Performance Measurement of Exchange Traded Funds

132

Department of Banking and Finance Performance Measurement of Exchange Traded Funds Master Thesis in Banking and Finance Lodged with Prof. Dr. Markus Leippold Under the supervision of Nikola Vasiljevic Lodged at Chair of Financial Engineering Author Thomas Schär Alte Bernstrasse 75b 3075 Rüfenacht BE E-Mail: [email protected] Matriculation number: 08-125-684 Zurich, August 18 th , 2014

Transcript of Performance Measurement of Exchange Traded Funds

Department of Banking and Finance

Performance Measurement of Exchange

Traded Funds

Master Thesis in Banking and Finance

Lodged with Prof. Dr. Markus Leippold

Under the supervision of Nikola Vasiljevic

Lodged at Chair of Financial Engineering

Author Thomas Schär

Alte Bernstrasse 75b

3075 Rüfenacht BE

E-Mail: [email protected]

Matriculation number: 08-125-684

Zurich, August 18th, 2014

i

Executive Summary

The selection of actively managed funds aims at identifying an investment that is likely to

outperform a selected benchmark. In contrast, excess performance is not a focus in choosing

Exchange Traded Funds (ETFs). This paper argues that the performance measures of active

funds are often not only irrelevant, but may be misleading when being applied to passively

managed ETFs. Investors of ETFs want to buy and sell a diversified bundle of assets with the

same return profile as the benchmark which is replicated. Since investing directly into the

benchmark is not possible, unlevered, passive ETFs aim to mirror, or track the performance of

the benchmark. Therefore the ETFs’ performance relative to the benchmark and the

competing ETFs is more significant than absolute returns. The key research question of this

study is therefore how to comprehensively measure and assess the tracking ability of ETFs. The

thesis aims to design an intuitive efficiency measure that helps selecting the most efficient ETF

amongst its peers replicating the same benchmark. The most distinctive feature of this paper is

that it does not only take several statistical considerations into account, but also adjusts for a

selection of typical trading strategies on the ETFs primary and secondary market.

As suggested by Hassine and Roncalli (2013), the theoretical framework of the ETF efficiency

measure is based on the Value-at-Risk (VaR) methodology and combines tracking difference,

tracking error and the bid-ask spread. The theoretical processing of the efficiency measure is

completed with empirical research conducted on unlevered, passively managed ETFs listed on

SIX. ETFs replicating the Swiss Market Index and the EURO STOXX 50 over the observation

period from May 2013 to May 2014 are considered. The VaR framework is extended

throughout this study by considering both the underlying assumptions about the distributions

of relative returns and the measurement methods of ETF risk-factors. Alternative calculation

techniques, robust and unilateral measures of tracking error are applied. Gaussian and non-

Gaussian distribution assumptions as well as intra-horizon risk are taken into account by

considering the historical VaR, Cornish-Fisher VaR, Expected Shortfall and Intra-Horizon VaR.

The empirical evidence in this study suggests that the ETF rankings according to the efficiency

measures are largely consistent across the data sample. More efficient funds tend to perform

better in most of the methods considered. However, the results of strongly depend on the

underlying statistical assumptions of the risk metrics as well as the trading characteristics of

the investor. The sample data is found to suffer from strong non-normality and data outliers.

The findings show that investors need to consider several ETF performance measurement

alternatives in their ETF selection process while adjusting the efficiency measures to their

underlying investment objectives and trading circumstances.

ii

Contents

List of Figures ............................................................................................................................... iv

List of Tables .................................................................................................................................. v

Chapter 1 Introduction ................................................................................................................ 1 1.1 Outline ........................................................................................................................................................ 2

Chapter 2 Exchange Traded Funds .............................................................................................. 3 2.1 Delimitation .............................................................................................................................................. 3 2.2 Historical Background ............................................................................................................................ 4 2.3 Replication Strategies ............................................................................................................................ 5

2.3.1 Physical Replication .............................................................................................................................. 6 2.3.2 Synthetic Replication ............................................................................................................................ 7 2.3.1 Net Asset Value ...................................................................................................................................... 8

2.4 ETF Costs .................................................................................................................................................... 8 2.4.1 Internal Costs ........................................................................................................................................... 9 2.4.2 External Costs .......................................................................................................................................... 9

2.5 Extra Revenue – Securities Lending ................................................................................................ 10 2.6 Indices ....................................................................................................................................................... 11 2.7 Market Environment ............................................................................................................................ 12

2.7.1 Providers ................................................................................................................................................. 12 2.7.2 Authorized Participants .................................................................................................................... 13 2.7.3 Creation- Redemption Process ...................................................................................................... 13 2.7.4 Investors and Trading Strategies ................................................................................................. 15

Chapter 3 ETF Risk Metrics ........................................................................................................ 16 3.1 Delimitation ............................................................................................................................................ 16 3.2 Tracking Efficiency: Tracking Difference and Tracking Error .................................................. 17

3.2.1 Tracking Difference ............................................................................................................................ 17 3.2.2 Tracking Error - Based on the Standard Deviation ............................................................... 18 3.2.3 Sources of Tracking Difference and Tracking Error .............................................................. 18

3.3 Liquidity Metrics .................................................................................................................................... 20 3.3.1 Delimitation: Relative versus Absolute Liquidity ................................................................... 20 3.3.2 AuM and Trading Volume ............................................................................................................... 21 3.3.3 Bid-Ask Spread ..................................................................................................................................... 21 3.3.4 Market Impact Costs and the Notional Traded ...................................................................... 23

3.4 Pricing Efficiency .................................................................................................................................... 24

Chapter 4 Literature Review ...................................................................................................... 25 4.1 ETF Performance ................................................................................................................................... 25 4.2 Tracking Efficiency, Liquidity and Pricing Efficiency ................................................................... 27

Chapter 5 Performance Measurement ...................................................................................... 30 5.1 ETF Selection Principles ....................................................................................................................... 30 5.2 Sharpe Ratio and Information Ratio ............................................................................................... 31

5.2.1 Pitfalls of the Information Ratio ................................................................................................... 33 5.3 The ETF Efficiency Measure by Hassine and Roncalli ................................................................ 35

iii

Chapter 6 Empirical Research .................................................................................................... 39 6.1 Data Sample ............................................................................................................................................ 39 6.2 Data Treatment ...................................................................................................................................... 40 6.3 Sample Statistics .................................................................................................................................... 41 6.4 Results for the ETFs on SMI ............................................................................................................... 42 6.5 Results for the ETFs on EURO STOXX 50 ........................................................................................ 45

6.5.1 Information Ratio versus Efficiency Measure ......................................................................... 48

Chapter 7 Adjustments to the Efficiency Measure .................................................................... 49 7.1 Pricing Efficiency .................................................................................................................................... 49 7.2 Alternative Tracking Error Measures .............................................................................................. 50

7.2.1 TE – Based on Correlation of Returns ......................................................................................... 50 7.2.2 Tracking Error based on the Residuals of a Linear Regression ........................................ 53 7.2.3 Tracking Error based on Robust Measures .............................................................................. 54 7.2.4 Tracking Error based on Semi-Variance .................................................................................... 57 7.2.1 Autocorrelation ................................................................................................................................... 61

7.3 Alternative Bid-Ask Spread Measurement .................................................................................... 63 7.4 Alternative Value-at-Risk Measures ................................................................................................ 66

7.4.1 Cornish-Fisher Value-at-Risk .......................................................................................................... 70 7.4.1 Historical Value-at-Risk .................................................................................................................... 72 7.4.2 Intra-horizon Value-at-Risk ............................................................................................................ 74 7.4.1 Expected Shortfall ............................................................................................................................... 78

7.5 Alternative Interpretation of the Efficiency Measure ............................................................... 80

Chapter 8 Conclusion and Outlook ............................................................................................ 81

iv

List of Figures

Figure 1: ETP Classification ............................................................................................................ 4

Figure 2: Global ETP Numbers and AuM ....................................................................................... 5

Figure 3: ETF Replication Strategies .............................................................................................. 6

Figure 4: Internal and External Costs ............................................................................................ 8

Figure 5: Dividend Distribution ................................................................................................... 12

Figure 6: Creation - Redemption Process .................................................................................... 14

Figure 7: Tracking and Pricing Efficiency ..................................................................................... 16

Figure 8: Sources of Tracking Error and Tracking Difference ...................................................... 19

Figure 9: Impact Factors on Bid-Ask Spread................................................................................ 22

Figure 10: Information Ratio based on Benchmark .................................................................... 32

Figure 11: Information Ratio based on Tracker .......................................................................... 34

Figure 12: Illustration of the Efficiency Measure ........................................................................ 36

Figure 13: Larger Tracking Difference ......................................................................................... 37

Figure 14: Larger Bid-Ask Spread ................................................................................................ 37

Figure 15: Larger Tracking Error .................................................................................................. 37

Figure 16: Percentage Spread ETF 2# SMI................................................................................... 43

Figure 17: Tracking Difference ETF 2# SMI .................................................................................. 43

Figure 18: Tracking Difference ETF 1# SMI .................................................................................. 44

Figure 19: Tracking Difference ETF 5# SMI .................................................................................. 45

Figure 20: Tracking Difference ETF 7# EURO STOXX 50 .............................................................. 46

Figure 21: Percentage Spread ETF 2# EURO STOXX 50 ............................................................... 47

Figure 22: Sample Regression with Data Outliers ....................................................................... 52

Figure 23: Sample Regression without Data Outliers ................................................................. 52

Figure 24: Tracking Difference ETF 5# EURO STOXX 50 .............................................................. 56

Figure 25: Tracking Difference ETF 3# EURO STOXX 50 .............................................................. 58

Figure 26: Autocorrelation Function ETF 3# SMI ........................................................................ 62

Figure 27: Autocorrelation Function ETF 1# EURO STOXX 50 ..................................................... 62

Figure 28: Relative Tracking Difference Distribution .................................................................. 66

Figure 29: Absolute Tracking Difference Distribution ................................................................. 69

Figure 30: Cumulative Tracking Error ETF 1# and 3# on SMI ...................................................... 74

Figure 31: Decision Tree of ETF Efficiency Measures .................................................................. 85

Figure 32: Time Series ETF Tracking Difference ........................................................................ 107

Figure 33: ETF Autocorrelation Function .................................................................................. 113

Figure 34: Percentage Bid-Ask Spreads ..................................................................................... 117

v

List of Tables

Table 1: Information Ratio .......................................................................................................... 31

Table 2: Results for the ETFs on SMI ........................................................................................... 42

Table 3: Results for the ETFs on EURO STOXX 50 ........................................................................ 46

Table 4: Information Ratio ETF SMI............................................................................................. 48

Table 5: Information Ratio ETF EURO STOXX 50 ......................................................................... 48

Table 6: Pricing Efficiency ETF SMI .............................................................................................. 49

Table 7: Pricing Efficiency ETF EURO STOXX 50 .......................................................................... 49

Table 8: Tracking Error ................................................................................................................ 51

Table 9: Alternative TE ETF SMI .................................................................................................. 53

Table 10: Data Outliers ETF SMI .................................................................................................. 54

Table 11: Data Outliers ETF EURO STOXX 50 .............................................................................. 54

Table 12: Robust TE ETF SMI ....................................................................................................... 55

Table 13: Robust TE ETF EURO STOXX 50 .................................................................................... 56

Table 14: IQR ETF SMI ................................................................................................................. 57

Table 15: IQR ETF EURO STOXX 50 .............................................................................................. 57

Table 16: Semi-Variance ETF SMI ................................................................................................ 59

Table17: Semi-Variance ETF EURO STOXX 50 ............................................................................. 60

Table 18: Adjusted Spread ETF SMI ............................................................................................. 64

Table 19: Adjusted Spread ETF EURO STOXX 50 ......................................................................... 65

Table 20: Normality Test ETF SMI ............................................................................................... 68

Table 21: Normality Test ETF EURO STOXX 50 ............................................................................ 69

Table 22: Cornish-Fisher VaR ETF SMI ......................................................................................... 70

Table 23: Cornish-Fisher VaR ETF EURO STOXX 50 ..................................................................... 71

Table 24: Historical VaR ETF SMI ................................................................................................. 72

Table 25: Historical VaR ETF EURO STOXX 50 ............................................................................. 72

Table 26: Intra-horizon VaR ETF SMI ........................................................................................... 76

Table 27: Intra-horizon VaR ETF EURO STOXX 50 ....................................................................... 77

Table 28: Expected Shortfall ETF SMI .......................................................................................... 79

Table 29: Expected Shortfall EURO STOXX 50 ............................................................................. 79

Table 30: EURO STOXX 50 ......................................................................................................... 100

Table 31: Swiss Market Index .................................................................................................... 101

Table 32: ETF Sample ................................................................................................................ 102

Table 33: Fund Information ....................................................................................................... 103

Table 34: Trading Information .................................................................................................. 105

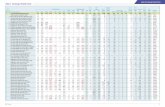

Table 35: Efficiency Measures Overview .................................................................................. 121

Table 36: Efficiency Measures Overview without Spread ......................................................... 123

vi

Abbreviations

AP Authorized Participant

AuM Asset under Management

Bps Basis Points

CHF Swiss Franc

CESR Committee of European Securities Regulators

ES Expected Shortfall

ESMA European Securities and Markets Authority

ETF Exchange Traded Fund

ETI Exchange Traded Instrument

ETN Exchange Traded Note

ETP Exchange Traded Product

FINMA Swiss Financial Market Supervisory Authority

iid independent and identically distributed

iNAV indicative Net Asset Value

IQR Interquartile Range

IOSCO International Organization of Securities Commissions

IR Information Ratio

LOB Limit Order Book

LPM Lower Partial Moment

MAD Median Absolute Deviation

MiFID Markets in Financial Instruments Directive

NAV Net Asset Value

OTC Over-the-Counter

PnL Profit and Loss

SIX SIX Swiss Exchange

SMI Swiss Market Index

TD Tracking Difference

TE Tracking Error

TER Total Expense Ratio

UCITS Undertakings for Collective Investment in Transferable Securities Directives

USD United States Dollar

VaR Value-at-Risk

Chapter 1 Introduction

1

Chapter 1 Introduction

Over the past decade, Exchange Traded Products (ETP) have experienced a surge in popularity

whereas the possibilities of their application has increased. iShares, being the largest ETP

provider in the world with more than 440 funds and over USD 480 billion of Assets under

Management (AuM), estimates that the ETP industry grew from worldwide 106 products with

USD 79,4 billion AuM in 2002 to 5’025 ETPs with USD 2’300 billion AuM in January 2014

(iShares, 2014, p.5). This trend seems to continue as the industry grows across all markets and

segments.

Above all, the subcategory of Exchange Traded Funds (ETF) was responsible for a large amount

of the growth in ETPs (Blackrock, 2012, p.4). In Switzerland, the number of ETFs increased from

888 listed products in 2012 to 940 in 2013 with a rise in volume of roughly 20% (SIX, 2013a,

p.3). Moreover, during the financial crisis in 2008 ETFs boosted their volume unlike any other

investment class (SIX, 2009, p.5). Institutional as well as retail investors gained interest in these

products, which offer index tracking, the main purpose of ETFs, at relative modest costs.

In accordance with the enormous increase in size, came an increase in variety and complexity

of ETFs. Nevertheless, ETFs are praised for their high level of transparency and are thus

awarded a special role in comprehensive due diligence procedures and risk management to

investors. Guidelines from regulatory bodies such as the Undertakings for Collective

Investment in Transferable Securities Directives (UCITS) in Europe on the one hand and

enhanced due diligence procedures by the ETF providers on the other hand, helped to increase

the investment knowledge on ETFs. Nevertheless investors need to be aware of several factors

when looking for ETFs suiting their portfolio and investment needs. They not only need to take

into account investor-related factors such as the underlying investment objective, horizon and

universe, they also need to compare and contrast ETFs from a range of providers according to

their structure, tradability, risk and performance.

As selecting the most excellent fund is core for any investor, the efficiency and performance1

of an ETF is a primary concern. Where traditional mutual funds are judged by how much they

outperform their opponents and benchmark, the performance measurement of ETFs is not

straightforward, as their aim is not to beat the performance of their underlying benchmark,

1 ETF Efficiency and performance are used as synonyms in the context of this thesis. In order to achieve a consistent terminology

throughout the study, the official ETF terminologies by the European Securities and Markets Authority (ESMA) and the naming of

the ETFs according to SIX Swiss Exchange are applied. If not stated otherwise, the term ETF refers to long only, passively managed,

unlevered exchange traded funds. ETF performance and ETF efficiency measurement are used conterminously.

Chapter 1 Introduction

2

but to replicate it as close as possible. Since many tools developed for traditional funds fail

when being applied to ETFs, standalone measures such as the tracking error and the tracking

difference are used to compare the ETF’s tracking ability. However, little is known about their

consolidation and joint interpretation as one comprehensive ETF performance measure.

1.1 Outline

The overall structure of the study takes the form of eight chapters, including this introductory

chapter. In order to acquire a fundamental knowledge about the ETFs history, replication

strategies, costs, revenues, market environment and trading characteristics, Chapter 2

presents thorough discussion of the specific features of the ETFs. As for every section of the

thesis, the theoretical outlay in Chapter 2 focuses on factors relevant for efficiency

measurement.

Chapter 3 holds the processing of both qualitative and quantitative performance

measurement and provides the full mathematical framework of the ETFs performance metrics.

Chapter 4 will complement the theoretical insight on the performance of ETFs with an

extensive literature review.

Looking at existing performance figures, Chapter 5 presents both empirical as well as

mathematical assessment on existing funds evaluation methods. Ultimately, the framework

for the efficiency measurement of ETFs, initially designed by Hassine and Roncalli (2013), will

be set up.

Chapter 6 presents the data sample processed in this study and calculates the efficiency

measure for the ETFs selected. Moreover, comprehensive insight on the data sample and data

treatment is given.

The analysis in Chapter 7 enhances the basic model by applying Gaussian and non-Gaussian

efficiency measures, as well as liquidity risk and alternative tracking error measures.

The conclusion Chapter 8 summarizes and critically evaluates the empirical and mathematical

findings. As a final point, areas for further ETF research are identified.

Chapter 2 Exchange Traded Funds

3

Chapter 2 Exchange Traded Funds

According to the European Securities and Markets Authority (ESMA), ETFs are open-ended

collective investment schemes that trade throughout the day like a stock on the secondary

market, which takes place on the exchange. Generally, ETFs seek to mirror the performance of

a target benchmark and are structured and operate in a similar way. Like operating companies,

ETFs register subscriptions and redemptions of shares and list their shares for trading (ESMA,

2011, p.9). From a legal perspective, ETFs are considered to be special assets not included in

the bankruptcy assets, should the ETF provider become insolvent. Unlike index funds which

are priced only once at the end of each trading session, ETF prices adjust throughout the day

and can be bought without any direct subscription and redemption fee on the secondary

market (Picard & Braun, 2010, p.2).

2.1 Delimitation

Since the inception of the first ETP, a large number of products have been introduced in the

financial market. Whereas ETFs have to pursue strict guidelines the widening of the ETP

product universe put forth many, partially regulated products such as Exchange Traded Notes

(ETNs). For the sake of clarity, it is crucial to consistently distinguish these instruments

according to their types. The classification in this paper generally follows the suggestion by

iShares (2014, p.17).

ETPs are understood as an umbrella term of three subcategories. Besides the mentioned ETFs,

the second subcategory subsumes ETNs as well as Exchange Traded Commodities (ETCs),

whereas the third subcategory covers the remaining Exchange Traded Instruments (ETIs). ETNs

are structured products that are issued as non-interest paying debt instruments, whose prices

fluctuate with an underlying index or an underlying basket of assets. Because they are debt

obligations, ETNs are backed by the issuer and subject to the solvency of the issuer (ESMA,

2012b, p.10). The remaining ETP-spectrum that is neither defined as funds nor as notes, is

classified as ETIs. Here included are listed options, warrants and hybrid instruments (iShares,

2014, p.11). Figure 1 highlights the important distinction of these product classes.

Chapter 2 Exchange Traded Funds

4

Figure 1: ETP Classification

The distinction of ETPs is illustrated. The term Exchange Traded Product covers Exchange Traded Funds, Exchange Traded Notes/ Exchange Traded Commodities and Exchange Traded Instruments. (Source: Own illustration following iShares, 2014)

The subcategories, ETNs, ETCs and ETIs will not be subject to analysis in this paper.

2.2 Historical Background

Eugene Fama set the cornerstone for passive management in 1965 with his study on market

efficiency. He suggested that, since the prices of securities instantly and fully reflect all public

and inside information available, price movements cannot be predicted using past prices. In

consequence, investors on average can only perform the same as the market. They come off

best by simply buying and holding a diversified basket of stocks, whilst minimizing fees and

taxes (Fama, 1965). Following the idea by Fama, Wells Fargo, an American banking and

financial services company, commercially adapted a passive strategy and launched the first

institutional index fund in 1976. The first index fund available for retail investor was launched

by Vanguard only five years later (Hehn, 2006, p.120).

Nonetheless, it was not until 1993 that ETFs initially became a viable investment opportunity.

Indeed, the first registered index-tracker was launched that year by State Street Global

Advisors under the name of SPDR tracking the US-Stock index S&P 500. Today, this fund

remains one of the most heavily traded funds in the world, with more than USD 37 billion AuM

(Picard & Braun 2010, p.17).

Whereas the story of success of ETFs in Europe began in the 2000, the total amount of ETFs

available globally had grown to 169 a year later only, whereby 103 of ETFs were traded

exclusively on U.S. markets (Wiandt & McClatchy, 2001, p.73). Apart from Switzerland, it was

Germany, Great Britain and Sweden who were the vanguards by offering ETFs in Europe

(Picard & Braun, 2010). Deutsche Börse emerged as the most important trading platform for

ETFs in Europe, significantly contributing to its success story (Hehn, 2006, p.120). In 2004 the

first ETFs on Emerging Markets, Real Estate and Commodities were introduced, whereas two

Exchange Traded Products (ETPs)

Exchange Traded Funds (ETFs)

Exchange Traded Notes (ETNs) /

Exchange Traded Commodities

(ETCs)

Exchange Traded Instruments (ETIs)

Chapter 2 Exchange Traded Funds

5

years later, the first ETFs taking short positions have been launched (Picard & Braun, 2010,

p.17). Figure 2 presents the global development of number and AuM of both ETFs and ETPs

since 1993. Only the financial crisis in 2008 resulted in a yearly decrease AuM of both ETFs and

ETPs. The amount of products on the market however steadily increased since the first

inception of an ETF.

Figure 2: Global ETP Numbers and AuM

The development of ETP and ETF AuM and the number of products are illustrated over the period from 1993 to June 2014. The ETF AuM figures for June 2014* are estimations, as official figures are not available. (Source: Own illustration following Blackrock 2009, 2012 & 2014)

2.3 Replication Strategies

ETFs can be categorized by their way of replicating a benchmark. Two main types of index

replication, namely physical and synthetic replication, can be differentiated. Physically

replicating ETFs hold all or a selection of constituents of an index, whereas synthetic

replication refers to the usage of derivatives in order to achieve benchmark returns. Synthetic

ETFs deliver the performance of a benchmark through the use of swaps and other derivatives

(IOSCO, 2013, p.2).

The style of replication has a significant influence on the ETFs tracking ability and subsequently

is explained in more detail. The explanations follow the principles for the regulation of ETFs,

issued in 2013 by the board of the International Organization of Securities Commission

(IOSCO), which regulates more than 95% of the world’s securities markets. Figure 3 gives an

overview on the commonly used segmentation of ETFs according to their replication strategy.

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013June

2014*

ETF AuM 0.8 1.1 2.3 5.3 8.2 17.6 39.6 74.3 105 142 212 310 412 566 796 711 1036 1311 1351 1644 2010 2207

ETP AuM 0 0 0 0 0 0 2 79.4 109 146 218 319 428 598 851 772 1156 1483 1525 1944 2396 2632

# of ETFs 3 3 4 21 21 31 33 92 202 280 282 336 461 713 1170 1595 1944 2460 3011 3297 3490 3650

# of ETPs 0 0 0 0 0 0 2 106 219 297 300 357 524 883 1541 2220 2694 3543 4311 4759 4988 5217

0

1000

2000

3000

4000

5000

0

500

1000

1500

2000

2500

3000

Nu

mb

er

of

pro

du

cts

Au

M i

n m

illi

on

US

D

Chapter 2 Exchange Traded Funds

6

Figure 3: ETF Replication Strategies

The ETF Replication Strategies are depicted. Physical and synthetic replication is differentiated. Physical replication can be further split into the full replication and the sampling methods, which furthermore comprises the representative and optimized sampling. Synthetic replication includes the unfunded and the fully funded swap model. (Source: Own illustration following the classification by IOSCO, 2013; iShares, 2014; Picard & Braun, 2010)

2.3.1 Physical Replication

Physically replicating ETFs can be segmented according to the share of benchmark constituents

they hold. ETFs which contain all elements of a benchmark are referred to as fully replicating.

Whereas ETFs that hold a selection of the underlying constituents are denoted as optimized or

partially replicating (IOSCO, 2013, p.2). If the physically replicating ETF does not conduct

securities lending, a process described later on in more detail, the strategy generally does not

expose an investor to counterparty risk (Hehn, 2006, p.16). Derivatives are only used in order

to equitize cash dividends of the constituents. In this process, the ETF avoids building up

unprofitable cash-positions by reinvesting the cash trough futures and other derivatives

(Wiandt & McClatchy, 2001, p.42).

2.3.1.1 Full Replication

A fully replicating ETF generally invests in the component securities of the underlying

benchmark in the same approximate proportions as in the benchmark itself. In consequence,

this type of ETF commonly displays a high degree of transparency (IOSCO, 2013, p.2).

Besides offering relatively close tracking of the benchmark, certain methodical problems might

arise with full replication as Benchmark constituents often are published with rounded down

decimal places only. Furthermore, dividend distributions may result in a higher cash

component of the ETFs. The reason is that the ETF distributes dividends each quarter or

semester only, whereas the benchmark may assume to distribute dividends on a daily basis.

Replication

strategies

Physical replication

Full replication

Sampling methods

Representative sampling

Optimized sampling

Synthetic replication

Unfunded swap model

Fully funded swap model

Chapter 2 Exchange Traded Funds

7

Replicating broad indices such as the MSCI World furthermore is costly, as more securities

have to be bought in order to fully replicate the index. On the one hand this increases

corresponding transaction costs, on the other hand, it leads to frequent rebalancing within the

index. The cancellation and admission of new benchmark constituents increases the

rebalancing costs for the ETF. Finally, if the index holds illiquid constituents, prices might be

driven up by the additional demand triggered by the ETF (Picard & Braun, 2010, p.47-48).

2.3.1.2 Replication by Sampling

With sampling techniques, the ETF overcomes some of the problems previously mentioned.

The ETFs thus acquires only a subset of the underlying indexes constituents whilst adding

securities that exhibit similar return patterns as the constituents omitted (IOSCO, 2013, p.2).

This method has the advantage of lower management fees and administrative costs but the

ETF may suffer from more inaccurate return tracking (Picard & Braun, 2010, p.42).

2.3.2 Synthetic Replication

Synthetic or derivative replicating ETFs invest in a diversified basket of assets while entering

into a derivative contract, typically through a total return swap (IOSCO, 2013, p.2). The swap

counterparty guarantees to deliver the return of the index in exchange for a variable swap

spread (Picard & Braun, 2010, p.52).

Although this replication strategy avoids the high rebalancing costs and tracking inaccuracy

associated with physical replication, it exposes the investor to counterparty risk. Regulatory

requirements reduce the risk arising. A UCITS fund in Europe e.g. is allowed to maximally

allocate 10% of its total assets into derivatives such as swaps (ESMA, 2012b, p.7). In case of

default of the swap counterparty, the ETF should be fully covered by the collateral of the swap

contract (Picard & Braun, 2010, p.61).

According to IOSCO Guidelines, the unfunded and the funded structure of a synthetic

replicating ETF can be further differentiated. In an unfunded structure, the ETF manager

invests in a substitute or reference basket of securities. This baskets return is used as collateral

in the derivative contract in exchange for the return of the index (IOSCO, 2013, p.3). In the

funded model, synthetic ETFs engage in a swap in exchange for cash without the creation of a

substitute basket (IOSCO, 2013, p.3). The fund transfers the cash proceeds from investors to

the counterparty, which in return provides collateral in excess of the subscription value and

further guarantees the performance of the benchmark (iShares, 2014, p.14).

Chapter 2 Exchange Traded Funds

8

2.3.1 Net Asset Value

The value of an ETFs underlying constituents is described by its Net Asset Value (NAV). The

NAV is calculated by summing the value of all constituents of the fund including cash positions

and deducting all liabilities. The sum is divided by the amount of outstanding ETF shares on a

daily basis, in order to receive the NAV (iShares, 2014, p.50). A unique feature of ETFs is that a

so-called indicative Net Asset Value (iNAV) is issued. It is calculated throughout the day from

current market prices and is published every 15 seconds (iShares, 2014, p.50). This process

allows for real-time tradability of an ETF. Conversely, traditional mutual funds are prices once

a day (Picard & Braun, 2010, p.6).

2.4 ETF Costs

ETFs attract a broad range of investors due to their diversification benefits coming at low fees.

Depending on the provider, the benchmark and the replication method, ETF costs may

however diverge and therefore need to be watched closely (Picard & Braun, 2010, p.8). This

section therefore assesses the total costs of ETF ownership. In line with the classification of

iShares (2014, p.44), internal cost, being ongoing charges to the ETF, are differentiated from

external costs, which are costs incurred at the time of trading the ETF. Figure 4 presents the

classification of costs for both physically and derivative replicating ETFs.

Figure 4: Internal and External Costs

The internal cost of holding the ETF and the external cost from trading the ETF are listed for both physical and synthetic replicating ETFs. (Source: Own illustration following iShares, 2014, p.44)

Fund structure

Physical replicating

synthetic replicating

Internal costs

- Total expense ratio

- Rebalancing Costs

-Additional factors

- Total expense Ratio

- Swaps Spread

-Additional factors

External costs

-Bid- / Ask -Spreads

-Transaction Costs

- Taxation

Chapter 2 Exchange Traded Funds

9

2.4.1 Internal Costs

The set of internal costs include all expenses of the ETF on an ongoing basis. The most

prominent, being the Total Expense Ratio (TER) and the rebalancing costs, are discussed

subsequently.

TER is expressed in percentages and includes all ongoing fees charged to the ETF (Picard &

Braun, 2010, p.27). The TER must be officially published by the ETF provider and has to

comprise the following indicative, but not exhaustive list of charges:

It has to include all payments to the management company, directors, depositary, custodians,

investment adviser as well as any outsourced services of the ETF. The management fee hereby

covers all costs arising from ETF administration, maintenance and management (Picard &

Braun, 2010, p.27). Furthermore, registration and regulatory fees as well as audit fees must be

included in the TER. Entry and exit charges, as well as performance related fees are not

covered by the TER (Committee of European Securities Regulators, 2010). The TER is deducted

from a fund’s NAV on a daily basis and therefore influences an ETFs daily tracking performance

(iShares, 2014, p.45).

Rebalancing cost arise when a change in the benchmark requires a reweighting of the ETFs

constituents. Equivalently, costs arising from a change in the variable swap spread are

regarded as internal costs for synthetic ETFs (iShares, 2014, p.45). Both cost types negatively

influence an ETFs tracking performance.

2.4.2 External Costs

External costs are defined as costs that are charged to the investor only at the time of ETF

trading. They include trading costs such as the bid-ask spread and transaction costs as well as

any taxes levied on the ETF trade.

Bid and ask prices indicate the best price at which a security can be sold and bought at a given

point in time (Picard & Braun, 2010, p.88). The bid-ask spread of an ETF is defined as the

difference between the bid price and the ask price. The bid-ask spread is always positive as the

maximal price for which an investor is willing to sell his ETF shares is always larger than the

price for which he is willing to buy them (Picard & Braun, 2010, p.28). The spread does not

directly influence the tracking performance of the ETF. However, it is crucial factor in ETF

liquidity measurement and will be subject to profound evaluation in Chapter 3.

Chapter 2 Exchange Traded Funds

10

Transaction costs comprise all additional costs that arise when an ETF is sold or bought. Such

costs include brokerage and custody feed and provisions for banks and brokerage dealers

(Picard & Braun, 2010, p.102).

The taxation of an investment in an ETF may occur on the ETF, the underlying securities and

the investor level.

On a fund level the applicable jurisdiction of the domicile country as well as the legal structure

of the ETF are relevant (iShares, 2014, p.21). For all ETF structures in Switzerland, income and

capital taxes have to be paid only on a dividend and investor level, as ETFs do not represent a

legal entity (Picard & Braun, 2010, p.83). Withholding taxes on income or on capital gains

received by the fund are charged at the ETF constituents’ level. They arise in the country

where the underlying securities are situated and strongly depend on the treaty between the

country of the securities and the country in which the ETF is domiciled. Those two layers of

taxation become especially important as the benchmark and the ETF may have diverging

taxation principles. Benchmarks such as gross total return indices assume that dividends are

reinvested without any tax deductions, whereas the ETF will have to pay withholding taxes

when disbursing dividends. Net total return indices may assume that withholding taxes are

paid on dividends, whereas the ETF is able to reclaim its taxes partially. This practice, known as

dividend tax enhancement, may boosts ETF returns relative to the benchmark (Johnson et al.,

2013, p.6). An additional example of tax optimization is called dividend tax arbitrage. In this,

ETFs lend stocks that are subject to dividend withholding taxes to counterparties located in

more tax-efficient jurisdictions during dividend season (Bioy & Rose, 2013, p.6).

Taxes levied on an investor level are not subject to ETF performance measurement. In

consequence the taxation of investors is not discussed in this thesis.

2.5 Extra Revenue – Securities Lending

Apart from the revenues generated trough the rise in value of the underlying constituents, an

ETF can generate additional revenue from securities lending. Securities lending refers to

additional revenue trough the transfer of securities from the ETF to a third party, who will

provide collateral to the lender and pay a fee. The extra revenue can be used to partially offset

the internal costs the ETF. It even can lead to an over performance of the ETF with respect to

the benchmark, which does not exert securities lending (Picard & Braun, 2010, p.68). However,

since lending activities can be executed in direct agreements between the lender and the

borrower, true magnitude is difficult to assess (Bioy & Rose, 2013, p.3). In Europe, the UCITS

Chapter 2 Exchange Traded Funds

11

regulation requires all revenues, net of direct and indirect operational costs, to be returned to

the ETF (ESMA, 2012a, p.7).

Securities lending may be undertaken in physical as well as synthetic replicating ETFs. As the

lending in physically replication ETFs is more straightforward, securities lending possibilities for

synthetic ETFs are more complex. Physically lending the securities inherits the risk that the

borrower of the security becomes insolvent and is unable to return the loaned securities.

Therefore physical ETFs engaged in lending expose investors to counter party risk.

In synthetic ETFs, the lending process takes place within the reference basket and thus does

expose the investor to counterparty risk. (iShares, 2014, p.49). Securities lending is an

important factor in total return assessment of an ETF and has to be kept in mind when

evaluating the tracking performance of an ETF.

2.6 Indices

Even though ETFs are found to replicate a variety of benchmarks, this thesis is confined to ETFs

replicating equity indexes only. Picard and Braun (2010, p.33) define an index as a statistical

figure, representing a basket of financial assets, which can only be bought by investors through

the use of ETFs or index-certificates.

The underlying assumptions of the index thereby have an important impact on the relative

performance of the ETF. In this context, the indexes’ most relevant feature is their dividend

reinvestment assumption. Divergent assumption on the dividend treatment of ETF and index

result in tracking dissimilarity. In general, price and total return indices are differentiated. Price

indices only return the prices of the underlying assets whilst assuming that all dividends of the

constituents are distributed. Total return indices on the other hand assume that all dividends,

interest payments and other income are reinvested (Picard & Braun, 2010, p.36). They can be

further separated according to their assumption on taxation on the dividends reinvested. A net

total return index assumes that dividends are taxed at the biggest available rate, whereas

gross total return indexes assume that no taxes are levied on the reinvested dividends (iShares

2014, p.22). These assumptions are particularly important as they results in performance

differences of the ETF and the index whenever dividends are paid or reinvested (Hassine &

Roncalli, 2013).

The timing of dividend reinvestment can lead to further performance differences between ETF

and its benchmark. Whereas many indices assume dividends to be disbursed at ex-dividend

dates of the corresponding constituents, the dividend payouts by ETFs are often cumulatively

administered (Picard & Braun 2010, p.24).

Chapter 2 Exchange Traded Funds

12

From the time series of the SMI price index and the DB X-TRACKERS SMI UCITS ETF in Figure 5,

it can for instance be seen that the ETFs dividend payment on July 25th, 2013 results in an

instant drop of NAV compared to the NAV of the benchmark. By the end of March 2014

however, the NAV of the ETF and the benchmark return to similar values, as the SMI price

index distributes dividends throughout the investment horizon.

Figure 5: Dividend Distribution

The development of the NAV of the SMI price index and the DB X-TRACKERS SMI UCITS ETF are illustrated. The period covers May 2013 to May 2014. The red circle indicates the period of the dividend payment of the ETF. (Source: Own calculations/ illustrations)

2.7 Market Environment

Due to its size, distinctive structure and easy accessibility, the ETF market consists of various

types of participants. In the following, the most relevant, market participants and market

characteristics are presented.

2.7.1 Providers

The ETF provider is in charge of all defining aspects of an ETF such as the replication strategy,

pricing and dividends attribution. Therefore, he is the main responsible for the ETF

performance (Picard & Braun 2010, p.29).

Following a recent statistic by Deutsche Bank (2014, p.37), by the end of 2013, a total of 180

ETF providers existed across the globe. However, 85.8% of the ETF industries total assets were

concentrated amongst the top 10 providers only. Blackrock, the mother company of iShares, is

the largest ETP provider with 40.3% of total market share, followed by State Street GA (17%)

and Vanguard (15.1%). Holding a total of 72.4% of the global ETF market in 2013, those three

big players provide nine of the ten biggest ETFs by AuM.

Deutsche Bank AG (2.3%) is the biggest provider located in Europe, whereas UBS, the biggest

Swiss provider, holds USD 16 billion AuM (0.7%). The ETF market is mainly dominated by banks

7000

7200

7400

7600

7800

8000

8200

8400

8600

8800

9000

SMI

ETF SMI

Chapter 2 Exchange Traded Funds

13

and bank-owned providers such as Deutsche Bank, Lyxor of Société Général, UBS and Zürcher

Kantonalbank (Deutsche Bank, 2014, p.41). In Switzerland iShares covers 53.36% of the Swiss

ETF market by the end of 2013. Out of a total of 18 ETF providers, the five biggest providers

including UBS (19.3%), Zürcher Kantonalbank (6.4%), Lyxor (6.25%) and db x-trackers (6%)

covered 97.5% of the ETF market (SIX, 2013a, p.3).

2.7.2 Authorized Participants

Authorized participants (AP), also referred to as Market Makers, govern the ETFs creation-

redemption process in which ETF shares are issued or redeemed. Typically being large

investment banks or brokerage businesses, APs conclude participation agreements with the

ETF, which allow the AP to subscribe and redeem units of the ETF on an in-kind basis. APs may

act as distributors of the ETF shares on various stock exchanges as well (Hehn, 2006, p.96). The

process in its details will be explained in chapter 2.7.3.

On the Swiss exchange platform SIX, at least one AP is employed for each ETF. APs are obliged

provide continuous liquidity in the ETF (Picard & Braun, 2010, p.30). APs have to provide bid

and ask prices for a fixed minimum of trading volume and have to avoid prices, which exceed a

maximum bid-ask spread of 5% in the case of an inexistent Over-the-Counter (OTC)2 market or

2% where a functioning OTC market exists (SIX, 2014).

As the spread is going to be integral part of the performance analysis, it’s important to

understand the role of APs in the ETF market. By providing liquidity through their so-called

Limit Order Books (LOB) 3, APs have an important influence on the prices that need to be paid

when trading an ETF. According to Roncalli and Zheng (2014), during a trading day, all selling

and buying orders are matched against the best order of their counterpart. If the volume of

the market order is larger than the quantity available at the corresponding best limit order, the

best limit price will be adapted and executed on the second limit order. Therefore the spread

between the best bid and the best ask price increases with the ETF notional traded (Roncalli &

Zheng, 2014).

2.7.3 Creation- Redemption Process

The creation- redemption process of ETF shares is administered through several steps.

At the beginning of the trading day, the portfolio manager of the ETF designates the APs with

the basket of securities to be taken into the fund at the closing of the market in exchange for

new units of the ETF. The AP will buy the corresponding basket of securities on the capital

2 OTC trades are administered on the primary market directly between the AP and the ETF. The final price for the ETF share is negotiated directly between the two counterparties. 3 LOB is the set of all active trading order of buyers and sellers of ETFs listed on any electronic system (Gould et al., 2013).

Chapter 2 Exchange Traded Funds

14

markets. The AP exchanges this basket against the equivalent amount of ETF-shares, which he

now is able to sell on the secondary market or OTC (Picard & Braun, 2010, p.63-65). This

process eliminates transaction fees and avoids tax events borne by the ETF, as the ETF does

generally not need to buy and sell component securities directly (Hehn, 2006, p.96). The main

benefit of the creation-redemption process is that it causes the market price of an ETF to

remain closely linked to its NAV, despite being priced continuously (Charupat & Miu, 2011,

p.968). If the price of the ETF moves sufficiently far outside the bid and ask band of the

underlying basket of securities, an arbitrage opportunity arises. If for example the price of the

ETF is sufficiently below the price of the underlying basket, the AP takes advantage of this

opportunity by buying ETF shares and selling the basket of securities short. At the end of the

day the AP uses the ETF shares to receive the underlying basket of securities and employ those

to cover the short position previously entered. By doing so, the AP receives the difference

between the two prices. The AP exploits the arbitrage opportunity until the price difference

between ETF and the underlying basket erode. As a consequence, the ETF is traded within the

bid-ask-spread of the underlying basket in normal market conditions. Figure 6 gives an

overview on how the primary and secondary markets are interlinked and how the creation-

redemption process is administered through the AP.

Figure 6: Creation - Redemption Process

The process of creating and redeeming ETF shares is depicted. The AP administers the process and acts as an intermediary of the capital markets, the ETF management and the Investors. Institutional investors can trade directly with the AP, on the primary as well as on the secondary market. Retail investors generally are only able to trade on exchange. (Source: Own Illustration following Hehn, 2006, p.123)

Institutional

Investor

Retail

Investor

Au

tho

rize

d P

arti

cip

ant

Capital

markets:

Stocks, ETFs,

Futures etc.

ETF / Fund manager

Cash

ETFs

ETFs

Securitie

s Secu

riti

es

ETFs

Redemption

Subscription

Cash

Securiti

OTC trading

Secondary Market Primary Market

Bro

kers

/ B

anks

Exch

ange

Cash

ETFs

Chapter 2 Exchange Traded Funds

15

2.7.4 Investors and Trading Strategies

Retail as well as institutional investors gained interest in ETFs as they use ETFs as an effective

mean of asset allocation by combining investments throughout different markets and asset

classes. Pension funds, insurance companies, foundations and other corporates typically use

ETFs in order to track selected markets precisely and transparently. As indicated in Figure 6,

institutional investors furthermore have the possibility to acquire ETF directly on the primary

market through OTC transactions. By trading OTC at the NAV of the ETF, an investor can get

ETF units created or redeemed at a premium only, without paying the bid-ask spread. The

investor however bears the risk that the constituents of the ETF might lose in value by the

official close of trading (Picard et al., 2014, p.16).

ETFs can be used as building blocks in a variety of strategies such as in core-satellite portfolios.

Hereby, ETFs are suitable for the core portfolio, which tries to achieve the broadest possible

diversification across the various asset classes. In the satellite portfolio the ETFs can be used to

build up diversified satellite positions in emerging markets, specific sectors or alternative asset

classes (Picard et al., 2014, p.10). ETFs can furthermore be used as a hedging tool against

declining markets, as they either can be sold short or short-ETFs can be bought (Picard &

Braun, 2010, p.11). Similar to the derivatives used to equitize cash, ETFs can be used to

manage short or medium-term cash holdings.

The variety of trading strategies indicates that investors may have completely heterogonous

interest in ETFs. The span reaches from buy-and-hold investors, who profit from a ETFs low

fees, tax efficiency and broad diversification, to a frequent trader who benefits from the low

volatility of ETFs compared to individual equities (Wiandt & McClatchy, 2001, p.98).

Having discussed the ETFs history, replication strategies, costs, revenues and market

environment, the following chapter will focus on the most prominent ETF performance

metrics. Both tracking and liquidity measures are considered.

Chapter 3 ETF Risk Metrics

16

Chapter 3 ETF Risk Metrics

As indicated in the preceding chapters, ETFs combine many advantageous features such as

security, good transparence, permanent pricing and trading, diversification as well as dividend

participation for relatively low costs. However, ETFs do also bear risks. In fact, many of the

existing statistical performance measures of ETFs are in fact risk figures due to the fact that

ETFs do not aim to outperform, but replicate a benchmark as closely as possible (Hassine &

Roncalli, 2013). This section hence provides the mathematical framework of key ETF risk

figures and reviews their sources. The most common metrics are the tracking difference

(subchapter 3.2), tracking error (subchapter 3.2), liquidity measures (subchapter 3.3) and the

pricing efficiency (subchapter 0). Besides pricing efficiency, those risk factors jointly depict the

building blocks for the efficiency measure derived in this thesis.

3.1 Delimitation

Much of the literature considered does not clearly distinguish tracking efficiency from pricing

efficiency. The term tracking efficiency refers to how closely the NAV of an ETF corresponds to

the NAV of the benchmark, whereas pricing efficiency measures how closely the price of the

ETF follows the NAV of the ETF. Figure 7 presents the difference between pricing and tracking

efficiency.

Figure 7: Tracking and Pricing Efficiency

The difference of pricing efficiency, measuring the equality of the ETFs price and NAV, and the tracking efficiency, measuring the equality of the ETFs NAV and benchmarks NAV are illustrated. (Source: Own illustration following Charupat & Miu, 2011)

By analyzing daily or even intraday data, pricing efficiency is concerned about the prevalence

of market inefficiencies such as failures in the creation-redemption process and its underlying

arbitrage mechanisms. However, resulting premiums or discounts over the NAV are not

expected to persist over the long run and are likely to lie within transaction costs (Charupat &

Miu, 2011). While tracking difference may be accounted to the ETF management, pricing

deviations are more likely to be market inefficiencies caused by the AP and therefore need to

be distinguished strictly.

Pricing Efficiency Tracking Efficiency

Price ETF NAV ETF NAV

Benchmark

Chapter 3 ETF Risk Metrics

17

3.2 Tracking Efficiency: Tracking Difference and Tracking Error 4

The ESMA Guidelines on ETFs and other UCITS defines Tracking Difference (TD) as the total

return difference of the annual return of the ETF and the annual return of the tracked

benchmark. Tracking Error (TE) is defined as the average daily volatility of the difference

between the return of the ETF and the return of the tracked benchmark (ESMA, 2012, p.4).

Both backward-looking coefficients measure the quality of benchmark tracking, whereas the

closer their values are to zero, the better is the tracking. There exist several methodologies to

calculate TE, whereas the calculation of TD is generally consistent across studies. To begin

with, Subchapter 3.2.2 provides the most prominent calculation method of TE following Pope

and Yadav (1994). In a later chapter, additional methods to compute TE are presented.

Calculating both the TD and TE requires the calculation of ETF and benchmark returns. The

mathematical formulas applied in the herein thesis are illustrated below, where and

denote the NAV of the ETF and of the benchmark at the time respectively. The returns

of the ETF and of the benchmark compute as indicated below.

(1)

(2)

3.2.1 Tracking Difference

The difference in ETF and benchmark returns, denoted by in formula (3) is calculated

according to Pope and Yadav (1994). The vector of weights of the ETF and the benchmarks

constituents are denoted with and respectively, whereby it is assumed that the number

of ETF and benchmark constituents is the same for the funds considered in this thesis.

(3)

4 Tracking Error is labeled differently in academic literature. Pope and Yadav (1994) as well as Frino and Gallagher (2001) define TE as the standard deviation of the difference between ETF returns and benchmark returns. Roll (1992) as well as Hassine and Roncalli (2013) define TE as the difference in portfolio and benchmark returns. In the herein thesis, the term TD will be used to describe the difference in returns, whereas TE refers to the standard deviation of the return differences.

Chapter 3 ETF Risk Metrics

18

The annual TD in returns computes as the return difference of ETF and the benchmark over the

time period of one year. The expression in the below formula denotes the vector of expected

return differences

| (4)

3.2.2 Tracking Error - Based on the Standard Deviation

The most widely used methodology used in the ETF industry is based on the day-to-day

variability of the difference in returns between a fund and its benchmark (Frino & Gallagher,

2001; Pope & Yadav, 1994). The TE | is calculated as the standard deviation of the

difference in daily returns as indicated below. The term hereby denotes the covariance

matrix of asset returns.

| √ (5)

Pope and Yadav (1994) indicate an estimation bias arising from the usage of the above formula

with daily or weekly data, inflating the TE measured. The issue can be resolved by either using

monthly data (Pope & Yadav, 1994) or make use of the correction based on the Lo and

MacKindlay (1988) analysis. iShares (2014, p.27) suggest the usage of at least 30 observation

points in order to receive a significant TE coefficient. In consequence the calculation of TE

based on monthly data requires a track record of at least two and a half years. As this trading

horizon may not reflect the average holding period of an ETF, this paper calculates TE on a

daily basis, as the average over one trading year.

3.2.3 Sources of Tracking Difference and Tracking Error

In order to get a sense for what may cause TD and TE, the sources ETF and benchmark return

differences are discussed in the following. Figure 8 lists the causes of TD and TE for both

physically and synthetically replicating ETF. The illustration additionally indicates the direction

of impact of the various factors. Whereas it can be seen from formula (3) and (4) that TD can

take both positive and negative values, TE, by squaring the return differences, only takes

positive values. A positive TD is desirable as it indicates an outperformance of the ETF over the

benchmark, whereas a high TE indicates many deviations in the returns. Thus Figure 8

allocates the direction negative to all factors increasing TE, whereas the classification negative

(positive) indicates a resulting excess performance of the benchmark (ETF).

Chapter 3 ETF Risk Metrics

19

Figure 8: Sources of Tracking Error and Tracking Difference

The causes of TD and TE for both physical and synthetic ETFs are depicted, indicating the direction of their impact. Negative impact indicates that the TD and TE increase. No influence* for synthetic ETFs indicates that the impact may be compensated indirectly through the swap price quoted by the swap counterparty. (Source: Own illustration following Johnson et al., 2013)

The illustration indicates an unambiguous relationship between the method how an ETF

replicates his benchmark and the quantity of potential TD and TE sources. Continuous factors

such as the daily deduction of the TER influence TD, but do generally not inflate TE. Non-

recurring and impermanent sources as for instance transaction and rebalancing costs, taxes

and diverging dividend reinvestment assumptions may influence both measures.

Many of the factors listed and their direction of impact on tracking have been discussed in the

previous chapters and thus will not be discussed again. An additional source of tracking

deviation comes from different cash holdings due to time lags during index composition

changes, where the ETF is forced to hold returns from cancelled constituents in cash (Johnson

et al., 2013, p.5). Another reason is that the ETF daily deducts a fraction of the annual

management fee. This will result in the fund holding smaller amounts of cash until payout.

Finally cash drag can arise from the lag between dividend or coupon payments by the index

constituents and the distribution of dividends to the ETF investors. Cash drag influences TE

negatively in up- and positively in down markets (Picard & Braun, 2010, pp. 22 - 23).

Cause

TER

Transaction and Rebalancing Costs

Dividend reinv. assumption

Taxation

Securities Lending

Swap Spread

Sampling method

Cash Drag

Tracking Difference

physical ETFs

Negative

Negative

Negative / Positive

Negative / Positive

Positive

No Influence

Negative / Positive

Negative / Positive

Tracking Difference

Synthetic ETFs

Negative

No influence*

No influence*

No influence*

No influence*

Negative / Positive

No influence*

No influence*

Tracking Error

physical ETFs

No Influence

Negative

Negative

Negative

Negative

No Influence

Negative

Negative

Tracking Error

Synthetic ETFs

No Influence

No influence*

No influence*

No influence*

No influence

Negative

No influence*

No influence*

Chapter 3 ETF Risk Metrics

20

3.3 Liquidity Metrics

Not only do the ETF constituents and their sizes have an important impact on an ETFs liquidity,

but it is likewise important to look at the property of the platforms on which the ETFs are

traded and the functioning of the underlying arbitrage mechanism. In the following, common

liquidity metrics and their applicability in the context of efficiency measurement are discussed.

Firstly, it is important to distinguish the absolute and the relative liquidity of ETFs (Roncalli &

Zheng, 2014).

Depending on the investment horizon of an investor, liquidity becomes a key criterion. The

investment of the investor determines whether to invest in a liquid or illiquid asset. A short

investment horizon may require an asset to be regularly traded at no or little discount,

whereas a long-time investor may benefit from higher returns by investing in illiquid assets

(Amihud & Mendelson, 1991). In addition, liquidity is important for risk-management purposes

in order to react quickly to changing market situations (Picard & Braun, 2010, p.9).

The subscription and redemption of ETF shares may become at risk in times of financial

distress. Recent events such as the downgrading of Greece to a non-investment grade, as well

as the earthquake in Japan in 2011 showed that ETF benchmarked to the corresponding

indices became difficult to trade (Hassine & Roncalli, 2013). Finally the liquidity of an ETF may

indicate the liquidity cost at which the ETF is traded.

3.3.1 Delimitation: Relative versus Absolute Liquidity

Relative liquidity refers to a comparison of both the ETFs and the underlying indexes liquidity.

As the liquidity of the index may be crucial when deciding for a benchmark, relative liquidity is

not relevant for intra-provider comparison as the benchmarks’ liquidity is same for all ETFs and

providers. Absolute liquidity on the other hand refers to the liquidity of the ETF himself and

does not relate to the liquidity of the underlying benchmark (Roncalli & Zheng, 2014). As

absolute liquidity is relevant in the context of this study, a selection of absolute liquidity

measures are presented.

In practice, there exist a range of measures to approximate the absolute liquidity of a fund,

however not all are appropriate when it comes to measuring the liquidity of an ETF. Why some

traditional liquidity metrics such as the AuM and the trading volume may be misleading in the

context of ETFs is explained subsequently. In order to design a comprehensive measure in

combination with TE and TD, the liquidity measure should furthermore allow for precise

scaling of ETF liquidity cost. The bid-ask spread and market impact costs are hereby found to

be the most relevant.

Chapter 3 ETF Risk Metrics

21

3.3.2 AuM and Trading Volume

The simplest approach to approximate the liquidity of an ETF is to look at total AuM.

Comparing the proportion of trades in the ETF allows to a certain extend to approximate how

liquid and costly trading the ETF is. Practitioners however argue, that the fund size and trading

volume allow little inference on the true liquidity of an ETF, as it is the constituent’s tradability

and their availability on the exchange that determines the liquidity of an ETF (iShares, 2013,

p.34; Justice & Rawson, 2012, p.4). Especially for ETFs, it is advisable to apply those two

measures with caution. As previously mentioned, the so-called on-screen activity coming from

trades on the secondary market which is measured and published by the exchange platforms

may only be a fraction of what is actually traded in the ETF due to OTC trades on the primary

market. Calamia, Devilla and Riva (2013) and iShares (2013, p.45) indicate that significant

portions of the ETF turnover is traded on the primary market. As those trades are not

consistently reported, overall ETF liquidity measurement with trading volume and AuM may be

misleading and are therefore not used to draw inference about the ETFs liquidity in this thesis.

3.3.3 Bid-Ask Spread

It is important to understand, that depending on whether a trade is executed on the primary

or secondary market, different liquidity costs arise. OTC trading orders can be entered at a

fixing with no bid-ask spread, whereas the price is at the discretion of the AP and the investor.

Such orders are generally handled at the NAV, meaning on the closing price of the benchmark

index plus a fee negotiated with the AP. While these fees certainly depend on the taxes, the

hedging costs as well as any operational costs of the AP, it certainly may also depend on the

negotiation power the investors.

The bid-ask spread to be paid on the secondary market is calculated throughout the day and is

generally not negotiable. Amundi (2011) stated, that the bid-ask spread for buying the ETF

MSCI World for the year 2010 on NYSE Euronext was 0.20%, whereas set-up and redemption

fees at the NAV were only 0.045%. Figure 9 lists again some of the most common factors which

influence the size of the bid-ask spread.

Chapter 3 ETF Risk Metrics

22

Figure 9: Impact Factors on Bid-Ask Spread

The factors influencing the bid-ask spread are illustrated. They include the costs of buying/- selling the securities, taxes levied, foreign exchange and hedging costs, the costs of holding the ETF shares and the margin of the AP. Larger trading volume and AuM furthermore are expected to have an impact on the size of the bid-ask spread. (Source: Own illustration following Amundi, 2011; Amihud & Mendelson, 1991)

From a mathematical point of view, the bid-ask spread is calculated as the difference of the bid

price and the ask price

In order to incorporate the bid-ask spread into the design of

an efficiency measurement, the relative bid-ask spread has to be calculated. This spread

measures the percentage difference in prices. Following the suggestions by Hassine and

Roncalli (2013), the relative bid-ask-spread | is calculated as the difference between the

quoted bid price and the quoted ask price

divided by their mid-price :

|

(6)

The mid-price is thereby defined as the average of both prices.

(7)

Formula (6) indicates the costs of a full market cycle, meaning purchasing an ETF share for the