Pay for Performance? CEO Compensation and … for Performance? CEO Compensation and Acquirer Returns...

42

Pay for Performance? CEO Compensation and Acquirer Returns in BHCs by Kristina Minnick 1 , Haluk Unal 2 , Liu Yang 34 Forthcoming Review of Financial Studies 1 Bentley College, Department of Finance, Waltham, MA, 02452, phone: 781-891-2941, fax: 781-891-2494, email: [email protected]. 2 University of Maryland, Robert H. Smith School of Business, College Park, MD, 20742, phone: 301-405-2256, fax: 301-405-0359, email: [email protected]. 3 University of California at Los Angeles, Anderson School of Management, Los Angeles, CA, 90095, phone: 310-206-0664, fax: 310-206-5455, email: [email protected]. 4 We thank the anonymous referee and Paolo Fulghieri (editor) for constructive suggestions. In addition we were fortunate enough to receive suggestions and comments from Santiago Carb-Valverde, Ethan Cohen-Cole, Michael Faulkender, Kim Gleason, Jun Yang, Marcia Cornett, Paul Kupiec, Nagpurnanand Prabhala, and Jack Reidhill as well as seminar participants at UCLA, Federal Deposit Insurance Corporation, University of Hong Kong, the 2007 FDIC/JFSR Mergers and Acquisitions of Financial Institutions Conference, the 2008 European FMA Conference, the 2008 Frontiers of Finance Conference, and the 2009 China International Finance Conference.

-

Upload

truongkhuong -

Category

Documents

-

view

218 -

download

2

Transcript of Pay for Performance? CEO Compensation and … for Performance? CEO Compensation and Acquirer Returns...

Pay for Performance?

CEO Compensation and Acquirer Returns in BHCs

by Kristina Minnick 1, Haluk Unal 2, Liu Yang 3 4

Forthcoming Review of Financial Studies

1Bentley College, Department of Finance, Waltham, MA, 02452, phone: 781-891-2941, fax: 781-891-2494, email:[email protected].

2University of Maryland, Robert H. Smith School of Business, College Park, MD, 20742, phone: 301-405-2256,fax: 301-405-0359, email: [email protected].

3University of California at Los Angeles, Anderson School of Management, Los Angeles, CA, 90095, phone:310-206-0664, fax: 310-206-5455, email: [email protected].

4We thank the anonymous referee and Paolo Fulghieri (editor) for constructive suggestions. In addition we werefortunate enough to receive suggestions and comments from Santiago Carbó-Valverde, Ethan Cohen-Cole, MichaelFaulkender, Kim Gleason, Jun Yang, Marcia Cornett, Paul Kupiec, Nagpurnanand Prabhala, and Jack Reidhill aswell as seminar participants at UCLA, Federal Deposit Insurance Corporation, University of Hong Kong, the 2007FDIC/JFSR Mergers and Acquisitions of Financial Institutions Conference, the 2008 European FMA Conference,the 2008 Frontiers of Finance Conference, and the 2009 China International Finance Conference.

Pay for Performance?

CEO Compensation and Acquirer Returns in BHCs

Abstract

We examine how managerial incentives a¤ect acquisition decisions in the banking industry. We

�nd that higher pay-for-performance sensitivity (PPS) leads to value-enhancing acquisitions. Banks

whose CEOs have higher PPS have signi�cantly better abnormal stock returns around the acquisition

announcements. On average, acquirers in the High-PPS group outperform their counterparts in the Low-

PPS group by 1:4% in a three-day window around the announcement. Ex ante, higher PPS helps to reduce

the incentives to make value-destroying acquisitions, while at the same time promote value-enhancing

acquisitions. The positive market reaction can be rationalized by post-merger performance. Following

acquisitions, banks with higher PPS experience greater improvement in their operating performance. We

show that the e¤ect of PPS is mainly driven by small and medium-sized banks, but is not present in large

banks.

1 Introduction

Top executive pay has increased substantially over the past three decades: the average total remu-

neration for CEOs in S&P 500 �rms (in 2002 constant dollars) increased from $850,000 in 1970 to over

$14 million in 2000. During the same period, the average value of options soared from near zero to over

$7 million (Jensen, Murphy, and Wruck, 2004). Despite the public�s long-standing general belief, partic-

ularly among disenchanted stockholders, that chief executives make too much money, economic theories

recognize that performance based compensation can better align managers�interests with shareholders�,

and, as a result, can create value through more e¢ cient investment decisions (e.g., Morck, Shleifer, and

Vishny, 1988; McConnell and Servaes, 1990; Jensen and Murphy, 1990).

In this paper, we examine how the pay-for-performance sensitivity in executive compensation af-

fects acquisition decisions in bank holding companies (BHCs). We show that the more closely a bank

CEOs�wealth is tied to the stock, the more consistent acquisition decisions are with shareholder value

maximization. Speci�cally, when CEO�s are paid for performance, they are less likely to make acquisitions

that do not create shareholder value and more likely to seek out value-enhancing investments. Although

various papers have examined the relation between managerial incentives and corporate investment de-

cisions, this paper is one of the �rst attempts to investigate the channels through which this e¤ect takes

place.

Banks provide a natural laboratory for assessing the role of compensation in acquisition decisions.

Since the late 1980s, the banking industry has gone through rapid consolidation, which makes it possible

for us to observe a large number of cross-sectional relationships. Because the industry is homogeneous in

its business and most banks operate only in the �nancial industry, acquisitions are usually not driven by

the need to rebalance between di¤erent industries. Finally, focusing on a single homogeneous industry

alleviates the challenges that multi-industry studies face in having to use �xed-e¤ect controls that may

not be broad or detailed enough in terms of industry de�nitions.

It is also very important to study the role of corporate governance in the banking industry. Healthy

banks are vital to economic development and growth, and as evidenced by the recent �nancial crisis,

have a resounding e¤ect on the rest of the economy. Unlike most non-�nancial �rms, banks are regulated

to a higher degree, but it remains unclear whether the governance issues identi�ed as signi�cant in

non-�nancial �rms such as managerial compensation, board structure and anti-takeover provisions are

1

signi�cant in banks (Adams and Mehran, 2003; Barth, Caprio, and Levine, 2004). Regulatory supervision

that ensures that banks comply with regulatory requirements can play a general monitoring role that

can either substitute for or complement other monitoring mechanisms. By understanding how incentive-

based compensation works in a regulatory environment, we can gain insight into the optimal design of

regulation and internal corporate governance for banks.

Our sample consists of 159 bank mergers between publicly traded bank holding companies (BHCs)

from 1991 to 2005.1 We use the CEO�s pay-for-performance sensitivity (PPS) in a bank as a proxy for

managerial incentives. PPS measures the change of the CEO�s wealth from both current and existing

stock and option holdings given a one percent increase in the stock price. We present our �ndings at

three levels.

First, we analyze the announcement returns around the acquisition and �nd that acquirer banks with

higher PPS have higher announcement returns. Acquirers in the top third PPS group outperform their

counterparts in the bottom third PPS group by 1:43% in a three-day window around the announcement.

Second, we examine the e¤ect of PPS on a bank�s probability to make acquisition and use a multinomial

logit model to capture the dual roles of incentive compensation. We show that banks with higher PPS

are less likely to engage in value-destroying acquisitions, while at the same time more likely to promote

acquisitions that create value for shareholders. A one unit increase in the log of PPS lowers the odds

of making a value-destroying acquisition by 36% while increasing the odds of making a value-enhancing

acquisition by 59%. This dual roles of incentive-based compensation is a novel �nding in this paper.

Finally, to capture the �real�e¤ect, we analyze how incentive-based compensation relates to changes in

performance after the acquisition. We �nd that acquirers with higher pre-acquisition PPS also experience

greater improvements in return on assets, return on equity, e¢ ciency, and stock returns up to three years

following the acquisition. In addition, we observe a size e¤ect in PPS sensitivity. We �nd that PPS

matters for small and medium banks, but not for large banks.

Our paper contributes to the literature in several ways. First, we extend the �ndings in Bliss and Rosen

(2001) to broaden our understanding about the role of managerial incentives in acquisition decisions. Bliss

and Rosen (2001) show that bank CEOs with high PPS are less likely to make acquisitions because of the

wealth e¤ects from the negative stock price reaction. In this paper, we �rst document the fact that not all

1Because of our selection criterion (due to data availability), most of the acquirers in our sample are large national banks.The average deal value is about $1.7 billion.

2

acquisitions have negative price impact. In fact, half of the acquisitions in our sample create signi�cant

value for shareholders. We then show that managerial incentives achieve two goals simultaneously. They

prevent value-destroying acquisitions and motivate value-improving acquisitions. Thus, we provide some

evidence that not only shareholders but all stakeholders bene�t.

Next, we add to the governance literature by showing that managerial incentives are important even

in the presence of regulation. Using a sample of non-�nancial �rms, Datta, Iskandar-Datta, and Raman

(2001) show that high equity-based compensation leads to better stock announcement returns for non-

�nancial acquirers. In this paper, we �nd similar results for banks, which are much more heavily regulated.

Our �ndings suggest that regulation cannot fully substitute for managerial incentives, and therefore

incentive schemes, such as pay-for-performance may be used e¤ectively in the regulated industries. Other

studies have shown that governance mechanisms may work di¤erently for banks than for non-�nancial

�rms. For example, Adams and Mehran (2002) �nd that banks with larger boards have higher value,

contrary to non-�nancial �rms in which board size is negatively related to �rm value (Yermack, 1996).

The question of whether and how various governance mechanisms can a¤ect banks and non-�nancial �rms

di¤erently falls beyond the scope of our current paper and deserves future study.

Third, this paper joins a small number of studies that aim to explore the channel through which

corporate governance a¤ects �rm performance. Speci�cally, our �ndings corroborate those of Masulis,

Wang, and Xie (2007), who show that among non-�nancial �rms, acquirers with strong shareholder rights,

measured by the anti-takeover provision (ATP) index, have higher abnormal announcement returns in

mergers. We �nd that acquirer returns around the merger announcement are jointly a¤ected by incentive-

based compensation and the market for corporate control. Moreover, among the group of governance

measures examined in this paper, such as board size, market for corporate control, and managerial

incentives we �nd that managerial incentives have the most signi�cant e¤ect in creating value for acquirer�s

shareholders.

The rest of the paper proceeds as follows: In Section 2 we describe our data and compare governance

measures between the acquirer and the non-acquirer banks. In Section 3 we study the stock returns to

the acquisition announcement. We estimate the probability to acquire in Section 4 and examine changes

of operating performance after acquisitions in Section 5. Section 6 concludes.

3

2 Data

2.1 Sample Construction

We construct our acquisition sample using the Thompson Financial�s SDC Platinum Mergers and Ac-

quisitions database (SDC). Our sample includes acquisitions made between January 1991 and December

2005 in the banking industry that meet the following criteria:

� The acquisition is completed.

� The deal value disclosed in SDC is greater than $25 million.

� The acquirer is classi�ed as a national commercial bank with an SIC code of 6021 in the SDC.2

� The target is publicly traded.3

� The target�s book value of asset is at least 1% of that of the acquirer before the acquisition.4

� The acquirer has annual �nancial information available from Compustat, Compustat Bank or the

FDIC�s Call Report and the acquirer has stock return data from Center for Research in Security

Prices (CRSP).

� Managerial compensation data are available for the acquirer from Compustat�s Execucomp database

or from proxy statements a year prior to the acquisition.5

Our full sample includes 159 acquisitions made by 64 bank holding companies, with some acquir-

ers having multiple acquisitions. Table I Panel A shows the number of transactions by year, together

with information on deal value, acquirers�market capitalization, and relative size between targets and

acquirers. Consistent with the merger activity of non-�nancial �rms reported in Masulis, Wang, and

Xie (2007), more bank acquisitions occurred between 1997 and 2000 than at other times. The average

deal has a transaction value of $1:7 billion. The average acquirer�s market capitalization is about $8:4

billion, increasing from $4:1 billion in 1991 to $26 billion in 2005. Bank acquirers are much bigger than

2We restrict acquirers to be national commercial banks so that we can obtain relevant information from Compustat Bank.3We require targets to be public so that we can obtain information before acquisitions. However, very few deals that

satisfy our other data requirements involve private targets, and including those deals (about 5 transactions) does not changeour results qualitatively.

4Similar cuto¤ point (1%) is used in Masulis, Wang and Xie (2007).5For acquisitions before 1992 (when Execucomp started), we use the same sample as in Penas and Unal (2004) and

hand-collect the compensation information from proxy reports whenever it is available.

4

non-�nancial acquirers. The average acquirer listed in Masulis, Wang, and Xie (2007) has a market

capitalization of $5:59 billion, which is 67% of the average size of the banks in our sample. The average

deal value is about 18% of the acquirer�s pre-acquisition market capitalization (compared with 16% in

Masulis-Wang-Xie sample), and the average target is about 13% of the size of the acquirer prior to the

acquisition. Table I Panel B shows that among the 64 acquirers in our sample, 32 banks (50%) have

undertaken only one acquisition, and 8 banks (13%) make at least �ve acquisitions during the sample

period.

[INSERT TABLE I HERE]

Table II presents summary statistics that capture the deal characteristics. Almost all acquisitions

involve a full ownership transfer.6 We �nd a remarkable di¤erence in �nancing between bank acquisitions

and acquisitions involving non-�nancial �rms. In our sample, 5% of the acquisitions are fully �nanced with

cash (ALLCASH=1) and 79% of the acquisitions are �nanced exclusively with stock (ALLSTOCK=1).

In contrast, 46% of the non-�nancial acquisitions were fully �nanced by cash in Masulis, Wang, and Xie

(2007). We de�ne an indicator variable D_STOCK to represent deals that are mainly �nanced through

stock. It takes the value of one if the acquisition is more than 75% �nanced by equity and the value of

zero otherwise. This variable has a mean of 82% and is used in our regressions as a control for �nancing

method used in the acquisition. All of our results hold when we use 100% as an alternative cuto¤ to

de�ne D_STOCK. About 70% of the acquisitions in our sample involve banks that have headquarters in

a di¤erent state. We capture this characteristic by the binary variable, OUTOFSTATE, which takes the

value of one if the acquisition involves an out-of-state bank and zero otherwise.

[INSERT TABLE II HERE]

To compare acquiring banks with their non-acquiring counterparts, we construct a benchmark sample

using bank-years during which there is no acquisition, i.e., years in which the bank is neither an acquirer

nor a target. In contrast, we identify acquirer years as years when banks are acquirers. A bank that

has made multiple acquisitions in the same year is counted only once for this identi�cation purpose.

Because Execucomp does not have data prior to 1992, our benchmark sample period starts in 1992.

6Only 4 deals has less than 100% ownership transferred, among which the minimum percentage is 92%.

5

This restriction causes us to lose six acquirer years that are before 1992. Data availability in other

control variables further causes us to lose additional bank years in both acquirer sample and benchmark

sample. Our �nal sample consists of 109 acquirer years and 568 non-acquirer years. About 25% of our

acquirer banks also appear in our benchmark sample at some point during our sample period. For a

robustness check, we also use an alternative benchmark sample, which consists of only banks that have

never participated in acquisitions (unreported, but available upon request), and all of the main results

are qualitatively the same.

Table II Panel B presents the bank characteristics for the two groups. The two samples are very

similar, with comparable total assets (TA), market capitalization (MVE), stock returns (RET), stock

return volatility (RET_VOL), ratio of loan loss provisions(PRV), cash holding (CASH), and return on

assets (ROA).

2.2 CEO Compensation

We collect data on CEO compensation, such as annual salary, bonus, new grants of restricted stocks

and options, and stocks and options from previous grants from the Compustat�s Execucomp database.

For acquirers before 1992, we hand collect data from the proxy statements whenever they are available.

Following Core and Guay (1999), we measure the pay-for-performance sensitivity (PPS) as the change of

the CEO�s total wealth (in thousands of dollars) from her stock and option holdings, given a 1% increase

in stock price. Our PPS measure is di¤erent from the incentive compensation proxy used in Bliss and

Rosen (2001) or Datta, Iskandar-Datta and Raman (2001). We include equity and option holdings from

new and previous grants for a total wealth e¤ect while the other papers only consider new equity based

compensation. In our sample, the PPS from new grants only accounts for 9 � 15% of the total PPS.

Similar to Core and Guay (1999), we use the Black and Scholes (1973) formula to value the options,

assuming a ten-year maturity on options and a return volatility based on the monthly stock returns

in the past twelve months. In addition to the total PPS, we also calculate PPS based on individual

components, such as stock holdings (SPPS) and option holdings (OPPS). We use the natural logarithm

of PPS instead of the raw value in our regressions as the distribution is heavily skewed to the right.7

We compare the CEO compensation between the acquirer and benchmark banks in Table III, Panel

A. The cash compensation (Cash Comp) includes payments in salary, bonus and other income, and

7We use log(PPS+1) to eliminate the extreme outliers for bank-years with PPS equal to zero.

6

the total compensation (Total Comp) includes both the cash compensation and the current stock and

option grants.8 On the univariate level, the acquirer sample and the benchmark sample have very similar

compensation structures. The median acquirer CEO received cash compensation of $1:55 million, which

is 51% of her total compensation and the median benchmark CEO received a cash compensation of

$1:60 million, 54% of her total compensation. For both groups, the mean compensation is higher than

the median, suggesting that the distribution is skewed to the right. On pay-for-performance sensitivity,

acquirer CEOs have slightly lower average (median) Total PPS than the benchmark CEOs: 480 versus

515 (217 versus 268) although the di¤erence is not signi�cant.

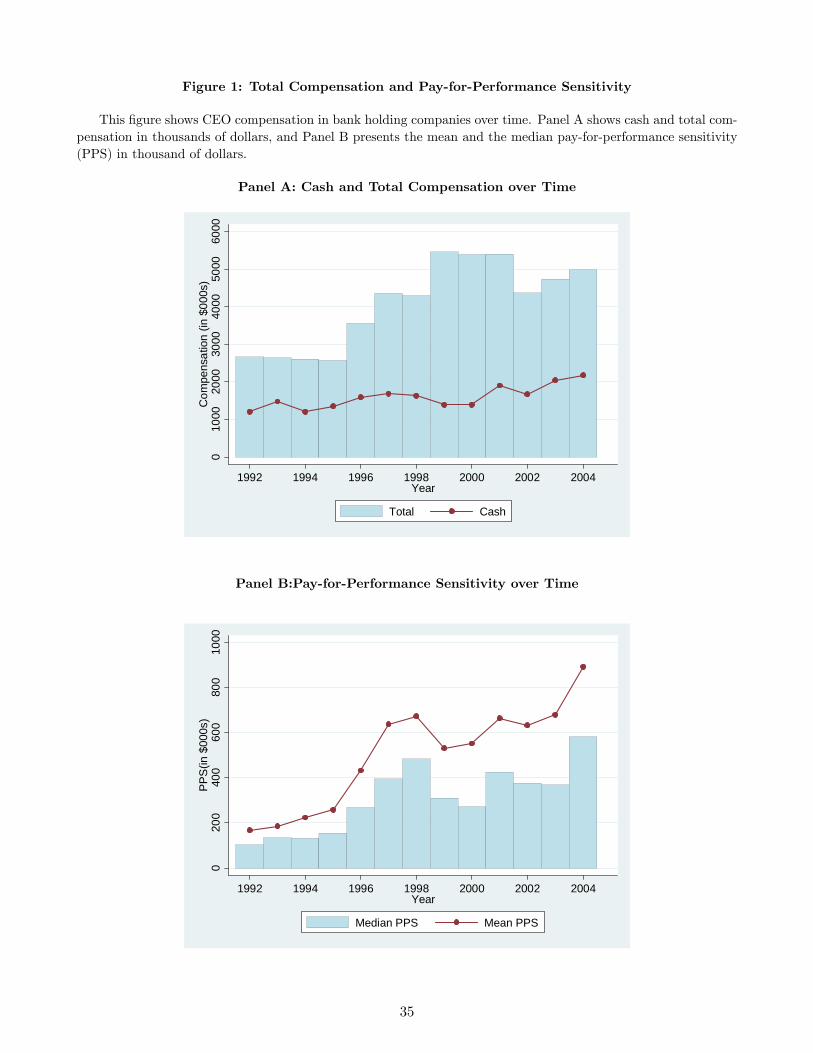

Figure 1 presents the change of CEO compensation over time during our sample period. Table III

Panel A shows that over the past thirteen years, the average total compensation for bank CEOs rises from

$2:7 million in 1992 to $4:9 million in 2004. Meanwhile, pay-for-performance sensitivity has increased

even more. We observe in Panel B that in 2004, for every 1% increase in stock price, a median bank CEO

gains about $583; 000 in her personal portfolio in terms of stocks and options, more than �ve times as

much as she would have in 1992. Despite the common increasing trend, there exists a wide cross-sectional

dispersion in the PPS. For example, in 2004, among our sample banks, 13% CEOs have PPS less than

50, while more than 31% of CEOs have PPS greater than 1000.

[INSERT FIGURE 1 HERE]

2.3 Other Corporate Governance Variables

To control for other internal and external governance mechanisms that can potentially a¤ect the

acquisition outcome, we also collect information on the board of directors and the strength of shareholder

rights from the Investors�Responsibility Research Center (IRRC). Since the IRRC data start in 1996,

our sample size is further reduced whenever we include those variables. It is also worth noting that

since larger banks are more likely to be included in the IRRC database, regression results based on the

subsample with the available board and anti-takeover provision variables may potentially re�ect more on

larger banks.

Board Structure Many studies document that the size and composition of a board of directors can

in�uence the e¤ectiveness of internal monitoring (Yermack, 1996; Hermalin and Weisbach, 1998). To

8The total compensation is based on data item TDC1 in Execucomp.

7

control for the impact of board structure on acquisition success, we obtain information on board size

(BSIZE), the percentage of independent directors (BINDEP), and whether the CEO is also the chairman of

the board (D_CEO) from the IRRC�s Director database. The acquirers have signi�cantly more directors

than the benchmark banks - 16 versus 15 directors, and in both samples, about 69% of the directors

are independent. The larger boards in acquiring banks are likely to be related to acquisition. After

acquisitions, acquirers often take some directors from the target �rms onto their Board of Directors.

Thus, to the extent that banks tend to make multiple acquisitions, the larger boards of acquirer banks

may re�ect prior acquisition activities. Therefore, we control for previous acquisitions whenever we

include board size as a control for governance. In the majority of the banks, the CEO also serves as

the chairman of the board (the average D_CEO is 94% for the benchmark banks and 90% for acquirer

banks).

Shareholder Rights A number of recent papers con�rm the governance role of the market for corporate

control. They �nd that �rms with fewer anti-takeover provisions (ATPs) or weaker shareholder rights

have lower value. These studies measure the level of shareholder rights in a number of ways. Gompers,

Ishii, and Metrick (2003) construct a governance index (GINDEX) using all twenty-four ATPs collected

by IRRC, while Bebchuk, Cohen and Ferrell (2004) choose six out of the twenty-four ATPs to form

an entrenchment index(EINDEX).9 Bebchuk and Cohen (2005) show that a binary variable based on

whether a �rm has a staggered board (CBOARD) e¤ectively captures the strength of market discipline.

Among our sample of banks, the average GINDEX is 10:07 for the benchmark sample and 10:18 for

the acquirer sample. Both of them are higher than the GINDEX of 9:15 reported in Gompers, Ishii,

and Metrick (2003) for non-�nancial �rms. The average EINDEX for our acquirer banks is 2:76, and

76% of the acquirer banks have staggered boards. In comparison, non-�nancial acquirers have an average

EINDEX of 2:24, and a likelihood of 61% for staggered board, as reported by Masulis, Wang, and Xie

(2007). Although banks are bigger than non-�nancial �rms and larger �rms tend to have more ATPs,

these observations still bring up an important issue.10 That is, despite that most mergers in the banking

industry are friendly rather than hostile due to the process of regulatory approval for bank mergers, banks

still adopt more ATPs than the non-�nancial �rms. For brevity, we only report results based on EINDEX

9The six ATPs used by Bebchuck, Cohen and Ferrell are staggered boards, limits to shareholder by�law amendments,super�majority requirement for mergers, super�majority requirement for charter amendments, poison pills and golden para-chutes.10Gompers, Ishii and Metrick (2003) show that G-INDEX is positively correlated with �rm size.

8

for all of our tables, but results are qualitatively the same when GINDEX or CBOARD is used.

[INSERT TABLE III]

Other Considerations Both the decision to acquire and the pay-for-performance sensitivity can

change with the CEO�s tenure or age. Bliss and Rosen (2001) �nd that younger CEOs are much more

likely to do acquisitions. We use the Execucomp to collect data on the CEO�s age and her tenure at the

current position. We �nd that the CEOs of acquirer banks are marginally younger than the CEOs in

the benchmark sample, but do not di¤er signi�cantly in tenure (the median age of acquirers is 55 versus

57 for benchmark banks). Similar to Bliss and Rosen, we create a dummy variable D_AGE to indicate

whether the CEO is greater than 60 years old.11

Di¤erent governance measures can be related. Panel B of Table III presents the correlation matrix

among various governance measures. Banks with higher PPS also tend to have their CEO as the chairman

of the board, and stronger market discipline (lower GINDEX and EINDEX). Older CEOs with longer

tenure have higher PPS. The presence of signi�cant correlation between PPS and other governance

variables further con�rms the needs for controlling for both variables when we analyze the impact of PPS

on acquisition outcomes. Finally, to control for macro-economic conditions that might in�uence decisions

to acquire and changes in PPS over time, we include a year �xed e¤ect in all of our regressions.

3 PPS and Announcement Stock Returns

In this section, we examine the relation between pay-for-performance sensitivity and stock returns

acquisition announcements using the event study methodology.

3.1 Univariate Analysis

We measure acquirer announcement returns using the market-adjusted model. We obtain the an-

nouncement dates from the SDC and compute the cumulative abnormal returns (CARs) in a three-day

(�1;+1) and a �ve-day window (�2;+2) where day zero is the announcement date. We use CRSP

value-weighted returns as the benchmark returns to calculate abnormal stock returns. Panel A of Table

IV shows that the three-day and �ve-day acquirer CARs are widely dispersed, ranging from �8:78%11Bliss and Rosen use a cut-o¤ point of 50. However, in our sample only 8% of the CEOs are under 50 years of age, and

32% of the CEOs are under 60. Our main results still hold if we use 50 as the cuto¤ point.

9

to 8:82% and from �10:65% to 10:96%, respectively. Neither the mean nor the median is signi�cantly

di¤erent from zero. Figure 2 presents the returns in histogram.

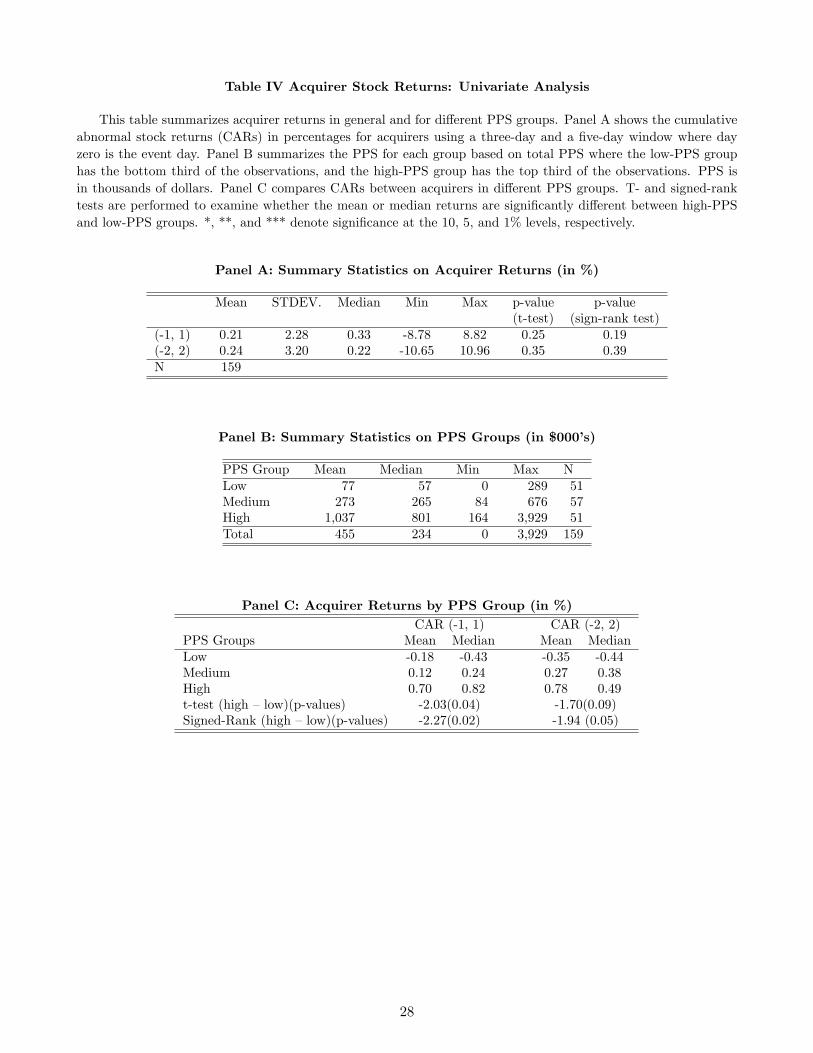

[INSERT TABLE IV AND FIGURE 2]

We take special note of two results. First, the acquisitions in our sample do not in general �lead

to a decline in acquirer stock prices,� as noted by Bliss and Rosen. In fact, acquirers have positive

announcement returns in more than half of the acquisitions (54%) and the average three-day CAR

for those acquirers is about 1:74%:12 Our �ndings here are also consistent with �ndings in Moeller,

Schlingemann and Stuz (2004) who show that the equal weighted abnormal announcement return for a

large sample of acquisitions averages about 1.1%. Second, although a value-destroying acquisition can

lead to loss of value in the CEO�s personal portfolio, the reverse can also occur. That is, the CEO can gain

a signi�cant amount of wealth when the acquisition creates value for shareholders. For example, for over

half the acquirers that experienced positive three-day CAR, the increase in stock price can translate to a

wealth increase of $835; 000 to the CEO, which is about half of the CEO�s annual cash compensation.13

Given both directions, our hypothesis is that managerial incentives can serve a dual purpose in the context

of acquisitions. That is, higher PPS can increase the likelihood that the CEO rejects value-destroying

acquisitions, while at the same promotes acquisitions that create value for both shareholders and the

CEO.

We test this hypothesis �rst at the univariate level. For every year, we divide all banks in that year

(both acquirers and non-acquirers) into three groups based on their CEOs�PPS. The Low-PPS group

includes the bottom third of banks and the High-PPS group includes the top third of banks. We include

the benchmark sample in our calculation for cuto¤ points of PPS because PPS itself can a¤ect decisions

to acquire (which we discuss in detail in the next section). Identifying groups by year helps to control for

changes of PPS over time. Among 159 acquisitions in our sample, 51 acquirers belong to the low-PPS

group and 51 to the high-PPS group, with the remaining 57 acquirers in the Medium-PPS group. Table

IV Panel B reports the mean and median PPS for each group. For a 1% increase in stock price, the

median CEO in the Low-PPS group has an average wealth increase of $57; 000, compared to an increase

of $801; 000 for the median CEO in the High-PPS group.12Among the 159 acquisitions, we have 72 acquisitions with negative 3-day CARs and 87 acquisitions with positive 3-day

CARs.13We calculate this number based on the average acquirer PPS of $480,000 (Table III Panel A).

10

Comparing the announcement returns (both three-day and �ve-day) across di¤erent groups, we �nd

a positive relation between PPS and stock returns. Table IV Panel C shows that the Low-PPS acquirers

have an average (median) 3-day CAR of �0:18% (�0:43%), while the High-PPS acquirers have an average

(median) CAR of 0:70% (0:82%) around the acquisition announcement. The di¤erence is signi�cant at

the 4% and 2% level based on t-test and signed-rank test, respectively. We �nd similar results using

�ve-day CARs. Box plots in Figure 3 further illustrate the comparison. These observations provide the

initial evidence that higher PPS creates value for the shareholders. The following section examines the

issue in a multivariate setting.

[INSERT FIGURE 3 HERE]

3.2 Multivariate Analysis

To test our focal hypothesis we use the following speci�cation:

yi;t = �0 + �1PPSi;t�1 + �2Ai;t�1 + �3Gi;t�1 + �4Di;t + Ft + "it (1)

The dependent variable, yi;t, is the cumulative abnormal stock return around the announcement for

acquirer i with the deal occurring in year t, and our key explanatory variable is the pay-for-performance

sensitivity of the acquirer bank�s CEO (PPSi;t�1). We control for acquirer�s characteristics (Ai;t�1),

other governance variables (Gi;t�1), and deal characteristics (Dit). We also include a year �xed e¤ect

(Ft) and "it is the error term.

For acquirer characteristics (Ai;t�1), we include log of total assets (SIZE), return on assets (ROA),

cash holdings (CASH), and previous merger activity (D_PMERGER). Moeller, Schlingemann, and Stulz

(2004) �nd evidence that acquirer returns are negatively related to bidder size, regardless of the method

of payment or whether the target is public or private. In addition, Penas and Unal (2004) document a

signi�cant too-big-to-fail (TBTF) factor when they examine returns around acquisitions. They show that

both bond- and stock-holders of medium-sized banks realize the highest returns when the acquiring banks

push the combined bank�s asset size above the TBTF threshold. Acquisitions can be driven by better

opportunities (Jovanovic and Rousseau, 2002) or manager�s private bene�ts. We include a performance

measure - return on assets (ROA) and the banks�cash holdings as a percentage of total assets (CASH)

11

to control for both motivations. For other governance measures (Gi;t�1), we include board structure

(BSIZE, BINDEP), strength of shareholder rights (EINDEX), and CEO age (D_AGE).

For deal characteristics (Di;t), we control for the relative size between the target and the acquirer banks

(SIZE_RATIO), the method of payment (D_STOCK), and geographic diversi�cation (OUTOFSTATE).

The existing empirical evidence is mixed on how relative size a¤ects acquirer returns. Asquith, Bruner

and Mullins (1983) show that acquirer announcement returns are positively related to relative deal size,

but Moeller, Schlingemann and Stulz (2004) �nd that the reverse is true for large acquirers. Our sample

is more similar to Moeller, Schlingemann and Stulz�s large-acquirer sample: the market capitalization for

the average (median) acquirer in our sample is $10:0 ($3:5) billion. We de�ne relative size (SIZE_RATIO)

as the ratio between deal value and acquirer�s market value of equity.14 In unreported regressions, we

also use the asset size ratio between target and acquirer banks prior to the acquisition as an alternative

measure, and all of our results hold qualitatively. Many merger studies have reported lower acquirer

returns when acquisitions are paid using stock. We include the method of payment (D_STOCK) in our

regression as a control. Interstate bank mergers are shown to o¤er less opportunity for increasing market

power and fewer cost savings (Prager and Hannan, 1998). Therefore, we include an indicator variable

(OUTOFSTATE) to control for geographic diversi�cation.

Table V summarizes our regression results using the three-day CARs. In Columns 1 - 3, we use

di¤erent measures of PPS such as total PPS, stock PPS and option PPS. In Column 4, we separate

acquirers into three groups based on their total PPS. D_MPPS and D_HPPS are indicator variables

that equal one if the acquirer is in the middle or top third among all banks in that year, respectively

(this is the same variable used in the univariate analysis above). Columns 5 and 6 present the estimation

results when other governance variables are included in the regression. The sample size is slightly smaller

(from 159 to 116) when we include other governance variables.

[INSERT TABLE V HERE]

In all speci�cations, the estimated coe¢ cients for PPS are positive and signi�cant, implying that

acquirers with higher PPS tend to consistently outperform acquirers with lower PPS. A one unit increase

in total PPS (in the logarithm) increases the announcement return by 0:50% and the e¤ect is even stronger

at 0:62% when we control for other governance variables. When we separate acquirers into three groups14A similar de�nition is used in Masulis, Wang and Xie (2007).

12

based on PPS, we �nd that the positive e¤ect of PPS on returns increases monotonically: compared to

acquirers in the Low-PPS group, acquirers in the Medium- and High-PPS groups outperform by 0:93%

and 1:43%, respectively in a three-day announcement return. The di¤erence between the Low- and the

High-PPS group is signi�cant at 5% level regardless of whether other governance variables are included

or not.

Among other governance variables, we �nd that announcement returns are higher when the acquiring

banks have lower EINDEX (or fewer anti-takeover provisions and stronger shareholder rights). On the

other hand, neither board structure nor CEO age seems to matter for acquirer returns. The signi�cance

of the EINDEX is noteworthy for at least two reasons. First, it is consistent with the �ndings of Masulis,

Wang, and Xie (2007), who show that more ATPs (higher EINDEX) lead managers of non-�nancial �rms

to make value-destroying acquisitions. Here, we �nd that the same dynamics is at work for �nancial �rms.

Second, EINDEX and PPS are negatively correlated and they in�uence returns in opposite directions.

Masulis, Wang and Xie fail to �nd any signi�cance for CEO compensation variables in their regressions.

Our �ndings, however, suggest that incentive-based compensation promotes better acquisition decisions

in the presence of market for corporate control.

In terms of the control variables, we �nd that returns are higher for small acquirers. Operating

performance and cash holdings consistently show positive e¤ects on announcement returns, although the

coe¢ cients are not signi�cant. Acquirers which undertook prior acquisitions consistently have lower stock

returns, and this e¤ect is stronger in our subsample sample in which other governance variables available.

When we examine the deal characteristics, we observe that returns are higher when the target is smaller

relative to the acquirer�s own size, consistent with �ndings from Moeller, Schlingemann and Stulz (2004)

for their large-acquirer sample. Unlike acquisitions in non-�nancial �rms, the method of payment does

not signi�cantly a¤ect returns for bank acquirers. This �nding may be due to the fact that majority of

the acquisitions in the banking industry are �nanced mainly by stock. Acquisitions of out-of-state targets

do not signi�cantly outperform acquisitions in which the acquirer and the target bank have headquarters

in the same state. Although unchanged in signs and signi�cance level, the magnitude of our estimates

on certain variables change (e.g. CASH and SIZE_RATIO) when we use the sample with governance

variables. This is mainly due to sample di¤erence. Since governance variables are more likely available

for larger banks, our subsample with governance variables re�ects more on larger banks. In unreported

regressions, we also use alternative event windows, such as (-2, 2), (-3, 1), and (-5, 1), and results are

13

qualitatively the same.

3.3 Robustness Checks

To check the robustness of our result on stock returns, we perform additional tests in this section

based on di¤erent sample splits. For brevity, we only report results for the overall sample (n=159).

Regressions based on subsample with governance variables (n=116) yield qualitatively similar results.

Opportunity Sets Not all banks face the same opportunities. Large national banks are more likely

to be diversi�ed in their businesses than small local banks (Prager and Hannan, 1998). Even large

banks di¤er in what they do. Regional banks focus more on traditional banking while multinational

banks generate substantial income from trading complex products, such as derivatives. For too-big-to-

fail banks, there may be fewer potential bene�ts to shareholders from acquisitions, as compared to smaller

banks (Penas and Unal, 2004). Therefore, it is instructive to examine the role of PPS within our sample

of banks.

We divide our acquirers into three size categories. We de�ne a �small bank�as a bank that has asset

size in the bottom one-third among all acquirers, a �medium bank�as a bank that has asset size in the

medium one-third, and a �large bank�as a bank that has asset size in the top one-third.15 We also de�ne

size-dummy based on the overall sample to eliminate the potential problem that the size distribution of

acquiring banks can be changing overtime. The thinking behind this grouping is that as the amount of

assets under management increases in a bank, the business focus changes as well from being traditional

to being more complex. We also de�ne size-dummy based on the overall sample to eliminate the potential

problem that the size distribution of acquiring banks can be changing overtime.

The results are reported in Table VI Column 1 and 2. We observe that the e¤ect of PPS is not

uniform across our size groups. PPS is positive and signi�cant for small and medium-sized banks, but

becomes negative and insigni�cant for large banks. In unreported regression when we further separate

mega-size banks (those above $100 billion) within the large bank group, we observe that the negative

sign on PPS for large bank group is mostly driven by mega-size banks.16 These �ndings suggest that in

15We de�ne �small�and �large�on a relative basis - a small bank in our sample has less than $15 billion in assets, and alarge bank has more than $32 billion in assets.16Similar criterion is used in Penal and Unal (2004) to de�ne mega banks. In our sample, we have 13 acquisitions from

mega-banks.

14

contrast to smaller banks, the market participants do not believe that the PPS a¤ects the outcome of

acquisitions for large banks. We turn to this issue in the next section.

[INSERT TABLE VI HERE]

Before and After 1999 In 1999, the US Congress passed the Financial Services Modernization Act,

which allowed commercial banks to merge with investment banks.17 This legislation has motivated a

large number of acquisitions across the business lines. Because our sample spans over the pre- and post-

legislation periods, it is reasonable to question whether the positive e¤ect of PPS on acquirer returns

holds in both periods.

We divide our sample into two sub-periods around the year of 1999 (1992-1999 and 2000-2005) and

run the return regression separately in each subsample. Within our sample of 159 acquisitions, we have

108 acquisitions occurred before and 51 acquisitions after 1999. Our results are presented in Table VI,

Columns 3 and 4. PPS has signi�cant positive e¤ects on acquirer returns in both periods. The coe¢ cient

is marginally signi�cant for the second period, potentially due to fewer number of observations. Our

�ndings suggest that although acquisitions in two sub-periods might be driven by di¤erent motivations,

in both periods, having the CEO�s incentive aligned with the incentive of the shareholders helps to create

value for shareholders in the context of acquisitions.

4 Probability to Acquire

In this section, we examine whether higher PPS predicts better acquisition decisions ex-ante. Bliss

and Rosen (2001) argue that CEOs with high incentive-based compensation are less likely to engage

in acquisitions because of the negative wealth e¤ect due to declining stock prices post acquisition. As

we show in the previous section, not all acquisitions lead to negative stock returns. In fact, in our

sample, more than half of the acquisitions generate positive returns for their shareholders (see Figure 2

Panel A). For a CEO who holds signi�cant wealth in stocks and options, an unsuccessful acquisition can

reduce the value of her personal portfolio. However, she can also be greatly rewarded if the acquisition

creates value for the shareholders. In addition, merely investigating the relation between the acquisition

decision and PPS, as in Bliss and Rosen, cannot show the channel through which PPS a¤ects the CEO�s

17 It is also referred to as the Gramm-Leach-Bliley Act of 1999 (http://banking.senate.gov).

15

acquisition decision. For example, incentive-based compensation can prevent CEOs from engaging in

value-destroying acquisitions or encourage them to invest in value-enhancing acquisitions or serve a dual

purpose and incentives the CEO to do both.

To examine the channels through which PPS a¤ects acquisition decisions, we divide our acquisition

sample into two groups: winners and losers, based on the three-day cumulative abnormal returns around

the announcement. Then, we estimate a multinomial logit model in which the dependent variable is an

indicator variable that equals one if the bank makes an acquisition announcement and the announcement

return is negative(D_ACQ = 1), and two if the bank makes an acquisition announcement with positive

return(D_ACQ = 2). We use the non-acquirer sample as the benchmark and set the variable equal to zero

(D_ACQ = 0). For acquirers that made multiple acquisitions within a year, we use the weighted average

return based on deal value to identify the indicator variable. In our �nal sample with other governance

variables available, we have 80 acquirer years (with 39 negative returns and 41 positive returns) and 323

benchmark bank years.

Our basic speci�cation is as follows:

Pr (D_ACQi;t) = �0 + �1PPSi;t�1 + �2Bi;t�1 + �3Gi;t�1 + Ft + �i;t (2)

The dependent variable, D_ACQi;t, is the indicator variable for bank i in year t, as speci�ed above, and

our key explanatory variable is the pay-for-performance sensitivity (PPSi;t�1). We also control for bank

characteristics(Bi;t�1) and other governance variables (Gi;t�1). Ft is the year �xed e¤ect and vit is the

error term.

We draw our variables that re�ect bank characteristics (Bi;t�1) from �ndings in the existing merger

and banking literature. Neoclassical theory suggests that acquisitions help to reallocate resources to their

best use (Jovanovic and Rousseau, 2002). Meanwhile, agency theory presents that when there is free cash

�ow, managers have incentives to over invest for their private bene�t (Jensen, 1986). However, banks

typically have a lot of easily marketable government securities on their balance sheets as well as the ability

to raise insured deposits, which makes the free cash �ow argument more complex. Taking both arguments

into account, we control for the acquirer�s operating performance using return on assets (ROA) and the

banks�cash holdings, as a percentage of total assets (CASH). Banks may also engage in acquisitions to

take advantage of the recent increase in stock price or high volatility in market valuation (Rhodes-Kropf,

16

Robinson, and Viswanathan, 2005). To control for the motivation due to market valuation we use the

average stock return(RET) and the volatility of returns (RET_VOL) one year prior to the acquisition

announcement. Banks with riskier assets expect to have higher default rates in the future and may choose

to hold higher level of loan loss provisions to meet future needs. We use the ratio of loan loss provisions

(PRV) over the total amount of loans outstanding as our proxy for the portfolio risk. Acquisitions may be

positively or negatively auto-correlated, depending on whether the bank follows an acquisition strategy.

To control for past activity, we add an indicator variable that denotes whether the bank has participated

in acquisitions in previous years (D_PMERGER). Finally, we include the logarithm of total book assets

(SIZE) in our regression to control for bank size. The governance variables (Gi;t�1) are similar to those

used in the previous section.

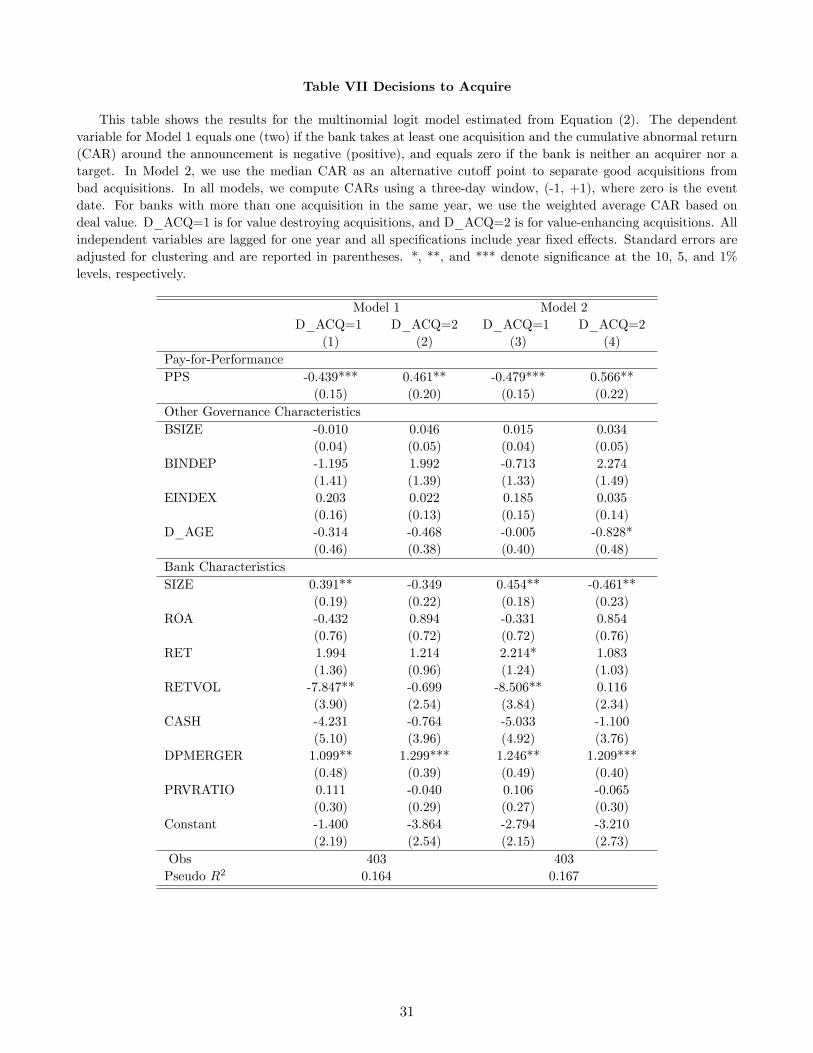

Table VII presents our �ndings. In Column 1 and 3 the dependent variable is D_ACQ=1, which

re�ects the value destroying (negative abnormal return) acquisition decision. The coe¢ cient on PPS

is negative and signi�cant in both speci�cations indicating that higher PPS leads to signi�cantly lower

probability of making value-destroying acquisitions. On the other hand, in Columns 2 and 4 the dependent

variable is D_ACQ=2 re�ecting the value enhancing decisions. Here the coe¢ cient of PPS becomes

positive and signi�cant implying that higher PPS leads to higher probability of making value-enhancing

acquisitions. These �ndings hold with or without the presence of other governance variables. A one unit

increase in PPS lowers the odds of making value-destroying acquisitions by 36% while increasing the odds

of making value-enhancing acquisitions by 59%.18

To ensure that our breakpoint for value destroying and enhancing mergers is robust, we also use

the median abnormal returns as our breakpoint. Acquisitions with returns below or at the median

are deemed value destroying, while acquisitions with returns above the median are identi�ed as value

enhancing. Columns 4 and 5 show the results, which are consistent with using the zero breakpoint. The

results remain unchanged when we use the zero breakpoint.

[INSERT TABLE VII HERE]

These �ndings support our earlier �nding on stock returns. More importantly, they show that when

CEO�s interests are well aligned with those of the shareholders, two e¤ects are at work. High PPS reduces18The changes in odds ratio are calculated using estimates from Table VII Model 2. For one unit increase in PPS,

change in odds ratio of making value-destroying acquisition =1 - exp(�0:439) = 0.36, and change in odds ratio of makingvalue-improving acquisition=exp(0:461) - 1 = 0.59.

17

a CEO�s incentives to make acquisitions which destroy value (such as empire building acquisitions).

However, since the CEO will be rewarded for investing in value-enhancing acquisitions, it also encourages

the CEO to search out for new projects that bene�t shareholders. By examining the mechanisms on how

PPS a¤ects acquisition decisions, these �ndings provide insights on the channel through which incentive-

based compensation improves the value of a �rm. In unreported regressions, we also run an alternative

speci�cation allowing the e¤ect of PPS to vary by size, and �nd that the e¤ect of PPS on decisions to

acquire does not di¤er signi�cantly across size categories.

Examining bank characteristics, Table VII shows that large banks are more likely to make value-

destroying acquisitions. Prior acquisition history leads to a higher likelihood of future acquisitions,

regardless if they create value or not.

As is the case with many empirical studies, our study is potentially subject to endogeneity problems

as our main explanatory variable, PPS, is not entirely exogenous. Therefore, before we can draw the

conclusion that high PPS causes bank CEOs to avoid value-destroying acquisitions and search for value-

improving acquisitions, we need to address two types of endogeneity issues.

The �rst issue is in the form of reverse causality. That is, CEOs planning to pursue empire building or

make unpro�table acquisitions could �rst structure their compensation to have low pay-for-performance

sensitivity. To examine this possibility, we use changes in PPS as an alternative measure in our multino-

mial logit regressions. The idea is that if an increase in PPS (i.e. improvement in interest-alignment)

leads to lower probability of engaging in value-destroying acquisitions but higher probability of value-

improving acquisitions, then the e¤ect between PPS and probability to acquire is more likely to be causal.

Since option grants can be lumpy over time, we �rst calculate the two-year moving average of PPS. The

smoothing process, if anything, biases against us �nding results that changes in PPS a¤ect decisions to

acquire. The results are in Table VIII Columns 1-2. Our main result continues to hold. Increase in PPS

lowers the probability of value-destroying acquisitions and increases the probability of value-enhancing

acquisitions.

[INSERT TABLE VIII HERE]

The other form of the endogeneity problem is an omitted variable bias. The concern is that some

unobservable acquirer traits could be responsible for both the level of PPS and the bank�s probability to

18

acquire. To address this concern, we perform a two-stage estimation. In the �rst stage, we estimate a

regression to predict acquirer�s announcement return using the speci�cation in Equation (1), excluding

PPS. In the second stage, instead of using the actual returns to separate out winners from losers, we

estimate a multinomial logit model using the predicted returns from the �rst stage. We identify value-

improving acquisitions as transactions with predicted returns greater than zero and value-destroying

acquisitions as transactions with predicted returns less than zero. We report results in Table VIII Columns

3-4. Our main �nding continues to hold. Higher PPS prevents value destroying acquisitions, while

promoting value enhancing acquisitions.

In the previous section, we show that PPS signi�cantly predicts announcement returns for small and

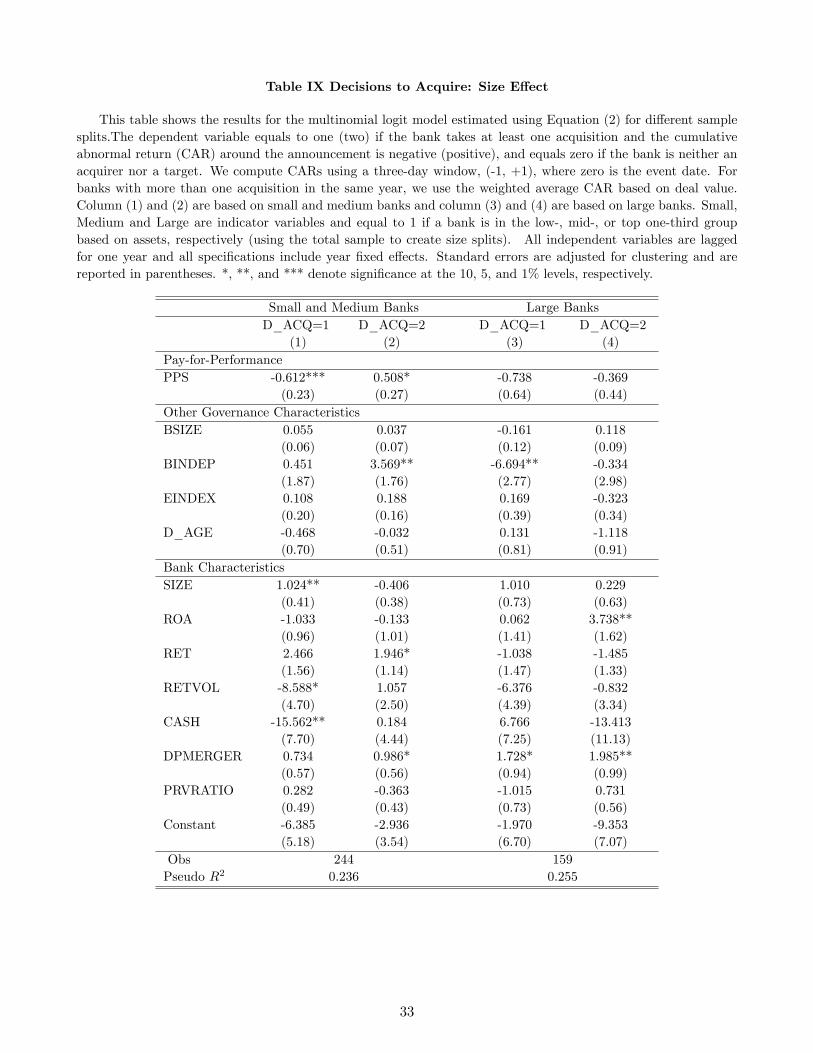

medium banks, but not large banks. Here, we investigate how PPS a¤ects the acquisition decisions

of banks having di¤erent opportunity sets. In Table IX we estimate the decision regression separately

for our large banks and the rest of the sample. We observe that in large banks, PPS neither helps to

prevent bad acquisitions nor does it promotes good acquisitions. For the rest of the banks, PPS continues

to incentivize the CEO to make sound acquisition decisions. This �nding is consistent with our early

�ndings from return regressions.

One plausible explanation for the insigni�cance of PPS in large banks is that it is caused by the CEO�s

self-serving interests. As bank size grows, total compensation for CEOs may rise to such a high level that

the marginal e¤ect of PPS on behavior diminishes. For large bank acquisitions, the absolute dollar value

of the CEO compensation gain based on the size of the target alone is likely to be extremely large. Thus,

the marginal impact of the additional gain from increasing the stock return may be relatively small. This

argument has some support in Bliss and Rosen (2001), where they show that large-bank CEOs try to

grow bank size to increase their compensation level. Our sample also con�rms the observation that the

CEO-pay increases as bank size grows. For example, the annual CEO total compensation averages to

$2.54 million in small and medium bank and it is $4.21 million for large banks and $12.33 million for

mega banks. The correlation between bank size and total compensation is 80%. The weight of PPS

within the total compensation also di¤ers signi�cantly. The ratio of PPS to total compensation is 10%

for large banks and almost doubles to 19% for the rest of the banks.

To further test the e¤ect of the level of compensation on the marginal e¤ect of PPS, we split the

acquirers in two groups based on total cash compensation (which includes salary, bonus, and other annual

compensation). In unreported regressions, we �nd that PPS has a signi�cant e¤ect on announcement

19

CAR for acquirer CEOs with low and medium cash compensation (the bottom and mid one-third), but

not for CEOs with high cash compensation (top one-third).

Thus, when a bank exceeds a certain size, the stock market might discount claims that PPS will provide

meaningful managerial incentives for the acquiring bank to achieve increased operational e¢ ciencies and

economies of scale and scope. This argument also has support in Penas and Unal (2003). They show

that medium size banks, which attain asset size of $100 billion as a result of the merger (and attaining

a TBTF status), experience a decline in credit spreads, but the credit spreads of banks exceeding this

threshold do not show the same pattern. Therefore, it is plausible that TBTF status replaces PPS to be

the dominant factor that aligns interests of managers and shareholders.

[INSERT TABLE IX HERE]

5 Performance Change Following the Acquisition

So far, we show that acquirers with higher PPS have better abnormal returns around acquisition

announcements and that higher PPS reduces value-reducing acquisitions and promotes value-enhancing

acquisitions ex-ante. In this section, we analyze changes in performance following the acquisitions to

examine whether the positive reaction on the stock market can be justi�ed by real economic gains from

the acquisitions.

Studies on banks�performance-change after an acquisition provide mixed results. Cornett and Tehranian

(1992) show that merged banks outperform the industry in the post-merger period, while Pillo¤ (1996)

�nds no substantial evidence that mergers are associated with any signi�cant change in performance.

We use four performance measures to capture changes around the acquisitions: return on assets

(ROA), return on equity (ROE), an e¢ ciency ratio, and long run buy and hold abnormal return (BHAR).

We calculate ROA as the ratio of operating income to total book value of assets and ROE as the ratio of

operating income to total book value of equity.19 The e¢ ciency ratio is similar to that used in Cornett

and Tehranian (1992) and we compute it as the ratio of book value of assets to the number of full-time

employees. While ROA and ROE measure the overall operating performance to capital invested, and the

e¢ ciency ratio captures the employee productivity.19We measure the operating income as pre-tax income minus special items plus interest and related expense minus (the total

periodic expense for using deposit accounts of customers plus total periodic expense for using interbank deposit accounts)plus depreciation and amortization.

20

We calculate changes of ROA and ROE based on quarterly data to better re�ect the timing of the

acquisition. Since it may take several years for an acquirer to completely absorb a target, we use a three-

year window to allow full integration. That is, changes are computed as the di¤erence between a ratio in

the �rst quarter after the acquisition became e¤ective and that of twelve quarters later. We use the �rst

quarter following the e¤ective date to measure pre-acquisition performance assuming that following the

acquisition, earnings and assets from both parties are simply pooled together under the acquirer. Out of

the 80 acquirer years in which other governance variables are available, we have 73 acquirer years with

changes of ROA available and 62 acquirer years with changes of ROE available.20 For e¢ ciency ratio, we

use the annual data since Compustat does not have quarterly data on the number of employees.

To calculate the holding period returns (BHAR), we use an approach similar to Kothari and Warner

(1997), and Barber and Lyon (1997). First we calculate monthly buy-and-hold returns (BHR) by com-

pounding monthly returns calculated using the monthly returns from CRSP over a (0, 36) month horizon.

If a sample bank is delisted before the end of the time horizon, the BHR of that particular bank over

that time horizon is calculated over the period from the �rst to the last dates when return index data are

available in CRSP. We then calculate BHRs of the CRSP Value matched portfolios over the same time

horizon. Finally, BHARs are calculated by subtracting the corresponding average BHRs of benchmark

index from the relevant average BHRs of our sample banks.

We use the following speci�cation to estimate the impact of PPS on changes in performance:

�PERFi;t = 0 + 1PPSi;t�1 + 2Ai;t�1 + 3Di;t + 4Gi;t�1 + Ft + !i;t (3)

The dependent variable, �PERFi;t is the change of performance for acquirer i with acquisition in year t

(for the BHAR estimation, �PERFi;t is the BHAR for the (0,t) horizon) , and our key explanatory vari-

able is the pay-for-performance sensitivity for the acquirer bank CEO before the acquisition (PPSi;t�1).

We control for acquirer�s characteristics (Ai;t�1), deal characteristics (Di;t), and other governance vari-

ables (Gi;t�1). Ft is the year �xed e¤ect, and !it is the error term.

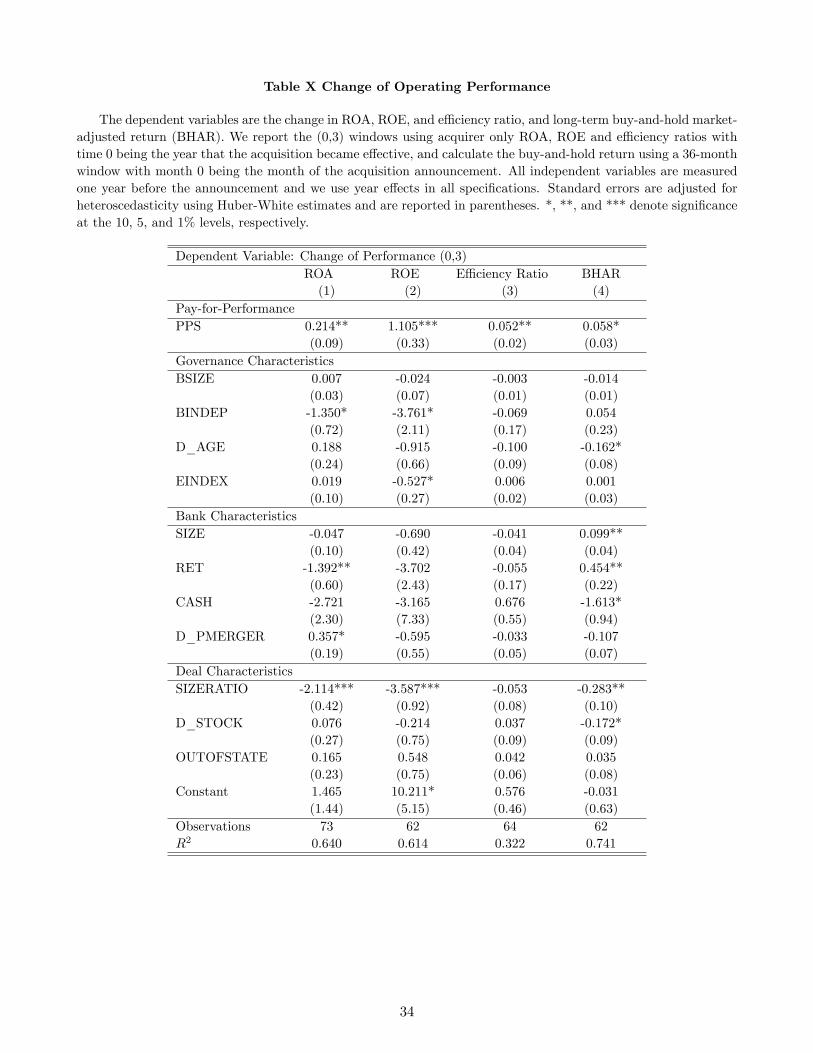

Table X reports the results. For all four measures, we run separate regressions including governance

variables. Columns 1-4 show the results for ROA, ROE, the e¢ ciency ratio, and BHAR, respectively.

20We lose observations on ROA and ROE on acquisitions from later years due to missing value for future years (threeyears after the acquisition) and we lose a few more observations on ROE due to missing values of book value of equity inCompustat.

21

The estimated coe¢ cients for PPS are positive and signi�cant across all speci�cations. Banks with higher

pay-for-performance sensitivity show a greater improvement in their operating performance following an

acquisition. A one unit increase in the log of PPS leads to a 0:21 percent point increase in changes of

ROA, suggesting a positive bene�t for all stakeholders. Focusing on equity holders, we �nd that they

experience even better improvements in their wealth - a one unit increase in the log of PPS leads to a 1:11

percent point increase in changes of ROE. We also observe that higher PPS is signi�cantly associated

with gains in employee productivity, such that managerial incentives lead to more assets being managed

by fewer number of employees. Long run returns can be noisy since they include numerous factors in

addition to the acquisition itself. Nevertheless, we �nd that PPS has a signi�cant impact (at 10%) - a

one unit increase in the log of PPS leads to a 5:8 percent point increase in the three-year long run return.

These �ndings suggest that high PPS results in improvements in long-run performance.

[INSERT TABLE X HERE]

Meanwhile, we �nd that other governance variables have considerably weak e¤ect on changes in

performance. For deal characteristics, we �nd that acquisitions with lower relative size ratio show more

improvements in ROA and ROE, and lead to higher long-run stock return.

Bank mergers during our sample period are split between the use of purchase and pooling methods

of accounting. Under the pooling method, the assets are combined at their book value while under the

purchase method, the assets of the target company are recorded at their purchase price. The di¤erence in

accounting methods can potentially a¤ect the calculation of ROA and ROE. To control for it, we add an

indicator variable for whether pooling method is used in our estimation and our results continue to hold.

Given our �ndings on size e¤ect, we also investigate the post-performance by size group. Our results also

hold when we use a (-1,3) window in which we examine changes from one year before to three years after

the acquisition.21

6 Conclusion

In this paper, we examine the relation between executive compensation and shareholder interests

in bank mergers. Speci�cally, we show how pay-for-performance sensitivity in executive compensation

21Results are not reported but are available upon request.

22

a¤ects the acquirers�stock returns around the announcement, the probability of acquiring ex-ante, and

changes in operating performance after acquisitions.

We �nd that banks with higher pay-for-performance sensitivity have signi�cantly higher stock re-

turns around the acquisition announcements. Acquirer banks in the High-PPS group outperform their

counterparts in the Low-PPS groups by 1:43% in a three-day window.

We also show that incentive-based compensation accomplishes two objectives simultaneously in align-

ing the interests of the CEO with the interests of shareholders. On the one hand, higher PPS lowers the

probability of engaging in value-destroying acquisitions. On the other hand, it encourages CEOs to search

for acquisitions that are consistent with shareholder value maximization. The dual role of incentive-based

compensation is a novel �nding in our paper and it provides insights into the channels through which

incentive compensation may a¤ect corporate decisions. Stock markets view acquisitions made by CEOs

with high pay-for-performance sensitivity as more pro�table and react favorably to those announcements.

We provide evidence that those positive reactions can be justi�ed by changes in operating performance

following acquisitions. Banks in which CEOs�interests are better aligned experience greater improvement

in operating performance.

It is worth pointing out that given the high leverage ratio and the implicit government guarantee

on banks, the incentives of all stake-holders (including the FDIC, bond-holders, shareholders, and tax

payers) are not always aligned (Buser, Chen, and Kane,1981; and Kane, 2004). In fact, other stake-holders

can be hurt from higher PPS if the higher abnormal returns from acquisitions come at the expense of

other stake-holders. As a result, decisions that bene�t the shareholders may not always be optimal for

other stake-holders. We provide additional insight into this dynamic. High PPS creates value through

bigger improvements in operating performance following the acquisitions and a lower likelihood of making

unpro�table investments. Both bene�ts accrue to not only shareholders, but other stakeholders as well.

Our study suggests that regulation may not fully substitute for managerial incentives. Although

banks are regulated to a much higher degree, incentive-based compensation can still signi�cantly improve

shareholders�value in the context of acquisitions. One explanation for this observation is that regulation

and incentive-based compensation each have their own relative strengths in monitoring. Therefore, our

�ndings justify the close regulatory scrutiny of executive compensation at �nancial institutions following

the sub-prime crisis. If incentive-based compensation a¤ects the incentives of bank managers to take

23

actions that are consistent with value maximization, then regulators can extract valuable information on

the health of the banks by adding this information to the regulatory process.

We also �nd that the motivating e¤ect of PPS is stronger for smaller banks and that PPS fails to

be an e¤ective tool in motivating the CEOs of larger banks to enhance shareholders value. We explain

the di¤erence by noting that for large bank acquisitions, the increase in CEO�s compensation due to

size e¤ect is likely to be very large and therefore the marginal impact of PPS is relatively small. The

recent regulatory steps that aim to curb risk taking at large banks through restraints on compensation

structures are certainly warranted. However, the insigni�cance of PPS for large banks indicates that it

may be di¢ cult to e¤ectively in�uence the quality of acquisitions through pay for performance in these

institutions.

24

Table I Summary Statistics: Acquisitions by Year

Panel A describes the deals in our sample by year. Deal value is de�ned by SDC as the total value of con-sideration paid by the acquirer to the target. MVE denotes the market value of equity of the acquirer. TAssetand AAsset denote the total assets of the target and the acquirer, respectively. Panel B presents the number ofacquisitions taken by banks during our sample period. All deal data are taken from SDC Platinum Mergers andAcquisitions database.

Panel A: Deals by Year

Number of Deal Value Acq. MVE Deal Value/ Target Asset/Deals (in $ million) (in $ million) Acq. MVE Acq. Asset

1991 3 1,565 4,136 0.31 0.291992 4 395 1,264 0.29 0.231993 14 273 2,744 0.13 0.091994 11 391 3,921 0.11 0.081995 10 1,089 3,133 0.31 0.191996 10 286 1,310 0.23 0.131997 13 1,153 4,020 0.29 0.151998 21 816 4,709 0.17 0.121999 22 679 9,255 0.12 0.112000 13 1,546 15,650 0.10 0.132001 6 328 4,708 0.17 0.112002 4 246 10,027 0.08 0.052003 10 5,511 16,743 0.19 0.132004 9 9,101 17,557 0.29 0.162005 9 4,623 26,048 0.18 0.14Total 159 1,742 8,364 0.18 0.13

Panel B: Number of Deals by AcquirersNumber of Acquisitions Frequency Percent1 32 50.002 9 14.063 11 17.194 4 6.255 or more 8 12.50Total 64 100

25

Table II Summary Statistics: Deal Characteristics and Bank Characteristics

Panel A summarizes the deal characteristics for acquirers. Panel B compares acquirers with the benchmarksample, which contains all bank�years that are not related to mergers (where the bank is neither an acquirer nor atarget). TA is the book value of assets. N shows the number of bank years. Banks that make multiple acquisitionsin a single year are only counted once per year. We use pairwise t-tests to examine whether there is a signi�cantdi¤erence between the benchmark and the acquirer sample. *, **, and *** denote signi�cance at the 10, 5, and 1%levels, respectively.

Panel A: Deal Characteristics

Mean STDEV MedianPCT_STOCK 0.89 0.25 1.00PCT_CASH 0.11 0.25 0.00ALLSTOCK 0.79 0.38 1.00ALLCASH 0.05 0.22 0.00D_STOCK 0.82 0.41 1.00SIZE_RATIO 0.18 0.24 0.20REL_SIZE 0.13 0.15 0.08OUTOFSTATE 0.70 0.46 1.00N 159

Panel B: Bank CharacteristicsAcquirers Benchmark

Mean Median Mean MedianTA 58,928 21,247 54,494 17,336MVE 10,046 3,487* 7,999 2,510RET 0.23 0.19 0.21 0.17RET_VOL 0.22** 0.20* 0.24 0.22ROA (in %) 1.21 1.20 1.19 1.19PRV 0.94 0.60 0.92 0.59CASH 0.07 0.06 0.07 0.06N 109 568

26

Table III Summary Statistics: Governance Variables

This table provides summary statistics on governance variables. Panel A compares the acquirer banks withthe benchmark sample, and Panel B presents the correlation matrix. A bank is an acquirer if it makes at leastone acquisition in the current year. The benchmark sample contains all bank years that are not related to mergers(where the bank is neither an acquirer nor target). N is the number of bank years. Banks that make multipleacquisitions in a year are only counted once per year. We use pairwise t-tests and rank tests to examine whetherthere is a signi�cant di¤erence between the benchmark and the acquirers in mean and median, respectively.*, **,and *** denote signi�cance at the 10, 5, and 1% levels, respectively.

Panel A: Summary Statistics: Acquirer Sample and Benchmark Sample

Acquirers Benchmark

Mean Median N Mean Median NCompensation CharacteristicsCash Comp ($ 000�s) 1,546 1,160 109 1,599 1,122 568Total Comp ($ 000�s) 3,978 2,393 109 4,170 2,315 568Pct_CashComp 0.51 0.50 109 0.54 0.52 568Stock PPS ($ 000�s) 269 97 109 298 127 568Option PPS ($ 000�s) 210 77 109 217 86 568Total PPS ($ 000�s) 480 217 109 515 268 568Board CharacteristicsBSIZE 16.3** 16.0** 80 15.7 15.0 323BINDEP 0.69 0.71 80 0.69 0.71 323D_CEO 0.90 1.00 80 0.94 1.00 323Anti-Takeover ProvisionsEINDEX 2.76 3.00 80 2.62 3.00 323GINDEX 10.07 10.00 80 10.18 11.00 323CBOARD 0.76 1.00 80 0.67 1.00 323CEO CharacteristicsTenure 5.3 3.0 109 6.0 5.0 568Age 55.7* 55.0* 109 56.7 57.0 568

Panel B: Correlation of Governance Variables

Total PPS BSIZE BINDEP D_CEO EINDEX GINDEX TENURE AGETotal PPS 1BSIZE -0.004 1BINDEP -0.039 0.053 1D_CEO 0.079� 0.094�� 0.019 1EINDEX -0.286��� -0.244��� -0.055 0.030 1GINDEX -0.282��� -0.154��� 0.034 0.069 0.757��� 1TENURE 0.129��� 0.064��� -0.083 0.134��� -0.102��� -0.045 1AGE 0.212��� 0.151��� -0.155��� 0.171��� -0.174��� -0.053 0.316��� 1

27

Table IV Acquirer Stock Returns: Univariate Analysis

This table summarizes acquirer returns in general and for di¤erent PPS groups. Panel A shows the cumulativeabnormal stock returns (CARs) in percentages for acquirers using a three-day and a �ve-day window where dayzero is the event day. Panel B summarizes the PPS for each group based on total PPS where the low-PPS grouphas the bottom third of the observations, and the high-PPS group has the top third of the observations. PPS isin thousands of dollars. Panel C compares CARs between acquirers in di¤erent PPS groups. T- and signed-ranktests are performed to examine whether the mean or median returns are signi�cantly di¤erent between high-PPSand low-PPS groups. *, **, and *** denote signi�cance at the 10, 5, and 1% levels, respectively.

Panel A: Summary Statistics on Acquirer Returns (in %)

Mean STDEV. Median Min Max p-value p-value(t-test) (sign-rank test)

(-1, 1) 0.21 2.28 0.33 -8.78 8.82 0.25 0.19(-2, 2) 0.24 3.20 0.22 -10.65 10.96 0.35 0.39N 159

Panel B: Summary Statistics on PPS Groups (in $000�s)

PPS Group Mean Median Min Max NLow 77 57 0 289 51Medium 273 265 84 676 57High 1,037 801 164 3,929 51Total 455 234 0 3,929 159

Panel C: Acquirer Returns by PPS Group (in %)CAR (-1, 1) CAR (-2, 2)

PPS Groups Mean Median Mean MedianLow -0.18 -0.43 -0.35 -0.44Medium 0.12 0.24 0.27 0.38High 0.70 0.82 0.78 0.49t-test (high �low)(p-values) -2.03(0.04) -1.70(0.09)Signed-Rank (high �low)(p-values) -2.27(0.02) -1.94 (0.05)

28

Table V: Acquirer Stock Returns: Multivariate Analysis

This table shows results for regressions using Equation(1) where the dependent variable is the acquirer�s three-day cumulative abnormal stock returns (CARs) around the acquisition announcement. D_MPPS and D_HPPSare indicator variables that equal one if the acquirer has pre-acquisition PPS in the middle or top one-third amongall banks in that year, respectively. All independent variables are measured one year before the announcement, andwe control for year �xed e¤ects. We use Huber-White adjusted standard errors. *, **, and *** denote signi�canceat the 10, 5, and 1% levels.

Dependent Variable: CAR(-1,1)(1) (2) (3) (4) (5) (6)

Pay-for-PerformancePPS 0.502*** 0.624***

(0.16) (0.20)SPPS 0.293**

(0.15)OPPS 0.350***

(0.10)D_MPPS 0.928** 0.638

(0.41) (0.50)D_HPPS 1.425*** 1.267**

(0.44) (0.54)Other Governance CharacteristicsBSIZE -0.036 -0.010

(0.06) (0.06)BINDEP -0.148 -0.084

(1.56) (1.55)D_AGE 0.181 0.359

(0.51) (0.50)EINDEX -0.371* -0.272

(0.19) (0.20)Bank CharacteristicsSIZE -0.552*** -0.397** -0.480*** -0.488*** -0.657** -0.517*

(0.19) (0.19) (0.18) (0.18) (0.28) (0.27)ROA 0.383 0.500 0.274 0.555 0.648 0.989

(0.61) (0.63) (0.60) (0.62) (0.81) (0.80)CASH 7.017 6.401 8.065* 6.302 0.991 0.467

(4.48) (4.66) (4.38) (4.53) (5.86) (5.81)D_PMERGER -0.471 -0.601 -0.035 -0.515 -1.327** -0.955

(0.45) (0.47) (0.47) (0.45) (0.58) (0.59)Bank CharacteristicsSIZE_RATIO -0.607 -0.200 -1.110 -1.164 -3.265*** -3.683***

(0.72) (0.74) (0.71) (0.72) (0.81) (0.80)D_STOCK 0.294 0.284 0.022 0.212 0.554 0.293

(0.49) (0.51) (0.47) (0.48) (0.58) (0.57)OUTOFSTATE 0.174 0.155 0.259 0.276 0.132 0.386

(0.40) (0.42) (0.39) (0.40) (0.49) (0.50)Constant 3.889* 3.223 4.096* 4.864** 7.219* 5.389

(2.26) (2.33) (2.24) (2.31) (3.68) (3.65)Observations 159 159 159 159 116 116R2 0.162 0.123 0.197 0.188 0.386 0.408

29

Table VI: Acquirer Stock Returns: Multivariate Analysis (Robustness Checks)

This table shows results from regressions using Equation (1) where the dependent variable is the acquirer�sthree-day cumulative abnormal stock returns (CARs) around acquisition announcement. All independent variablesare measured one year before the announcement, and we control for year �xed e¤ect. Small, Medium and Large areindicator variables and equal to 1 if a bank is in the low-, mid-, or top one-third group based on assets, respectively.We de�ne size indicators based on the acquirer sample for (1) and entire sample for (2). In columns (3) and (4), wereport results based on sample splits around 1999. *, **, and *** denote signi�cance at the 10, 5, and 1% levels.We use Huber-White adjusted standard errors.

Dependent Variable = CAR(-1,1)(1) (2) (3) (4)

Pay-for-Performance 1992-1999 2000-2005PPS 0.632*** 0.379*

(0.23) (0.21)PPS * Small 0.551*** 0.483*

(0.21) (0.26)PPS * Medium 0.489** 0.482**

(0.20) (0.19)PPS * Large -0.148 -0.006

(0.25) (0.25)Medium -0.531 -0.536

(1.54) (1.64)Large 2.665 1.536

(1.81) (2.00)Bank CharacteristicsSIZE -0.443 -0.750**

(0.32) (0.28)ROA 0.626 0.637 0.413 0.916

(0.58) (0.59) (0.79) (1.09)CASH 5.349 4.270 6.181 18.707

(3.79) (3.85) (5.24) (12.54)D_PMERGER -0.357 -0.354 -1.007* -0.658

(0.43) (0.44) (0.58) (0.95)Deal CharacteristicsSIZE_RATIO 0.629 0.237 -2.444*** 0.640

(0.67) (0.69) (0.86) (1.92)D_STOCK 0.204 0.066 0.432 0.054

(0.42) (0.43) (0.75) (0.58)OUTOFSTATE 0.450 0.225 -0.258 0.499

(0.39) (0.39) (0.52) (0.71)Constant -3.577*** -2.922** 3.427 3.468

(1.33) (1.44) (3.82) (2.32)Observations 159 159 108 51R2 0.126 0.099 0.066 0.041

30

Table VII Decisions to Acquire