ระบบเตรียมข้อมูล Payroll · Payroll และ การมอบอํานาจ ระบบเตรียมข้อมูล Payroll 1.งด.6

PAYROLL ACCOUNTING 2014

Bernard J. Bieg and Judith A. Toland

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license

distributed with a certain product or service or otherwise on a password-protected website for classroom use.

SOCIAL SECURITY TAXES

Chapter 3

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

Learning Objectives

1. Identify which persons are covered under social security law

2. Identify types of compensation that are defined as wages

3. Apply current tax rates and wage base for FICA/SECA purposes

4. Describe different requirements/procedures for depositing FICA/FIT taxes

5. Complete Form 941 © 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

Coverage under FICA

FICA (1935)

◦ Federal Insurance Contributions Act

◦ Tax paid both by employees and employers

◦ 6.2% employer OASDI plus 1.45% HI

◦ 6.2% employee OASDI plus 1.45% HI

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-1

Coverage under FICA (cont.)

SECA (1951)

◦ Self-Employment Contributions Act

◦ Tax upon net earnings of self-employed

◦ (6.2% + 6.2%) = 12.4% OASDI plus (1.45% +

1.45%) = 2.9% HI

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-1

Coverage under FICA (cont.)

3 issues

◦ Are you an employee or an independent

contractor?

◦ Is service rendered considered employment?

◦ Is compensation considered taxable wages?

◦ http://www.socialsecurity.gov/employer

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-1

Independent Contractor (SECA)

vs. Employee (FICA) ◦ Every person is an employer if “person

employs one or more individuals for

performance of services in U.S.”

“Person includes trusts, estates, individual,

partnership or corporation”

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-1

Independent Contractor (SECA)

vs. Employee (FICA) (cont.) ◦ Certain occupations specifically covered by

FICA

Full-time life insurance salespersons

Agent- and commission-drivers of food/beverages

or dry cleaning

Full-time traveling salespersons

Individual working at home on products that

employer supplies and are returned to furnished

specifications

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-1

Independent Contractor (SECA)

vs. Employee (FICA) (cont.) ◦ If employer misclassifies employees, there is a

penalty

Generally equal to employer’s share of FICA plus

income taxes/FICA that were not withheld from

employees’ earnings

However, if employee reported earnings on 1040,

penalty is voided

Penalty may be reduced if employer filed a 1099

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-1

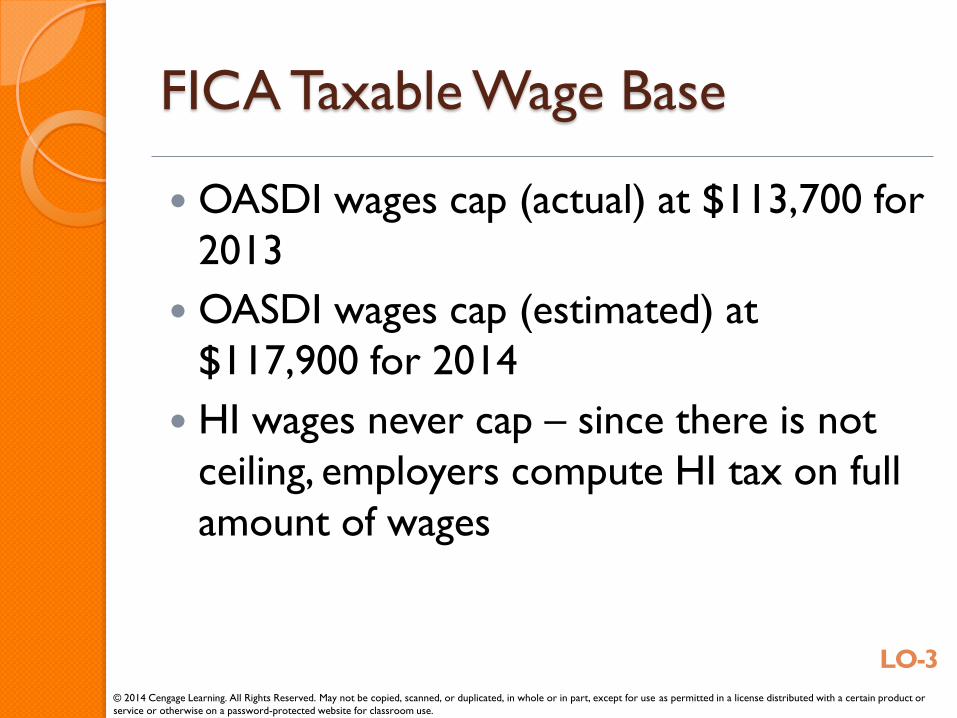

FICA Taxable Wage Base

OASDI wages cap (actual) at $113,700 for

2013

OASDI wages cap (estimated) at

$117,900 for 2014

HI wages never cap – since there is not

ceiling, employers compute HI tax on full

amount of wages

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-3

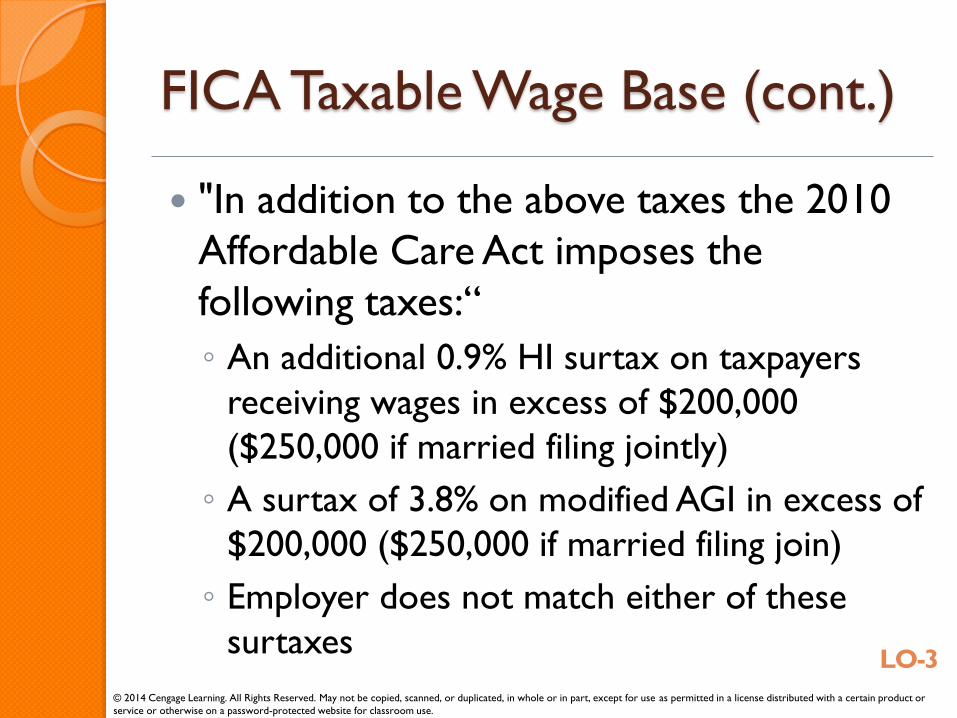

FICA Taxable Wage Base (cont.)

"In addition to the above taxes the 2010

Affordable Care Act imposes the

following taxes:“

◦ An additional 0.9% HI surtax on taxpayers

receiving wages in excess of $200,000

($250,000 if married filing jointly)

◦ A surtax of 3.8% on modified AGI in excess of

$200,000 ($250,000 if married filing join)

◦ Employer does not match either of these

surtaxes

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-3

FICA Taxable Wage Base (cont.)

Interesting note: In 1950 there were 16

workers paying into Social Security for

every one person collecting benefits.

By 2042, that ratio is projected to be 2 to

1.

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-3

Calculating FICA

Facts: Tamara earns $138,000/year and is

paid semimonthly on the15th and 30th;

determine FICA for October 30th payroll

◦ First must find prior payroll year-to-date gross

$138,000/24 =$ 5,750.00

◦ Hint: how many payrolls were run before the

10/30 payroll? Multiply that by the gross per

payroll:

$5,750.00 x 19 payrolls (before today)=

$109,250.00

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-3

Calculating FICA (cont.)

◦ How much will be taxed for OASDI?

$113,700– $109,250.00 = $4,450

Tamara’s OASDI tax is $4,450 x 6.2% = $275.90

Employer’s OASDI tax is $4,450 x 6.2% = $275.90

Both Tamara’s and the employer’s HI tax is

$5,750.00 x 1.45% =$ 83.38

◦ How much is total FICA?

Total FICA for Tamara is $275.90 + $83.38 =

$359.28

Total FICA for employer is $275.90 + $83.38

=$359.28

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-3

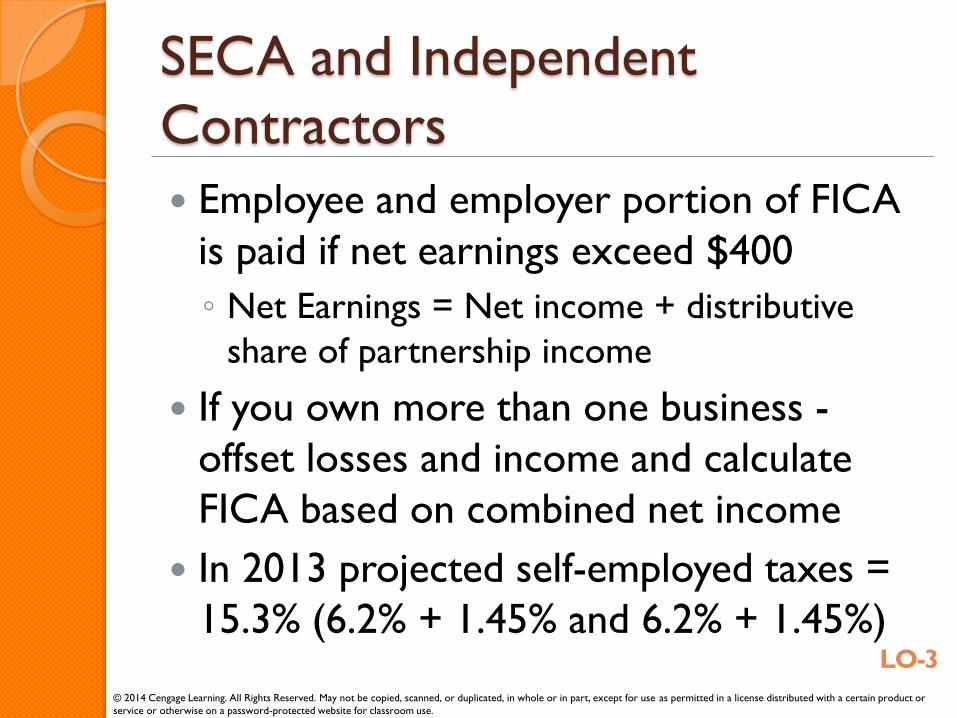

SECA and Independent

Contractors

Employee and employer portion of FICA

is paid if net earnings exceed $400

◦ Net Earnings = Net income + distributive

share of partnership income

If you own more than one business -

offset losses and income and calculate

FICA based on combined net income

In 2013 projected self-employed taxes =

15.3% (6.2% + 1.45% and 6.2% + 1.45%)

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-3

SECA and Independent

Contractors (cont.)

Can have W-2 and self employment

income

◦ Count both towards calculating cap of

$113,700 for OASDI

Report on Schedule C (Form 1040)

“Profit or Loss from Business”

Also file Schedule SE (Form 1040) “Self-

Employment Tax”

◦ Must include SECA taxes in quarterly

estimated payments

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-3

Calculating FICA with W-2 and

Self-Employed Earnings ◦ Facts: Celia’s W-2 = $117,768 and her self-

employment income = $14,500; how much is

her FICA on $14,500?

No OASDI is due because Celia capped on W-2

HI = $14,500 x 2.9% = $420.50

Total FICA is therefore = $420.50

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-3

Depositing FIT & FICA

FICA & FIT always deposited together

Each November, IRS notifies ER whether

they will be a monthly or semiweekly

depositor for next calendar year

(“lookback period”)

◦ Monthly - pay FICA and FIT by 15th of

following month

◦ Semiweekly – if payday is W, Th or F then due

following W and if payday is S, S, M or T then

due following F © 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-4

Depositing FIT & FICA (cont.)

◦ However, there is an exception: One-day rule

states that if $100,000 or more of federal

payroll tax liability is due, taxpayer has until

close of next banking day

◦ New employers are monthly depositors

unless $100,000+ of liability triggers one-day

rule and converts them to semiweekly

◦ Different requirements for agricultural and

household employees

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-4

How to Deposit FIT

and FICA Electronically

Old paper-based system has been

replaced by an electronic depositing

system

Most employers are now on EFTPS

(Electronic Federal Tax Payment System) -

only exception is for businesses owing

$2,500 or loss in quarterly tax liabilities

◦ Enroll in EFTPS Online at

http://www.eftps.gov

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-4

How to Deposit FIT

and FICA Electronically (cont.) ◦ All new employers automatically pre-enrolled

◦ Two methods:

EFTPS (direct) – withdraw funds from employer’s

bank account and route to Treasury

EFTPS (through financial institution) – employer

instructs his/her bank to send payment directly to

Treasury

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-4

How to Report and Reconcile

FIT/FICA

File Form 941 (Employer’s Quarterly

Federal Tax Return)

◦ Download at www.irs.gov/formspubs/ or call

1-800-829-3676

Due on last day of month following close

of quarter

◦ January 31, April 30, July 30, October 31

◦ If that falls on weekend or legal holiday, file

next business day

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-5

How to Report and Reconcile

FIT/FICA (cont.) Make deposit with Form 941 if taxes for

quarter are less than $2,500 ◦ Use 941-V when making payment or can pay by

credit card

Electronic filing options available for employers who meet requirements ◦ Complete an e-file application and then

electronically submit 941 or apply for a PIN on IRS website and file electronically through third-party transmitter

◦ Can correct errors on previously filed Form 941 by filing Form 941-X

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-5

Types of Penalties

Failure-to-comply penalties will be added

to tax and interest charges; negligence can

also result in fines/imprisonment

◦ Interest set quarterly, based on short-term

Treasury bill rate

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-5

Types of Penalties (cont.)

Penalties imposed for following:

◦ Not filing employment tax returns on time

◦ Not paying full taxes when due

◦ Not making timely deposits

◦ Not furnishing W-2s to employees on timely

basis

◦ Not filing information returns with IRS on

time

◦ Not supplying identification numbers

◦ Writing bad checks © 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-5

Types of Penalties (cont.)

Note: IRS reports that 100,000 businesses owe

more than two years of payroll taxes (estimated

at $58 billion)!!

© 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

LO-5