Performance of the Thai Banking System in the Second ...

15

No. 63/2021 Performance of the Thai Banking System in the Second Quarter of 2021 Ms. Suwannee Jatsadasak, Senior Director, Bank of Thailand, reported on the Thai banking system’s performance in the second quarter of 2021 that the Thai banking system remained resilient with high levels of capital fund, loan loss provision and liquidity to cushion economic impacts from COVID-19 pandemic as well as play an important role in facilitating assistances for borrowers in need and accommodating loan demand. Credit assistance measures, coupled with revisions to rules on loan classification and provisioning helped alleviate the deterioration of bank loan quality. Meanwhile, banking system’s profitability improved from the same period last year due mainly to lower provisioning expenses as banks set aside high levels of provision in the previous year. Details are as follows: Capital Fund of the Thai banking system was at 3,038. 1 billion baht, equivalent to capital adequacy ratio (BIS ratio) of 20.0%. Loan loss provision remained high at 851 . 5 billion baht with NPL coverage ratio of 152.2%. Liquidity coverage ratio (LCR) registered at 186.7%. In the second quarter of 2021, banks ’ overall loan growth was 3.7% year - on- year, slightly lower than 3. 8% in the previous quarter. Details on bank loan are as follows: Corporate loan growth decelerated to 2. 6% year -on- year due to an increase in large corporates ’ 1 loan usage during the second quarter of last year when financial markets were volatile, causing funding switch from corporate bond issuances to bank loan . Furthermore, there was also an increase in funding from corporate bond issuances in this quarter . SME loans 2 improved and registered positive year - on-year growth partly owing to soft loan and rehabilitation credit scheme. Consumer loans expanded at 5 . 7 % year -on- year, increasing from 5 . 3 % year -on-year growth rate in the previous quarter. The expansion was mainly attributed to mortgage loan, which continued to grow, consistent with an increase in demand for low- rise properties. Auto loan growth, on the other hand, slightly declined in line with a reduction in domestic car sales from the previous quarter. At the same time, credit card loan expanded at a lower rate due to a lower level of 1 Corporates with a credit line of more than 500 million baht with a bank as of June 2021. 2 Corporates with a credit line not exceeding 500 million baht with a bank as of June 2021.

Transcript of Performance of the Thai Banking System in the Second ...

No. 63/2021

Performance of the Thai Banking System in the Second Quarter of 2021

Ms. Suwannee Jatsadasak, Senior Director, Bank of Thailand, reported on the Thai banking system’s performance in the second quarter of 2021 that the Thai banking system remained resilient with high levels of capital fund, loan loss provision and liquidity to cushion economic impacts from COVID-19 pandemic as well as play an important role in facilitating assistances for borrowers in need and accommodating loan demand. Credit assistance measures, coupled with revisions to rules on loan classification and provisioning helped alleviate the deterioration of bank loan quality. Meanwhile, banking system’s profitability improved from the same period last year due mainly to lower provisioning expenses as banks set aside high levels of provision in the previous year. Details are as follows:

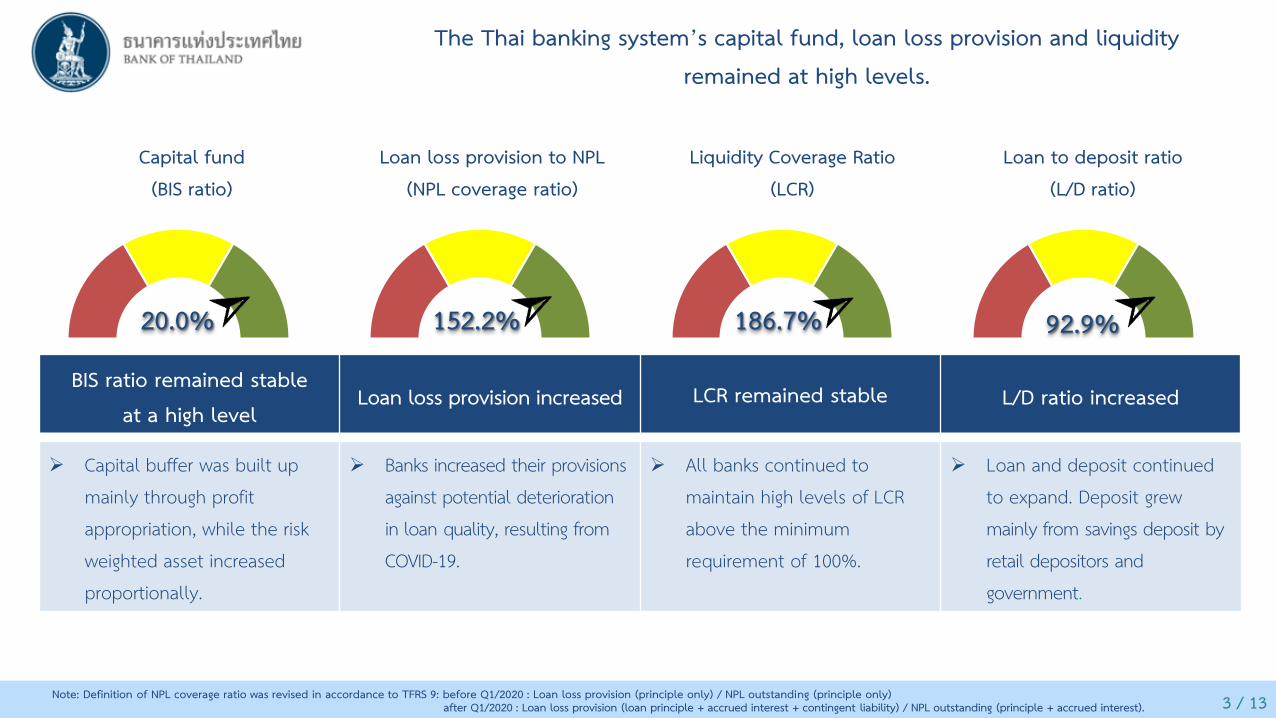

Capital Fund of the Thai banking system was at 3,038. 1 billion baht, equivalent to capital adequacy ratio (BIS ratio) of 20.0%. Loan loss provision remained high at 851.5 billion baht with NPL coverage ratio of 152.2%. Liquidity coverage ratio (LCR) registered at 186.7%.

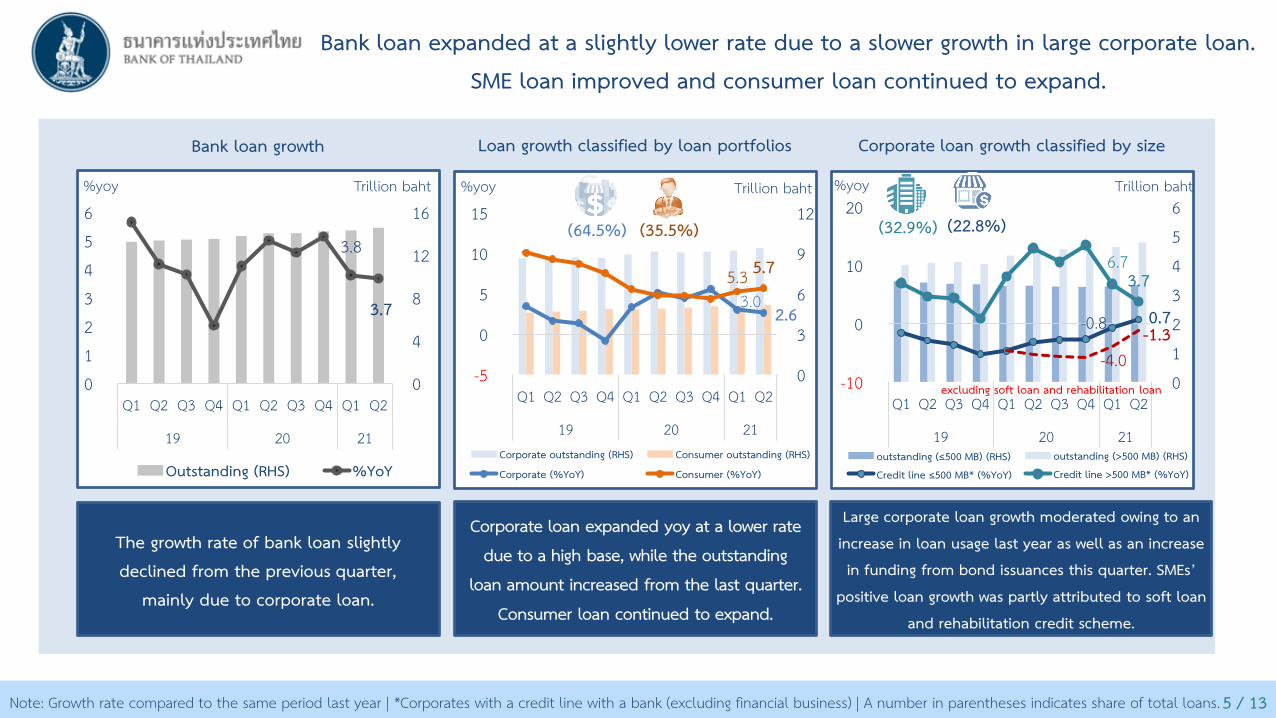

In the second quarter of 2021, banks’ overall loan growth was 3.7% year-on-year, slightly lower than 3.8% in the previous quarter. Details on bank loan are as follows:

Corporate loan growth decelerated to 2.6% year-on-year due to an increase in large corporates’1 loan usage during the second quarter of last year when financial markets were volatile, causing funding switch from corporate bond issuances to bank loan . Furthermore, there was also an increase in funding from corporate bond issuances in this quarter. SME loans2 improved and registered positive year-on-year growth partly owing to soft loan and rehabilitation credit scheme.

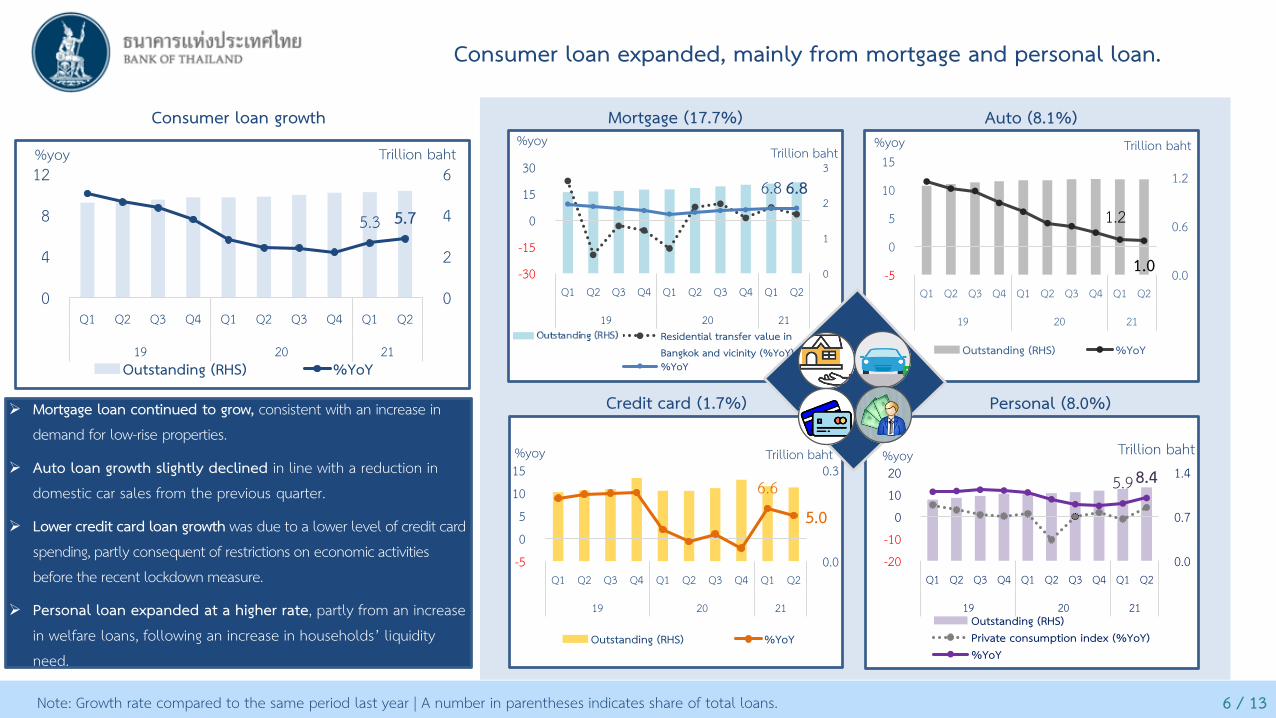

Consumer loans expanded at 5.7% year-on-year, increasing from 5.3% year-on-year growth rate in the previous quarter. The expansion was mainly attributed to mortgage loan, which continued to grow, consistent with an increase in demand for low-rise properties. Auto loan growth, on the other hand, slightly declined in line with a reduction in domestic car sales from the previous quarter. At the same time, credit card loan expanded at a lower rate due to a lower level of

1 Corporates with a credit line of more than 500 million baht with a bank as of June 2021. 2 Corporates with a credit line not exceeding 500 million baht with a bank as of June 2021.

credit card spending compared to the previous quarter, partly consequent of restrictions on economic activities before the recent lockdown measure. Meanwhile, personal loan grew at a higher rate, in parts from an increase in welfare loans, following an increase in households’ liquidity need.

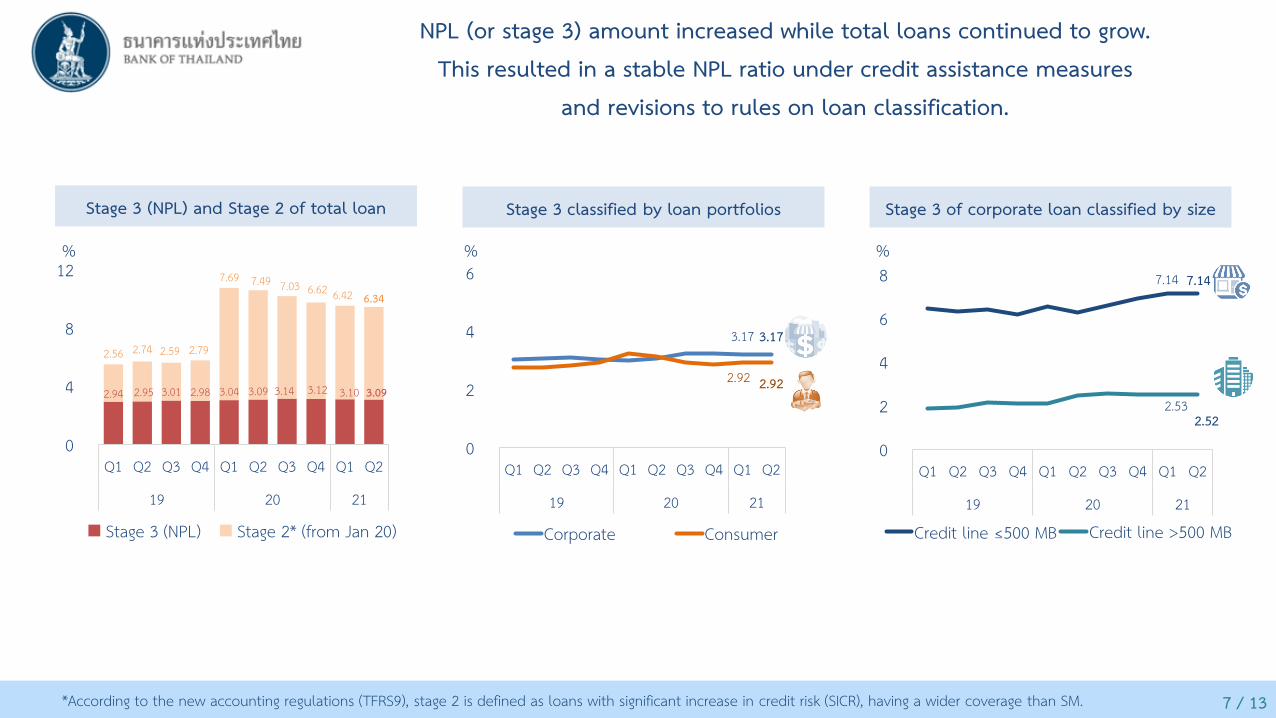

Bank loan quality in the second quarter of 2021 continued to be supported by financial assistance as well as revisions to rules on loan classification. As a result, the gross non-performing loan (NPL or stage 3) outstanding slightly increased to 545.5 billion baht, equivalent to NPL ratio of 3.09%. Meanwhile, the ratio of loans with significant increase in credit risk (SICR or stage 2) to total loans registered at 6.34%, declining from 6.42% in the previous quarter.

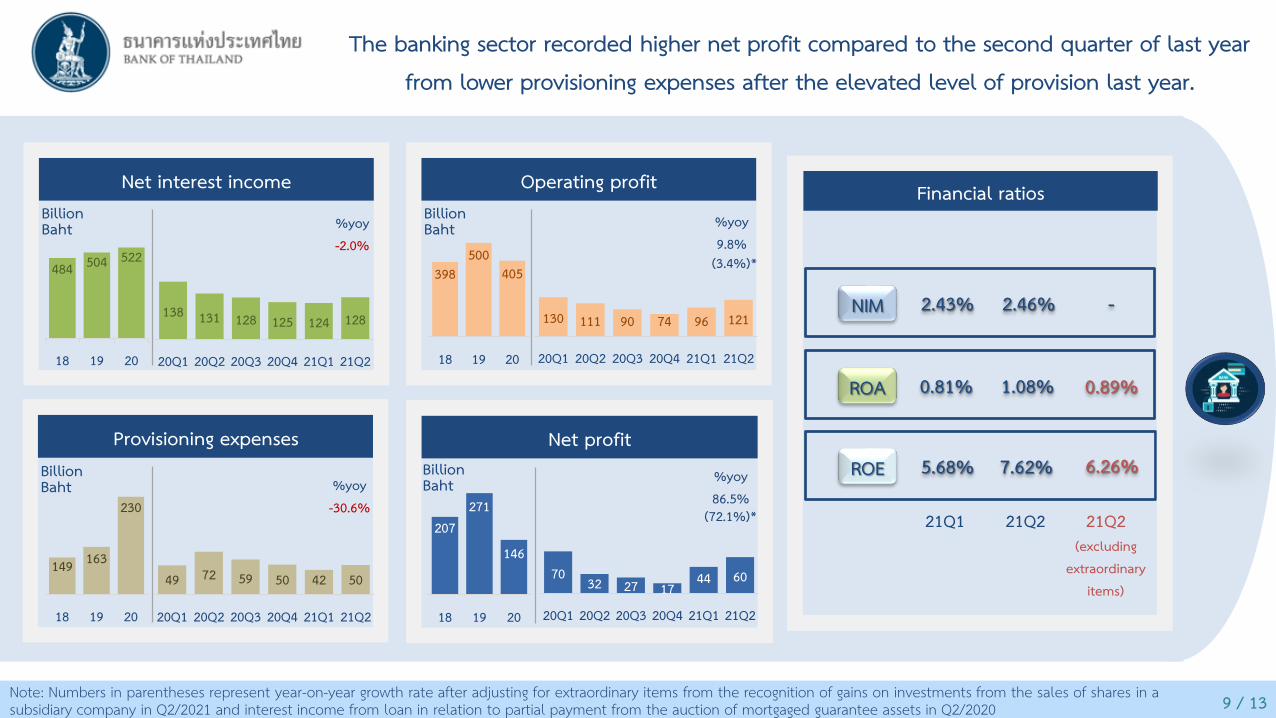

The banking system recorded net profit of 60.4 billion baht in the second quarter of 2021, increasing from the same quarter last year by 72.1%3. This was mainly attributed to a decline in provisioning expenses as banks had already set aside an elevated level of provision in 2020, together with higher non-interest income arising from dividend income and fee income. Compared to the previous quarter, net profit adjusted for the extraordinary items rose. This was due to an increase in dividend income and net interest income from an increase in interest revenue from loan expansion. Consequently, the ratio of return on asset (ROA) went up to 1.08% (or 0.89%4 after adjusting for the extraordinary item) in this quarter, from 0.81% in the previous quarter. At the same time, the ratio of net interest income to average interest-earning assets (Net Interest Margin: NIM) registered at 2.46%, at par with the previous quarter’s NIM of 2.43%.

The merger between TMB Bank and Thanachart Bank to TMBThanachart Bank (TTB) was completed on July 5, 2021. TTB hence becomes a larger bank, having greater connectedness with the rest of the banking system and provides a greater volume of essential financial services such as loans, deposits, payment transactions as well as servicing a larger number of customers. As a result, this year TTB is identified as one of domestic systemically important banks (D-SIBs) in addition to the existing 5 D-SIBs, namely Bangkok Bank, Krung Thai Bank, Bank of Ayudhya, Kasikornbank, and the Siam Commercial Bank. All D-SIBs are robust, maintaining capital ratios significantly above the level prescribed by the Bank of Thailand.

Bank of Thailand August 23, 2021

For further information, please contact: Banking Risk Assessment Division and Prudential Regulation 1 Tel: +66 2283 5980 and +66 2283 5874 (D-SIBs) Email: [email protected]

3 The year-on-year change after adjusting for extraordinary items from gains on investments from the sales of shares in a subsidiary company in Q2/2021 and interest income from loan in relation to partial payment from the auction of mortgaged guarantee assets in Q2/2020. 4 After adjusting for extraordinary items from gains on investments from the sales of shares in a subsidiary company in Q2/2021

Performance of the Thai Banking System

in the Second Quarter of 202123 August 2021

2 / 13

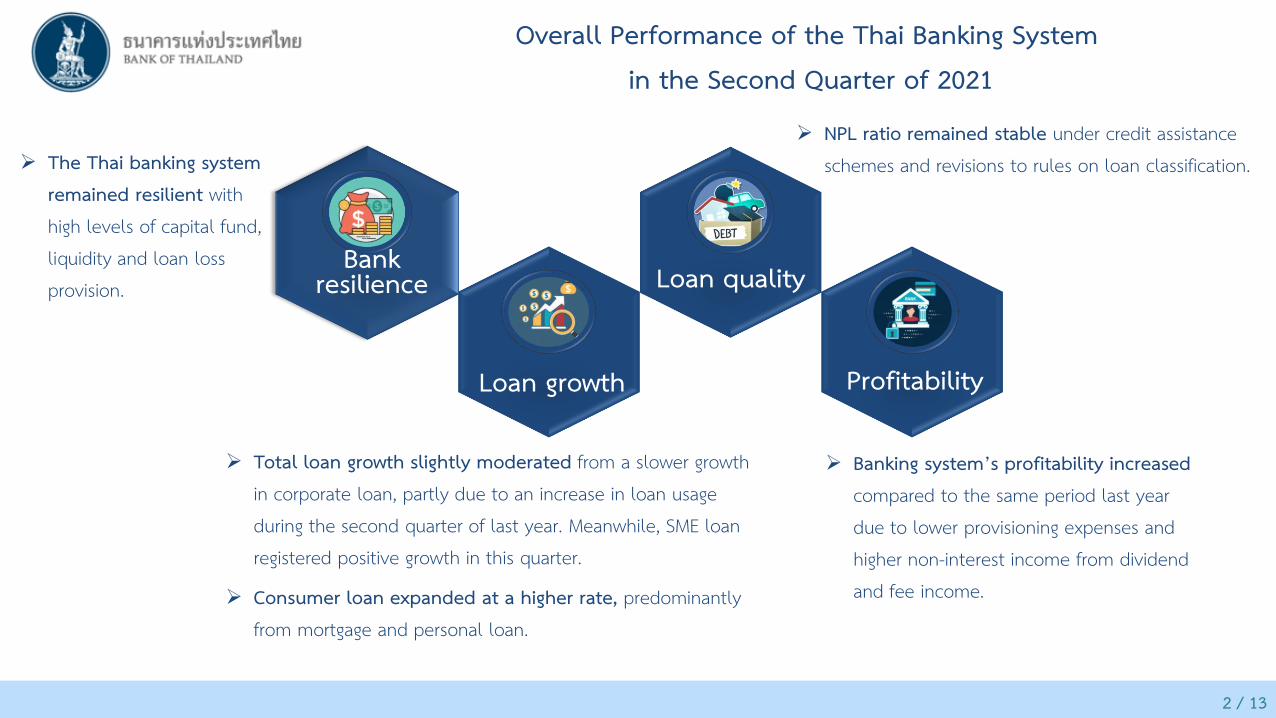

Overall Performance of the Thai Banking Systemin the Second Quarter of 2021

Bankresilience

Loan growth

Loan quality

Profitability

The Thai banking system remained resilient with high levels of capital fund, liquidity and loan loss provision.

Total loan growth slightly moderated from a slower growth in corporate loan, partly due to an increase in loan usage during the second quarter of last year. Meanwhile, SME loan registered positive growth in this quarter.

Consumer loan expanded at a higher rate, predominantly from mortgage and personal loan.

NPL ratio remained stable under credit assistance schemes and revisions to rules on loan classification.

Banking system’s profitability increased compared to the same period last year due to lower provisioning expenses and higher non-interest income from dividend and fee income.

3 / 13

The Thai banking system’s capital fund, loan loss provision and liquidity remained at high levels.

20.0% 152.2% 186.7% 92.9%

Capital buffer was built up mainly through profit appropriation, while the risk weighted asset increased proportionally.

Banks increased their provisions against potential deterioration in loan quality, resulting from COVID-19.

All banks continued to maintain high levels of LCR above the minimum requirement of 100%.

Loan and deposit continued to expand. Deposit grew mainly from savings deposit by retail depositors and government.

BIS ratio remained stableat a high level

Loan loss provision increased LCR remained stable L/D ratio increased

Capital fund(BIS ratio)

Loan loss provision to NPL(NPL coverage ratio)

Liquidity Coverage Ratio(LCR)

Loan to deposit ratio(L/D ratio)

Note: Definition of NPL coverage ratio was revised in accordance to TFRS 9: before Q1/2020 : Loan loss provision (principle only) / NPL outstanding (principle only)after Q1/2020 : Loan loss provision (loan principle + accrued interest + contingent liability) / NPL outstanding (principle + accrued interest).

4 / 13

4.2 4.46.0

4.26.0

12.4

2.3 2.0

9.6

-2.1

4.1

7.7

-12.1

5.0 4.5

-6.4

4.6 7.5

-4.2

5.1 3.8

-2.6

3.81.2

7.5

3.77.0

Real GDP Bank loan Bond

2017 2018 2019 20Q1 20Q2

Bank loan expanded at a slightly slower pace due to funding switch in 20Q2 from bond issuances to bank loans, coupled with an increase in funding from bond issuances this quarter.

Meanwhile, the economy registered positive growth from last year’s low base.

Note: Growth rate compared to the same period last year

20Q3 20Q4

%yoy %yoy %yoy

21Q1 21Q2

5 / 13

3.8

3.7

0

4

8

12

16

0123456

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

19 20 21Mi

llions

Outstanding (RHS) %YoY

Trillion baht

Bank loan growth Loan growth classified by loan portfolios Corporate loan growth classified by size

3.02.6

5.3 5.7

0

3

6

9

12

-5

0

5

10

15

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

19 20 21

Millio

ns

Corporate outstanding (RHS) Consumer outstanding (RHS)Corporate (%YoY) Consumer (%YoY)

Trillion baht

-0.8 0.7

6.7 3.7

0123456

-10

0

10

20

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

19 20 21

Milli

ons

outstanding (≤500 MB) (RHS) outstanding (>500 MB) (RHS)Credit line ≤500 MB* (%YoY) Credit line >500 MB* (%YoY)

Trillion baht

-1.3-4.0

(35.5%)(64.5%) (22.8%)(32.9%)

excluding soft loan and rehabilitation loan

%yoy %yoy %yoy

The growth rate of bank loan slightly declined from the previous quarter,

mainly due to corporate loan.

Corporate loan expanded yoy at a lower rate due to a high base, while the outstanding

loan amount increased from the last quarter. Consumer loan continued to expand.

Large corporate loan growth moderated owing to an increase in loan usage last year as well as an increase in funding from bond issuances this quarter. SMEs’

positive loan growth was partly attributed to soft loan and rehabilitation credit scheme.

Bank loan expanded at a slightly lower rate due to a slower growth in large corporate loan. SME loan improved and consumer loan continued to expand.

Note: Growth rate compared to the same period last year | *Corporates with a credit line with a bank (excluding financial business) | A number in parentheses indicates share of total loans.

6 / 13

Consumer loan expanded, mainly from mortgage and personal loan.

Consumer loan growth Mortgage (17.7%) Auto (8.1%)

Credit card (1.7%) Personal (8.0%)

6.65.0

0.0

0.3

-505

1015

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

19 20 21

Millio

ns

Outstanding (RHS) %YoY

%yoy%yoy

%yoy

Trillion baht%yoy Trillion baht

Trillion baht

5.3 5.7

0

2

4

6

0

4

8

12

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

19 20 21

Millio

ns

Outstanding (RHS) %YoY

Trillion baht

Trillion baht

Mortgage loan continued to grow, consistent with an increase in demand for low-rise properties.

Auto loan growth slightly declined in line with a reduction in domestic car sales from the previous quarter.

Lower credit card loan growth was due to a lower level of credit card spending, partly consequent of restrictions on economic activities before the recent lockdown measure.

Personal loan expanded at a higher rate, partly from an increase in welfare loans, following an increase in households’ liquidity need.

Note: Growth rate compared to the same period last year | A number in parentheses indicates share of total loans.

6.8 6.8

0

1

2

3

-30

-15

0

15

30

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

19 20 21Residential transfer value inBangkok and vicinity (%YoY)%YoY

5.98.4

0.0

0.7

1.4

-20-10

01020

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

19 20 21Outstanding (RHS)Private consumption index (%YoY)%YoY

1.2

1.0 0.0

0.6

1.2

-5

0

5

10

15

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

19 20 21

Outstanding (RHS) %YoY

%yoy

7 / 13

7.14 7.14

2.532.52

0

2

4

6

8

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

19 20 21Credit line ≤500 MB Credit line >500 MB

Stage 3 classified by loan portfolios Stage 3 of corporate loan classified by sizeStage 3 (NPL) and Stage 2 of total loan

2.94 2.95 3.01 2.98 3.04 3.09 3.14 3.12 3.10 3.09

2.56 2.74 2.59 2.79

7.69 7.49 7.03 6.62 6.42 6.34

0

4

8

12

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

19 20 21

Stage 3 (NPL) Stage 2* (from Jan 20)

%

3.17 3.17

2.92 2.92

0

2

4

6

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

19 20 21

Corporate Consumer

% %

NPL (or stage 3) amount increased while total loans continued to grow. This resulted in a stable NPL ratio under credit assistance measures

and revisions to rules on loan classification.

*According to the new accounting regulations (TFRS9), stage 2 is defined as loans with significant increase in credit risk (SICR), having a wider coverage than SM.

8 / 13

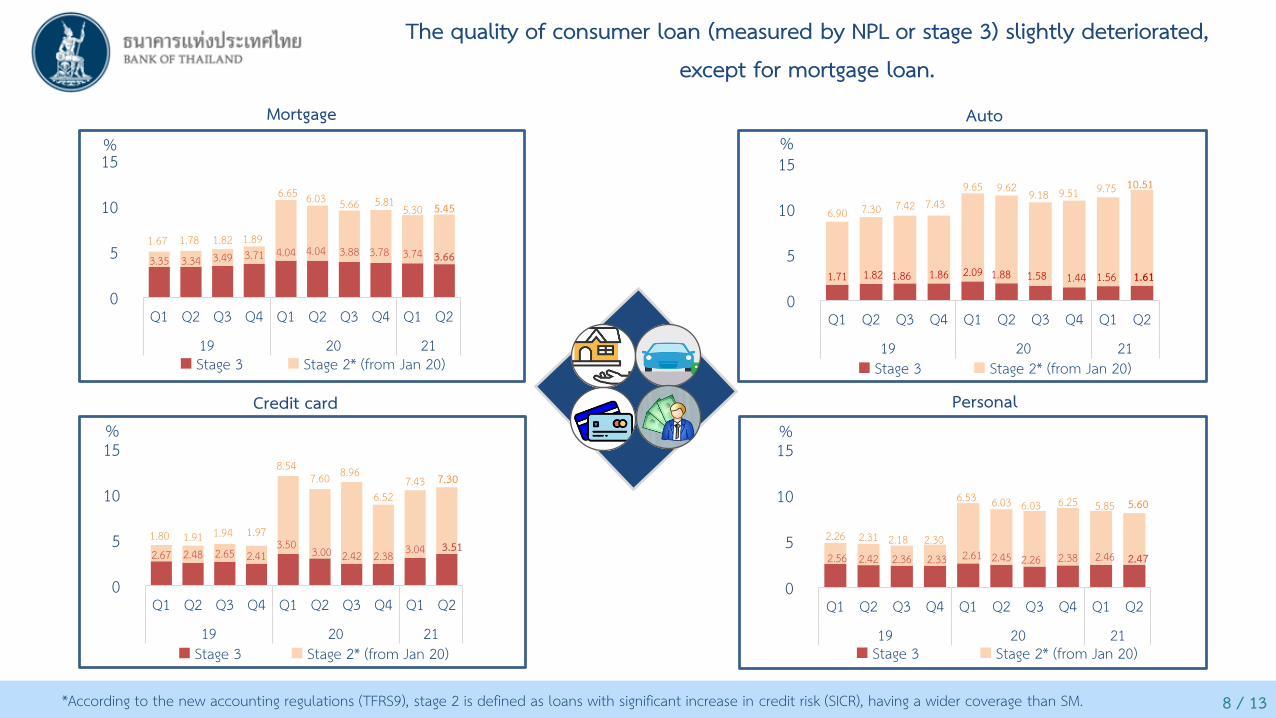

The quality of consumer loan (measured by NPL or stage 3) slightly deteriorated, except for mortgage loan.

Mortgage Auto

Credit card Personal

%

%

%

%

3.35 3.34 3.49 3.71 4.04 4.04 3.88 3.78 3.74 3.661.67 1.78 1.82 1.89

6.65 6.03 5.66 5.81 5.30 5.45

0

5

10

15

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q219 20 21Stage 3 Stage 2* (from Jan 20)

1.71 1.82 1.86 1.86 2.09 1.88 1.58 1.44 1.56 1.61

6.90 7.30 7.42 7.439.65 9.62 9.18 9.51 9.75 10.51

0

5

10

15

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q219 20 21

Stage 3 Stage 2* (from Jan 20)

2.67 2.48 2.65 2.413.50 3.00 2.42 2.38 3.04 3.51

1.80 1.91 1.94 1.97

8.547.60 8.96

6.527.43 7.30

0

5

10

15

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q219 20 21

Stage 3 Stage 2* (from Jan 20)

2.56 2.42 2.36 2.33 2.61 2.45 2.26 2.38 2.46 2.47

2.26 2.31 2.18 2.30

6.53 6.03 6.03 6.25 5.85 5.60

0

5

10

15

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q219 20 21

Stage 3 Stage 2* (from Jan 20)

*According to the new accounting regulations (TFRS9), stage 2 is defined as loans with significant increase in credit risk (SICR), having a wider coverage than SM.

9 / 13

NIM

ROA

ROE

2.43%

0.81%

5.68%

2.46%

1.08%

7.62%

21Q1 21Q2 21Q2 (excluding

extraordinary items)

Financial ratios

484 504 522

18 19 20

Net interest income

Provisioning expenses

138 131 128 125 124 128

20Q1 20Q2 20Q3 20Q4 21Q1 21Q2

%yoy-2.0%

149 163

230

18 19 20

49 72 59 50 42 50

20Q1 20Q2 20Q3 20Q4 21Q1 21Q2

%yoy-30.6%

Operating profit

398500

405

18 19 20

130 111 90 74 96 121

20Q1 20Q2 20Q3 20Q4 21Q1 21Q2

%yoy9.8%

(3.4%)*

Net profit

207271

146

18 19 20

70 32 27 1744 60

20Q1 20Q2 20Q3 20Q4 21Q1 21Q2

%yoy86.5%

(72.1%)*

0.89%

6.26%

-

The banking sector recorded higher net profit compared to the second quarter of last year from lower provisioning expenses after the elevated level of provision last year.

Note: Numbers in parentheses represent year-on-year growth rate after adjusting for extraordinary items from the recognition of gains on investments from the sales of shares in a subsidiary company in Q2/2021 and interest income from loan in relation to partial payment from the auction of mortgaged guarantee assets in Q2/2020

BillionBaht

BillionBaht

BillionBaht

BillionBaht

10 / 13

Debt Restructuring throughAsset Warehousing*

Rehabilitation Loan

Well-distributed by size, business sector and region

92,316 MBAverage credit line

3.1 MB/debtor30,194 debtors

Approved loan amount

10,511 MB 65 debtorsFinancial institutions and debtors have to negotiate

the terms and conditions.

42.6%of debtors are in

commerce and service sectors.

of debtors are from provincial areas.

67.5% 68.5%by existing credit lines

by credit lineby debtors

Note: Related laws on tax benefits and bad debt disposal for operations under asset warehousing scheme have been effective from July 14, 2021 onwards.

Debtors (%) Debtors (%) Debtors (%)

Development in financial rehabilitation measures as of August 16, 2021

Number of debtors under loan schemeApproved loan amount

of debtors are small businesses

(existing credit lines not exceeding 5 MB)

Number of debtors under the scheme

Many entrepreneurs have shown interests and are in the process of negotiating with financial institutions.

New debtors New debtors

11 / 13

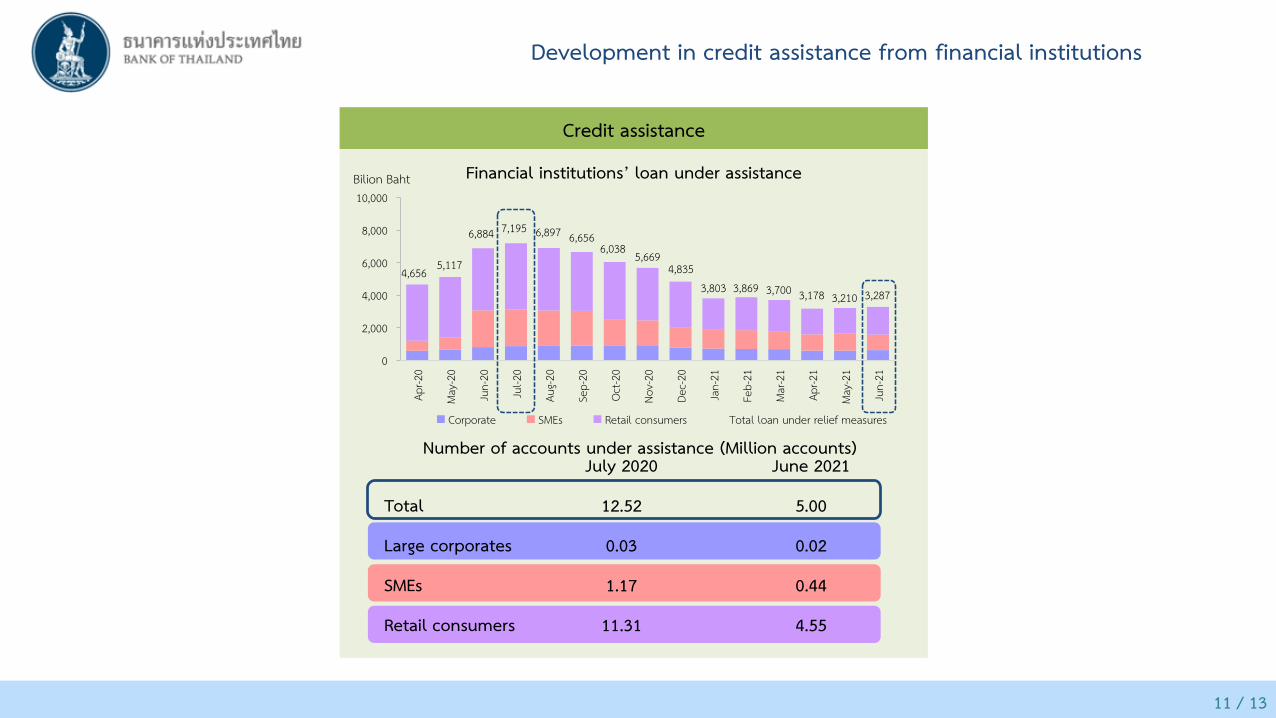

Development in credit assistance from financial institutions

Credit assistance

Financial institutions’ loan under assistance

4,656 5,117

6,884 7,195 6,897 6,6566,038 5,669

4,8353,803 3,869 3,700 3,178 3,210 3,287

0

2,000

4,000

6,000

8,000

10,000

Apr-2

0

May-2

0

Jun-

20

Jul-2

0

Aug-2

0

Sep-

20

Oct-2

0

Nov-

20

Dec-2

0

Jan-

21

Feb-

21

Mar-2

1

Apr-2

1

May-2

1

Jun-

21

Bilion Baht

Corporate SMEs Retail consumers Total loan under relief measures

July 2020 June 2021

Total 12.52 5.00

Large corporates 0.03 0.02

SMEs 1.17 0.44

Retail consumers 11.31 4.55

Number of accounts under assistance (Million accounts)

12 / 13

The result of this year’s assessment on Domestic Systemically Important Banks: D-SIBs

Merger

The merger between TMB Bank and Thanachart Bank to TMBThanachart Bank (TTB) resulted in TTB being identified as one of domestic systemically important banks (D-SIBs) this year.

D-SIBs from 2017 New D-SIBs in 2021

Indicators for identifying D-SIBs

Size Interconnectedness with other financial institutions

Key providers of payment system / Number of depositors

Complexity of products

All D-SIBs are robust, maintaining capital ratios significantly above the level prescribed by the BOT.

13 / 13

Key takeaways

1Thai banking system remained resilient with high levels of capital fund, liquidity and loan loss provision to cushion

economic impacts from COVID-19 pandemic as well as play an important role in facilitating assistances for borrowers in need.

2

The loan quality remained stable, partly due to revisions to rules on loan classification and assistance measures. However,

there is a sign of increasing vulnerability, especially in consumer loan. Going forward, debtors would likely require continued assistance following the prolonged and widespread impact of

COVID-19 outbreak.