Payment methods on the internet 1.Credit cards. 2.Debit cards. 3.ACH transfers (ACH – Automated...

25

Payment methods on the internet 1. Credit cards. 2. Debit cards. 3. ACH transfers (ACH – Automated Clearing House). 4. Foreign and Cross-Border Payments. 5. Mobile Payments.

-

Upload

frederica-woods -

Category

Documents

-

view

220 -

download

2

Transcript of Payment methods on the internet 1.Credit cards. 2.Debit cards. 3.ACH transfers (ACH – Automated...

Payment methods on the internet

1. Credit cards.

2. Debit cards.

3. ACH transfers (ACH – Automated Clearing House).

4. Foreign and Cross-Border Payments.

5. Mobile Payments.

Credit cards

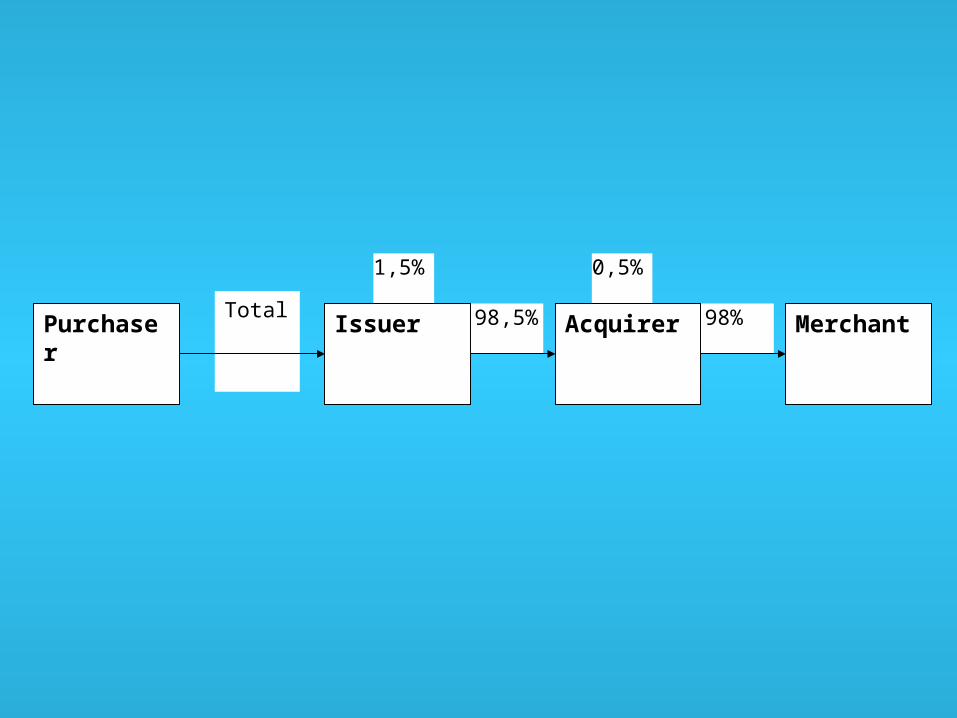

Credit-card transactions generally involve four participants:

1. Purchaser – who holds a credit card.2. Issuer – that issues the credit card.3. Merchant.4. Acquirer – that collects payment for the

merchant. (the acquirer is so named because it “acquires” the transaction from the merchant and then processes it to obtain payment from the issuer)

Issuer and acquirer could be the same person

The relationship between the card-holder and the card issuer

• The issue commits to pay for purchases made with credit card.

• Cardholder promise to reimburse the issuer over time.

That relationship is exactly the opposite of the common cheking relationship

The merchant have to pay an amount of the transaction, which

based on:• The type of transaction (the fee is

higher for transactions in which a card isnot swiped);

• network (American Express and Discover charge

more than Visa and MasterCard);• The characteristics of the merchant

(high-volume and creditworthy merchants pay less)

This fee aprox. 1-3 percent.

0,5%

98,5% 98%

1,5%

TotalPurchaser Issuer Acquirer Merchant

Features of credit cards

• The consumer have a right to cancel a payment (on the basis of any defense that the cardholder could assert against the original merchant)

• Protection for error in credit-card transaction (the merchant failed to deliver the goods and services)

• Protection against unauthorised charges

Truth-in-Lending Act (USA)

Problems

• Fraud

• Privacy

• Micropayments

Credit cards on the internet

• Enter credit card number, vaalidity, nema and surname (3 digit card verification code) on the merchant web-page

• Identification by PIN code

• “Smart” card or “chip” cards

• “Biometric” identification

Apsisaugojimas nuo sukčiavimo kreditinėmis kortelėmis

• “Hot list”• Sophisticated analysis of transaction information

to identify transactions that match profiles of fraudulent behavior

• Geolocation technology, which examines the ISP through which the purchaser is connecting (to assess the likelihood that the purchaser would be contacting the merchant from that location)

• digit card verification code

MasterCard „SecureCode“ programa

Privacy

• The interlopers will steal data from internet merchants

• The merchants and issuers themselves will make use of data for reasons that trouble consumers

The sofware response in the form of disposable credit-card numbers that inhibit the aggregation of payment information (Orbiscom)

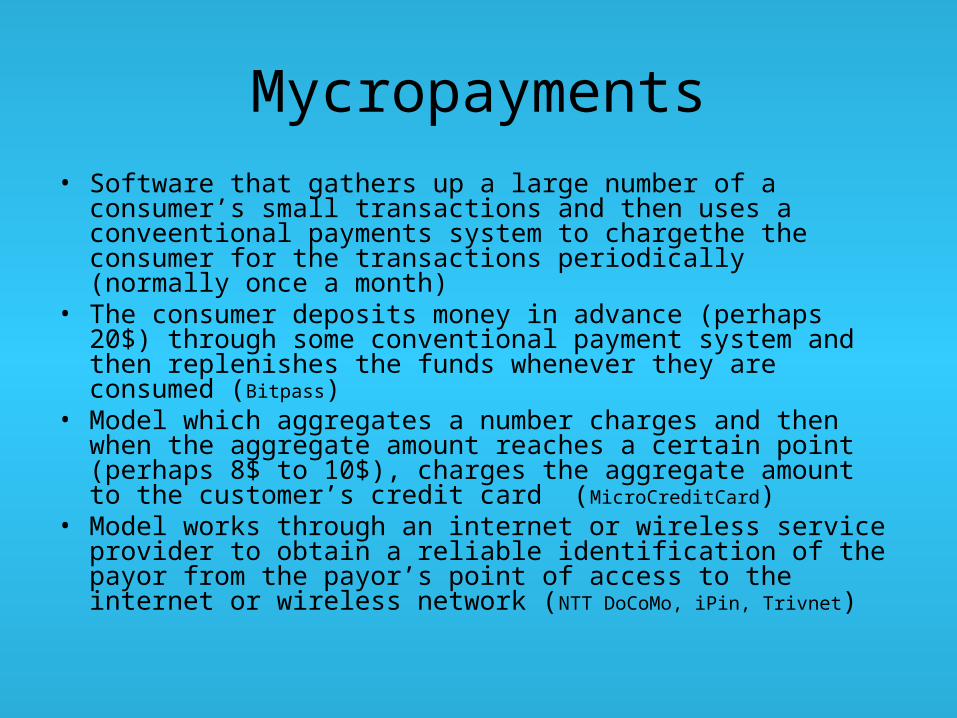

Mycropayments• Software that gathers up a large number of a consumer’s

small transactions and then uses a conveentional payments system to chargethe the consumer for the transactions periodically (normally once a month)

• The consumer deposits money in advance (perhaps 20$) through some conventional payment system and then replenishes the funds whenever they are consumed (Bitpass)

• Model which aggregates a number charges and then when the aggregate amount reaches a certain point (perhaps 8$ to 10$), charges the aggregate amount to the customer’s credit card (MicroCreditCard)

• Model works through an internet or wireless service provider to obtain a reliable identification of the payor from the payor’s point of access to the internet or wireless network (NTT DoCoMo, iPin, Trivnet)

Debit cards

Two classes of debit card

• PIN-based (online) cards (lowers the risk of fraud. The charges to merchants for PIN-based transactions are much lower than the charges for conventional credit-card tranactions (rarely more than 35 cents per transaction))

• PIN-less (offline) cards (are authorised by presentation of the card and the cardholder’s signature (the transaction cost roughly 1 percent of the transaction amunt))

ACH transfers (ACH – Automated Clearing House)

(www.nacha.org) The Electronic Payments

Association

In 2003, customers initiated almost 700 million of those transactions, with an average amount of 291$

• 80% of the payment have been to pay bills.

• 18% - to transfer funs.

• 1% - to make purchases.

Foreign and Cross-Border Payments

Bank transfers shoud satisfy

• A consumer can request a bank transfer directly from the merchant’s site

• The merchant can verify the transfer in real time

• Shipment can be made immediately

Mobile Payments

Mobile payments in 2005

• JAV – 600 million $

• Europe – 1.7 billion $

• Japan – 3.5 billion $

• Estonia – 40% of parking meter charges

The main mobile payments categories

• So-called “in-band” or content payments, normally payments for information or content delivered diretly to the telephone. (DoCoMo)

• „out-of-bands“ payments – purchases in which a telephone is used to purchase something that cannot be delivered to the telephone.

• Proximity payments – when telephone is used to makea payment by communication with a local device such as a parking meter or vending machine.

The methods of collecting for those payments

• Aggregation method. (charges for i-Mode usage are simply added to the monthly mobile-phone bill; payments can be forwarded from the telephone company to the appropriate content provider)

• The second method is for the merchant to use information sent from the telephone to conduct a contemporaneous credit- or debit-card transaction. (that method makes much more sense for larger transactions)