Sub-recipient Monitoring and Management - BDO …NFE) as a sub-recipient includes when the NFE: 1....

27

BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms. Sub-recipient Monitoring and Management Eric Sobota, Partner, BDO USA, LLP Giacomo Apadula, Manager, BDO USA, LLP May 2014

Transcript of Sub-recipient Monitoring and Management - BDO …NFE) as a sub-recipient includes when the NFE: 1....

BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms.

Sub-recipient Monitoring and Management

Eric Sobota, Partner, BDO USA, LLP Giacomo Apadula, Manager, BDO USA, LLP

May 2014

Page 2

Agenda

Overview Sub-recipient & Contractor Determinations Sub-recipient Selection & Planning Sub-recipient Monitoring Activities Sub-recipient Monitoring - Performance and Cost

Recovery Strategies

BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms.

Overview

Page 4

Omni-Circular Overview Key dates

On December 26, 2013, the Office of Management and Budget (OMB) effectively consolidated and streamlined these administrative requirements for not-for-profit entities into what has been referred to as the “Omni-circular”

Federal agencies must submit draft implementing regulations to OMB by June 26, 2014

Full text of uniform requirements go in effect for non-federal entities on December 26, 2014

Page 5

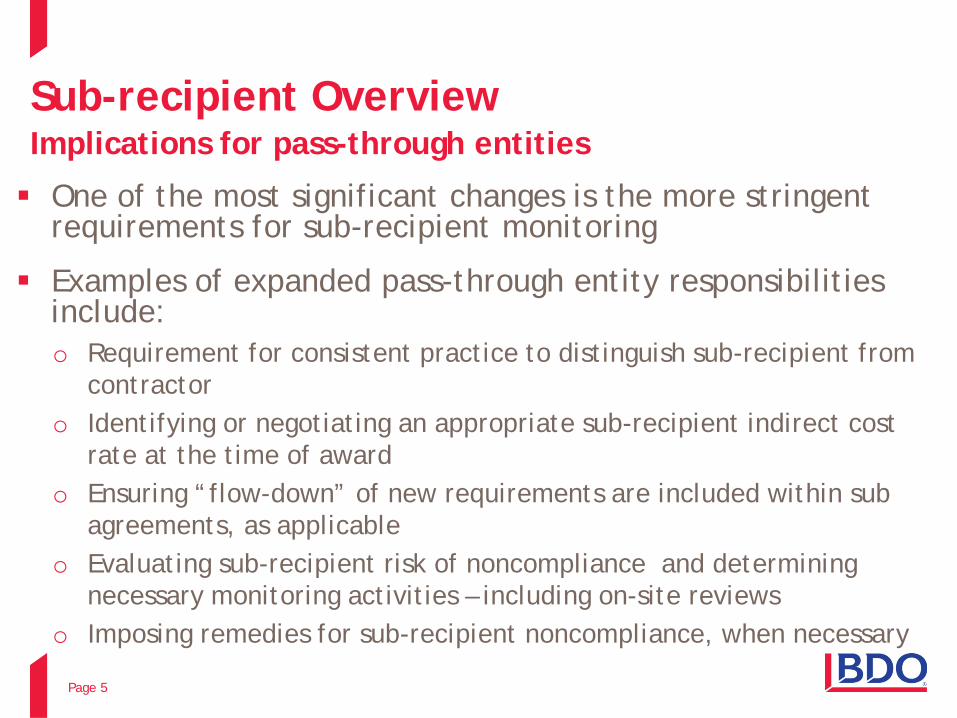

Sub-recipient Overview Implications for pass-through entities

One of the most significant changes is the more stringent requirements for sub-recipient monitoring

Examples of expanded pass-through entity responsibilities include: o Requirement for consistent practice to distinguish sub-recipient from

contractor o Identifying or negotiating an appropriate sub-recipient indirect cost

rate at the time of award o Ensuring “flow-down” of new requirements are included within sub

agreements, as applicable o Evaluating sub-recipient risk of noncompliance and determining

necessary monitoring activities – including on-site reviews o Imposing remedies for sub-recipient noncompliance, when necessary

Page 6

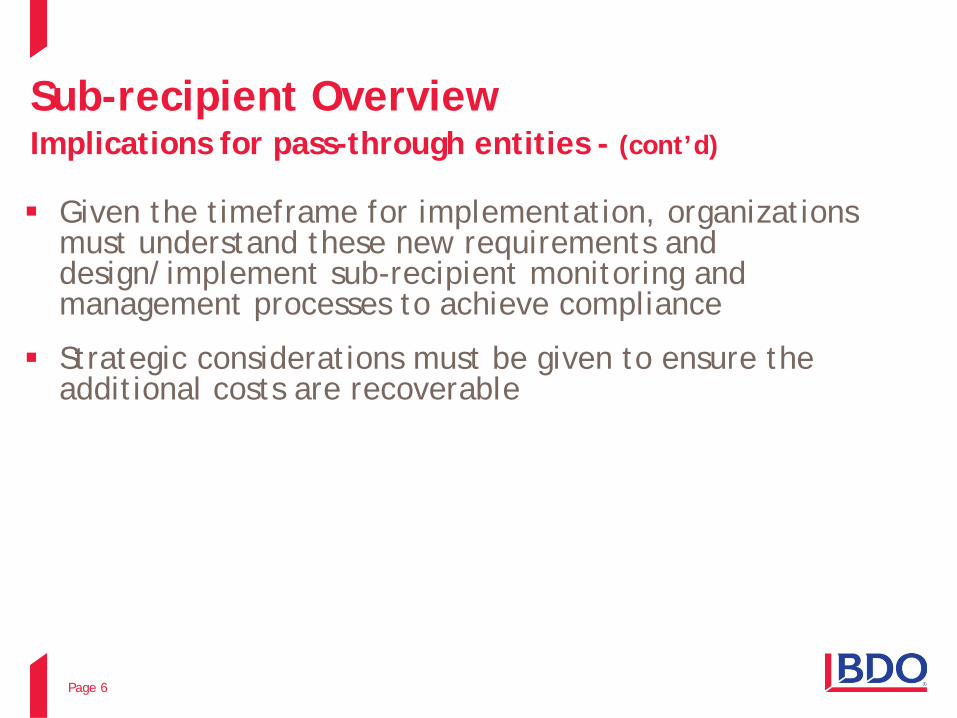

Sub-recipient Overview Implications for pass-through entities - (cont’d)

Given the timeframe for implementation, organizations must understand these new requirements and design/implement sub-recipient monitoring and management processes to achieve compliance

Strategic considerations must be given to ensure the additional costs are recoverable

BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms.

Sub-recipient & Contractor Determinations

Page 8

Sub-recipient or Contractor… What’s the difference?

Sub-recipient: o A sub-recipient “uses the Federal funds to carry out a program for a

public purpose specified in authorizing statute” o Characteristics which support classification of the non-Federal entity

(NFE) as a sub-recipient includes when the NFE: 1. Determines who is eligible to receive what Federal assistance; 2. Has its performance measured in relation to whether objectives of a

Federal program were met; 3. Has responsibility for programmatic decision making; 4. Responsible for adherence to applicable Federal program requirements

specified in the Federal award; and 5. In accordance with its agreement, uses Federal funds to carry out a

program for a public purpose specified in authorizing statute, as opposed to providing goods or services for the benefit of the pass-through entity.

Page 9

Sub-recipient or Contractor… What’s the difference? - (cont’d)

Contractor:

o A contract is for the purpose of obtaining goods and services for the non-Federal entity’s own use and creates a procurement relationship with the contractor

o Characteristics indicative of a relational between a NFE and a contractor are when the NFE who is receiving federal funds: 1. Provides similar goods or services to many different purchasers; 2. Normally operates in a competitive environment; 3. Provides goods or services that are ancillary to the operation of the Federal

program; and 4. Is not subject to compliance requirements of the Federal program as a

result of the agreement, though similar requirements.

Page 10

Sub-recipient or Contractor… How do we make this determination? Pass-through entities must make case-by-case

determination

The nature & substance of the agreement will drive classification

Consider that financial risks for sub-recipient and contractor are mitigated in different manners

Page 11

Sub-recipient or Contractor… How do we make this determination? – (cont’d) Agencies may require pass-through entities to comply with

additional guidance to support such determinations

Nuances between these terms will lead to varying practices to procure such services

Best Practice Recommendation: Establish a clear and concise policy/procedure which requires full documentation of each case-by-case determination

BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms.

Sub-recipient Selection & Planning

Page 13

Sub-recipient Selection & Planning What’s required?

Establish formal process to properly structure sub-recipient agreements. Be sure to include: o All flow-down requirements necessary to ensure appropriate sub-

recipient use of Federal award o Any additional flow-down requirements necessary for pass-through

entity to meet its own responsibilities o A requirement that the sub-recipient permit access to records and

financial statements through the period of performance

Consider expanded pass-through entity responsibilities o Required information to be provided to sub-recipients o Use of appropriate sub-recipient indirect cost rates o Conduct sub-recipient risk assessment

Page 14

Sub-recipient Selection & Planning Required information Must clearly identify every sub-award to the sub-

recipient and must include the following information at the time of the sub-award:

o Federal Award Identification and Federal Award Identification Number (FAIN)

o Sub-recipient name and DUNS number o Federal award date o Sub-award period of performance (start and end dates) o Funding information o Federal award project description o Name of the Federal awarding agency o Catalog of Federal Domestic Assistance (CFDA) title and number o Identify if award is for Research & Development (R&D) o Indirect cost rate for the Federal award

Page 15

Sub-recipient Selection & Planning Required information – (cont’d)

Changes to data elements previously provided must be reflected in subsequent sub-award modifications

Should some of the required information not be available at the time of award, pass-through entity may include the best information available to describe the Federal award and sub-award

Best Practice Recommendation:

Establish a clear and concise policy/procedure which details how required information will be collected/provided

Page 16

Sub-recipient Selection & Planning Indirect cost rate

Consider if sub-recipient has an approved/federally recognized indirect cost rate

If no such rate exists, consider alternative options: o Negotiate rate with sub-recipient o Use de minimis rate of 10% of modified total direct cost (MTDC) o Utilize fixed amount sub-awards Requires prior written approval from the Federal awarding agency May only be used when total sub-award value does not exceed the

Simplified Acquisition Threshold (i.e. $150,000) Must consider requirements of section 200.201 “Use of grant

agreements (including fixed amount awards) cooperative agreements, and contracts”

BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms.

Sub-recipient Risk Assessment & Monitoring Plan

Page 18

Sub-recipient Monitoring Activities Risk assessment

Sub-recipient monitoring plan must ensure that the sub-award: o Is used only for authorized purposes o Is in compliance with Federal statutes/regulations & sub-award T&Cs o Achieves its performance goals

Consider risk of sub-recipient noncompliance

Risk assessment is based on: o Prior/past experience with similar sub-awards o Previous audit results o Significant changes in personnel or systems o Extent and results of Federal awarding agency monitoring

Page 19

Sub-recipient Monitoring Activities Monitoring plan Minimum monitoring activities must include:

o Reviewing financial and programmatic reports o Conducting on-site reviews/audits based on risk assessment o Conducting follow-up reviews to ensure timely completion of

corrective actions required to address deficiencies – as identified through on-site reviews, audits, or other means

o Issuing a management decision for audit findings pertaining to the Federal award

o Verifying that each sub-recipient receive completed audits, as required

Design of monitoring plan will vary based on sub-recipient risk assessment: o i.e., more stringent monitoring plan is required for high risk sub-

recipients

Page 20

Sub-recipient Monitoring Activities Additional considerations

Based on results of monitoring activities, pass through entities should o Provide training and technical assistance to appropriate sub-recipient

staff o Determine if on-site reviews/audits necessitate adjustments to own

records o Consider taking enforcement action against noncompliant sub-recipients

If sub-recipient noncompliance is determined, pass through entities may apply enforcement action through specific conditions (§200.207)

If noncompliance cannot be remedied through specific conditions, more severe enforcement action may be taken (§200.338)

Page 21

Sub-recipient Monitoring Activities Imposing specific conditions

Specific conditions can o Dictate how sub-award receives payment o Require additional reporting requirements or prior approvals o Require sub-recipient obtain technical or management assistance

When imposed, specific conditions must be clearly communicated to sub-recipients

Any specific conditions must be promptly removed once corrected

Page 22

Sub-recipient Monitoring Activities Additional enforcement action If noncompliance cannot be remedied through specific

award conditions, consider more severe enforcement action, such as: o Applying temporary cash withholds o Disallowing all or part of the cost of the activity o Suspending or terminating the sub-award o Recommending the Federal awarding agency initiate suspension or

debarment proceedings o Withholding future awards to the sub-recipient o Pursuing other remedies legally available

Best Practice Recommendation: Establish a clear and concise policy/procedure which details the sub-recipient risk assessment process. Establish criteria for determining an appropriate sub-recipient monitoring plan, based on risk assessment.

BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms.

Sub-recipient Monitoring Performance & Cost Recovery

Strategies

Page 24

Sub-recipient Monitoring Performance strategies

Internal:

o All sub recipient monitoring task can be performed “in house” using staff

o Omni-circular provides for opportunity to augment and refine existing processes to address new compliance requirements

o Consider timing requirements and resource bandwidth

External: o New requirement allows for outsourced sub recipient monitoring

functions o Considered an allowable direct cost provided that agreed upon

procedures are: Conducted in accordance with Generally Accepted Government Auditing

Standards (GAGAS) Paid for and arranged by the pass-through entity Limited in scope to specific compliance requirements

Page 25

Sub-recipient Monitoring Cost recovery strategies

Limited cost recovery afforded through an indirect rate

o Only first $25,000 of sub-recipient costs receive indirect cost allocation

New guidance allows for outsourced sub-recipient monitoring

costs to be recovered directly to awards Organizations who plan to outsource sub-recipient monitoring

must: o Determine the mechanics and allocate costs prior to finalizing budgets o Ensure these are costs included in upcoming proposals Otherwise, these costs may not be allowed as direct cost going forward

Page 26

Sub-recipient Monitoring Activities General best practices Sub-recipient monitoring procedures should include:

o Informing your sub-recipient of pertinent information o Ensuring your sub-recipients are receiving audits when necessary o Reviewing financial and programmatic reports Reconcile the sub-recipient's budgeted expenditures to actual expenditures Perform an on-site visit to the sub recipient to review financial and

programmatic records and observe operations Desk review - review financial and program reports submitted by sub

recipients for allowable use of the grant funds. o Establishing a tracking system to assure timely submission of required

reporting o Having a 2nd party within your organization periodically review the

adequacy of sub recipient monitoring for all programs o Document! Document! Document!

Remember, your program’s success is contingent upon their ability to comply!

BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms.

Questions?