PERFORMANCE BASED CONTRACTING AS SEEN … · PERFORMANCE BASED CONTRACTING AS SEEN FROM ... •...

31

PERFORMANCE BASED CONTRACTING AS SEEN FROM THE LSP’S PERSPECTIVE PUBLIC ESCF Workshop Eindhoven, 11 June 2014

Transcript of PERFORMANCE BASED CONTRACTING AS SEEN … · PERFORMANCE BASED CONTRACTING AS SEEN FROM ... •...

PUBLIC

PERFORMANCE BASED CONTRACTING AS SEEN FROM THE LSP’S PERSPECTIVE

PUBLIC

ESCF WorkshopEindhoven, 11 June 2014

PUBLIC

2

1 DHL Introduction

2 DHL Value propositions – Contract types

3 Case study

Agenda

PUBLIC

3

DHL at a Glance – “A Test”

1. Do you know the mother company of DHL

2. What size is the company

3. What are the main services offered by DHL

4. DHL is market leader in contract logistics, what is the market share

PUBLIC

4

DHL Supply Chain is part of the DPDHL group with a global network and an extensive logistics portfolio

GLOBAL FORWARDING & FREIGHT

Employees: ~ 475,000/Revenue: EUR 55.5bn1)

Employees: ~ 285,000/Revenue: EUR 42.8bn

The logistics company for the world

Employees: ~ 175,000/Revenue: EUR 13.9bn

The postal service for Germany

SUPPLY CHAINEXPRESS

Contract Logistics & Business Process Outsourcing

InternationalExpress

Air and Ocean Freight

RoadFreight

PUBLIC

5

DHL at a Glance

DHL Revenues: 42.8 bn€(2012)

DHL’s customer base includes 50% of Forbes

top 500 companies

DHL hasa global presence within over 220 countries and territories

DHL employsapprox. 285,000 people

8.4 %~37%

2.3%European

MarketShare 2009

Global Market Leader

One of the world's leading courierand express service providers

World's largest

contract logistics service

provider

World'slargest airfreight forwarder

World'slargest ocean

freight forwarder (in both FCL & LCL1))

One of Europe's leading

road freight forwarders

Global Market Share 2008

Global MarketShare 2009

European International ExpressMarket Share 2009

1) Full-container load; Less-than-container load ; 2) All Market Share Data and revenue figures as per DP DHL Media Mail 2011

12.9%Global Market Share 20089.1%

PUBLIC

6

1 DHL Introduction

2 DHL Value propositions – Contract types

3 Case study

Agenda

PUBLIC

7

Varied Value Propositions to suit our Customers DemandsCustomer value propositions of LSPs beyond lower freight rates

Customer value proposition Key levers

4.

Lower lost sales/additional revenues • Increased delivery accuracy and quality• SC reconfiguration (e.g., postponement)• Inventory optimization

2.

Lower inventory carrying cost • Inventory optimization/stockholding location optimization• SC transparency• SC reconfiguration (e.g., postponement)• Warehousing process optimization • Customs process streamlining

3.

Lower obsolescence cost • Mode switch (e.g., move from OFR to AFR)• Direct transportation• Reduction of warehousing steps• Warehousing process optimization• SC reconfiguration (e.g., postponement)• Inventory optimization• Customs process streamlining

1.

Lower direct logistics cost (beyond lower rates) • Mode switch• Direct transportation• Reduction of warehousing legs, lean warehousing• SC reconfiguration (e.g., postponement)• Backhaul optimization

Direct logistics cost

Indirect logistics cost

5.

Reducing asset/resource intensity of shipper's business, variablising fix cost, reducing complexity for shipper

• Taking assets/resources of shipper's balance sheet/payroll, charging variable fee

• Reducing complexity for shipper

Operating resources/complexity

6.

Reducing shipper's SC risk • Reducing SC risk (e.g., through better transparency)• Transforming/carrying part of SC risk for which LSP is

better ownerSC risk

Trans-parency

Transparency on direct and indirect logistics cost as well as on current SC setup

7.

• Rapid SC mapping and analysis capabilities

Integrated SC optimization

Integrated optimization of direct and indirect logistics cost(also on global level)

8.

• Holistic analysis of SC setup options

PUBLIC

8

DHL can take on different roles in customers' supply chains, offering different value propositions

Value propositionPotential SC roles

The SC Manager – get management fees for serviceD

• Manage parts of customers' SC to improve efficiency and effectiveness(for longer period of time/ongoing)

Contract types used

The SCM consultant – get consulting fees for serviceC

• Consult customers to improve efficiency and effectiveness of their SC setup(project based)

• Consulting fee

The end-to-end SC solution provider – deliver an integrated/end-to-end service and bear cost and/or performance risk

F• Take over and guarantee service level

and cost reductions for parts of customer's SC

• Closed book/unit rates for integrated logistics services

The commodity service provider –get a big share of wallet for executional services

A/B• Provide high-quality executional

logistics services at a competitive price (e.g., FF, EXP business, warehousing)

• Unit rates for standard services (fix or quoted)

• Open book cost plus

The gain sharer – get part of the impact achievedE

• Take over and optimize parts of the SC • Open book gain share– Reward/penalty– Gain share– Value share

• Enhanced unit rates/closed book (value/gain sharing component)

• Commercial JV

Examples provided on next page

• Management fee

PUBLIC

9

Multiple Case Studies for Each Value Proposition (1/2)

The SC Manager – get management fees for serviceD

The gain sharer – get part of the impact achievedE

• Open book gain share

– Gain share • DESC Ford LLP contract– Redesign the inbound flow into 12 plants from 1,500 suppliers, including

return flows of packaging– Open book contract with shared savings; Each gain share was timebound

so that all of the saving would be retained by Ford after 3 years.

– Reward/penalty • DESC Reckitt Benckiser contract– Warehousing and value added activites (e.g., co-packing)– Open book with reward/penalty scheme based on service level; significant

proportion of management fee offered as incentive for ongoing improved service, no reward/penalty for average service

• E.g., Jaguar , Erricson , Unilever, Airbus– SCM related services (e.g., transport planning, customer service, control tower

management, material call off management, inventory management)– Compensation via open book plus management fee (esp. for transport related services)

or variabilized in service rate (esp. for warehousing related services, e.g., per order-line)

• Management fee

– Value share • DESC PDO contract– Managing movements of oil rig derricks for drilling– Compensation based on management fee plus value share based on

equipment uptime if outperformance of uptime targets

For reference only

PUBLIC

10

DHL has ample experience with advanced value propositions and suitable contract types (2/2)

• Commercial JV • DESC Goodyear SCM partnership– SC partnership including warehousing, transport management and value

added activities– DHL formed a JV with Goodyear and is rewarded with a share of the entire

value created through the SCM partnership

• Enhanced unit rates/closed book (value/gain sharing component)

• DESC Intel contract– AFR shipping of semiconductors from Hong Kong with additional end-to-

end service to reduce damages– AFR rates plus cargo packing charge based on improvement of damage

rate– Open book with reward/penalty scheme based on service level; significant

proportion of management fee offered as incentive for ongoing improved service, no reward/penalty for average service

The end-to-end SC solution provider – deliver an integrated/end-to-end service and bear cost and/or performance riskF

• DESC Sun SPL– E2E SC mgt for service logistics (call centre order management,

warehousing, transport management, forward inventory positioning , reverse logistics incl. parts screening, testing)

– Unit rate depending on service level (e.g., 2h, 24h, …) covering cost of all services

• Closed book/unit rates for integrated logistics services

For reference only

PUBLIC

11

DHL is not Risk Adverse! …but the returns have to be propotionateRisk type

Utilization risk

Shipper's business risk

Cost risk

Performance risk

Compensation logic risk

Description

Risk of underutilizing logistics infrastructure

Risk of customer's business, e.g., declining prices/margins

Risk of incurring higher cost than expected to achieve an agreed service level

Risk of not delivering the expected performance

Risk of overlooking a key determinant

• LSP best owner if assets can be utilized for other customers as well (portfolio effect)

• Shipper best owner if assets are dedicated/specific to customer

• Shipper best owner

• LSP in general best owner as higher expertise than shipper

• Shipper best owner for risk of fluctuation of inputs (e.g., fuel cost)

• LSP best owner for part under his control

• Shipper best owner for aspects beyond LSPs control (e.g., force majeure)

• To be minimized

Best ownership

LSP potential to take on risk not fully leveraged in most contracts today

For reference only

PUBLIC

12

There are suitable contract types for all value propositions,implying different levels of risk

* Beyond risk of losing contract/damaging other business ** Performance incentives as gain share on indirect cost savings

Source: DHL SCO team

Value propositionsSuitable contract types (not comprehensive)

Risk by exposure*Cost risk (e.g., overshooting cost in high-season)

Performance risk Utilization risk

If performance penalties agreed

Commodity service providerB

• Unit rates/closed book

• Open book cost plus

If performance penalties agreed

-

SCM consultantC

• Consulting fee

SC ManagerD

• Management fee If performance penalties agreed

-

Gain sharerE

• Open book gain share/JV with perfor-mance penalties

• Unit rates/closed book plus performance incentives/penalties**

Not realizing gains/incurring penalties

-

- -

End-to-end SC solution provider

F -Not realizing gains/incurring penalties

-• Closed book/unit rates for integrated

logistics services combined with strong bonus/malus system

PUBLIC

13

A careful assessment is required before taking risks on

Decide on viability of proposal

Assess …

Implement ability of scenarios

Stability of scenarios

Sustainability of scenarios

Determinepayout range of possible outcomes

• Determine im-plementation complexity/via-bility (consulting, logistics ser-vices) and (risk, scope complex-ity, innovative-ness, …)

• Sensitivities reg. contract parameters (e.g., cost for cost-plus)

• Sensitivities reg. scope parameters

• Shipper's per-spective – maxi-mize savings

• LSPs perspec-tive – achieve "good" margin

• Determine payout matrix of scope/con-tracting options

• How high (or low) can we get?

• Can we buildthe solutions?

• What if we change key parameters?

• Will the solution fall down a few months/years down the road?

Source: DHL SCO team

Due diligence can be extended to a 'honeymoon' open book period to gain a better understanding of customer situation and risks

PUBLIC

14

1 DHL Introduction

2 DHL Value propositions – Contract types

3 Case study

Agenda

PUBLIC

15

BAT – DHL Lead Logistics Provider case study

History Relationship Implementation

• What were the challenges?

• How did the relationship develop?

• How does the contract look like?

• Structure: 2 parties 1 team

• Benefits BAT

• How can we make sure the value is actually shared?

In 2010 DHL started a relation ship with BAT, in this case study we like to elaborate on the following

PUBLIC

16

Where have BAT come from?

A clear focus on optimisation..!

Full alignment with TM&D..!

Joking aside, in short, logistics had not been a major focus for the business and there was (and still is) significant scope to improve, integrate and optimise

how we plan and execute our network

Strong relationship with procurement..!

PUBLIC

17

How did Logistics WE BAT look like when we started?

All commodities from leaf to finished goods,

inbound & outbound

Total warehouse estate of over

220k sqm,

28,000+ primary movements per year,

covering 12.5 million km

Significant primary cost base linked to complex route to market supply

models

Core BAT Logistics team in partnership with DHL

LLP

75+ different freight carriers, multimodal -

sea, road, air

PUBLIC

18

What were BAT’s Key Business Challenges?

Key business challengesWhere BAT sees these challenges…

Plan Buy Make Move Service

1) Lack of supplier management

2) Commercial integration and understanding

3) Process standardisation and maturity

4) The cost we incur to deliver our service levels

5) Visibility of information and exception management

6) The degree and speed of change

BAT’s business suffered from some traditionally complex supply chain challenges – “we know the problems and that the solutions require an integrated approach”

Only 50% of inbound on time,

plus up to 21 days early (Plo)

2009 – Gross WMS write off’s of

£14m

No formal contracts or

performance SLA’s in place

GOM is only a framework – we have to operationalise processes, standards, governance & controls

5 different plan processes

20% vol x regional – GOM unclear

All manual processes

Demand decline outstrips capacity

reduction

Commercial relationships are

reactive, not responsive

Duplication of effort across

networks

Inefficient & manually intensive

processes

Running a mature thinking supply chain set up on manually intensive reporting & analysis

No real scenario plan capability

Manual status & order tracking

No EDI links for real time info

We are executing 18 regional transformation projects / Average time in G36 role (& below) is 18 months

Closure of manuf. sites

Average SKU life is 9 months

Forecast accuracy at 62%

Duplication & policing of data

No joint S&OP –clock speed is

different (2 month lag)

Separate networks between primary &

secondary

SKU schedule adherence < 50% over 3 wks (Bay)

PUBLIC

19

Solutions Framework

DHL - Lead Logistics Provider

CustomerSupply Chain Strategy

DESIGN MANAGE OPERATE

Supply Chain Transformation

World class systems and people to optimise your

supply chainDHL Managed 3rd Party Operations

Supply Chain Visibility

Freight Control Towers

Continuous Improvement across all layers

Presentation title | Location | xx Month 20xx

PUBLIC

20

Workshop questions

1. What type of contract would you go for?

2. What KPIs to include in contract?

3. Would you include penalties and/or incentives and if so how?

Break out in 3-4 groups

Presentation title | Location | xx Month 20xx

PUBLIC

21

Western Europe Control Tower – The Beginning

• BAT European SC Steering Committee 2003• Western Europe Control tower Implemented in 2006 (DHL)

o 5 factories• Establishment of routes and look to optimise and develop network savings

o Load Fillo Vehicle Reduction

• Transport planning via Ethos and manual spread sheets

• Lead Logistics Provider (LLP) for BAT in Western Europeo Local Services Agreement for WE

• Move from a Control Tower to a Transport Service Centre (TSC)• System led operation• Continuous improvement culture• Challenging BAT ways of working

PUBLIC

22

Expansion of LLP

Primary Transport

Solution Design

2010

Primary Transport

Solution Design

2011

Proc’ment

Factory Reviews

Primary Transport

Solution Design

2012

Proc’ment

Secondary

Contract Novation of 3PL

Contracts

WMs

Factory Reviews

Primary Transpo

rt

Solution Design

Proc’ment

Secondary

Contract Novation of 3PL Contract

s

Inventory Mgmt

WMs

Project Mgmt

Factory Reviews

Contract Mgmt and

Handling

Shared Proc’me

nt

Multi User

Control Tower

2013

PUBLIC

23

Our Solution - 2 partners 1 team

WE LLP

TLCM

Transport Service Centre

Carriers & Procureme

nt

Solution Design

BAT Finance

SC Developme

nt Mgr

WE Freight

Ops Mgr

PUBLIC

24

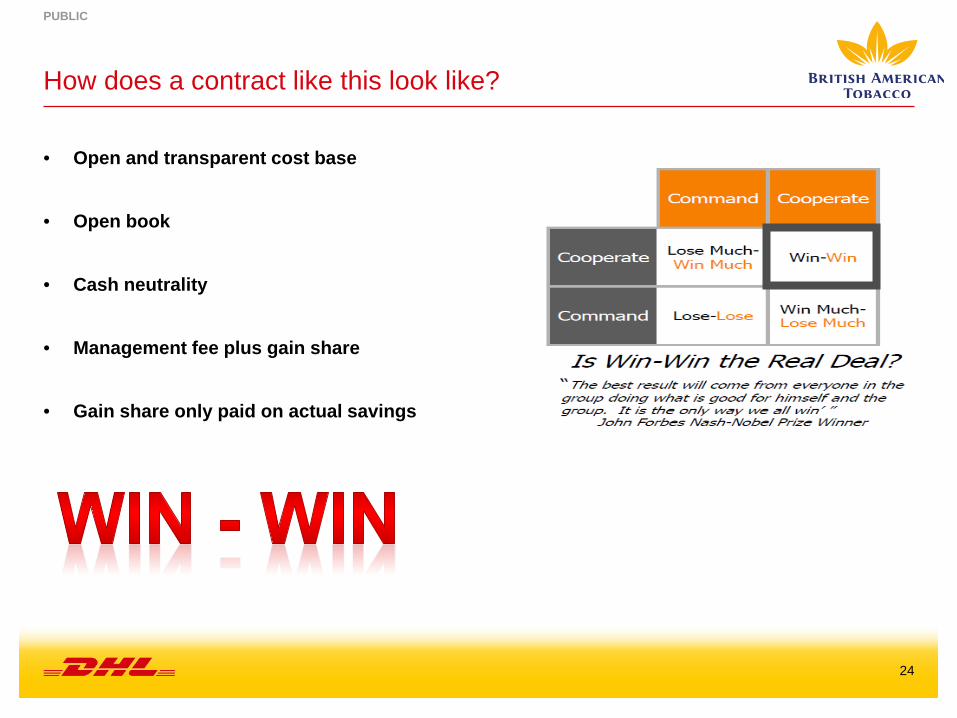

• Open and transparent cost base

• Open book

• Cash neutrality

• Management fee plus gain share

• Gain share only paid on actual savings

How does a contract like this look like?

PUBLIC

25

Benefits to Date for BAT

• 2010 – 2013 savings totalling +20% original baseline

• Increased V1 security carrier base equals 20% increase in transport capacity

• Average finished goods vehicle fill increase of +15%

o 7.35 million (2011) – 9.11 million (2013)

• Significant reduction in truck re-positioning

• Visibility and control across the supply chain

• One Standard Carrier Agreement for all suppliers

• ISO 9001 accreditation

• Short listed for CILT award 2013

PUBLIC

26

KPI Dashboard

050

100150200250300

Dec Jan Feb Mar Apr May

SlipSheet Loads Monthly Trend

0

10

20

30

40

50

Dec Jan Feb Mar Apr May

Loose Loads Monthly Trend

350

400

450

500

Dec Jan Feb Mar Apr May

Pallets Loads Monthly Trend • Full KPI suite available to direct operational focus and

continuously improve supply chain efficiency

• Information availability is providing the backbone of operational excellence and identifying project initiatives

KPI Highlights• Decreased Cost per Mille• Improved vehicle Fill despite optimum stretch• Increased OTIF deliveries• Reduced cost of poor quality due to improved and ingrained

process• Production volatility proactively used to plan fleet• Reduced re-positioning to zero for 3 consecutive months

Presentation title | Location | xx Month 20xx

PUBLIC

27

Pipeline to Profit

Blue Sky Meetings

Look

afte

r you

r Ide

a P

ool Customer’s own Tactics

DHL Development Team Meetings

Knowing the customer’s business

Personal experience & ideas

Customer non-Logistics Functions manufacturing, sales , planning, finance

Stealing with Pride !

STOPReasonsPoliticalPracticalFinancialToo Far Too FastHoldBack BurnerOther priorities‘Next Year’

Go !

Produce Charter 1

Customer Head of Function (HoF)Customer Logistics

DHL Head of LLP DHL Development GM

Support as needed

LLP

Charter 1

Monthly

Progressed thru Dragon’s Den

• Overview of idea• Success Criteria• Savings Estimate• Resource indication• External costs and time• Data Requirements

LSA Review Board

• Customer HoF• Customer Procurement• Customer Finance• DHL Global LLP • DHL Head of LLP• Support as needed

Go !

Produce Charter 2Presentation title | Location | xx Month 20xx

PUBLIC

28

Pipeline to profitComplete Analysis& Business CaseTimelineImplementation planCostsResourcesBenefitsMeasurement CriteriaBase LineGain Share

Programme members include LLP and Customer ownersof Operations, Finance & Development. Agree at eachstage of development.

DHL LLP own the process

LSA Review Board

• Customer HoF• Customer

Procurement• Customer Finance• Customer Country

Mgrs• DHL Global LLP • DHL Head of LLP• Programme Lead• Support as required

Go !

ImplementationDHL ExclusivityGainshare Approved

Track Results to Base Line

Track Results to BaselineImplementation to planCosts on targetResources in placeBenefits DeliveredGain Share Signed offGain Share Realised

Charter 2

Presentation title | Location | xx Month 20xx

PUBLIC

29

Summary

DHL as an LSP can offer different value propositions, taking different

roles in the supply chain and taking different types and levels of risk

each having their own type of contract.

The LLP model gives BAT access to world class supply chain

professionals with a flexible cost effective commercial model.

This has led to a true WIN-WIN relationship.

DHL has developed a methodology to be sure the value is accurately

recognized and shared.

Today DHL is led by our customers demand for services however

tomorrow we recognize our customers will look for more and more

partnership to shape future solutions together

“Performance based contracting as seen from the LSP’s perspective”

PUBLIC

PUBLIC

31

Jeroen MartensDirector of Network Design & Supply Chain ConsultingDHL Supply ChainBD EuropePhone +31 611 [email protected]

Contact