PDF generated by 'Newgen elango'leeds-faculty.colorado.edu/bhagat/Chapter-5.pdf110 Sanjai Bhagat,...

38

Chapter 5 IPO Valuation The International Evidence Sanjai Bhagat, Jun Lu, and Srinivasan Rangan 5.1. Introduction Initial public offerings (IPOs) are an economically significant contributor to the amount of capital raised by firms around the world. Over US$4.1 trillion was raised by over 36,000 firms that completed an IPO between 1998 and 2015 (omson SDC Global New Issues database). Further, IPO firms are also considered the drivers of innovation and employment in the economy, and hence their success is critical to economic growth. Beginning with Loughran, Ritter, and Rydqvist (1994), several studies have documented cross-country differences in the IPO process and how these differences influence the decision to go public and subsequent pricing (Henderson, Jegadeesh, Weisbach, 2006; Kim and Weisbach, 2008; Caglio, Hanley, Westburg, 2010). While a few studies have focused on underpricing (change in price on the first day of trading) of IPOs around the world, no previous study has examined cross-country differences in determinants of the level of the IPO value. 1 e valuation of IPOs occupies an important place in finance, perhaps because an IPO provides public capital market participants their first opportunity to value a set of corporate assets and growth opportunities. e valuation of IPOs is also quite relevant from an economic efficiency perspective: the IPO is the first opportunity that managers of such (usually young) companies get to observe price signals from the public capital markets. Such signals can either affirm or repudiate management’s beliefs regarding the firm’s future growth opportunities, which have obvious implications for real economic activity—for example, employment and corporate investment. e finance literature has several hundred papers on IPO underpricing, which is the dif- ference between the market price at the end of the offer day and the offer price. However, there is little in the literature on the offer price itself. It is the offer price that is of greater interest to investors, issuing companies, regulators, and investment bankers; investors are OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN Part-1.indd 108 27-Jul-18 10:11:09 PM

Transcript of PDF generated by 'Newgen elango'leeds-faculty.colorado.edu/bhagat/Chapter-5.pdf110 Sanjai Bhagat,...

Chapter 5

IP O ValuationThe International Evidence

Sanjai Bhagat, Jun Lu, and Srinivasan Rangan

5.1. Introduction

Initial public offerings (IPOs) are an economically significant contributor to the amount of capital raised by firms around the world. Over US$4.1 trillion was raised by over 36,000 firms that completed an IPO between 1998 and 2015 (Thomson SDC Global New Issues database). Further, IPO firms are also considered the drivers of innovation and employment in the economy, and hence their success is critical to economic growth.

Beginning with Loughran, Ritter, and Rydqvist (1994), several studies have documented cross- country differences in the IPO process and how these differences influence the decision to go public and subsequent pricing (Henderson, Jegadeesh, Weisbach, 2006; Kim and Weisbach, 2008; Caglio, Hanley, Westburg, 2010). While a few studies have focused on underpricing (change in price on the first day of trading) of IPOs around the world, no previous study has examined cross- country differences in determinants of the level of the IPO value.1

The valuation of IPOs occupies an important place in finance, perhaps because an IPO provides public capital market participants their first opportunity to value a set of corporate assets and growth opportunities. The valuation of IPOs is also quite relevant from an economic efficiency perspective: the IPO is the first opportunity that managers of such (usually young) companies get to observe price signals from the public capital markets. Such signals can either affirm or repudiate management’s beliefs regarding the firm’s future growth opportunities, which have obvious implications for real economic activity— for example, employment and corporate investment.

The finance literature has several hundred papers on IPO underpricing, which is the dif-ference between the market price at the end of the offer day and the offer price. However, there is little in the literature on the offer price itself. It is the offer price that is of greater interest to investors, issuing companies, regulators, and investment bankers; investors are

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 108 27-Jul-18 10:11:09 PM

IPO Valuation: The International Evidence 109

more interested in IPO valuation, which is the offer price times the number of shares out-standing. In light of this, it is especially surprising that the finance literature has devoted so much intellectual effort to understanding IPO underpricing but so little to understanding the more primitive economic variable: the offer price, or the value of the IPO.

In this chapter, we study the valuation of 6,199 IPOs during 1998– 2015 for the fol-lowing countries: Australia, Canada, China, Germany, India, Japan, the United Kingdom, and the United States. We construct a model to value IPOs. Conceptually, the value of an asset is the sum of the present value of its expected future cash flows. Estimating the expected future cash flow of most any company is nontrivial; this task is even more challenging for IPO firms given that, in general, less is known about their past performance, and there is greater uncertainty about their future prospects. Instead of directly estimating future cash flows and the cost of capital to discount these cash flows, we construct proxies for the cash flows and discount rates; these proxies involve financial and nonfinancial variables. We discuss these proxies in the following.

In a seminal article, Ohlson (1990) develops a model that expresses the market value of equity as a linear function of earnings, book value of equity, and other information. Subsequently, a sizable body of empirical research (see, for example, Penman, 1998, and Francis and Schipper, 1999) has used this model to motivate empirical investigations of the value relevance of earnings and book value of equity. Myers (1977) has suggested that the market value of a firm is positively related to its growth opportunities. Growth opportunities are especially critical for IPOs given that more, if not most, of an IPO’s value is based on them. More recently, Abel and Eberly (2005) propose a valuation model that explicitly incorporates the possibility that firms may upgrade to or adopt a new technology. In their model, the value of the firm is composed of three components: the replacement cost of the firm’s physical capital, the net present value of the firm’s expected future cash flows from assets in place, and the value of growth options associated with future technological upgrades.

There is a substantive literature in financial accounting on the value relevance of ac-counting variables in explaining cross- sectional variation in the market value of stocks; Kothari (2001) and Barth, Beaver, and Landsman (2001) review this literature. Collins, Maydew, and Weiss (1997) document the increasing importance of net income in explaining the cross- sectional variation in market value. Lev (2001) has argued that the value- relevance of book value has declined over time, since intangible assets comprise a larger fraction of the value of most firms today; this would be especially true for IPOs whose value, as noted earlier, would be drawn from their growth opportunities (intan-gible assets). Rhodes- Kropf, Robinson, and Viswanathan (2005) (RRV) draw on this lit-erature and propose a simple model that includes only book value and net income to explain the cross- sectional variation in stock market values. We adopt and extend the RRV model in our analysis.

The main variables that prior literature on accounting and finance has shown to influence IPO prices in the United States are earnings, book value, expected growth, pre- IPO insider ownership, underwriter reputation, and auditor reputation (Ohlson, 1990; Aggarwal, Bhagat, and Rangan, 2009). The accounting and finance literatures document that earnings opacity influences a range of capital market outcomes

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 109 27-Jul-18 10:11:09 PM

110 Sanjai Bhagat, Jun Lu, and Srinivasan Rangan

(Bhattacharya, Daouk, and Welker, 2003; Gelos and Wei, 2005; Jin and Myers, 2006). We expect that the impact of pre- IPO data on IPO prices will be lower in countries where earnings are more opaque. Recently, several countries, especially in the European Union, have adopted International Financial Reporting Standards (IFRS). An open question is whether the adoption of these standards has influenced the quality of accounting data in these countries and if market participants perceive differences in quality.

In a series of influential papers, La Porta et al. (1997, 2000) analyze the role of a country’s legal system in protecting investor rights. They argue that “diverse elements of countries’ financial systems as the breadth and depth of their capital markets, the pace of new security issues, corporate ownership structures, dividend policies, and the effi-ciency of investment allocation appear to be explained both conceptually and empir-ically by how well the laws in these countries protect outside investors. (2000, p. 4.)” Further, they postulate that the commercial legal codes of most countries are based on four legal traditions: the English common law, the French civil law, the German civil law, and the Scandinavian law. They find that common law countries provide the most protection to investors and that they have the deepest stock markets and most dispersed corporate ownership structures. They also document that countries develop substitute mechanisms for poor investor protection, such as mandatory dividends and greater ownership concentration. Finally, they find that investor protection is posi-tively correlated with valuation across countries. To the extent that IPO valuations are correlated with valuations of financial securities, in general, investor protection would be a determinant of IPO valuation.

In a recent paper, Cumming et al. (2016) document a positive correlation between IPO valuations and backing of such IPOs by international venture capital syndicates. Additionally, listing requirements across exchanges and countries have been found to be correlated with IPO valuation; see Carpentier et al. (2012); Johan (2010); Carpentier et al. (2012); and Cumming et al. (2016).

The remainder of the chapter is organized as follows. The next section (5.2) describes our sample and data, and section 5.3 discusses descriptive statistics of several pre- IPO financial and offering variables. Section 5.4 details our empirical results for the determinants of IPO valuation across countries. The final section (5.5) concludes with a summary.

5.2. Sample and Data

5.2.1. Sample

An initial sample of 21,577 observations for the years 1998– 2015 is obtained from the Thomson Reuters SDC Platinum New Issues database (SDC) for eight coun-tries: Australia, Canada, China, Germany, India, Japan, the United Kingdom, and the

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 110 27-Jul-18 10:11:09 PM

IPO Valuation: The International Evidence 111

United States. In Table 5.1, we report the type and number of IPOs that are excluded to arrive at our final sample, by country and for all countries combined. Our filters are similar to those applied in prior research on IPO pricing— we exclude financial firms, privatizations, unit offerings, private placements, spinoffs, rights offerings, offerings by limited partnerships, offerings that do not involve common shares (for example, loan

Table 5.1 Sample Selection Screens for International IPOs, 1998– 2015

All Australia Canada China Germany India JapanUnited Kingdom

United States

Start: 21,527 2,205 4,061 4,677 955 958 2,193 1,890 4,588

(–) Financial firms

5,757 402 2,546 327 116 126 362 574 1,304

(−) Privatizations 30 6 3 15 0 0 2 3 1

(−) Offerings of units (shares + warrants)

703 93 462 2 0 0 0 10 136

(−) Private placements

73 12 3 8 20 2 4 21 3

(−) Spinoffs 1,470 149 24 452 63 15 300 100 367

(−) Rights offerings

19 14 0 0 2 0 0 0 3

(−) Limited partnerships

69 1 11 1 0 0 0 3 53

(−) Loan stock, options, or flow through shares

31 1 30 0 0 0 0 0 0

(−) Not underwritten

4 0 0 0 0 4 0 0 0

(−) Missing SEDOL and CUSIP

395 65 10 88 63 0 20 149 0

(−) Follow- on offerings

29 3 5 9 3 1 2 3 3

(−) Multiple tranches of same IPO

2,417 120 24 1,278 261 125 126 86 397

10,534 1,342 943 2,497 427 686 1,377 941 2,321

(−) Missing prospectus or IPOs not qualifying per screens

4,335 814 657 852 205 217 850 488 252

Final Sample: 6,199 528 286 1,645 222 469 527 453 2,069

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 111 27-Jul-18 10:11:09 PM

112 Sanjai Bhagat, Jun Lu, and Srinivasan Rangan

stock), offerings that are not underwritten, offerings by firms with missing CUSIPS and SEDOLs, and follow- on offerings.2 These exclusions enable us to achieve a relatively ho-mogenous sample of underwritten offerings of common shares to new investors that result in a cash infusion to the firm or its pre- IPO shareholders. The basic unit of obser-vation on SDC is an offering tranche; while some IPOs have a single tranche, others have more than one tranche. To achieve a sample of unique IPOs (one observation per firm), we also eliminate 2,417 tranches that relate to multiple- tranche IPOs.

For each of the remaining 10,534 IPOs (except for Chinese IPOs), we attempt to ob-tain final IPO prospectuses from the following sites: www.sec.gov for US firms, www.sedar.com for Canadian firms, www.sebi.gov.in for Indian firms, and the Filings Library of the Thomson One Banker database for Australian, German, Japanese, and UK firms. For Chinese firms, we obtain pre- IPO data from the Guo Tai An (GTA) database, and not from prospectuses. When reading prospectuses, we discovered firms that would be eliminated based on the aforementioned filters. Our final “filter- compliant” sample for which we have prospectuses consists of 6,199 IPOs. China and the United States have the highest number of IPOs among the eight countries, and Canada and Germany the lowest. Figure 5.1 presents a pie chart of the country- wise shares of the number of completed IPOs.

Table 5.2 presents the time series of offering frequencies in percentages for the eight countries. In general, IPO volumes display cyclicality, with peak volumes varying across countries. IPO frequencies rose during the years 1998– 2000 before dropping in 2001— the year following the crash of the dot- com bubble. Subsequently, IPO markets

USA33%

Australia8%

Canada5%

China27%

Germany4%India

8%

Japan8%

UK7%

Australia Canada China Germany India Japan UK USA

Figure 5.1. Distribution of 6,199 IPOs in countries during 1998– 2015

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 112 27-Jul-18 10:11:09 PM

Tabl

e 5.

2 Di

strib

utio

n of

IPO

s ove

r Tim

e (1

998–

2015

)

Year

Freq

uenc

yFr

eque

ncy

%

All

All

Aust

ralia

Cana

daCh

ina

Ger

man

yIn

dia

Japa

nU

nite

d Ki

ngdo

mU

nite

d St

ates

1998

332

5%1%

6%5%

6%0%

2%3%

9%

1999

553

9%5%

6%3%

18%

0%4%

1%19

%

2000

659

11%

6%9%

6%32

%3%

9%14

%15

%

2001

182

3%1%

1%3%

5%0%

7%6%

3%

2002

148

2%2%

3%2%

1%0%

4%6%

2%

2003

193

3%5%

1%3%

0%1%

6%4%

2%

2004

414

7%10

%6%

5%1%

4%6%

15%

7%

2005

347

6%10

%6%

1%2%

10%

7%13

%6%

2006

440

7%13

%6%

3%11

%14

%9%

9%6%

2007

506

8%18

%12

%6%

11%

16%

5%7%

6%

2008

166

3%3%

6%4%

1%7%

2%1%

1%

2009

177

3%4%

4%6%

0%3%

0%0%

2%

2010

493

8%5%

8%19

%2%

10%

3%2%

3%

2011

421

7%3%

9%15

%4%

6%4%

1%3%

2012

252

4%2%

6%5%

3%3%

6%2%

3%

2013

190

3%3%

5%0%

0%4%

6%4%

4%

2014

336

5%5%

2%5%

1%6%

9%8%

5%

2015

390

6%5%

3%9%

1%12

%11

%4%

3%

6,19

952

828

61,

645

222

469

527

453

2,06

9

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 113 27-Jul-18 10:11:09 PM

114 Sanjai Bhagat, Jun Lu, and Srinivasan Rangan

around the world recovered to grow in volume from 2002 to 2007. With the advent of the financial crisis in the years 2008– 2009, IPO volume fell for all countries. Thereafter, during the most recent period, 2010– 2015, volumes returned to pre- crisis levels, but never exceeded levels attained between 2002 and 2007. The peak offering frequency year varies across countries and is as follows: Australia— 2007, Canada— 2007, China— 2010, Germany— 2000, India— 2007, Japan— 2015, United Kingdom— 2004, and United States— 1999. Figure 5.2 plots the time series of offering frequency for the eight countries combined.

5.2.2. Data Sources and Definitions

SDC is our primary data source for the following 13 offering- related variables: offer price in local currency, offer date, offering proceeds in US dollars, primary shares offered, sec-ondary shares offered, total shares offered, shares outstanding after the offering, shares outstanding before the offering, name of the auditor, names of the lead underwriters, exchange, currency in which shares are offered, and four- digit SIC code. When these variables are missing, we filled in their values from prospectuses. We verify the accuracy of these SDC- sourced variables (except for SIC codes, offering proceeds, and under-writer names) by comparing their values with those in prospectuses; whenever we find a difference, we replace SDC data with values from the prospectuses. As stated earlier, for Chinese firms, we rely on the GTA database rather than SDC for offering data.

We obtain founding years from IPO prospectuses, except for China and the United States. Founding years for Chinese firms are from the GTA database. For US firms, we obtain founding years from Professor Jay Ritter’s IPO database;3 when founding years were not available on that database, we obtain them from prospectuses. We de-fine firm age as the difference between the offering year based on the offer date and the founding year.

700

600

500

400

300

200

100

01998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Figure 5.2. Aggregate number of IPOs for Australia, Canada, China, Germany, India, Japan, the United Kingdom, and the United States.

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 114 27-Jul-18 10:11:09 PM

IPO Valuation: The International Evidence 115

Besides age, we construct four measures that we expect to influence IPO valua-tion: auditor reputation, underwriter reputation, industry Price- Earnings (PE) ratio, and pre- IPO market returns. Consistent with a large body of auditing literature, we measure auditor reputation as a 1– 0 dummy variable based on whether or not the firm’s financials were audited by a Big- N (N largest auditors, where N varies from 4 to 8) au-ditor. To measure underwriter reputation, we employ the method of Megginson and Weiss (1991). For each underwriter j and for every year t, we define xjt as the three- year moving average (t- 3, t- 2, t- 1) of IPO proceeds. Then, for the set of underwriters I, for the year t, the Megginson- Weiss rank for underwriter j is:

UWRANKx

Max xjt

jt

j I jt

= ( )

∈

log( )

log (5.1)

This measure of underwriter reputation is market- share based and is a continuous variable on the interval [0,1]. When an IPO has multiple lead underwriters, we divide IPO proceeds by the number of underwriters.

To measure industry PE, for each IPO firm, we obtain the market capitalizations at the end of the month before the offering date for all firms in that firm’s country that had the same two- digit SIC code (industry peers). We chose two- digit SIC codes to mini-mize data loss because of industries having too few firms. For these industry peers, we obtain the income before extraordinary items for the most recent year relative to the month- end at which market capitalization is measured. We compute industry medians of PE, market capitalization divided by income before extraordinary items. Market cap-italization and income before extraordinary items are from The Center for Research on Security Prices (CRSP) and North America COMPUSTAT for US firms, Global Compustat for firms from Australia, Canada, China, Germany, Japan, and United Kingdom, and from the CMIE Prowess database for Indian firms.

To compute three- month market return before each firm’s offering date, we sum daily market returns over 63 trading days ending on the day before the offering date. Daily market returns are measured as the value- weighted market- wide return for US stocks from CRSP and as percent changes in daily market index values from CMIE prowess for Indian firms and from Global Compustat for the other six countries (Appendix 5.1 details the specific market indices used for the seven countries).

Turning to the financial statement variables, we manually collect the following eight financial statement variables for years – 1 to – 3 relative to the offering date from prospectuses, whenever available: sales, research and development (R&D) costs, income before extraordinary items, cash flows from operations, capital expenditures, long- term debt, book value of equity, and total assets. All numbers were coded in millions of the local currency. For the empirical work, we converted flow numbers such as sales into US dollars by using the average of the daily exchange rates over the fiscal year. Stock num-bers such as total assets were converted into US dollars based on the exchange rate on the last day of the fiscal year. When an exchange rate was unavailable on the last date, we

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 115 27-Jul-18 10:11:09 PM

116 Sanjai Bhagat, Jun Lu, and Srinivasan Rangan

used the most recent exchange rate before the fiscal year end date. Daily exchange rates are from www.federalreserve.gov.

All financial data items obtained are audited historical numbers.4 In general, all flow numbers were measured over 12 months; however, to minimize data loss, when a firm reported either 13 months or 11 months of data, we converted those numbers into 12- month values. If a firm reported flow numbers for more than 13 months or less than 11 months, we set those numbers to missing. Additionally, if a firm changed its fiscal year, data for the year of the fiscal year change was set to missing. For stock numbers, we collected the numbers reported on the fiscal year end date; if the only balance sheet num-bers available were reported on a date other than the fiscal year end date, we set those numbers to missing. Detailed definitions of financial statement variables are provided in Appendix 5.1.

5.3. Descriptive Statistics

Table 5.3 presents descriptive statistics for several offering variables. All variables, ex-cept for the auditor reputation dummy variable, are winsorized at the 1% and 99% levels. Because most of the variables are skewed, we discuss only median values. Our primary dependent variable is post- IPO market capitalization, measured as the product of offer price and shares outstanding on completion of the offering (MCAP). To achieve com-parability, MCAP is expressed in US dollars using exchange rates on the offer date.5 US IPOs record the highest median MCAP ($312.8 million), followed by China ($256.3 mil-lion), and then by Canada at a distant third ($50.4 million). Median offering proceeds are largest for the United States ($75.0 million), and smallest for Australia ($4.8 million). Median offer prices range from $770 for Japan to $0.32 for Australia.

Prior literature has documented that insider retention (percentage of offering retained by insiders) is a significant determinant of IPO valuation. We compute insider retention by subtracting secondary shares sold during the IPO from shares outstanding before the IPO and dividing that difference by post- IPO shares outstanding. Table 5.3 indicates that median post- IPO insider retention varies from 61% in Australia to 80% in Japan. We also report data on the frequency of secondary offerings. Secondary offerings are very frequent in Japan, with 89% of Japanese IPOs having a secondary component. At the other extreme, only 3% of Chinese IPOs have a secondary component.

A large body of evidence documents that IPOs are underpriced and that first- day prices are higher than offer prices, on average. Table 5.3 indicates that this is true of our sample as well, with two additional insights. First, the mean percentage change in price from offer to open is indeed positive for all eight countries, ranging from 1% for Japan to 182% for the United Kingdom. However, medians are negative for Australia (– 18%), Germany (– 6%) and Japan (– 8%). Second, the underpricing evidence is largely driven by the change from the offer to the first- day open. The magnitude of price changes from open to close on the first day are relatively small. Mean open- to- close percent change

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 116 27-Jul-18 10:11:09 PM

Tabl

e 5.

3 O

ffer

ing

Desc

riptiv

e St

atis

tics

Aust

ralia

Cana

daCh

ina

Ger

man

yIn

dia

Japa

nU

nite

d Ki

ngdo

mU

nite

d St

ates

Mar

ket C

ap. a

t Off

er P

rice

(Mill

ions

of U

S$)

Mea

n11

8.2

192.

643

0.0

208.

120

5.1

111.

465

.756

1.9

Med

ian

27.2

50.4

256.

310

6.5

38.0

46.7

14.6

312.

8

No.

of o

bs.

528

286

1,64

522

246

952

745

32,

069

Off

er P

roce

eds (

Mill

ions

of U

S$)

Mea

n29

.152

.099

.771

.137

.822

.852

.411

9.1

Med

ian

4.8

14.8

66.9

35.6

13.0

9.1

13.2

75.0

No.

of o

bs.

528

286

1,64

522

246

952

745

32,

069

Off

er P

rice

(US$

)

Mea

n0.

804.

622.

6519

.55

3.13

770.

040.

7313

.50

Med

ian

0.32

1.96

2.07

15.9

81.

8319

.96

0.49

13.0

0

No.

of o

bs.

528

286

1,64

522

246

952

745

32,

069

Insi

der R

eten

tion

Mea

n61

%66

%73

%67

%69

%79

%63

%73

%

Med

ian

61%

71%

75%

71%

72%

80%

66%

75%

No.

of o

bs.

528

286

1,63

922

246

952

745

32,

069

Seco

ndar

y O

ffer

ings

Freq

uenc

y12

%12

%3%

65%

17%

89%

34%

29%

No.

of o

bs.

528

286

1,64

522

246

952

745

32,

069

Firs

t- Da

y Cl

ose

(US$

)

Mea

n2.

265.

763.

9529

.20

3.94

449.

972.

4120

.03

Med

ian

0.30

2.52

3.27

12.2

82.

1819

.36

1.13

15.5

0

No.

of o

bs.

512

269

1,64

521

546

752

644

91,

987

(Contin

ued)

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 117 27-Jul-18 10:11:09 PM

Aust

ralia

Cana

daCh

ina

Ger

man

yIn

dia

Japa

nU

nite

d Ki

ngdo

mU

nite

d St

ates

Firs

t- Da

y O

pen

(US$

)

Mea

n1.

685.

343.

8220

.36

3.73

22.8

52.

2219

.00

Med

ian

0.30

2.19

3.15

12.1

52.

1415

.35

1.05

15.2

5

No.

of o

bs.

509

266

1,64

521

446

737

743

51,

970

% C

hang

e fr

om O

ffer

to F

irst-

Day

Ope

n

Mea

n7%

30%

68%

15%

18%

1%18

2%31

%

Med

ian

– 18%

6%43

%−6

%8%

−8%

199%

11%

No.

of o

bs.

509

266

1,64

521

446

737

743

51,

970

% C

hang

e fr

om F

irst D

ay O

pen

to C

lose

Mea

n−1

%−1

%4%

1%3%

0%4%

3%

Med

ian

−2%

0%2%

0%0%

0%1%

0%

No.

of o

bs.

509

265

1,64

521

446

737

743

51,

970

Age

Mea

n4.

66.

07.

311

.313

.325

.44.

012

.5

Med

ian

1.0

3.0

7.0

7.0

11.0

19.0

1.0

7.0

No.

of o

bs.

500

286

1,64

522

246

952

345

32,

069

Unde

rwrit

er R

eput

atio

n

Mea

n0.

550.

570.

740.

670.

590.

800.

580.

77

Med

ian

0.59

0.60

0.75

0.68

0.55

0.89

0.58

0.81

No.

of o

bs.

528

286

1,64

522

246

952

745

32,

069

Tabl

e 5.

3 (C

ontd

.)

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 118 27-Jul-18 10:11:09 PM

Big-

N A

udito

r

Freq

uenc

y (%

)32

%55

%3%

40%

15%

85%

42%

87%

No.

of o

bs.

528

286

1,64

522

246

925

745

32,

067

Indu

stry

PE

Mea

n18

.047

.733

.413

.021

.622

.324

.7

Med

ian

16.7

46.4

20.7

10.8

20.3

21.5

24.4

No.

of o

bs.

513

01,

577

215

457

521

446

2,06

7

Pre-

Off

erin

g 63

- Day

Ret

urn

Mea

n2.

9%2.

8%3.

3%2.

5%5.

6%3.

4%2.

5%3.

8%

Med

ian

2.1%

1.9%

3.0%

2.8%

4.7%

2.6%

1.6%

4.5%

No.

of o

bs.

528

286

1,64

522

246

952

745

32,

069

Not

e: V

aria

ble

Defin

ition

s are

in A

ppen

dix

5.1.

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 119 27-Jul-18 10:11:09 PM

120 Sanjai Bhagat, Jun Lu, and Srinivasan Rangan

ranges from – 1% for Australia and Canada to 4% for China and the United Kingdom; medians range from – 2% to 2%.

Table 5.3 also reports descriptive statistics for our three nonfinancial value drivers: age, underwriter reputation, and auditor reputation. IPO firms in Australia, Canada, and the United Kingdom are relatively young, with a median age of one to three years. Japanese and Indian IPOs have the highest median ages of 11 and 19 years, re-spectively. Chinese, German, and US firms have a median age of seven years. Median underwriter reputation values are highest for Japan and the United States (0.89, 0.81). For the other countries, median reputation values range from 0.55 for Australia to 0.75 for China. The frequency with which IPO firms employ Big- N auditors varies consid-erably across countries, ranging from a mere 3% in China to 85% in Japan and 87% in the United States. Overall, it appears that US and Japanese firms prefer high reputation auditors and underwriters. Alternately stated, the audit markets in the United States and Japan are more oligopolistic than those of other countries.

Finally, we report means and medians for pre- IPO industry PE ratios and three- month market returns. Median industry multiples, except for China, range from 10 to 25; these numbers are comparable with the median PE ratio of 24 for the S&P 500 over our sample period, 1998– 2015 (http:// www.multpl.com/ table). Median Chinese in-dustry PEs are relatively high at 44. Pre- IPO market returns are in general positive, with median returns ranging from 1.6% to 4.7%.

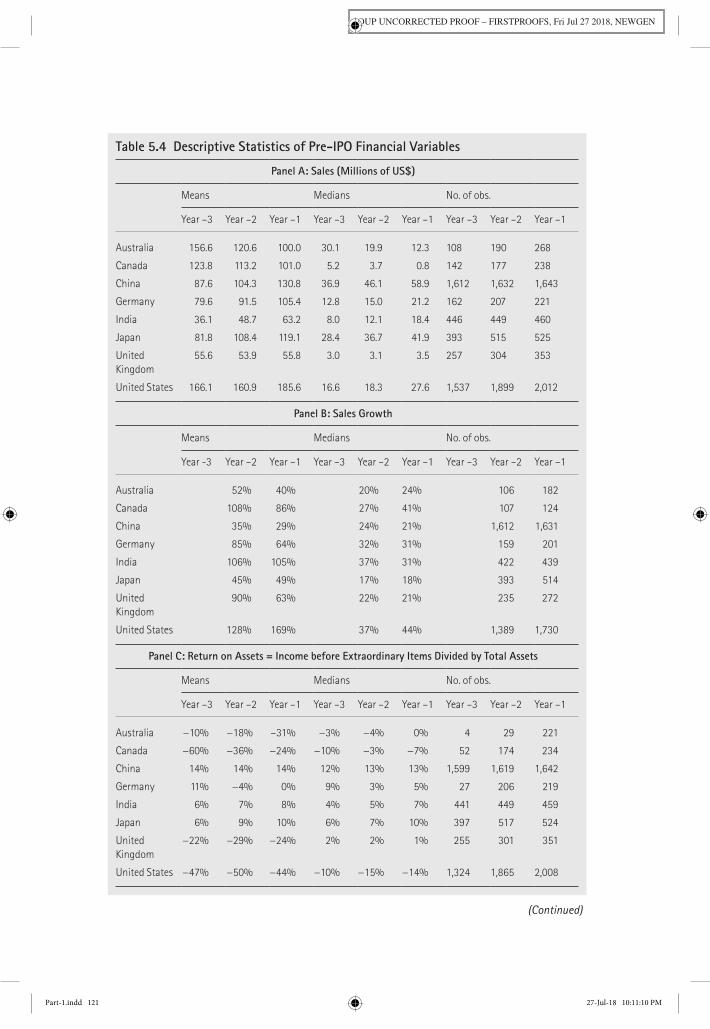

Table 5.4 reports, via a series of panels, the mean and median values of several finan-cial indicators over years – 3 to – 1. Again, all variables are winsorized at the 1% and 99% levels. Panel A reports that median sales increases monotonically for six of the eight countries; Australian and Canadian IPOs record average declining sales. The surprising decline for these two countries can be explained by the fact that their sample sizes increases from year – 3 to – 1 and the firms that enter the sample for the first time in year – 1 tend to have low sales.6 Panel B presents sales growth rates in year – 2 and – 1. Median sales growth rates in year – 2 range from 17% for Japanese firms to 37% for US firms. In year – 1, growth rates decline for China, Germany, India, and the United Kingdom, but rise for the remaining countries.

Panels C and D in Table 5.4 provide information on pre- IPO trends in return on assets (ROA) and loss frequency. ROA is defined as income before extraordinary items divided by ending total assets. While the median Australian, Canadian, and US firm is in the red or fails to achieve profitability for all three pre- IPO years, the median firms in the other five countries generate positive ROA in all three years. Further, median ROA trends up-ward in India and Japan. In data in Panel D, suggest that pre- IPO loss frequencies in the three Asian countries— China, India, and Japan, are relatively low, ranging from 0% to 6%. In contrast, close to two- thirds of the US and Canadian firms are unable to turn a profit in year – 1.

To gain further understanding of the profit differentials across countries, we present in Panels E and F, a decomposition of ROA into operating cash flows scaled by total assets and its complement, accruals scaled by total assets (accruals = income before ex-traordinary items−operating cash flows). The poor profitability of US and Canadian

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 120 27-Jul-18 10:11:09 PM

Table 5.4 Descriptive Statistics of Pre- IPO Financial Variables

Panel A: Sales (Millions of US$)

Means Medians No. of obs.

Year – 3 Year – 2 Year – 1 Year – 3 Year – 2 Year – 1 Year – 3 Year – 2 Year – 1

Australia 156.6 120.6 100.0 30.1 19.9 12.3 108 190 268

Canada 123.8 113.2 101.0 5.2 3.7 0.8 142 177 238

China 87.6 104.3 130.8 36.9 46.1 58.9 1,612 1,632 1,643

Germany 79.6 91.5 105.4 12.8 15.0 21.2 162 207 221

India 36.1 48.7 63.2 8.0 12.1 18.4 446 449 460

Japan 81.8 108.4 119.1 28.4 36.7 41.9 393 515 525

United Kingdom

55.6 53.9 55.8 3.0 3.1 3.5 257 304 353

United States 166.1 160.9 185.6 16.6 18.3 27.6 1,537 1,899 2,012

Panel B: Sales Growth

Means Medians No. of obs.

Year - 3 Year – 2 Year – 1 Year – 3 Year – 2 Year – 1 Year – 3 Year – 2 Year – 1

Australia 52% 40% 20% 24% 106 182

Canada 108% 86% 27% 41% 107 124

China 35% 29% 24% 21% 1,612 1,631

Germany 85% 64% 32% 31% 159 201

India 106% 105% 37% 31% 422 439

Japan 45% 49% 17% 18% 393 514

United Kingdom

90% 63% 22% 21% 235 272

United States 128% 169% 37% 44% 1,389 1,730

Panel C: Return on Assets = Income before Extraordinary Items Divided by Total Assets

Means Medians No. of obs.

Year – 3 Year – 2 Year – 1 Year – 3 Year – 2 Year – 1 Year – 3 Year – 2 Year – 1

Australia −10% −18% –31% −3% −4% 0% 4 29 221

Canada −60% −36% −24% −10% −3% −7% 52 174 234

China 14% 14% 14% 12% 13% 13% 1,599 1,619 1,642

Germany 11% −4% 0% 9% 3% 5% 27 206 219

India 6% 7% 8% 4% 5% 7% 441 449 459

Japan 6% 9% 10% 6% 7% 10% 397 517 524

United Kingdom

−22% −29% −24% 2% 2% 1% 255 301 351

United States −47% −50% −44% −10% −15% −14% 1,324 1,865 2,008

(Continued)

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 121 27-Jul-18 10:11:10 PM

Panel D: Loss Frequency

Means No. of obs.

Year – 3 Year – 2 Year – 1 Year – 3 Year – 2 Year – 1

Australia 17.0% 31.5% 44.9% 100 181 264

Canada 59.2% 55.1% 65.7% 142 178 238

China 0.2% 0.0% 0.0% 1,612 1,620 1,643

Germany 27.2% 29.0% 26.7% 162 207 221

India 11.2% 7.6% 5.9% 446 449 459

Japan 10.1% 8.7% 6.1% 397 517 526

United Kingdom

44.2% 44.1% 45.6% 258 304 353

United States 65.1% 66.3% 65.4% 1,529 1,893 2,010

Panel E: Operating Cash Flows/Assets

Means Medians No. of obs.

Year – 3 Year – 2 Year – 1 Year – 3 Year – 2 Year – 1 Year – 3 Year – 2 Year – 1

Australia −10% −8% −6% 0% 0% 6% 4 27 148

Canada −32% −23% −18% −6% −2% −5% 50 171 232

China 11% 13% 12% 10% 11% 11% 1,174 1,235 1,409

Germany 10% 2% 2% 11% 8% 8% 26 190 208

India 4% 3% 3% 4% 3% 5% 398 415 428

Japan 6% 9% 9% 7% 8% 9% 26 416 465

United Kingdom

−8% −14% −10% 6% 7% 7% 249 296 338

United States −30% −33% −24% −2% −5% −4% 1,270 1,847 1,999

Panel F: Accruals / Assets; Accruals = Income before Extraordinary Items minus Operating Cash Flows before Discontinued Operations

Means Medians No. of obs.

Year – 3 Year – 2 Year – 1 Year – 3 Year – 2 Year – 1 Year – 3 Year – 2 Year – 1

Australia −1% −8% −18% −2% −5% −5% 4 27 142

Canada −24% −13% −8% −7% −5% −5% 50 171 232

China 3% 2% 2% 3% 2% 2% 1,174 1,229 1,409

Germany 1% −7% −2% 0% −3% −2% 26 190 208

India 2% 3% 4% 1% 2% 2% 398 415 428

Japan 3% 0% 2% −1% 0% 1% 26 416 465

United Kingdom

−14% −13% −14% −6% −7% −7% 249 296 338

United States −18% −17% −18% −8% −8% −10% 1,270 1,845 1,997

Table 5.4 (Contd.)

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 122 27-Jul-18 10:11:10 PM

Panel G: Research & Development (R&D)/ Assets (When R&D is Non−Zero)

Means Medians No. of obs.

Year – 3 Year – 2 Year – 1 Year – 3 Year – 2 Year – 1 Year – 3 Year – 2 Year – 1

Australia 9% 8% 34% 9% 7% 22% 2 7 24

Canada 41% 34% 22% 18% 20% 16% 22 68 77

China 0 0 0

Germany 27% 15% 15% 10% 0 45 50

India 26% 18% 14% 2% 1% 1% 19 26 28

Japan 10% 28% 1% 2% 0 119 198

United Kingdom

30% 27% 30% 14% 14% 12% 64 78 81

United States 49% 48% 41% 27% 29% 26% 806 1,171 1,248

Panel H: Capital Expenditures / Assets

Means Medians No. of obs.

Year – 3 Year – 2 Year – 1 Year – 3 Year – 2 Year – 1 Year – 3 Year – 2 Year – 1

Australia 6% 7% 11% 2% 3% 4% 50 89 135

Canada 6% 11% 21% 3% 5% 11% 133 172 231

China 6% 7% 9% 5% 6% 8% 1,173 1,224 1,368

Germany 6% 9% 13% 3% 5% 8% 136 190 208

India 6% 8% 12% 3% 5% 8% 402 416 429

Japan 2% 4% 6% 2% 2% 3% 3 411 481

United Kingdom

6% 7% 9% 3% 3% 4% 250 297 339

United States 7% 8% 12% 3% 4% 7% 1,453 1,853 1,968

Panel I: Book Value of Equity (Millions of US$)

Means Medians No. of obs.

Year – 3 Year – 2 Year – 1 Year – 3 Year – 2 Year – 1 Year – 3 Year – 2 Year – 1

Australia 138.1 62.6 31.7 8.2 2.7 1.6 6 31 371

Canada 1.2 10.4 21.5 0.2 0.8 0.7 53 199 282

China 35.3 46.9 61.2 18.6 26.1 34.6 1,364 1,380 1,393

Germany 46.8 18.2 21.2 15.3 2.5 5.0 27 207 220

India 13.6 18.2 25.3 2.7 4.0 6.2 443 452 465

Japan 5.9 17.0 18.4 2.2 3.1 4.0 412 518 524

United Kingdom

10.3 6.6 5.7 0.3 0.5 0.6 266 310 433

United States 26.2 20.9 19.7 0.1 −0.1 −0.1 1,416 1,936 2,059

Table 5.4 (Contd.)

(Continued)

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 123 27-Jul-18 10:11:10 PM

124 Sanjai Bhagat, Jun Lu, and Srinivasan Rangan

firms holds up even with operating cash flows; median numbers are negative for all three years. The median IPO firm in the remaining six countries are generating posi-tive operating cash flows in all three years; however, only Japanese firms report a strictly monotonic trend.

Because accruals tend to be dominated by a large negative accrual— depreciation— we expect average pre- IPO accruals to be negative. Surprisingly, median accruals divided by assets are positive for all three years for China and India, ranging from 1% to 3%. The unusual nature of these positive accruals becomes more stark, when contrasted with the median accruals divided by assets for all US firms on COMPUSTAT for our sample period. This number is – 6%. While a portion of the pos-itive accruals can be attributed to high sales growth rates, the possibility that Chinese and Indian firms are managing their pre- IPO accruals upward remains. For the other six countries, median accruals scaled by assets are in general negative, as expected, and do not display any particular trend.

We also examine the investing patterns of IPO firms before they conduct their offerings. Panel G and H report averages for R&D deflated by assets, when R&D is non- zero, and capital expenditures deflated by assets. US and Canadian firms are the most R&D intensive, with R&D rates ranging from 26% to 29%— this partly explains the poor profitability of IPOs in these two countries. India and Japanese IPOs fall on the low end of the R&D investing spectrum, with R&D rates of only 1%– 2% of assets in the year before the IPO. With respect to median capital expenditure spending rates, Panel H indicates that IPO firms in all eight countries display an increasing trend over years – 3 to – 1.

Panel I and J report data on two balance sheet characteristics— book value of eq-uity (in millions of $) and long- term debt to assets ratio. Except for US firms that have a small negative median book value, IPO firms in general report a positive book

Panel J: Long- Term Debt by Total Assets (%)

Means Medians No. of obs.

Year - 3 Year - 2 Year - 1 Year - 3 Year - 2 Year - 1 Year - 3 Year - 2 Year - 1

Australia 11% 13% 8% 0% 2% 0% 6 30 369

Canada 13% 13% 11% 0% 1% 0% 34 153 230

China 7% 7% 7% 2% 3% 3% 1,551 1,575 1,581

Germany 11% 17% 17% 0% 9% 10% 27 204 217

India 26% 26% 26% 23% 23% 24% 441 451 465

Japan 23% 19% 17% 25% 14% 11% 6 503 515

United Kingdom

24% 20% 20% 4% 5% 3% 255 304 429

United States 20% 21% 23% 4% 6% 7% 849 1,816 1,981

Table 5.4 (Contd.)

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 124 27-Jul-18 10:11:10 PM

IPO Valuation: The International Evidence 125

value of equity. In terms of leverage, Indian firms have the highest levels, 24% in the year before the offering. The median German and Japanese firm funds about 10%– 11% of their assets with long- term debt. Pre- IPO leverage is relatively low for other countries.

Figures 5.3 through 5.9 illustrate some of the key descriptive statistics.

400

300

200

100

0Australia Canada China Germany India Japan UK US

Median Market Capitalization at Offer Price (Millions of US$)Median Offer Proceeds (Millions of US$)

Figure 5.3. Median IPO market capitalization, median IPO offer proceeds (US$ millions).

20

18

16

14

12

10

8

6

4

2

0Australia Canada China Germany India Japan UK US

Figure 5.4. IPO company median age (years).

Australia Canada China Germany India Japan UK US

70

60

50

40

30

20

10

0

Figure 5.5. Median sales of IPO companies during the past 12 months (US$ millions).

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 125 27-Jul-18 10:11:10 PM

Australia Canada China Germany India Japan UK US

70.00%

60.00%

50.00%

40.00%

30.00%

20.00%

10.00%

0.00%

Figure 5.7. Percentage of IPOs with an earnings loss during the past 12 months.

Australia Canada China Germany India Japan UK US

30%

25%

20%

15%

10%

5%

0%

Figure 5.8. Median R&D/ assets during the past 12 months (when R&D is non- zero).

Australia Canada China Germany India Japan UK US

50%45%40%35%30%25%20%15%10%5%0%

Figure 5.6. Median sales growth of IPO companies during the past 12 months.

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 126 27-Jul-18 10:11:10 PM

IPO Valuation: The International Evidence 127

5.4. IPO Valuation

5.4.1. Cross- Country Differences in Relation of Financial Variables to IPO Valuation

Our research objective is to examine the relation between IPO market valuations and financial variables and to document the existence and magnitude of cross- country differences in the same. To do so, we estimate a simple and parsimonious valuation model estimated for US mergers by Rhodes- Kropf, Robinson, and Viswanathan (2005; RRV hereafter). The model, which is an adaptation of the seminal work of Ohlson (1990), is specified for each country j as follows:

LOGMCAP BV LOGABSNI LOSSDUM LOGABSNI

Lj j j j j j j j

j

= + + ++

α α α αα

0 1 2 3

2

*EEVj j+ α (5.2)

where LOGMCAP is the log of market value of equity on the offer date, BV is the book value of common equity at the end of the year before the offering (year – 1), LOGABSNI is the log of the absolute value of income before extraordinary items in year – 1, LOSSDUM is a dummy variable that equals one when income before extraordinary items in year – 1 is negative and 0 otherwise, and LEV is the ratio of long- term debt to total assets as the end of year – 1.

We employ log values for market capitalization and absolute value of income be-fore extraordinary items considering the significant skewness in these variables. By interacting LOSSDUM and LOGABSNI, we allow for the valuation of income to differ based on its sign. We expect the coefficients of BV and ABSNI, α1 and α2, to be positive. Because loss firms tend to have income that is less persistent, we expect α3 to be negative. RRV interpret leverage as a proxy for cost of capital and expect that higher leverage will be associated with lower market values. Alternately, leverage can also be viewed a source of monitoring that could benefit shareholders (Jensen, 1989). Under this interpretation, the sign of the coefficient on leverage would be positive.

Australia Canada China Germany India Japan UK US

12%

10%

8%

6%

4%

2%

0%

Figure 5.9. Median capital expenditure/ assets during the past 12 months.

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 127 27-Jul-18 10:11:10 PM

128 Sanjai Bhagat, Jun Lu, and Srinivasan Rangan

We first estimate Eq. (5.1) for each country j, individually. Then, we estimate a global valuation model that combines data for all eight countries and allows us to test for differences in coefficients of value- drivers across countries. All variables, except dummy variables, are winsorized at the 1% and 99% levels. Standard errors are adjusted for heteroscedasticity and clustering across firms within each year. For the country- level models, financial variables are in local currencies; for the global valuation model, finan-cial data are expressed in US dollars.

Table 5.5, Panel A, presents the results for the RRV valuation model for IPOs in the eight countries. As expected, income before extraordinary items (LOGABSNI) is pos-itively related to IPO valuation in each of the eight countries. The economic impact of net income is largest for Chinese IPOs and smallest for Australian IPOs. Specifically, a 1% increase in net income in China is associated with a 0.82% increase in IPO valua-tion. A 1% increase in net income in Australia is associated with a mere 0.07% increase in IPO valuation. In contrast to income, book value of equity that reflects assets in place is valued significantly in only four countries: Canada, Germany, India, and the United States. We do not observe a significant relation between book value and IPO valuation for Australia, China, Japan, and the United Kingdom.

The interaction between the LOSS dummy and ABSNI measures the differential val-uation of loss firms and profitable firms. For IPOs in the United States, the valuation effect of income when it is negative is lower than when it is positive; the magnitude of this differential is, however, economically small with a coefficient of – 0.10 on the in-teraction. We find that LOSS times ABSNI and IPO value are negatively related for UK IPOs as well. However, Canadian and Japanese IPOs that have incurred a loss in earn-ings are associated with a higher valuation. We do not observe a statistically significant loss- versus- profit valuation differentials for Australia, Germany, and India. Because all Chinese firms report positive pre- IPO profits, the loss- profit interaction is not relevant for them.

The results in Panel A of Table 5.5 indicate that leverage’s effect on market capitaliza-tion varies across countries. The effect is positive and statistically significant in Canada, India, and the United Kingdom, consistent with the idea that debt provides monitoring benefits to shareholders. However, it is negative and significant in Japan, suggesting that Japanese investors interpret it as a proxy for cost of capital. Leverage is not significantly related to market values in Australia, China, Germany, and the United States.

Table 5.5, Panel B, highlights the results for the RRV valuation model augmented with investment, growth, and nonfinancial variables for the IPOs in the eight different coun-tries. The magnitudes and significance of the coefficients of the RRV model for China and Germany are similar to those reported in Panel A. While ABSNI loses statistical significance in Canada and Japan, BV becomes statistically and significantly related to market values in Australia and Japan. Further, BV is no longer significantly related to value for Canadian firms. In terms of the differential valuation of loss firms, the results change for UK firms alone; LOSS*ABSNI remains negatively related to market values, but is no longer statistically significant. Finally, leverage is no longer significantly related to market value for Canadian and Indian firms; interestingly, leverage is valued posi-tively by US investors under the augmented RRV model.

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 128 27-Jul-18 10:11:10 PM

Tabl

e 5.

5 Co

untr

y- Le

vel V

alua

tion

Regr

essi

ons

Pane

l A: R

hode

s- Kr

opf,

Robi

nson

, and

Vis

hwan

atha

n (2

005)

(RRV

) Mod

el

Aust

ralia

Cana

daCh

ina

Germ

any

Coef

.t-

stat

SLCo

ef.

t- st

atSL

Coef

.t-

stat

SLCo

ef.

t- st

atSL

Inte

rcep

t0.

1135

.18

*3.

8122

.51

*4.

1323

.23

*4.

5726

.32

*

BV0.

001.

000.

002

4.03

*0.

000.

960.

002

2.93

*

LOG

ABSN

I0.

075.

77*

0.47

4.37

*0.

8223

.60

*0.

263.

86*

LOSS

*LOG

ABSN

I0.

100.

270.

191.

89**

*0.

00- 0

.04

DTOA

0.32

−0.1

51.

003.

22*

−0.2

7−1

.06

0.05

0.11

Adju

sted

R2

47.4

%50

.9%

67.3

%29

.6%

No.

of o

bs.

218

185

1,38

121

7

Indi

aJa

pan

Unite

d Ki

ngdo

mUn

ited

Stat

es

Coef

.t-

stat

SLCo

ef.

t- st

atSL

Coef

.t-

stat

SLCo

ef.

t- st

atSL

Inte

rcep

t5.

0525

.92

*7.

3024

.06

*3.

4835

.64

*5.

0143

.36

*

BV0.

0004

7.27

*0.

001.

250.

000.

560.

004.

8*

LOG

ABSN

I0.

4710

.52

*0.

234.

26*

0.59

11.0

1*

0.41

12.0

8*

LOSS

*LOG

ABSN

I−0

.02

−0.3

30.

153.

39*

−0.1

6−2

.63

**−0

.10

−3.7

4*

DTOA

0.78

2.92

*−0

.54

−1.8

1**

*0.

453.

38*

0.03

0.29

Adju

sted

R2

75.4

%14

.0%

50.2

%31

.2%

No.

of o

bs.

459

515

345

1,92

5

Not

es: T

he d

epen

dent

var

iabl

e is

the

log

of m

arke

t cap

italiz

atio

n at

the

offe

r dat

e. S

L is

sign

ifica

nce

leve

l. * i

ndic

ates

sign

ifica

nce

at th

e 1%

leve

l, **

at t

he 5

% le

vel,

and

*** a

t the

10%

leve

l. St

anda

rd e

rror

s acc

ount

for c

lust

erin

g ac

ross

firm

s with

in a

yea

r. Va

riabl

e de

finiti

ons a

re in

App

endi

x 5.

1.

(Contin

ued)

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 129 27-Jul-18 10:11:10 PM

Pane

l B: R

RV M

odel

, Aug

men

ted

with

Inve

stm

ent,

Grow

th, N

onfin

anci

al V

aria

bles

Aust

ralia

Cana

daCh

ina

Ger

man

y

Coef

.t-

stat

SLCo

ef.

t- st

atSL

Coef

.t-

stat

SLCo

ef.

t- st

atSL

Inte

rcep

t2.

333.

21*

3.11

4.84

*1.

251.

301.

874.

48*

BV0.

001

5.39

*0.

000.

390.

00−0

.15

0.00

13.

24*

LOG

ABSN

I0.

524.

40*

−0.0

3−0

.27

0.71

22.5

9*

0.27

6.38

*

LOSS

*LOG

ABSN

I−0

.15

−1.1

90.

201.

84**

*−0

.07

−1.2

5

DTOA

−0.5

6−1

.71

0.31

0.71

0.11

0.71

0.25

1.08

LOG

_ CAP

EX0.

152.

40**

0.25

3.32

*0.

000.

170.

135.

11*

LOG

_ RD

0.01

0.27

0.00

0.06

0.04

1.83

***

LOG

_ SG

RO−0

.18

−0.6

10.

070.

270.

211.

570.

231.

65

LOG

_ IN

DPE

0.28

0.85

0.11

0.58

0.15

2.45

**

RETE

NTI

ON0.

450.

600.

080.

143.

325.

11*

1.39

5.45

*

UN

DREP

0.47

0.96

1.49

2.36

**0.

773.

16*

1.80

5.71

*

BIG

N_ A

UD

0.37

1.04

0.56

1.88

***

−0.0

6−0

.90

0.15

1.96

***

AGE

0.00

−1.1

50.

010.

76−0

.02

−1.7

5**

*0.

00−1

.31

Adju

sted

R2

69.2

%45

.7%

73.1

%65

.6%

No.

of o

bs.

6574

1,30

917

9

Tabl

e .5

.5 (

Cont

d.)

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 130 27-Jul-18 10:11:10 PM

LOG

ABSN

I0.

316.

11*

0.10

0.97

0.30

7.64

*0.

158.

63*

LOSS

*LOG

ABSN

I−0

.01

−0.11

0.16

3.07

**−0

.12

−1.3

7−0

.06

−3.7

9*

DTOA

0.13

0.50

−0.9

8−2

.55

**0.

502.

15**

0.25

4.83

*

LOG

_ CAP

EX0.

113.

97*

0.08

1.73

0.20

6.37

*0.

127.

86*

LOG

_ RD

−0.0

6−1

.52

0.03

0.93

0.03

1.21

0.00

0.25

LOG

_ SG

RO−0

.02

−0.2

90.

100.

760.

010.

060.

031.

80**

*

LOG

_ IN

DPE

0.16

2.30

**1.

014.

33*

0.12

0.64

−0.0

4−0

.30

RETE

NTI

ON1.

261.

79**

*1.

812.

72**

1.10

3.49

*2.

1410

.94

*

UN

DREP

1.93

6.59

*0.

571.

86**

*1.

759.

68*

2.24

12.2

8*

BIG

N_ A

UD

0.14

1.15

0.24

1.89

***

0.44

5.23

*0.

212.

70**

AGE

0.01

3.60

*0.

00−1

.54

0.00

−0.0

80.

000.

69

Adju

sted

R2

81.8

%29

.6%

68.4

%63

.9%

No.

of o

bs.

340

228

249

1,60

0

Not

es: T

he d

epen

dent

var

iabl

e is

the

log

of m

arke

t cap

italiz

atio

n at

the

offe

r dat

e. S

L is

sign

ifica

nce

leve

l. * i

ndic

ates

sign

ifica

nce

at th

e 1%

leve

l, **

at t

he 5

% le

vel,

and

*** a

t the

10%

leve

l. St

anda

rd e

rror

s acc

ount

for h

eter

osce

dast

icity

and

clu

ster

ing

acro

ss fi

rms w

ithin

a y

ear.

Varia

ble

defin

ition

s are

in A

ppen

dix

5.1.

Indi

aJa

pan

Uni

ted

King

dom

Uni

ted

Stat

es

Coef

.t-

stat

SLCo

ef.

t- st

atSL

Coef

.t-

stat

SLCo

ef.

t- st

atSL

Inte

rcep

t2.

958.

89*

2.55

3.64

*1.

452.

54**

1.95

4.85

*

BV0.

0002

4.33

*0.

0001

2.52

**0.

000.

050.

007.

85*

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 131 27-Jul-18 10:11:10 PM

132 Sanjai Bhagat, Jun Lu, and Srinivasan Rangan

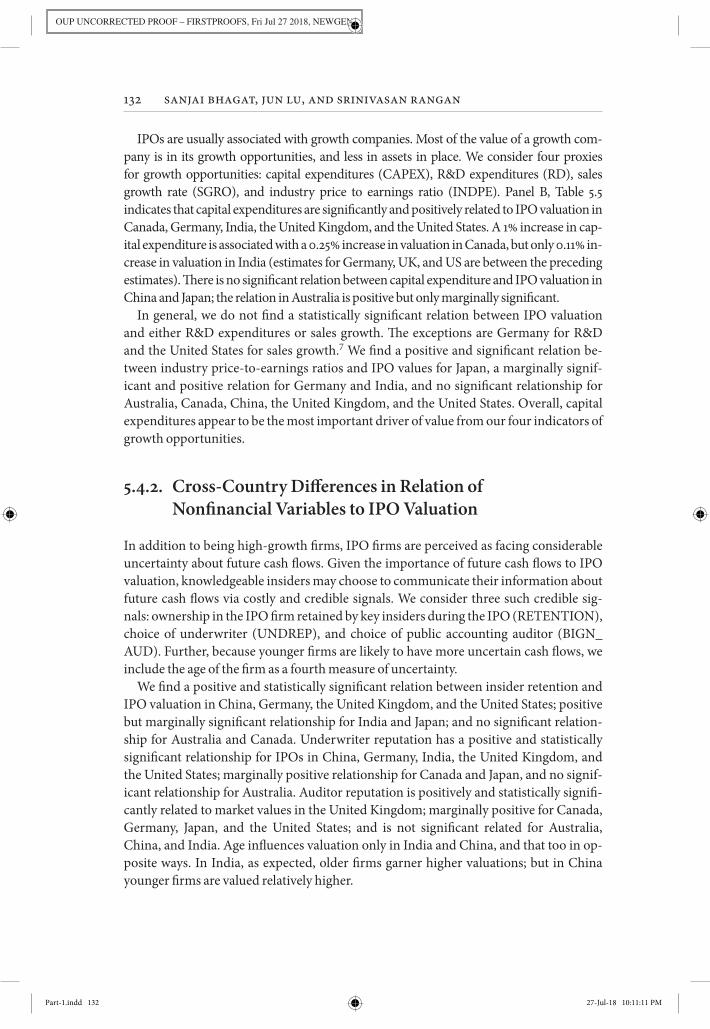

IPOs are usually associated with growth companies. Most of the value of a growth com-pany is in its growth opportunities, and less in assets in place. We consider four proxies for growth opportunities: capital expenditures (CAPEX), R&D expenditures (RD), sales growth rate (SGRO), and industry price to earnings ratio (INDPE). Panel B, Table 5.5 indicates that capital expenditures are significantly and positively related to IPO valuation in Canada, Germany, India, the United Kingdom, and the United States. A 1% increase in cap-ital expenditure is associated with a 0.25% increase in valuation in Canada, but only 0.11% in-crease in valuation in India (estimates for Germany, UK, and US are between the preceding estimates). There is no significant relation between capital expenditure and IPO valuation in China and Japan; the relation in Australia is positive but only marginally significant.

In general, we do not find a statistically significant relation between IPO valuation and either R&D expenditures or sales growth. The exceptions are Germany for R&D and the United States for sales growth.7 We find a positive and significant relation be-tween industry price- to- earnings ratios and IPO values for Japan, a marginally signif-icant and positive relation for Germany and India, and no significant relationship for Australia, Canada, China, the United Kingdom, and the United States. Overall, capital expenditures appear to be the most important driver of value from our four indicators of growth opportunities.

5.4.2. Cross- Country Differences in Relation of Nonfinancial Variables to IPO Valuation

In addition to being high- growth firms, IPO firms are perceived as facing considerable uncertainty about future cash flows. Given the importance of future cash flows to IPO valuation, knowledgeable insiders may choose to communicate their information about future cash flows via costly and credible signals. We consider three such credible sig-nals: ownership in the IPO firm retained by key insiders during the IPO (RETENTION), choice of underwriter (UNDREP), and choice of public accounting auditor (BIGN_ AUD). Further, because younger firms are likely to have more uncertain cash flows, we include the age of the firm as a fourth measure of uncertainty.

We find a positive and statistically significant relation between insider retention and IPO valuation in China, Germany, the United Kingdom, and the United States; positive but marginally significant relationship for India and Japan; and no significant relation-ship for Australia and Canada. Underwriter reputation has a positive and statistically significant relationship for IPOs in China, Germany, India, the United Kingdom, and the United States; marginally positive relationship for Canada and Japan, and no signif-icant relationship for Australia. Auditor reputation is positively and statistically signifi-cantly related to market values in the United Kingdom; marginally positive for Canada, Germany, Japan, and the United States; and is not significant related for Australia, China, and India. Age influences valuation only in India and China, and that too in op-posite ways. In India, as expected, older firms garner higher valuations; but in China younger firms are valued relatively higher.

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 132 27-Jul-18 10:11:11 PM

IPO Valuation: The International Evidence 133

In Table 5.6, we report the results of a global valuation model that combines data for all eight countries. We include all variables from the augmented RRV model except R&D and INDPE; we exclude these two variables to minimize sample size reduction because of missing data. To formally test for differences across countries in mean valuations as well as in the coefficients of the augmented RRV model, we include country dummies for seven countries and the interactions between these dummy variables and the variables in the augmented RRV model. In terms of estimation method, we report results based on ordinary least squares (OLS) as well as quantile regression. The latter is robust to the effect of outliers in the data; therefore, in our discussion, we emphasize results that are consistent across the two estimation methods.

Because we choose the United States as the base country, the coefficients on the main independent variables measure the effect of these variables on market values for US firms. The interaction term coefficients measure the country- level differences in valuation effects relative to US firms. Our first key finding is that, for US firms, the ef-fect of most of the independent variables are significant and in the expected direction. Absolute value of net income and book value of equity are positively related to market capitalization and loss firms’ net income are valued less. Leverage is valued positively consistent with a monitoring effect. Among the growth variables, capital expenditures alone are valued positively and significantly under both estimation methods. Market valuations are increasing in our three nonfinancial signals— insider retention, under-writer reputation, and auditor reputation.

Our second finding relates to the country- level dummies. Among the seven coun-tries, the dummy on China alone is negative and significant at the 1% level— after con-trolling for firm characteristics, Chinese firms alone are valued less than US firms. The cause for this difference is an interesting subject for future research.

Our third set of findings relate to the relative differences in the effect of various value- drivers between the United States and the other seven countries. We summarize these findings:

(1) The absolute value of net income of IPO firms in Australia, China, India, and the United Kingdom is valued more than that of US firms. Negative values of income are valued more for Canadian IPOs.

(2) The book value of equity of German and Japanese firms are valued more, whereas the book value of Chinese firms is valued less, relative to that of US firms.

The cross- country differences in the valuation could be attributed to the differences in financial reporting standards. For example, the accounting and finance literatures document that earnings opacity and financial reporting standards influence a range of capital market outcomes (Bhattacharya, Daouk, and Welker, 2003; Gelos and Wei, 2005; Jin and Myers, 2006). Difference in investor sophistication across countries could also drive these differences. For example, while US IPOs are largely bought by institutional investors, in India, retail investors have significant participation. More research that disentangles these alternate explanations is needed.

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 133 27-Jul-18 10:11:11 PM

Tabl

e 5.

6 Gl

obal

Val

uatio

n Re

gres

sion

s for

Inte

rnat

iona

l IPO

s (19

98– 2

015)

OLS

Qua

ntile

Reg

ress

ion

Varia

ble

Coef

.t-

stat

SLCo

ef.

t- st

atSL

Inte

rcep

t1.

868.

06*

1.77

12.9

7*

BV0.

005.

21*

0.00

6.55

*

LOG

ABSN

I0.

158.

50*

0.18

10.7

0*

LOSS

*LOG

ABSN

I−0

.07

−4.4

4*

−0.0

8−4

.71

*

DTOA

0.21

3.74

*0.

182.

94*

LOG

_ CAP

EX0.

137.

93*

0.14

12.6

7*

LOG

_ SG

RO0.

031.

80**

*0.

041.

53

RETE

NTI

ON2.

029.

70*

2.28

13.8

2*

AGE

0.00

1.27

0.00

2.03

**

UN

DREP

2.30

11.3

*2.

1517

.06

*

BIG

N_ A

UD

0.22

2.59

**0.

131.

95**

AUS

1.02

1.52

0.53

0.88

CAN

0.63

1.55

0.88

2.03

**

CHN

−1.0

5−2

.42

*−1

.16

−3.3

6*

GER

0.01

0.01

0.45

1.17

IND

−0.5

9−1

.15

−0.3

0−0

.92

JAP

0.18

0.21

0.78

1.39

UK

−0.5

8−1

.92

*−0

.51

−1.5

8

AUS*

LOG

ABSN

I0.

151.

76**

*0.

141.

83**

*

CAN

*LOG

ABSN

I−0

.02

−0.1

7−0

.07

−1.0

2

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 134 27-Jul-18 10:11:11 PM

CHN

*LOG

ABSN

I0.

5416

.68

*0.

5311

.59

*

GER

*LOG

ABSN

I0.

030.

62−0

.05

−1.1

5

IND*

LOG

ABSN

I0.

255.

29*

0.25

6.86

*

JAP*

LOG

ABSN

I−0

.12

−1.2

3−0

.07

−1.3

7

UK*

LOG

ABSN

I0.

173.

48*

0.19

4.19

*

AUS*

BV0.

000.

590.

000.

74

CAN

*BV

0.00

1.75

***

0.00

0.71

CHN

*BV

0.00

−6.1

9*

0.00

−3.6

4*

GER

*BV

0.00

3.33

*0.

002.

91*

IND*

BV0.

002.

26**

0.00

0.34

JAP*

BV0.

004.

77*

0.00

5.77

*

UK*

BV0.

00−0

.90.

00−1

.04

AUS*

LOSS

*LOG

ABSN

I0.

101.

210.

131.

29

CAN

*LOS

S*LO

GAB

SNI

0.22

2.27

**0.

303.

98*

GER

*LOS

S*LO

GAB

SNI

0.06

0.98

0.17

1.86

***

IND*

LOSS

*LOG

ABSN

I0.

101.

440.

111.

41

JAP*

LOSS

*LOG

ABSN

I0.

391.

70.

282.

37**

UK*

LOSS

*LOG

ABSN

I−0

.01

−0.2

10.

030.

49

AUS*

DTOA

−0.0

2−0

.04

0.34

0.77

CAN

*DTO

A0.

341.

20.

521.

84**

*

CHN

*DTO

A−0

.16

−0.8

9−0

.16

−0.6

2

GER

*DTO

A−0

.02

−0.1

30.

130.

40

IND*

DTOA

0.13

0.47

−0.0

6−0

.26

(Contin

ued)

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 135 27-Jul-18 10:11:11 PM

OLS

Qua

ntile

Reg

ress

ion

Varia

ble

Coef

.t-

stat

SLCo

ef.

t- st

atSL

JAP*

DTOA

−0.9

7−2

.04

*−0

.59

−1.6

8**

*

UK*

DTOA

0.28

1.5

0.45

2.68

*

AUS*

CAPE

X0.

071.

350.

040.

69

CAN

*CAP

EX0.

040.

750.

071.

29

CHN

*CAP

EX−0

.12

−5.8

1*

−0.1

2−5

.17

*

GER

*CAP

EX0.

020.

99−0

.02

−0.6

1

IND*

CAPE

X−0

.01

−0.4

2−0

.02

−0.7

6

JAP*

CAPE

X−0

.05

−1.1

4−0

.08

−2.2

2**

UK*

CAPE

X0.

061.

360.

030.

97

AUS*

SGRO

−0.2

8−1

.59

−0.2

9−1

.34

CAN

*SG

RO0.

070.

430.

130.

69

CHN

*SG

RO0.

150.

950.

171.

62

GER

*SG

RO0.

171.

530.

151.

14

IND*

SGRO

0.01

0.08

0.01

0.14

JAP*

SGRO

0.22

1.85

***

0.28

1.88

***

UK*

SGRO

−0.0

3−0

.26

−0.0

2−0

.20

AUS*

RETE

NTI

ON−1

.31

−2.1

6**

−1.1

9−2

.09

**

CAN

*RET

ENTI

ON−1

.64

−3.1

0*

−1.5

8−3

.93

*

CHN

*RET

ENTI

ON1.

702.

56**

1.58

3.28

*

GER

*RET

ENTI

ON−0

.26

−0.7

6−0

.75

−1.6

8**

*

IND*

RETE

NTI

ON−0

.88

−1.11

−1.0

6−2

.54

*

JAP*

RETE

NTI

ON−0

.65

−0.7

1−1

.55

−2.5

8*

Tabl

e 5.

6 (C

ontd

.)

OUP UNCORRECTED PROOF – FIRSTPROOFS, Fri Jul 27 2018, NEWGEN

Part-1.indd 136 27-Jul-18 10:11:11 PM

UK*

RETE

NTI

ON−0

.86

−2.9

8*

−1.2

8−3

.97

*

AUS*

AGE

0.00

−1.0

3−0

.01

−1.0

3

CAN

*AG

E0.

00−0

.13

0.01

0.76

CHN

*AG

E−0

.02

−1.7

3**

*−0

.02

−5.1

4*

GER

*AG

E−0

.01

−1.9

7**

*−0

.01

−1.4

4

IND*

AGE

0.00

0.60

0.00

−1.1

2

JAP*

AGE

−0.0

1−2

.76

*−0

.02

−4.8

4*

UK*

AGE

0.00

−0.0

70.

010.

79

AUS*

UN

DREP

−1.3

3−2

.87

*−0

.66

−1.2

0

CAN

*UN

DREP

−0.8

1−1

.87

***

−1.6

0−3

.44

*

CHN

*UN

DREP

−1.4

5−4

.23

*−1

.26

−6.4

6*

GER

*UN

DREP

−0.2

2−0

.59

−0.3

8−1

.04

IND*

UN

DREP

−0.3

8−1

.1−0

.37

−1.3

0

JAP*

UN

DREP

−1.6

0−4

.22

*−1

.71

−6.4

4*

UK*

UN

DREP

−0.5

2−1

.74

***

−0.2

6−0

.88

AUS*

BIG

N_ A

UD

0.10

0.34

0.13

0.56

CAN

*BIG

N_ A

UD

0.45

2.94

*0.

552.

71*

CHN

*BIG

N_ A

UD

−0.2

8−2

.14

**−0

.22

−1.4

8

GER

*BIG

N_ A

UD

−0.0

4−0

.43

−0.0

3−0

.22

IND*

BIG

N_ A

UD

−0.0

1−0

.04

0.02

0.15

JAP*

BIG

N_ A

UD

0.01

0.09

0.08

0.51

UK*

BIG

N_ A

UD

0.30

2.76

*0.

181.

38

Adju

sted

R2

/ Pse

udo

R280

.7%

56.4

%

No.

of o

bs.

4,22

14,

221

Not

es: T

he d

epen

dent

var

iabl

e is

the

log

of m

arke

t cap