Performing Productivity Improvement for … Productivity Improvement for Performance Recovery an...

15

5/25/2012 1 1 Performing Productivity Improvement for Performance Recovery an ELSA’s presentation to capital market analysts: 1Q-2012 performance, strategy & 2012 projection Financial Club Jakarta - 24 May 2012 2 Discussion Agenda : 1. Corporate & Business Overview 2. Management’s Continuous Action for Performance Recovery 3. 2011 Performance Highlights 4. Industry & Prospect in Brief 5. 1Q-2012 Performance Highlights 6. 2012 Business Strategy 7. 2Q-2012 Performance Projection

Transcript of Performing Productivity Improvement for … Productivity Improvement for Performance Recovery an...

5/25/2012

1

1

Performing Productivity Improvement

for Performance Recovery

an ELSA’s presentation to capital market analysts:

1Q-2012 performance, strategy & 2012 projection

Financial Club Jakarta - 24 May 2012

2

Discussion Agenda :

1. Corporate & Business Overview

2. Management’s Continuous Action for

Performance Recovery

3. 2011 Performance Highlights

4. Industry & Prospect in Brief

5. 1Q-2012 Performance Highlights

6. 2012 Business Strategy

7. 2Q-2012 Performance Projection

5/25/2012

2

3

Corporate Overview :

Reputable Oil & Gas Services Business

PT Elnusa Tbk (“ELSA”) is a publicly listed

Oil & Gas Services company which has been

operating for almost 40 years in oil & gas

industry. ELSA focuses in Upstream Oil & Gas

Services business : Geoscience-Drilling-Oilfield

and also manages Downstream Oil& Gas

Services as well as Support Upstream Oil & Gas

Services in its Subsidiaries. In 2011, ELSA

established a Joint-Venture company for marine

seismic services business.

Controlling Shareholders :

- PT Pertamina (Persero)

- PT Benakat Petroleum Energy Tbk

4

Division & Joint Venture Company Businesses:

Upstream Oil & Gas Services

Seismic Survey:

2D & 3D Land Seismic

2D & 3D Transition Zone

2D & 3D Marine Seismic

Processing:

Processing, Re-processing

Special processing,

Modeling & GGR Study

Other Services:

MT (Magnetotelluric)

4D Microgravity

Geomagnet & GPR

Drilling :

(550 HP – 1600 HP)

Drilling Fluid Services

&

Reservoir Testing

Services

Drilling support :

Wireline logging &

Perforating, Pumping,

Cementing,

Mud logging & H2S,

Well Services:

Hydraulic Workover/

Snubbing

Wireline/Slickline

Well Testing service

CTU (Coiled Tubing

Unit)

EPF :

O&M Production

Facility

O&M Pipeline

TSA – IOR

Integrated Field Mgt

Ge

osc

ien

ce S

erv

ice

s(G

SC

)

Dri

llin

g S

erv

ice

s(E

DS

)

Oil

fie

ld S

erv

ice

s(O

FS

)

Marine Seismic Survey:

2D Marine Data Acq.

3D Marine Data Acq.

JV C

om

pa

ny

(E C

S)

5/25/2012

3

5

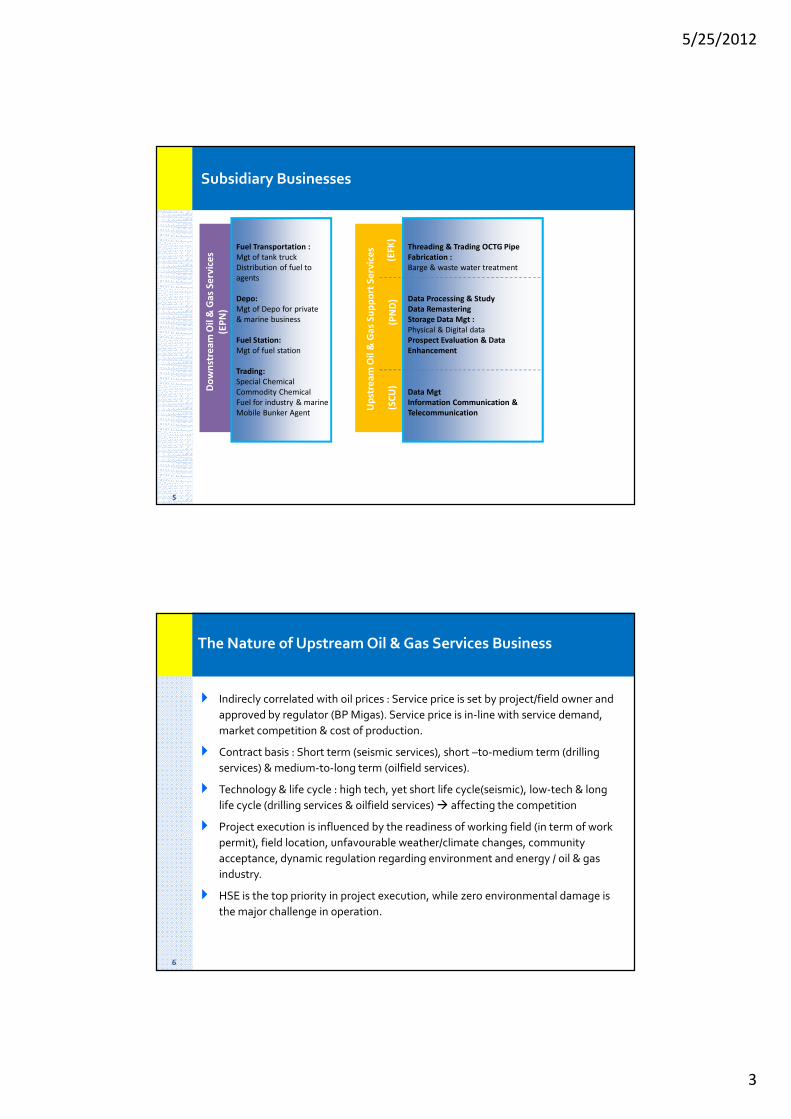

Subsidiary Businesses

Fuel Transportation :

Mgt of tank truck

Distribution of fuel to

agents

Depo:

Mgt of Depo for private

& marine business

Fuel Station:

Mgt of fuel station

Trading:

Special Chemical

Commodity Chemical

Fuel for industry & marine

Mobile Bunker Agent

Threading & Trading OCTG Pipe

Fabrication :

Barge & waste water treatment

Data Processing & Study

Data Remastering

Storage Data Mgt :

Physical & Digital data

Prospect Evaluation & Data

Enhancement

Data Mgt

Information Communication &

Telecommunication

Do

wn

stre

am

Oil

& G

as

Se

rvic

es

(EP

N)

Up

stre

am

Oil

& G

as

Su

pp

ort

Se

rvic

es

(EF

K)

(PN

D)

(SC

U)

6

The Nature of Upstream Oil & Gas Services Business

� Indirecly correlated with oil prices : Service price is set by project/field owner and

approved by regulator (BP Migas). Service price is in-line with service demand,

market competition & cost of production.

� Contract basis : Short term (seismic services), short –to-medium term (drilling

services) & medium-to-long term (oilfield services).

� Technology & life cycle : high tech, yet short life cycle(seismic), low-tech & long

life cycle (drilling services & oilfield services) � affecting the competition

� Project execution is influenced by the readiness of working field (in term of work

permit), field location, unfavourable weather/climate changes, community

acceptance, dynamic regulation regarding environment and energy / oil & gas

industry.

� HSE is the top priority in project execution, while zero environmental damage is

the major challenge in operation.

5/25/2012

4

7

Major Risk & Key Success Factor

5 major operational risks :

� Project Delay

� Project Cost Overrun

� Client Contract

� Investment Planning &

Execution

� Service Pricing

5 key success factors:

� Project Selection & Customer

Focus

� Utility & On-schedule Project

Execution

� Project Recovery Handling

� Prudent Investment & Excellent

Competency

� On-track operation cost &

collection

8

Ensuring Project Delivery:

Improved Project Management & Monitoring

� In 2011, several big-value projects experienced delays in their execution.

� Project delivery can be constrained by :

� Delivering project delivery needs a comprehensive effort, both in term of operation

and financial :

� Proper & detailed project planning � to ensure risk mitigation

� Good communication with government � to help client obtain work permit

� Strict project monitoring � to review & ensure project execution

� Quick corective action � to minimize delay/loss

� Prompt decision making � to step in/takeover unperformed subcon

� Strong working capital position � to provide adequate operational fund

Operation Permit (from forestry, local autonomy) Projects in Papua, Lampung, Kalimantan

Social Problem Projects in Subang, Aceh

Lithology Projects in Aceh

Force Majeure (flood, climate change) Projects in Papua, Jambi

5/25/2012

5

9

Management’s Continuous Action for Performance Recovery

� Structural Change :

� Business structure repositioning (Oilfield Services

enhancement),

� Profitability & Cash flow as KPI,

� Isolated loss projects/business unit & review for next

action (Drilling, ECS),

� Streamlining organization for effectivity & efficiency.

� Fundamental Change :

� Work culture for integrity & professionalism,

� Strenghten awareness of ‘HSE is my culture,

Equipment is my life & Cost awareness is my

attitude”,

� Business process improvement.

� Performance Change :

� Focus on major & reputable clients,

� Strict monitoring on new proposal project & risk

mitigation,

� Project management improvement for execution,

� Invoice acceleration, refinancing for better & lower

interest rate,

� HSE strenghtening for zero fatality.

o Business Structure & Organization

Improvement

o Profitability, Productivity & Cash Flow

Management Improvement

o Work Culture Improvement

Improvement

10

2.1

1.1 0.8

0.1

2.5

1.7

0.6

0.1

3.7

2.3

1.1

0.2

4.2

2.2 1.9

0.2

4.7

2.1 2.3

0.3

Pendapatan Usaha Hulu Hilir Support

2007 2008 2009 2010 2011

� 2011 revenues was dominated by Downstream Oil and Gas Services (48%) derived

from industrial fuel & transport business, while Upstream Oil and Gas Services

contributed 45%, decreased compare to last year contribution, due to delay projects.

2011 Review Revenue Growth : Downstream Business as the Most Contributor

Consolidated Upstream Oil & Gas

Services

Downstream Oil &

Gas ServicesUpstream Oil & Gas

Support Services

12%

21%

-3%

105%

In Trio Rp

5/25/2012

6

11

� High cost of operating revenue (94% - increase 17%) was caused by delay cost & provision for loss making

contracts (Rp43 bio), it has made 31% decrease in Gross Profit (GPM : 6%).

� Provision for the decrease of advances of investment in shares of stock (TAC Ramok) amounting Rp13.6 bio

and JV (ECS) loss to Rp14.4 bio have contributed to Net Loss amounting to minus Rp42.8 bi0.

� Earning Before Income Tax( if excluded those provisions) reached Rp30.5 bio, instead of minus Rp26,1 bio.

� Interest Bearing Debt increased due to FRN issuance (which later was refinanced).

2011 Review

Profitability Drop : The Burden of Delayed/Loss Projects

399

144

100

395

180

134

543

276

466

416

134

64

285

(22) (43)

Gross Profit Income from operation Net Profit

2007 2008 2009 2010 2011

-31%

-117%

-167%

In Bio Rp

12

2011 Review :

Major Loss Projects - Affected 2011 Financial Performance

� 2D Transition zone seismic project in Papua : delay project due to remote

operational area � recorded loss realization up to Rp63 bio and loss

provision amounting Rp43 bio.

� ECS net loss � recorded Rp14,4 bio (as 51% Elnusa’s share in the JV)

� Upgrading Gas Station : project decline to anticipate more loss � recorded

penalty of Rp9 bio

� IPAL : project delivery delay due to procurement delay � recorded penalty

of Rp3.5 bio

� TAC Ramok Senabing : impairment of Down Payment due to the period of

the TAC � recorded provision Rp13.6 bio (equiv. to USD1.5 mio).

5/25/2012

7

13

2011 Review :

Tz Seismic in Papua : Between remote area & work permit

� Management is currently in a final discussion & negotiation with the Client to get

contract escalation to recover project profitabiliy.

� 1170 km Transition zone Seismic project,

awarded in August 2010, worth USD35 mio.

� Main Obstacles :

� Area : Primary forest & no access (limited

tract line - mostly used river & air) .

� Late Forestry Permit (end of Feb 2011), Strict

local government regulation, while we

conducted mobilization in Sept 2010.

� Local Wisdom: delay 2 months due to

traditional ceremony.

� Late arrival of Helicopters for operations.

� Poor HSE & Operational performance of local

Sub-Contractors & high workforce turnover

14

2011 Review

JV Company (ECS) : Unexpected Performance & Risk

� Established in April 2011 for marine seismic business , as Joint

Venture company with CGGVeritas Seismic (Singapore) Pte Ltd.

� Type of business is high investment and high fixed cost without

long term contract assurance � contract basis & short term

projects.

� Missed the quality of revenue achievement in 2011� Planned for

3D seismic, while in realization dominated by 2D seismic (60%)

� Later on, the JV can not fully absorbed its high fixed cost which was overburdened by un-

estimated cost.

� In 2011, the business contributed a loss reached to Rp14,4 bio to consolidated ELSA

performance, while in 1Q-2012 it continued to contribute a loss reached to Rp10,7 bio.

� Marine seismic market in the coming years is still predicted as a highly volatile industry that has

a high degree of risk due to several factors such as limited market in Indonesia, oil prices and

unfavourable weather.

� Due to its performance, risk & business model, management has come to a solid decision to

review the business .

5/25/2012

8

15

19 fields of Working Area in 1st round Bidding 2012 : 50% of Onshore & Offshore Onshore : East Java, Aceh, North Sumatera, Riau, West Sumatera, Central kalimantan, Arafura, West Papua

Offshore : Natuna, East Java, Bengkulu, East Kalimantan, Maluku, Makasar, Arafura, West Papua.

Indonesia – 2012 Petroleum Contract Area

Source : BP Migas

16

$-

$5,000

$10,000

$15,000

$20,000

$25,000

2011 2012

Adm & GA

Exploration

Field Development

Operational Production

Indonesia – Upstream Oil&Gas Services Market (Plan)

954

977

949945

902

950

2007 2008 2009 2010 2011 2012

Oil Production (Tho Barrel per Day) Upstream Oil&Gas Investment Budget

Source : BP Migas

5/25/2012

9

17

357

135

86

45 38 28 35 23 17 17

1 2 3 4 5 6 7 8 9 10

47%

16%10%

6% 6%

58%

23%

8% 5%

21%

Pertamina Total EP Chevron VICO Others

2011

2012P

Major Clients – Upstream Services Market

2012P

Pertamina

Capital Expenditure 52.8

Pertamina EP

Capital Expenditure 6

Operational Expenditure 26

Pertamina Hulu Energy

Capital Expenditure 11.6

Operational Expenditure 5.5

In Rp TrioRevenue by Client of Upstream Services

Chevron Pacific Indonesia, Pertamina EP, Total E&P

(Kalimantan), ConocoPhillips (Natuna), CNOOC, Chevron

Indonesia, PHE (ONWJ), Medco Sumatera, BOB Bumi Siak

Pusako, Petrochina International (Jabung)

10 KKKS as Oil Production Driver in 2012 (Tho barrel oil per day) :

18

79

wells

38

wells

26

wells

Oilfield Services : “the bread & butter” business in the future

Own-Operation

Workover Wells

Partner Workover

Wells

Exploitation Wells

Well Target of Pertamina EP in 2012

� Significant experience (27 years) in workover/oilfield services business.

� More than 25 years serves Total E&P Indonesie with proudly HSE records (10 awards of safety

performance recognition).

� Long contract basis with relatively easy-to-managed risk exposure and quite attractive margin.

� Wide business opportunity in production well/ workover well / brown/marginal field.

Gross Profit Margin Oilfield Services

5/25/2012

10

19

Oilfield Services : “the bread & butter” business in the future

Pursuing Market of Coiled Tubing Unit (CTU), Pressure Pumping & Nitrogen

� Coiled Tubing & Associated Services using

Multipurpose Barge is a new business with

high technology, aims to increase revenue

& profitability.

� The major market of the services are from :

Total , Chevron,& Pertamina . Estimated

Yearly Indonesia market value : USD85 mio.

� Elnusa has been awarded a 5-year contract

worth USD46,9 mio for CTU and Pumping

(including the barge).

� Elnusa is the first national upstream oil &

gas services company owns this

Multipurpose Barge, equipped with CTU &

Associates.

20

Oilfield Services : “the bread & butter” business in the future

Pursuing Market of Coiled Tubing Unit (CTU), Pressure Pumping & Nitrogen

5/25/2012

11

21

2012 Business Strategy & Corporate Action

GSC • Less marine seismic business for more managable risk & performance

EDS• Focus on drilling rig services > 1500 HP

• Penetrate drilling business for CBM market

OFS• Business enlargement to coiled tubing and pressure pumping services

• Refocusing on more sustaineable projects

Portfolio

• Strenghten downstream oil & gas business as one of corporate prime business

• Divest low margin business unit and non-core subsidiaries

22

Key Contracts 2012 :

Acquired 71% of targeted Revenues

� To retain the performance achievement and to improve market position, Elnusa targets to

obtain high-profitable projects and long term contracts, while strictly monitor the project

execution/delivery.

Business Unit Carry over Value New Contract Value Total Contract Onward Prospect

from 2011 2012 Value 2012

GDL 47.70 5.92 53.63 - 41.05

GDM 41.45 27.43 68.72 - 21.71

GDP 4.61 0.66 5.45 - 2.52

Total GSC 93.76 34.02 127.80 - 65.29

Drilling 16.62 - 16.62 - 1.83

Total EDS 16.62 - 16.62 1.83

Drilling Support 24.81 2.94 30.76 34.48 15.92

Well Services 33.28 11.05 43.31 81.04 2.29

O&M & EPF 9.72 - 9.72 - -

Total OFS 67.81 13.99 83.79 115.52 18.20

EPC 2.60 - 2.60 - 6.29

Total EPC 2.60 - 2.60 - 6.29

Total contract 180.80 48.00 230.82 115.52 91.61

In USD mio

5/25/2012

12

23

Operational Assets & 2012 Key Contracts :

Geoscience Services & Drilling Services

Geoscience Services Number of

Unit

Utilization up to

1Q-2012

2012 Dedicated Projects

SN 408 - GDL 3 units 22% Medco Tomori

SN 428 XL - GDL 5 unit 67% Pertamina (Alamanda, Akasia

Bagus, Manduru, Ginaya,

Puspa)

SN 428 XL - GDM 2 units 67% Chevron Papua & Total Handil

Drilling Services Number of

Unit

Utilization 2012 Dedicated Projects

Rig 1600 Hp 1 unit 100% Vico Kalimantan

Rig 550 Hp 3 units 8% Pertamina Ubep jambi

Rig 900 Hp 1 unit 0% Standby

SFT 3 units 0% -

DST 4 units 0% -

LMP 1 units 100% Pertamina

*Program Advance GSC is counted as project

** Standby Under Contract is counted as standby (un-utilized)

24

2012 Operational Assets & Key Contracts :

Oilfield Services

Oilfield Services Number of

Unit

Utilization Rate

up to 1Q-2012

2012 Dedicated Projects

Hydraulic Rig – 150 K 5 units 47% Total, Chevron

Hydraulic Rig –225 K 3 units 100% Pertamina, Chevron

Hydraulic Rig – 340 K 3 units 11% Chevron

Wireline Double

Drum

5 units 60% Total

DST Surface 3 units 100% Total

Barge & LCT 7 units 100% Total

RES Logging 7 units 100% Pertamina, PPEJ

Cementing 3 units 67% Pertamina, POG, Indrillco

Mud Logging 16 units 48% Medco, Pertamina, Chevron,

EML

H2S 9 units 48% Pertamina, Petrochina,

*Standby Under Contract is counted as standby (un-utilized)

5/25/2012

13

25

1,043

395

567

80

1,085

572

458

55

Consolidated Upstream Services Downstream Services Upstream Support

Services

1Q-2011 1Q-2012

1Q-2012 Highlights:

Revenue growth: Consolidated & Upstream Services

� Consolidated revenue grow by4% compared to 1Q last year, derived from the increase of

Upstream services revenue (45%), from Rp395 bio to Rp572 bio.

� The hike of Upstream Revenue in 1Q-2012 was due to increase sales of Geoscience Services (87%)

and Oilfield Services (118%), mostly from carry-over contracts realization. On the other hand, the

performance was actually still affected by several delay GDL & Tz Seismic projects.

� Downstream services revenue decrease 19% to Rp457 bio due to selecive customer policy on

Industry & marine fuel trading.

4%

45%

-31%

In Bio Rp19%

26

1Q-2012 Highlights:

On-track Cost Management

Cost of Revenue (in Bio Rp) % Cost of Revenue VS Revenue

� As consolidated, cost of revenue grew by 3% to Rp959 bio while in Upstream Oil & Gas

services it grew by 42% to Rp487 bio.

� Cost management can be seen from a lower growth of cost of revenue compared to growth

of revenue in Consolidation (3% vs 4%)and Upstream services (42% vs 45%). In addition, the

cost proportion compared to revenue was also decrease in 1Q-2012 (from 90% to 88%) .

90%

87%

99%

88%

85%

99%

Consolidated Upstream Services Downstream Services

935

344

560

960

488 452

Consolidated Upstream Services Downstream Services

1Q-2011 1Q-2012

3%

42%

-19%

5/25/2012

14

27

1Q-2012 Highlights:

Better Gross Profitability of Upstream Oil & Gas Services

� Due to managed cost of revenue,

the Gross Profit in 1Q-2012 grew by

16% to Rp125 bio and derived gross

margin increase to 12% .

� Yet, net income in 1Q-2012

reached Rp15 bio with 1.4%

margin, still decreased compared

to the achievement in 1Q-2011.

� This was primarily due to loss

contribution from ECS (JV Co)

which recorded at Rp10,7 bio. The

decrease in net income was also

derived from increased interest

expense (52%) amounting to Rp10

bio due to recognition of interest &

financing cost.

Gross Profit Margin

In Bio Rp

108

29 20

125

27 15

Gross Profit Earning Before Income

Tax

Net Income

1Q-2011

1Q-2012

10%13%

4%

42%

12%

15%

5%

29%

Consolidated Upstream Services Downstream Services Upstream Support

Services

28

1Q-2012 Highlights:

Improvement Cash Flow Generated from Operation

� Operating activities cash

flows have significantly

improved from deficit

Rp135 bio to positif

Rp246 bio this 1Q-2012.

� This growth derived from

cash-in acceleration from

several prime customers:

Pertamina, Chevron &

Vico.

� Cash flows used in

investing activities

decreased sharply due to

selective investment .

2011 2012Cash Flows from Operating Activities

Cash receipts from customer 955 1,529

Cash paid to supplier & contractors (923) (1,110)

Cash paid to employees (52) (62)

Cash generated from Operations (20) 357

Other receipts/payments (116) (111)

Net Cash generated from Operating Activities (135) 246

Net Cash used in Investing Activities (55) (21)

Net Cash generated from Financing Activities 162 4

Effect exchange rate changes on cash & cash equivalents 5 1

Increase/(decrease) in cash & cash equivalents (46) 229

Cash & cash equivalents at beginning of the year 735 688

Cash & cash equivalents at the end of the year 689 917

� Significant funding activities in 1Q-2012 was the realization of the loan refinancing.

The refinancing resulted in interest expense savings of USD6 mio over the next 5

years.

5/25/2012

15

29

2Q-2012 Performance Projection

125

220

573

69 102

242

15 33

111

1Q-2012 2Q-2012 Target 2012

Gross Profit

Operating Profit

Net Income

1,085

2,665

5,602

1Q-2012 2Q-2012 Target 2012

Revenue

56%

40%

4%

Upstream Services

Downstream Services

Upstream Support

Services

Potential - 2012 :

� 2D Transition zone seismic

project in papua which

experienced a huge loss in 2011

is expected recovered in 2012.

� Sale of shares from Patrakom

divestment (still on process).

Estimation

Estimation

2Q-2012Estimation

In Bio Rp

In Billion Rp

30

Thank You…

DISCLAIMER :

The information in this document has not been independently verified. No representation or warranty

expressed or implied is made as to, and no reliance should be placed on, the fairness, accuracy, completeness

or correctness of such information or opinions contained herein. None of PT Elnusa Tbk (the “Company“), nor

any of its affiliates, advisers or representatives shall have any liability whatsoever (in negligence or otherwise)

for any loss whatsoever arising from the use of this document or its contents or otherwise arising in connection

with this document.

This document is being furnished to you solely for your information on a confidential basis and may not be

reproduced, redistributed or passed on, in whole or in part, to any other person. Any failure to comply with

these restrictions may constitute a violation of the laws of any such other jurisdiction. By accepting this

document you agree to be bound by the foregoing limitations.

This document does not constitute or form part of an offer or invitation to purchase any shares in the Company

and neither shall any part of it form the basis of nor be relied upon in connection with any contract or

commitment whatsoever. Any decision to purchase shares should be made solely on the basis of information

contained in the prospectus.