Paul Ahlstram Alta Ventures -...

45

1 MitaTech Talks Cross Border Investing Presentation, 2016 @PaulAhlstrom

Transcript of Paul Ahlstram Alta Ventures -...

11

MitaTech TalksCross Border Investing Presentation, 2016

@PaulAhlstrom

22

2006 to 2016 Investing in Mexican Innovation: Cross-border venture investing lessons learned

33

Heber M. Cluff

President Diaz said– The colonists were not only welcome in Mexico, but the Government was anxious to have them help in the development of the country.

44

Pioneer

VS

55

Phase I: The Alta Selection Process

Primary & Secondary Research In Search of the Next Emerging Market…

66

In Search of Stability & Growth The Ring of Fire

Source: Data from World Economic Outlook Database 2012, The Ring of Fire, PIMCO, 2009

Macroeconomic Fundamentals

-15.0%

-12.5%

-10.0%

-7.5%

-5.0%

-2.5%

0.0%

2.5%

5.0%

7.5%

10.0%

12.5%

0.0% 50.0% 100.0% 150.0% 200.0% 250.0%

Public Sector Deficit (% of

GDP)

Chile

Australia

Sweden

Mexico

Finland

Norway

Brazil

NetherlandsSpain

Germany

UK

Canada

France

USAIreland

Portugal

Italy

GreeceJapan

Public Sector Debt (% of GDP)

Argentina

Denmark

Colombia

77

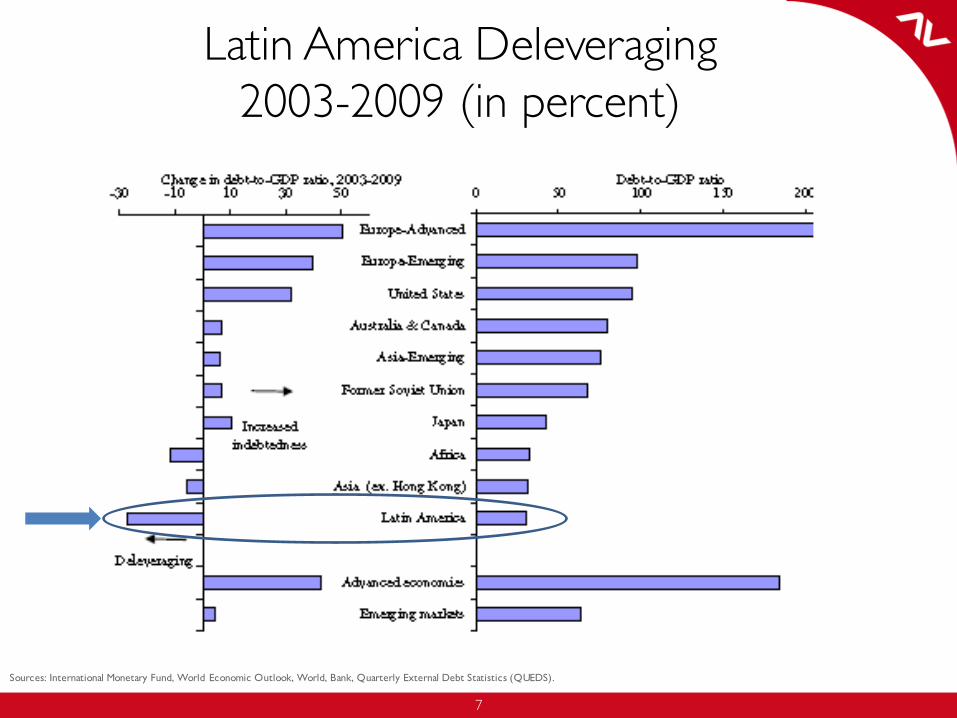

Latin America Deleveraging 2003-2009 (in percent)

Sources: International Monetary Fund, World Economic Outlook, World, Bank, Quarterly External Debt Statistics (QUEDS).

88

Continued Growth in Emerging Markets – Rising Tide

Emerging Markets

Source: IMF, World Economic Outlook Database, 2009

GDP Growth In Emerging Markets Predicted to Outperform Developed Countries

GDP Growth Predicted to Remain Positive in Most Emerging Markets

99

The centers of rapid wealth creation are shifting from Developed to Emerging Markets

Source: IMF, World Economic Outlook Database, April 2012,Data for years 2012-2019 are estimates

Contribution to Global GDP Growth (Share of World Total)

Key Drivers are:• Rapid industrialization• Significant income growth

• Improved long-term household financial confidence

Emerging Markets GDP Growth1995 to 2005 Snapshot

Advanced Economies

Emerging & DevelopingEconomies

30%35%40%45%50%55%60%65%70%

Emerging markets are responsible for over half of the world’s GDP

10

10

Countries of the WorldAlbania Chad Grenada Lesotho Papua New Guinea SwazilandAlgeria Chile Guatemala Liberia Paraguay SwedenAngola China Guinea Libya Peru SwitzerlandAntigua and Barbuda Colombia Guinea-Bissau Lithuania Philippines Syrian Arab RepublicArgentina Comoros Guyana Luxembourg Poland Taiwan Prov of ChinaArmenia Costa Rica Haiti Madagascar Portugal TajikistanAustralia Croatia Honduras Malawi Qatar TanzaniaAustria Cyprus Hong Kong SAR Malaysia Republic of Congo ThailandAzerbaijan Czech Republic Hungary Maldives Republic of Yemen The BahamasBahrain Dem. Rep. of Congo Iceland Mali Romania The Gambia

BangladeshDem. Rep. of Timor-Leste India Malta Russia Togo

Barbados Denmark Indonesia Mauritania Rwanda TongaBelarus Djibouti Iraq Mauritius Samoa Trinidad and TobagoBelgium Dominica Ireland Mexico Saudi Arabia TunisiaBelize Dominican Republic I. Rep. of Afghanistan Moldova Senegal TurkeyBenin Ecuador I. Rep. of Iran Mongolia Serbia TurkmenistanBhutan Egypt Israel Montenegro Seychelles UgandaBolivia El Salvador Italy Morocco Sierra Leone UkraineBosnia and Herzegovina Equatorial Guinea Jamaica Mozambique Singapore United Arab EmiratesBotswana Eritrea Japan Myanmar Slovak Republic United KingdomBrazil Estonia Jordan Namibia Slovenia United StatesBrunei Darussalam Ethiopia Kazakhstan Nepal Solomon Islands Uruguay

Bulgaria Fiji Kenya NetherlandsSÒo TomÚ and PrÝncipe Uzbekistan

Burkina Faso Finland Kiribati New Zealand South Africa VanuatuBurundi F. Y. Rep. of Macedonia Korea Nicaragua Spain VenezuelaCote d'Ivoire France Kosovo Niger Sri Lanka VietnamCambodia Gabon Kuwait Nigeria St. Kitts and Nevis ZambiaCameroon Georgia Kyrgyz Republic Norway St. Lucia ZimbabweCanada Germany Lao People's D.R. Oman St. Vincent &GrenadinesCape Verde Ghana Latvia Pakistan SudanCentral AfricanRepublic Greece Lebanon Panama Suriname

11

11 Albania Chad Grenada Lesotho Papua New Guinea SwazilandAlgeria Chile Guatemala Liberia ParaguayAngola China Guinea Libya PeruAntigua and Barbuda Colombia Guinea-Bissau Lithuania Philippines SyrianArabRepublicArgentina Comoros Guyana PolandArmenia Costa Rica Haiti Madagascar Tajikistan

Honduras Malawi TanzaniaMalaysia Republic of Congo Thailand

Azerbaijan Hungary Maldives Republic of YemenDem. Rep. of Congo Mali Romania The Gambia

BangladeshDem. Rep. of Timor-Leste India Russia Togo

Barbados Indonesia Mauritania Rwanda TongaBelarus Djibouti Iraq Mauritius Samoa

Dominica Mexico TunisiaBelize DominicanRepublic I. Rep. of Afghanistan Moldova Senegal TurkeyBenin Ecuador I. Rep. of Iran Mongolia Serbia TurkmenistanBhutan Egypt Seychelles UgandaBolivia El Salvador Morocco Sierra Leone UkraineBosnia and Herzegovina Equatorial Guinea Jamaica MozambiqueBotswana Eritrea MyanmarBrazil Jordan Namibia

Ethiopia Kazakhstan Nepal SolomonIslands UruguayBulgaria Fiji Kenya SÒoTomÚ and PrÝncipe UzbekistanBurkina Faso Kiribati South Africa VanuatuBurundi F. Y. Rep. of Macedonia Nicaragua VenezuelaCote d'Ivoire Niger Sri Lanka VietnamCambodia Gabon Nigeria St. Kitts and Nevis ZambiaCameroon Georgia KyrgyzRepublic St. Lucia Zimbabwe

Lao People's D.R. St. Vincent &GrenadinesCape Verde Ghana Latvia Pakistan SudanCentral African Republic Lebanon Panama Suriname

*Based on IMF Information.

Narrow the Field: Emerging MarketsPer capita GDP below $14k in 2005

12

12Algeria Chile

China PeruColombia Philippines

Argentina Poland

Malaysia ThailandHungary

RomaniaBangladesh India Russia

Indonesia

MexicoTurkey

I. Rep. of IranEgypt

Morocco Ukraine

BrazilKazakhstan

South AfricaVenezuelaVietnam

Nigeria

Pakistan

Narrow the Field: Larger EconomiesGDP over $75 billion in 2005

*Based on IMF Information.

13

13China

Philippines

Thailand

Bangladesh India RussiaIndonesia

MexicoTurkey

I. Rep. of IranEgypt

Brazil

VietnamNigeria

Pakistan

Narrow the Field: Larger Populations over 50 Million People

*Based on IMF Information.

1414

14

Country Population GDP 2009 (billion)

GDP per capita

China 1,334.74 $ 4,909 * $ 3,678 India 1,199.06 $ 1,236 * $ 1,031 Indonesia 231.55 $ 539 $ 2,329 Brazil 191.48 $ 1,574 $ 8,220 Bangladesh 165.71 $ 95 * $ 574Pakistan 163.77 $ 167 * $ 1,017 Nigeria 151.87 $ 173 * $ 1,142 Russia 141.39 $ 1,229 * $ 8,694 Mexico 107.55 $ 875 $ 8,135 Philippines 92.23 $ 161 $ 1,746 Vietnam 87.21 $ 92 * $ 1,060 Egypt 76.70 $ 188 * $ 2,450 Iran 74.10 $ 330 * $ 4,460 Turkey 70.54 $ 615 $ 8,723 Thailand 66.98 $ 264 $ 3,940

Source: International Monetary Fund

Narrowed Field: Largest 15 Emerging Markets

*Estimated

1515

• Launched in 2005, GES was developed to capture the factors that crucially affect the ability of an economy to grow.

• This tool helps Goldman to predict if their BRIC theory will become a reality in the next 20-40 years. (Variables include inflation, government deficit, external debt, investment rate, penetration of phones, PC’s, and Internet, education, life expectancy,political stability, rule of law and corruption)

Source: Goldman Sachs

BRICS and N-11 Goldman Sachs Growth Environment Score (GES) 2009

Narrowed the Field: BRICS + N11Goldman Sachs Growth Environment Score

1616

Alta Analysis of Key Indicators BRICS vs. other Markets (as of 2005)

17

‘05 Summary Analysis of Top LatAmMexico Brazil Chile Argentina Columbia

Population 114,975,406 199,321,413 17,067,369 42.192,494 45,239,079

GDP GDP Growth: 3.2%PerCapita: $10,514

GDP Growth: 3.2%Per Capita: $12,465

GDP Growth: 5.5%Per Capita:

GDP Growth: 9.2%Per Capita: $11,453

GDP Growth: 5.0%Per Capita: $8,127

Strength/Opportunities

- Relatively low competition- Fast-growing IT market- Skilled labor- Open to foreign investment- Standard corporate regulations- Strong public and private universities- Huge capital gap

- Market Size- Economic stability- Political stability- Trained IT labor- Strong US business presence- Strong exit markets/liquidity

- Ease to do business- Very low trade barriers- Economic stability- Political stability- Highly trained IT labor- Strong US business presence- Channel of distribution follows US models- Port of entry for Asian products- Great base for South American operations

- Demand for technology products- Undergoing positive economic changes- US business presence- World class software and design talent- High level of sophistication and quality of life

- Demand for technology products- Government sector offers good opportunities- Channel of distribution- Some US business presence- Dramatically improved public safety

Weaknesses/Risks

- Weak framework for fund activity- Bankruptcy & judicial system remains inefficient- Perceptions of corruption- Concerns about ongoing drug trade

- Regulated economy- Bureaucratic government & legal system- Time required to start a business (58 days)- Difficult to transfer profits back to US- Trade barriers- Cost of capital- Government is the largest IT customer- Social discrepancies- High crime rates

- Small internal market- High shutdown costs- Business permitting process

- Relatively smallcorporate market in spite of US presence- Currency fluctuation- Government debt- Government perception- Bureaucratic environment- Social discrepancies- High crime rates

- Social discrepancies- Columbian peso fluctuations- Relatively high cost of labor- Perception of safety

1818

Top Choices: Mexico & the BRICS (Based on 2005-2009Analysis)

• Trending First choice*: Mexico • Second place: Brazil• Solid option: India• Largest market: China• Fading star: Russia

* based on market PE/VC attractiveness and underserved capital

19

Hypothesis: Mexico

2020

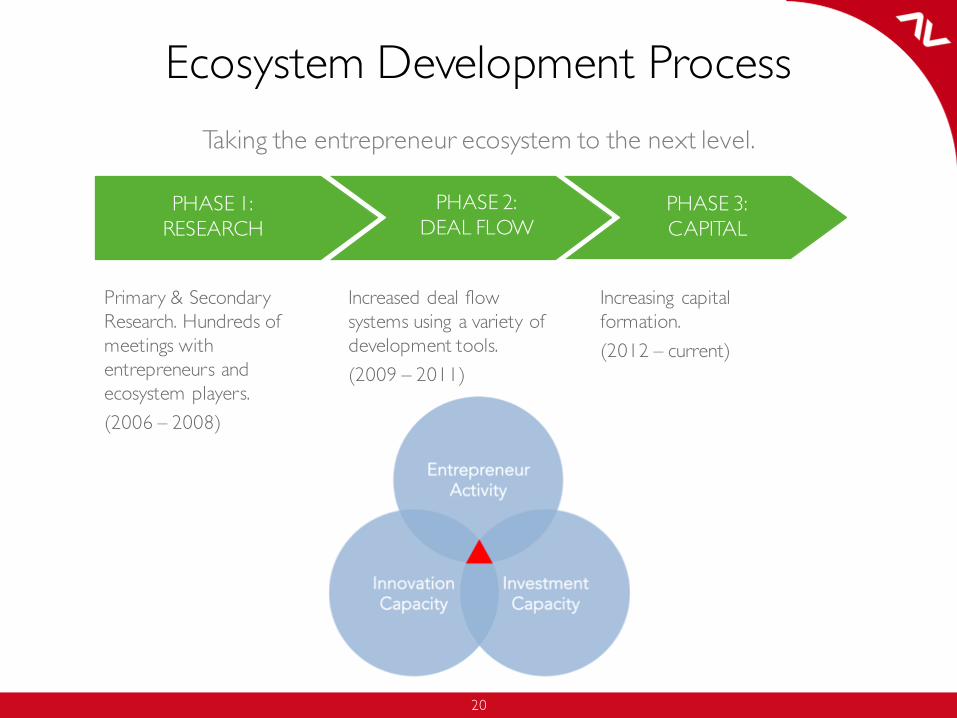

Taking the entrepreneur ecosystem to the next level.

PHASE 1:RESEARCH

PHASE 2:DEAL FLOW

PHASE 3:CAPITAL

Primary & Secondary Research. Hundreds of meetings with entrepreneurs and ecosystem players.(2006 – 2008)

Increased deal flow systems using a variety of development tools.(2009 – 2011)

Increasing capital formation.(2012 – current)

20

Ecosystem Development Process

2121

Sovereign Debt Rating as of 2013

Country Debt RatingChile A+Mexico BBB+Brazil BBBPeru BBBColumbia BBB-Uruguay BBB-

Country Debt RatingParaguay BB-Venezuela B+Bolivia B+Argentina BEcuador B-

Country Debt RatingChina AA-Russia BBBIndia BBB-

Investment Grade Non-Investment Grade

Non-Latin America Countries

Source: Standard & Poor’s.

21

Phase 1 Secondary Research: Mexico’s Sovereign Risk Environment

2222

81%

4%15%

0%

20%

40%

60%

80%

100%

US Canada Other

Mexico’s export productsIn %

Commodities Automotive Electronics Other0%

10%

20%

30%

40%

Mexico’s export partners (2011 in %)

(18%): oil, fruits and vegetables, coffee, cotton

(22%): vehicles, auto parts

(23%): TVs, mobile phones, refrigerators & appliances

(37%): Other manufactured

goods

* 2010. 53 foot container from Mexico to Chicago and 40 foot container from China to Chicago

Mexico’s Export Advantages

Transportation cost*USDs

Lead time*Days

Mexico China

$3058

5 22

$5239

With Significant Export Upside

Labor Unit CostUSDs $4.40 $4.50

0.00

2.00

4.00

6.00

01 03 05 07 09

China

Mexico

Labor unit costUSDs

Mexico’s export oriented manufacturing industry will continue to fuel growth

Source: World Bank, 2012.

22

Phase 1 Research: Mexico’s Manufacturing Advantage– Cost, Quality & Speed

23

Baja CaliforniaChihuahuaCoahuilaNuevo LeónTamaulipasSan Luis PotosíGuanajuatoQuerétaroJaliscoEdo. de MéxicoDistrito FederalTlaxcalaPuebla

VentiladoresCopacabana

Merrytech

G.S.E.B

TIMCO

More than 32 firms*

Mexico Mexico’s Home Appliances Industry: 2005

* Snapshot of 2005 analysis

2424

Increase in Household Appliance Ownership in Mexico

Appliance 2000 2005 2010 2011 2012 2015

Dishwasher 3.8 6.3 9.2 9.8 10.3 11.5

Freezer 4.2 5.3 5.9 6.0 6.1 6.4Microwave Oven 13.0 22.3 29.5 30.8 32.0 35.4

Refrigerator 68.5 79.0 82.1 82.3 82.5 83.2

Telephone 36.2 48.8 46.6 46.0 44.6 42.3

Tumble Drier 4.7 5.0 5.2 5.2 5.3 5.5Vacuum Cleaner 14.1 24.0 35.9 38.2 40.2 46.6Washing Machine 52.0 62.7 66.4 67.0 67.5 68.8

*All figures represent a percentage of households**Source: Euromonitor International

Mexicans are buying modern conveniences

2525

Mexico Aerospace IndustryMexico’s Aerospace Industry grew from 100 in 2004 to 300+ Manufacturers in 2013

26

Querétaro� VISTAR� VITROMATIC (2)

CuernavacaCuernavaca( NEC

Torreónº THOMSON

Monterrey¹ PIONNER� DANFOSS COMPRESSORS� VITROMATIC (3)� MABE (2)º KODAKº NIPPON DENSO (Automotriz)º AXA YAZAKI (Automotriz)

Mexicali¹ SONY¹ DAEWOO(SLRC)¹ MITSUBISHI¹ GOLDSTAR

Aguascalientes�WHITE�WESTINGHOUSE� MEX*º TEXAS INTS.º XEROXº SIEMENS

Querétaro¹ CLARION� DAEWOO� BLACK & DECKER� MABE (2)� SINGERº SIEMENS

MexicoEstado de Mexico� MABE� BRAUN� ELECTROLUX� SUNBEAM� KOBLENZ( ERICSSON( ALCATEL/INDETELº AMP

Puebla� GESTAR� SINGER� VITROMATIC

SaltilloSaltillo� MABE� HAMILTONBEACH*

Reynosa

� VITROMATIC( NOKIA

¹ DELCO (Automotriz)¹ PHILIPS¹ SONY¹ MATSUSHITA (Automotriz)

( LUCENT TECHNOLOGIESº FUJITSU (Automotriz)º CONDURA (Automotriz)º DELNOSA (Automotriz)

SanLuis SanLuis PotosíMABE GE�MABE SANYO�

Chihuahua( MOTOROLAº ALTELº KIOCERAº JABIL

Juárez

¹ KENWOOD� ELECTROLUX7 ACER

¹ TOSHIBA¹ PHILIPS¹ THOMSON

º ELAMEXº PLEXUS

Tijuana¹ SANYO¹ SONY¹ HITACHI¹ MATSUSHITA¹ JVC¹ SAMSUNG¹ PIONNER

º SANYO ELECTRODOMÉSTICOSº PHILIPSº CASIOº KODAKº CANONº KIOCERAº INTERNACIONAL RECTIFIER

¹ MITSUBISHI¹ SHARP

Guadalajara7 I.B.M7 H.P.( NECLUCENT TECHNOLOGIES(

º MOTOROLAº KODAKº CUMEXº SIEMENSº SOLECTRON DE MEXICOº FLEXTRONICSº JABIL CIRCUITº MTI ELECTRONICSº SCI SANMINA

Estado de MéxicoEstado de México

� ELECTROLUX� FILTER QUEEN� HOOVER� IMAN� KOBLENZ� MABE� PHILIPS� SUNBEAMº OLIVETTI

¹ PANASONIC

º OLIMPIA

¹ AUDIO & VIDEO� Home Appliance

7 Computer Equipment

( Telecommunicationsº Other

Mexico’s Consumer Electronics Industry 2005

* Snapshot of 2005 analysis

27

Mexico’s Automotive and Heavy Duty Industry

2828

Fast and sustainable growth

Growing Population and Urbanization

0.85

1.040.88

1.171.29

1.43

05 07 09 11 13 15

GDP (USD tr)

4.0%4.0%

5.3%

3.6%

3.0%3.0%

05 07 09 11 13 15

Inflation (Avg CPI)

12.514.2 13.7

15.116.4

17.6

05 07 09 11 13 15

GDP /capita (USD thds)

23.9%

24.7%

23.2%

25.6%

25.8%

25.9%

05 07 09 11 13 15

Savings rate

103 105 107 110 112 114

05 07 09 11 13 15

Total population (million)

2.2 2.3 2.3 2.4 2.4 2.5

05 07 09 11 13 15

Urban population growth (million)

Healthy population pyramid with increased aging

Age ranges

20302010

Percentage of total population

10% 5% 5% 10%

6%

55%

39%

11%

59%

30%0-45-910-1415-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-7980-8485-8990-9495-99100+

Increasing Spending Power

Source: IMF Outlook Apr 13, CIA World Fact Book, EIU.

28

Phase 1 Research: Mexico’s Continued Growth& Stability Creating a Middle Class

2929

Mexico mobile phone penetration exceeding 80% by 2009

29

Although developing countries globally trend to 58% penetration rate, mobile users in Mexico have passed the 85 million figure in 2010 (78% penetration rate).

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 p/ Apr-‐10

Prepaid 12,450 19,974 23,922 28,070 35,943 43,861 51,092 61,361 69,152 73,098 74,298

Postpaid 1,628 1,784 2,006 2,028 2,509 3,268 4,304 5,199 6,152 10,430 10,979

Total 14,078 21,758 25,928 30,098 38,451 47,129 55,395 66,559 75,303 83,528 85,277

Penetration rate 14% 22% 25% 29% 36% 45% 53% 63% 70% 77% 78%

14,078 21,758

25,928 30,098

38,451 47,129

55,395

66,559 75,303

83,528 85,277

0%10%20%30%40%50%60%70%80%90%

-‐10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000

Pene

tration rate

Num

ber o

f users (th)

Mobile users in Mexico

Source: COFETEL. *Penetration rate for Apr-10, self calculated

3030

Internet Adoption Growing(2000 to 2009)

30

Mexico has over 28 million internet users, and has seen a significant increase in home internet access in recent years (COFETEL). According to AMIPCI, Internet users can be estimated as 30.6 million in 2009. DSL connections dominate.

Source: COFETEL

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 p/

Other 103,341 41,291 29,314 34,125 34,596 54,753 138,785 177,844 239,910 514,744

XDSL -‐ 5,300 78,120 213,494 695,912 1,198,725 1,960,557 3,150,190 5,663,947 7,308,791

Coaxial Cable 8,622 64,479 124,052 180,752 326,774 668,874 987,802 1,236,239 1,690,272 2,097,872

Dial Up 1,023,024 1,772,568 1,864,929 2,015,996 2,134,042 1,959,544 1,718,795 1,283,288 684,188 393,276

Total Suscriptions 1,134,987 1,883,638 2,096,415 2,444,367 3,191,324 3,881,896 4,805,939 5,847,561 8,278,317 10,314,683

Estimated users 5,057,533 7,097,172 10,718,133 11,883,041 13,983,492 17,966,001 20,564,256 22,104,096 23,260,328 28,439,250

1,135 1,884 2,096 2,444 3,191 3,882 4,806 5,848 8,278

10,315

5,0587,097

10,718 11,88313,983

17,96620,564

22,104 23,260

28,439

-‐

5,000

10,000

15,000

20,000

25,000

30,000

Num

ber o

f suscriptio

ns/users

Thou

sand

s

Internet suscriptions and users in Mexico

3131

Companies are starved for growth capital to keep up with the market demand. As a rule consumer lending has far outstripped new business lending save for a short period during the financial crisis.

Source: Comision Nacional Bancaria y de Valores

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Year-over-year growth

Loan Growth in the Mexican Banking System

Business

Consumer

Housing

Significant Growth in Consumer Lending, Limited Business Lending

3232

* Bank credit in Latin America weighted by GDP share. Includes mortgages, credit to consumers and to firmsSource: EMPEA, EIU, LAVCA, Banco de México and S&P Ratings Service; Vander Capital Partners analysis;

PE Penetration vs Attractive Business Environment

3333

Source: Emerging Markets – EMPEA, United Kingdom – Centre for Management Buy-Out Research, United States – PitchBook, Israel – Israel Venture Capital Research Center, Japan – Asia Private Equity Review, All GDP data – International Monetary Fund

OpportunityUp Until 2011 Mexico had very little PE capital & No VCMexico has low private equity participation compared to the BRIC’s.

Private Equity Penetration, 2011

3434

No Debt Financing Avaialable for Small & MediumMexican Businesses 1% of firms get 87% of the financing

Source: AMB Report: “Lending in Mexico” February 2011 and Banco de México; Base de datos ahorro y financiamiento CNBV, diciembre 2010; Endeavor Mexico; Vander Capital Partners analysis.

12%

13%

12%

12%

13%

$56.07

$74.69

$8.38

$11.16

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

ABM CNBV

Small & Med

Large

408,884 smalland med firms

3,033 largefirms

BANK CREDIT TO MEXICAN FIRMS BY SIZE$US Billion

3535

Source: INEGI Preliminary 2009 results

No Debt or Equity Financing Available to the 3.7Million Micro, Small & Medium Business in Mexico (2008)

3636

All Net New Jobs last 30 Years From Small Companies

Source: http://www.kauffman.org/newsroom/u-s-job-growth-driven-entirely-by-startups.aspx.

373737

Venture Capital Accelerates Creation of Knowledge Economy Jobs

3838

Significant Gap in Mexico’s Funding Continuum

SEED/START-UPFUNDING

DEVELOPMENTFUNDING

EXPANSIONFUNDING

OPPORTUNITYDEVELOPMENT

CONTINUEDGROWTH

ANGELS, FOUNDERS & SEED FUNDS

VENTURE CAPITAL – GROWTH EQUITY

PE - PUBLIC MARKETS

VALUATIONS INCREASE

BUSINESS RISKS DECREASE

MENTORING NEEDS DECREASE

$5M-20M$500K-5M$50K-500K >$20MSweat

Financing Gap in Mexico

3939

Without Capital…How can Mexican entrepreneurs create Jobs?

4040

On-The-Ground Research

4141

Driving Questions 2008• Catalyst. Mexico has trillion dollar economy and

is neighbor to the world’s largest economy– Why is the VC asset class missing in Mexico? Could the VC Industry be a catalyst for change and help accelerate a meritocracy in Mexico?

• Corruption. Corruption has been holding back the Mexican people. VC requires trust… can we really create a VC industry in Mexico?

• Capital. Could new sources of capital must be identified and cultivated?

4242

Mexico has come a long wayfrom how I remembered Mexico

4343

Reality –There are many Mexicos

4444

• Violence

• Drug Cartels

• Immigration

Border Issues Obscure US’s view of Mexico

4545

The Alta team Held 120+ meetings to understand oppor tunities and challenges of doing business in Mexico & create a unified vision.

Government

Industry

Mexican Families

Research/Universities

LPs/Financial

Federal Competition Commission; Economic Bureau; Undersecretary of the Treasury; ProMexico; Economic Bureau, Foreign Investment; Telecommunications and Transportation Bureau; Mexican Senators; Governor of State of Mexico; Former Ambassador to US; Mayor of Mexico City; Undersecretary of North America; Mexican Legislature; Executive Director, NAFINSA; ProMexico; FOCIR

GE Mexico, Cisco, Corporate and Investment Bank of Banamex (Citigroup), Intel Capital Mexico, IXE Grupo Financiero, American Chamber of Commerce—Mexico, Cavlemas, US Hispanic Chamber of Commerce; Banorte Insurance, Deutsche Bank Mexico

Visited with more than 30+ families who are among the most influential in Mexico

Tecnologico de Monterrey (TEC) , UNAM, CEPII, Conacyt, Pan American Univ. (CEPii)

More than 20 limited partners and 3 institutional investors and multilaterals including IFC, NAFIN, CMIC, IADB/MIF

45

Phase 1: Fresh Look– 120+ Meetings