PCD Impact Assessment on Food Security in Tanzania

82

PCD Impact Assessment on Food Security in Tanzania Assessing Linkages between OECD Policies and Tanzania’s Agro-Food Systems and Food Security Conditions Workshop 2, Dar Es Salaam, 27/11/2014 With support from the Ministry for Foreign Affairs of Finland Page 1 ECDPM

-

Upload

european-centre-for-development-policy-management-ecdpm -

Category

Presentations & Public Speaking

-

view

30 -

download

0

Transcript of PCD Impact Assessment on Food Security in Tanzania

PCD Impact Assessment on Food Security in Tanzania

Assessing Linkages between OECD Policies and Tanzania’s Agro-Food Systems and Food Security

Conditions

Workshop 2, Dar Es Salaam, 27/11/2014

With support from the Ministry for Foreign Affairs of Finland Page 1ECDPM

INTRODUCTION AND REMINDER

Page 2ECDPM

Policy Coherence for Development: Concepts

• Non-development cooperation policies of OECD countries (e.g., agriculture, trade, international investment, tax, science and technology, migration, etc.) can have (negative/positive) spillover effects on developing countries

• Those effects can be incoherent with development objectives (whether they are the objectives of a particular developing country, a region, developing countries as a whole, or the objectives of development cooperation policies of OECD countries)

• Different dimensions of development: economic growth, poverty reduction, food security, health, human development, environmental sustainability, etc.

Page 3ECDPM

OECD Member States Map

Source: Wikimedia CommonsPage 4ECDPM

Policy Coherence for Development: Concepts

• European Union: ‘The EU seeks to minimise contradictions and to build synergies between policies other than development cooperation that have an impact on developing countries, for the benefit of overseas development’

• OECD: ‘The pursuit of development objectives through the systematic promotion of mutually reinforcing policy actions on the part of both OECD and development countries’

• Two implications: “Do not harm”; “do good”– Ensure that all policies are “development-friendly”– Promote synergies among policies with regards to development

objectives

Page 5ECDPM

PCD Concept—Case of Food Security

Source: OECDPage 6ECDPM

PCD as a Policy and Institutional Mechanism

Source: OECD

Page 7ECDPM

PCD Impact Assessment Approaches

Ex ante Ex post

OECD-Policy-based

Country-/region-based X

Page 8ECDPM

Our PCD Impact Assessment Approach

• Developing a methodology for ex post, country-level PCD assessments with a focus on food security

• Involving local and OECD stakeholders (participatory approach)

• Supporting OECD Development Assistance Committee in improving PCD, fostering policy change and addressing trade-offs between domestic and international goals based on evidence

• Supporting developing country actors (governments, private sector and civil society) in understanding OECD policies’ impacts on their countries, advocating for improved PCD and formulating policy responses

Page 9ECDPM

Food Security Analysis Framework

• Food availability• Access to food• Food utilization• Stability

Page 10ECDPM

Page 11ECDPM

OECD-Tanzania Linkages

Commodity Tanzania’s net trade balance Primary linkage Secondary

linkageFood security factor(s)

Grains and riceSmall exporter/importer

Int’l markets Foreign direct investment

Availability and access (pr. & inc.)

Dairy products Importer Int’l markets - Availability and access (pr. & inc.)

Sugar Importer Int’l markets OECD Market access

Access (inc.) and utilization*

Coffee, tea, and tobacco Exporter OECD Market

access - Access (inc.)

Cotton Exporter Int’l markets OECD Market access Access (inc.)

Horticultural crops Exporter OECD Market

access - Access (inc.)

Fisheries Exporter OECD Market access - Access (inc.)

* Local development Page 12ECDPM

OECD-Tanzania Linkages

• Investigating changes in OECD policies and market outcomes over an adequate period of time and identifying negative/positive spillover effects

• Taking into account contextual changes (e.g., domestic/regional market and policy changes, global market and policy changes, etc.)

Page 13ECDPM

Objectives of Workshop 2

1. Providing an overview of OECD agricultural and trade policies and their spillover effects on international markets and domestic markets in developing/emerging countries and Sub-Saharan Africa

2. Assessing the impacts of OECD agricultural and trade policies in specific agro-food sub-sectors in Tanzania

3. Assessing the implications of OECD countries’ agro-food market regulations and private standards on Tanzanian exporters’ access to OECD markets

4. Assessing the influence of OECD policies on foreign direct investment and international businesses’ practices in Tanzania’s agricultural and food sectors

5. Soliciting views of stakeholders on ways and extent to which OECD policies affect the agro-food system and food security in Tanzania

6. Discussing methodological aspects

Page 14ECDPM

Q&A

• According to you, what does Policy Coherence for Development mean for Tanzania?

Page 15ECDPM

MODULE 3 PART 1

OECD domestic agricultural policies and spillover effects on Tanzania through international marketsOverview of OECD domestic agricultural

policies and spillover effects on international markets

Page 16ECDPM

Objectives

1/ Have a common understanding of the global context in which Tanzania operates

Þ Reality check on the recent evolutions globally and in Tanzania

2/ Present assumptions on theoretical impact pathways through international prices and evidence of their relevance in the litterature

Page 17ECDPM

Methodology

• So far desk-based research– Official data (OECD etc.)– Academic literarure and « grey » literature (reports)

• Limitations:– Limited up to date data– Publications on very specific commodities or

dimensions (2008 crisis)

=>Risk of using specific cases as general lessons

=> Your feedbacks are key

Page 18ECDPM

Initial assumptions: Impact of OECD policies through intl markets

Assumption 1: OECD policies act as discentives to produce food for Tanzanian farmers, lowering supply of locally produced food and income of farmers

Assumption 2: OECD policies act as barriers to trade (through tariffs) reducing the quantity exported to OECD markets by Tanzanian farmers, lowering their income

Page 19ECDPM

Assumption 1: discentives to supply of locally produced food

Channel 1:

=> depress price levels for Tanzanian farmers Through competition from low cost imports

Page 20ECDPM

Assumption 1: discentives to supply of locally produced food

Support policies and exports subsidies : increase supply on intl markets Þ depress intl pricesÞ Lower intl prices transmit to local pricesÞDepress farmers gates prices of import competing commodities

Farmers incomeNet food buyers

Page 21ECDPM

Assumption 1: discentives to supply of locally produced food

Channel 2:

=> increase price volatility which act as a discentive for farmers to invest in ag production

Page 22ECDPM

Assumption 1: discentives to supply of locally produced food

Temporary subsidized exports

Þ increase volatility of intl pricesÞ More volatile intl prices transmit to local prices

Þ Increase volatiliy of farmers gates prices of import competing commodities

Farmers incomeNet food buyers

Page 23ECDPM

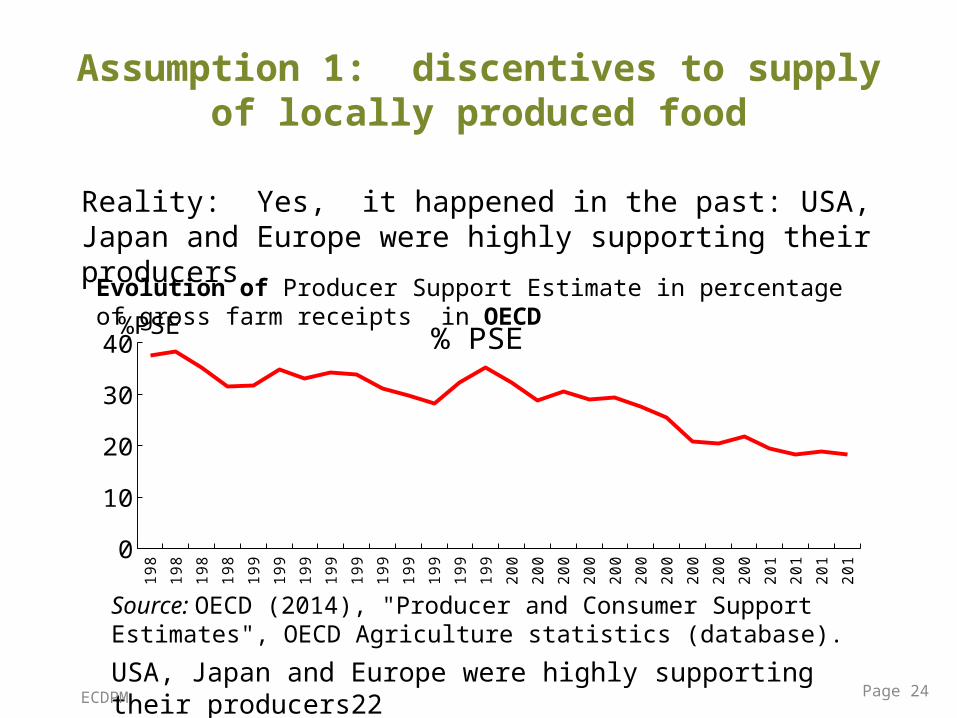

Assumption 1: discentives to supply of locally produced food

Reality: Yes, it happened in the past: USA, Japan and Europe were highly supporting their producers

19

8

19

8

19

8

19

8

19

9

19

9

19

9

19

9

19

9

19

9

19

9

19

9

19

9

19

9

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

0

20

1

20

1

20

1

20

1 0

10

20

30

40 % PSE %PSEEvolution of Producer Support Estimate in percentage of gross farm receipts in OECD

Source: OECD (2014), "Producer and Consumer Support Estimates", OECD Agriculture statistics (database).

USA, Japan and Europe were highly supporting their producers22

Page 24ECDPM

Assumption 1: discentives to supply of locally produced food

Reality: Yes, it happened in the past=> Those countries are considered to have contributed to the decrease in international price of grains, milk, butter, sugar, cotton

Page 25ECDPM

Assumption 1: discentives to supply of locally produced food

Yes, but

- has since become self sufficient in maize and rice

- local prices in Tanzania have been shown to be higher than intl markets prices more volatile

Þ Availability and accessibility problems of grains in Tanzania are due DOMESTIC factors and inefficiencies

lack of market integration within Tanzania and price transmission with intl

Globally

Tanzania

- Since then reduction of supports by OECD, increase in non OECD emerging economies (China, India)

- Since 2000s increase in international prices (3 spikes,:2008, 2010, 2011)

Page 26ECDPM

Assumption 1: discentives to supply of locally produced food

Yes, but

REALITY CHECK: Regarding international prices of grains, no case to accuse OECD policies of incoherence nowadays

ÞCoton USA ?

Page 27ECDPM

Assumption 2: Reduced market access for exporters

Channel 1 Barriers to entrance in the OECD markets - tariffs - non tariff measures

Page 28ECDPM

Assumption 2: Reduced market access for exporters

Tariffs

Þ decrease OECD demand of Tanzanian goods

Þ decrease income of export producing farmers

Farmers income

Page 29ECDPM

Assumption 2: Reduced market access for exporters

Channel 2 Increase of tariff with stage of processing in the value

chain (« tariff escalation ») => Disencentives to transform products locally and

capture higher share of value addition

Page 30ECDPM

Assumption 2: Reduced market access for exporters

Tariff escalation

Þ decrease OECD demand of Tanzanian processed ag productsÞ decrease income of export producing farmersÞDecrease employment creation in agroindustreis

Farmers incomeEmployment creation

Page 31ECDPM

Assumption 2: Reduced market access for exporters

Yes, historically agricultural products more protected than other types of products

But Tanzania has benefitted from preferences :

- Historically from the EU as an ACP country (Lomé, Cotonou etc.)-Since 2000s from preferential agreements from other OECD countries as a LDC (EBA from EU, AGOA from USA etc.)

-=> Many preferential agreements: question is what is also provided to competitors ?-=> Example of sugar. Page 32ECDPM

IMPACTS OF OECD POLICIES ON TANZANIA’S SECTOR

CASE OF SUGAR

Page 33ECDPM

Tanzanian Sugar Sector

• A major agro-food sector• Tanzania, a net importer of sugar• Four large sugar factories, some new projects

underway• Low sugar cane yields relatively to Southern

African producers and other Eastern African producers (lack of irrigation, low-performance varieties, low fertiliser use and other production and marketing factors)

• Privatization and efforts to rehabilitate the sector in the 1990s led to productivity enhancement and production increase

Page 34ECDPM

Sugar Production and Trade in Tanzania

Left axis, sugar cane production in tonnes; right axis, sugar production and trade in tonnes

Page 35ECDPM

Sugar Trade

• Tanzania exports sugar mostly to the EU under the EBA regime (10,000 tonnes, but export licenses are difficult to obtain reportedly)

• Import duties and quotas (licenses)• Large volumes of sugar imported illegally• Sugar factories have experience difficulty competing

with cheap sugar imports, notably sugar from Latin America, Southern Africa, and some Asian exporters

• Import surges/dumping cases in the late 1990s and early 2000s, incl. sugar from the EU among other origins

• Need to strengthen capacity to implement countervailing duties and other safeguard measures

Page 36ECDPM

Sugar Production and Trade in Tanzania

Left axis, sugar cane production in tonnes; right axis, sugar production and trade in tonnes

Page 37ECDPM

International Sugar Markets

• 2/3 of world sugar production from Brazil, Australia, Cuba and Thailand

• Other big producers: India, EU, and South Africa• Net exporting regions: Americas, Oceania• Net importing regions: Asia, Europe, Africa• Largest exporters: Brazil, EU, Australia, Cuba and Thailand• Largest importers: Russia, EU, and Japan• Concentrated sector; e.g., EU imports done by a few multi-

national companies• About ⅓ of world sugar production is trade internationally• Most of international trade in sugar is done under trade

agreements; residual trade thru spot markets; as a result (in addition to the fact that sugar cane is a perennial crop), this market is very volatile

Page 38ECDPM

International Sugar Markets

• Decline in international prices in the 1990s (rise of Brazil as a producer and an exporter), rise in prices in the 2000s; EU and US became net exporters after having been net importers (e.g., in the 1970s)

Page 39ECDPM

Sugar Production in OECD Group

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

0

2

4

6

8

10

12

0%

10%

20%

30%

40%

50%

60%

70%

80%

EU productions (LA) US productions (LA) Other OECD (LA)

US share (RA) EU share (RA) All OECD share (RA)

Pro

du

ctio

ns

(to

ns

)

Sh

are

in w

orl

d p

rod

uc

tion

s (

%)

Page 40ECDPM

Sugar Exports of OECD Group

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

0

2

4

6

8

10

12

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

EU exports (LA) US exports (LA) Other OECD exports (LA)

US share (RA) EU share (RA) All OECD share (RA)

Ex

po

rts

(to

ns

)

Sh

are

in w

orl

d e

xp

ort

s (

%)

Page 41ECDPM

Sugar Imports of OECD Group

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

0

2

4

6

8

10

12

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

EU imports (LA) US imports (LA) Other OECD imports (LA) US share (RA) EU share (RA)

All OECD share (RA)

Pro

du

ctio

ns

(to

ns

)

Sh

are

in w

orl

d im

po

rts

(%

)

Page 42ECDPM

International Sugar Markets

• Sugar trade regimes– EU’s preferential tariff and quota trade regimes:

• EU Special Preferential Sugar (SPS) arrangements, bilateral agreements with ACP countries, annual TRQ for raw cane sugar

• Sugar protocol of the EU-ACP Cotonou Partnership Agreement, TRQ with guaranteed prices

– US’ preferential tariff and quota regime (Puerto Rico, Philippines and other countries with whom the US has special trade relations—not for EA countries and excl. other low-cost producers)

– Commonwealth Sugar Agreement: TRQ for exports to UK until Lomé Agreement Sugar Protocol

• Other international agreements for sugar, incl. bilateral agreements (e.g., Cuba-Russia Sugar Agreement)

• WTO MFN regime (residual spot market)Page 43ECDPM

EU Sugar Policy

• Major reform of the sugar sector started in 2006– Cut in subsidies to farmers; cut in the target price of

white sugar; farmers compensated by decoupled payment for a 4-year period, additional to the single farm payment; abolition of the intervention price

– Closure of obsolete sugar mills– Losses for countries with preferential access to EU

market– Full liberalization of imports from LDCs in 2009 (duty-

free access to EU sugar market for 48 LDCs in 2009 under the EBA agreement signed in 2001)

• Elimination of production quotas after 2015; production will increase, prices will go down

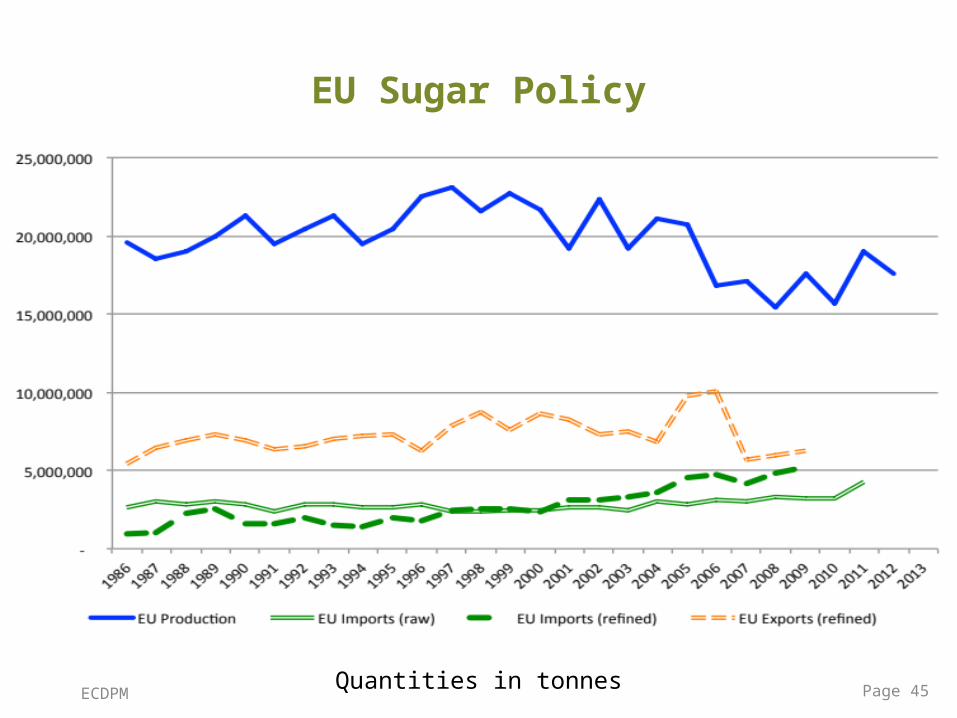

Page 44ECDPM

EU Sugar Policy

Quantities in tonnes Page 45ECDPM

Support to the Sugar Sector in OECD Group

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

0

10

20

30

40

50

60

70

80

SCT OECD (value LA) SCT EU (value LA) SCT US (value LA) SCT OECD (% RA) SCT EU (% RA) SCT US (% RA)

Page 46ECDPM

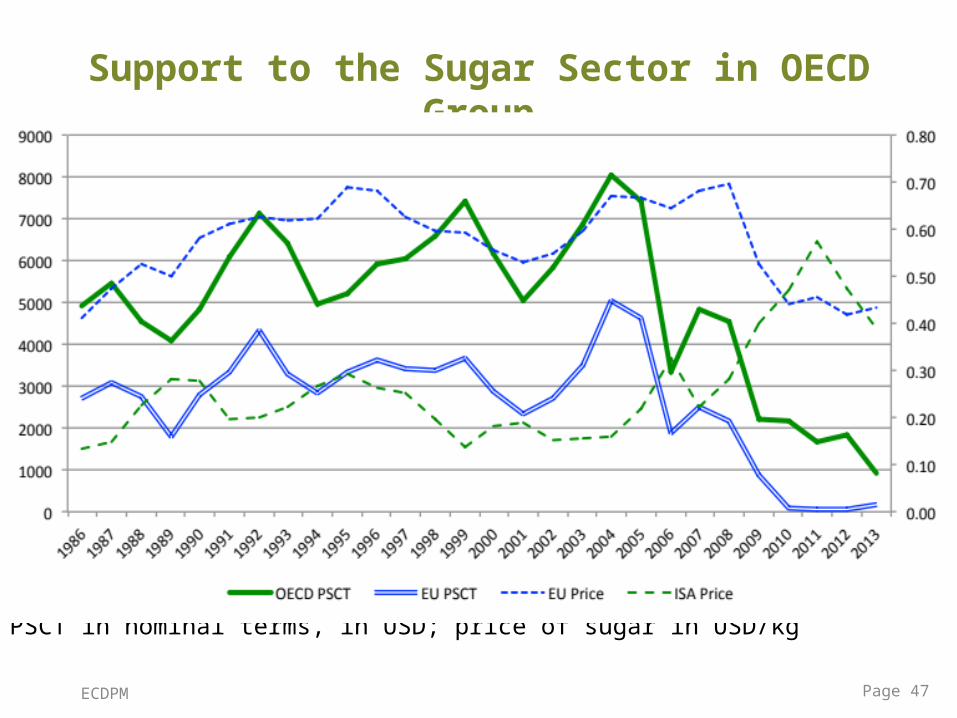

Support to the Sugar Sector in OECD Group

PSCT in nominal terms, in USD; price of sugar in USD/kg

Page 47ECDPM

Support to the Sugar Sector in OECD Group

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

0

10

20

30

40

50

60

70

80

0

100

200

300

400

500

600

700

800

900

SCT EU (% RA) SCT US (% RA) SCT OECD (% RA) EU price ($/ton LA) US price ($/ton LA)

World price ($/ton LA)

SC

T (

%)

Pri

ce

($

/to

n)

Page 48ECDPM

Sugar Markets in Africa

• Southern African producers more cost-competitive than Eastern and Central Africa producers– Malawi, Mauritius, Sudan, Zambia, Zimbabwe, South

Africa: low-cost sugar producers (SADC more competitive than EAC in general, production costs relatively high in Eastern Africa)

– Kenya, Swaziland, and Tanzania: higher-cost producers (indebted sugar companies in Kenya and Tanzania in early 2000s, late payments to farmers)

• Regional market protection in the EAC customs union; tariff protection; sensitive industry

• In the late 1990s, near collapse of the industry in the region (period of low prices, consumer prices at or below sugar production costs); after that, development of safeguard measures; due to lack of policy planning and administrative capacities, the regional industry is still affected by cases of dumping (as of 2006); low-cost imports from Brazil, Southern Africa and Australia

Page 49ECDPM

EU Development Assistance for the Sugar Sector

• Sugar Protocol Accompanying Measures introduced as part of the 2006 reform; assistance package for ACP countries; 40m euros

• ACP Sugar Research and Innovation Programme, to fund research to enhance sugar productivity, diversify uses of sugar cane (biofuels, bio-fertilisers, bio-polymers, etc.) and generally ensure that the sugar industry remains viable; about 20m US$, mostly from EU, also from Australia, US and ACP countries

Page 50ECDPM

Q&A

Page 51ECDPM

MODULE 3 PART 2

OECD non-tariff measures and private standards

Overview of OECD standards and implications for market access for Tanzania’s exports and food security conditions

Page 52ECDPM

ECDPM Page 53

Non-Tariff Measures in OECD and other countries

UNCTAD, 2010

“policy measures, other than ordinary customs tariffs, that can potentially have an economic effect on international trade in goods, changing quantities traded, or prices or both”

Non-Tariff Measures are :

• Most NTMs are governed by WTO laws and closely monitored• Members are ‘required’ to notify new and revised measure to

the WTO• TBT and SPS measures are by far the most important

ECDPM Page 54

Examples of NTMs measures in OECD countries

SPS TBT• Microbiological

standard

• Pesticide residue limits

• Contaminants in foodstuffs standards

• Veterinary drug residue limits

• Restrictions on antibiotic use in aquaculture

• Fumigation requirements

• Factory hygiene

• Quality attributes (size, shape, design, freshness, quality )

• Labeling requirements

• Packaging standards

• Traceability requirements for food and animal

• Health certificates

• Pest risk analysis requirements

• Import licensing and quota

• price control

• Bans/Restriction in Illegal Fishing

• Rule of Origin for manufactured products

Source: EU Helpdesk, 2014 and various other sources

Other NTMs

ECDPM Page 55

Increasing use of SPS and TBT19

95

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

0

2000

4000

6000

8000

10000

12000

EU (28) US Other OECD BRICS Other Countries

Figure 2: Cumulative number of SPS Notifications to the WTO

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

0

1000

2000

3000

4000

5000

6000

7000

8000

EU (28) US Other OECD BRICS Other Countries

Source: SPS and TBT notifications from the WTO Available at http://spsims.wto.org/web/pages/search/notification/regular/Search.aspx and at http://tbtims.wto.org/web/pages/search/notification/BasicSearch.aspx

Figure 3: Cumulative number of TBT Notifications to the WTO

• As of August 31st, 2014, a total of 10,945 SPS measures and 7,158 TBT measures has been notified to the WTO

• Reflect the increase in exports • But poses the question policy substitution in a context of

decreasing tariffs

ECDPM Page 56

Non-Tariff Measures by sectors

Table 1: Number of NTMs by economic sectors (all countries)

Source: Adapted from Gourdon and Nicita (2012)

• Food and agricultural products are the most affected

• Important implication of food security

ECDPM Page 57

Working definition proposed by China and New Zeeland to WTO

“are written requirements or set of written requirements of a non-governmental entity which are related to food safety, animal or plant life or health and for common and repeated use”

Private Voluntary Standards are :

Rising role of Private Voluntary Standards

ECDPM Page 58

Too many PVS ?

Source: Standardmap, ITC

More than 400 (UNCTAD and EU estimates)

ECDPM Page 59

Rising role of Private Voluntary Standards…

• Despite their voluntary nature, PVSs are ‘de facto’ mandatory for to access developed countries markets (Henson and Northen, 1998).

• PVSs versus Public Standards?• PVSs are used by retailers to establish and maintain

reputations, minimise monitoring and inspection costs due to public standards

• PVSs are more complex and stringent and are not necessarily being based on scientific evidences (Henson and Humphrey 2009).

• PVSs cover number of dimension (social, environment, equity, organic production, etc.) not covered by public standards

Increase regulation and standard

Þ Restrict OECD market access

Þ decrease income of export producing farmers

ÞDecrease employment creation in agroindustreis

Farmers incomeEmployment creation

Causal chain of the impact of standards on food security…

ECDPM Page 60

ECDPM Page 61

NTM for Traditional exports crops : Coffee, tea, tobacco and cotton

Coffee and tea• Microbiological

standard• Pesticide residue

limits• Quality attributes • Labelling and

Packaging standards

Tobacco• Prohibition of certain types of tobacco

• Restriction of certain substances (nicotine limit) in cigarette

• Labeling requirements

• Packaging standards

Cotton

• Pesticide residue limits in textile products

• Contaminants in feedstuffs

• Quality attributes

Several private standards, mostly social, sustainability and environmental : Fair Trade, Rainforest Alliance, UTZ certified, Ethical Trading Initiative

• Mostly exported raw will little or no value addition• Regulated sectors by commodity boards

Public sta

nd

ard

sPriv

ate

s sta

ndard

s

ECDPM Page 62

Example of Coffee

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

0%

20%

40%

60%

80%

100%

0

50

100

150

200

Export to OECD (LA) Export to EU (LA) Export to US (LA)Share to OECD (RA) Share to EU (RA) Share to US (RA)

Sh

are

(%

)E

xpo

rts

($U

S m

illio

n)

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

Total value and share of Tanzania export of coffee to OECD

Share of Tanzania in OECD total coffee import

Note : RA=Rigth Axis, LA = Left AxisSource : UNCOMTRADE 2014

ECDPM Page 63

Traditional exports crops access to OECD

• Standards are realities in traditional export crops• But, they are not major barrier to access OECD market

• Other factors are major constraints to the development of these sectors

• Domestics policies• Low value addition (but why?)• Lack infrastructures and low productivity

• Instead private certification offer the opportunity :• to expand trade and access niche markets (coffee and

tea) • earn ‘decent’ prices (fair trade)

• In the medium term, private standards could become majors challenges (carbon footprint, etc.)

ECDPM Page 64

NTM and Non-traditional exports crops Fish and horticulture

Fish• EU bans on lake

victoria fish• Microbiological

standards• Pesticide residue

limits• Quality attributes • Packaging

standards

Flower

• Plant material quarantine

• Phytosanitary certification

• Pest risk analysis• Fumigation

requirements

Fruit, vegetable and spices• Pesticide residue

limits• Contaminants in

foodstuffs• Quality attributes• Labeling

requirements• Packaging standards

Several private standards, food safety, social, sustainability and environmental : GlobalGap, BRC, Fair Trade

• Emerging sectors with large potential (horticulture)

• Important for export diversification

• Regulated sectors by boards and GoT

Public sta

nd

ard

sPriv

ate

s sta

ndard

s

ECDPM Page 65

Example of FishFigure 18: Total value and share of Tanzania export of fish to OECD Figure 19: Share of Tanzania in OECD total fish import

Note : RA=Rigth Axis, LA = Left AxisSource : UNCOMTRADE 2014

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

0%20%40%60%80%100%

0

50

100

150

200

Export to OECD (LA) Export to EU (LA) Export to US (LA)Share to OECD (RA) Share to EU (RA) Share to US (RA)

Sh

are

(%

)

Exp

orts

($U

S m

il-lio

n)

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

0.0%

0.1%

0.2%

0.3%

0.4% Share of Tanzania in OECD total fish import

Total value and share of Tanzania export of fish to OECD

ECDPM Page 66

Note : RA=Rigth Axis, LA = Left AxisSource : UNCOMTRADE 2014

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

0%

20%

40%

60%

80%

100%

0

5

10

15

Export to OECD (LA) Export to EU (LA) Export to US (LA)Share to OECD (RA) Share to EU (RA) Share to US (RA)

Sh

are

(%

)E

xpo

rts

($U

S m

illio

n)

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

0.0%

0.1%

0.1%

Total value and share of Tanzania export of vegetables to OECD

Share of Tanzania in OECD total vegetables import

Example of Vegetables

ECDPM Page 67

• Non-traditional sectors face high public and private standards

• They are major barriers to market access, especially by small producers and exporters

• Limit the (rapid?) expansion of these sectors (horticulture)

• Other factors are also constraints to the development of these sectors

• Domestics policies (slow but increasing support to these sectors-horticulture)

• Lack infrastructures (cold storage, high transport cost, etc.) and low productivity

• Certification offers access to OECD market but requires high cost

• Small farmers are locked out of export market

Non-traditional exports crops access to OECD

Summary

ECDPM Page 68

Technical assistances to Developing countries

The SPS agreement mentions, “members shall take account of the special needs of developing country Members, and in particular of the least-developed country Members” (Article 10.1).

Example of initiative

• WTO/FAO Standards and Trade Development Facility• Support to Horticulture Development Council of

Tanzania • EU /COLEACP Pesticide Initiative Program (PIP)

• 11 producing/exporting companies/farmers’ groups supported in Tanzania

• Many programs/project from other partners

These supports are essential to ensure the compliance of smallholldersBut what about the million of non-beneficiary smallholders?

Q&A

MODULE 3 PART 3

Foreign direct investment and land acquisition

Overview of FDI and implication for food security in Tanzania

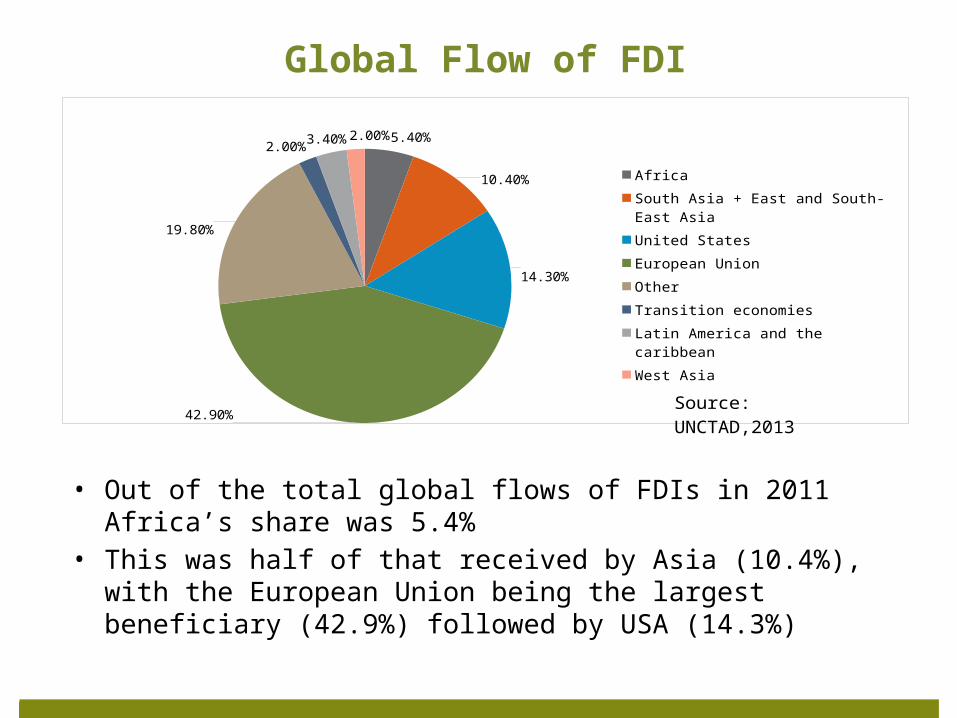

• Out of the total global flows of FDIs in 2011 Africa’s share was 5.4%• This was half of that received by Asia (10.4%), with the European

Union being the largest beneficiary (42.9%) followed by USA (14.3%)

Global Flow of FDI

5.40%10.40%

14.30%

42.90%

19.80%

2.00% 3.40% 2.00%

Africa

South Asia + East and South-East Asia

United States

European Union

Other

Transition economies

Latin America and the caribbean

West Asia

Source: UNCTAD,2013

• financial and banking services (16.8%) taking the lead, • real estate development (15.4%), • primary mining (10.1%) • electricity, gas and water (8.8%), and • motor vehicle assembly (8.7%)

Globally, Agriculture is among the least sectors attracting FDI

Other Services; 26.8

Finance; 16.8

Real Estate; 15.4

Construction; 2.6

Electricty,Gas+water; 8.8

Primary Mining; 10.1

Coke&Petroleum; 4.7

M-Vehicles; 8.7Manufacturing (others); 6.2

FDI, % by Sector/Industry

Source: UNCTAD,2013

• Generally, the pace of land acquisition globally has been increasing• After an inventory of the media reports on GRAIN blog (farmlandgrab.org),

the World Bank (Deininger et al. 2011) reports that between 2008-2009 there have been land acquisitions for 56.6 million hectares worldwide

Global Pace of Land Acquisition

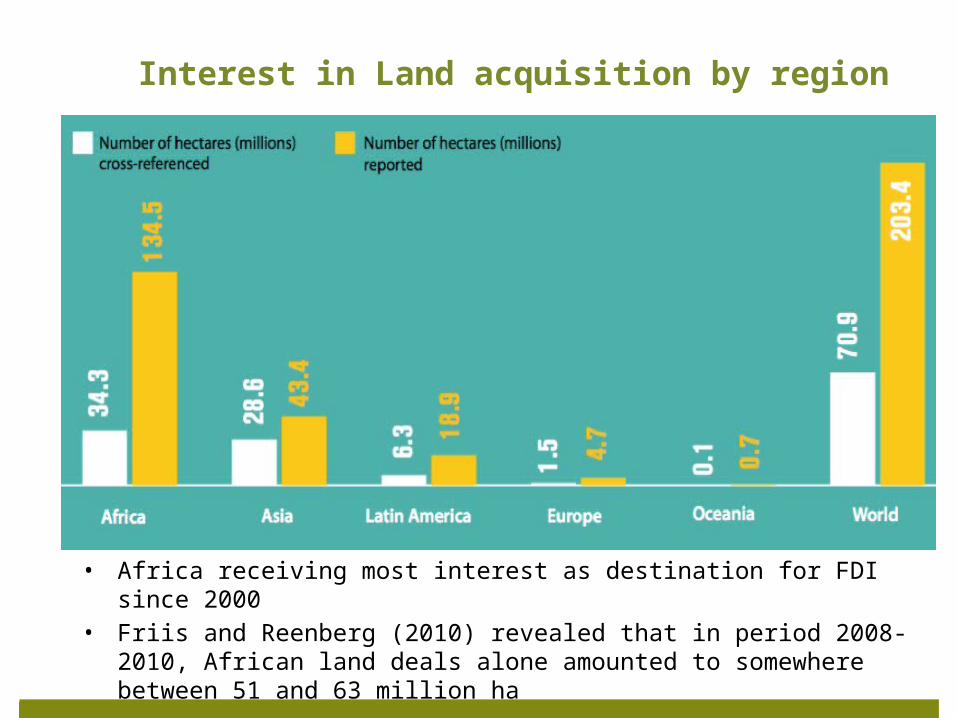

• Africa receiving most interest as destination for FDI since 2000• Friis and Reenberg (2010) revealed that in period 2008-2010,

African land deals alone amounted to somewhere between 51 and 63 million ha

Interest in Land acquisition by region

• Structural reforms and investment promotion facilities and strategies contributed increase in FDI inflow in last decade

• Mining & quarrying, manufacturing, wholesale & retail, accommodation share the largest share while agriculture sector attracted 4 percent of FDI stock

• Despite low FDI stock in agriculture sector, Land acquisition has been associated with agriculture FDI in the recent years for production of biofuel crops

Mining&Quarrying28%

Manufacturing21%

Wholesale,Retail Trade.

Catering&Accommodation Services

15%Agriculture, Hunting & Forestry

4%

Finance Insurance, Retail

Estate&Business Services

12%

Construction5%

Transport, Storage& Communication

7%

Others1%

Community, Social & Personal Services

0%

Electricity, Gas & Water6%

FDI inflow in Tanzania

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 -

200,000,000

400,000,000

600,000,000

800,000,000

1,000,000,000

1,200,000,000

1,400,000,000

1,600,000,000

1,800,000,000

2,000,000,000

0

1

2

3

4

5

6

7

8

9

Inflow FDI inflow/GDP

FDI i

nflow

(USD

)

FD

I/G

DP

(%)

• Weak regulatory enforcement in land ownership and resource poor small holder farmers are at risk of losing livelihoods and food production land due to random sale of their land assets

• More than 4 million hectares of land are in the hand of large investors

• Local medium and small investors in agricultural land is rising but few land is optimally used

Land acquisitions

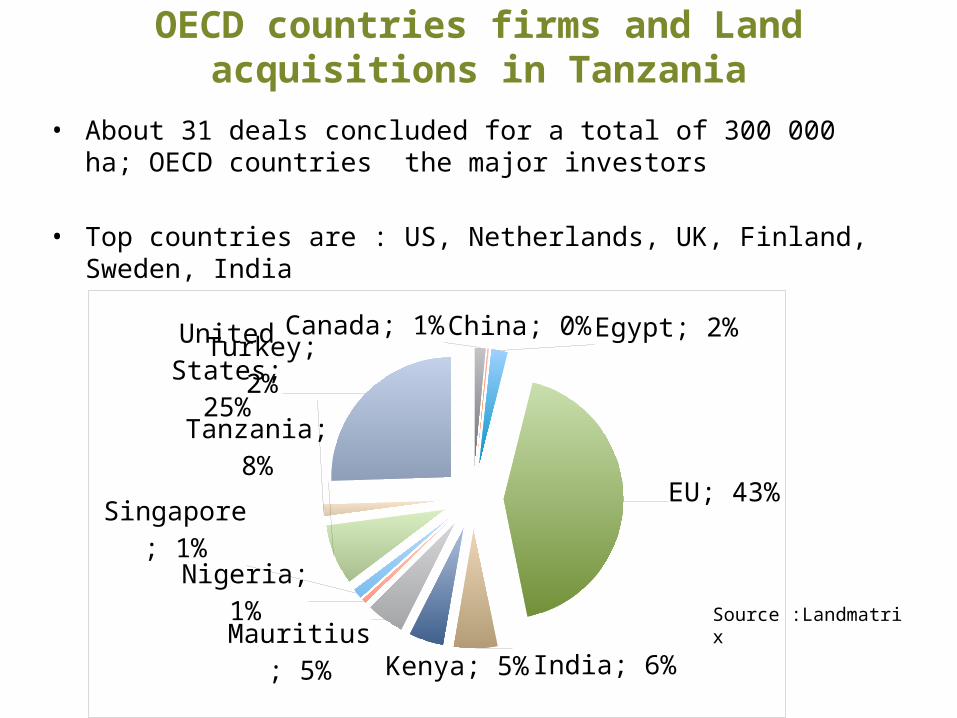

• About 31 deals concluded for a total of 300 000 ha; OECD countries the major investors

• Top countries are : US, Netherlands, UK, Finland, Sweden, India

OECD countries firms and Land acquisitions in Tanzania

Canada; 1% China; 0% Egypt; 2%

EU; 43%

India; 6%Kenya; 5%Mauritius;

5%

Nigeria; 1%

Singa-pore; 1%

Tanzania; 8%

Turkey; 2%

United States;

25%

Source :Landmatrix

What is produced?

Biofuels, 56%

Food crops, 24%

Other, 20%

• Food crops : Maize, Rice, Barley, horticulture• Biofuel : Jatropha, Oil palm, Sugar cane• Other : Carbon sequestration

Source :Landmatrix

What are links with OECD policies

• EU and US biofuel policies?

• Implication of land acquisition for local economy and food security?

• OECD/EU code for responsible investment in Agricultures

What are the impacts to:

• Livelihoods of local communities

• Food security

• Agriculture production

Q&A

ECDPM Page 81

Thank youwww.ecdpm.org

www.slideshare.net/ecdpm

Page 82