PE & VC Fundraising Report

14

2017 PE & VC Fundraising Report

Transcript of PE & VC Fundraising Report

2017

PE & VC Fundraising

Report

2 PITCHBOOK 2017 PE & VC FUNDRAISING REPORT

Credits & ContactPitchBook Data, Inc.

JOHN GABBERT Founder, CEO

ADLEY BOWDEN Vice President,

Market Development & Analysis

Content

KYLE STANFORD Analyst

DYLAN E. COX Analyst II

CAMERON STANFILL Analyst

REILLY HAMMOND Data Analyst

JENNIFER SAM Senior Graphic Designer

Contact PitchBook pitchbook.com

RESEARCH

EDITORIAL

SALES

COPYRIGHT © 2017 by PitchBook Data, Inc. All rights reserved. No part of this publication may be reproduced in any form or by any means—graphic, electronic, or mechanical, including photocopying, recording, taping, and information storage and retrieval systems—without the express written permission of PitchBook Data, Inc. Contents are based on information from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. Nothing herein should be construed as any past, current or future recommendation to buy or sell any security or an offer to sell, or a solicitation of an offer to buy any security. This material does not purport to contain all of the information that a prospective investor may wish to consider and is not to be relied upon as such or used in substitution for the exercise of independent judgment.

Introduction 3

PE Fundraising Overview 4-5

PE Fundraising by Size 6

PE Capital Overhang 7

VC Fundraising Overview 8-9

VC Fundraising by Size 10

First-time VC Funds 11

Venture Capital Overhang 12

Methodology 13

Contents

The PitchBook PlatformThe data in this report comes from the PitchBook Platform—our

data software for VC, PE and M&A. Contact [email protected]

to request a free trial.

3 PITCHBOOK 2017 PE & VC FUNDRAISING REPORT

A crowded market impendingIntroduction

Key takeaways

• Private equity firms are raising more capital than at any point since 2007. Funds

based in North America and Europe garnered $212.6 billion in commitments

from limited partners across 214 vehicles through August 1—on pace for a 24%

increase in value from the already stellar 2016.

• Venture capital fundraising hasn’t slowed down either. 2017 is on pace to be the

fourth consecutive year with more than $40 billion in VC commitments.

• 2017 has seen the largest PE and VC funds of all time close: Apollo Investment

Fund IX ($24.7 billion) and New Enterprise Associates 16 ($3.3 billion).

• We expect PE markets to be crowded in the years to come. Dry powder levels

in North American and European PE funds reached new heights of $738.7 billion

as of year-end 2016, exceeding the levels seen at the end of the last fundraising

cycle in 2007 and 2008.

Since year-end 2016, interest in the private markets has only intensified. PE and

VC firms continue to enjoy immense success on the fundraising trail, adding to

their already hefty stores of available capital. Neither asset class shows any signs

of slowing down, which could drive valuations higher, leaving dealmakers in a

precarious position.

We hope you find this report useful in your practice and feel free to reach out

with any comments or questions at [email protected].

Look up a company.

And its cap table.

And its investors.

And its EBITDA

multiples.

And its board

members.

In seconds.

The PitchBook Platform

has the data you need

to close your next deal.

Learn more at

pitchbook.com

DYLAN E. COX

Analyst II

4 PITCHBOOK 2017 PE & VC FUNDRAISING REPORT

PE fundraising still boomingPE fundraising overview

Commitments at post-recession high

PE firms are raising more capital than

at any point since 2007. Funds based

in North America and Europe garnered

$212.6 billion across 214 vehicles

through August 1—on pace for a 24%

increase in value from the already-

stellar 2016. Notably, that capital is

accumulating in the hands of fewer

fund managers, as successful repeat

funds have been able to dominate a

larger part of the market. The number

of individual vehicles has decreased

every year since 2014 and is on track

to do so again this year.

The main reasons for the exuberance

surrounding exposure to PE

include the asset class’s continued

outperformance of public markets,

unprecedented low yields on credit,

lackluster performance by other

alternatives such as hedge funds, and,

2017 on pace for new record?

PE fundraising activity

Source: PitchBook

*As of 8/1/2017

PE fundraising activity

$32

$22

$28

$23

$38

$47

$29

$37

$45

$39

$29

$40

$43

$93

$57

$91

$66

$93

$44

$65

$68

$52

$65

$76

$72

$81

$56

$85

$73

$89

$51

34

0

20

40

60

80

100

120

140

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q

2010 2011 2012 2013 2014 2015 2016 2017*

Capital Raised ($B) # of Funds Closed

$292

$376

$259

$176

$106

$150

$154

$283

$268

$261

$294

$213

476519

437

283 283317 317

414 427393 387

214

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017*

Capital Raised ($B) # of Funds Closed

Source: PitchBook

*As of 8/1/2017

5 PITCHBOOK 2017 PE & VC FUNDRAISING REPORT

PE funds (#) that hit target

finally, strong recent distributions to

LPs of PE funds, allowing those LPs

to recycle distributions back into the

asset class. These factors, in addition

to the fact that the number of publicly

traded firms in the US remains well

below its 1996 high, contribute to

an environment where capital is

incentivized to chase returns through

the private markets.

Prominent names top the list,

technology booming

Some of the biggest names in PE—

including Apollo, CVC, Silver Lake,

KKR, Vista, and Clayton, Dubilier &

Rice—have closed funds in the first

seven months of the year. The Apollo

Investment Fund IX raised $24.7 billion,

surpassing Blackstone’s 2007 vehicle

worth $21.7 billion to become the

largest buyout fund ever raised. Less

than two months earlier, CVC Capital

Partners closed their seventh flagship

buyout fund worth ¤16 billion ($17.95

billion), which set a record for largest

European buyout fund.

Silver Lake Management and Vista

Equity Partners closed technology-

focused funds totaling $15 billion and

Average & median PE fund size ($M)

$11 billion, respectively. Such closings

at ample sums exemplify the success

that general partners have had in the

IT sector, as well as LPs’ continued

interest in gaining exposure to the

industry outside of FANG-skewed

public stocks. About one-fifth of all PE

deals now involve tech companies.

Further signs of ease for IR teams

Not only are PE firms raising enormous

sums, but they seem to be doing

it more quickly and with more

consistency than they have in the past.

The average time to close for PE funds

in 2017 rests at just 13.2 months, down

from 15.9 months for 2016 funds and

the lowest figure recorded since 2006.

Further, 92% of all funds to close this

year have hit their stated target. Very

rarely do firms come back from the

fundraising trail without having met

their expectations.

PE funds’ closing time

$273.6$225.0

$208.0$162.9

$191.4

$217.0

$173.5 $174.0

$194.1 $200.0$288.0 $282.6

$738.6

$813.4

$663.0

$703.7

$422.8

$545.3

$540.5

$719.2

$646.4

$687.6$768.8

$1,007.6

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017*

Median ($M) Average ($M)

Source: PitchBook

*As of 8/1/2017

11.8 12.0 12.0

13.5

19.8

16.9

14.1 14.5 14.3 14.8 14.8

11.8

12.4

14.015.3 15.6

19.6 18.3

16.715.6

16.8 16.815.9

13.2

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017*

Median (Months) Average (Months)

Source: PitchBook

*As of 8/1/2017

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

*

Hit Target Missed TargetSource: PitchBook

*As of 8/1/2017

6 PITCHBOOK 2017 PE & VC FUNDRAISING REPORT

PE fundraising (#) by fund size

PE fundraising ($B) by fund size

Funds trend largerPE fundraising by size

Megafunds dominate capital

commitments

PE funds with at least $5 billion in

commitments have accounted for

nearly half (49.8%) of all capital

committed to the asset class this

year. The flurry of mega-buyout

funds is driven by a multitude of

factors. First, intense LP demand

has allowed successful GPs to

increase their target AUM. Second,

committing larger amounts of

capital across fewer funds allows

LPs to whittle down administrative

costs, streamline tracking

processes, and gain leverage

when it comes to negotiating for

co-investment rights. CalPERS is

even considering opening its own

direct investment arm, similar to

a plethora of Canadian LPs. Third,

soaring prices in both public and

private markets require that firms

raise more capital to compete

for the largest targets. For

consideration, the S&P 500 now

trades at a P/E ratio of around 24x,

compared to 14x in 2012, just prior

to the most recent buyout boom.

Middle market provides the most

opportunity

Though megafunds have dominated

the fundraising scene in terms

of dollars raised, middle-market

firms account for a larger portion

of final closes this year. There

have been 105 funds with between

$100 million and $500 million in

commitments that have closed

through August 1, representing

about 50% of all fund closes, the

highest since at least 2006. In

an ultracompetitive environment,

lower and core-middle-market

exposure provides a way to avoid

such rich valuations by targeting

companies that aren’t on the

traditional investment banking

circuits and thus not as likely to go

through an auction process.

0

50

100

150

200

250

300

350

400

450

2010 2011 2012 2013 2014 2015 2016 2017*

Under $100M $100M-$250M $250M-$500M

$500M-$1B

$1B-$5B

$5B+

Source: PitchBook

*As of 8/1/2017

$0

$50

$100

$150

$200

$250

$300

$350

2010 2011 2012 2013 2014 2015 2016 2017*

Under $100M

$100M-$250M

$250M-$500M

$500M-$1B

$1B-$5B

$5B+

Source: PitchBook

*As of 8/1/2017

7 PITCHBOOK 2017 PE & VC FUNDRAISING REPORT

Dry powder at record highPE capital overhang

2017 PE capital overhang ($B)

by vintage

Source: PitchBook

*Data pulled as of 7/10/2017

Note: The LP reporting cycle is two quarters behind the

most recent quarter ended. PitchBook’s most recent

fund returns data is through the end of 2016. 2017

numbers are from vehicles that have begun reporting.

Dry powder climbs to staggering

heights

Dry powder levels in North

American and European PE funds

reached new heights of $738.7

billion as of year-end 2016. The

packed coffers contain slightly

more than the $732.8 billion

that was available at year-end

2015 and also surpass capital

overhang levels at the end of the

last fundraising cycle in 2007 and

2008. The market is crowded, to

say the least.

Barring a severe economic

downturn, these sums will support

future deal flow, putting further

upward pressure on pricing

for buyout targets. Since more

of this capital continues to be

amassed in larger funds, which

necessitate larger minimum

equity deployments, we expect

the average size of PE deals to

continue growing. Late-cycle

vintages tend to underperform

their early-cycle peers, but that

certainly hasn’t deterred LPs from

committing to PE recently. We may

experience a future market where

expected PE returns are far lower

than historical norms.Source: PitchBook

Closing in on three-quarters of a trillion dollars available for deployment

PE capital overhang ($B) by year

$587.4

$700.4 $703.5$663.9

$611.5 $641.0 $618.2

$687.6$714.7 $732.8 $738.7

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

2017*

2016

2015

2014

2013

2012

2011

2010

2009

Cumula�ve overhang

Overhang by vintage

1%1%

2% 6%

12%

14%

26%

30%

8%

2009 2010 2011

2012 2013 2014

2015 2016 2017*

8 PITCHBOOK 2017 PE & VC FUNDRAISING REPORT

2017 set for $40B+?VC fundraising overview

VC fundraising activity

Unprecedented consecutive successes

VC fundraising activity

Venture fundraising in Europe and

North America is well on pace to

make 2017 the fourth consecutive

year with more than $40 billion raised

across all vehicles. Moreover, the tally

may approach last year’s record $51

billion figure when final numbers are

calculated. Through July, $27.5 billion

has been raised across 165 vehicles, a

number that will likely lead to a year-

over-year decrease in the number

of funds closed as LPs continue to

consolidate commitments across fewer

managers. That decline in number of

funds has been offset by some of the

largest funds we have ever seen. In

June, NEA raised the largest VC fund

ever—its $3.3 billion New Enterprise

Associates 16—and in Europe there

have already been two vehicles closed

this year on more than $750 million

(Rocket Internet Capital Partners SCS

and Atomico IV), only the second time

in the past decade that more than one

such fund has been closed in a single

year in Europe.

$42.

9

$43.

2

$42.

7

$17.

5

$28.

5

$33.

8

$31.

2

$29.

0

$42.

6

$44.

7

$51.

1

$27.

5

315 296

337

235

276 279309 316

363335

353

165

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017*

Capital Raised ($B) # of Funds Closed

$14

$5 $5 $5 $10

$10

$4 $10

$11

$6 $9 $5 $8 $7 $6 $8 $11

$12

$9 $10

$9 $15

$8 $13

$14

$17

$12

$9 $11

$14

$3

15

0

20

40

60

80

100

120

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q

2010 2011 2012 2013 2014 2015 2016 2017

Capital Raised ($B) # of Funds Closed

Source: PitchBook

*As of 8/1/2017

Source: PitchBook

*As of 8/1/2017

9 PITCHBOOK 2017 PE & VC FUNDRAISING REPORT

Record average VC fund size

VC fund size metrics

Convergence as industry trends larger

VC fund time to close

More and more targets continue to be hit

VC funds (#) that hit target

Moving into 2017, we expected to

see fundraising slow given that both

Europe and North America had just

experienced near-record fundraising

years. That hasn’t been the case,

however, as managers have continued

to raise outsized sums of capital.

Since 2012, the proportion of all funds

closed with less than $50 million in

commitments has declined from almost

60% to 34% this year. Conversely,

the proportion of vehicles raised with

between $100 million and $250 million

in commitments has increased from

just 15.2% to near 28% during that same

time period.

Cyclical effects come full circle

As the venture market has evolved,

so has the GP fundraising landscape.

Companies continue to raise larger

rounds and valuations have only

increased. While these trends have

partially been driven by the sheer

amount of capital raised since 2014

began ($166 billion), the effects they

have wrought have come full circle as

managers continue to raise massive

pools. To illustrate, the median fund

size has tripled from just $28 million in

2012 to $84 million as of 1H 2017.

We believe today’s fundraising levels

will underpin the current trends in VC

for the foreseeable future. Further,

as companies continue to raise larger

rounds, managers will continue to

adjust their fundraising strategies to

align well with the current dynamics of

the industry.

$64$70

$63

$33

$35 $35

$28

$35 $34$46

$65

$84

$161 $164

$139

$85

$116$135

$111

$101

$129$138

$153

$170

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017*

Median ($M) Average ($M)

Source: PitchBook

*As of 8/1/2017

14.2

10.9

12.9

15.6 19.5

10.7

13.514.9

12.413.1

19.4

15.9

19.1

13.0

16.3

14.1

20.9

15.915.7

18.1

14.8

16.1

20.3

15.7

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017*

Median (Months) Average (Months)

Source: PitchBook

*As of 8/1/2017

0%

20%

40%

60%

80%

100%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

*

Hit Target Missed TargetSource: PitchBook

*As of 8/1/2017

10 PITCHBOOK 2017 PE & VC FUNDRAISING REPORT

Upper & mid-market strongVC fundraising by size

Fund sizes in 2017 continued their

growth trajectory, increasing every

year since 2012. Much of this we

attribute to the upturn of deal sizes

in all stages. For that reason, GPs

needed to increase fundraising to

be able to maintain their strategy

and participate in follow-on rounds.

Logically, the number of funds

raising under $50 million has been

hit the hardest, sliding to the

category’s lowest percentage of

total funds in over a decade.

On the other end of the spectrum,

while there have only been two

funds of over $1 billion raised

through the first seven months of

2017, June saw NEA close a $3.3

billion vehicle—the largest VC

fund ever. Interestingly, the focus

of $1 billion+ funds has not been

solely on outsized late-stage deals.

Specifically, many recent mega-

funds have invested a meaningful

portion of their capital into seed

and early-stage deals, putting even

more pressure on small funds. For

traditional firms investing earlier

in the company lifecycle, their

strategies of deploying capital

might need to evolve to consider

the competition, or at minimum

the presence, of these mega-funds

creeping into the stage where they

typically invest.

Smaller funds sliding relative to the whole

VC fundraising (#) by fund size

VC fundraising ($B) by fund size

0

50

100

150

200

250

300

350

400

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017*

Under $50M $50M-$100M $100M-$250M

$250M-$500M $500M-$1B $1B+

Source: PitchBook

*As of 8/1/2017

$0

$10

$20

$30

$40

$50

$60

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017*

Under $50M $50M-$100M $100M-$250M

$250M-$500M $500M-$1B $1B+

Source: PitchBook

*As of 8/1/2017

11 PITCHBOOK 2017 PE & VC FUNDRAISING REPORT

First-timers set to break a record?

First-time VC fundraising activity

First-time funds2017 has been an especially strong

year for first-time fundraisers. The

amount raised in the first seven

months of the year exceeds full-

year totals for 2012 to 2014, and is

currently on pace to best 2008’s

record-breaking mark.

The spike in first-time fund closings

in 2016, which has continued into

this year, has been driven by a

very diverse set of geographies,

strategies and manager

backgrounds. Our data shows

that both 2016 and 2017 were

dominated by funds in California,

representing 41% and 52% of total

first-time funds, respectively. That

said, London saw the largest first-

time funds raised in both years.

Strangely, the diverse geographic

scope of these top funds doesn’t

stop there. Both were raised with

a focus on aiding businesses

expand into China, and both had

large Chinese backers like the

State-owned Assets Supervision

and Administration Commission

(SASAC) and ChinaEquity Group.

Although in general we saw

managers trend toward focused

funds, there was still a wide

variance in strategies. Obviously,

there were some centered around

currently popular strategies like

fintech, SaaS, biotech and artificial

intelligence. However, we also saw

funds raised to target startups

co-founded by designers, retail

technology and real estate tech.

$3.9

$3.8

$4.1

$1.7

$2.7

$3.1

$2.2

$2.1

$2.0

$2.8

$3.8

$2.6

61

48

49

39

50

31

35

28

42

29

32

25

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017*

Capital Raised ($B) # of Funds Closed

Source: PitchBook

*As of 8/1/2017

The managers of these first-time

funds also boast a wide range

of backgrounds. While there

were many who had served as

founders or partners at other

VC firms (Google Ventures, FTV

Capital, Andreessen Horowitz, etc.)

there were also a host of serial

entrepreneurs raising VC funds,

including co-founders of Palantir,

Cabify and Invitation Homes.

SELECT FIRST-TIME FUNDS

CLOSE DATE CAPITAL RAISED FOCUS

Cocoon Network Venture Capital Fund

1/19/2016 $721.5M UK & Europe

SILK Ventures Fund 5/16/2017 $500M China

Geodesic Capital Fund I 5/17/2016 $335M Japan

Pivotal bioVenture Partners Fund I

3/16/2017 $300MLife sciences & biotechnology

Centana Growth Partners 6/12/2017 $250M Fintech

Fifth Wall Ventures 5/1/2017 $212MReal estate technology

Section 32 Fund 1 5/16/2017 $151.3MLife sciences & biotechnology

Maniv Mobility Fund 7/26/2017 $42M Mobility

Campfire Capital Fund I 10/21/2016 $31MRetail technology

Source: PitchBook

*As of 8/1/2017

12 PITCHBOOK 2017 PE & VC FUNDRAISING REPORT

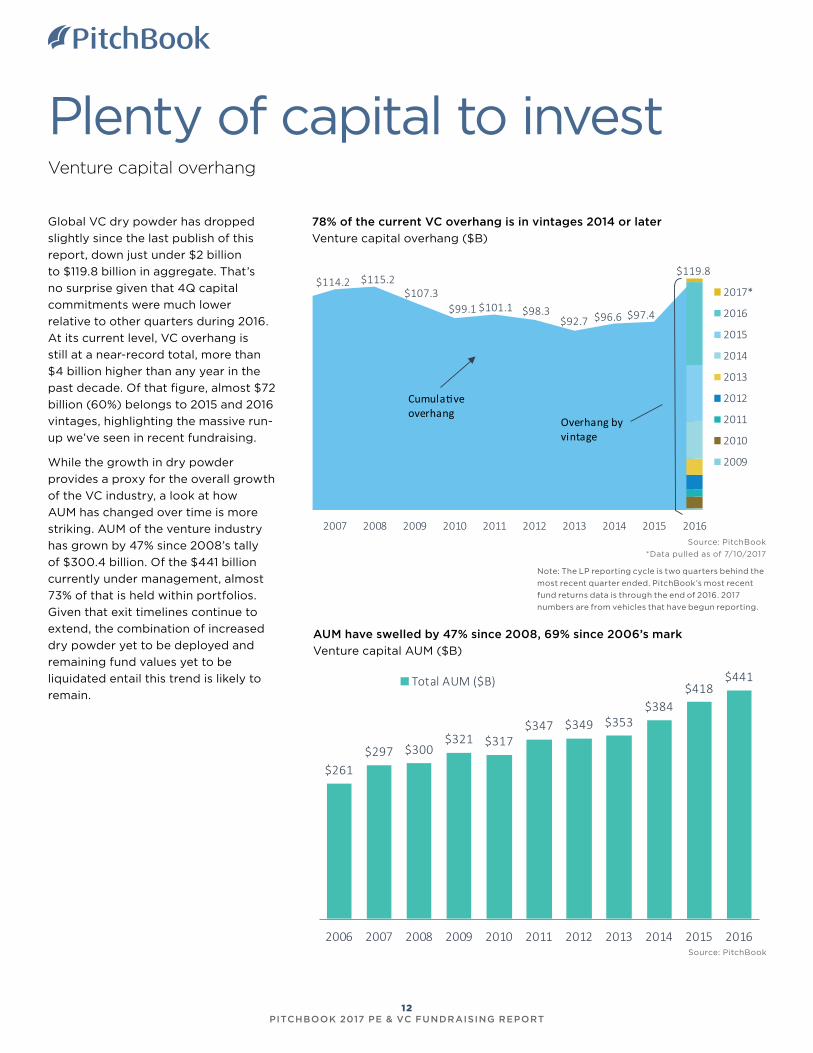

Plenty of capital to investVenture capital overhang

Global VC dry powder has dropped

slightly since the last publish of this

report, down just under $2 billion

to $119.8 billion in aggregate. That’s

no surprise given that 4Q capital

commitments were much lower

relative to other quarters during 2016.

At its current level, VC overhang is

still at a near-record total, more than

$4 billion higher than any year in the

past decade. Of that figure, almost $72

billion (60%) belongs to 2015 and 2016

vintages, highlighting the massive run-

up we’ve seen in recent fundraising.

While the growth in dry powder

provides a proxy for the overall growth

of the VC industry, a look at how

AUM has changed over time is more

striking. AUM of the venture industry

has grown by 47% since 2008’s tally

of $300.4 billion. Of the $441 billion

currently under management, almost

73% of that is held within portfolios.

Given that exit timelines continue to

extend, the combination of increased

dry powder yet to be deployed and

remaining fund values yet to be

liquidated entail this trend is likely to

remain.

78% of the current VC overhang is in vintages 2014 or later

Venture capital overhang ($B)

Note: The LP reporting cycle is two quarters behind the

most recent quarter ended. PitchBook’s most recent

fund returns data is through the end of 2016. 2017

numbers are from vehicles that have begun reporting.

Source: PitchBook

Source: PitchBook

*Data pulled as of 7/10/2017

$99.7$108.0

$114.2 $115.2$107.3

$99.1 $101.1 $98.3$92.7 $96.6 $97.4

$119.8

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

2017*

2016

2015

2014

2013

2012

2011

2010

2009

Cumula�ve overhang

Overhang by vintage

AUM have swelled by 47% since 2008, 69% since 2006’s mark

Venture capital AUM ($B)

$261$297 $300

$321 $317$347 $349 $353

$384$418

$441

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Total AUM ($B)

13 PITCHBOOK 2017 PE & VC FUNDRAISING REPORT

MethodologyPRIVATE EQUITY FUNDS

The following fund types are used in PitchBook’s PE fundraising data: buyout, PE growth/expansion, co-

investment, mezzanine, mezzanine captive, diversified PE, energy and restructuring/turnaround. This report

only includes funds based in North America or Europe that have held their final close. Note: for PE and VC

contributions versus capital raised, the contributions are the sums called down from limited partners by

general partners, compared to overall capital raised, in a given timeframe.

VENTURE CAPITAL FUNDS

In addition to traditional VC funds, PitchBook also includes corporate VC funds and seed-stage funds in our

VC fundraising total. Funds that identify themselves as growth-stage vehicles are classified as PE funds in

this report. Only funds based in North America or Europe that have held their final close are included in the

fundraising numbers.

CLOSE DATE AND VINTAGE

Unless otherwise noted, the fundraising data in this report is based on a fund’s close date. The vintage year

is based on the vintage year reported by the GP, otherwise the year in which a fund holds its final close or

the year of first investment is used.

CAPITAL OVERHANG

Calculated using the most recently available fund cash flow data, the capital overhang in this report is

updated through July 10, 2017. The capital overhang is based on vintage year and only capital that is held in

closed funds is considered. (It is important to note that evergreen funds are included). If a fund closed on

January 1, 2017 or later, it is only included in the dry powder figure if it previously held a first close and has

cash flow data available.

FUND LOCATION

A fund’s location is determined by the country or region where the majority of its investments have been or

will be made. Only funds based in North America or Europe are included in this report.

We do

The PitchBook Platform is the leading

web-based data software for limited partners

and other private market professionals.

custom fund benchmarks, cash flows,dry powder,valuations,GP co-investments.

You drive stronger portfolio returns.