisstatement. 13

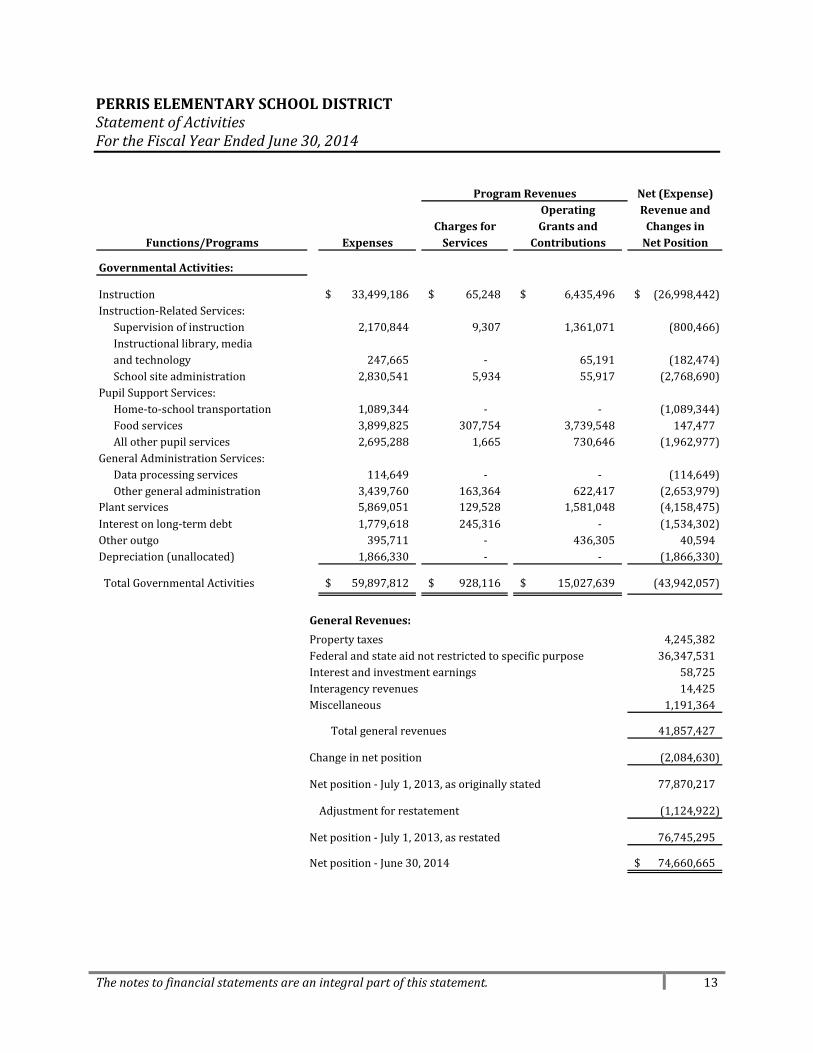

PERRISELEMENTARYSCHOOLDISTRICTStatementofActivitiesFortheFiscalYearEndedJune30,2014

Net(Expense)Operating Revenueand

Chargesfor Grantsand ChangesinExpenses Services Contributions NetPosition

GovernmentalActivities:

Instruction 33,499,186$ 65,248$ 6,435,496$ (26,998,442)$Instruction‐RelatedServices:

Supervisionofinstruction 2,170,844 9,307 1,361,071 (800,466)Instructionallibrary,mediaandtechnology 247,665 ‐ 65,191 (182,474)Schoolsiteadministration 2,830,541 5,934 55,917 (2,768,690)

PupilSupportServices:Home‐to‐schooltransportation 1,089,344 ‐ ‐ (1,089,344)Foodservices 3,899,825 307,754 3,739,548 147,477Allotherpupilservices 2,695,288 1,665 730,646 (1,962,977)

GeneralAdministrationServices:Dataprocessingservices 114,649 ‐ ‐ (114,649)Othergeneraladministration 3,439,760 163,364 622,417 (2,653,979)

Plantservices 5,869,051 129,528 1,581,048 (4,158,475)Interestonlong‐termdebt 1,779,618 245,316 ‐ (1,534,302)Otheroutgo 395,711 ‐ 436,305 40,594Depreciation(unallocated) 1,866,330 ‐ ‐ (1,866,330)

TotalGovernmentalActivities 59,897,812$ 928,116$ 15,027,639$ (43,942,057)

GeneralRevenues:

Propertytaxes 4,245,382Federalandstateaidnotrestrictedtospecificpurpose 36,347,531Interestandinvestmentearnings 58,725Interagencyrevenues 14,425Miscellaneous 1,191,364

Totalgeneralrevenues 41,857,427

Changeinnetposition (2,084,630)

Netposition‐July1,2013,asoriginallystated 77,870,217

Adjustmentforrestatement (1,124,922)

Netposition‐July1,2013,asrestated 76,745,295

Netposition‐June30,2014 74,660,665$

Functions/Programs

ProgramRevenues

Thenotestofinancialstatementsareanintegralpartofthisstatement. 14

PERRISELEMENTARYSCHOOLDISTRICTBalanceSheet–GovernmentalFundsJune30,2014

GeneralFund

CharterSchoolFund

SpecialReserveforCapitalOutlayProjectsFund

Non‐MajorGovernmental

Funds

TotalGovernmental

FundsASSETS

Cash 9,870,807$ 3,597,295$ 382,021$ 8,990,372$ 22,840,495$Investments ‐ ‐ ‐ 636,904 636,904Accountsreceivable 8,077,142 957,139 ‐ 882,862 9,917,143Duefromotherfunds 1,026,164 685,318 6,692,568 502,355 8,906,405Inventories ‐ ‐ ‐ 39,387 39,387

TotalAssets 18,974,113$ 5,239,752$ 7,074,589$ 11,051,880$ 42,340,334$

LIABILITIESANDFUNDBALANCES

LiabilitiesAccountspayable 4,130,067$ 471,091$ ‐$ 605,559$ 5,206,717$Unearnedrevenue 8,937 ‐ ‐ ‐ 8,937Duetootherfunds 7,597,772 777,176 ‐ 531,457 8,906,405

TotalLiabilities 11,736,776 1,248,267 ‐ 1,137,016 14,122,059

FundBalancesNonspendable 5,000 ‐ ‐ 39,387 44,387Restricted 1,475,499 254,645 7,074,589 9,313,359 18,118,092Committed ‐ ‐ ‐ 562,118 562,118Assigned 1,846,721 3,736,840 ‐ ‐ 5,583,561Unassigned 3,910,117 ‐ ‐ ‐ 3,910,117

TotalFundBalances 7,237,337 3,991,485 7,074,589 9,914,864 28,218,275

TotalLiabilitiesandFundBalances 18,974,113$ 5,239,752$ 7,074,589$ 11,051,880$ 42,340,334$

Thenotestofinancialstatementsareanintegralpartofthisstatement. 15

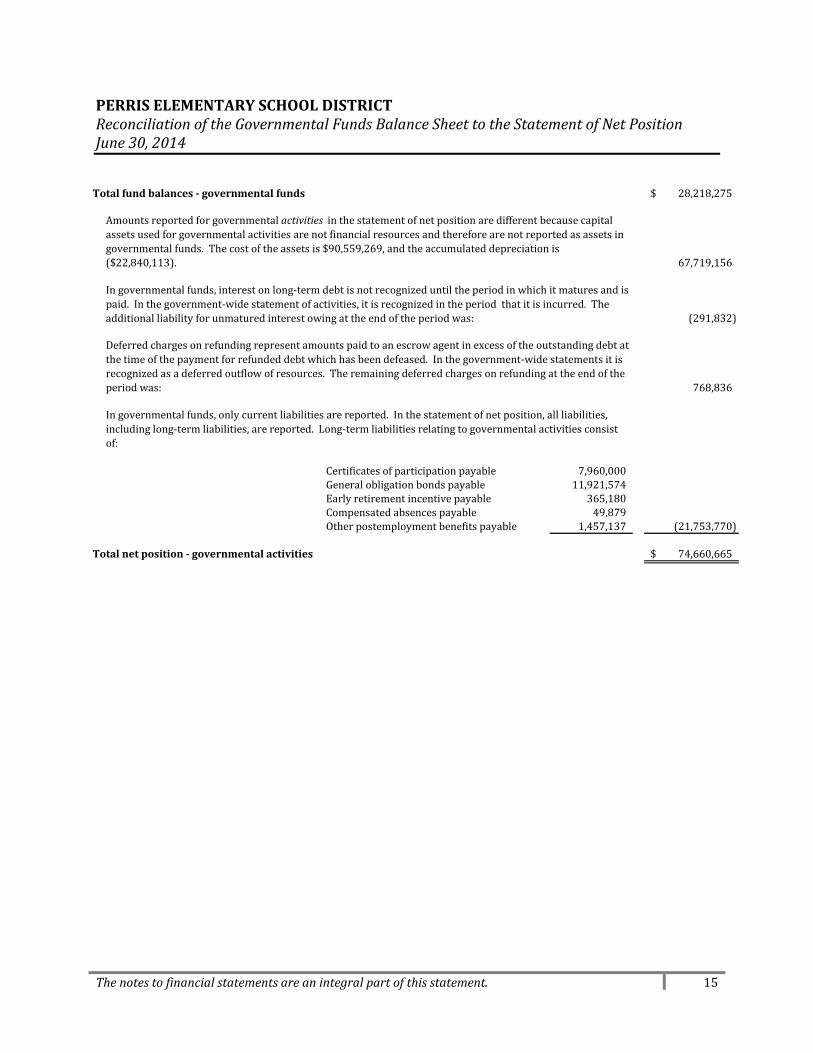

PERRISELEMENTARYSCHOOLDISTRICTReconciliationoftheGovernmentalFundsBalanceSheettotheStatementofNetPositionJune30,2014Totalfundbalances‐governmentalfunds 28,218,275$

67,719,156

(291,832)

768,836

Certificatesofparticipationpayable 7,960,000Generalobligationbondspayable 11,921,574Earlyretirementincentivepayable 365,180Compensatedabsencespayable 49,879Otherpostemploymentbenefitspayable 1,457,137 (21,753,770)

Totalnetposition‐governmentalactivities 74,660,665$

Amountsreportedforgovernmentalactivities inthestatementofnetpositionaredifferentbecausecapitalassetsusedforgovernmentalactivitiesarenotfinancialresourcesandthereforearenotreportedasassetsingovernmentalfunds.Thecostoftheassetsis$90,559,269,andtheaccumulateddepreciationis($22,840,113).

Ingovernmentalfunds,interestonlong‐termdebtisnotrecognizeduntiltheperiodinwhichitmaturesandispaid.Inthegovernment‐widestatementofactivities,itisrecognizedintheperiodthatitisincurred.Theadditionalliabilityforunmaturedinterestowingattheendoftheperiodwas:

Deferredchargesonrefundingrepresentamountspaidtoanescrowagentinexcessoftheoutstandingdebtatthetimeofthepaymentforrefundeddebtwhichhasbeendefeased.Inthegovernment‐widestatementsitisrecognizedasadeferredoutflowofresources.Theremainingdeferredchargesonrefundingattheendoftheperiodwas:

Ingovernmentalfunds,onlycurrentliabilitiesarereported.Inthestatementofnetposition,allliabilities,includinglong‐termliabilities,arereported.Long‐termliabilitiesrelatingtogovernmentalactivitiesconsistof:

Thenotestofinancialstatementsareanintegralpartofthisstatement. 16

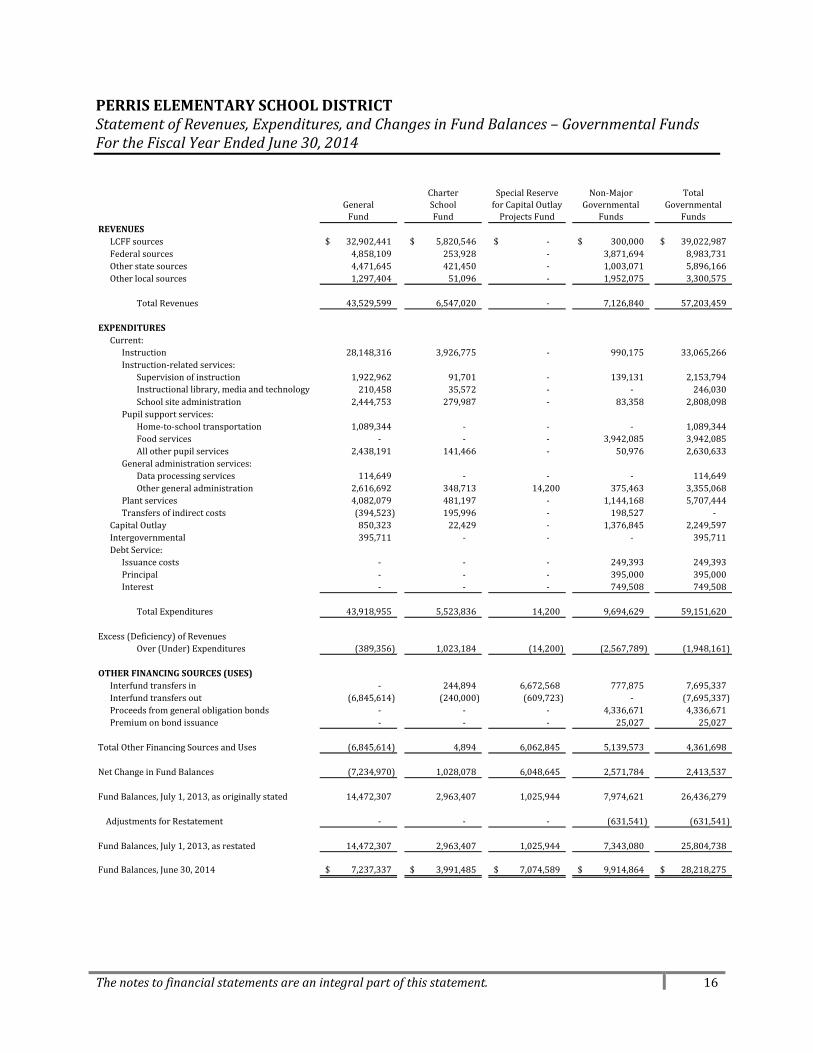

PERRISELEMENTARYSCHOOLDISTRICTStatementofRevenues,Expenditures,andChangesinFundBalances–GovernmentalFundsFortheFiscalYearEndedJune30,2014

GeneralFund

CharterSchoolFund

SpecialReserveforCapitalOutlayProjectsFund

Non‐MajorGovernmental

Funds

TotalGovernmental

FundsREVENUES

LCFFsources 32,902,441$ 5,820,546$ ‐$ 300,000$ 39,022,987$Federalsources 4,858,109 253,928 ‐ 3,871,694 8,983,731Otherstatesources 4,471,645 421,450 ‐ 1,003,071 5,896,166Otherlocalsources 1,297,404 51,096 ‐ 1,952,075 3,300,575

TotalRevenues 43,529,599 6,547,020 ‐ 7,126,840 57,203,459

EXPENDITURESCurrent:

Instruction 28,148,316 3,926,775 ‐ 990,175 33,065,266Instruction‐relatedservices:

Supervisionofinstruction 1,922,962 91,701 ‐ 139,131 2,153,794Instructionallibrary,mediaandtechnology 210,458 35,572 ‐ ‐ 246,030Schoolsiteadministration 2,444,753 279,987 ‐ 83,358 2,808,098

Pupilsupportservices:Home‐to‐schooltransportation 1,089,344 ‐ ‐ ‐ 1,089,344Foodservices ‐ ‐ ‐ 3,942,085 3,942,085Allotherpupilservices 2,438,191 141,466 ‐ 50,976 2,630,633

Generaladministrationservices:Dataprocessingservices 114,649 ‐ ‐ ‐ 114,649Othergeneraladministration 2,616,692 348,713 14,200 375,463 3,355,068

Plantservices 4,082,079 481,197 ‐ 1,144,168 5,707,444Transfersofindirectcosts (394,523) 195,996 ‐ 198,527 ‐

CapitalOutlay 850,323 22,429 ‐ 1,376,845 2,249,597Intergovernmental 395,711 ‐ ‐ ‐ 395,711DebtService:

Issuancecosts ‐ ‐ ‐ 249,393 249,393Principal ‐ ‐ ‐ 395,000 395,000Interest ‐ ‐ ‐ 749,508 749,508

TotalExpenditures 43,918,955 5,523,836 14,200 9,694,629 59,151,620

Excess(Deficiency)ofRevenuesOver(Under)Expenditures (389,356) 1,023,184 (14,200) (2,567,789) (1,948,161)

OTHERFINANCINGSOURCES(USES)Interfundtransfersin ‐ 244,894 6,672,568 777,875 7,695,337Interfundtransfersout (6,845,614) (240,000) (609,723) ‐ (7,695,337)Proceedsfromgeneralobligationbonds ‐ ‐ ‐ 4,336,671 4,336,671Premiumonbondissuance ‐ ‐ ‐ 25,027 25,027

TotalOtherFinancingSourcesandUses (6,845,614) 4,894 6,062,845 5,139,573 4,361,698

NetChangeinFundBalances (7,234,970) 1,028,078 6,048,645 2,571,784 2,413,537

14,472,307 2,963,407 1,025,944 7,974,621 26,436,279

‐ ‐ ‐ (631,541) (631,541)

14,472,307 2,963,407 1,025,944 7,343,080 25,804,738

FundBalances,June30,2014 7,237,337$ 3,991,485$ 7,074,589$ 9,914,864$ 28,218,275$

FundBalances,July1,2013,asoriginallystated

AdjustmentsforRestatement

FundBalances,July1,2013,asrestated

Thenotestofinancialstatementsareanintegralpartofthisstatement. 17

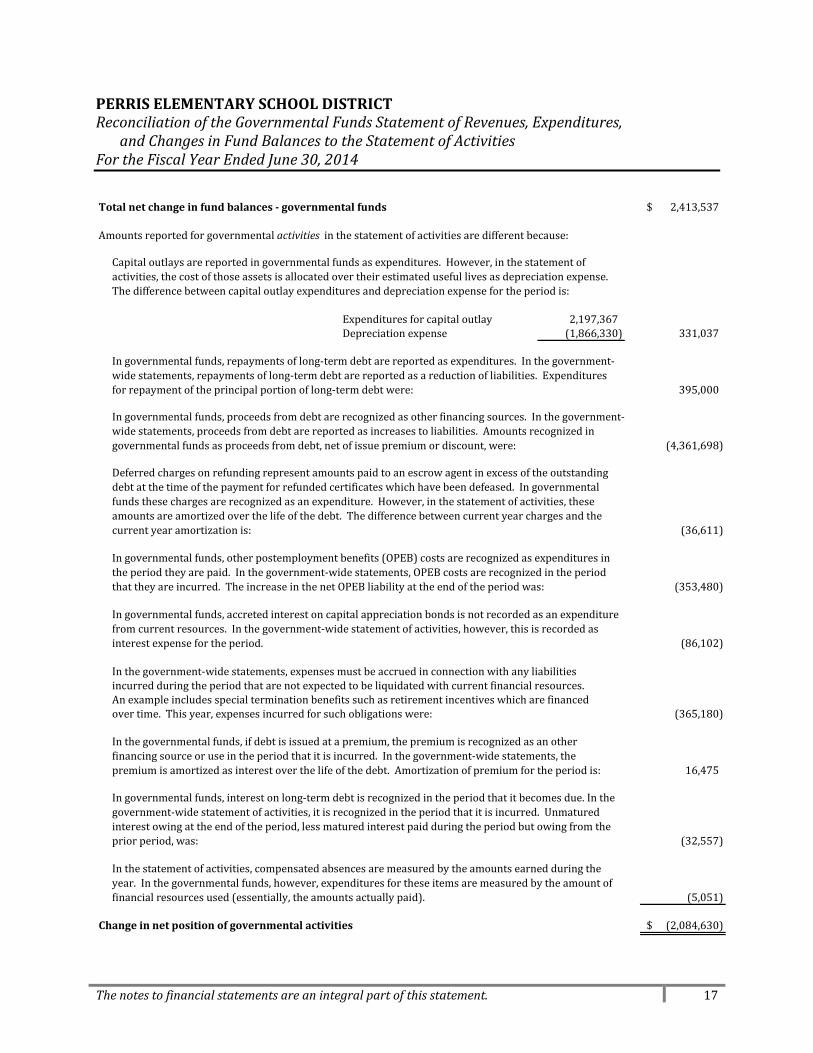

PERRISELEMENTARYSCHOOLDISTRICTReconciliationoftheGovernmentalFundsStatementofRevenues,Expenditures, andChangesinFundBalancestotheStatementofActivitiesFortheFiscalYearEndedJune30,2014Totalnetchangeinfundbalances‐governmentalfunds 2,413,537$

Expendituresforcapitaloutlay 2,197,367Depreciationexpense (1,866,330) 331,037

395,000

(4,361,698)

(36,611)

(353,480)

(86,102)

incurredduringtheperiodthatarenotexpectedtobeliquidatedwithcurrentfinancialresources.Anexampleincludesspecialterminationbenefitssuchasretirementincentiveswhicharefinancedovertime.Thisyear,expensesincurredforsuchobligationswere: (365,180)

16,475

(32,557)

(5,051)

Changeinnetpositionofgovernmentalactivities (2,084,630)$

Ingovernmentalfunds,interestonlong‐termdebtisrecognizedintheperiodthatitbecomesdue.Inthegovernment‐widestatementofactivities,itisrecognizedintheperiodthatitisincurred.Unmaturedinterestowingattheendoftheperiod,lessmaturedinterestpaidduringtheperiodbutowingfromthepriorperiod,was:

Inthestatementofactivities,compensatedabsencesaremeasuredbytheamountsearnedduringtheyear.Inthegovernmentalfunds,however,expendituresfortheseitemsaremeasuredbytheamountoffinancialresourcesused(essentially,theamountsactuallypaid).

Amountsreportedforgovernmentalactivities inthestatementofactivitiesaredifferentbecause:

Capitaloutlaysarereportedingovernmentalfundsasexpenditures.However,inthestatementofactivities,thecostofthoseassetsisallocatedovertheirestimatedusefullivesasdepreciationexpense.Thedifferencebetweencapitaloutlayexpendituresanddepreciationexpensefortheperiodis:

Ingovernmentalfunds,repaymentsoflong‐termdebtarereportedasexpenditures.Inthegovernment‐widestatements,repaymentsoflong‐termdebtarereportedasareductionofliabilities.Expendituresforrepaymentoftheprincipalportionoflong‐termdebtwere:

Deferredchargesonrefundingrepresentamountspaidtoanescrowagentinexcessoftheoutstandingdebtatthetimeofthepaymentforrefundedcertificateswhichhavebeendefeased.Ingovernmentalfundsthesechargesarerecognizedasanexpenditure.However,inthestatementofactivities,theseamountsareamortizedoverthelifeofthedebt.Thedifferencebetweencurrentyearchargesandthecurrentyearamortizationis:

Ingovernmentalfunds,otherpostemploymentbenefits(OPEB)costsarerecognizedasexpendituresintheperiodtheyarepaid.Inthegovernment‐widestatements,OPEBcostsarerecognizedintheperiodthattheyareincurred.TheincreaseinthenetOPEBliabilityattheendoftheperiodwas:

Ingovernmentalfunds,proceedsfromdebtarerecognizedasotherfinancingsources.Inthegovernment‐widestatements,proceedsfromdebtarereportedasincreasestoliabilities.Amountsrecognizedingovernmentalfundsasproceedsfromdebt,netofissuepremiumordiscount,were:

Ingovernmentalfunds,accretedinterestoncapitalappreciationbondsisnotrecordedasanexpenditurefromcurrentresources.Inthegovernment‐widestatementofactivities,however,thisisrecordedasinterestexpensefortheperiod.

Inthegovernment‐widestatements,expensesmustbeaccruedinconnectionwithanyliabilities

Inthegovernmentalfunds,ifdebtisissuedatapremium,thepremiumisrecognizedasanotherfinancingsourceoruseintheperiodthatitisincurred.Inthegovernment‐widestatements,thepremiumisamortizedasinterestoverthelifeofthedebt.Amortizationofpremiumfortheperiodis:

Thenotestofinancialstatementsareanintegralpartofthisstatement. 18

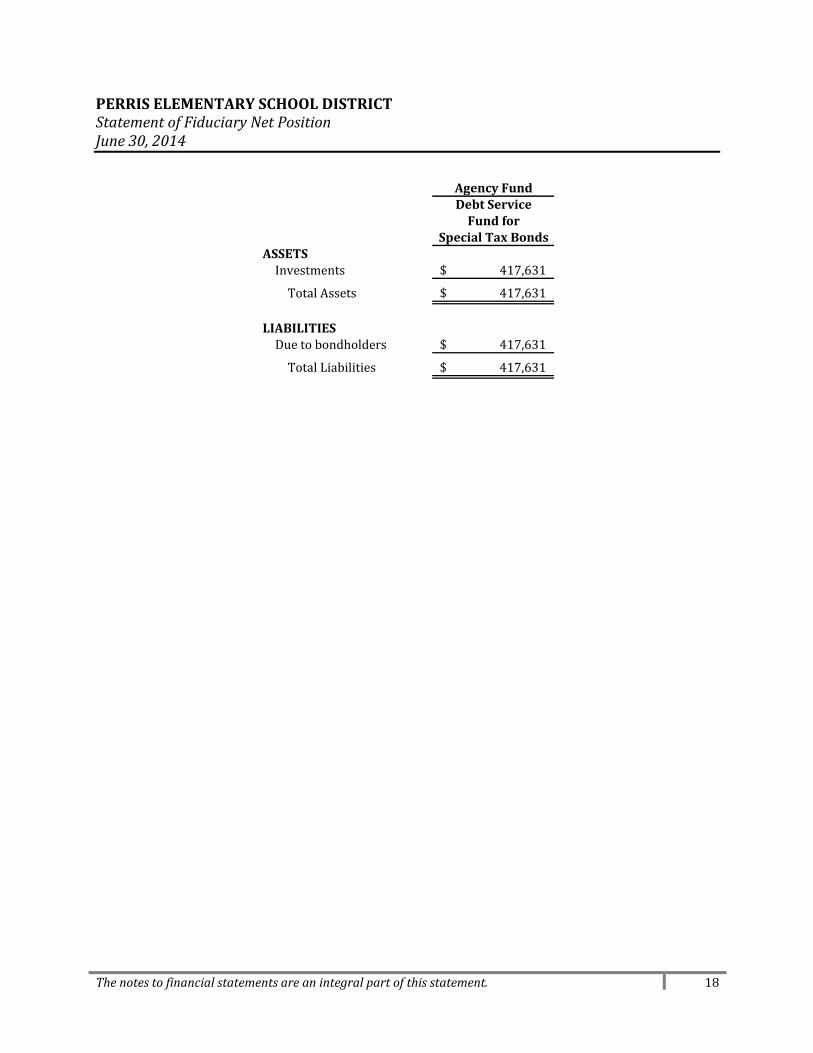

PERRISELEMENTARYSCHOOLDISTRICTStatementofFiduciaryNetPositionJune30,2014

AgencyFundDebtServiceFundfor

SpecialTaxBondsASSETSInvestments 417,631$

TotalAssets 417,631$

LIABILITIESDuetobondholders 417,631$

TotalLiabilities 417,631$

19

PERRISELEMENTARYSCHOOLDISTRICTNotestoFinancialStatementsJune30,2014NOTE1–SIGNIFICANTACCOUNTINGPOLICIESA. ReportingEntity

A reporting entity is comprised of the primary government, component units, and other organizationsthatareincludedtoensurethefinancialstatementsarenotmisleading.TheprimarygovernmentoftheDistrictconsistsofallfunds,departments,andagenciesthatarenotlegallyseparatefromtheDistrict.ForPerris Elementary School District, this includes general operations, food service, and student relatedactivitiesoftheDistrict.ComponentunitsarelegallyseparateorganizationsforwhichtheDistrictisfinanciallyaccountable.TheDistrict'scomponentunitsaresointertwinedwiththeDistrictthattheyare,insubstance,thesameastheDistrict and, therefore, are blended and reported as if they were part of the District. The District'sGoverningBoardalsoservesasthegoverningboardforthePerrisSchoolDistrictFacilitiesCorporationandtheCommunityFacilitiesDistricts.AlthoughtheboardmembersofthecorporationandCommunityFacilitiesDistrictsarethesameastheDistrictBoard,thecorporationandCFDsexistsolelytofinancetheacquisitionandconstructionofequipmentandfacilitiesfortheDistrict.

ComponentUnit

IncludedintheReportingEntityBecause:

SeparateFinancialStatements

Perris School District FacilitiesCorporationwasformedforthesolepurpose of providing financialassistance to the District byacquiring, constructing, financing,selling and leasing public facilities,land, personal property andequipment for theuseandbenefitofthe District. The District leasescertain school facilities from thecorporation under a lease‐purchaseagreementdatedJune1,1994.

GoverningboardcomposesboardofFacilitiesCorporation

Notprepared.

Community Facilities Districts(CFD): On August 13, 2002, theDistrictenteredintoanagreementtoform Community Facilities District(CFD) No. 2002‐1 of PerrisElementary School District. Thepurpose of the agreements is toprovide for the issuance of bonds toprovide and finance the design,acquisition and construction ofcertain public facilities, pursuant totheMello‐Roos Community FacilitiesActof1982,asamended.TheCFDisauthorized to levy special taxes onparcelsoftaxablepropertywithintheCFDtopaytheprincipalandinterestonthebonds.

GoverningboardcomposesboardofCFD

Notprepared.

20

PERRISELEMENTARYSCHOOLDISTRICTNotestoFinancialStatementsJune30,2014NOTE1–SIGNIFICANTACCOUNTINGPOLICIES(continued)B. BasisofPresentation,BasisofAccounting

1. BasisofPresentationGovernment‐WideFinancialStatementsThestatementofnetpositionandthestatementofactivitiesdisplayinformationabouttheprimarygovernment(theDistrict)anditscomponentunits.Thesestatementsincludethefinancialactivitiesoftheoverallgovernment,exceptforfiduciaryactivities. Eliminationshavebeenmadetominimizethe double‐counting of internal activities. Governmental activities generally are financed throughtaxes,intergovernmentalrevenues,andothernonexchangetransactions.ThestatementofactivitiespresentsacomparisonbetweendirectexpensesandprogramrevenuesforeachfunctionoftheDistrict'sgovernmentalactivities.Directexpensesarethosethatarespecificallyassociatedwithaprogramorfunctionand,therefore,areclearlyidentifiabletoaparticularfunction.Program revenues include (a) fees, fines, and charges paid by the recipients of goods or servicesoffered by the programs and (b) grants and contributions that are restricted to meeting theoperational or capital requirements of a particular program. Revenues that are not classified asprogramrevenues,includingalltaxes,arepresentedasgeneralrevenues.FundFinancialStatementsThefundfinancialstatementsprovide informationabouttheDistrict's funds, including its fiduciaryfunds (andblended componentunits). Separate statements for each fundcategory ‐governmentaland fiduciary ‐arepresented. Theemphasisoffundfinancialstatementsisonmajorgovernmentalfunds,eachdisplayed inaseparatecolumn. All remaininggovernmental fundsareaggregatedandreportedasnonmajorfunds.MajorGovernmentalFundsTheDistrictreportsthefollowingmajorgovernmentalfunds:

GeneralFund:ThisfundisthegeneraloperatingfundoftheDistrict.Itisusedtoaccountforallfinancialresourcesexceptthoserequiredtobeaccountedforinanotherfund.TheDistrictalsomaintains a SpecialReserveFund forOtherThanCapitalOutlayProjects. TheSpecialReserveFund for Other Than Capital Outlay Projects is not substantially composed of restricted orcommitted revenue sources, anddoes notmeet thedefinitionof a special revenue fundunderGASB54.TheactivityinthefundisbeingreportedwithintheGeneralFund.CharterSchoolFund:ThisfundisusedtoaccountfortheoperationsoftheInnovativeHorizonsCharterSchool.SpecialReserveFundforCapitalOutlayProjects: ThisfundisusedtoaccountforfundssetasideforBoarddesignatedconstructionprojects.

21

PERRISELEMENTARYSCHOOLDISTRICTNotestoFinancialStatementsJune30,2014NOTE1–SIGNIFICANTACCOUNTINGPOLICIES(continued)

B. BasisofPresentation,BasisofAccounting(continued)

1. BasisofPresentation(continued)

Non‐MajorGovernmentalFundsTheDistrictmaintainsthefollowingnon‐majorgovernmentalfunds:

SpecialReserveFunds:

ChildDevelopmentFund: This fund isused to account for resources committed to childdevelopmentprogramsmaintainedbytheDistrict.CafeteriaFund:ThisfundisusedtoaccountforrevenuesreceivedandexpendituresmadetooperatetheDistrict'sfoodserviceoperations.DeferredMaintenance Fund: This fund is used to account for resources committed tomajorrepairorreplacementofDistrictproperty.

CapitalProjectsFunds:

CapitalFacilitiesFund:ThisfundisusedtoaccountforresourcesreceivedfromdeveloperimpactfeesassessedunderprovisionsoftheCaliforniaEnvironmentalQualityAct.CapitalProjectsFundforBlendedComponentUnits:ThisfundisusedtoaccountfortheactivityoftheCertificatesofParticipationandoftheCommunityFacilitiesDistricts.

DebtServiceFunds:

BondInterestandRedemptionFund:Thisfundisusedtoaccountfortheaccumulationofresourcesfor,andtherepaymentof,Districtbonds,interest,andrelatedcosts.DebtServiceFund forBlendedComponentUnits: This fund is used to account for theaccumulationofresourcesfortherepaymentofcertificatesofparticipation.

FiduciaryFundFiduciary fund reporting focuses onnet position and changes in net position. Fiduciary funds areusedtoreportassetsheldinatrusteeoragencycapacityforothersandthereforecannotbeusedtosupport the District’s own programs. The fiduciary fund category includes pension (and otheremployeebenefit)trustfunds,investmenttrustfunds,private‐purposetrustfunds,andagencyfunds.TheDistrictmaintainsthefollowingfiduciaryfund:

DebtServiceFundforSpecialTaxBonds:Thisfundisusedtoaccountfortheaccumulationofresourcesfortherepaymentofspecialtaxbonds.

22

PERRISELEMENTARYSCHOOLDISTRICTNotestoFinancialStatementsJune30,2014NOTE1–SIGNIFICANTACCOUNTINGPOLICIES(continued)

B. BasisofPresentation,BasisofAccounting(continued)

2. MeasurementFocus,BasisofAccounting

Government‐WideandFiduciaryFundFinancialStatementsThe government‐wide and fiduciary fund financial statements are reported using the economicresources measurement focus and the accrual basis of accounting. Revenues are recorded whenearnedandexpensesarerecordedatthetimeliabilitiesareincurred,regardlessofwhentherelatedcash flows take place. Nonexchange transactions, in which the District gives (or receives) valuewithout directly receiving (or giving) equal value in exchange, include property taxes, grants,entitlements,anddonations. Onanaccrualbasis,revenuefrompropertytaxes isrecognizedinthefiscalyearinwhichalleligibilityrequirementshavebeensatisfied.GovernmentalFundFinancialStatementsGovernmental fundsarereportedusingthecurrent financialresourcesmeasurement focusandthemodifiedaccrualbasisofaccounting.Underthismethod,revenuesarerecognizedwhenmeasurableandavailable.TheDistrictconsidersallrevenuesreportedinthegovernmentalfundstobeavailableif the revenues are collectedwithin 60 days after year‐end. Expenditures are recordedwhen therelatedfundliabilityis incurred,exceptforprincipalandinterestongenerallong‐termdebt,claimsandjudgments,andcompensatedabsences,whicharerecognizedasexpenditurestotheextenttheyhave matured. Capital asset acquisitions are reported as expenditures in governmental funds.Proceedsofgenerallong‐termdebtandfinancingfromcapitalleasesarereportedasotherfinancingsources.

C. BudgetaryDataThe budgetary process is prescribed by provisions of the California Education Code and requires thegoverningboardtoholdapublichearingandadoptanoperatingbudgetnolaterthanJuly1ofeachyear.TheDistrictgoverningboardsatisfiedtheserequirements.Theadoptedbudgetissubjecttoamendmentthroughouttheyeartogiveconsiderationtounanticipatedrevenueandexpendituresprimarilyresultingfromeventsunknownatthetimeofbudgetadoptionwiththelegalrestrictionthatexpenditurescannotexceedappropriationsbymajorobjectaccount.Theamountsreportedastheoriginalbudgetedamountsinthebudgetarystatementsreflecttheamountswhentheoriginalappropriationswereadopted.Theamountsreportedasthefinalbudgetedamountsinthebudgetarystatementsreflecttheamountsafterallbudgetamendmentshavebeenaccountedfor.Forbudgetpurposes,onbehalfpaymentshavenotbeen includedasrevenueandexpendituresasrequiredundergenerallyacceptedaccountingprinciples.

D. EncumbrancesEncumbranceaccounting isused inallbudgeted funds toreserveportionsofapplicableappropriationsforwhichcommitmentshavebeenmade.Encumbrancesarerecordedforpurchaseorders,contracts,andother commitmentswhen they arewritten. Encumbrances are liquidatedwhen the commitments arepaid.AllencumbrancesareliquidatedasofJune30.

23

PERRISELEMENTARYSCHOOLDISTRICTNotestoFinancialStatementsJune30,2014NOTE1–SIGNIFICANTACCOUNTINGPOLICIES(continued)E. Assets,DeferredOutflowsofResources,Liabilities,andNetPosition

1. CashandCashEquivalents

The District considers cash and cash equivalents to be cash on hand and demand deposits. Inaddition, because theTreasuryPool is sufficiently liquid to permitwithdrawal of cash at any timewithoutpriornoticeorpenalty,equityinthepoolisalsodeemedtobeacashequivalent.

2. InventoriesandPrepaidItemsInventoriesarevaluedatcostusingthefirst‐in/first‐out(FIFO)method.Thecostsofgovernmentalfund‐typeinventoriesarerecordedasexpenditureswhenconsumedratherthanwhenpurchased.Certainpaymentstovendorsreflectcostsapplicabletofutureaccountingperiodsandarerecordedasprepaiditems.

3. CapitalAssetsPurchased or constructed capital assets are reported at cost or estimatedhistorical cost. Donatedfixed assets are recorded at their estimated fair value at thedateofdonation. The costofnormalmaintenanceandrepairs thatdonotaddtothevalueof theassetormateriallyextendassets' livesarenotcapitalized.Capital assets are depreciated using the straight‐line method over the following estimated usefullives:

Description EstimatedLivesBuildingsandImprovements 25‐50yearsFurnitureandEquipment 15‐20yearsVehicles 8years

4. CompensatedAbsences

The liability for compensated absences reported in the government‐wide statements consists ofunpaid, accumulated vacation leave balances. The liability has been calculated using the vestingmethod,inwhichleaveamountsforbothemployeeswhocurrentlyareeligibletoreceiveterminationpayments and other employeeswho are expected to become eligible in the future to receive suchpaymentsuponterminationareincluded.

5. PropertyTaxCalendarTheCountyisresponsiblefortheassessment,collection,andapportionmentofpropertytaxesforalljurisdictionsincludingtheschoolsandspecialdistrictswithintheCounty.TheBoardofSupervisorsleviespropertytaxesasofSeptember1onpropertyvaluesassessedonJuly1.Securedpropertytaxpaymentsaredueintwoequalinstallments.ThefirstisgenerallydueNovember1andisdelinquentwithpenaltiesonDecember10,andthesecondisgenerallydueonFebruary1andisdelinquentwithpenaltiesonApril10.SecuredpropertytaxesbecomealienonthepropertyonJanuary1.

24

PERRISELEMENTARYSCHOOLDISTRICTNotestoFinancialStatementsJune30,2014

NOTE1–SIGNIFICANTACCOUNTINGPOLICIES(continued)E. Assets,DeferredOutflowsofResources,Liabilities,andNetPosition(continued)

6. FundBalances

Thefundbalanceforgovernmentalfundsisreportedinclassificationsbasedontheextenttowhichthegovernment isboundtohonorconstraintsonthespecificpurposesforwhichamounts inthosefundscanbespent.Nonspendable: Fund balance is reported as nonspendable when the resources cannot be spentbecausetheyareeitherinanonspendableformorlegallyorcontractuallyrequiredtobemaintainedintact.Resourcesinnonspendableformincludeinventoriesandprepaidassets.Restricted: Fund balance is reported as restricted when the constraints placed on the use ofresourcesareeitherexternallyimposedbycreditors,grantors,contributors,orlawsorregulationsofothergovernments;orimposedbylawthroughconstitutionalprovisionorbyenablinglegislation.Committed:TheDistrict'shighestdecision‐makinglevelofauthorityrestswiththeDistrict'sBoard.Fund balance is reported as committed when the Board passes a resolution that places specifiedconstraints on how resources may be used. The Board can modify or rescind a commitment ofresourcesthroughpassageofanewresolution.Assigned:ResourcesthatareconstrainedbytheDistrict'sintenttousethemforaspecificpurpose,but are neither restricted nor committed, are reported as assigned fund balance. Intent may beexpressedbyeithertheBoard,committees(suchasbudgetorfinance),orofficialstowhichtheBoardhasdelegatedauthority.Unassigned: Unassigned fund balance represents fund balance that has not been restricted,committed,orassignedandmaybeutilizedbytheDistrictforanypurpose.Whenexpendituresareincurred,andbothrestrictedandunrestrictedresourcesareavailable,itistheDistrict'spolicytouserestrictedresourcesfirst,thenunrestrictedresourcesintheorderofcommitted,assigned,andthenunassigned,astheyareneeded.

7. DeferredOutflows/InflowsofResourcesIn addition to assets, the statement of net position will sometimes report a separate section fordeferred outflows of resources. This separate financial statement element, deferred outflows ofresources,representsaconsumptionofnetpositionthatappliestoafutureperiodandsowillnotberecognizedasanoutflowof resources (expense/expenditure)until then. TheDistricthasonlyoneitemthatqualifiesforreportinginthiscategory. Thisitemisdeferredamountonrefunding,whichresultedfromthedifferenceinthecarryingvalueofrefundeddebtanditsreacquisitionprice. Thisamountisshownasdeferredandamortizedovertheshorterofthelifeoftherefundedorrefundingdebt.

Inaddition to liabilities, the statementofnetpositionwill sometimes reporta separate section fordeferred inflows of resources. This separate financial statement element, deferred inflows ofresources, represents an acquisition of net position that applies to a future period andwill not berecognizedasaninflowofresources(revenue)untilthattime.TheDistricthasnodeferredinflowsofresources.

25

PERRISELEMENTARYSCHOOLDISTRICTNotestoFinancialStatementsJune30,2014

NOTE1–SIGNIFICANTACCOUNTINGPOLICIES(continued)E. Assets,DeferredOutflowsofResources,Liabilities,andNetPosition(continued)

8. NetPositionNet position is classified into three components: net investment in capital assets; restricted; andunrestricted.Theseclassificationsaredefinedasfollows: Net investment in capitalassets ‐ This component of net position consists of capital assets,

including restricted capital assets, net of accumulated depreciation and reduced by theoutstandingbalancesofanybonds,mortgages,notes,orotherborrowingsthatareattributabletothe acquisition, construction, or improvement of those assets. If there are significant unspentrelateddebtproceedsatyear‐end,theportionofthedebtattributabletotheunspentproceedsarenotincludedinthecalculationofnetinvestmentincapitalassets.Rather,thatportionofthedebtisincludedinthesamenetpositioncomponentastheunspentproceeds.

Restricted ‐This componentofnetposition consistsof constraintsplacedonnetpositionusethroughexternal constraints imposedby creditors (suchas throughdebt covenants), grantors,contributors,orlawsorregulationsofothergovernmentsorconstraintsimposedbylawthroughconstitutionalprovisionsorenablinglegislation.

Unrestrictednetposition‐Thiscomponentofnetpositionconsistsofnetpositionthatdoesnotmeetthedefinitionof"netinvestmentincapitalassets"or"restricted".

Whenbothrestrictedandunrestrictedresourcesareavailableforuse,itistheDistrict'spolicytouserestrictedresourcesfirst,thenunrestrictedresourcesastheyareneeded.

F. UseofEstimates

The preparation of financial statements in conformity with generally accepted accounting principlesrequiresmanagementtomakeestimatesandassumptionsthataffectthereportedamountsofassetsandliabilitiesanddisclosureofcontingentassetsandliabilitiesatthedateofthefinancialstatementsandthereportedamountsofrevenuesandexpendituresduringthereportedperiod. Actualresultscoulddifferfromthoseestimates.

G. NewGASBPronouncement

Duringthe2013‐14fiscalyear,thefollowingGASBPronouncementbecameeffective:StatementNo.65,ItemsPreviouslyReportedasAssetsandLiabilities(Issued03/12)This Statement establishes accounting and financial reporting standards that reclassify, as deferredoutflows of resources or deferred inflows of resources, certain items thatwerepreviously reported asassetsandliabilitiesandrecognizes,asoutflowsofresourcesorinflowsofresources,certainitemsthatwerepreviouslyreportedasassetsandliabilities.Duetotheimplementationofthisstatement,thecalculationofdeferredamountonrefundingwasrevisedto eliminate the inclusionof costs that shouldbe recognizedas anexpense in theperiod incurredandeliminated debt issuance costs which should be recognized as an expense in the period incurred.Accounting changes adopted to conform to the provisions of this statement should be appliedretroactively.TheresultoftheimplementationofthisstandardwastodecreasethenetpositionatJuly1,2013by$493,381,whichistheamountofunamortizeddebtissuancecostsatJuly1,2013.

26

PERRISELEMENTARYSCHOOLDISTRICTNotestoFinancialStatementsJune30,2014NOTE1–SIGNIFICANTACCOUNTINGPOLICIES(continued)G. NewGASBPronouncement(continued)

StatementNo.65(continued)Concepts Statement No. 4, Elements of Financial Statements, introduced and defined the elementsincluded in financial statements, including deferred outflows of resources and deferred inflows ofresources.Inaddition,ConceptsStatement4providesthatreportingadeferredoutflowofresourcesoradeferredinflowofresourcesshouldbelimitedtothoseinstancesidentifiedbytheBoardinauthoritativepronouncementsthatareestablishedafterapplicabledueprocess.This Statement also provides other financial reporting guidance related to the impact of the financialstatementelementsdeferredoutflowsofresourcesanddeferredinflowsofresources,suchaschangesinthe determination of themajor fund calculations and limiting the use of the termdeferred in financialstatementpresentations.

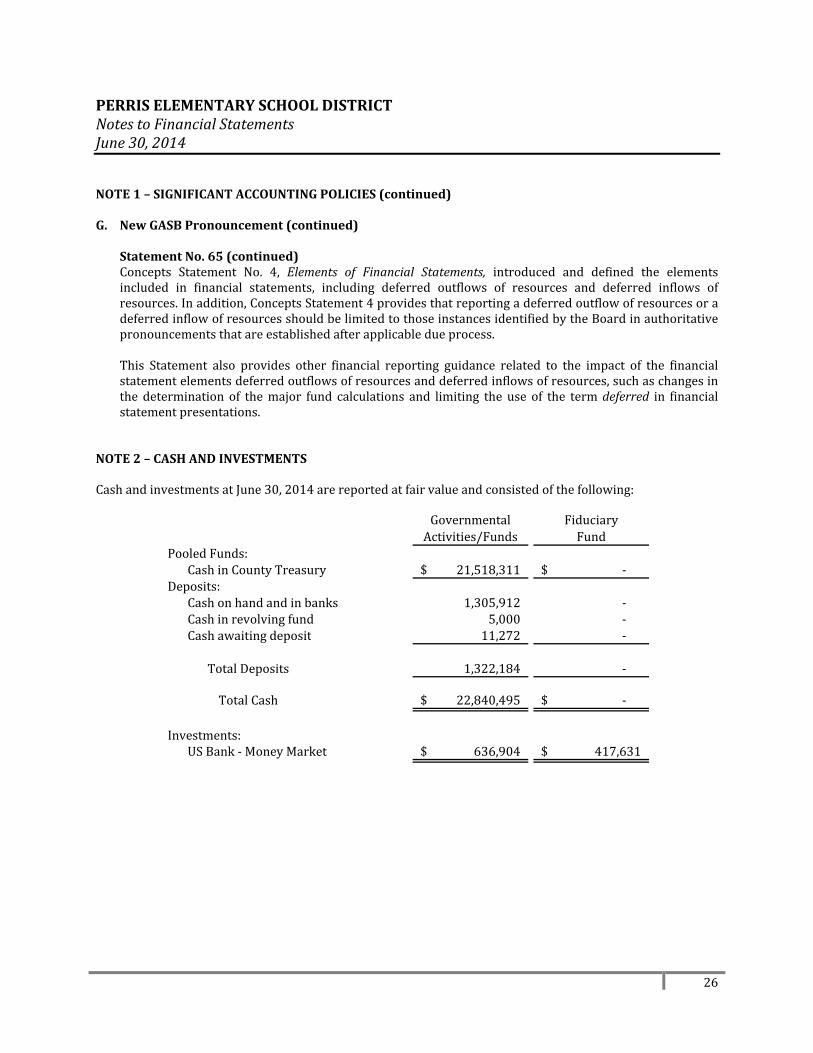

NOTE2–CASHANDINVESTMENTSCashandinvestmentsatJune30,2014arereportedatfairvalueandconsistedofthefollowing:

GovernmentalActivities/Funds

FiduciaryFund

PooledFunds:CashinCountyTreasury 21,518,311$ ‐$

Deposits:Cashonhandandinbanks 1,305,912 ‐Cashinrevolvingfund 5,000 ‐Cashawaitingdeposit 11,272 ‐

TotalDeposits 1,322,184 ‐

TotalCash 22,840,495$ ‐$

Investments:USBank‐MoneyMarket 636,904$ 417,631$

27

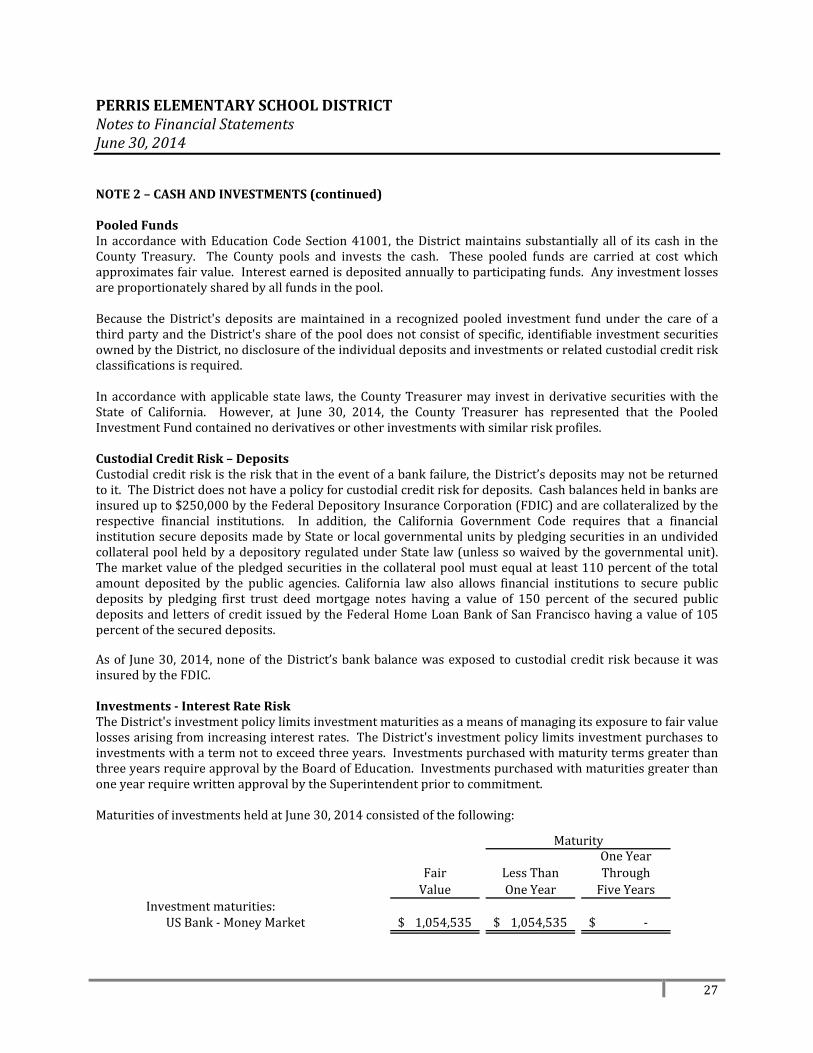

PERRISELEMENTARYSCHOOLDISTRICTNotestoFinancialStatementsJune30,2014NOTE2–CASHANDINVESTMENTS(continued)PooledFundsIn accordancewithEducationCodeSection41001, theDistrictmaintains substantiallyallof its cash in theCounty Treasury. The County pools and invests the cash. These pooled funds are carried at cost whichapproximatesfairvalue.Interestearnedisdepositedannuallytoparticipatingfunds.Anyinvestmentlossesareproportionatelysharedbyallfundsinthepool.Because theDistrict's deposits aremaintained in a recognizedpooled investment fundunder the careof athirdpartyandtheDistrict'sshareofthepooldoesnotconsistofspecific,identifiableinvestmentsecuritiesownedbytheDistrict,nodisclosureoftheindividualdepositsandinvestmentsorrelatedcustodialcreditriskclassificationsisrequired.Inaccordancewithapplicablestate laws, theCountyTreasurermay invest inderivativesecuritieswith theState of California. However, at June 30, 2014, the County Treasurer has represented that the PooledInvestmentFundcontainednoderivativesorotherinvestmentswithsimilarriskprofiles.CustodialCreditRisk–DepositsCustodialcreditriskistheriskthatintheeventofabankfailure,theDistrict’sdepositsmaynotbereturnedtoit.TheDistrictdoesnothaveapolicyforcustodialcreditriskfordeposits.Cashbalancesheldinbanksareinsuredupto$250,000bytheFederalDepositoryInsuranceCorporation(FDIC)andarecollateralizedbytherespective financial institutions. In addition, the California Government Code requires that a financialinstitutionsecuredepositsmadebyStateorlocalgovernmentalunitsbypledgingsecuritiesinanundividedcollateralpoolheldbyadepositoryregulatedunderStatelaw(unlesssowaivedbythegovernmentalunit).Themarketvalueofthepledgedsecuritiesinthecollateralpoolmustequalatleast110percentofthetotalamount deposited by the public agencies. California law also allows financial institutions to secure publicdeposits by pledging first trust deedmortgage notes having a value of 150 percent of the secured publicdepositsandlettersofcredit issuedbytheFederalHomeLoanBankofSanFranciscohavingavalueof105percentofthesecureddeposits.Asof June30,2014,noneof theDistrict’sbankbalancewasexposedtocustodialcreditriskbecauseitwasinsuredbytheFDIC.Investments‐InterestRateRiskTheDistrict'sinvestmentpolicylimitsinvestmentmaturitiesasameansofmanagingitsexposuretofairvaluelossesarisingfromincreasinginterestrates.TheDistrict'sinvestmentpolicylimitsinvestmentpurchasestoinvestmentswithatermnottoexceedthreeyears.InvestmentspurchasedwithmaturitytermsgreaterthanthreeyearsrequireapprovalbytheBoardofEducation.InvestmentspurchasedwithmaturitiesgreaterthanoneyearrequirewrittenapprovalbytheSuperintendentpriortocommitment.MaturitiesofinvestmentsheldatJune30,2014consistedofthefollowing:

FairValue

LessThanOneYear

OneYearThroughFiveYears

Investmentmaturities:USBank‐MoneyMarket 1,054,535$ 1,054,535$ ‐$

Maturity

28

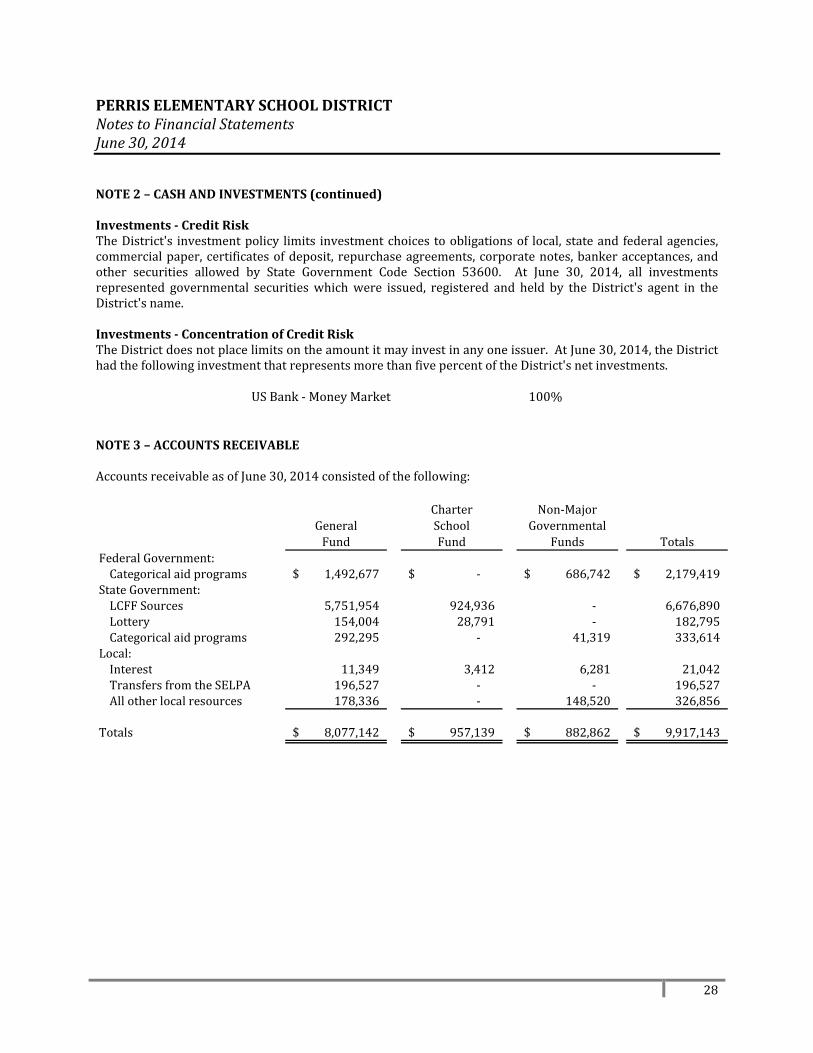

PERRISELEMENTARYSCHOOLDISTRICTNotestoFinancialStatementsJune30,2014NOTE2–CASHANDINVESTMENTS(continued)Investments‐CreditRiskTheDistrict's investmentpolicy limits investmentchoices toobligationsof local, stateandfederalagencies,commercialpaper,certificatesofdeposit, repurchaseagreements,corporatenotes,bankeracceptances,andother securities allowed by State Government Code Section 53600. At June 30, 2014, all investmentsrepresented governmental securitieswhichwere issued, registered and held by the District's agent in theDistrict'sname.Investments‐ConcentrationofCreditRiskTheDistrictdoesnotplacelimitsontheamountitmayinvestinanyoneissuer.AtJune30,2014,theDistricthadthefollowinginvestmentthatrepresentsmorethanfivepercentoftheDistrict'snetinvestments.

USBank‐MoneyMarket 100% NOTE3–ACCOUNTSRECEIVABLEAccountsreceivableasofJune30,2014consistedofthefollowing:

GeneralFund

CharterSchoolFund

Non‐MajorGovernmental

Funds TotalsFederalGovernment:Categoricalaidprograms 1,492,677$ ‐$ 686,742$ 2,179,419$

StateGovernment:LCFFSources 5,751,954 924,936 ‐ 6,676,890Lottery 154,004 28,791 ‐ 182,795Categoricalaidprograms 292,295 ‐ 41,319 333,614

Local:Interest 11,349 3,412 6,281 21,042TransfersfromtheSELPA 196,527 ‐ ‐ 196,527Allotherlocalresources 178,336 ‐ 148,520 326,856

Totals 8,077,142$ 957,139$ 882,862$ 9,917,143$

29

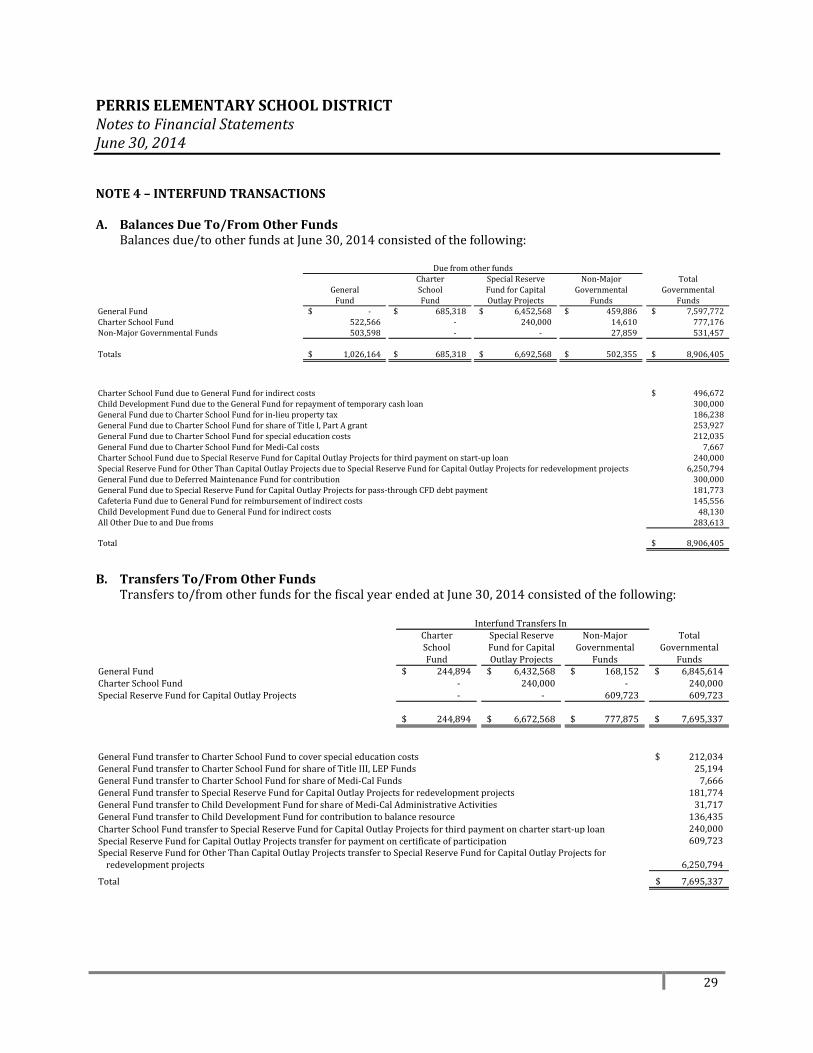

PERRISELEMENTARYSCHOOLDISTRICTNotestoFinancialStatementsJune30,2014NOTE4–INTERFUNDTRANSACTIONSA. BalancesDueTo/FromOtherFunds

Balancesdue/tootherfundsatJune30,2014consistedofthefollowing:

Charter SpecialReserve Non‐Major TotalGeneral School FundforCapital Governmental GovernmentalFund Fund OutlayProjects Funds Funds

GeneralFund ‐$ 685,318$ 6,452,568$ 459,886$ 7,597,772$CharterSchoolFund 522,566 ‐ 240,000 14,610 777,176Non‐MajorGovernmentalFunds 503,598 ‐ ‐ 27,859 531,457

Totals 1,026,164$ 685,318$ 6,692,568$ 502,355$ 8,906,405$

CharterSchoolFundduetoGeneralFundforindirectcosts 496,672$ChildDevelopmentFundduetotheGeneralFundforrepaymentoftemporarycashloan 300,000GeneralFundduetoCharterSchoolFundforin‐lieupropertytax 186,238GeneralFundduetoCharterSchoolFundforshareofTitleI,PartAgrant 253,927GeneralFundduetoCharterSchoolFundforspecialeducationcosts 212,035GeneralFundduetoCharterSchoolFundforMedi‐Calcosts 7,667CharterSchoolFundduetoSpecialReserveFundforCapitalOutlayProjectsforthirdpaymentonstart‐uploan 240,000SpecialReserveFundforOtherThanCapitalOutlayProjectsduetoSpecialReserveFundforCapitalOutlayProjectsforredevelopmentprojects 6,250,794GeneralFundduetoDeferredMaintenanceFundforcontribution 300,000GeneralFundduetoSpecialReserveFundforCapitalOutlayProjectsforpass‐throughCFDdebtpayment 181,773CafeteriaFundduetoGeneralFundforreimbursementofindirectcosts 145,556ChildDevelopmentFundduetoGeneralFundforindirectcosts 48,130AllOtherDuetoandDuefroms 283,613

Total 8,906,405$

Duefromotherfunds

B. TransfersTo/FromOtherFunds

Transfersto/fromotherfundsforthefiscalyearendedatJune30,2014consistedofthefollowing:

Charter SpecialReserve Non‐Major TotalSchool FundforCapital Governmental GovernmentalFund OutlayProjects Funds Funds

GeneralFund 244,894$ 6,432,568$ 168,152$ 6,845,614$CharterSchoolFund ‐ 240,000 ‐ 240,000SpecialReserveFundforCapitalOutlayProjects ‐ ‐ 609,723 609,723

244,894$ 6,672,568$ 777,875$ 7,695,337$

GeneralFundtransfertoCharterSchoolFundtocoverspecialeducationcosts 212,034$GeneralFundtransfertoCharterSchoolFundforshareofTitleIII,LEPFunds 25,194GeneralFundtransfertoCharterSchoolFundforshareofMedi‐CalFunds 7,666GeneralFundtransfertoSpecialReserveFundforCapitalOutlayProjectsforredevelopmentprojects 181,774GeneralFundtransfertoChildDevelopmentFundforshareofMedi‐CalAdministrativeActivities 31,717GeneralFundtransfertoChildDevelopmentFundforcontributiontobalanceresource 136,435CharterSchoolFundtransfertoSpecialReserveFundforCapitalOutlayProjectsforthirdpaymentoncharterstart‐uploan 240,000SpecialReserveFundforCapitalOutlayProjectstransferforpaymentoncertificateofparticipation 609,723SpecialReserveFundforOtherThanCapitalOutlayProjectstransfertoSpecialReserveFundforCapitalOutlayProjectsforredevelopmentprojects 6,250,794

Total 7,695,337$

InterfundTransfersIn

30

PERRISELEMENTARYSCHOOLDISTRICTNotestoFinancialStatementsJune30,2014NOTE5–FUNDBALANCESMinimumFundBalancePolicyDuring the 2010‐11 fiscal year, pursuant to GASB StatementNo. 54, theDistrict adopted aminimum fundbalancepolicyfortheGeneralFundinordertoprotecttheDistrictagainstrevenueshortfallsorunpredictedexpenditures. UnassignedFundBalancemaybeaccessedintheeventofunexpectedexpendituresuptotheminimumestablishedleveluponapprovalofabudgetrevisionbytheDistrict'sgoverningboard.Intheeventofprojectedrevenueshortfalls,itistheresponsibilityoftheChiefBusinessOfficialtoreporttheprojectionstotheDistrict'sgoverningboardonaquarterlybasisandshallberecordedintheminutes.AnybudgetrevisionthatwillresultintheUnassignedFundBalancedroppingbelowtheminimumlevelwillrequiretheapprovalofa2/3voteoftheDistrict'sgoverningboard.The fund balance of the District's General Fund is intended to contain reserves to provide stability andflexibilityinresponsetounexpectedadversityand/oropportunities.Thetargetistomaintainanunrestrictedfund balance of not less than 5% of combined general fund expenditures and other financing uses in theassignedfundbalancecategoryforeconomicuncertainty.Therationaleforthislevelofreservesistoprovidethefollowing:

Tomeetstate‐requiredreservelevels inaccordancewiththestandardsandcriteriaadoptedbytheStateBoardofEducation(EducationCode33128)

Toprovideadequatecashtomeetfinancialobligations Toprovideavailablefundstomeetunanticipatedoremergencyfinancialobligations Toprovidestabilityduringperiodsofeconomicdistress

When an expenditure is incurred for purposes for which both restricted and unrestricted fund balance isavailable,theDistrictconsidersrestrictedfundstohavebeenspentfirst.Whenanexpenditureisincurredforwhichcommitted,assigned,orunassignedfundbalancesareavailable,theDistrictconsidersamountstohavebeenspentfirstoutofcommittedfunds,thenassignedfunds,andfinallyunassignedfunds,asneededunlessthegoverningboardhasprovidedotherwiseinitscommitmentorassignmentactions.

31

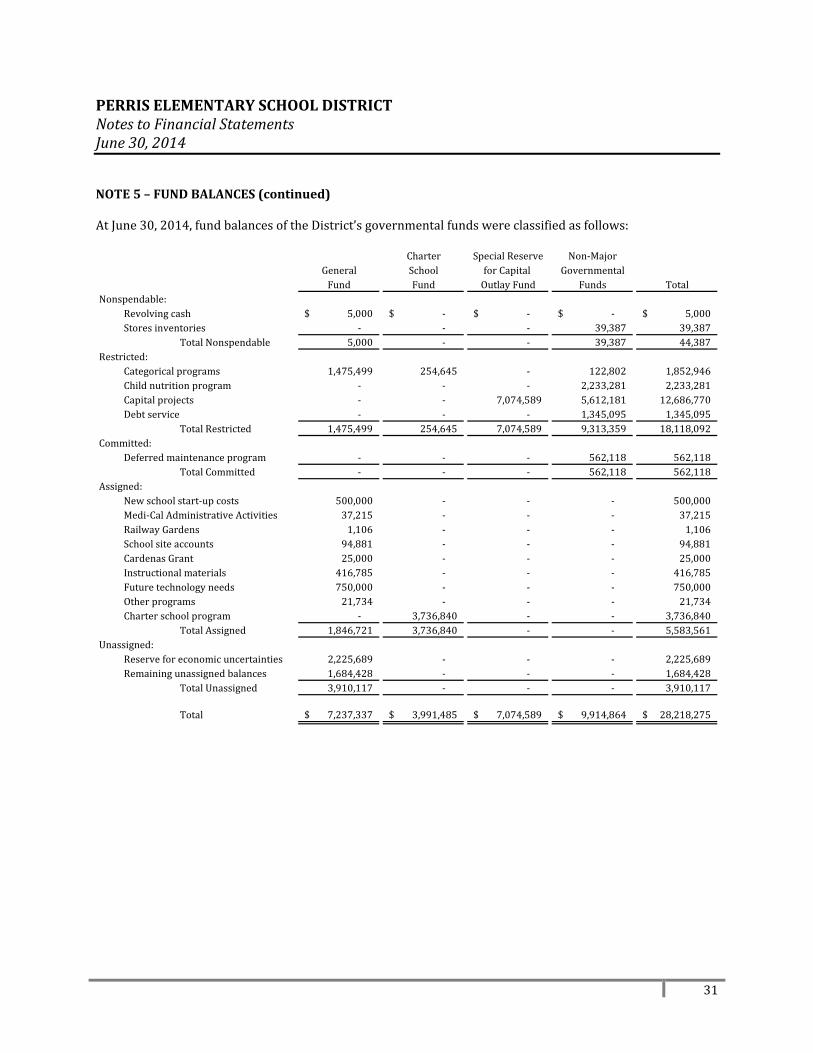

PERRISELEMENTARYSCHOOLDISTRICTNotestoFinancialStatementsJune30,2014NOTE5–FUNDBALANCES(continued)AtJune30,2014,fundbalancesoftheDistrict’sgovernmentalfundswereclassifiedasfollows:

Charter SpecialReserve Non‐MajorGeneral School forCapital GovernmentalFund Fund OutlayFund Funds Total

Nonspendable:Revolvingcash 5,000$ ‐$ ‐$ ‐$ 5,000$Storesinventories ‐ ‐ ‐ 39,387 39,387

TotalNonspendable 5,000 ‐ ‐ 39,387 44,387Restricted:

Categoricalprograms 1,475,499 254,645 ‐ 122,802 1,852,946Childnutritionprogram ‐ ‐ ‐ 2,233,281 2,233,281Capitalprojects ‐ ‐ 7,074,589 5,612,181 12,686,770Debtservice ‐ ‐ ‐ 1,345,095 1,345,095

TotalRestricted 1,475,499 254,645 7,074,589 9,313,359 18,118,092Committed:

Deferredmaintenanceprogram ‐ ‐ ‐ 562,118 562,118TotalCommitted ‐ ‐ ‐ 562,118 562,118

Assigned:Newschoolstart‐upcosts 500,000 ‐ ‐ ‐ 500,000Medi‐CalAdministrativeActivities 37,215 ‐ ‐ ‐ 37,215RailwayGardens 1,106 ‐ ‐ ‐ 1,106Schoolsiteaccounts 94,881 ‐ ‐ ‐ 94,881CardenasGrant 25,000 ‐ ‐ ‐ 25,000Instructionalmaterials 416,785 ‐ ‐ ‐ 416,785Futuretechnologyneeds 750,000 ‐ ‐ ‐ 750,000Otherprograms 21,734 ‐ ‐ ‐ 21,734Charterschoolprogram ‐ 3,736,840 ‐ ‐ 3,736,840

TotalAssigned 1,846,721 3,736,840 ‐ ‐ 5,583,561Unassigned:

Reserveforeconomicuncertainties 2,225,689 ‐ ‐ ‐ 2,225,689Remainingunassignedbalances 1,684,428 ‐ ‐ ‐ 1,684,428

TotalUnassigned 3,910,117 ‐ ‐ ‐ 3,910,117

Total 7,237,337$ 3,991,485$ 7,074,589$ 9,914,864$ 28,218,275$

32

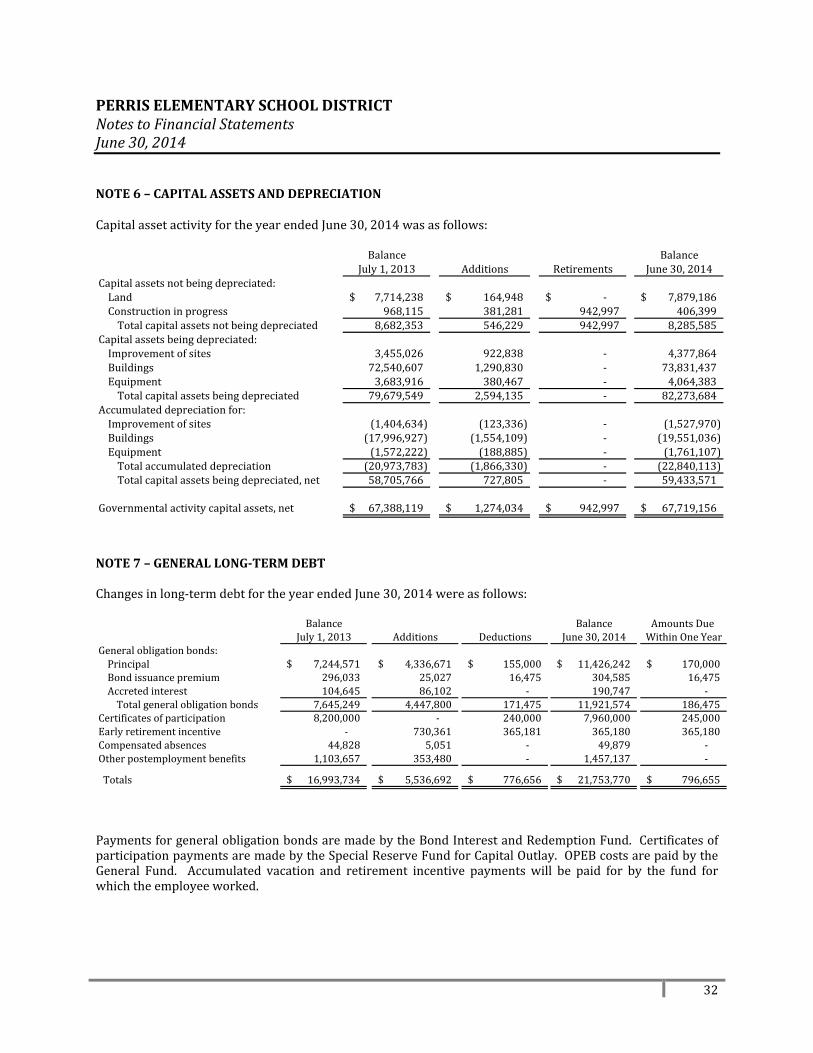

PERRISELEMENTARYSCHOOLDISTRICTNotestoFinancialStatementsJune30,2014NOTE6–CAPITALASSETSANDDEPRECIATIONCapitalassetactivityfortheyearendedJune30,2014wasasfollows:

Balance Balance

July1,2013 Additions Retirements June30,2014Capitalassetsnotbeingdepreciated:Land 7,714,238$ 164,948$ ‐$ 7,879,186$Constructioninprogress 968,115 381,281 942,997 406,399Totalcapitalassetsnotbeingdepreciated 8,682,353 546,229 942,997 8,285,585

Capitalassetsbeingdepreciated:Improvementofsites 3,455,026 922,838 ‐ 4,377,864Buildings 72,540,607 1,290,830 ‐ 73,831,437Equipment 3,683,916 380,467 ‐ 4,064,383Totalcapitalassetsbeingdepreciated 79,679,549 2,594,135 ‐ 82,273,684

Accumulateddepreciationfor:Improvementofsites (1,404,634) (123,336) ‐ (1,527,970)Buildings (17,996,927) (1,554,109) ‐ (19,551,036)Equipment (1,572,222) (188,885) ‐ (1,761,107)Totalaccumulateddepreciation (20,973,783) (1,866,330) ‐ (22,840,113)Totalcapitalassetsbeingdepreciated,net 58,705,766 727,805 ‐ 59,433,571

Governmentalactivitycapitalassets,net 67,388,119$ 1,274,034$ 942,997$ 67,719,156$

NOTE7–GENERALLONG‐TERMDEBTChangesinlong‐termdebtfortheyearendedJune30,2014wereasfollows:

Balance Balance AmountsDueJuly1,2013 Additions Deductions June30,2014 WithinOneYear

Generalobligationbonds:Principal 7,244,571$ 4,336,671$ 155,000$ 11,426,242$ 170,000$Bondissuancepremium 296,033 25,027 16,475 304,585 16,475Accretedinterest 104,645 86,102 ‐ 190,747 ‐Totalgeneralobligationbonds 7,645,249 4,447,800 171,475 11,921,574 186,475

Certificatesofparticipation 8,200,000 ‐ 240,000 7,960,000 245,000Earlyretirementincentive ‐ 730,361 365,181 365,180 365,180Compensatedabsences 44,828 5,051 ‐ 49,879 ‐Otherpostemploymentbenefits 1,103,657 353,480 ‐ 1,457,137 ‐

Totals 16,993,734$ 5,536,692$ 776,656$ 21,753,770$ 796,655$

PaymentsforgeneralobligationbondsaremadebytheBondInterestandRedemptionFund.CertificatesofparticipationpaymentsaremadebytheSpecialReserveFundforCapitalOutlay.OPEBcostsarepaidbytheGeneral Fund. Accumulated vacation and retirement incentive payments will be paid for by the fund forwhichtheemployeeworked.

33

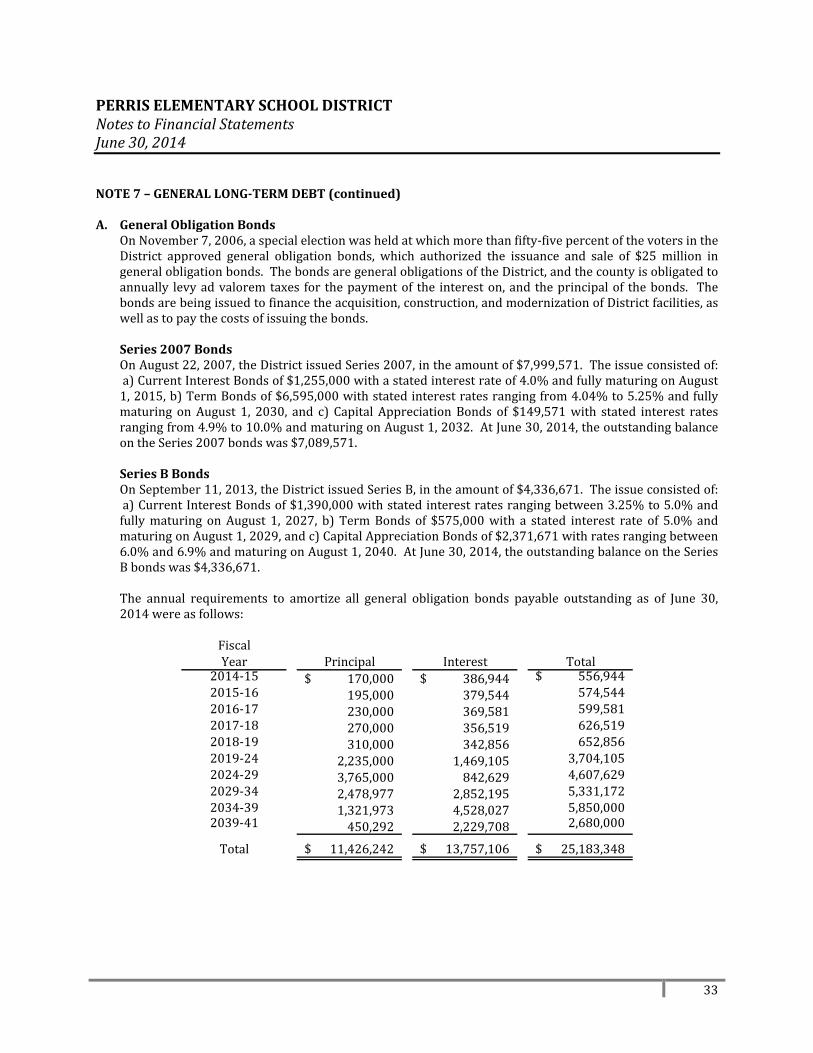

PERRISELEMENTARYSCHOOLDISTRICTNotestoFinancialStatementsJune30,2014NOTE7–GENERALLONG‐TERMDEBT(continued)A. GeneralObligationBonds

OnNovember7,2006,aspecialelectionwasheldatwhichmorethanfifty‐fivepercentofthevotersintheDistrict approved general obligation bonds, which authorized the issuance and sale of $25 million ingeneralobligationbonds.ThebondsaregeneralobligationsoftheDistrict,andthecountyisobligatedtoannually levyadvaloremtaxes for thepaymentof the intereston,andtheprincipalof thebonds. Thebondsarebeingissuedtofinancetheacquisition,construction,andmodernizationofDistrictfacilities,aswellastopaythecostsofissuingthebonds.Series2007BondsOnAugust22,2007,theDistrictissuedSeries2007,intheamountof$7,999,571.Theissueconsistedof:a)CurrentInterestBondsof$1,255,000withastatedinterestrateof4.0%andfullymaturingonAugust1,2015,b)TermBondsof$6,595,000withstatedinterestratesrangingfrom4.04%to5.25%andfullymaturing onAugust 1, 2030, and c) Capital AppreciationBonds of $149,571with stated interest ratesrangingfrom4.9%to10.0%andmaturingonAugust1,2032.AtJune30,2014,theoutstandingbalanceontheSeries2007bondswas$7,089,571.SeriesBBondsOnSeptember11,2013,theDistrictissuedSeriesB,intheamountof$4,336,671.Theissueconsistedof:a)CurrentInterestBondsof$1,390,000withstatedinterestratesrangingbetween3.25%to5.0%andfullymaturing onAugust 1, 2027, b) TermBonds of $575,000with a stated interest rate of 5.0%andmaturingonAugust1,2029,andc)CapitalAppreciationBondsof$2,371,671withratesrangingbetween6.0%and6.9%andmaturingonAugust1,2040.AtJune30,2014,theoutstandingbalanceontheSeriesBbondswas$4,336,671.